overview of private equity & venture capital in brazil breakfast seminar new york – november...

TRANSCRIPT

Overview of Private Equity & Venture Capital in BrazilOverview of Private Equity & Venture Capital in Brazil

Breakfast SeminarBreakfast Seminar

New York – November 2008New York – November 2008

Luiz Eugenio Junqueira Figueiredo, Chairman ABVCAPLuiz Eugenio Junqueira Figueiredo, Chairman ABVCAP

22

I. ABVCAP

II. PE&VC – Economic Importance

III. Brazil: An Enabling Environment

IV. Brazilian PE&VC Industry

V. Conclusions

AgendaAgenda

33

ABVCAPABVCAP

• The Association of the Brazilian PE & VC industryThe Association of the Brazilian PE & VC industryWho Are WeWho Are We

Our MissionOur Mission

MembershipMembership

• Promote and develop long-term investments in BrazilPromote and develop long-term investments in Brazil

• 100+ including PE & VC managers, LPs, invested 100+ including PE & VC managers, LPs, invested companies and service providerscompanies and service providers

PE&VC Economic Importance - USAPE&VC Economic Importance - USA

Fonte: NVCA

44

Fonte: NVCA

55

PE&VC Economic Importance - USAPE&VC Economic Importance - USA

66Source: Monitor Analysis

Brazil: An Enabling Environment….. Brazil: An Enabling Environment…..

AttractiveInvestment

Opportunities

Viable ExitOptions

Favorable Macroeconomics

DevelopedInstitutional &

RegulatoryLandscape

DevelopedCapital Markets

World-ClassCorporate

Governance

QualifiedHuman

Resources

77

Internal Debt and Interest Rates

Slow legal system

Limited funds for

PE & VC

Some companies still reluctant to good Corporate

Governance

Labor laws

……..with typical challenges of emerging markets ..with typical challenges of emerging markets

88

Investment Grade Stable economy de-linked from politicsFalling interest rates and country-riskSocial inclusion of low-income families

Source: BACEN; Social Security Ministry; IBGE ; CVM; Interviews with PE / VC specialists; BOVESPA; ANBID; BEST

Favorable Favorable MacroeconomicsMacroeconomics

Enabling Environment….. Enabling Environment…..

99

Improvement in the recent years, today Brazil is stronger and less vulnerable to external crises.

• Investment Grade• GDP growth;• Inflation down, interest rates falling and trade surplus;• International reserves are increasing and FDI is growing;• Still needed adjustment of public accounts;• Important legal and tax system reforms under discussion;• The Federal Program, PAC (Growth Acceleration Plan), which projects to

invest more than US$ 250 billion in the infrastructure sector in the next 5 years;

Enabling Environment….. Enabling Environment…..

Favorable Macroeconomics

1010

Source: Social Security Ministry; CVM; Interviews; BOVESPA; Monitor Analysis

Pension Funds Assets represents 16% of Brazilian GDP (2005)

Alternative Investments mixed within the Equity and Real Estate classes

Pension Funds may allocate up to 20% of total assets to alternative investments

SPC Regulatory Review

Pension Funds Assets (US$ billion)Pension Funds Assets (US$ billion)

Developed Developed Capital MarketsCapital Markets

Enabling Environment….. Enabling Environment…..

1111

• Stock Exchange

• Regulation

• Private Institution

World-ClassWorld-Class

Corporate GovernanceCorporate Governance

Enabling Environment….. Enabling Environment…..

1212

Source: BOVESPA; CVM; Brazilian Institute for Corporate Governance (IBGC)

Stock Stock ExchangeExchange

Brazilian Securities & Exchange

Commission

Brazilian Institute for Corporate

Governance

Established in 1995 by demand from the market

Develops and Recommends CG programs

Advanced regulation on disclosure and shareholders’ rights = Public Companies and PE & VC Funds

Most restrictive levels of CG represents 60% of the Market Cap and Daily VolumeMost restrictive levels of CG represents 60% of the Market Cap and Daily Volume

3 levels of world-class

corporate governance

standards (1, 2 and ‘Novo

Mercado’)

‘‘Novo Mercado’Novo Mercado’

Highest Corporate Governance requirements in BOVESPA

Information disclosure and standards– IFRS or US GAAP

Protection to minority shareholders– 100% tag along– All stocks with voting rights– Minimum free float: 25%

Mandatory use of arbitration

Enabling Environment….. Enabling Environment…..

World Class CG

1313

Developed Institutional & Developed Institutional & Regulatory LandscapeRegulatory Landscape

Enabling Environment….. Enabling Environment…..

