overview of the system of accounts - … or... · web viewoverview of the system of national...

TRANSCRIPT

OVERVIEW OF THE SYSTEM OF NATIONAL ACCOUNTS(CHAPTER 1 OF THE ESA 2010 GNI INVENTORY)

LUXEMBOURG201

following the agreed recommendations as laid down in document GNIC/280 rev. 2 EN - "ESA2010 GNI Inventory Guide".

VERSION JUNE 2016

LUXEMBOURG

GROSS NATIONAL INCOME INVENTORY

ESA 2010

1st editionJune 2016

CHAPTER 1: OVERVIEW OF THE SYSTEM OF ACCOUNTS....................................................17

1.1 Introduction..................................................................................................................................................171.1.1 Organisation and responsibilities within the National Statistical Institute (NSI)...................................171.1.2 Supervisory and control system..............................................................................................................17

1.1.2.1 National accounts compilation process..............................................................................................181.1.2.2 Graph of data flow (GOD).................................................................................................................181.1.2.3 Version analysis and backups.............................................................................................................201.1.2.4 « Doors » and « GateKeeper » applications.......................................................................................201.1.2.5 « MASTER » application for supply and use balancing....................................................................21

1.1.3 Source data.............................................................................................................................................221.1.4 Formal control and supervision instruments..........................................................................................22

1.1.4.1 Quality reports....................................................................................................................................221.1.4.2 Audits.................................................................................................................................................221.1.4.3 Data flow inventory (DFI)..................................................................................................................23

1.1.5 Organisation and management...............................................................................................................231.1.6 Main approaches used............................................................................................................................231.1.7 Geographical coverage...........................................................................................................................24

1.2 Revisions policy and timetable for revising and finalising the estimates................................................24

1.3 Outline of the production approach...........................................................................................................251.3.1 Reference framework.............................................................................................................................251.3.2 Main data sources...................................................................................................................................271.3.3 Calculation of gross value added and Gross Domestic Product.............................................................291.3.4 The role of direct and indirect estimation methods and of benchmarks and extrapolation....................301.3.5 Independence of the different approaches to GDP.................................................................................311.3.6 Main compilation steps of the production approach..............................................................................311.3.7 Exhaustiveness.......................................................................................................................................32

1.3.7.1 Business register (Répertoire des entreprises)....................................................................................321.3.7.2 Rectifications on the basis of tax audits (VAT fraud)........................................................................321.3.7.3 Tips.....................................................................................................................................................321.3.7.4 Undeclared work................................................................................................................................331.3.7.5 Representatives of foreign companies................................................................................................331.3.7.6 Illegal activities..................................................................................................................................33

1.4 Outline of the income approach..................................................................................................................351.4.1 Reference framework.............................................................................................................................351.4.2 Main data sources...................................................................................................................................351.4.3 Compensation of employees...................................................................................................................361.4.4 Other taxes on production......................................................................................................................371.4.5 Other subsidies on production................................................................................................................371.4.6 Gross operating surplus and mixed income............................................................................................371.4.7 Consumption of fixed capital.................................................................................................................371.4.8 Main approaches taken with respect to exhaustiveness.........................................................................37

1.5 Outline of the expenditure approach..........................................................................................................381.5.1 Reference framework.............................................................................................................................381.5.2 Households’ final consumption expenditure..........................................................................................391.5.3 NPISH final consumption expenditure...................................................................................................411.5.4 Government final consumption expenditure..........................................................................................421.5.5 Gross capital formation..........................................................................................................................44

1.5.5.1 Gross fixed capital formation.............................................................................................................441.5.5.1.1 Data validation.............................................................................................................................461.5.5.1.2 Adjustment for exhaustiveness....................................................................................................461.5.5.1.3 Conceptual adjustments...............................................................................................................46

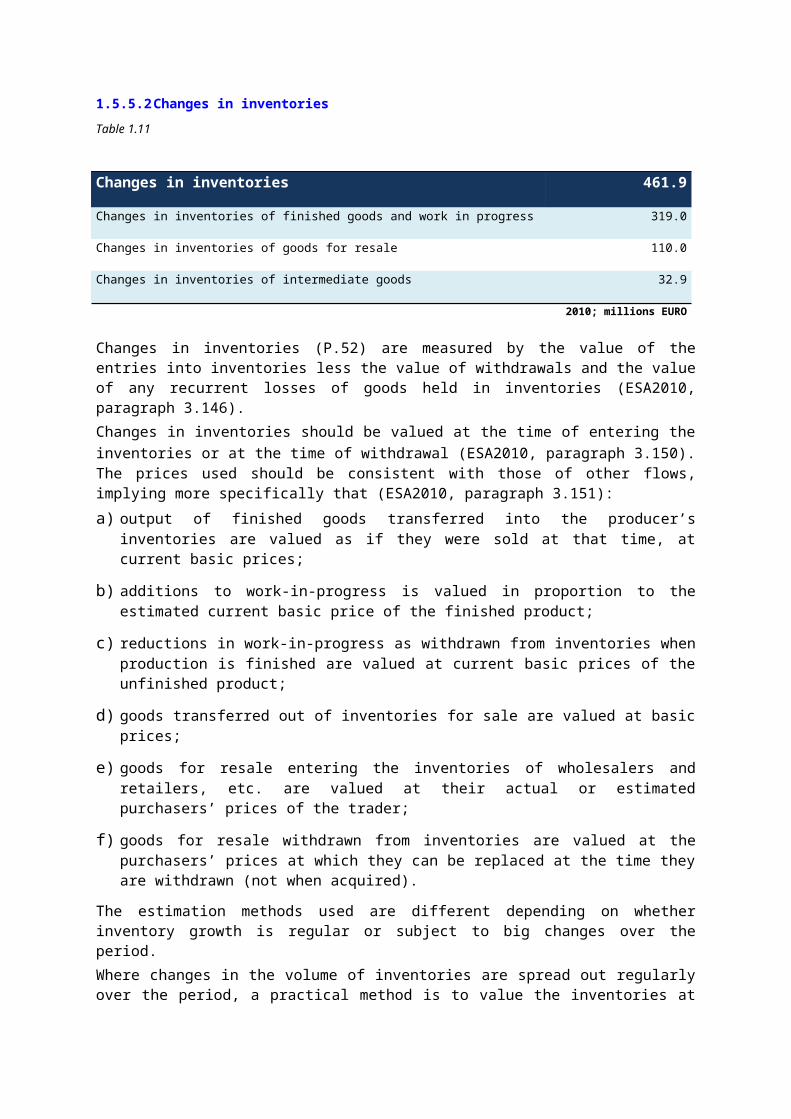

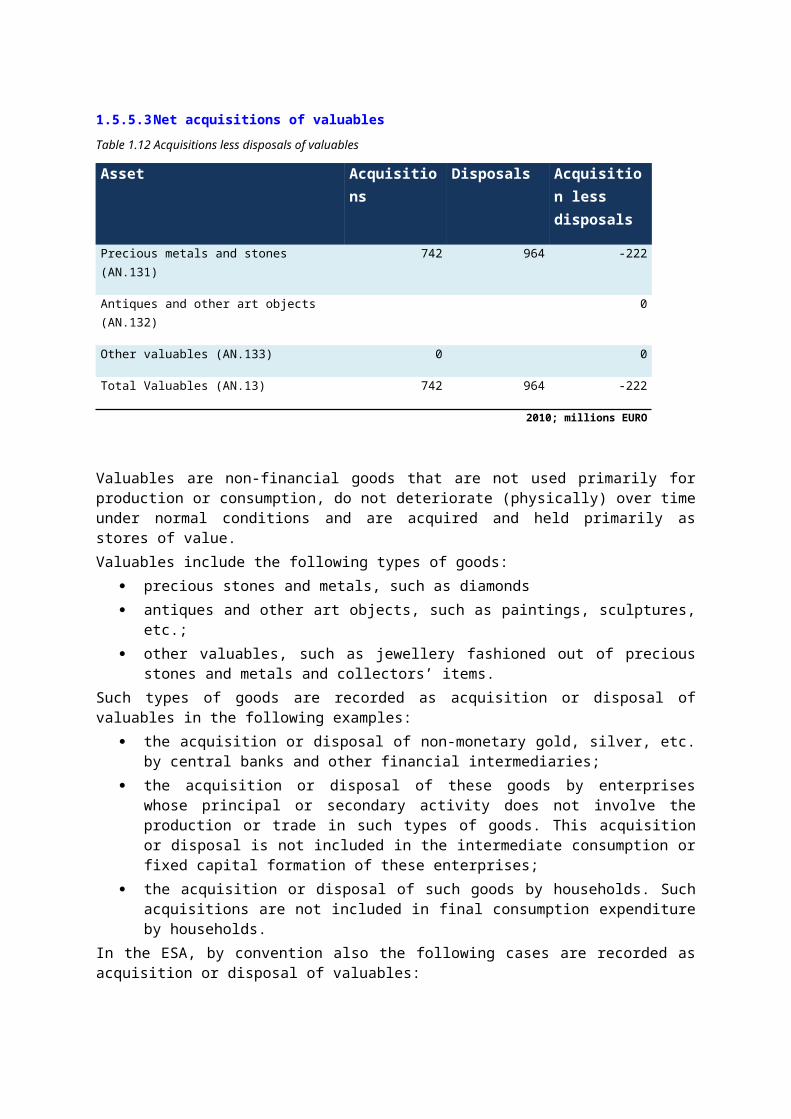

1.5.5.1.4 Balancing......................................................................................................................................471.5.5.2 Changes in inventories.......................................................................................................................471.5.5.3 Net acquisitions of valuables..............................................................................................................48

