pakistan joint venture financial institutions – an overvie · pakistan joint venture financial...

TRANSCRIPT

Pakistan Joint Venture Financial Institutions – An Overview

April 2013

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

BackgroundPost world war concept.“Development banks are government-sponsoredDevelopment banks are government sponsored financial institutions concerned primarily with the provision of long-term capital to industry’’ 1

Unique objective of the economic developmentPakistan Industrial Development Corporation of p pPakistan (PIDC) - first Development Financial Institution (DFI) - established in 1950.

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

Leading DFIs in INDIALeading DFIs in INDIAIndustrial Credit and Investment Corporation of India(ICICI) formed in 1955 transformed its business from2(ICICI), formed in 1955, transformed its business froma development financial institution to a diversifiedfinancial services group in 1990s.g pMerger of ICICI and two of its wholly-owned retailfinance subsidiaries, with ICICI Bank in 2002.ICICI Bank – second-largest bank of India – with totalassets of INR 4,736bln at March 31, 2012 earned aprofit of INR 64bln for the same period.

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

L di DFI i INDIALeading DFIs in INDIAIndustrial Development Bank of India Limited (IDBI),established in 1964 was transformed into a commercial

3

established in 1964, was transformed into a commercialbank in 2004.Merger of IDBI Bank Limited with IDBI Limited – theMerger of IDBI Bank Limited with IDBI Limited – theparent company in 2005.Currently working as IDBI Bank Limited the bank’sCurrently working as IDBI Bank Limited, the bank s total assets size reached to INR 2,908bln as on March 31, 2012, while it registered a profit of INR 20bln for that period.

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

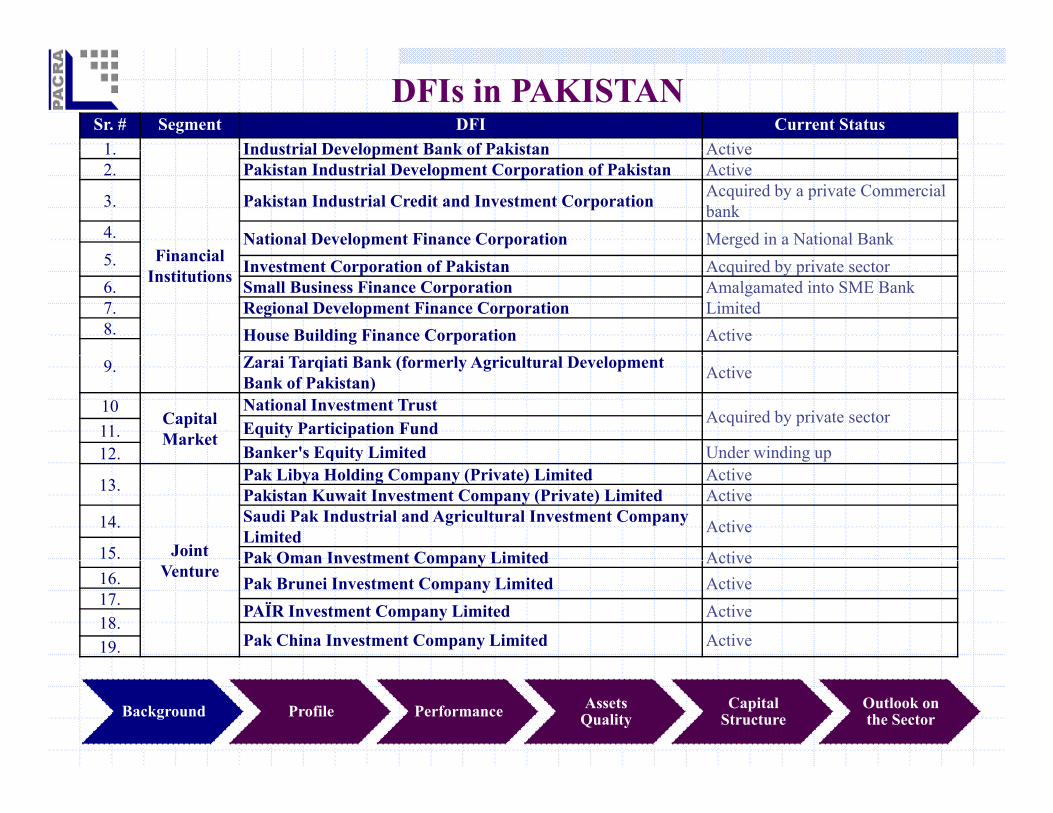

DFIs in PAKISTANSr. # Segment DFI Current Status

1 Industrial Development Bank of Pakistan Active1.

Fi i l

Industrial Development Bank of Pakistan Active2. Pakistan Industrial Development Corporation of Pakistan Active

3. Pakistan Industrial Credit and Investment Corporation Acquired by a private Commercial bank

4. National Development Finance Corporation Merged in a National Bank Financial

Institutions5. Investment Corporation of Pakistan Acquired by private sector 6. Small Business Finance Corporation Amalgamated into SME Bank

Limited7. Regional Development Finance Corporation8. House Building Finance Corporation Active

9. Zarai Tarqiati Bank (formerly Agricultural Development Bank of Pakistan) Active

10Capital Market

National Investment TrustAcquired by private sector

Equity Participation Fund11.Banker's Equity Limited Under winding up12. a e s qu ty ted U de w d g up12.

13.

Joint

Pak Libya Holding Company (Private) Limited ActivePakistan Kuwait Investment Company (Private) Limited Active

14. Saudi Pak Industrial and Agricultural Investment Company Limited Active

15. Pak Oman Investment Company Limited ActiveVenture

Pak Oman Investment Company Limited Active16. Pak Brunei Investment Company Limited Active17.

PAΪR Investment Company Limited Active18.

Pak China Investment Company Limited Active19.

