overview of ad-hoc budget review committee recommendations dick dietrich, chair, senate fiscal...

TRANSCRIPT

Overview of Ad-hoc Budget Review

Committee Recommendations

Dick Dietrich, Chair, Senate Fiscal CommitteePrepared from multiple sources with appreciation

2

Committee Members Members Deborah Larsen, Co-Chair, College of Medicine Jozef C. Raadschelders, Co-Chair, John Glenn School of Public Affairs Anil Arya, Fisher College of Business Morgan Cichon, Council of Graduate Students Donna Hobart, Office of the President Shane Ingalls, Undergraduate Student Government Betsy Lindsey, College of Education and Human Ecology Marie Mead, College of Engineering Robert Perry, College of Arts and Sciences James Phelan, College of Arts and Sciences Kris Devine, Office of Business and Finance, ex officio Brad Harris, Office of Academic Affairs, ex officio

Staff Support Suzi Ballinger, Financial Planning and Analysis Dawn Romie, Financial Planning and Analysis Jim Schiefferle, Financial Planning and Analysis

3

Review Process1. Understand the university budget (all areas, including

student life, athletics, medical center)2. Understand the University Budget Model and Budget

System3. Understand historical context of last five years4. Understand the data5. Survey the colleges6. Evaluate the BSAC recommendations and outcomes7. Discussion of risks, challenges and opportunities8. Formulate conclusions and recommendations

4

Recommendations Overarching Recommendation“The guiding principles and design of the university budget model are fundamentally sound. The committee recommends the budget model should be retained. To fully take advantage of the budget model, central university decisions must be made in a coordinated, holistic, transparent manner with the impact of decisions on colleges and support units modeled prior to the decisions being finalized”

Specific Recommendations—three areas•Annual Planning and Review Process•Budget Model•Management Reporting and Training

5

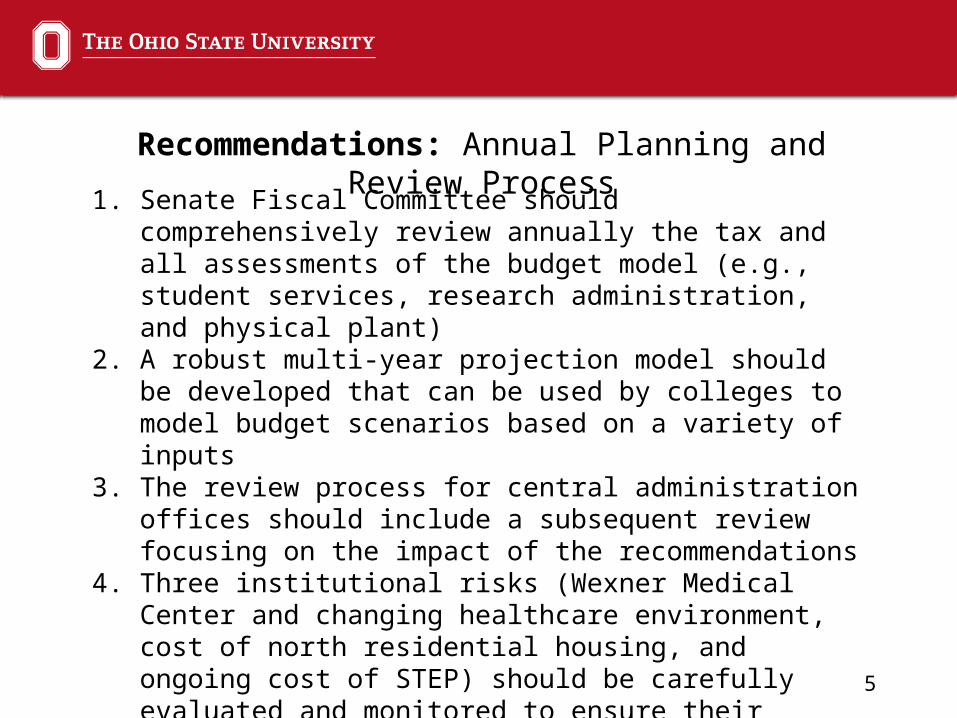

Recommendations: Annual Planning and Review Process

1. Senate Fiscal Committee should comprehensively review annually the tax and all assessments of the budget model (e.g., student services, research administration, and physical plant)

