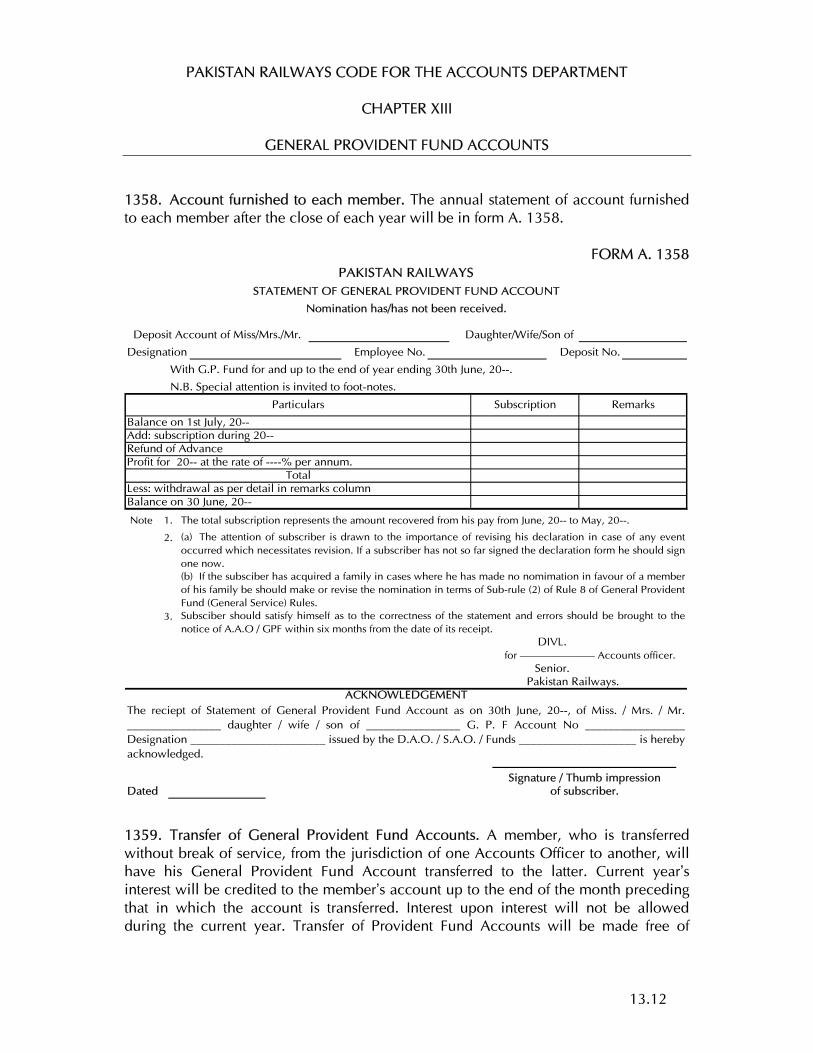

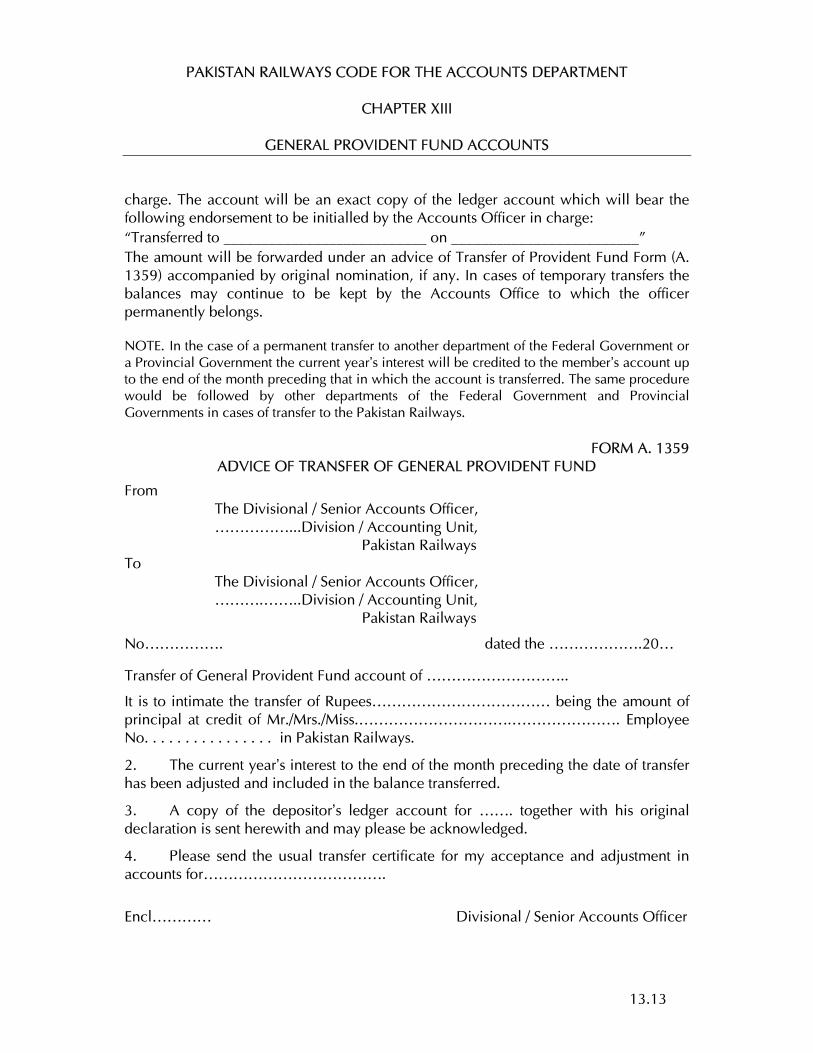

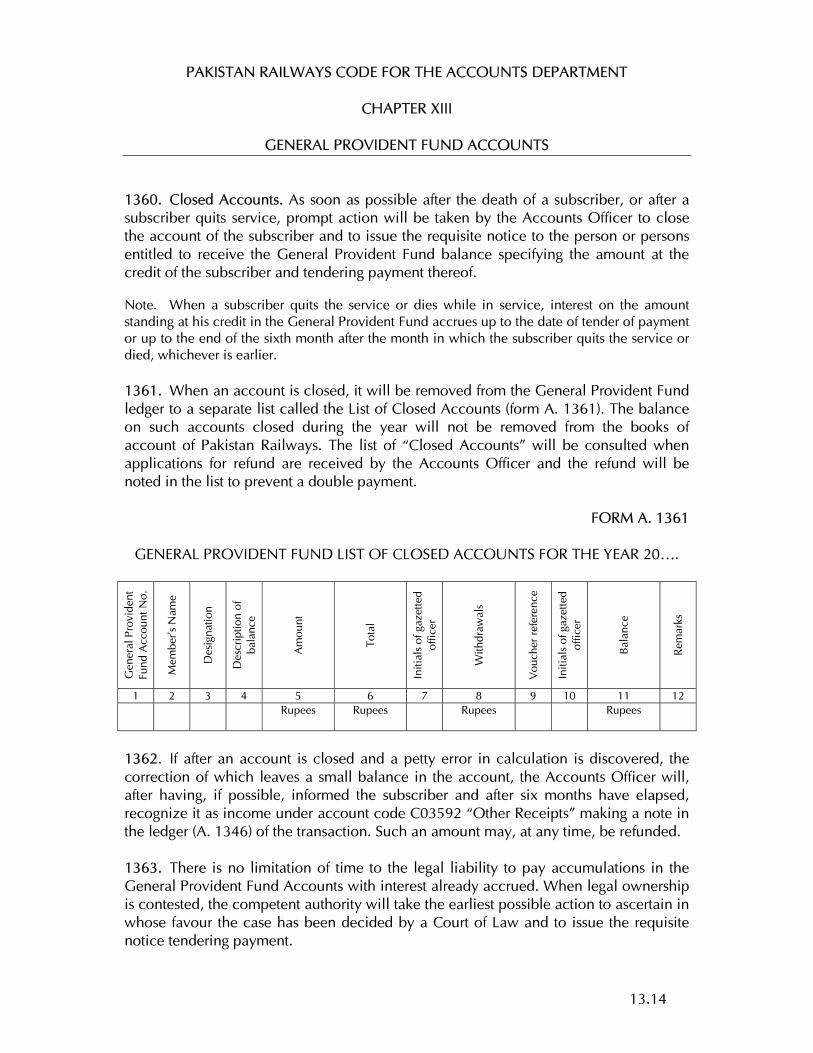

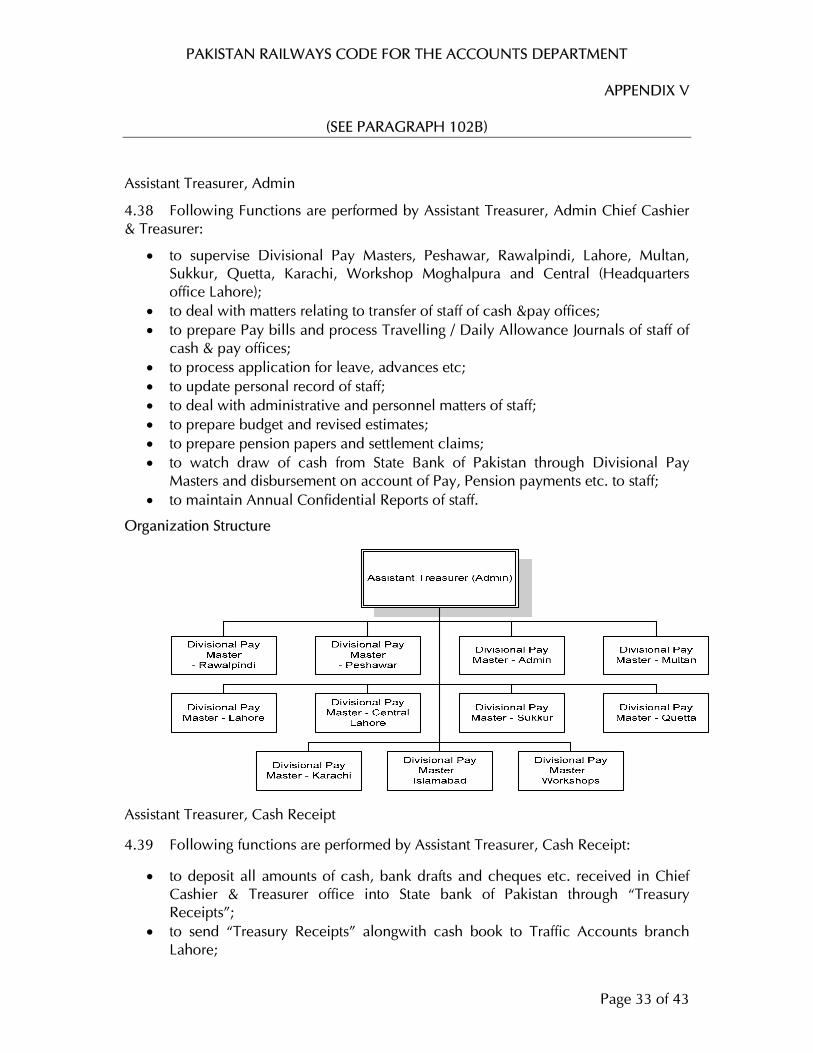

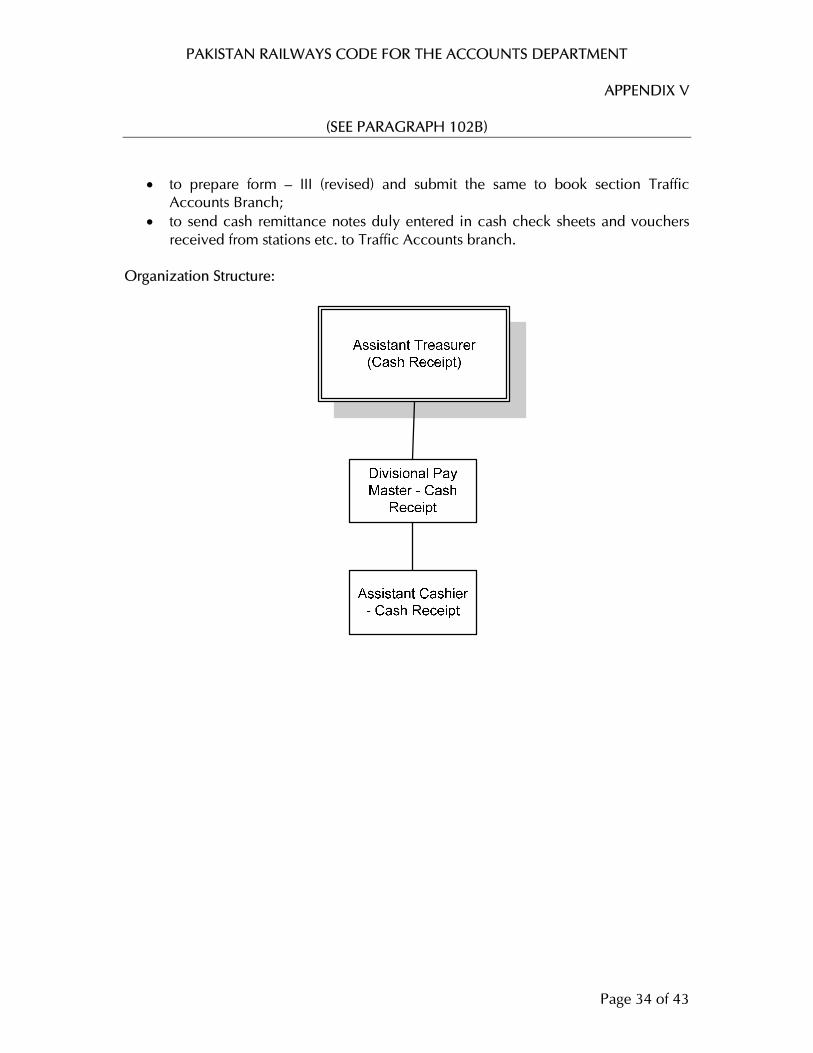

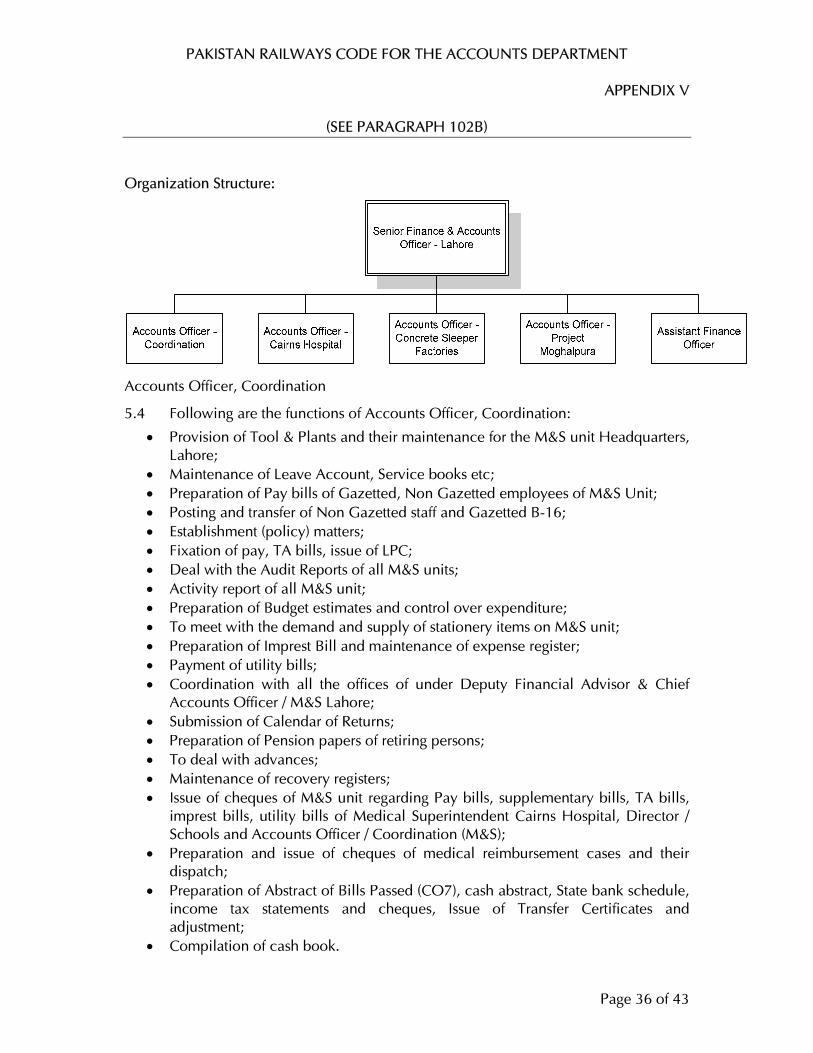

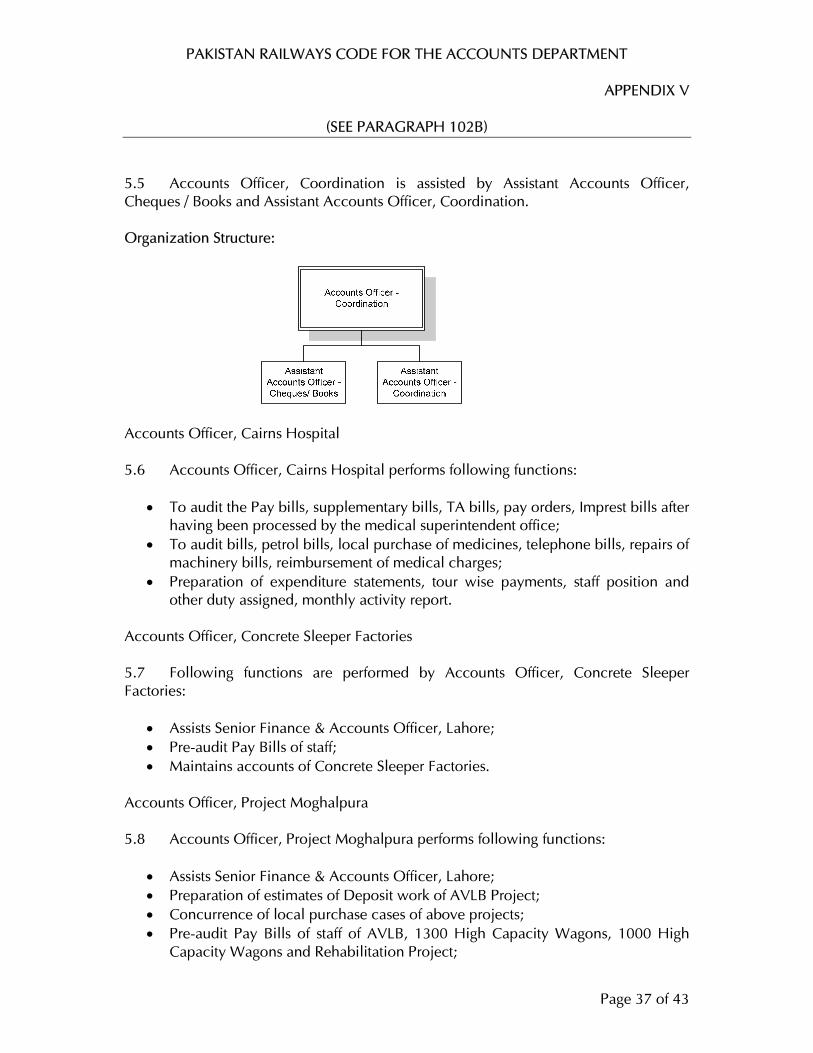

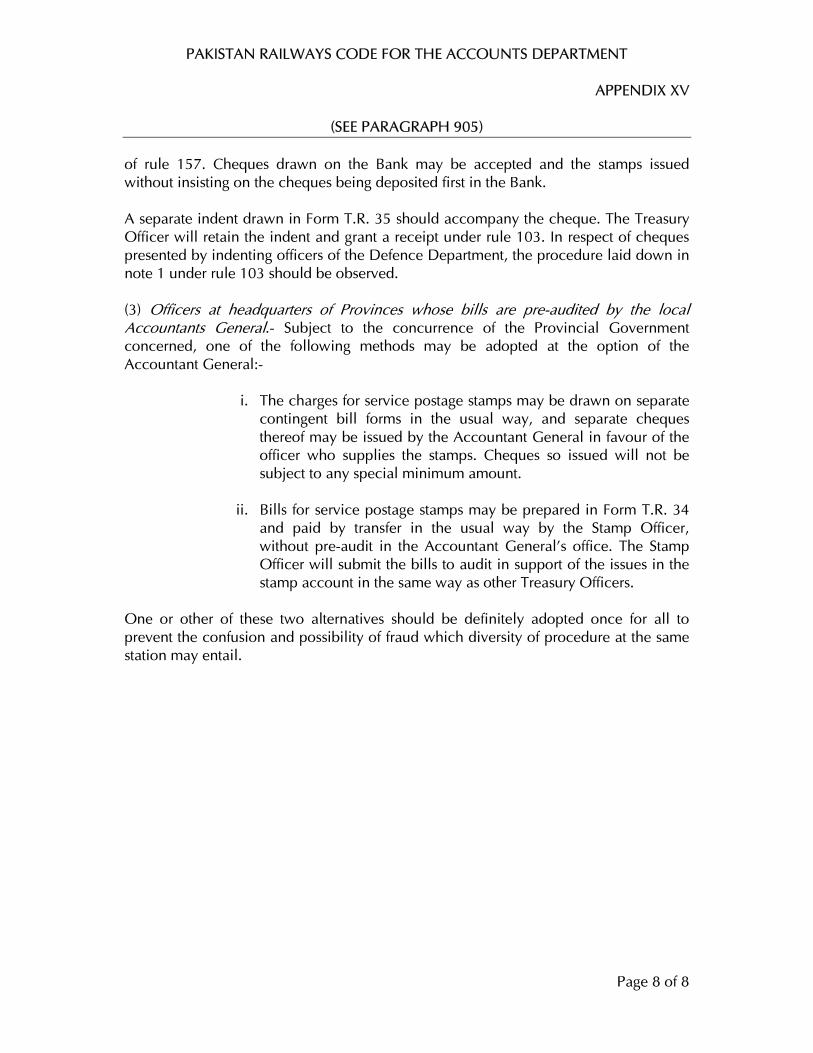

pakistan railways pakistan railways code for the … · railways servant actually retires, or is...

TRANSCRIPT

01.1

(PART I) CHAPTERS I TO XVII

20 October, 2011

PAKISTAN RAILWAYS

Riaz Ahmad & Company Chartered Accountants

P A K I S T A N R A I L W A Y S C O D E F O R T H E A C C O U N T S D E P A R T M E N T ( P A R T I )

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

PREFACE

1. The first edition of this code was brought in 1940 and reprinted after modification on 1st December 1952. Now, an elaborate exercise has been carried out to revise “Pakistan Railways Code for the Accounts Department” for upgraded Financial and Management Information System, under supervision and control of Mr. Mubarik Khan, Project Director, Project Management Unit (PMU), Ministry of Railways and expert review of Mr. Khalid Mehmood Financial Adviser and Chief Accounts Officer Railways (Retired).

2. This code is divided into two parts. Part I contains:

Departmental regulations, bills, internal check, establishment charges, inspection of executive offices, communications from audit and action thereon, cash and pay department, structure of railway accounts, compilation of railways accounts, annual accounts, general provident fund accounts, financial statements as per International Financial Reporting Standards, remittance transactions, control accounts, security deposits, etc.

Part II contains:

Traffic earnings, other coaching traffic, goods traffic receipts, station balance sheet, accounts office debits and their clearance, carriage bills and the accounts office balance sheet, handling bills, traffic book, inspection of station accounts.

3. The rules and orders embodied in this Code are to be followed with due care and caution and are applicable to Pakistan Railways.

4. In case, Financial Adviser & Chief Accounts Officers or any other concerned Principal Officers desire to make any amendment in the procedure laid down in this Code they should address to Member Finance for such authorization in each case.

5. Contributions made by Messrs Saeed Akhtar, General Manager Operations, Muhammad Ali, Deputy Director, (PMU) and efforts made by Riaz Ahmad & Company, Chartered Accountants, Consultants, in accomplishing this task are highly appreciated and placed on record.

Islamabad,

00-00-2012

M.S. Idrees Tarar

Member Finance

Ministry of Railways

Government of Pakistan

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

INTRODUCTORY NOTES

1. Index Letters for Codes The following index letters are used for distinguishing the several Pakistan Railways Codes from each other.

S for the Stores Department. W Mechanical Department (Workshops). A Accounts Department. T Traffic Department (Commercial). E Engineering Department. G General Code.

2. Paragraph Numbers For convenience of indexing and of reference, the paragraphs have been numbered according to a 3/4 figure “code”, in which the last two figures give the number of the paragraph and the remaining figures the number of the chapter. Thus paragraph 101 of any code is paragraph 1 of chapter 1 of that code and paragraph 1421, paragraph 21 of chapter XIV. 3. References to Paragraphs Reference in a code to the paragraphs of any other code is made by putting the paragraph number first, followed by the index letter of the code concerned as the suffix. Thus 1236T means paragraph 36 of Chapter XII of the Pakistan Railways Code for the Traffic Department and 3 App. 5A means paragraph 3 of Appendix V to the Pakistan Railways Code for the Accounts Department. 4. References to “Forms” The “forms” referred to in any of the Pakistan Railways Codes take the number of the paragraph of the code in which they are described, the index letter of the code in question being prefixed to the number of the paragraph in which the form is illustrated. Thus T647 is the form that is described and illustrated in paragraph 47 of Chapter VI of the Pakistan Railways Code for the Traffic Department.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

INDEX (PART-I)

1

DESCRIPTION CHAPTER NO.

DEPARTMENTAL REGULATIONS I

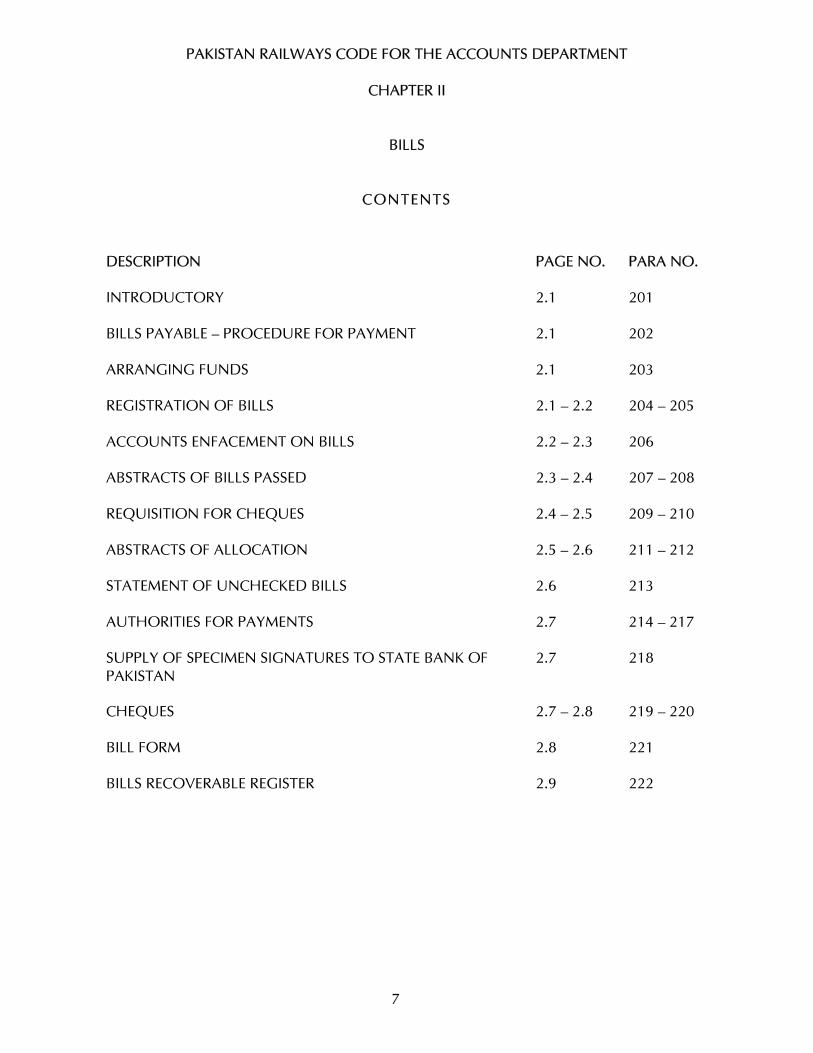

BILLS II

INTERNAL CHECK III

CHECK OF ESTABLISHMENT CHARGES-GENERAL IV

CHECK OF ESTABLISHMENT CHARGES-GAZETTED STAFF V

CHECK OF ESTABLISHMENT CHARGES-NON GAZETTED STAFF VI

INSPECTION OF EXECUTIVE OFFICES VII

COMMUNICATIONS FROM AUDIT AND ACTION THEREON VIII

CASH AND PAY DEPARTMENT IX

STRUCTURE OF RAILWAY ACCOUNTS X

COMPILATION OF RAILWAY ACCOUNTS XI

ANNUAL ACCOUNTS AND RETURNS XII

GENERAL PROVIDENT FUND ACCOUNTS XIII

REMITTANCE TRANSACTIONS XIV

REMITTANCE TRANSACTION-ENGLAND XV (Deleted)

CONTROL ACCOUNTS XIV

SECURITY DEPOSITS XVII

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

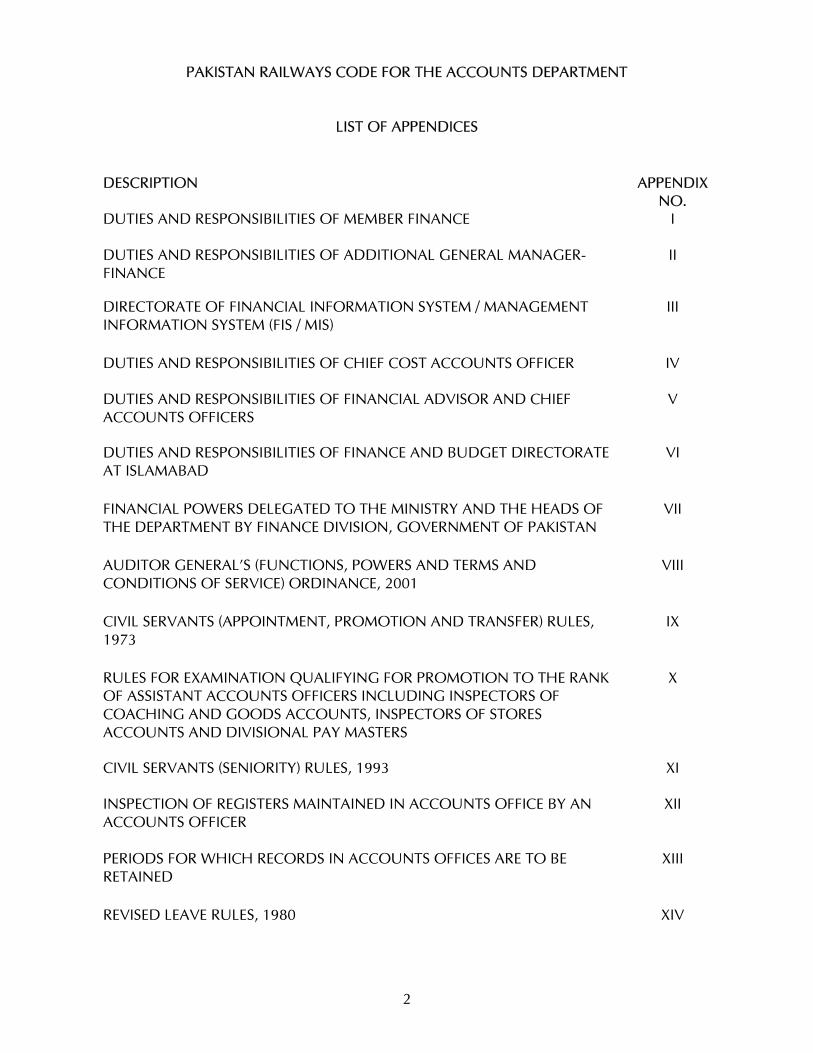

LIST OF APPENDICES

2

DESCRIPTION APPENDIX NO.

DUTIES AND RESPONSIBILITIES OF MEMBER FINANCE I

DUTIES AND RESPONSIBILITIES OF ADDITIONAL GENERAL MANAGER-FINANCE

II

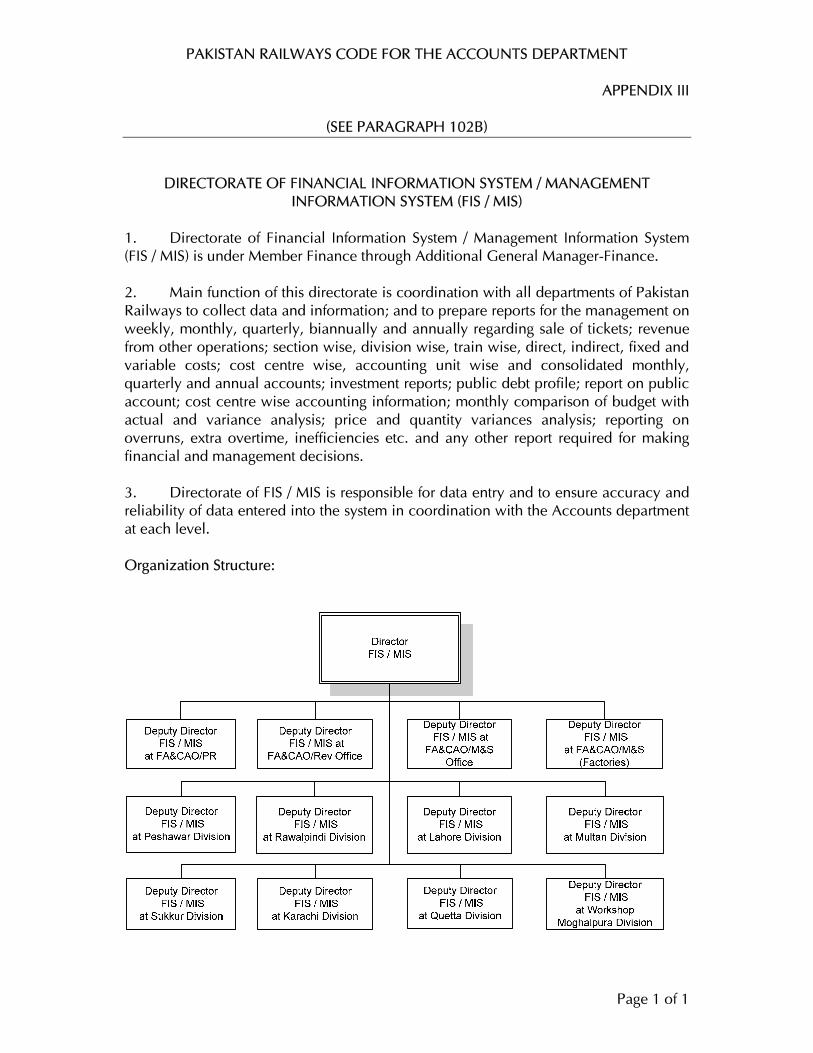

DIRECTORATE OF FINANCIAL INFORMATION SYSTEM / MANAGEMENT INFORMATION SYSTEM (FIS / MIS)

III

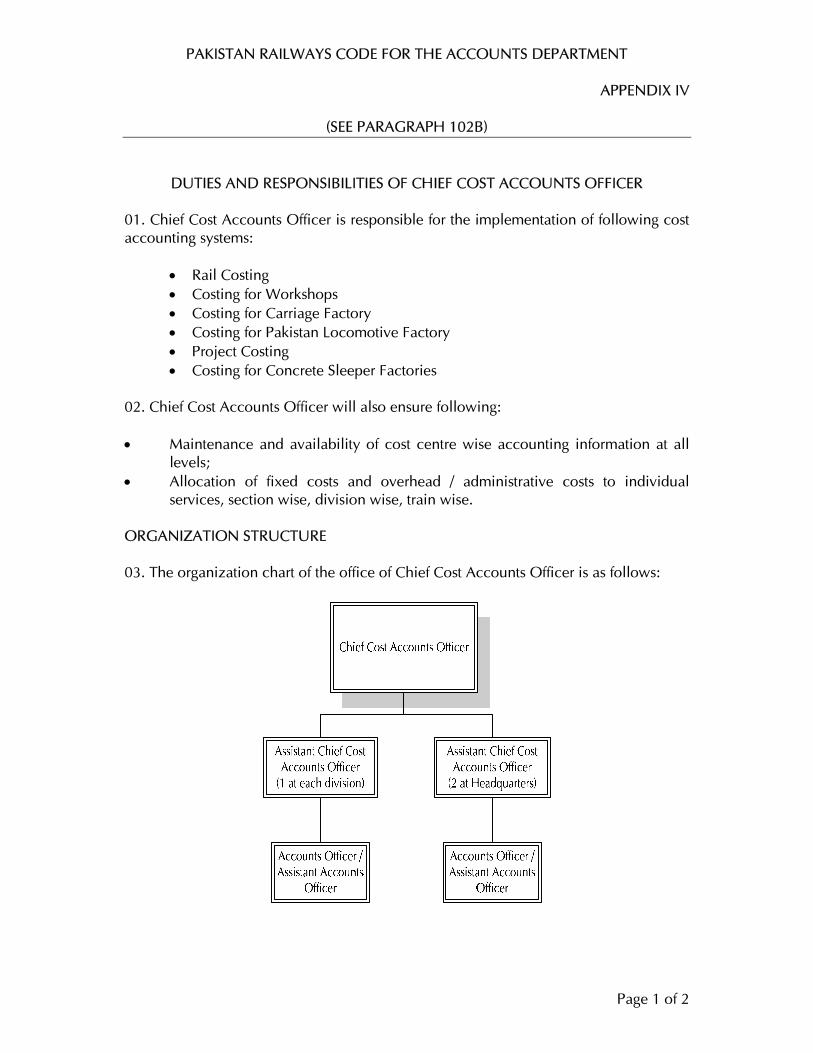

DUTIES AND RESPONSIBILITIES OF CHIEF COST ACCOUNTS OFFICER IV

DUTIES AND RESPONSIBILITIES OF FINANCIAL ADVISOR AND CHIEF ACCOUNTS OFFICERS

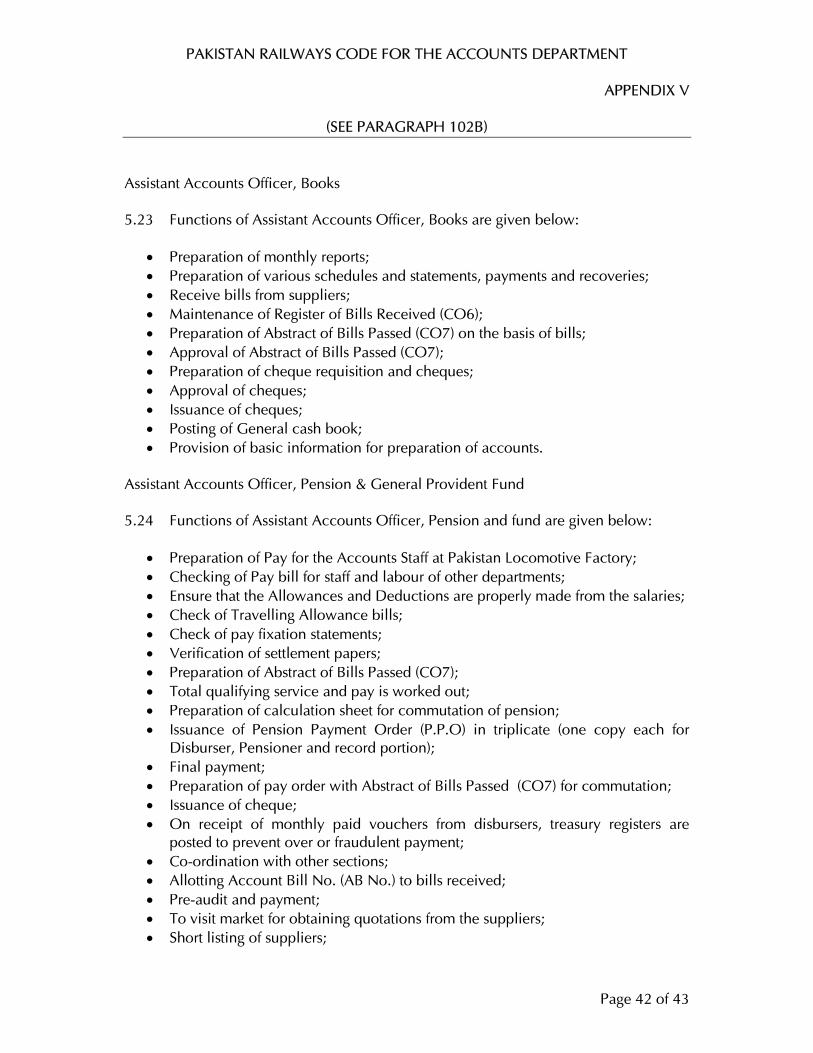

V

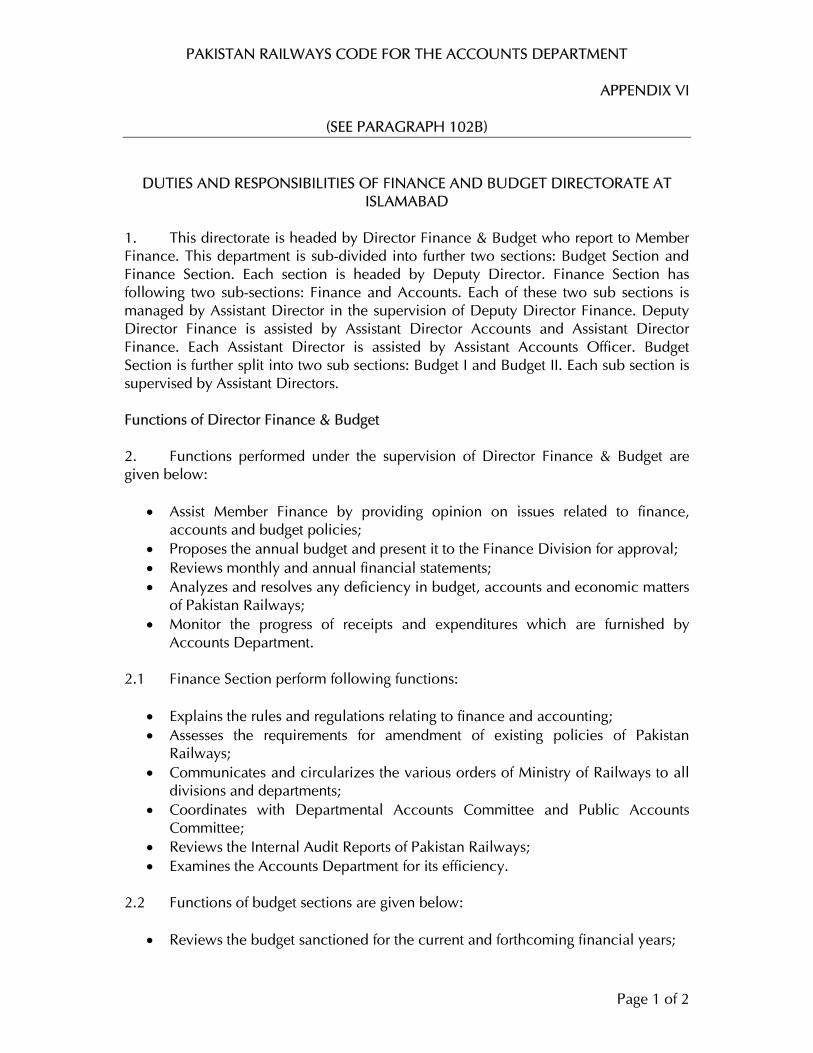

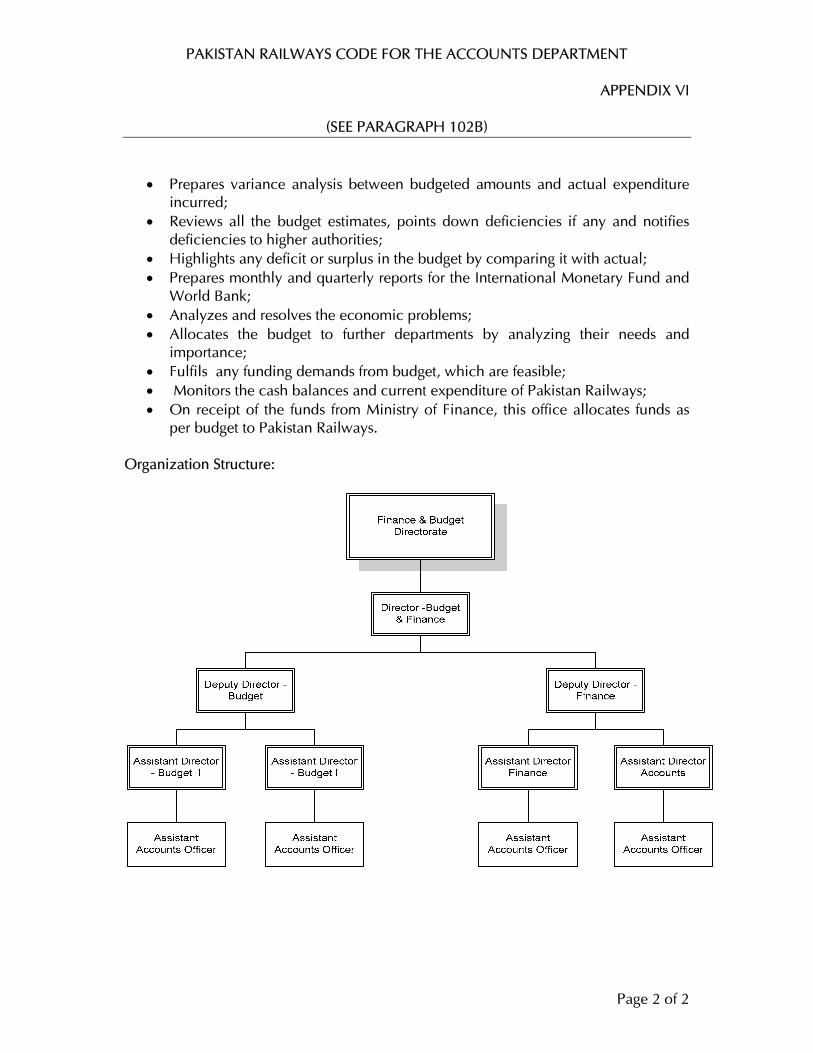

DUTIES AND RESPONSIBILITIES OF FINANCE AND BUDGET DIRECTORATE AT ISLAMABAD

VI

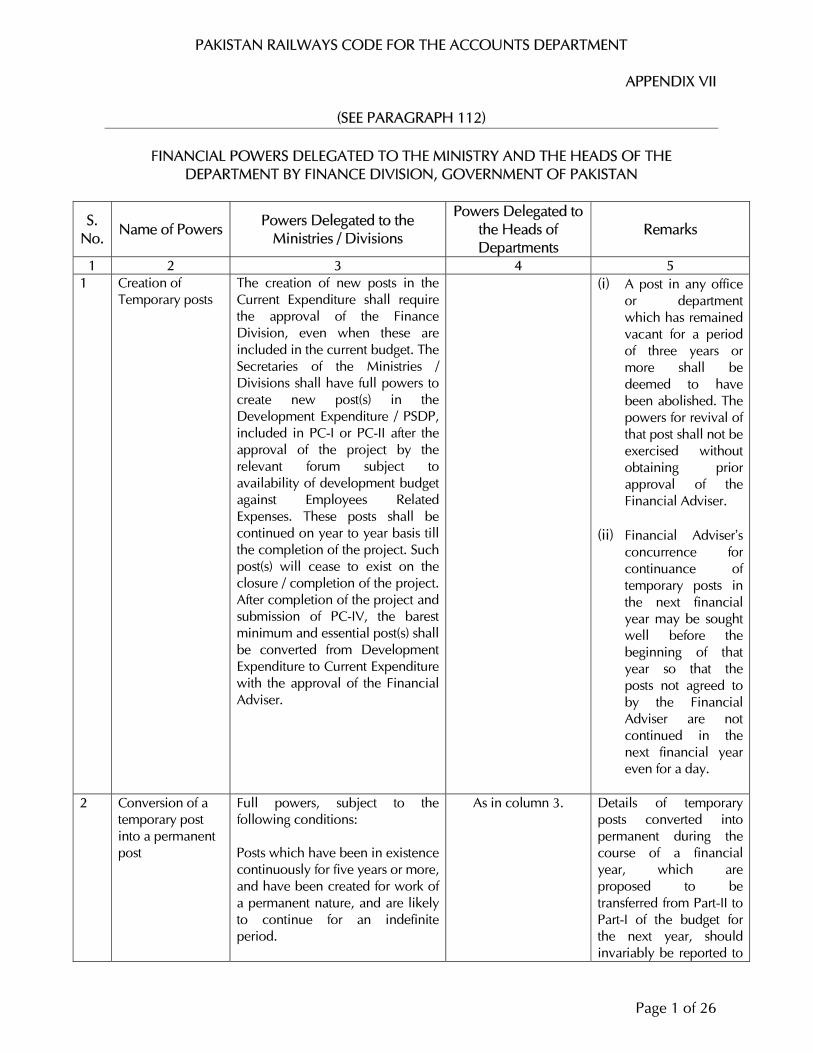

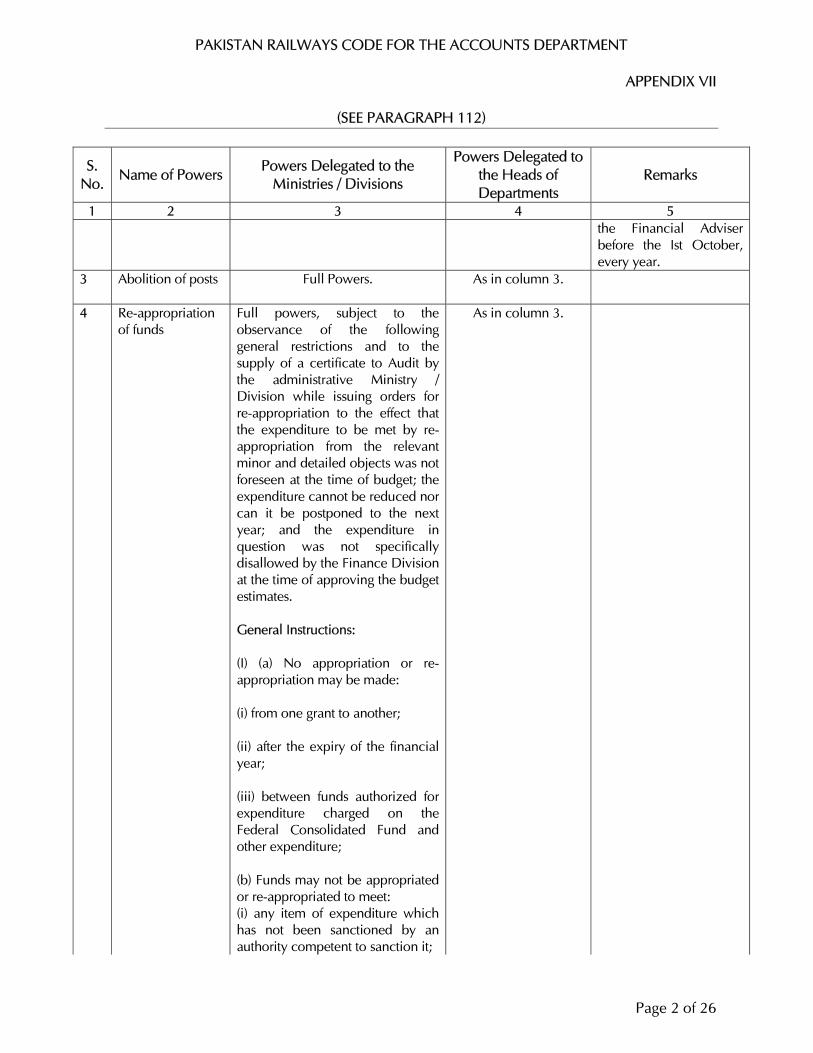

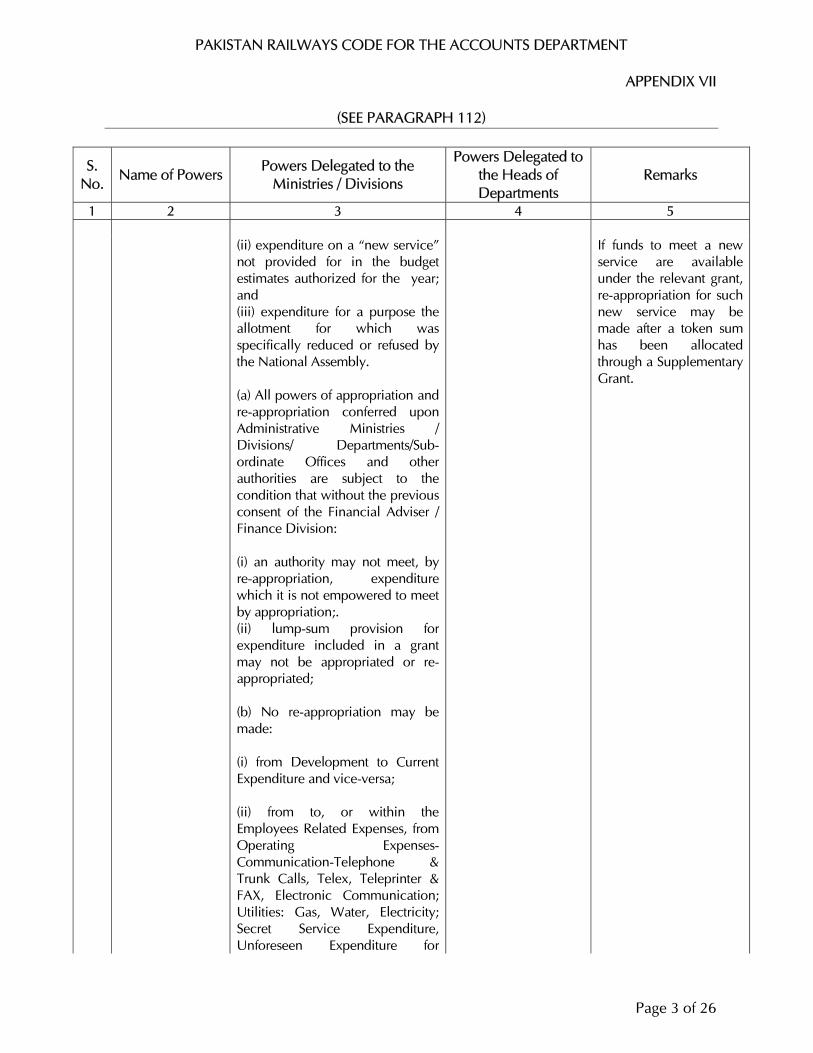

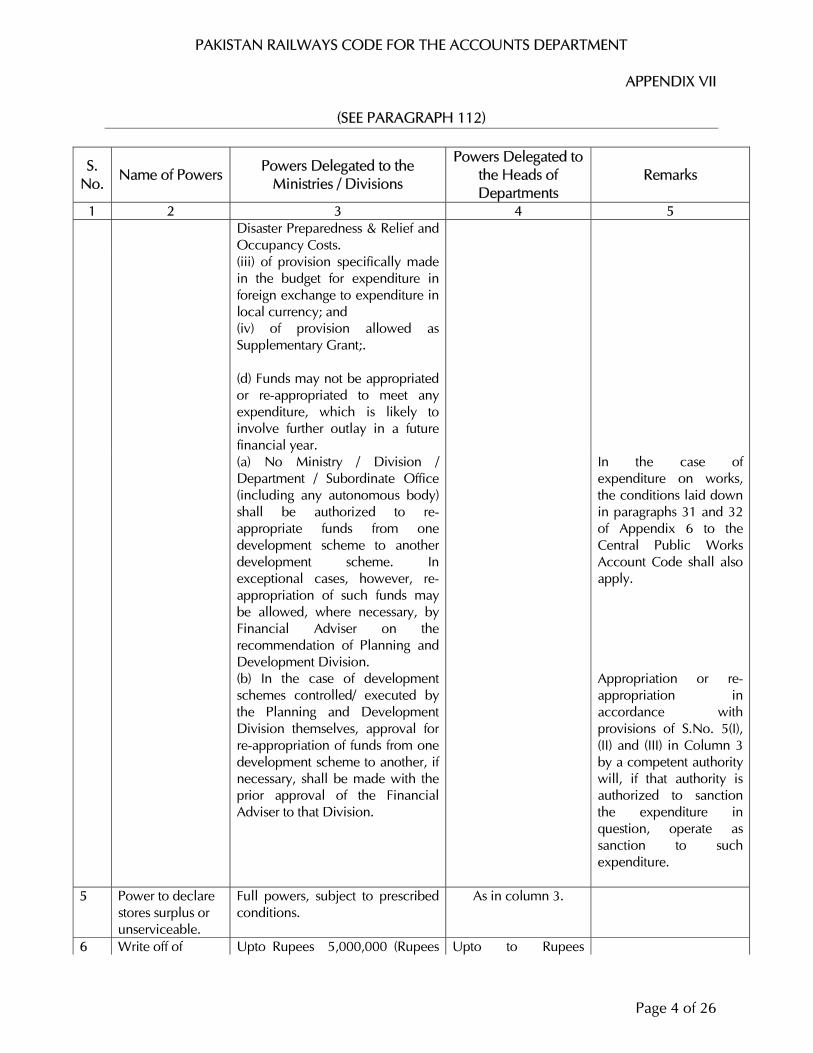

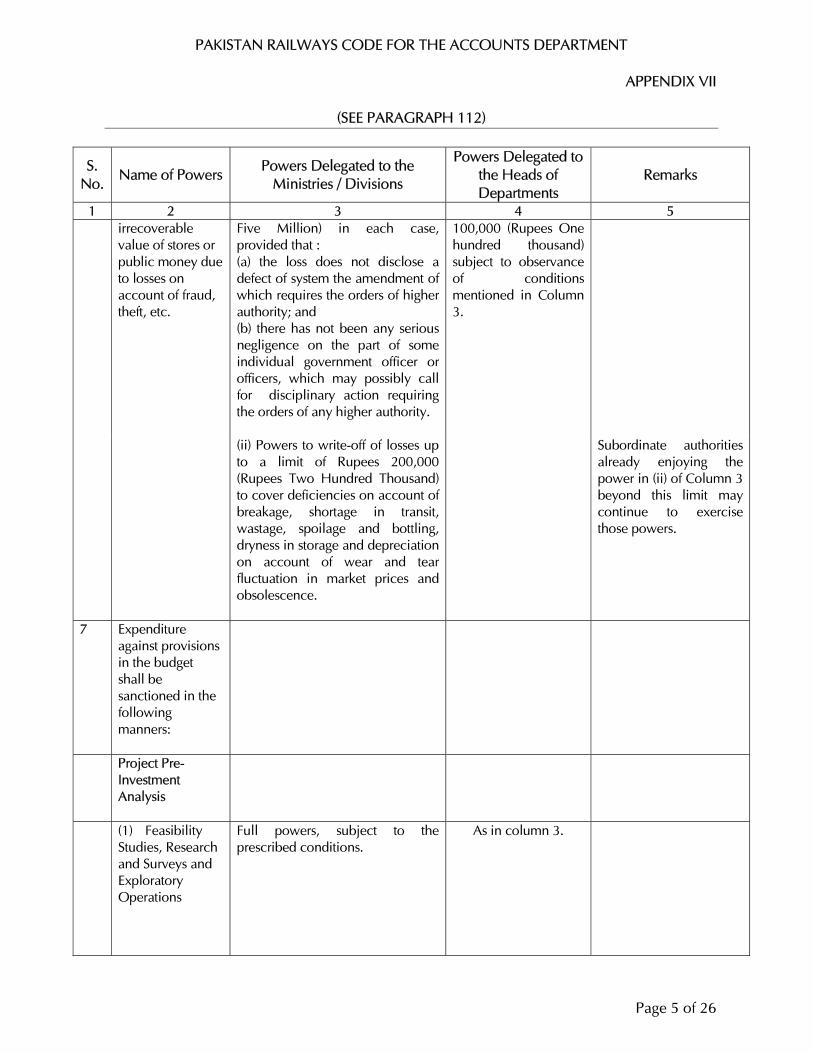

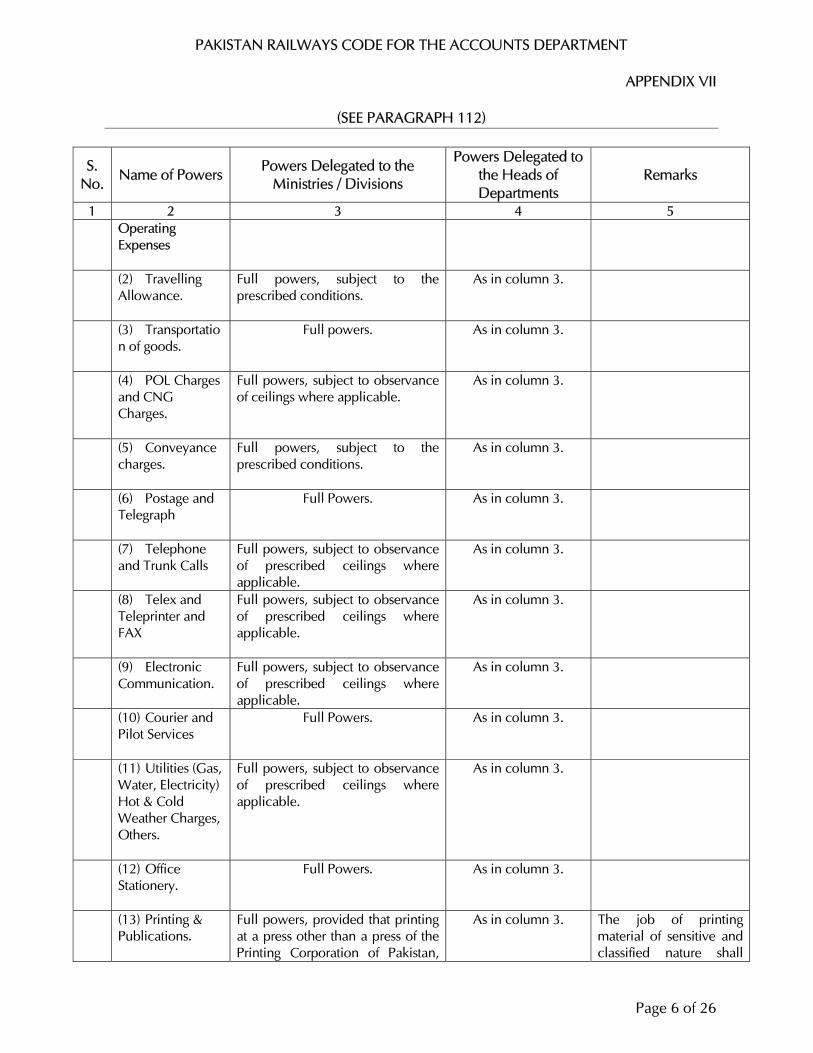

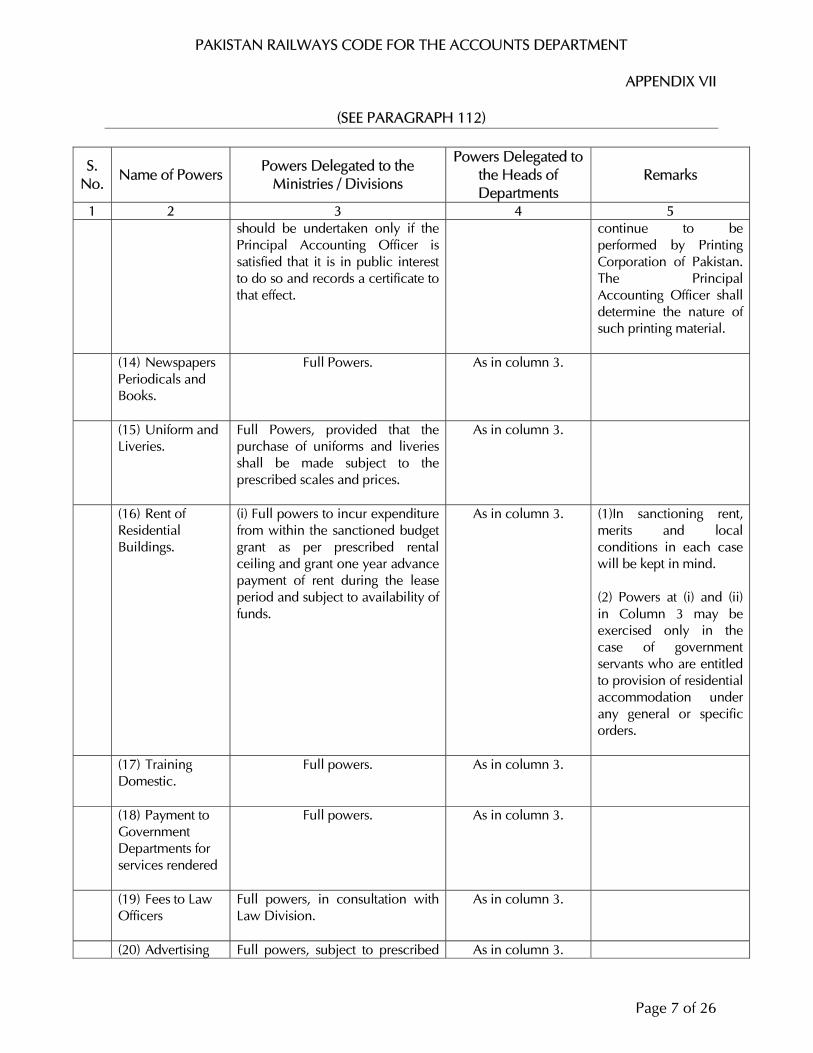

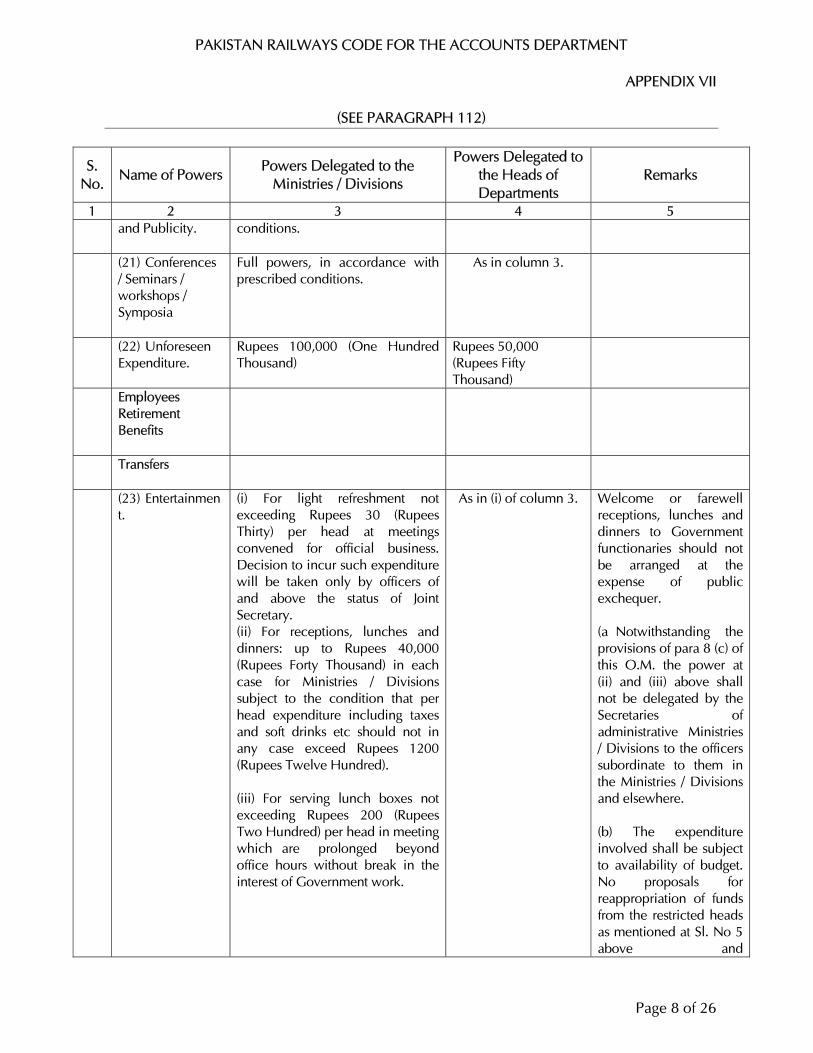

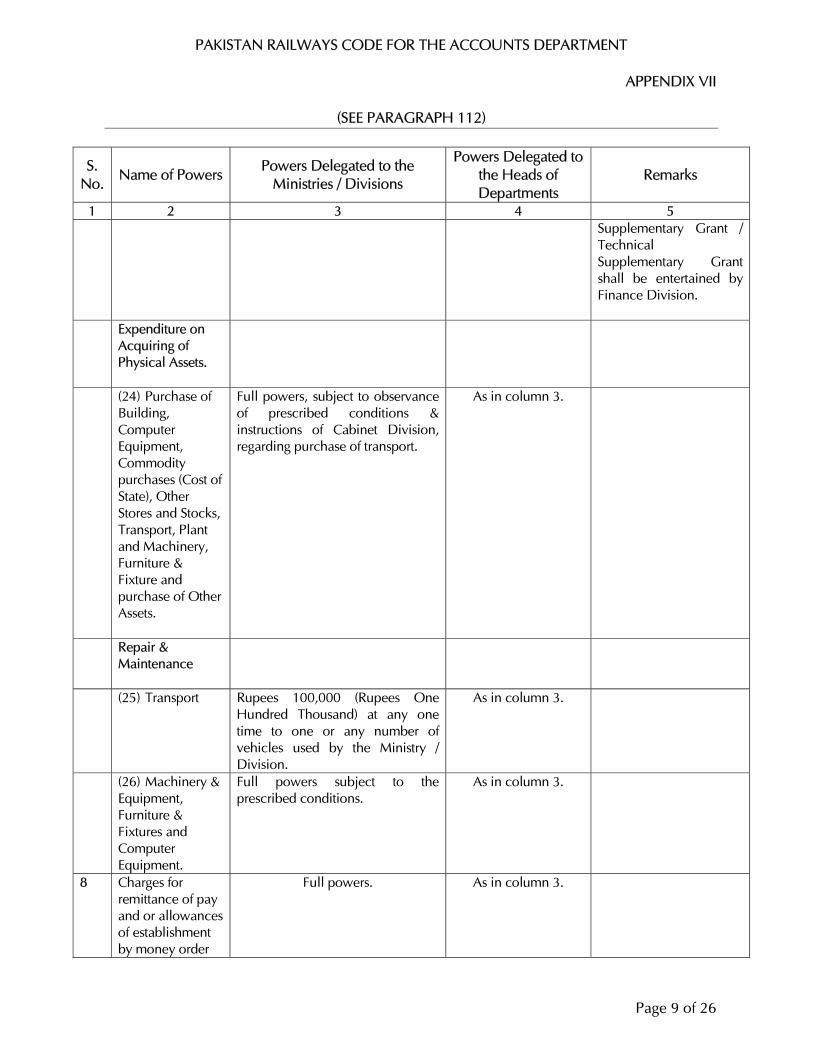

FINANCIAL POWERS DELEGATED TO THE MINISTRY AND THE HEADS OF THE DEPARTMENT BY FINANCE DIVISION, GOVERNMENT OF PAKISTAN

VII

AUDITOR GENERAL'S (FUNCTIONS, POWERS AND TERMS AND CONDITIONS OF SERVICE) ORDINANCE, 2001

VIII

CIVIL SERVANTS (APPOINTMENT, PROMOTION AND TRANSFER) RULES, 1973

IX

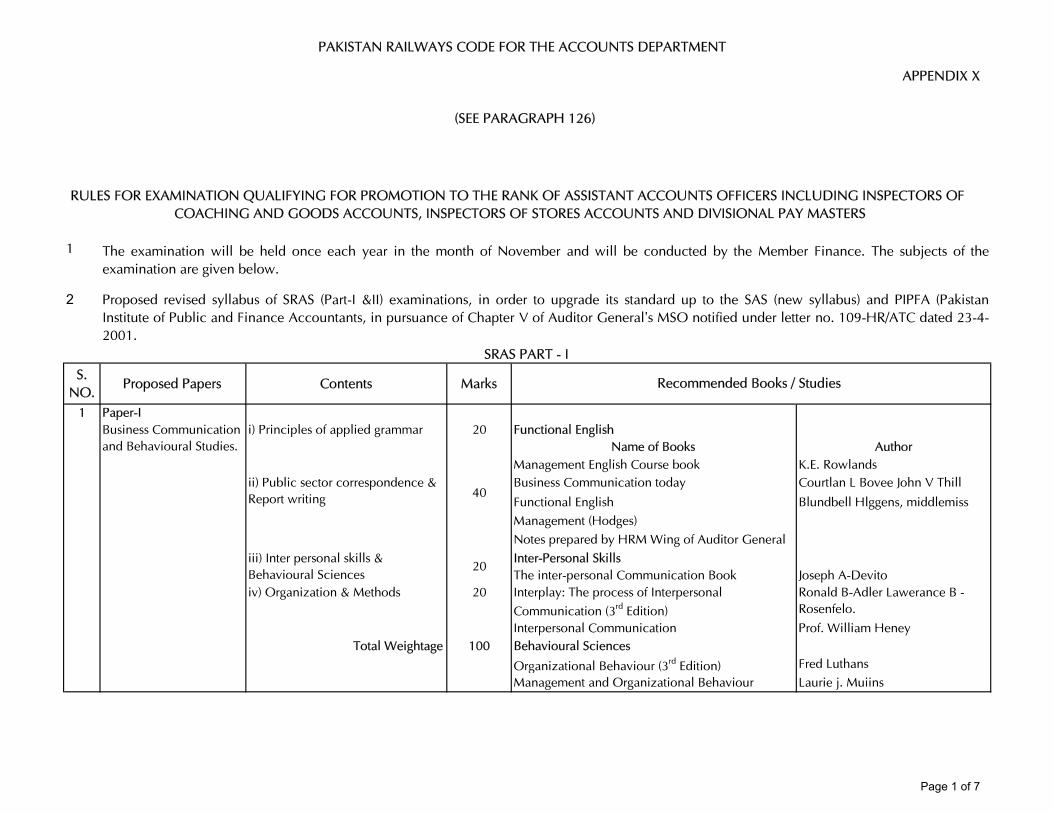

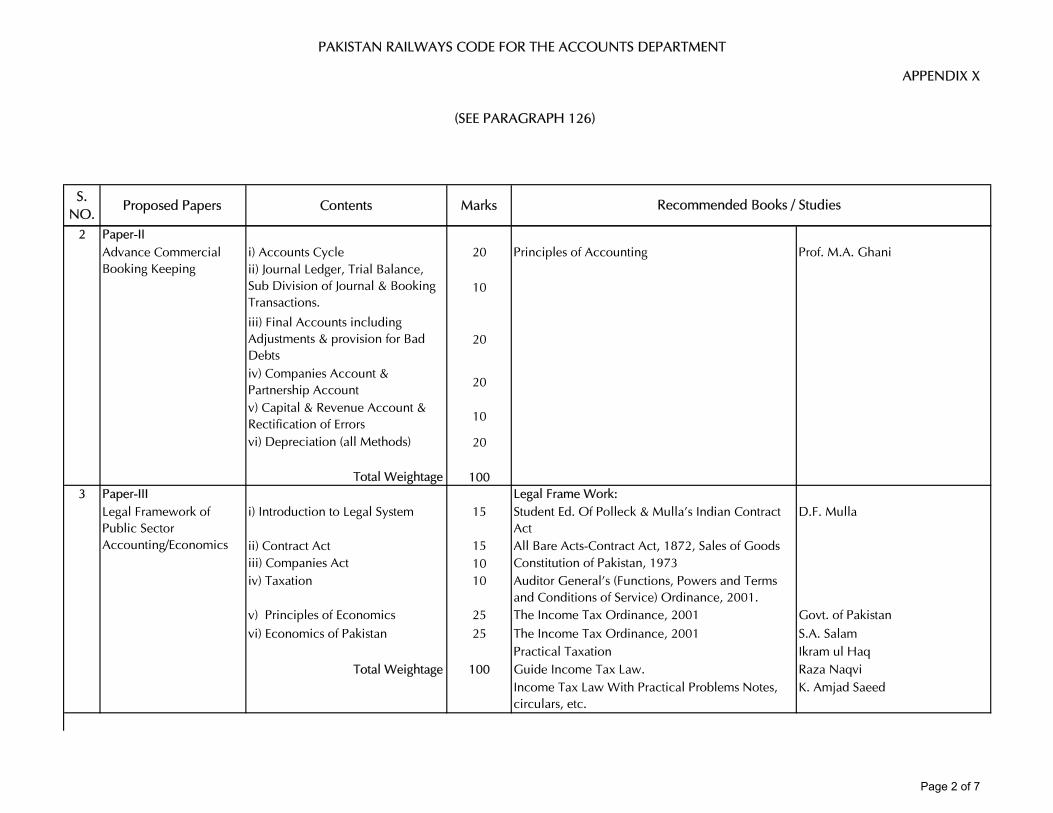

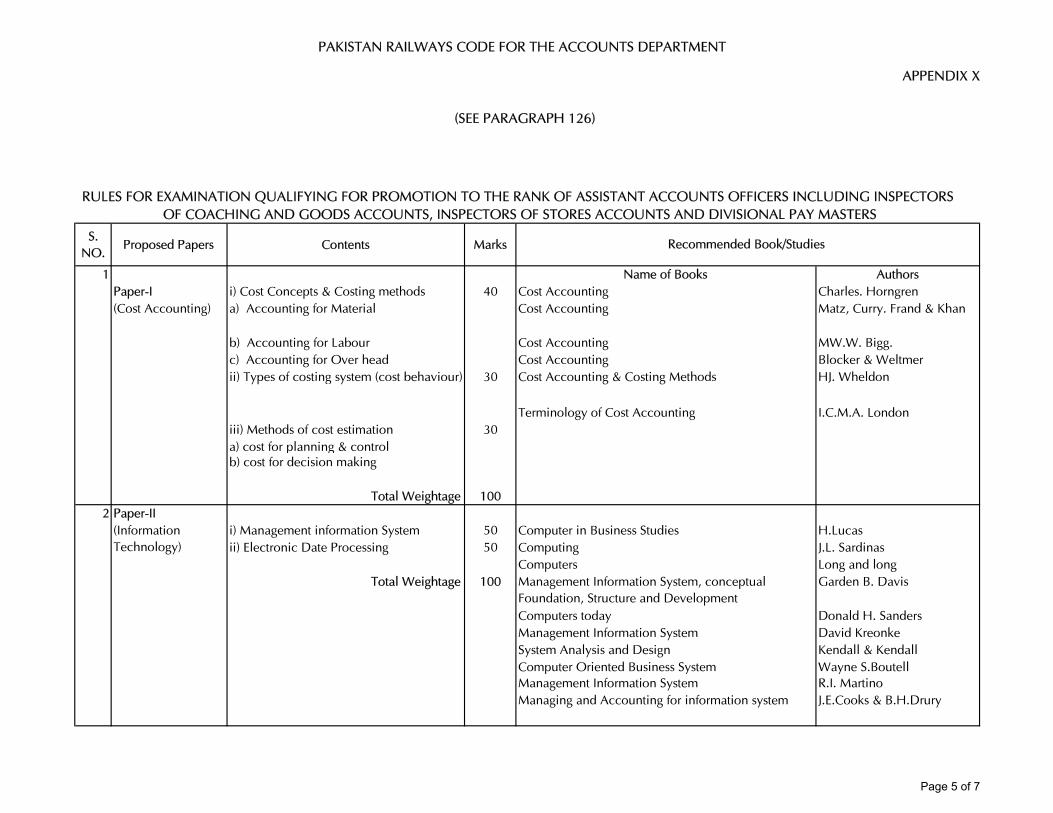

RULES FOR EXAMINATION QUALIFYING FOR PROMOTION TO THE RANK OF ASSISTANT ACCOUNTS OFFICERS INCLUDING INSPECTORS OF COACHING AND GOODS ACCOUNTS, INSPECTORS OF STORES ACCOUNTS AND DIVISIONAL PAY MASTERS

