panorama - accueil | proparco · renewable energy electrification pro-jects in africa and...

TRANSCRIPT

P A N O R A M A

A N N U A L R E P O R T 2 0 1 6

2016 was a significant year for Proparco: i m p l e m e n t a t i o n of the Sustainable Development Goals (SDGs), the Addis Ababa Action Agenda

on financing for development, and the Paris Climate Agreement which all became integral to the new miles-tones of the Agence Française de Développement (AFD) Group, of which Proparco has been the private-sector financing arm for 40 years.

To meet these new challenges, Proparco has adopted a new strategy for 2017–2020. By the year 2020, Proparco is committed to doubling its financial commitments to €2bn per year and tripling the impact of its actions for creating employment, fostering innovation and climate awa- reness and promoting access to essential services.

Proparco began working towards those goals in 2016 with €1.3bn in approved financing, including €504m for climate

projects (up 74% compared to 2015) and €509m for Africa. €177m of that total is invested in equity, quasi-equity instru-ments and subordinated loans designed to boost the strength and growth poten-tial of private companies operating in developing and emerging countries.

Other important developments in 2016 included Proparco’s first accession to European Union funds for off-grid renewable energy electrification pro-jects in Africa and accreditation from the Green Climate Fund.

Grégory Clemente, Chief Executive Officer, Proparco

Rémy Rioux,Chief Executive Officer, AFD

President of the Board of Proparco

A NEW ACTION STRATEGY GEARED TO THE SUSTAINABLE DEVELOPMENT GOALS

Proparco Annual Report 201603

Editorial

All of these results confirm that Proparco has resolutely embarked on a growth path that will enable it to meet the ambitious goals it has set for 2020.

Over the next few years, Proparco will continue to expand its work in the key development sectors where it has extensive expertise (climate, infrastructure, health, education, financial institutions), at the same time stepping up project support for customers, in particular through the provision of technical assistance, and with a commitment to back innovative projects targeting vulnerable popula-tion groups, especially in fragile States. Proparco will mobilize additional third-party resources to increase the impact of that work, continuing to pur-sue the implementation of its strategy of equity and quasi-equity investments in response to strong customer demand.In order to offer its customers increased levels of financing and relevant solu-tions, notably through co-financing, Proparco will work to enhance the existing cooperation arrangements with the other French, European and multilateral financing institutions.

Finally, Proparco will continue to work in synergy with its parent company; AFD plays a vital role in enlisting sup-port from public partners and deve-loping an attractive environment for private companies. The AFD Group’s added value vis-à-vis the private sector lies in its ability to provide assistance on all aspects of sectoral strategies, from public policy support to the financing of both public and private operators. This public-private continuum is a strong attribute of the Group that is important to capitalize on.

“Boosting the strength and growth

potential of private

companies operating in developing

and emerging economies.”

PROPARCO OBJECTIVES: JOBS, CLIMATE, ACCESS TO ESSENTIAL SERVICES, TECHNICAL ASSISTANCE, INNOVATION Proparco’ priority impacts for 2020 target the following key components of sustainable development:

• 1.7 million direct and indirect jobs supported per year

• 15 million teq CO2 avoided per year

• 12 million people with acces to essential goods or services per year

• 180 companies assisted by Proparco in environmental and governance issues during the period 2017–2020

• 45 innovative programmes for vulnerable population groups per year

€2 bn FOR THE CLIMATE

€2.7 bn FOR AFRICA

€1 bnFOR FRAGILE STATES

€1 bn ADDITIONAL THIRD-PARTY RESOURCES

MOBILIZED BY PROPARCO

€1.5 bn IN QUASI-EQUITY

AND SUBORDINATED LOANS

Ambitious operational goals for 2017–2020:

Proparco Annual Report 2016 04

Our ambition for 2020

ODDODD

ODD

ODD

ODD ODD

ODD

ODD

ODD ODD

ODD

ODD

PROPARCO CLIENTSX2 X32020: €2bn per year

2015: €1.05bn per year

COMMITMENTS IMPACTS

INNOVATION45 innovative programmes per year for vulnerable population groups

JOBS 1.7m direct or indirect jobs supported per year

CLIMATE 15m teq CO2 avoided per year

SERVICES EDUCATION, HEALTHCARE, ENERGY INFRASTRUCTURE12m peoplewith access to essential goods and services per year

ASSISTANCE TO BUSINESSES180 companies assisted by Proparco on environmental and governance issues

How we plan to achieve our ambition

2017-2020

CONS

OLID

ATIO

N

EXPE

RTIS

E

INNO

VATI

ON

RESO

URCE

S

Stepping up our work in areas of key

importance to development

Strengthening our role as providers of expert

assistance to our customers

Supporting innovative

projects aimed at vulnerable

population groups

Mobilizing resources to

maximize impact

€2.7 bn IN FINANCING DEDICATED

TO THE CONTINENT

120 INNOVATIVE PROJECTS

FINANCED OVER THE PERIOD€1 bn

MOBILIZED BY PROPARCO

180 CUSTOMERS ASSISTED

WITH IMPROVING THEIR ENVIRONMENTAL AND

SOCIAL PERFORMANCE, ABOVE ALL THROUGH OUR

TECHNICAL ASSISTANCE OFFER

€2 bn DEVOTED TO PROGRAMMES THAT MOVE FORWARD THE

FIGHT AGAINST CLIMATE CHANGE

€1bn DEDICATED TO LEAST

ADVANCED, LOW-INCOME, TRANSITION OR POST-CRISIS

COUNTRIES

€1.5 bn

ADDITIONAL THIRD-PARTY RESOURCES

INNOVATIONCSRAFRICA

CLIMATE FRAGILE STATES

EQUITY AND SIMILAR INSTRUMENTS

Proparco Annual Report 201605

Strategy

Content

Strategy 2017–2020 03

Project map 08

CSR as core component of Proparco’s strategy 10

Impacts in 2016 11

How Proparco invests 12

40 years 14

03E D I T O R I A LPROPARCO –

A FINANCIAL INSTITUTION

SERVING THE PRIVATE SECTOR

AND SUSTAINABLE DEVELOPMENT

© O

rian

e Ze

rah

Proparco Annual Report 2016 06

The Chiaka Sidibé Hotel School: The future on a silver platter 16

The lights of Kingo in Guatemala 24

Microcredit: A solution under certain conditions 32

The economic power of women boosted by microfinance 38

Senegal trying to break free from reliance on oil 42

Winds of hope in Pakistan 48

Insurance in Africa: An economic growth catalyser 52

56

PROJECTS

SUPPORTED BY

PROPARCO

16

O U R F I N A N C I A L

R E S U LT S

Private Sector

& Development 62

Contact us 63

© C

lem

ent T

ardi

f

© S

arah

Car

olin

e M

ülle

r

Proparco Annual Report 201607

PROPARCO – A FINANCIAL INSTITUTION SERVING

the private sector and sustainable development

roparco, a subsidiary of the Agence Française de Développement (AFD) devoted to pri-vate sector financing, has been supporting sustainable economic,

social and environmental development for 40 years. Operating in Africa, Asia, Latin America and the Middle East, the institution extends loans, makes equity investments and provides guarantees to help finance and support financial ins-titutions and corporate private-sector projects. Proparco focuses on the key development areas, such as renewable energy-based infrastructure, agribu-siness, financial institutions, health and education. Through its work, Proparco seeks to bolster the contribution of private enterprise to the achievement of the Sustainable Development Goals (SDGs) adopted by the international community in 2015. A significant share of its financing therefore goes to com-panies likely to create jobs with decent pay, supply essential goods and services and, more broadly, help reduce poverty and mitigate climate change. Moreover,

to achieve its aims, Proparco takes a broad-based approach to governance. Alongside majority shareholder AFD, its governing bodies include public- and private-sector financial institu-tions from France, the rest of Europe, Africa and Latin America. Proparco has a staff of over 200, divided up between Paris and its 11 offices abroad. Proparco can also rely on the AFD’s network of 72 agencies and offices around the world. Financing is only part of the picture, however. Proparco’s role is also to promote the emergence of responsible business and financial organizations in developing and emerging economies. This means helping its clients improve their environmental and social perfor-mance and their governance. Proparco is one of Europe’s leading development finance institutions, and spearheads a large number of joint programs with its peers.