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

Lack of proper supervision poor management andDFIs in PAKISTAN

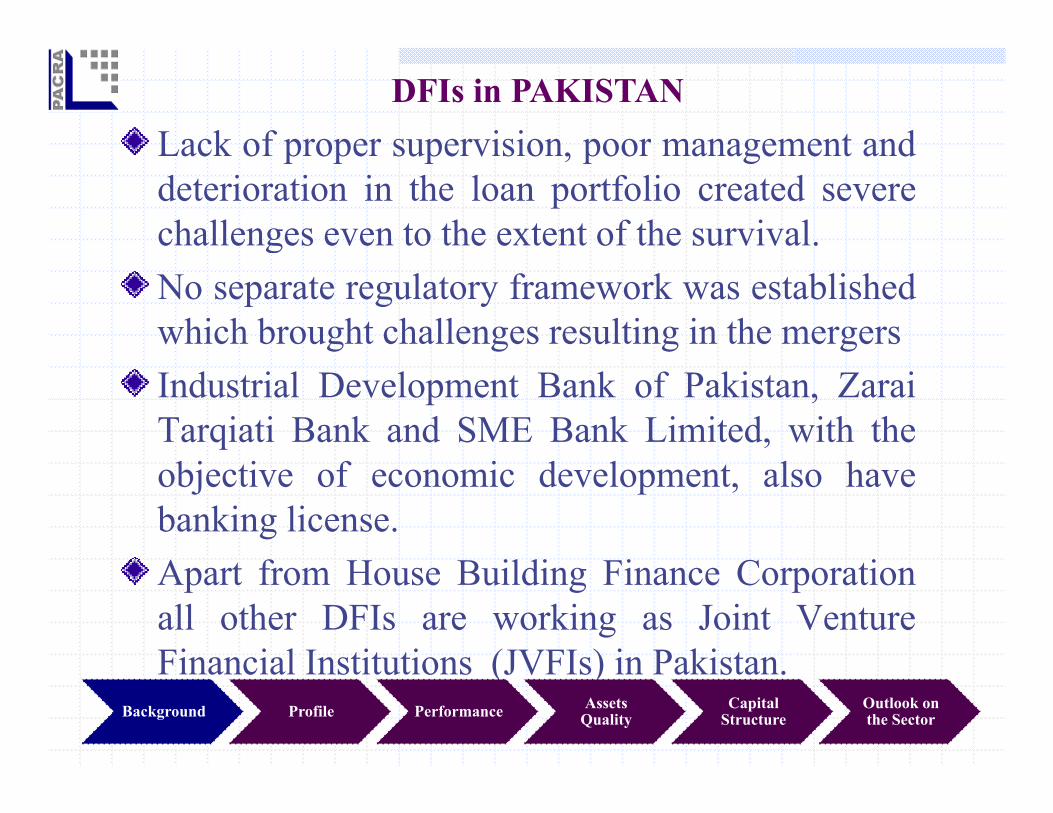

Lack of proper supervision, poor management anddeterioration in the loan portfolio created severechallenges even to the extent of the survival.gNo separate regulatory framework was establishedwhich brought challenges resulting in the mergersIndustrial Development Bank of Pakistan, ZaraiTarqiati Bank and SME Bank Limited, with theobjective of economic development, also havebanking license.A f H B ildi Fi C iApart from House Building Finance Corporationall other DFIs are working as Joint VentureFinancial Institutions (JVFIs) in PakistanFinancial Institutions (JVFIs) in Pakistan.

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

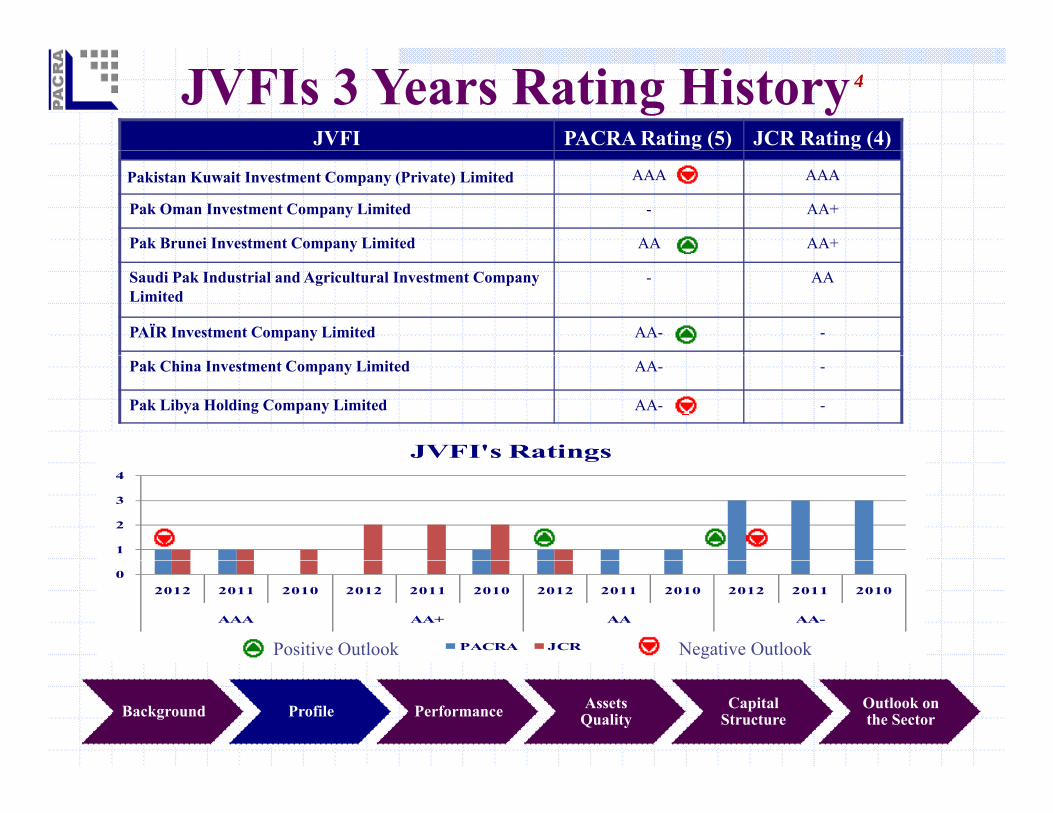

JVFIs 3 Years Rating HistoryJVFI PACRA Rating (5) JCR Rating (4)

4

Pakistan Kuwait Investment Company (Private) Limited AAA AAA

Pak Oman Investment Company Limited - AA+

Pak Brunei Investment Company Limited AA AA+

Saudi Pak Industrial and Agricultural Investment Company Limited

- AA

PAΪR Investment Company Limited AA- -

Pak China Investment Company Limited AA- -

Pak Libya Holding Company Limited AA- -

JVFI's Ratings

1

2

3

4

g

02012 2011 2010 2012 2011 2010 2012 2011 2010 2012 2011 2010

AAA AA+ AA AA-

PACRA JCR Negative OutlookPositive Outlook

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

Regulatory Framework

Regulatory supervision is done by two government bodiesI. State Bank of Pakistan - SBP (as these are financial

institutions) II Ministr of Finance MoF (ha ing in estment inII. Ministry of Finance – MoF (having investment in

these JVFIs directly and through SBP)

