overview of concepts and definitions - bank for ... · control over key aspects of the financial...

TRANSCRIPT

IMF Statistics Department

The views expressed herein are those of the author and should not necessarily be attributed to the IMF, its Executive Board, or its management

Venkat Josyula

Developing and Improving Sectoral Financial AccountsAlgiers, January 20-21, 2016

OVERVIEW OF CONCEPTS AND DEFINITIONS

IMF Statistics Department

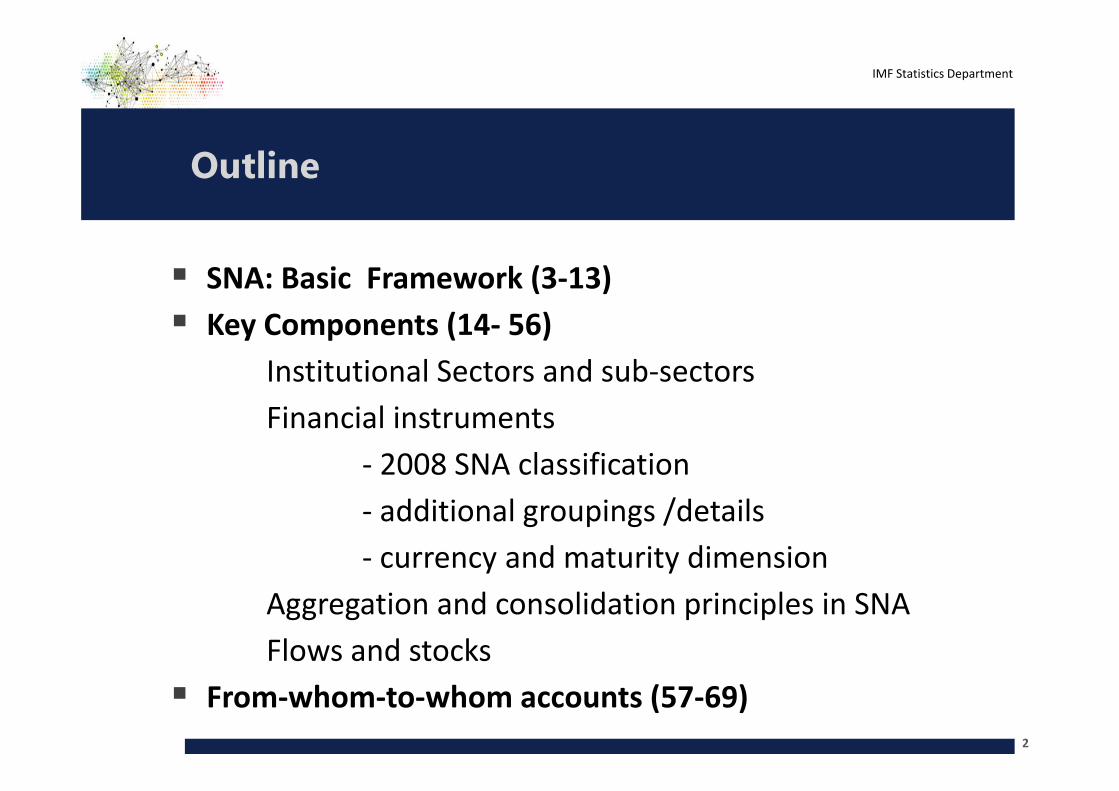

SNA: Basic Framework (3-13) Key Components (14- 56)

Institutional Sectors and sub-sectorsFinancial instruments

- 2008 SNA classification- additional groupings /details- currency and maturity dimension

Aggregation and consolidation principles in SNAFlows and stocks

From-whom-to-whom accounts (57-69)2

Outline

IMF Statistics Department

SNA: Basic Framework

3

IMF Statistics Department

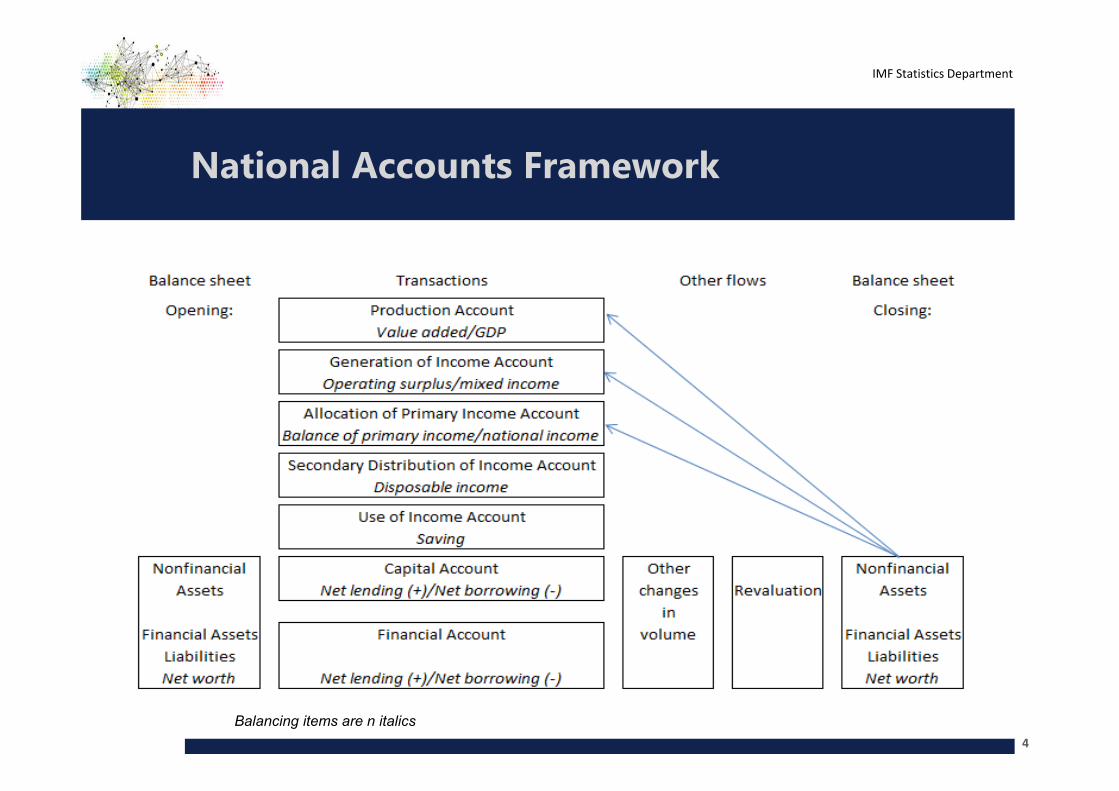

National Accounts Framework

4

Balancing items are n italics

IMF Statistics Department

National Accounts Framework

Shows economic processes and their relationships• Column shows transactions:

Production generates income; Income not spent on consumption is saving; Saving can be used to finance acquisition of financial and

nonfinancial assets incurrence of liabilities allows acquisition of more assets;

If saving greater than investment in nonfinancial assets, there is net lending

Other changes in revaluations and revaluations not transactions

Shows stocks and flows and their relationships• Row shows stock-flow identities:

Beginning value + transactions + other flows = Ending value

5

IMF Statistics Department

Balance Sheet and Accumulation Accounts (1)

Transactions in financial assets/liabilities• Recorded in the financial account

All entries relating only to financial transactions Explains how net lending or net borrowing arises Explains how financial assets owned by one unit are put at the disposal

of another Recorded as net acquisition of assets or net incurrence of liabilities by

instrument over an accounting period

• Lead to financial asset/liability positions

6

Balance Sheet and Accumulation Accounts (1)

IMF Statistics Department

Balance Sheet and Accumulation Accounts (2)

Positions in financial assets/liabilities• Recorded in the balance sheet

Refer to a particular point in time Show values of assets and liabilities at that time Record gross values of assets and liabilities on the balance sheet date

• Changes in positions occur due to Transactions Revaluation (holding gains and losses) Other changes in volume of assets

• Opening position + transactions + revaluation + other changes in volume = closing position

7

IMF Statistics Department

Balance Sheet and Accumulation Accounts (3)

Revaluation of financial assets/liabilities• Recorded in the revaluation account

Measures changes in the value of financial asset and liabilities due to Changes in their prices Exchange rates

Recorded as net revaluation of assets or liabilities by instrument over an accounting period

8

IMF Statistics Department

Balance Sheet and Accumulation Accounts (4)

Other changes in volume of financial assets/liabilities• Recorded in the other changes in volume of assets account

Measures changes in the value of financial asset and liabilities due to Changes in classification

• Type of financial asset or sector Write-off of debts by creditors Uncompensated seizures and catastrophic losses Changes in pension entitlements and insurance reserves due to changes in

model assumption or imposition Recorded as net changes in the value of assets or liabilities by

instrument over an accounting period

9

IMF Statistics Department

National Accounts Framework

10

Framework not just applicable to national accounts (GDP and other macro-aggregates)

but also SECTORAL ACCOUNTS• 5 main sectors and a quasi-sector

Financial corporations Nonfinancial corporations Households Nonprofit institutions serving households General government Rest of the World

• Shows how different parts of the economy behave and interact. Different motivations and functions

IMF Statistics Department

Financial Account – Total economy

11

S1 S1

Assets Liabilities

10

436 426

-1 F1 Monetary gold and SDRs -

89 F2 Currency and deposits 102

86 F3 Debt securities 74

78 F4 Loans 47

107 F5 Equity and investment fund shares 105

48 F6 Insurance, pension and standardized guarantee schemes 48

14 F7 Financial derivatives and employee stock options 11

15 F8 Other accounts receivable/payable 39

Total Economy

Total

Total Economy

Net lending(+) / Net borrowing(-)

Balance sheet version is the same (different numbers and codes)

IMF Statistics Department

Financial Account – by sectors

12

Households Households

+NPISH +NPISH

S11 S12 S13 S14/S15 S1 S11 S12 S13 S14/S15 S1

-56 -1 -103 173 10

83 172 -10 191 436 139 173 93 21 426-1 -1 F1 Monetary gold and SDRs -

39 10 -26 66 89 F2 Currency and deposits 65 37 102

7 66 4 9 86 F3 Debt securities 6 30 38 74

19 53 3 3 78 F4 Loans 21 9 17 47

10 28 3 66 107 F5 Equity and investment fund shares 83 22 105

1 7 1 39 48 F6 Insurance, pension and standardized guarantee schemes 48 48

3 8 3 14 F7 Financial derivatives and employee stock options 3 8 11

4 1 5 5 15 F8 Other accounts receivable/payable 26 9 4 39

Total

Nonfinancial corporations

Financial corporations

General government

LiabilitiesNonfinancial corporations

Financial corporations

General government

Total Economy

Assets

Net lending(+) / Net borrowing(-)

Total Economy

Same as the previous slide – with information on sectors

IMF Statistics Department

Financial Account –Sectoral Accounts + From-Whom-To-Whom

13

Households

+NPISH

Net inc. of liabilities: S11 S12 S13 S14/S15 S2

Nonfinancial corporations 24 57 2 42 14 139Financial corporations 24 51 -8 93 13 173General government 5 26 0 42 20 93Households + NPISH 4 8 -2 11 0 21

Rest of World 26 30 -2 3 - 57Total 83 172 -10 191 47 483

Total

Net acquisition of financial assets:

Nonfinancial corporations

Financial corporations

General government

Rest of World

Columns expanded to matrix. Numbers in italics not from 2008 SNA.

IMF Statistics Department

Key Components

14

IMF Statistics Department

Institutional sectors

Institutional sectors made up of institutional units• Individual decision-making entities in the economy• Households; legal and social entities• Borderline cases

artificial subsidiaries, holding companies vs. headquarters, special purpose entities, unincorporated branches, land ownership, quasi-corporations

• Proper identification necessary to avoid gaps and double-counting

• Institutional sectors combine units with common motivations and behavior

• 5 main sectors and a quasi-sector15

IMF Statistics Department

Financial corporations

Financial Corporations – 9 subsectors Central bank Deposit-taking corporations except CB (DTC) Money market funds Non-money market investment funds Other financial intermediaries except insurance corporations and

pension funds Financial auxiliaries Captive financial institutions and money lenders Insurance corporations Pension funds