• Independent Institutions

• Legal System

• Financial Market Structure

• Coordinated Public and Private Efforts

1414

Source: ANBID; Bacen; BEST 2006; Brazilian Company for Custody and Liquidity (CBLC); CVMNote: *Except countries considered tax havens by Brazilian Tax Authority

Legislation for investors fully reviewed (1999 / 2000)– Reduced legal and credit risk for investors– New “Bankruptcy Law” made investments safer

Favorable tax regime* for foreigner investors

Independent Independent InstitutionsInstitutions

Legal SystemLegal System

Financial Market Financial Market StructureStructure

Solid and safe financial infrastructure: around 2,500 institutions Electronic payments system – compliance with BIS Brazil follows all 20 recommendations of G30 regarding custody,

settlement, payments system and data security

Central Bank and Securities Commission are autonomous Stock and Futures Exchanges are listed

Enabling Environment….. Enabling Environment…..

Developed Institutional & Regulatory Landscape

Coordinated Public Coordinated Public and Private Effortsand Private Efforts

Fostering innovation and industrial development FINEP – Inovar Program BNDES – focused PE/VC department ABDI/MDIC – Productive Development Police (PDP)

1515

• Experienced and skilled Fund Managers

• Wide availability of qualified Managers and other personnel for Portfolio Companies

QualifiedQualified

Human ResourcesHuman Resources

Enabling Environment….. Enabling Environment…..

1616

Source: ANBID; MCT; IBGC; FGV; Monitor Analysis

Financial Mkt / Auditor

High Executive

Consultant

Entrepreneur

Other

Extension

Graduate

PhD >20 yrs

>15 yrs

>10 yrs

>5 yrs

High School

Undergrad

Enabling Environment….. Enabling Environment…..

Qualified Human Resources

1717Source: Monitor Analysis

The Enabling Environment in BrazilThe Enabling Environment in Brazil

AttractiveInvestment

Opportunities

Viable ExitOptions

Favorable Macroeconomics

DevelopedInstitutional &

RegulatoryLandscape

DevelopedCapital Markets

World-ClassCorporate

Governance

QualifiedHuman

Resources

1818

Attractive Investment OpportunitiesAttractive Investment Opportunities

Source: MCT; Merrill Lynch; IBGE; Global Entrepreneurship Monitor; IDG; Monitor Analysis* US$ constant 2000

SectorsSectorsRegional GrowthRegional Growth

-4

-2

0

2

4

6

8

10

12

14

0.1 1 10 100 1000

GNP

(%)

GNP (US$BB*) – logarithmic scale

DF

SE

TOGO

MT

MS

PAMA

AM

SC

ES

RSBA

PR

MG

RJ

SP

Infrastructure - US$ 30 billion need

Real Estate – Housing Deficit 8 million

IT - US$ 19 billion in 2007 – IDG

Biotechnology

Tourism

Telecom

Retail

Agribusiness– Biomass– Ethanol - 26 billion liter by 2010– Green Beef– Grains– Arable land and favorable conditions

1919

Viable Exit OptionsViable Exit Options

9%

242%

199%

40%

38%

36%

26%

22%

481%

Construction

Energy

Sector

Airline

IT

Medical Services

E-commerce

Airline

Logistics

Car rental

Time to Exit

2 years

1 year

<1 year

5 years

6 years

9 years

8 years

7 years

8 years

Net Revenues 2005 (US$ million)

273

1,100

90

217

172

202

2,317

70

350

Equatorial

Company

GOL

TOTVS1

DASA

Submarino

Gafisa

TAM

ALL

Localiza

Investment (US$ million)

11

26

16

100

83

78

77

202

49

12%

130%

32%

20%

IT

Logistics

Telecom

IT

4 years

7 years

4 years

6 years

n/a

137

353

n/a

Akwan

Autotrac

Atrium

Microsiga2

n/a

2,5

20,5

7

IPO

sIP

Os

Tra

de-

Sal

eT

rad

e-S

ale

Estimated IRRs in US$

Source: Press Clippings; Company websites; Interviews; Monitor Analysis;Brazilian Capital Markets and Private Equity (R. Freitas, P. Passoni); Note: 1 BNDESPar; 2) Buyback; 3) 2004