1.5.6 Exports and imports of goods.................................................................................................................491.5.7 Exports and imports of services.............................................................................................................521.5.8 Main approaches taken with respect to exhaustiveness.........................................................................54

1.6 The balancing or integration procedure, and main approaches to validation.......................................54

1.7 Overview of the allowances for exhaustiveness.........................................................................................561.7.1 Production approach...............................................................................................................................56

1.7.1.1 Statistical register of businesses and legal persons............................................................................561.7.1.2 Rectifications on the basis of tax audits (VAT fraud)........................................................................561.7.1.3 Tips.....................................................................................................................................................561.7.1.4 Undeclared work................................................................................................................................571.7.1.5 Representatives of foreign companies................................................................................................571.7.1.6 Illegal activities..................................................................................................................................57

1.8 The transition from GDP to GNI................................................................................................................591.8.1 Compensation of employees (D.1).........................................................................................................591.8.2 Taxes on production and imports paid to the Institutions of the EU and subsidies granted..................601.8.3 Property income (D.4)............................................................................................................................60

1.9 Main classifications used..............................................................................................................................61

1.10 Main data sources used................................................................................................................................611.10.1 Production approach...............................................................................................................................611.10.2 Expenditure approach............................................................................................................................621.10.3 Statistical surveys and other data sources used for the income approach..............................................631.10.4 Statistical surveys and other sources used for the transition from GDP to GNI....................................63

CHAPTER 1: OVERVIEW OF THE SYSTEM OF ACCOUNTS

1.1 Introduction

This inventory describes the sources and methods used for the compilation of gross domestic product (GDP), gross national income (GNI) and other national accounts main aggregates at current prices for Luxembourg. National Accounts are compiled according to the ESA 2010 methodology as laid out in Annex A of regulation (EU) No 549/2013.

1.1.1 Organisation and responsibilities within the National Statistical Institute (NSI)Compiling the national accounts is the responsibility of the National Institute of statistics and economic studies of the Grand Duchy of Luxembourg ( Institut national de la statistique et des études économiques du Grand-Duché de Luxembourg (STATEC)). Article 2 (2) of the Law of the 10th of July 2011 on the organisation of the National Institute for Statistics and Economic Studies states that “STATEC’s remit is ... to draw up national, global or sectoral accounts”. By the terms of the convention of the 18th of December 2009, STATEC collaborates with the Central bank of Luxembourg (BCL) for the compilation of the financial sector accounts. Nevertheless STATEC has the full responsibility for the transmission to Eurostat of the financial sector accounts tables of the ESA 2010 transmission program.STATEC is placed under the authority of the Minister of the Economy and is, in administrative terms, an integral part of the Ministry. However the law of the 10th of July 2011 assures through article 11 that “In carrying out its remit … STATEC is endowed with scientific and professional independence. The director of STATEC decides on the statistical methods, standards and procedures as well as on the content and the date of dissemination of the statistical publications. …Statistics are drawn up and statistical sources and techniques are chosen according to statistical considerations.” Thus STATEC has full scientific independance. Within STATEC, units “MAC1 – National Accounts”, “MAC2 - Sector accounts “, and “MAC4 - General government accounts” located inside Division MAC – “Macroeconomic statistics”, are in charge of compiling the annual and quarterly national accounts (see the organisation chart). Unit MAC1 has currently a statff of 7.5 permanent full time equivalent persons. For MAC2 there are 6.5, and for MAC4 4. This makes a total of 18, of which 16 have a university degree, most of them in economics or business administration. Currently there are also 2 external experts with medium term contracts.STATEC’s small size (199 staff members in total) allows its various divisions and units to cooperate closely in providing basic statistics, in developing methodologies and questionnaires, and in providing direct access to specific pieces of information.

1.1.2 Supervisory and control systemThe present subchapter describes the supervisory and control system. This system ensures the quality of the production process of the Luxembourgish national accounts. The first subchapter provides a brief description of the national accounts’ compilation process by focusing on the elements which ensure the consistency and minimise the risk of errors in a system as complex as a national accounting system.The second subchapter indicates the benchmarks for the analysis and the treatment of current risks of the production approach’s main data source, namely the structural business survey (SBS). The third subchapter deals with the more formal, existing tools to ensure and improve the quality of Luxembourg’s national accounts. These tools are quality reports, audit processes as well as data flow inventories.

Finally the last subchapter deals with the work organisation and the work management in the unit MAC1 – National accounts.

1.1.2.1 National accounts compilation process

The compilation of national accounts is a complex process which is characterized by the following elements:

Existence of a variety of source data : with diverging formats (structure and format of files) derived from diversified collection systems (surveys, administrative sources, etc.) available at different moments subject to regular or occasional revision of varying quality

Necessity to adapt the source data to the concepts of national accounts : By ensuring the transition from business accounting standards, or conventions

adopted by administrative sources, to national accounting concepts. By imputing some flows foreseen in national accounting but not directly observable

in the real economy (example: imputed rents)

Necessity to ensure an exhaustive coverage of the national economy: By using survey results and administrative sources if they are available By extrapolating data collected by sampling to the overall observation universe By completing, when appropriate, source data by estimations (statistical reporting

threshold, activities with minor importance, undeclared work, illegal economy, etc.)

Necessity to integrate all source data (surveys, administrative data, estimations) in a system of nomenclatures and economic accounts forming an integrated and consistent representation of the national economy

Necessity to arbitrate between diverging source data in order to fulfil production accounting identities (equilibria between uses and resources) and to ensure alignment of production equilibria by breaking down the economy into branches and institutional sectors. All of this in an integrated supply and use framework

Necessity to set up coherent time series of the main aggregates and the different breakdowns of national accounting (branches, institutional sectors, functional nomenclatures (COICOP, COFOG)). This in current prices as wells as previous year prices.

Necessity of total coherence with the ESA2010 methodological framework. On a conceptual level as well as regarding the compulsory elements of the transmission program.

1.1.2.2 Graph of data flow (GOD)

During the production of national accounts data processing is a determining factor. A significant effort in computing is needed in order to process and organise multiple statistical sources as well as numerous data formats. To ensure that all the different programs in the national accounts chain of production are successfully executed, data flows are documented and modelled using graphs of data flow (GOD – Graph of Dataflow).

GODs are diagrams (see Figure 1.1) constructed in EXCEL, using the flowchart tool. Input and output files are shown graphically for each program in the production chain of national accounts. Furthermore each program and file is directly accessible via hypertext links. GODs can be used to navigate through the execution of the different programs ensuring that each step is executed.

Figure 1.1

Procédure Analyse_Production_Par_EntrepriseLa procédure sert à confronter la répartition par produits CPA3 par entreprise issue de trois souces différentes à savoir:

enquête structurelle d'entreprises (Unité C3)enquête d'activité mensuelle (Unité C4)commerce extérieur Intrastat/Extrastat (Unité D1)

L'outil Analyse_Production_Par_Entreprises sert alors à eventuellement appliquer des taux de répartitions par produits aux résultats de l'enquête structurelle d'entreprises. Environnement UNIX sous controle de l'unité C1

Fichier de base mensuel unité C1:Fichier de base annuel unité C1: NomenclaturesNomenclatures Numunitleg ; UnitéActiviteNumunitleg ; UnitéActivite NumNaceRev1 (5 positions)NumNaceRev1 (5 positions) ; NA60e NC8 ; CPA6 ; P60eCPA3CPA6 ; P60eCPA3 CodePays (détaillé) ; CGCECodePays (agrégé) ; CGCE (réduite dans variables) Nature de la transaction (ntra)Données annuelles Données mensuelles

cextXXXX -> cextXXXX..\METHODE\Commerce extérieur\Fichiers de base commerce extérieur.doc ..\METHODE\Commerce extérieur\Fichiers de base commerce extérieur.doc(contient description des variables et explications sur ajustement INTRASTAT) (contient description des variables et explications sur ajustement INTRASTAT)

Procédure désactivée le 28/2/2005 (fichier mdb trop volumineux). John.

