overview of private equity in the real estate market irf conference 20 august 2013

TRANSCRIPT

Overview ofPrivate Equity inthe Real Estate

Market

IRF Conference 20 August 2013

The Basics – A Generic PE Structure

Private Equity Firm (General Partner or GP)

Limited Partner or LP (Public Pension Funds, Corporate Pension Funds, Insurance Companies,

High Net-Worth Individuals, Family Offices, Endowments, Foundations, Sovereign Wealth Funds)

Private Equity Fund (generally an LLP)

Investment Investment Investment

Fund ownership of portfolio investments

Ownership of the Fund

Fund Investment & Management

Alignment between GP and LPs

• GPs and LPs are aligned as minimum watermark IRR for LPs needs to be achieved before GP participates in the carry

• Common carry split between LPs and GPs is 80/20, and the common base fee is 2%, hence the PE jargon of “2 and 20”

• A preferred return or watermark IRR is usually determined by the sector

• In African property, the watermark IRR ranges from 8 to 10%, depending on the type of real estate fund (income vs development)

• LPs are also starting to take positions in GPs

Private Equity in South Africa

• South Africa’s Pension Funds Act was reformed in 2011, with key amendments to Regulation 28 of the Act which sets out the allocation cap for various asset classes.

• South African pension funds can now invest up to 10% of their total assets in private equity subject to limitations (an increase from previous allocation caps of 2.5%)

• Over the last year total PE funds under management increased by 10% to over R126.4 billion, but pension funds are slow on the uptake.1

• As at 2012, it is estimated that despite considerable GEPF investments, less than 1% of South African pension fund assets under management (“AUM”) was invested in private equity.2

1 South African Venture Capital Association

2 E. Pickworth (2012) “Pension fund ‘missing out on private equity”, Business Day (South Africa), 11 September 2012

Private Equity Concerns Allayed: Swensen and Markowitz

• Liquidity concern regarding PE is perhaps a red-herring in the context of pension funds. It is relevant only when issues of short-term solvency are to be considered. Is this a material consideration for pension funds, which have long-term liabilities and thus logically should also be adopting long-term investment strategies?

• Other asset classes are not in fact nearly so illiquid as they may at first appear. There is a thriving secondary market for private equity partnership interests. Property, certainly prime property in a prime location, is always saleable.

• Property, as an “alternative” asset pre-dates quoted equities as an investment by at least 2,000 years.

• Legally defined liquidity creates the ability to convert securities into cash at a moment's notice is naïve and unsound. Many investors on Black Monday were unable to sell even FTSE100 shares as the demand for dealing capacity simply overwhelmed the system. Trading in large blocks of listed equities is not as liquid as imagined.

• There is a tendency among trustees and consultants alike to regard “illiquid” and “alternative” assets as the same, and it seems followers of “alternative” assets might be compared to the original protestants who brought about the Reformation.

Private Equity Funds looking for a homeGPs stockpiled with dry powder fuelling deal demand

Source: Bain and Company

Funds on the road and capital split by fund type in 2012

Source: Bain and Company

PE versus other Asset Classes:Developed Markets

Note: Data based on review of public pension funds in North America and EuropeSource: Bain and Company

Median returns for public pension funds by asset class, 10 year horizon IRR, June 2012

What Emerging Market Investors are saying…

LPs planning to begin or expand investment in Select Emerging Markets by Institution Type

Investors in Private Equity

Source: Emerging Markets Private Equity Association LP Survey 2013

Investors in Private Equity – Views on Africa

The Attractiveness of Emerging Markets for GP Investment Over the Next 12 Months – LP Views Overall Ranking 2013 2012 2011Sub-Saharan Africa 1 5 7Southeast Asia* 2 4 2=Latin America (ex-Brazil) 3 1 4China 4 3 2=Turkey 5 7 6Brazil 6 2 1Central and Eastern Europe 7 10 8Russia/CIS 8 8 10India 9 6 5Middle East and North Africa 10 9 9*Classified as “Other Emerging Asia” in 2011 and 2012

• Sub-Saharan Africa for the first time leads a new tier of Emerging Markets, for the first time, jumping from 5th place in 2012

• Displaced BRICs as most attractive • First time In the EMPEA survey’s nine-year history, none of the BRIC markets

broke the top three.

Why we like Africa...