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

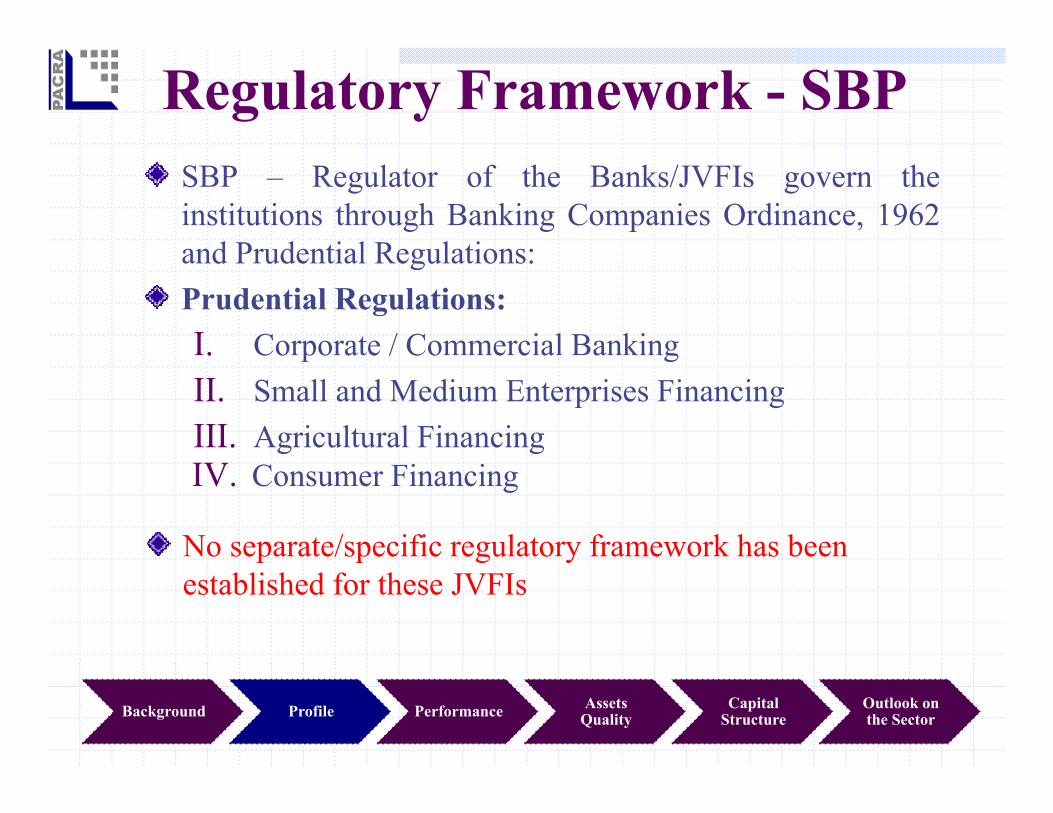

Regulatory Framework - SBPSBP – Regulator of the Banks/JVFIs govern theinstitutions through Banking Companies Ordinance, 1962and Prudential Regulations:and Prudential Regulations:Prudential Regulations:I. Corporate / Commercial Banking . Co po a e / Co e c a a gII. Small and Medium Enterprises Financing III. Agricultural FinancingIV. Consumer Financing

No separate/specific regulatory framework has been p p g yestablished for these JVFIs

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

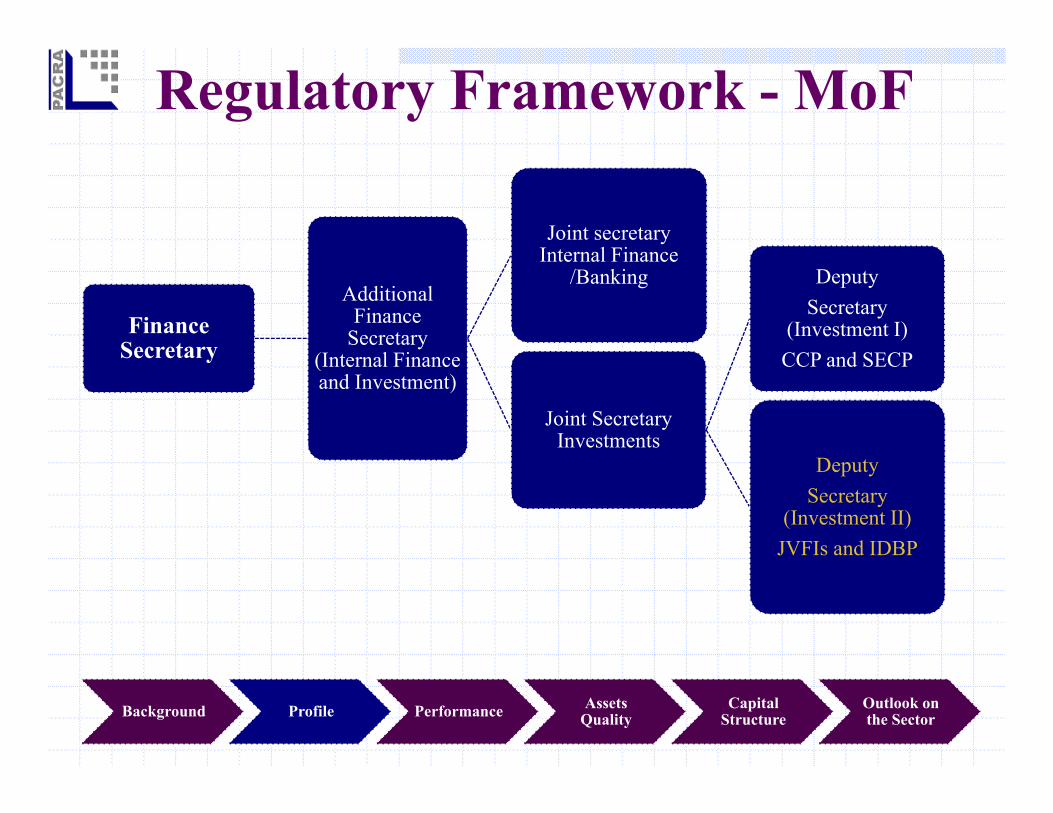

Regulatory Framework - MoF

Joint secretary Internal Finance

Finance Secretary

Additional Finance

Secretary (I t l Fi

Internal Finance /Banking Deputy

Secretary (Investment I) CCP d SECPSecretary (Internal Finance

and Investment)

