parmalat s.p.a. · exportação de laticinios ltda, with registered office at 2012 faria lima, in...

TRANSCRIPT

Courtesy Translation

PARMALAT S.P.A.

INFORMATION MEMORANDUM

REGARDING

THE IMPLEMENTATION OF THE MECHANISM

TO ADJUST THE PURCHASE PRICE OF

LACTALIS AMERICAN GROUP, INC.

Prepared pursuant to Article 5 of the Regulations adopted by the Consob with Resolution No.

17221 of March 12, 2010, as amended by Resolution No. 17389 of June 23, 2010.

June 2013

This Information Memorandum has been made available to the public at the registered office of

Parmalat S.p.A. (4 Via delle Nazioni Unite, Collecchio, Parma) and on the website of Parmalat

S.p.A. (www.parmalat.com).

CONTENTS

DEFINITIONS ................................................................................................................................................................ 3

INTRODUCTION .......................................................................................................................................................... 9

1. DISCLAIMER .................................................................................................................................................. 14

1.1 RISKS RELATED TO POTENTIAL CONFLICTS OF INTEREST ARISING FROM THE RELATED‐PARTY TRANSACTION

14 1.2 PENDING PROCEEDINGS ..................................................................................................................................... 15

2. INFORMATION ABOUT THE TRANSACTION .................................................................................... 16

2.1 OVERVIEW OF THE TRANSACTION’S CHARACTERISTICS, MODALITIES, TERMS AND CONDITIONS ................... 16 2.2 DESCRIPTION OF THE RELATED PARTIES WITH WHOM THE TRANSACTION WAS EXECUTED, THE NATURE OF

THE RELATIONSHIP AND THE NATURE AND SCOPE OF THE INTEREST OF THE ABOVEMENTIONED PARTIES IN

THE TRANSACTION ............................................................................................................................................ 23 2.3 DESCRIPTION OF THE ECONOMIC MOTIVATIONS FOR THE TRANSACTION AND OF ITS BENEFITS FOR

PARMALAT ......................................................................................................................................................... 24 2.4 METHODS FOR DETERMINING THE CONSIDERATION AND ASSESSMENT OF ITS FAIRNESS COMPARED WITH

MARKET VALUES FOR SIMILAR TRANSACTIONS ............................................................................................... 25 2.5 EFFECTS OF THE TRANSACTION ON THE FINANCIAL POSITION, INCOME STATEMENT AND CASH FLOW ...... 30 2.6 IMPACT OF THE TRANSACTION ON THE COMPENSATION OF THE MEMBERS OF THE MANAGEMENT ENTITIES

OF THE COMPANY AND/OR ITS SUBSIDIARIES .................................................................................................... 31 2.7 LISTING OF ANY MEMBERS OF THE MANAGEMENT AND CONTROL ENTITIES, GENERAL MANAGERS AND

EXECUTIVES OF THE COMPANY INVOLVED IN THE TRANSACTION ................................................................... 31 2.8 TRANSACTION APPROVAL PROCESS .................................................................................................................... 34 2.9 IF, PURSUANT TO ARTICLE 5, SECTION 2, OF THE RELATED‐PARTY REGULATIONS, THE MATERIALITY OF THE

TRANSACTION DERIVES FROM THE AGGREGATION OF MULTIPLE TRANSACTIONS EXECUTED DURING THE

YEAR WITH THE SAME RELATED PARTY OR WITH PARTIES RELATED TO IT OR TO THE COMPANY, THE

INFORMATION PROVIDED IN THE PRECEDING SECTIONS OF THIS MEMORANDUM MUST BE PROVIDED FOR ALL

OF THE ABOVEMENTIONED TRANSACTIONS. ..................................................................................................... 36

3. ANNEXES ........................................................................................................................................................ 37

3.1 LIST OF DOCUMENTS RELATED TO THE LAG ACQUISITION PUBLISHED ON THE PARMALAT WEBSITE

(WWW.PARMALAT.COM): ................................................................................................................................... 37 3.2 OPINION OF THE COMMITTEE FOR RELATED‐PARTY TRANSACTIONS DATED MAY 30, 2013 .......................... 37

3

DEFINITIONS

A list of the main terms used in this Information Memorandum is provided below.

“Acquired Companies” LAG and its subsidiaries, as listed in the

Introduction to the Information Memorandum,

Lactalis Brazil and Lactalis Mexico.

“Acquisition” The purchase of the Equity Stakes by Parmalat

through LAG Holding, Parmalat Belgium and

Dalmata.

“BSA” B.S.A. S.A., with registered office at 33 avenue

du Maine – Tour Maine‐Montparnasse, (75015)

Paris (France), entered into the Paris (France)

Registre du Commerce et des Sociétés under

Identification No. 557 350 253 R.C.S. Paris.

“BSA International” B.S.A. International S.A., with registered office

at 5 Place du Champ de Mars – boite 20 (1050)

Brussels (Belgium), entered into the Brussels

(Belgium) Registre des Personnes Morales under

Identification No. 443.205.173 RPM Bruxelles.

“Buyer” or “LAG Holding” LAG Holding Inc., with registered office at 1209

Orange Street, Wilmington, Delaware (USA),

Employer Identification No. 45‐5524252, a

subsidiary wholly owned by Parmalat, through

Parmalat Belgium, which Parmalat designated

as the buyer of the LAG Shares pursuant to

Article 2.5 of the Share Purchase Agreement.

“Closing” The implementation of the Acquisition, through

the transfer of title to the Equity Stakes and

payment of the Provisional Price, subject to the

concurrent signing of the Commercial

Agreements.

“Closing Date” July 3, 2012.

“Commercial Agreements” The following agreements executed on the

Closing Date:

(a) Distribution agreement between LEA, a

newly established wholly owned

4

subsidiary of LAG, and BSA

(Distribution Agreement), by virtue of

which LEA acquired the right to

distribute, on an exclusive basis and

with the option to appoint

subdistributors, the Lactalis Group

products (excluding the Parmalat

Group) in the Western Hemisphere for a

period of 20 years, extendible for

additional periods of 5 years each.

(b) Licensing agreement between LAG and

Egidio Galbani (License Agreement), by

virtue of which LAG acquired the right

to use, on an exclusive basis and with a

sublicensing option, the “Galbani”

trademarks for the production and sale

of dairy products in the Western

Hemisphere for a period with a term of

20 years, extendible for additional

periods of 5 years each.

(c) Licensing agreement between LAG and

BSA (License Agreement), by virtue of

which LAG acquired the right to use, on

an exclusive basis and with a

sublicensing option, the “Président”

trademarks for the production and sale

of dairy products in the Western

Hemisphere for a period with a term of

20 years, extendible for additional

periods of 5 years each.

(d) Sub‐distribution agreement between

LEA and Lactalis Brazil (Sub‐

distribution Agreement), by virtue of

which LEA appointed Lactalis Brazil as

the exclusive distributor of the Lactalis

Group products (excluding the Parmalat

Group) in Brazil, based on terms and

conditions substantively equivalent to

those of the Distribution Agreement

referred to sub (a) above.

(e) Sub‐distribution agreement between

LEA and Lactalis Mexico (Sub‐

distribution Agreement), by virtue of

which LEA appointed Lactalis Mexico as

5

the exclusive distributor of the Lactalis

Group products (excluding the Parmalat

Group) in Mexico, based on terms and

conditions substantively equivalent to

those of the Distribution Agreement

referred to sub (a) above.

“Consob” The National Commission for Companies and

the Securities Markets, with registered office at

3 Via G.B. Martini, in Rome.

“Dalmata” Dalmata S.p.A. with registered office in Via

delle Nazioni Unite, Collecchio (PR) – VAT No.

0202341034 – Tax I.D. and Parma Company

Register No. 01967970235 (REA 204775), a

wholly owned subsidiary of Parmalat,

designated by Parmalat as the buyer of equity

stakes representing 0.01% of the share capital of

Lactalis Brazil and 0.02% of the share capital of

Lactalis Mexico, pursuant to Article 2.5 of the

Share Purchase Agreement.

“Distribution Agreement” The distribution agreement executed on the

closing date by LEA and BSA, described more

in detail sub (a) within the definition of the

Commercial Agreements.

“Equity Stakes” The LAG Shares and the equity stakes

corresponding, in the aggregate, to the entire

equity capital of Lactalis Brazil and Lactalis

Mexico.