X

CIVIL SERVANTS (SENIORITY) RULES, 1993 XI

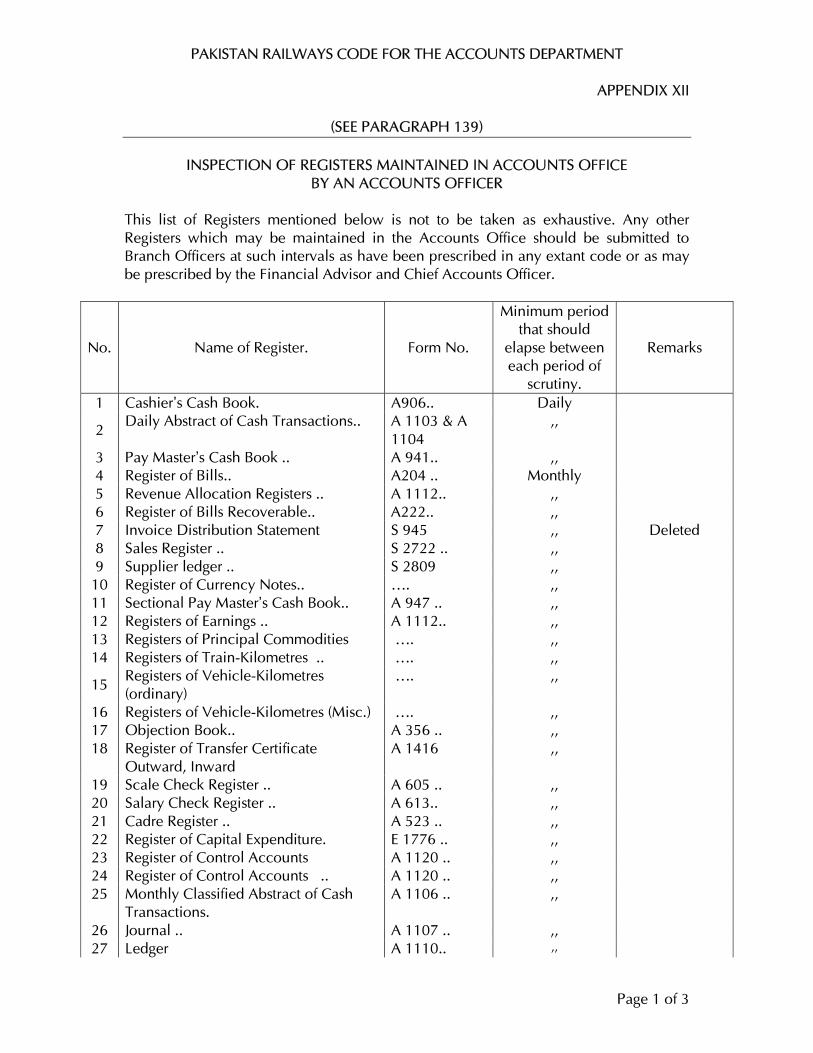

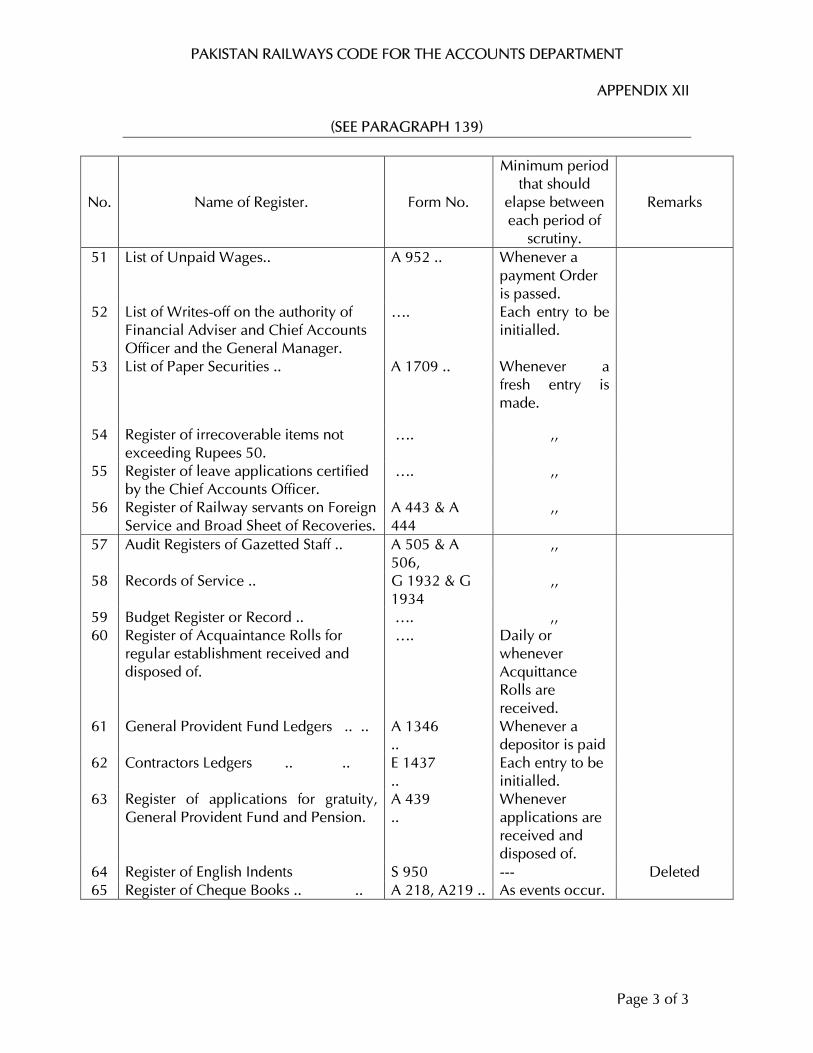

INSPECTION OF REGISTERS MAINTAINED IN ACCOUNTS OFFICE BY AN ACCOUNTS OFFICER

XII

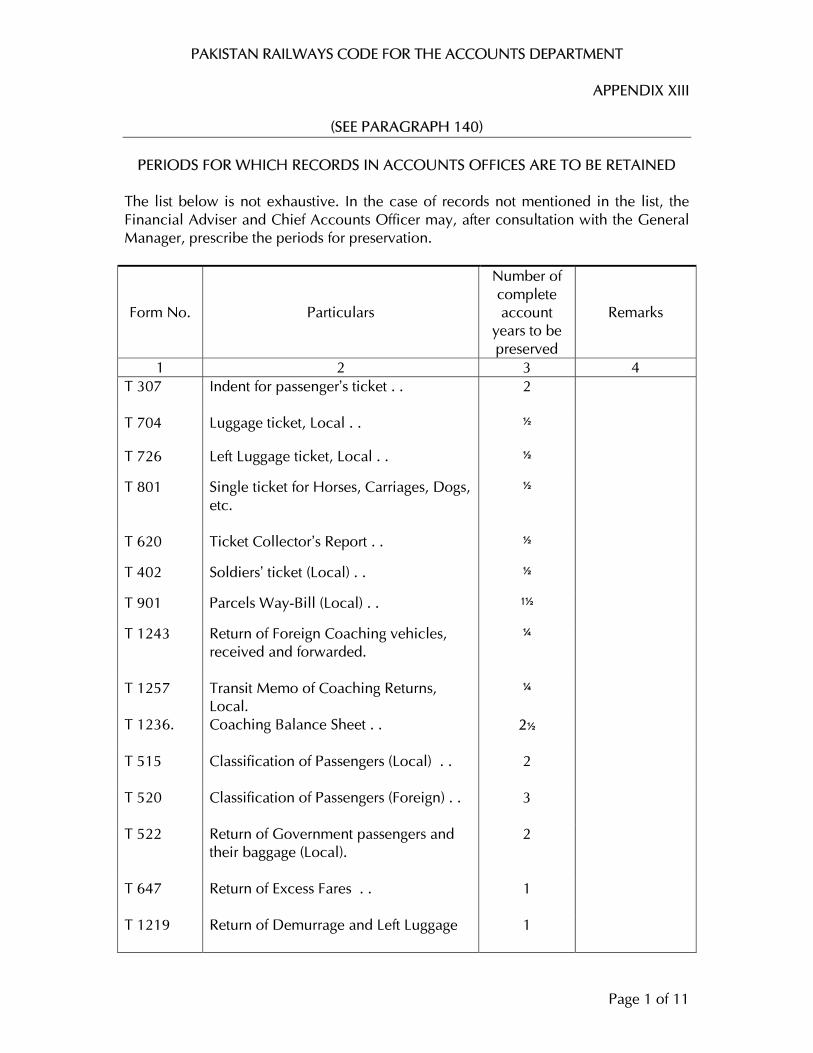

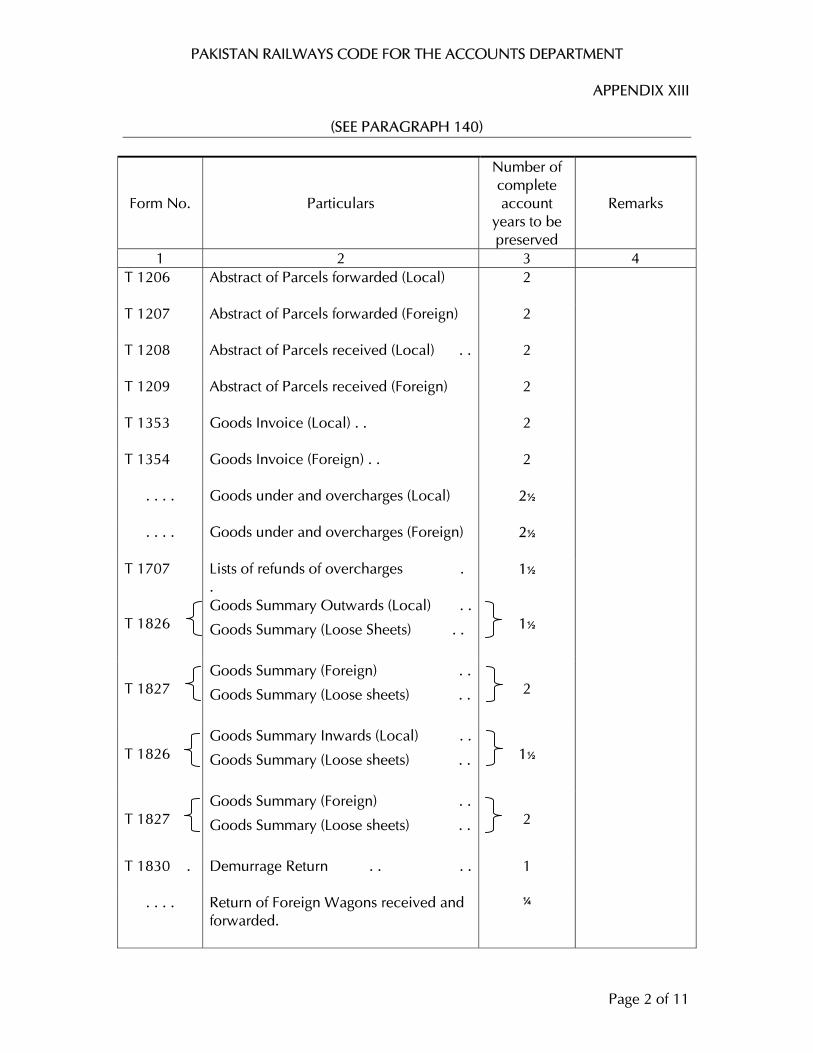

PERIODS FOR WHICH RECORDS IN ACCOUNTS OFFICES ARE TO BE RETAINED

XIII

REVISED LEAVE RULES, 1980 XIV

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

LIST OF APPENDICES

3

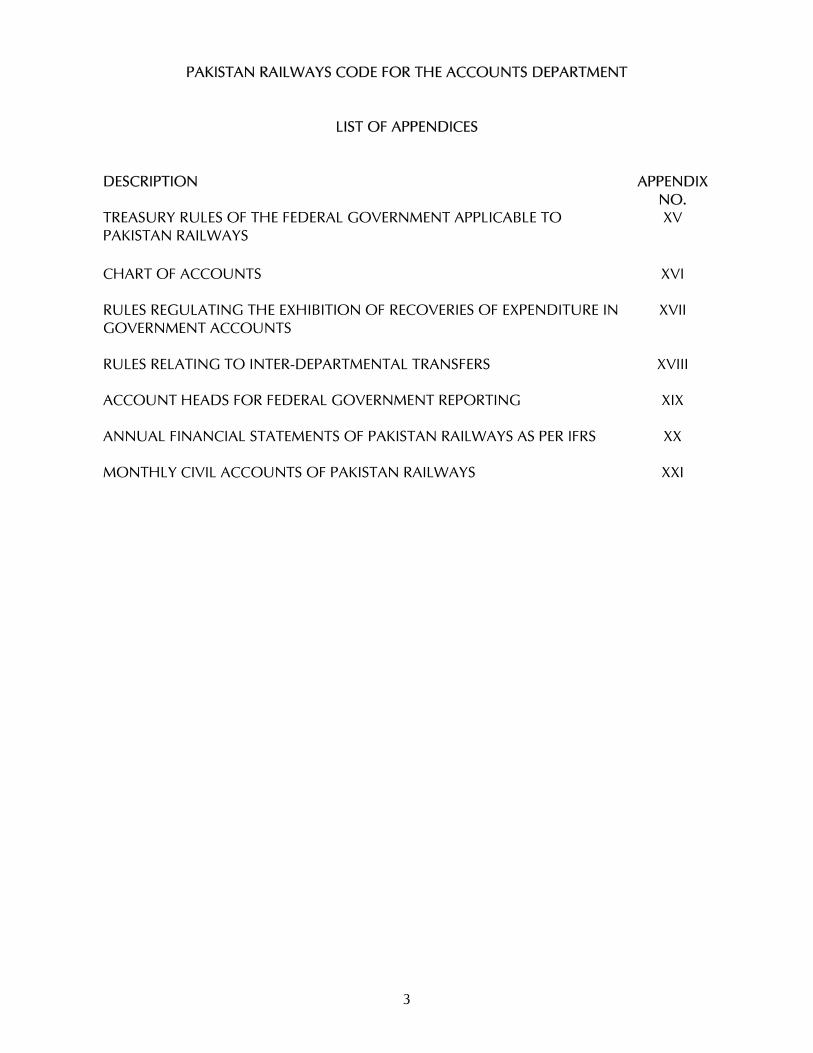

DESCRIPTION APPENDIX NO.