Etape manuelle !!!1) Ouvrir cextnathnorm.mdb 3) Importer cextnath.mdb2) Effacer table cext 4) Effacer fichier cextnath.mdb3) Compacter base

Remarque:L'outil ne permet d'afficher que celle des entreprises quisont compris dans la source enquête structurelle etfigurent en même temps dans au moins une des deuxautres sources.

cext_base_XXXX.dbfXXXX = 1993 à année la plus récente

ana_vent_produit_95-99.sps

comp_enq_prod_cext.xls

analyse_production_par_entreprise.xlsConfrontation de la répartition par produits CPA3 des sources enquête structurelle, enquête d'activité mensuelle et Intrastat/Extrastat au niveau entreprise

comp_enq_prod_cext_taux.xls

comp_enq_prod_unique_entreprise.xls

cextnathnorm.mdb

cextnath.mdb

commerce extérieur unix.sas

\usr\haas\cext\base\cextXXXXXXXX = 1993 à année la plus récente

Furthermore, the Metadata of the main files (databases, intermediate files showing important steps (for example CNTOT, BASTOT)) are included in the GODs. Metadata sheets inform about stratification variables (nomenclatures, periods and other subdivisions) as well as variables containing statistical information (production, intermediate consumption, wages, employment etc.) (see Figure 1.2).

Figure 1.2: Example of a metadata template

Métadonnées fichier: G:\CN\EMPLOI\CN-empsal.sav1) Caractéristiques généralesNom/localisation: ..\..\EMPLOI\CN-empsal.savAuteur principal: MarcSource: base de données IGSSRythme de mis à jour: mensuelPrincipales utilisations: Estimation des variables emploi et salaires par branches et par secteurs institutionnelsPrincipaux utilisateurs: Teams T4 et T1Taille:Descriptif: Avant corrections travail au noir et bateliers rhénansFichiers descriptifs: néant2) Nomenclatures - variables de catégoriesNom variables: Descriptif variables: Link classifi:annee annéenarev NACE Rév.1.1 ..\..\CLASSIFI\Nac

e\NaceRev11.xlssecteur secteur (CN)narev narev23) Variables de donnéesNom variables: Descriptif variables: Link:frouv nombre d'ouvrierscsouv coût salarial (y compris cotisations patronales, hors cotisations bénévoles) ouvrierssbouv salaire brut (y compris gratifications) ouvriershoouv heures rémunérées ouvriershtouv heures travaillées ouvriershmouv heures maladies ouvriershcouv heures chômées ouvriersfremp nombre d'employéscsemp coût salarial (y compris cotisations patronales, hors cotisations bénévoles) employéssbemp salaire brut (y compris gratifications) employéshoemp heures rémunérées employéshtemp heures travaillées employés

For the moment GODs are available for the majority of the production chains. However, due to the implementation in simple Excel flowcharts, regular maintenance and updating is a major challenge. There are plans to replace the Excel tool with GSBPMN modelling tools.

1.1.2.3 Version analysis and backups

A second tool to ensure the quality of national accounting data is the analysis of the version of a file associated to the system of backups.Key files are analysed on a regular basis and have several backups of successive versions. This is particularly important to be able to analyse the consistency and the impact of revisions on the times series. Hence, for example the two main databases BASTOT (main reference for the results of the structural business statistics) and CNTOT (main input in the integration process of the production and expenditure approach into the framework of annual supply and use tables) have version analyses at a very detailed level at the start of a new annual campaign when the newly available data as well as all revised data are integrated. Analysis happens at a more and more detailed level of the NACE, going up to the 5-position NACELux level. If any anomalies are detected, a return to the microdata files is possible. If needed, the data supplier can be contacted to provide explanations and/or to correct the observed errors.It is possible to compare older versions of key files, available via the archiving system, over time given the standardised structure over several years. For each annual campaign, a large number of basic, intermediate as well as final files are saved in a read-only archive.While feeding the data into the supply and use balancing tool, the “MASTER”, another very detailed analysis of versions is realised and major changes are archived for future reference.

1.1.2.4 « Doors » and « GateKeeper » applications

Prior to the loading of the supply and use balancing tool, all data are saved in the database “Doors”. This database is the only and compulsory entry point, the unique “door”, for the data in transit towards the “MASTER”.The “Doors” are a large collection of files with the following characteristics:

complete standardisation concerning the nomenclatures and the variables included one single file per year per variable

Data are regrouped in subsets: MAKE matrix, USE matrix, vectors of imports and exports, vectors of trade margins, etc.

documentation of the date and time of the creation of the file existing for each record in each file (TDate and TTime)

During the loading of the balancing tool, the concerned data is loaded one by one through the tool “GateKeeper” towards the balancing tool “MASTER”.“GateKeeper”allows to:

select years and/or variables to be loaded into the “MASTER” individually compare the version of the concept to be loaded (for example exports) to the version

previously loaded. This is helpful during the revisions of national accounting series (production of semi-final and final accounts).

visualise differences between versions by products and by branches used in the balancing of resources and uses, respectively the MAKE and USE matrixes in the most detailed level of the nomenclature available

visualise differences between the loaded version and an already balanced version for the year under review. This allows to control if potential changes in the database will have the same effect as previous arbitrages in the “MASTER” during previous campaigns.

keep an automatic and time stamped trace of the main differences while loading (“GateKeeper Log”)

keep track of the time, the hour and the user having charged the selected variable in the “MASTER”.

“GateKeeper” and “GateKeeper Log” make it possible to retrace each change on a database level during its transition to the “MASTER”. The “Doors” database is subject to a read-only backup in the archives and serves as a documentation of the national accounts successive versions.

1.1.2.5 « MASTER » application for supply and use balancing

The arbitrage between resources and uses per product is made in the tool “MASTER”. The tool “MASTER ERE” allows visualising and working on three “MASTER”-files simultaneously. For example, this three “MASTER”-files can be for different years (balancing a 3-year time series) or multiple versions of the same year. The following is an often used constellation: an old, already balanced version for the year’s t-1 and t and a version to be balanced for year t. Other constellations are possible as well.The arbitrage between resources and uses is a manual process. All disequilibria need to be resorbed manually based on decisions by the responsible national accountant. In order to make the best arbitrage possible, all the decisions are based on archive previous balancing decisions made available in the tools “MASTER” and “MASTER ERE”. However, an automatic rule is never applied. The products which need to be balanced are allocated to different members of the units MAC1 and MAC2 in respect of their specialization. For example the main financial services are treated by the specialists of the financial sector. The products whose final uses are largely composed by households’ final consumption (for example meat, tobacco, etc.) are balanced by the person in charge of households’ final consumption.Meetings are organised to balance larger disequilibria and to arbitrate products with a very high importance within the Luxembourgish economy. During these meetings, the supply and use equilibria are projected on a large screen (“cinema” meetings) and resorbed interactively by a team. The decisions taken are documented in a statement: “Remarks on the balancing campaign XXXX”.The “MASTER” allows documenting each arbitrage decision in a special information file. This file memorizes all the decisions taken and helps to make consistent arbitrage decisions.

1.1.3 Source dataA particularly elaborated control system has been developed to exploit the data of the structural business survey (SBS) by ENT3 - Structural Business Statistics. Since GDP is largely estimated in the production approach, this control system is very important for Luxembourg’s national accounts Hence, for the SBS survey an analysis and risk treatment system has been elaborated. The goal of this risk analysis is to document the production chain relative to the structural business statistics by refocussing the validation environment of the quality of these statistics. This risk analysis1:

allows to define guiding principles on how to document the processes and the methodology and thus allows to adapt the detail level of such a documentation.

provides an identification method for the evaluation criteria and the risks impacting the latter, yielding in a more trustworthy auto-evaluation process.

links the methodological documentation to the evaluation of statistics with respect to quality and methodology criteria

1.1.4 Formal control and supervision instruments

1.1.4.1 Quality reports

To determine the contribution of each member state of the EU to the 4 th own resource GNI, Luxembourg communicates the GNI, calculated according to the SEC2010 concepts, each year on the 22nd of September.The notification questionnaire of the GNI is accompanied by a quality report informing on:

the main changes made to the national accounts’ sources and methods revision policy and national publication date the quality inquiry results recent developments of statistical sources which may impact GNI changes of sources and methods made to the final estimates of national accounts revisions of years n-1, n-2, n-3 and n-4

The GNI questionnaire and the quality report are then submitted to the « Comité relatif à l'harmonisation du revenu national brut aux prix du marché » (GNI committee) for formal approval.

1.1.4.2 Audits

In the light of its rather small size the STATEC has no internal audit service.Nevertheless the units MAC1 – National Accounts, MAC2 – Sector accounts and MAC4 – General government accounts have been subject to audits by external advisers.

Firstly there are the regular audits by services of the European Commission (Eurostat, General-Directorate Economy and Finance, General-Directorate Budget) and by the European Court of Auditors. Generally these audits position themselves in the European regulatory environment relating to own resources (4th own resource GNI and 3rd own resource VAT) or the notification of excessive deficits (Stability Pact).

Secondly, STATEC has commissioned an external audit by an independent external auditor from French INSEE. The conclusions of this audit (available in written final report) are currently under review and some important medium and long term decisions have already taken account of them (e.g. the need for a fundamental redesign of the IT production process of Luxembourg’s national accounts).