“Final Price” The total consideration paid by LAG Holding to

buy the Equity Stakes based on the enterprise

value, determined, after the Price Adjustment,

as amounting to USD 774 million.

“Groupe Lactalis” Groupe Lactalis S.A., with registered office at 10

rue Adolphe Beck, (53000) Laval (France),

entered into the Laval (France) Registre du

Commerce et des Sociétés under Identification No.

331 142 554 R.C.S. Laval.

“Information Memorandum” This information memorandum.

“Issuer,” “Parmalat” or “Company” Parmalat S.p.A., with registered office at 4 Via

6

delle Nazioni Unite, in Collecchio (Parma), Tax

I.D. and Parma Company Register No.

04030970968.

“Issuers’ Regulations” The Regulations adopted by the Consob with

Resolution No. 11971 of May 14, 1999, as

amended.

“Lactalis Brazil” Lactalis do Brazil, ‐ Comercio, Importação e

Exportação de Laticinios Ltda, with registered

office at 2012 Faria Lima, in São Paulo (Brazil).

“Lactalis Group” The group of companies comprised of BSA and

its direct and indirect subsidiaries.

“Lactalis Mexico” Lactalis Alimentos Mexico Sociedad de

Responsabilitad Limitada, with registered office

at 104 Protasio Tagle, San Miguel Chapultepec

11850, México City (Mexico).

“LAG Group” The group of companies comprised of LAG and

it direct and indirect subsidiaries, as listed in

the Introduction to the Information

Memorandum.

“LAG Shares” The 10,000 common shares (Common Stock),

without par value, and the 1,400 Series A

Preferred Shares (Series A Preferred Stock), par

value USD 100,000 each, representing in the

aggregate LAG’s entire share capital.

“LAG” Lactalis American Group, Inc., with head office

at 2376 South Park Avenue, Buffalo, NY 14220

(USA), Employer Identification No. 39‐1429105.

“LEA” Lactalis Export Americas SAS, with registered

office at 16 Avenue Jean Jaurès – Immeuble Orix

(94600) Choisy Le Roi (France), entered into the

Creteil (France) Registre du Commerce et des

Sociétés under Identification No. 751 701 756

R.C.S. Creteil.

“Parmalat Belgium” Parmalat Belgium S.A., with registered office in

Brussels (Belgium), Bastion Tower, Place du

Champ de Mars 5 boîte 20, 1050, Numéro

dʹentreprise 0463.897.154, a wholly owned

7

subsidiary of Parmalat, directly and through

Dalmata, designated by Parmalat as the buyer

of equity stakes representing 99.99% of the

share capital of Lactalis Brazil and 99.98% of the

share capital of Lactalis Mexico, pursuant to

Article 2.5 of the Share Purchase Agreement.

“Parmalat Group” Parmalat and its subsidiaries, in accordance

with Article 93 of the TUF.

“Price Adjustment” The procedure governed by Article 2.3 of the

Share Purchase Agreement or, depending on

the context, the amount of USD 130 million

owed by BSA to the Buyer as an adjustment to

the price of the Equity Stakes upon completion

of the abovementioned procedure.

“Provisional Price” The amount of USD 904 million paid by the

Buyer to the Sellers on the Closing Date.

“Related‐party Committee” or “Committee” Parmalat’s Committee for Related‐party

Transactions, comprised, as of April 11, 2013 of

the independent Directors Gabriella Chersicla

(Chairperson), Antonio Aristide Mastrangelo

and Riccardo Zingales; before that date the

function of this Committee was performed by

the Internal Control and Corporate Governance

Committee.

“Related‐party Procedure” or “Procedure” The Procedure Governing Transactions with

Related Parties approved by Parmalat’s Board

of Directors on November 11, 2010.

“Related‐party Regulations” The Regulations setting forth provisions

governing related‐party transactions adopted

by the Consob with Resolution No. 17221 of

March 12, 2010, as amended.

“Sellers” BSA, BSA International and Groupe Lactalis.

“Share Purchase Agreement” or “Agreement” The agreement for the sale of the Equity Stakes

(Share Purchase Agreement) executed on May

29, 2012 by Parmalat, as buyer, and BSA, BSA

International and Groupe Lactalis, as sellers.

8

“Transaction” The transaction described in this Information

Memorandum, the subject of which is the Price

Adjustment

“Uniform Financial Code” or “TUF”

(for its abbreviation in Italian)

Legislative Decree No. 58 of February 24, 1998,

as amended.

9

INTRODUCTION

This Information Memorandum (the “Information Memorandum”) was prepared by Parmalat

S.p.A. (the “Issuer,” “Parmalat” or the “Company”) pursuant to Article 5 of the Regulations

governing related‐party transactions, adopted by the Consob with Resolution No. 17221 of March

12, 2010, as amended (the “Related‐party Regulations”), and Article 9 of the Procedure Governing

Transactions with Related Parties approved by Parmalat’s Board of Directors on November 11,

2010 (the “Related‐party Procedure” or the “Procedure”).

This Information Memorandum was prepared to provide shareholders and the market with

exhaustive information about the outcome of the implementation of the price adjustment

procedure, in accordance with the provisions of the contract for the purchase of Equity Stakes (as

defined infra) executed on May 29, 2012 by Parmalat, in its capacity as buyer, and BSA S.A.

(“BSA”), BSA International S.A. (“BSA International”) and Groupe Lactalis S.A. (“Groupe

Lactalis”), in their capacity as sellers (the “Share Purchase Agreement” of the “Agreement”).

The abovementioned procedure (the “Transaction”) represents the fulfillment of the final

requirement for determining the final price of the acquisition (the “Acquisition”), by the Issuer

through its wholly owned subsidiaries identified infra, of the equity stakes (the “Equity Stakes”)

representing the entire share capital of Lactalis American Group, Inc. (“LAG”) and the equity

stakes representing the entire share capital of Lactalis do Brazil ‐ Comercio, Importação e

Exportação de Laticinios Ltda (“Lactalis Brazil”) and Lactalis Alimentos Mexico S. DE RL

(“Lactalis Mexico” and, collectively with LAG and Lactalis Brazil, the “Acquired Companies”).

Specifically, the Acquisition concerns:

(i) 10,000 common shares (Common Stock), without par value, and 1,400 Series A Preferred

Shares (Series A Preferred Stock), par value USD 100,000 each, representing in the

aggregate LAG’s entire share capital (the “LAG Shares”);

(ii) the equity stakes representing the entire share capital of Lactalis Brazil; and

(iii) the equity stakes representing the entire share capital of Lactalis Mexico.

In accordance with the provisions of the Share Purchase Agreement, the transfer of title to the

Equity Stakes and the payment of the Provisional Price (as defined infra), conditional on the

concurrent execution of the Commercial Agreements (the “Closing”), took place on July 3, 2012

(the “Closing Date”).

Prior to the Closing Date, availing itself of the option provided under Article 2.5 of the Share

Purchase Agreement, Parmalat designated its subsidiary LAG Holding, Inc. (“LAG Holding”) as

the buyer of the LAG Shares and the subsidiaries Parmalat Belgium S.A. (“Parmalat Belgium”)

and Dalmata S.r.l. (“Dalmata”) as the buyers of the equity stakes representing the entire share

capital of Lactalis Brazil and Lactalis Mexico.