16

IMF Statistics Department

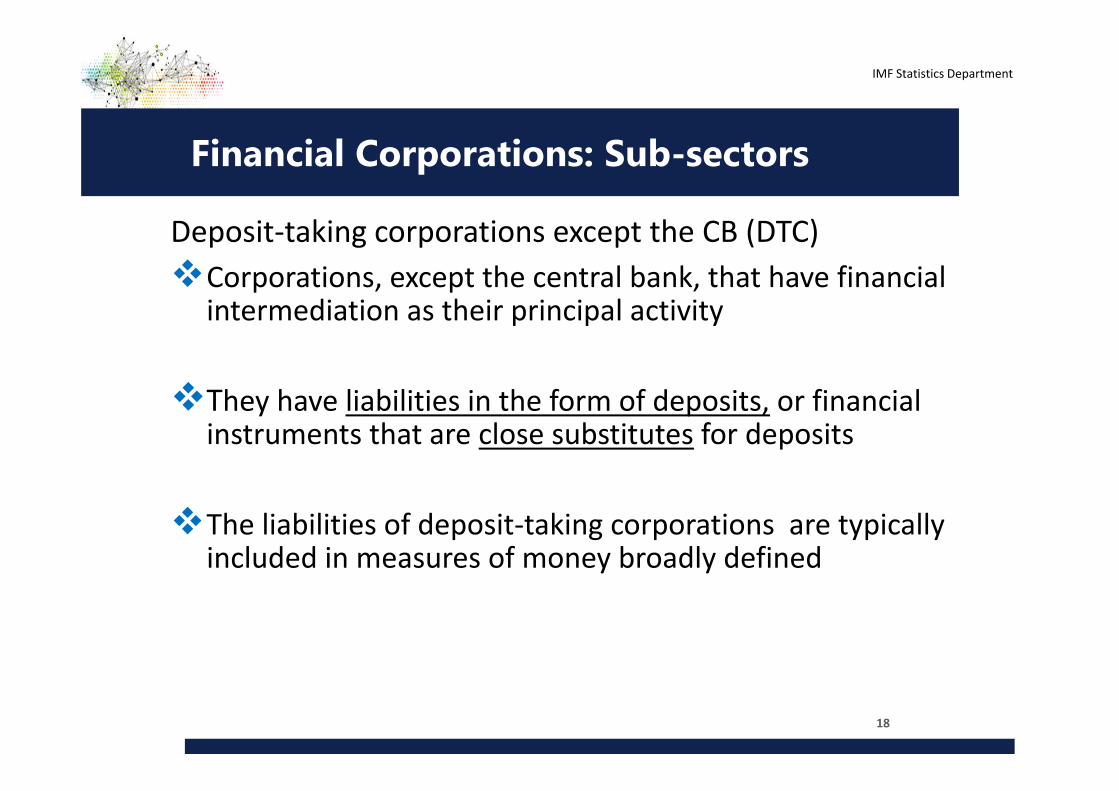

Financial Corporations: Sub-sectors

Central bank: National financial institution exercising control over key aspects of the financial system

Typical central bank functions: Currency issue International reserves management Transacting with the IMF Lender of last resort Government fiscal agent Supervising financial system

17

IMF Statistics Department

Financial Corporations: Sub-sectors

Deposit-taking corporations except the CB (DTC)Corporations, except the central bank, that have financial

intermediation as their principal activity

They have liabilities in the form of deposits, or financial instruments that are close substitutes for deposits

The liabilities of deposit-taking corporations are typically included in measures of money broadly defined

18

IMF Statistics Department

Financial Corporations: Sub-sectors

Units that might be classified as DTCs include:Merchant banksCommercial banksOffshore banksSpecialized banks (savings, agricultural, credit

unions)Finance companiesMicro finance companiesCredit unions and cooperatives

19

IMF Statistics Department

Financial Corporations: Sub-sectors

Money market funds (MMF) Collective investment schemesRaise funds by issuing sharesInvest in money market instruments (MMI)MMF shares may be transferred by check or other means

MMI are short-term debt securities or deposits—very low risk

20

IMF Statistics Department

Financial Corporations: Sub-sectors

Non-MMF investment funds Collective investment schemesRaise funds by issuing sharesAssets are not MMI – debt, equity, nonfinancial

assetsLiabilities are not substitutes for deposits

21

IMF Statistics Department

Financial Corporations: Sub-sectors

Other financial intermediaries except insurance corporations and pension funds -- financial intermediaries, but their liabilities are not deposits or substitutesSecuritization companiesSecurity and derivatives dealers (own account)Lending and leasingClearing housesSpecialized financial corporations

22

IMF Statistics Department

Financial Corporations: Sub-sectors

Financial auxiliaries Brokers Guarantors Exchanges Financial regulators Fund managers Foreign exchange bureaus

23

IMF Statistics Department

Financial Corporations: Sub-sectors

Captive financial institutions & money lendersMost of their financial assets or liabilities are not

transacted on open financial markets Transact with a limited number of units or subsidiaries of the same

corporation or entities that provide loans from own funds/one sponsor

Basically two distinct groupsCaptive financial institutions Trusts, estates; holding corporations; special

purpose entities Money lenders with a full set of accounts

24

IMF Statistics Department

Financial Corporations: Sub-sectors

Insurance corporationsMutual and other financial entities providing life and/or

non-life insurance to individual units or groups of unitsPension funds Provide retirement benefits for specific groups of employees

Own assets/liabilities and transact on own account

Separate from the units that have created them

Employee and/or employer contribution

Social security schemes are NOT included here

25

IMF Statistics Department

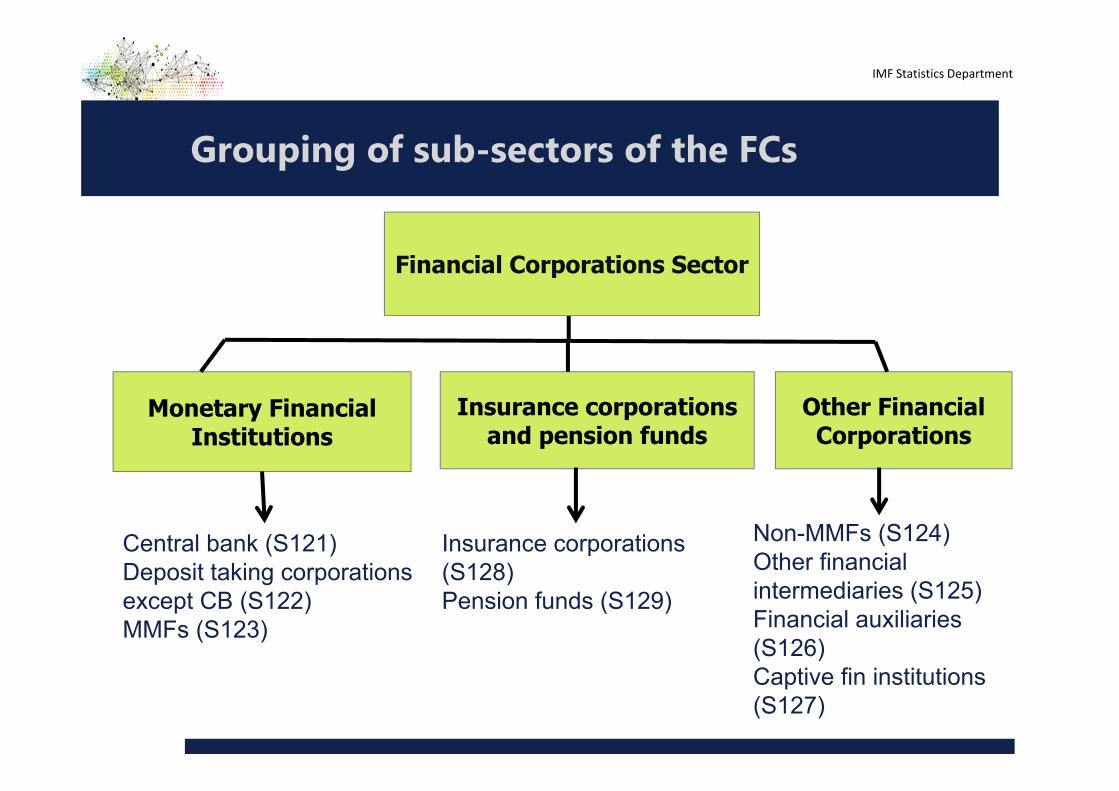

Grouping of sub-sectors of the FCs

Financial Corporations Sector

Insurance corporations and pension funds

Other FinancialCorporations

Monetary Financial Institutions

Central bank (S121)Deposit taking corporations except CB (S122)MMFs (S123)

Insurance corporations (S128)Pension funds (S129)

Non-MMFs (S124)Other financial intermediaries (S125)Financial auxiliaries (S126)Captive fin institutions (S127)