TREASURY RULES OF THE FEDERAL GOVERNMENT APPLICABLE TO PAKISTAN RAILWAYS

XV

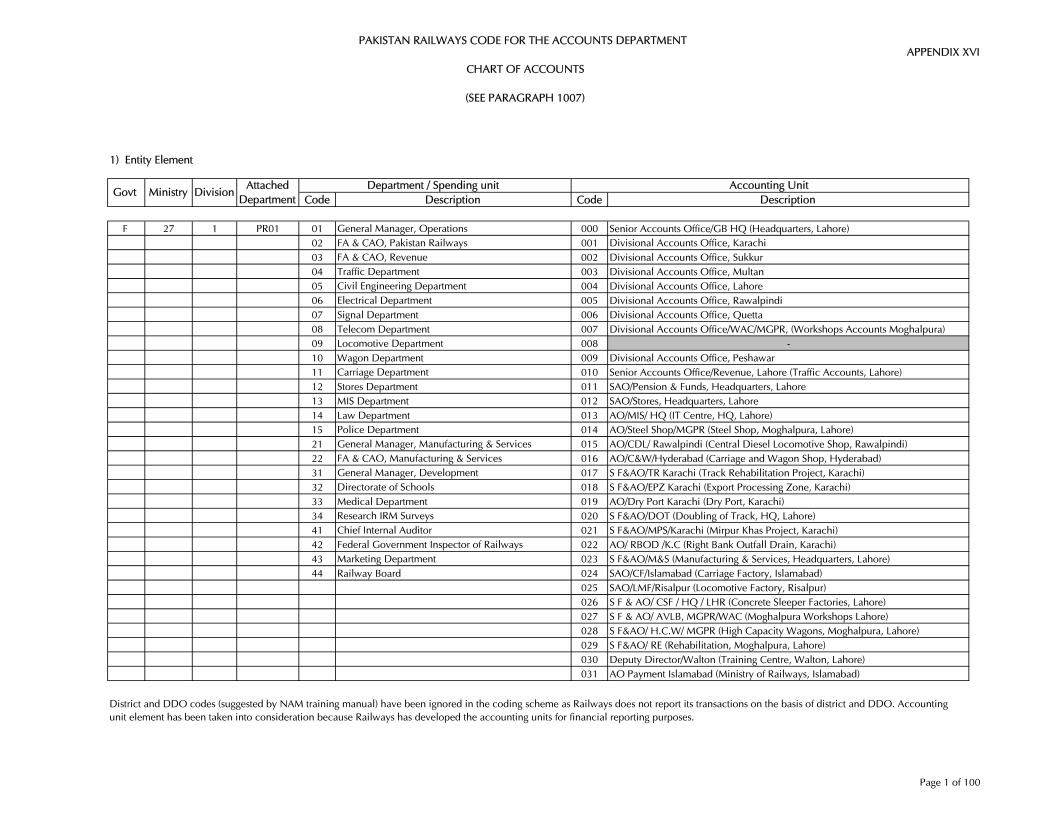

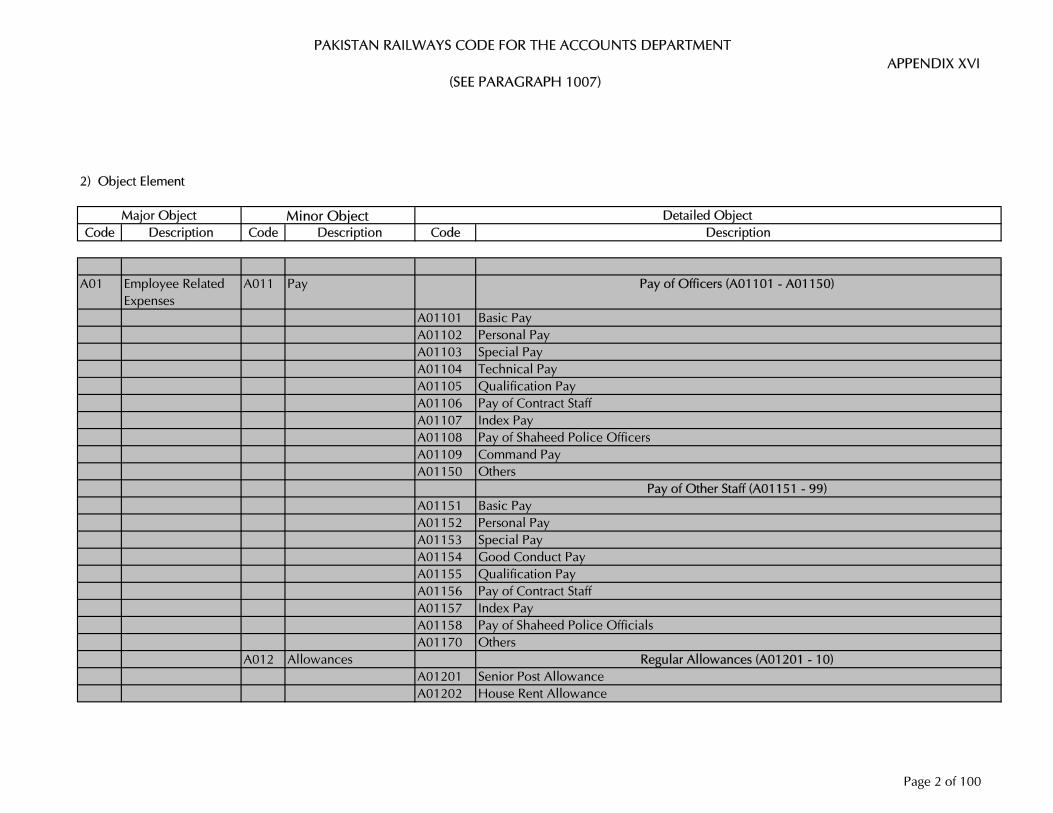

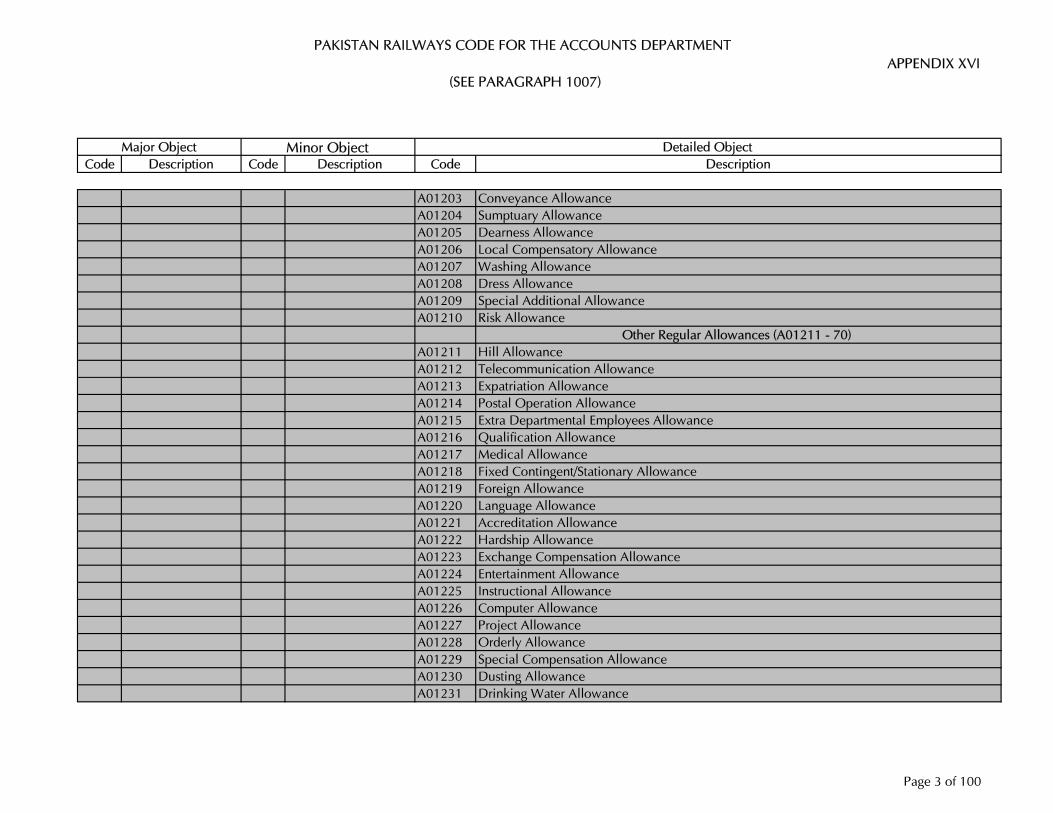

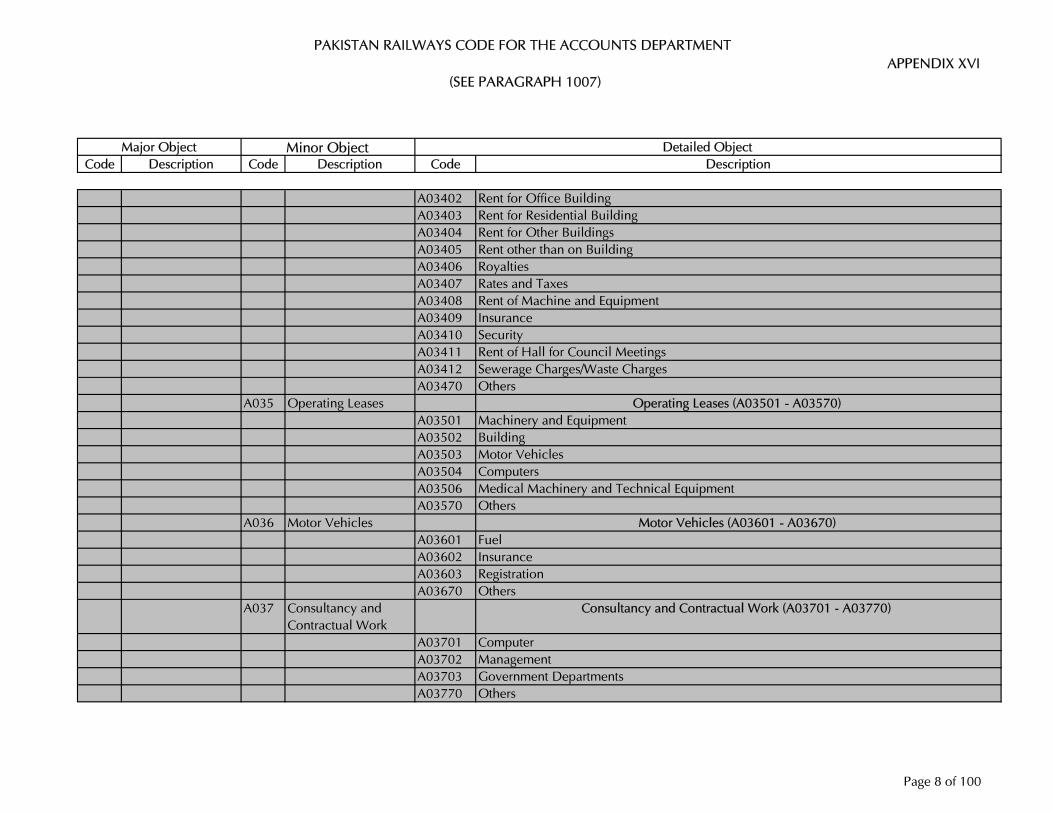

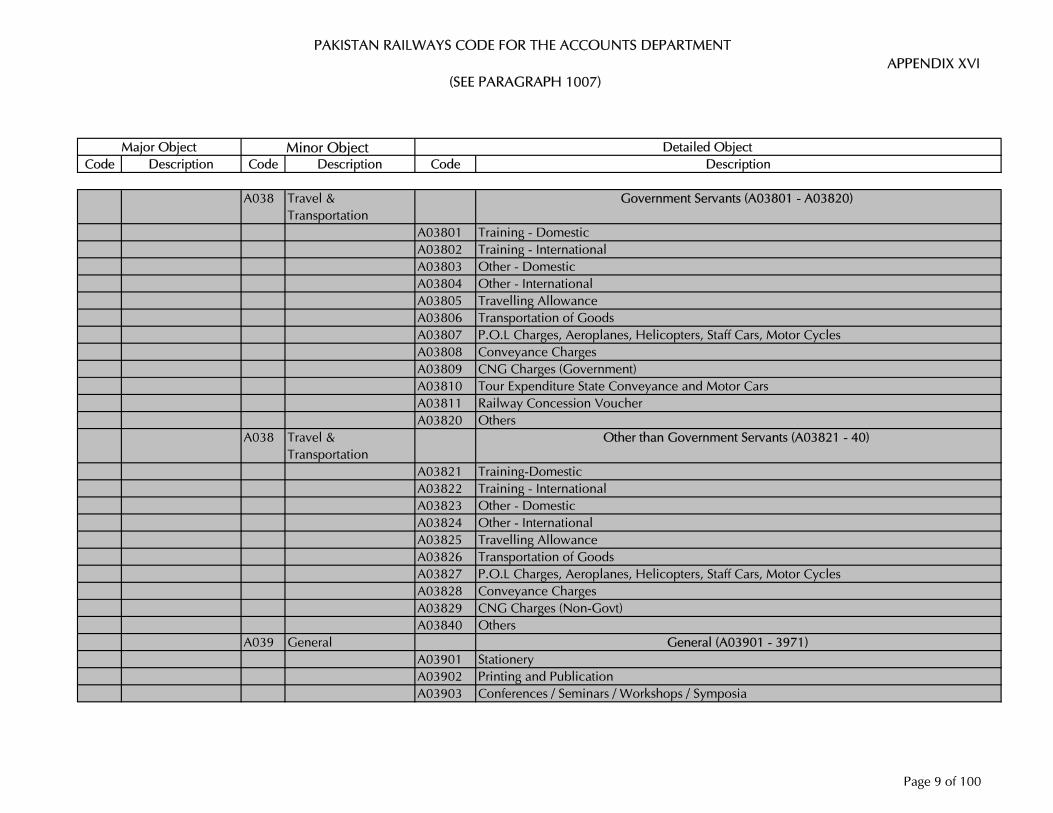

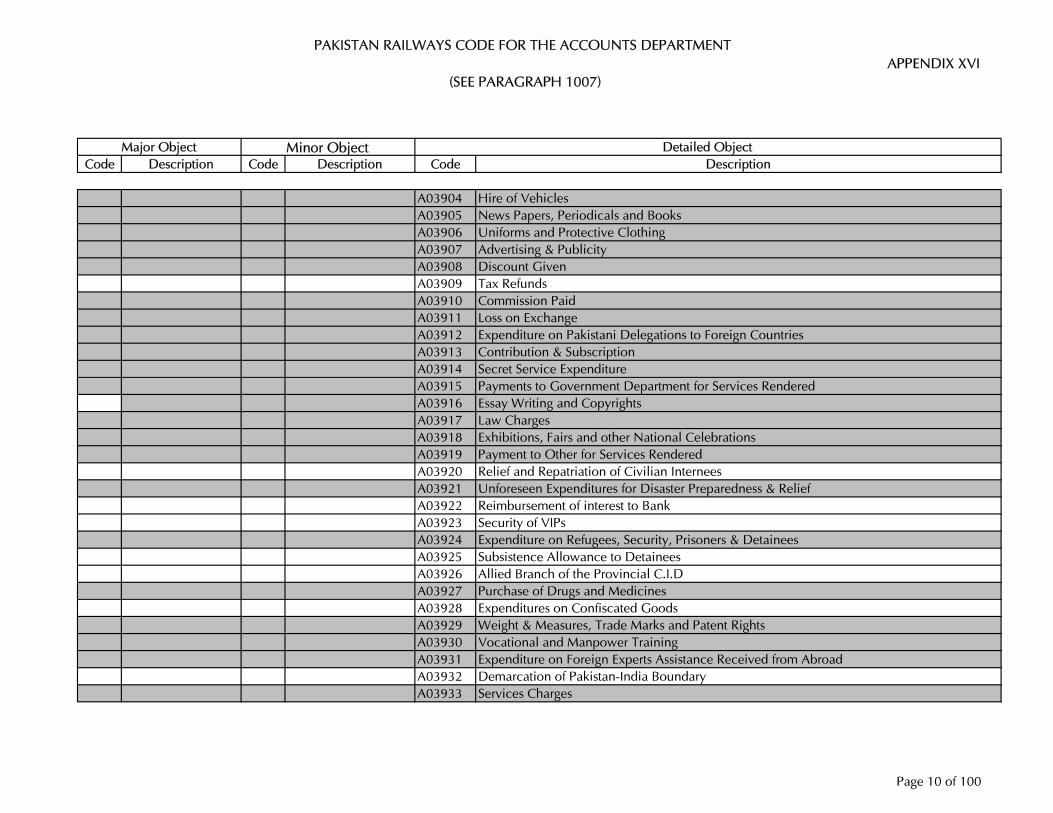

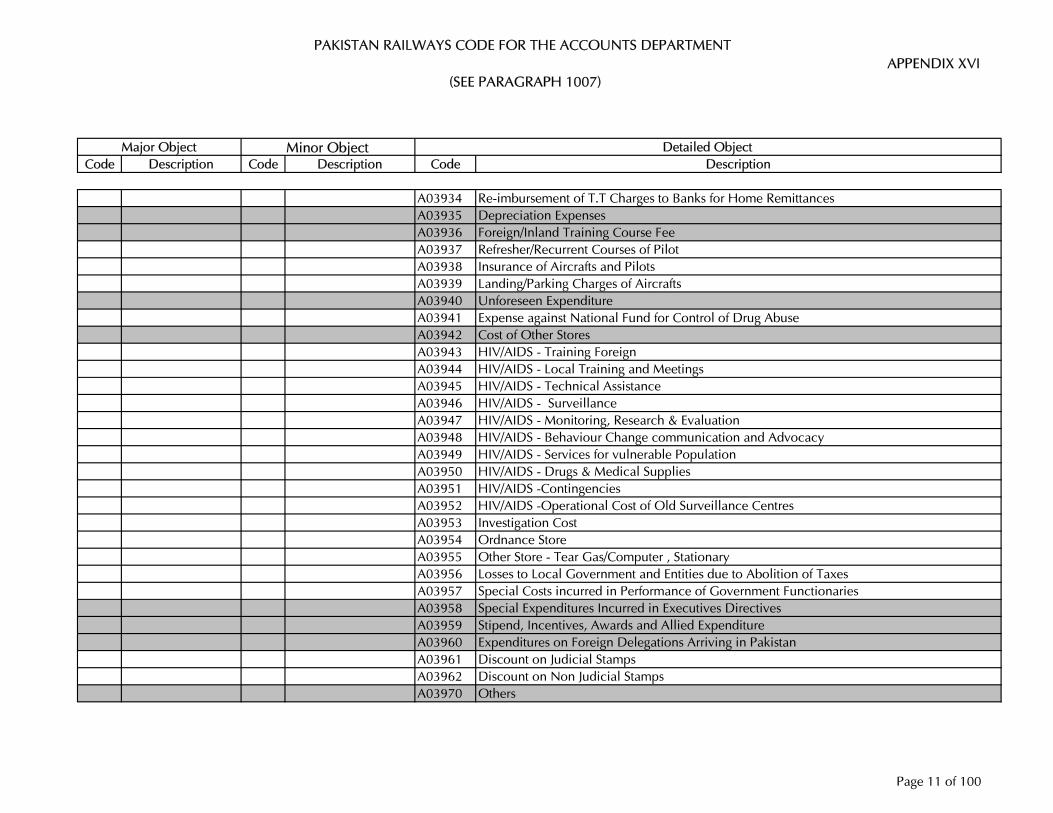

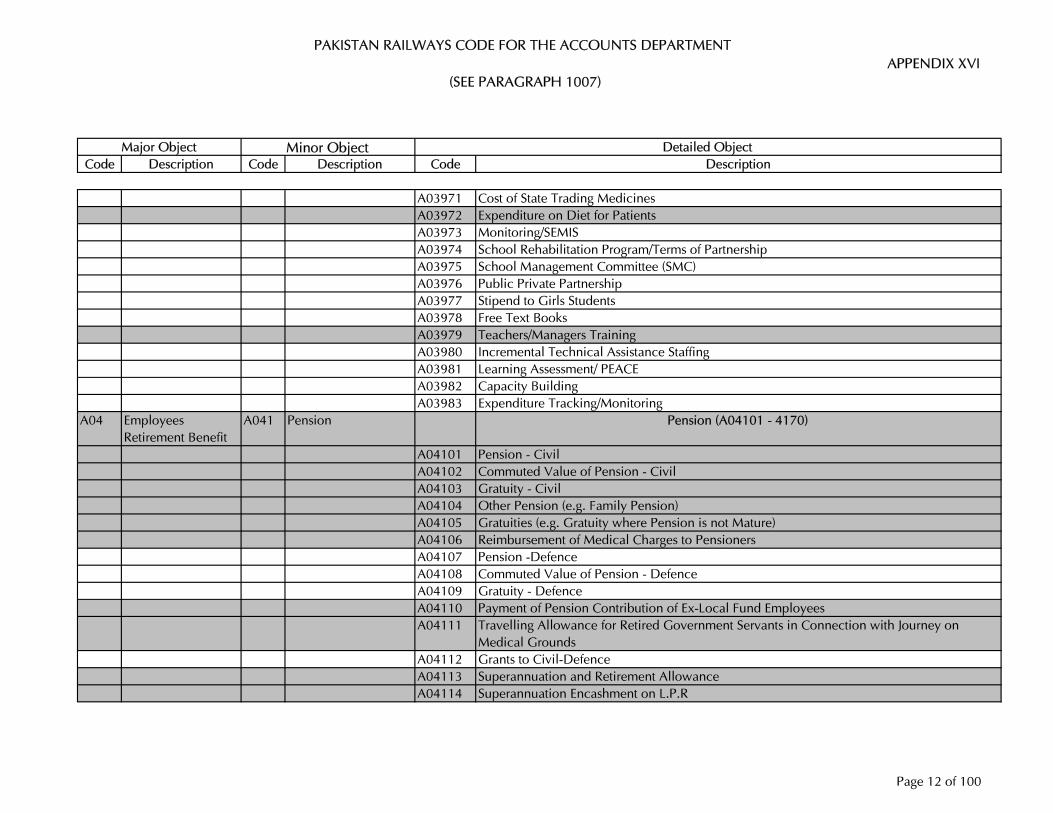

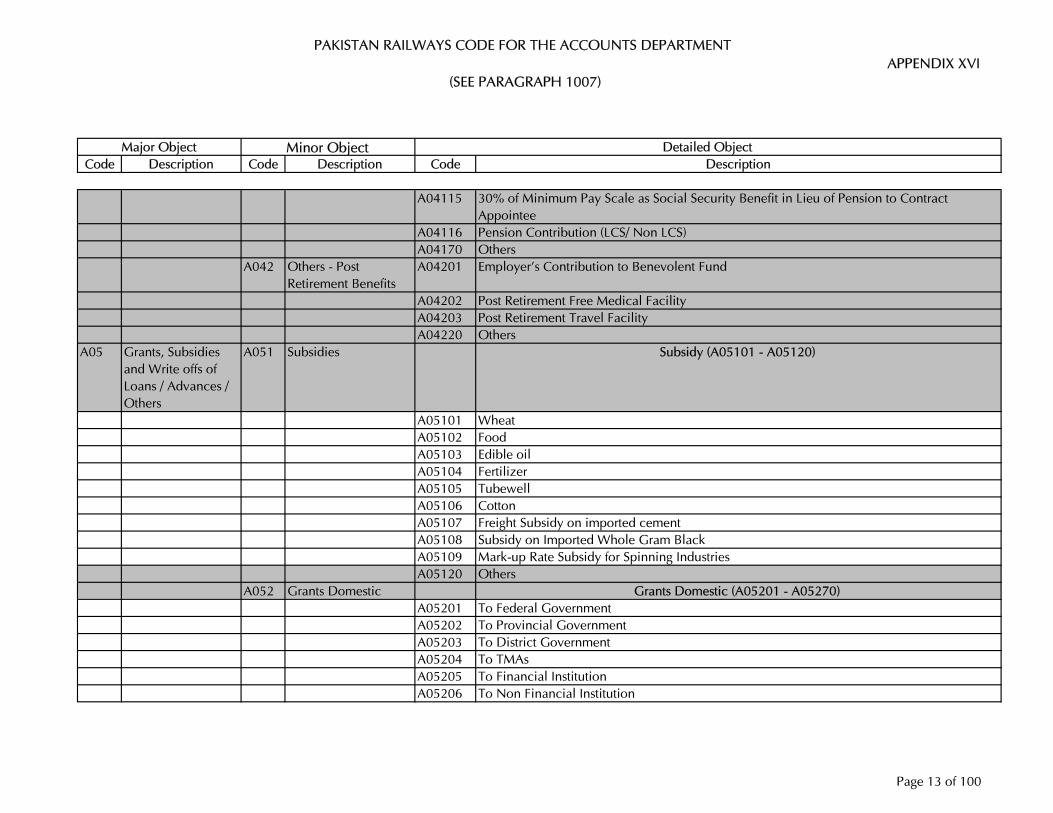

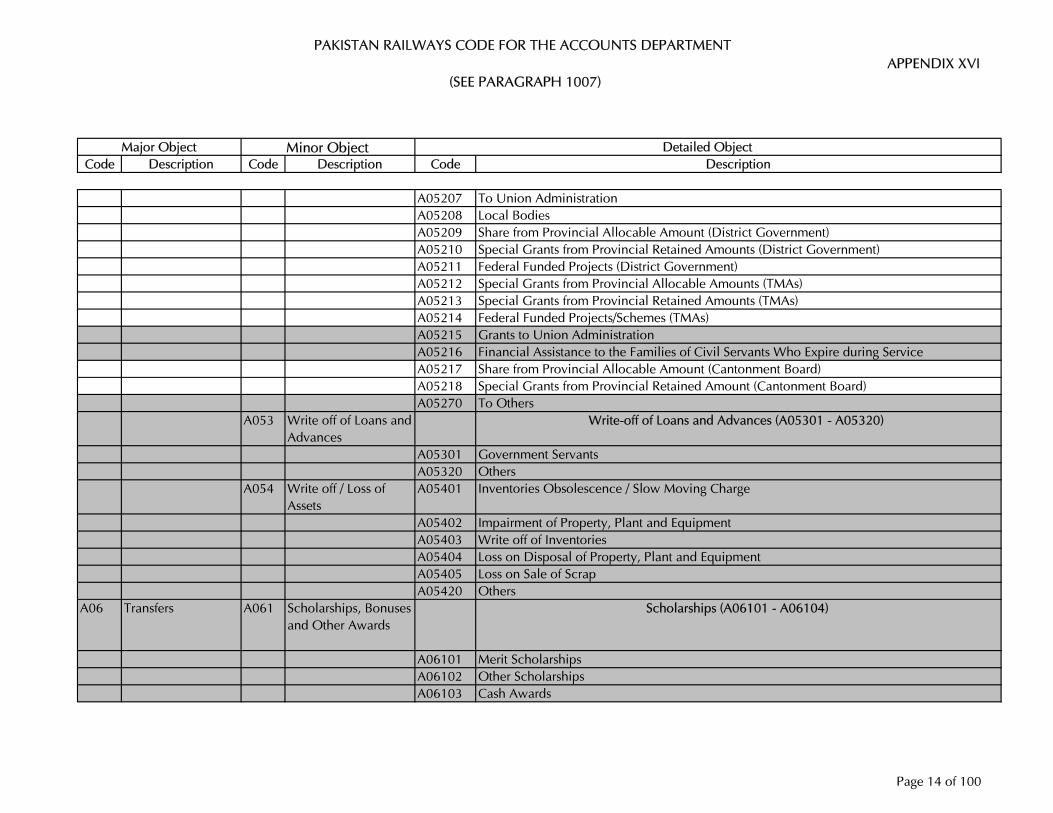

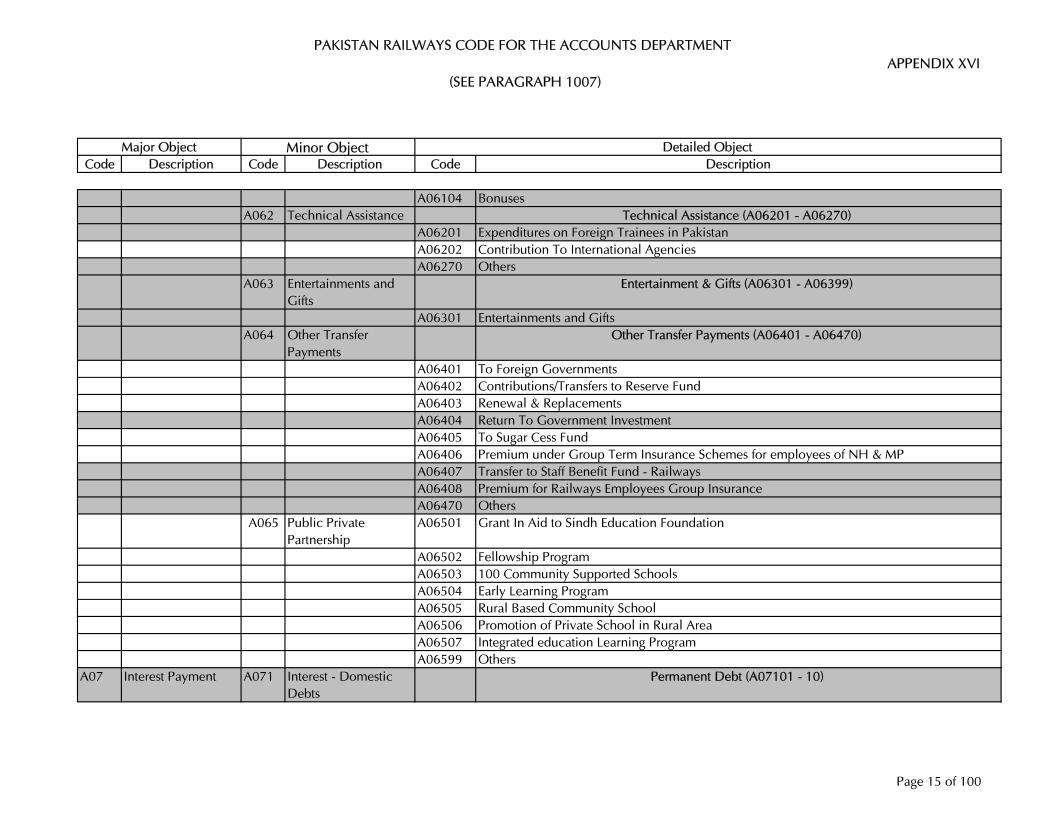

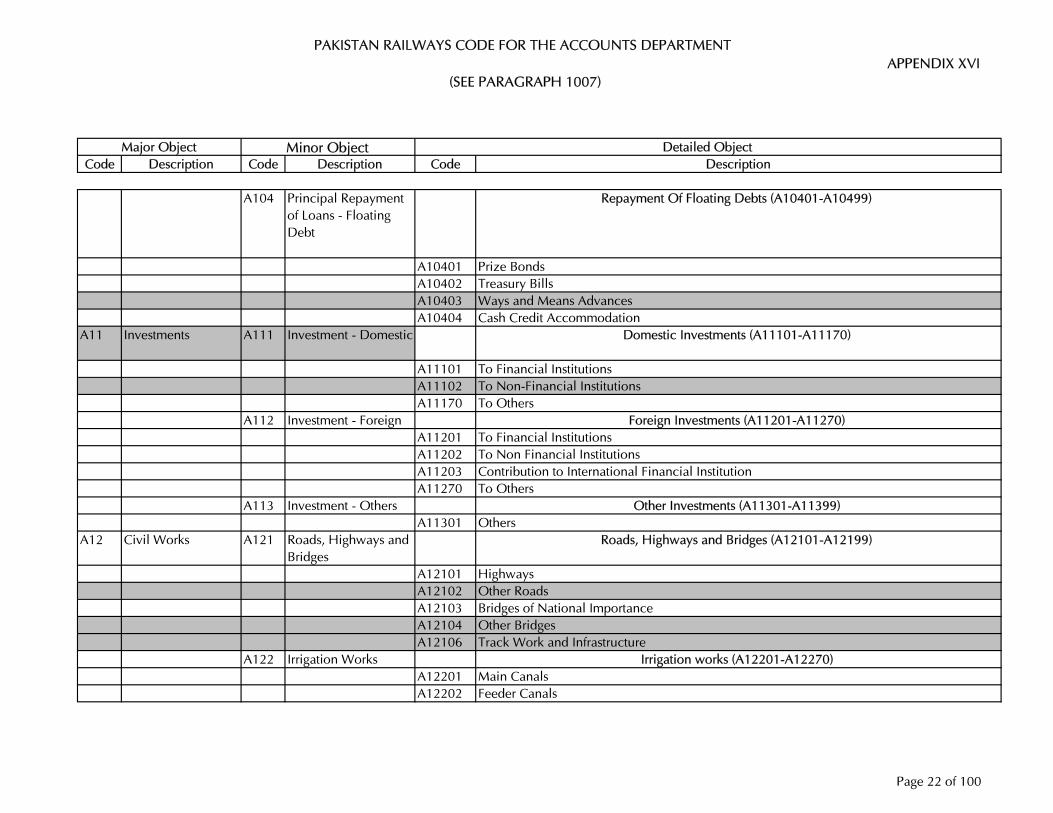

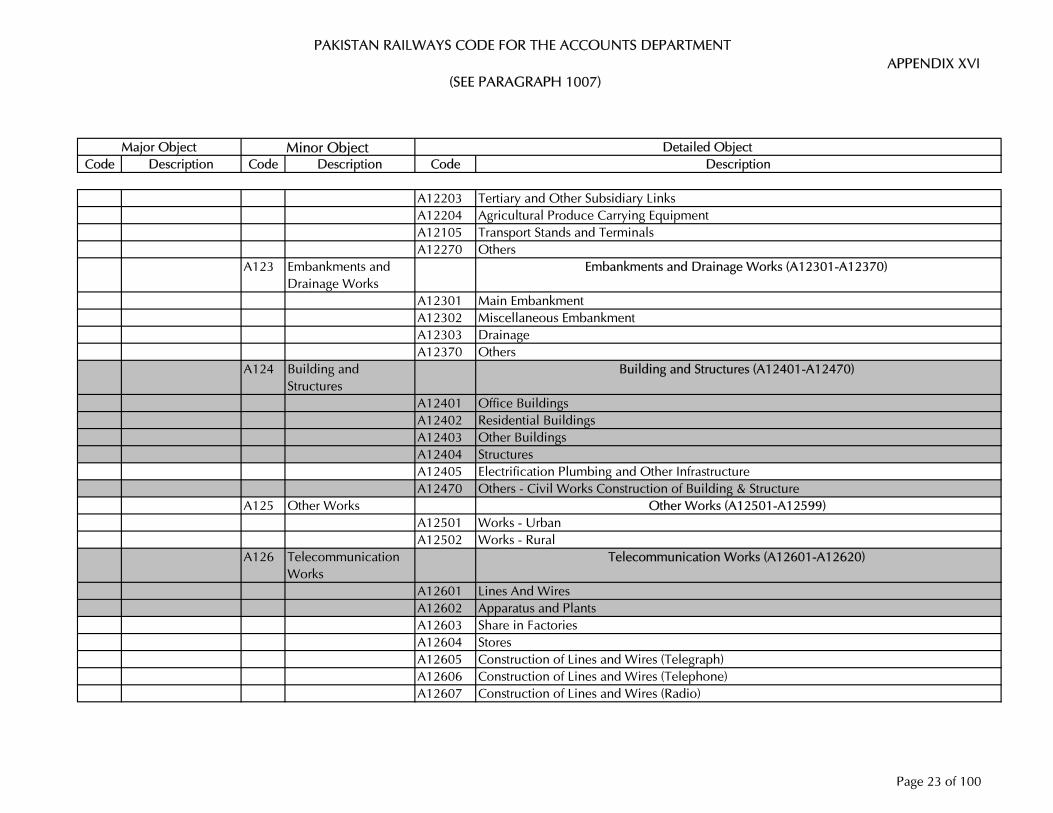

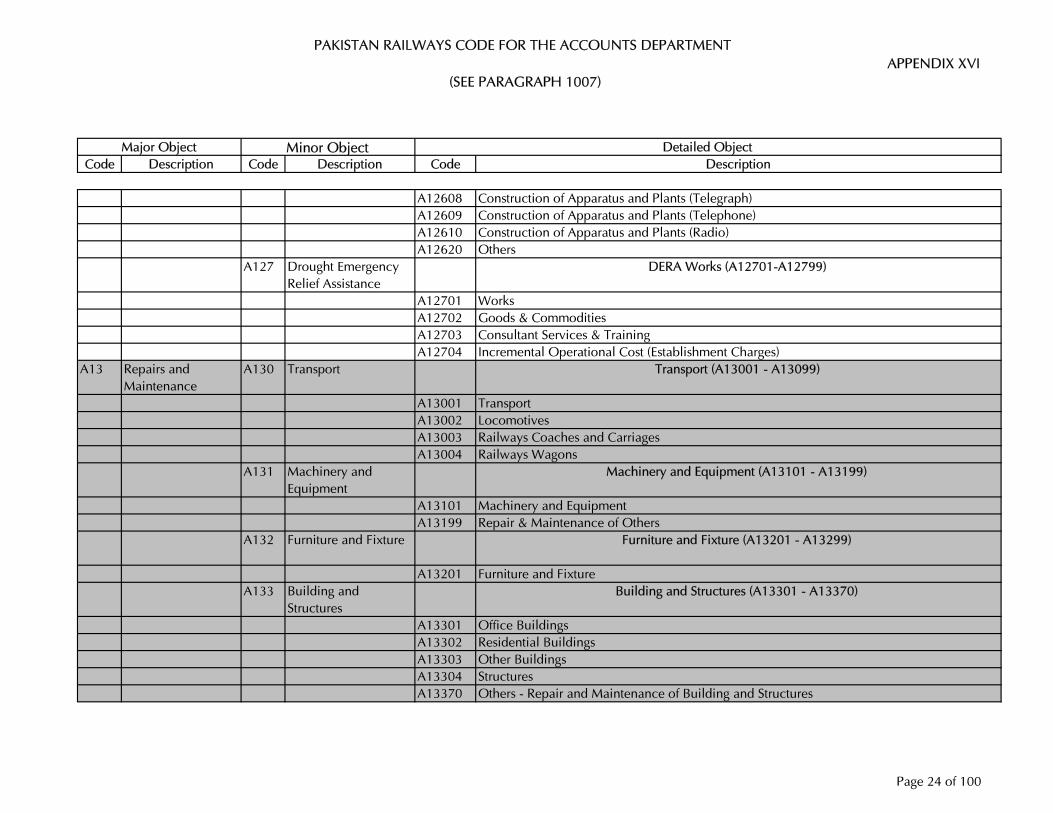

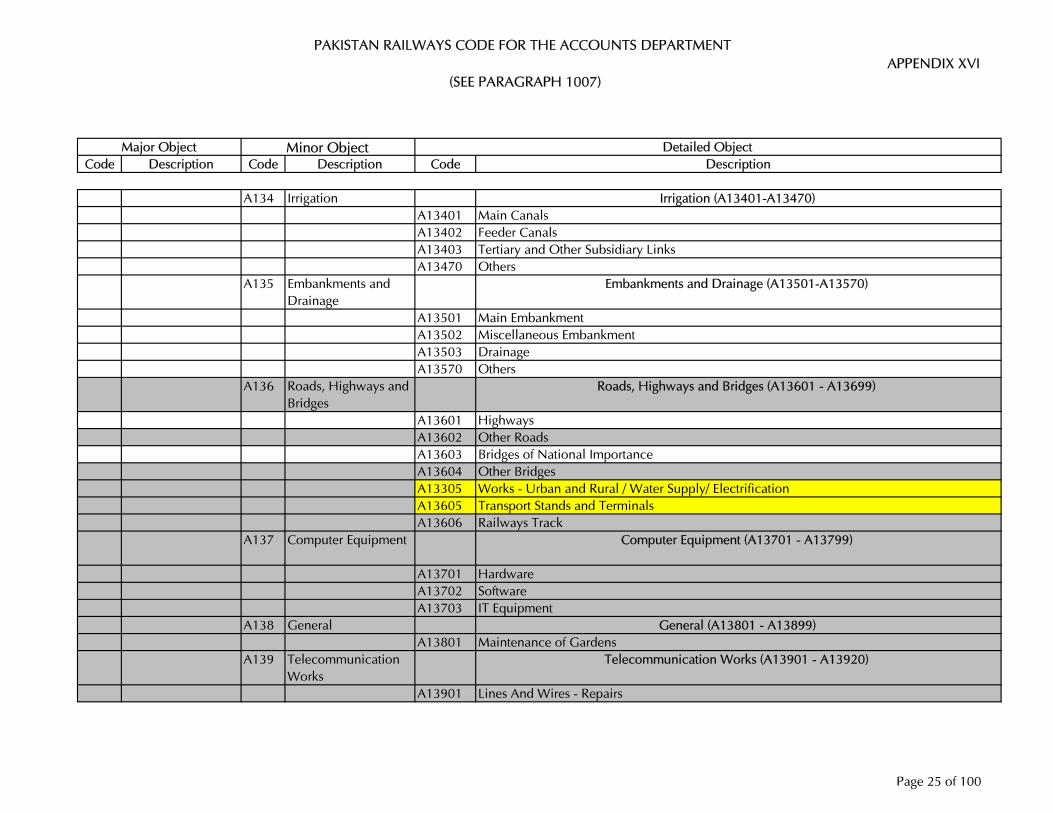

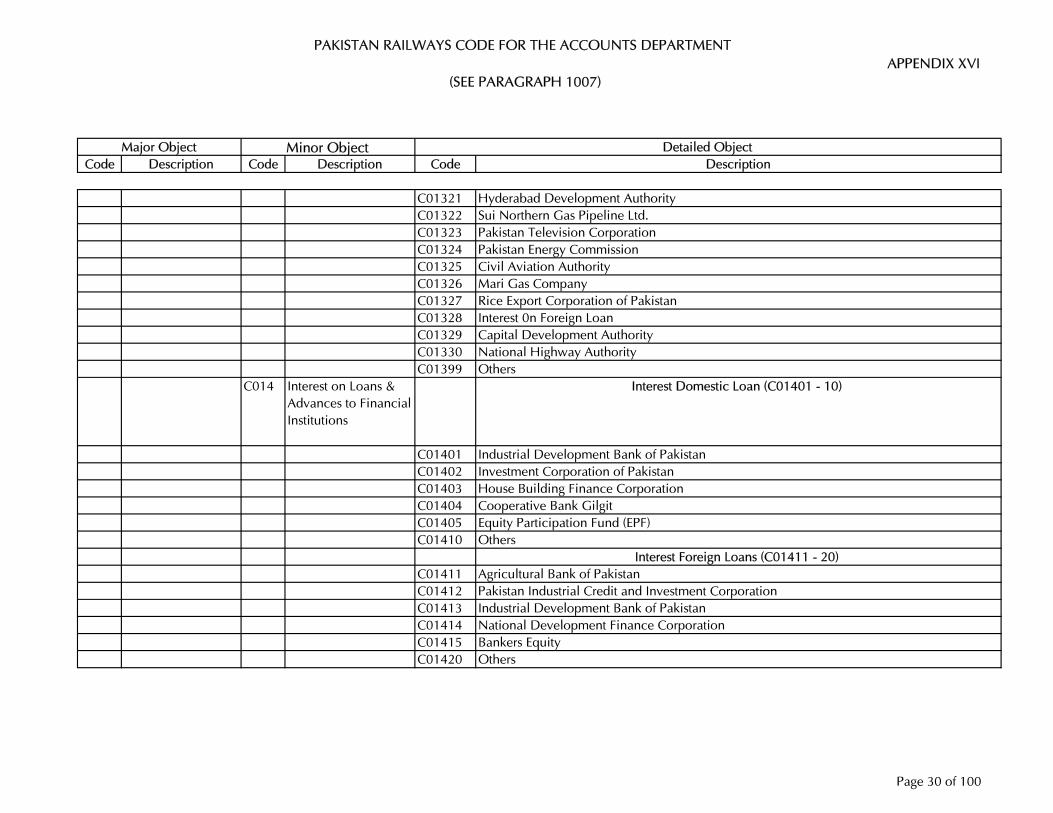

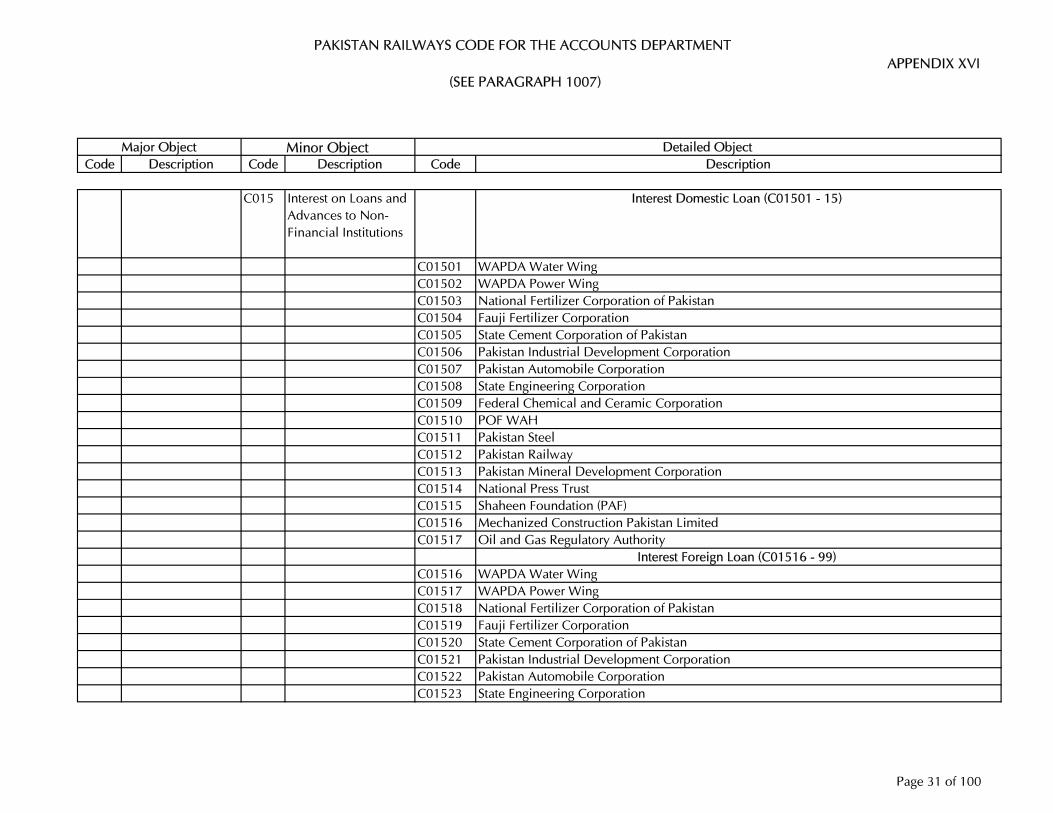

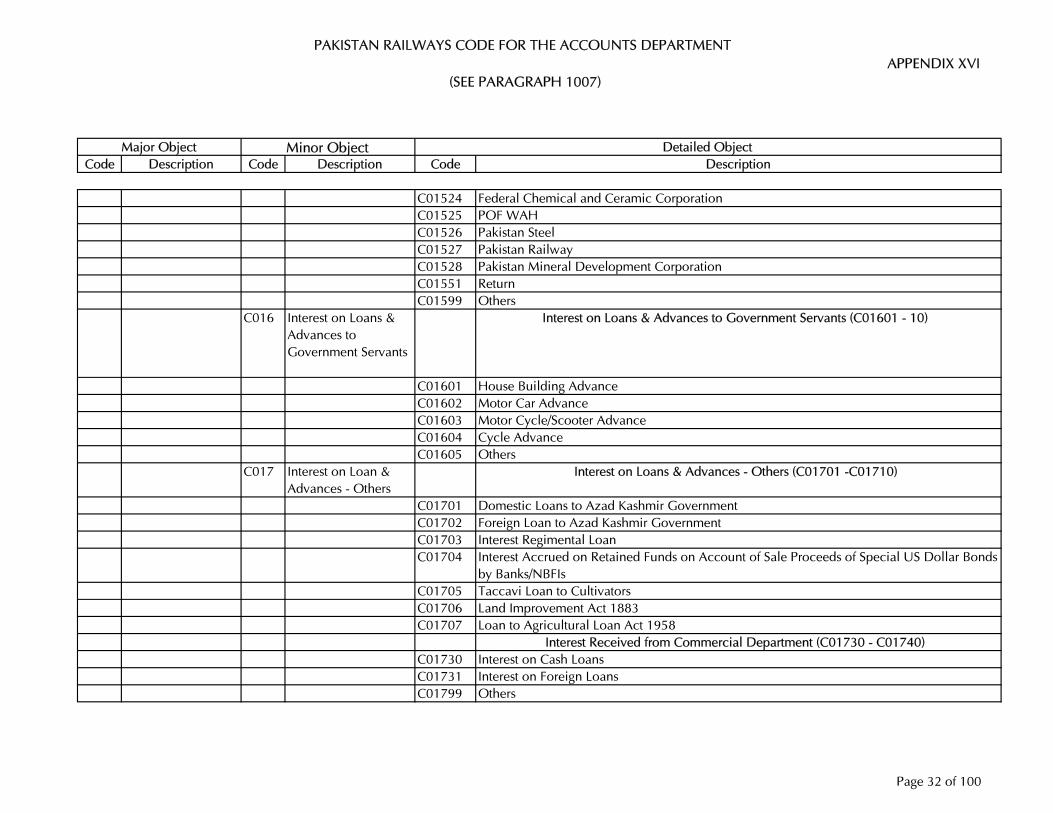

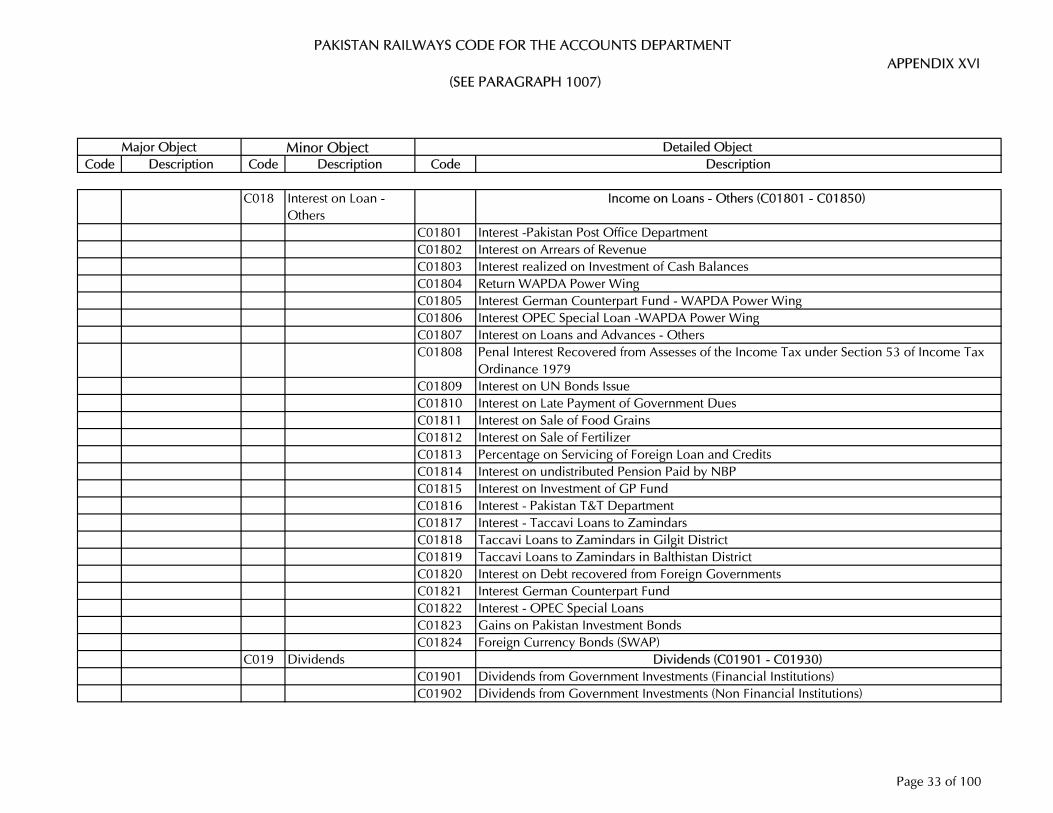

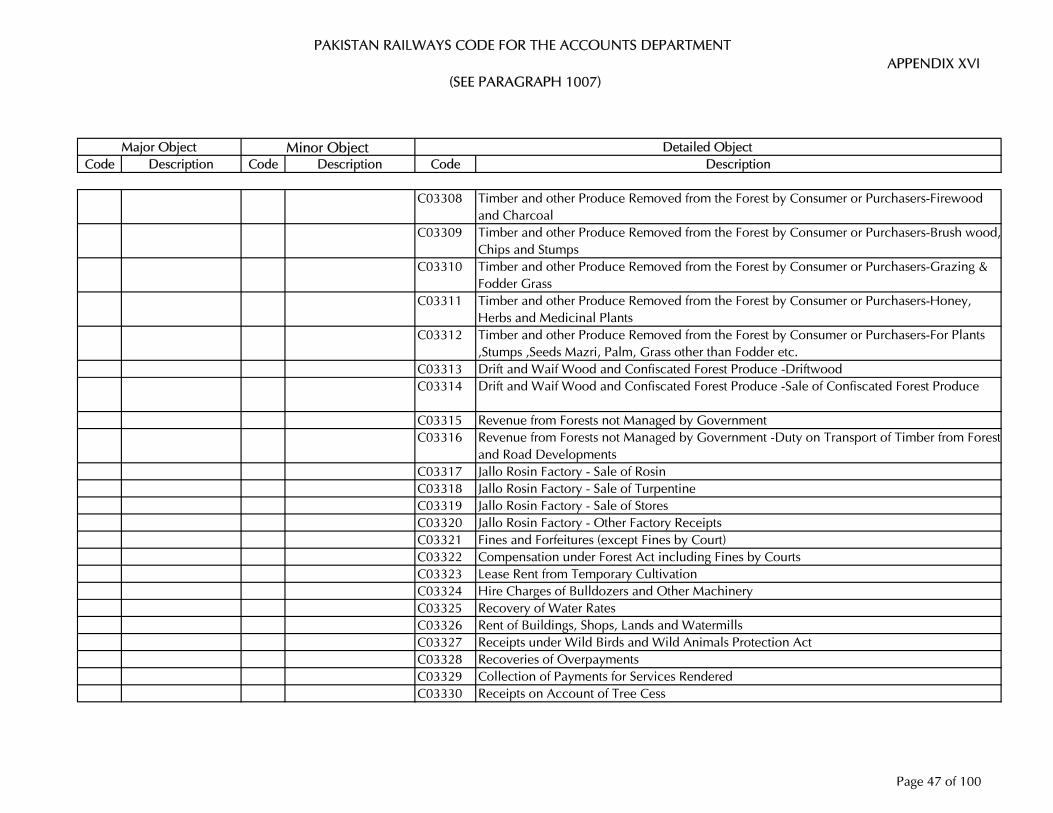

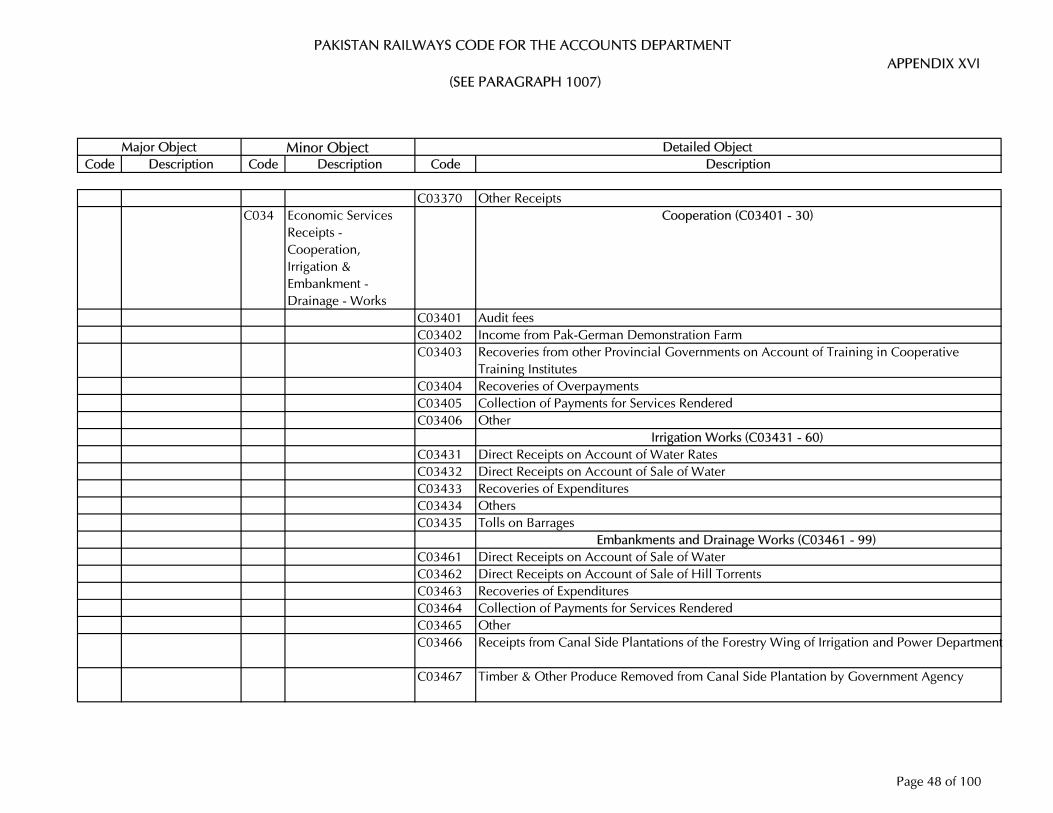

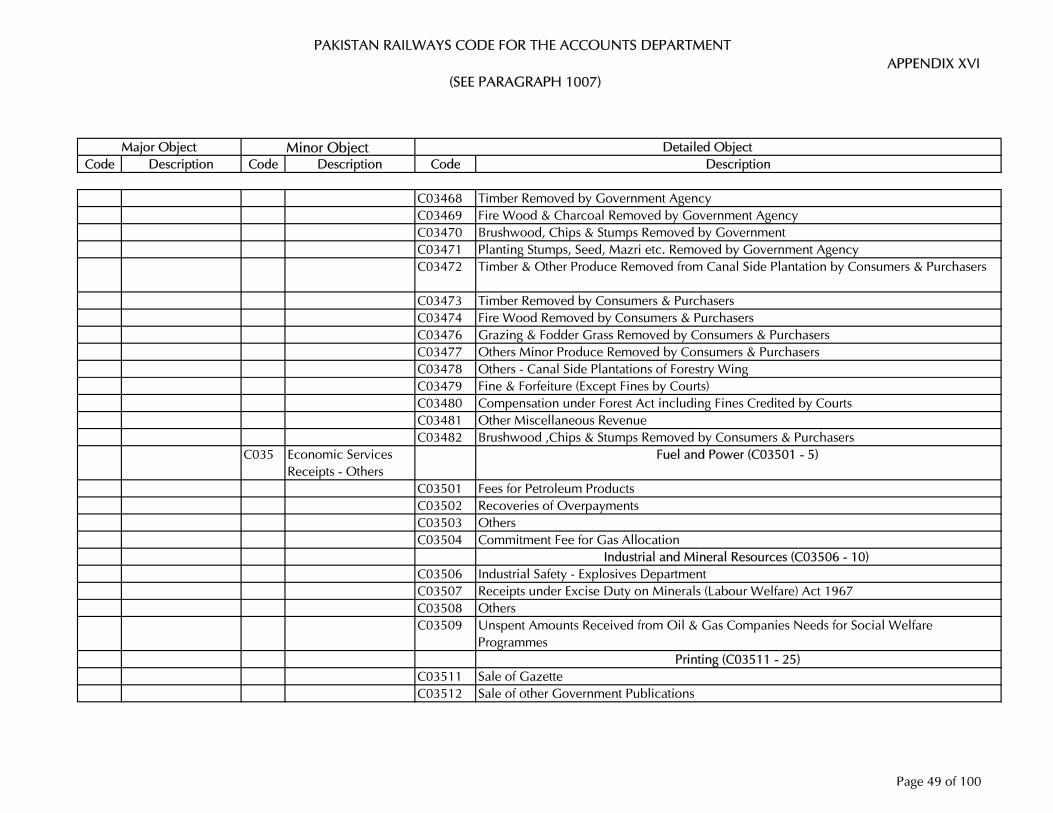

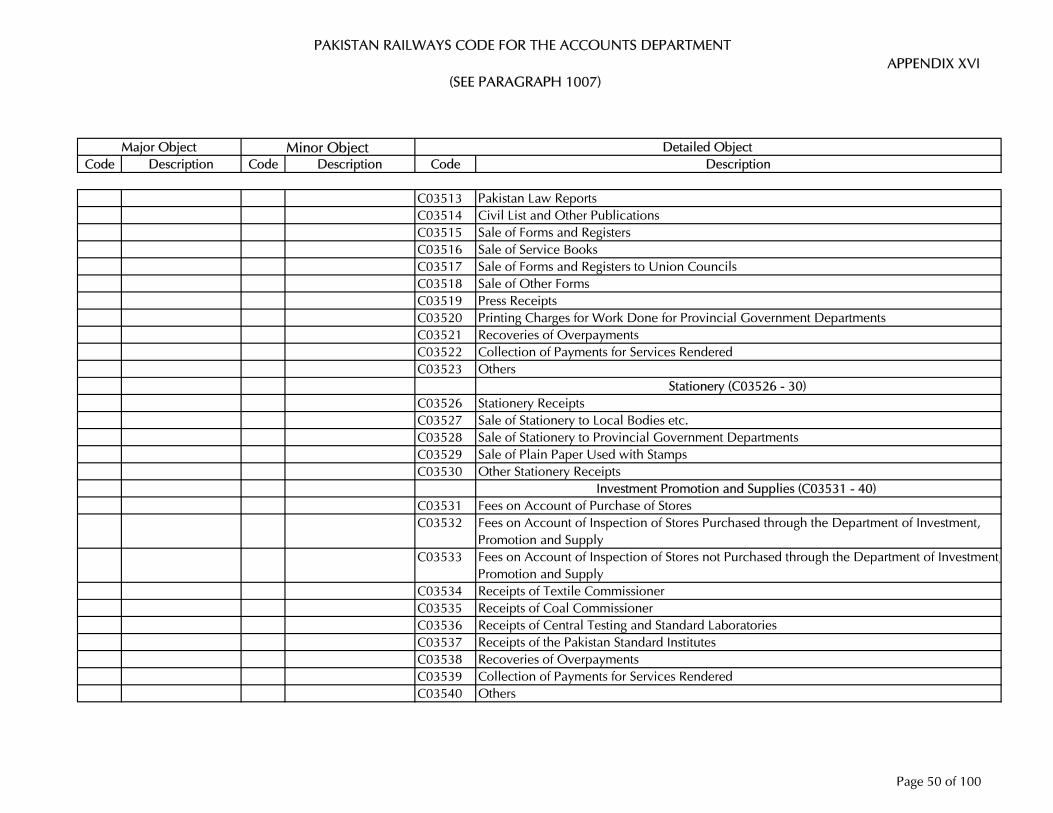

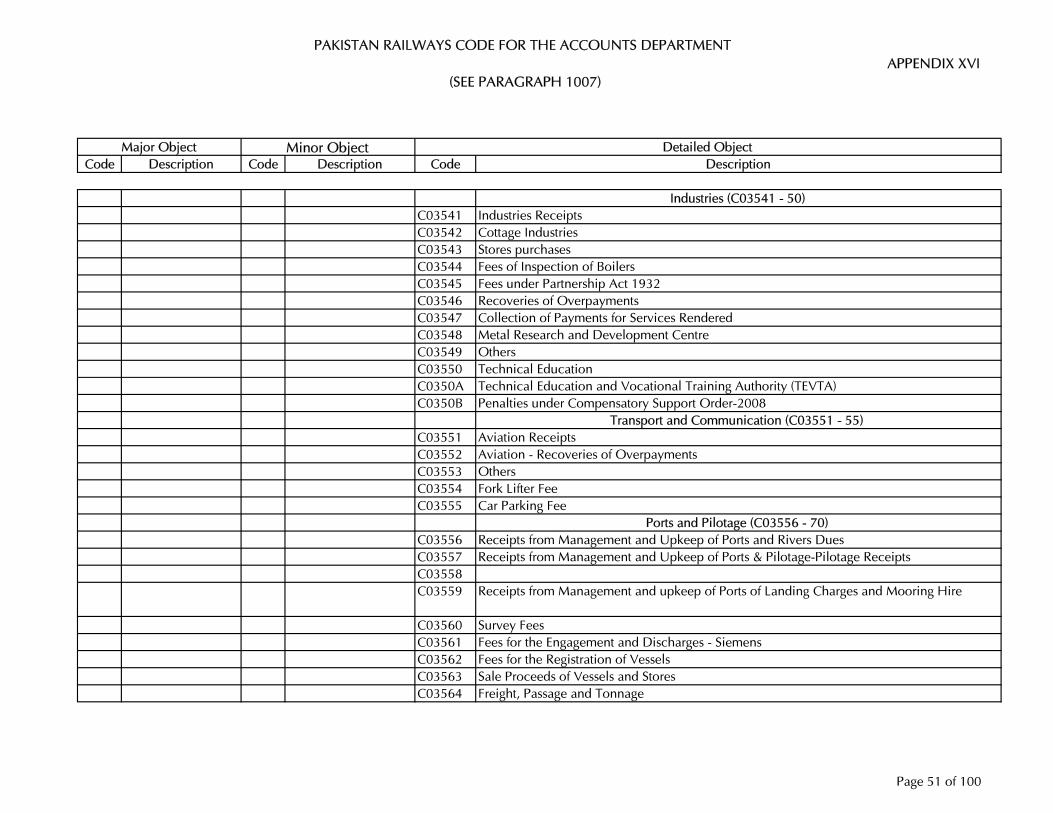

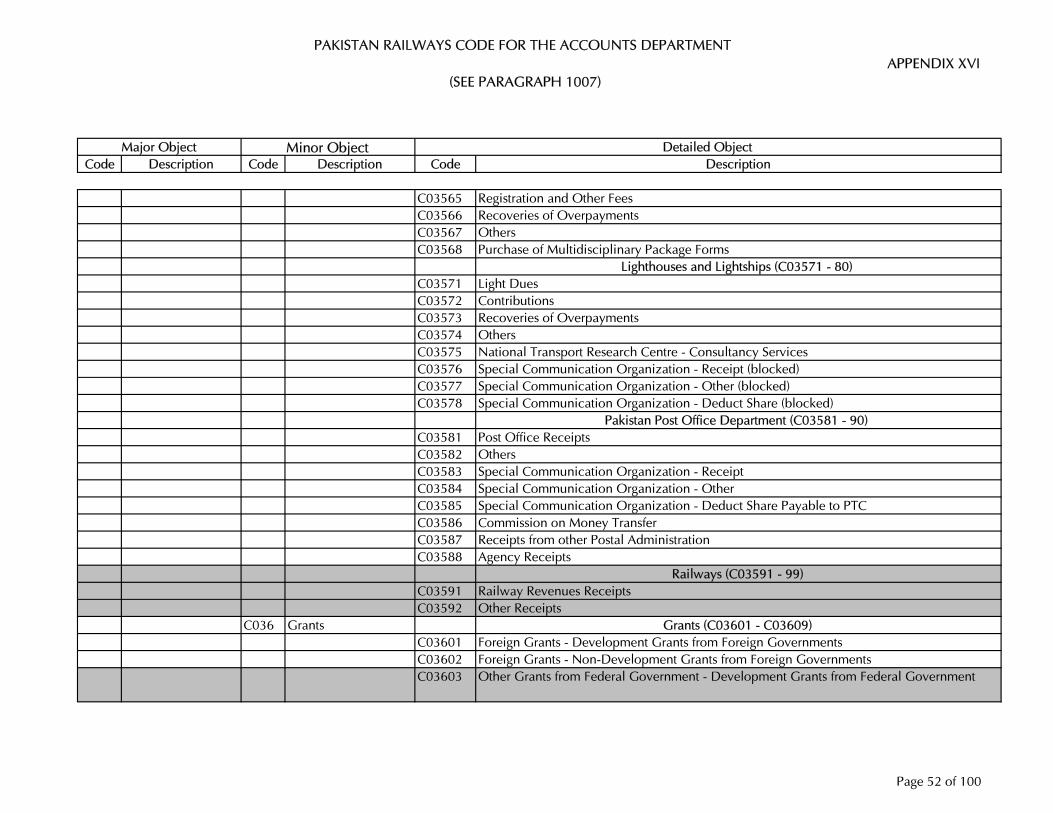

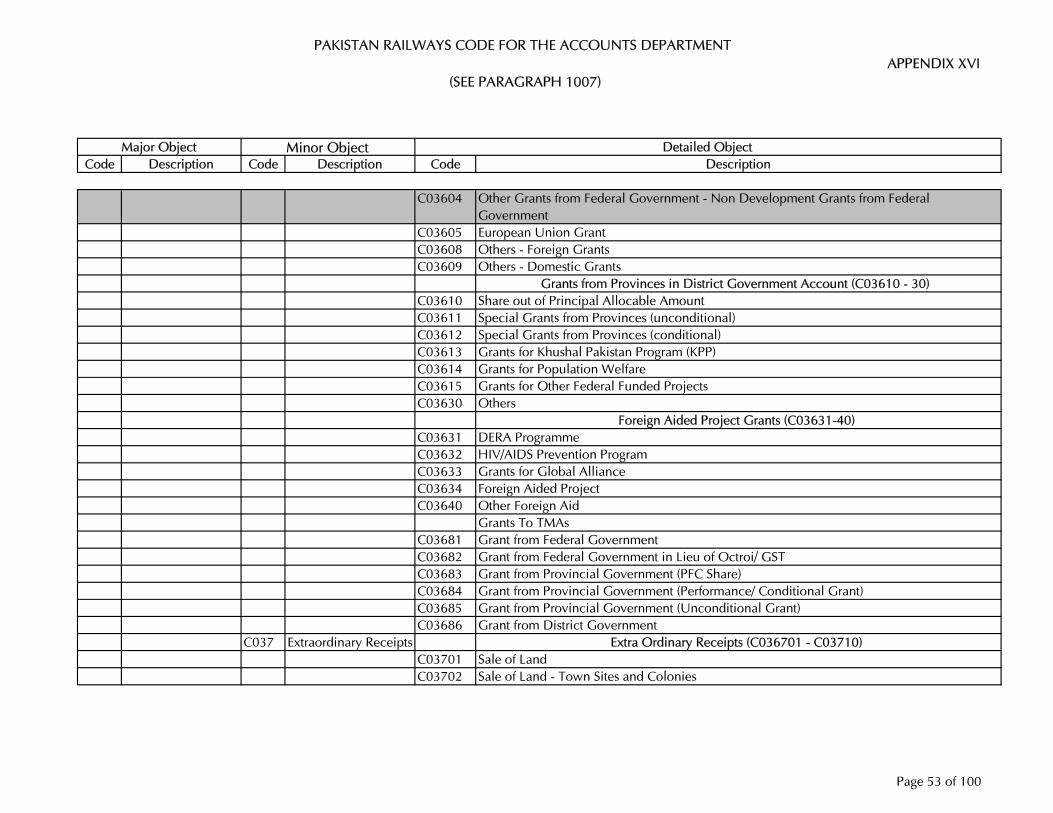

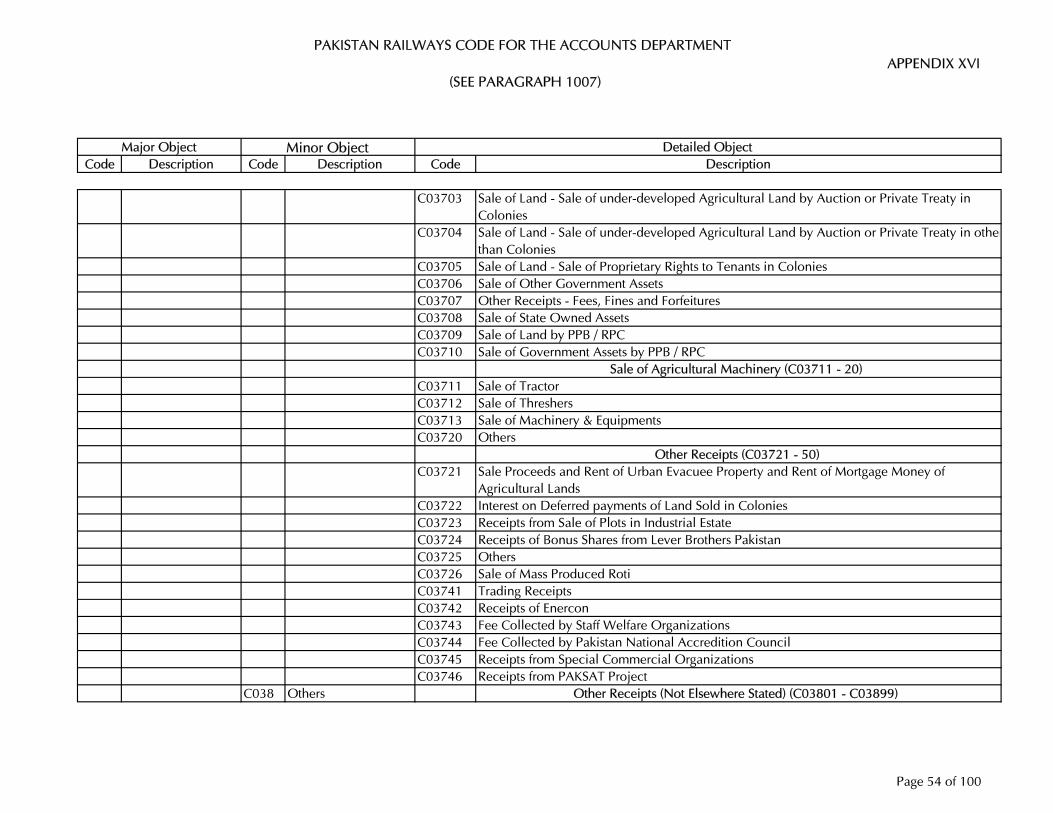

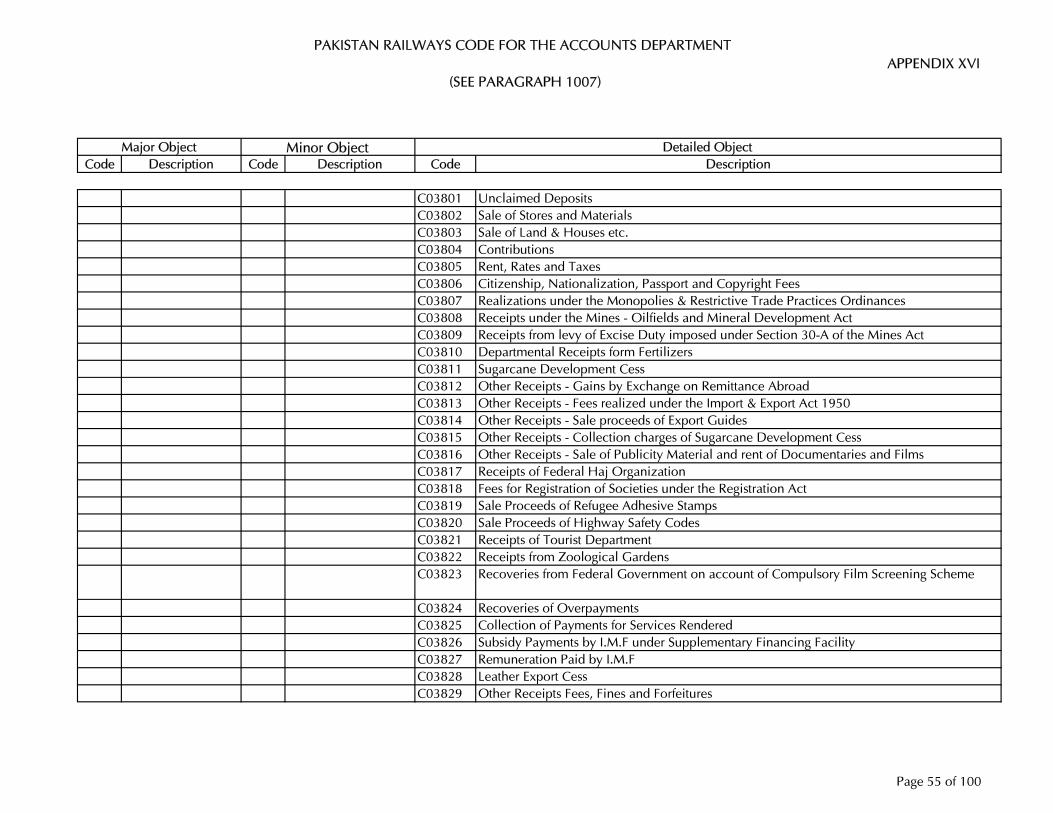

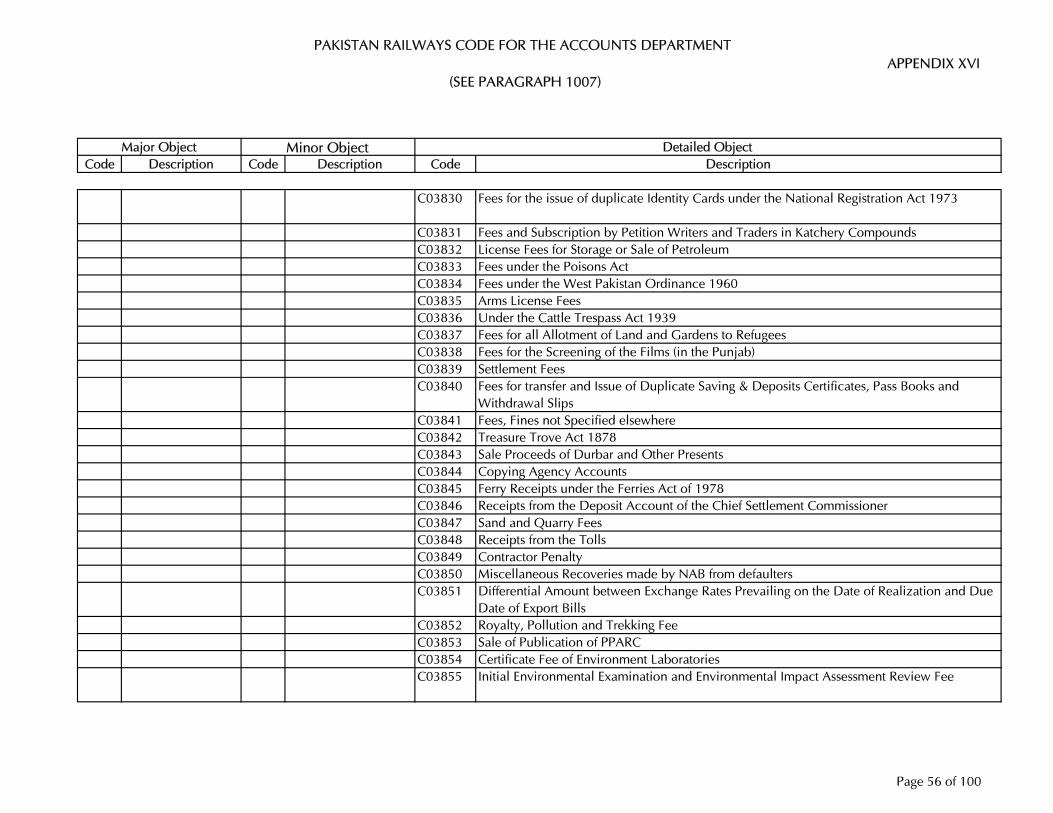

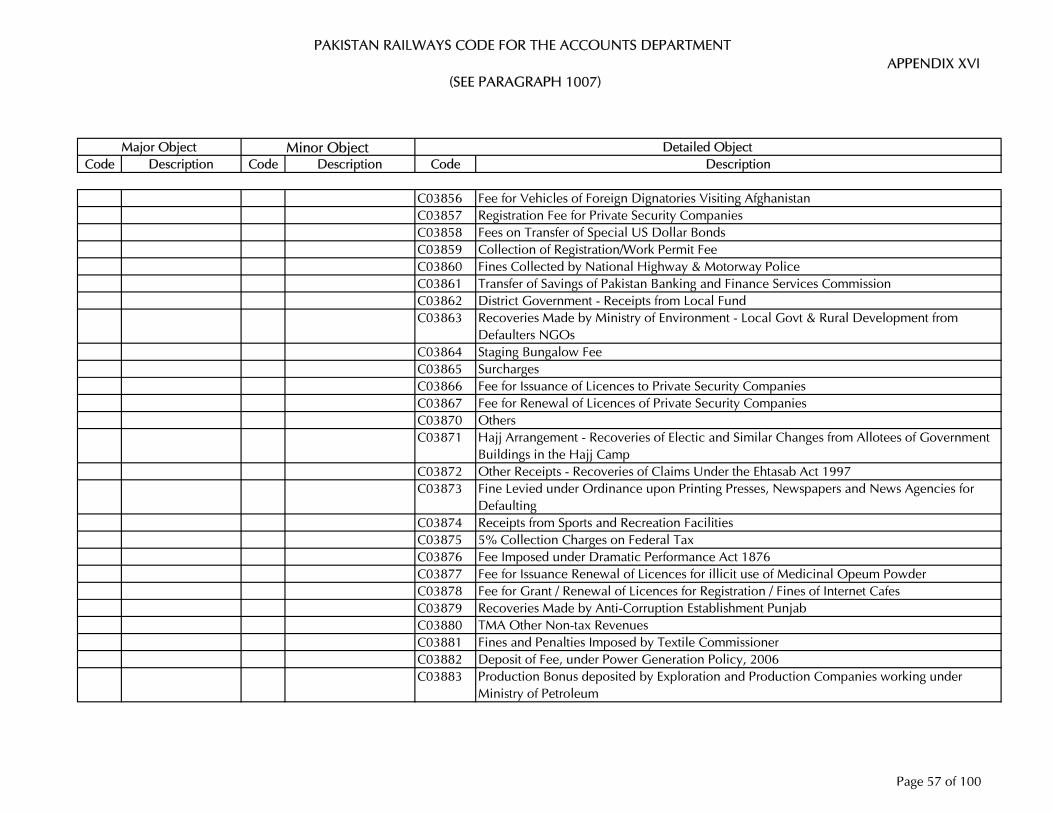

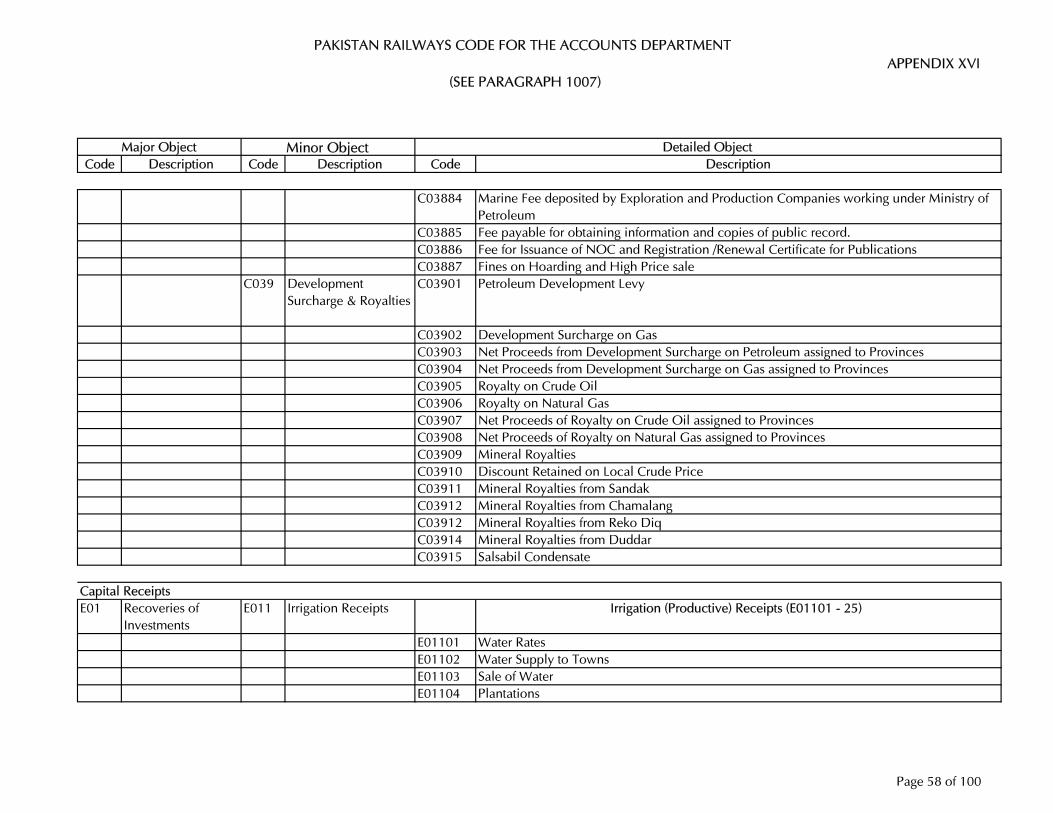

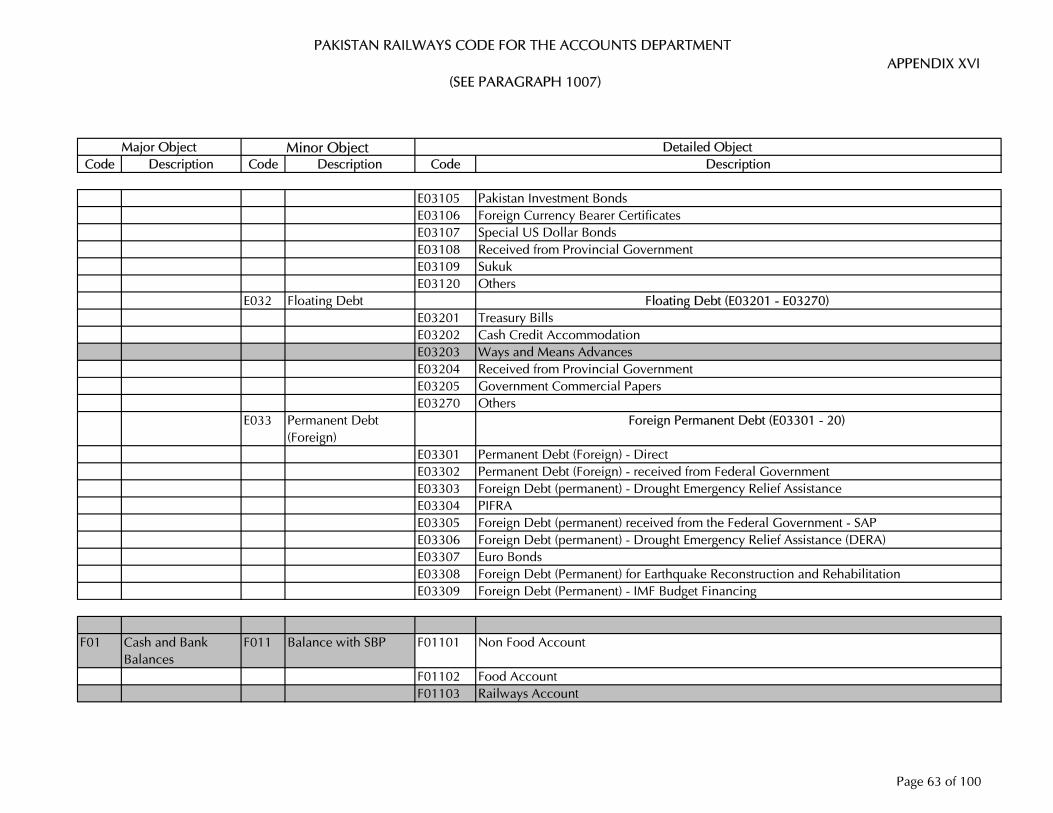

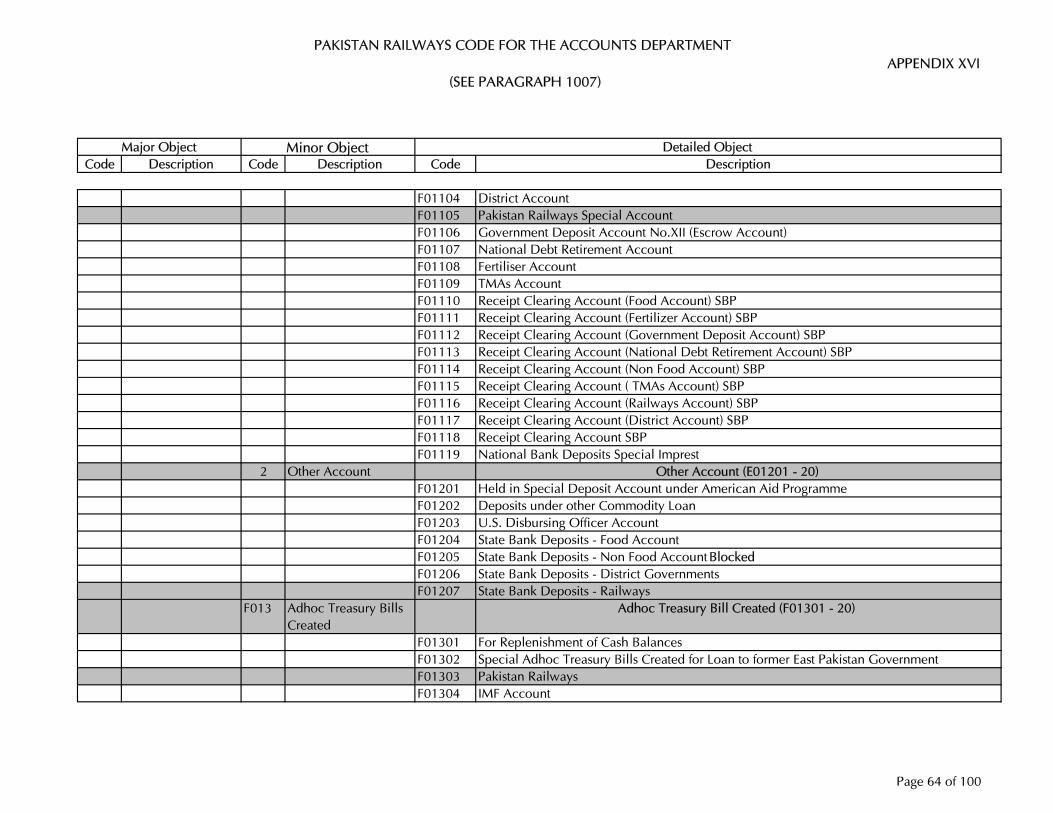

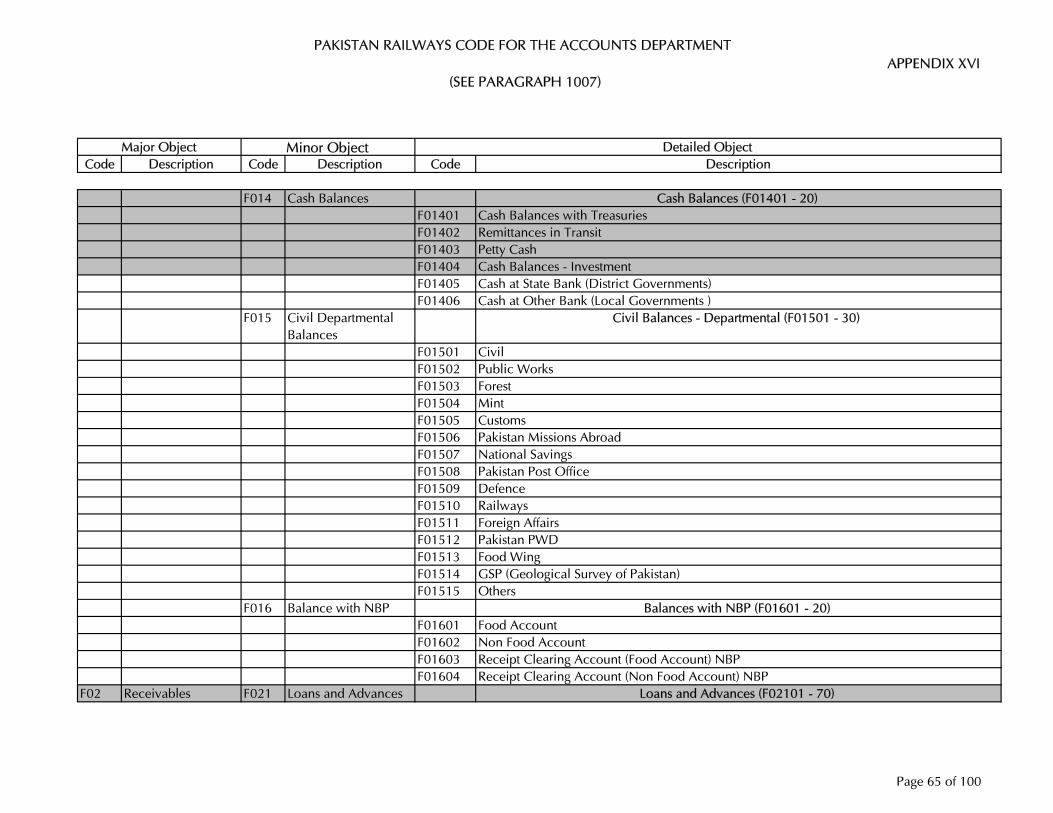

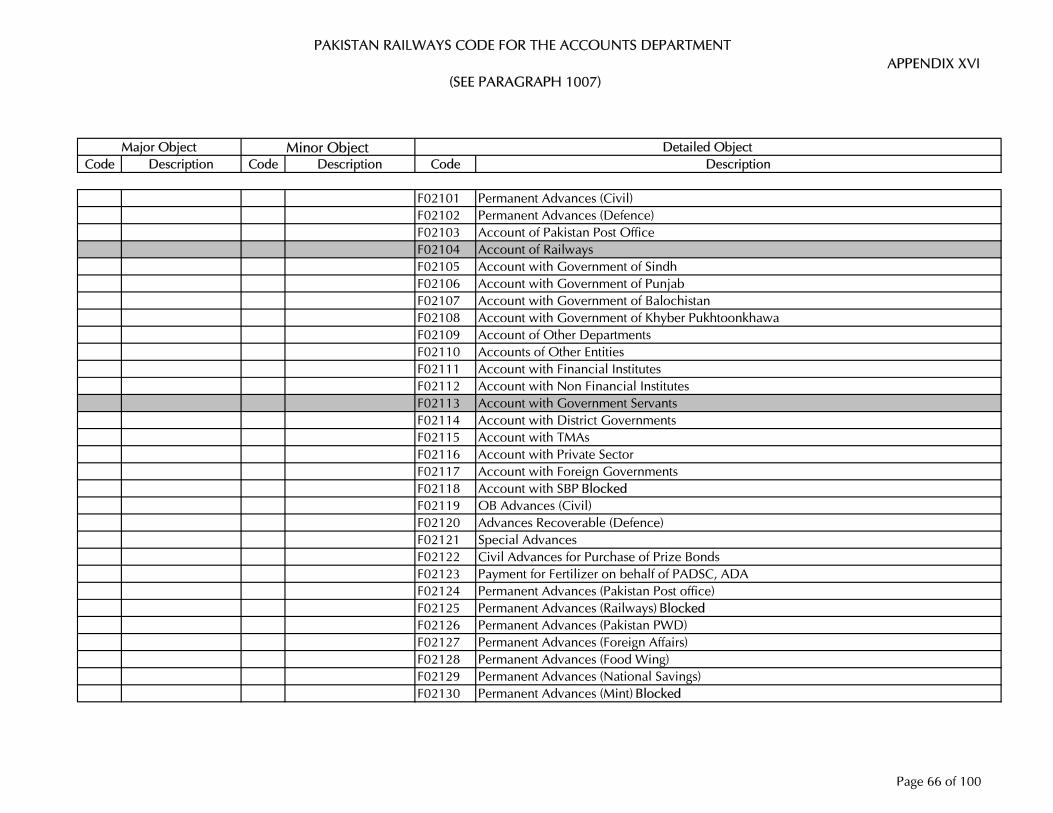

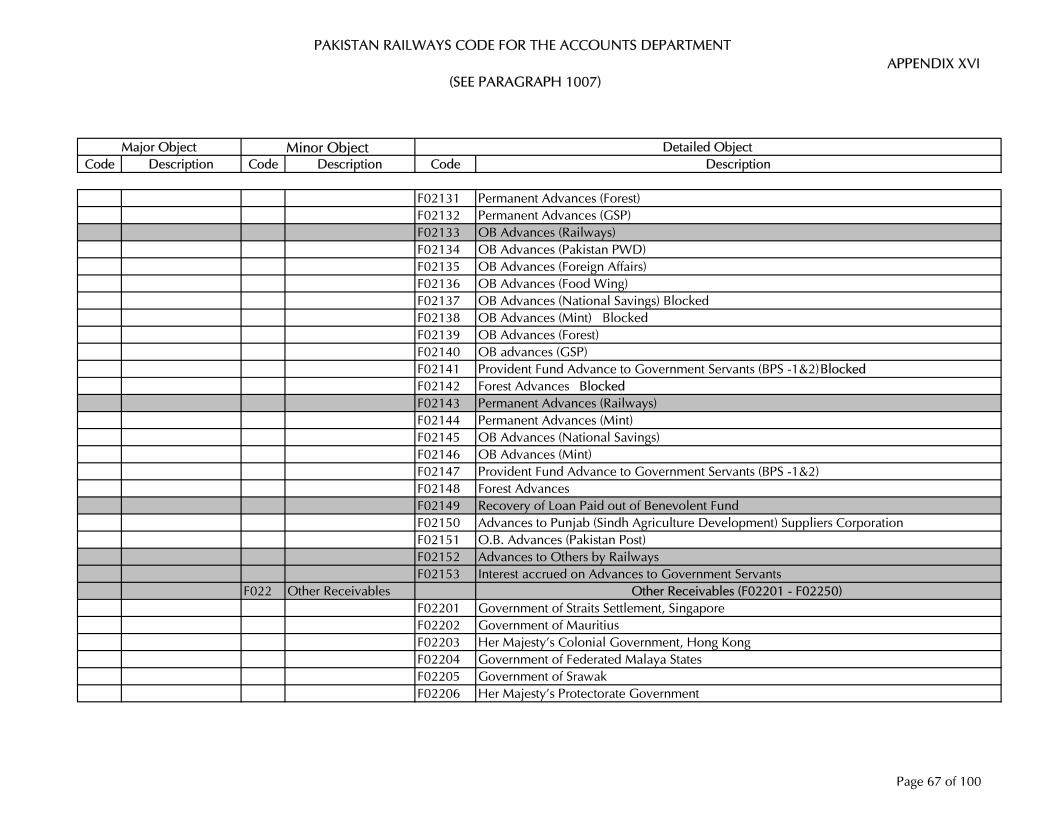

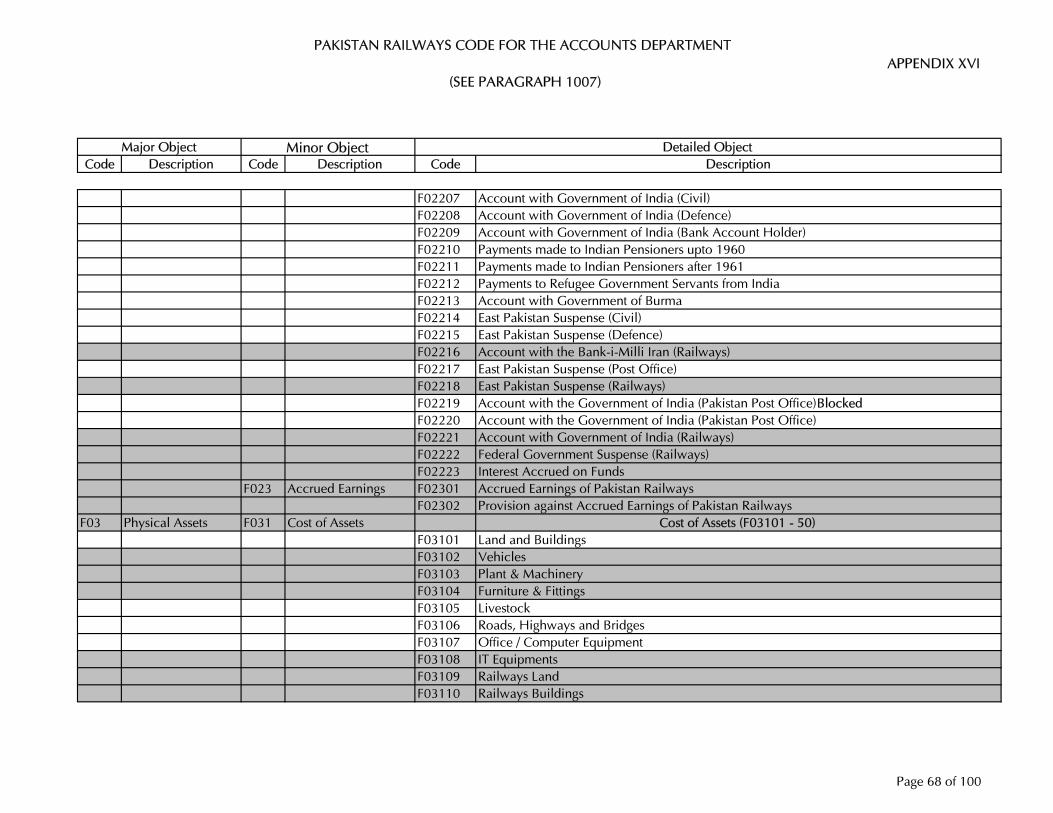

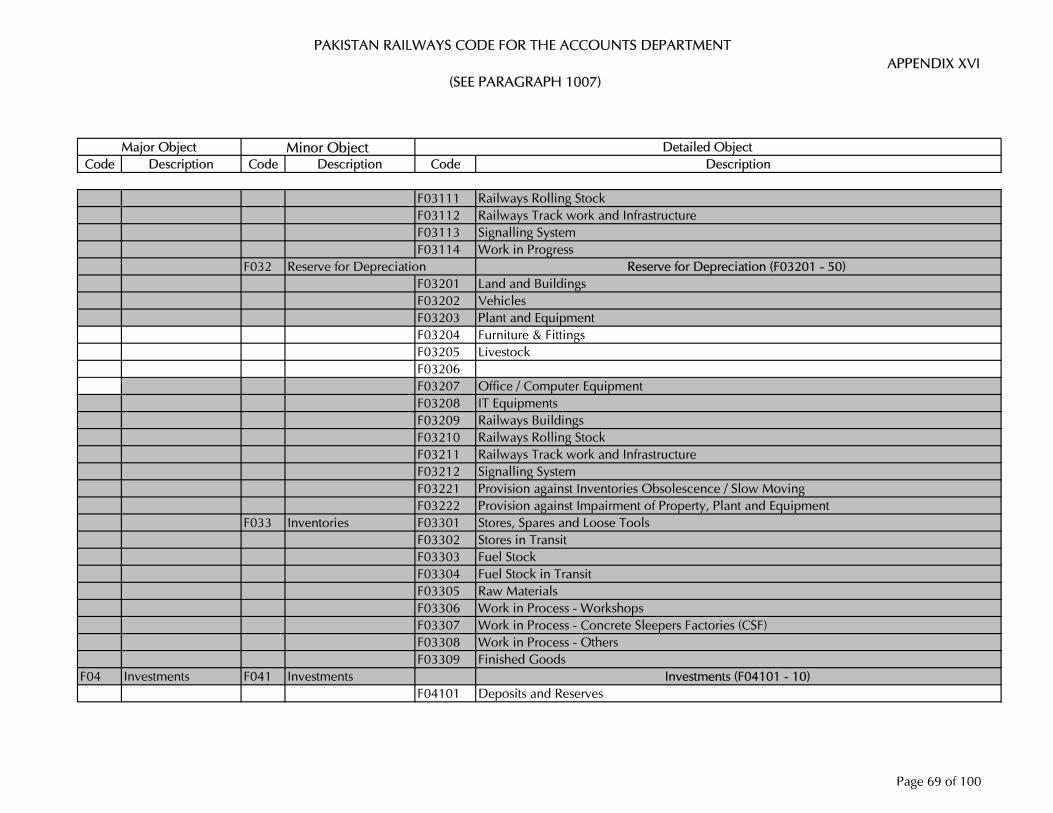

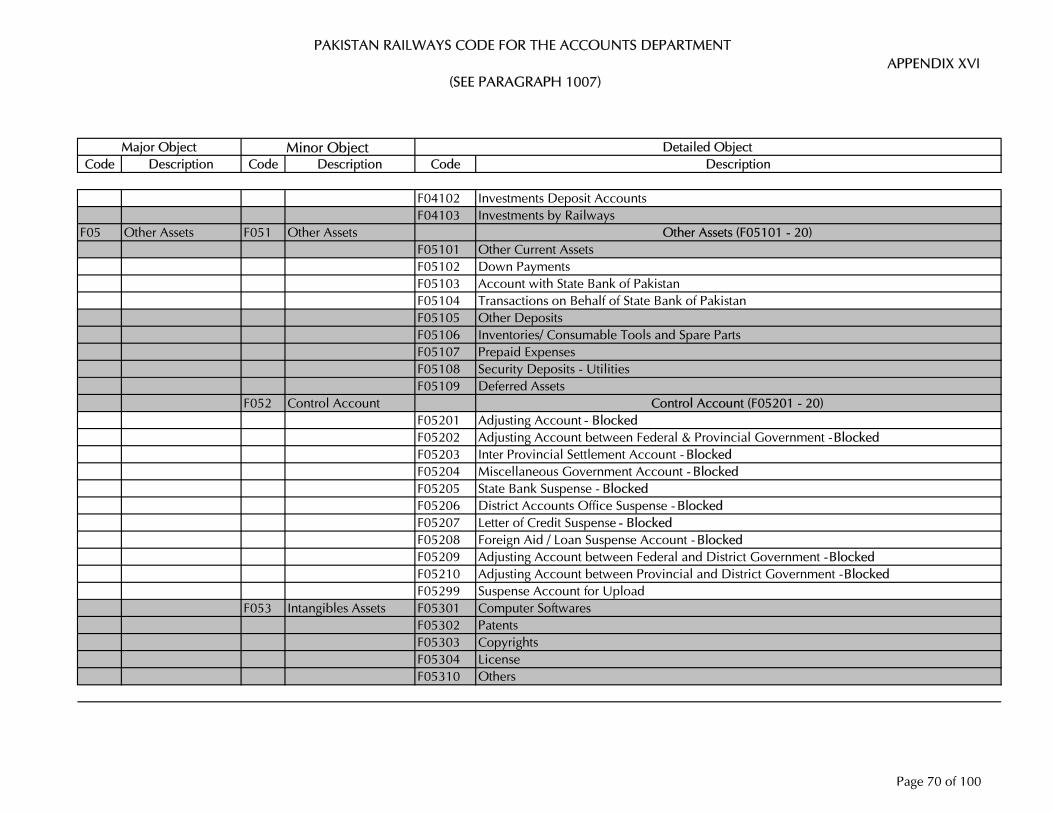

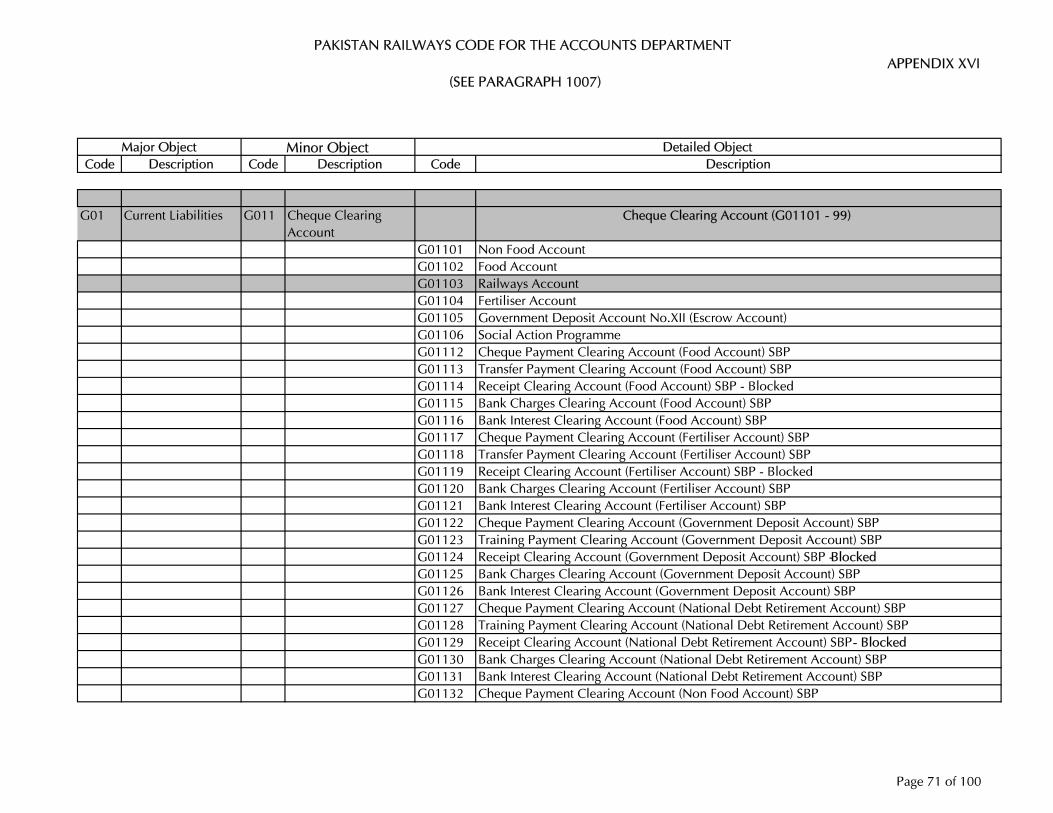

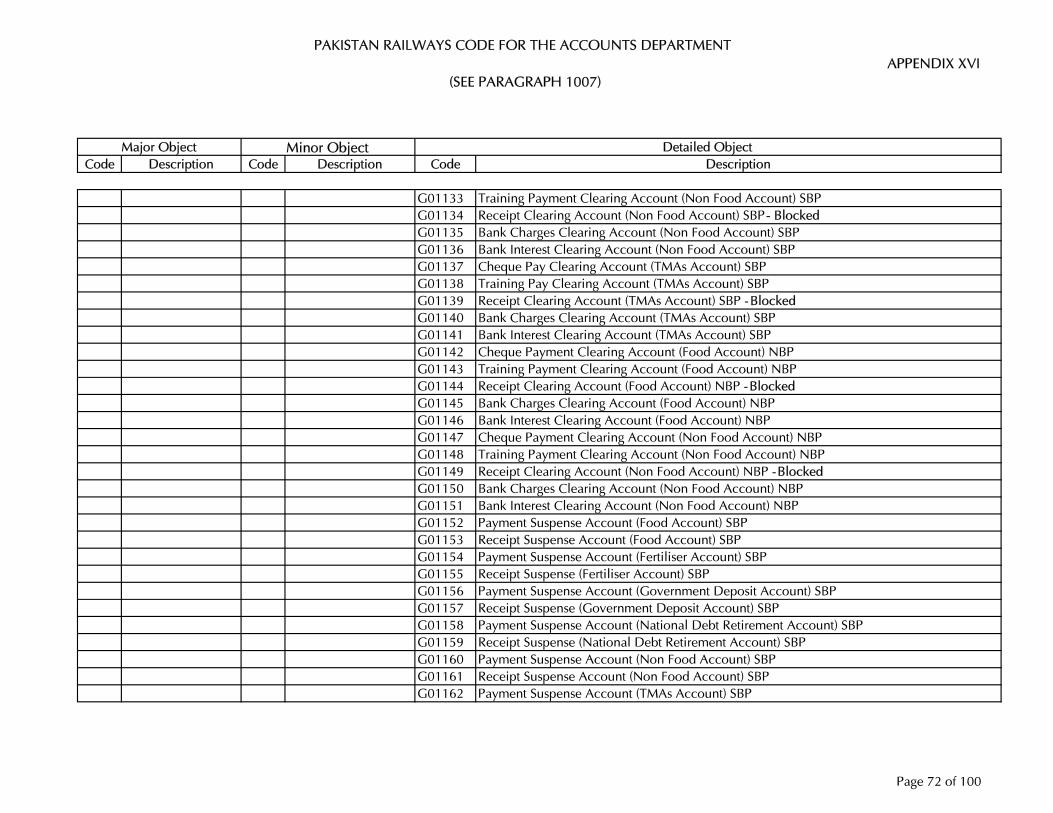

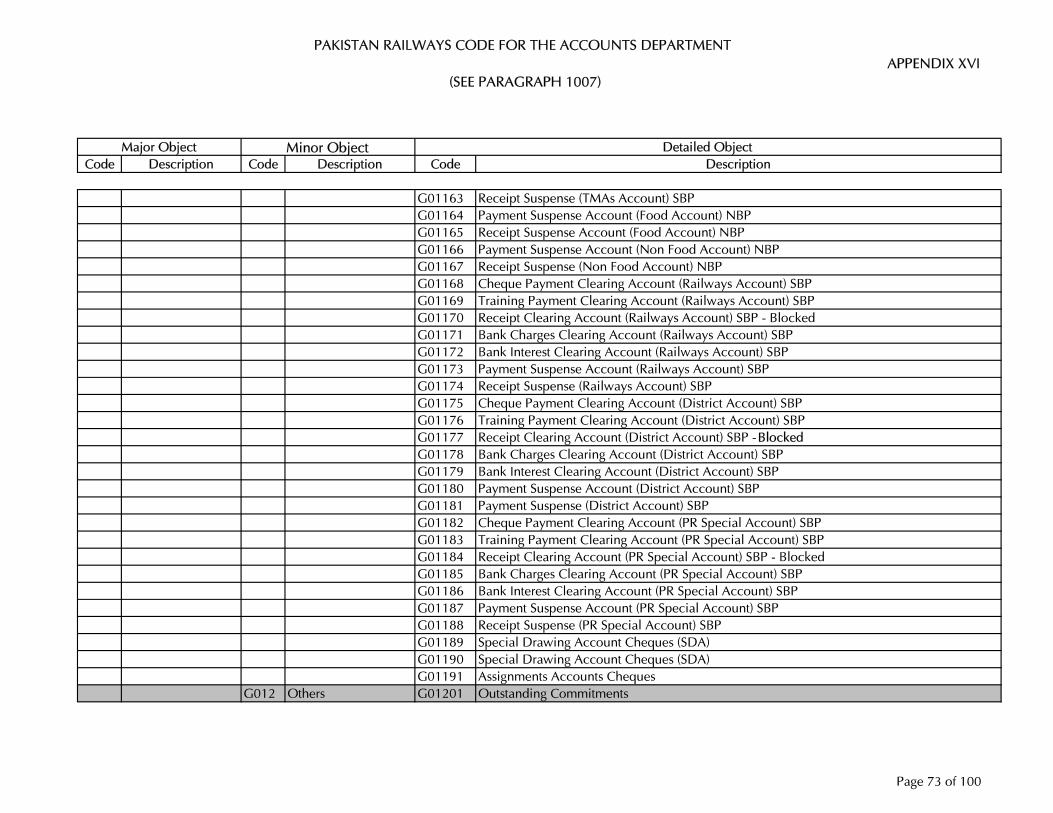

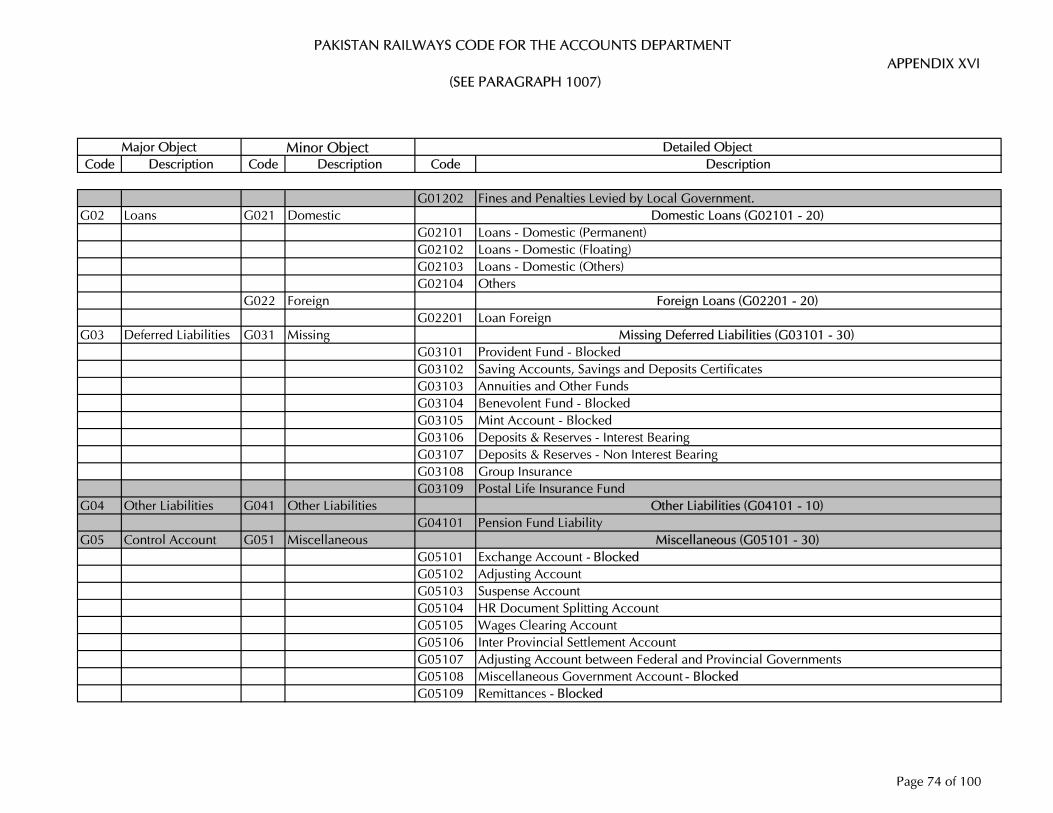

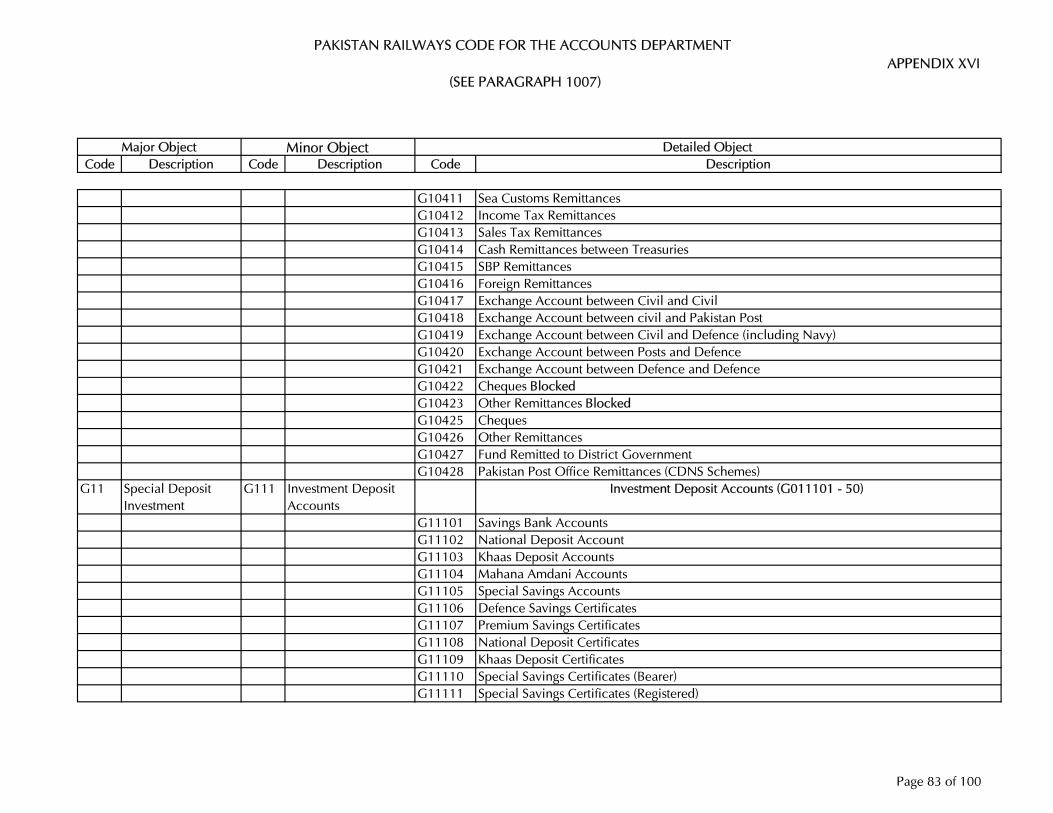

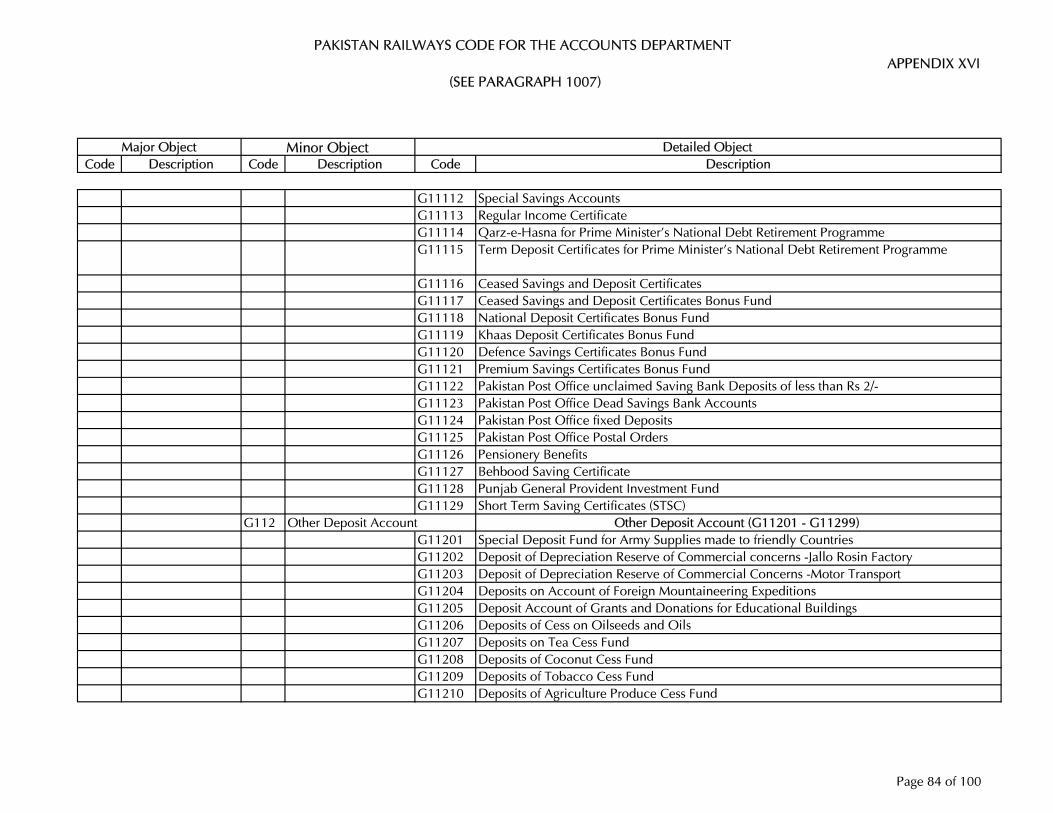

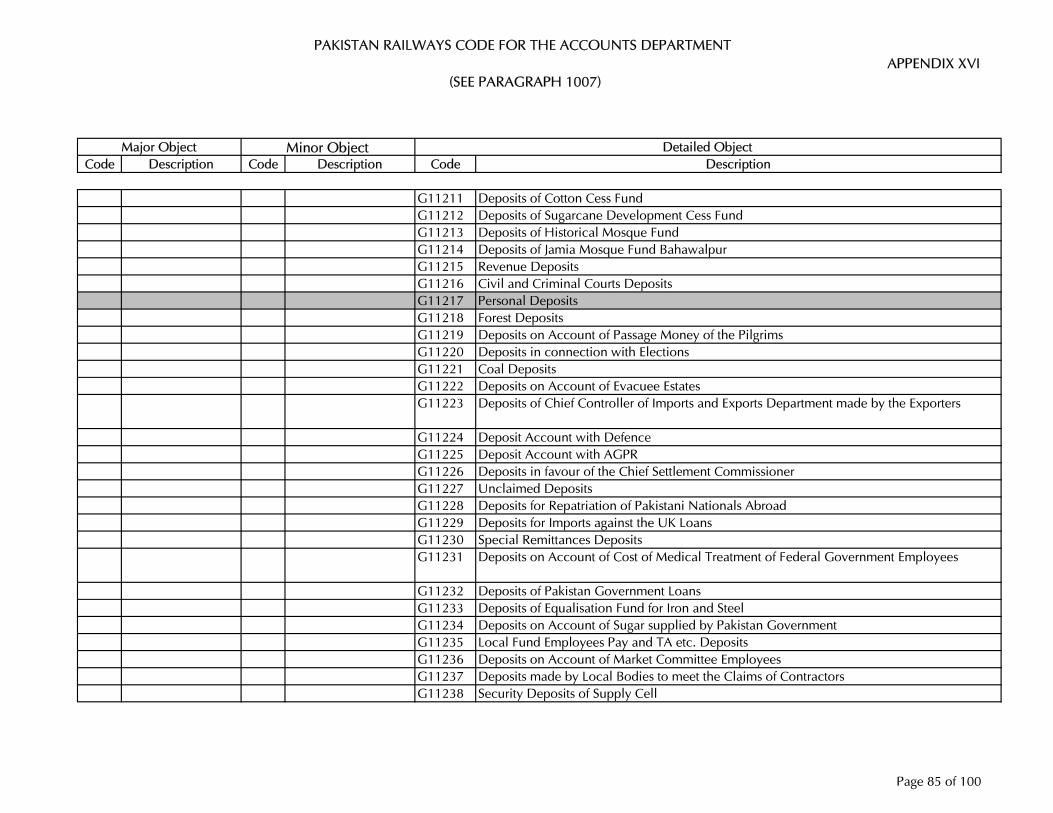

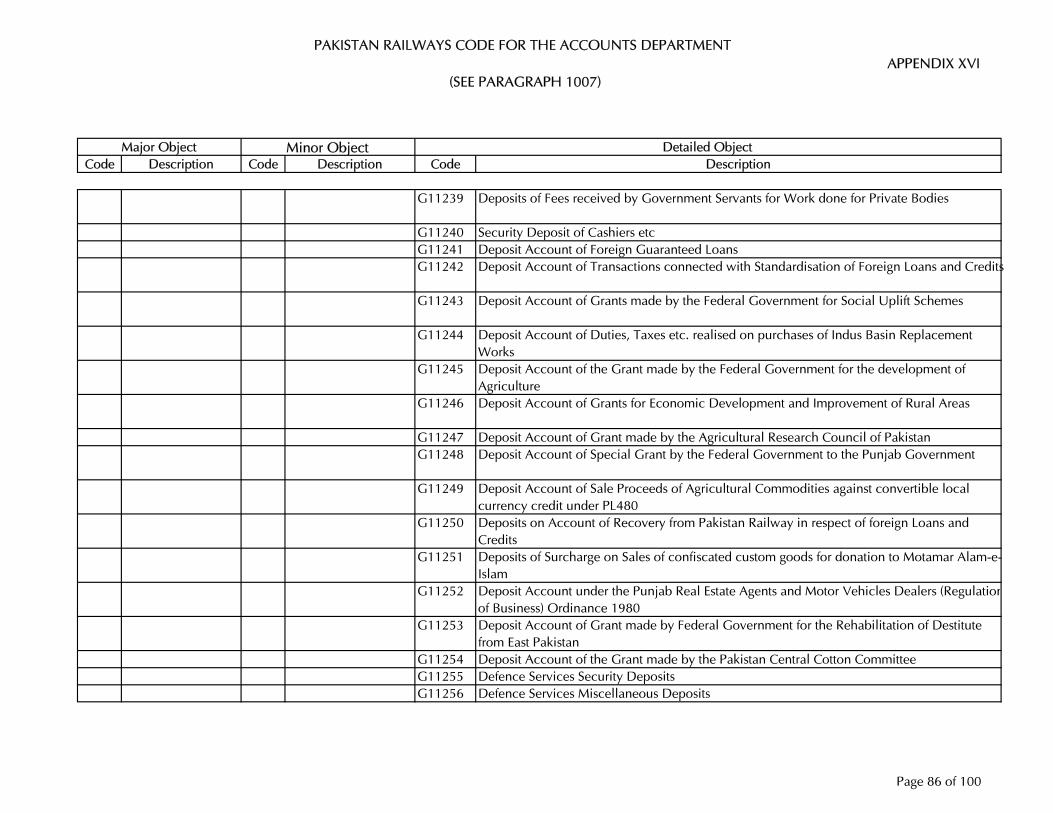

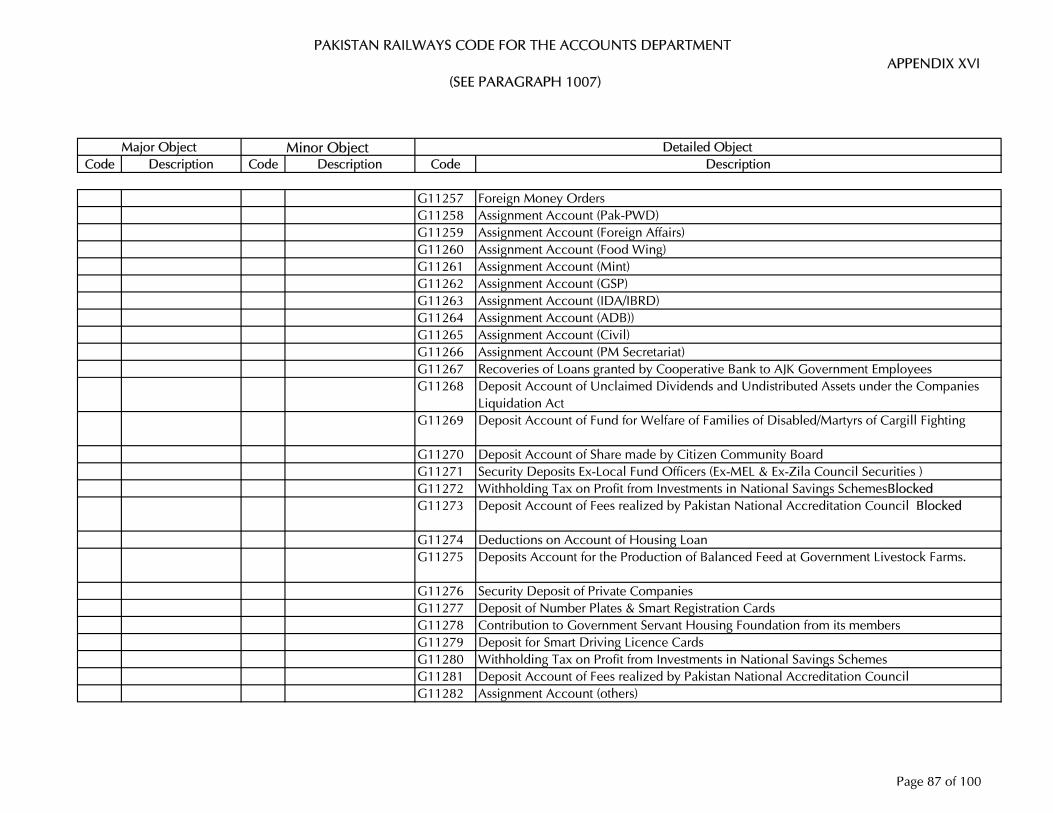

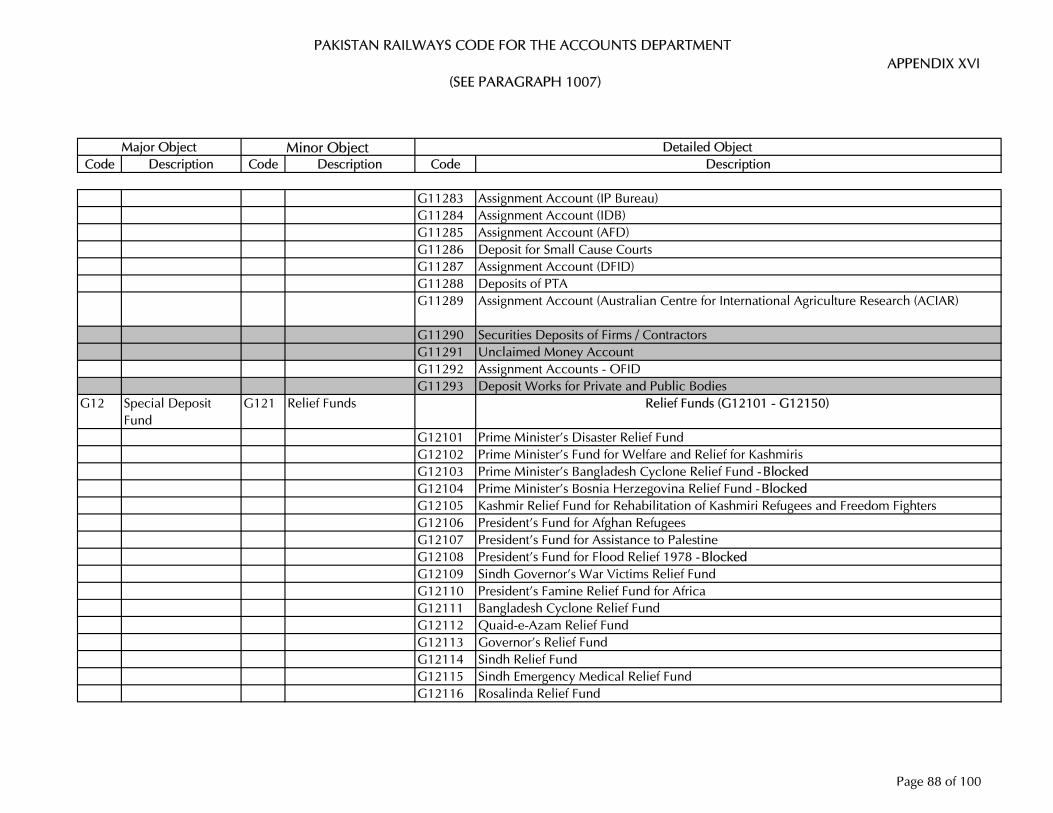

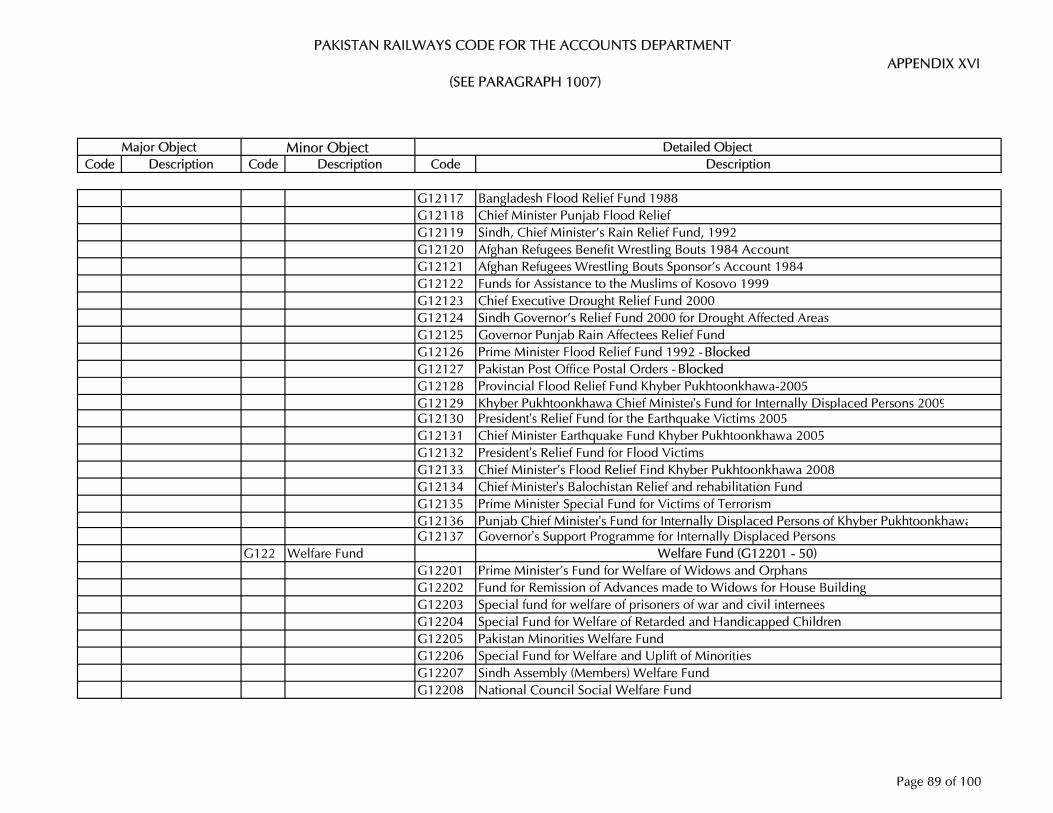

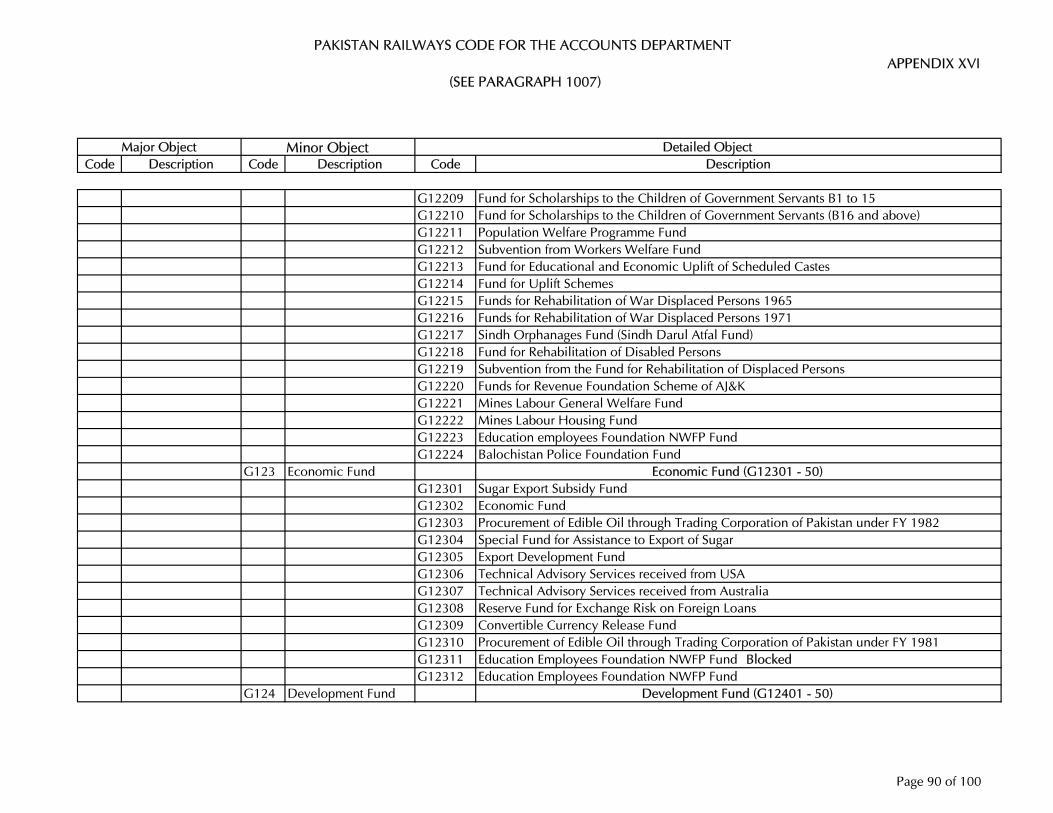

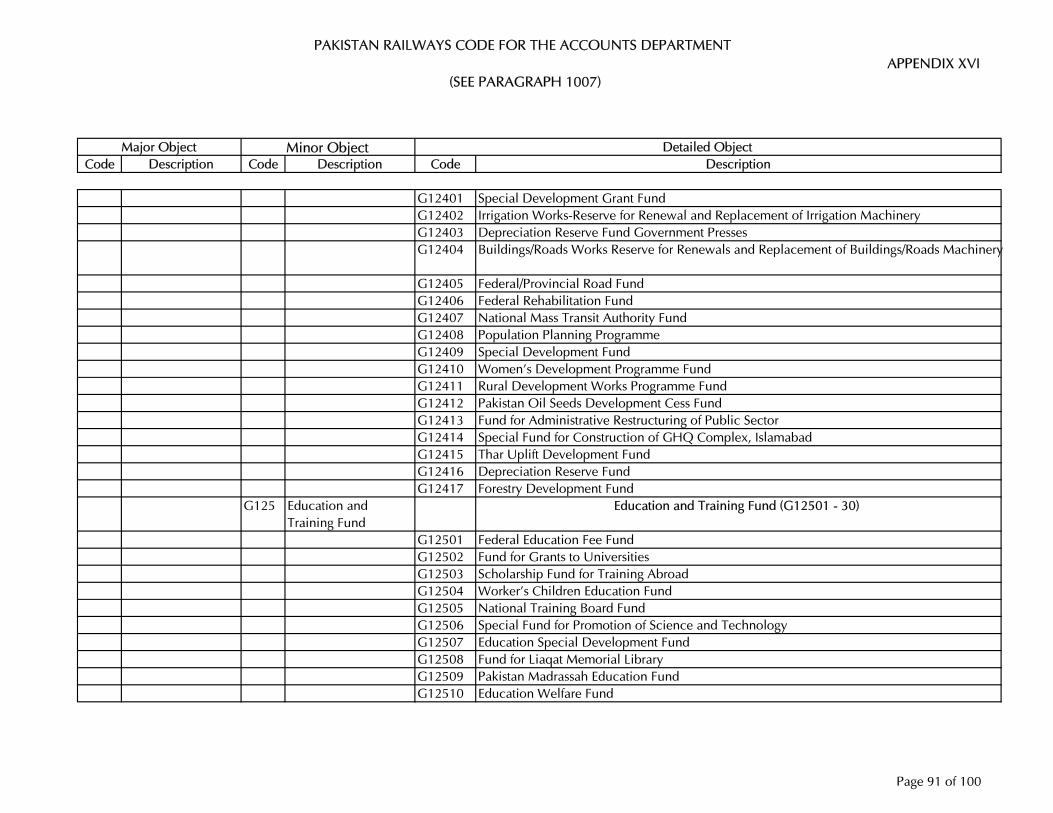

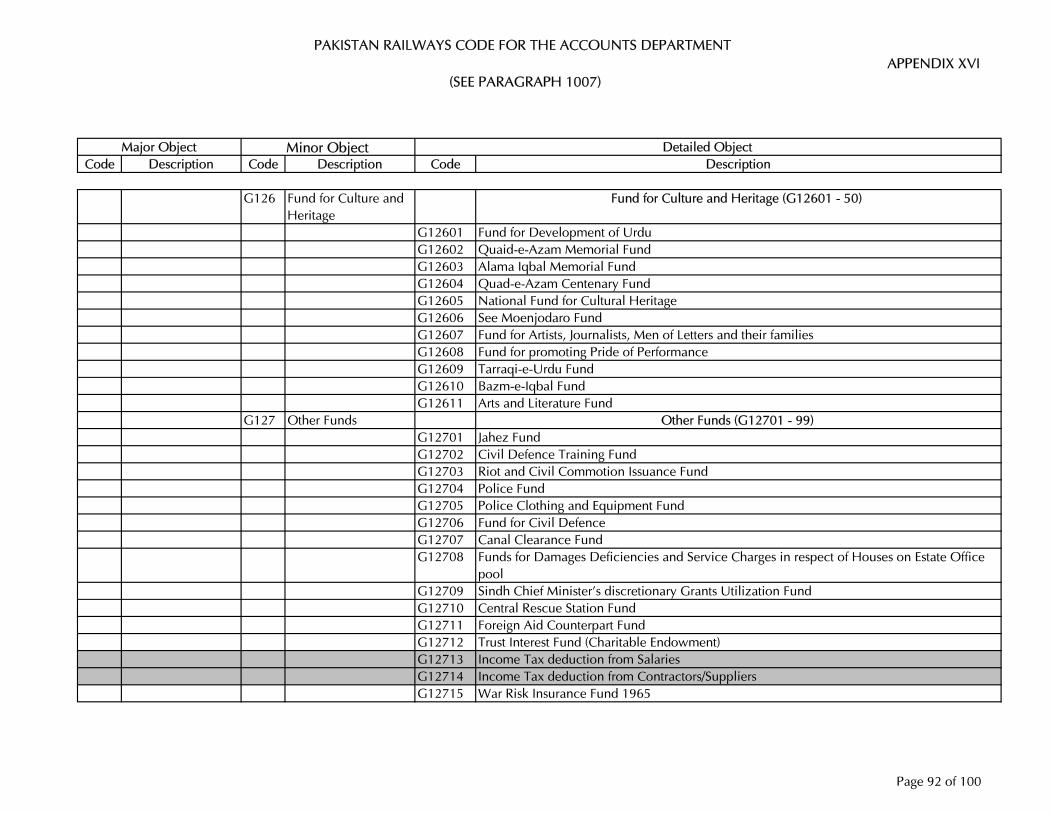