10

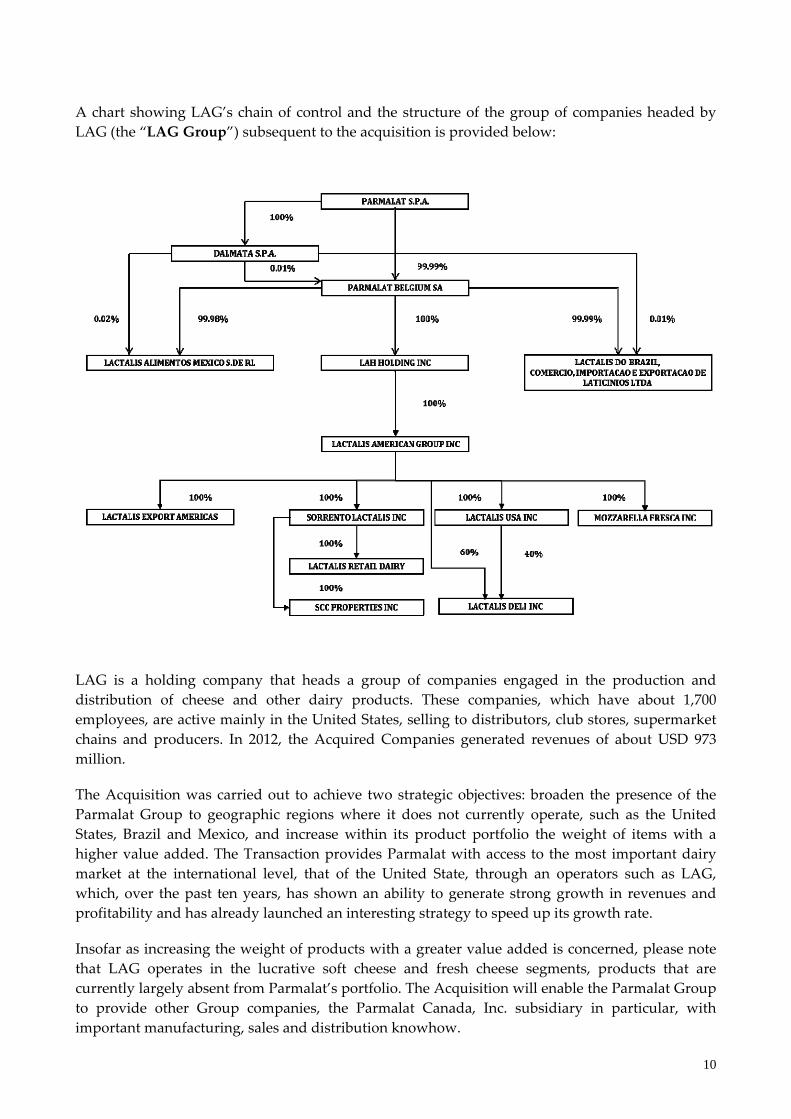

A chart showing LAG’s chain of control and the structure of the group of companies headed by

LAG (the “LAG Group”) subsequent to the acquisition is provided below:

LAG is a holding company that heads a group of companies engaged in the production and

distribution of cheese and other dairy products. These companies, which have about 1,700

employees, are active mainly in the United States, selling to distributors, club stores, supermarket

chains and producers. In 2012, the Acquired Companies generated revenues of about USD 973

million.

The Acquisition was carried out to achieve two strategic objectives: broaden the presence of the

Parmalat Group to geographic regions where it does not currently operate, such as the United

States, Brazil and Mexico, and increase within its product portfolio the weight of items with a

higher value added. The Transaction provides Parmalat with access to the most important dairy

market at the international level, that of the United State, through an operators such as LAG,

which, over the past ten years, has shown an ability to generate strong growth in revenues and

profitability and has already launched an interesting strategy to speed up its growth rate.

Insofar as increasing the weight of products with a greater value added is concerned, please note

that LAG operates in the lucrative soft cheese and fresh cheese segments, products that are

currently largely absent from Parmalat’s portfolio. The Acquisition will enable the Parmalat Group

to provide other Group companies, the Parmalat Canada, Inc. subsidiary in particular, with

important manufacturing, sales and distribution knowhow.

11

The Acquisition will also improve the Group’s position in Latin America, expanding its presence

to new markets, such as Mexico and Brazil, and opening the Venezuelan and Colombian markets,

where Parmalat is already present, to LAG’s products. Moreover, the distribution agreement

signed on the Closing Date by LEA and BSA (the “Distribution Agreement”) will significantly

broaden the Group’s presence in the countries of Central and South America, where the cheese

market is projected to enjoy high growth rates.

Pursuant to the Share Purchase Agreement, the total consideration owed for the Equity Stakes was

agreed to for an amount equal to the algebraic sum of (i) the Enterprise Value of the Acquired

Companies at the close of the 2012 reporting year and (ii) their net financial position (cash and cash

equivalents) at the end‐of‐month date closest to the Closing Date (hence, June 30, 2012).

The Enterprise Value of the Acquired Companies was estimated on a preliminary basis at USD 904

million, which corresponds to the amount provisionally paid by the Buyer on the Closing Date (the

“Provisional Price”), based on the assumption that the EBITDA1 of the Acquired Companies for

the 2012 reporting year would amount to USD 95.2 million. Therefore, the Provisional Price

reflected an EBITDA multiple of 9.5.

The Share Purchase Agreement provides a price adjustment a mechanism in order to allow a

determination of the Final Price of the Equity Stakes based on the results actually reported by the

Acquired Companies at the close of the 2012 reporting year, with the price amount ranging

between a cap of USD 960 million and a floor of 760 million.

The Agreement also requires that the Final Price of the Equity Stakes be determined based on data

presented in audited financial statements and further to negotiations between the parties, and that,

should no agreement be reached upon the conclusion of the negotiations, the price determination

would be left to an independent auditing firm, serving as Arbitrator, pursuant to and for the

purposes of Articles 1349 and 1473 of the Italian Civil Code, all of the above in accordance with the

procedure described in greater detail in Section 2.1 of this Information Memorandum.

For the purposes of the clauses governing the determination of the final price of the Equity Stakes,

Article 2.2.5 of the Share Purchase Agreement stipulated that marketing expenses (which are a

component of the EBITDA computation that, by its very nature, is highly discretionary) would be

carried out in accordance with the business plan of the Acquired Companies or, in any case, “in

the ordinary course of business” and “in accordance with best management practices.” As a result,

any variance in these expenses compared with the business plan that could not be justified in

accordance with the abovementioned criteria of ordinary business and consistency with best

management practices would authorize Parmalat to obtain a price reduction.

In accordance with the provisions of the Share Purchase Agreement, in order to secure the

payment of any amount that may be due to the Buyer as a Price Adjustment, on the Closing Date,

BSA Finances gave to Société Générale, in its capacity as paying agent, an irrevocable mandate to

use for that purpose the Revolving Loan Facility provided to BSA Finances on April 25, 2011 by a

pool of banks headed by Société Générale (the “Irrevocable Mandate”).

1 Pursuant to the Share Purchase Agreement, the EBITDA of the Acquired Companies for the 2012 reporting year was

defined as the sum of the following line items in the Price Revision Financial Statements (as defined infra):

EBIT

+ Depreciation, amortization and writedowns of non‐current assets,

– Non‐recurring and extraordinary income (expense).

12

Moreover, the Share Purchase Agreement provides ample representations and warranties in favor

of the Buyer, supported by compensation obligations with no restriction as to their amount. More

specifically, in addition to the warranties that are customary for transactions of this type, the Seller

provided express warranties for the historical and projected data supplied to Parmalat within the

framework of the due diligence process. By virtue of said warranties, should the information

obtained as part of the due diligence process prove to be untrue, incorrect or incomplete or if the

projected data supplied by the Sellers should prove not to have been based on reasonable

assumptions and/or not developed consistent with the underlying assumptions, the Buyer shall be

entitled to compensation without any limitation, for the full amount of the damage it may have

incurred. These warranties shall expire within five years from the Closing Date.

On September 25, 2012, Parmalat’s Board of Directors met to review the certified semiannual

results of the acquired companies for the first half of 2012. More specifically, it was informed that

the net financial position amounting to USD 53.2 million at June 30, 2012 was identified as an

addition to the Provisional Price of USD 904 million paid pursuant to the Share Purchase

Agreement. The amount of the net financial position was paid on October 19, 2012, within the

deadline required under the Share Purchase Agreement.

The amount paid by the Buyer, before Price Adjustment, thus totaled USD 957.2 million, equal to

750.3 million euros.

Parmalat’s Committee for Related‐party Transactions (the “Related‐party Committee” or the

“Committee”) and its Board of Directors, seeking to comply with the deadlines of the Share

Purchase Agreement and considering that the first formal compliance obligation of the Sellers

under the Agreement was the delivery of the Price Adjustment Certificate by March 1, 2013, began

in November 2012 the preparatory activities required for Price Adjustment purposes.

These activities included retaining the services of independent third parties, as described more in

detail infra, which enabled the Committee and Parmalat’s Board of Directors to adopt the

necessary resolutions, comforted by and based on the analyses performed and the opinions

rendered by (i) the Transactional Services Group of PricewaterhouseCoopers following an audit of

the EBITDA of the Acquired Companies at December 30, 2012, performed for normalization

purposes and/or to identify any nonrecurring, not applicable or non‐operating items with an

impact on the profitability of the Acquired Companies, and the analyses of marketing expenses

and any variances compared with the business plan of the Acquired Companies; (ii) the Panel of

Experts, whose members (Mario Cattaneo, Paolo Andrei and Marco Ziliotti), relying on the

contribution of Luca Pellegrini for marketing issues, considered whether or not the negative

variance in marketing expenses compared with the business plan of the Acquired Company could

be viewed as having occurred in the “ordinary course of business” and “in accordance with best

management practices;” and (iii) Guido Rossi and Giorgio De Nova (the latter retained by the

Board of Statutory Auditors) with regard to the interpretation of the clause set forth in Article 2.25

of the Share Purchase Agreement and its effectiveness in protecting the Company’s interest.