Large consumer marketHome to more than 1 billion people

1 dot = 100,000 people

Source: Market Decisions

• Fast growing economies, underpinned by domestic consumption

• CAGR in consumption of 11.4% over the next three years1

• Increased urbanisation, 47% of Africans will live in cities by 20251

• Emerging middle class; 95% of the market currently informal; 20% of the market to be formal by 20302

1 United Nations Human Settlements Programme (UN-HABITAT) 2 BofA Merrill Lynch Global Research

Africa continues to riseFDI has grown considerably over the last decade

• FDI in SSA has grown to 5.6% of world FDI over the past five years• South Africa invested over US$ 800 million in SSA during 20121

1 Real Capital Analytics

0

1

2

3

4

5

6

7

8

%y/y

Sub-Saharan Africa real GDP growth

Source: STANLIB Research

1.8

2.0

2.2

2.4

2.6

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

% of world GDP, PPP

Sub-Saharan Africa percentage of World GDP

Source: STANLIB Research

-20

-15

-10

-5

0

5

10

15

20

25

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

$ billion

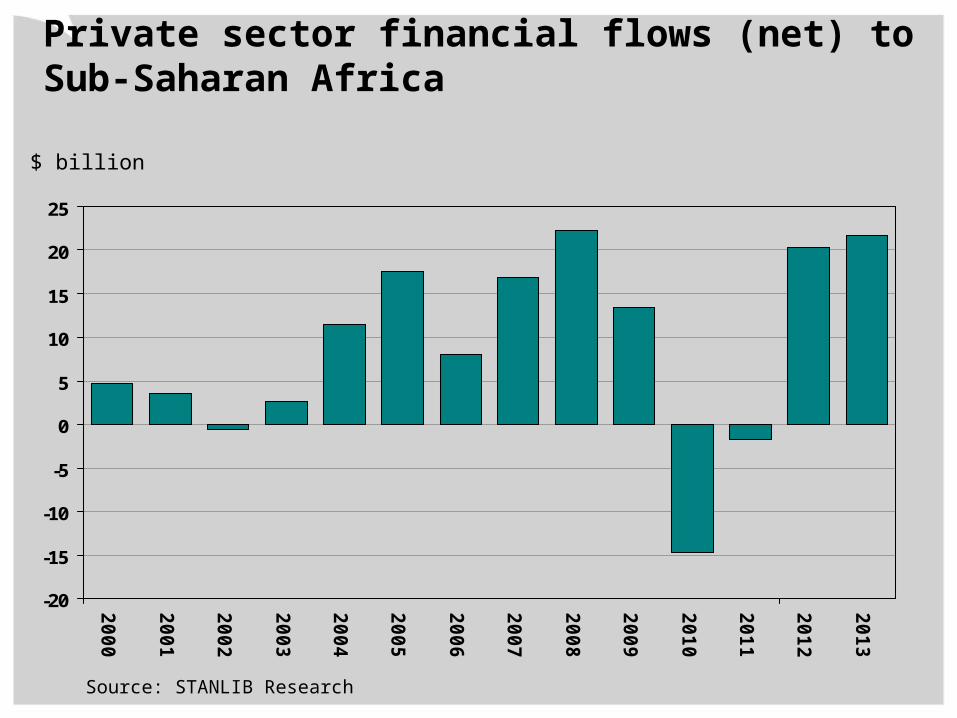

Private sector financial flows (net) to Sub-Saharan Africa

Source: STANLIB Research

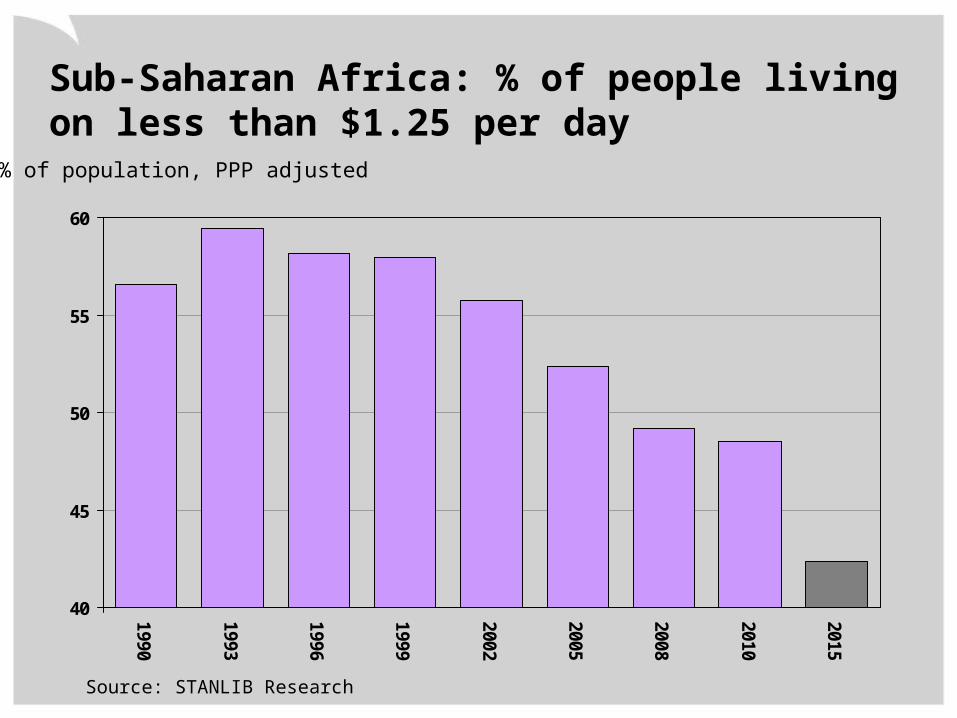

40

45

50

55

60

1990

1993

1996

1999

2002

2005

2008

2010

2015

% of population, PPP adjusted

Sub-Saharan Africa: % of people living on less than $1.25 per day

Source: STANLIB Research

RISING STRIVER PROFILE- 27 year old father of 2- Thriving taxi business- Lives in city centre and has a car- Most of income on household needs + a new smartphone + drink after work

Aspirational consumer market

Growing consumer expenditure

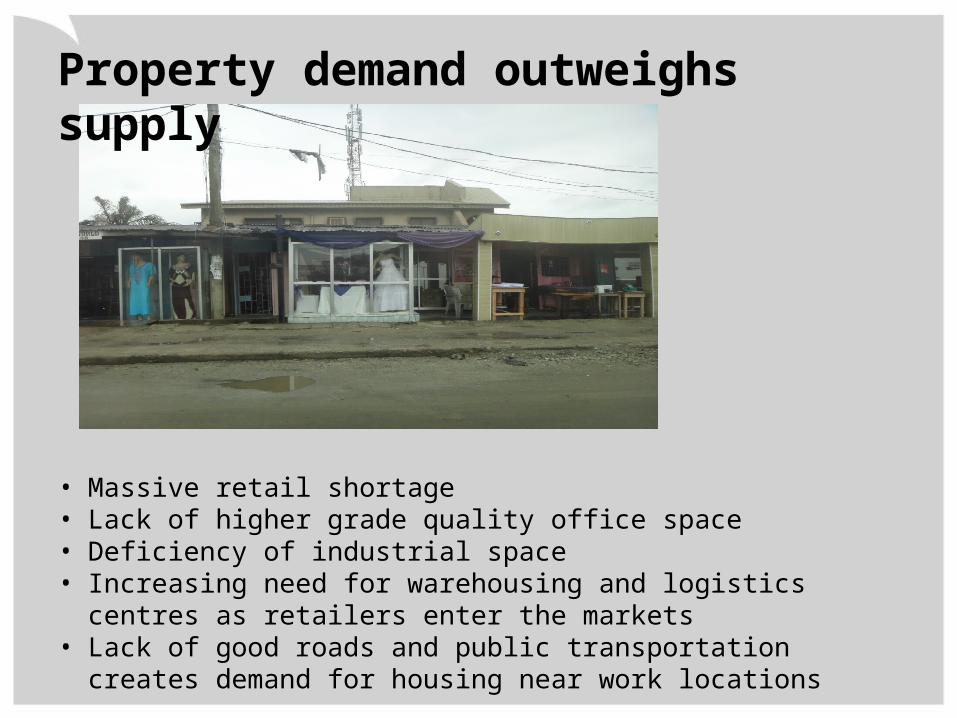

African Property Fundamentals…

• Massive retail shortage• Lack of higher grade quality office space• Deficiency of industrial space• Increasing need for warehousing and logistics centres as retailers enter the