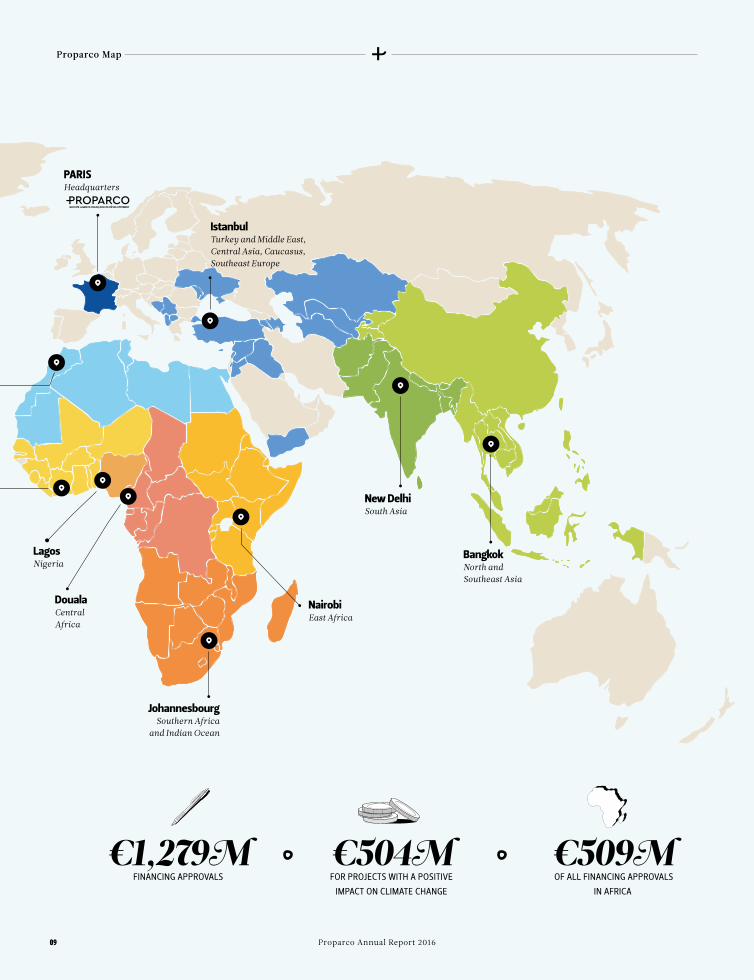

P

38 COUNTRIES

60DEALS SIGNED

MexicoCentral Americaand the Caribbean

São PauloSouth America

CasablancaNorth Africa

AbidjanWest Africa

08Proparco Annual Report 2016

€504MFOR PROJECTS WITH A POSITIVE

IMPACT ON CLIMATE CHANGE

€1,279M FINANCING APPROVALS

€509M OF ALL FINANCING APPROVALS

IN AFRICA

DoualaCentralAfrica

LagosNigeria

JohannesbourgSouthern Africa

and Indian Ocean

NairobiEast Africa

BangkokNorth andSoutheast Asia

IstanbulTurkey and Middle East,Central Asia, Caucasus,Southeast Europe

New DelhiSouth Asia

PARISHeadquarters

Proparco Annual Report 201609

Proparco Map

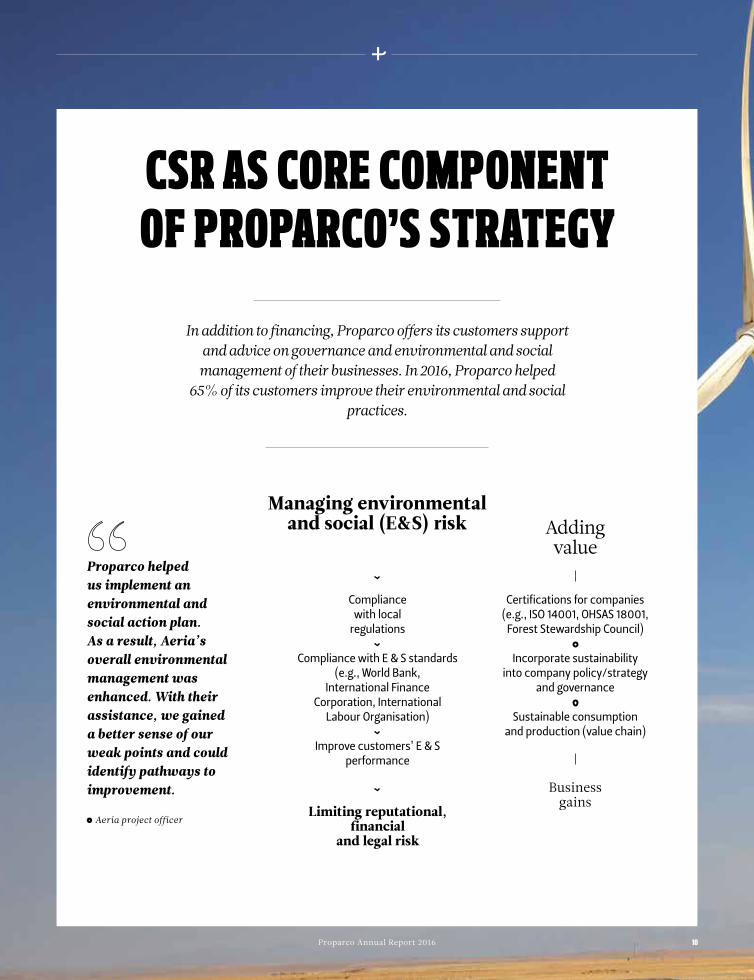

CSR AS CORE COMPONENT OF PROPARCO’S STRATEGY

In addition to financing, Proparco offers its customers support and advice on governance and environmental and social management of their businesses. In 2016, Proparco helped

65% of its customers improve their environmental and social practices.

Proparco helped us implement an environmental and social action plan. As a result, Aeria’s overall environmental management was enhanced. With their assistance, we gained a better sense of our weak points and could identify pathways to improvement.

Aeria project officer

Certifications for companies (e.g., ISO 14001, OHSAS 18001, Forest Stewardship Council)

Incorporate sustainability into company policy/strategy

and governance

Sustainable consumption and production (value chain)

Adding value

Business gains

Compliance with local

regulations

Compliance with E & S standards (e.g., World Bank,

International Finance Corporation, International

Labour Organisation)

Improve customers’ E & S performance

Managing environmental and social (E&S) risk

Limiting reputational, financial

and legal risk

Proparco Annual Report 2016 10

142,000 JOBS DIRECTLY CREATED OR MAINTAINED

AT PROPARCO-FINANCED BANKS, BUSINESSES AND INFRASTRUCTURE OPERATORS

732,000 JOBS INDIRECTLY CREATED OR MAINTAINED

AT THOSE ENTITIES’ SUPPLIERS AND CUSTOMERS, OVER 350,000 OF THEM ENGAGED

IN SMALL FARMING

47% OF THE WORKFORCE AT PROPARCO-FINANCED

BANKS, BUSINESSES, INFRASTRUCTURE OPERATORS AND INVESTMENT FUNDS

ACCOUNTED FOR BY WOMEN

IMPACTS IN 2016

D I R E C T A N D I N D I R E C T C O N T R I B U T I O N

T O E M P L O Y M E N T

A C C E S S T O E S S E N T I A L G O O D S

A N D S E R V I C E S

C L I M A T E A N D

E N E R G Y

A S S I S T A N C E T O B U S I N E S S E S

Proparco is committed to accountability and transparency. And meeting that commitment involves measuring the results and impact of its work.

In 2017, financing and co-financing by Proparco will impact development on several fronts.

680,500 TEQ CO2

WILL BE AVOIDED PER YEAR

898MEGAWATTS (MW) OF POWER CAPACITY WILL BE INSTALLED, INCLUDING 802 GWH FROM

RENEWABLE ENERGY SOURCES

1,700 ADDITIONAL BEDS

IN HOSPITALS

52,000 STUDENTS ENJOYING QUALITY EDUCATION

AT PROPARCO-FINANCED SCHOOLS

13.4 million

PEOPLE WITH POTENTIAL ACCESS TO ELECTRIC POWER SOURCES

65% OF ALL PROJECTS WILL BE SUPPORTED

TO HELP IMPROVE ENVIRONMENTAL AND SOCIAL PERFORMANCE

2 million

MORE PEOPLE WILL BE MICROCREDIT BENEFICIARIES,

WITH LOANS TOTALLING €192M

A D D E D V A L U E

€140 million

NET CONTRIBUTION TO TAX REVENUE

C O N T R I B U T I O N T O P U B L I C F I N A N C E S

€406 million

GENERATED IN THE FORM OF WAGES AND BENEFITS IN COUNTRIES WHERE

PROPARCO OPERATES

Proparco Annual Report 201611

Impacts

HOW PROPARCO INVESTS

In line with the AFD’s overall strategic direction and France’s international cooperation policy, Proparco works to promote the emergence of a buoyant, innovative, socially responsible private sector in developing and emerging economies that can effectively contribute to sustainable economic growth, creating jobs, supplying essential goods and services and, more broadly,

helping to reduce poverty and mitigate climate change.

TARGETS

Proparco supports the development of companies and financial institutions that are active in areas of key importance to

development, both local organizations and international companies (particularly French)

with operations developing countries or seeking to develop subsidiaries there.

ADDITIONALITY

Proparco works to supplement the activity of local and international commercial banks,

but without coming into competition with them. Its operations focus on areas

where its assistance is most needed and where it has the highest added value.

KNOCK-ON EFFECT

Proparco’s financing aims to demonstrate the economic and financial viability of

private enterprise in businesses and/or regions that investors tend to shy away

from. In this sense, Proparco’s operations have a significant knock-on effect.

CLIENT RELIABILITY

All financing decisions are based on an in-depth analysis of the various risk

factors – credit, social, environmental and other risks – related to clients

and their projects.

PROJECT PROFITABILITY

Projects cannot last unless they are profitable. Moreover, profitability is critical to the business model of an organization like Proparco and to its ability to win over

additional providers of funding.

DEVELOPMENT IMPACT

The contribution that the companies it finances make to local development is

central to Proparco’s approach to investment.

Investment conditions and principles

Proparco Annual Report 2016 12

+ Expertise spanning multiple sectors and geographies

+ Ability to organize complex projects+ An international network

+ Third-party funding (arrangement, syndication, credit facility management)

+ Good control of financial, environmental, social and other risks

+ Financial strength (as part of the AFD Group)+ Co-financing arrangements with fellow

development finance organizations (DEG, FMO, IFC)

O U R A D D E D V A L U E

O U R M I S S I O N

Strengthen the private sector’s contribution to the achievement

of the Sustainable Development Goals (SDGs)

Loans

Equity and quasi-equity investments

Investment funds

Guarantees

Technical assistance

O U R T O O L S

O U R A R E A S O F I N V O L V E M E N TAgriculture

and agribusinessBanks and financial

marketsClimate

EducationIndustry

Infrastructure (energy,

telecommunications, transport, water and

sanitation) Microfinance

HealthTourism

Proparco Annual Report 201613

Invest

PROPARCO 1977/2017

“If Proparco were a person, you’d have to wonder whether it makes sense to write the biography of someone who’s still growing – like a teenager. Still, this 40th birthday is a great opportunity to explore how Proparco came into being, return to the ideas that motivated its founders and initial staff, bring to light the many continuities in its history. The institution has changed swiftly, but the pace of change seems less impressive than the shift to greater scale scheduled to take place between now and 2020.”

