pad-77-70 government agency transactions with the … · government agency transactions with the...

TRANSCRIPT

DOCUVFNT RESUME

03102 - .A21732841

Government Agency Transactions with the Federal Financing Bank

Should Be Included on the Budget. PAD-77-70; B-174958. Augu-t 3,

1977. 41 pp. + 2 appendices (15 pp.).

Report to the Congress; by Flmer B. Staats, Comptroller General.

Contact: Program Analysis Div.Budget Function: General Government (800); Interest: Other

Interest (902).Organization Concerned- Department of the Treasury; Federal

Financing Bank; Office of anagement and Budget.congressional Relevance: House Committee on Banking, Finance ani

Trban Affairs: Congress,Authority: Federal Financing Bank Act 12 U.S.C. 2281). P.L.

93-135, title II.

Excluding the Federal Financing Bank from Federal

budget totals and other questionable budget practices combine to

produce an inadequate and incomplete picture of Federal credit

assistance. Findings/Conclusions: In its 4 years of operation,the Federal Financing Bank hes helped agencies to borrow money

at a cost savings. Although it was oricinally thought that the

Bank would finance its activity by issuing its own securities in

the private money and capital markets, nearly all of the Bank's

borrowing has been from the Department of the Treasury. This

borrowing arrangement saves money for agency borrowers and at

present has small effect upon debt management and monetary

policy. Problems created by the off-budget status of the Bank

combine with other deviations of current budget practices to

provide an understatement of federal outlays. Purchase of

Government-guaranteed borrowings is one of the most troublesome

aspects of the Bank's off-budget status. Recommendations:Congres'; should: require that the Bank's receipts and

disbursemets be included in the Federal budget totals; require

that the receipts and disbursements of all off-budget Federal

agencies that borrow from the Bank be included in the budget

totals: require that sales of Certificates of Beneficial

ownership be treated as borrowing it. agency budgets rather than

as asset sales; and monitor the 3ank's growth ti determine when,

if ever, the indirect costs of the current borrowing arrangement

with the Treasury outweigh the benefits of savings achievablR oa

agency borrowing that this practice provides. (Authsr/SC)

REPORT TO TiHE CONGRESS

BY THE' COMPTROLLER ,GENERAL OF THE UNITED STATES

Government Agency TransactionsWith The Federal Financing BankShould Be Included On The Budget

In its 4 years of opera-ion, the Federal Fi-nancing Bank has helped Federal agencies bor-,ow money, at a cost savings. However, thetransactions of ;he Federal Financing Bankaffect the Gov:rnment's budget and policy.

Excluding he Federal Financing Bank fromFederal budget totals and oher questio)ablebudget practices combine to produce aninadequate and incomplete picture of Federa,credit assistance. The current borrowing ar-rangement w;th the reasury saves monev foragency borrowers and at oresent has smalleffects upon debt management and monetarypolicy.

PAD-77-70 AUGUST 3, 1977

COMPTROLLER GENERAL OF THE UNITED STATAsWASINGTON, D.C. 20g48

B-174958

To the President of the Senate and theSpeaker of the House of Representatives

This report is an analysis of the problems associatedwith the off-budget status of the Federal Financing Bankand its borrowing relationship with the Treasury. Neitherthe Bank's status nor its borrowing arrangement is crucialto the fundamental intermediation role the Bank was in-tended to play. They result, however, in real costs andinefficiencies.

The report addresses two issues:

-- What is the best means of reflecting thecredit assistance activity of the FederalGovernment in the budget while preservingthe benefits from the intermediation rolethe Federal Financing Bank was intended toplay?

-- Does the borrowing arrangement between theFederal Financina Bank and the Treasuryhave any significant ill effects on theconduct o Treasury debt management andmonetary policy?

We made our review pursuant to the Budget and AccountingAct, 1921 (31 U.S.C. 53), and the Accounting and Auditing Actof 1950 (31 U.S.C. 67).

We are sending copies of this report to the Director,Office of Management and Budget, and the Secreta of theTreasury.

Comptroller Generalof the United States

COMPTROLLER GENERAL'S GOVERNMENT AGFNCY TRANSACTIONSREORT TO THE CONGRESS WITH THE FEDERAL FINANCING BANK

SHOULD BE INCLUDED ON THE BUDGET

D I G E S T

The Federal Financing Bank was established onDecember 29, 1973. It was created to functionas a financial go-between, purchasing the dif-ferent kinds of debt and guaranteed obligationsof Federal agencies and pri:,ate borrowers andsubstituting its own borrowin.g for that of theagencies. Its accomplishments have been note-worthy. Throucih coordination of the timing as-pects of agency borrowing and its standardiza-tion, agency borrowing costs have been reduced.

Two aspects of the Bank's activities are notstrictly related to its essential role as afinancial conduit. First, when the FedfralFinancing Bank was established, its receiptsand disbursements were excluded from the budgettotals. Second, it was originally thought thatthe Bank would finance its activity y issuingits own securities in the private money andcapital markets. Instead, nearly all of theBank's borrowing has been from the Departmentof the Treasury.

This report considers how these factorscause substantive changes in the meaning ofFederal outlays and deficits, the design ofFederal assistance programs, and the alloca-tion of Federal resources. It also considerschanges that have occurred in the level, com-position, and maturity structure of the Federaldebt, which may in turn affect the conduct ofTreasury debt management and monetary policy.

These changes are not related to the basicrole that the Bank was intended to play. Theyrelate to the way the Bank's transactionsintermingle with questionable budget practicesto produce an inadequate and incomplete pic-ture of Federal credit assistance activity.They could also potentially relate to the cur-rent borrowing arrangement with the Treasury.

The problems created by the off-budcet statusof the Bank combine with other deviations of

IauSurs. upon removal, the report PAD-77-70covwr*td should noted heron.i

current budget practices from those recommendedby the President's Commission on Budget Concepts.Most notable among these are the budget treat-ment of Certificates of Beneficial Ownership,Bank purchases of agency assets, and Bank pur-chases of Government-guaranteed bcrrowings ofprivate entities. The combined effect of thesefactors provides an understatement of ederaloutlays estimated to accumulate to nearly $30billicn by the end of fiscal year 19?8.

Federal Finaincing Bank purchases of theGovernment-quaranteed borrowings of privateentities is ne of the most troublesome con-sequences of the Bank's off-budget status.This practice has a potential for failures todesign into loan guarantee programs the essen-tial element of risk sharing and the poten-tial for oversubsidization when guaranteepLZgrams are appropriate and use of creditassistance devices when such devices may beinappropriate.

Including the Bank's receipts and disbursementsin the budget totals would eliminate mst ofthe understated outlays that currently resultfrom the way credit assistance that goesthrough the Bank is reflected in the budget.But, it would not greatly increase the ration-ality of decisions made regarding allocationsof resources among Federal assistance programs.

Concerns about on-budget status for the Bankare valid largely because of the budget treat-ment given certain credit assistance trans-actions. If budget conventions were changed toreflect the true nature of these transactions,much of the agency borrowing currently goingthrough an on-budget Bank would continue at acost savings. Bank origination of theGovernment-backed borrowings of private entitiesis a questionable practice, and an on-budgetFederal Financing Bank might eliminate thispractice. The benefit;3 of reduced interestcosts to assisted private borrowers are ques-tionable, and the cost savings from thispractice may also be illusory.

ii

When the Bank finances its purchases of agencydebt through the Treasury, the liquidity mix ofpublic holdings of the Federal debt is changed.The Treasury finances its lending to the Bankby issuing its own securities. Treasury secu-rities are shorter term than the displacedagency securities the Bank purchases and, inall likelihood, the securities that the Bankwould sell in the private money and capitalmarkets if it could not rely on the Treasury.

Because of this, the maturity structure of theFederal debt is shortened. We estimate that bythe end of fiscal year 1978, the average matur-ity of the Federal debt will ' ve been reducedby about 3 percent as a rsult f the Bank'soperations and its borrowing arrangement withthe Treasury. We also estimate that the pub-lic's short-term Federal dent holdings willhave increased by about $12.1 billion and thatlong-term Feaeral debt holdings will have beenreduced by nearly the same amount as a resultof the Bank's activities and its borrowing ar-rangement with the Treasury.

Theoretically, this compositional shift in thematurity structure of the Federal debt shouldaffect the Treasury debt management through itseffect on the term structure of interest rates.It may also affect monetary policy by providingcommercial banks with a greater stock of read-ily marketable assets that may be easily liq-uidated co finaince loan expansion at the sametime that the Federal Reserve Board is tryingto curb loan expansion.

The empirical evidence generally supports thetheory. But, the Bank's operations are smallin relation to the operations of the Treasuryand the commercial banking system. Thus, thecompositional shift out of agency securitiesinto Treasury securities induced by the Bankis estimated to have small effects on thematurity structure of the Federal debt, theterm structure of interest rates, or monetarypolicy through fiscal year 1978. The Bank'slending activity would have to grow quite largebefore such effects could be considered serious.

