parque arauco day colombia · parque arauco day colombia october 2017. 2 agenda • parque arauco...

TRANSCRIPT

Parque Arauco Day ColombiaOctober 2017

2

Agenda

• Parque Arauco Corporate Overview

• Parque Arauco Colombia Overview

•

Industry• Managing Parque La Colina• Organizational Improvements• Mixed Use Rationale for Malls• Parque Arboleda Overview

3

40

76

104

147186208

/

1

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

/

1

Parque Arauco Corporate OverviewOctober 2017

CONTACTSSARAH INMON (HEAD OF INVESTOR RELATIONS) |

EDUARDO PEREZ MARCHANT (CORPORATE FINANCE MANAGER) |

CLAUDIO CHAMORRO (CFO) |TEL: (562) 22990510 | EMAIL: [email protected]

/

2

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Important Disclaimer

This document has been prepared by Parque Arauco for the purpose of providing general information about the Company.

The Company assumes no responsibility for, or makes any representation or warranty, express or implied, with respect to,

the accuracy, adequacy or completeness of the information contained herein. The Company expressly disclaims any liability

based on such information, errors therein or omissions therefrom.

This presentation includes certain statements, estimates and forecasts provided by the Company with respect to it’s anticipa-

ted future performance and involves significant elements or subjective judgment and analysis that may or may not prove to

be accurate or correct. There can be no assurance that these statements, estimates and forecasts will be attained and actual

outcomes and results may differ materially from what is estimated or forecast herein.

The information contained herein has been prepared to assist interested parties in making their own evaluation of the

company and does not purport to be all - inclusive or to contain all the information that a potential counterparty may desire.

In all cases, interested parties should conduct their own independent investigation and analysis of the Company. Interested

parties can only rely on the result of their own investigation and the representations and warranties made in any definitive

agreement that may be executed.

/

3

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

INTRODUCTION

OUR OPERATIONS

INVESTMENT HIGHLIGHTS

FUTURE DEVELOPMENTS

/

4

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Parque AraucoOPERATIONAL METRICS BY COUNTRY

OPERATIONAL METRICS BY FORMAT

46.0% 60.6%

14.4%

10.3%

29. 1%39.6%Parque Arauco is the third largest shopping center operator in Chile and Peru, and the fourth largest in Colombia.