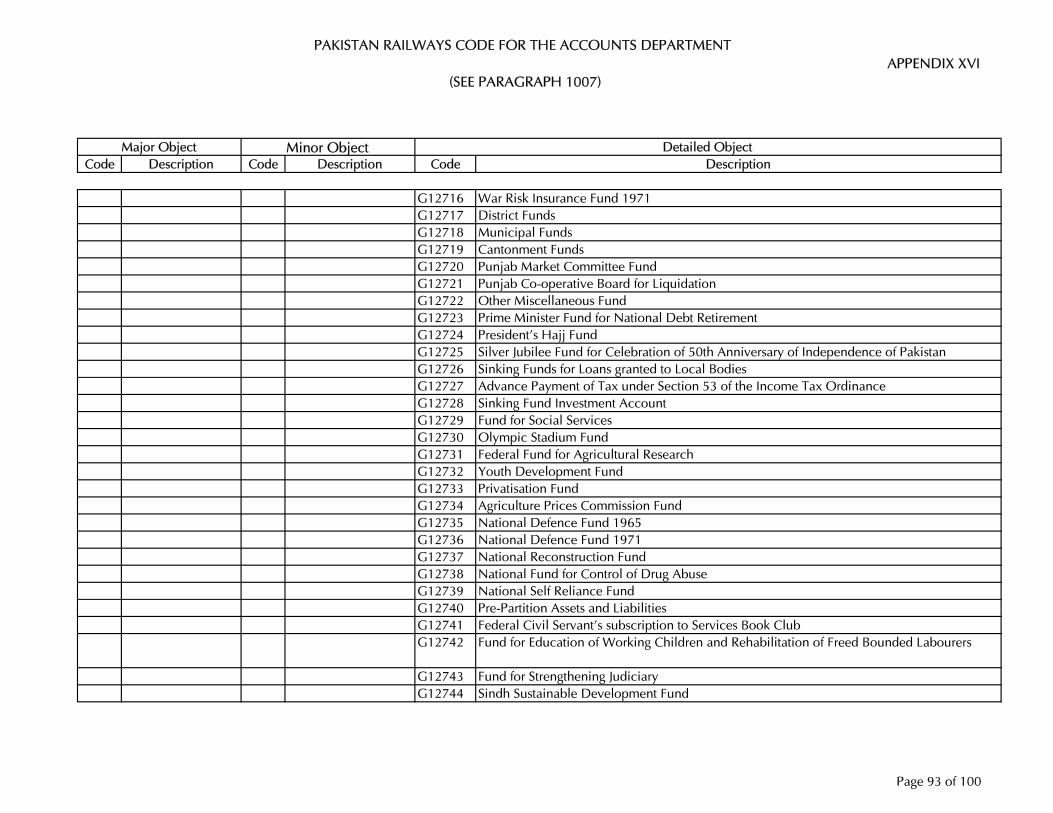

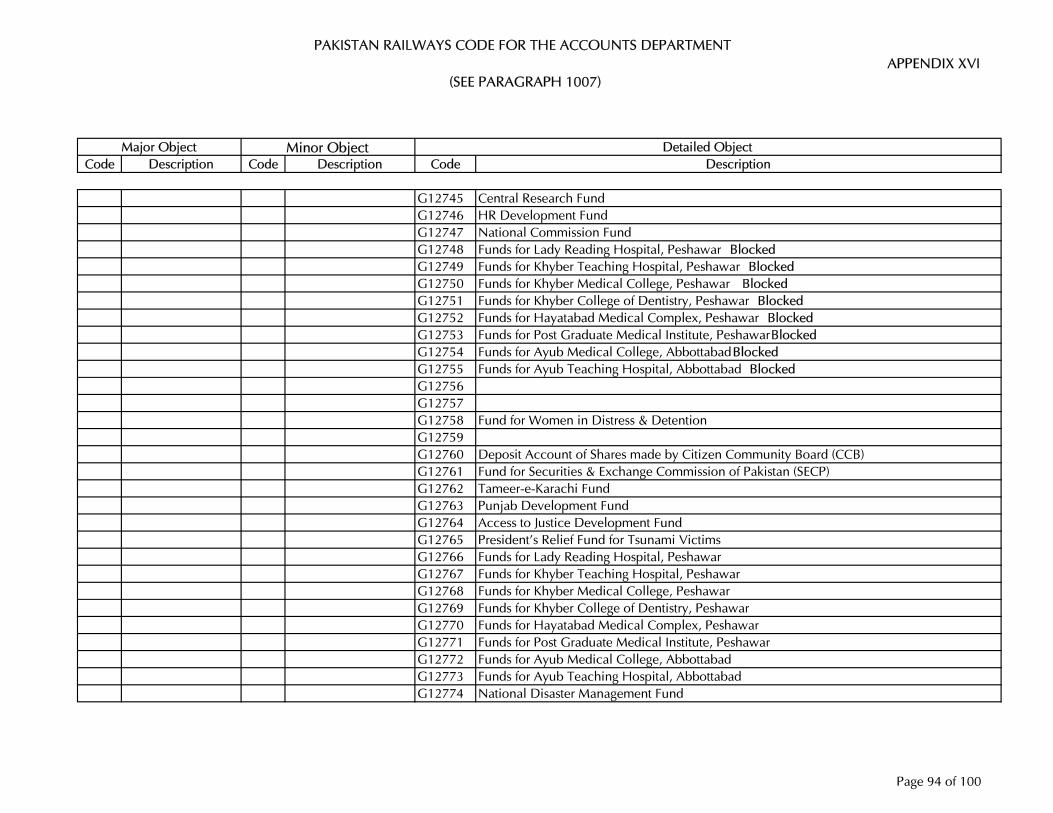

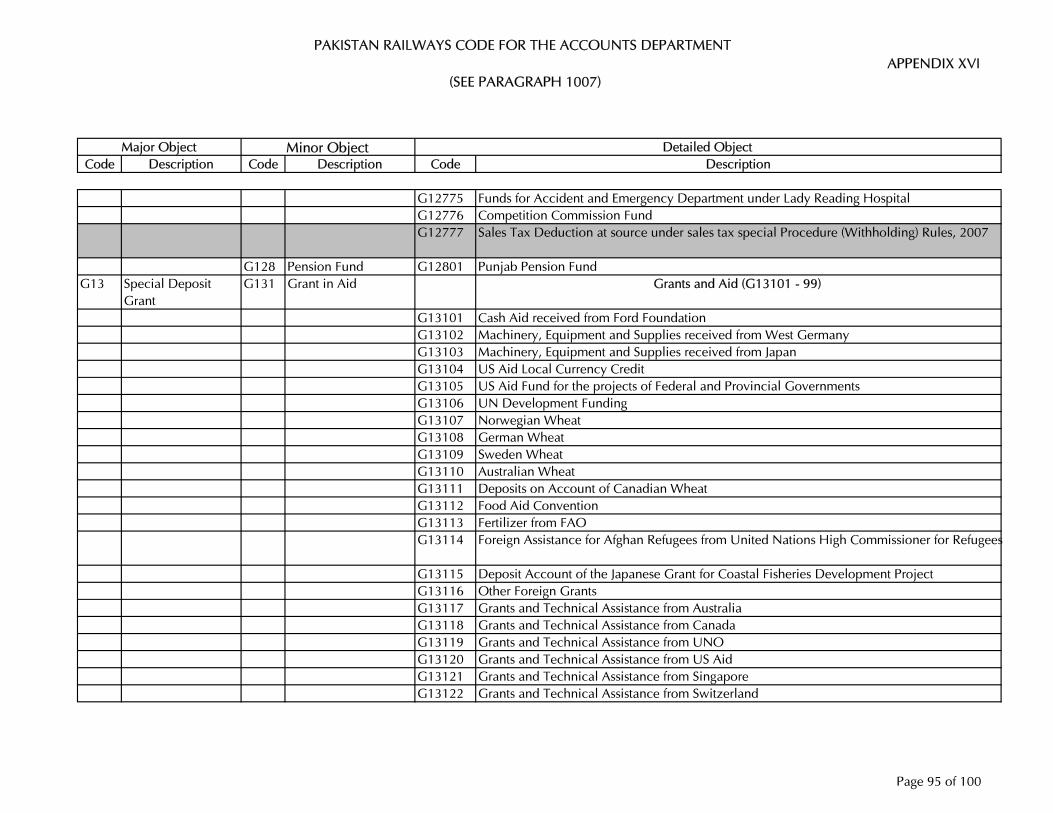

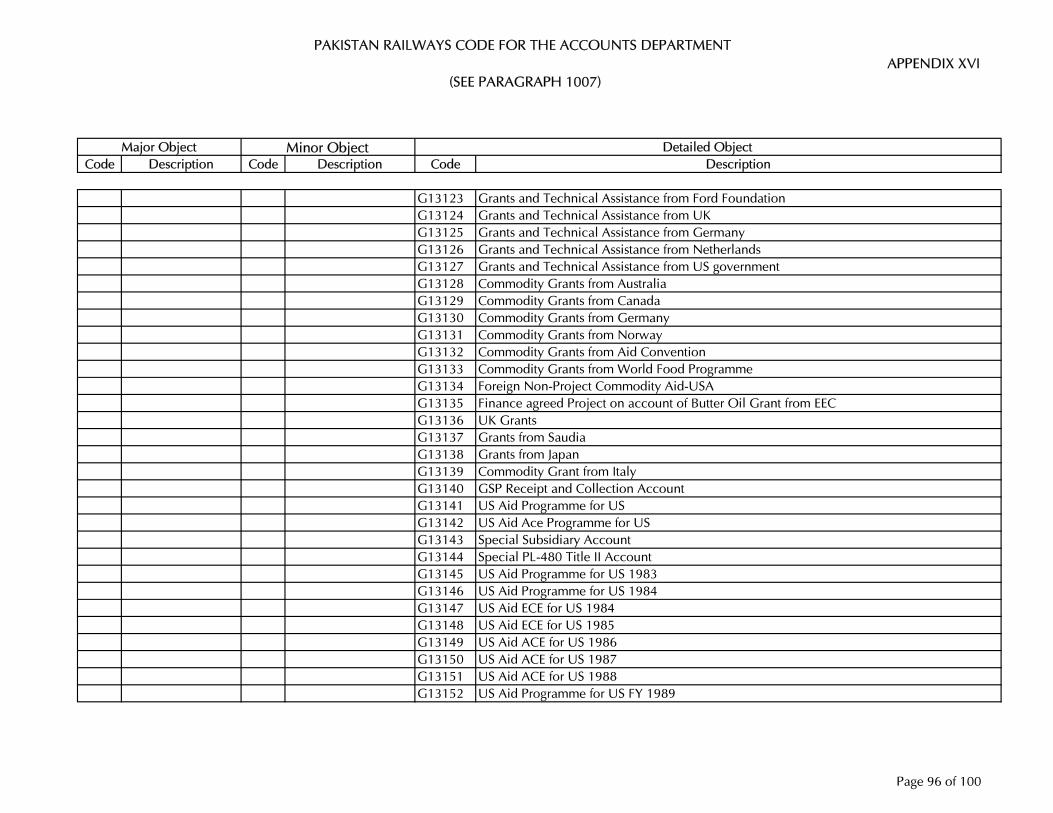

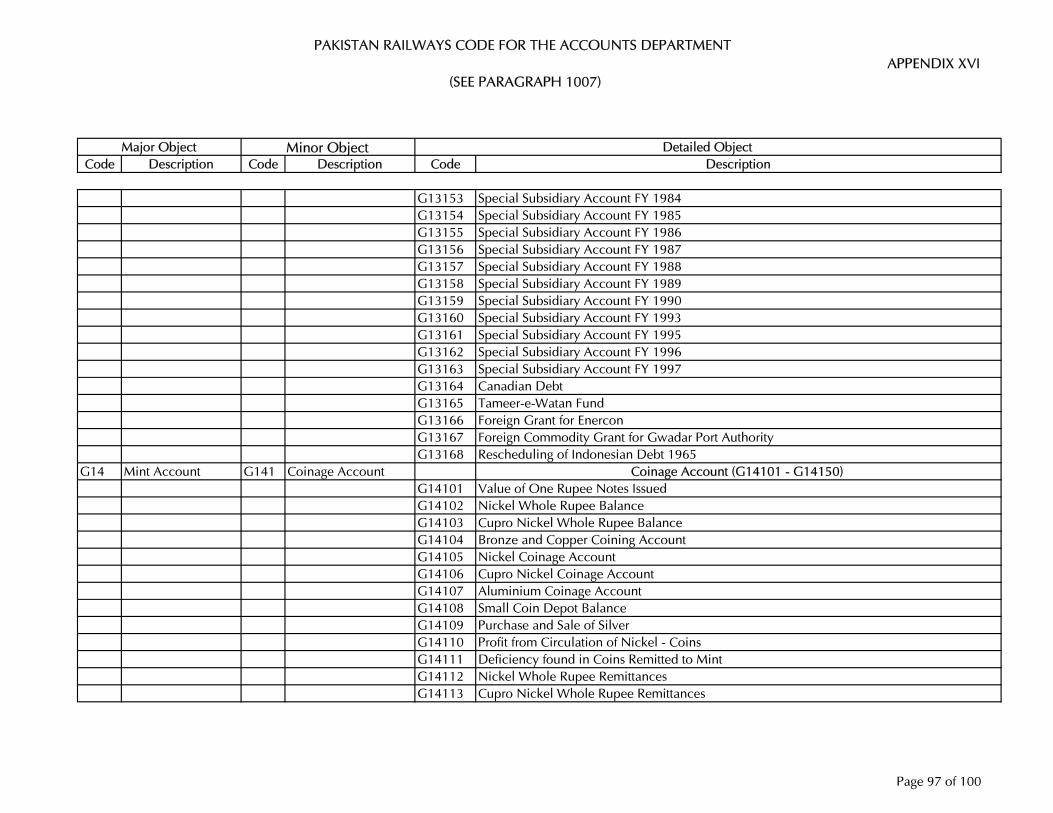

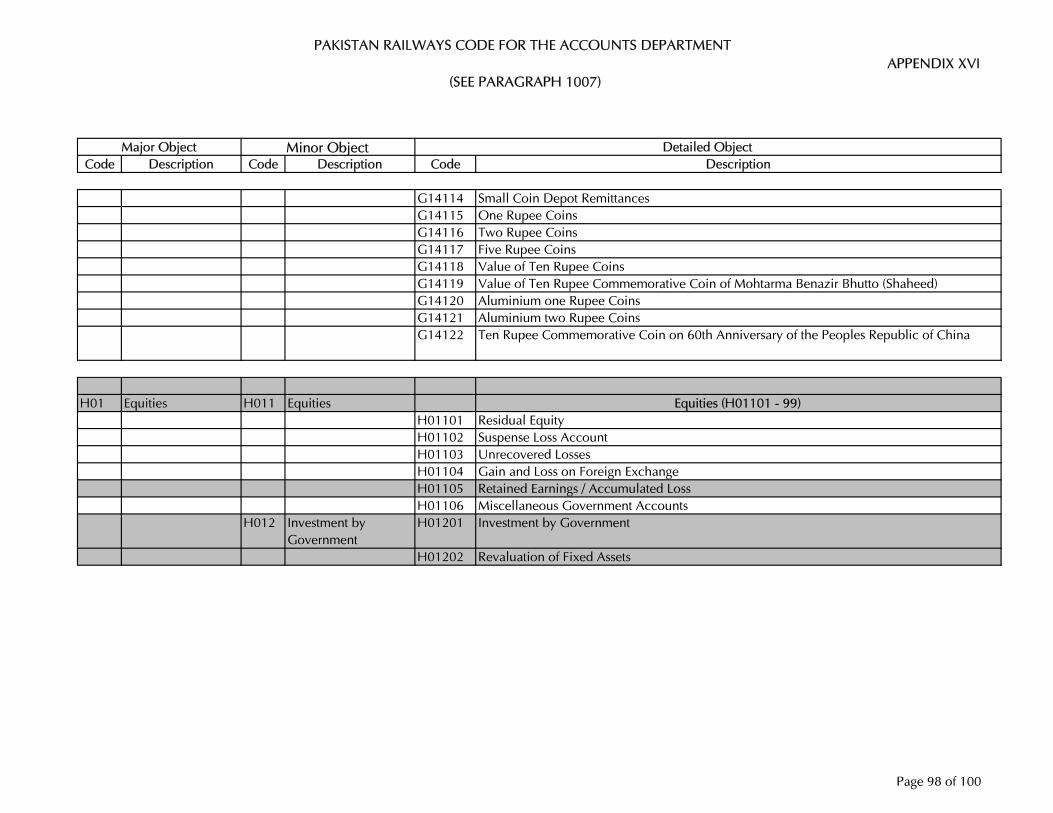

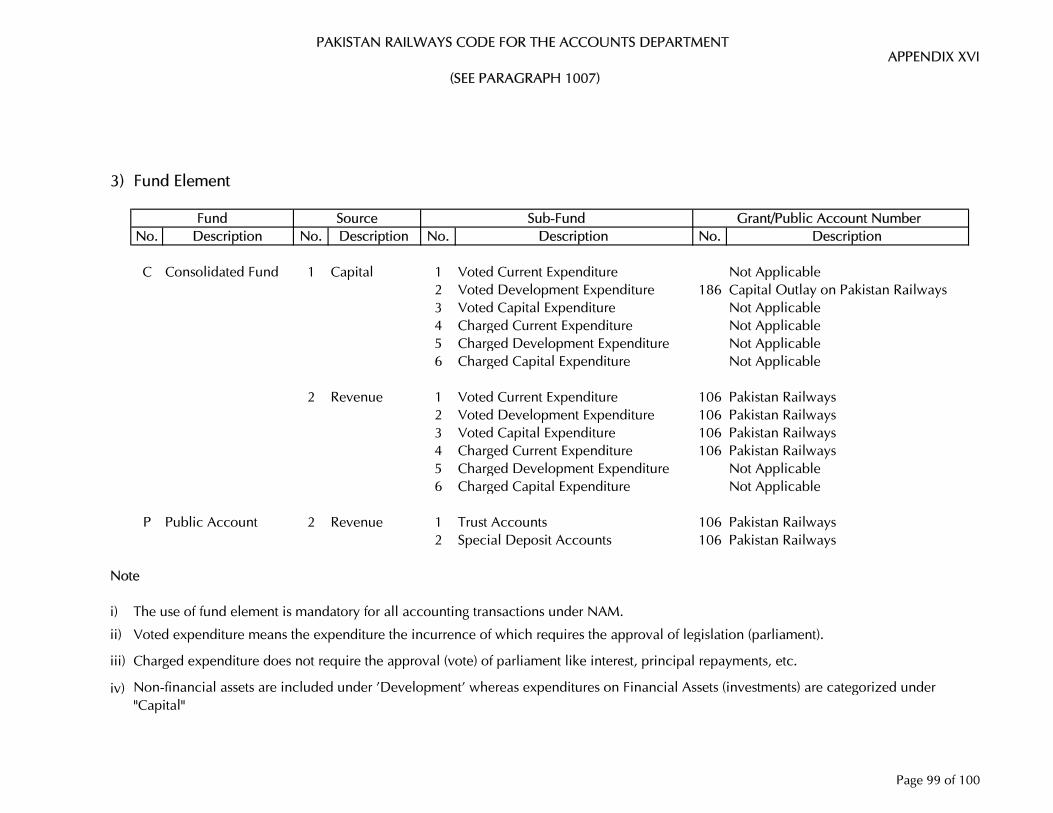

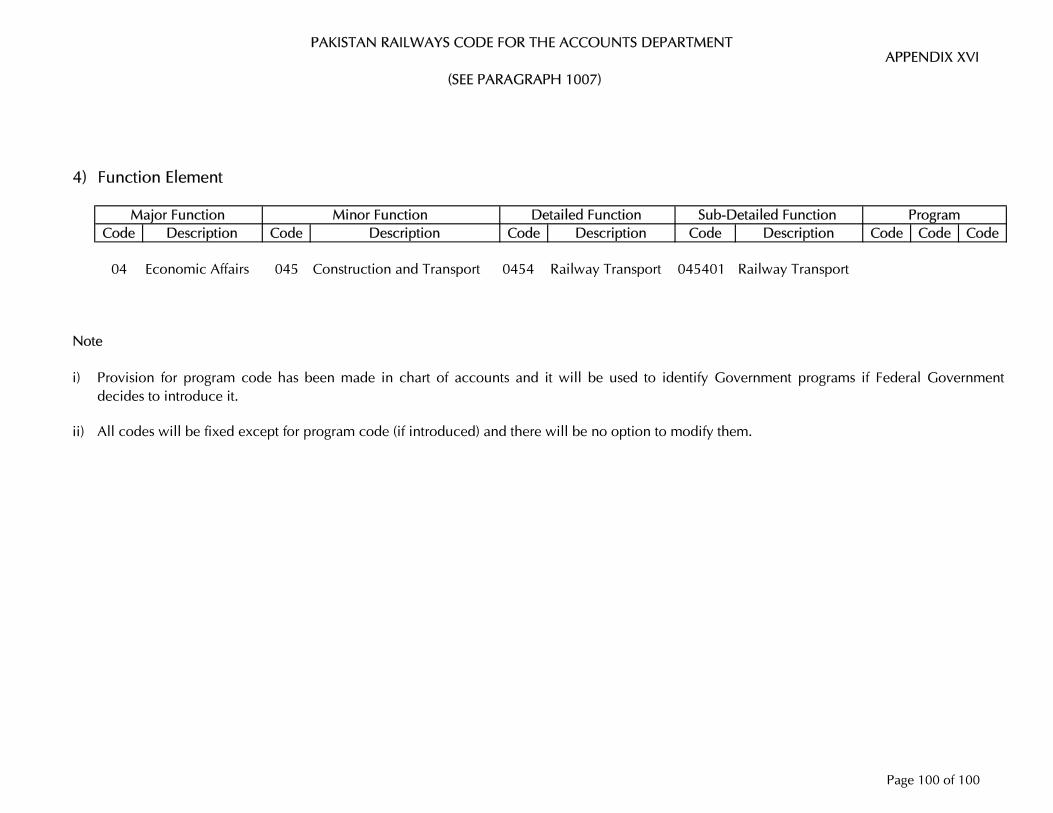

CHART OF ACCOUNTS XVI

RULES REGULATING THE EXHIBITION OF RECOVERIES OF EXPENDITURE IN GOVERNMENT ACCOUNTS

XVII

RULES RELATING TO INTER-DEPARTMENTAL TRANSFERS XVIII

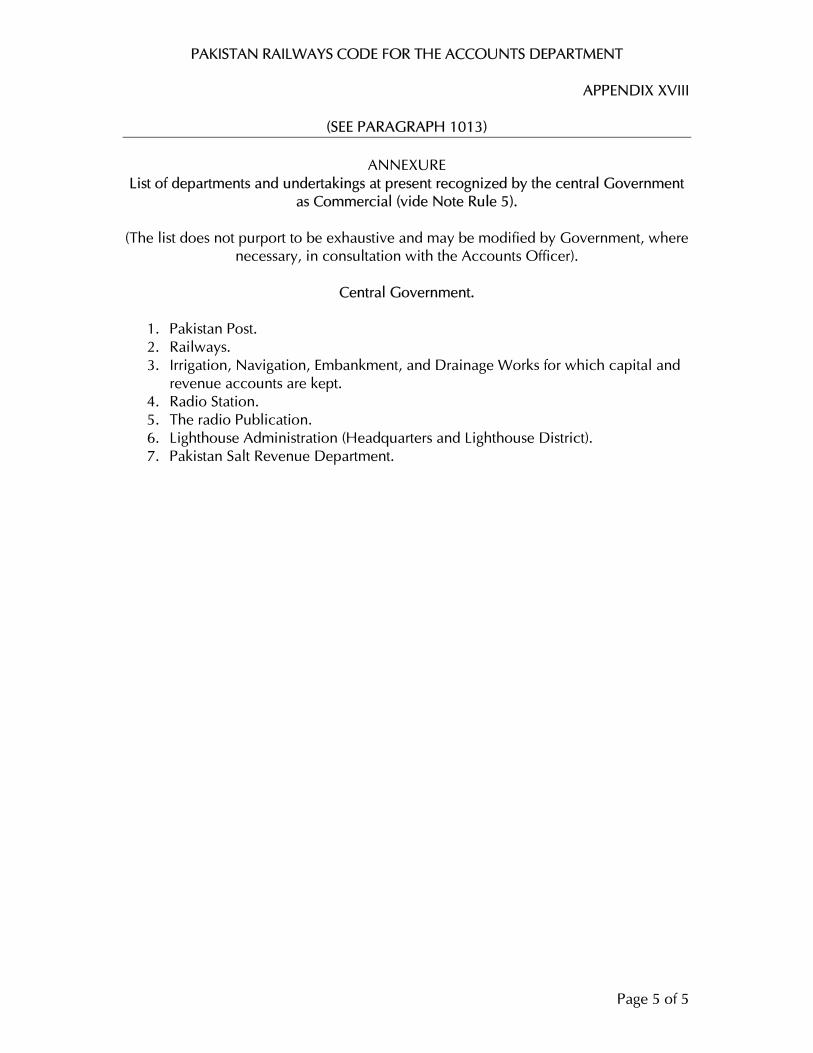

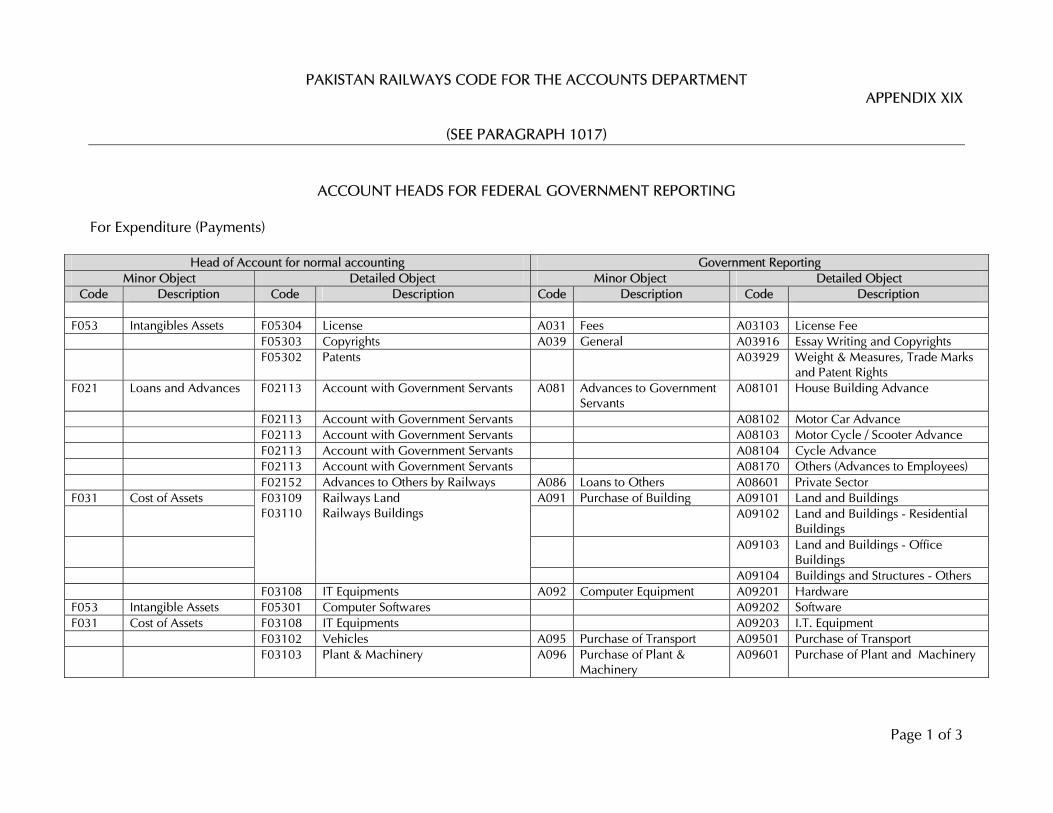

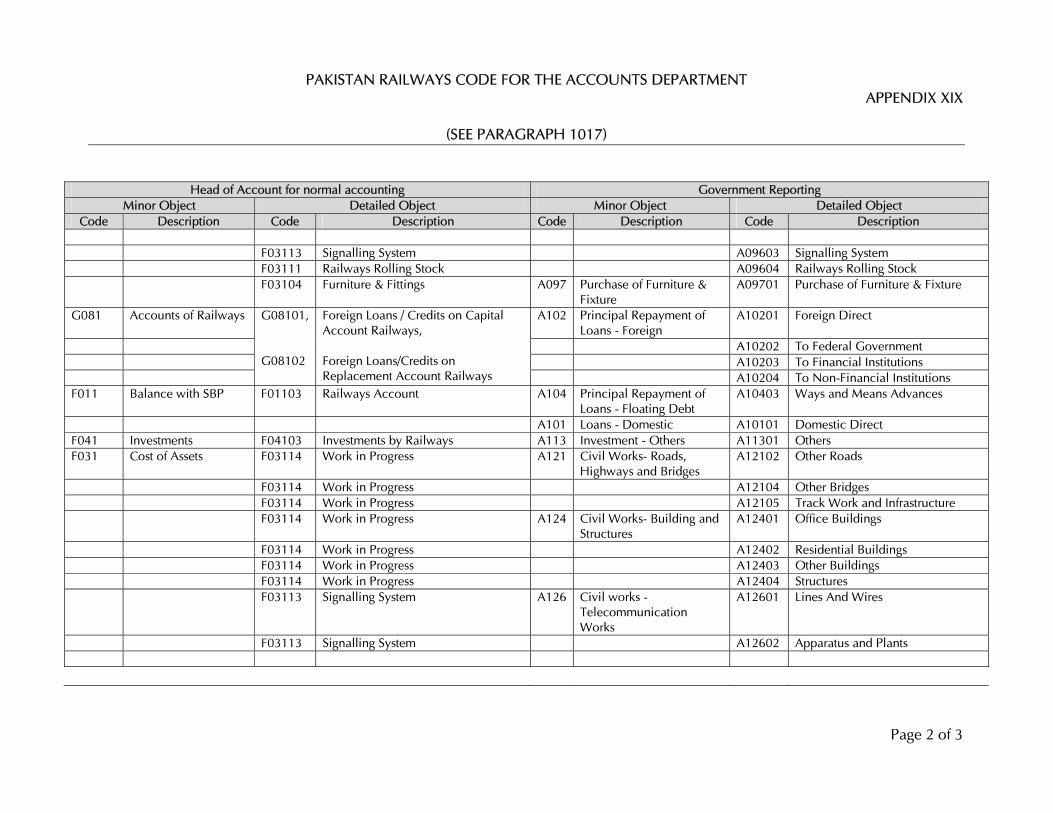

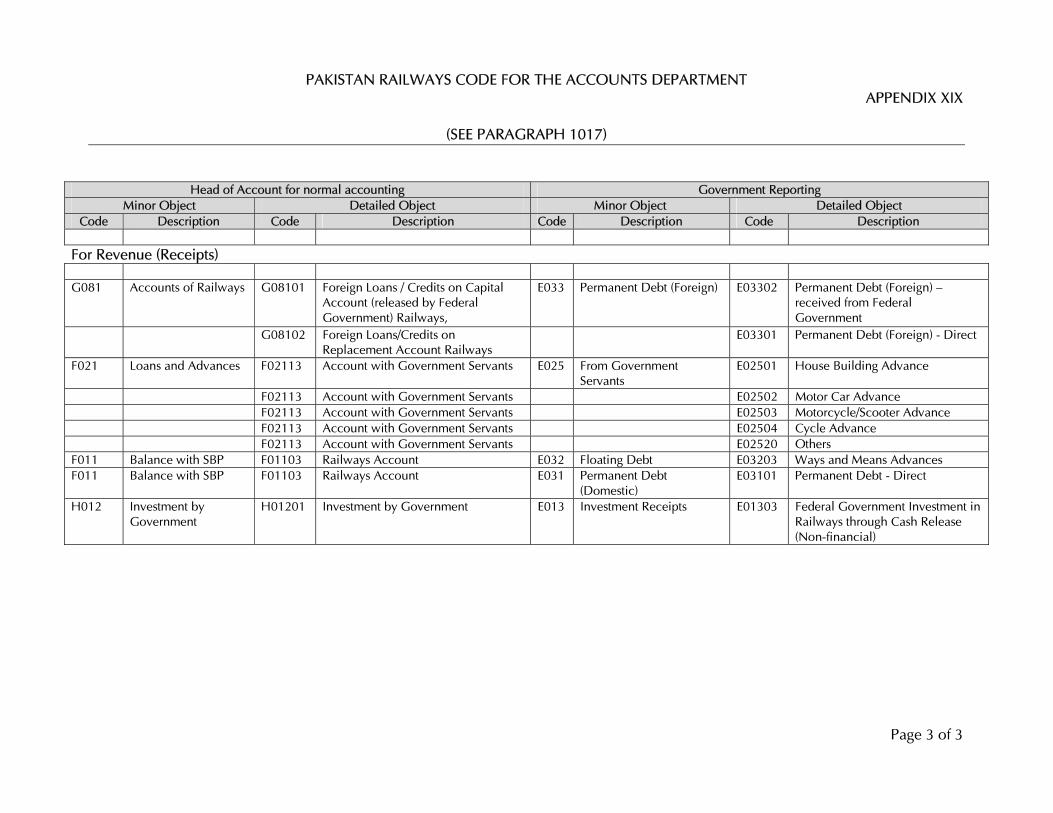

ACCOUNT HEADS FOR FEDERAL GOVERNMENT REPORTING XIX

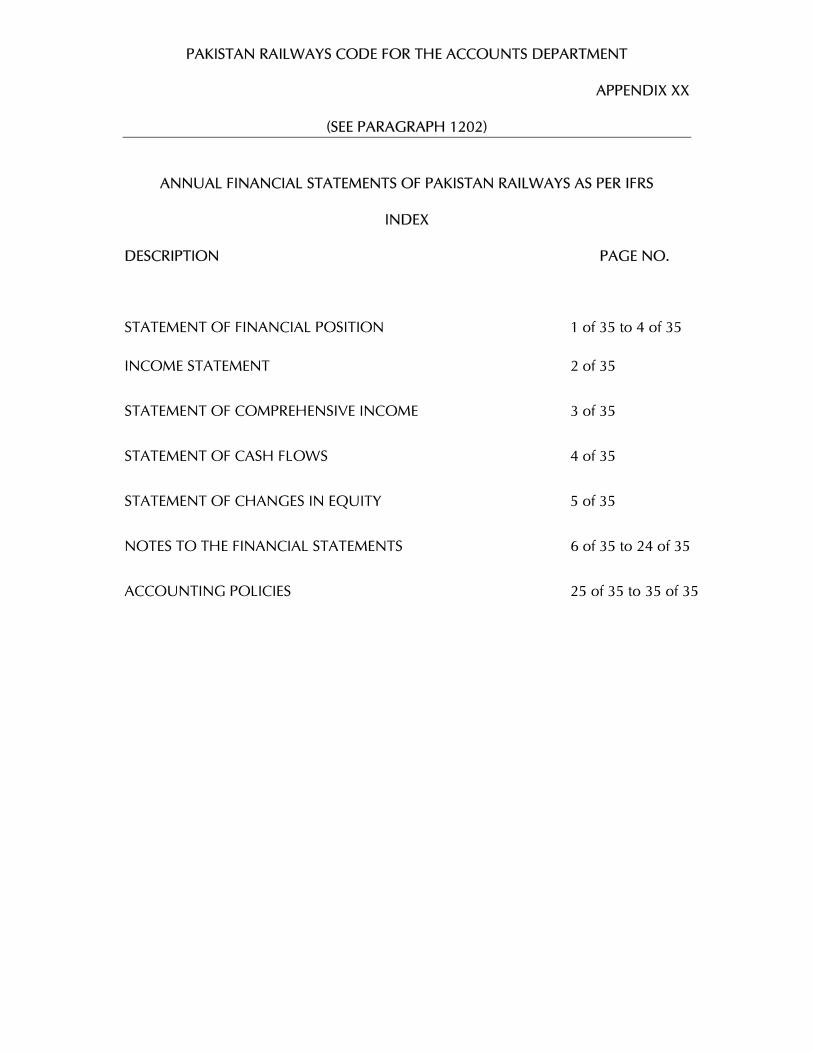

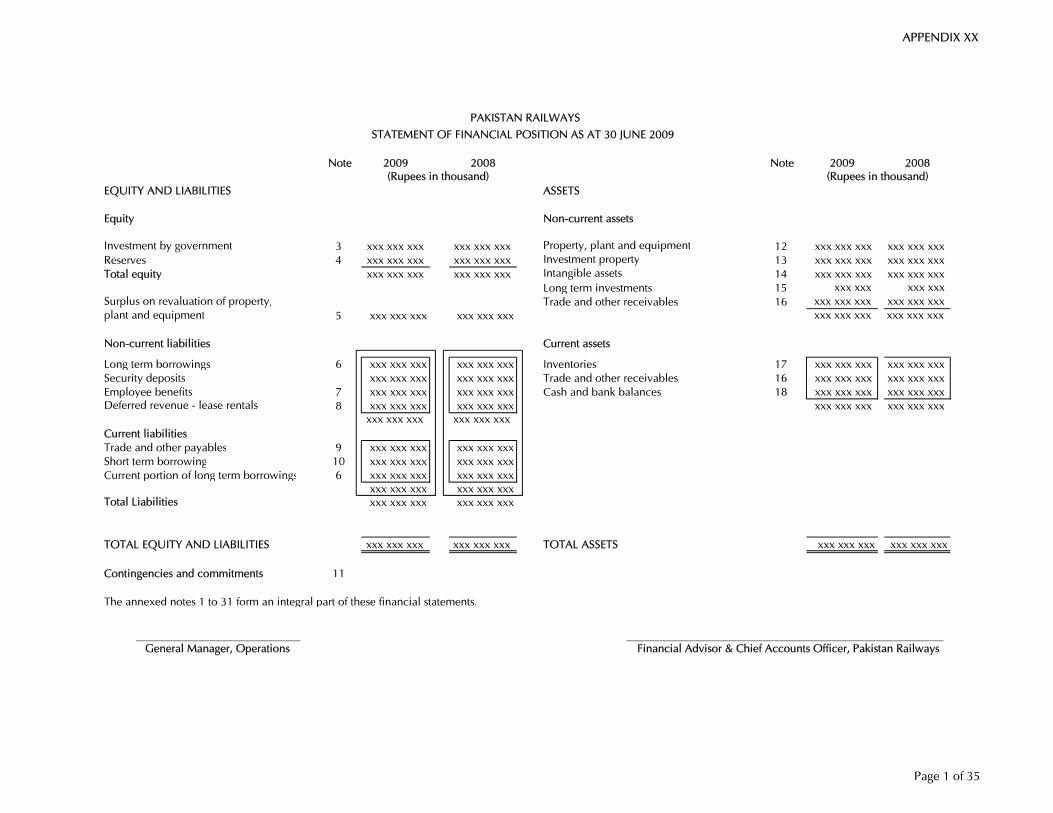

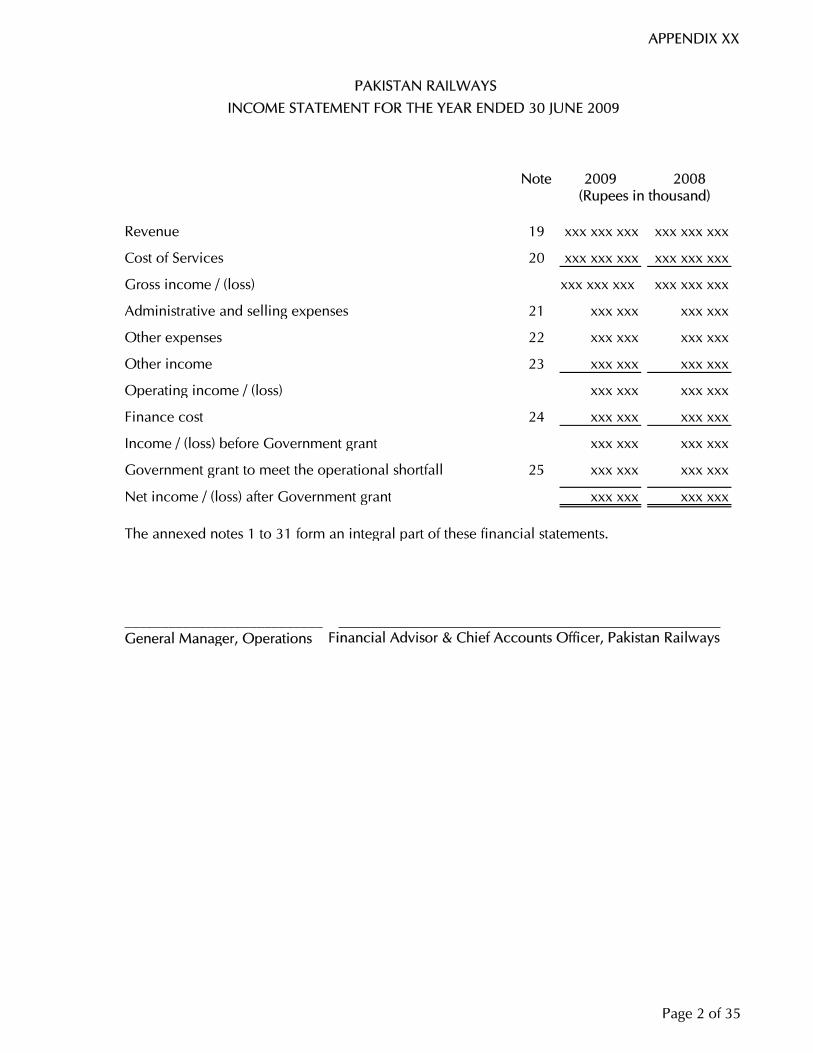

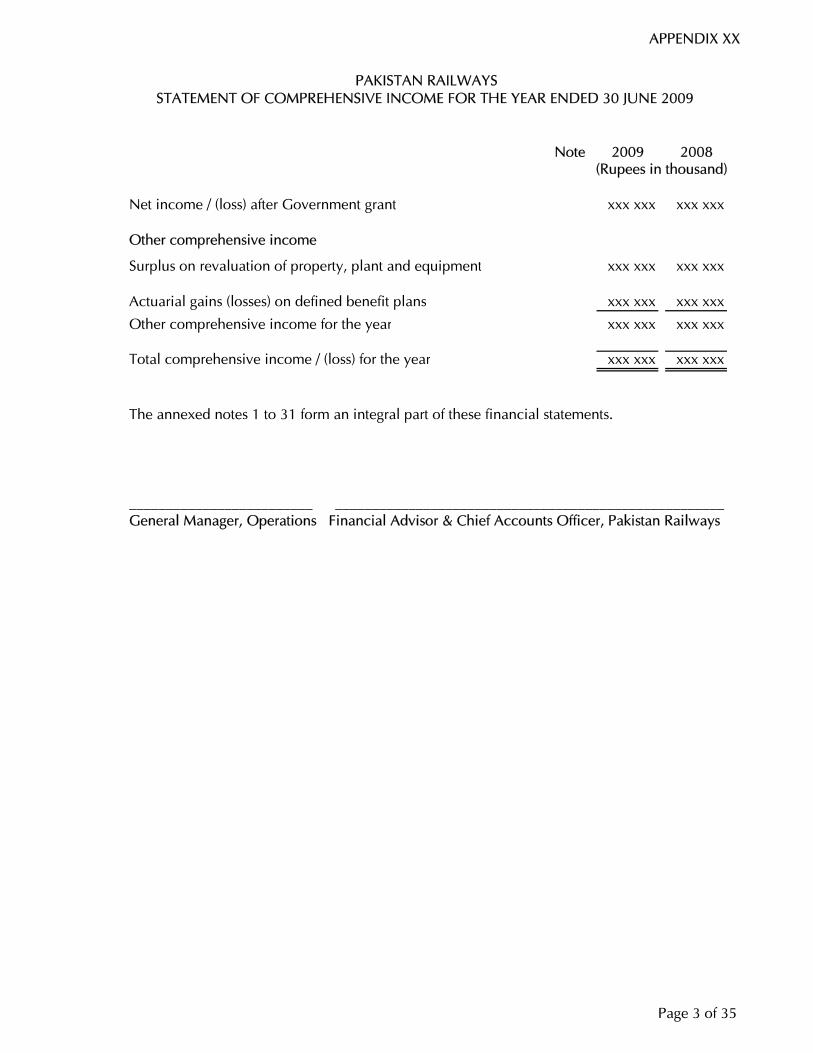

ANNUAL FINANCIAL STATEMENTS OF PAKISTAN RAILWAYS AS PER IFRS XX

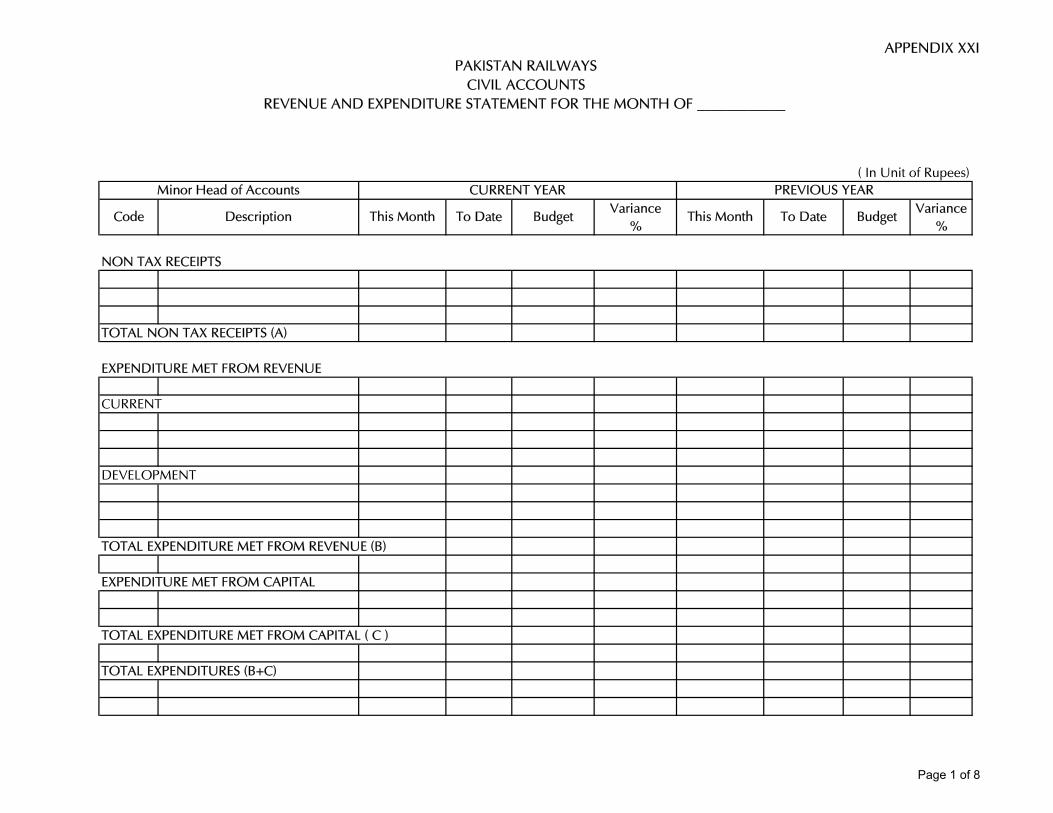

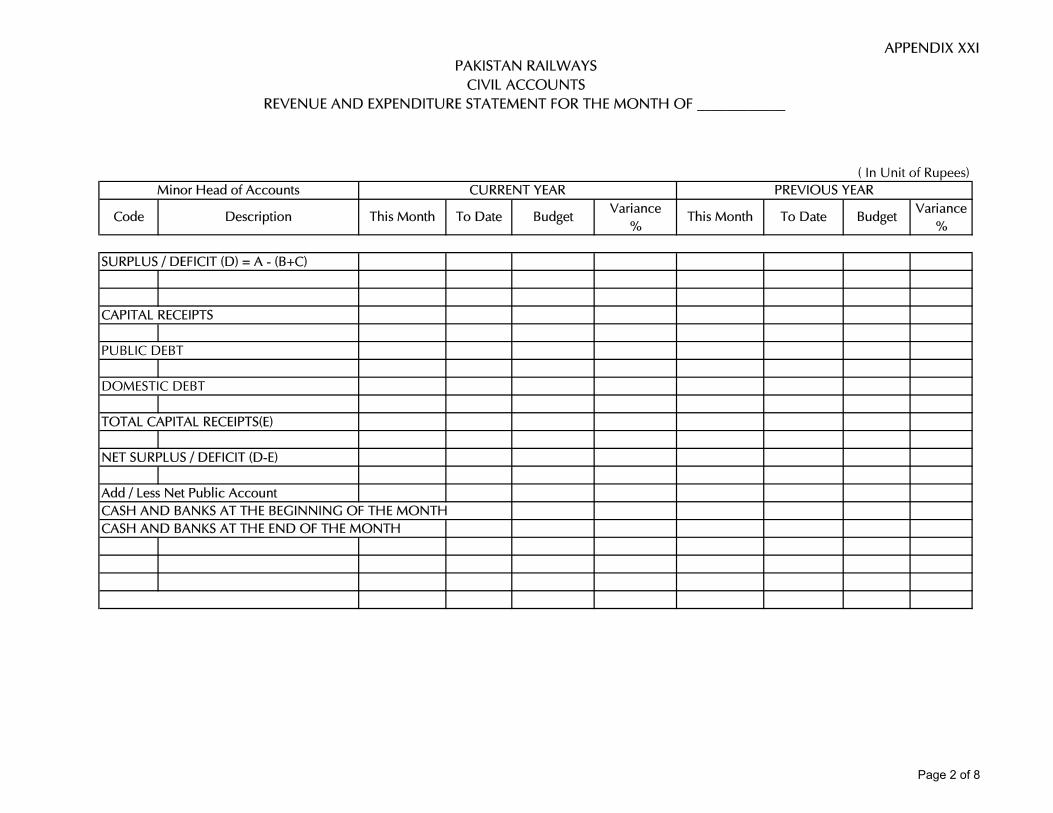

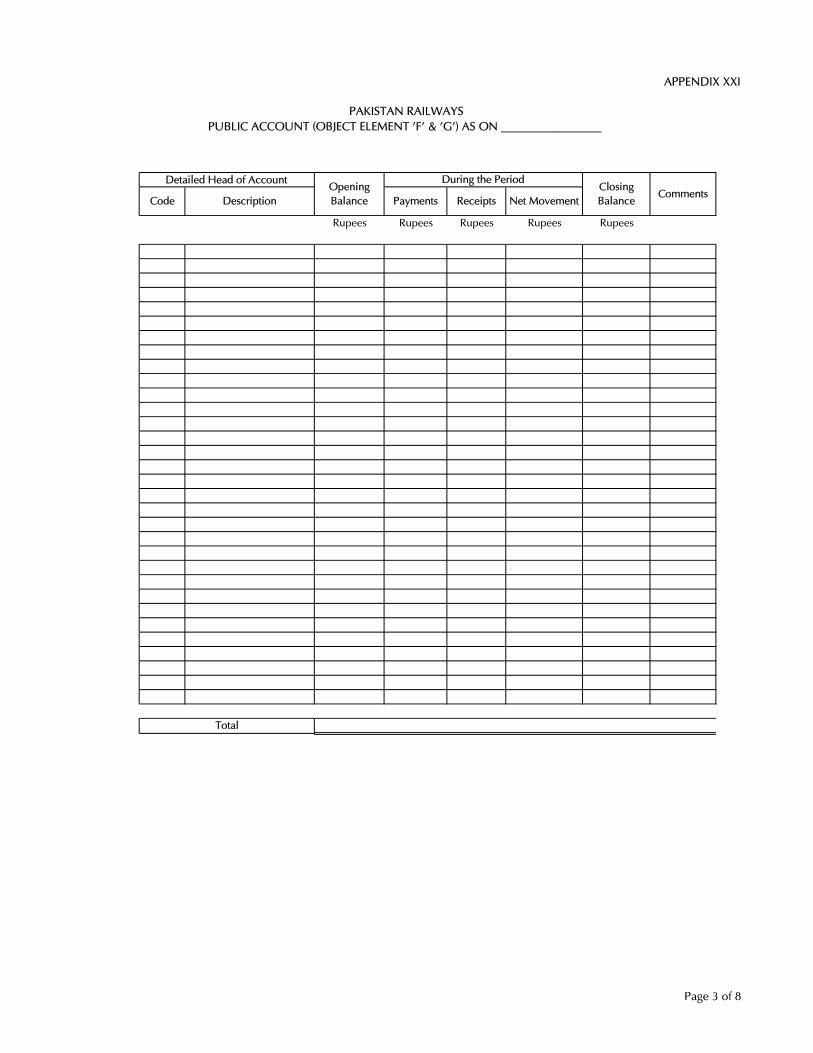

MONTHLY CIVIL ACCOUNTS OF PAKISTAN RAILWAYS XXI

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

4

CONTENTS

DESCRIPTION PAGE NO. PARA NO.

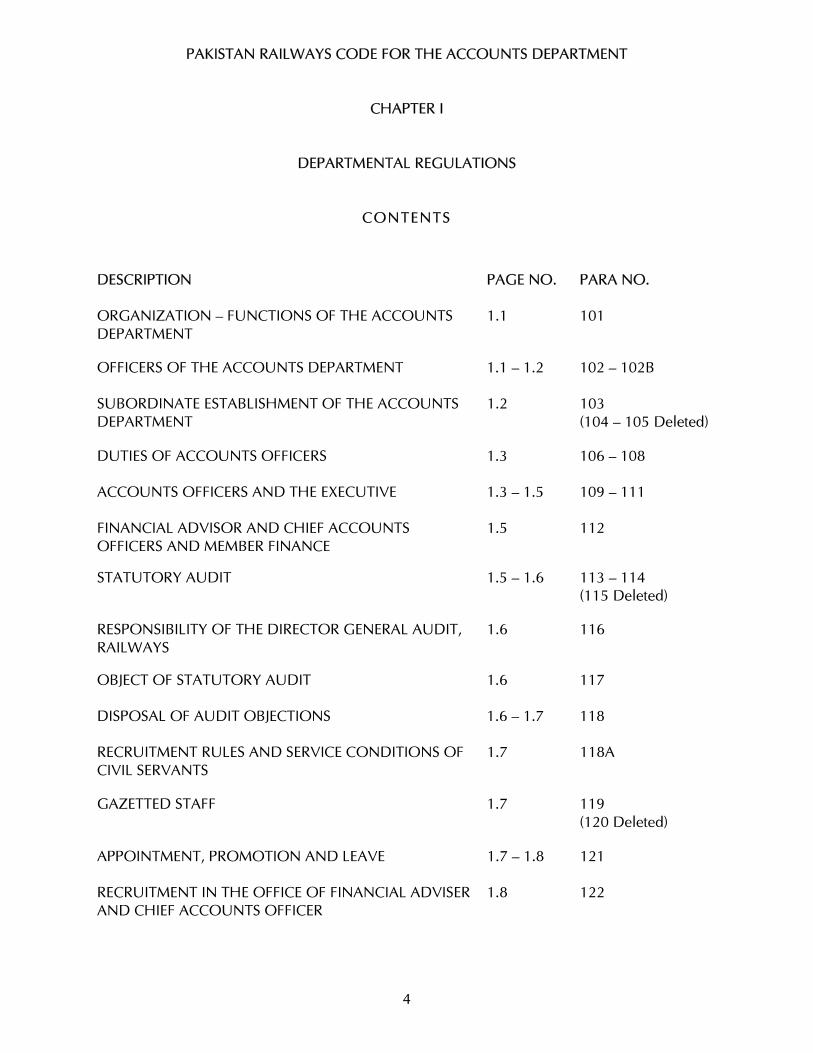

ORGANIZATION — FUNCTIONS OF THE ACCOUNTS DEPARTMENT

1.1 101

OFFICERS OF THE ACCOUNTS DEPARTMENT 1.1 — 1.2 102 — 102B

SUBORDINATE ESTABLISHMENT OF THE ACCOUNTS DEPARTMENT

1.2 103 (104 — 105 Deleted)

DUTIES OF ACCOUNTS OFFICERS 1.3 106 — 108

ACCOUNTS OFFICERS AND THE EXECUTIVE 1.3 — 1.5 109 — 111

FINANCIAL ADVISOR AND CHIEF ACCOUNTS OFFICERS AND MEMBER FINANCE

1.5 112

STATUTORY AUDIT 1.5 — 1.6 113 — 114 (115 Deleted)

RESPONSIBILITY OF THE DIRECTOR GENERAL AUDIT, RAILWAYS

1.6 116

OBJECT OF STATUTORY AUDIT 1.6 117

DISPOSAL OF AUDIT OBJECTIONS 1.6 — 1.7 118

RECRUITMENT RULES AND SERVICE CONDITIONS OF CIVIL SERVANTS

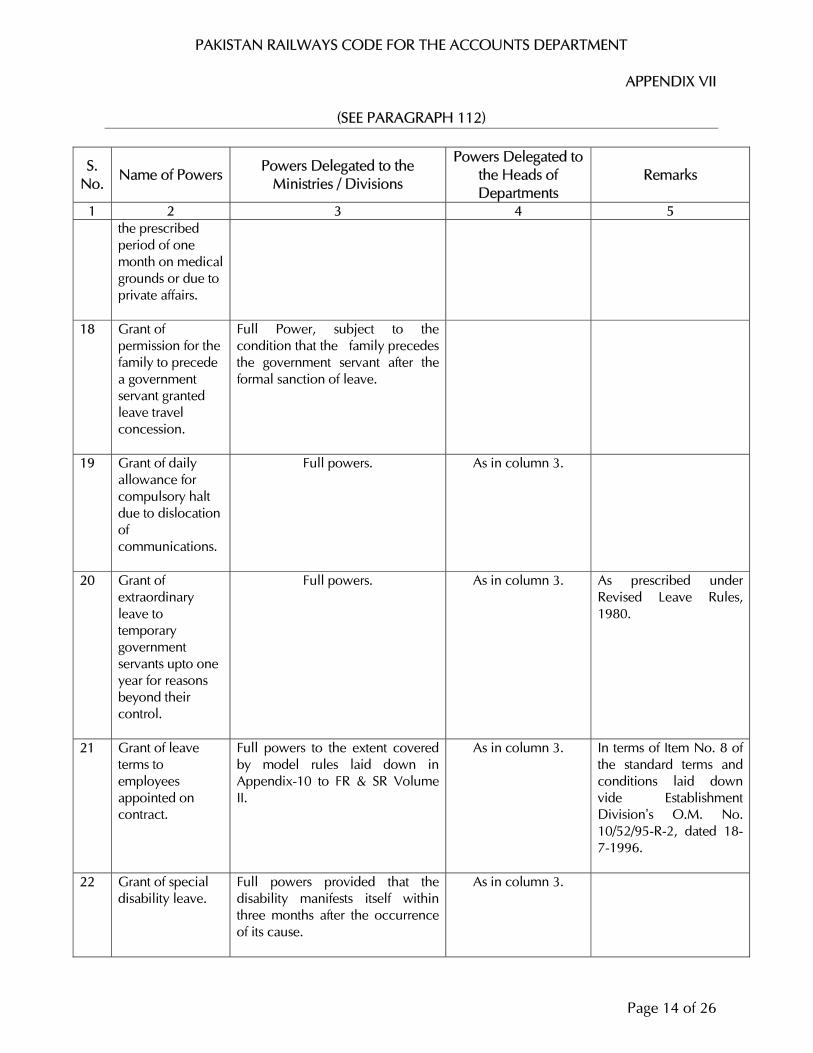

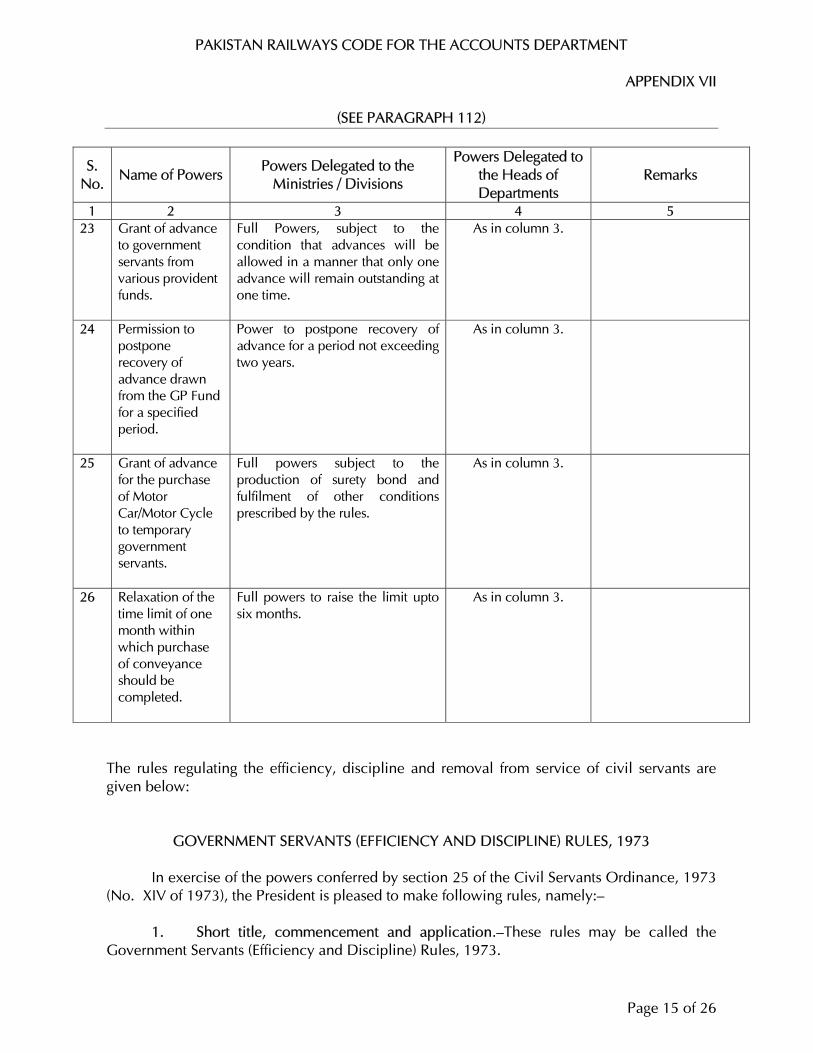

1.7 118A

GAZETTED STAFF 1.7 119 (120 Deleted)

APPOINTMENT, PROMOTION AND LEAVE 1.7 — 1.8 121

RECRUITMENT IN THE OFFICE OF FINANCIAL ADVISER AND CHIEF ACCOUNTS OFFICER

1.8 122

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

5

CONTENTS

DESCRIPTION PAGE NO. PARA NO.