IMF Statistics Department

General Government Sector

General Government Exercises legislative, judicial, or executive authority over other institutional units within a

specified area; has authority to impose taxes, provide goods and services free of charge or at prices that are not economically significant, redistribute income

Motivation is policy rather than commercial

• Subsectors Central government State government Local government Social security funds

alternative structure where social security funds at each level of government are included at that level

• NPIs engaged in non-market production and are controlled by government are part of General Government sector

27

IMF Statistics Department

Public Sector

Not the same as the general government sectorComposition:1. General government2. Public Non-financial corporations3. Public Non-financial sector (1+2)4. Public financial corporations5. Public sector (1+2+4)

28

IMF Statistics Department

Financial Instruments

2008 SNA Classification• Monetary gold (asset side only) and SDRs• Currency and deposits• Debt securities• Loans• Equity and investment fund shares• Insurance, pension and standardized guarantee schemes• Financial derivatives and employee stock options• Other accounts receivable/payable

• Sequence based broadly on liquidity29

IMF Statistics Department

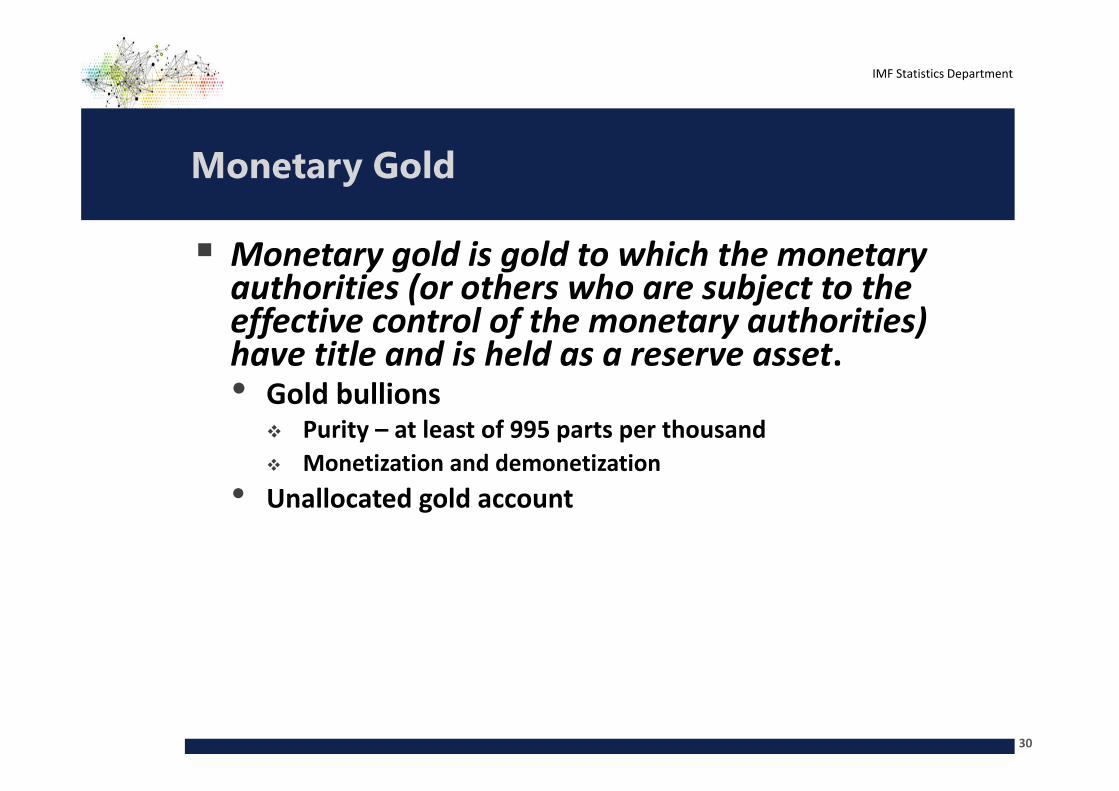

Monetary Gold

Monetary gold is gold to which the monetary authorities (or others who are subject to the effective control of the monetary authorities) have title and is held as a reserve asset.• Gold bullions

Purity – at least of 995 parts per thousand Monetization and demonetization

• Unallocated gold account

30

IMF Statistics Department

31

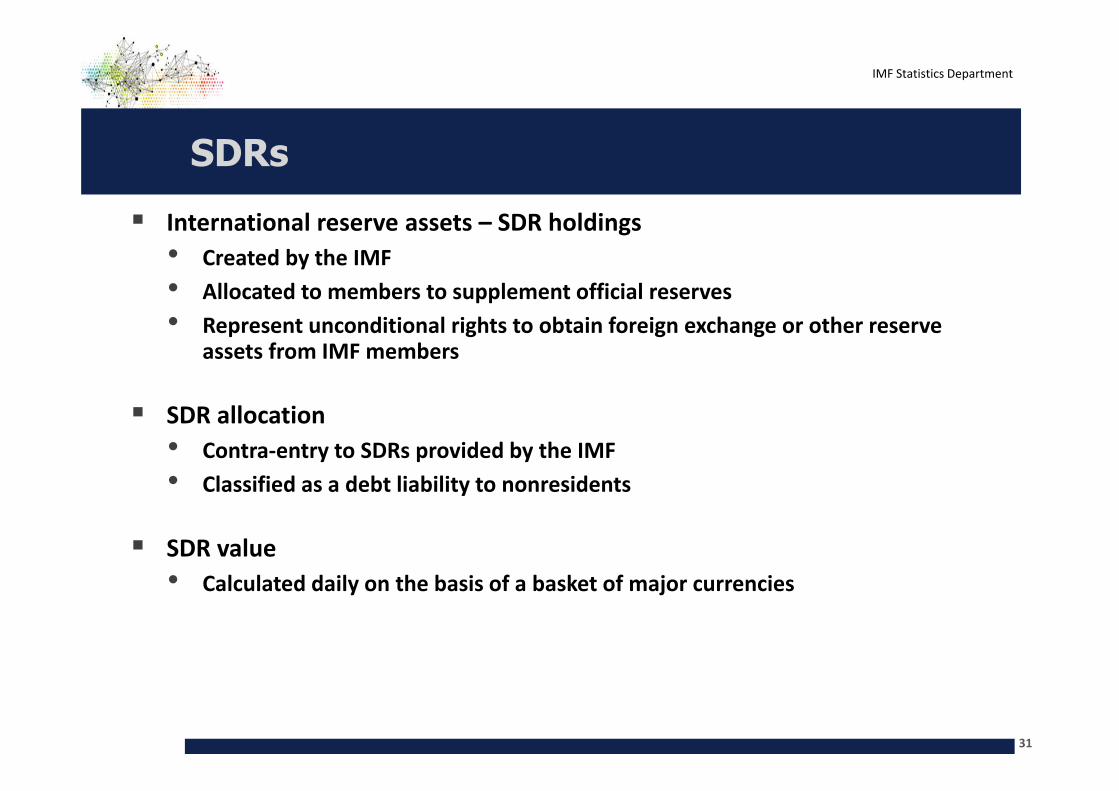

SDRs

International reserve assets – SDR holdings• Created by the IMF• Allocated to members to supplement official reserves• Represent unconditional rights to obtain foreign exchange or other reserve

assets from IMF members

SDR allocation • Contra-entry to SDRs provided by the IMF• Classified as a debt liability to nonresidents