Additional information about the Acquisition is available in the information memorandum for the

13

acquisition of LAG and the corresponding Addendum published by the Issuer on May 29, 2012

and June 27, 2012, respectively, both available on Parmalat’s website (www.parmalat.com).

14

1. DISCLAIMER

A description of the main risks and uncertainties inherent in the Transaction is provided

below, with special emphasis on those related to its status as a related‐party transaction

and those that could have a material impact on the Issuer’s activities.

The content of this Disclaimer should be read in conjunction with the other information

provided in this Information Memorandum.

1.1 Risks related to potential conflicts of interest arising from the Related‐party Transaction

The Transaction qualifies as a related‐party transaction executed through a subsidiary

because:

1. Parmalat is controlled by BSA, which, pursuant to the Share Purchase Agreement,

sold the LAG Shares and is required to pay the amount owed as Price Adjustment;

2. LAG Holding, which, pursuant to the Share Purchase Agreement, was designated

by Parmalat as the buyer of the LAG Shares and is the party entitled to receive the

amount owed as Price Adjustment, is indirectly controlled by Parmalat through

Parmalat Belgium. More specifically:

(i) the Issuer owns the entire share capital of Parmalat Belgium (99% directly and

the remaining 1% indirectly through Dalmata, a wholly owned subsidiary); and

(ii) Parmalat Belgium owns the entire share capital of LAG Holding.

The Transaction’s risk profiles arising from the presence of potential conflicts of interest

have to do with the possibility that the Transaction may entail terms different from those

that would have been applies in an arm’s length transaction.

In this regard, it is worth mentioning that the Related‐party Committee—which constitutes

the committee of independent Directors who are not related parties qualified to render a

reasoned opinion on the Company’s interest in executing the Transaction and the benefits

and substantive fairness of the Transaction’s terms, in accordance with the Procedure

Governing Transactions with Related Parties approved by Parmalat’s Board of Directors on

November 11, 2010 (the “Related‐party Procedure” or the “Procedure”)—was promptly

informed, pursuant to Article 5 of the abovementioned Procedure, of the Transaction’s

terms and conditions and was actively involved in the preparatory phase and negotiation

phase through the delivery of a complete and timely flow of information and its

participation in the negotiations. The Related‐party Committee then agreed by majority

vote to render a favorable reasoned opinion, with Director Mastrangelo voting against the

resolution for the reasons stated below in Section 2.3 of this Information Memorandum.

The abovementioned opinion is appended to this Information Memorandum as Annex

“3.2.”

Pursuant to Article 6.1.2 of the Related‐party Procedure, the Committee relied on the

support of a panel of three independent experts, namely Mario Cattaneo, Paolo Andrei and

Marco Ziliotti (the “Panel of Experts”), tasked with performing verifications concerning

the variances that occurred between marketing expenses actually incurred in 2012 and

15

those defined in the business plan of the Acquired Companies, in accordance with the

provisions of the Share Purchase Agreement.

Please note that the Director Daniel Jaouen is an officer of Lactalis Group companies.

Consequently, at the meeting held by Parmalat’s Board of Directors on May 10, 2013, when

it approved the Notice of Disagreement as defined infra, and on May 30, 2013, when it

approved the mutually agreeable determination of the Price Adjustment, he disclosed any

interest that he may have in the Transaction, directly or on behalf of third parties, by virtue

of the abovementioned posts he held, specifying the type, terms, origin and scope of said

interest, thereby providing the disclosures required pursuant to Article 2391 of the Italian

Civil Code.

Lastly, please note that the Parmalat Director Antonio Sala, who is an officer of Lactalis

Group companies, did not attend the Board meetings of May 10 and May 30, 2013, in

compliance with the order issued by the Court of Parma on March 28, 2013.

1.2 Pending proceedings

On October 8, 2012, Parmalat received a copy a notice that the Court of Parma, granting a

motion by the Public Prosecutor at the same court, activated proceedings pursuant to

Article 2409 of the Italian Civil Code, targeting the Issuer further to a complaint filed by

Amber Capital L.P., a Parmalat shareholder, concerning alleged management irregularities,

specifically with regard to the LAG acquisition. Additional information about this issue is

provided below in Section 2.7 of this Information Memorandum

In addition, the Public Prosecutor of the Court of Parma launched an investigation in

connection with the LAG acquisition. On December 11, 2012, the Chairman, the Chief

Executive Officer, the Chief Operating Officer and the some Directors were served notice

that they were the target of an investigation regarding the crime of aggravated

embezzlement. On the same day, the Parma and Bologna Tax Enforcement Units of the

Revenue Police executed, at the request of the Public Prosecutor of the Court of Parma,

search warrants at the Company’s offices aimed at securing documents concerning the

LAG acquisition.

On November 5, 2012, the Consob informed the members of Parmalat’s Board of Statutory

Auditors in office at that time that it had activated administrative proceedings charging

them with violating their oversight obligation pursuant to Article 149, Section 1, Letter a),

of the TUF, with regard to the correct implementation, within the context of the

Acquisition, of the rules governing related‐party transactions set forth in Article 2391‐bis of

the Italian Civil Code and the Related‐Party Regulations. As of the date of this Information

Memorandum, no action has been taken against Parmalat’s Statutory Auditors and the

Company is waiting for new developments by the Consob in connection with the

abovementioned administrative proceedings.

16

2. INFORMATION ABOUT THE TRANSACTION

2.1 Overview of the Transaction’s characteristics, modalities, terms and conditions

Provisional Price

As stated in the Introduction, pursuant to the Share Purchase Agreement, the total

consideration owed for the Equity Stakes was agreed to for an amount equal to the

algebraic sum of (i) the Enterprise Value of the Acquired Companies at the close of the 2012

reporting year and (ii) their net financial position (cash and cash equivalents) at the end‐of‐

month date closest to the Closing Date (hence, June 30, 2012).

The Enterprise Value of the Acquired Companies was estimated on a preliminary basis as

amounting to USD 904 million, which corresponds to the Provisional Price, based on the

assumption that the EBITDA of the Acquired Companies for the 2012 reporting year would

amount to USD 95.2 million.2

Therefore, the Provisional Price reflected an EBITDA multiple of 9.5.

Pursuant to the Share Purchase Agreement, the net financial position of the Acquired

Companies was computed based on the data shown in the combined financial statements

of the Acquired Companies at June 30, 2012, prepared in accordance with U.S. generally

accepted accounting principles (US GAAP), certified by Ernst & Young, in its capacity as

independent auditor of LAG.

On September 25, 2012, Parmalat’s Board of Directors met to review the abovementioned

certified semiannual results of the Acquired Companies. Specifically, it was informed of the

net financial position, amounting to USD 53.2 million at June 30, 2012, identified as an

addition to the provisional price of USD 904 million, in accordance with the Share Purchase

Agreement. The net financial position amount was paid on October 19, 2012, in accordance

with the deadline stipulated in the Share Purchase Agreement.

The amount paid for the Acquired Companies, before Price Adjustment, thus totaled USD

957.2 million, equal to 750.3 million euros. The Acquisition was financed entirely with

internal funds of the Parmalat Group.

Price Adjustment Mechanism

The Share Purchase Agreement provides a price adjustment a mechanism in order to allow

a determination of the Final Price of the Equity Stakes based on the results actually

reported by the Acquired Companies at the close of the 2012 reporting year, with the price

amount ranging between a cap of USD 960 million and a floor of 760 million.

2 Pursuant to the Share Purchase Agreement, the EBITDA of the Acquired Companies for the 2012 reporting year was

defined as the sum of the following line items in the Price Revision Financial Statements (as defined infra):

EBIT

+ Depreciation, amortization and writedowns of non‐current assets,

– Non‐recurring and extraordinary income (expense).