2. A robust multi-year projection model should be developed that can be used by colleges to model budget scenarios based on a variety of inputs

3. The review process for central administration offices should include a subsequent review focusing on the impact of the recommendations

4. Three institutional risks (Wexner Medical Center and changing healthcare environment, cost of north residential housing, and ongoing cost of STEP) should be carefully evaluated and monitored to ensure their impact is understood, and strategic decisions should be made to minimize the impact to the model

6

Recommendations: Budget Model

1. Assessments outside the budget model should be limited2. The subsidy allocation methodology should be re-evaluated when

the Ohio Board of Regents methodology is finalized3. A re-basing analysis should be completed for all colleges

7

Recommendations: Management Reporting and Training

1. Colleges should have a college level committee for fiscal and budget issues with adequate department level faculty and staff representation

2. To increase transparency, fiscal presentations by college leadership, such as the dean and senior fiscal officer, to faculty and staff are desirable and expected

3. Financial training for unit leaders, including deans, associate deans, department chairs and senior fiscal officers, should be implemented

4. Centralized financial reports that are easily accessible and provide multi-year data by college and department should be developed and maintained

5. The Senate Fiscal Committee should review these recommendations in early FY2016 to determine the implementation status

8

OSU Budget and Budget Model:

Background

9

General Funds BudgetBUDGETED RESOURCES GENERAL FUNDS

COLUMBUS CAMPUS – FY 2014 (IN THOUSANDS)

State Support342,366

Instructional Fees957,641

Other121,236

TOTAL 1,421,243

10

General Funds BudgetComparison of State Support* to Tuition** Income: Columbus Campus