Tear Shet

iii

AGENCY COMMENTS

Formal agency comments on this report were notrequested. The draft report, however, wasreviewed by staff of the Office of Managementand Budget and the Department of the Treasuryon an informal basis. These comments wereconsidered in preparing the final report.

Treasury officials maintain that the overallmaturity of the Bank's portfolio is about 4years. The calculations in chapter 4 includethe Bank's transactions in agency debt andCertificates of Beneficial Ownership in thefourth quarter of 1976 and the first quarterof 1977. Therefore, they do not include allof the Bank's transactions since its inception.

RECOMMENDATIONS

In view of te current and potential consequencesresulting fr.m the off-budget status of theFederal Financing Bank, deviations of currentfrom recommended budget treatment of some Fed-eral credit assistance activity, and the curLentborrowing arrangement between the Bank and theTreasury, GAO recommends that the Congress:

-- Require that the Bank's receipts and disburse-ments be included in the Federal budgettotals.

-- Require that the receipts and disbursementsof all off-budget Federal agencies that bor-row froma the Bank be included in the budgettotals.

-- Require that sales of Certificates of Bene-ficial Ownership be treated as borrowing inagency budgets rather than as asset sales.

-- Monitor the Bank's growth to determine when,i. ever, the indirect costs of the currentborrowing arrangement with the Treasury out-weigh the benefits of savings achievable onagency borrowing that this practice provides.

iv

C o n t e t s

Page

DIGEST

CHAPTER

I INTRODUCTION 1Perspective of the report 2

2 FFB'S ROLE, FUNCTIONS AND IMPLICATIONS 5FFB as an intermediary 5Effect of FFB transactions on

Federal outlays 7Budget outlays and the nature of

Federal assistance 7Federal debt flows 10

3 IMPLICATIONS OF FFB'S OFF-BUDGET STATUS 12Recommendations of the President'sCommission on Budget Concepts 13

Potential for poor design of Feeralassistance programs 16

Effect on outlay totals of anon-budget FFB 19

Should the FFB be placed on thebudget? 20

Recommendations to the Congress 24

4 IMPLICATIONS OF FFB OPERATIONS ON THECONDUCT OF DEBT MANAGEMENT AND MONETARYPOLICY 26

Debt nianagment policy 26Monetary policy 35Summary 39Agency comments 40Recommendation to the Congress 41

APPENDIX

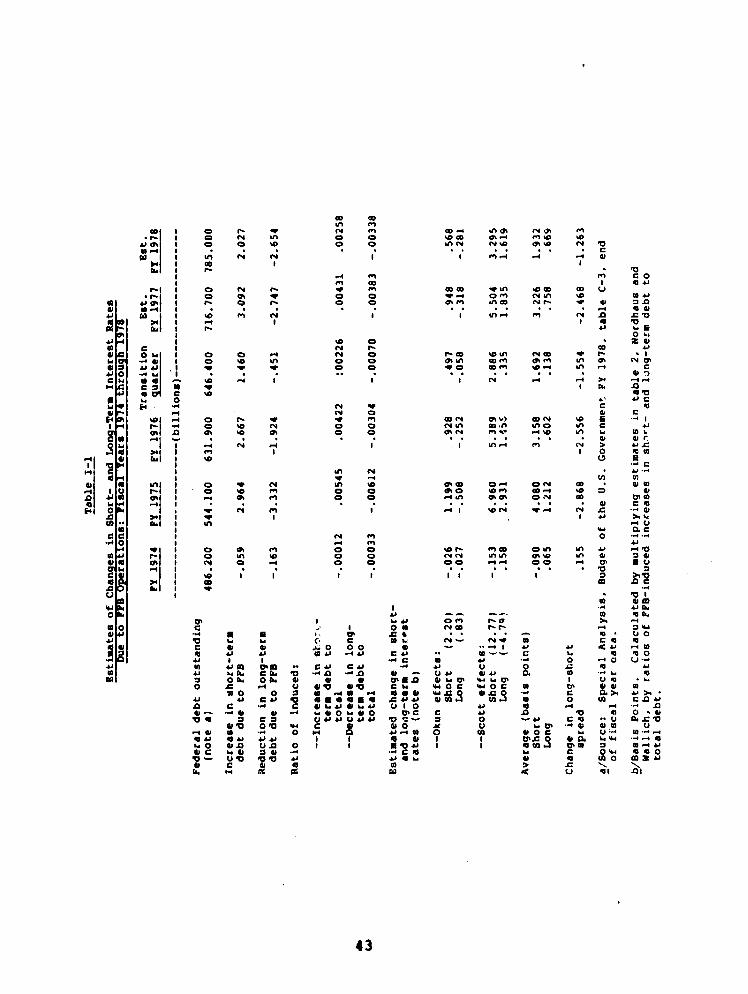

I Estimated effect of FFB-induced changesin the maturity composition of theFederal debt on interest rates 42

II Estimated commercial bank portfoliorecompositions during periods ofrestrictive monetary policy 45

ABBREVIATIONS

CBO Certificate of Beneficial Ownership

FFB Federal Financing Bank

GAO General Accounting Office

CHAPTER 1

INTRODUCTION

One of the more significant innovation; in Federalfinance in recent years was establishing the FederalFinancing Bank (FFB) on December 29, 1973. According totestimony given for PFB's establishment, it was neededbecause: 1/

"Many existing 4.deral agencies are nowrequired to finance their programs directlyin the securities markets * * *. Theseagencies must develop their own financingstaffs, and their abilities to cope withtheir principal rogram functions arelessened by the eed also to deal with thecomplex debt mar erent operations essentialto minimizing their borrowing costs andavoiding cash flow problems which coulddisrupt their basic lending programs.

qInterest costs of the various Federal agencyfinancing methods rnrmally exceed Treasuryborrowing costs by substantial amounts, despitethe fact that these issues are backed by theFederal Government. Borrowing costs areincreased because of the sheer proliferationof competing issues crowding each other in thefinancing calendar, the cumbersome nature ofmany of the securities, and the limited marketsin which they are sold * * *.

"Under the proposed legislation these essentiallydebt management problems could be shifted fIthe program agencies to the Federal FinancingBank. Many of the obligations which are nowplaced directly in the private market undernumerous Federal programs would instead befinanced by the Bank. The Bank in turn wouldissue its own securities. The Bank would havethe necessary experti., flexibility, volume,

1/ U.S. Congress, House Committee on Ways and Means, FederalFinancing Bank Act Hearings, Mar. 1, 1973, 93rd Cong.,Ist sess., p. 2.

1

and marketing power to minimize financingcosts and to assure an effective flow ofcredit for programs established by theCongress."

FFB has reduced the cost of borrowing by the executivebranch agencies. FFB'i establishment coordinated at leastsome agency borrowing. Standardizing the financial instru-ments used to finance Federal credit programs has occurredsince all of FFB's current borrowing is from the Treasury.

We believe that creating a central facility for coor-dinating the debt management aspects of Federal credit pro-grams is a good idea. The benefits of coordinating, stand-ardizing, and hence reducing costs that accrue to such aninstitution within the Federal Government are substantial.In 1975 the cost savings resulting from FFB and its borrowingarrangement with the Treasury was estimated to be $70 million.These savings are partly due to FFB's borrowing from theTreasury instead of the public.

PERSPECTIVE OF THE REPORT

Indirect costs resulting from FFB are not fully recog-nized. This report analyzes these indirect costs. Some ofthe costs are potential; isae currently exist. They may begrouped into two main categories. First, FFB affects themeaning of Federal budget outlays and deficits. Relatedto this are considerations regarding the potentials foralterations in credit program design and questionablechoices of Federal policy tools to achieve particularprogram objectives. Second, a potential exists for FFBto adversely affect the conduct of debt management andmonetary policy. In this latter context, debt mangementpolicy does not refer to the coordination aspects of agencyfinancing in which FFB's function provides definite bene-fits. Instead, we are referring to the Treasury debtmanagement policy. Neither the off-budget status of FFB norits borrowing arrangement with th- Treasury is essential toits basic intermediation role.

In he next chapter we discuss certain aspects of theFederal Financing Bank Act, explain the basic role that FBplays as a financial intermediary, and describe the types oftransactions that FFB engages in. This is provided as a back-ground for the analysis in the remainder of the report.

2

In chapter 3 the ways in which the off-budget status ofFFB affects the meaning of budget outlays and deficits arediscussed. FFB was established as an off-budget ent:ity, butwe believe that its operations are an integral part of theFederal Government operations and should be assessed t-o-gether with other Federal operations within the context ofthe Federal budget. FFB's off-budget status removes a largesegment of direct lending activity from the Federal budgettotals.

Related to this are concerns about FFB's

--purchase of Government-backed loans that wouldhave otherwise been financed in private markets;

-- budget treatment of Certificates of BeneficialOwnership (CBOS), 1/ most notably those of-theFarmers Home Adminstration, and FFB's purchaseof these securities; and

-- purchase of agency assets that would have other-wise been sold in private capital markets.