17

Specifically, it was stipulated that, should the Enterprise Value of the Acquired Companies

at December 30, 2012 (closing date of LAG’s reporting year) be equal to an amount

different from USD 904 million, due to EBITDA of an amount different from USD 95.2

million, the Price would be adjusted, upwards or downwards, to reflect the actual amount

of the Enterprise Value, it being understood that Enterprise Value amounts greater than

USD 960 million or smaller than USD 760 million would not be taken into account for price

adjustment purposes. More specifically:

‐ if the actual Enterprise Value was lower than USD 904 million, BSA would be

required to pay the difference to the Buyer, it being understood that the amount

thus owed by BSA could not be greater than USD 144 million;

‐ if the actual Enterprise Value was higher than USD 904 million, the Buyer would be

required to pay the difference to BSA, it being understood that the amount thus

owed could not be greater than USD 56 million.

Therefore, it was agreed that the Enterprise Value of the Acquired Companies and, if owed,

the related adjustment to the price of the Equity Stakes at the close of the 2012 reporting

year would be computed based on the data shown in the combined financial statements of

the Acquired Companies at December 30, 2012 (closing date of LAG’s reporting year),

prepared in accordance with U.S. generally accepted accounting principles (US GAAP),

certified by Ernst & Young, in its capacity as independent auditor of LAG (the “Price

Adjustment Financial Statements”) and verified through negotiations between the Buyer

and the Sellers.

To that effect, within 60 days from the close of the 2012 reporting year (i.e., by March 1,

2013), LAG was required to deliver to the Buyer and the Sellers the Price Adjustment

Financial Statements, accompanied by the certification report issued by Ernst & Young and

by a certificate, signed by LAG’s Chief Executive Officer and Chief Financial Officer,

containing a computation of the EBITDA and Enterprise Value of the Acquired Company,

as well as, if applicable, the amount owed as a price adjustment (the “Price Adjustment

Certificate”).

The Buyer was required to communicate any disagreement with the data contained in the

Price Adjustment Financial Statements and/or the Price Adjustment Certificate by means of

a special notice (the “Notice of Disagreement”), sent to the Seller within 20 business days

from the date of receipt of the abovementioned documents (i.e., not later than March 29,

2013). Absent such notice, the determinations set forth in the Price Adjustment Certificate

would become final and binding on the parties.

On the other hand, in the event of a disagreement, the Buyer and the Sellers were to

attempt reaching an agreement within 10 business days from the date when the Notice of

Disagreement was received by the Sellers (i.e., not later than April 15, 2013).

If the disagreement could not be resolved, the price adjustment would be submitted to the

determination of a firm of independent auditors, acting in the capacity as arbitrator

pursuant to Articles 1349 and 1473 of the Italian Civil Code.

18

In order to secure the payment of any amount that may be due to the Buyer as a Price

Adjustment, by a contract executed on the Closing Date, BSA Finances gave to Société

Générale an irrevocable mandate.

For the purposes of the clauses governing the determination of the final price of the Equity

Stakes, the parties agreed that marketing expenses (which are a component of the EBITDA

computation that, by its very nature, is highly discretionary) shall be carried out in

accordance with the business plan of the acquired companies or, in any case, “in the ordinary

course of business” and “in accordance with best management practices.” As a result, any

variance in these expenses compared with the business plan that could not be justifies in

accordance with the abovementioned criteria of ordinary business and consistency with best

management practices would authorize Parmalat to obtain a price reduction.

Implementation of the price adjustment process

On March 1, 2013, as required by the Share Purchase Agreement, LAG forwarded to

Parmalat the Price Adjustment Financial Statements and a Price Adjustment Certificate.

The Certificate showed pro forma EBITDA at December 30, 2012 of the Acquired

Companies amounting to USD 96,051,903, which corresponds to an enterprise value of

USD 912,493,077, based on a contractually stipulated EBITDA multiple of 9.5. This amount

is about USD 0.9 million higher than the USD 95.2 million estimated in the business plan of

the Acquired Companies, which served as the basis for determining the provisional price.

These documents were reviewed by the Related‐party Committee at a meeting held on

March 6, 2013.

Consistent with the contractual price adjustment mechanism, this provisional result was

analyzed by the Committee and the Board of Directors, which were supported in their

work by the Transaction Services Group of PricewaterhouseCoopers (“PwC‐TS”), pursuant

to an assignment awarded at the end of November 2012 and amended at the end of

December 2012, and by the Panel of Experts, whose services were retained at the end of

January 2013. The outcome of the work performed in connection with these assignments is

reviewed below.

Pursuant to the Share Purchase Agreement, the Buyer was required to send the Notice of

Disagreement by March 29, 2013. Because the Company found that this deadline was

incompatible with the time technically necessary to perform the reviews subject of the

assignments entrusted to PwC‐TS and the Panel of Experts, the Sellers forwarded to the

Buyer a proposed amendment to the Share Purchase Agreement, extending the

abovementioned deadline to May 10, 2013. This proposal was approved by the Board on

March 14, 2013. Consequently, the deadline by which, if a written challenge was sent by the

Buyer, the parties were required to reach an agreement was extended to May 31, 2013

(instead of April 15, 2013).

Findings from the work performed by PwC‐TS

PwC‐TS completed its assignment and delivered to Parmalat its final report on April 15,

2013. The assignment entrusted to PWC‐TS entailed performing an analysis of the

19

components of the revision of the price of the Acquired Companies, as stated in the Price

Adjustment Certificate, and pointing out any elements that could require downward (or

upward) adjustments to the acquisition price.

The report prepared by PWC‐TS identified a series of restatements of the EBITDA used in

the Price Adjustment Certificate for a total negative amount of USD 3.0 million, reducing

EBITDA from USD 96.1 million to USD 93.1 million.

The adjustments identified by PWC‐TS regard revenues and expenses deemed to be

nonrecurring that resulted in reductions/increases of the EBITDA amount, in accordance

with a specific contract clause, and, to that effect, fall into the following categories:

(i) reversals into the income statement of provisions recognized in previous years

totaling USD 1.9 million;

(ii) elimination of a pro forma adjustment not contractually identified and listed in the

ʺPrice Adjustment Calculation Certificate” amounting to USD 0.6 million;

(iii) other nonrecurring revenues and expenses totaling USD 0.4 million.

As for the marketing expenses, PWC‐TS prepared a comparison between the marketing

expenses projected in the business plan of the Acquired Companies and those, lower,

incurred in 2012, quantifying the difference at USD 13.3 million.

Findings from the work performed by the Panel of Experts

The document prepared by PwC‐TS was made available to the Panel of Experts, whose

specific assignment was to determine whether any negative variance of marketing

expenses compared with the business plan of the Acquired Companies, as shown in the

actual 2012 data of the Acquired Companies, occurred within the “ordinary course of

business” and was consistent with “best management practices” and, consequently, also

with respect to future years, was justified and consistent with the stipulations of the Share

Purchase Agreement, or whether it gave Parmalat the right and standing to demand from

the seller the payment of a price adjustment amount, in accordance with the criteria of the

contract’s provisions.

The Panel of Experts completed its assignment and delivered its final report to Parmalat on

April 30, 2013.

The Panel of Experts reviewed the reasons for the adjustments to the 2012 EBITDA

recommended by PwC‐TS and, further to its own assessments, indicated that it concurred

with the proposed adjustments for a total negative amount of USD 3.0 million. The Panel of

Experts also analyzed the other items identified by PwC‐TS but not used as part of the

EBITDA normalization process, defined as “other items for consideration.” Because the

amounts of most of these items were uncertain, the Panel of Experts thought it reasonable to

follow the practice of accepting a figure equal to 50% of the total amount of USD 0.9 million.

Lastly, the Panel of Experts analyzed the negative variance in marketing expenses

compared with the business plan of the Acquired Companies, concluding that a

preponderant portion of this variance, quantified at USD 11.3 million, did qualify as

20

necessary for correctly determining the price difference pursuant to the Share Purchase

Agreement. This amount does not include USD 2 million for efficiencies in packaging and

purchasing of advertising space. The Panel of Experts believed that these efficiencies could

be construed as being consistent with “best management practices” if properly

documented.

The Panel of Experts thus concluded that a price adjustment in favor of Parmalat of about

USD 134 million appears to be a “reliable and robust reference basis for Parmalat in the

upcoming price adjustment procedure with the vendor.”

LAG price adjustment letter to the Sellers (Notice of Disagreement)

The price adjustment request qualifies as a highly material, related‐party transaction

requiring a favorable opinion by the Committee.

The Committee made the necessary adjustments to the EBITDA computed by LAG, making

adjustments of USD 2.34 million for nonrecurring costs and items and USD 13.3 million for

the difference between the marketing expenses projected in the business plan of the

Acquired Companies and those recognized in 2012.