markets• Lack of good roads and public transportation creates demand for housing

near work locations

Property demand outweighs supply

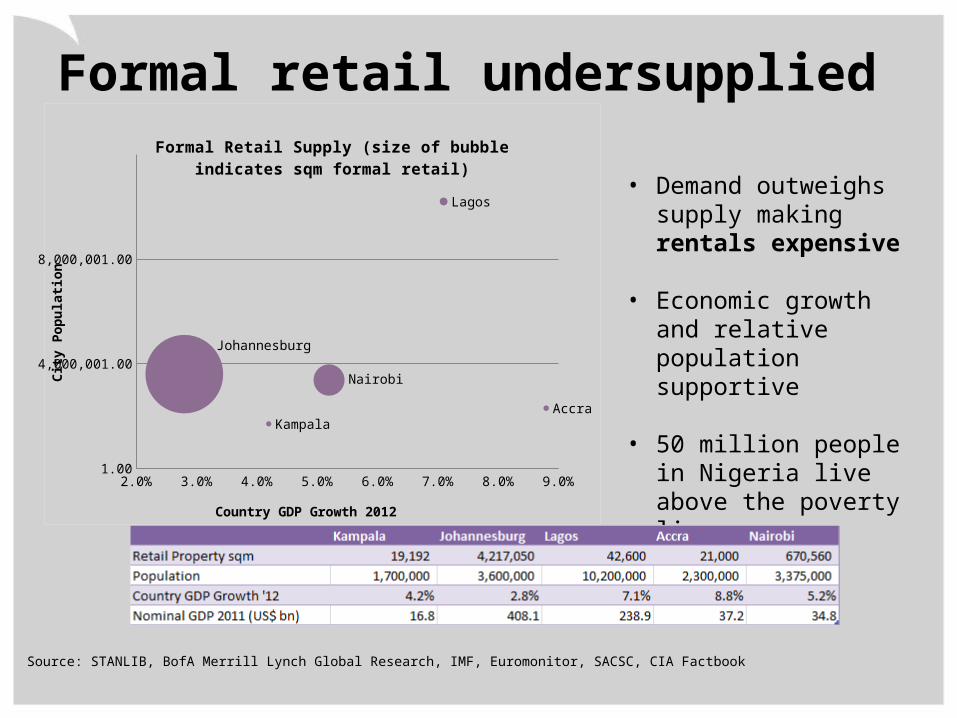

Property fundamentals are strongAn opportunity for further 3 million m2 of retail in Lagos

Source: BofA Merrill Lynch Global Research, IMF, Euromonitor, SACSC, CIA Factbook

• Johannesburg: 4,200,000m2 formal retail & 3.6 million people

• Lagos: 42,000m2 formal retail & 10.2 million people

City m² : people

Johannesburg > 1 m² per capita

Lagos 0.005m² per capita

City m² : people

Johannesburg >1m² per capita

Lagos 0.2m² per capita

and if 1 person’s spending power in Johannesburg equals 4 people’s spending power in Lagos

This represents an opportunity to develop up to 3,000,000m2 of formal retail property in Lagos.

Formal retail undersupplied

Source: STANLIB, BofA Merrill Lynch Global Research, IMF, Euromonitor, SACSC, CIA Factbook

• Demand outweighs supply making rentals expensive

• Economic growth and relative population supportive

• 50 million people in Nigeria live above the poverty line

2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0%

1.00

4,000,001.00

8,000,001.00

Kampala

Johannesburg

Lagos

Accra

Nairobi

Formal Retail Supply (size of bubble indicates sqm formal retail)

Country GDP Growth 2012

City

Pop

ulati

on

Sound underlying drivers of return

Source: Knight Frank, Africa Report 2013STANLIB Research

• Average Regional retail rentals / m²• Lagos $65 Nairobi $31• Accra $45 Johannesburg $45

• Average High grade office rentals / m²• Lagos $85 Nairobi $15• Accra $40 Johannesburg $20

• Average yields are in the region of 11 – 14%;