François Pacquement, Project Manager, History and Strategic

Thinking, Agence Française de Développement

When first established in 1977, Proparco was a wholly-owned subsidiary of the Caisse Centrale de Coopération Economique (CCCE, since renamed AFD) with share capital of 10m French francs (or €1.5m).

Over the past 40 years, the institution has gradually broadened the range of its financing tools, target countries and shareholders, making it one of the leading European development finance institutions today, with share capital of €693m.

With its top-grade

equipment, the school’s

kitchen is one of the most

modern in Bamako. “A

kitchen is like a hospital,”

says culinary instructor

Thomas Brissiaud.

Proparco Annual Report 2016 16

THE CHIAKA SIDIBÉ HOTEL SCHOOL :

the future on a silver platter

CHIAKA SIDIBÉ, MALI’S FIRST WORK-STUDY HOTEL SCHOOL,

BEGAN OPERATING IN BAMAKO IN 2015 WITH THE AIM OF

EXPANDING HOSPITALITY TRAINING OPPORTUNITIES IN THE

COUNTRY. THE SCHOOL GREW OUT OF THE ENCOUNTER

BETWEEN MOSSADECK BALLY, THE VISIONARY CEO OF THE

AZALAÏ HOTEL GROUP, AND PROPARCO AND ITS PARTNERS.

ALL OF THEM ARE BETTING ON MALI’S YOUTH AND FUTURE.

Pho

to c

redi

t: ©

Séb

asti

en R

ieu

ssec

REPORT

Proparco Annual Report 201617

Vocational training

ali is a vast, land-locked country in West Africa exten-ding from the Tropic of Capricorn to the

Equator, with a population of 17.6 mil-lion – and expanding at an annual rate of 3.6%. Several years of economic expansion gave way to a political and security crisis triggered by the 2012 coup d’état and the occupation of the north of the country by Tuareg rebels and Islamist groups. International mili-tary intervention came in response.

Those dramatic events have taken their toll on Mali’s largely undiversified economy, where cotton remains king. Although tourism grew in the first decade of the new century, it has since collapsed. Mali is a fragile state indeed, ranked 179th out of 188 countries on the UN’s Human Development Index. And yet the resumption of foreign aid in 2013, measures planned by the govern-ment, the mobilization of part of the business community and initiatives to bring about a return to normal provide grounds for the hope that the country will soon be back on the path to growth – and that further projects like Chiaka Sibidé will take shape.

While the Land of the Dogons and Timbuktu are still off limits for now, business travel has picked up in Bamako. The World Tourism Organization (UNWTO) reported 168,000 visitors in 2014, a figure that reflects government efforts to create an investment-friendly environment.

Five months to open the schoolThe Chiaka Sidibé Hotel School (EHCS) thus emerged against a background of political instability tempered by hopes for economic recovery and inclusive development. “This is a project we’ve been deeply attached to for ten years, one that took several tries,” explains Aminata Soumah, the Azalaï HR

M Manager and project coordinator. With French-speaking West Africa forecast to grow faster than any other region of Africa for the third year straight, and with the hospitality and tourism sector working to establish higher standards, EHCS’s time has come, she says.

“The school grew out of the need to close a gap,” adds Mossadeck Bally, the CEO of Azalaï Hotels. “We realized we couldn’t find young people who already had basic hotel training, so we decided to tackle the problem on our own, found a school and train young people ourselves.” As it happens, what set the wheels in motion was an encounter with Bernard Creff, a native of Brittany and former Accor Hotels executive. Restless, always game for new challenges, known for his pioneering work in Cambodia, where he started a hospitality indus-try vocational school in Siem Reap that currently has over 40 trainees a year, he started the project in Mali at the begin-ning of 2015. Creff moved swiftly to bring in Nicolas Huet, a former Campus France executive, to run the programme. Named for a trusted colleague of Bally’s who died in 2010, Chiaka Sidibé opened in September 2015 on the premises of the Azalaï Dunia Hotel. “Once Mossadeck Bally got me involved in this great pro-ject, it barely took us five months to set up the Bamako school,” recalls Creff.

Proparco, back after 15 years’ absenceBut that wasn’t the end of the story for the head of Azalaï. Returning to Mali after 15 years’ absence, Proparco reached out to the hotel group as part of its focus on fragile states in Sub-Saharan Africa and its policy of suppor-ting the private sector. Convinced that a thriving hospitality industry would be crucial to luring investors back to Mali, the institution’s leadership granted a €16.4m loan to renovate and expand the Salam Hotel, Azalaï’s pride and joy in Bamako. The loan was accompanied by a three-year technical assistance

This is aproject we’ve been deeply attached to

for ten years, one that took

several tries.

Aminata Soumah, Azalaï HR Manager

18Proparco Annual Report 2016

€16,4 mLOANED BY PROPARCO

TO RENOVATE

AND EXPAND

THE SALAM HOTEL

11 months OF TRAINING

over 40TRAINEES

A YEAR

The one-year elite training programme takes

the form of cooperative education, with

students spending half their time in class and

the other half on the job at Bamako’s hotels

and restaurants. Even during their school

periods, they engage every lunch hour in

practical exercises at a learning restaurant

open to the public

programme to conso-lidate the school’s business model and help put the curricu-lum in place.

Cooperative education –an approach previously unknown in MaliThe cooperative edu-cation model offered at EHCS, with students spending half their time in class and the other half on the job, is a novelty in Mali. Existing training programmes tend to be confined to the classroom, parti-cularly in the hospitality industry. But while the new hotel school has made hands-on experience a priority, it also gives students courses in French, English, computer science and other subjects that contribute to a broad-based education.

To be admitted, applicants must pass a written test comparable to the one taken by French pupils at the end of middle school and go in for an indi-vidual interview. Annual tuition is 250,000 West African CFA francs (equal to roughly €380). Virtually from the outset, trainees get down to work, handling dishes, wielding carving

knives and the like. They soon move on to the adjoining Grand Hotel for a first real taste of work in a dining room and, barely two months later, they start in on internships at hotels and restaurants in Bamako.

Daniel Hougnon, the owner of the Badala Hotel whose stunning restaurant overlooks the Niger River, immediately agreed to partner with EHCS. This for-mer figure at Accor with fifty years of hotel experience – primarily in Africa – has taken on five interns. He has even hired one of them from last year’s gra-duating class. Initially a waiter, Luc Kassogué gets kitchen training on his days off and dreams of opening a hotel of his own.

The right attitudeAn extremely demanding employer, Mr Hougnon appreciates how little time it takes his young recruits to be operatio-nal, and that they show “real passion for their work and the right attitude”. Stressing that he is constantly in need of skilled staff, he asserts that he is prepared to hire interns. The Azalaï Hotel Group likewise plans to hire 30% of the students in each gradua-ting class. For the class of 2016–2017, the school has partnered with an NGO, SOS Villages Mali, to provide training to 25 young people from the country-side. Meanwhile, the Server and Line Cook programme has been expanded to include baking and pastry-making, a skill in great demand in Bamako, with the result that the group has been increased from 40 to 60 students.

“We have eleven months to turn them into professional staff,” comments

Interns employed at N’Ice Cream, an ice cream chain

founded in Dakar that has since fanned out across the

entire continent. Operating in Bamako for over a year

now, the company has branched out into breads and

pastries under the leadership of Ryan Souleiman, one

of the founder’s sons.

They know that they’re here to learn a trade, that this is the key to escaping unemployment. Thomas Brissiaud, culinary instructor

20Proparco Annual Report 2016

director Nicolas Huet. Graduates leave the programme with recognized voca-tional competence and maximum employability. “Everyone from the first year who wanted to work found a job,” he adds. Thomas Brissiaud, an international service volunteer who teaches culinary arts at the school, fully agrees. Impressed with how motivated his students are, the young chef says, “They do their utmost. They know that they’re here to learn a trade, that this is the key to escaping unemployment.”

Working to avoid disasterToday more than ever, young people in Mali need economic opportunities and solutions that address their aspirations. Even those with diplomas may find themselves unemployed, given that many university curricula are ill-suited to labour-market demand and the sta-tus of apprenticeship programmes is very much up in the air. Moreover,

the 10.3% official unemployment rate only partially reflects the dramatic conditions affecting a country where, according to a UN Population Division estimate, at least 50% of people in the 15-to-39 age cohort are unemployed or underemployed.

Mossadeck Bally discusses the challenge in no uncertain terms, saying, “We consider reinvestment in training for youth as part of our cor-porate social responsibility. We have to give a chance to young people who might otherwise gravitate towards terrorist groups or set out on a high-risk journey across the desert and the Mediterranean.”

Gratifying for everyoneFemale students are now in the majo-rity, an outcome of the school’s com-mitment to gender equality and the sign that a modest but real cultural

OF MALIANS AGED 15 TO 39

ARE UN- OR UNDEREMPLOYED

ACCORDING TO THE UNDP

50 %

Cooperative education gives

young women like this student

the opportunity to increase

their self-reliance by increasing

their knowledge, skills and

professional aptitude.