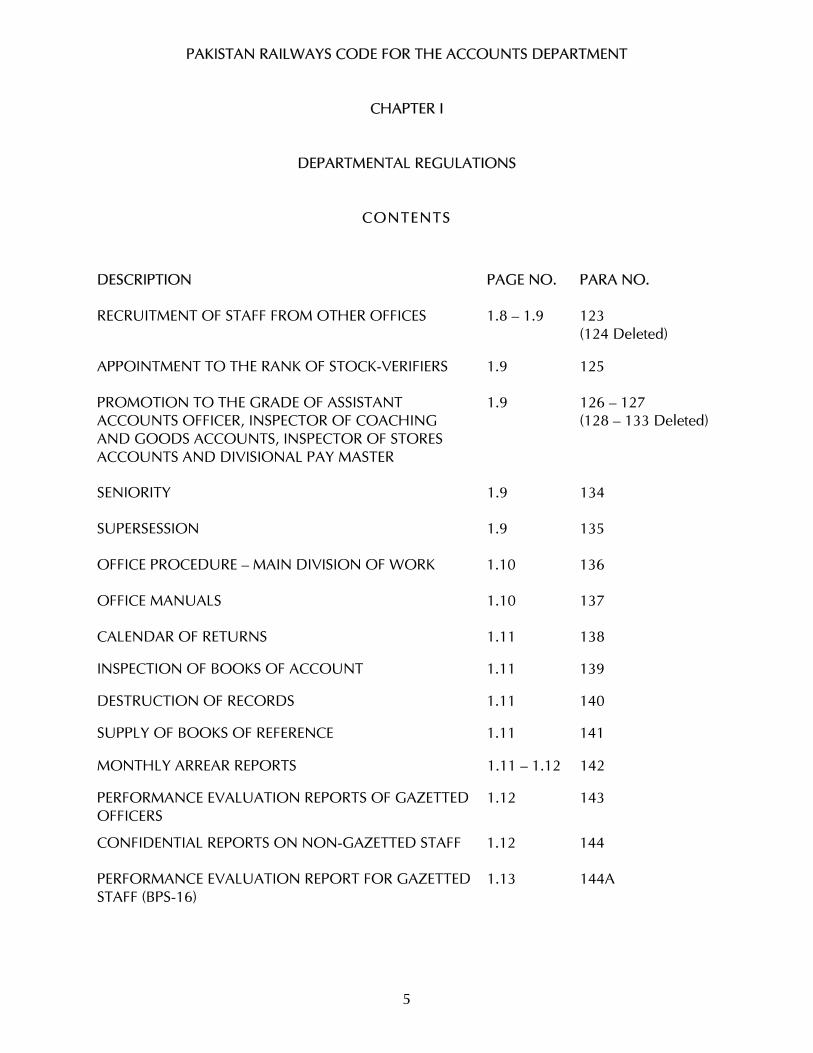

RECRUITMENT OF STAFF FROM OTHER OFFICES 1.8 — 1.9 123 (124 Deleted)

APPOINTMENT TO THE RANK OF STOCK-VERIFIERS 1.9 125

PROMOTION TO THE GRADE OF ASSISTANT ACCOUNTS OFFICER, INSPECTOR OF COACHING AND GOODS ACCOUNTS, INSPECTOR OF STORES ACCOUNTS AND DIVISIONAL PAY MASTER

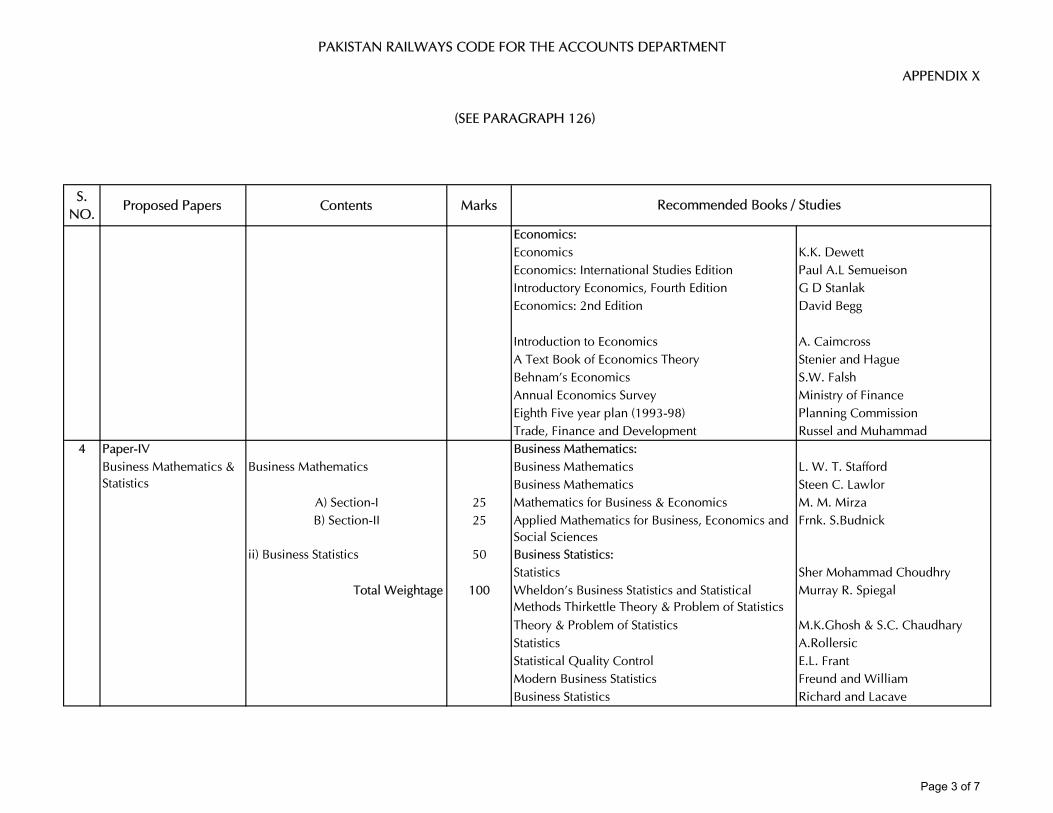

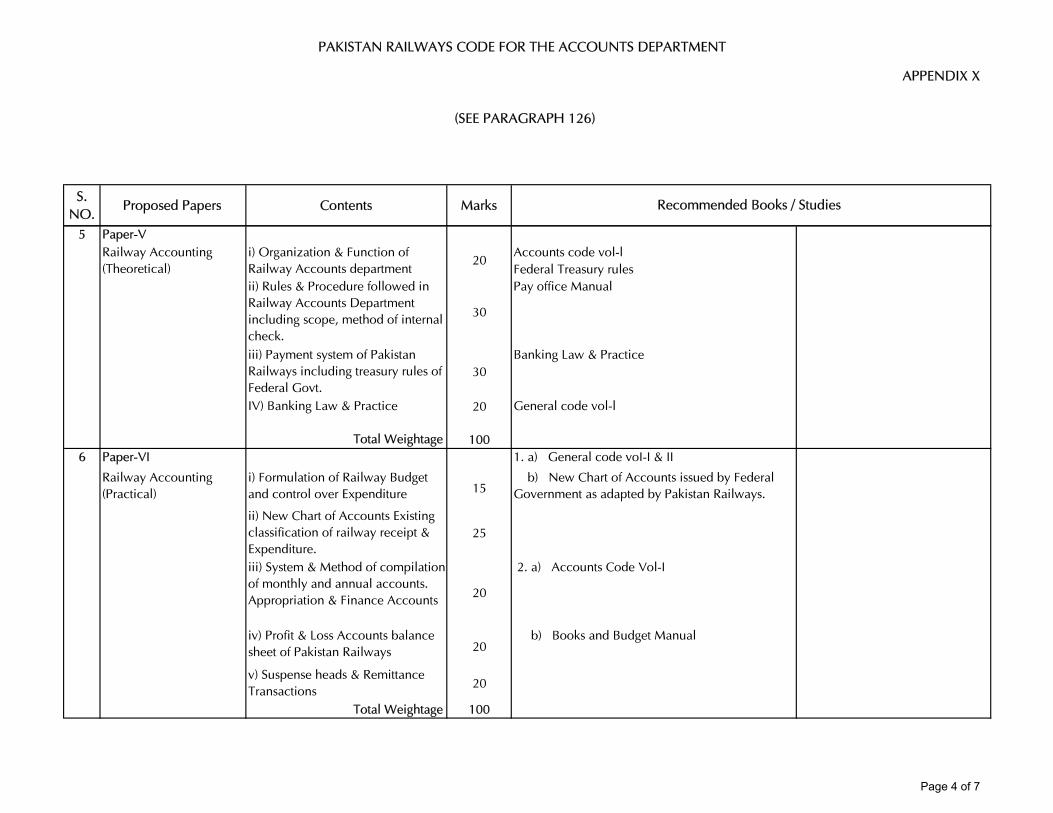

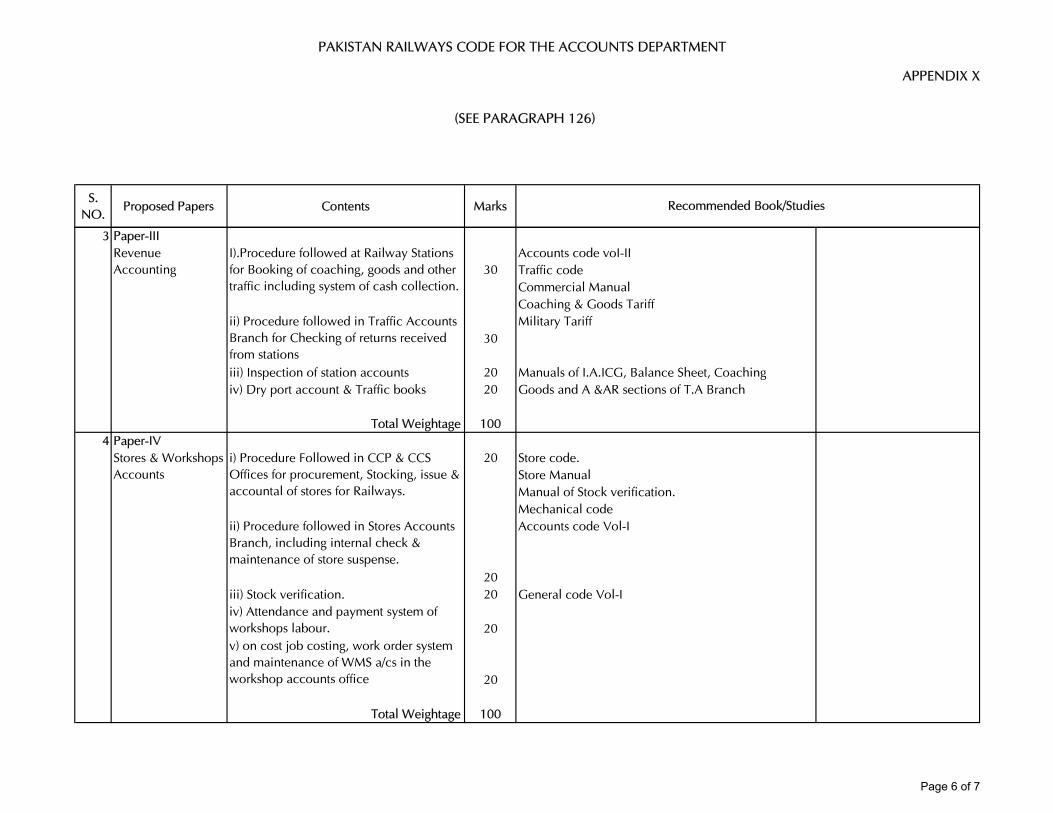

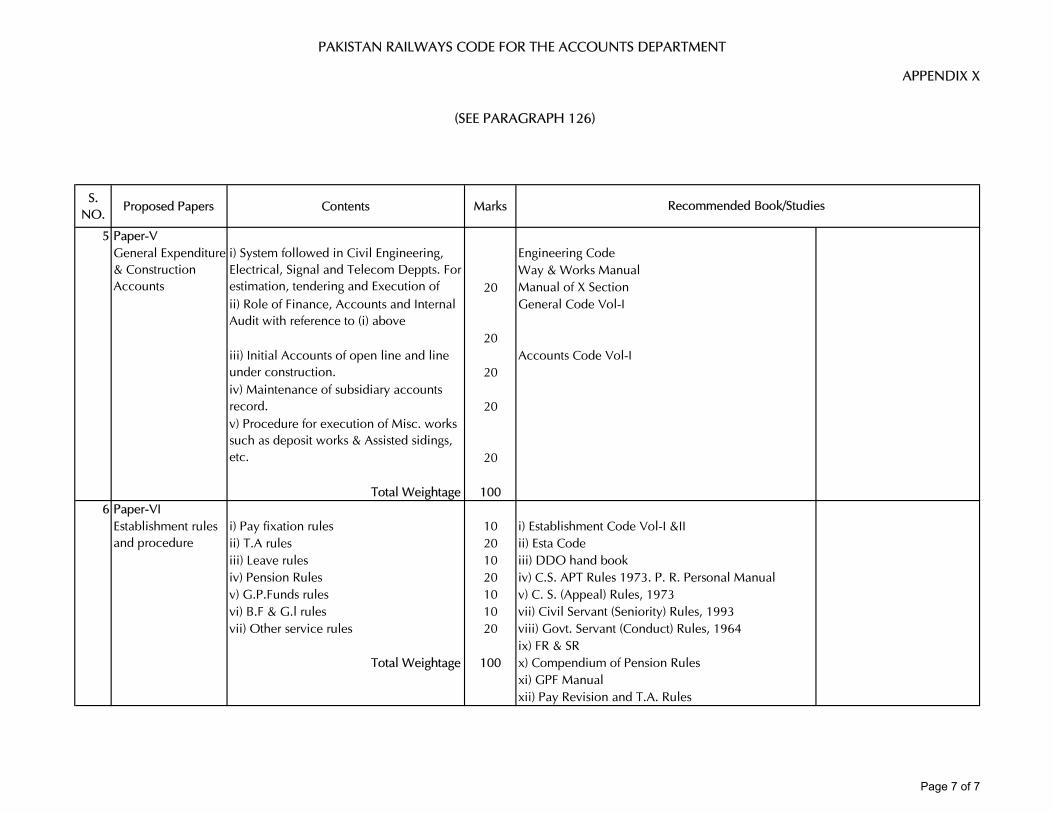

1.9 126 — 127 (128 — 133 Deleted)

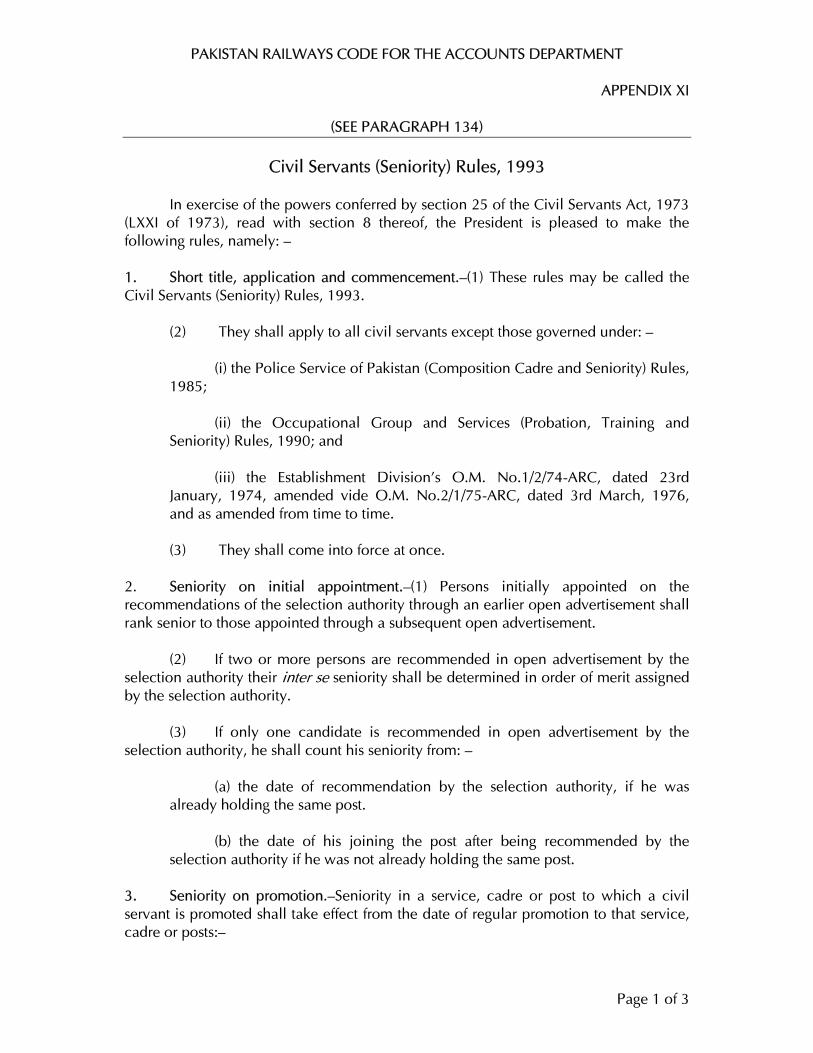

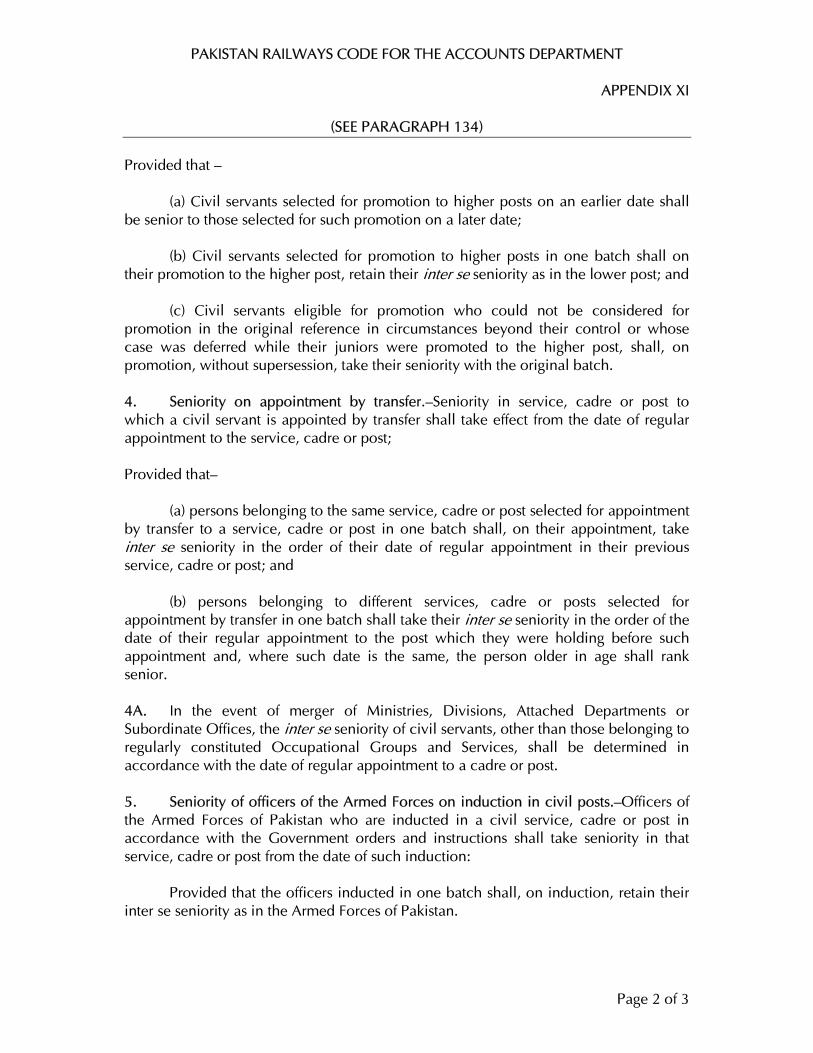

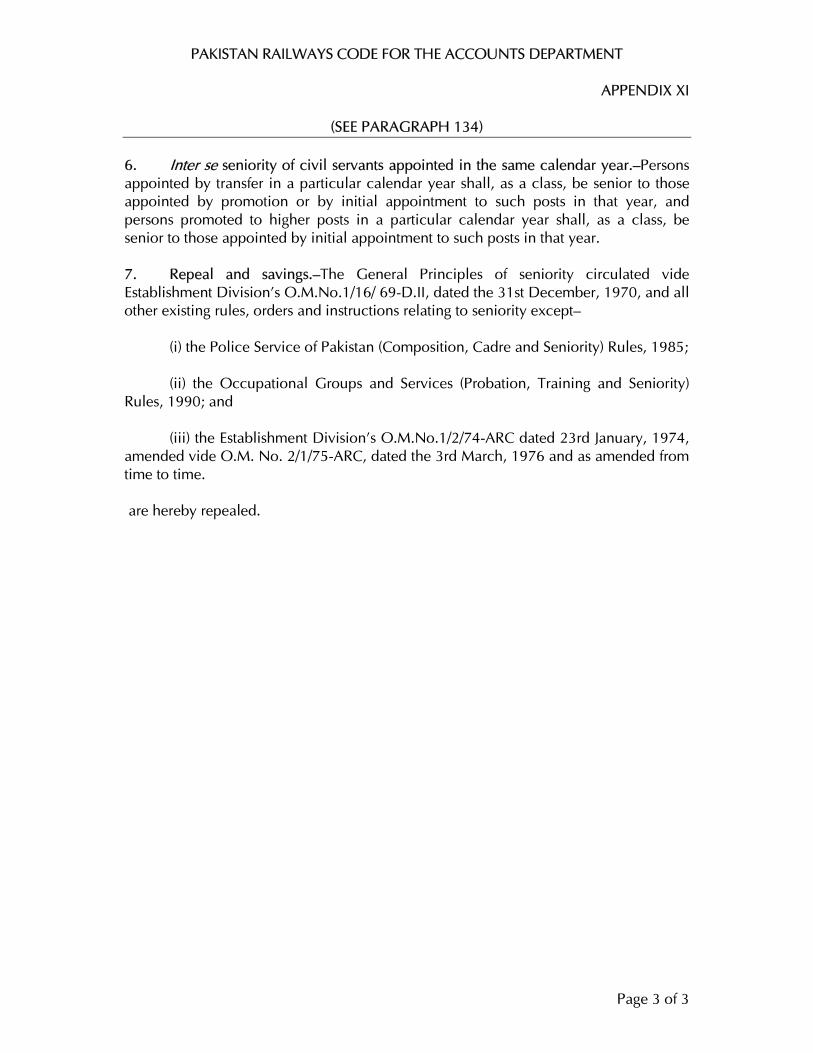

SENIORITY 1.9 134

SUPERSESSION 1.9 135

OFFICE PROCEDURE — MAIN DIVISION OF WORK 1.10 136

OFFICE MANUALS 1.10 137

CALENDAR OF RETURNS 1.11 138

INSPECTION OF BOOKS OF ACCOUNT 1.11 139

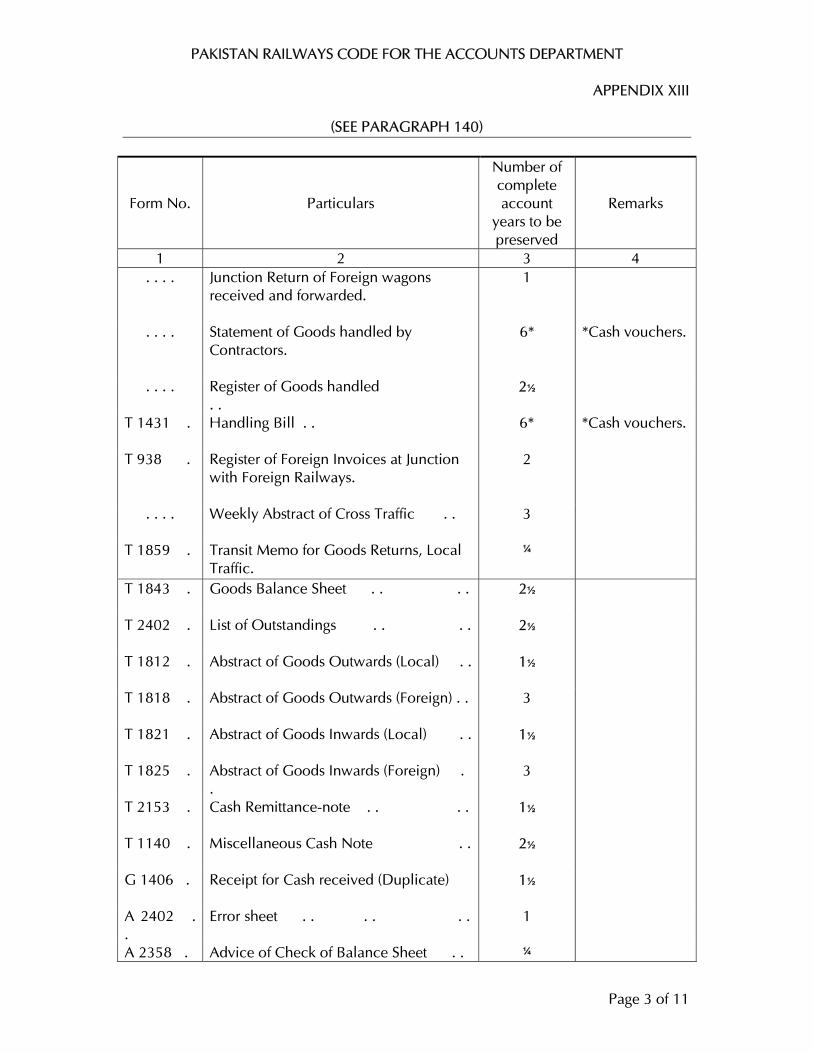

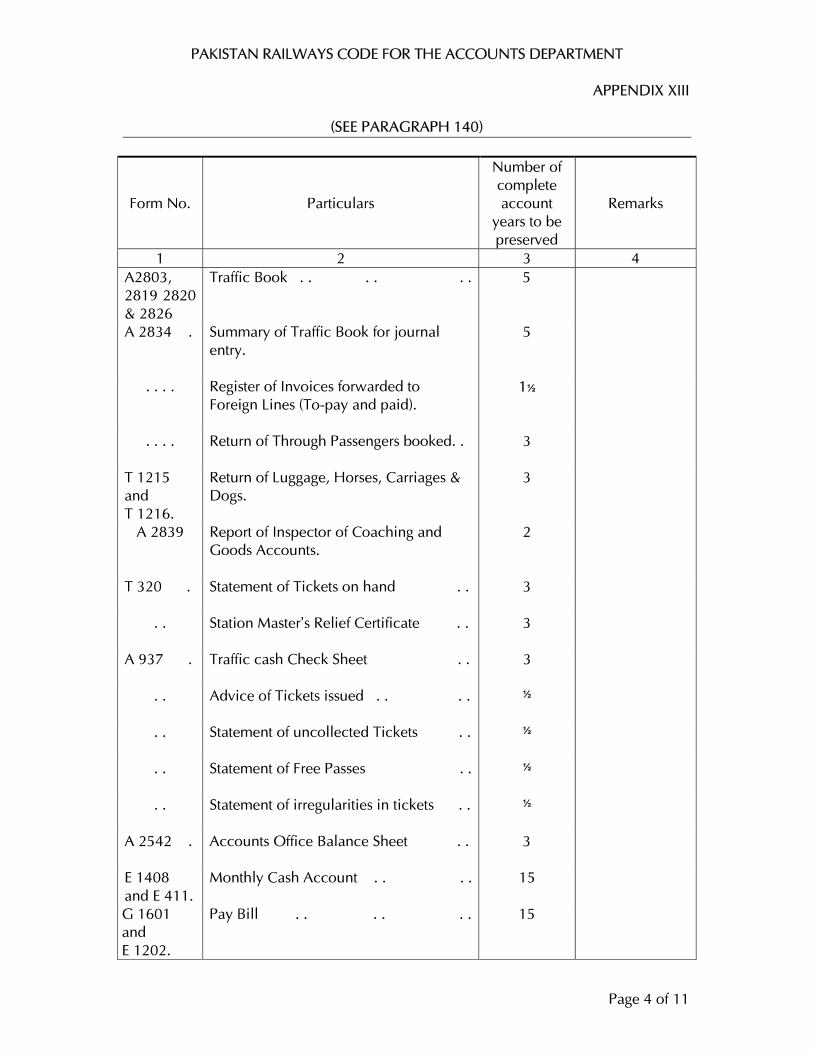

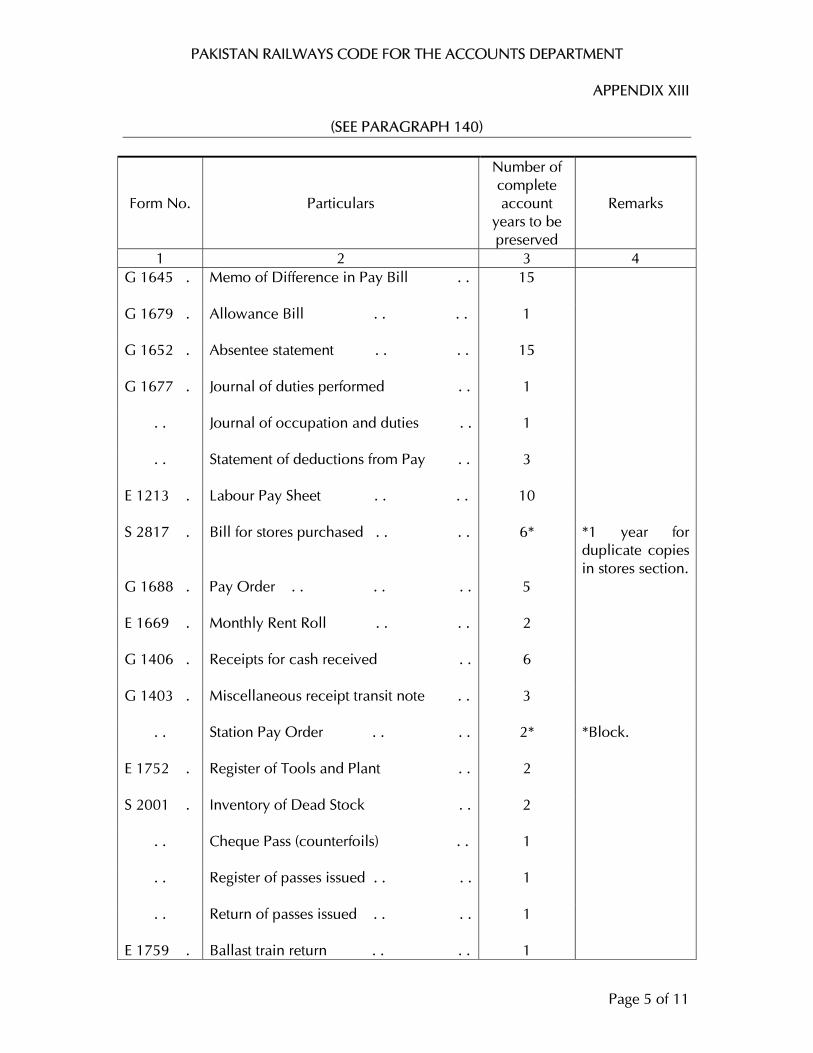

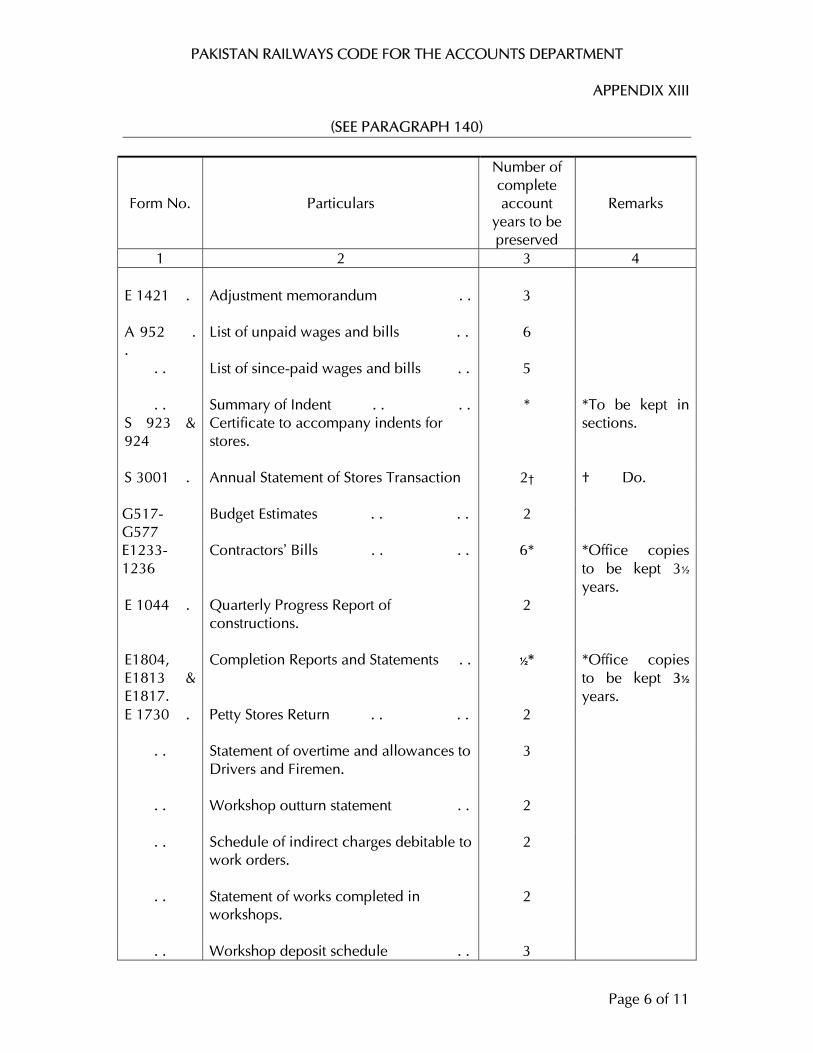

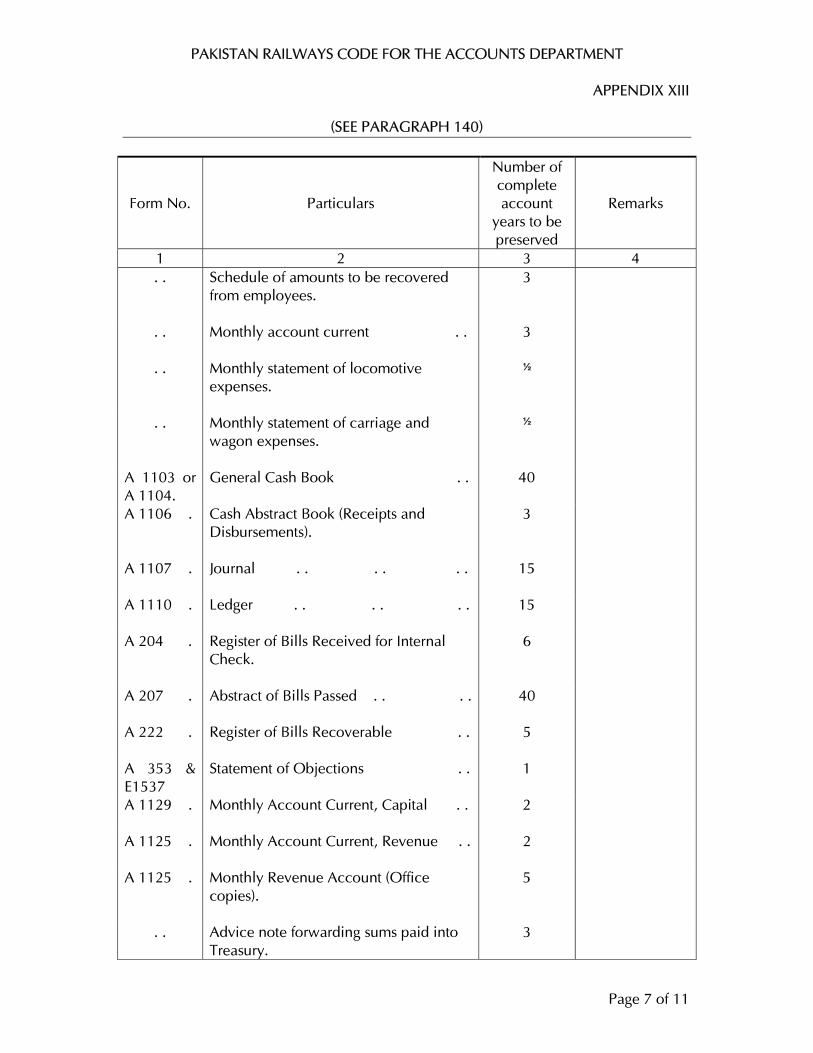

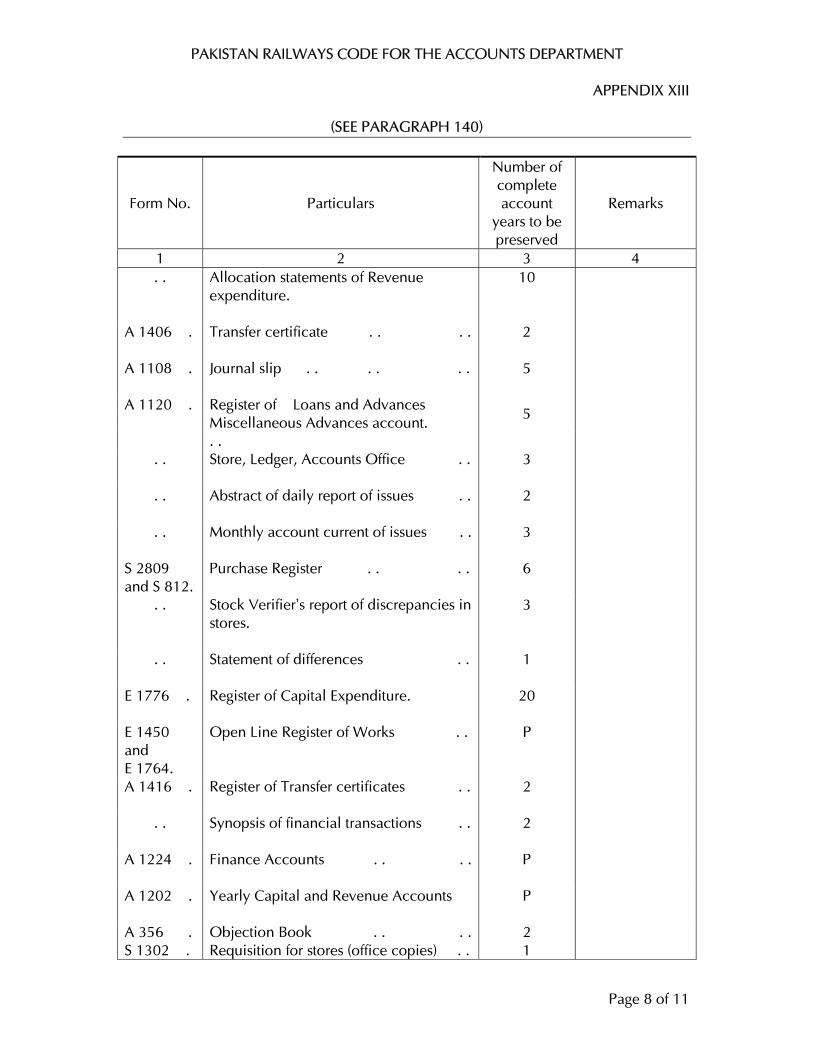

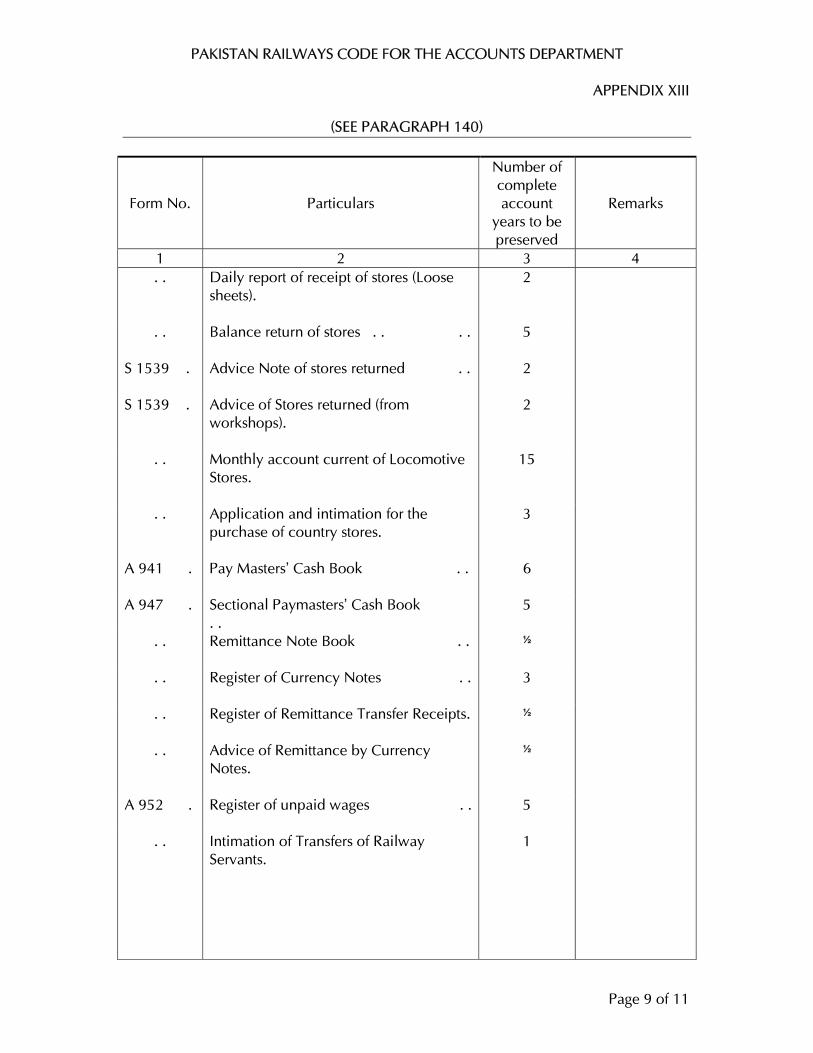

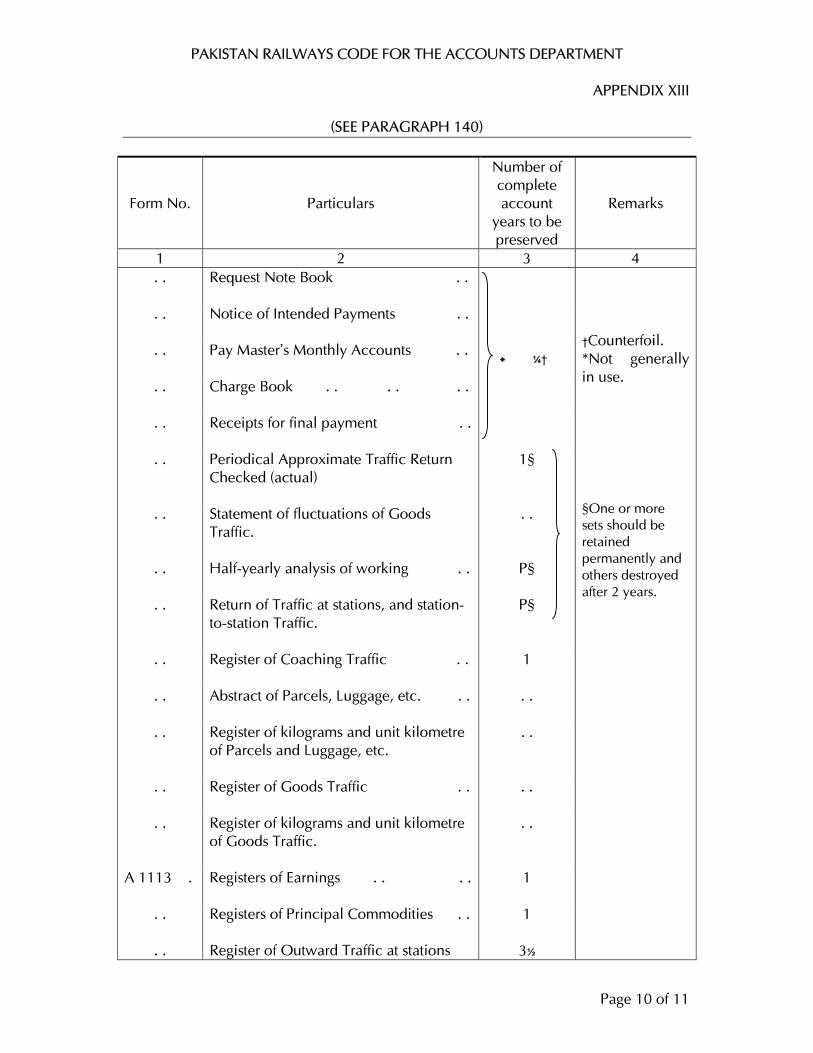

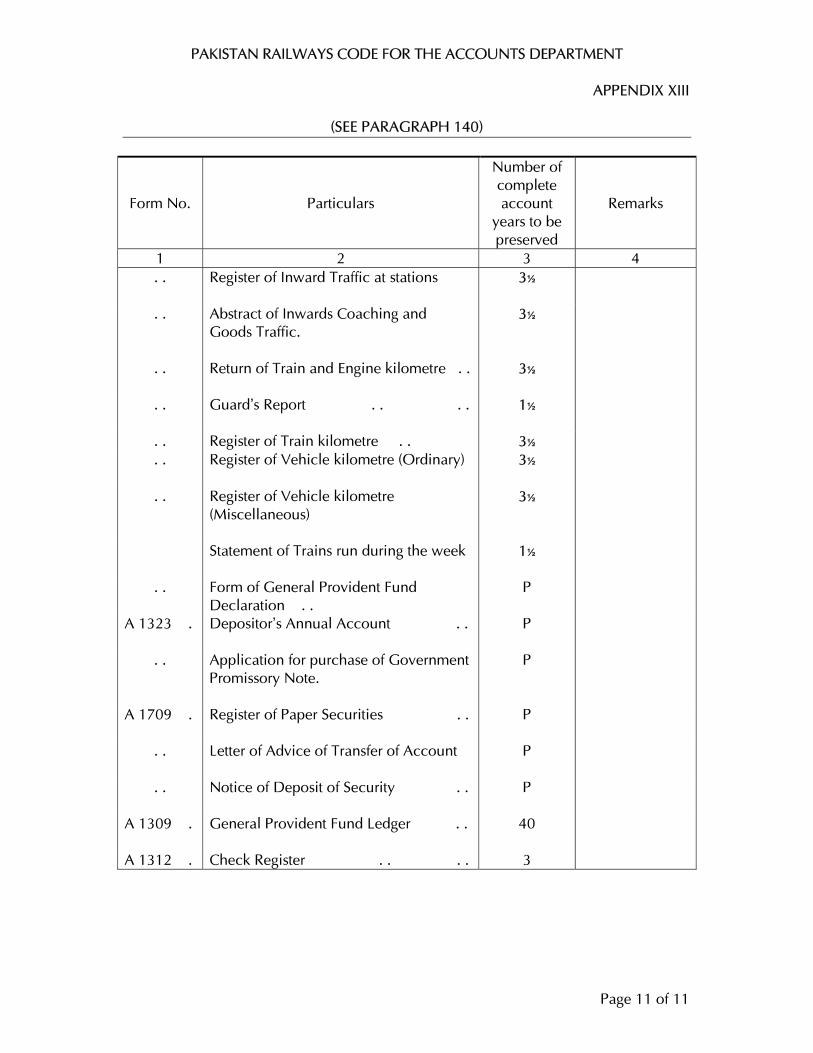

DESTRUCTION OF RECORDS 1.11 140

SUPPLY OF BOOKS OF REFERENCE 1.11 141

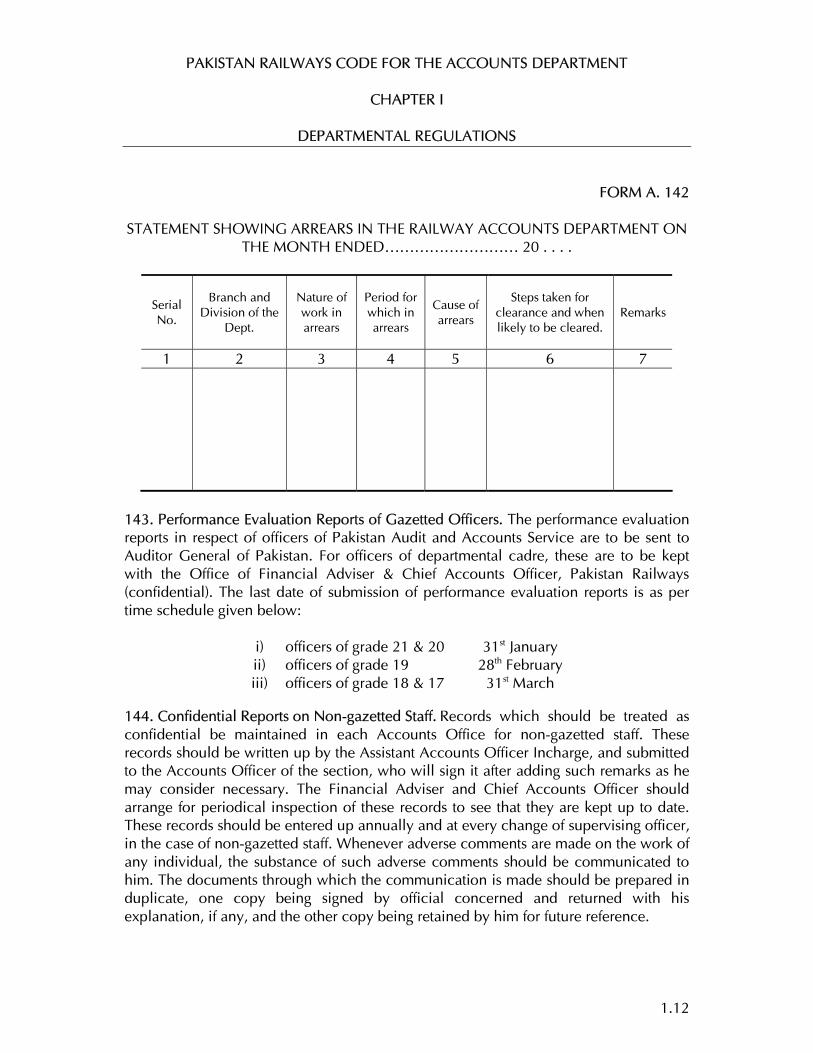

MONTHLY ARREAR REPORTS 1.11 — 1.12 142

PERFORMANCE EVALUATION REPORTS OF GAZETTED OFFICERS

1.12 143

CONFIDENTIAL REPORTS ON NON-GAZETTED STAFF 1.12 144

PERFORMANCE EVALUATION REPORT FOR GAZETTED STAFF (BPS-16)

1.13 144A

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

6

CONTENTS

DESCRIPTION PAGE NO. PARA NO.

PERFORMANCE EVALUATION REPORT FOR OFFICERS IN (BPS-17 & 18)

1.22 145

CONFIDENTIAL REPORT ON NON-GAZETTED STAFF 1.35 146

CONFIDENTIAL REPORTS ON SUBORDINATES CONSIDERED FIT FOR PROMOTION TO ACCOUNTS OFFICER

1.38 147

REGISTER OF VALUABLE AND SECRET DOCUMENTS 1.39 148

TRANSFER OF CHARGES — HANDING—OVER NOTES 1.39 149 — 150

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.1

A. ORGANIZATION

101. Functions of the Accounts Department. This Department of Pakistan Railways is mainly responsible for:

(a) the internal check of transactions affecting the receipts and expenditure of Pakistan Railways; (b) the prompt settlement of proper claims against Pakistan Railways; (c) keeping the accounts of Pakistan Railways in accordance with the prescribed rules; (d) helping the administration and executive officers of Pakistan Railways with advice whenever required or found necessary, in all matters involving Pakistan Railways finance; (e) Generally discharging other management accounting functions such as providing financial data for management reporting, assisting inventory management, participation in purchase/contracting decisions and surveys for major schemes in accordance with the relevant rules and orders; and (f) Seeing that there are no financial irregularities in the transactions of Pakistan Railways.

102. Officers of the Accounts Department. Member Finance heads the Accounts Department of Pakistan Railways and reports to Chairman / Secretary Railways. Member Finance is assisted by Director—FIS/MIS, Chief Cost Accounts Officer, Financial Adviser & Chief Accounts Officer—Pakistan Railways, Financial Adviser & Chief Accounts Officer—Revenue through Additional General Manager—Finance, and Financial Adviser & Chief Accounts Officer—Manufacturing & Services Unit and Director—Finance & Budget. Subordinate to the heads of the Accounts Department are various accounts officers attached to the Divisions, Workshops, Stores, Depots, and Construction Projects of Pakistan Railways. For the sake of brevity all accounts officers of Pakistan Railways, including the heads of the Accounts Department are referred to hereafter as “Accounts Officer(s)”. Where, however, it is necessary to refer particularly to the heads of the Accounts Department of Pakistan Railways, the term “Financial Adviser and Chief Accounts Officer,” has been used. The term “Accounts” has, in some places, been used to denote the Accounts Department.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.2

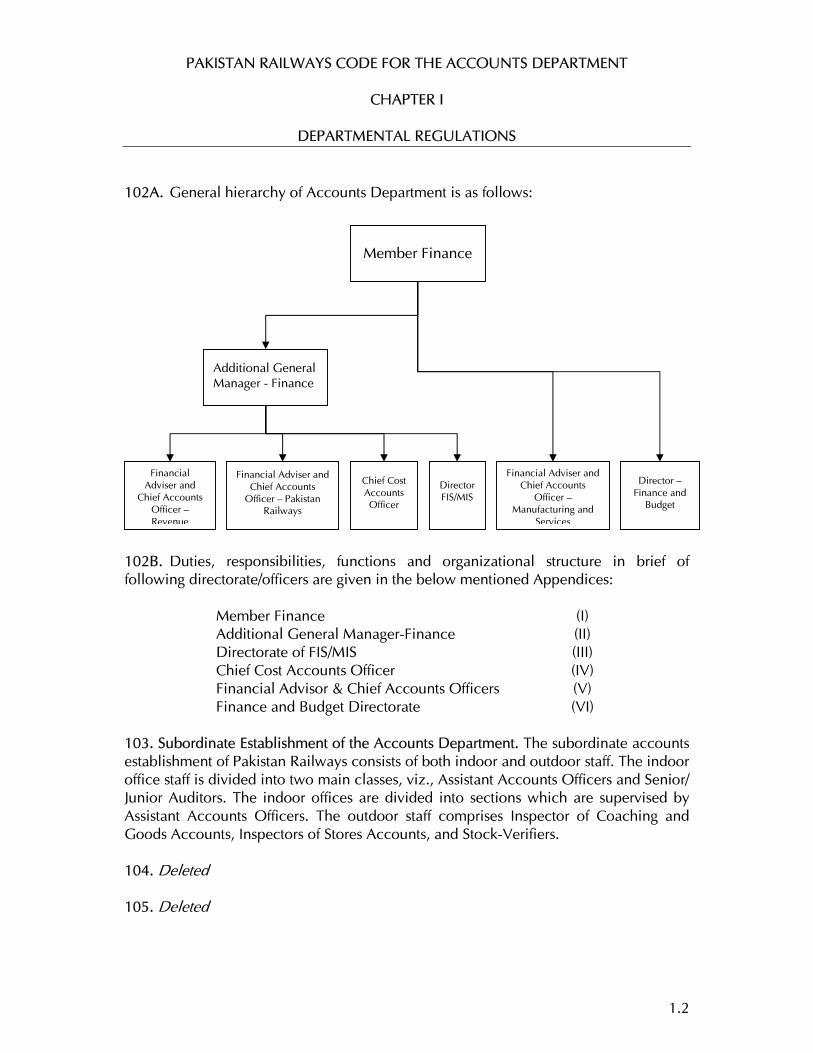

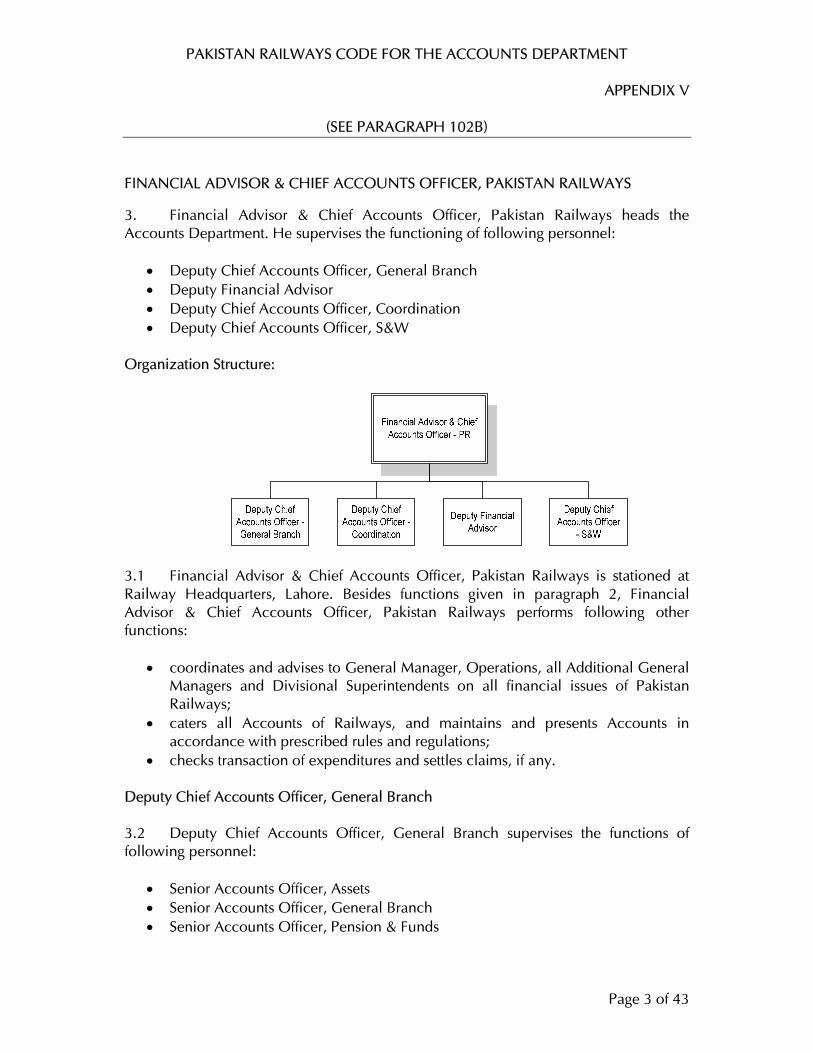

102A. General hierarchy of Accounts Department is as follows:

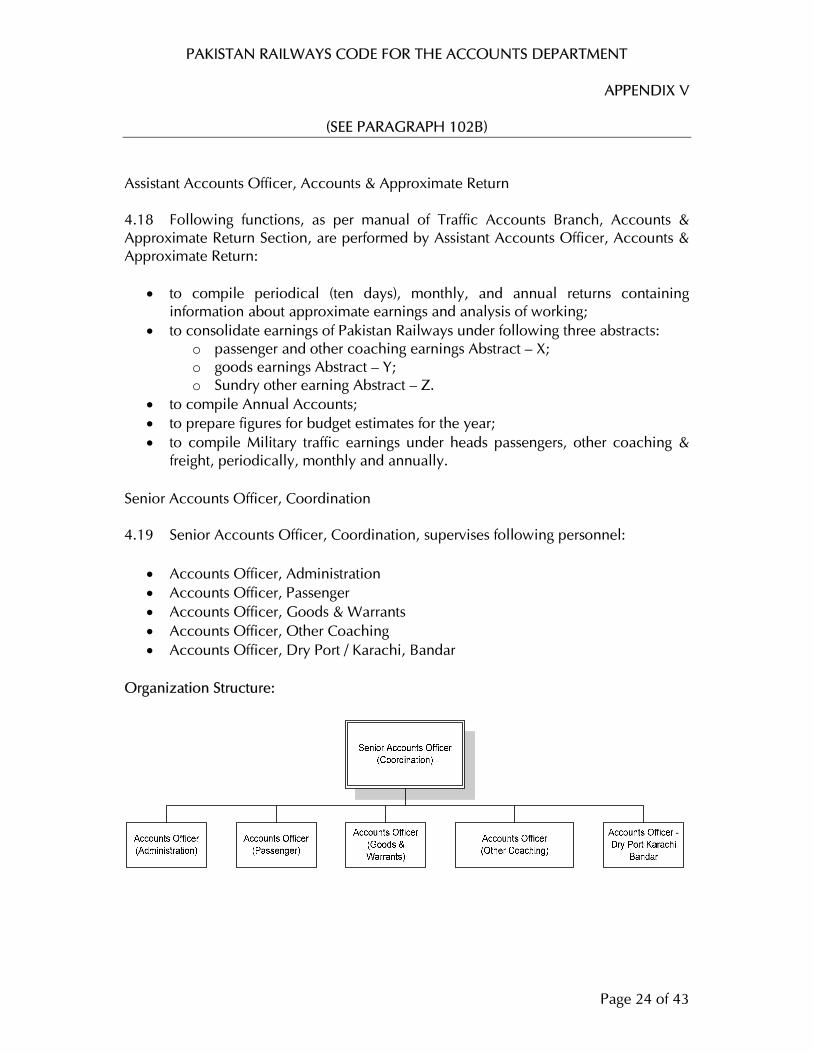

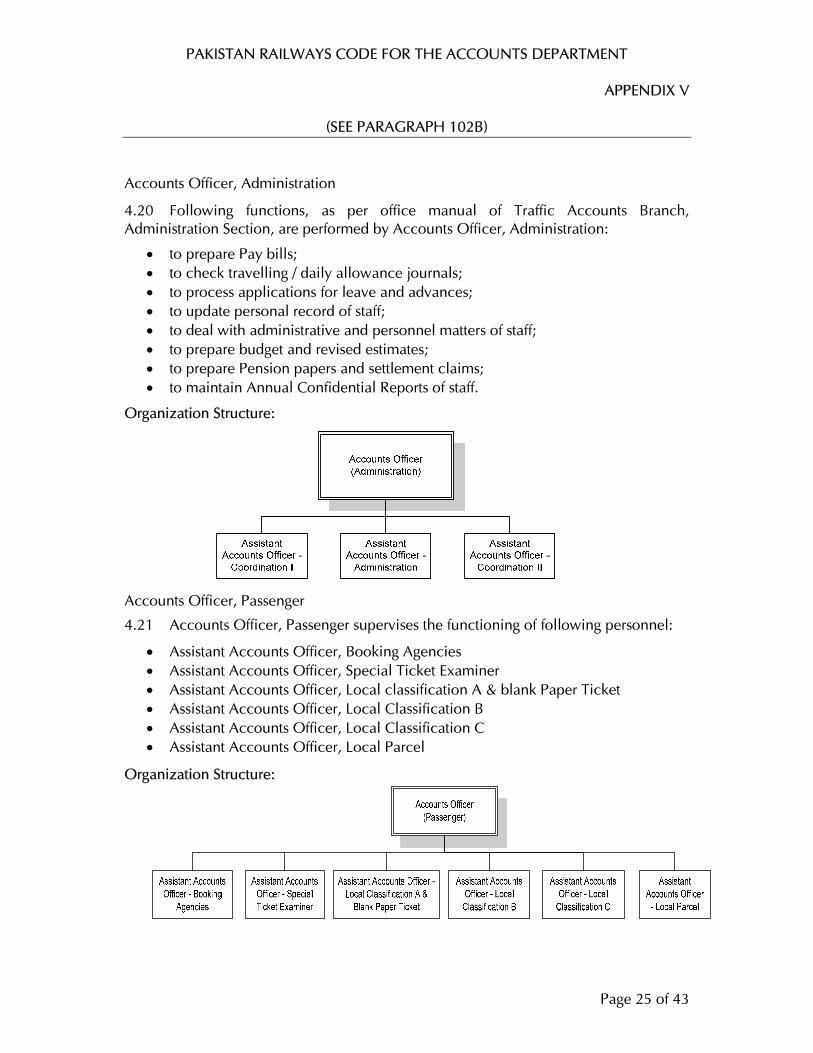

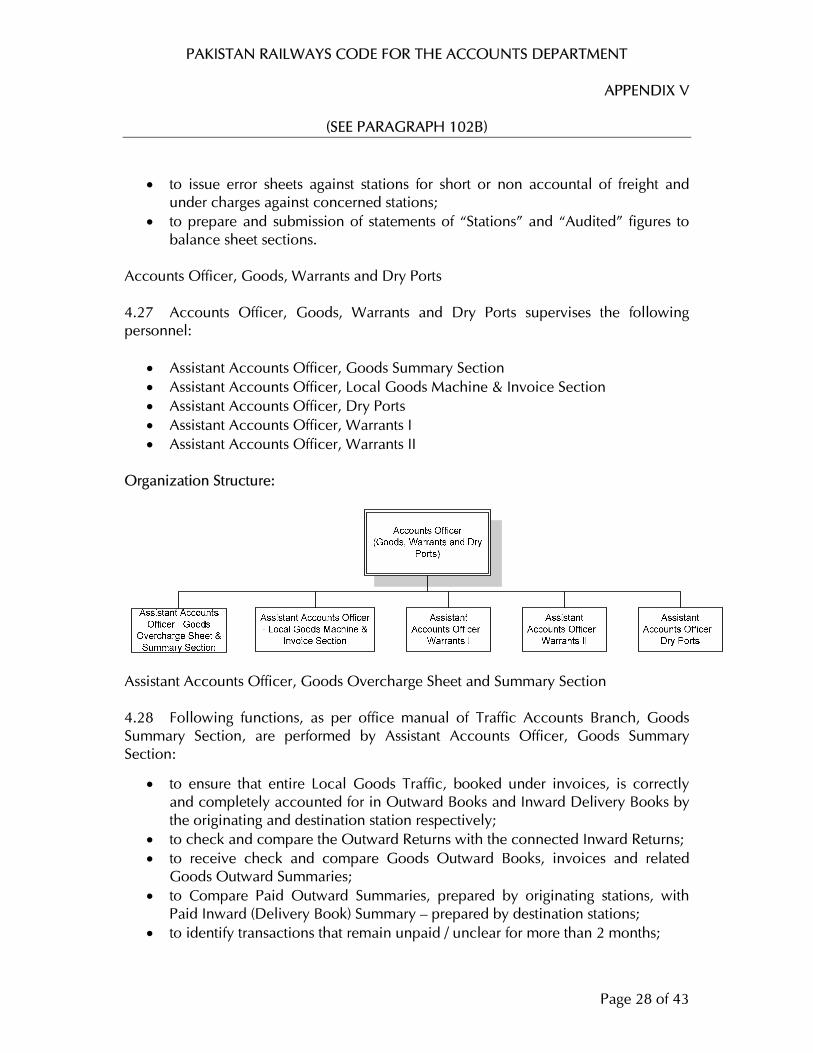

102B. Duties, responsibilities, functions and organizational structure in brief of following directorate/officers are given in the below mentioned Appendices:

Member Finance (I) Additional General Manager-Finance (II) Directorate of FIS/MIS (III) Chief Cost Accounts Officer (IV) Financial Advisor & Chief Accounts Officers (V) Finance and Budget Directorate (VI)

103. Subordinate Establishment of the Accounts Department. The subordinate accounts establishment of Pakistan Railways consists of both indoor and outdoor staff. The indoor office staff is divided into two main classes, viz., Assistant Accounts Officers and Senior/ Junior Auditors. The indoor offices are divided into sections which are supervised by Assistant Accounts Officers. The outdoor staff comprises Inspector of Coaching and Goods Accounts, Inspectors of Stores Accounts, and Stock-Verifiers.

104. Deleted

105. Deleted

Member Finance

Additional General Manager - Finance

Director FIS/MIS

Chief Cost Accounts Officer

Financial Adviser and Chief Accounts

Officer —Manufacturing and

Services

Financial Adviser and

Chief Accounts Officer — Revenue

Director — Finance and

Budget

Financial Adviser and Chief Accounts

Officer — Pakistan Railways

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.3

106. Duties of Accounts Officers. An Accounts Officer may not:

(a) without the permission of his immediate superior, reverse any deliberate or important orders, passed by an officer who preceded him in office; (b) propose increases in department other than his own; (c) on any account, join in protesting against any retrenchment or economy which a competent authority may order; (d) suggest expedients for the evasion of the natural operations of a rule when reporting on claims of pension or allowances of any kind, his duty being merely to report how a claim is affected by the rules; (e) advise upon any questions relating to pensionary claims until Pakistan Railways servant actually retires, or is about to retire from the service, except upon a reference from the Member Finance.

107. In making proposals for economy or improvement affecting other departments of Pakistan Railways, the Accounts Officer should always consult the executive officers of the department, and such proposals, should as a rule, come before the competent executive authority through the departmental officers. But the Financial Adviser and Chief Accounts Officers are empowered, if they think it necessary, to make such references direct to the competent authority.

108. In addition to the prescribed returns and accounts, the Accounts Officer should furnish the executive officers with such other accounts and returns as may be called for. Any statistical or other information required by the executive officers which can be obtained from the records of the accounts office should also be promptly supplied.

109. Accounts Officers and the Executive. The head of Pakistan Railways administration, referred to hereafter as the General Manager, and the various executive officers subordinate to him are responsible for the construction, maintenance and operations of Pakistan Railways. In the proper and legitimate discharge of their responsibilities the executive officers are authorized to incur expenditure within the limits of their financial powers. All claims arising out of such expenditure are checked (in accordance with the prescribed rules), on behalf of the Administration by the Accounts Officer, who arranges to liquidate claims which are found to be in order. In functioning thus and in giving financial advice to the executive, the Accounts Officer acts solely in the interest of the executive officers. The Accounts Officer’s relations with executive should therefore, be that of a friendly critic. The Accounts Officer should accordingly avoid all unnecessary objections and assist the executive officers to devise and follow legitimate means toward obtaining legitimate ends.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.4

110. In cases where an Accounts Officer is unable to accept as proper any orders of an executive authority or any claims arising therefrom, he should bring to the notice of such executive authority the nature of the impropriety or irregularity and suggest the proper and regular course of action under the extant rules and orders. In the event of a disagreement between the Accounts Officer and the executive, the following procedure should be followed:

(a) If the disagreement is between an executive officer other than the General Manager and an Accounts Officer other than the Financial Advisor and Chief Accounts Officer, the Accounts Officer should furnish a short note of his objection to the executive officer and ask him to obtain the decision of the General Manager. He should at the same time furnish a copy of his note to the Financial Adviser and Chief Accounts Officer.