Under current budget conventions, each of these transac-tions is treated in a way which disguises the true natureof the transaction and leads to an understatement of thetotal financing activity of the Federal Government. All ofthese practices offer the potential for favoring credit as-sistance devices rather than alternative Federal assistancedevices, which may be more efficient in assuring the achieve-ment of program goals. This problem is most important incases in which FFB purchases the Government-backed borrowingof private entities. 2/

l/Certificates of Beneficial Ownership represent "ownership"of interests in a pool of loans made and still held by aselling agency. These securities are sold by the agencyand guaranteed by the Government. When they are sold, bystatute they are treated in the budget as a sale of a loanasset, although the loans in which CBOs nominally evidenceinterest are still held by the administering agency. Thereare no real benefits to purchasers from the transactions inthe underlying loans. GAO believes that sales of thesesecurities do not differ i a meaningful way from borrowingand should be so reflected in the budget.

2/An excellent source for the budget implications of FFB isRobert W. Kilpatrick and Thomas J. Cuny, The FederalFinancing Bank and the Budget, Executive Office of thePresident, Office of Management and Budget, TechnicalPaper Series BRD/FAB 76-1, Jan. 26, 1976.

3

Concerns are also expressed about FFB financing ofother off-budget activities.

In chapter 4 FFB's implications for the conduct of debtmanagement and monetary policy are analyzed. It was origi-nally thought that FFB would generally finance its lend-ing by borrowing in the private money and capital markets.The possibility of borrowing from the Treasury was not ruledout, however. Currently, all FFB borrowing is from theTreasury. Treasury funds its lending to FFB by issuing itsown securities, Treasury securities are more marketable thanthe agency securities that would have been issued in theabsence of FFB. They are also Etore marketable than FFB bor-rowings would have been if FFB could not have relied on theTreasury for financing. Much of the savings attributable touse of FFB is the result of tne greater marketability ofTreasury securities. However, these conditions have led toa shortened maturity structure of the Federal debt and haveincreased the liquidity and marketability of the public's assetholdings.

As a result of the current borrowing arrangement withthe Treasury, the efficiency with which debt management andmonetary policy are conducted may be affected. The way inwhich this happens is complex, but the existence of thisrelationship between alterations in the maturity structureof public asset holdings and conduct of stabilization policyis reasonably well established. Despite this relationship,the present size of FFB is insufficient to raise concernsabout detrimental effects. And, FFB would have to grow muchlarger before these effects would be cause for substantialconcern.

4

CHAPTER 2

FFB's ROLE, FUNCTIONS, AND IMPLICATIONS

The Federal Financing Bank functions as a financialintermediary or go-between. It either lends funds to orpurchases the loans of Federal agencies responsible for ad-ministering Federal credit programs and to those directlybenefiting from Federal credit assistance. It obtains thesefunds by issuing its own securities. Its borrowings areheld almost entirely by the Treasury. In this chapter wedescribe the types of transactions FFB engages in and theeffects of these transactions on the nature of Federalassistance. We also summarize the effects of these trans-actions o the meaning of budget outlays and deficits andon the composition of the Federal debt.

FFB AS AN INTERME"IARY

FFB was created on December 29, 1973, by the FederalFinancing Bank Act (12 U.S.C. 2281). Its purpose is spelledout in section 2 of the act.

"The Congress finds that demands for fundsthrough Federal and federally assisted borrowingprograms are increasing faster than the totalsupply of credit and that such borrowings arenot adequately coordinated with overall Federalfiscal and debt management policies. The purposeof this Act is to assure coordination of theseprograms with the overall economic and fiscalpolicies of the Government, to reduce the costsof Federal and federally assisted borrowingsfrom the public, and to assure that suchborrowings are financed in a manner leastdisruptive of private financial markets andinstitutions."

Section 9 of the act authorizes FFB to issue in theprivate markets and have outstanding up to $15 billion of itsown securities. FFB is also authorized to borrow from theSecretary of the Treasury without limit, subject to the Treas-ury's approval. Section 6 declares that FFB may purchase "anyobligation which is issued, sold, or guaranteed by a Federalagency."

It is clear from the testimony given prior to approvaluf the act that FFB was not intended to be a program agency.Neither FFB nor the Secretary of the Treasury is authorizedto make such judgments regarding the purposes of Federal

5

agency programs. Discretion is authorized only with regard tothe debt management aspects of an agency borrowing operation.Accordingly, section 7(b) prohibits the Secretary of the Treas-ury from withholding approval of an agency borrowing operationfor a period longer than 60 days unless there is a detailedexplanation of the Secretary's reasons for doing so. In nocase may approval be withheld for more than 120 days.

These above sections of the act imply that FFB is no morethan a financial conduit. Prior to FFB, agencies sought theTreasury's approval of the terms and timing of most offerings,though these relationships were not formalized in all cases.In this sense, the relationship of the agencies to the Treas-ury is unchanged by the creation of FFB.

Through creation of a centralized Federal intermediary,it was felt that FFB would be a more attractive source offinancing for agency borrowers than the private capital marketbecause FFB could borrow more cheaply. There is little doubtthat this is true. Lack of standardization, which translatesinto poor or nonexistent secondary markets, and the accompany-ing limited market interest in these securities caused inter-est rates to be higher than those that could be achievedthrough larger and more standardized FFB or Treasury offerings.

The potential benefits of FFB are related closely tothose that flow from any intermediation process. That is,interest rates are reduced because of an ability to offer amore attractive source of loanable funds financed through theissuance of claims that are more attractive to lenders thanface-to-face transactions. In spite of this, there are impor-tant differences between FFB and private sector intermediaries.For all practical purposes, FFB is a "blind" intermediary. Be-cause of the constraints outlined in its act, FFB is a captivelender with decisions regarding important considerations, suchas use of proceeds, outside of its control. The responsibilityfor those decisions remains with the borrowing or guaranteeingagency. Regardless of whether the original intent of the actwas that FFB would be a private market borrower, the fact isthat virtually all FFB borrowing has been from the Treasury.

FFB is one step removed from the discipline of themarket. Interest rates set on its borrowing are those which'the Treasury faces and adjusts to in view of its borrowingcosts. The interest rates set on the loans FFB makes to theagencies or private credit market borrowers are set at a one-eighth of one percentage point markup from the Treasury

6

borrowing rates. In our report 1/ we found that FFB hac ac-cumulated a surplus of $126 million. We recommended that FFBdiscontinue the practice of adding a fraction of a percent tothe rates it charges on its loans in view of the lack of evi-dence supporting the existence of risks faced y FFB or theTreasury under the current arrangement that the markup issupposed to cover.

FFB is nothing more than a financial conduit. Neverthe-less, FFB's existence has affected financial flows between theprivate and public sectors, and the alterations in these flowshave repercussions which go beyond being strictly financial.

EFFECT OF FFB TRANSACTIONSN FDERAL OUTLAYS

FFB engages in four types of transactions. It purchases:

1. On- and off-budget agency debt securitis that wouldotherwise have been sold to the private apital mar-kets.

2. Agency Certificates of Beneficial Ownership that areguaranteed by the issuing agency and would otherwisehave been sold in private capital markets.

3. Agency assets guaranteed by the agency that wouldotherwise have been sold to private capital markets.

4. Federally guaranteed borrowings of nongovernmentalentities that would otherwise have been sold in theprivate capital markets.

Important differences exist between these transactions.These differences currently affect Federal budget outlaysand the level and composition of Federal indebtedness. Theyalso potentially affect choices made between types of Federalassistance devices.

BUDGET OUTLAYS AND TENATURE OF FEDERAL ASSISTANCE

Except for Federally guaranteed loans to private bor-rowers, the paper which Federal agencies sell to FFB is used

1/"Audit of the Financial Statements of the Federal FinancingBank--Fiscal Years 1975 and 1976."

7

mainly to finance direct lending programs. 1/ Mone isborrowed by agencies and then it is loaned out. T'ere aretwo basic ways to do this. Government agencies can borrowfunds throuah issuance of their own debt obligations andloan t'ie roceeds from this borrowing, taking back pRdershowing the obligation of the borrower t pay back principaland interest. Or, they can make loans and then sell thatpaper in private capital markets.

In the first case, t;.e Government retains ownership ofthe loans agencies have made. In the second case, ownershipof the loan is transferred to the private sector; and thepaper showing the loan, which is sold by the agency, isGovernment-backed for principal and interest. 2/

In the case of agency obligations and CBOs, the firstmethod of financing is used. When agency assets are sold,the second method of financing is used. 3/

Two aspects of these three types of transactionsneed to be emphasized. First, the paper sold in all threeof these transactions is used to finance direct loans.Regardless of whether the paper is sold to the private capitalmarkets or FFB, the programs remain irect loan programs.Second, budget treatment of these transactions difflers.Borrowing (debt transactions) is not reflected in he budgetto . On ythe leni ir expenditure activity~nanced y the borrowing counts as outlays.

In agency lending financed by the sale of agency obliga-tions, the lending is reflected in the budget regardlessof whether the source of loanable funds is the privatecapital markets or FFB (provided that the agency is on thebudget) because sale of agency obligations is a debt trans-action.

l/Two exceptions to this are borrowing by the TennesseeValley Authority and the United States Postal Service.They borrow to finance direct expenditures.