Joint Secretary Investments

CCP and SECP

DDeputySecretary

(Investment II)JVFIs and IDBP

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

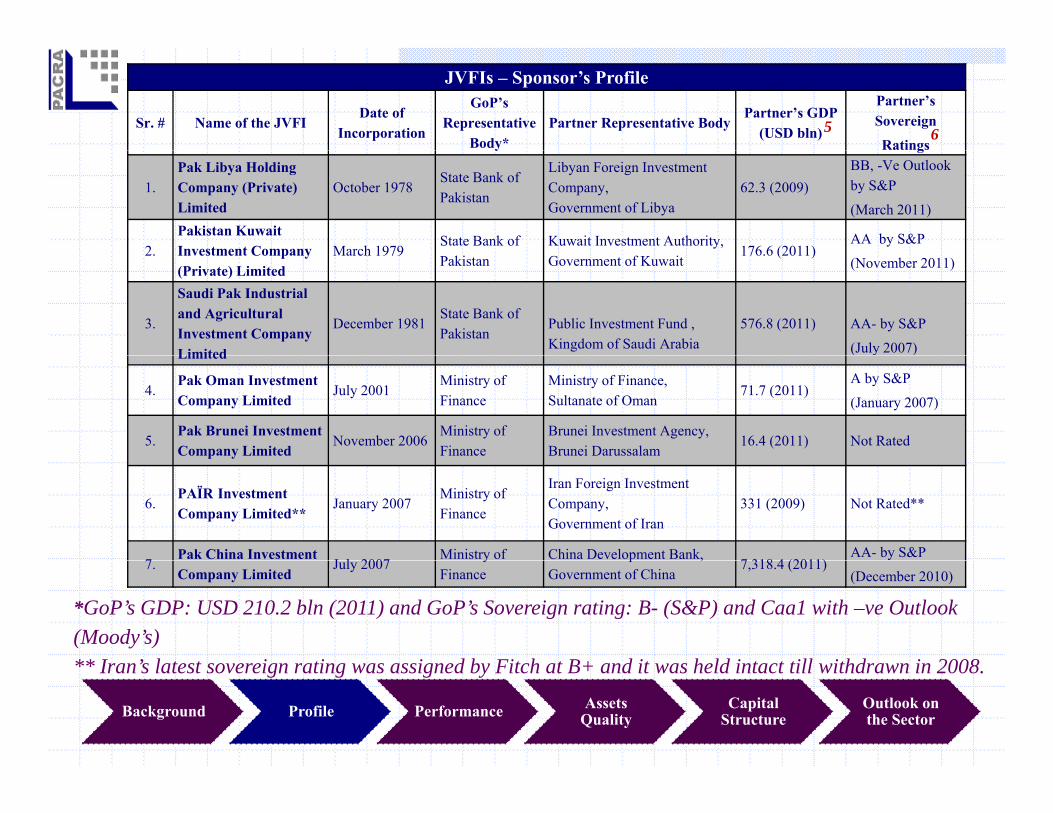

JVFIs – Sponsor’s Profile

Sr. # Name of the JVFIDate of

Incorporation

GoP’s Representative

Body*Partner Representative Body

Partner’s GDP (USD bln)

Partner’s Sovereign

Ratings 5 6y g

1.Pak Libya Holding Company (Private) Limited

October 1978State Bank of Pakistan

Libyan Foreign Investment Company, Government of Libya

62.3 (2009)BB, -Ve Outlook by S&P

(March 2011)

2Pakistan Kuwait Investment Company March 1979

State Bank of Kuwait Investment Authority, 176 6 (2011)

AA by S&P 2. Investment Company

(Private) Limited March 1979

Pakistan Government of Kuwait 176.6 (2011)

(November 2011)

3.

Saudi Pak Industrial and Agricultural Investment Company Limited

December 1981State Bank of Pakistan

Public Investment Fund , Kingdom of Saudi Arabia

576.8 (2011) AA- by S&P

(July 2007)Limited ( y )

4.Pak Oman Investment Company Limited

July 2001Ministry of Finance

Ministry of Finance,Sultanate of Oman

71.7 (2011)A by S&P

(January 2007)

5.Pak Brunei Investment Company Limited

November 2006Ministry of Finance

Brunei Investment Agency, Brunei Darussalam

16.4 (2011) Not Ratedp y

6.PAΪR Investment Company Limited**

January 2007Ministry of Finance

Iran Foreign Investment Company,Government of Iran

331 (2009) Not Rated**

7Pak China Investment

J l 2007Ministry of China Development Bank,

7 318 4 (2011)AA- by S&P

*GoP’s GDP: USD 210.2 bln (2011) and GoP’s Sovereign rating: B- (S&P) and Caa1 with –ve Outlook (Moody’s) ** I ’ l t t i ti i d b Fit h t B+ d it h ld i t t till ithd i 2008

7.Company Limited

July 2007y

Finance p ,

Government of China7,318.4 (2011)

(December 2010)