(b) If the matter is settled to the satisfaction of the Financial Adviser and Chief Accounts Officer he will issue the necessary orders to the subordinate Accounts Officer. If, however, the General Manager and the Financial Adviser and Chief Accounts Officer are unable to come to an agreement, the former should obtain the orders of the Ministry of Railways (Railway Board), and the latter should act on the Ministry of Railways’ (Railway Board) orders which will be furnished to him by the General Manager (vide paragraph 302).

(c) Should the General Manager be unwilling to refer to the Ministry of Railways (Railway Board) for orders any point on which there is disagreement between himself and the Financial Adviser and Chief Accounts Officer, the latter should refer the point to the Member Finance for orders.

(d) The above procedures will apply mutatis mutandis in cases where the Financial Advisor and Chief Accounts Officer himself (without the intervention of his subordinate officers) considers that any order of an executive officer or any claims arising therefrom irregular or improper in internal check.

111. In matters of interpretation of rules and obtaining sanction of the Ministry of Railways (Railway Board) or higher authorities, the duty of the Accounts Officer is to address the executive officer concerned and ask him to obtain the orders of the Ministry of Railways (Railway Board). In such cases, the opinion of the Accounts Officer should be furnished to the executive officer in the form of a short note, which should be included verbatim in the report made by the General Manager to the Ministry of Railways (Railway Board) for orders. When the matter is really very urgent, as for instance, when delay in the issue of orders by the Ministry of Railways (Railway Board) may involve a serious financial loss to Pakistan Railways or dislocation of business or when a financial irregularity or defect in the working of a department of Pakistan

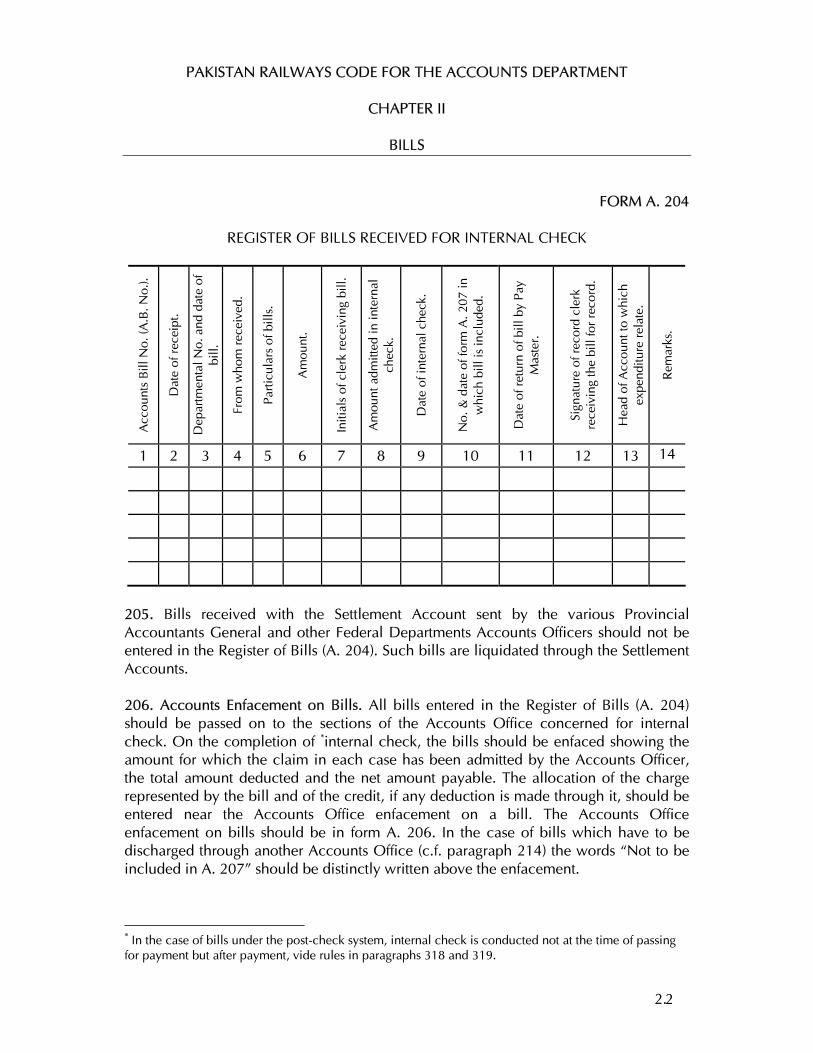

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

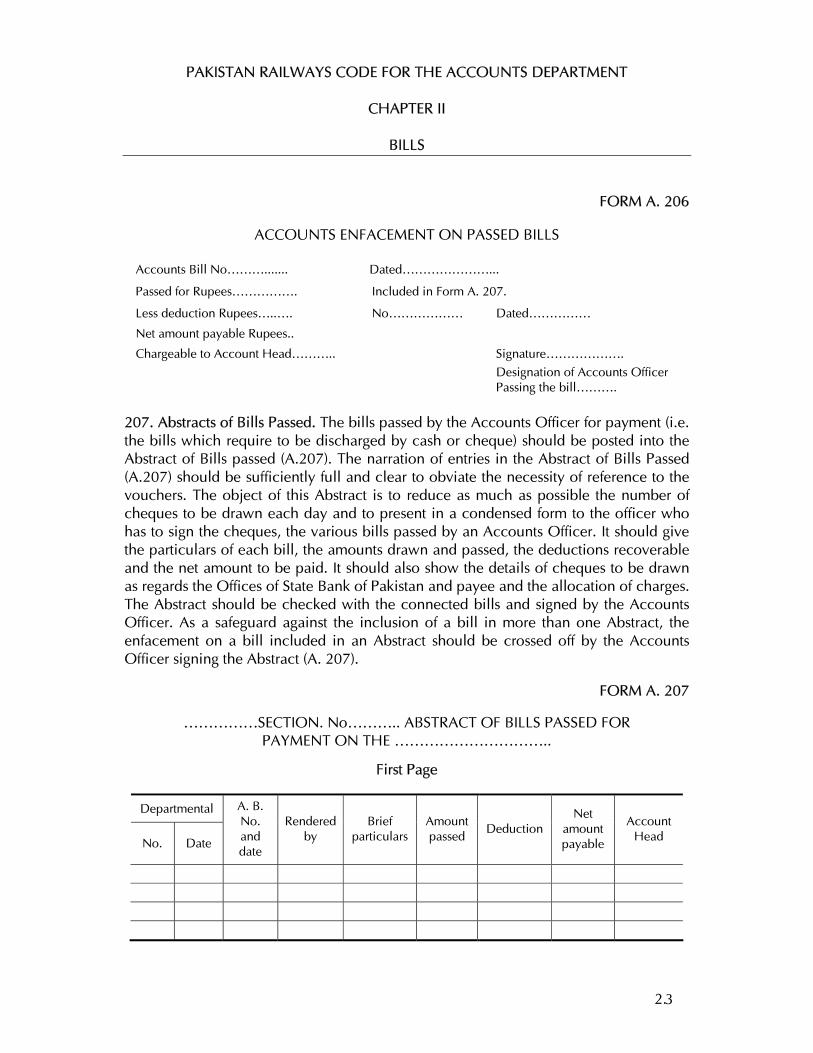

DEPARTMENTAL REGULATIONS

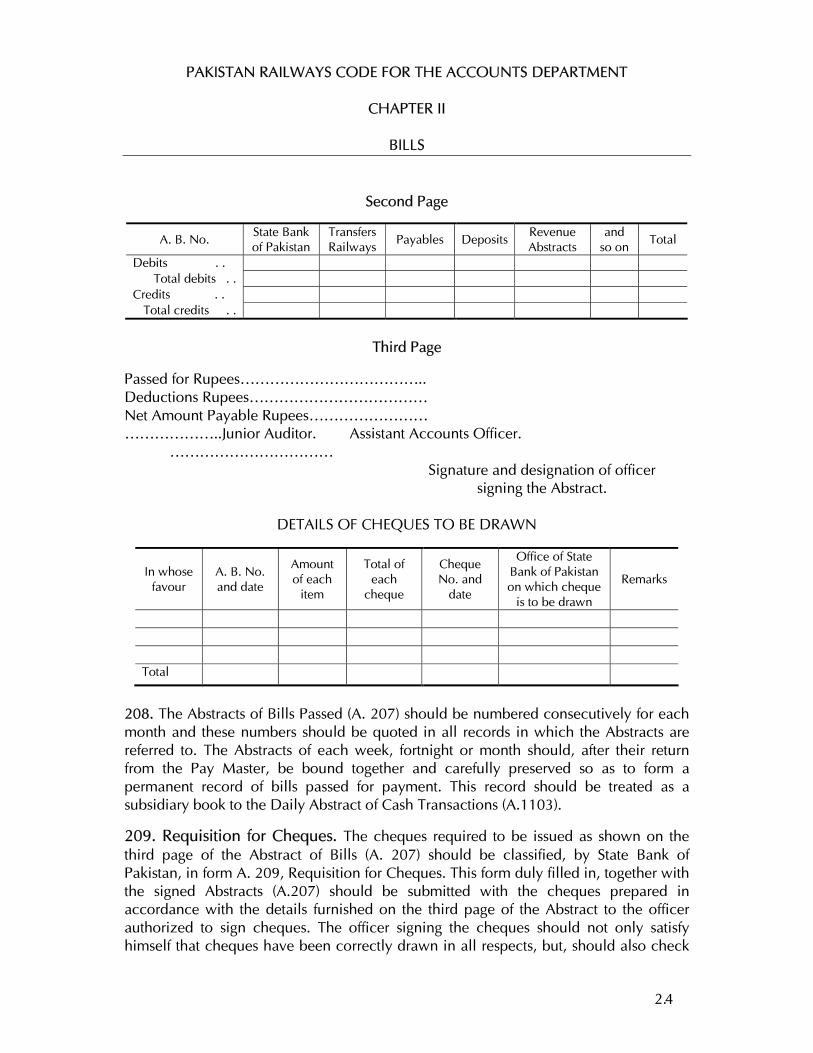

1.5

Railways has to be promptly brought to the notice of the Ministry of Railways (Railway Board), the Financial Adviser and Chief Accounts Officer may, after addressing the General Manager, send a copy of his note to the Member Finance for information with an explanation of the urgency of the case and a request for the issue of early orders by the Ministry of Railways (Railway Board). In all such cases the Financial Adviser and Chief Accounts Officer should await the orders of the Ministry of Railways (Railway Board).

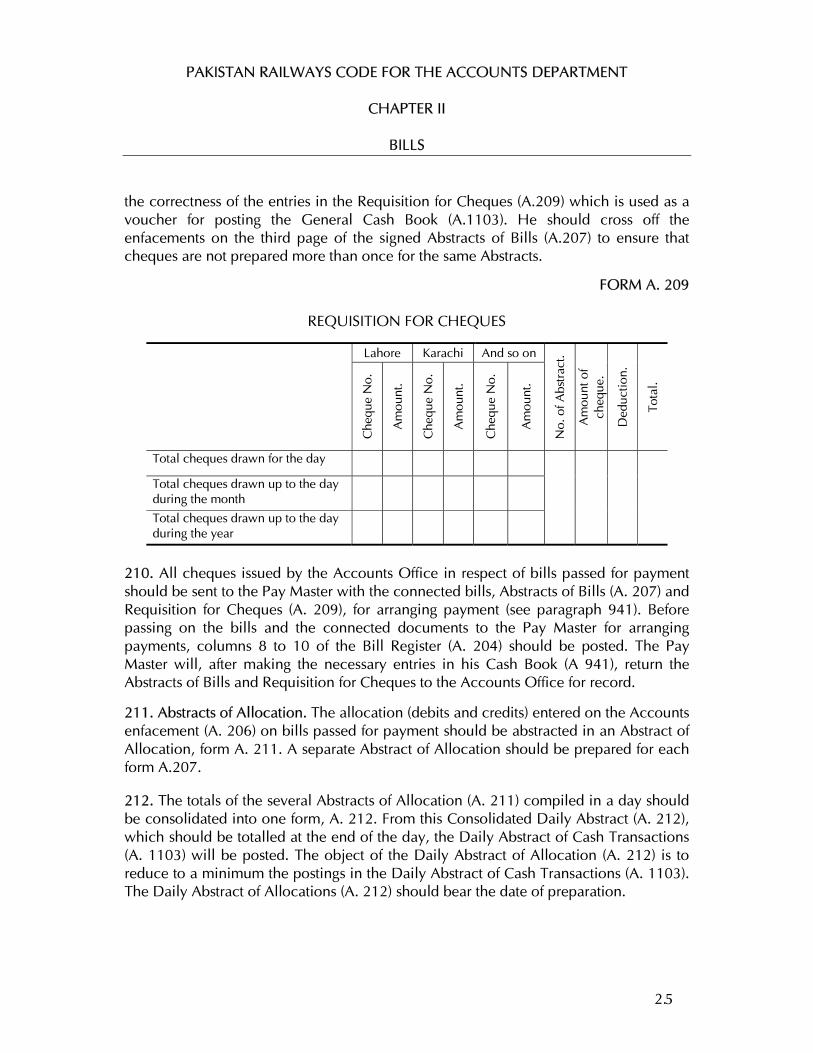

112. Financial Adviser and Chief Accounts Officers and Member Finance. Member Finance is responsible for the compilation of the whole of the accounts relating to the receipts and expenditure under the heads of accounts prescribed in Appendix XVI. In discharge of this responsibility he will issue instructions to the Financial Adviser and Chief Accounts Officers relating to the preparation and submission of the accounts and returns required by him, and it is the duty of the Financial Adviser and Chief Accounts Officers to carry out such instructions. The financial powers delegated to the Ministry and the heads of the Departments (Financial Advisor and Chief Accounts Officers in case of Pakistan Railways Accounts Department) are given in Appendix VII to this Code. 113. Statutory Audit. The Auditor General of Pakistan is the final audit authority in Pakistan. His duties and powers as regards audit are set out in “Auditor-General’s (Functions, Powers and Terms and Conditions of Service) Ordinance, 2001” (Appendix VIII) issued under Article 169 of the Constitution of Islamic Republic of Pakistan, 1973 as amended from time to time. Under Article 169 of the Constitution of Islamic Republic of Pakistan the Auditor General of Pakistan is responsible for the audit of the accounts of the Pakistan Railways but has no responsibility for the compilation of such accounts. However, compilation of accounts is the responsibility of Controller General of Accounts through Financial Advisor and Chief Accounts Officer. The form in which the accounts of the Pakistan Railways should be kept and changes in Chart of Accounts affecting the recording of expenditure in the Finance Accounts, Appropriation Accounts, Civil Accounts and Financial Statements are, however, subject to his approval as required under Article 170 of the Constitution of Islamic Republic of Pakistan. He may also require such compiled accounts to be submitted to him to carry out his statutory obligations.

114. In all matters relating to the audit of Pakistan Railways accounts, the Auditor General of Pakistan is assisted by the Director General Audit, Railways. Subordinate to the Director General Audit, Railways are the Audit Officers. It is the duty of these officers to audit the accounts of the Pakistan Railways. These Officers have been referred to in the rest of this Code as “Audit Officers” or “Audit”. Where, however, it is necessary to refer to the head of the Statutory Audit Office, the term “Director General Audit, Railways” has been used.

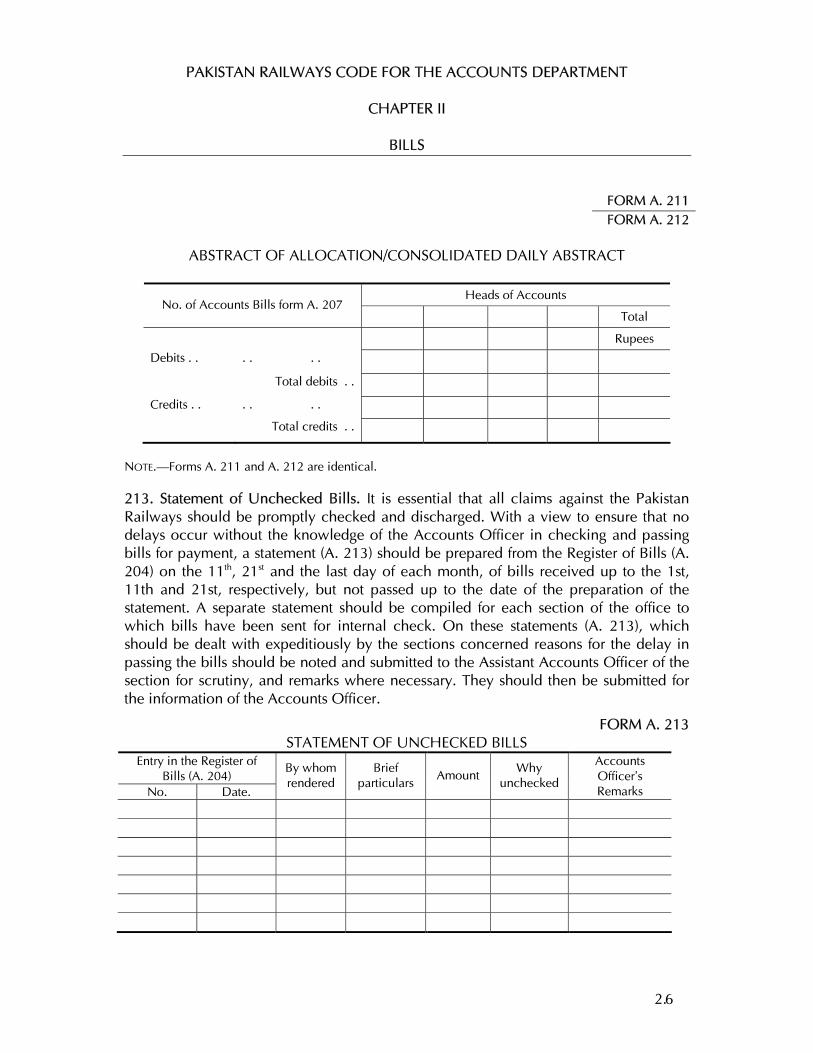

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.6

115. Deleted.

116. The responsibility of the Director General Audit, Railways for the audit of accounts is briefly as follows:

(a) to audit all expenditure from the Consolidated Fund and to ascertain whether the moneys shown in the accounts as having been disbursed were legally available for and applicable to, the service or purpose to which they have been applied or charged and whether the expenditure conforms to the authority which governs it; (b) in respect of receipts, it includes receipts of Pakistan Railways, whether under construction or open to traffic including receipts relating to accounts of manufacture; (c) it includes stores and stock accounts to the extent prescribed by the Auditor General of Pakistan and the Director General Audit, Railways; (d) to audit all transactions of Pakistan Railways relating to Public Accounts; and (e) to audit all trading, manufacturing, profit and loss accounts, balance sheets and other subsidiary accounts kept and maintained by Pakistan Railways.

117. Object of Statutory Audit. The main object of audit is to ensure that the system of accounts used by the internal check authority is correct, that the method of check applied at every stage of the accounts is sufficient, that the accounts are maintained and the checks applied with due accuracy, and that arrangements exist in the accounts offices to ensure attention to the financial interests of Pakistan Railways on the part of all concerned. This object is generally secured by a percentage check to be applied to the vouchers and connected accounts record of the Accounts Office and by inspection on the spot of initial records and documents in the offices in which the transactions originate. Accounts Officers should afford all facilities to Audit Officers in the discharge of their audit duties. 118. Disposal of Audit Objections. All audit objections and notes should be promptly attended to by the Accounts Officers. Audit objections may either relate to matters which can be disposed of by the Accounts Officer himself without reference to the executive or to matters which can be elucidated only by the executive. In the former case, no reference should ordinarily be made by the Accounts Office to the executive except to advise disallowances, if any, arising out of the audit objections. In regard to the latter, the Accounts Officer should arrange to elicit necessary information for the

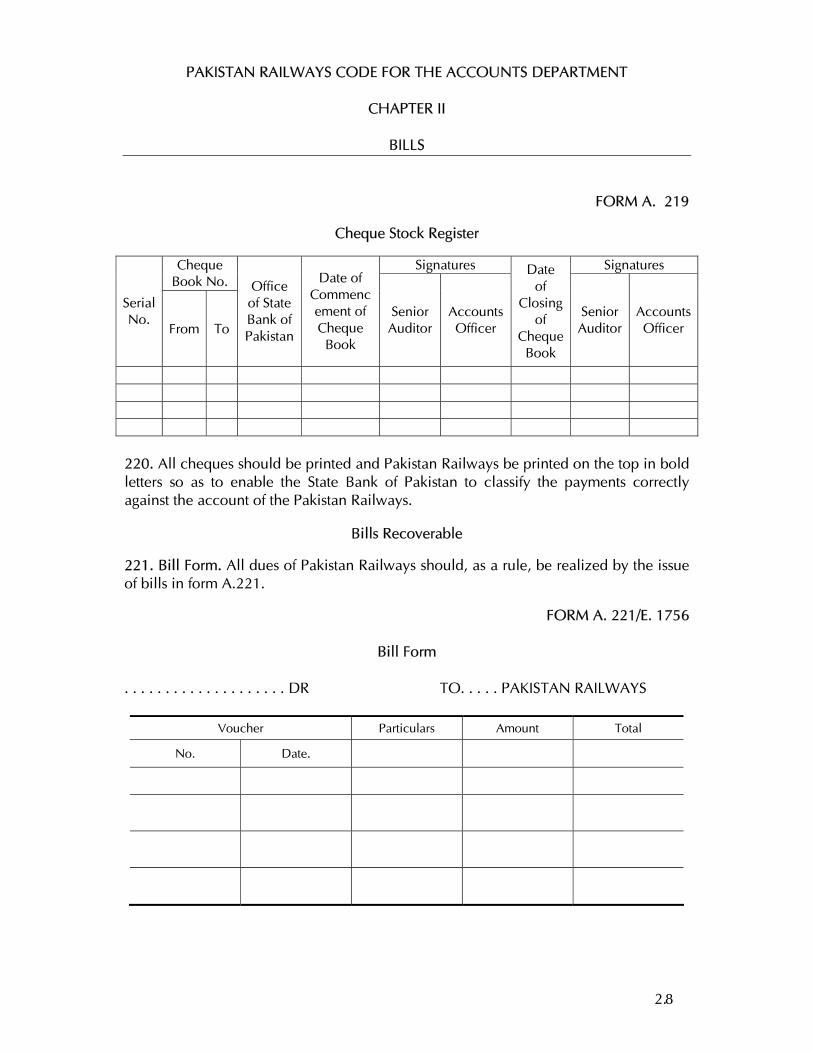

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

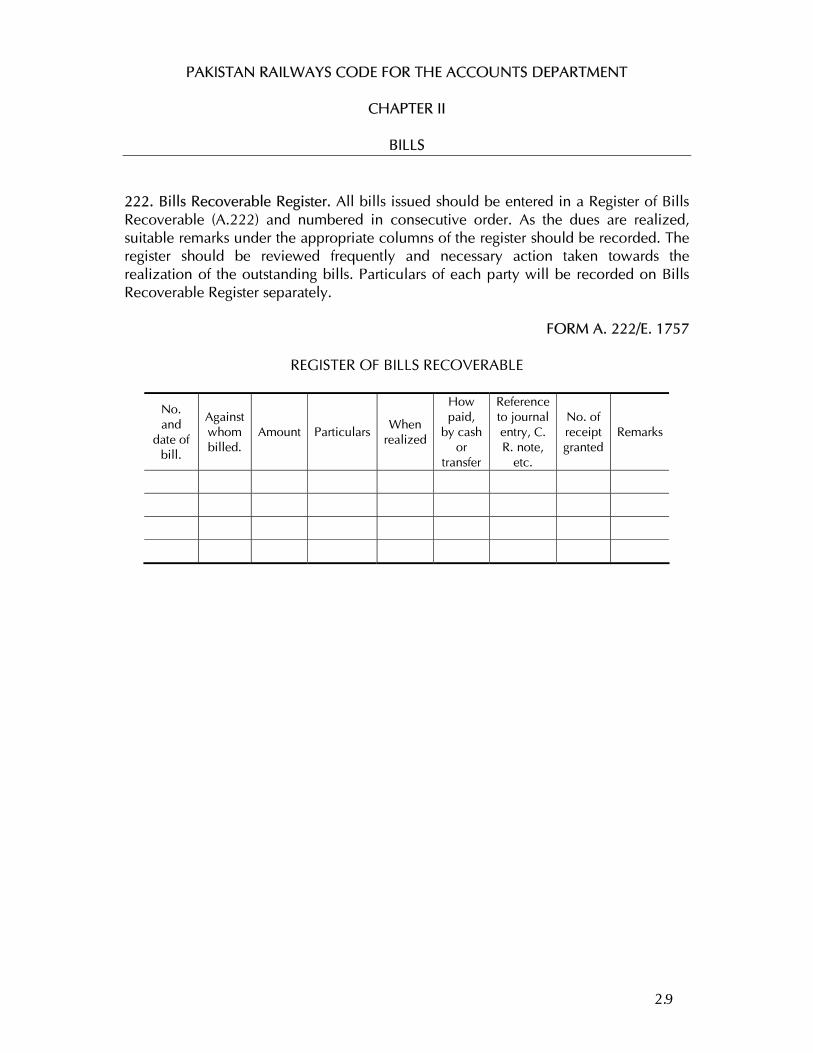

1.7

disposal of the audit objection; and, if in his opinion, the audit objection should be upheld, he should arrange to see that suitable action is taken. In the event of a disagreement between the Audit Officer and the Accounts Officer, procedure prescribed in Chapter VIII should be followed.

B. RECRUITMENT RULES AND SERVICE CONDITIONS OF CIVIL SERVANTS 118A. Civil Servants (Appointment, Promotion and Transfer) Rules, 1973 are given in Appendix IX to this Code. 119. Gazetted Staff. The gazetted establishment of Pakistan Railways Accounts Department comprises:

(a) Officers of Pakistan Audit and Accounts service, and

(b) Officers of departmental cadre of Pakistan Railways Accounts Department promoted from lower ranks, or

(c) Officers transferred from other departments of Pakistan Railways, or

(d) On deputation from any other service. 120. Deleted.

121. Appointment, Promotion and Leave. (1) (a)The recruitment to Pakistan Audit and Accounts Service and training thereof is controlled by the Auditor General of Pakistan. The department is left with the option of posting the officers within the department itself. However, for the purpose of in-service training, Member Finance or Financial Adviser & Chief Accounts Officer can depute them. The officers of departmental cadre in the rank of Accounts Officers are appointed by the Member Finance from the rank of Assistant Accounts Officers and later on inducted into Pakistan Audit and Accounts Service in accordance with the quota laid down from time to time. Leave is governed by Revised Leave Rules 1980.

(b) The post of Senior Accounts Officer will be filled by the promotion of Accounts Officers. When no Accounts Officer is available or can be made available without conflicting with the interest of the administration, an Accounts Officer may be appointed to officiate as a Senior Accounts Officer.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.8

(c) With a view to facilitating contact with officers on leave all such officers should, before proceeding on leave report to the Member Finance through Financial Adviser & Chief Accounts Officer.

(2) Assistant Accounts Officers. The post of Assistant Accounts Officers will be filled by selection from staff, who have passed the examination prescribed in Appendix X to this Code. (3) Senior Auditors. The posts of Senior Auditors will be ordinarily filled by transfer of selected persons from accounts offices of Pakistan Railways.

Non — Gazetted Staff

122. Recruitment in the office of Financial Adviser & Chief Accounts Officer.

Junior Auditors. Permanent and temporary vacancies shall be filled by recruitment in accordance with the Civil Servants (appointment, promotion and transfer) Rules, 1973 (Appendix IX to this code).

123. Recruitment of Staff from other Offices. (a) All first appointments, from other Offices/Government Departments, will be made by Selection Committees.

(b) All new Junior Auditors will be taken in the lowest class of Junior Auditors on the minimum pay of that class. (c) The provision of clauses (a) and (b) of this rule will also apply to appointments to the following classes of establishments:

Stenographers. Computer Operators. Junior Auditors.

(d) The Financial Adviser and Chief Accounts Officer will appoint a Selection Committee consisting of not less than three officers of the Accounts Department. At least one should be of a status not lower than that of a Deputy Financial Adviser and Chief Accounts Officer and should preside over the Committee. (e) Rules regarding conditions of service, eligibility to appear before the Committee, etc. will be as prescribed by the Financial Adviser and Chief Accounts Officer or the Member Finance as the case may be from time to time.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.9

Note: In following the Rules framed by Administration, preference should be given to the children of railway employees if other things are equal and not otherwise.

124. Deleted.

125. Appointment to the rank of Stock-Verifiers. As the seniority of Stock-verifiers has been combined with Senior Auditors, therefore, selection to the rank of stock verifiers will be made from the Senior Auditors.

126. Promotion to the grade of Assistant Accounts Officer, Inspector of Coaching & Goods Accounts, Inspector of Stores Accounts and Divisional Pay Master. No railway servant will be eligible for promotion to the rank of Assistant Accounts Officer, Inspector of Coaching and Goods Accounts, Inspector of Stores Accounts and Divisional Pay Master unless he has passed the examination qualifying for promotion to these grades as laid down in Appendix X to this Code.

127. The promotion of Assistant Accounts Officer of the office of the Member Finance to the rank of Assistant Director, whether in his own office or elsewhere, will be regulated under the same rules as followed in other offices of Pakistan Railways.

128. Deleted. 129. Deleted. 130. Deleted. 131. Deleted. 132. Deleted 133. Deleted. 134. Seniority. The rules for determining the relative seniority of civil servants employed in Accounts Offices are contained in Civil Servants (Seniority) Rules, 1993 as amended from time to time. These rules are reproduced in Appendix XI to this Code. 135. Supersession. Except in leave vacancies not exceeding four months in duration where purely local arrangement may be required to be made, no employee shall be superseded for promotion without the personal sanction of the Head of the Office or such higher authority as may be prescribed by any rule or order.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.10

C. OFFICE PROCEDURE

136. Main Division of Work. The work in Pakistan Railways Accounts Office generally falls under following main divisions:

(1) Establishment. (2) Stores. (3) Workshops. (4) Engineering Accounts. (5) Other Expenditure Accounts. (6) Cash and Pay. (7) Traffic. (8) General Provident Fund and Pension. (9) Booking and Compilation.

(10) Inspection. (11) Cost Accounting (i.e. Rail Costing, workshops and factories costing, etc.)

The actual division into branches and sections and the distribution of work among the gazetted staff is left to the discretion of the head of the office, in the absence of orders to the contrary as regards any particular charge. All the above items of work have been dealt with generally in this Code. Detailed rules relating to items of work numbered 2, 3 and 4 have been laid down in the respective departmental codes. 137. Office Manuals. Detailed working instructions in conformity with and subsidiary to the rules contained in this and other Pakistan Railway Codes should be laid down in the office manuals of each Accounts Office, issued under the authority of the head of the office, and these should be kept up to date. The office manuals should also contain:

(a) detailed rules of procedure for the conduct of business in the Accounts office; (b) orders defining the duties and responsibilities of the supervising staff; and (c) instructions for the periodical inspections of the books of account maintained in each section, for the test check of some portion of the work done by each member of the staff once a month (see note under paragraph 344), for the submission of progress reports about the state of work in each section and for periodical reviews of all correspondence awaiting disposal.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.11

138. Calendar of Returns. Each section of an Accounts Office should maintain a Calendar of Return showing the due and actual dates of (i) dispatch of returns due from the section, and (ii) submission to Accounts Officers of all accounts, objection statements, registers, etc. The calendar so maintained should be submitted periodically, on prescribed day, to the Accounts Officer in charge for review. The result of the review should be placed on record either in the periodical progress reports or elsewhere. 139. Inspection of Books of Account. The intervals at which books of account are required to be inspected by Accounts Officer in charge of the section concerned are laid down in Appendix XII to this Code. Books of account which are required to be checked and initialled by Accounts Officer at the time they are made, need not be subjected to a separate periodical inspection, but the detailed procedure prescribed in the office manuals (c.f. paragraph 137) for the posting and checking of such books of account should ensure a continuous review thereof by the officer in charge. 140. Destruction of Records. The destruction of records in an Accounts Office will be carried out under the order of the Financial Adviser and Chief Accounts Officer, subject to the retention of certain records for the minimum periods prescribed in Appendix XIII to this Code. 141. Supply of Books of Reference. Every gazetted officer should be supplied with a copy of all the Pakistan Railways Codes in force. Books so supplied will be treated as personal copies and may be carried away by the officer, on his transfer from one office to another. Corrections issued from time to time will be supplied by the office in which an officer is employed, but such officer will be personally responsible for the books and for keeping them corrected up to date. Permanent staff of the office, who desire the concession, may be supplied with priced Government publications together with sets of correction slips thereto. 142. Monthly Arrear Reports. Statement showing arrears of work on the last day of each month end in each Accounts Office should be submitted to the Member Finance so as to reach him not later than 7th of the following month. These statements should be in form A.142 given below. A list of important cases which remain outstanding for over a year with reasons therefore and the action taken to expedite settlement should be appended to the arrear reports.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.12

FORM A. 142

STATEMENT SHOWING ARREARS IN THE RAILWAY ACCOUNTS DEPARTMENT ON THE MONTH ENDED……………………… 20 . . . .

Serial No.

Branch and Division of the

Dept.

Nature of work in arrears

Period for which in arrears

Cause of arrears

Steps taken for clearance and when likely to be cleared.

Remarks

1 2 3 4 5 6 7

143. Performance Evaluation Reports of Gazetted Officers. The performance evaluation reports in respect of officers of Pakistan Audit and Accounts Service are to be sent to Auditor General of Pakistan. For officers of departmental cadre, these are to be kept with the Office of Financial Adviser & Chief Accounts Officer, Pakistan Railways (confidential). The last date of submission of performance evaluation reports is as per time schedule given below:

i) officers of grade 21 & 20 31st January ii) officers of grade 19 28th February iii) officers of grade 18 & 17 31st March

144. Confidential Reports on Non-gazetted Staff. Records which should be treated as confidential be maintained in each Accounts Office for non-gazetted staff. These records should be written up by the Assistant Accounts Officer Incharge, and submitted to the Accounts Officer of the section, who will sign it after adding such remarks as he may consider necessary. The Financial Adviser and Chief Accounts Officer should arrange for periodical inspection of these records to see that they are kept up to date. These records should be entered up annually and at every change of supervising officer, in the case of non-gazetted staff. Whenever adverse comments are made on the work of any individual, the substance of such adverse comments should be communicated to him. The documents through which the communication is made should be prepared in duplicate, one copy being signed by official concerned and returned with his explanation, if any, and the other copy being retained by him for future reference.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.13

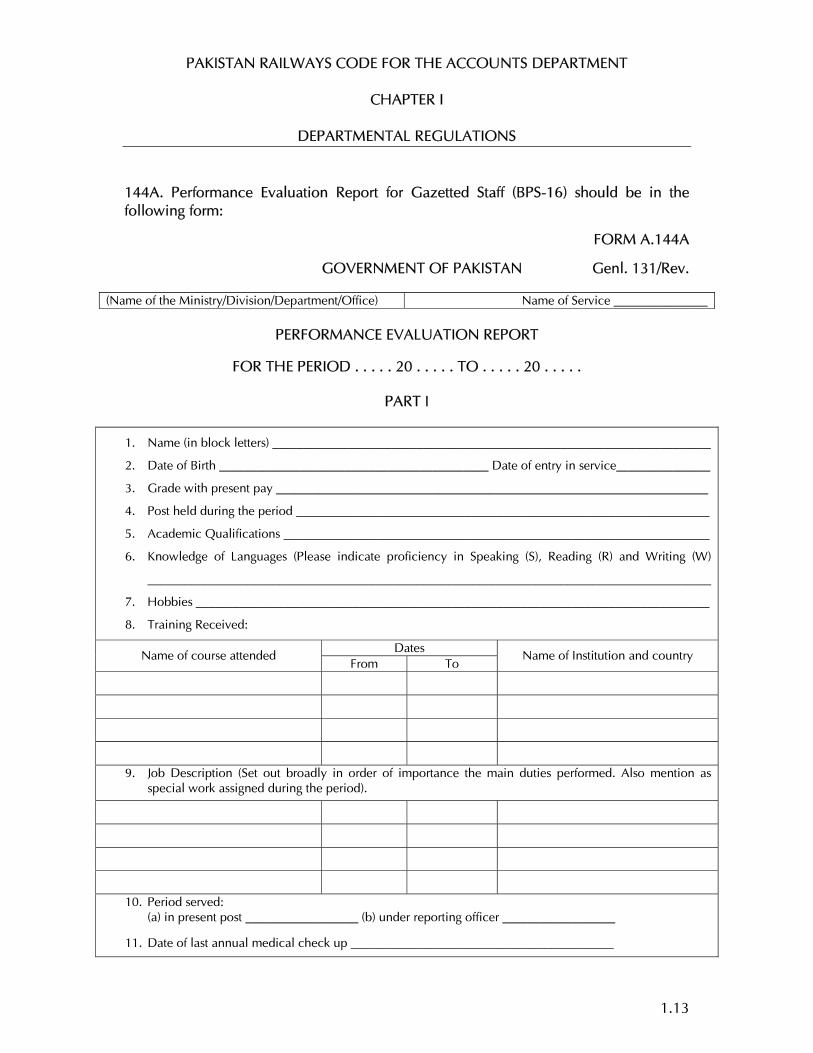

144A. Performance Evaluation Report for Gazetted Staff (BPS-16) should be in the following form:

FORM A.144A

GOVERNMENT OF PAKISTAN Genl. 131/Rev.

(Name of the Ministry/Division/Department/Office) Name of Service _______________

PERFORMANCE EVALUATION REPORT

FOR THE PERIOD . . . . . 20 . . . . . TO . . . . . 20 . . . . .

PART I

1. Name (in block letters) ______________________________________________________________________

2. Date of Birth ___________________________________________ Date of entry in service_______________

3. Grade with present pay _____________________________________________________________________

4. Post held during the period __________________________________________________________________

5. Academic Qualifications ____________________________________________________________________

6. Knowledge of Languages (Please indicate proficiency in Speaking (S), Reading (R) and Writing (W)

__________________________________________________________________________________________

7. Hobbies __________________________________________________________________________________

8. Training Received:

Dates Name of course attended

From To Name of Institution and country

9. Job Description (Set out broadly in order of importance the main duties performed. Also mention as special work assigned during the period).

10. Period served: (a) in present post __________________ (b) under reporting officer __________________

11. Date of last annual medical check up __________________________________________

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.14

The rating in Parts II, III & IV should be recorded by initialling the appropriate box. The ratings denoted by alphabets is as follows: “AI” Very Good, “A” Good, “B” Average, “C” Below Average, “D” Poor For uniform interpretation of qualities listed in those parts two extreme shades are mentioned against each item. Please see para. 7 of instructions.

PART II

PERSONAL QUALITIES

AI A B C D 1. Intelligence Exceptionally bright; Excellent

comprehension Dull, slow

2. Confidence and will power

Exceptionally confident and resolute

Uncertain: hesitant

3. Emotional stability Mature, balanced Unstable immature

4. Adaptability Alert & highly responsible Rigid inflexible

5. Understanding & tolerance

Considerate & Co-operative Lacks ability to appreciate other’s point of view unsympathetic

6. Appearance and bearing

Creates excellent impression Clumsy: Unimpressive

7. OVERALL GRADING IN PART II

PART III

ATTITUDE

1. *Knowledge of Islam Well read Narrow and superficial

2. *Attitude towards Islamic ideology

Deeply motivated: enlightened

Indifferent: intolerant

Irreproachable

Unserupulous 3. Integrity

(a) General (b) Intellectual Honest & straight forward Deviaus: Sycophant

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.15

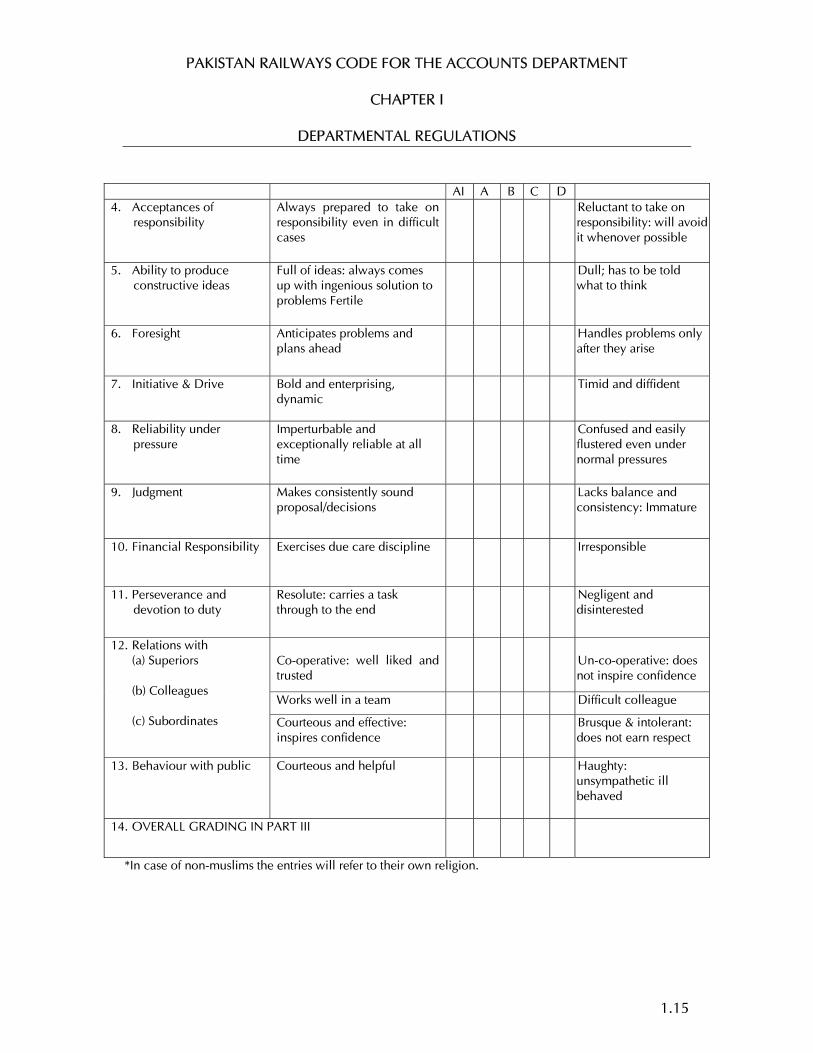

AI A B C D 4. Acceptances of

responsibility Always prepared to take on responsibility even in difficult cases

Reluctant to take on responsibility: will avoid it whenover possible

5. Ability to produce constructive ideas

Full of ideas: always comes up with ingenious solution to problems Fertile

Dull; has to be told what to think

6. Foresight Anticipates problems and plans ahead

Handles problems only after they arise

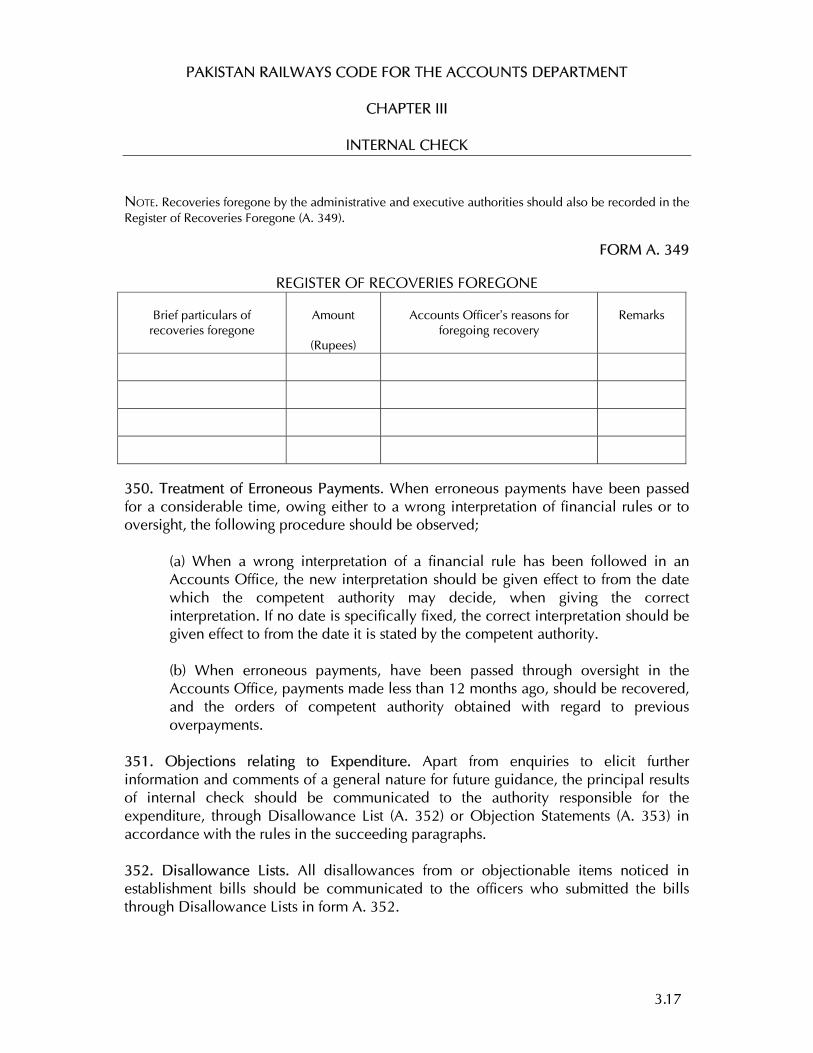

7. Initiative & Drive Bold and enterprising, dynamic

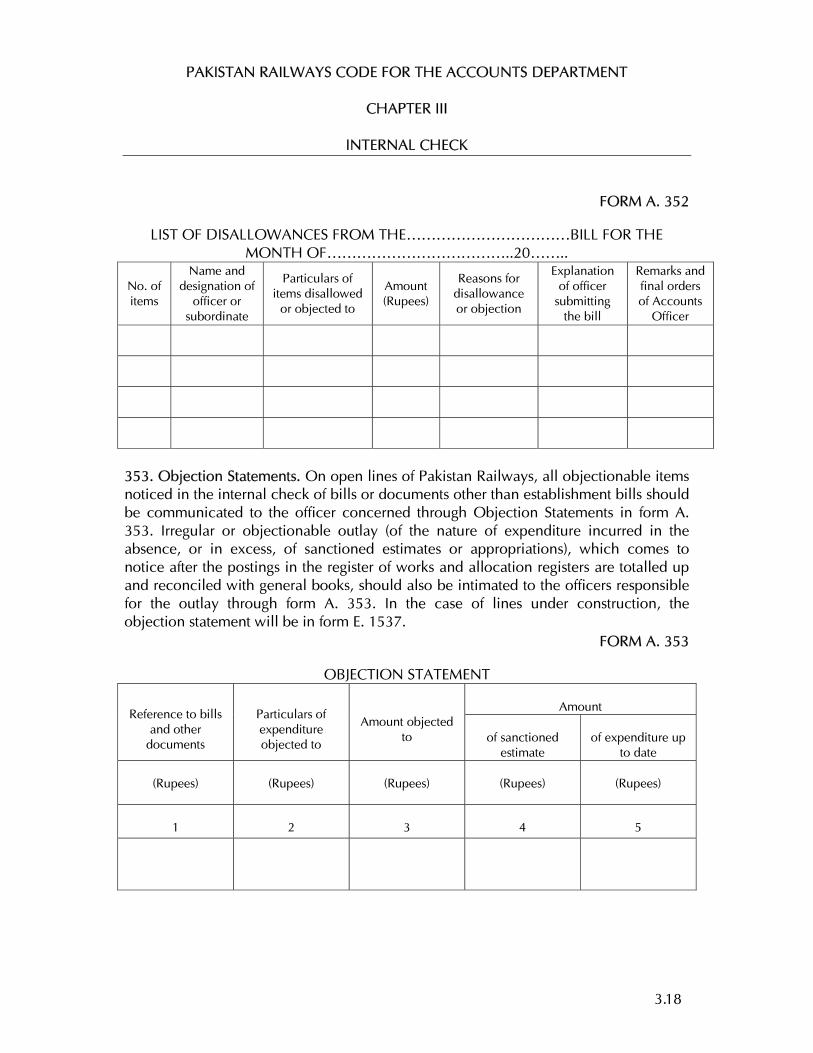

Timid and diffident

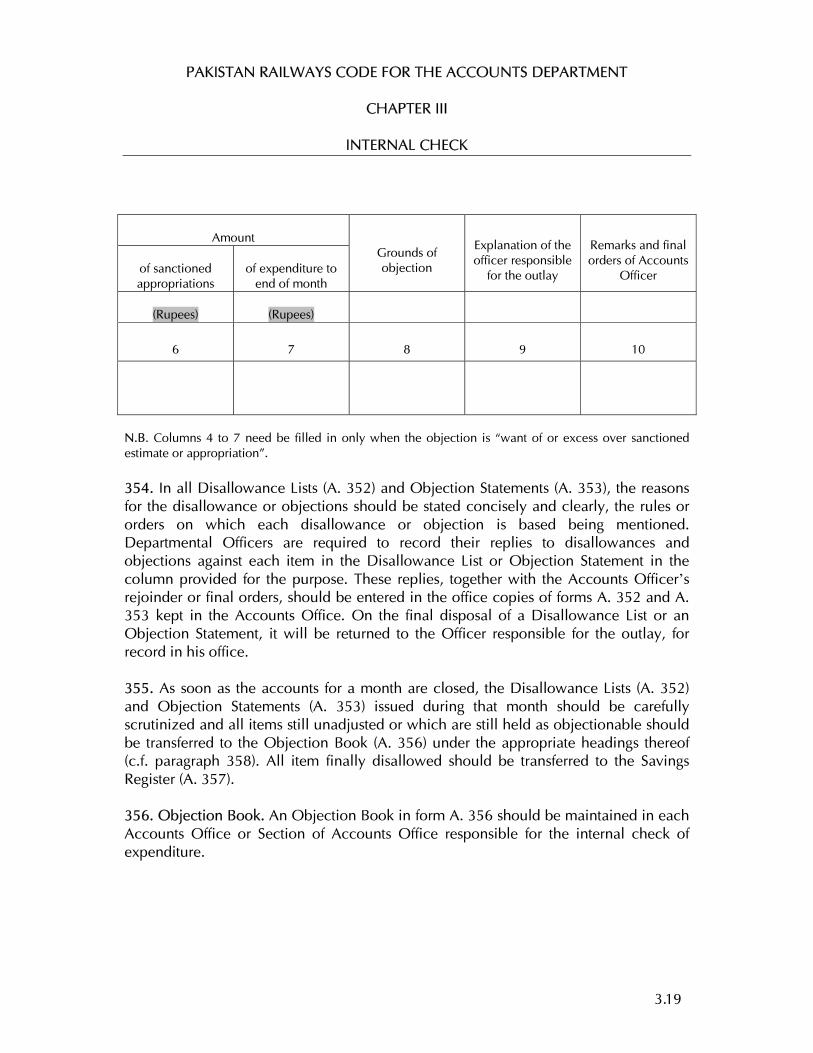

8. Reliability under pressure

Imperturbable and exceptionally reliable at all time

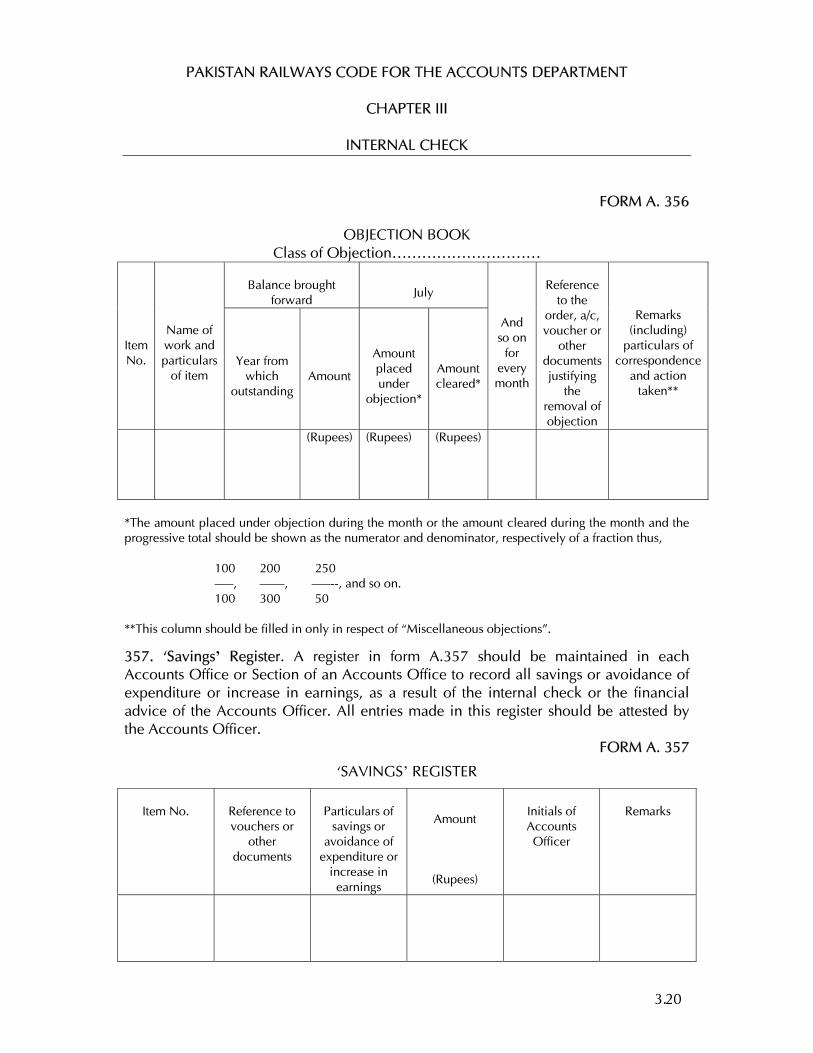

Confused and easily flustered even under normal pressures

9. Judgment Makes consistently sound proposal/decisions

Lacks balance and consistency: Immature

10. Financial Responsibility Exercises due care discipline Irresponsible

11. Perseverance and devotion to duty

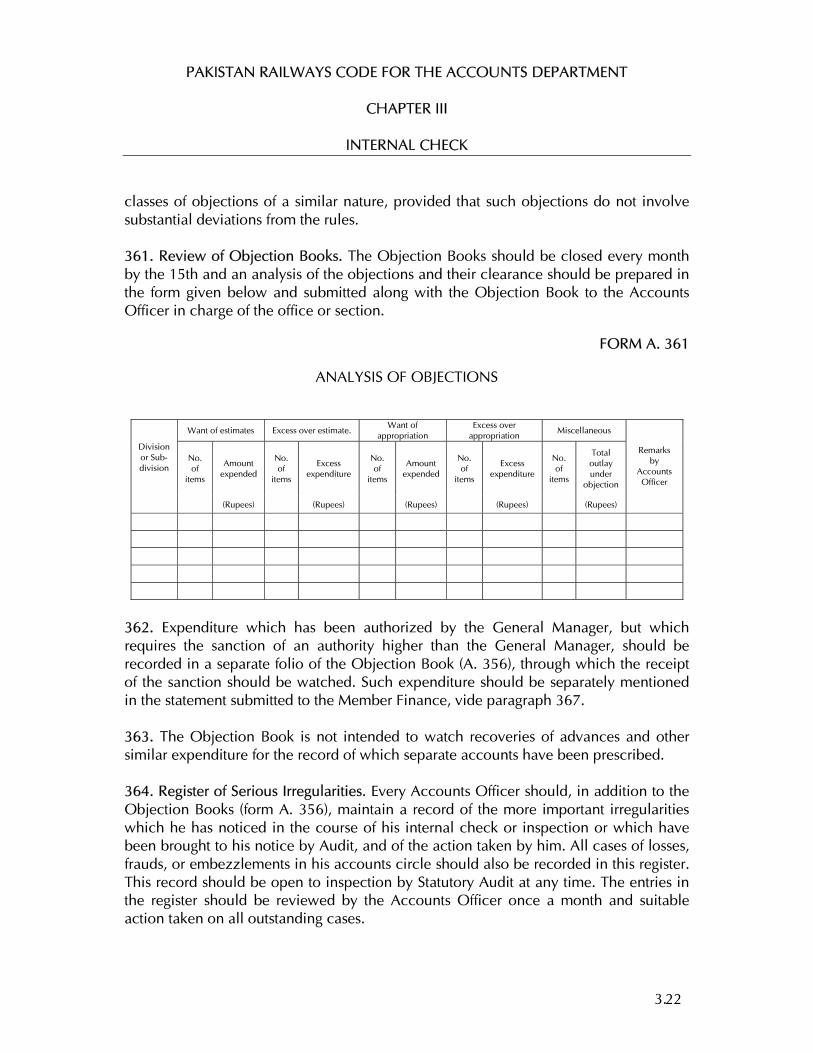

Resolute: carries a task through to the end

Negligent and disinterested

Co-operative: well liked and trusted

Un-co-operative: does not inspire confidence

Works well in a team Difficult colleague

12. Relations with (a) Superiors (b) Colleagues (c) Subordinates

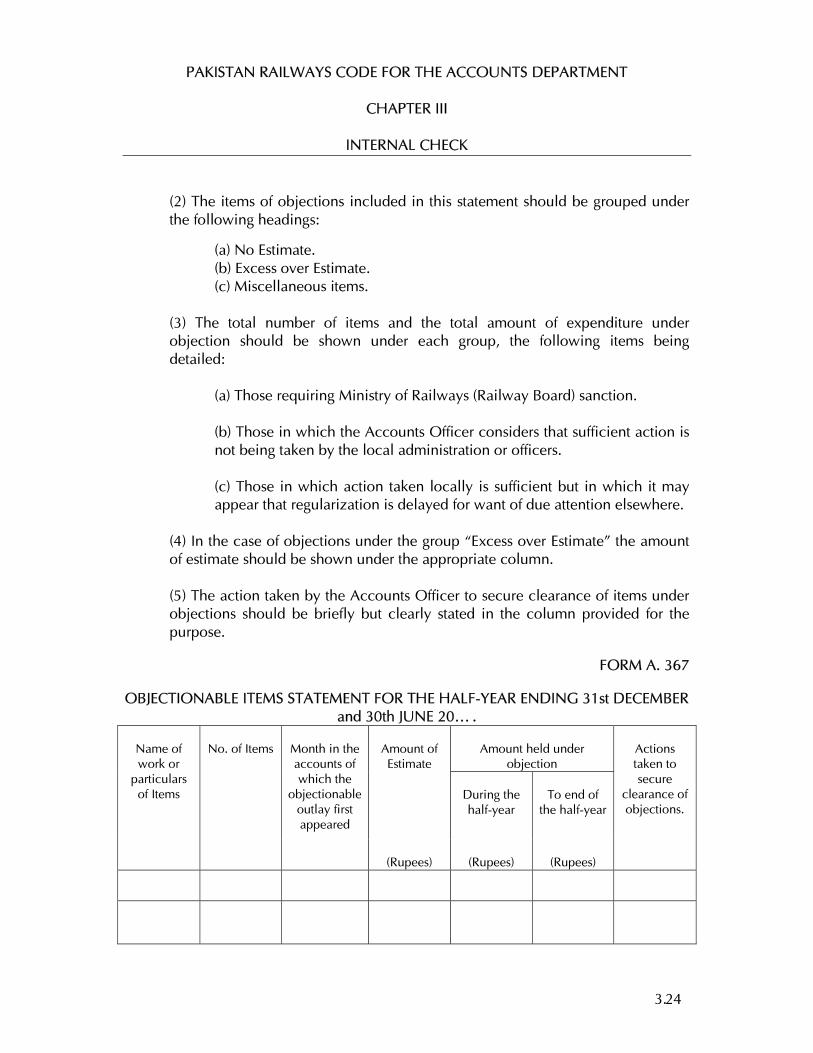

Courteous and effective: inspires confidence

Brusque & intolerant: does not earn respect

13. Behaviour with public Courteous and helpful Haughty: unsympathetic ill behaved

14. OVERALL GRADING IN PART III

*In case of non-muslims the entries will refer to their own religion.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.16

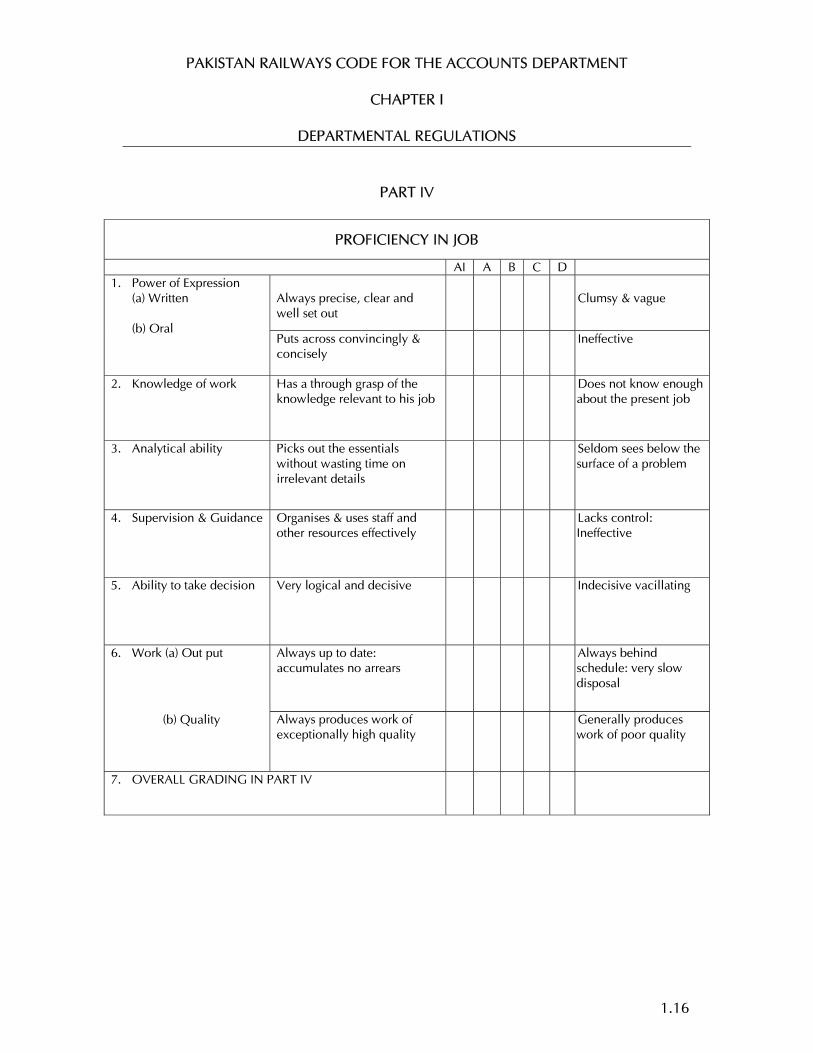

PART IV

PROFICIENCY IN JOB

AI A B C D Always precise, clear and well set out

Clumsy & vague

1. Power of Expression (a) Written (b) Oral Puts across convincingly &

concisely Ineffective

2. Knowledge of work Has a through grasp of the knowledge relevant to his job

Does not know enough about the present job

3. Analytical ability Picks out the essentials without wasting time on irrelevant details

Seldom sees below the surface of a problem

4. Supervision & Guidance Organises & uses staff and other resources effectively

Lacks control: Ineffective

5. Ability to take decision Very logical and decisive Indecisive vacillating

Always up to date: accumulates no arrears

Always behind schedule: very slow disposal

6. Work (a) Out put

(b) Quality Always produces work of exceptionally high quality

Generally produces work of poor quality

7. OVERALL GRADING IN PART IV

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.17

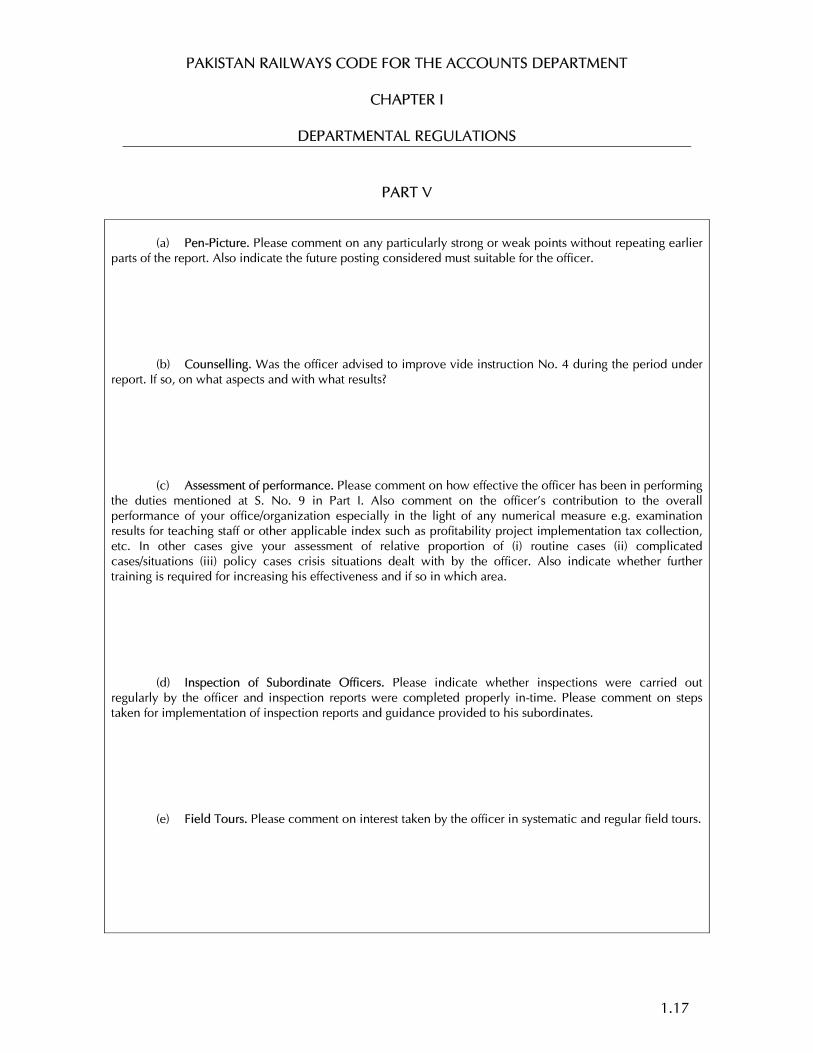

PART V

(a) Pen-Picture. Please comment on any particularly strong or weak points without repeating earlier

parts of the report. Also indicate the future posting considered must suitable for the officer.

(b) Counselling. Was the officer advised to improve vide instruction No. 4 during the period under report. If so, on what aspects and with what results?

(c) Assessment of performance. Please comment on how effective the officer has been in performing the duties mentioned at S. No. 9 in Part I. Also comment on the officer's contribution to the overall performance of your office/organization especially in the light of any numerical measure e.g. examination results for teaching staff or other applicable index such as profitability project implementation tax collection, etc. In other cases give your assessment of relative proportion of (i) routine cases (ii) complicated cases/situations (iii) policy cases crisis situations dealt with by the officer. Also indicate whether further training is required for increasing his effectiveness and if so in which area.

(d) Inspection of Subordinate Officers. Please indicate whether inspections were carried out regularly by the officer and inspection reports were completed properly in-time. Please comment on steps taken for implementation of inspection reports and guidance provided to his subordinates.

(e) Field Tours. Please comment on interest taken by the officer in systematic and regular field tours.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.18

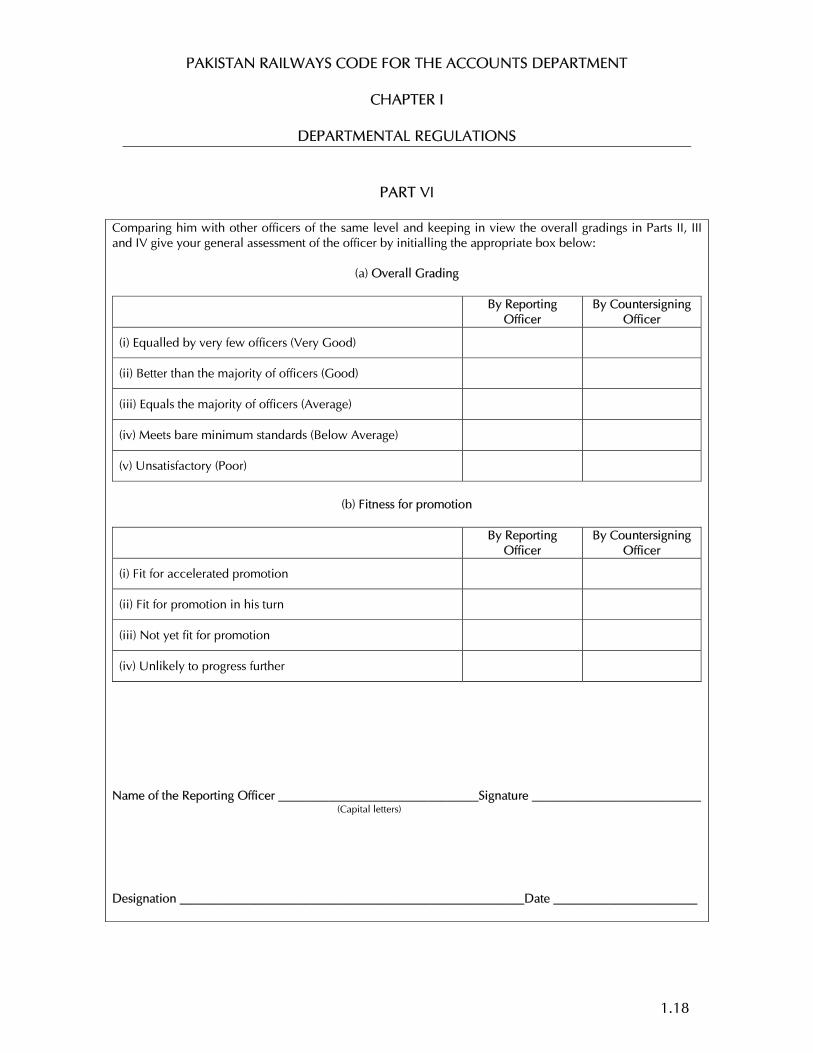

PART VI

Comparing him with other officers of the same level and keeping in view the overall gradings in Parts II, III and IV give your general assessment of the officer by initialling the appropriate box below:

(a) Overall Grading

By Reporting Officer

By Countersigning Officer

(i) Equalled by very few officers (Very Good)

(ii) Better than the majority of officers (Good)

(iii) Equals the majority of officers (Average)

(iv) Meets bare minimum standards (Below Average)

(v) Unsatisfactory (Poor)

(b) Fitness for promotion

By Reporting

Officer By Countersigning

Officer

(i) Fit for accelerated promotion

(ii) Fit for promotion in his turn

(iii) Not yet fit for promotion

(iv) Unlikely to progress further

Name of the Reporting Officer ________________________________Signature ___________________________ (Capital letters) Designation _______________________________________________________Date _______________________

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.19

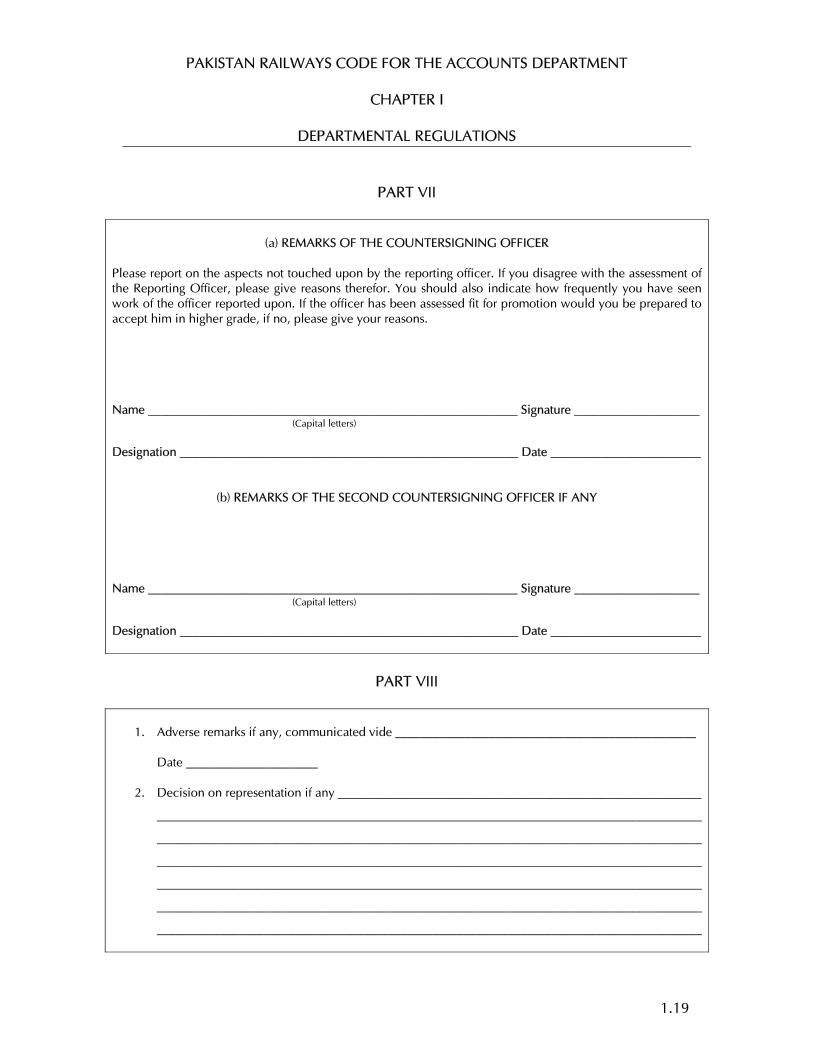

PART VII

(a) REMARKS OF THE COUNTERSIGNING OFFICER

Please report on the aspects not touched upon by the reporting officer. If you disagree with the assessment of the Reporting Officer, please give reasons therefor. You should also indicate how frequently you have seen work of the officer reported upon. If the officer has been assessed fit for promotion would you be prepared to accept him in higher grade, if no, please give your reasons. Name ___________________________________________________________ Signature ____________________ (Capital letters)

Designation ______________________________________________________ Date ________________________

(b) REMARKS OF THE SECOND COUNTERSIGNING OFFICER IF ANY Name ___________________________________________________________ Signature ____________________ (Capital letters)

Designation ______________________________________________________ Date ________________________

PART VIII

1. Adverse remarks if any, communicated vide ________________________________________________ Date _____________________

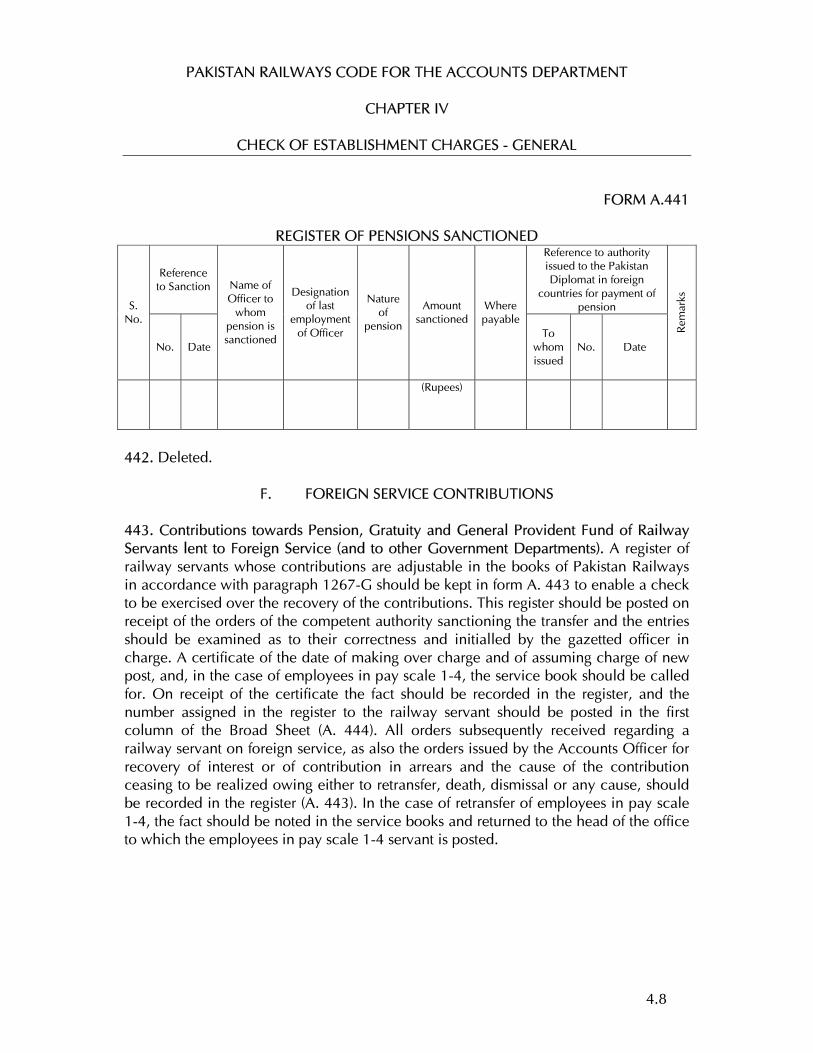

2. Decision on representation if any __________________________________________________________

_______________________________________________________________________________________

_______________________________________________________________________________________

_______________________________________________________________________________________

_______________________________________________________________________________________

_______________________________________________________________________________________

_______________________________________________________________________________________

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.20

INSTRUCTIONS FOR FILLING UP THE ACR FORMS

1. (i) ACR is the most important record for the assessment of an officer. At the same time the quality of ACR is a measure of the competence of the Reporting Officer and Countersigning Officer. It is, therefore, essential that utmost care is exercised by all Reporting and Countersigning Officers.