2/In some cases, agencies may sell loans without such aguarantee. Since unguaranteed loans are relatively rareand since FFB could not purchase them, they are ignoredfor purposes of this report.

3/We consider CBO sales as agency borrowing. This is in con-flict with current budget treatment, but iE supported bythe recommendations of the President's Commission onBudget Concepts.

8

In the case of an asset sale, though the FederalGovernment loars the funds, the administering agency offsetsthis loun outlay by selling the loan k9r-the private capitalmarkets or FFB. When the agency sells the loan to theprivate capital markets, it no longer holds the loan and,therefore, its original loan outlay is canceled by theproceeds from its sale. There was an outlay when the loanwas made, and there is a negative outlay when the loan issold. This same treatment applies when an agency sells aloan to FFB. That is, the net outlay effect in the agency'saccount is still zero. But the Federal Government stillretains possession of the loan; and, logically, the loanshould show up as an outlay in the budget as an asset purchase.There are two loan outlays--that made when the agency loansthe funds and that made when FFB purchases the loan from theagency. There is one receipt--the proceeds to the agency whenit sells the paper to FFB. But FFB's outlay does not show upon the budget totals because its outlays do not show up onthe budget.

Under existing budget conventions and existing statutes,CBO sales are treated exactly the same as asset sales eventhough the loans which CBOs finance are still held by theagency. 1/ Regardless of whether these securities are soldinto private capital markets or to FFB, thi outlay effect inthe agency account is the same. CBOs are :nt reflected in thebudget as borrowing. If CBOs were reflected in the budget asborrowing, as we believe they should, the loan outlays of theagency financed by CBO sales would be reflected in the budgetregardless of whether the private sector or FFB purchased

1/With regard to he Farmers Home Administration, PublicLaw 93-135, title II provides "That the SecLetary [ofAgriculture] may, on an insured basis or otherwise, sellany notes in the fund or sell certificates of beneficialownership therein to the Secretary of the Treasury, to theprivate market, or to such other sources as the Secretarymay determine. Any sale by the Secretary of notes or ofbeneficial ownership therein shall be treated as a saltof assets for the purpose of the Budget and AccountirAct, 1921, notwithstanding the fact that the Secretary,under an agreement with the purchaser or purchasers, holdsthe debt instruments evidencing the loans and holds orreinvests payments thereon for the purchaser or purchasersof the notes or of the certificates of beneficial ownershiptherein * * *

9

them. In terms of current budget treatment, when FFB pur-chases CBOs, the Federal Government retains the asset or loan.The agency's sale of this paper is reflected as a negativeoutlay, and the corresponding FFB outlay does not show up onthe budget.

When FFB purchases the guaranteed obligations of privateborrowers, guaranteed loans are converted into direct loans.When this occurs, Federal outlays that are not reflected inthe budget increase. The outlay effects of this transactiondo not appear in the administering agency's budget, regardlessof whether the source of funds for the Government-backed ob-ligations is the private securities market or FFB. Thispractice results in the most troublesome consequences forbudgetary control of resource transfers within the FederalGovernment and between the public and private sectors.

FFB's off-budget status leads to direct loans occurringoutside of the budget in the guise of guaranteed loans. Con-sequently, it offers the potential for a failure to designinto appropriate loan guarantee programs the essential in-gredients of risk sharing. In addition, the potential existsto favor credit assistance programs when they may not be ap-propriate. The potential for this to occur exists in allFFB transactions that occur off the budget under currentbudget conventions. It is most likely to be realized, how-ever, for FFB purchases of Government-guaranteed borrowingof private borrowers.

The aspects of FFB's off-budget status are discussedin the next chapter.

FEDERAL DEBT FLOWS

FFB's transactions affect both the level and composi-tion of Federal indebtedness. These effects are reviewedbriefly for each of the four types of transactions we havedescribed. In each of these transactions, it is importantto keep in mind that the ultimate source of funds is alwaysprivate money and capital markets.

1. FFB purchase of an agency obligation. Currently,,all FFB borrowing is from the Treasury. Treasury financesits loans to FFB by selling its own securities. Becauseof this, when agencies sell their obligations to FFB,agency debt held by the public is reduced (over what itwould have been) and holdings of the Treasury debt are in-creased. The level of Federal indebtedness is unchanged,but its composition does chanige. Agency debt is swappedfor Treasury debt.

10

2. FFB purchase of Certificates of Beneficial Owner-ship. Because CBOs are not presently considered agency debt,FFB s purchase of this paper raises the level of Federalindebtedness. We believe that CBOs should be consideredagency borrowing since the original loan remains in thehands of the agency. If one adopts this view, the levelof Federal indebtedness is unchanged, but its composition ischanged. Agency debt is swapped for Treasury debt.

3. FFB purchase of an agency asset. When th'.s trans-action occurs, the FeeralGovernment retains possessionof the loan. The transaction is financed through an in-crease in the Treasury debt, which increases the level ofFederal indebtedness over what it would have been had theloan been sold in the private capital markets.

4. FFB purchase of the guaranteed loans of privateborrowers The effect of this transaction on the Treasurydebt and on the level of Federal indebtedness is identicalwith the third transaction. The level of Federal indebted-ness increases, all of which is in the form of the Treasurydebt.

We believe, in a substantive sense, the first two typesof transactions change the composition of Federal indebted-ness, but not its level. Agency debt is swapped for Treasurydebt. In the last two types of transactions, Federal indebted-ness increases. All of the increase is in the form of Treasurydebt. This also involves a compositional change in Federalindebtedness because the Federal debt has a heavier concentra-tion of Treasury debt.

Changes in the composition and level of Federal debtaffect the liquidity mix of the public's asset holdings.These changes in liquidity mix have implications for theefficiency with which debt management and monetary policyare conducted. We address this issue in chapter 4.

11

CHAPTER 3

IMPLICATIONS OF FB'S OFF-BUDGET STATUS

Section ll(c) of the Federal Financing Bank Act placesthe receipts and disbursem.ents of the Federal Financing Bankoutside of the totals of the U.S. budget. To some extentFFB's off-budget status reflects the Department of theTreasury view that FFB is merely a passthrough mechanism forfinancing agencies using FFB. 1/ In this regard, Paul A.Volker, then Undersecretary of the Treasury for MonetaryAffairs, said:

"The Federal Financing Bank is a deviceto remove programs from the Fedeadl budget; noris it a device to bring programs back into thebudget. The Bank would in no way affect theexisting budget treatment of Federal creditprograms. If a program is now financed outsideof the budget, that treatment would continue.If a program is now financed in the budget, thattreatment would continue. The bank is intendedto improve the financing of all Federal borrowingactivities regardless of theii budget treatment." 2/

This statement does not address the appropriateness ofthe "existing budget treatment." Under the FFB arrangement,the way in which budget totals reflect credit assistance ac-tivity does not change. Regardless of FFB, guaranteed loansappear outside the budget; CBO sales are still used to offsetagency lending, asset sales are similarly treated, directloans by on-budget agencies show up in the budget, and loansby off-budget agencies do not.

Concern about on-budget status for FFB rests on a pre-servation of budget neutrality. Related to this is thecontentior that because of outlay effects which would resultwith an on-budget FFB, agencies whose credit assistance ac-tivity is currently not reflected in the budget may have toreturn to the private capital markets for borrowing needs to

1/The Federal Financing Bank--Its Role and Functions, Congres-sional Research Service, Library of Congress, June 1975,p. CRS-6.

2/Hearings before the Committee on Banking, nhusing and UrbanAffairs, U.S. Senate, May 15, 17, and 18, 1972, p. 7.

12

avoid the outlay effects. This in turn would eliminate muchof the cost savings resulting from FFB.

But, the question remalnls whether ezxisting budget treat-ment best reflects Federal activities and, in addition,whether FFB's inclusion on the budget or changes in currentbudget practices would provide a different and more accuratedepiction of Federal credit assistance activities.

RECOMMENDATIONS OF THE PRESIDENT'SCOMMISSION ON BUDGET CONCEPTS

In its report, the Preident's Commission on Budget Con-cepts noted that

"To work well, the governmental budget processshould encompass the full scope of programs andtransactions that are within the Federal sectorand not subject to the economic disciplinesof the marketplace." 1/

According to this principle, if the marketplace does not imposethe discipline fcr allocating resources, the budget processmust. The Commission's 1967 report represents the last majorreview of budget presentation for the Federal Government.

The current budget treatment of FFB's transactionsdirectly, or indirectly in combination with other budgetpractices, deviates from the Commission's recommendations.

FFB is off the budget. By the Commission's criteriafor budget inclusion, FFB should be included in the budgettotals. The primary criterion for exclusion was that theactivity in question be fully owned and controlled by privateparties. FFB is unquestionably owned and controlled by theFederal Government.

FFB makes direct loans to on- and off-budget agenciesand to economic units outside the Federal establishment.The President's Commission on Budget Concepts ecomm.endedthat direct lending activity be included in the Budget totals.The Commission recognized that although loans were probablydifferent from direct expenditures in their economic impact,

1/Reprt of the President's Commission on Budget Concepts,U.S. Government Printing Office, Washington, D.C., Oct.1967, p. 24.