However, the Committee, similarly to the Panel of Experts, found a certain degree of

subjectivity in the redetermination of EBITDA, due to the presence of certain uncertainty

factors that could not be eliminated.

Consequently, the Board of Directors, in light of the opinion rendered by the Committee,

unanimously agreed to authorize the LAG Holding subsidiary to send to the seller B.S.A.

S.A., which, through Sofil S.a.s., holds an 82.2% interest in Parmalat S.p.A., a letter

requesting a price adjustment of USD 144 million, which is the maximum adjustment

permissible under the Agreement.

The price adjustment request does not originate from a different strategic value of the

Acquired Companies but from the implementation of contract clauses; the request was

destined to be the subject of negotiations with the Sellers as part of the final phase of a

contractually defined process and, consequently, its amount was subject to change

Response by the Sellers

On May 24, 2013, the Sellers sent to LAG Holding and Parmalat a letter in response to the

Notice of Disagreement, which set forth the Price Adjustment request, contesting some of

the EBITDA adjustment it contained. Specifically, the Sellers asked that the adjusted

EBITDA be increased by adding back the total amount of USD 1.5 million, broken down as

follows: (i) USD 0.6 million for the margin that LEA was entitled to receive for the first half

of 2012 pursuant to the Distribution Agreement; (ii) USD 0.65 million for the reversal of a

provision for slotting expenses, which should be treated as a recurring item and,

consequently, as a positive EBITDA component; and (iii) USD 0.3 million for the reversal of

a workers’ compensation provision recognized in 2012, The Sellers also took a different

position with regard to an adjustment totaling USD 13.3 million for the reduction in

marketing expenses compared with the business plan of the Acquired Companies, on the

one hand, contesting that this reduction was not made “in the ordinary course of business”

21

and “in accordance with best management practices” and, on the other hand, pointing out

the existence of marketing efficiencies realized in 2012 amounting to USD 2 million. The

Sellers proposed a price adjustment in an amount ranging between USD 67 million and

USD 76 million and asked Parmalat and LAG Holding to set up a meeting in order to

achieve a mutually agreeable solution as to the amount of the Price Adjustment.

Meeting between the parties

The parties met on May 28, 2013; this meeting was attended, for the Sellers, by the top

management of the Lactalis Group, supported by representatives of Ernst&Young; for the

Buyer, by Parmalat’s management, supported by all Committee members; for the Panel of

Experts by Paolo Andrei and Marco Ziliotti, supported by Luca Pellegrini; and by a

representative of PwC‐TS. Angelo Manaresi, Commissioned ad acta appointed by the Court

of Parma within the framework of the proceedings activated pursuant to Article 2409 of the

Italian Civil Code was also present.

In the course of the meeting, the Sellers initially reaffirmed their positions, as presented in

their letter of May 24, 2013; in turn, Parmalat’s management confirmed the statements

made in the Notice of Disagreement. Subsequently, both parties mutually agreed to

concessions about marketing expenses, including efficiencies, as no supporting documents

were provided either by the Sellers, to justify these efficiencies, or by the Buyer, for the

EBITDA restatements.

At the end of the meeting, the parties were still in disagreement with regard to the

recognition, requested by the Sellers, of a reduction in marketing expenses attributable to

LEA/LINT amounting to USD 0.7 million.

Sellers’ proposal received on May 30, 2013

Subsequent to the meeting, in the course of which the parties were unable to reach a

possible agreement, contacts between the parties continued and, on May 30, 2013, the

Sellers submitted to Parmalat a proposal by which, while not agreeing on the merit with

the arguments put forth by Parmalat and LAG Holding, for the sole purpose of reaching a

mutually acceptable determination of the Final Price and thus avoid remitting this

determination to an arbitrator, they indicated their willingness to pay to LAG Holding the

sum of USD 130 million as a Price Adjustment; this proposals was valid until midnight on

May 30, 2013.

Acceptance of the proposal by Parmalat and LAG Holding

Parmalat’s Board of Directors met on May 30, 2013 and, having received the Opinion

rendered by the Committee, which met on the same date, resolved to authorize the Buyer

to accept the Sellers’ proposal, thereby agreeing to a mutually agreeable determination of

the Price Adjustment in the amount of USD 130 million. Specifically, the Board of Directors

concurred with the remarks of the Committee, which, without changing the adjustment for

the full difference in marketing expenses, agreed to the positive accounting adjustment to

EBITDA, finding that the adjustment for the margin attributable to LEA/LINT for the first

half of 2012 was “was reasonable, based on a substantive interpretation of the intent of the parties”

and that the workers’ compensation adjustment was “acceptable,” and allowing the

22

adjustment for slotting expenses (as explained un Section 2.4) based on the adoption of

fairness criteria. In this manner, Parmalat was able to quickly achieve a resolution of the

dispute, while avoiding the uncertainties that always characterize arbitration proceedings

in accordance with Article 1349 of the Italian Civil Code, in which the arbitrator is required

to “rule in equity,” taking into account the fact that, as noted by the Panel of Experts, there

also were certain items benefiting the Sellers, albeit not supported by sufficient evidence,

for which no amount was recognized.

The agreed Price Adjustment amount, plus contractually stipulated accrued interest, will be

paid to LAG Holding within 15 days from the conclusion of the agreement between the

parties, i.e., by June 14, 2013.

In implementation of a specific clause of the Share Purchase Agreement, in order to secure

the payment of the abovementioned amount, on the Closing Date, an irrevocable mandate

was given to Société Générale, in its capacity as paying agent, calling for the payment of up

to USD 144 million, plus accrued interest, drawn from a revolving credit line available to

the Lactalis Group. While this mandate was in effect, Parmalat and LAG Holding received

every two months information certifying the availability of said amount drawn from the

abovementioned credit line.

Additional safeguards for Parmalat

In addition to the warranties that are customary for transactions of this type, the Share

Purchase Agreement provided express warranties for the historical and projected data

supplied to Parmalat within the framework of the due diligence process. By virtue of said

warranties, should the information obtained as part of the due diligence process prove to

be untrue, incorrect or incomplete or if the projected data supplied by the Sellers should

prove not to have been based on reasonable assumptions and/or not developed consistent

with the underlying assumptions, the Buyer shall be entitled to compensation without any

limitation, for the full amount of the damage it may have incurred. These warranties shall

expire within five years from the Closing Date.

As noted in a press release published by Parmalat on April 5, 2013, the assignments

entrusted to the Commissioner ad acta include that of verifying “that the Board of Directors of

Parmalat S.p.A. is taking full and timely action to detect any indications that the historical data

supplied may not be truthful and/or that the projected data used in the so‐called vendor due diligence

prepared by Ernst & Young pursuant to Clauses 5.24.3 and 5.24.4 of the Share Purchase Agreement

may be unreasonable, also based on the documentation of L.A.G., Lactalis Brazil and Lactalis

Mexico, indicating any corrective action, if needed.”

To that effect, on April 23, 2013, the Committee retained the services of PwC‐TS for the

purpose of assisting the Board of Directors in the process of detecting any indications that

the historical data supplied may not be truthful.

Meeting on May 30, 2013, the Board of Directors, having been informed of the Committee’s

opinion, agreed that, based on the verifications performed and the concluding document

with the findings of PwC‐TS dated May 16, 2013, no indications that the historical data

supplied may not be truthful were detected.

23

On May 3, 2013, the Committee also retained the services of Deloitte Financial Advisory for

the purpose of assisting the Board of Directors in the process of detecting any indications

that the that the projected data used in the so‐called Vendor Due Diligence may be

unreasonable. Deloitte Financial Advisory is expected to prepare a final report with his

findings by the end of June.

2.2 Description of the related parties with whom the Transaction was executed, the nature of

the relationship and the nature and scope of the interest of the abovementioned parties

in the Transaction

The Transaction qualifies as a related‐party transaction executed through a subsidiary

because:

a) Parmalat is controlled by BSA, which, pursuant to the Share Purchase Agreement, sold

the LAG Shares and is required to pay the amount owed as Price Adjustment;

b) LAG Holding, which, pursuant to the Share Purchase Agreement, was designated by

Parmalat as the buyer of the LAG Shares and is the party entitled to receive the amount

owed as Price Adjustment, is indirectly controlled by Parmalat through Parmalat

Belgium. More specifically:

i. the Issuer owns the entire share capital of Parmalat Belgium (99% directly and the

remaining 1% indirectly through Dalmata, a wholly owned subsidiary); and

ii. Parmalat Belgium owns the entire share capital of LAG Holding.