SDR value• Calculated daily on the basis of a basket of major currencies

IMF Statistics Department

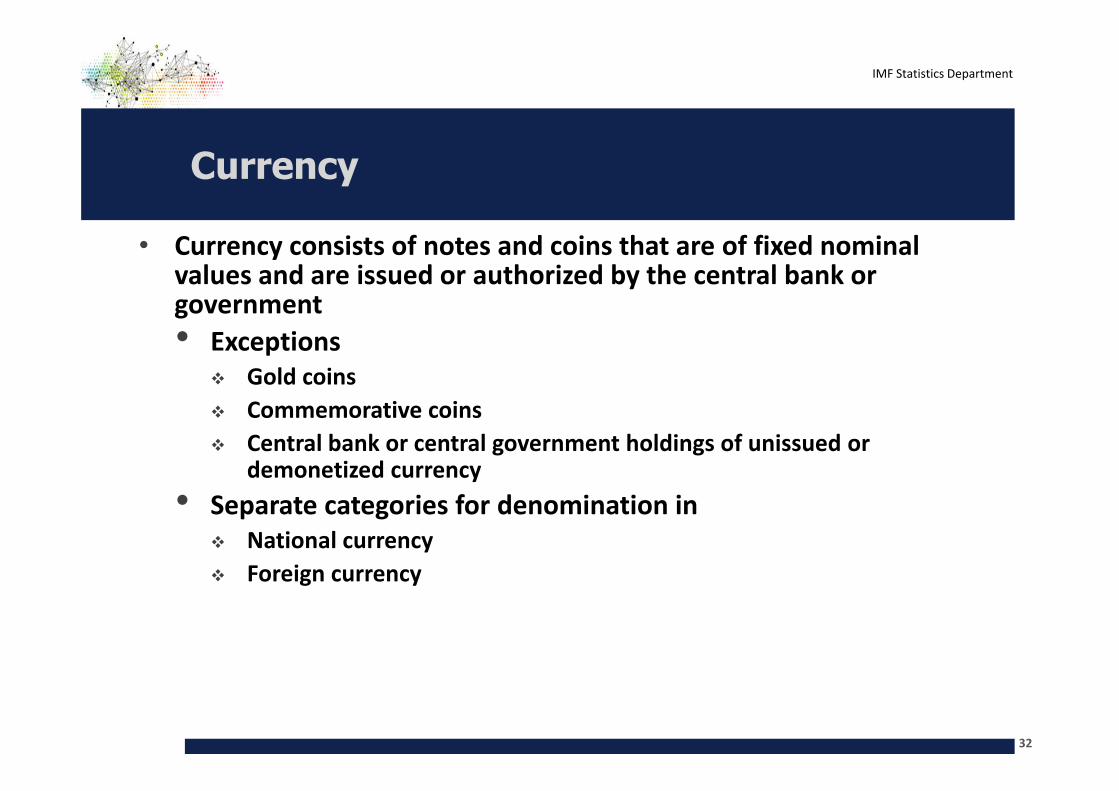

Currency

• Currency consists of notes and coins that are of fixed nominal values and are issued or authorized by the central bank or government• Exceptions

Gold coins Commemorative coins Central bank or central government holdings of unissued or

demonetized currency• Separate categories for denomination in

National currency Foreign currency

32

IMF Statistics Department

Deposits

Transferable deposits comprise all deposits that: • are exchangeable for bank notes and coins on demand at par and

without penalty or restriction; and • are directly usable for making payments by cheque, draft, giro order,

direct debit/credit, or other direct payment facility. Interbank positions Other transferable deposits

Other deposits• All other claims that are represented by evidence of deposit

Currency of denomination

33

IMF Statistics Department

Debt Securities

Debt securities are negotiable instruments serving as evidence of a debt• Original maturity• Remaining maturity• Currency of denomination

Examples• Bills, bonds, asset-backed securities, stripped securities, index-

linked securities Valuation issues

34

IMF Statistics Department

Loans Loans are financial assets that:

• are created when a creditor lends funds directly to a debtor, and • are evidenced by documents that are not negotiable.

Further classifications• Original maturity• Remaining maturity• Currency of denomination

Valuation issues

35

IMF Statistics Department

Equity and Investment Fund Shares

• Equity comprises all instruments and records acknowledging claims on the residual value of a corporation or quasi-corporation after the claims of all creditors have been met.

• Investment funds are collective investment undertakings through which investors pool funds for investment in financial or non-financial assets or both.

36

IMF Statistics Department

37

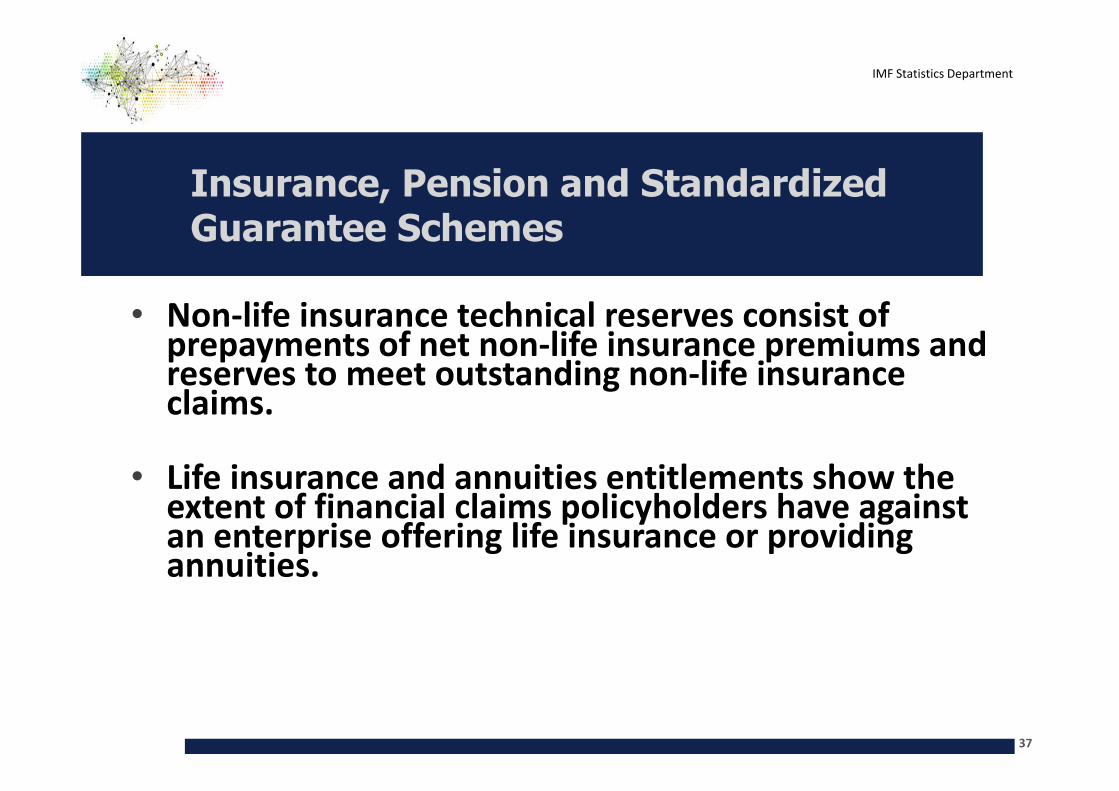

Insurance, Pension and Standardized Guarantee Schemes

• Non-life insurance technical reserves consist of prepayments of net non-life insurance premiums and reserves to meet outstanding non-life insurance claims.