** Iran’s latest sovereign rating was assigned by Fitch at B+ and it was held intact till withdrawn in 2008.

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

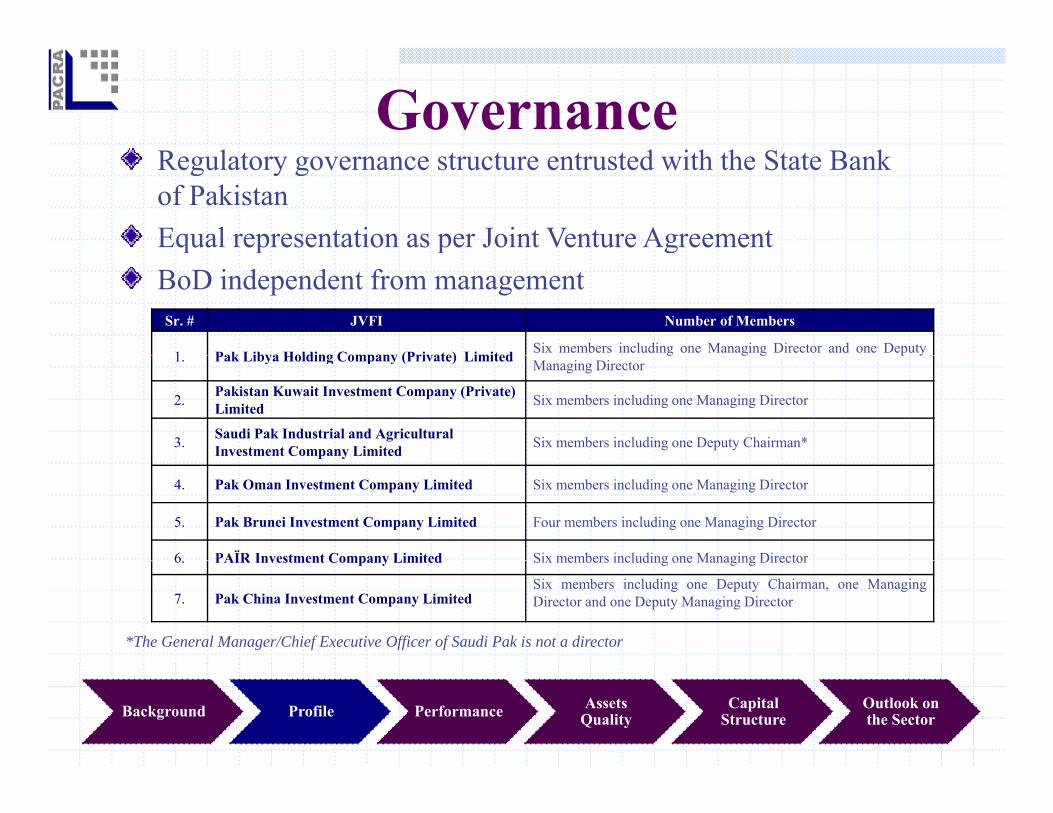

Governancel d i h h S kRegulatory governance structure entrusted with the State Bank

of PakistanEqual representation as per Joint Venture Agreement q p p gBoD independent from management

Sr. # JVFI Number of Members

1 Pak Libya Holding Company (Private) Limited Six members including one Managing Director and one Deputy1. Pak Libya Holding Company (Private) Limited g g g p yManaging Director

2. Pakistan Kuwait Investment Company (Private) Limited Six members including one Managing Director

3. Saudi Pak Industrial and Agricultural Investment Company Limited Six members including one Deputy Chairman*p y

4. Pak Oman Investment Company Limited Six members including one Managing Director

5. Pak Brunei Investment Company Limited Four members including one Managing Director

6 PAΪR Investment Company Limited Six members including one Managing Director

*The General Manager/Chief Executive Officer of Saudi Pak is not a director

6. PAΪR Investment Company Limited Six members including one Managing Director

7. Pak China Investment Company Limited Six members including one Deputy Chairman, one ManagingDirector and one Deputy Managing Director

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

GovernanceExpose to political intervention as no transparentframework available for the nomination of directorLimited guidance due to frequent changes indirectors holding Ex officio positionsStrategic void due to lesser number of meetings

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

ManagementgManaging Director (MD)/Chief Executive Officer(CEO) f JVFI i ibl t th ff i f(CEO) of JVFI is responsible to manage the affairs ofthe company under the supervision of the BoDPressure at the leadership positionsPressure at the leadership positionsEstablishment of stable teams remains critical

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

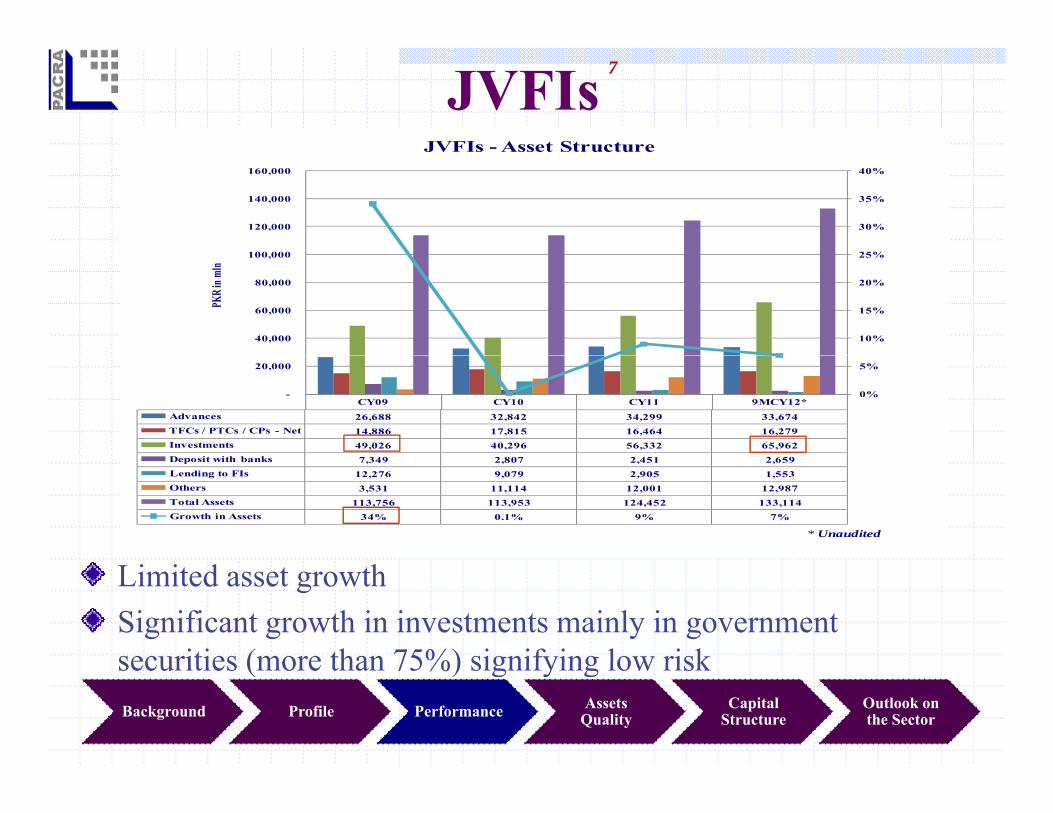

JVFIs JVFIs - Asset Structure

7

25%

30%

35%

40%

100 000

120,000

140,000

160,000

JVFIs Asset Structure

10%

15%

20%

25%

40,000

60,000

80,000

100,000

PKR i

n mln

CY09 CY10 CY11 9MCY12*Advances 26,688 32,842 34,299 33,674 TFCs / PTCs / CPs - Net 14,886 17,815 16,464 16,279 Investments 49,026 40,296 56,332 65,962 Deposit ith banks 7 349 2 807 2 451 2 659

0%

5%

-

20,000

Deposit with banks 7,349 2,807 2,451 2,659 Lending to FIs 12,276 9,079 2,905 1,553 Others 3,531 11,114 12,001 12,987 Total Assets 113,756 113,953 124,452 133,114 Growth in Assets 34% 0.1% 9% 7%

* Unaudited

Limited asset growth Significant growth in investments mainly in government securities (more than 75%) signifying low risksecurities (more than 75%) signifying low risk Background Profile Performance Assets