1 From « Analyse de risque dans le domaine de l’information statistique – appliquée aux données de l’enquête structurelle sur les entreprises » ; Georges Zangerlé ; 28/07/2009 ; Economie et statistiques Working papers du STATEC Nr 29/2009 (a free pdf version can be downloaded here : http://www.statistiques.public.lu/fr/publications/series/Economie_et_statistiques/2009/29_2009/index.html )

1.1.4.3 Data flow inventory (DFI)

A recurring requirement/request made by the different institutions of the EU (Eurostat, Court of Auditors) during their audits is about the implementation of more formal service agreements (“Service level agreement” (SLA)) between suppliers and users of the statistical data. This should be done for both, internal and external suppliers of STATEC. STATEC is an administration with a small size (199 staff members in total), the setup of SLAs can be seen as a disproportionate venture with respect to STATEC’s size. Therefore STATEC rather opted for the implementation of a data flow inventory (DFI) without formal service agreements.The main goal of the DFI is to formalize data flow between suppliers and users by determining the persons in charge of data supply, the supply deadlines, the timetables of availability and of updates, etc. All of this is possible without the administrative and legal background accompanying “real” SLAs (for example formal agreement, no respect clauses, etc.). A DFI allows to ensure transparency of data flows and to raise the awareness of STATEC’s members as well as external suppliers of their obligations towards the users of their data. Currently the DFI is work in progress.

1.1.5 Organisation and managementIn general the work program for a year t is fixed during the annual planning of STATEC’s executives in year t-1. The planning is forward looking on the three next years. The strategical objectives for years t, t+1 and t+2 are fixed during the annual planning. At that moment the tasks of year t-1 are critically reviewed. The work program then needs to be formally approved by the “Conseil supérieur de la statistique”.The follow-up of the work program is made on multiple levels. Subgroups of STATEC’s executives meet and discuss transversal issues:

Issues concerning multiple divisions at the same time are discussed in the “Comité de direction”

Each week all head of units of the MAC division meet to discuss the working plan.Most of the follow-up of the work program concerning national accounts is done internally in the MAC division. In order to be more efficient, MAC division is subdivided into 5 units (see Figure 1.3):

MAC1 – National Accounts (including quarterly and annual accounts) MAC2 – Sector Accounts (including financial institutions) MAC3 – Balance of payments MAC4 – Government Accounts MAC5 – Environmental accounts and energy statistics

Each head of unit meets with the full staff of the unit once a week to monitor progress and discuss problems.

1.1.6 Main approaches usedThe production approach is the main approach for calculating GDP (Gross Domestic Product) both for the provisional and the final accounts. For the expenditure approach, STATEC aims to do an idenpendant estimate of all the components of final demand (provided that the supply and production approaches are not conceptually linked (e.g. public consumption)). Nevertheless there are cases where elements of the production and expenditure approach are confronted at earlier stage in the production process of the accounts. The annual supply-and-use tables ensure the full integration and coherence of the two approaches at the level of 135 industries and 270 products. In contrast, the income approach plays no role in assessing the level of GDP. Gross operating surplus is derived as a balancing item.

Figure 1.3: STATEC organisational chart (1.6.2016)

STATEC Organisation Chart

Director(Serge Allegrezza)

Division SG General Services(Denise Schroeder)

SG1 - Dissemination and Communication

(Guy Zacharias)Deputy head of

division

SG2 - Information Technology

(Laurent Maretti)

SG3 - Human Resources and

Budget(Denise Schroeder)

SG4 - Central Balance Sheet Office(Patricia Gonzalez)

Division SOCSocial Statistics

(Jérôme Hury)

SOC1 - Living Conditions(Liliane Reichmann)

SOC2 - Labour Market and Education

(Marco Schockmel)

SOC2 - Marché du travail et éducation(Jan Ries) SOC3 - Population et eChef de division adjoint

SOC4 - Price Statistics(Claude Lamboray)

Division ENTBusiness Statistics

(Lucia Gargano)

ENT1 - External Trade(Alain Hoffmann)

Deputy head of division

ENT2 - Foreign Direct Investments

(Gilles Genson)

ENT3 - Structural Business Statistics(Georges Zangerlé)

ENT4 - Short Term Indicators

(Frank Hansen)

ENT5 - Business Register

(Mike Hartmann)

Division MAC Macroeconomic

Statistics(John Haas)

MAC1 - National Accounts

(René Krippes)

MAC2 - Sector Accounts

(Laurent Pütz)Deputy head of division

MAC3 - Balance of Payments

(Nico Weyer)

Division CMP Economic, Modelling

and Forecast(Ferdy Adam)

CMP1 - Short Term Economics

(Bastien Larue)Deputy head of division

Secretary's Office(Sandra Paul, Anne-Marie Koltz, Arlette

Steffen)

MAC5 - Energy and Environment

(Olivier Thunus)

Deputy Director(Nico Weydert)

MAC4 - Government Accounts

(David Soppelsa)

SG5 -Documentation

Centre(Simone Casali)

Division RED Applied Research

(Chiara Peroni)

SOC3 - Population and Housing

(Germaine Thill) Deputy head of division

ANECResearch

CMP2 - Modelling and Forecast

(Ferdy Adam)

1.1.7 Geographical coverageThe economic territory of Luxembourg comprises: the geographic territory; customs warehouses; national airspace; geostationary positions in space; territorial enclaves in the rest of the world (embassies).However, it excludes all of the parts of the national territory used by other countries (embassies) or international organisations, particularly the institutions of the European Union and NATO.

1.2 Revisions policy and timetable for revising and finalising the estimates

The timetable for revising the accounts is mainly based on the timetable for submitting the ESA2010 tables to Eurostat (annex B of regulation (EU) No 549/2013) :

t + 85 days: preliminary estimate for the year t by adding together the 4 quarters of the year t taken from the quarterly national accounts (t+85 days is set according to a transmission program derogation which will expire on 1st of January 2019)

t + 9 months: provisional figures, preliminary “annual” estimate for the year t;t + 21 months: revised provisional figures;t + 33 months: semi-finalised figures;t + 45 months: final figures.The valuation methods used for the different versions vary insofar as the variables which are initially updated on the basis of trend indicators are replaced by figures from direct sources as soon as they become available. Only the data sources and statistical methods used for the final accounts are described in this inventory. In accordance with what was agreed by the EU Member States, the Luxembourg accounts undergo “benchmark revision” every five years. These major revisions are an opportunity to implement major changes in methodology or take account of significant changes in the data sources. The latest benchmark revision was carried out in 2014 (ESA 2010 benchmark revision). The next is scheduled for 2020.Transition from ESA 95 to ESA 2010 can be qualified as an “exceptional benchmark revision”, since it combined major methodological revisions with the usual benchmark revisions of longer time series.

1.3 Outline of the production approach

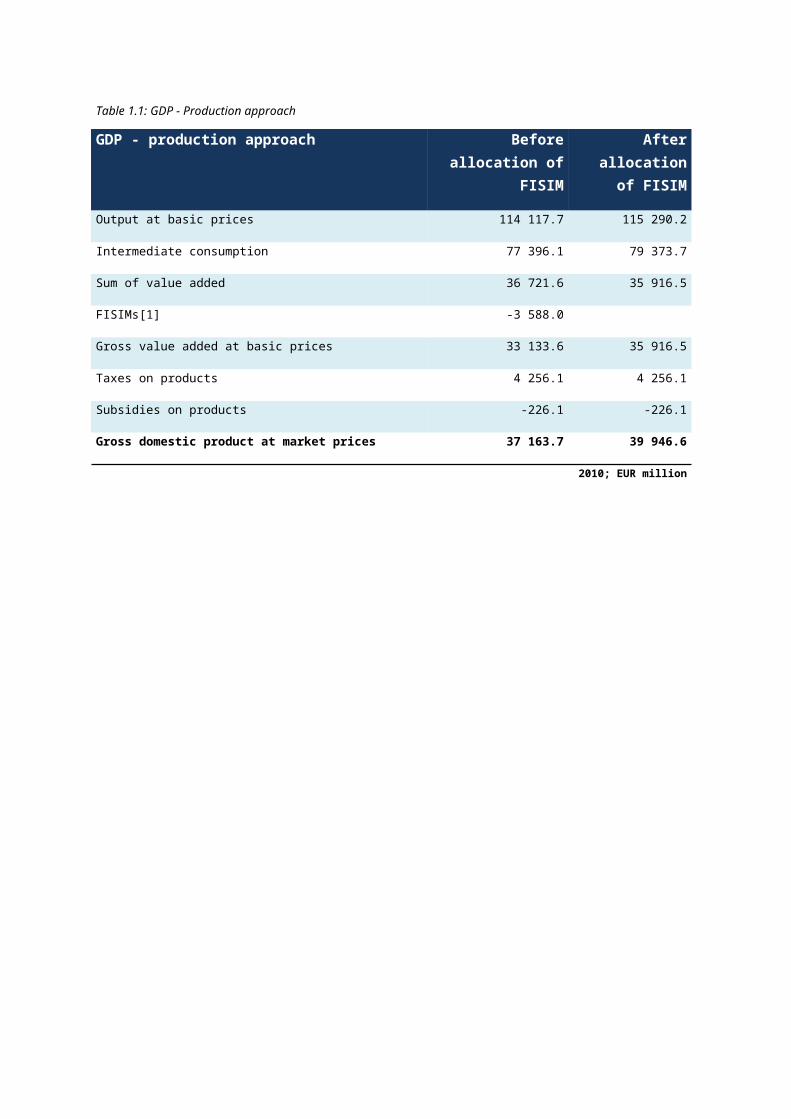

1.3.1 Reference frameworkIn the production approach, GDP is valued on the basis of the production accounts of the institutional units, industries, or institutional sectors. Gross value added of economic units is calculated by substracting intermediate consumption from the value of production.GDP is calculated by adding net taxes on products (taxes less subsidies on products) to the sum of value added for all industries. Production and gross value added are calculated at basic prices. GDP is valued at market prices.In Luxembourg the production approach is the dominant approach for valuing Gross Domestic Product.