• Life insurance and annuities entitlements show the extent of financial claims policyholders have against an enterprise offering life insurance or providing annuities.

IMF Statistics Department

Insurance, Pension and Standardized Guarantee Schemes

• Pension entitlements show the extent of financial claims both existing and future pensioners hold against either their employer or a fund designated by the employer to pay pensions earned as part of a compensation agreement between the employer and employee.

• Provisions for calls under standardized guarantees consist of prepayments of net fees and provisions to meet outstanding calls under standardized guarantees.

38

IMF Statistics Department

39

Financial Derivatives and Employee Stock Options

Financial derivatives are financial instruments that are linked to a specific financial instrument or indicator or commodity, through which specific financial risks can be traded in financial markets in their own right.

IMF Statistics Department

• An employee stock option is an agreement made on a given date (the “grant” date) under which an employee may purchase a given number of shares of the employer’s stock at a stated price (the “strike” price) either at a stated time (the “vesting” date) or within a period of time (the “exercise” date) immediately following the vesting date.

40

Financial Derivatives and Employee Stock Options

IMF Statistics Department

41

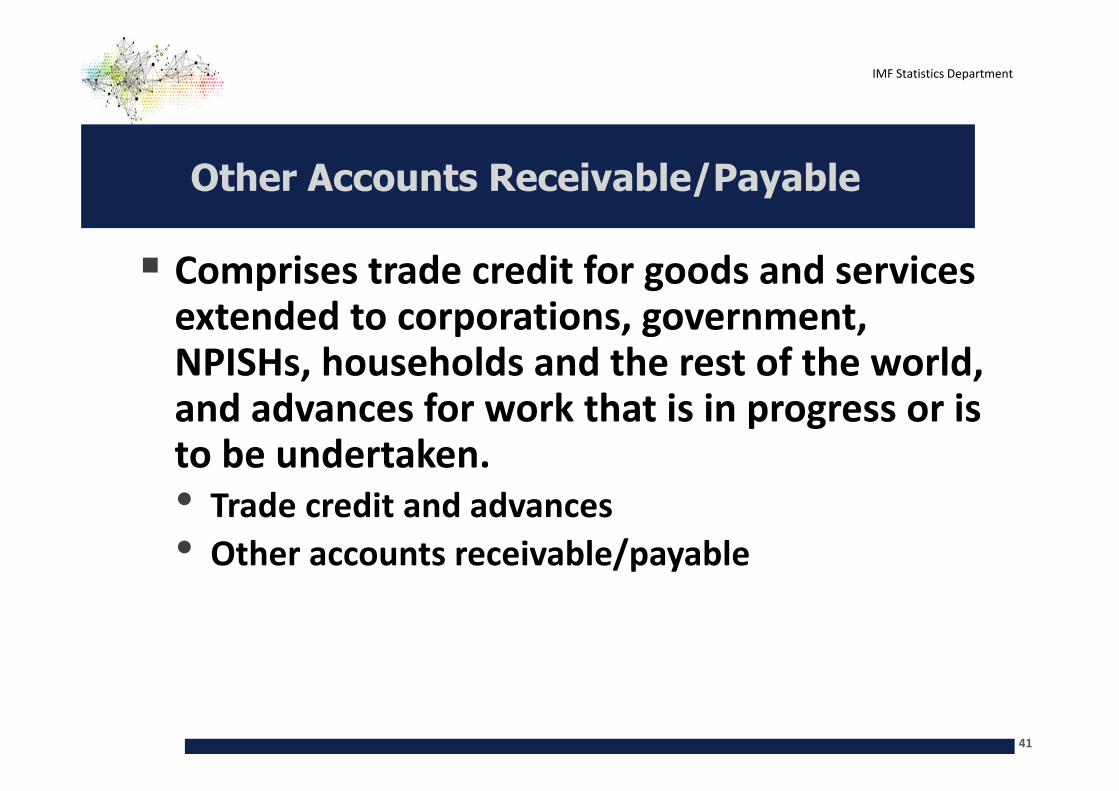

Other Accounts Receivable/Payable

Comprises trade credit for goods and services extended to corporations, government, NPISHs, households and the rest of the world, and advances for work that is in progress or is to be undertaken.• Trade credit and advances• Other accounts receivable/payable

IMF Statistics Department

Financial Instruments –additional grouping

Additional grouping for analysis:

Debt: Liabilities only F1 + F2 + F3 + F4 + F6 + F8 That is: all but equity and investment fund shares, financial derivatives and

ESOs Of particular interest because of vulnerability

External Debt Database; Public Sector Debt DatabaseExternal Debt Guide; Public Sector Debt Guide

42

IMF Statistics Department

Financial Instruments –additional details

F2 Currency and depositsF21 CurrencyF22 Transferable deposits

F221 Interbank positionsF229 Other transferable deposits

F29 Other deposits

F5 Equity and investment fund sharesF51 Equity

F511 Listed sharesF512 Unlisted sharesF519 Other equity

F52 Investment fund shares/unitsF521 Money market fund shares/unitsF522 Non MMF investment fund shares/units

43

IMF Statistics Department

Financial Instruments –additional details

F6 Insurance, pension and standardized guarantee schemesF61 Non-life insurance technical reserves

F62 Life insurance and annuity entitlements

F63+F64+F65 Retirement entitlements

F63 Pension entitlements

F64 Claim of pension fund on pension managers

F65 Entitlements to non-pension benefits

F66 Provisions for calls under standardized guarantees

44

IMF Statistics Department

Financial Instruments –additional details

F7 Financial derivatives and employee stock optionsF71 Financial derivatives

F711 OptionsF712 Forwards

F72 Employee stock options

F8 Other accounts receivable/payableF81 Trade credits and advancesF89 Other accounts receivable/payable