The Transaction’s risk profiles arising from the presence of potential conflicts of interest

have to do with the possibility that the Transaction may entail terms different from those

that would have been applies in an arm’s length transaction.

In this regard, it is worth mentioning that the Committee for Related‐party Transactions—

which constitutes the committee of independent Directors who are not related parties

qualified to render a reasoned opinion on the Company’s interest in executing the

Transaction and the benefits and substantive fairness of the Transaction’s terms, in

accordance with the Procedure Governing Transactions with Related Parties—was

promptly informed, pursuant to Article 5 of the abovementioned Procedure, of the

Transaction’s terms and conditions and was actively involved in the preparatory phase and

negotiation phase through the delivery of a complete and timely flow of information and

its participation in the negotiations. The Related‐party Committee then agreed by majority

vote to render a favorable reasoned opinion, with Director Mastrangelo voting against the

resolution for the reasons stated below in Section 2.3 of this Information Memorandum.

The abovementioned opinion is appended to this Information Memorandum as Annex

“3.2.”

Pursuant to Article 6.1.2 of the Related‐party Procedure, the Committee relied on the

support of a panel of three independent experts, namely Mario Cattaneo, Paolo Andrei and

Marco Ziliotti, tasked with performing verifications concerning the variances that occurred

between marketing expenses actually incurred in 2012 by LAG and LINT and those defined

24

in the business plan upon which the Acquisition was based, in accordance with the

provisions of the Share Purchase Agreement.

Please note that the Director Daniel Jaouen is an officer of Lactalis Group companies.

Consequently, at the meeting held by Parmalat’s Board of Directors on May 10, 2013, when it

approved the Notice of Disagreement, and on May 30, 2013, when it approved the mutually

agreeable determination of the Price Adjustment, he disclosed any interest that he may have

in the Transaction, directly or on behalf of third parties, by virtue of the abovementioned

posts he held, specifying the type, terms, origin and scope of said interest, thereby providing

the disclosures required pursuant to Article 2391 of the Italian Civil Code.

Lastly, please note that the Parmalat Director Antonio Sala, who is an officer of Lactalis

Group companies, did not attend the Board meetings of May 10 and May 30, 2013, in

compliance with the order issued by the Court of Parma on March 28, 2013.

As of the date of this Information Memorandum, BSA, which is at the apex of the corporate

pyramid of the Lactalis Group, exercises guidance and coordination over Parmalat.

2.3 Description of the economic motivations for the Transaction and its benefits for

Parmalat

The Board of Directors, in assessing the Transaction’s benefits for Parmalat, concurred with

the remarks of the Related‐party Committee, which, without changing the adjustment for

the full difference in marketing expenses, agreed to the positive accounting adjustment to

EBITDA, finding that the adjustment for the margin attributable to LEA/LINT for the first

half of 2012 was “was reasonable, based on a substantive interpretation of the intent of the parties”

and that the workers’ compensation adjustment was “acceptable,” and allowing the

adjustment for slotting expenses based on the adoption of fairness criteria. In this manner,

Parmalat was able to quickly achieve a resolution of the dispute, while avoiding the

uncertainties that always characterize arbitration proceedings in accordance with Article

1349 of the Italian Civil Code, in which the arbitrator is required to “rule in equity,” taking

into account the fact that, as noted by the Panel of Experts, there were also certain items

benefiting the Sellers, albeit not supported by sufficient evidence, for which no amount was

recognized.

In assessing the benefits of the Transaction for Parmalat, the Committee note, inter alia,

that:

i) The proposed Price Adjustment amount differs from the amount requested in the

Notice of Disagreement by not more than 10%;

ii) The Price Adjustment proposal is close to the maximum contractually permissible

amount of USD 144 million;

iii) The conclusions reached by the Committee in the final analysis are substantially in

line with guidance provided by the Panel of Experts, which, in its report of April 30,

2013, concluded that an “Enterprise Value amount of about $770 million appears to be (…)

a reliable and robust reference basis for Parmalat in the upcoming price adjustment procedure

with the Vendor.” Upon conclusion of the negotiation phase, the defined Price

25

Adjustment amount differs by not more than 3% from the one recommended by the

Panel of Experts, for an implied multiple of 2012 reported EBITDA of about 8.1.

Parmalat’s Board of Directors met on May 30, 2013 and, having received the Committee’s

opinion, agree by a majority vote, with the Directors Mastrangelo and Mosetti voting

against the resolution, to authorize the acceptance of the Sellers’ proposal, thereby

achieving a mutually acceptable determination of the Price Adjustment in the amount of

USD 130 million.

Director Mastrangelo voted against the resolution not because he disagreed that reaching

an agreement with the Sellers was beneficial, but objected to the amount offered, finding it

inappropriate to stray from the amount of USD 134 million recommended by the Panel of

Experts.

Director Mosetti explained his negative vote by stating, inter alia, that he could not support

an agreement entailing a price adjustment of an amount lower than the one recommended

by the Panel of Experts, which earlier the Company’s Board of Directors deemed

appropriate, and that the timing and method by which the Company agreed to accept the

proposal it received from the Sellers could have been handled differently, specifically by

immediately beginning negotiations and requesting the support of experts only at the end

of the negotiations.

The Board of Directors, being cognizant of the positions stated by the Directors

Mastrangelo and Mosetti, concluded that (i) the difference of USD 4 million from the

amount recommended by the Panel of Experts, when compared with the total amount of

the transaction, is relatively minor and, consequently, entirely reasonable within the

framework of complex negotiations; and (ii) the modalities by which the Company agreed

to accept the proposal received from the Sellers were fully consistent with contractual

stipulations and, thus, protective of Parmalat’s interest. Moreover, had the Company failed

to abide by said stipulations and moved forward the phases of the procedure, it would

have lost the option of enforcing its rights with the effectives that it later achieved.

2.4 Methods for determining the consideration and assessment of its fairness compared with

market values for similar transactions

As described in detail in Section 2.1, the Share Purchase Agreement provides a price

adjustment a mechanism in order to allow a determination of the Final Price of the Equity

Stakes based on the results actually reported by the Acquired Companies at the close of the

2012 reporting year, with the price amount ranging between a cap of USD 960 million and a

floor of 760 million.

The Agreement also requires that the determination of the Final Price be carried out based

on data presented in audited financial statements and through negotiations between the

parties and that if disagreements could not be resolved through negotiations, the price

adjustment would be submitted to the determination of a firm of independent auditors,

acting in the capacity as arbitrator pursuant to Articles 1349 and 1473 of the Italian Civil

Code.

26

The main arguments put forth by the parties in support of their position in the course of the

negotiations and which resulted in the determination of the Final Price are summarized

below.

The Price Adjustment Certificate, the Notice of Disagreement and the Sellers’ reply show

the significant distance that existed between the positions of the parties. In the course of the

subsequent meeting with the Sellers, further to intense negotiations, the parties reached a

basis for the achievement of an agreement on the amount of the price adjustment in favor

of the Buyer.

More specifically, with regard to marketing expenses, the Sellers claimed that a significant

portion of the variance between the expenses incurred in 2012 and those listed in the

business plan of the Acquired Companies, amounting to USD 13.3 million should be

viewed as having occurred “in the ordinary course of business” and consistent with “best

management practices” and, consequently, was in compliance with the provisions of the

Agreement and, specifically, with Article 2.2.5 of the Share Purchase Agreement.

In this regard, please note that, pursuant to the abovementioned clause of the Agreement,

marketing expenses (which are a component of the EBITDA computation that, by its very

nature, is highly discretionary) were to be carried out in accordance with the business plan

of the Acquired Companies or, in any case, “in the ordinary course of business” and “in

accordance with best management practices.” As a result, any variance in these expenses

compared with the business plan that could not be justifies in accordance with the

abovementioned criteria of ordinary business and consistency with best management

practices would empower Parmalat to obtain a price reduction.

In support of their position, the Sellers asserted compliance with the “ordinary course of

business” requirement based on the following circumstances: (i) in 2012, the marketing

expenses of the Acquired Companies increased by about 20.2% compared with the

previous year; (ii) a Parmalat subsidiary that operates in a neighboring country, i.e.,

Canada, cut its marketing expenses by 16% compared with its budget in 2012 (13% for the

Parmalat Group as a whole); (iii) already in 2011, LAG reduced marketing expenses by

about 23.6% compared with projections in the 2011 budget.