QualityCapital

StructureOutlook on the Sector

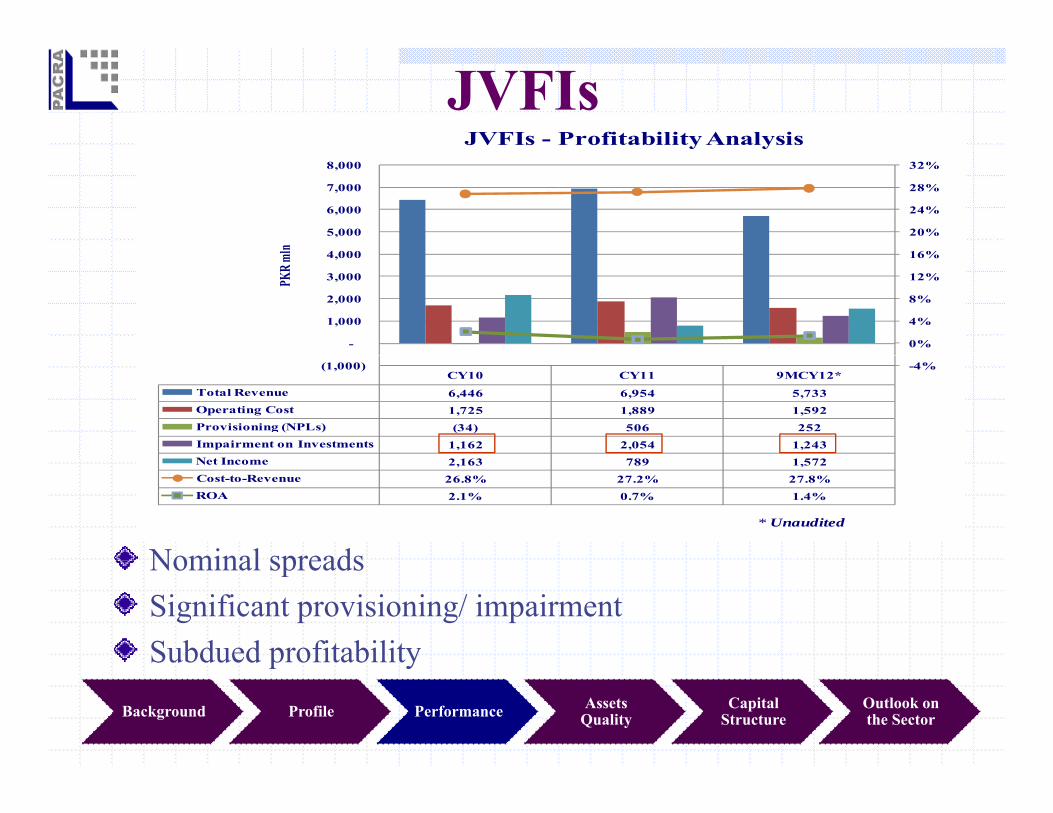

JVFIsJVFIs - Profitability Analysis

16%

20%

24%

28%

32%

4 000

5,000

6,000

7,000

8,000

ln

0%

4%

8%

12%

16%

-

1,000

2,000

3,000

4,000

PKR m

l

CY10 CY11 9MCY12*Total Revenue 6,446 6,954 5,733 Operating Cost 1,725 1,889 1,592 Provisioning (NPLs) (34) 506 252 Impairment on Investments 1,162 2,054 1,243 N I

-4%(1,000)

Nominal spreads

Net Income 2,163 789 1,572 Cost-to-Revenue 26.8% 27.2% 27.8%ROA 2.1% 0.7% 1.4%

* Unaudited

Nominal spreadsSignificant provisioning/ impairmentSubdued profitabilityp y

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

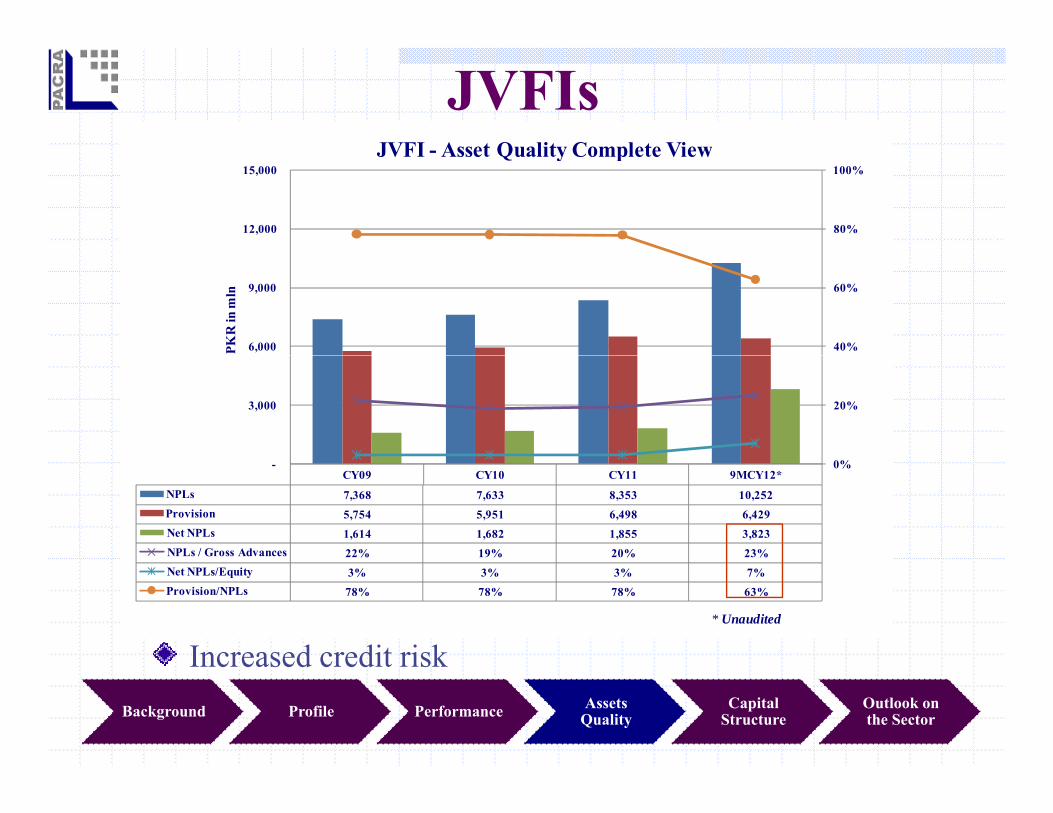

JVFIsJVFI Asset Quality Complete View

80%

100%

12,000

15,000 JVFI - Asset Quality Complete View

40%

60%

6,000

9,000

PKR

in m

ln

20%3,000

CY09 CY10 CY11 9MCY12*NPLs 7,368 7,633 8,353 10,252 Provision 5,754 5,951 6,498 6,429 Net NPLs 1,614 1,682 1,855 3,823 NPLs / Gross Advances 22% 19% 20% 23%