2020

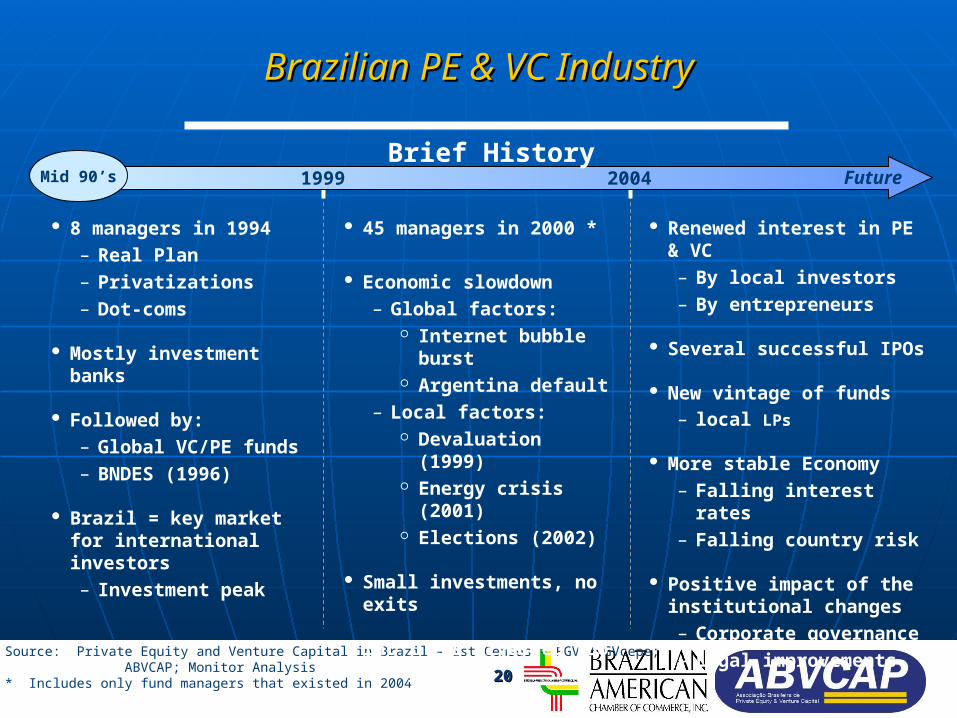

Source: Private Equity and Venture Capital in Brazil – 1st Census – FGV / GVcepe; ABVCAP; Monitor Analysis* Includes only fund managers that existed in 2004

1999 Future

8 managers in 1994– Real Plan– Privatizations– Dot-coms

Mostly investment banks

Followed by:– Global VC/PE funds– BNDES (1996)

Brazil = key market for international investors– Investment peak

45 managers in 2000 *

Economic slowdown– Global factors:

Internet bubble burst Argentina default

– Local factors: Devaluation (1999) Energy crisis (2001) Elections (2002)

Small investments, no exits

Int’l LPs divested too early

Improvements in legislation and corporate governance

Renewed interest in PE & VC– By local investors– By entrepreneurs

Several successful IPOs

New vintage of funds– local LPs

More stable Economy– Falling interest rates– Falling country risk

Positive impact of the institutional changes– Corporate governance– Legal improvements

2004Mid 90’s

Brazilian PE & VC IndustryBrazilian PE & VC Industry

Brief History

2121

Limited PartnersLimited Partners

General PartnersGeneral Partners

CompaniesCompanies

• US$ 16,72 billion of committed capital (Jul/07)

• 89 PE&VC firms• 153 funds• 984 professionals (357 partners)

• 404 portfolio companies• 194 new investments between 2004 and 2007• 28 IPOs between 2004 and 2007

Brazilian PE & VC IndustryBrazilian PE & VC Industry

Main Figures

2222

Brazilian PE & VC IndustryBrazilian PE & VC Industry

Impressive Recent Growth

Source: GV-CEPE

2323

Brazilian PE & VC IndustryBrazilian PE & VC Industry

Surprising updated figures

to be released in two weeks

2424

Brazilian PE & VC IndustryBrazilian PE & VC Industry

Attractive Pos-IPO Performance

Source: GV-CEPE

2525

Brazilian PE & VC IndustryBrazilian PE & VC Industry

Well Positioned

Source: LAVCA

2626

an enabling an enabling environment for PE&VC environment for PE&VC

with sound investment with sound investment opportunitiesopportunities

• Favorable Macroeconomics• Developed Capital Markets• World Class Corporate Governance• Developed Institutional & Regulatory Landscape• Qualified Human Resources

• In different regions • Across different sectors • Consolidation of fragmented sectors• Distressed assets• Economic inclusion

and viable exitsand viable exits• IPO• Trade Sale• at attractive returns

ConclusionConclusion

Brazil offers

Thank You !

Luiz Eugenio Junqueira FigueiredoLuiz Eugenio Junqueira FigueiredoChairman Associação Brasileira de Private Equity & Venture Capital

www.abvcap.com.br