• Targeted IRR’s (10 year) are between 20 – 25%

• Good risk-adjusted returns

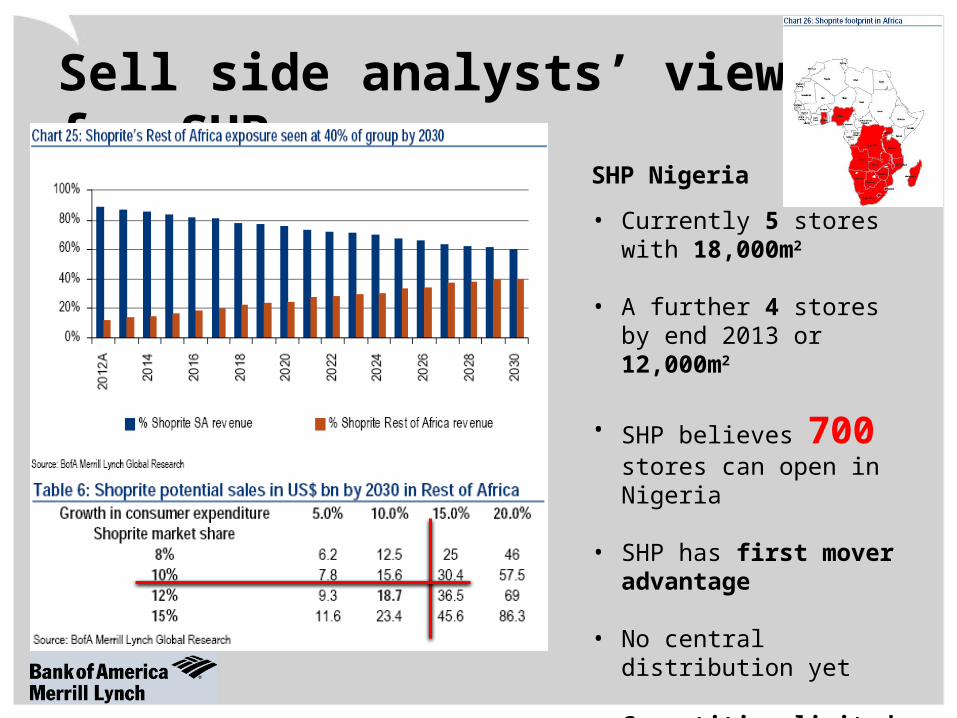

Sell side analysts’ view for SHP

SHP Nigeria

• Currently 5 stores with 18,000m2

• A further 4 stores by end 2013 or 12,000m2

• SHP believes 700 stores can open in Nigeria

• SHP has first mover advantage

• No central distribution yet

• Competition limited with 95% of the market still informal

Private Equity in Property Development: a different type of investment

• Spend time on the ground walking the streets

• Develop partnerships with long term local developers

• Entrench in the economic environment

• Long – term sustainable, responsible investing

• Take time to understand how things work

Recognise the Opportunities

but alsoRecognise the

Risks

Opportunities are bright, but challenges remainAfrica clustered toward the bottom of global rankings

• The World Bank recognises progress made by African countries since its first listing in 2005

• African countries have a long way to go

Long list of risks to be considered

• Buckets of Risk to Manage

Country• Political risk• Bribery and corruption • Bleak international perception

Currency and Interest Rates• Currency risk• Rental payments in local currency• Interest rate and tenor risk

Operating Environment• Lack of infrastructure• Credibility of partners• Lack of available debt funding