Proparco Annual Report 201621

Vocational training

revolution is unfolding. Not only has empowering women become a key issue in Mali, but women are under-re-presented in the country’s hotels and restaurants, both in management and non-management positions. For them even more than for their male coun-terparts, training thus takes on crucial importance. Cooperative education at EHCS enables young women to increase their knowledge, skills and professional aptitude. In addition, young men and women working together fosters dynamic collaboration and encourages parity that will benefit both.

Better still, Chiaka Sidibé now has its own fan base. The restaurant used for on-the-job training has become a popular venue where Bamako’s gourmets get a chance to taste dishes prepared by the students and the renowned bread baked at the school, all for just 10,000 West African CFA francs (roughly €15). In this way, the restaurant can advertise the quality of its cuisine while covering its costs.Furthermore, enthusiasm for the school extends well beyond local food lovers. A growing number of employers are eager to hire EHCS stu-dents even before they have comple-ted the programme. “In light of how successful the first year was and how much positive feedback we have received from partner businesses, we have increased the size of the class of

2017. We also plan to offer additional courses in 2018 and recruit enough staff to be able to accommodate a hun-dred students a year. So we are trai-ning more young people and stepping up our work with African companies and other partners,” says Mossadeck Bally.

Convinced that there is plenty of opportu-nity and a genuine will among hospitality pro-viders to enhance their industry, Bally wants to get his approach more widely adopted in the region. EHCS is the-refore seeking further investors to give that approach the staying power it needs and make

the school “an autonomous, solid, recognized structure throughout West Africa”, explains Aminata Soumah, the head of Human Resources. The aim is to broaden the choice of courses and build new classrooms to provide trai-ning across the spectrum of hospita-lity industry work, from the reception desk to room service and ultimately on to management positions. Ms Soumah would also like to see the certifica-tions of EHCS graduates recognized as State diplomas. “In a few years, we hope to replicate our business model elsewhere in Africa and start up ini-tiatives similar to Chiaka Sidibé,” she adds. That may sound ambitious, but such a plan responds to actual needs. Observers claim that the number of unfilled job vacancies at restaurants in sub-Saharan Africa increases every year.

The students have bought into the mindset evinced by

the founder of Azalaï Hotels, who grew up in a family of

merchants where “entrepreneurship was second nature”.

Today, Mossadeck Bally wants to steadily expand the hotel

school’s student body to be able to train more young people.

In a few years, we hope to replicate our business model elsewhere in Africa.

Aminata Soumah, Azalaï HR Manager

© Ib

rahi

m D

iarr

asso

uba

Proparco Annual Report 201623

Vocational training

in Guatemala

THELIGHTS

OF KINGO

Innovations combining solar energy

with digital are on the rise in

countries inadequately covered by

conventional power grids to date.

Driving the boom are agile, ‘pay-as-

you-go’ schemes based on actual

day-to-day power consumption and

software applications that help make

access to electricity more widely

available.

REPORT

© J

J Es

trad

a

large share of the population in Central America still has to get along without utility-supplied elec-

tricity. While significant progress was made between 1990 and 2010, most notably in Guatemala, Honduras and Nicaragua, the region’s least electri-fied countries, millions of people are still unconnected to the power grid. In Guatemala, for example, over 300,000 households are dependent for their lighting on candles, kerosene lamps or diesel-powered generators.

But alongside those widespread makeshift arrangements, an inno-vative alternative has been gaining ground in the country’s most remote areas. Kingo, a battery box that takes

just twenty minutes to install and connect to a solar panel, is an off-the-grid power solution, i.e., with no connection to the national power grid. This makes it fully independent of Guatemala’s centralized electricity infrastructure, which relies heavily on hydropower. “This is the quickest and cheapest way to boost access to elec-tric power among country-dwellers,” explains Juan Fermín Rodríguez, the CEO and co-founder of Kingo Energy, a Guatemalan start-up that designs and markets the orange-coloured battery boxes bearing its name.

Off-grid power or no powerCost is obviously a key consideration in a country marked by grinding poverty and high inequality. Half the popula-tion lives below the poverty line and

13% lives in extreme poverty — with an even higher proportion among Mayas, who make up 40% of Guatemala’s population and are for the most part farmers in remote areas. As it happens, off-grid solutions have begun to take root in just such areas. Prime examples are Alta Verapaz and Petén, two of the country’s poorest Departments, where conventional power grid coverage is only 44% and 66%, respectively.

“It’s taken us under two years to equip more than 15,000 Guatemalan households,” states Kingo Energy’s CEO. “This has not only given fami-lies improved living conditions and greater home security. It also means less time devoted to household chores and more time for children to do school work.” Off-grid lighting systems

A

This is the quickest and cheapest way to boost access to

electric power among country-dwellers.

Juan Fermin Rodriguez, CEO and co-founder of Kingo Energy

ONE OUT OF TEN GUATEMALANS HAS NO ACCESS TO THE NATIONAL POWER GRID. THAT MEANS 1.5 MILLION

PEOPLE DEPENDENT ON CANDLELIGHT, EXPERIENCING THE DISCOMFORT AND INSECURITY OF HOMES

AND STREETS SHROUDED IN DARKNESS EVERY NIGHT. UNTIL KINGO CAME ALONG.

Proparco Annual Report 201625

Energy

unquestionably have a lot of upside. Cheaper, more efficient, brighter, they are also safer and produce less pollu-tion than candles and kerosene lamps. Moreover, Kingo requires no cultural adjustment, as users already pay their mobile phone top-ups in the same way.

A solar panel on the roofHow exactly does this environmental friendly offer work? To start with, a solar panel is installed on the rooftop of each user who signs a no-commit-ment contract that provides for pre-payment per unit of time (hour, day, week or month), very much as with a mobile phone top-up. Once the kit has been installed and the prepaid codes have been entered by the customer, they unlock the system for the spe-cified time period. The verification is done independently of GSM coverage, making the service accessible to people in even the remotest areas. With this ‘pay-as-you-go’ system, there is no need to purchase equipment or pay for installation. Each user gets a guarantee and a perpetual service commitment, so that it all takes is a phone call for Kingo teams to step in.

Customers who opt for the basis Kingo 15 kit, which can light three lamps for five hours and recharge one mobile

phone per day, pay 60 centavos (€0.70) a day or 110 centavos (€13) a month. Those who sign up for the high-end Kingo 100 offer will have enough power to light up the main room of

their homes for five hours, recharge three mobile phones and run two electrical appliances like fans, TVs, compu-ters and radios. Kingo customers will be able in the future to prepay on their mobile phones, for example by going through the financing department of a finan-cial intermediary. But given the current size of Guatemala’s unban-ked population, for the time being users have to purchase their top-up

cards either at local grocery shops or at directly from Kingo representatives, who pocket a 6% commission.

“It’s been a game-changer for me”Elena Laj Yuja de Gua and her husband Jorge moved two years ago to a village called Caserío El Limón located two hours away from Flores, the capital of Petén Department. A mother of four children, she claims that the arrival of Kingo was a game-changer for her. “We used to get up at 4 or 5 in the mor-ning to prepare meals for the whole day by candlelight. We don’t have to do that anymore. I can get up later, spend more time with the family and do my part for the village women’s association. Above all, the child-ren can devote an hour a day to their homework. I never dreamt that Kingo would come here. Ours is now one of

Making daily life easier, increasing home safety and creating better conditions for children to do school work.

© Ju

an Jo

sé E

stra

da

Proparco Annual Report 2016 26

20 minutes

100 %From Guatelama

4 years

US$100

Kingo – a kit that can change

your life

This little box gives Guatemala’s poorest inhabitants access to

electricity. For a few euros a month to be paid up front

on flexible terms, customers can have indoor lighting in

the evening, keep animals out and give their children better

conditions for doing their school work. Here are Kingo’s

five essential features.

THAT’S HOW LONG IT TAKES TO

INSTALL A KINGO KIT, WHICH IS

CONNECTED TO A SOLAR PANEL

ON THE CUSTOMER’S ROOFTOP.

THAT’S ALL THERE IS TO IT.

THAT’S THE BASE RATE CHARGED

BY KINGO. IT’S ENOUGH TO POWER

3 LAMPS, LIGHT UP A HOUSE FOR

5 HOURS A DAY AND TOP UP A

MOBILE PHONE. USERS SPEND AN

AVERAGE OF US$15 A MONTH.KINGO COMES STRAIGHT FROM GUATEMALA CITY.

THOUGH INSPIRED BY PREVIOUS SOLUTIONS

DEVELOPED ELSEWHERE – IN AFRICA, FOR EXAMPLE –

IT’S A HOME-GROWN OFFER CREATED BY TWO YOUNG

GUATEMALANS.

THAT’S HOW LONG THE PROJECT

HAS BEEN AROUND.

IT WAS STARTED BY JUAN FERMÍN

RODRÍGUEZ AND JUAN JOSÉ

ESTRADA IN 2013.

THAT’S WHAT IT COSTS TO

PRODUCE AND INSTALL A

KINGO KIT. NO CHARGE TO THE

CUSTOMER FOR THE EQUIPMENT,

INSTALLATION OR AFTER-SALES

SERVICE.

€O.70 cents a day

Proparco Annual Report 201627

Energy

The kits include solar panels

along with batteries to store

the electrical energy produced.

Customers can use them to light

their homes and power low-

energy electrical appliances.

© S

arah

Car

olin

e M

ülle

r

28Proparco Annual Report 2016

fifteen families with access to electricity. Everybody wants electricity!”With her Kingo 15 plan, Elena can have indoor ligh-ting for over five hours a day, recharge her phone, orga-nize her children’s school work and keep her home safe, while saving 25% on monthly expenses. “I used to buy candles and go through three or four of them a day,” she says. “There was always a risk of setting fire to the house, not to mention the danger that snakes would slither inside after nightfall while the children were still playing. With electric light, animals no longer approach and the children can play or do school work whenever they need to.”