(ii) The Reporting and Countersigning Officer should be (a) as objective as possible and (b) clear and direct, not ambiguous or evasive in their remarks.

(iii) The over-riding importance of Part IV should be clearly understood in the overall grading.

(iv) Over-rating should be as showed by all Reporting/Countersigning Officers. (v) Vague impressions based on inadequate knowledge or isolated incidents

should be avoided.

2. The forms are to be filled in duplicate. Part I will be filled by the officer being reported upon and should be type written. Parts II to VI will be filled by the Reporting Officer and Part VII by the Countersigning Officers. Both the Reporting Officer and Countersigning Officer should give their assessment of the officer reported upon in respective boxes in Part VI. The Ministry/Division/Department concerned will fill Part VIII, if any adverse remarks are recorded in the report.

3. Assessment in the ACR should be confined to the work done by the officer reported upon during the period covered by the report.

4. Reporting Officer is expected to counsel the officer being reported upon about his weak points and advise him how to improve. Adverse remarks should normally be recorded when the Officer fails to improve despite counselling.

5. The ACR form should be filled in a neat and tidy manner. Cuttings/erasures should be avoided and must be initialled, where made.

6. The ratings in Part II, III, IV & VI should be recorded by initialling the appropriate box.

7. For uniform interpretation of qualities, etc., listed in Parts II, III & IV the two extreme shades are mentioned against each item. For example an exceptionally bright officer with excellent comprehension will be rated “AI” in Intelligence (box I of Part II). A dull and slow officer will merit a “D” rating. A, B & C ratings will denote shades between the above two extremes.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.21

8. The ratings should be clear and given in one of the boxes provided for the purpose in Parts II, III, IV & VI. Do not grade an officer between two shades i.e. between “Very Good” and “Good” or “Average” or Average and “Below Average”.

9. The Countersigning Officers should weigh the remarks of the Reporting Officer against his personal knowledge of the officer being reported upon compare him with other officers of the same grade working under different Reporting Officers but under the same Countersigning Officer and then give his overall assessment in Part VI and remarks in Part VII (a). In certain categories of cases remarks of a Second Countersigning Officer may also be required to be recorded. The Establishment Division will identify such cases, from time-to-time and also designate an officer as the Second Countersigning Officer for each category. The Second Countersigning Officer will record his remarks in Part VII (b).

10. If the Countersigning Officer differs with the grading or remarks given (in parts other than Part VI) by the Reporting Officer he should score it out and give his own grading in red ink. In Part VI he is required to give his own assessment in addition to that of the Reporting Officer.

11. The Countersigning Officer should underline, in red ink, remarks which in his opinion are adverse and should be communicated to the officer reported upon.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.22

145. Performance Evaluation Report for Officers in (BPS-17 & 18) and (BPS-19 & 20) should be in the following forms:

FORM A. 145

CERTIFICATE

Certified that I (Name of Officer)

Personnel Number (if allotted)

have on Submitted my(Group/Service) (BPS) (Date)

Performance Evaluation Report for the period to

(Name/Designation of Countersigning Officer)

My Countersigning officer is (Name/Designation of Countersigning Officer) Signatures Designation / Department Note:- This certificate is required to be dispatched by the officer being reported upon to the

Officer Incharge entrusted with the maintenance of his/her C.R dossier on the same date the PER is forwarded to his/her reporting officer.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.23

FORM A. 145 (I) S-121-G (i)

FOR OFFICERS IN BPS 17 & 18 CONFIDENTIAL

GOVERNMENT OF PAKISTAN

Service/Group Ministry/Division/ Department/Office

PERFORMANCE EVALUATION REPORT

FOR THE PERIOD 20 TO 20

PART I

(TO BE FILLED IN BY THE OFFICER REPORTED UPON)

1. Name (in block letters)

2. Personnel number

3. Date of birth

4. Date of entry in service

5. Post held during the period (with BPS)

6. Academic qualifications

7. Knowledge of languages (Please indicate proficiency in speaking (S), reading (R) and writing (W)

8. Training received during the evaluation period

Name of course attended Duration with dates Name of institution and country

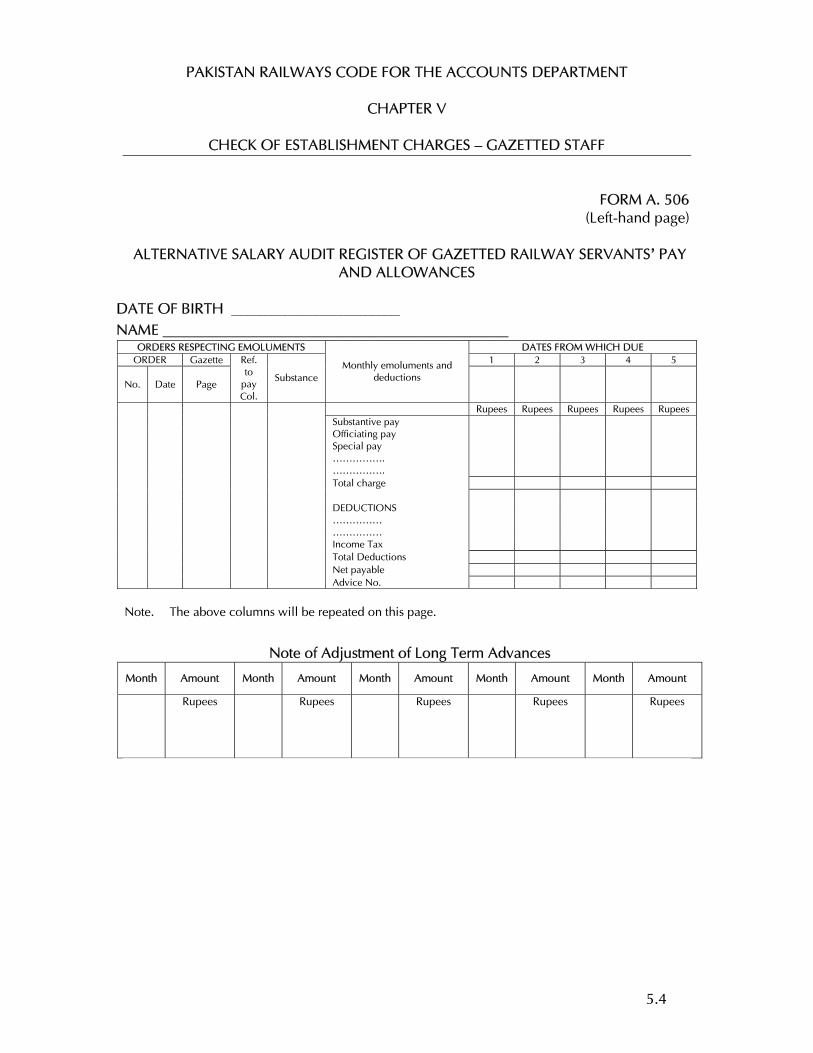

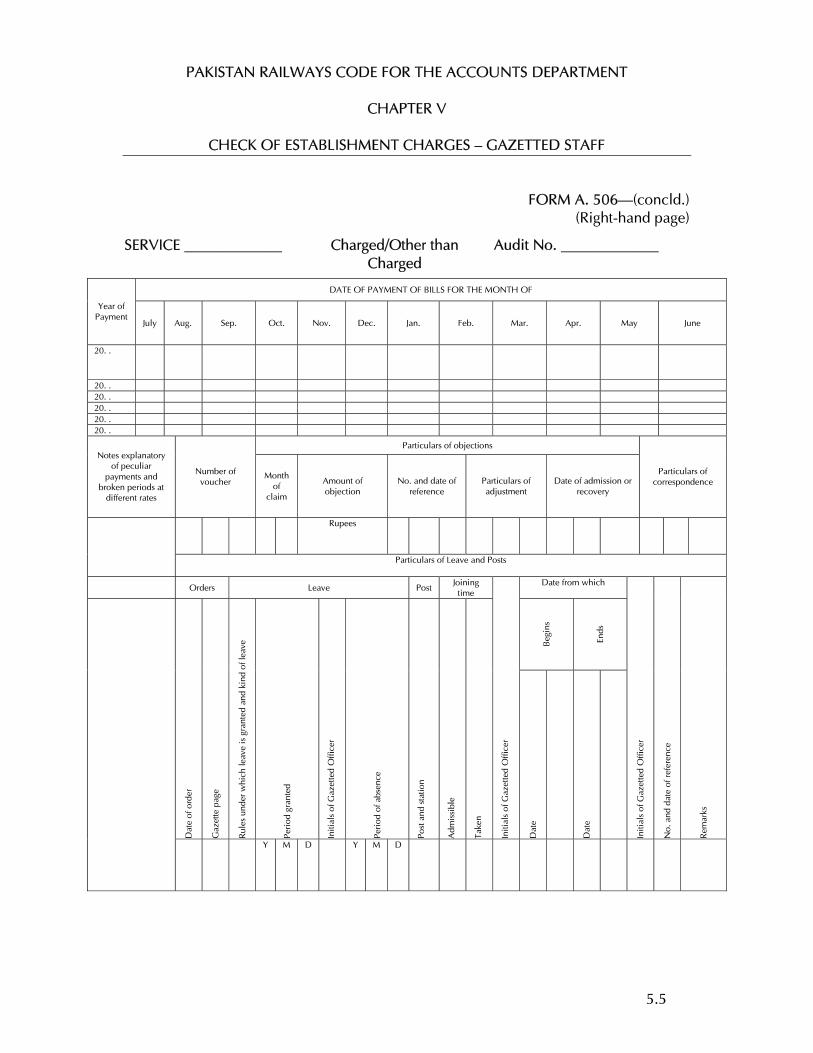

9. Period served (i) In present post ————————— (ii) Under the reporting officer—————————————————

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.24

PART II

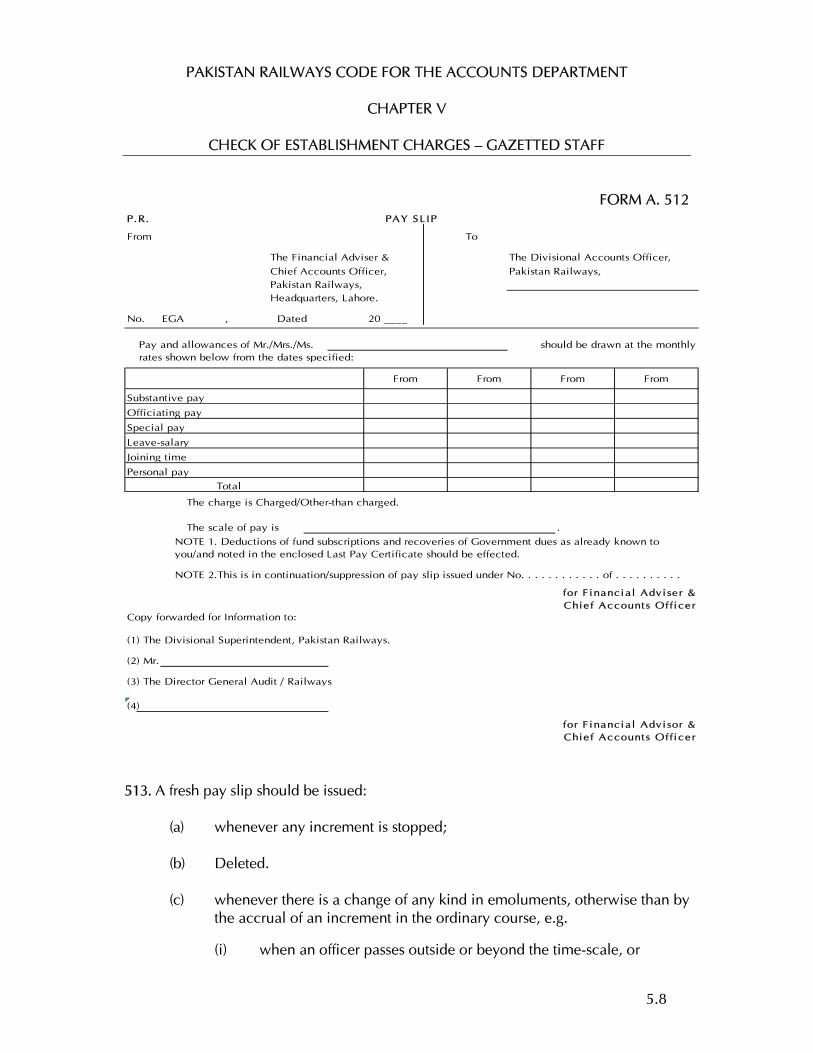

(TO BE FILLED IN BY THE OFFICER REPORTED UPON)

1. Job description

2. Brief account of performance on the job during the period supported by statistical data where possible. Targets given and actual performance against such targets should be highlighted. Reasons for shortfall, if any, may also be stated.

PART III

(EVALUATION BY THE REPORTING OFFICER)

The rating in Part III should be recorded by initialing the appropriate box.

The ratings denoted by alphabets are as follows: ‘A’ Very Good, ‘B” Good, ‘C’ Average, ‘D’ Below Average

For uniform interpretation of qualities, two extreme shades are mentioned against each quality.

A B C D 1. Intelligence

Exceptionally bright; excellent comprehension

Dull; slow

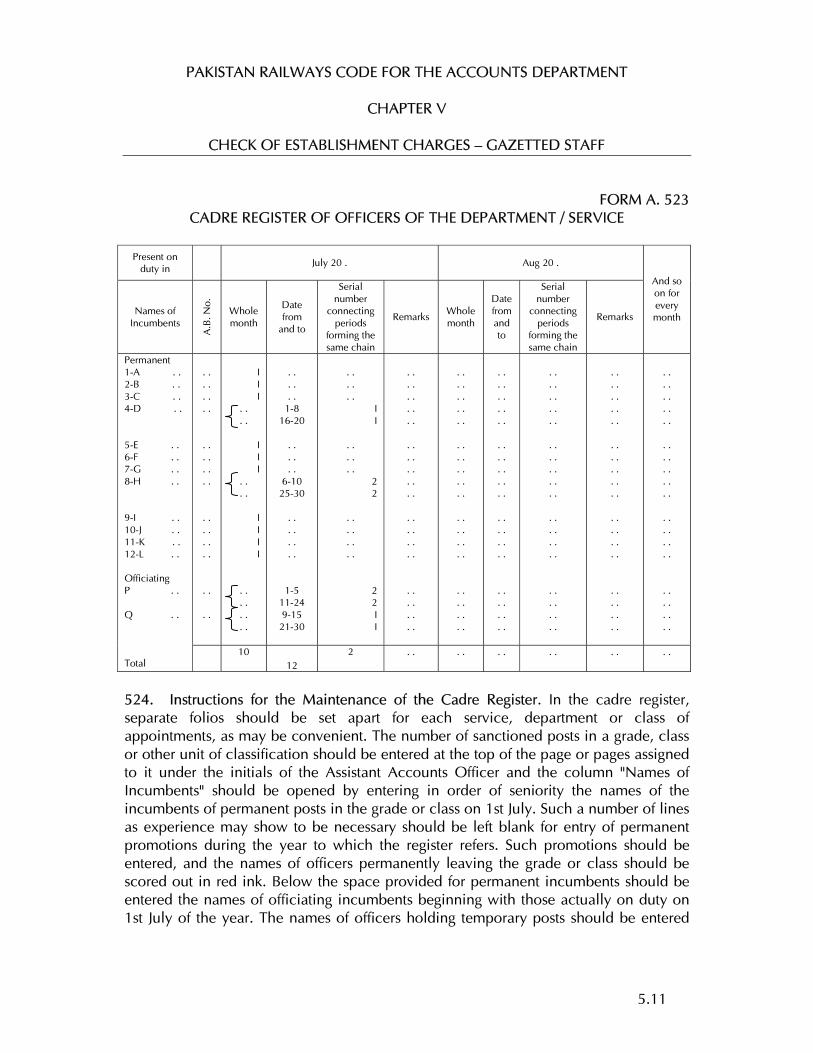

2. Confidence and will power Exceptionally confident and resolute

Uncertain; hesitant

3. Acceptance of responsibility Always prepared to take on responsibility even in difficult cases

Reluctant to take on responsibility

will avoid it whenever possible.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.25

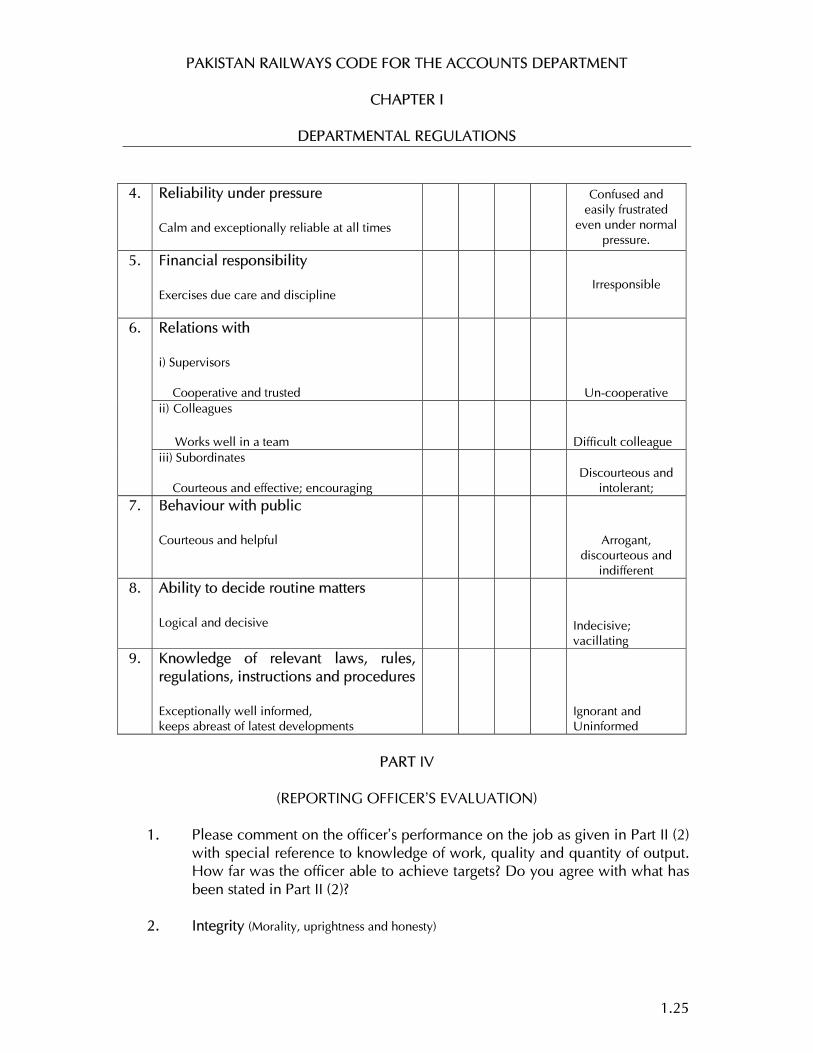

4. Reliability under pressure Calm and exceptionally reliable at all times

Confused and easily frustrated

even under normal pressure.

5. Financial responsibility Exercises due care and discipline

Irresponsible

Relations with i) Supervisors Cooperative and trusted

Un-cooperative ii) Colleagues Works well in a team

Difficult colleague

6.

iii) Subordinates Courteous and effective; encouraging

Discourteous and

intolerant; 7. Behaviour with public

Courteous and helpful

Arrogant, discourteous and

indifferent 8. Ability to decide routine matters

Logical and decisive

Indecisive; vacillating

9. Knowledge of relevant laws, rules, regulations, instructions and procedures Exceptionally well informed, keeps abreast of latest developments

Ignorant and Uninformed

PART IV

(REPORTING OFFICER’S EVALUATION)

1. Please comment on the officer’s performance on the job as given in Part II (2)

with special reference to knowledge of work, quality and quantity of output. How far was the officer able to achieve targets? Do you agree with what has been stated in Part II (2)?

2. Integrity (Morality, uprightness and honesty)

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.26

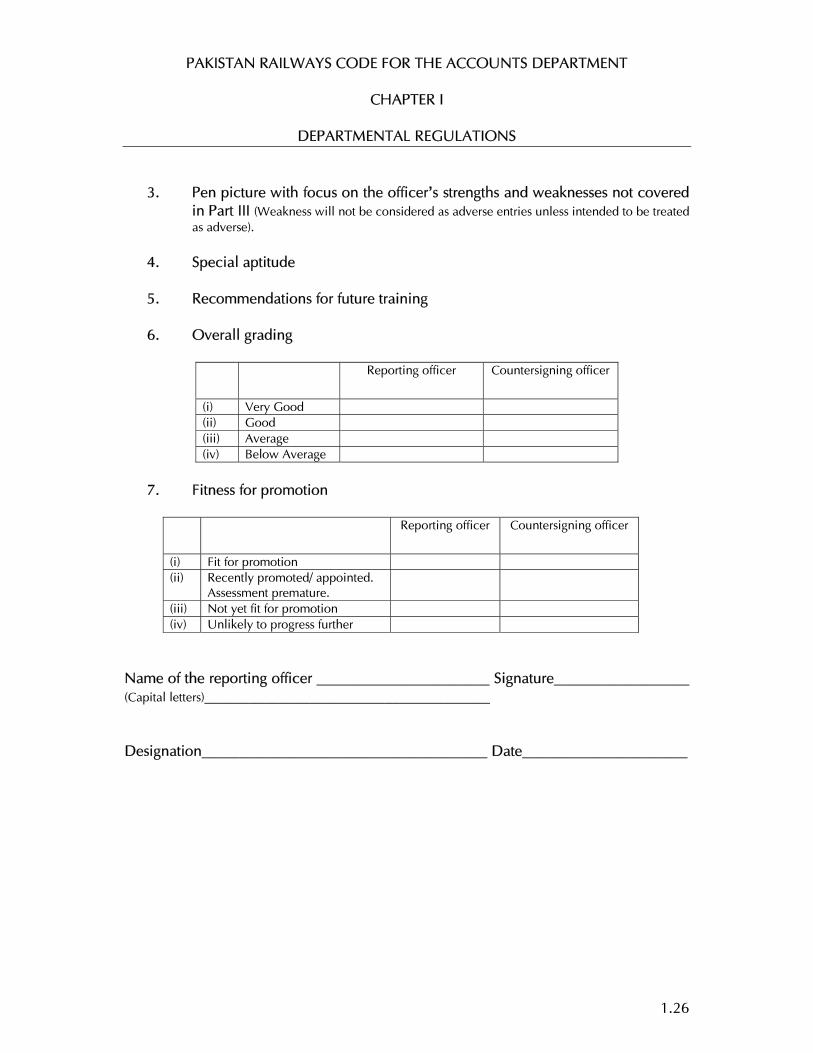

3. Pen picture with focus on the officer’s strengths and weaknesses not covered in Part III (Weakness will not be considered as adverse entries unless intended to be treated as adverse).

4. Special aptitude

5. Recommendations for future training

6. Overall grading

Reporting officer Countersigning officer

(i) Very Good (ii) Good (iii) Average (iv) Below Average

7. Fitness for promotion

Reporting officer Countersigning officer

(i) Fit for promotion (ii) Recently promoted/ appointed.

Assessment premature.

(iii) Not yet fit for promotion (iv) Unlikely to progress further

Name of the reporting officer _______________________ Signature__________________ (Capital letters)______________________________________ Designation______________________________________ Date______________________

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.27

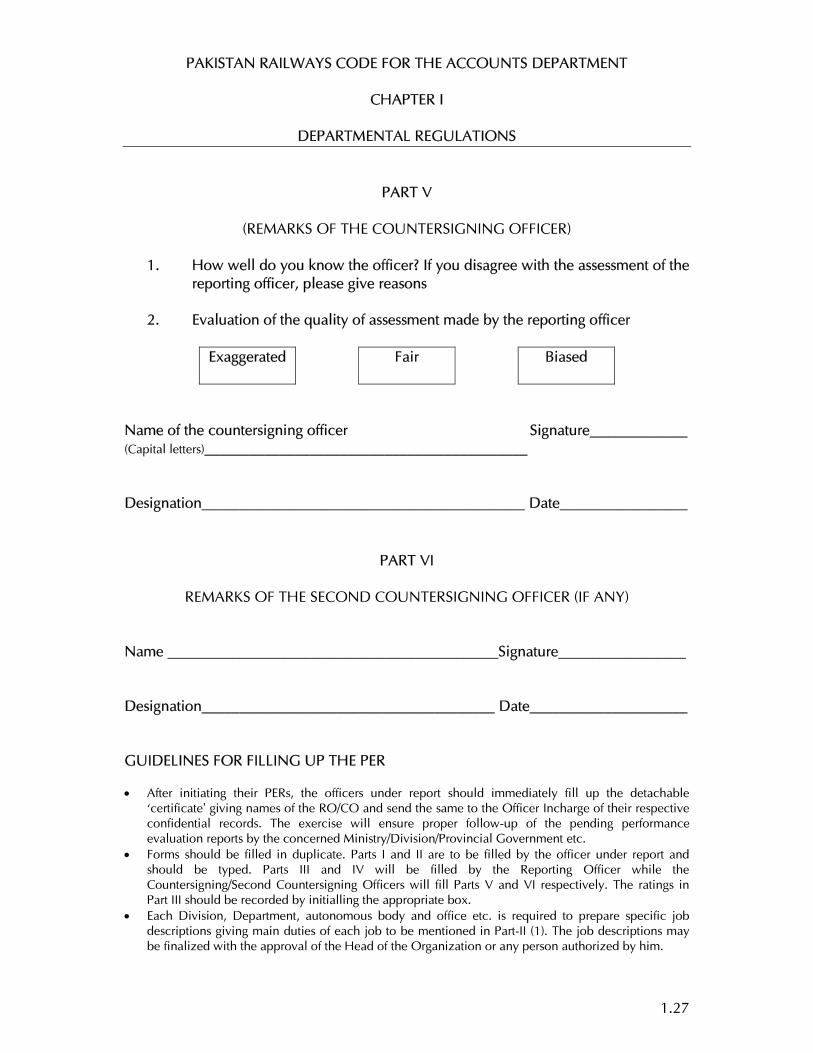

PART V

(REMARKS OF THE COUNTERSIGNING OFFICER)

1. How well do you know the officer? If you disagree with the assessment of the reporting officer, please give reasons

2. Evaluation of the quality of assessment made by the reporting officer

Exaggerated

Fair Biased

Name of the countersigning officer Signature_____________ (Capital letters)___________________________________________ Designation___________________________________________ Date_________________

PART VI

REMARKS OF THE SECOND COUNTERSIGNING OFFICER (IF ANY) Name ____________________________________________Signature_________________ Designation_______________________________________ Date_____________________ GUIDELINES FOR FILLING UP THE PER • After initiating their PERs, the officers under report should immediately fill up the detachable

‘certificate’ giving names of the RO/CO and send the same to the Officer Incharge of their respective confidential records. The exercise will ensure proper follow-up of the pending performance evaluation reports by the concerned Ministry/Division/Provincial Government etc.

• Forms should be filled in duplicate. Parts I and II are to be filled by the officer under report and should be typed. Parts III and IV will be filled by the Reporting Officer while the Countersigning/Second Countersigning Officers will fill Parts V and VI respectively. The ratings in Part III should be recorded by initialling the appropriate box.

• Each Division, Department, autonomous body and office etc. is required to prepare specific job descriptions giving main duties of each job to be mentioned in Part-II (1). The job descriptions may be finalized with the approval of the Head of the Organization or any person authorized by him.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.28

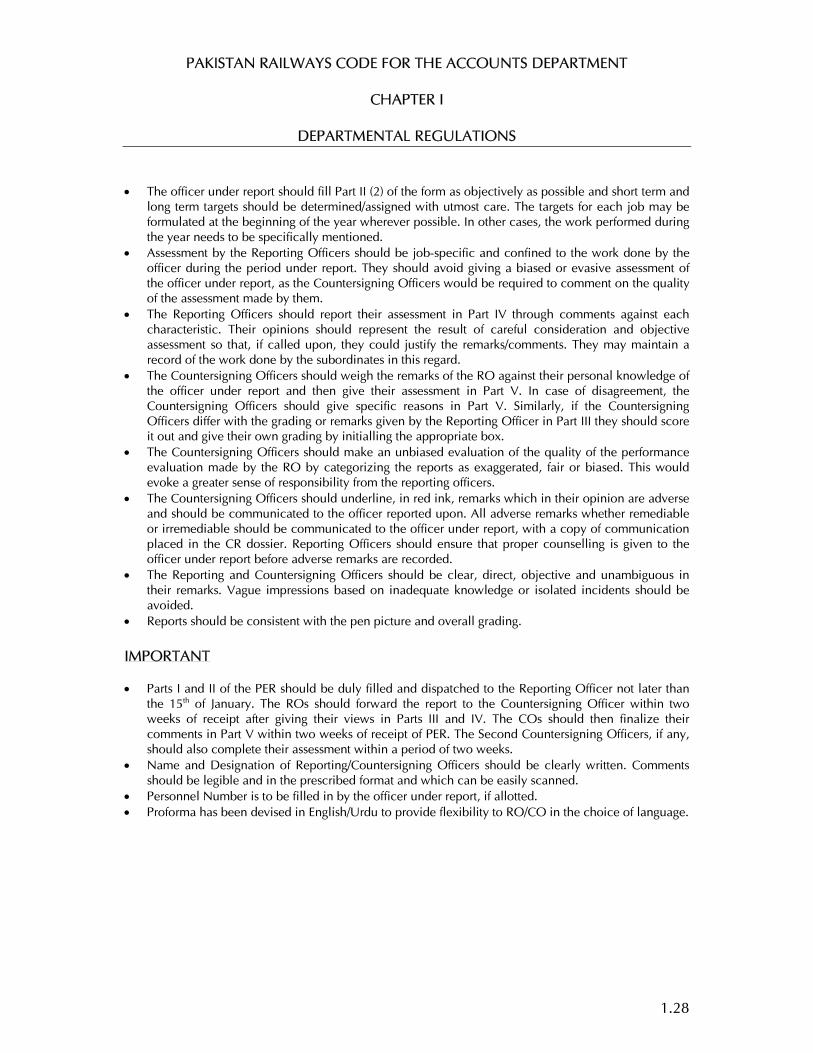

• The officer under report should fill Part II (2) of the form as objectively as possible and short term and long term targets should be determined/assigned with utmost care. The targets for each job may be formulated at the beginning of the year wherever possible. In other cases, the work performed during the year needs to be specifically mentioned.

• Assessment by the Reporting Officers should be job-specific and confined to the work done by the officer during the period under report. They should avoid giving a biased or evasive assessment of the officer under report, as the Countersigning Officers would be required to comment on the quality of the assessment made by them.

• The Reporting Officers should report their assessment in Part IV through comments against each characteristic. Their opinions should represent the result of careful consideration and objective assessment so that, if called upon, they could justify the remarks/comments. They may maintain a record of the work done by the subordinates in this regard.

• The Countersigning Officers should weigh the remarks of the RO against their personal knowledge of the officer under report and then give their assessment in Part V. In case of disagreement, the Countersigning Officers should give specific reasons in Part V. Similarly, if the Countersigning Officers differ with the grading or remarks given by the Reporting Officer in Part III they should score it out and give their own grading by initialling the appropriate box.

• The Countersigning Officers should make an unbiased evaluation of the quality of the performance evaluation made by the RO by categorizing the reports as exaggerated, fair or biased. This would evoke a greater sense of responsibility from the reporting officers.

• The Countersigning Officers should underline, in red ink, remarks which in their opinion are adverse and should be communicated to the officer reported upon. All adverse remarks whether remediable or irremediable should be communicated to the officer under report, with a copy of communication placed in the CR dossier. Reporting Officers should ensure that proper counselling is given to the officer under report before adverse remarks are recorded.

• The Reporting and Countersigning Officers should be clear, direct, objective and unambiguous in their remarks. Vague impressions based on inadequate knowledge or isolated incidents should be avoided.

• Reports should be consistent with the pen picture and overall grading. IMPORTANT • Parts I and II of the PER should be duly filled and dispatched to the Reporting Officer not later than

the 15th of January. The ROs should forward the report to the Countersigning Officer within two weeks of receipt after giving their views in Parts III and IV. The COs should then finalize their comments in Part V within two weeks of receipt of PER. The Second Countersigning Officers, if any, should also complete their assessment within a period of two weeks.

• Name and Designation of Reporting/Countersigning Officers should be clearly written. Comments should be legible and in the prescribed format and which can be easily scanned.

• Personnel Number is to be filled in by the officer under report, if allotted. • Proforma has been devised in English/Urdu to provide flexibility to RO/CO in the choice of language.

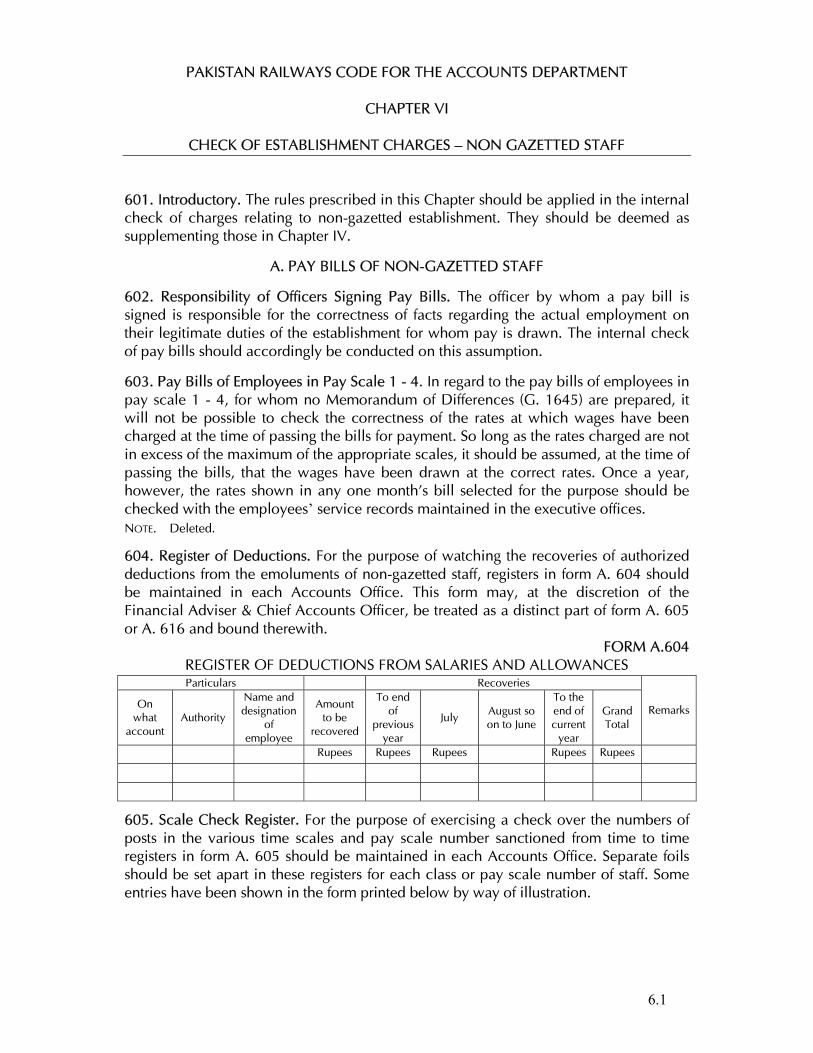

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

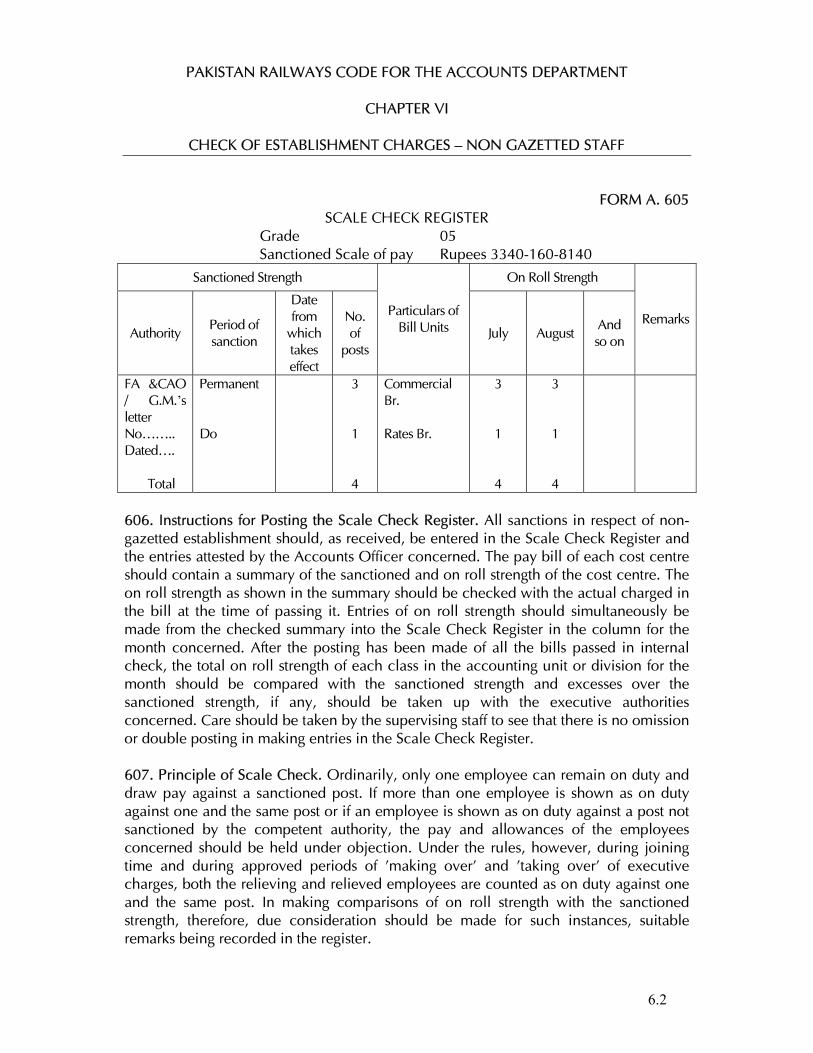

CHAPTER I

DEPARTMENTAL REGULATIONS

1.29

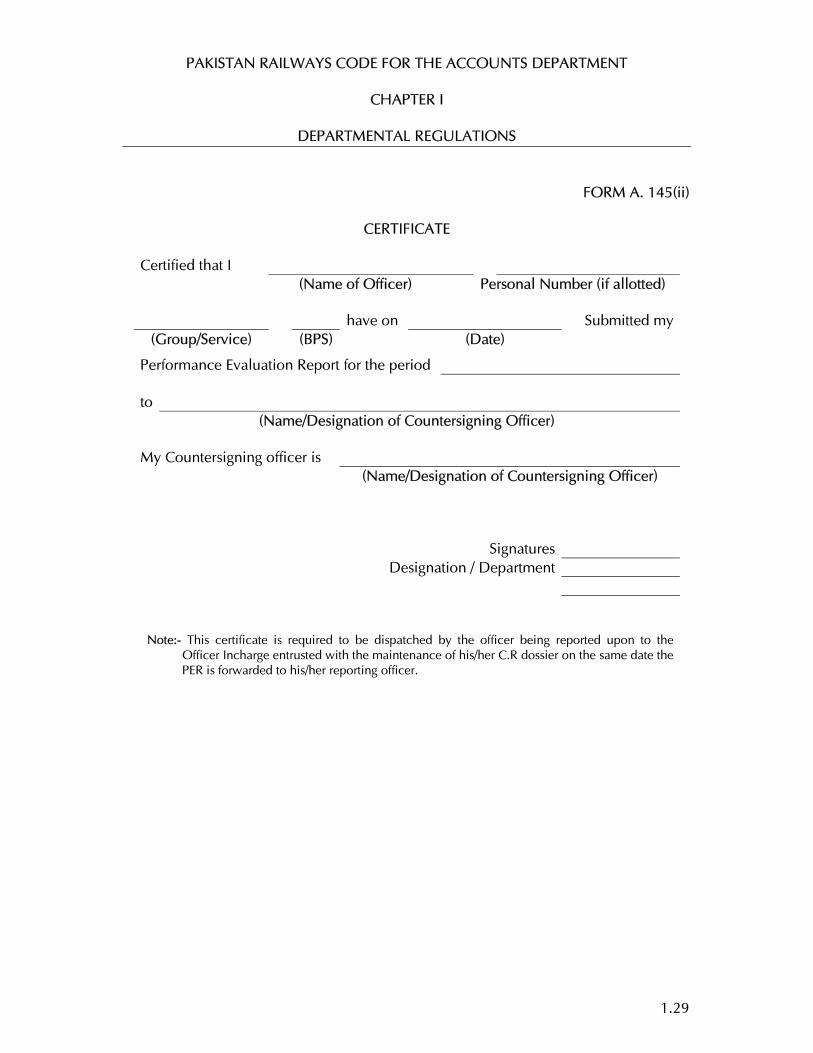

FORM A. 145(ii)

CERTIFICATE

Certified that I (Name of Officer)

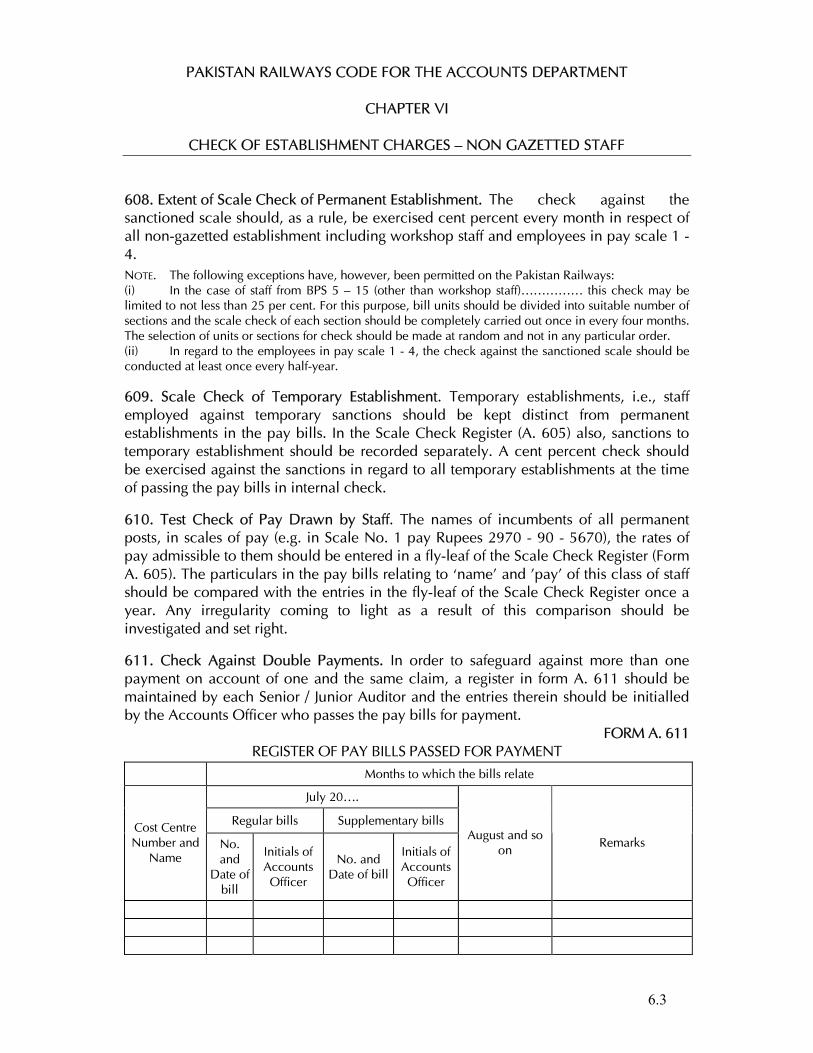

Personal Number (if allotted)

have on Submitted my(Group/Service) (BPS) (Date)

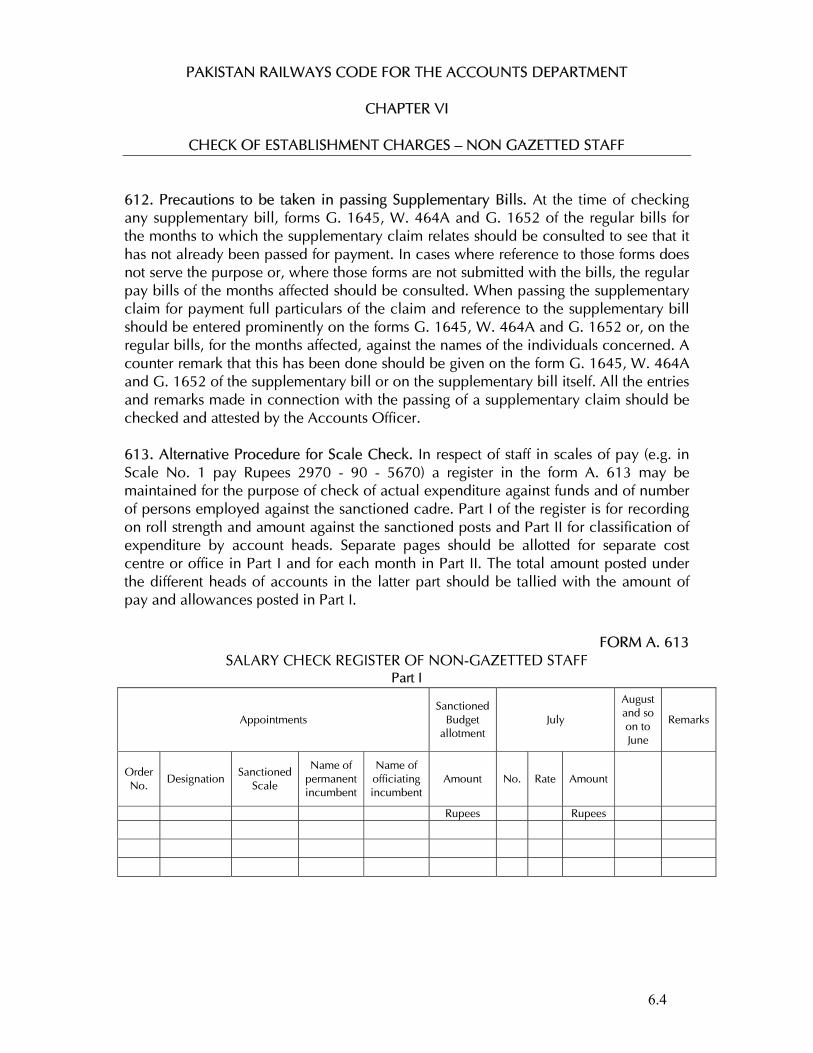

Performance Evaluation Report for the period to

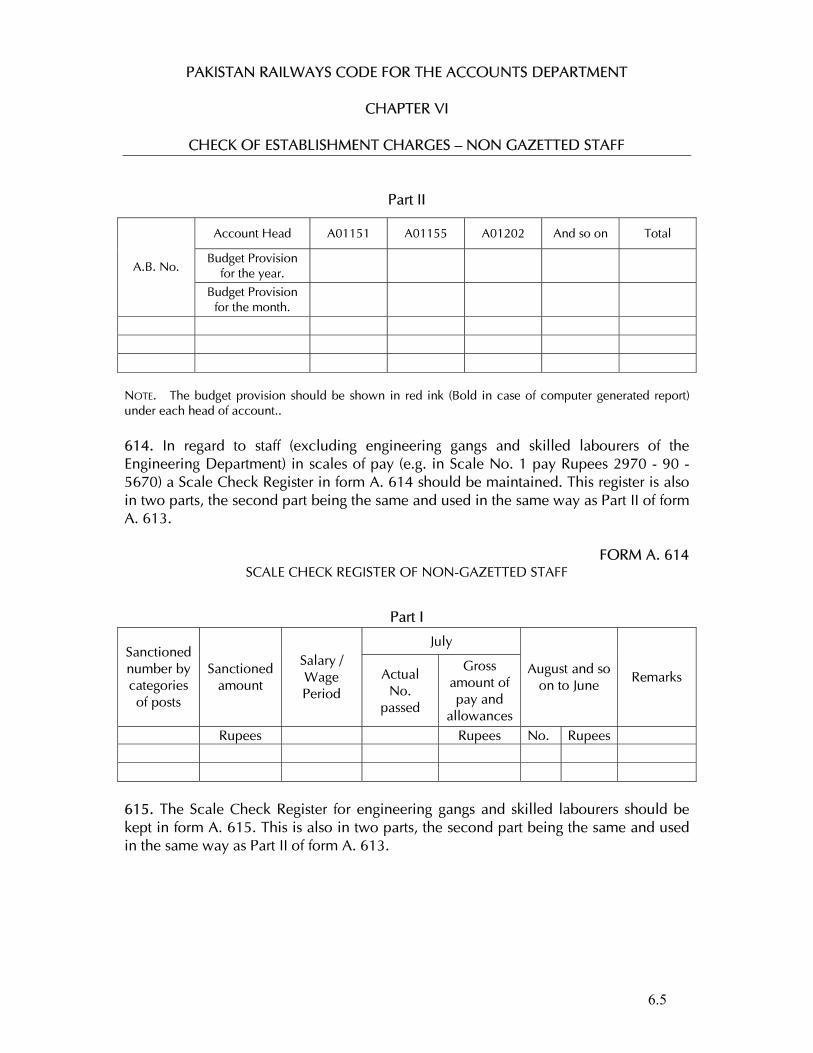

(Name/Designation of Countersigning Officer)

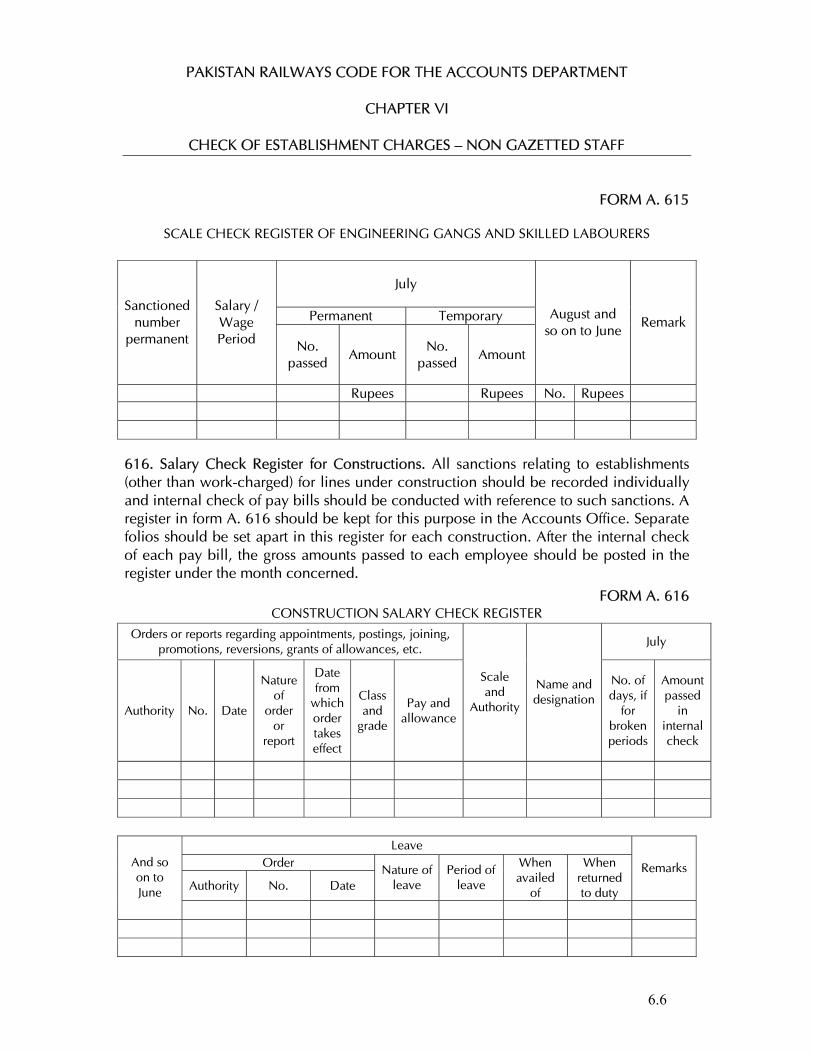

My Countersigning officer is (Name/Designation of Countersigning Officer) Signatures Designation / Department Note:- This certificate is required to be dispatched by the officer being reported upon to the

Officer Incharge entrusted with the maintenance of his/her C.R dossier on the same date the PER is forwarded to his/her reporting officer.

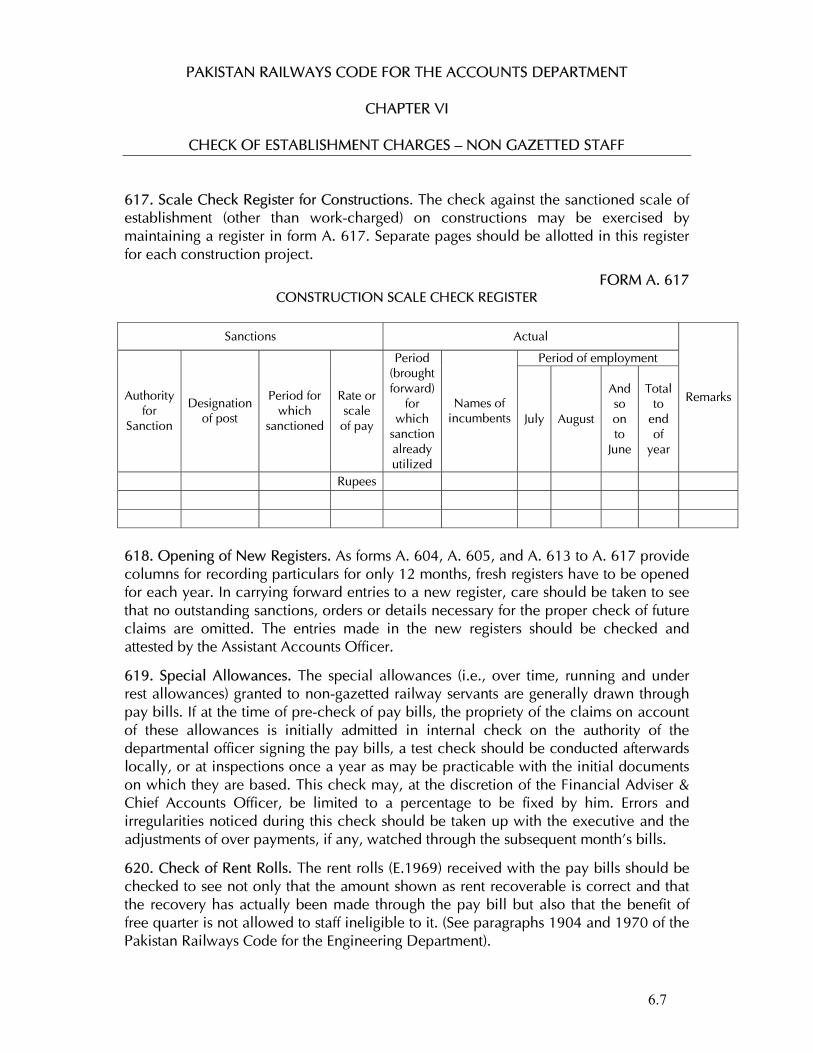

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.30

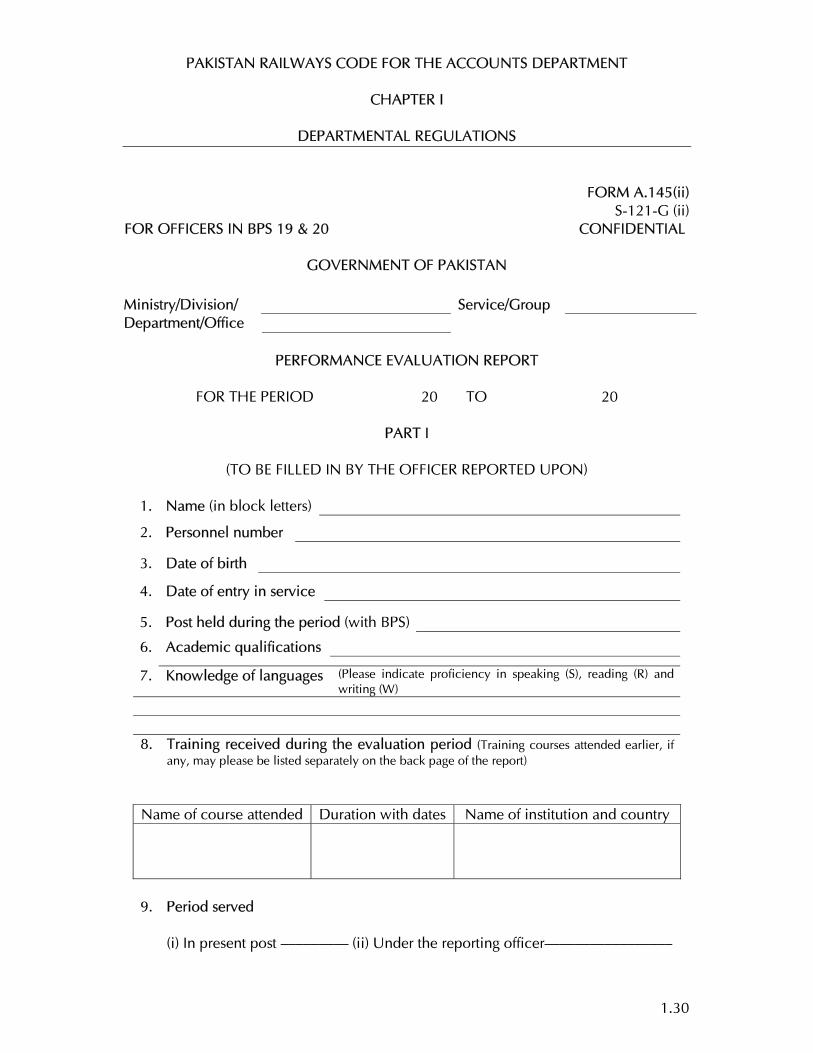

FORM A.145(ii) S-121-G (ii)

FOR OFFICERS IN BPS 19 & 20 CONFIDENTIAL

GOVERNMENT OF PAKISTAN

Service/Group Ministry/Division/ Department/Office

PERFORMANCE EVALUATION REPORT

FOR THE PERIOD 20 TO 20

PART I

(TO BE FILLED IN BY THE OFFICER REPORTED UPON)

1. Name (in block letters)

2. Personnel number

3. Date of birth

4. Date of entry in service

5. Post held during the period (with BPS)

6. Academic qualifications

7. Knowledge of languages (Please indicate proficiency in speaking (S), reading (R) and writing (W)

8. Training received during the evaluation period (Training courses attended earlier, if any, may please be listed separately on the back page of the report)

Name of course attended Duration with dates Name of institution and country

9. Period served (i) In present post ————————— (ii) Under the reporting officer—————————————————

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.31

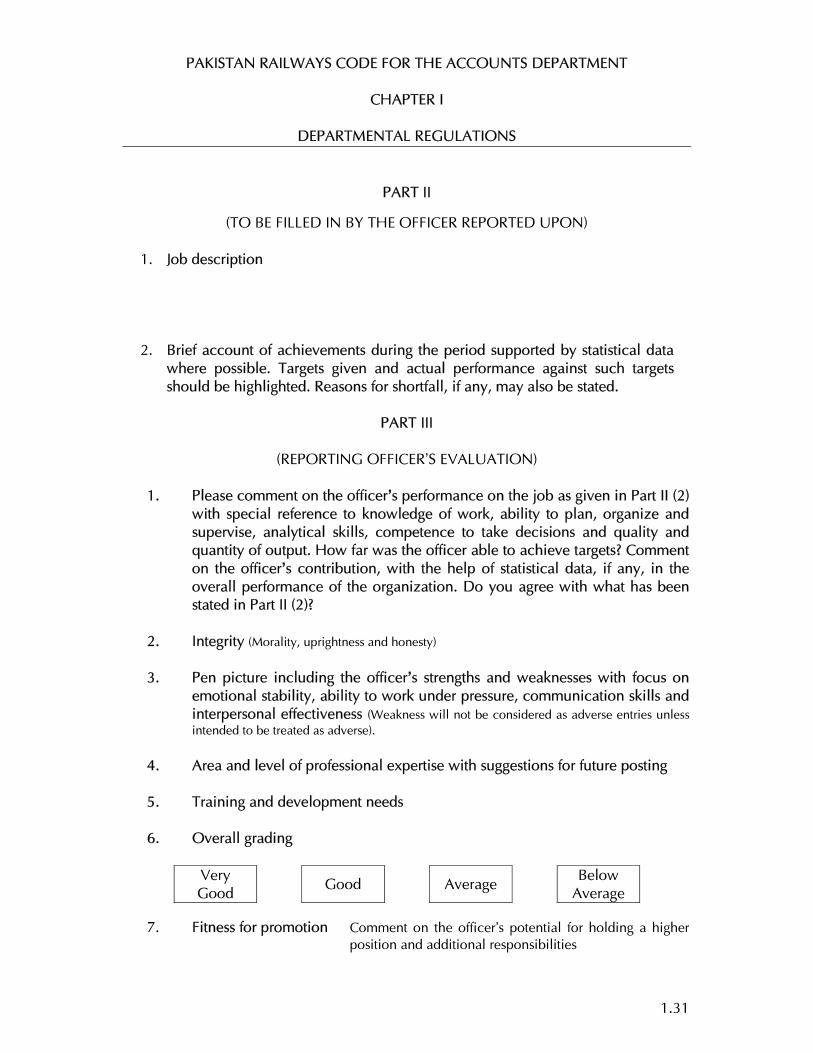

PART II

(TO BE FILLED IN BY THE OFFICER REPORTED UPON)

1. Job description

2. Brief account of achievements during the period supported by statistical data where possible. Targets given and actual performance against such targets should be highlighted. Reasons for shortfall, if any, may also be stated.

PART III

(REPORTING OFFICER’S EVALUATION)

1. Please comment on the officer’s performance on the job as given in Part II (2)

with special reference to knowledge of work, ability to plan, organize and supervise, analytical skills, competence to take decisions and quality and quantity of output. How far was the officer able to achieve targets? Comment on the officer’s contribution, with the help of statistical data, if any, in the overall performance of the organization. Do you agree with what has been stated in Part II (2)?

2. Integrity (Morality, uprightness and honesty)

3. Pen picture including the officer’s strengths and weaknesses with focus on

emotional stability, ability to work under pressure, communication skills and interpersonal effectiveness (Weakness will not be considered as adverse entries unless intended to be treated as adverse).

4. Area and level of professional expertise with suggestions for future posting

5. Training and development needs

6. Overall grading

Very Good

Good Average Below

Average

7. Fitness for promotion Comment on the officer’s potential for holding a higher position and additional responsibilities

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.32

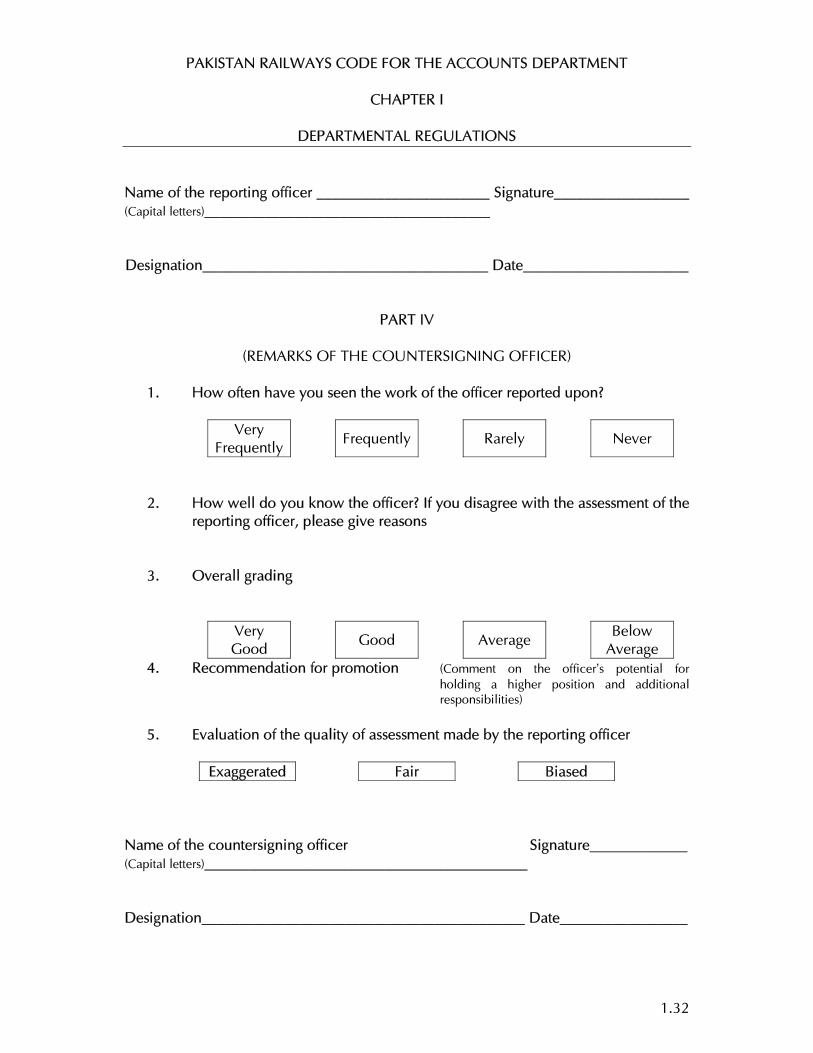

Name of the reporting officer _______________________ Signature__________________ (Capital letters)______________________________________ Designation______________________________________ Date______________________

PART IV

(REMARKS OF THE COUNTERSIGNING OFFICER)

1. How often have you seen the work of the officer reported upon?

Very Frequently

Frequently Rarely Never

2. How well do you know the officer? If you disagree with the assessment of the reporting officer, please give reasons

3. Overall grading

Very Good

Good

Average

Below Average

4. Recommendation for promotion (Comment on the officer’s potential for holding a higher position and additional responsibilities)

5. Evaluation of the quality of assessment made by the reporting officer

Exaggerated Fair Biased

Name of the countersigning officer Signature_____________ (Capital letters)___________________________________________ Designation___________________________________________ Date_________________

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.33

PART V

(REMARKS OF THE SECOND COUNTERSIGNING OFFICER (IF ANY))

Name ____________________________________________Signature_________________ Designation_______________________________________ Date_____________________ GUIDELINES FOR FILLING UP THE PER • After initiating their PERs, the officers under report should immediately fill up the detachable

‘certificate’ giving names of the RO/CO and send the same to the Officer Incharge of their respective confidential records. The exercise will ensure proper follow-up of the pending performance evaluation reports by the concerned Ministry/Division/Provincial Government etc.

• Forms should be filled in duplicate. Parts I and II are to be filled by the officer under report and should be typed. Parts III will be filled by the Reporting Officer while the Countersigning/Second Countersigning Officers will fill Parts IV and V respectively.

• Each Division, Department, autonomous body and office etc. is required to prepare specific job descriptions giving main duties of each job to be mentioned in Part-II (1). The job descriptions may be finalized with the approval of the Head of the Organization or any person authorized by him.

• The officer under report should fill Part II (2) of the form as objectively as possible and short term and long term targets should be determined/assigned with utmost care. The targets for each job may be formulated at the beginning of the year wherever possible. In other cases, the work performed during the year needs to be specifically mentioned.

• Assessment by the Reporting Officers should be job-specific and confined to the work done by the officer during the period under report. They should avoid giving a biased or evasive assessment of the officer under report, as the Countersigning Officers would be required to comment on the quality of the assessment made by them.

• The Reporting Officers should report their assessment in Part III through comments against each characteristic. Their opinions should represent the result of careful consideration and objective assessment so that, if called upon, they could justify the remarks/comments. They may maintain a record of the work done by the subordinates in this regard.

• The Reporting Officers should be careful in giving the overall and comparative gradings. Special care should be taken so that no officer is placed at an undue disadvantage.

• The Countersigning Officers should weigh the remarks of the RO against their personal knowledge of the officer under report, compare him with other officers of the same grade working under different Reporting Officers, but under the same Countersigning Officer, and then give their overall assessment of the officer. In case of disagreement with the assessment done by the Reporting Officer, specific reasons should be recorded by the Countersigning Officers in Part IV (2).

• The Countersigning Officers should make an unbiased evaluation of the quality of the performance evaluation made by the RO by categorizing the reports as exaggerated, fair or biased. This would evoke a greater sense of responsibility from the reporting officers.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.34

• The Countersigning Officers should underline, in red ink, remarks which in their opinion are adverse and should be communicated to the officer reported upon. All adverse remarks whether remediable or irremediable should be communicated to the officer under report, with a copy of communication placed in the CR dossier. Reporting Officers should ensure that they properly counsel the officer under report before adverse remarks are recorded.

• The Reporting and Countersigning Officers should be clear, direct, objective and unambiguous in their remarks. Vague impressions based on inadequate knowledge or isolated incidents should be avoided.

• Reports should be consistent with the pen picture, overall grading and comparative grading.

IMPORTANT • Parts I and II of the PER should be duly filled and dispatched to the Reporting Officer not later than

the 15th of January. The ROs should forward the report to the Countersigning Officer within two weeks of receipt after giving their views in Parts III. The COs should then finalize their comments in Part IV within two weeks of receipt of PER. The Second Countersigning Officers, if any, should also complete their assessment within a period of two weeks.

• Name and Designation of Reporting/Countersigning Officers should be clearly written. Comments should be legible and in the prescribed format and which can be easily scanned.

• Personnel Number is to be filled in by the officer under report, if allotted. • Proforma has been devised in English/Urdu to provide flexibility to RO/CO in the choice of language. • Comparative grading only applies to officers falling in very good, good and average categories. This

grading would not apply to anyone falling in below average category in Part III (6).

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.35

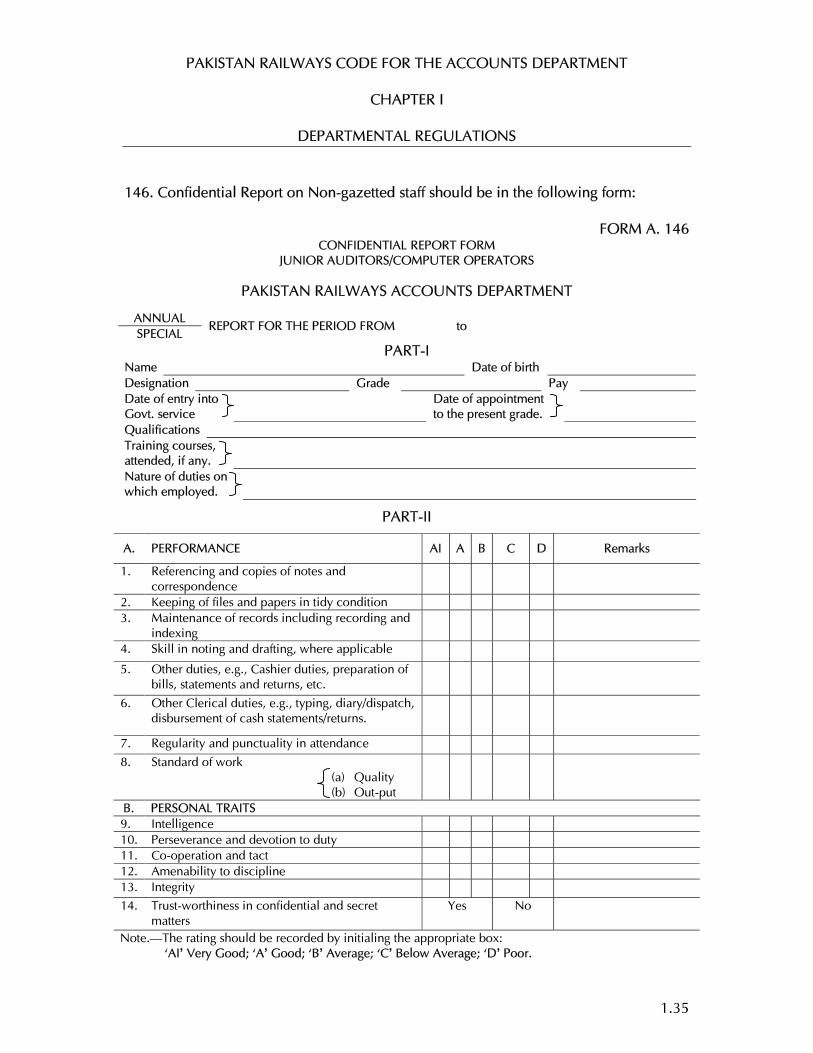

146. Confidential Report on Non-gazetted staff should be in the following form:

FORM A. 146 CONFIDENTIAL REPORT FORM

JUNIOR AUDITORS/COMPUTER OPERATORS

PAKISTAN RAILWAYS ACCOUNTS DEPARTMENT

ANNUAL SPECIAL

REPORT FOR THE PERIOD FROM to

PART-I Name Date of birth Designation Grade Pay Date of entry into Govt. service

Date of appointment to the present grade.