11

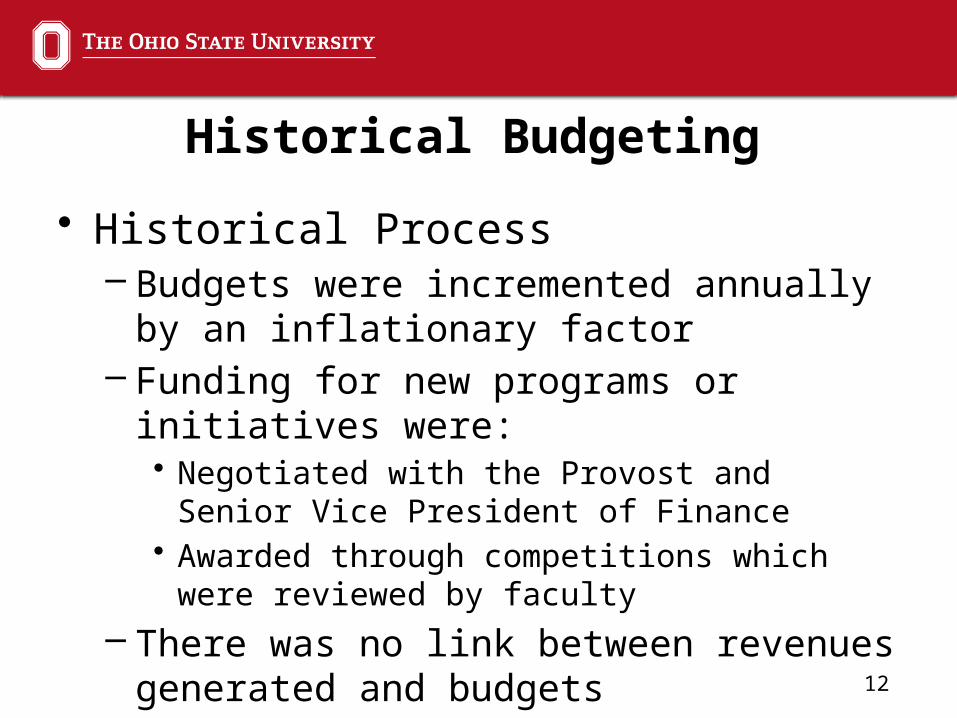

Historical Budgeting

12

Historical Budgeting

• Historical Process– Budgets were incremented annually by an

inflationary factor– Funding for new programs or initiatives were:

• Negotiated with the Provost and Senior Vice President of Finance

• Awarded through competitions which were reviewed by faculty

– There was no link between revenues generated and budgets

13

Historical Budgeting

• Weaknesses identified with the historical process–Budget process was not sufficiently

supportive of the University’s mission–Budget process did not provide incentives to

reduce costs or generate additional revenues–Budget process did not provide sufficient

accountability

14

Guiding Principles of the

Budgeting Process

(Responsibility Centered Budgeting)

15

Principles

• General Fund allocation informed by Academic Plan• General Fund revenues and departmental/college

expenses explicitly linked to generating units• A portion of General Fund revenues dedicated to the

support of university-wide services• Maintenance of a certain level of budget stability and

predictability• Appropriate oversight and accountability• Continuous review and improvement

16

Budget Model vs. Budget System

• Budget Model – Mechanical allocations of funds driven primarily by enrollments

• Budget System – Includes central funding allocated for strategic initiatives at the Provost’s discretion

17

Key Elements of the

Budgeting Process

18

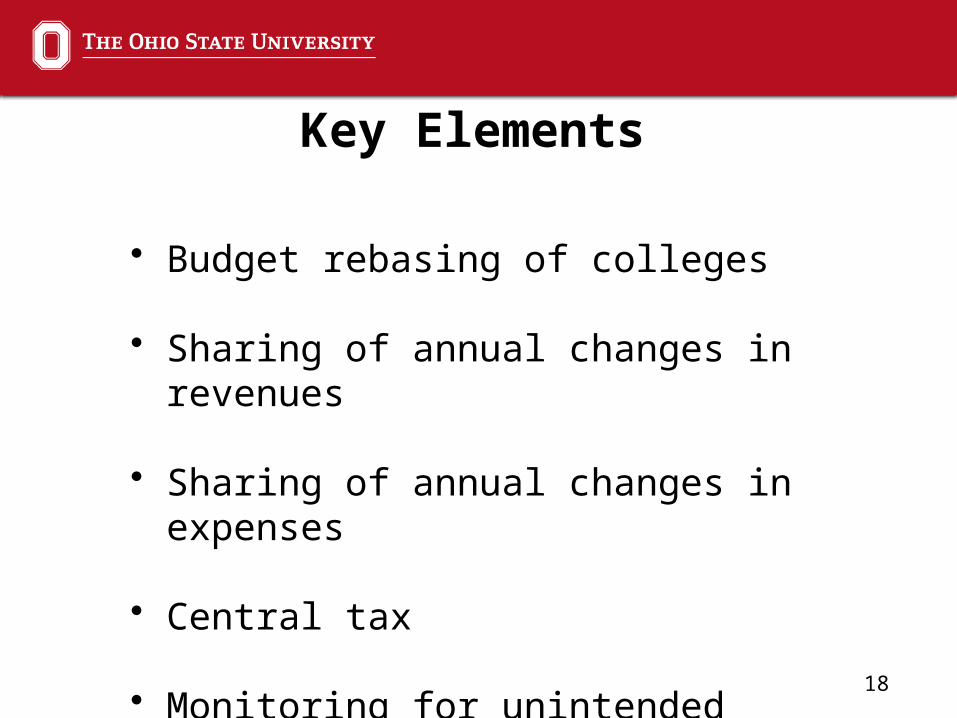

Key Elements

• Budget rebasing of colleges

• Sharing of annual changes in revenues

• Sharing of annual changes in expenses

• Central tax

• Monitoring for unintended consequences

19

Rebasing:When RCB was implemented

• Revenues and expenses for each college were measured• Significant differences between revenues and expenses were

identified• Colleges were placed into three groups in relationship to the

goals of the Academic Plan• Rebasing goals were established to reallocate over $15.5

million among the colleges through the Provost’s Strategic Investment funds and reductions in some college base budgets