This is obviously the kind of feedback that motivates Kingo Energy staff to increase the availability of their offer in

remote parts of the country. In fact, the aim is to equip two million households by 2020 and extend the company’s business to other countries. As Kingo’s leaders see it, Petén is only part of a much larger potential market. After

receiving $5m plus a $4m loan conver-tible into shares from FMO, they plan to raise another $8m to be able to branch out across the region and provide ser-vice in Colombia, Honduras, Nicaragua and even Mexico.

I never dreamt that Kingo would come here. Ours is now one of fifteen families with access to electricity. Everyone wants electricity!” Elena Laj Yuja de Gua, an inhabitant of Caserío El Limón

Elena Laj Yuja de Gua and her husband

Jorge moved two years ago to a village

called Caserío El Limón located two

hours away from Flores, the capital

of Petén Department. Education for

girls and access to electricity are both

preconditions to controlling population

growth. Innovative, alternative ways

of making electric power available are

therefore crucial to social and economic

development.

© C

hris

telle

Thom

as

Proparco Annual Report 201629

Energy

In addition to tracking

conventional performance

and impact indicators, Kingo

maintains a User Happiness

Index.

40,000 users

SINCE IT WAS LAUNCHED IN 2015,

THE KINGO ENERGY SOLUTION

HAS BEEN ADOPTED BY 40,000

USERS. IT COULD WELL WIN OVER

ANOTHER 2 MILLION USERS

BY 2020.

© S

arah

Car

olin

e M

ülle

r

Altruism and profitability According to the International Energy Agency’s projections for sub-Saharan Africa, “Two-thirds of the mini-grid and off-grid systems in rural areas in 2040 will be powered by solar vol-taics, small hydropower or wind”. For several years now, a large number of start-ups have risen to the challenge of providing electricity to Africa. Some have turned to off-grid solar power and their investments are starting to pay off.

Juan Fermín Rodríguez, who left a career at Procter & Gamble to “bet the farm” on his start-up, considers it a vital necessity for Kingo to both meet its commitments and turn a profit. “I strongly believe that we’ve taken the right approach and that we can make a profit while serving the public inte-rest,” he states. When asked whether that outlook reflects the altruistic upbringing he received from a father already engaged in cooperation pro-grammes in rural Guatemala, he com-ments: “The most important thing in our eyes is to have increasingly high-quality offerings, software and raw materials in our equipment so that we can deliver better service to our users. With new components coming out in the market, we should be able to develop smaller, longer-lasting batte-ries, which means that we can reach even more remote regions and offer an accessible alternative to more and more people.”

No progress without private capitalHave these progresses made us closer

to make to make clean energy avai-lable across the region? A decade after the first pioneering solutions in this area emerged, no business model – whether pay-as-you-go, rent-to-own or perpetual leases of the kind offered by Kingo – has achieved global domi-nance so far, even though the alter-native energy market has followed much the same trajectory as mobile telephony, according the International Energy Agency. On the basis of this outlook, Kingo anticipates a return on investment in short order. “Due to our knowledge of the market and our adaptability, we can profitably invest while narrowing the poverty gap. But with the financing requirements we face, it’s essential to enlist support from financial partners like Proparco and FMO who are willing to take on risks that may seem like too much for local banks,” Kingo’s CEO stresses.

In any case, only massive investment can make a difference in Guatemala. In a country where 57% of GDP – that is, $30bn – accrued to just 260 citizens in 2014, there will be no progress without private capital. Nor can financial ins-titutions be expected to step in, given the commitment to keeping govern-ment debt under control. Yet, private investment and help from financial institutions could make it possible to reduce the gap in both energy supply and economic opportunities between rural communities and the urban popu-lation.

THE ART OF BOUNCING BACK

For Juan Fermín Rodríguez, it all started in 2010 when he left Procter & Gamble to become the co-founder of a first, pay-as-you-go business called Quetsol. With backing from local microfinance institutions, the company set out to supply cheap electric power to Guatemala’s poorest households, many of them dependent on candlelight and diesel generators. This laudable initiative failed, however. The need to repay the initial loan, combined with customer insolvency and high unit costs for solar panels and batteries, made this an unsustainable business model.

But Juan Fermín is one of those responsive, agile entrepreneurs who can reinvent their business at the drop of a hat. He bounced back, and fast. With his partner Juan José Estrada – alias “J. J.” – he crafted a telecom-style approach and came out with a solar power service offering that had his new company, Kingo Energy, bear the cost of installation.

Two key factors rendered their solution workable. For one thing, Kingo raised funds from several investors including FMO and Proparco. For another, solar installation costs have declined by 80% since 2008, making the technology cost-competitive with fossil fuels.

Proparco Annual Report 201631

Energy

32Proparco Annual Report 2016

MICROCREDIT: A SOLUTION

under certain conditions

BY OFFERING FINANCIAL SERVICES TO THE NEEDIEST

POPULATION GROUPS, MICROFINANCE INSTITUTIONS SUPPORT

MICRO-ENTERPRISES AND HELP ENHANCE LIVING CONDITIONS

FOR THEIR CUSTOMERS. MICROFINANCE PROVIDES

ASSISTANCE IN STARTING UP A BUSINESS, MOBILIZING SAVINGS

OR TAKING OUT INSURANCE TO COPE WITH THE HAZARDS OF

LIFE. THIS MEANS IT HAS A POTENTIAL FOR GROWTH THAT IS

COMMENSURATE WITH THE DEGREE OF FINANCIAL EXCLUSION

THAT CONTINUES TO PLAGUE SO MANY DEVELOPING

COUNTRIES. AT FIRST BLUSH, THIS LOOKS LIKE AN IDEAL WAY

OUT OF POVERTY.

REPORTP

hoto

cre

dit:

Sam

Lam

Proparco Annual Report 201633

Microfinance

icrofinance came into being as a means to promote financial viabi-lity, and is there-

fore governed in part by a commercial mindset. In fact, a number of buoyant markets have seen intense competi-tion between microfinance providers, and while this has led to a welcome decrease in lending rates, it has also spawned a variety of practices that are detrimental to customers. In many countries, the microfinance sector has experienced spectacular growth, cor-related with a bidding war and a ten-dency to overheating that may result in unsustainable debt levels that can only hurt the sector itself. Significant micro-finance crises have already unfolded in such places as Peru, Bosnia, Nicaragua, Bolivia and Andhra Pradesh, India. Due to competition between microfinance institutions and increased lending, some loans have been used to pay off previous ones in a well-documented vicious circle that now seems to be loo-ming in Cambodia as well.

Experts ringing the alarm bell in CambodiaA mere 22% of all Cambodians over fifteen years of age have accounts at formal financial institutions, whether banks or microfinance institutions (MFIs). This stands in stark contrast to the situation in neighbouring Thailand, where 78% of the population was ‘ban-ked’ in 2014.* With a population of 15 million, Cambodia boasts an advanced regulatory environment and therefore a high degree of transparency, along with sound market infrastructure that includes a central credit registry and the Cambodia Microfinance Association (CMA). This favourable environment has offered considerable opportunity to MFIs and made this a highly compe-titive market. Today, however, experts are ringing the alarm bell. They empha-size the risk of market saturation in spe-cific provinces, the growing average

M size of microcredits and the presence of informal lenders engaged in reckless practices, from usurious interest rates to shoddy assessment of customers’ creditworthiness.

Stiffer regulationOn 13 March 2017, the National Bank of Cambodia issued a new regulation setting an interest-rate ceiling for all microfinance institutions from April 1st, 2017 onward. This creates an additional challenge for the country’s regulated MFIs, particularly those operating in rural areas and offering small loans that entail high operating costs.Daniel Rozas, a microfinance specia-list and consultant in Cambodia, has developed a tool for forecasting micro-finance saturation that he has pleasingly named MIMOSA.*According to the World Bank’s Findex study.

17,6 %

2.4 millions

OF ALL ADULT

CAMBODIANS HAD

CONTRACTED A LOAN

IN THE PRECEDING

12 MONTHS, ACCORDING TO

THE CREDIT BUREAU.

BORROWERS

IN CAMBODIA’S

MICROFINANCE MARKET,

ACCORDING TO THE

CAMBODIA MICROFINANCE

ASSOCIATION (CMA).

THE TWO PRIMARY CAUSES

OF OVERINDEBTEDNESS ARE

THE TENDENCY OF INDIVIDUAL

BORROWERS TO TAKE OUT

SEVERAL LOANS FROM

SEVERAL INSTITUTIONS AND

THE TENDENCY TO REFINANCE

(SEVERAL) SMALL LOANS WITH A

LARGER ONE.

The kingdom benefits from a professional legal framework but experts raise the alarm about risks of saturation.

Proparco Annual Report 2016 34

MIMOSA AND GOOD PRACTICE

Since the 1990s, the number of MFIs in the world has seen exponential growth that has not always been accompanied by stricter regulation with regard to responsible lending, financial soundness or transparency on lending activity. With signs of overheating already experienced by several countries, for example in Morocco, Bosnia and Nicaragua in 2008, followed by India in 2010, experts have come forward to warn the microfinance institutions. MIMOSA (Microfinance Index of Market Outreach and Saturation) provides country studies based on metrics that track market saturation, regulation and competition as well as the maturity of MFIs and how transparent and risky their lending activities are. Studies have already been conducted on Cambodia, Kyrgyzstan, Bolivia, Morocco, Peru, Azerbaijan and Senegal.