Qualifications Training courses, attended, if any.

Nature of duties on which employed.

PART-II

A. PERFORMANCE AI A B C D Remarks

1. Referencing and copies of notes and correspondence

2. Keeping of files and papers in tidy condition 3. Maintenance of records including recording and

indexing

4. Skill in noting and drafting, where applicable

5. Other duties, e.g., Cashier duties, preparation of bills, statements and returns, etc.

6. Other Clerical duties, e.g., typing, diary/dispatch, disbursement of cash statements/returns.

7. Regularity and punctuality in attendance

8. Standard of work (a) Quality (b) Out-put

B. PERSONAL TRAITS 9. Intelligence 10. Perseverance and devotion to duty 11. Co-operation and tact 12. Amenability to discipline 13. Integrity 14. Trust-worthiness in confidential and secret

matters

Yes No

Note.–The rating should be recorded by initialing the appropriate box: ‘AI’ Very Good; ‘A’ Good; ‘B’ Average; ‘C’ Below Average; ‘D’ Poor.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.36

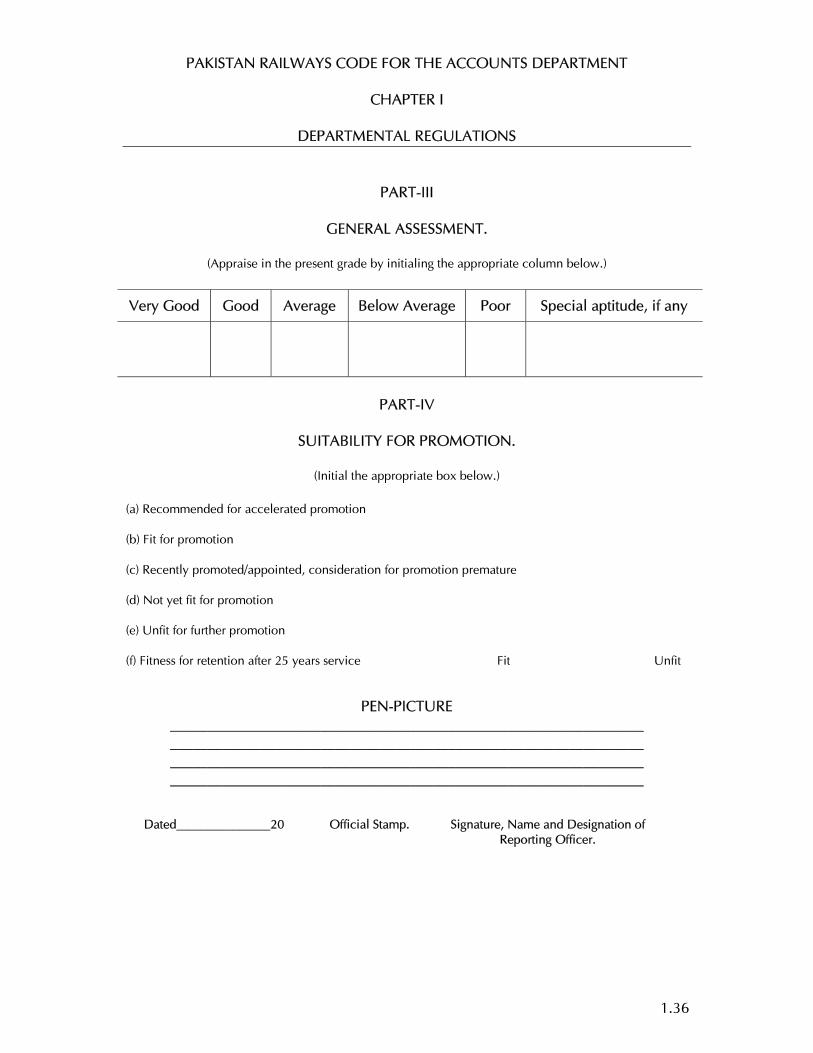

PART-III

GENERAL ASSESSMENT.

(Appraise in the present grade by initialing the appropriate column below.)

Very Good Good Average Below Average Poor Special aptitude, if any

PART-IV

SUITABILITY FOR PROMOTION.

(Initial the appropriate box below.)

(a) Recommended for accelerated promotion (b) Fit for promotion (c) Recently promoted/appointed, consideration for promotion premature (d) Not yet fit for promotion (e) Unfit for further promotion (f) Fitness for retention after 25 years service Fit Unfit

PEN-PICTURE _______________________________________________________________ _______________________________________________________________ _______________________________________________________________ _______________________________________________________________

Dated_______________20 Official Stamp. Signature, Name and Designation of Reporting Officer.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.37

PART-V

REMARKS OF THE COUNTERSIGNING OFFICER.

_______________________________________________________________ _______________________________________________________________ _______________________________________________________________

Dated_______________20 Official Stamp. Signature, Name and Designation.

A. INSTRUCTIONS FOR MINISTRIES, DEPARTMENTS, ETC.

1. The reports will be initialed by the Branch/Section Officer incharge and will be countersigned by the next higher officer, both being concerned with the work of the person reported upon.

2. When an adverse remark is made in the confidential report of the official reported upon, a copy of the whole report should be furnished to him at the earliest opportunity and in any case within one month from the date the report is countersigned with a memorandum a copy of which should be signed and returned by him in acknowledgement of the report and be in turn placed in the character roll for record. A serious view should be taken of any failure on the part or the official concerned to furnish a copy of the report containing adverse remarks to the person reported upon.

3. The officials making representations against adverse remarks recorded in their confidential reports should not make any personal remark or remarks against the integrity of the reporting officers. Violation of this rule will be considered misconduct and will also render the representation liable to be summarily rejected.

4. When a report is built upon or the individual opinions of the reporting and countersigning officers it is only the opinion as accepted by the latter which should be communicated.

5. Remarks in case where the reporting/countersigning officer suspends judgment should not be communicated.

6. Any remarks to the effect that the person reported upon has or has not taken steps to remedy the defects pointed out to him in a previous year should also be communicated.

7. The adverse remarks should be communicated by the senior officer incharge of establishment matters to the Ministry/Division/Department/Office concerned.

8. Annual Confidential Report containing adverse remarks should not be taken into consideration until they have been communicated following rule A-2 above and a decision taken on the representation, if any, of the person reported upon.

B. INSTRUCTIONS FOR THE OFFICERS RESPONSIBLE FOR THE CUSTODY OF CHARACTER ROLES.

1. Arrange for the completion of the routine part of the form and send it to the reporting officer

concerned. 2. On receipt of the completed form from the reporting officer submit it along with relevant

character roll to the countersigning officer concerned. 3. Go through each report carefully in order to see if there are any adverse remarks underlined in

red ink. If so, arrange to have them communicated to the person concerned immediately with the Direction that his representation, if any should be submitted within a fortnight of the receipt of those remarks by him.

PAKISTAN RAILWAYS CODE FOR THE ACCOUNTS DEPARTMENT

CHAPTER I

DEPARTMENTAL REGULATIONS

1.38

4. Arrange to obtain a decision on the representation, if any and communicate it to the official concerned within the month. Place a copy of the decision in the dossier.

5. Keep the duplicate as well as the original copies of the confidential reports in your office. 6. If an official has been receiving adverse remarks for two successive years from the same

reporting officer, take up the question of placing him under another reporting officer.

C. INSTRUCTIONS FOR THE REPORTING OFFICERS.

1. While reporting on your subordinates:-- (i) Be as objective as possible. (ii) Be as circumspect as possible. (iii) Be clear and direct, not ambiguous or evasive in your remarks. (iv) Avoid exaggeration and gross understatement.

2. State whether any of the defects reported have already been brought to the notice of the person concerned and also whether he has or has not taken steps to remedy them.

3. Fill his form in duplicate and affix your signature in both, at the end of the general remarks. 4. After remarking relevant entries send the form to the officer responsible for the custody of the

character roll.

D. INSTRUCTIONS FOR THE COUNTERSIGNING OFFICERS.

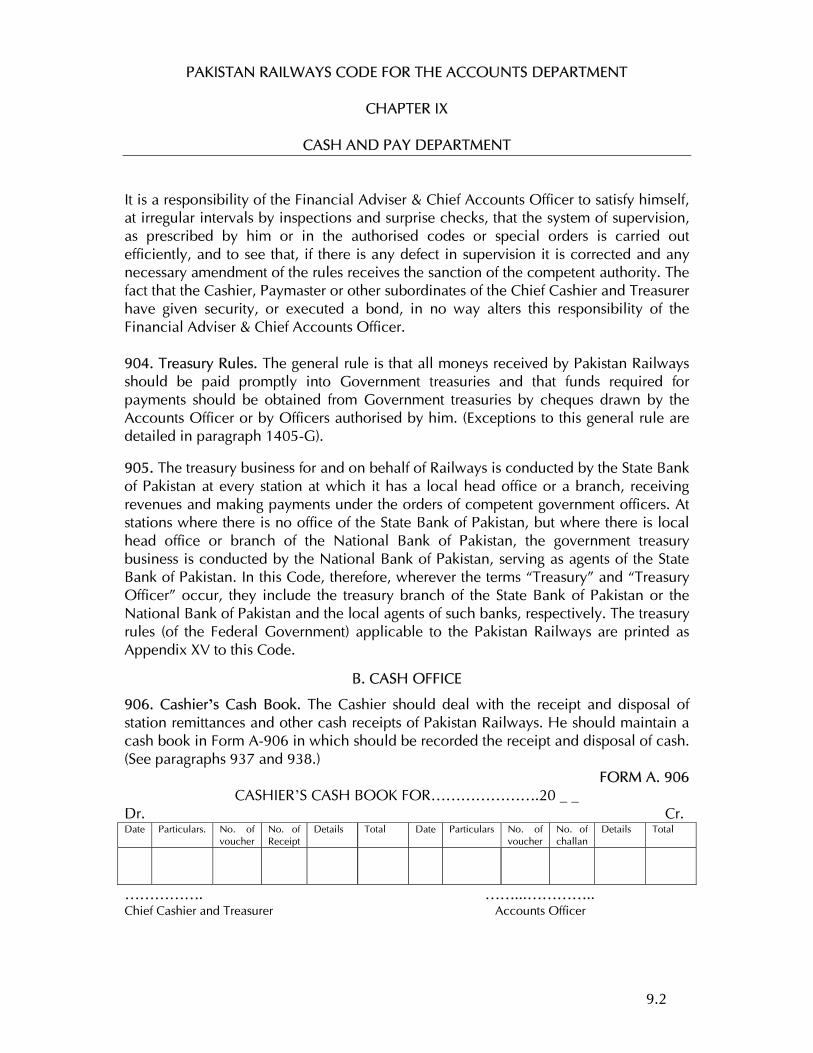

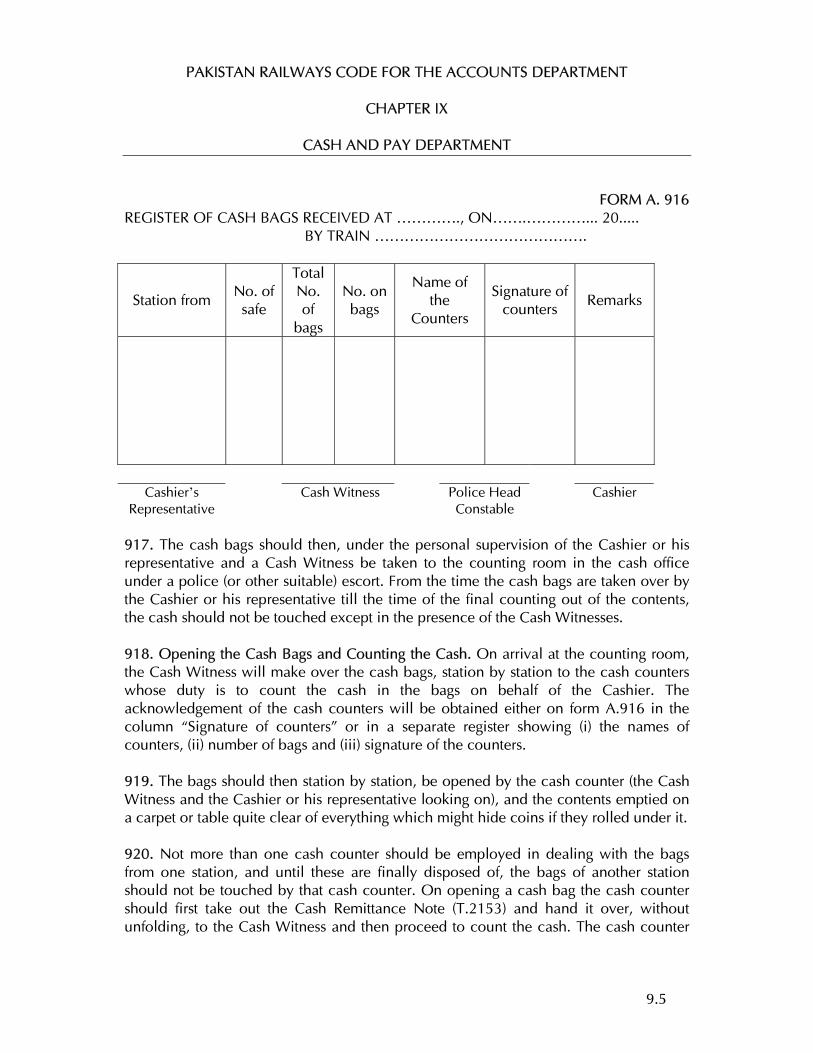

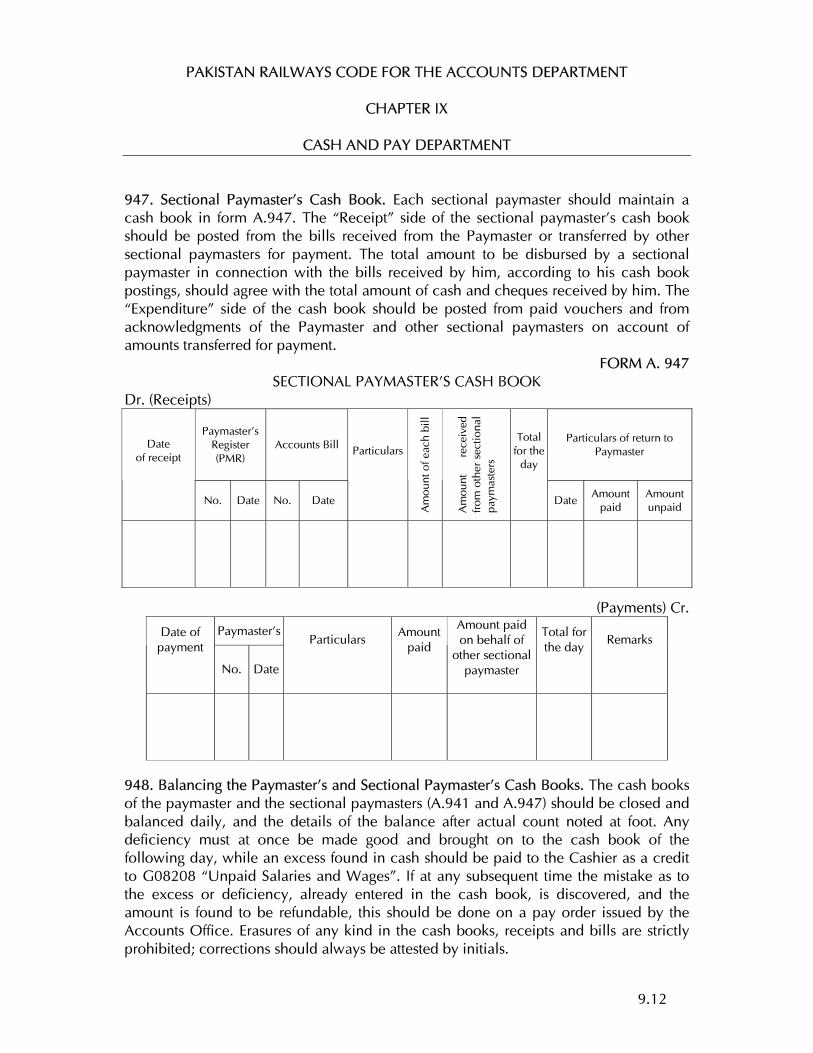

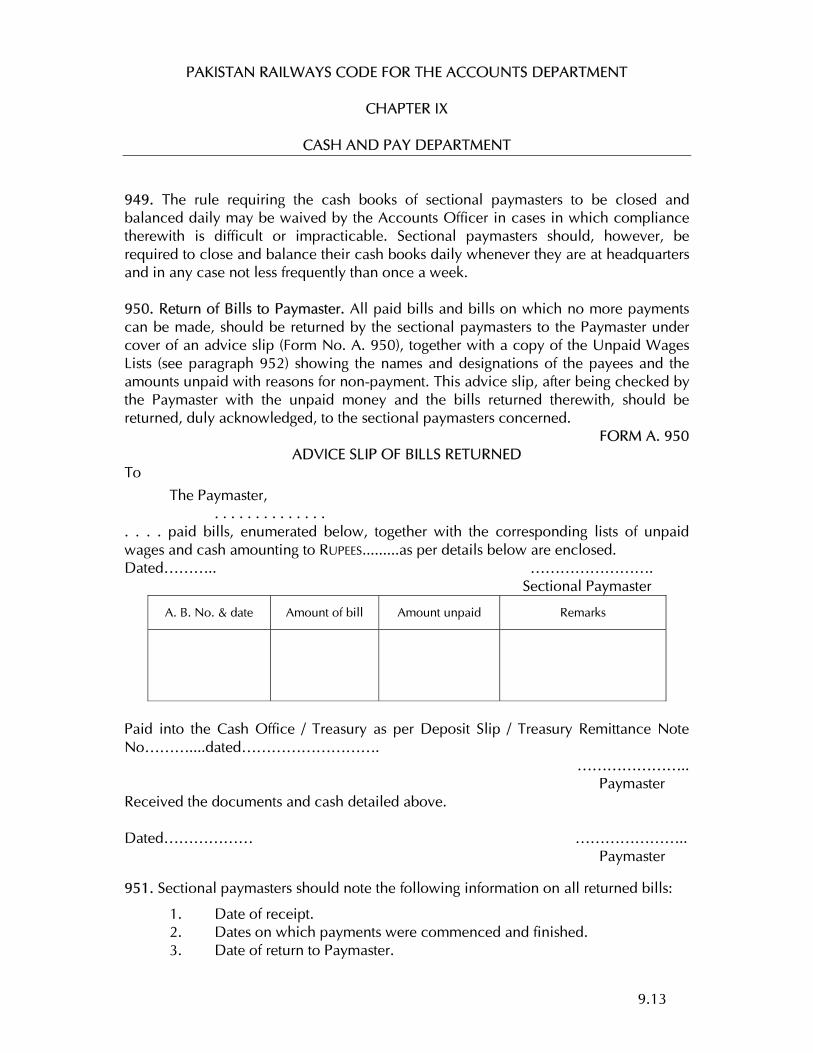

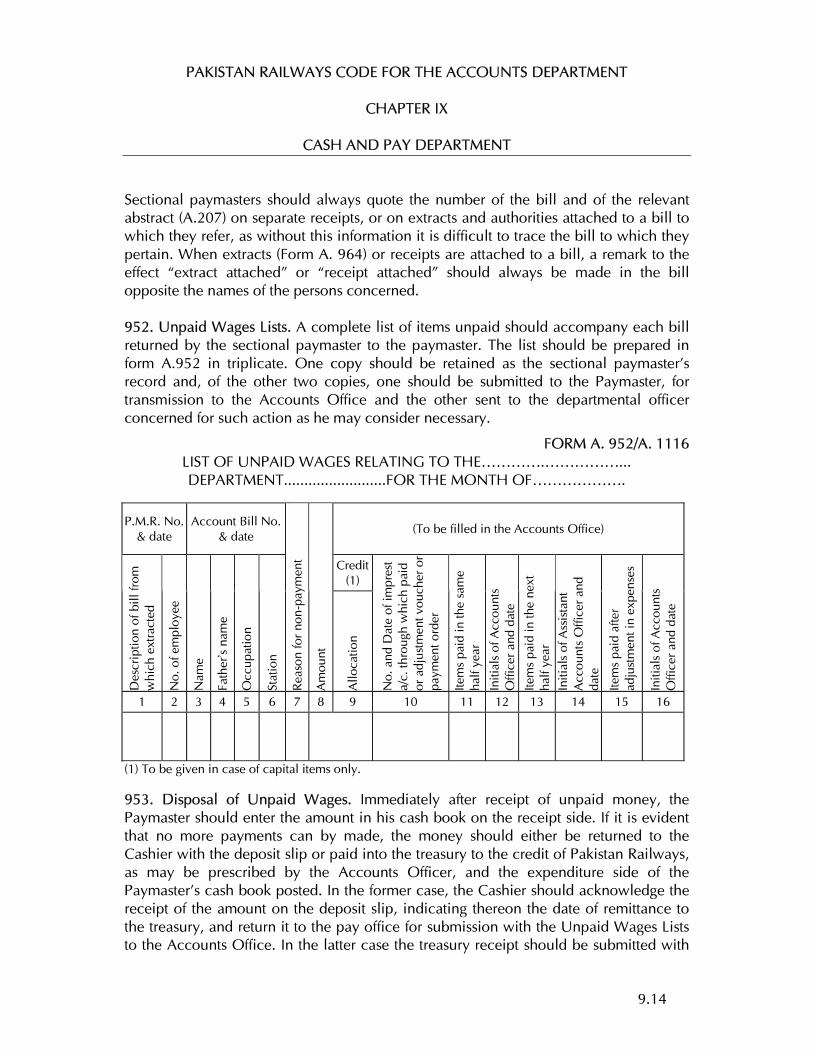

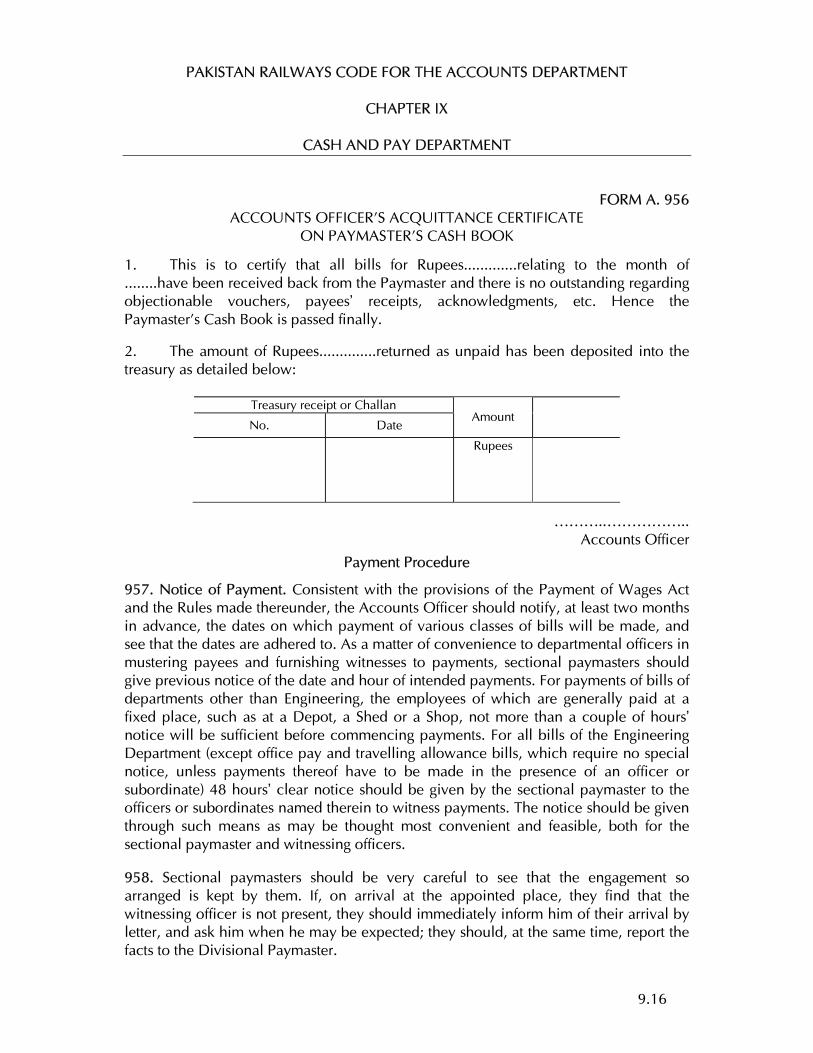

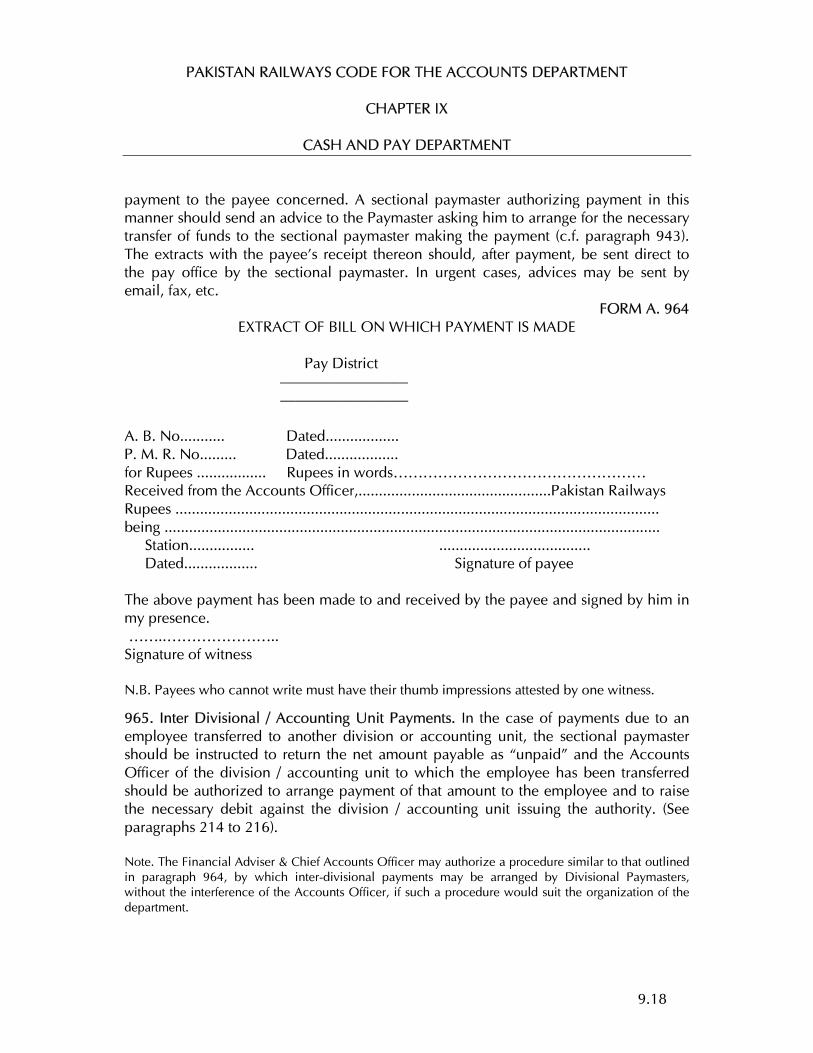

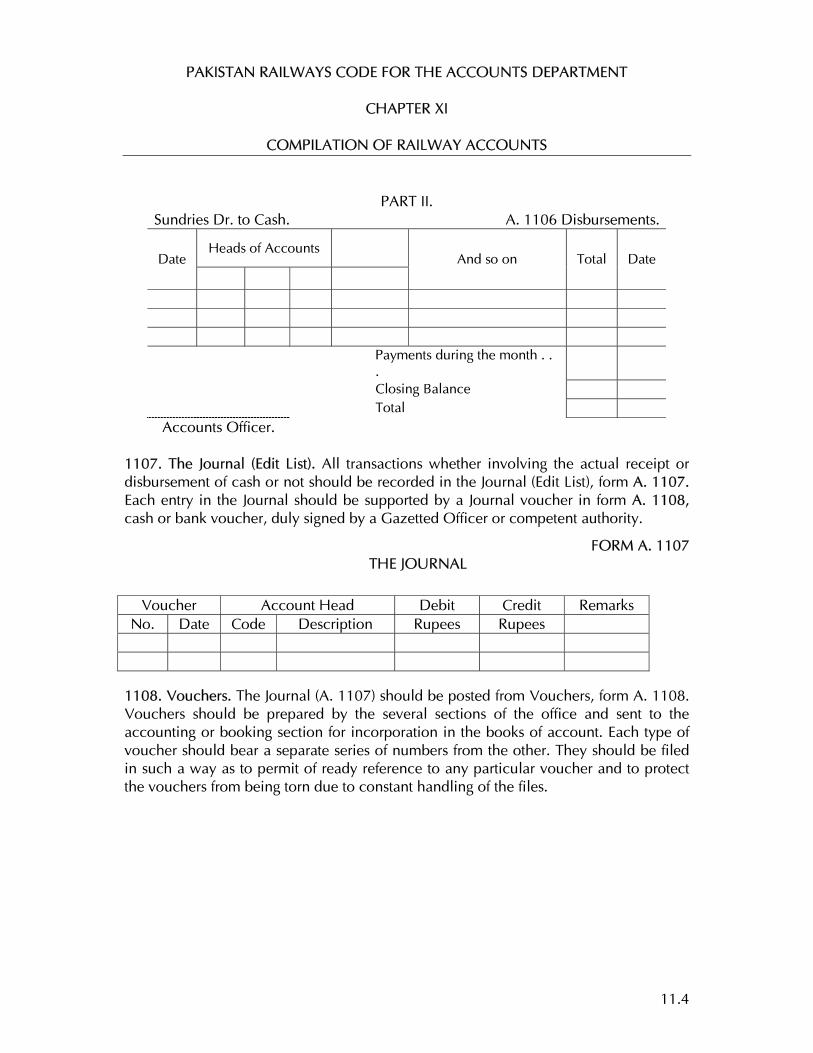

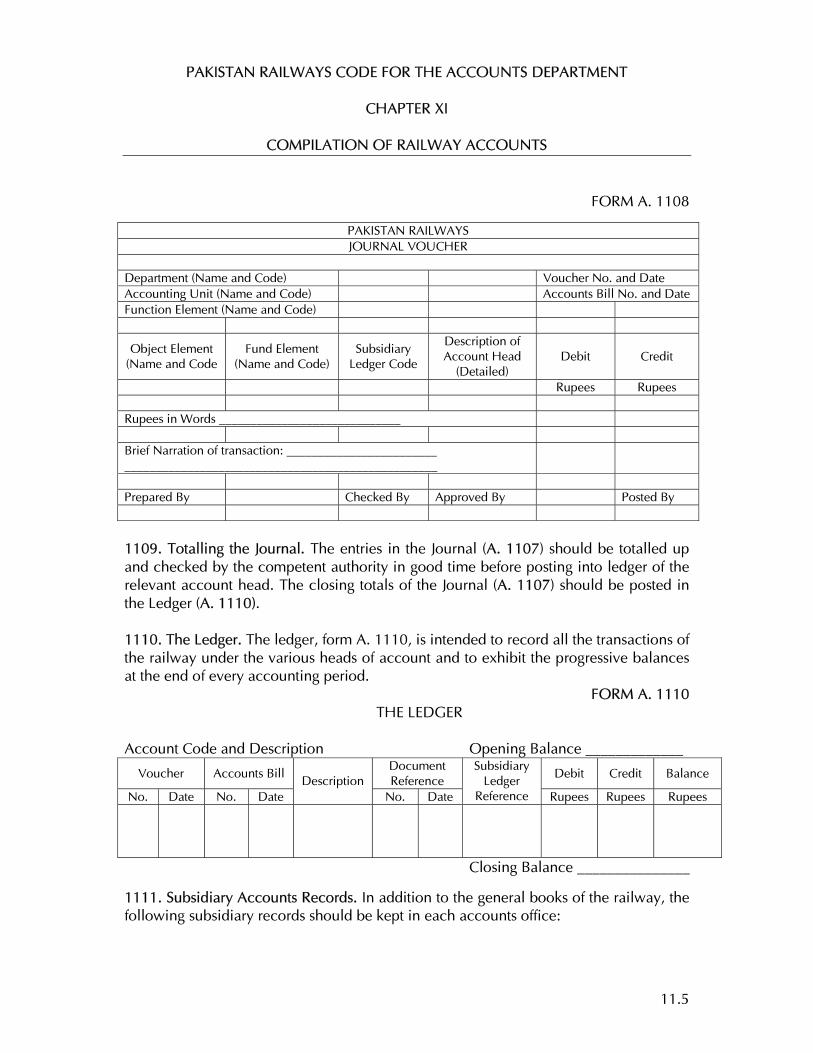

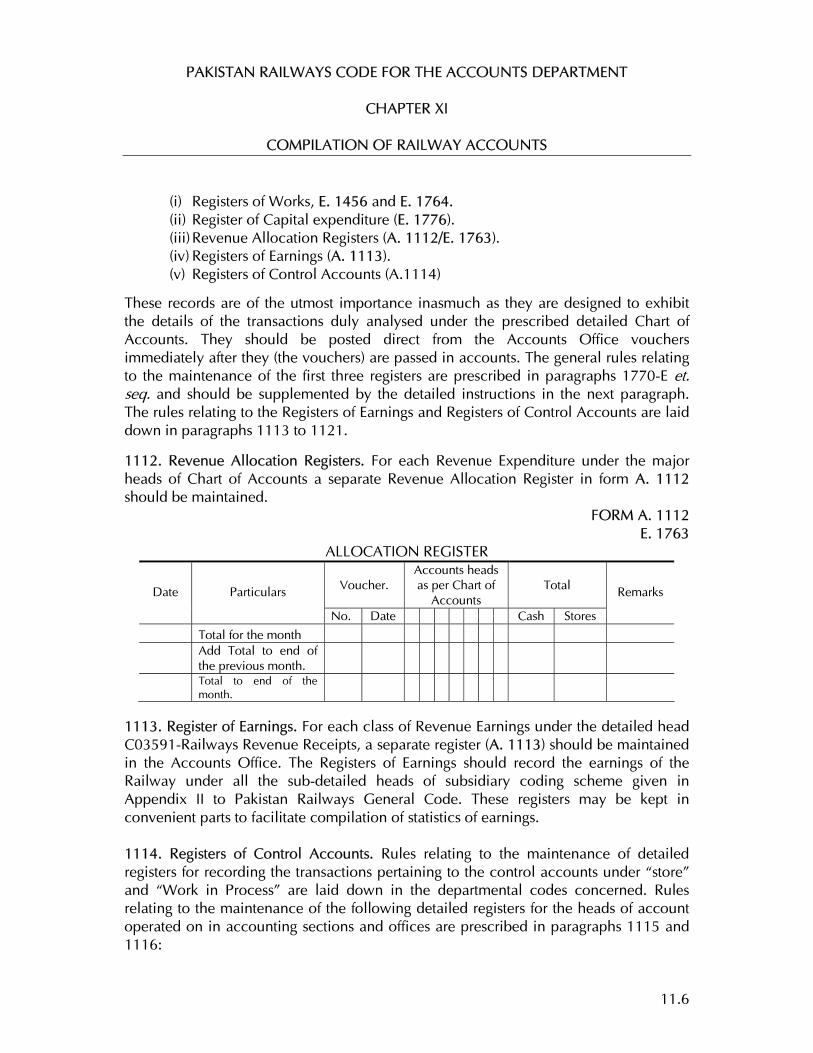

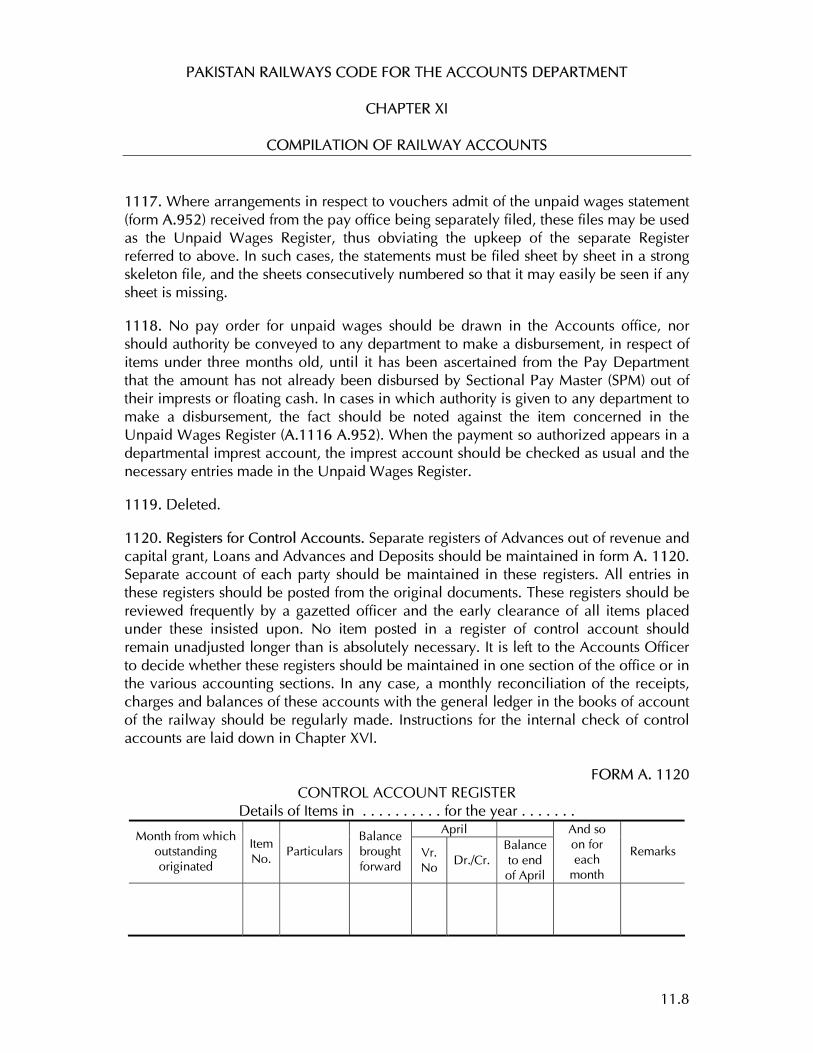

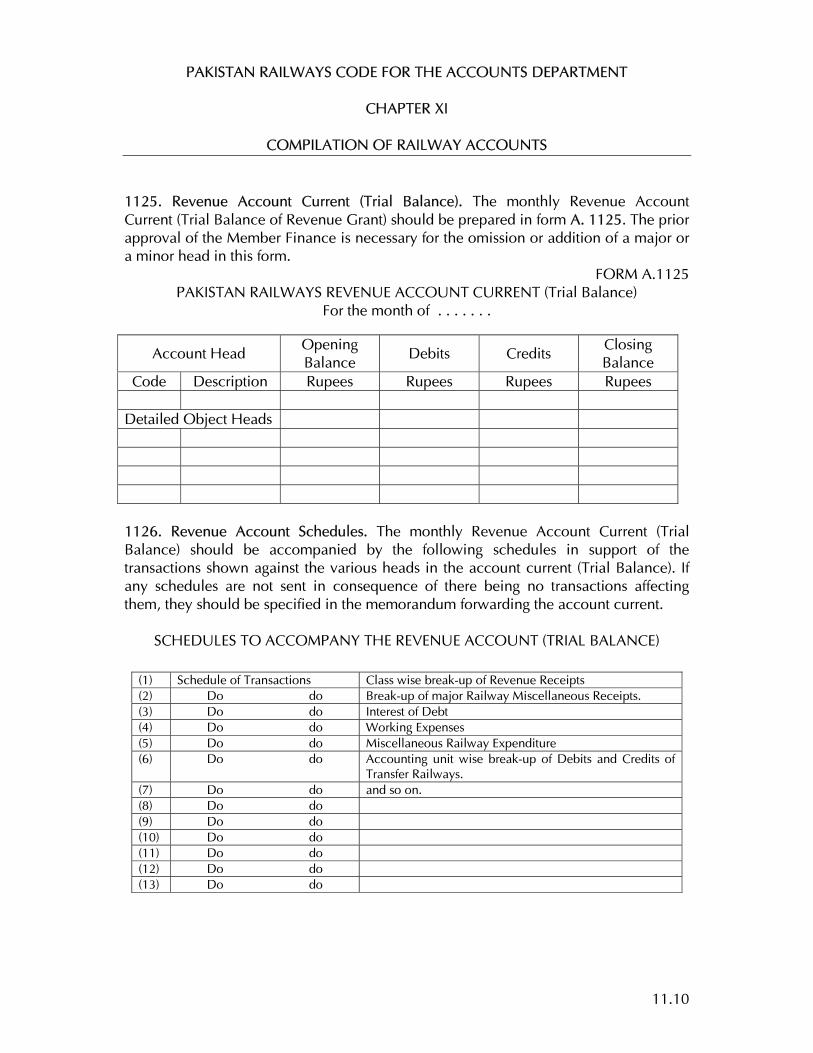

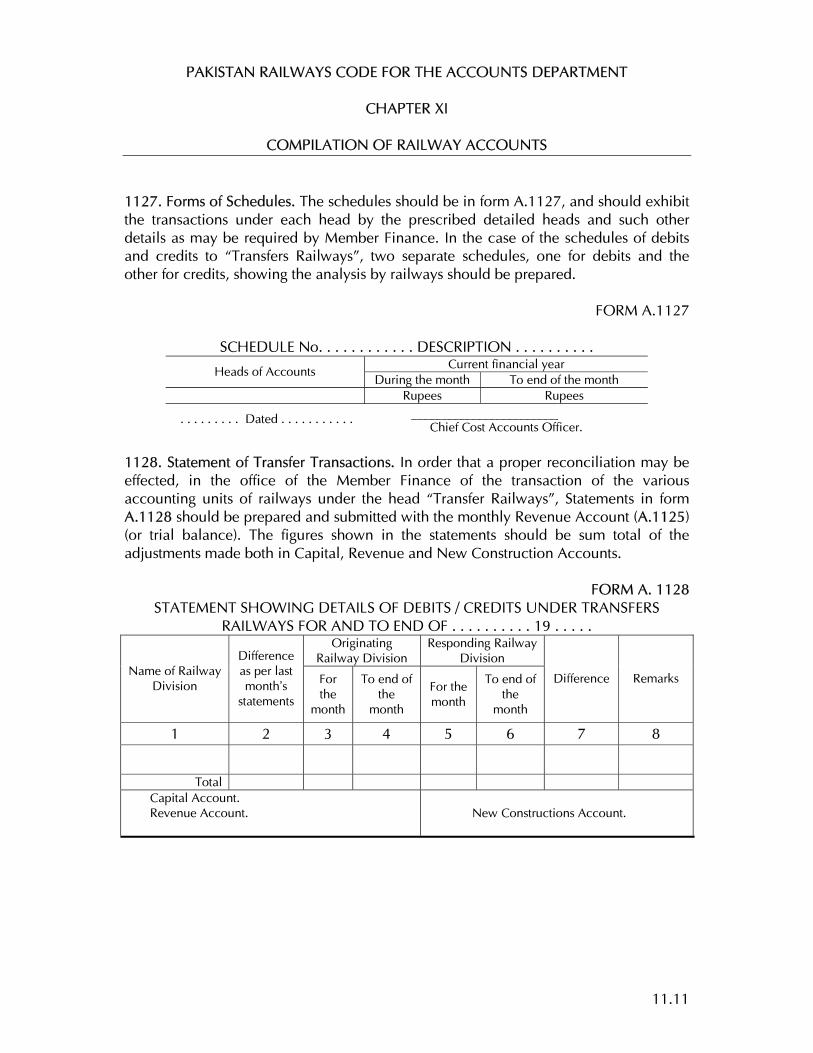

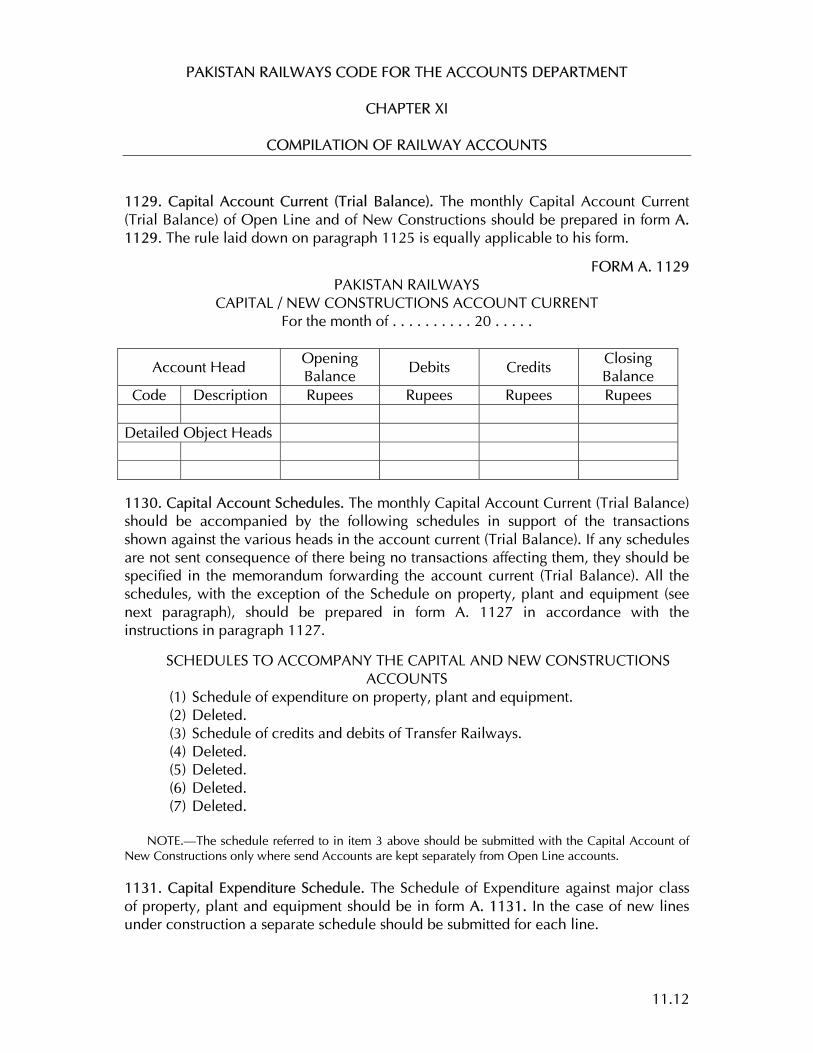

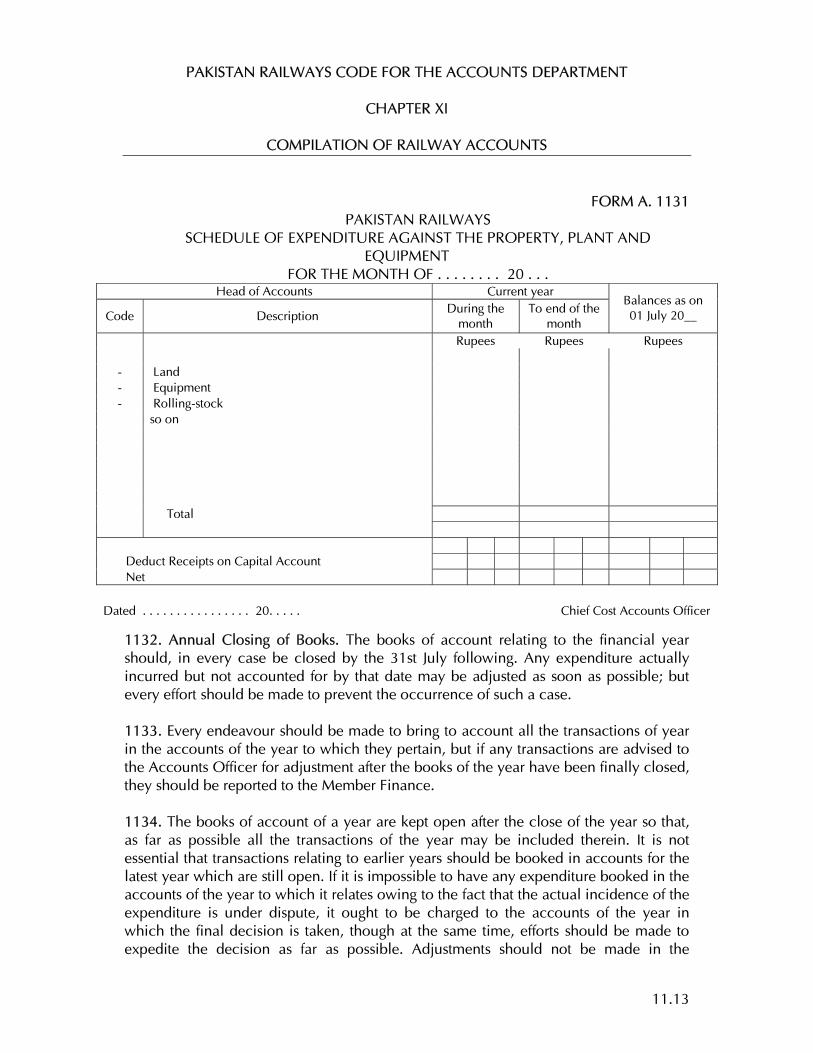

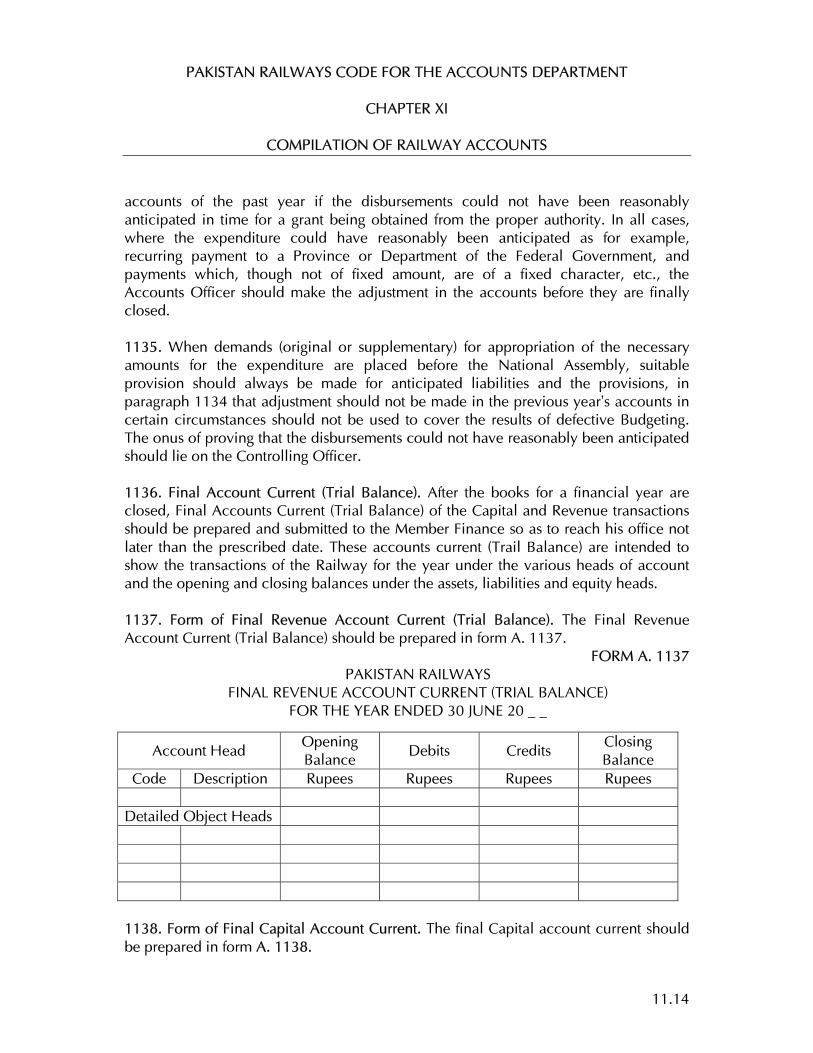

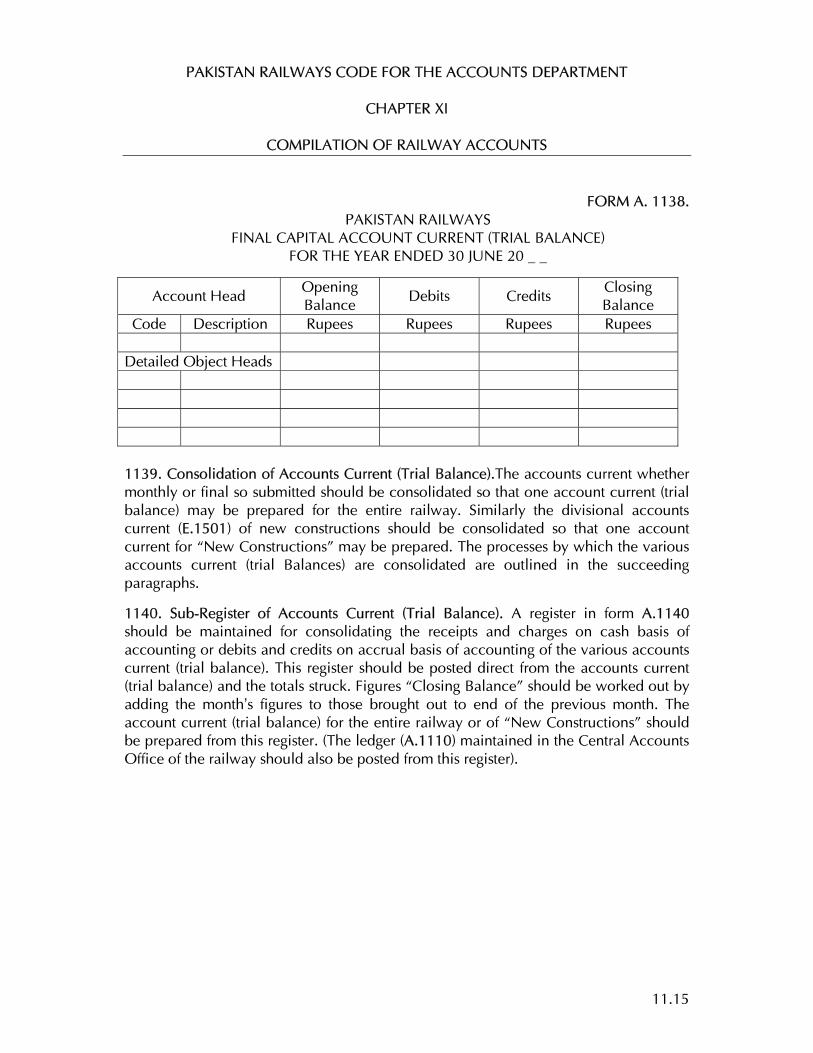

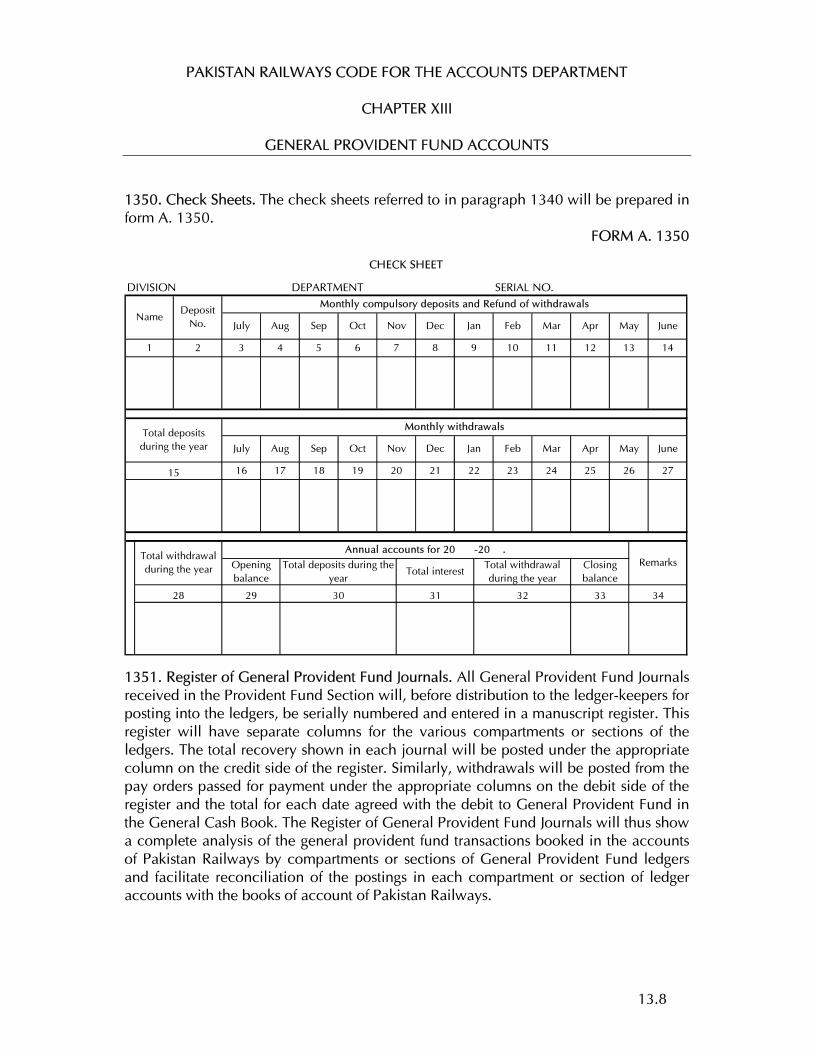

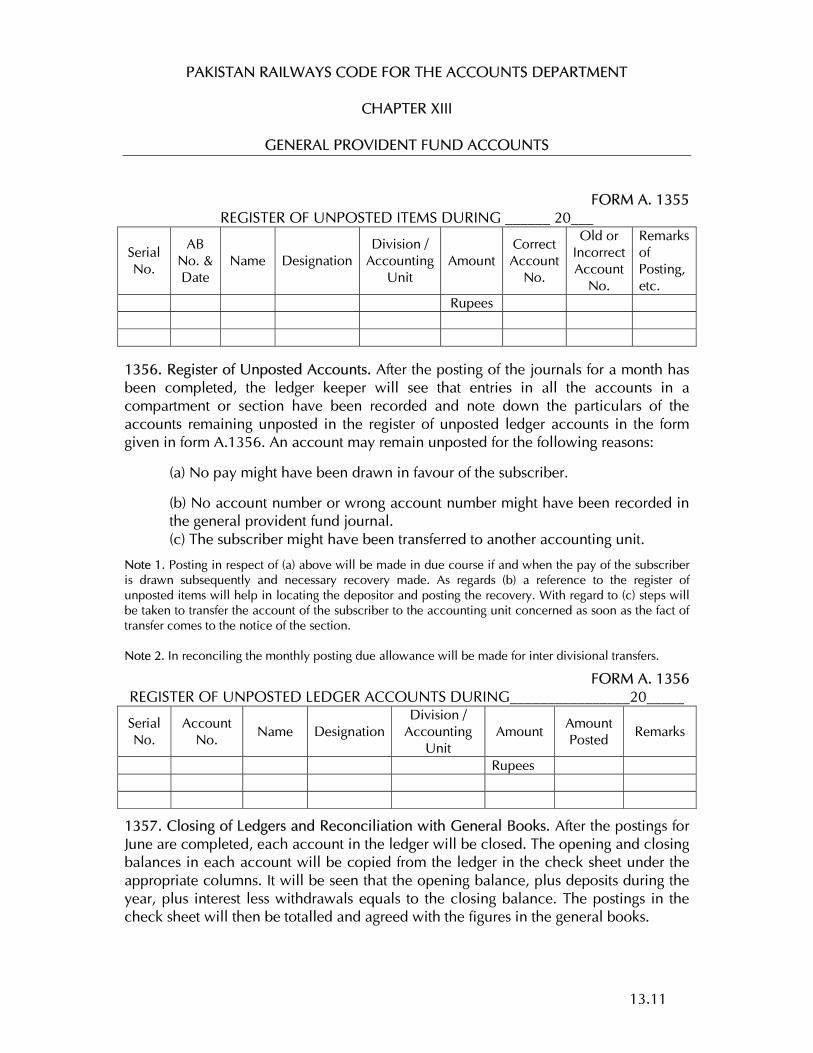

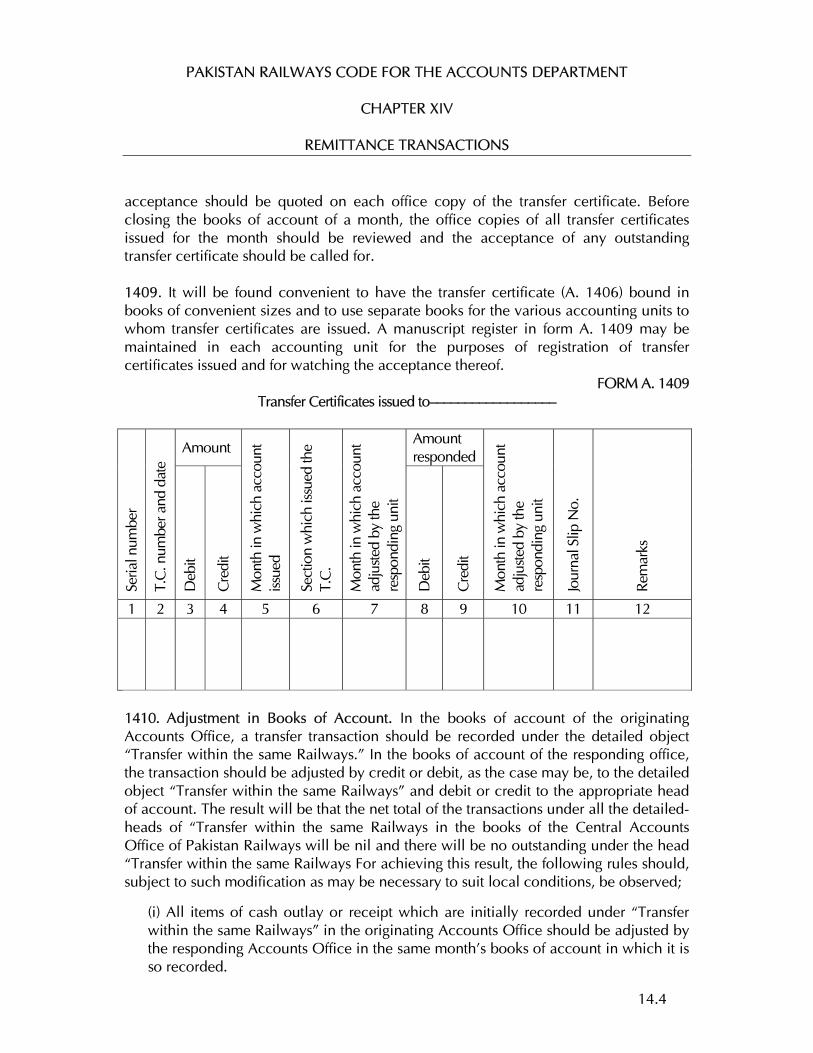

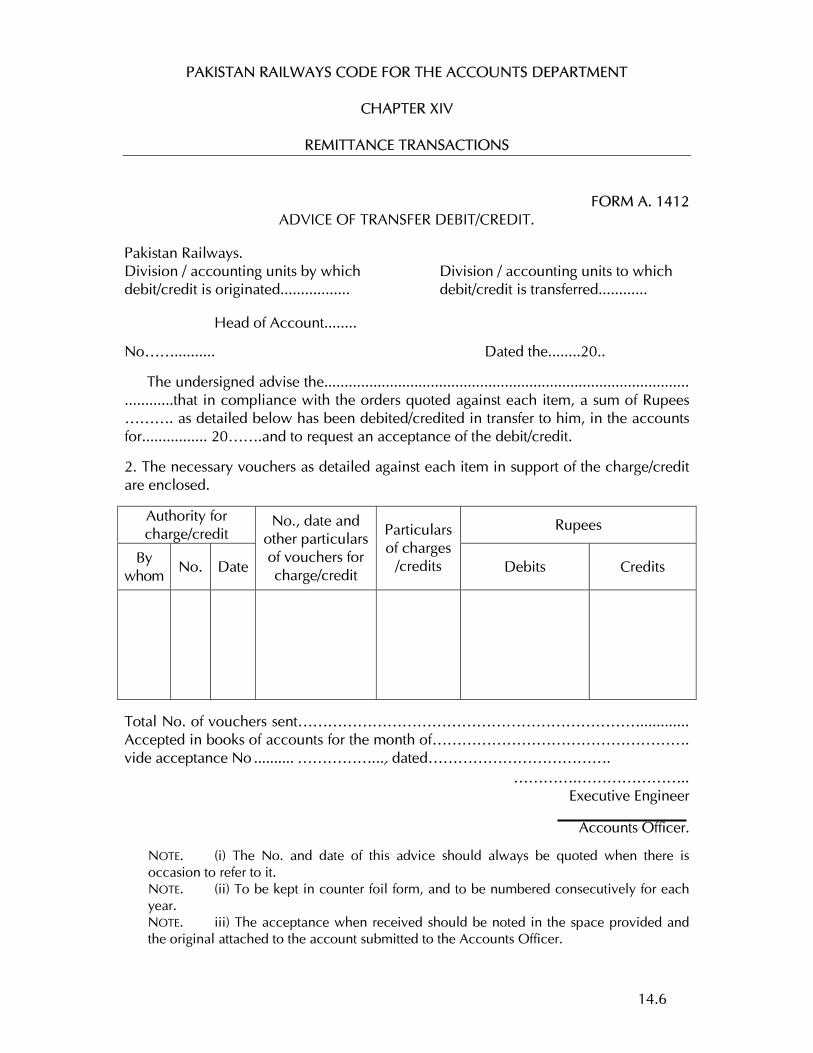

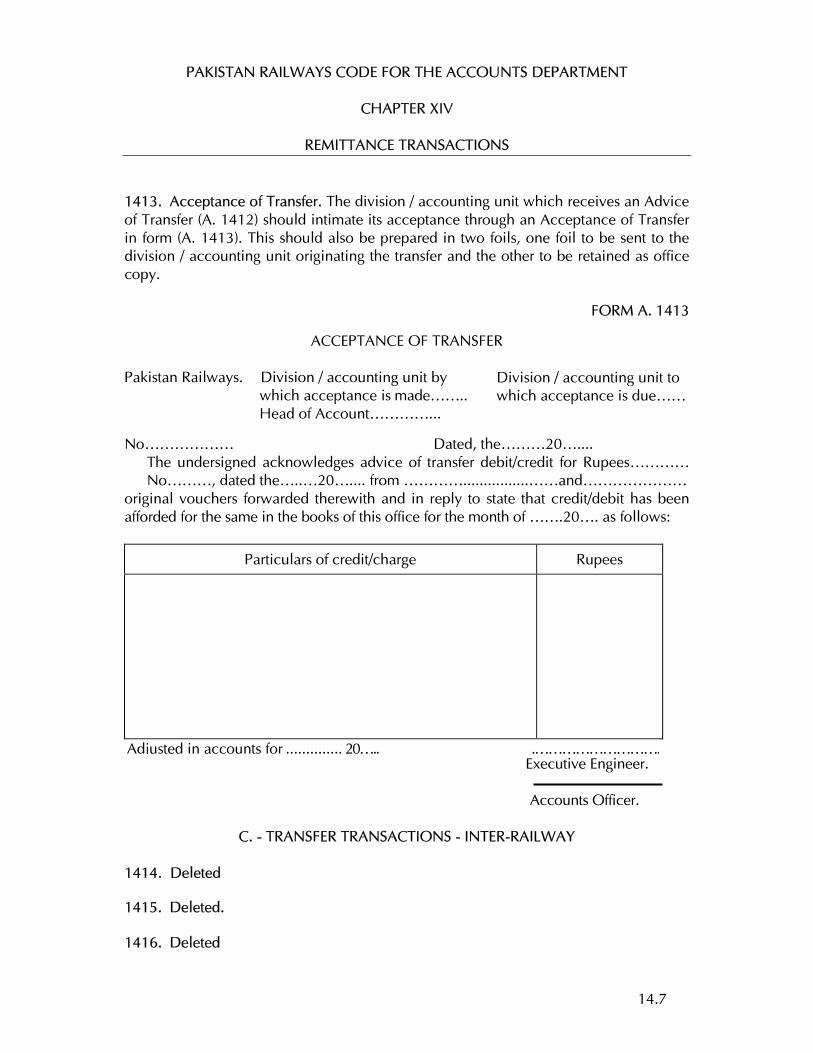

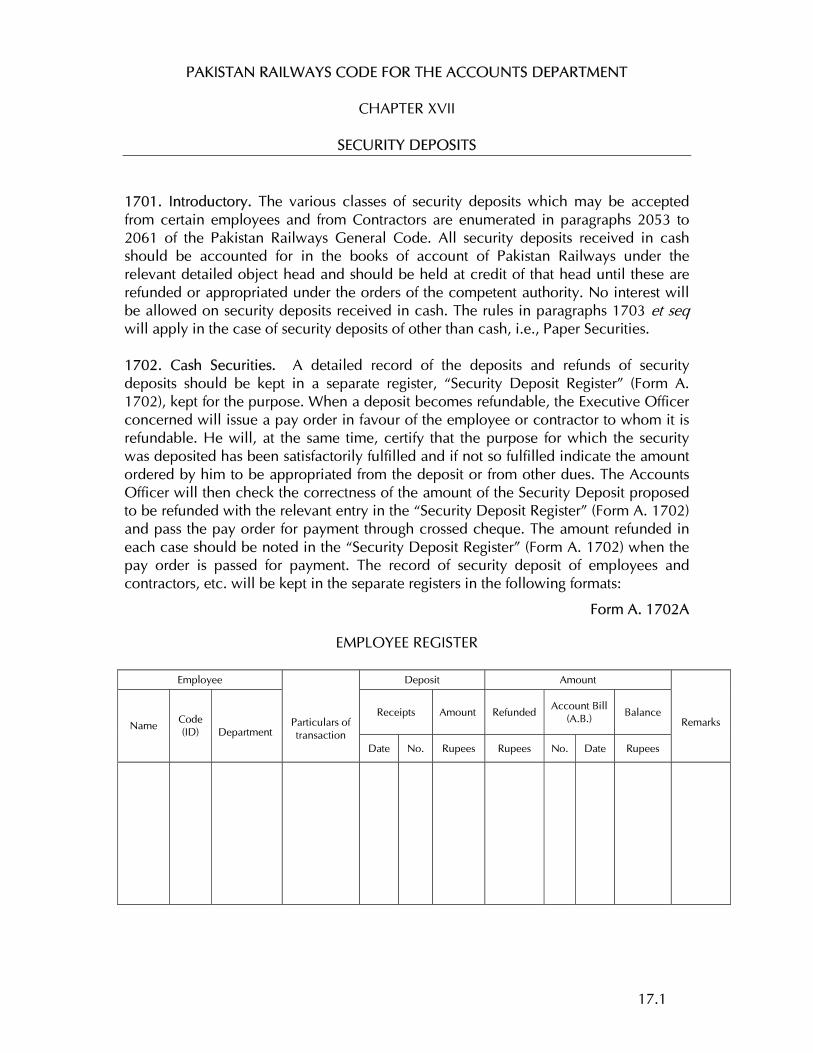

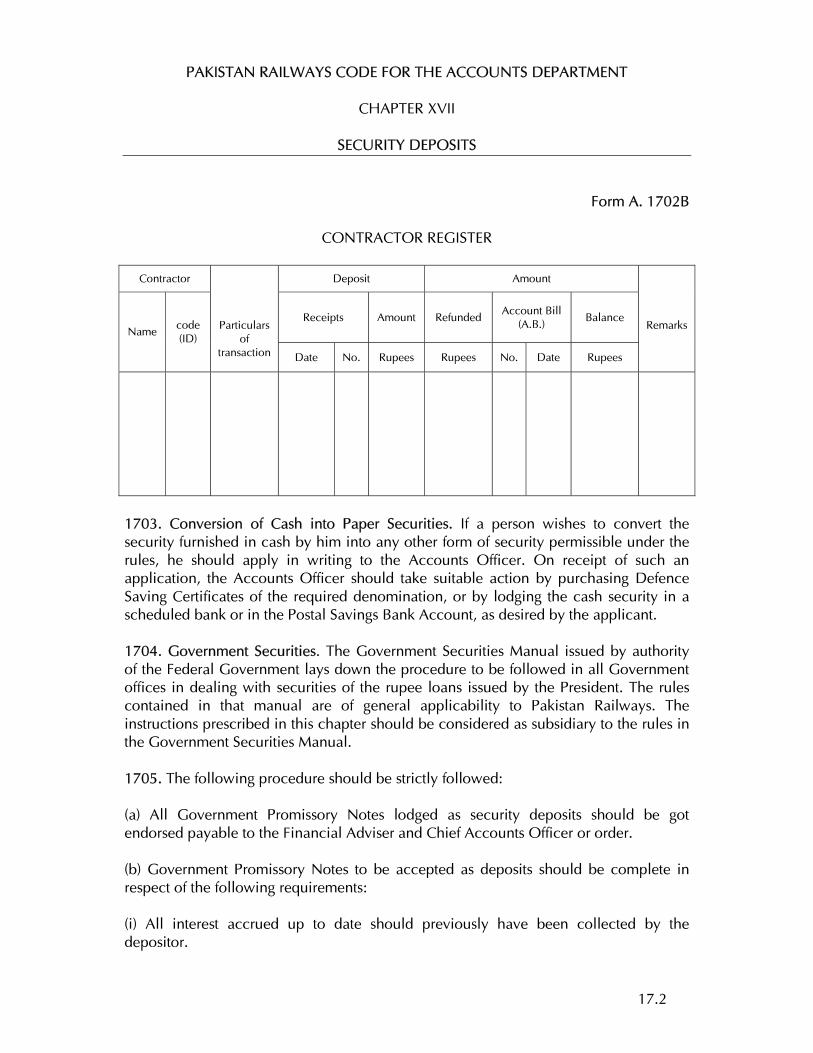

1. Weigh the remarks of the reporting officer against (a) your personal knowledge, if any, of the person reported upon; (b) the previous reports in his character role and then give your own remarks at the end of the report.