24% Foreign

investment funds

22% Local brokers

1% Local mutual funds

6% Others 26%

Controlling Group

5% Said Yarur Family

3% Abumohor Family

13%Local pension funds

DAILY TRADED VOLUME 2Q17: US$MM 2.9

85.6%

6.7%2.7%

5.0%

78.9%

6.4%4.0%

10.7%

Parque Arauco at a glance

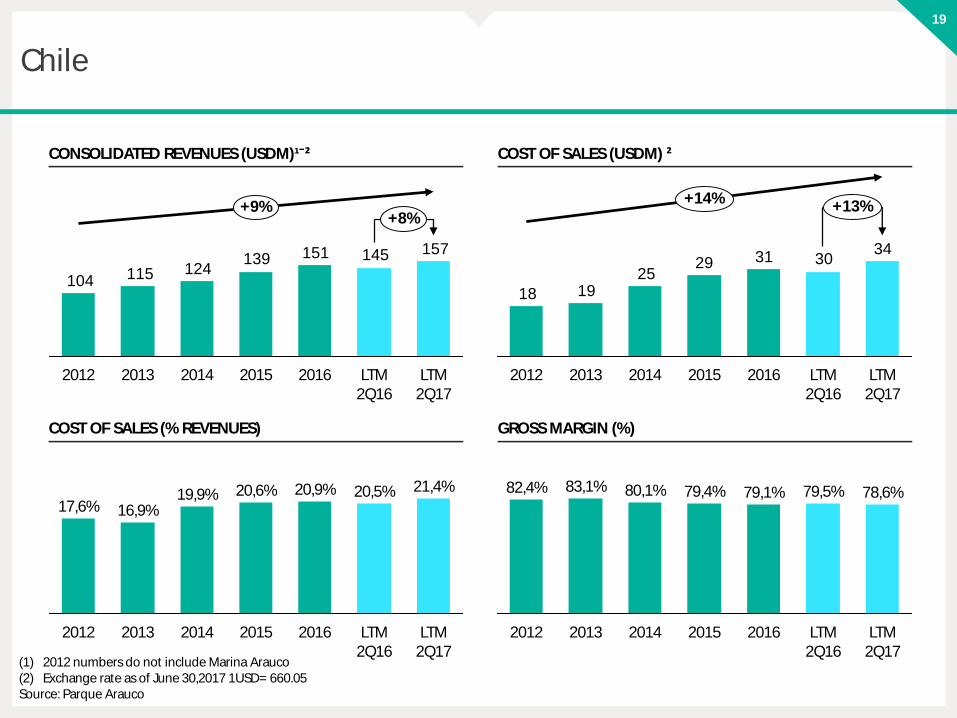

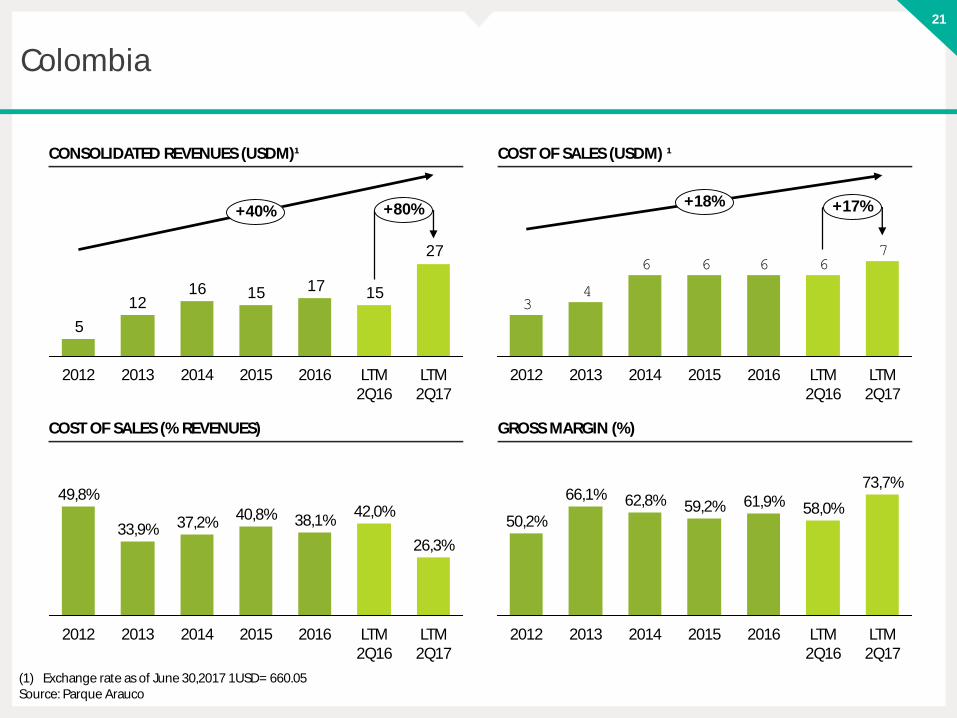

Indicator/ Country CHILE PERU COLOMBIA TOTAL

Total GLA (m2)1 455,500 391,500 142,500 989,500

Owned GLA (m2) 418,685 276,750 124,050 818,485

Revenues LTM 2Q17 (US$MM)2 157 76 27 260

# of operations 25 19 3 47

MARKET CAP3

US$MM 2,263

SHAREHOLDER STRUCTURE (JUNE 2017)

Chile Peru Colombia

Regional Neighborhood Outlet Strip center

TOTAL GLA1

989,500 M2

TOTALREVENUES2

US$MM 260

TOTAL GLA1

989,500 M2

TOTAL REVENUES2

US$MM 260

Source: Parque Arauco. (1) Does not include Marina Arauco nor Mall Center Curicó.(2) Revenues from July 2016- June 2017. Exchange Rate: US$= 660.05