13

they still represent a transfer of resources within theFederal domain and between the public and private sectors. 1/

When FFB purchases on-budget agency debt obligations,the budget totals are not affected because the agency loansto the private sector from borrowed funds are reflected inthe budget. When FFB purchases off-budget agency debt obliqa-tions used to finance lending or direct expenditure activity,the transaction is not reflected in the budget totals becausethe activities of other off-budget agencies are excluded fromoutlays. When FFB loans funds to economic units outside ofthe Federal estab.ishment or purchases assets that would haveotherwise been purchased by the private sector, budaet out-lays are understated by the amount of FFB outlays. It is notrelevant to argue that had the private sector, instead ofFFB, been on the other side of either of these transactions,the budget totals would be unaffected. What is important isthat the private sector is not the source of funds; the Fed-eral sector is. nd, the outlays associated with those kindsof transactions do not appear in the budget totals.

FFB purchases CBOs from Government agencies. 2/ The mostnotable of these types of transactions are those which occurbetween FFB and the Farmers Home Administration. The discus-sion of budget treatment of CBOs is for the most part refer-enced to these securities. 3/

At the time of the Commission's report, sales of thesetypes of instruments were treated as asset sales. Proceedswere used to reduce the loan outlays of the agencies sellinqthis type of paper. The Commission was critical of thispractice and recommended that:

i/Report of the President's Commission on Budget ConceptsLU.S. Government Printing Office, Washington, D.C., Oct.1967, pp. 48 and 49.

2/CBOs are sold to FFB by Farmers Home Administration, whichis on the budget, and by the Rural Electrification andTelephone Revolving Fund of the Rural Electrification Ad-ministration, which is off the budget.

3/This is done to avoid greatly complicating the discussion.

14

"Participation certificates should be treated as a meansof financing, not s an offset to expenditures whichoperates to reduce a budget deficit." 1/

The reason for the recommended treatment was that saleof these instruments does not involve the transfer of aGovernment-held asset to the private sector. Instead, thetransaction involves sale of paper which is nominally tiedto an underlying pool of direct loans made, serviced, andstill held by the agency. No meaningful difference existsbetween the sale of a CBO and the sale of an agency obliga-tion. These certificates are borrowings and should betreated as such in the budget. 2/

The complexities introduced by FFB purchase of thesesecurities are as follows. If these certificates were giventhe recommended budget treatment, FFB purchases would haveno effect on outlay totals. The transaction would beidentical to FFB's purchase of on-budget agency debt withthe outlay reflected in the budget through the lending activityof the agency (provided the agency is on the budget). Sincecurrent budget practice does not treat the obligations inthe recommended way, FFB's purchase is an PB outlay, the pro-ceeds are used to reduce on-budget agency loan expenditures,and the budget totals are reduced by the amount of the FFBpurchase.

1/Report of the President's Commission on Bud et Concepts,U.S. Government Printing Office, Washington, D.C., Oct.1967, p. 48.

2/Treasury Secretary Fowler and Budget Director Schultze dis-agreed with this recommendation. They felt that the saleof any credit agency obligation should be treated as anoffset to loan expenditures. Their rationale was that aslong as these obligations do not call upon the revenues orgeneral borrowing of the Treasury, the net lending fig-ireshould reflect sale of these obligations as well as repay-ments. Regardless of which position one favors, FFB pur-chases of these instruments are a drain on Federal revenuesor borrowing and these outlays are not reflected in thebudget.

15

POTENTIAL FOR POOR DESIGN OFFEDERAL ASSISTANCE PROGRAMS

The Federal Financing Bank Act permits FFB to act aslender when agencies guarantee the debt of private sectorborrowers. FFB purchases only fully guaranteed obligations;most of these are securities market instruments. This practiceconverts guaranteed loans into direct loans, which are notreflected in the Federal budget totals at the present time.

Loan guarantee programs are growing. Part of their pop-ularity stems from the belief that they are costless. Becauseof this and because of FFB's off-budget status, there is apotential for the unwarranted growth of loan guarantees withan FFB connection. But the growth in loan guarantees would,to a large extent, be in name only. More important is thepotential for poorly designed assistance programs becausethere is a potential for increasing use of full guaranteesto achieve program goals where partial guarantees or moredirect forms of Federal'assistance are more appropriate.

P:inciples of risk sharing

As a general financial principle, 100-percent loanguarantees are something to be avoided--not encouraged. Loanguarantee programs t the maximum extent feasible shouldincorporate into their 6esign risk sharing by both borrowersand private lending institutions. If borrowers and lendersare not exposed to commercial risk, the normal incentivesfor successful completion and management of the project onwhich funds are loaned are absent. Also, the probability thatthe loan guarantee program will achieve its intended objectiveis diminished.

Some fully guaranteed loan programs may require equityparticipation; others may not. If equity participatu... is re-quired, the incentive on the part of the borrower to completeand successfully manage the assisted project varies in directrelation to the borrower's rate of equity participation. Ifno equity participation is required, not only are the desir-able borrower incentives absent, but the risk to the projectis higher because of its highly leveraged position and vulner-ability to failure from variable revenue flows.

Regardless of the amount of equity participation required,fully guaranteed loans eliminate the normal incentives of pri-vate lenders to carefully evaluate the applicant's prospectsand provide the neceszary followup on the loan. In the absence

16

of normal lender incentives, the probability of the approvedborrower's success and repayment of principal is reduced.

ImpVjcit subsidy

Presumably, an advantage of FFB purchase of guaranteedloans is reduced interest costs to assisted borrowers. Thisis questionable. First, if a subsidy was not intended whenthe loan guarantee program was designed, reduced costs to as-sisted borrowers are not desirable. Second, the increasedsubsidy is only desirable when it increases the likelihoodof successful achievement of goals. An increased likelihoodof reduced debt service costs increasing success rates isdoubtful in view of the absence of normal commercial incen-tives on fully guaranteed loans. Third, although interestcosts to borrowers may be lower, costs to agencies may behigher. For, when FFB purchases fully guaranteed loans, agen-cies assume the full banking function with its attendantcosts, particularly in the case of new loan guarantee pro-grams.

Potential results

At the present time most FFB purchases of guaranteedloans are fully guaranteed instruments of private borrowers.For fully guaranteed loans the Government assumes all of therisk, and a close relationship between the borrower and theGovernment is desirable. A potential problem may arise ifnew loan guarantee programs are designed to conform withthe types of programs in which there is current FFB involve-ment, rather than being designed to most efficiently accom-plish program goals.

The design of loan guarantee programs and the meritsof loan guarantees, direct loans, and other direct formsof Federal assistance have long been discussed. / Loan

1/The major Government studies of Federal credit assistancethat have addressed this issue are: Commission on Organ-ization of the Executive Branch of the Government, "TaskForce Report on Lending Agencies," (Washington, D.C.: Gov-ernment Printing Office); Commission on Organization of theExecutive Branch of the Government, "Federal Business En-terprises," (H. Doc. 152, 81st Cong.); The Report of theCommission on Money and Credit, (Englewood Cliffs, I.J.:Prentice Hall, Inc., 1961); Report of the Committee n Fed-eral Credit Programs, which was published in 19636A Study of Federal Credit Programs, Subcommittee on )omes-tic Finance, Committee on Banking and Currency, Vol. 1(Washington, D.C.: Government Printing Office, 1964); andThe Report of the President's Commission on Budget ConceptsWashington, D.C.: Government Printing Office, 1967).

17

guarantees can be effective policy instruments in somecases and ineffective in oher cases. Partial guaranteesare generally to be preferred to full guarantees since com-mercial incentives are lacking for full guarantee programs.In general, fully guarante:d loans should be justifiable onabout the same basis as direct loans. Specifically, thereduced debt service costs from a partial guarantee are notsufficient to induce poteintial borrowers to undertake so-cially or economically worthwhile projects. Only a fullguarantee with lower debt service costs or a direct loanwith an even lower debt service cost will be sufficient toachieve program goals.

On the other hand, use of credit assistance in .he formof either direct or guaranteed loans may be entirely inappro-priate in cases where reduced debt service burdens chievedby the program are likely to be minor, because the r;sk tothe project is not the major impediment to its undertaking,or when debt service burdens pose so large an impedimentthat neither partial nor fully guaranteed loans or directloans are likely to achieve program goals.

As a general principle, we believe fully guaranteedloans should be avoided. If they can be justified, thendirect loans are probably a better assistance device fromthe Federal perspective, because the Federal oversight roleshould be greater.

Because of FFB's off-budget status and the currentbudget treatment of loan guarantees, however, a potentialexists for:

-- The use of full guarantees purchased by FFB, whenthe commercial risk sharing is a more appropriateand less costly means of ac'.ieving program goals.

-- Use of full guarantees, when the justifiable assis-tance device is direct loans, that instead of beingincluded in the budget totals can he excluded fromthe budget totals and the budget pocess.

--A choice of credit assistance over direct expendi-ture forms of credit assistance, when the latterseems more likely to achieve program goals.