45

IMF Statistics Department

Financial instruments – Currency and maturity

Domestic currency (national currency) Foreign currency

Some instruments mix both

Important for analysis:• Exposure to exchange rate risks• Currency mismatch

46

IMF Statistics Department

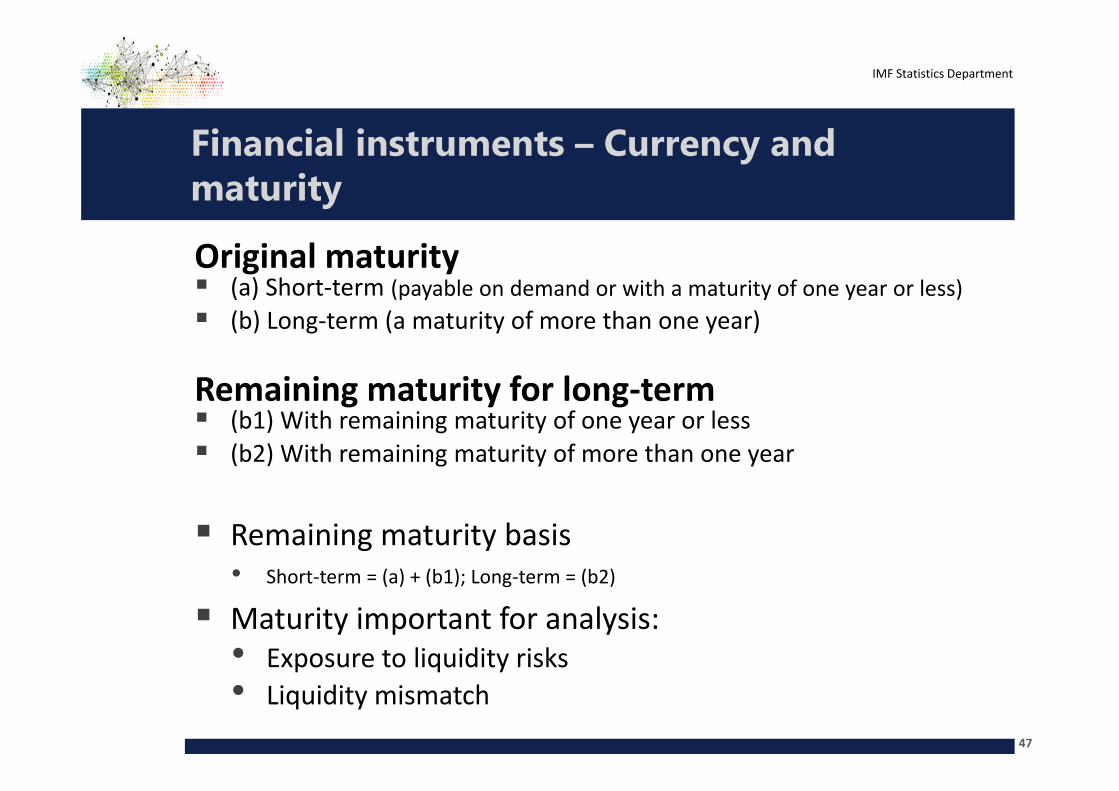

Financial instruments – Currency and maturity

Original maturity (a) Short-term (payable on demand or with a maturity of one year or less) (b) Long-term (a maturity of more than one year)

Remaining maturity for long-term (b1) With remaining maturity of one year or less (b2) With remaining maturity of more than one year

Remaining maturity basis• Short-term = (a) + (b1); Long-term = (b2)

Maturity important for analysis:• Exposure to liquidity risks• Liquidity mismatch

47

IMF Statistics Department

Aggregation

Aggregation is the simple sum of the values. The aggregation of data on financial accounts can be done both for institutional sectors and for financial assets and liabilities. • e.g.: S121 + S122 + S123 +...... +S129= S12

• F61+F62+F63+.....+F66=F6

48

IMF Statistics Department

Consolidation

Consolidation consists of eliminating transactions in financial assets and liabilities within institutional units, between institutional units in the same sub-sector, or between sub-sectors in the same sector.

Some consolidation necessary but SNA recommends compilation of non-consolidated data

Intra-entity and intra-sector consolidation• Narrow consolidation: artificial subsidiaries of same company;

different agencies of central government• Broad consolidation: the financial corporations sector• SNA recognizes that consolidated data may be useful in some

cases

49

IMF Statistics Department

Flows and stocks

Flows refer to the economic actions and effects of events during an accounting period- transactions- other flows

Stocks refer to the position in, or holding of assets and liabilities at a point in time

IMF Statistics Department

Relationship between stocks and flows

51

Transaction: Other flows:

Goods and services accountRevaluation

Other volume changesProduction account

Value added/GDP

Generation of income account Key:

Operating surplus Name of accountPrimary distribution of

income account SNA Balancing itemNational income

Secondary distribution of income account

Disposable income

Use of income accountSaving

Opening balance sheet

Closing balance sheet

Nonfinancial assets Capital account Other changes in nonfinancial assets

Nonfinancial assets

Net lending / net borrowing

Financial assets and liabilities

Financial accountOther changes in financial

assets and liabilitiesFinancial assets and

liabilitiesNet worth Net lending / net borrowing Net other changes Net worth

Arrows represent the contribution of assets to production and generation of income.

Accumulation accounts:

IMF Statistics Department

Accumulation Accounts –link flows and stocks

Capital accounts Show how goods and services (and some non-produced items) are acquired as assets or disposed of (i.e., by TRANSACTIONS)

Financial accounts Show how financial assets and liabilities are exchanged or created between institutional units and with the rest of the world (i.e., by TRANSACTIONS)

Revaluation accounts Show changes that are due only to prices, both in absolute and relative terms

Other changes in the volume of assets accounts

Show changes (flows) that are due neither to transactions nor to changes in prices

52

IMF Statistics Department

Balance Sheets: opening to closing

53

IMF Statistics Department

Valuation

For traded instruments, alternative valuations may be available

Market value is preferred in SNA definitions• Nominal value of non-traded loans and bonds includes

accrued interest• Face value is common for debtors (often called nominal value)

54

IMF Statistics Department

Valuation

Face value may occur commonly• Helpful for linking to business records• Limits of market value in crisis• May be more useful in deriving transactions

Risks of inconsistent recording between debtor and creditor

55

IMF Statistics Department

Deriving flows from stocks

From the formula, total flows can be derived from change in stocks

To calculate transactions, need to exclude • Other changes in volume (reclassifications, write-offs)• Exchange rate effects• Other price change

In practice ?

56

IMF Statistics Department

The views expressed herein are those of the author and should not necessarily be attributed to the IMF, its Executive Board, or its management

FROM-WHOM-TO- WHOM ACCOUNTS

IMF Statistics Department

Why are they needed ?

These statistics are designed for analysis of:• Spillovers• Linkages• Contagion• Vulnerability

Balance sheet in Fund Surveillance (IMF policy paper, June 2015) -- financial balance sheet from whom-to-whom

“Balance sheet analysis captures the role that financial frictions and mismatches play in creating fragility and amplifying shocks. This is key to understanding the macroeconomic outlook, identifying vulnerabilities, and tracing the transmission of potential shocks and policies.”