Legal Environment• Inefficient policies• Tax risk• Legal and contracting risks

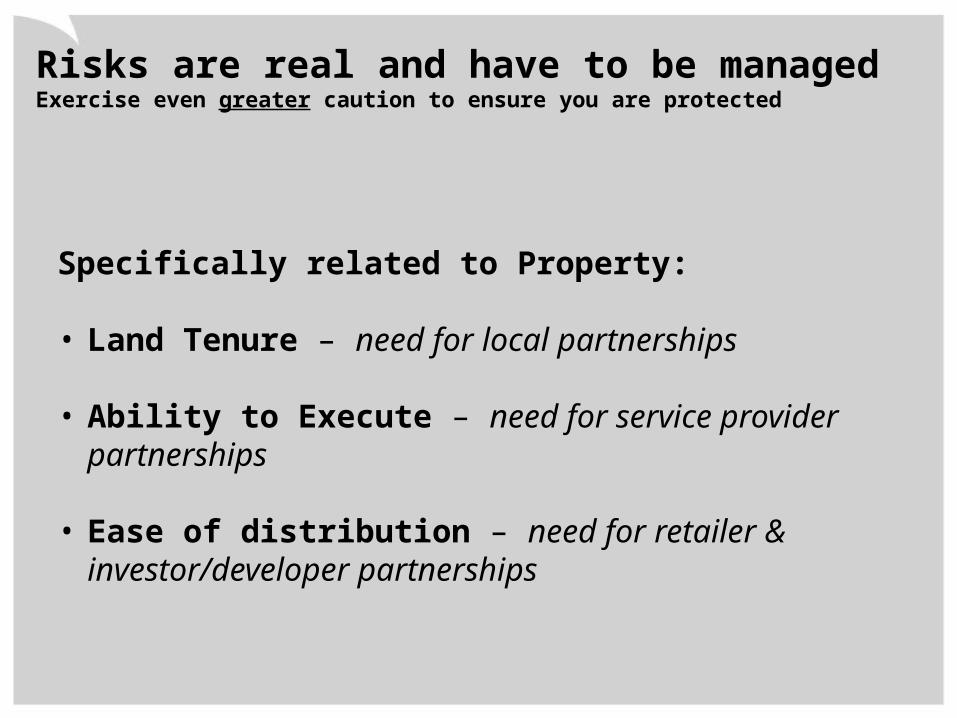

Risks are real and have to be managedExercise even greater caution to ensure you are protected

Specifically related to Property:

• Land Tenure – need for local partnerships

• Ability to Execute – need for service provider partnerships

• Ease of distribution – need for retailer & investor/developer partnerships

We need to take action

• Perspective: assuming a glass-half-full perspective that focuses first on opportunity, and only then on the risks that need to be managed

• Partnerships: investing in building strong collaborative partnerships across government, business and communities and with each other

• Planning: adopting careful long-term planning, and patience; persistence and flexibility in implementing those plans

• People: nurturing and developing Africa's human talent: arguably the continent’s greatest resource

Embracing Africa’s diversity unlocks opportunities

Source ERNST & YOUNG Business in Africa Survey

STANLIB Africa Direct Property Development

Fund

(“SADPDF”)

The Fund1. Scope

Stage of development Greenfield, brownfield, land acquisition, early development phase

Geographic focus Sub Sahara Africa (excluding CMA), with a key focus on Nigeria, Ghana, Kenya, and Uganda

Property segment Retail (60%-80%) and other commercial assets (20%-40%)

Project involvement Land acquisition, concept design/management, project management (construction), portfolio management (leasing, maintenance)

2. Role and Nature of Investments

Size range of investment $15 - $ 30 million

Where in capital structure Land owner (10-25%) / Fund equity (25-40%) / quasi equity (10-15%) / Senior debt (50-65%)

Targeted return profile 22-25% IRR (nominal gross)

Hurdle rate / Preferred return 10% IRR

Level of control Varied, but select reserved matters for Fund at shareholder level

Maximum deal size No more than 33% of the total Fund capital ($50 million)

Partnerships Local institutions (land access), SA retailers, private equity funds (e.g. Actis)

3. Fund scale and Structure

Size $150 million (4-6 projects)

Duration 4 year investment period, 4 year harvesting period (with a two year extension option)

Domicile Mauritius

Co-investment allowed Allowed for select investors

Minimum ticket size $5 million

Fees charged 1.5% (25% discount charged to usual rate)

Disclaimer

Information and Content

The information and content (collectively 'information') provided herein are provided by STANLIB Asset Management (“STANLIBAM”) as general information for information purposes only. STANLIB does not guarantee the suitability or potential value of any information or particular investment source. Any information herein is not intended nor does it constitute financial, tax, legal, investment, or other advice. Before making any decision or taking any action regarding your finances, you should consult a qualified Financial Adviser. Nothing contained herein constitutes a solicitation, recommendation, endorsement or offer by STANLIBAM.

Copyright

The information provided herein are the possession of STANLIBAM and are protected by copyright and intellectual property laws. The information may not be reproduced or distributed without the explicit consent of STANLIBAM.

Disclaimer

STANLIB has taken care to ensure that all information provided herein is true and accurate. STANLIB will therefore not be held responsible for any inaccuracies in the information herein. STANLIBAM shall not be responsible and disclaims all loss, liability or expense of any nature whatsoever which may be attributable (directly, indirectly or consequentially) to the use of the information provided.

STANLIB Asset Management LimitedRegistration No: 1969/002753/06. A Financial Services Provider licensed under the Financial Advisory and Intermediary Services Act, 37 of 2002. FSP license No: 719.