Table 1.1: GDP - Production approach

GDP - production approach Before allocation of FISIM

After allocation of FISIM

Output at basic prices 114 117.7 115 290.2

Intermediate consumption 77 396.1 79 373.7

Sum of value added 36 721.6 35 916.5

FISIMs[1] -3 588.0

Gross value added at basic prices 33 133.6 35 916.5

Taxes on products 4 256.1 4 256.1

Subsidies on products -226.1 -226.1

Gross domestic product at market prices 37 163.7 39 946.6

2010; EUR million

Table 1.2: Value added by industry

Value added by industries Production at basic

prices

Intermediate

consumption

Gross value

added at basic

prices

Agriculture, forestry and fishing A 345.4 246.0 99.3

Mining and quarrying B 66.9 36.6 30.3

Manufacturing C 9286.7 7206.3 2080.4

Electricity, gas, steam and air conditioning supply D 1087.8 787.5 300.3

Water supply; Sewerage, waste management and remediation activities

E 410.7 186.7 224.0

Construction F 4859.3 2932.5 1926.8

Wholesale ans retail trade; Repair of motor vehicles and motorcycles

G 8975.7 5279.1 3696.6

Transportation and storage H 4219.6 2526.1 1693.5

Accomodation and food service activities I 1289.4 634.1 655.3

Information and communication J 7192.3 4931.8 2260.5

Financial and insurance activities K 56333.4 46137.6 10195.8

Real estate activities L 3936.5 962.3 2974.2

Professional, scientific and technical activities M 4294.2 1782.2 2512.0

Administrative and support service activities N 4600.9 3543.6 1057.4

Public administration and defence; compulsory social security

O 2835.1 764.0 2071.1

Education P 1783.7 266.9 1516.8

Human health and social work activities Q 2681.0 750.2 1930.7

Arts, entertainment and recreation R 476.8 229.7 247.1

Other service activities S 497.9 170.6 327.3

Activities of households as employers; Undifferentiated goods- and services-producing activities of households for own use

T 117.0 0.0 117.0

Activities of extraterritorial organisations and bodies U 0.0 0.0 0.0

Total for Industries: 115 290.2 79 373.7 35 916.5

2010; EUR million

Table 1.3:Value added by institutional sector

Value added by institutional sector Production at basic prices

Intermediate consumption

Gross value added at basic prices

Non-financial corporate sector S.11 47 115.6 29 942.2 17 173.4

Financial corporate sector S.12 56 289.9 46 136.2 10 153.7

Government sector S.13 6 024.5 1 550.6 4 473.9

Household sector S.14 5 192.6 1 527.1 3 665.6

Non-profit institutions serving households S.15 667.6 217.2 450.4

Total of all sectors 115 290.2 79 373.3 35 917.0

2010; millions EURO

Production is defined by ESA2010 as “an activity carried out under the control and responsibility of an institutional unit that uses inputs of labour, capital and goods and services to produce goods and services. Production does not cover natural processes which have no human involvement or direction” (ESA2010, 3.07).Production essentially comprises:

a) the production of goods and services supplied or intended to be supplied to units other than their producers;

b) the own-account production of all goods that are retained by their producers for their own final consumption or gross fixed capital formation.

Volunteer activities that do not result in goods, e.g. caring for the elderly without payment, are excluded.Production also excludes domestic and personal services that are produced and consumed within the same household, with the exception of the services of owner-occupied dwellings and of employment of paid domestic staff (ESA2010, 3.09).Production comprises informal production (production not declared to the tax authorities, undeclared work etc.) as well as illegal or even criminal production (production and distribution of drugs, procurement, etc.) for the extent that it is not already included in legal activities (money laundering via “fictitious” legal activities). The base unit of observation used in the production approach is the kind-of-activity unit (KAU).However, it should be pointed out that basic data (production and use accounts) are available at the level of the kind-of-activity unit only for businesses of a certain size. For the others, the business, or more precisely, the legal unit, constitutes the base unit. KAUs are grouped into industries according to their main activity. The nomenclature used is NACELUX Rev 2 a more detailed version (coded to 5 digits) of the Classification of Economic Activities in the European Community NACE Rev 2. Moreover, the base units are classified by institutional sector, which makes it possible to compile production accounts and generation of income accounts by industry and by institutional sector, as

well as by type of producer (market producer, producer for own final use, or other non-market producer). Base units are managed within the framework of the “Répertoire des entreprises”.