As for “best management practices,” the Sellers put forth mainly arguments concerning

“marketing efficiencies.” More specifically, making reference to the analysis carried out by

PwC‐TS in its report of April 15, 2012, they pointed out that about USD 2 million were

attributable to efficiencies in the purchasing of advertising space (for USD 1.1. million) and

in packaging and other marketing costs (for USD 0.9 million), also specifying that the

Vizeum space purchasing agency succeeded in negotiating a lower CPM (cost per thousand

of impression), generating a savings of about 20% compared with the amount budgeted in

the business plan.

Consequently, in accordance with the position presented by the Sellers, it would have been

fair to exclude from the proposed adjustment to 2012 EBITDA the aggregate amount of

USD 5.9 million because these items were consistent with the “ordinary course of business”

and/or in line with “best management practices.”

27

With regard to requests concerning marketing expenses, Parmalat rejected all changes for

which additional supporting documents beyond those already available could not be

produced. The same conclusion was later confirmed with regard to a compromise proposal

put forth by the Sellers regarding lower marketing expenses incurred by LEA (USD 0.7

million), also because of lack of additional documents supporting the alleged savings.

In addition, the Sellers, in line with the provisions of Clauses 2.2 and 2.3 of the Share

Purchase Agreement, provided their remarks about the following adjustments to EBITDA:

a) “Distribution Agreement Q1‐Q2 commissions.” This item, which is a positive component

of 2012 EBITDA, was adjusted downward reducing EBITDA by USD 0.60 million,

further to the analyses performed by PwC‐TS, based on the pro forma nature of an

adjustment not provided for in the Share Purchase Agreement. With regard to this item,

the Sellers noted that the intent of the parties was to include in the EBITDA for the 2012

reporting year the distribution margins as from January 1, 2012, even though the

agreements were executed in July 2012. Consequently, they asked that the amount of

USD 0.6 million accrued in the first half of 2012 be treated as a positive adjustment to

the reported EBITDA of the Acquired Companies for the 2012 reporting year. Parmalat,

taking into account the input of the Panel of Experts, who classified this item as one of

those characterized by uncertainty, agreed that the allocation to LEA of the margins

earned in the first half of 2012 was consistent with the expressed intent of the parties to

the Distribution Agreement.

b) “Workers’ compensation.” This item, which is a positive component of 2012 EBITDA, was

deducted from EBITDA, further to the analyses performed by PwC‐TS, because it

represent a partial reversal of a provision recognized in previous years, i.e., a

nonrecurring income component. The Sellers pointed out that in 2013 the amount set

aside in 2012 (totaling USD 0.30 million) became a partial reversal of a provision

recognized the previous year. Consequently, they requested a restatement of 2012

EBITDA in the amount of USD 0.3 million. Parmalat, having verified that LAG

recognized the abovementioned reversal in the first quarter, agreed to make this

adjustment.

28

c) “Slotting expenses.” This item, which is a positive component of 2012 EBITDA, was

deducted, reducing EBITDA by USD 0.65 million, further to the analyses performed by

PwC‐TS. Because it represent a partial reversal of a provision recognized in previous

years, it is a nonrecurring income component. However, the Sellers specified that a

review of the trend of reversals in previous years shows that this item was not of a

nonrecurring nature. Parmalat disagreed with this approach but agreed to the inclusion

of this amount among the EBITDA adjustments only for the purpose of ending further

disputes.

29

The table below shows the determination of the Final Price (with rounded figures) further

to the negotiations carried out by the parties:

in millions of USD

Adjusted EBITDA – PwC 93.06

Net distribution commissions Q1 and Q2 2012 0.60

Slotting Expenses 0.65

Workers’ Compensation 0.30

Variance in marketing expenses of LAG and LINT (13.30)

Adjusted EBITDA 81.31

EV (Adjusted EBITDA X 9.5) 772.44

The final Enterprise Value was thus equal to USD 772.44 million, later rounded to USD 774,

for an implied multiple of 2012 EBITDA (as shown in the financial statements of the

acquired companies) of about 8.1.

The amount of the Price Adjustment (computed as the difference between the Provisional

Price of USD 904 million and the Enterprise Value computed above of USD 774 million) is

thus defined at USD 130 million.

With regard to the fairness of the Final Price (amounting to USD 774 million), please see the

information provided in Section 2.1.3 of the Addendum to the Information Memorandum

published by Parmalat on June 27, 2012. In addition, for the sake of complete information

and for comparison purposes, please note that, at the end of 2012, the Saputo Group of

Canada completed the acquisition of Morningstar, an operator active in the United States

market in the bread and cheese categories without having any major brands, based on an

EBITDA multiple (before tax effect) of 9.5.

Lastly, as part of its assessment of the Transaction, the Committee took into consideration

the contractually provided option of having the final price of the Equity Stakes determined

by a firm of independent auditors acting in the capacity as an arbitrator and the potential

consequences of such a solution.

In addition to the considerations about the timing , presumably long, of such a solution, the

Committee carefully assessed the risk that the determination of the arbitrator could be

penalizing for Parmalat compared with the determination reached jointly by the parties.

Specifically, the uncertainty related to the total exclusion of efficiencies from marketing

costs, quantifiable at about USD 2 million and the high probability that two of the three

EBITDA adjustments requested by the sellers be allowed further caused the Committee to

favor a mutually agreed determination of the Price Adjustment over one by the Arbitrator.

30

The Committee, in rendering a reasoned opinion about the Company’s interest in executing

the Transaction and the fairness of its economic terms, reviewed and took into account the

findings of the engagements entrusted to PwC‐TS and the Panel of Experts, as mentioned

earlier in this Memorandum.

The members of the Panel of Experts also provided attestations that they met the

independence requirements and had no economic, investment or financial relationship

with the Issuer, parties controlling it, its subsidiaries and joint ventures and Directors of

said parties.

Pursuant to Article 5 of the Related‐party Regulations, a copy of the Opinion of the

Committee for Related‐party Transactions is annexed to this Information memorandum.

The abovementioned document is also available on the Company website

(www.parmalat.com).

2.5 Effects of the Transaction on the financial position, income statement and cash flow

The Company prepared this Information Memorandum in accordance with Article 9 of the

Procedure, which requires the publication of an information memorandum whenever a

highly material transaction is executed.

The Acquisition qualified as a transaction under common control, i.e., as a business

combination in which the companies that are parties to the business combination (Parmalat

and LAG, in this case) are controlled by the same entity (BSA) both before and after the

business combination and the control is not temporary.

As a result, the criterion applied was that of the continuity of values for the net transferred

assets, which were recognized at the values at which they were carried before the

transaction in the accounting records of the companies that are parties to the business

combination.

Consequently, the difference between the Provisional Price and the net carrying amount of

the acquired assets and liabilities, equal in this case to 476.0 million euros, was recognized,

upon closing, as an adjustments to the reserves of the shareholders’ equity attributable to

the Parmalat Group, thereby creating a negative reserve of equal amount.

The Price Adjustment of USD 130 million (equal to 101.8 million euros) will generate, by

June 14, 2013, the collection of proceeds of equal amount, plus accrued interest, and, in the

Issuer’s consolidated financial statements, a reduction of 374.2 million euros in the negative

equity reserved originally recognized for the amount of 476.0 million euros.

The impact of the Price Adjustment described above, would bring the shareholders’ equity

of the Parmalat Group to 3,145.7 million euros at December 31, 2012 (3,043.9 million euros

in the draft statutory financial statements for the year ended December 31, 2012) and to

3,115.4 million euros at March 31, 2013 (3,013.6 million euros in the interim report on

operations at March 31, 2013).

31

The entries recognized in the separate financial statements of LAG Holding will reflect the

collection of proceeds totaling USD 130 million, plus accrued interest, and a concurrent

reduction of equal amount in the carrying value of the investment in LAG

The price adjustment will have no impact on the separate financial statements of Parmalat

and Parmalat Belgium.

The Company is currently defining the modalities for the utilization of the liquidity

generated by the Price Adjustment.

2.6 Impact of the Transaction on the compensation of the members of the management

entities of the Company and/or its subsidiaries

The Transaction will have no impact compensation of the members of the management

entities of the Company and/or its subsidiaries.

2.7 Listing of any members of the management and control entities, general managers and

executives of the Company involved in the Transaction

Except as specified below, no members of the Board of Directors and Board of Statutory