Putting FFB on the budget might eliminate these poten-tial problems, but it would not solve any of the longstandingproblems associated with the favored budget status of loanguarantees. Whether FFB is on or off the budget, loan guaran-tee programs might still be used where inappropriate, but at

18

least there would not be as large a potential for use of fullguarantees or direct loans where they are not appropriate.

EFFECT ON OUTLAY TOTALSOF AN ON-BUDET FFB

If FFB's transactions were included in the budget totals,outlays would be affected in the following ways.

1. FFB purchase of on-budget agency debt. Outlay totalswould be unchange because when te proceeds from an FFB debtpurchase are loaned out or otherwise spent by the agency, theywould be included in the budget totals. Other transactionsin this process would cancel each other, as they do now.

2. FFB purhase of off-budge t agency debt. Under cur-rent budget rules relating to off-budget agencles, debt trans-actions (borrowing) between these agencies and the Treasury,and presumably between these agencies and an on-budget FFB,are not treated as outlays. Only transactions with the publicare reflected as outlays. Thus, even if FFB were placed on thebudget, the outlays of most off-budget agencies which financetheir activity through FFB would remain outside the budget.If FFB is placed on the budget, then off-budget agencies bor-rowing from FFB should also be brought onto the budget.

3. FFB purchase of an agency asset. When there is aphysical transferof an on-budget or off-budget agency assetto FFB, the loan outlays of the agency would be reduced.FFB's purchase of the asset would be fully reflected in outlaytotals as an FFB direct loan expenditure under current budgetrules.

4. FFB purchase of CBOs. If current budget treatment ofthese transactions continues, FFB purchase of this paper wouldbe reflected on the budget as FFB loan outlay. If these se-curities were treated as agency ouligations (as we believethey should be), they would be included in the outlays of theagency selling the paper when the proceeds were loaned out.Either way, outlays would be increased by the amount of agencylending.

5. FFB purchase of uaranteed loans. I FFB continuedto purchase guaranteed loans that would have otherwise beenoriginated in private capital markets, the bdget totalswould fully reflect this direct loan expenditure in the FFBaccount.

Although FFB's transfer onto the budget would not correctall of the deviations of current from recommended budgetpractice, the effect on budget outlays would be nearly inkeeping with recommendations from the Commission on Budget

19

Concepts. Although the current budget treatment of CBOs isincorrect in our view, the true nature of the transactionswould be reflected in the outlay totals as FFB direct loans.But, they would not be reflected in the agency totals. Salesof assets to FFB would also be reflected as FFB direct loans,as would its purchases of loan guarantees if this practicecontinued. To the extent that agencies financing their lend-ing and direct expenditure activity through FFB debt trans-actions remain off the budget, outlays would remain under-stated by the amount of that activity.

FFB has grown considerably since it began operations in1974. Its loan holdings totaled $25 billion as of October 1,1976. Of this total, approximately $15 billion was not in-cluded in the budget attributable to FFB. By 1978 it isestimated that FFB will hold $48 billion in securities, ofwhich about $30 billion will represent a cumulative under-statement of the budget totals attributable to FFB.

FFB purchases of off-budget agency debt are estimatedto be a smaller proportion of its holdings in fiscal year1977 and fiscal year 1978 than in prior years. This is be-cause of the inclusion of the Export-Import Bank on the budgetbeginning in fiscal year 1977. Holdings of CBOs (primarilythose of the Farmers Home Administration) occupy the mostimportant portfolio position in future years. True agencyasset holdings, as distinct from CBOs, are estimated to com-prise only a small portion of FFB's portfolio in fiscal year1978. FFB holdings of private guaranteed borrowings areexpected to increase slightly in future years averaging about16 percent of all FFB holdings in fiscal years 1977 and 1978.(See table 1.)

The anticipated growth in FFB's CBO purchases is causefor concern. By fiscal year 1978 it is estimated that FFBwill hold $20.5 billion in Farmers Home Administration certi-ficates. These holdings are expected to account for almost43 percent of all FFB holdings. As a result, since FFB'screation a total of about $20 billion in direct lending act-ivity by the Farmers Home Administration of the Department ofAgriculture will have gone through FFB and, since FFB isoff the budget, been excluded from the budget totals

SHOULD FFB BE PLACED ON THE BUDGET?

Would an on-budget FFB be the best means of correctingthe way in which the Federal credit assistance which goes

20

Table 1

Relative Share of Outstanding Loans Held byFFB by Type of Transaction

FY Transition Est. FY Est. FYTransaction 1976 quarter 1977 1978

-------------- (Percent)----------------

FFB purchaseof on-budgetagency debt 9.73 10.57 27.57 28.25

FFB purchase ofoff-budgetagency debt 34.88 31.34 9.93 9.73

Purchase ofagency assets 1.26 5.26 3.75 1.14

Purchases ofCBOs 40.00 38.65 42.81 44.55

FFB purchases ofloan guarantees 14.08 14.19 15.94 16.33

Source: Special Analysis of the Budget of the U.S. Govern-ment, FY 1978, table E-2b.

through FFB would be reflected in the budget? PuttingFFB on the budget would include in the activities of theFederal establishment most of the outlays of agencies whichcurrently relate to FFB outside the budget. This would makethe Federal budget surplus or deficit more meaningful,because it would make more accurate the spending and bor-rowing implied by those deficits. This in turn would makemore meaningful conclusions about the aggregate economic im-pact of the Federal Government on the nation.

But, it would not include all of them; and, more impor-tant, under existing budget conventions, all on-budget agencylending and guaranteeing activity that is not now reflectedin the budget would appear in the account of an on-budget FFB.This activity would be included in the general Governmentfunction rather than in the functions in which the agencylending programs are included. This might be avoided by (1)splitting the FFB account among the Federal functions sothat the outlays are included in the same function as theagency's lending program or (2) devising a budget techniquethat would result in reporting the outlays in the accountsof he administering agency and offsetting these against theFFB account.

21

If the activities of lending agencies are not properlyreflected in individual program or functional accounts, itis difficult to see how the budget process can properly al-locate Federal resources among Federal credit pr3grams,between credit programs and direct expenditure programs, and,ultimately between the public and private sectors of theeconomy.

The way FFB affects the meaning of Federal outlays anddeficits is not solely a function of its off-budget status.The problem with the way Federal credit assistance goingthrough FFB is reflected in the budget results from thecombined effects of FFB's off-budget status and other devia-tions of actual from recommended budget treatment of theseactivities.

For example, FFB purchases of on-budget agency obliga-tions are properly reflected in the budget now because of theway that borrowing is reflected in the budget and becausethese agencies are on the budget. If off-budget agencieswhich currently engage in debt transactions (borrow) with FFBwere placed on the budget, their lending and direct expendi-ture activity would be reflected on the budget in their re-spective accounts, regardless of the budget status of FFB.

If CBOs were given the recommended budget treatment--namely, if sales of these securities were treated as borrowingrather than asset sales which reduce loan outlays--then FFBpurchase of these issues would be reflecl-d in the accountsof the borrowir agencies, regardless of the budget statusof FFB.

The combined effects of eliminating the off-budcet statusof agencies that borrow from FFB to finance lending andof proper budget treatment of CBOs would bring a considerableamount of lending and direct expenditures, currently oc-curring outside of the budget, onto the budget.

Asset sales to FFB are currently properly treated in theselling agency's account. When these securities are sold toFFB, a problem arises because the Federal Government retainspossession of the loans and overall outlays are understatedby the amount of FFB purchases. If FFB remains off the bud-get, this problem will ontinue to exist unless the FederalGovernment's continued ownership of the paper is reflected asan outlay in the account of the agency selling the paper. Itmight be argued that since the Federal Government still re-tains possession of the asset, the best place to reflect thisis in the agency account. This treatment would increase theagency's outlays and would technically be at variance withrecommended budget practices.

22

FiB purchase of guaranteed loans is a questionablepractice, because its off-budget status may lead to aninappropriate increase in direct loan programs disguised asloan guara-tee programs. Putting FFB on the budget mighteliminate he current and potential problems associatedwith this practice.

The concern that if FFB is included on the budget, manyof the transactions that currently go through FFB would nolonger occur appears legitimate in view of the currer' bud-get treatment of Federal creditprograms. Agencies may haveto return to the private capital markets to finance loan pro-grams in order to avoid the outlay impacts that would resultfrom dealing with FFB. This in turn would eradicate the costsavings that have been achieved through FFB's creation.

Because of outlay effects, guaranteed loans to privateborrowers might no longer L. purchased by an on-budget FFB.However, this is desirable. It is not an undesirable resultin view of the potential problem which FFB's current statusposes for design of Federal assistance programs and becausethe cost savings achievable under the present arrangement forloan guarantees may be illusory.

CBOs might also be sold in private capital markets ratherthan to an on-budget FFB. But the only reason this wouldoccur is because the present treatment of these transactionsdisguises their true nature. If such sales were treated asborrowing, they could continue to be sold to an on-budgetFFB at a cost savings.