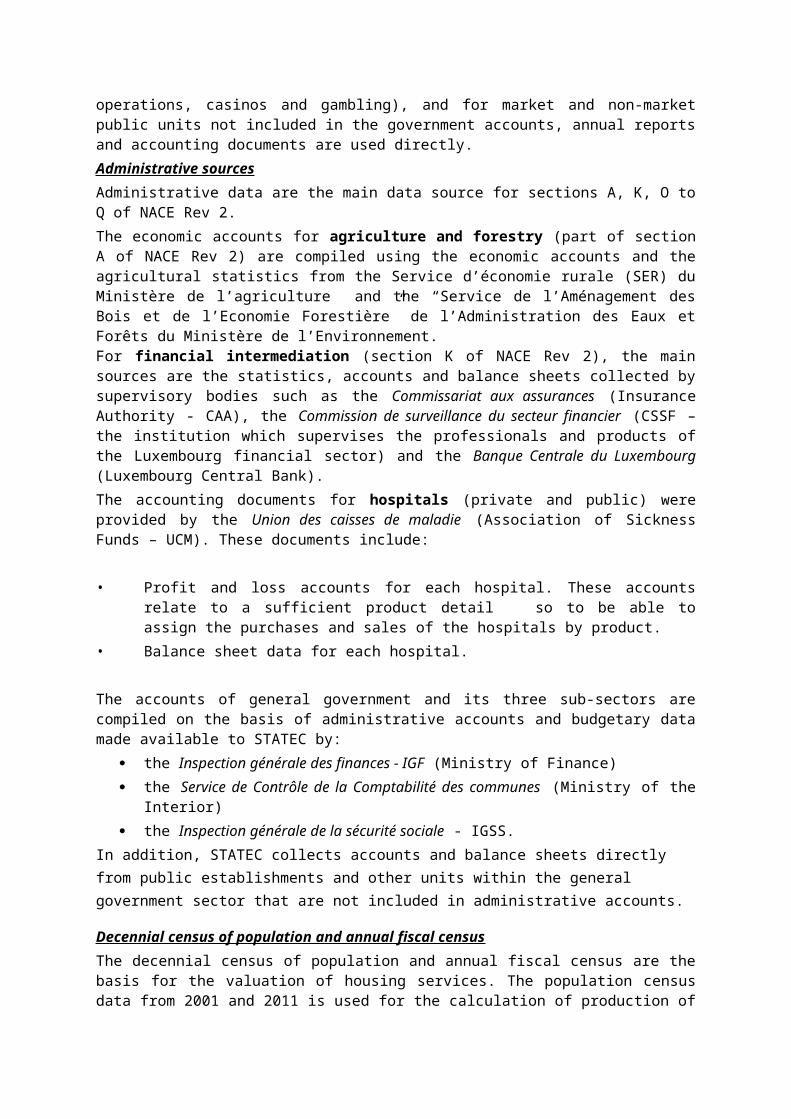

1.3.2 Main data sourcesOnly the data sources used to compile the final accounts are described in the scope of this inventory.Statistical register of businesses (“Répertoire des entreprises”)The statistical register of businesses and legal persons serves as the framework for identifying economic units and classifying them by industry and institutional sector; it is the basis for statistical surveys of businesses.The base unit is the legal unit (natural or legal person), as defined in the National register of natural and legal persons (“Répertoire national des personnes physiques et morales”) managed by the ”Centre des Technologies de l’Information de l’État” (CTIE).In the vast majority of cases, the legal unit corresponds to the institutional unit as defined in ESA2010 (“enterprise” for market industries). The directory includes all sole proprietorships which are subject to VAT or employ paid employees together with all businesses which are incorporated (legal persons). The statistical directory also includes all central and local government, social-security administration and non-profit institutions serving households.In addition to descriptive information on the statistical units, STATEC’s statistical directory also includes some accounting information (turnover, imports and exports, etc.) from VAT declarations and information on paid employment (by sex, status and duration of work) derived from the declarations of employment submitted to social security. The directory is also the basis for extrapolating from sample surveys and for estimating businesses which were not included in the survey samples.Annual VAT Declarations (“ESKORT” files)Since 2000, STATEC receives “ESKORT” files, which include legal units’ annual VAT declarations, from the CTIE. These declarations currently cover the period 1997 to 2014. The files contain 879 variables, as defined on the annual VAT declaration form (see chapter 10).One of main uses of the ESKORT files is to provide an estimate of gross fixed capital formation for missing legal units (see chapter 5).Annual Structural Business Survey (SBS) The main source for calculating GDP in the production approach is the annual Structural Business Survey first carried out in 1998 and covering the 1996 fiscal year (Council Regulation (EC, Euratom) No 295/2008 of 11th of March 2008 dealing with structural business statistics). The Annual Structural Business Survey replaced the annual survey of industrial enterprises and periodical surveys of service enterprises. It is a sample survey carried out using the quota method to ensure that all the industries at the group level of NACE Rev 2 are represented and that all businesses with a turnover exceeding EUR 7 million or having more than 45 employees are included in the sample. Estimates of businesses not included in the sample are made on the basis of the statistical register of businesses. The Structural Business Survey is the main data source for sections B to N (except for letting of own property) and R to S of NACE Rev 2.Accounting documentsFor certain large service enterprises (railways, postal services and telecommunications, radio and television, air transport, satellite operations, casinos and gambling), and for market and non-market public units not included in the government accounts, annual reports and accounting documents are used directly.Administrative sourcesAdministrative data are the main data source for sections A, K, O to Q of NACE Rev 2.

The economic accounts for agriculture and forestry (part of section A of NACE Rev 2) are compiled using the economic accounts and the agricultural statistics from the Service d’économie rurale (SER) du Ministère de l’agriculture and the “Service de l’Aménagement des Bois et de l’Economie Forestière” de l’Administration des Eaux et Forêts du Ministère de l’Environnement.For financial intermediation (section K of NACE Rev 2), the main sources are the statistics, accounts and balance sheets collected by supervisory bodies such as the Commissariat aux assurances (Insurance Authority - CAA), the Commission de surveillance du secteur financier (CSSF – the institution which supervises the professionals and products of the Luxembourg financial sector) and the Banque Centrale du Luxembourg (Luxembourg Central Bank).The accounting documents for hospitals (private and public) were provided by the Union des caisses de maladie (Association of Sickness Funds – UCM). These documents include:

• Profit and loss accounts for each hospital. These accounts relate to a sufficient product detail so to be able to assign the purchases and sales of the hospitals by product.

• Balance sheet data for each hospital.

The accounts of general government and its three sub-sectors are compiled on the basis of administrative accounts and budgetary data made available to STATEC by:

the Inspection générale des finances - IGF (Ministry of Finance) the Service de Contrôle de la Comptabilité des communes (Ministry of the Interior) the Inspection générale de la sécurité sociale - IGSS.

In addition, STATEC collects accounts and balance sheets directly from public establishments and other units within the general government sector that are not included in administrative accounts.

Decennial census of population and annual fiscal censusThe decennial census of population and annual fiscal census are the basis for the valuation of housing services. The population census data from 2001 and 2011 is used for the calculation of production of owner occupied dwelling services. The annual fiscal census is the base of the calculation of actual rents, although it is no longer be available for the years after 2012 (2009 for the town of Luxembourg). Household budget surveyThe annual household budget survey, together with data on paid employment and social security payments from the social-security registers are used as the basis for the valuation of domestic services. Data on paid employment and social security payments Statistics relating to paid employment and compensation by industry and institutional sector are calculated by the Centre informatique de la sécurité sociale and the Inspection générale de la Sécurité Sociale (IGSS) in close cooperation with STATEC. They relate to paid employment and payments declared to social security. These statistics are used to check the data from other statistical sources and for indirect estimates, particularly for non-profit institutions serving households.

1.3.3 Calculation of gross value added and Gross Domestic ProductUsing data sources described above, detailed production accounts are drawn up for all industries and institutional sectors.The basic statistics are processed to make it possible to classify units of production both by industry at the sub-class level of NACELux Rev 2 (breakdown of the five-digit NACE Rev. 2) and by institutional

sector (4 decimal places of ESA2010’s sectoral classification). The production account and generation of income account are calculated at this level of classification.Market output is initially valued at market prices. Subsidies and taxes on products are recorded at the level of basic statistics (surveys, company accounts, detailed administrative information per business for certain taxes or subsidies, etc.) and rendered consistent with the data from the general government accounts, thereby allowing the basic price to be calculated.Own-account production is in principle valued at basic prices of similar products sold on the market. In contrast, for one-of-a-kind investment goods, the production costs are used as best estimate.The valuation of other non-market output is calculated as some of costs:

Intermediate consumption (P.2);+ compensation of employees (D.1);+ other taxes on production (D.29);- other subsidies on production (D.39);+ consumption of fixed capital (K.1)

Intermediate consumption is valued at purchasers’ prices including trade and transport margins and non-deductible VAT.In principle, the basic data sources include all of the accounting details needed to calculate production and intermediate consumption according to ESA2010’s evaluation criteria.The following adjustments were made for the transition from business or administrative accounting to national accounting concepts: revaluation of changes in inventories to eliminate holding gains or losses included in the book

values of stocks; replacement of the charges for insurance premiums included in business or administrative

accounting by the value of the insurance service; reclassification as intermediate consumption of expenditures for market studies, impact studies

and certain start-up expenditure that business or administrative accounting allows to immobilize;

exclusion of financial leasing fees from intermediate consumption; valuation of consumption of fixed capital according to economic rather than fiscal criteria; recording of taxes on products at the time of the transaction giving rise to the tax rather than at

the time that the taxes are paid (which corresponds to traditional accounting in the administrative accounts of general government). No similar adjustment has been applied to subsidies on products since government expenditure – unlike revenue – are generally allocated to administrative accounts in the year where the related economic activity is occuring.

The balancing item in the production account for the various industries or institutional sectors is gross value added at basic prices.Gross Domestic Product at market prices (GDP) is calculated by adding taxes on products to the sum of value added at basic prices and deducting subsidies on products. Allocation to uses of financial intermediation services indirectly measured (FISIM) is made as a separate layer in the supply and use framework.Taxes on products comprise VAT (D.211), taxes and duties on imports, excluding VAT (D.212) and taxes on products except VAT and import taxes (D.214). Taxes on products are recorded at the time of the transaction giving rise to the tax (time adjusted cash registering), and thereby differ from the amounts recorded in the administrative accounts of general government which refer to the amounts received during the financial year (cash base registering).

Moreover, taxes on products except VAT and import taxes (D.214) need to be broken down by product, industry and institutional sector, as production and value added are valued at basic prices. The breakdown is achieved by benchmarking the data gathered from business accounts to the detailed data on taxes per product recorded in the general government accounts.Taxes on imports and other taxes on products mainly comprise customs duties, excise duties on mineral oils and on tobacco, and excise duties and consumption taxes on alcohol, taxes on gambling, taxes on insurance and registration fees.Subsidies on products include import subsidies (D.311) and other subsidies on products (D.319). Like taxes on products, subsidies on products are recorded at the time of the transaction giving rise to the subsidies. No adjustment similar to that applied to taxes on products has been applied to subsidies on products since government expenditure is generally allocated to administrative accounts in the year when the payables are created. The other subsidies on products are also broken down by industry and sector by adjusting the data gathered from business accounts to the detailed data per product recorded in the general government accounts.Subsidies on products mainly relate to public transport and agricultural products (as part of the common agricultural policy of the EU).

1.3.4 The role of direct and indirect estimation methods and of benchmarks and extrapolationDirect estimation methods are methods based on surveys (either census or sample surveys) or annual administrative data which include the main variables required (production, intermediate consumption, etc.). Indirect estimation methods include the following:

annual data estimated by extrapolating from the data of a base year using indicators; annual data not surveyed directly, but rather deduced from other sources of statistics.

Direct methods of estimation are predominant in the compilation process of Luxembourg’s GDP. They are used for all the industries covered by the Annual Structural Business Survey, accounting documents or administrative statistics.Indirect methods are used for a limited number of industries such as services provided by doctors, insurance agents, rental of commercial premises or owner-occupied dwellings and most non-market services of non-profit institutions serving households (NPISH). More frequently “combined” methods are used, whereby certain key components of the economic accounts are surveyed every year (e.g. production), while detailed breakdowns of production or general expenses are based on surveys with a less than annal frequency.

1.3.5 Independence of the different approaches to GDPAs the production approach is the main approach used for GDP evaluation, it can be considered to be independent of the expenditure approach.Nonetheless, in a limited number of cases production and final expenditure are valued on the basis of the same source data and in a completely integrated manner, meaning that the two approaches are not independent.This is the case for:• non-market government services;• non-market services of non-profit institutions serving households (NPISH);• housing services;• domestic services;• services of doctors, dentists and other health professionals.