20

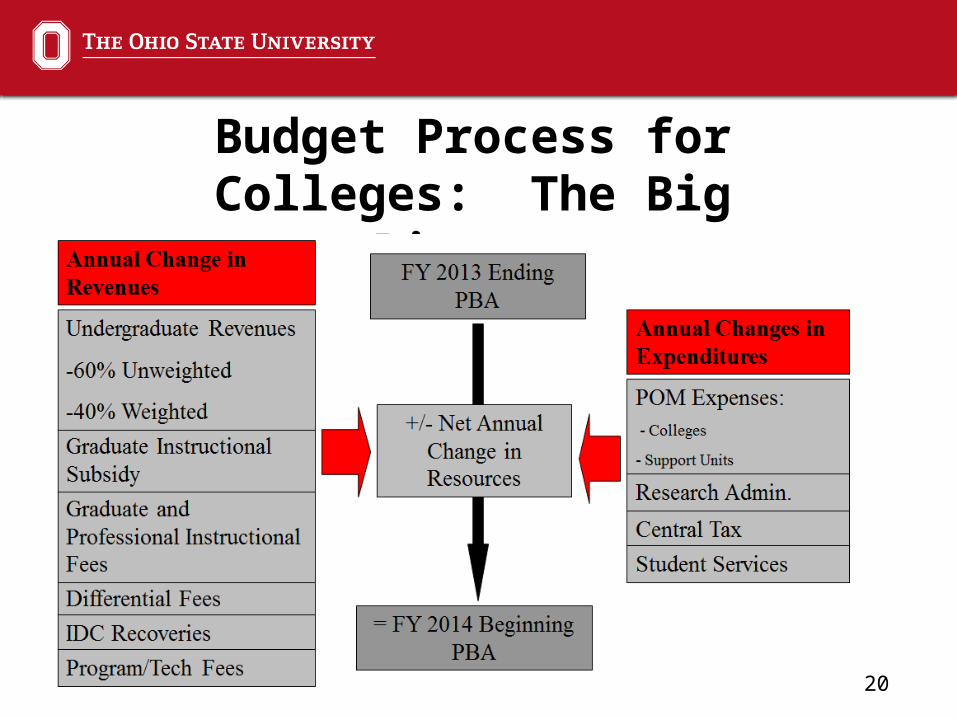

Budget Process for Colleges: The Big Picture

21

Allocation of Annual Revenue Changes

Allocation of Instructional Fees & State Support

• Colleges receive all revenue generated for new credit hours, including revenue generated from instructional fees and state share of instruction sometimes called subsidy

• Colleges receive the inflationary revenue generated for existing credit hours of instruction, including inflationary (which could increase or decrease) revenue generated by instructional fees and subsidy

*Does not apply to differential fees, program fees, technology fees, or general fees

22

Sharing of Revenue Instructional Fees

• Fee per credit hour was established for each fee category• College receives full fee per credit hour for each additional

credit hour they teach• College also receives the inflationary growth from previous

year in the fee per credit hour; this growth will be distributed based on the total credit hours taught

• The annual change in the instructional fee is shared based on the average of two prior years of credit hours

23

Sharing of Revenue State Share of Instruction

• State share of instruction per credit hour was established for each SSI category

• College receives full SSI per credit hour for each additional credit hour they teach