Asset sales by agencies are a more difficult problem.Since current budget treatment of these transactions in theagency's account is correct, the outlay effects of sales ofthese securities to an on-budget FFB might cause them to besold in the private capital markets, sacrificing the costsavings achievable through FFB. This problem could beovercome by scoring the outlays in the agency's account.Technically, this would be incorrect. In this case, oneneeds to decide whether the benefits from cost savings onasset sales to an off-budget FFB exceed the costs of failingto fully reflect the scope of Federal lending activity inthe budget. In view of the other problems that FFB's off-budget status creates, we believe that the benefits fromcost savings on asset sales are not worth the continuedoff-budget status of FFB.

Budget neutrality has to do with preserving the budgettreatment of agency transactions with FFB in the agency's

23

account. This in turn involves assuring continued fundingof programs. But there are two ways to view budget rnutralityas it relates to the budget status of FFB. It can either beviewed in terms of current budget treatment, or it can beviewed i terms of proper budget treatment of agency trans-actions FFB. Under existing budget conventions, theonly way . preserve budget neutrality and achieve the bene-fits that flow from FFB appears to be with an off-budget FFB.But, aside from FFB's off-budget status, if other budget con-ventions which we have raised concerns about were changedto more accurately reflect the true nature of credit assist-ance activity, certain activities would continue to befinanced through FFB.

If off-budget agencies financing activity through FFBwere placed on the budget, depending on the nature of theirtransactions with an on-budget FFB, some would continue(CBO sales and agency borrowing) with proper budget treat-ment. CBO sales by on-budget agencies would continue toflow through FFB because having changed the way that thesesecurities are reflected in the budget, FFB's budget statuswould be irrelevant to the agency selling CBOs. To thisextent, with proper budget treatment, an on-budget FFB shouldbe neutral in its effects under a proper regime of budget con-ventions. On the other hand, neutrality could not be pre-served in view of the outlay impacts for FFB loans to privateguaranteed borrowers and probably could not be preserved forloan sales to FFB. In the former case, this is desirable.In the latter case, a cost savings may have to be sacri-ficed.

RECOMMENDATIONS Tr ONGRESS

The combined effe. of FFB's off-budget status andother deviations of actual from recommended budget treatmentof credit assistance activities with an FFB connection re-sult in

--an inaccurate depiction of some Federal creditassistance;

-- the potential for poor design of creditassistance devices and poor choices betweenthose and other Federal assistance devices; and

--a dilution of the accuracy of Federal outlaysand deficits.

Placing FFB on the budget would, by itself, improveupon the last of these problems; but it would not solve theformer two.

24

In order for Federal credit assistance activity cur-rently going through FB to be more adequately reflected onthe budget, we recommend that the Congress require that

-- FFB's receipts and disbursements be included inthe Federal budget totals;

-- the receipts and disbursements of off-budgetagencies that borrow from FB be included inthe budget; and

-- CBOs be treated as agency obligations and,therefore, be treated in the Federal budqetas borrowing.

25

CHAPTER 4

IMPLICATIONS OF FFB OPERATIONS ON THE CONDUCT

OF DEBT MANAGEMENT AND MONETARY POLICY

Changes in the mix of public holdings of the Treasury andagency debt result from FFB operations. These changes affectthe liquidity of public asset holdings. Treasury securitiesare more liquid than agency securities. Through inducedchanges in the liquidity mix of the public's asset holdings,FFB may potentially affect monetary and debt managementpolicy.

The effect of changes in the maturity composition andliquidity of the public's holdings of Government securitieson the term structure of interest rates, on the maturitystructure of the Federal debt, and on the ease with which theFederal Reserve Board is able to control credit availabilitycannot be precisely quantified. But arguments with specificexamples and evidence may be cited to show that these effectsexist. The importance of FFB-induced shift3 in liquiditydepends on the size of the shift as well as on the strength ofrelationships between public holdings of liquid assets, thematurity structure of interest rates, and the ability of theFederal Reserve Board to control credit availability.

DEBT MANAGEMENT POLICY

Economic stabilization is not an explicit goal of debtmanagement policy. Deficits, the amount of borrowing nec-essary to finance deficits, and the effect of borrowing onthe level of the public debt are more appropriately cate-gorized as results of fiscal policy. Debt managementpolicy is oriented more toward manipulation of the existingstock of public debt toward shorter or longer maturitiesin order to reduce the costs of borrowing. But, in doingthis, debt management policy affects te liquidity mx ofthe public's asset holdings and therefore could have an in-direct effect upon economic stabilization.

All loans currently made by FFB are financed by bor-rowing from the Treasury. The Treasury in turn borrowsfrom the public by issuing its own securities. Thus, thannual incrase in Treasury debt resulting from FFB opera-tions is about equal to FFB's annual net lending activity.The accounting for outlays from FFB net lending are smallerthan its total net lending outlays because certain of itsloan outlays appear as outlays in the accounts of borrowing

26

agencies that are included in the agency budget totals. Toattribute these outlays to FFB would be double counting.Relationships between Federal outlays, FFB net lending out-lays, the Treasury and agency borrowing, and other means offinancing deficits are shown in table 1.

Changes in Federal debt aggregates

The increase in the Treasury debt induced by FFB since1974 accumulated to $25.9 billion by October 1, 1976, and isestimated to be $48 billion at the end of fiscal year 1978.(See line 17.) Gross Federal debt includes both agency debtand Treasury debt. Because the operations of the FFB displacea lrge amount of agency with Treasury debt, the increase ingross Federal debt is less than the increase in the Treasurydebt. This increase due to FFB was $15 billion on October1, 1976, and is estimated to be $29.8 billion by the end offiscal year 1978.

But, the FFB-induced increase in the gross Federal debtis a poor measure of FFB's effect on Federal indebtedness.This is because CBOs are not currently treated as borrowing,and therefore are not considered agency debt. In our opinion,there is no difference in substance between CBOs and agencydebt. If CBOs are treated this way, there is no effect onthe level of Federal indebtedness when they are sold to FFB.Agency debt is swapped for the Teasury debt. Because CBOsare not considered agency debt and therefore part of thegross Federal debt, the increase in gross Federal debt dueto FFB does not reflect the reduction in agency debt result-ing from FFB purchase of CBOs. Thus, the increase in grossFederal debt due to FFB overstates the effect of FFB trans-actions with agencies and private guaranteed borrowers onthe level of Federal indebtedness.

After adjusting for CEOs, the increase in Federalborrowing due to FFB operations accumulated to $5.5 billionon October 1, 1976. It is expected to total 8.8 billion bythe end of fiscal year 1978. This increase is the estimatedamount of increased Federal borrowing that will be requiredto finance FFB purchases of true agency assets and origina-tion of guaranteed loans that would have otherwise originatedin the private sector. This figure represents the increasein Federal liabilities attributable to the existence of FFB.It measures the extent to which contingent liabilities havebeen converted into direct liabilities. Without FFB, thisincrease in Federal indebtedness would probably not haveoccurred. Table 2 preseits the adjusted figures in lines 22through 24. CBO sales are shown in line 20.

27

44c0 V. C

b c

f', VOI -i Cl IN V co ,. , . I', ~"

... , 04r-I ON,0 ,.C M I - C C Wa"w f-I1 4 0 0N ON C C @ 4 C 5 SI

NJ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~,t

.40 I 4-0. I 4'lcl~ f III -n 041 44Wa a% @4 @4 0

'a ICI 04 4 14Il 444 4444 1f44 44 4S 4N

14. II I - I IA *.I M~~~~~~~~~~~~~ IA 444 44~~~~~~~~~~~~~~~~~~~~~~~~~~u IT N

at.I I

,,c,~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ ' ~

a ur a, a N~~~~t C e . 1 gml a~~~,

I I 0 05 M M C Nf

- ID

MOI rCI f-O N. 01 4'f .. NN a- 0 C SI N 4

C z~~~~S- C C " .4- C 44

444 '.44I 44 0 f I

.1 o Df II I CWGo o f-o SC f 4, N 4I 4 Co 4 1

"'" $1 -~?......

WI I I c O o 41

Co .0 a- a" mma- n ID m C4 v 6 'N ,

W1-I CCI I NIINI ~ -. WI C - M 4' CF f- 4' NA =4 4.£ fo nr-n( O~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~I

, !' -'-"

u4 C1 141 -- I - - - 04

A "IA -

'I4 1 C - 0

0- -C

la C a 9~ lociI0I~~ ~ '-·', .-4 ,,, : : a r -I a ..

44(a 4n - - C v 0 e a a

u C ~ ~ ~ ~ ~ ~~~~~o

C I II i4 .9 f- N i I4 I i . -& - C i - a 041 I 0. C D C44 .- A @ a 4.- - 00z -C

@44 - C.44 C @4N M N C 04~~~~~~" 1 -C f C a, I4 4, -, C, II -nr r a o ne a ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ a n 9~~~~~~~~~~ a N

Vl 4S-C MI Nf 4 4 4 04 @ - C 4 . 4 N C 4

0 U

'a C- C I~~~~~~~~~~~~~CC4E~~~~~~~~~~~~ju011 I C C to [aL

NI CII I I o I I I I

~~I 0~~1 IDL~~~L~~1 c~~C a w II I I I a 4 44444 4 0~~~~~~~~~ 0 0 2 l

IL·I -npdl sJlI

044.44-4 f-I 4 CCC C 4I444C1* @4~~~~~~~fi. C f- C @4 - 4 h. C 4 C

lul~Q~ 4 .0.4 44 .04- N M ,4 - NO C 4s 1I - CO

,, r l I , ul~~~~~~~~~~~~~~~~~~n n m r L( .-·~~~~~~~~~~~~~~~ . I

C~ ~~~~~~414 4' 4444 C - .