In contrast, the income approach is not independent and is completely integrated within the production approach. Gross operating surplus is a residual item.

1.3.6 Main compilation steps of the production approachThe accounts using the production approach are prepared in the following steps:a) From basic data to “BASTOT” collection of basic data (surveys, administrative data, indirect estimates) in an initial

comprehensive file comprising all the variables required to compile the production and generation of income accounts together with the main variables for the production of the income account by industry (at the five-digit level of NACELux Rev 2) and by institutional sector/sub-sector. Note that at that level, most adjustments made to take account of the differences between business accounting or administrative statistics and national accounting concepts have already been applied (reclassification as intermediate consumption of market studies expenditure, or exclusion of financial leasing fees from intermediate consumption)

valuation of undeclared work; comparison of variables concerning resources and compensation of employees with the social

security statistics, applying adjustments if necessary.Result: the “BASTOT” database. This database is also partly the reference for the results of business structural statistics.b) From “BASTOT” to “CNTOT”: revaluation of changes in inventories to eliminate holding gains or losses included in the book

values of inventories; replacement of the charges for insurance premiums included in business or administrative

accounting by the value of the insurance service after pre-balancing of the insurance gross premiums;

valuation of consumption of fixed capital according to economic rather than fiscal criteria (incorporation of the results of the capital stock calculation in the database);

adjustment of taxes on production (taxes on products and other taxes on production), of subsidies (subsidies on products and other subsidies on production) and of current taxes on income, wealth, etc. on the taxes recorded in the general government accounts (in line with the time adjusted cash recording principle);

estimate of tips; estimate of tax evasion (fraud on turnover in relation to VAT declarations).Result: the “CNTOT” database. This database, which can be regarded as the “intermediate accounts”, is an input for the process of integrating the production and expenditure approaches within the framework of annual supply-and-use tables. Lastly, the final step in preparing the accounts, following the integration of the production and expenditure approaches, consists of allocating financial intermediation services indirectly measured (FISIM) to the the various uses and, in the production approach, to intermediate consumption by institutional sector and industry.

1.3.7 ExhaustivenessThis subchapter provides an overview of the main instruments used for assuring exhaustiveness and of the adjustments done in order to guarantee exhaustiveness of the production approach. A more detailed description is provided in chapter 7.

1.3.7.1 Business register (Répertoire des entreprises)

The statistical register of businesses and legal persons covers all units and is the reference framework for assuring the exhaustiveness of the production approach. The register is the basis for identifying economic entities and industries and for carrying out surveys on businesses: survey sampling, calculation of sample coverage versus total population, grossing up from the results of the survey, and adjustment for non-response to the survey.

1.3.7.2 Rectifications on the basis of tax audits (VAT fraud)

The data reported to the STATEC unit in charge of the business register by the “Administration de l’Enregistrement et des Domaines” includes information on declared turnover, administrative tax assessments, tax returns audited and rectifications as a result of audits or on-site inspections.On the basis of the rectifications made by the “Administration de l’Enregistrement et des Domaines” after auditing the declared turnover by businesses, average adjustment rates (3 year averages) are calculated by NACE activity while making a distinction between individual business and companies. These adjustment rates are applied to the turnover and output of unaudited businesses when compiling the production accounts by industry and sector (for audited businesses, the rectified figures are already included in the basic data used to calculate the accounts).This adjustment covers non-exhaustiveness type N6 in terms of the N1-N7 taxonomy of the tabular approach to exhaustiveness.

1.3.7.3 Tips

For hotel, restaurant services, taxis and hairdressing services output, value added and compensation of employees are adjusted for tips which are common for these services. Tipping percentages judged to be reasonable by representatives of the different industries have been used.

Table 1.4: Tipping rates

Activity Rate for tips

Restaurants 3% of the turnover (excluding resales)

Cafés and bars 5% of the turnover (excluding resales)

Hotels with restaurant 2% of the turnover (excluding resales)

Hotels without restaurant 1% of the turnover (excluding resales)

Taxis 5% of turnover

Hairdressing and other beauty treatment

7% of turnover (excluding resales)

This adjustment covers non-exhaustiveness type N7 in terms of the N1-N7 taxonomy of the tabular approach to exhaustiveness.

1.3.7.4 Undeclared work

Undeclared work is explicitly taken into account for estimating the following services: paid domestic services, undeclared private teaching courses undeclared construction or extensions to dwellings.

This adjustment covers non-exhaustiveness types N1 or N7 in terms of the N1-N7 taxonomy of the tabular approach to exhaustiveness.

1.3.7.5 Representatives of foreign companies

Finally the activity of representatives of foreign companies that have no branch as such within the country is estimated on the basis of the salaries paid by these companies (source: social security statistics).This adjustment covers non-exhaustiveness type N7 in terms of the N1-N7 taxonomy of the tabular approach to exhaustiveness.

1.3.7.6 Illegal activities

Trading of drugs and prostitution services are considered as relevant illegal activities for the Luxembourg economy and therefore adjustment are done for these types of activity. This is not the case for smuggling.This adjustment covers non-exhaustiveness type N2 in terms of the N1-N7 taxonomy of the tabular approach to exhaustiveness.

For general government, STATEC can rely on exhaustive administrative data sets. No special adjustment to guarantee exhaustiveness is necessary.

Table 1.5: Adjustments for exhaustiveness

Transaction Exhaustiveness Adjustments

N1 N2 N3 N4 N5 N6 N7 Total

Illegal Economy Output of goods and services (at basic prices)

0.0 86.9 0.0 0.0 0.0 0.0 0.0 86.9

Intermediate consumption (at purchasers' prices )

0.0 0.5 0.0 0.0 0.0 0.0 0.0 0.5

Gross value added (at basic prices)

0.0 86.5 0.0 0.0 0.0 0.0 0.0 86.5

Tips Output of goods and services (at basic prices)

0.0 0.0 0.0 0.0 0.0 0.0 42.1 42.1

Intermediate consumption (at purchasers' prices )

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Gross value added (at basic prices)

0.0 0.0 0.0 0.0 0.0 0.0 42.1 42.1

Undeclared Work

Output of goods and services (at basic prices)

145.6 0.0 0.0 0.0 0.0 0.0 0.0 145.6

Intermediate consumption (at purchasers' prices )

61.0 0.0 0.0 0.0 0.0 0.0 0.0 61.0

Gross value added (at

84.6 0.0 0.0 0.0 0.0 0.0 0.0 84.6

Transaction Exhaustiveness Adjustments

N1 N2 N3 N4 N5 N6 N7 Total

basic prices)

Vat fraud with complicity

Output of goods and services (at basic prices)

0.0 0.0 0.0 0.0 0.0 134.9 0.0 134.9

Intermediate consumption (at purchasers' prices )

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Gross value added (at basic prices)

0.0 0.0 0.0 0.0 0.0 134.9 0.0 134.9

Representatives of foreign companies

Output of goods and services (at basic prices)

0.0 0.0 0.0 0.0 0.0 0.0 25.5 25.5

Intermediate consumption (at purchasers' prices )

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Gross value added (at basic prices)

0.0 0.0 0.0 0.0 0.0 0.0 25.5 25.5

Total Output of goods and services (at basic prices)

145.6 86.9 0.0 0.0 0.0 134.9 67.5 435.0

Intermediate consumption (at purchasers' prices )

61.0 0.5 0.0 0.0 0.0 0.0 0.0 61.5

Transaction Exhaustiveness Adjustments

N1 N2 N3 N4 N5 N6 N7 Total

Gross value added (at basic prices)

84.6 86.5 0.0 0.0 0.0 134.9 67.5 373.5

2010; millions EURO

1.4 Outline of the income approach

1.4.1 Reference frameworkTable 1.4 Gross domestic product at market prices in the income approach

Code Transaction Value

D1 Compensation of employees 19 899

B2G+B3G Gross operating surplus and mixed income 15 634

D2 Taxes on production and imports 4 933

D3 Subsidies 520

B.1*g Gross domestic product at market prices 39 947

2010; millions EURO

In Luxembourg’s national accounting system, only the production and expenditure approaches are available as independent compilation processes. The income approach, in contrast, is merely residual.The income approach places the emphasis on valuing compensation of employees (D.1), other taxes (D.29) and other subsidies (D.39) on production, while the operating surplus and mixed income are calculated as residual.