• College also receives the inflationary growth from previous year in the SSI per credit hour; this growth is distributed based on the total credit hours taught

• The annual change in SSI dollars is shared based on the average of two prior years of credit hours

24

Allocation of Annual Changes in Revenue

Indirect Costs• 100% of the annual changes in indirect cost recovery revenues

are allocated directly to the generating college or vice-presidential area except for that portion associated with University Library costs. Annual changes in the portion associated with the Libraries will be allocated to the Libraries

• OSU’s IDC rate for FY14 is 53.5%

25

Allocation of Annual Changes in Expenses

The budget model includes four categories of expenses, each of which is allocated to the colleges based on unique measures:

1. Student services (applies to colleges & any support units generating credit hours)

2. Physical plant (applies to colleges & support units)3. Research administration (applies to colleges &

support units)4. Central tax (applies to colleges)

26

Allocation of Annual Expense ChangesSTUDENT SERVICE ASSESSMENTS

– Cost Pool 1 (Undergraduate): 76% of this cost pool is Undergraduate Financial Aid. Also includes operating budgets for Financial Aid and First Year Experience. Expense is allocated by average undergraduate credit hours.

– Cost Pool 2 (Graduate): 76% of this cost pool is Non-Resident Fee Authorizations. This is the largest cost pool and includes operating budget of the Graduate School. Expense is allocated by average graduate credit hours.

– Cost Pool 3 (All Students): this is the smallest cost pool and includes portions of operating budgets for Student Affairs, Academic Affairs, and new Library Acquisitions. Expense is allocated by an average of ALL credit hours.

– Cost Pool 4 (Distance Education programs): this is a newly created cost pool used to support the Office of Distance Education and eLearning

27

Allocation of Annual Changes in Expenses

PLANT OPERATION AND MAINTENANCE

– Annual changes in expenses are allocated to the units based on the assigned square footage recorded in the university’s space inventory

– The square footage is multiplied by a flat rate per square foot for four types of costs: utilities, custodial service, maintenance, and renewal & replacement

– Units who have leased space are responsible for additional leased space and rent increases

28

Allocation of Annual Changes in Expenses

RESEARCH ASSESSMENT

– Research cost allocation covers the budgets of units that support sponsored research (e.g. OSP formerly OSURF)

– Individual colleges are allocated a research cost proportional to their Modified Total Direct Cost expenditures

– Central tax funds the administrative components of the Office of Research that have university-wide responsibilities (e.g. Office of Responsible Research Practices)

29

Allocation of Annual Changes in Expenses

CENTRAL TAX AT 24%

– Supports units such as the President’s Office, OAA, Treasurer’s Office, Controller, Public Safety, and University Landscaping are funded by a 19% Central Tax

– An additional 5% tax funds Strategic Investments– These taxes apply to:

• Subsidy (Instructional)• Instructional Fees

– These taxes do not apply to:• Indirect Cost Recoveries• Differential Fees• Program Fees• Technology Fees

30

FY14 Net Revenue per New Undergraduate Student

FY 14 Rates Standard Undergraduate 345.18$ 5,177.70$ 140.95$ 2,114.25$

7,291.95$ 150.00$

7,441.95$ 24% 1,750.07$

NA

107.39$ 1,610.85$ 5.00$ 75.00$

NANA

3,435.92$ 4,006.03$ 8,012.06$

267.07$

Notes: 1 - Assumes credit hours per semester per UG student = 15 2 - Subsidy category in this illustration is BES3 3 - Full impact of revenue is realized in 3 years

Development AssessmentTotal ExpensesNet Revenue per semesterNet Revenue per year assuming 2 semestersNet Revenue per credit hour

Research Admin Assessment

Unweighted UG Fee/SSI AllocationWeighted UG Fee/SSI AllocationTotal Taxable Revenue Program FeeTotal RevenueMarginal TaxPhysical Plant AssessmentStudent Services Assessment Undergraduate All Students