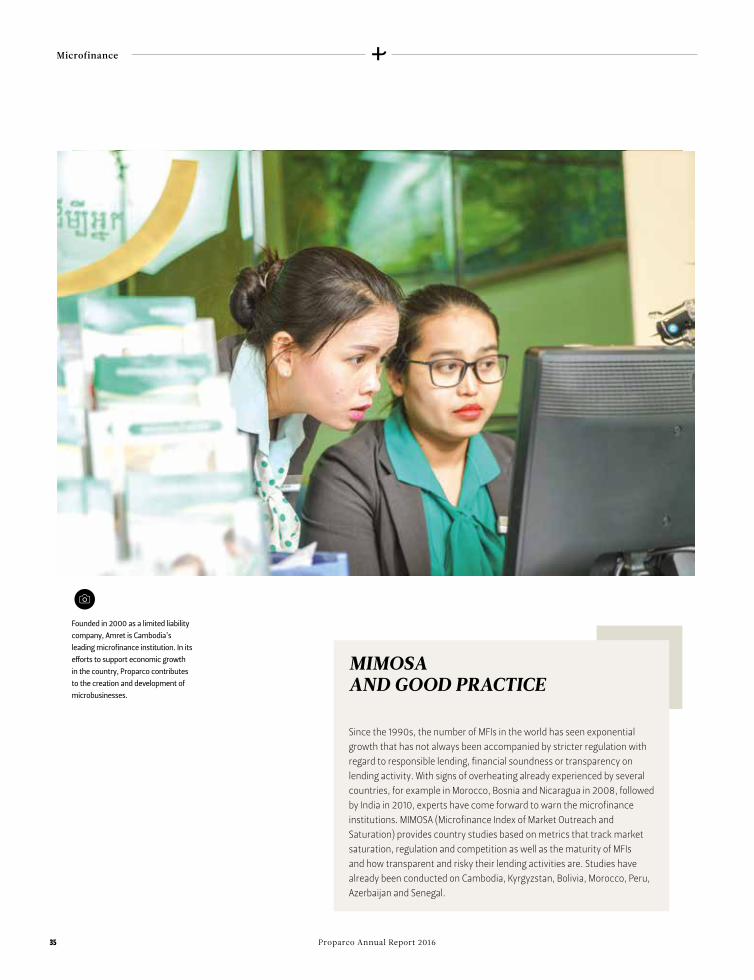

Founded in 2000 as a limited liability

company, Amret is Cambodia’s

leading microfinance institution. In its

efforts to support economic growth

in the country, Proparco contributes

to the creation and development of

microbusinesses.

Proparco Annual Report 201635

Microfinance

Cambodia at the crossroads

Proparco has been present in Cambodia’s microfinance sector for ten years and has played a part in setting the Lenders’ Guidelines adopted by the MFIs, whose purpose is to heighten cooperation among those institutions and reduce the risk

of overindebtedness. Launched in 2016 and jointly financed by Incofin Investment Management, a Belgian fund specializing in microfinance, and two other EDFIs – Belgium’s BIO and the Netherlands’ FMO – this initiative represents the first

attempt to establish common guidelines focused on the issue of overindebtedness by setting precise lending procedures and customer protection procedures. The aim

is to assist the Cambodia Microfinance Association (CMA) with the crafting and implementation of the guidelines.

INTERVIEW WITH

Daniel ROZAS

MIMOSA co-founder Daniel Rozas works

as a consultant to a variety of institutions

that range from the European Microfinance

Platform (E-MFP) to the Cambodia

Microfinance Association (CMA), as part of a

programme to prevent overindebtedness and

design common guidelines for MFIs. He holds

an MBA from the University of Maryland and

worked previously, from 2001 to 2008, for the

US mortgage lending institution Fannie Mae.

Dra

win

g: L

uca

Lau

ren

ti

Proparco Annual Report 2016 36

In terms of microfinance, Cambodia is the exception. Why is that?Cambodia is a particularly interesting case. During the first decade of this century, the country basically had no financial sector. The primary vehicle for developing local financing were microfinance institutions, rather than banks. All those MFIs were originally NGOs active in the countryside in a variety of development projects, inclu-ding microlending. What distinguishes Cambodia is that its MFIs got started in rural areas, not in cities. The result of microfinance has been to connect the rural economy to the financial sec-tor. A further point is that institutions from abroad, for example, foreign social investment funds and deve-lopment institutions like Proparco, have played an essential role in the sector since the early 1990s. Virtually all of the Cambodian microfinance sector’s financial resources initially came from development assistance, and that was still true five or six years ago. Microfinance NGOs gradually developed into MFIs and in some cases banks funded by foreign organizations. That has happened nowhere else in the world.

You claim that the decree of 13 March 2017 has created a lot of uncertainty. Could you elaborate on that?The decree shows confusion between interest rates charged by informal MFIs, which are considered usurious, and those charge by regulated MFIs. It could have a major impact on those institutions. If interest rates are kept at such a low level without any room for flexibility, a number of MFIs will find it hard to stay in business. They’ll

be forced to lend money at rates that don’t even cover their operating costs. If you slash interest rates over night, MFIs will stop offering specific pro-ducts. Rural borrowers are likely to be the first casualties, given that it costs more to provide service in remote areas.

You also take part in designing good practice guidelines together with the CMA. What needs does that project seek to meet? What are your goals?The CMA was concerned to lay down guidelines for preventing overindeb-tedness and guaranteeing sustainable expansion of the market. So a number of development finance institutions, among them Proparco, were asked to help out. These restrictive, self-regu-latory guidelines establish a framework for MFI activity that includes requi-rements on reporting to the Credit Bureau Cambodia (CBC). The CBC is responsible for producing a follow-up report that funding providers can access. A noteworthy feature is that the guidelines have been set exclusively by microfinance organizations themsel-ves. The CMA hopes that the National Bank of Cambodia will incorporate the guidelines into a law that applies to all financial sector institutions. In prac-tice, the guidelines will compel MFIs to collect more extensive customer infor-mation, provide the data to the CBC, limit the number of loans to any single borrower and more effectively protect customers.

Could you describe good practice in the sector?MFIs in Cambodia are eager to coope-rate with each other. For years now, they have strived to create a responsible

microfinance sector governed by com-mon principles. They routinely respond to requests from funding providers that they submit to social ratings, something you don’t see in other markets. This has given rise to a prescriptive framework covering both financial and social standards. In fact, a number of MFIs have distinguished themselves with socially responsible treatment of their customers. For example, they coope-rate with the Social Performance Task Force (SPTF) and the Smart Campaign, a global effort to safeguard the well-being and overall financial situation of indi-viduals and families involved in micro-finance projects. Above all, they make sure they understand their customers and zero in on the needs that are specific to their situation. This creates a more ethical framework. In this respect, too, Cambodia is in the vanguard.

We need to design regulations, but not just any regulations, and not at any price.

Proparco Annual Report 201637

Microfinance

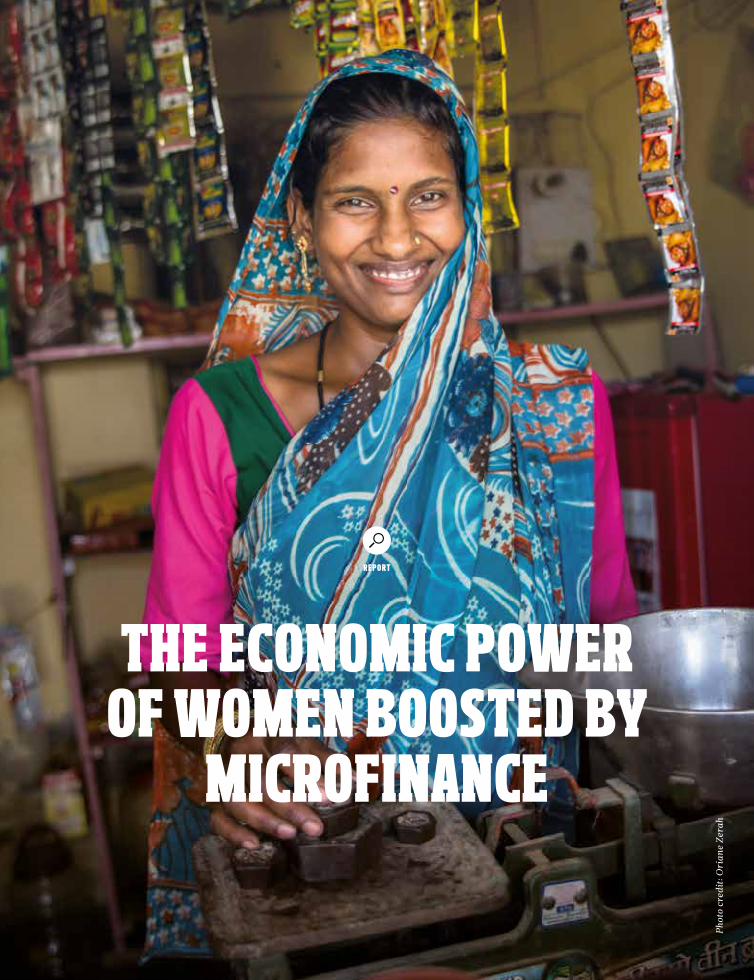

THE ECONOMIC POWER OF WOMEN BOOSTED BY

MICROFINANCE

REPORT

Pho

to c

redi

t: O

rian

e Ze

rah

handni, age 22, has been married for four years. She lives with her husband and two daughters in Saidapur, a vil-

lage 40 minutes away from Lucknow, the capital of Uttar Pradesh located between Delhi and Calcutta.

Two and a half years ago, shortly after their first daughter was born, the family found itself in financial trouble. Chandni’s husband, a farm labourer, didn’t have a regular job. His ear-nings were too low to cover their basic needs, i.e., healthcare, food, housing and education. That same year, a visit by a Sonata employee whose role is to go from door to door to acquaint vil-lage-dwellers with microcredit was to initiate a decisive change in the young woman’s life.