1.4.2 Main data sourcesThe same sources of data are used as for the production approach, e.g. the Annual Structural Business Survey, the accounting documents of large service enterprises, accounting statistics of supervisory bodies, general government budgets and accounts which include all of the information on compensation of employees. Additional data sources are:

• statistics relating to paid employment and compensation of employees are calculated by the “Inspection de la Sécurité Sociale2” in close cooperation with STATEC on the basis of data originating from the “Centre commun de la Sécurité Sociale” who is managing the affiliation process with legal social security . These statistics cover:

• gross wages; • bonuses;

2 Inspection de la Sécurité Sociale is the supervising body of the legal social security in Luxembourg. It collects as well statistics from the legal social security entities in Luxembourg. (http://www.mss.public.lu/acteurs/igss/index.html)

• employees’ and employers’ social contributions broken down by status (employed, self-employed, civil servants), duration of work (full or part time), sex and residence of the employee, along with the institutional sector, activity defined by NACE classification and residence of the employer;

• tax statistics from the various tax administrations (Administration des Douanes et Accises, Administration de l’Enregistrement et Administration des contributions directes) and from the Ministère de l’Intérieur (for municipal taxes);

• local and central government budgets and accounts for other subsidies on production.

1.4.3 Compensation of employeesCompensation of employees (D.1) includes:

• gross wages and salaries (D.11) prior to the deduction of income tax and employees’ social-security contributions; gross wages and salaries also include compensation for public holidays or paid leave, wages and salaries paid in kind, bonuses, allowances, 13th and 14th months, high-cost-of-living and remoteness allowances, commissions, tips, fees and percentages paid to employees, etc; • Employers’ social contributions (D.12), broken down into actual social contributions (D.121) and imputed social contributions (D.122).

Compensation of employees by industry and sector is evaluated on the basis of the same statistical sources as the other elements in the production approach. Statistics from “Inspection de la Sécurité Sociale” are mainly used to check the data from those other sources and to break compensation down by employees’ status in cases where the basic statistics do not provide such breakdowns and to estimate actual compulsory social contributions. For this component different adjustments are done in order to assure compliance with SEC2010 and exhaustiveness.

Table 1.6: Summary of the adjustments to compensation of employees

Data Value

Source data 19761

Data validation 0

Conceptual adjustment 23

Adjustment for exhaustiveness 116

N1 42

N2 32

N7a 42

Total adjustments 139

Total 19899

2010; millions EURO

1.4.4 Other taxes on productionOther taxes on production (D.29) are taken directly from general government accounts.

1.4.5 Other subsidies on productionLike other taxes, other subsidies on production (D.39) are taken directly from the public authorities’ accounts.

1.4.6 Gross operating surplus and mixed incomeSince the income approach does not exist as an independent method of GDP evaluation, gross operating surplus and mixed income are determined by deducting compensation of employees (D.1) and other taxes on production (D.29) from the gross value added at basic prices (as determined by the production and expenditure approaches) and by adding the other subsidies on production (D.39), or by deducting compensation of employees (D.1) and taxes on production and imports (D.2) from GDP and adding subsidies (D.3).

1.4.7 Consumption of fixed capitalConsumption of fixed capital (P.51c) is the decline in value of fixed assets owned, as a result of normal wear and tear and obsolescence. The estimate of decline in value includes a provision for losses of fixed assets as a result of accidental damage which can be insured against. (ESA2010, paragraph 3.139).Consumption of fixed capital is calculated during valuation of gross fixed capital stock and net fixed capital stock. As no direct survey-based observations for fixed assets are available, the capital stock is estimated using the Perpetual Inventory Method (PIM). 24 product categories are covered.

1.4.8 Main approaches taken with respect to exhaustivenessSTATEC considers that the data sources for taxes, subsidies and compensation of employees have a high degree of exhaustiveness since they stem from closely monitored administrative sources. Nevertheless national accountants need do some adjustments to assure exhaustiveness especially

for the component of compensations of employees (sub component wages and salaries). These adjustments concern:

Undeclared paid domestic services for cleaning Revenues from illegal activities Representatives of non-resident companies Tips and gratuities for different services

Table 1.7: Summary of the adjustments for exhaustiveness to compensation of employees

Adjustment methodType of non-exhaustiveness

N1 N2 N3 N4 N5 N6 N7 Total

Undeclared domestic services 42 42

Revenues from illegal activities 32 32

Representatives of non-resident companies

23 23

Tips and gratuities 42 42

Total 42 32 0 0 0 0 65 139

2010; millions EURO

1.5 Outline of the expenditure approach

1.5.1 Reference frameworkFor the expenditure approach, GDP can be calculated as the sum of the end use of goods and services, with imports deducted.Luxembourg’s national accounts are largely based on the production approach. The expenditure approach is not completely independent, despite the fact that it is largely estimated from databases and methods that are separate from those used for the production approach. Thus, as the various aggregates for the expenditure approach are compiled, reference elements from the production approach are often used, if only to validate an intermediate stage of the compilation of the expenditure approach by comparing a number of sources. The GDP estimate arrived at via the expenditure approach is not therefore fully independent. In fact, the definitive amounts for the various components of expenditure are determined using the annual supply-and-use tables.

Table 1.5 GDP according to the expenditure approach

Code Aggregate Value

P.3 Final consumption expenditure 20126

P.3 Household final consumption expenditure 12725

P.3 Final consumption expenditure of NPISHs 576

P.3 Public Administration final consumption expenditure 6826

P.5 Gross capital formation 7266

P.51 Gross fixed capital formation 7026

P.52 Changes in Inventories 462

P.53 Acquisition less disposals of valuables -222

P.6 Exports of goods and services 69949

Exports of goods 15964

Exports of services 50453

Final consumption expenditure of non-residents 3532

P.7 Imports of goods and services (FOB) 57394

Imports of goods (FOB) 16641

Imports of services (FOB) 39656

Final consumption expenditure of residents while abroad 1097

Gross domestic product at market prices (P.3+P.5+P.6-P.7) 39947

2010; millions EURO

1.5.2 Households’ final consumption expenditure

Definition:“Final consumption expenditure (P.3) consists of expenditure incurred by resident institutional units on goods or services that are used for the direct satisfaction of individual needs or wants or the collective needs of members of the community. (ESA2010, paragraph 3.94)Household final consumption expenditure includes the following borderline cases:a) services of owner-occupied dwellings;

b) income in kind, such as:

a. goods and services received as income in kind by employees;

b. goods or services produced as outputs of unincorporated enterprises owned by households that are retained for consumption by members of the household. Examples are food and other agricultural goods, housing services by owner-occupiers and household services produced by employing paid staff (servants, cooks, gardeners, chauffeurs, etc.);

c) items not treated as intermediate consumption, such as:

a. materials for small repairs to and interior decoration of dwellings of a kind typically carried out by tenants as well as owners;

b. materials for repairs and maintenance to consumer durables, including vehicles;

d) items not treated as capital formation, in particular consumer durables, that continue to perform their function in several accounting periods; this includes the transfer of ownership of some durables from an enterprise to a household (see transactions in existing goods, ESA2010, paragraph 3.181);

e) financial services directly charged and the part of FISIM used for final consumption purposes by households;

f) insurance services by the amount of the implicit service charge (see ESA2010, paragraph 3.74);

g) pension funding services by the amount of the implicit service charge (see ESA2010, paragraph 3.74);

h) payments by households for licences, permits, etc. which are regarded as purchases of services (see ESA2010, paragraphs 4.79 and 4.80);

i) the purchase of output at not economically significant prices, e.g. entrance fees for a museum (see ESA2010, paragraph 3.41).

Table 1.8 HFCE by concept

Household final consumptioon expenditure - by concept

on the domestic territory 15 159.2

of residents abroad 1 097.1

of non-residents on the domestic territory 3 531.7

of residents on the domestic territory and abroad 12 724.6

2010; millions EURO

Table 1.9 HFCE by purpose

Household final consumption expenditure by purpose - domestic concept

Coicop

FOOD AND NON-ALCOHOLIC BEVERAGES 01 1 438.9

Household final consumption expenditure by purpose - domestic concept

Coicop

Food 01.1 1 259.1

Non-alcoholic beverages 01.2 179.8

ALCOHOLIC BEVERAGES, TOBACCO AND NARCOTICS 02 1 295.4

Alcoholic beverages 02.1 319.2

Tobacco 02.2 918.4

Narcotics 02.3 57.8

CLOTHING AND FOOTWEAR 03 776.2

Clothing 03.1 631.4

Footwear 03.2 144.8

HOUSING, WATER, ELECTRICITY, GAS AND OTHER FUELS 04 3 393.6

Actual rentals for housing 04.1 517.0

Imputed rentals for housing 04.2 2 080.7

Maintenance and repair of the dwelling 04.3 192.7

Water supply and miscellaneous services relating to the dwelling 04.4 164.7

Electricity, gas and other fuels 04.5 438.5

FURNISHINGS, HOUSEHOLD EQUIPMENT AND ROUTINE HOUSEHOLD MAINTENANCE

05 986.7

Furniture and furnishings, carpets and other floor coverings 05.1 326.1

Household textiles 05.2 87.4

Household appliances 05.3 110.8

Glassware, tableware and household utensils 05.4 45.5

Tools and equipment for house and garden 05.5 48.9

Goods and services for routine household maintenance 05.6 368.1

HEALTH 06 335.9

Medical products, appliances and equipment 06.1 236.1

Out-patient services 06.2 73.6

Hospital services 06.3 26.2

TRANSPORT 07 2 596.8