0%-

Increased credit risk

Net NPLs/Equity 3% 3% 3% 7%Provision/NPLs 78% 78% 78% 63%

* Unaudited

Increased credit riskBackground Profile Performance Assets

QualityCapital

StructureOutlook on the Sector

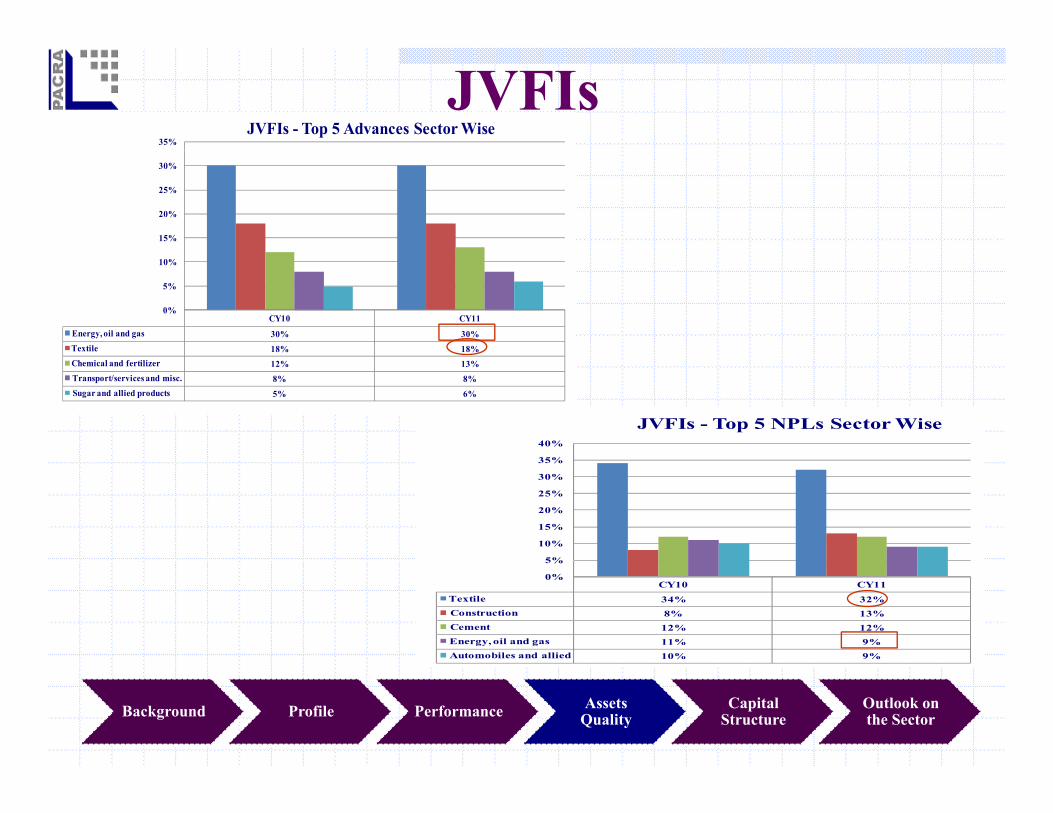

35%JVFIs - Top 5 Advances Sector Wise

JVFIs

15%

20%

25%

30%

CY10 CY11Energy, oil and gas 30% 30%Textile 18% 18%

0%

5%

10%

Chemical and fertilizer 12% 13%Transport/services and misc. 8% 8%Sugar and allied products 5% 6%

35%

40%

JVFIs - Top 5 NPLs Sector Wise

5%

10%

15%

20%

25%

30%

35%

CY10 CY11Textile 34% 32%Construction 8% 13%Cement 12% 12%Energy, oil and gas 11% 9%Automobiles and allied 10% 9%

0%

5%

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

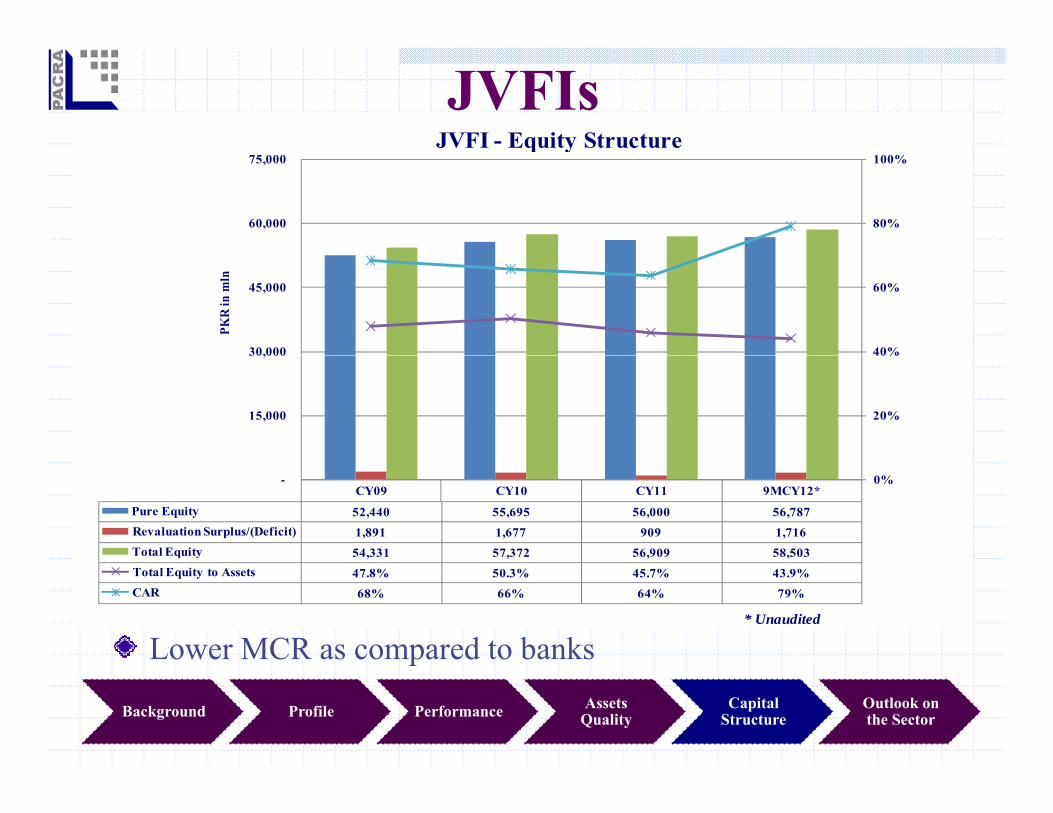

JVFIsJVFI - Equity Structure

80%

100%

60,000

75,000 q y

40%

60%

30,000

45,000

PKR

in m

ln

20%

40%

15,000

30,000

CY09 CY10 CY11 9MCY12*Pure Equity 52,440 55,695 56,000 56,787 Revaluation Surplus/(Deficit) 1,891 1,677 909 1,716 Total Equity 54,331 57,372 56,909 58,503