IAo i C o, 44

o4 C'A

2804 f 4 O N 0 N 0 N N 4f 4 C

l:1~~~~~~~~ 4.1 U 0os~~~~~~~~~~~~~~~~~~~~~44 '0 .4 n n~~~~~~~~~~~~I ~ ~ ~ ~ ~ ~ ~ ~ ~ ' 2,

~~~~~~~~~~*~~~~~~~~~ 44 V i·

01 a C - a U. 0X

0 0 2 ' 44 44 44 C 44C 44 00440 N 4' 0 C 0. *. 4 54 0 44 44 44 0

54 44 C 44 fl2 , 4. 54 U I . .. ,4441C IC .4 * .4 0h C " C * -

50. -.0 . . V 44 C -4

Va U 1. 44 44 44- C~ 144 4- .V. 44 4 4 44 V04 40 41N

54C 44 V C.44CCO 44 Caqa 4544 2.44444. C 222 0.40 . ON 14

440 0 3g· 5U 34-5 4.04 .4-Y CO COO O 44. 144141

4.4444. 44 44 r .4II4 44 4 .44 4 I 44 I I 44 4

CI I 0 ' 0 .4 0 0 2 44. 47 44 44

~~~Os 4. 44 0 0n 4.. 0C 5. 44 .( 44. .4 0 Ci

28

FFB-induced increases in the Treasury debt are largerelative to total increases in the Treasury debt after fiscalyear 1974, particularly during the transition quarter. Sim-ilar ratios for gross Federal debt are lower because of theagency debt offset, and the ratios for FFB-induced increasesin Federal borrowing are quite small except in the transi-tion quarter. These ratios are presented in lin:es 25, 26,and 27 of table 3.

The FFB-induced cumulative increase in Federal borrowingis about 2.9 percent of the increase in total Federal bor-rowing on October 1, 1976, and is estimated to decline to2.6 percent by the end of fiscal year 1978. Of a total of$337.5 billion increased Federal borrowing estimated to occurbetween fiscal years 1974 and 1978, only $8.8 billion isdirectly attributable to FFB.

Changes in the maturity compositionof the Federal debt

Compositional changes between agency and the Treasurydebt securities induced by FFB affect the maturity composi-tion of the Federal debt and the liquidity of public assetholdings. In general, agency debt is not as liquid as theTreasury debt of comparable maturity. If it were, there wouldbe a question about the effectiveness of FFB in achieving acost savings on agency borrowing. The main reason for thelower liquidity of agency securities is the lack of a wellorganized secondary market in these securities. This inturn is attributable to a lack of familiarity with agencysecurities. Treasury securities, on the other hand, aretraded in the deepest and most resilient secondary market inthe world, particularly in the shorter and intermediatematurities.

Aside fom this obvious difference in liquidity betweenagency and Treasury securities, the maturity structure alsodiffers. Agency securities have a longer maturity structurethan Treasury securities and are less liquid for this reason.We estimated this difference in order to measure changes thathave occurred in the average maturity of the Federal debt andin the public's liquid asset holdings. The latter measuremay be expected to affect the term structure of interestrates.

In order to measure changes in maturity composition ofthe Federal debt resulting from FFB-induced displacementeffects, we compared the maturity structure of new moneyTreasury financings with the maturity structure of FFBpurchases of agency obligations and CBOs. We assumed that

29

0 'a D 'a YIl 'a m a 000DI N O cu 0 in iN -4 0 N 0 00

· CII i Ir 9 9 0 9i 'a 0 Ni 0 00

ail~~ ~ ~~~ ~~~~~~ .4 14 1- 0r 010 a I i ct 0 m rl r roI 1rr i a r ~~~~~~~~~~~~~~~~~ m ~~~~~~~ mo"laC

a ct c~~~~~ r( mu (t %

1 u 'a MO 1. 0 1 0 -4 00CgN 0 4 0 r CD 0 " 004i01 Nin a co 0% m 0 00

Ie -% D -cood .l I 1- 0% 'a I 0 D 0 0 0 N 00

m 0 I"I 0 4 C 1- N 00CI 4=4D IC .I I . .) .I 0@1 *w1 0 0( 4 9 0 0% c In I 4 I 4 M

U -Ca £. 9 ' 0 g o g 00Ut~~~~~~~~~~~ I * 9

urrC) 1 r r (Y Ir) N *dpc ck UbC 0

'pi NI 4 Mp In .4m ,ro

IntI '( a 'a 0% 9 I 0 a C N5 0 00

0 on I 0 0 I 00

L.Io I 9 .4 N I 'a 'a In NA 0I m 0% 0 0 N i I O%

mi ~~ I 0 -0699 49 I~ N0 NI 0 I 0 - 'o a 0 N 0I rl P1 I I 'a 0) D 0 4 m0 0

L4 N m rn mO o 4 q

~~~~i~~· n: In I n I 0N0n 0*~I . . . . . . ..4 II Q 4 3 (% 04 LA U 0

4ll 00 N 0

o -AJ v r r r- .1 h a ct M co

U ,, h #A"I A N t-CS U ena

rr OI V n yU . h.51 I i In .

14 MatII III 1113~ l~ jf 9j 10 V1 >4 I I -1 InS o - cm N 0rA I, Aw -- '0 n LA

a C O MS B4*O O401.-Is.. 0beo I Oa In0

Bi ~ a m *e I~

M 4 a he Lo di me l

C 0 a O CC . * .(AAn a0- 0%h 0% -IN Ai42 I m 0O~~, - ' '

N N N N MM U

30~~~~~~~~~~~~~~~~~A

Ii :4 &4 + C .-O 'O I LnC+ --ucad in aI

I)~~r(~~ · · m Oc(·- ' r ~~~~~~L r. U U L. ... l .. + la·Y 4a a 10 I" 1 1 as 0:P L 1 14 0 I 0OI 0be -- 4nD. .0mmc >- O U40a

o lp A * IH "

: 4 a a la6P c 0 ais i i i S&O. A . 10Ja I caorcr cl~~~~~~~~~~~~~~~~~m ~a c(Y (Y ru rv~~~~~~~~~vm m mo m~~~~C

the maturity structure of displaced agency borrowings wouldhave been approximately the same as that which exists on FFEpurchases.

The average term to maturity differs substantially be--tween the Treasury debt and FFB financings. The Treasury'snew money financings had an average maturity of 3.57 years;FFB financing had maturities averaging 9.7 years. Thelargest difference occurs in the long and short ends of themarket. (See table 4.) The difference between long-termdebt relative shares is due partly to the fact that long-term Treasury borrowing is currently constrained by xistinjlaw.

For purposes of measuring the effect that FFB has had onthe average maturity of the Federal debt, it was necessaryto net the average maturity figure of FFB financings -f COs.For, in the absence of PFB, these securities would be part of the Federal debt. The average maturity o FFBpurchases of agency debt was 9.04 years. '(See footnote,table 4.) The average maturity of the increased Treasurydebt is estimated to be around 3.6 years.

Gross Federal debt is estimated to be $785 billion by theend of fiscal year 1978. With no FFB, this figure would beabout $30 billion less. We were unable to obtain a figure onthe average maturity of the Federal debt; but regardless ofwhat the true figure is, 1/ we estimate that the FFB-inducedcompositional shifts between the Treasury and agency securities

1/The average maturity of marketable interest-bearing publicdebt held by private investors was 2.75 years as of March1977. This debt comprises about 45 percent of total Federaldebt at the end f 1977, and its average maturity estab-lishes a lower bound on what the average maturity of theFederal debt is likely to be. An upper bound was estab-lished by assuming that all other securities comprisingthe Federal debt have an average maturity of 20 years. Ifthis is the case, the average maturity of the Federaldebt would be around 12 years.

31

0:

4i l

a~~~~~~~~~~~~~~a-u·0 h1. c4 I rc .A. -

0'

1' ~ .. 34 S U)

a'- 4 a 63 V. 633 o

E"I~ ~ ~~~~* .4C 0 G b . 0 c

UI 0~~~~~~~~~~~~~~~~~iI 1!. . 3 4.

21 dC a Ai~

63 a '.4 PU'*0

M iS *5 IA I l M 50 * 5t iS = * V 5

44 * ~~~~ V) O (Y ~~~~~~ r(O W'0*- 6

U* * t o c.-A

AJ l, a

i s ~~~~.n.¢

It. I f * * . I .. .s 5.4 n I*5 AANiS C 0 .'6

id8¢6 1% 4 , UUh

Wim

U *-*~~~~~~~~~~~~~~~~~~~~~~~~~~~~44 *50 4'.0 k k )4

Ai. 41 L.