(more on Balance Sheets later)58

IMF Statistics Department

Key Features

Main objective is to analyze vulnerabilities of sectors and transmission mechanisms• Maturity mismatches

Between short term liabilities and longer term assets expose borrowers to rollover risk and interest rate risk Unable to finance maturing debt Differential impact on assets and liabilities depending on interest structure• Currency mismatches

Liabilities are denominated in foreign currency but assets in domestic currency

Also exchange rate risk in fixed exchange rate regimes• Capital structure mismatches Reliance on debt rather than equity to finance investment Equity provides a buffer in downturn; dividends drop with earnings Debt payments remain unchanged

IMF Statistics Department

Key Features

Key indicators of a sector’s vulnerability• Net financial position

Large negative position may indicate solvency problems, especially if leverage is high (debt as a share of total liabilities)• Net foreign currency position

Large negative position indicates vulnerability to exchange rate depreciation• Net short-term position

Large negative position indicates vulnerability to interest rate increases and rollover risk

IMF Statistics Department

From-whom-to-whom in SNA

The core accounting structure of the SNA for financial flows and positions focuses on showing who does what.

However, the underlying principles and accounting rules allow compiling and presenting financial flows and positions on a from-whom-to-whom basis, showing who does what with whom.

Sometimes called “flow of funds”

61

IMF Statistics Department

From-whom-to-whom in SNA

Chapter 27 of the 2008 SNA describes detailed flow of funds and stocks as an extension of the core accounts.

Several countries have substantial experience in or started the compilation of financial flows and positions on a from-whom-to-whom basis.• Data for at least some financial corporations

available by counterparty sector in almost all cases.

62

IMF Statistics Department

Financial Account –Sectoral Accounts + To-Whom From-Whom

Net acquisition of financial assets:

Nonfinancial corporations Financial corporations General government

Households

Rest of World Total

+NPISH

Net inc. of liabilities:S11 S12 S13 S14/S15 S2

Nonfinancial corporations 24 57 2 42 14139

Financial corporations 24 51 -8 93 13173

General government 5 26 0 42 2093

Households + NPISH 4 8 -2 11 021

Rest of World 26 30 -2 3 -57

Total 83 172 -10 191 47 483

63

IMF Statistics Department

From-whom To-whom –Add instruments

64

Households

+NPISH

Net inc. of liabilities: S11 S12 S13 S14/S15 S2

Nonfinancial corporations 24 57 2 42 14 139 Debt securities Loans Equity and investment fund shares Ins, pension and st guar schemes Financial derivatives and ESOs

Other accounts payableFinancial corporations 24 51 -8 93 13 173 Monetary gold and SDRs Currency and deposits Debt securities Loans Equity and investment fund shares Ins, pension and st guar schemes Financial derivatives and ESOs

Other accounts payableGeneral government 5 26 0 42 20 93 ……Households + NPISH 4 8 -2 11 0 21 ……Rest of World 26 30 -2 3 - 57 ……Total 83 172 -10 191 47 483 ……

0 0 0 0 0 0

Net acquisition of financial assets:

Nonfinancial corporations

Financial corporations

General government

Rest of World Total

IMF Statistics Department

From-whom To-whom –Add maturity

65

Net acquisition of financial assets:

Nonfinancial corporations

Financial corporations General government

HouseholdsRest of World Total

+NPISH

Net inc. of liabilities: S11 S12 S13 S14/S15 S2

Nonfinancial corporations 24 57 2 42 14 139

Debt securities

Short-term

Long-term

Loans

Short-term

Long-term

Equity and investment fund shares

Ins, pension and st guar schemes

Financial derivatives and ESOs

Other accounts payable

Financial corporations 24 51 -8 93 13 173

Monetary gold and SDRs

Currency and deposits

Short-term

Long-term

…..

IMF Statistics Department

From-whom To-whom –Add currency

66

Net acquisition of financial assets:

Nonfinancial corporations

Financial corporations

General government

HouseholdsRest of World Total

+NPISH

Net inc. of liabilities: S11 S12 S13 S14/S15 S2

Nonfinancial corporations 24 57 2 42 14 139

Debt securities

Short-term

Of which: Domestic currency

Long-term

Of which: Domestic currency

Loans

Short-term

Of which: Domestic currency

Long-term

Of which: Domestic currency

…..

IMF Statistics Department

From-whom To-whom Multi-dimensional

• Sectors and subsectors• Add instruments

8 main SNA instruments Plus extra detail (e.g., F5 Equity and investment shares; F511 Listed Shares,

F512 Unlisted shares, F513 Other equity F521 Money market fund shares, F522 Non-MMF investment fund shares)

• Add maturity Short-term, long-term; original or remaining

• Add currency Domestic (national)/foreign (specify euro, USD, etc.?)

• Add stocks/flows/other flows Stock or flow Stocks at point in time OR Transactions during period.

• Add time series dimension67

IMF Statistics Department

From-whom To-whom : what else ?

Can enhance further by adding country detail on Rest of the World• BIS Banking statistics • IMF Coordinated Surveys:

Portfolio Investment (CPIS) Direct Investment (CDIS)

68

IMF Statistics Department

General Other depository Other financial Nonfinancial Other resident Central bank government corporations corporations corporations sectors Nonresidents

1. SRF 1SR 1. SRF 1SR 1. SRF 1SR 1. SRF 1SR 1. SRF 1SR 1. SRF 1SRCentral bank (Liabilities) (Liabilities) (Liabilities) (Liabilities) (Liabilities) (Liabilities)

2. SRF 2SR 2. IIP(Assets) 3. JEDH

1. SRF 1SR 1. SRF 2SR 1. SRF 4SR n.a. 1/ n.a. 1/ 1. IIPGeneral (Assets) (Assets) (Assets) 2. QEDSgovernment

1. SRF 1SR 1. SRF 2SR 1. SRF 2SR 1. SRF 2SR 1. SRF 2SR 1. SRF 2SROther depository (Assets) (Liabilities) (Liabilities) (Liabilities) (Liabilities) (Liabilities)corporations 2. SRF 2SR 2. IIP

(Liabilities) 3. QEDS

1. SRF 1SR 1. SRF 4SR 1. SRF 2SR 1. SRF 4SR 1. SRF 4SR 1. SRF 4SROther financial (Assets) (Liabilities) (Assets) (Liabilities) (Liabilities) (Liabilities)corporations 2. IIP

3. QEDS

1. SRF 1SR n.a. 1/ 1. SRF 2SR 1. SRF 4SR n.a. 1. IIPNonfinancial (Assets) (Assets) (Assets) 2. QEDScorporations 3. JEDH

1. SRF 1SR n.a. 1/ 1. SRF 2SR 1. SRF 4SR n.a. 1. IIPOther resident (Assets) (Assets) (Assets) 2. CPIS 2/sectors

1. SRF 1SR 1. IIP 1. SRF 2SR 1. SRF 4SR 1. IIP 1. IIPNonresidents (Assets) 2. CPIS (Assets) (Assets) 2. CPIS 2. CPIS

2. IIP 2. IIP 2. IIP3. CPIS 3. CPIS 3. CPIS

1/ This data gap can in the future be filled with data from the public debt data template (which also covers assets) which is being piloted in some countries. 2/ CPIS data acan be used to derive other resident sector's claims as residual.

Holder of liability

(creditor)

Issuer of liability (debtor)

Combining the MFS, GFS, BOP/IIP, many parts of the framework can be filled in

IMF Statistics Department

THANKS !

70