0%-

Lower MCR as compared to banks

Total Equity to Assets 47.8% 50.3% 45.7% 43.9%CAR 68% 66% 64% 79%

* Unaudited

p

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

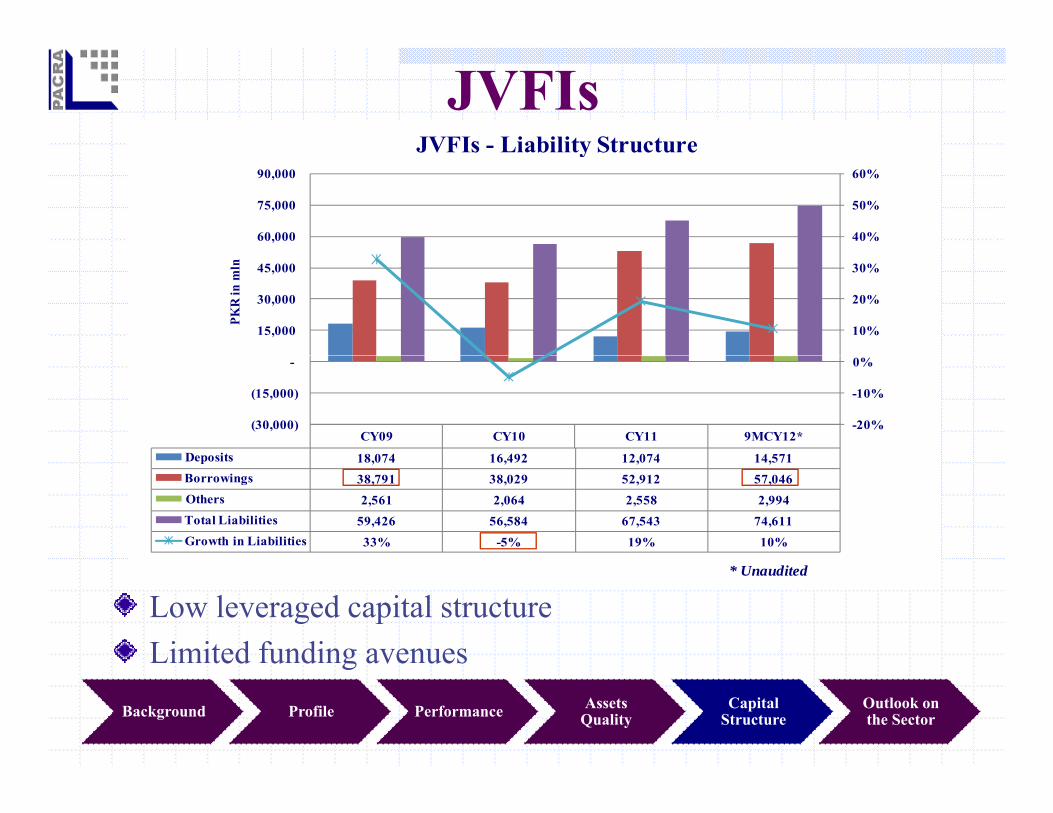

JVFIsJVFIs - Liability Structure

40%

50%

60%

60,000

75,000

90,000

JVFIs Liability Structure

10%

20%

30%

15,000

30,000

45,000

PKR

in m

ln

CY09 CY10 CY11 9MCY12*Deposits 18 074 16 492 12 074 14 571

-20%

-10%

0%

(30,000)

(15,000)

-

Deposits 18,074 16,492 12,074 14,571 Borrowings 38,791 38,029 52,912 57,046 Others 2,561 2,064 2,558 2,994 Total Liabilities 59,426 56,584 67,543 74,611 Growth in Liabilities 33% -5% 19% 10%

Low leveraged capital structureLimited funding avenues

* Unaudited

ted u d g ave ues

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

Opportunities ppLow leveraging providing significant room for expansion(Sector CAR: above 60%)Only few new projects/ventures have been started by fewJVFIs as against the mandate. These JVFIs may work aspartners for the development of industrial sectorpartners for the development of industrial sector

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

Ch llChallengesTransition to PSEs’ Corporate Governance structureE d li i l i i f i kExposed to political intervention for appointment at key positions Absence of a separate regulatory framework as these JVFIsAbsence of a separate regulatory framework as these JVFIs are supervised as a commercial institutionUnderdeveloped skill setup for evaluation of project fi ifinancingFew viable funding sources resulting in higher cost Limited outreachLimited outreach

Background Profile Performance AssetsQuality

Capital Structure

Outlook on the Sector

Bibliography

1. Armendáriz de Aghion (1999, p. 83)2. http://www.icicibank.com/aboutus/about-us.html 3 http://www idbi com/idbi bank history asp3. http://www.idbi.com/idbi-bank-history.asp4. http://www.pacra.com/

http://www.jcrvis.com.pk/5. The World Bank: http://data.worldbank.org/countryp g y6. http://www.standardandpoors.com/ratings/sovereigns/ratings-

list/en/us/?sectorName=Governments&subSectorCode=39&subSectorName=Sovereigns7. Financial statements:

i P k Lib H ldi C (P i t ) Li it di. Pak Libya Holding Company (Private) Limited, ii. Pakistan Kuwait Investment Company (Private) Limited, iii. Saudi Pak Industrial and Agricultural Investment Company Limited, iv. Pak Oman Investment Company Limited,iv. Pak Oman Investment Company Limited, v. Pak Brunei Investment Company Limited, vi. PAΪR Investment Company Limited, vii. Pak China Investment Company Limited

Analysts Rana M. Nadeemnadeem@pacra com

Aisha Khalidaisha@pacra com

Saira Rizwansaira rizwan@pacra com

M. Shahnawaz A. Khanzadashahnawaz aziz@pacra [email protected] [email protected] [email protected] [email protected]

Contact Number: +92 42 3586 9504

DISCLAIMERSCPACRA has used due care in preparation of this document. Our information has been obtainedfrom sources we consider to be reliable but its accuracy or completeness is not guaranteed.The information in this document may be copied or otherwise reproduced, in whole or in part,

id d th i d l k l d d Th t ti h ld t b li dprovided the source is duly acknowledged. The presentation should not be relied upon asprofessional advice.