At age 19, Chandni borrowed 40,000 rupees (c. €585) from Sonata with the aim of starting her own business – a grocery shop. She discussed it with her husband and relatives. Everyone encouraged her to go ahead.

C Chandni went out and joined a joint lia-bility group made up of village women who wanted to take out Sonata loans.

Joint liability groupsNinety-six per cent of the women who contract Sonata loans do so through joint liability groups. The groups usually have between ten and twenty members who know each other and live in the same area. It is an approach to credit grounded in trust and solidarity among group members. Although loans are granted on an individual basis, they are guaranteed by joint surety among the members. By using existing social bonds among the beneficiaries, the group creates a form of collective gua-rantee that encourages members to pay back their loans.

Such solidarity groups are loosely based on the ‘tontines’ that are highly popu-lar in sub-Saharan Africa. Tontines “are associations composed of members of a clan or family, neighbours and other individuals who agree to pool goods or services to benefit all members on a rotating basis” (F. Boman, economist). At the monthly meetings, all members

This credit has changed

my life; it’s made it better.

I am stronger now.

Chandni, age 22

SPOTLIGHT ON CHANDNI, A YOUNG WOMAN WHO BECAME

A MICRO-ENTREPRENEUR THANKS TO MICROCREDIT.

Proparco Annual Report 201639

Microfinance

HIGHLIGHTS

Chandni opened her own grocery shop to overcome her family’s financial difficulties. That move was made possible by a loan of 40,000 Indian rupees (c. €585) from Sonata Finance Private Limited (Sonata), a small-amount microfinance lender supported by Proparco.

Access to microcredit can contribute to the liberation and empowerment of women, giving them recognized social responsibility and including them in the labour market.

Many families in the rural and semi-urban areas of Uttar Pradesh (UP) benefit from microcredit. UP is one of India’s poorest states. It has a population of 200 million – as large as Brazil’s. Economic growth in the state is 6%, versus 8% in India as a whole.

contribute a predetermined amount to the kitty, and one member gets to take the whole sum on a rotating basis.

Chandni’s group is made up of about ten women. They meet once a week to review each member’s projects and collect repayments.

A sense of accomplishmentAfter taking out a two-year loan for 40,000 rupees from Sonata, Chandni opened her shop. The business soon prospered and she was able to make

her repayments on schedule. At long last, the family was enjoying financial stability.

Chandni, who rarely loses her smile, is proud of what she has accomplished, and she is confident about the future. “This credit has changed my life. Our life is better now. I am also stronger than before. Once I have paid off my loan, I plan to take out a larger one so that I can expand the premises and offer additional products.”

Weekly meeting of the solidarity group

that Chandni belongs to.

Proparco Annual Report 2016 40

Proparco’s roleIn November 2016, Proparco acquired a stake in Sonata for approximately US$6.5m. That investment reflects Proparco’s strategy of encouraging responsible microlending in emerging economies and assisting microfinance institutions that show a commitment to social performance.

Through the support it provides, Proparco helps Sonata to achieve its aim of delivering microfinance service to low-income women transparently, swiftly and efficiently.

To ensure that its work benefits the target population, Sonata uses poverty assessment tools that measure household living conditions and assets. Sonata’s lending activity also incorpo-rates the client protection principles developed by the Smart Campaign ini-tiative. The organization has demons-trated in particular its skill in managing the prevention of overindebtedness by steering clear of areas with high microfinance penetration rates. At the same time, despite the serious regula-tory constraints it faces, Sonata seeks to broaden its financial product offer to include home improvement loans, mobile banking and the like as a way of more effectively meeting client needs and cementing its reputation in a com-petitive market.

In India, as in many other countries, microfinance can be a highly competi-tive industry. Its members must there-fore strive for a proper balance between financial and social performance of the kind that can lead to responsible, sus-tainable development.

Chandni proudly and happily operates

a grocery shop that she opened with

the help of a microcredit from Sonata.

Microfinance

Proparco Annual Report 201641

It will take up to 200 or 250 employees

to build the power plant. For hiring, the

neighbouring villages have priority status.

A reforesting programme around the

construction site will make it possible to

prevent erosion and keep the PV panels

from sanding up.

SENEGAL TRYING TO BREAK FREE

from reliance on oil

HARDLY-HIT BY THE OIL-PRICE HIKE IN 2008, CONSTRAINED BY AN INADEQUATE

ENERGY SYSTEM, SENEGAL HAS BEGUN TO EXPLOIT ITS IMMENSE RENEWABLE

ENERGY POTENTIAL, WITH SOLAR POWER IN THE LEAD. THE NUMBER OF

PROJECTS HAS BEEN RISING FOR TWO YEARS NOW, A PRIME EXAMPLE BEING

SENERGY, THE COUNTRY'S FIRST PRIVATE SOLAR POWER PLANT AND

THE LARGEST ONE IN WEST AFRICA, 80% FINANCED BY PROPARCO.

THE AIM IS TO HELP BOOST SENEGAL’S ENERGY SECURITY AND FACILITATE

THE TRANSITION TO LOW-CARBON DEVELOPMENT.

REPORT

Pho

to c

redi

t: C

lém

ent T

ardi

f

s in several other African countries, Senegal’s economic and social deve-lopment is held back by sub-par performance in the energy sector. With

843 MW of nameplate power capacity in 2015 (whereas Morocco’s is ten times higher), the national power grid is ill-equipped to handle the growing needs of businesses and citizens alike. There are many reasons for that defi-ciency, among them over a decade of under-investment in generation capa-city and Senegal’s high dependency on fossil fuels, with thermal power plants accounting for 90% of total output. But things got even worse in the period from 2008 to 2011, when the global oil shock upended the country’s energy sector. The result was massive power cuts and a profound social crisis, as demonstrated by the ‘electricity riots’ of 2011. Moreover, Senegal’s electricity prices are among the highest in West Africa (almost twice as high as in the Ivory Coast), despite a 2009 freeze on rates and generous State subsidies to the national power company, Senelec, until 2014. According to an IMF esti-mate, those subsidies are equal to 2% of GDP.

No economic take-off without reliable, affordable, sustainable energyThis, then, was the backdrop to the ambitious roadmap for economic and social development adopted by the government in 2012. Titled Plan Sénégal Emergent (PSE), the plan places major emphasis on energy security. The government aims to increase national production capacity by 10% to 15% a year, while reducing the country’s reliance on high-polluting imported fossil fuels, which represent a burden for both households and Senegal’s public finances. If the plan is success-ful, the share of petroleum products in

the country’s energy mix could drop from 90% to 45% in 2017, while solar and other renewable energy sources could rise to 20% of nameplate capa-city, offsetting that drop. For Thierno Alassane Sall, Minister of Energy and Development of Renewable Energies, the goal is clearly “to break free of the tyranny of a single fuel source, which was the case with oil for seve-ral decades”.In line with the Sustainable Energy for All (SE4ALL) global initiative launched by the United Nations in 2012, President Macky Sall has also pledged to elec-trify the country’s rural areas. And rightly so. Whereas 90% of Senegal’s urban population is connected to the power grid, barely one out of four country-dwellers is. Moreover, that average encompasses large disparities, with some areas below the 5% mark.

A

Dakar accounts for 0.3% of

the country’s land surface,

but is home to one fourth of

its population. The peninsula

capital is also where the bulk

of Senegal’s economic activity

takes place, with the result that

the power grid is subject to

increasing pressure.

The goal is clearly to break free of the tyranny of a single fuel source, which was the case with oil for several decades. Thierno Alassane Sall,

Minister of Energy and Development of Renewable Energies

Proparco Annual Report 2016 44

West africa's largest private solar power plantTo carry out this large-scale change, the government has turned to independent private power producers. A number of power purchase agreements have been signed or are being negotiated. Initiated by the French investment company Meridiam, Senegal’s sovereign wealth fund Fonsis and the solar power firm Solairedirect (an Engie subsidiary), co-financed by Proparco, a member of the Agence Française de Développement (AFD) Group, Senergy is the largest pri-vate solar power plant project anywhere in West Africa. The project was launched in 2011 by an American-Senegalese entrepreneur. Due to the capital-in-tensive nature of solar energy projects, Fonsis threw its weight behind Senergy in 2013. The sovereign wealth fund then managed to bring Meridiam on board

(see box) to structure the deal and settle the basic engineering questions. In a country with no previous indus-trial-scale solar energy infrastructure, “we needed to address a whole host of regulatory and engineering issues, some of them complex and costly”, explains Mathieu Peller, who heads Meridiam’s West Africa office. “For example, securing land tenure in an area with multiple layers of property rights, devising adequate compensa-tion for the local population, working out contract terms and conditions and connecting to the power grid.”

Sited on 64 hectares of former farmland near Mekhé (130 km north of Dakar), the Senergy power plant will encom-pass 92,000 solar modules with total nameplate capacity of 29.5 MW. That will be enough to cover the annual

electric power needs of a city with over 200,000 inhabitants at a cost that makes it competitive with the country’s thermal power plants. The electricity it generates will be sold to Senelec under a 25-year power purchase agreement. In addition, 34,000 tonnes of C02 equivalent emissions will be avoided per year thanks to this low-carbon infrastructure.“On this project, Meridiam has made a long-term commitment that was a compelling argument for our partners,” says Peller. “Proparco’s involvement since 2013 was also essential to convin-cing Senelec and the government to invest. The organization’s reputation and demanding approach gave our consortium real credibility, not to men-tion that Proparco has provided 80% of the funding – through a €34.5m loan – on competitive terms.”

AFD GROUP AND THE ENERGY ISSUE IN SENEGALOver the past decade, the AFD, Proparco’s parent company, has provided close to €200m to Senegal’s energy sector, for the most part to help put Senelec’s finances and operations back on even keel. In 2008, €30m were invested to recapitalize the failing national electricity company. Three years later, following the ‘electricity riots’, the AFD was the first development finance institution to extend a loan (€60m) to rehabilitate Senelec’s production facilities, with the result that 110 MW of additional capacity was recovered and a total of 210 MW was put on a secure footing (equal to almost one fourth of nameplate capacity).At the same time, a €1m subsidy was made available to the energy industry, chiefly for research and to enhance capabilities at the Energy Ministry and Senelec through the work of three engineering assistants. The Agency also contributes to investment programmes to help West Africa’s SMEs reduce their energy bills through energy efficiency and renewable energy projects, chiefly in Benin, Burkina Faso, the Ivory Coast, Senegal and Togo, granting its commercial banking partners (in Senegal, Orabank and SGBS) ‘green’ lines of credit totalling €30m (see www.sunref.org), coupled with a programme of technical assistance to the small businesses involved. Lastly, the AFD works to promote electrification of the countryside, including an €8m subsidy in 2008 to provide electricity to 18,000 households via solar power kits and extend the power grid.

Proparco Annual Report 201645

Energy

Involving the local population from the outsetMeridiam is an investment firm specia-lizing in essential infrastructure. “Our goal is to have a positive impact on the areas where we invest, to meet the long-term development needs of the government and local population,” Peller states. Right from the start, the impact issue was central to the project negotiations. “The primary challenge was purchasing land owned by 66 small farmers,” explains Abdourahim Ba, Managing Director of the firm Engineering & Environment Services, in charge of the environmental and social (E&S) questions surrounding the project.

“The negotiations got going in 2013 with the chiefs of the neighbouring vil-lages, who called together all the inte-rested parties. The aim was to identify the ideal site and the people who would be affected, hold public outreach mee-tings and basically talk to everyone

until everyone approved.” In addi-tion to compensation for landholders as required by Senegalese law and in keeping with the demands of a funding provider like Proparco, the Senergy project includes a number of measures designed to benefit local communities. Unskilled labourers from neighbouring villages will be hired, preference will be given to local contractors and E&S work will be promoted. Furthermore, “a plan for restoring the livelihoods of local inhabitants has been drawn up. Under the plan, a well will be drilled and between 12 and 25 hectares of land will be purchased to offers farmers the means to engage in long-term agricul-ture. Most farming in Senegal takes place during the rainy season. But with the new well, the villagers can engage in ongoing, more diversified farming,” Mr Ba points out. In partnership with a local bank, a microcredit mutual bene-fit society will also be made available so that women and youth can develop business activities. A maternity clinic will likewise soon be built in Santhiou-Mékhé. Finally, a committee holding monthly meetings has been set up to monitor delivery on the project owner’s commitments.

More solar power, more know-howThe Senergy facility is scheduled to come on stream in July 2017, but Meridiam and Proparco are already working to develop a second, extre-mely similar solar power plant just a few kilometres away from the first one. And this new project won’t be the last one, either.

The Senegalese government’s renewable energy goals have won over bilateral and multilateral development finance institutions and aroused inte-rest among independent private power (IPP) producers. “Six solar power plant projects are currently in the deve-lopment or construction stages in Senegal,” says Papa Mademba Biteye,

Portrait

MERIDIAM AS A LONG-TERM DEVELOPER AND INVESTORMeridiam SAS (‘Meridiam’) is a French investment company founded in 2005 that develops, finances and manages public-sector infrastructure projects on a long-term basis (25 years). The company partners with key engineering and financial firms – from planning to implementation and operation. On most projects, Meridiam is the majority or reference shareholder. The company currently has €5bn worth of assets under management invested in 49 projects worldwide, most of them in Europe and North America.

In 2015, Meridiam created MIAF, an African investment fund endowed with €300m. Its brief is to make roughly a dozen investments of between €10m and €40m each in social, transport and clean energy infrastructure projects. While Senergy is its first project in mainland Africa, Meridiam is already working in Madagascar and has responded to calls for tenders across sub-Saharan Africa. “We aim to establish our position on the continent as partners and suppliers of proven, competitive solutions for providing long-term sustainable development assistance spanning economic, social and environmental issues,” states Mathieu Peller in conclusion.

In a global economy short of breath, Africa provides significant opportunities for stimulus and shared growth. Macky Sall,

President of the Republic of Sénégal

Proparco Annual Report 2016 46

More reliable electric power supply

should also have a positive impact

on productivity in the population and

eventually create jobs and stimulate

economic growth.

a technical advisor to the Ministry for Energy and Renewable Energy Development (Meder). “By the end of 2017, they will be generating another 105 MW of power, with 150 MW more to come in 2018 from Senegal’s first wind farm.” On top of those 255 MW, an additional 100 MW will be com-missioned in two years as part of the Scaling Solar programme launched by a World Bank subsidiary to support pri-vate-sector initiative.Even so, there is still insufficient fun-ding to fulfil Senegal’s ‘green’ aspi-rations. “The private sector is where the financial resources are,” stresses Mamadou Mbaye, the Executive Director in charge of Energy and Mining at Fonsis. “Our mission is to use the resources allocated by the State to attract private funding for greenfield projects by deconstructing investor apprehensions about financial risk in Senegal. For example, insurance

companies make 30% to 40% of their equity investments in North America, versus under 5% in Africa. We need to secure dedicated financing for low-carbon infrastructure quickly. So why not try to line up partial gua-rantees provided by development finance institutions or via the Green Climate Fund to obtain a higher credit rating for Senegal?”

In a similar frame of mind, Senegal’s President has urged public — and pri-vate — sector partners “not to ove-restimate the risk of investing on the continent. Africa has made substan-tial strides towards good governance and an improved business climate. Risk here is no higher than elsewhere. Besides, with the global economy clearly running out of steam today, Africa shouldn’t be equated with risk, but rather with opportunities to revive the economy and achieve shared

growth.” Apart from the funding issue, the future of renewable energy in Senegal will also depend on support for appropriate policies and regulations that can ensure the financial viability of the relevant projects, particularly with regard to drafting power pur-chase agreements, setting guaranteed feed-in tarifs for IPPs and establishing capped, harmonized rates for the popu-lation. And it will mean enhancing the ability of power companies and public services to respond locally to the requi-rements specific to solar power. The need to incorporate such intermittent energy sources into the national grid is an engineering challenge that escapes no one’s attention in Senegal. And from that standpoint, a project like Senergy will contribute to the transfer of know-how from Meridiam and Engie’s solar energy subsidiary Solairedirect to the people at Senelec and the Energy Ministry.

Proparco Annual Report 201647

Energy

WINDS OF HOPE IN PAKISTAN

REPORT

Proparco is investing $20m to support a new

wind farm in Sindh Province as part of a move

to increase renewable energy output and drive

economic development in Pakistan.

Pho

tos

cred

it: O

rian

e Ze

rah

PROPARCO IS INVESTING $20M IN A PAKISTANI WIND FARM, CONFIRMING ITS SUPPORT

FOR THE SHIFT TO RENEWABLE ENERGY SOURCES.

akistan suffers from an estimated annual energy shortfall of roughly 5,200 MW. To tackle this pres-

sing problem, Gul Ahmed Energy Group has developed a wind power project in partnership with Proparco. In October 2016, a first facility com-prising 20 wind turbines producing 2.5 MW each, and thus a total of 50 MW, was commissioned in the Jhimpir corridor located in southerly Sindh, Pakistan’s second most populous pro-vince. Ubaid Amanullah, the Executive Director of Gul Ahmed Energy, argues that wind farms deliver both environ-mental benefits, in that they entail lower greenhouse gas emissions and a smaller carbon footprint, and econo-mic benefits by reducing the country’s reliance on costly imported fossil fuels.

PThis project is a first step in the right direction. Now we need to go further.” Ubaid Amanullah, Executive Director of Gul Ahmed Energy

Wind power is an inexpensive,

appropriate energy source

chosen by Pakistan’s

government as a means to

diversify an energy mix that

is still overly dependent on

high-polluting fossil fuels.

Proparco Annual Report 201649

Renewable energy

And while he believes it is too soon to assess the ultimate impact of these new forms of energy on the population, he considers even these modest initial steps to be encouraging. “The first wind farm was commissioned in 2013, and most of the others weren’t built until 2015 or 2016,” he says. “Wind power isn’t a substitute at this stage; it’s merely a secondary energy source. The Sindh wind farm has nameplate capacity of 50 MW, and if you add that to the power generated by other wind farms, you get a total of 600 MW. That still repre-sents only 10% of Pakistan’s current energy needs, but what makes this project significant is that it marks the beginning of a new form of energy pro-duction that is essential for Pakistan. The country is starting to realize how important the shift to renewable energy is. This project is a first step in the right direction. Now we need to go further.”

€20 million and some guidelinesProparco has invested €20m in this project as part of AFD’s ‘Green growth and solidarity’ initiative, reflecting its commitment to developing renewable energy sources and combating climate change. “Without the contribution of Proparco, one of the key investors, this wind power project never would have got off the ground,” Amanullah states with conviction. “Our country really needs projects like this one.”But aside from the financial support – a loan of around $19m for a project with a total cost of $126m – Proparco also encouraged the recruitment of local labour. The construction phase created jobs for construction workers and secu-rity agents, and since the wind farm has been up and running, all of the security staff and wind turbine operatives have been recruited from among the inhabi-tants of Jhimpir.