(3) Source: Bloomberg

/

5

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

GLA(1) M2

In the last five years Parque Arauco has doubled GLA, revenues and EBITDA

1982 Parque Arauco Kennedy opens as first shopping center in Chile

1993 Arauco Maipu inaugurates in Santiago

1995 Parque Arauco S.A. IPO

1997 Inauguration of Marina Arauco in Viña del Mar, Chile

2006 Parque Arauco expands into Peru with the purchase of a 45% stake in MegaPlaza Norte in Lima

2008 Parque Arauco acquires Arauco Estación in Santiago, Chile

2010 Parque Arauco opens first mall in Colombia, Parque Arboleda in Pereira

2011 Capital increase for US$145 MM

2012 Parque Arauco enters outlet format in Chile by acquiring Arauco Premium Outlet Buenaventura

2014 Capital increase for US$182 MM

2015 Purchase of minority shareholders in Colombia and Peru

2016 Capital increase for US$100 MM2012 2013 2014 20162015 LTM

2Q17

559,700 693,100 728,500818,500 935,900

989, 500

+1.8x

EBITDA(1) US$ MM

99 113 130152 167

182

REVENUES(1) US$ MM

+1.8x

2012 2013 2014 20162015 LTM 2Q17

141 163 1191222 243

260

2012 2013 2014 20162015 LTM 2Q17

+1.8x

Source: Parque Arauco. Exchange Rate: US$= 660.05(1) Does not include Marina Arauco nor Mall Center Curicó.

/

6

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

The spread over the cost of capital of our last projects is approximately 3%

Source: Parque Arauco

(1) Real cap rate is the yield on cost rate averaged by amount invested and considers the following properties: Arauco Express Calama, Arauco Express Ciudad Empresarial I, Arauco Express Colón, Arauco Express Huechuraba, Arauco Express Irarrázaval, Arauco Express Las Brujas, Arauco Express Luis Pasteur, Arauco Express Manuel Montt, Arauco Express Palmares, Arauco Premium Outlet Buenaventura, Arauco Premium Outlet Curauma, Arauco Premium Outlet San Pedro, Arauco Premium Outlet Coqumbo, Arauco Quilicura, MegaPlaza Chimbote, MegaPlaza Express Villa El Salvador, MegaPlaza Express Chincha, InOutlet Faucett, Viamix Chorrillos, Viamix Las Malvinas, InOutlet Premium Lurín, MegaPlaza Cañete, MegaPlaza Express Barranca, MegaPlaza Pisco, El Quinde Cajamarca, El Quinde Ica, Plaza Jesús María, Parque Caracolí.

(2) Weighted Average Cost of Capital

9%

REAL CAP RATE(1) REAL WACC (2) SPREAD OVER REAL WACC

6%

3%

/

7

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Parque Arauco’s value creation is proven by the fact that it has had one of the highest “Total Return” of the real estate sector in the last years

Total ReturnPa

rque

Ara

uco

GGP

Fala

bella

S&P

500

Igua

tem

i

Mac

eric

h

Uni

bail

Ham

mer

son

Mul

tipla

n

Fibr

a U

no

Klep

ierr

e

Sim

on

IPSA

Taub

man

Intu

BR M

alls

Allia

nsce

Cenc

osud

14%

7%8%

4%

12%

4%

7%

-1%

12%

6%

8%

-1%

11%

4%

7%

-6% -7%

Source: Bloomberg(1) Total return includes dividends as of july 31, 2017.

-6%

TOTAL RETURN1, LAST 5 YEARSANNUALIZED, LOCAL CURRENCY

TOTAL RETURN1, LAST 15 YEARSANNUALIZED, LOCAL CURRENCY

Taubman

Klepierre

Falabella

Hammerson

Macerich

Simon

GGP

Parque Arauco

IPSA

Intu

S&P 500

4%

18%18%

11%11%

9%7%7%

4%

2%-4%

/

8

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

FIXED VS VARIABLE RENTAL REVENUES AS OF JUNE 30, 2017

CONTRACT LENGTH (BASED ON % OF REVENUES)

32%14%

14%

40% 100%

‹2 YEARS 2-3 YEARS 3-4 YEARS ›4 YEARS TOTAL

Our rental revenues are derived primarily from fixed contracts and are protected against inflation

40% of our contracts have a duration of more than 4 years and the average length is 6.0 years

14%Variable Revenues

86% Fixed Revenues

15% Other Revenues

Revenue type and contract duration

85% Rental Revenues

/

9

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

CORPORATE PURPOSE

Purpose, Mission and Corporate Values

Our purpose is to create spaces that contribute to improving people’s lives.

MISSION

Our mission is to be leaders in developing and operating real estate assets, through profitable andsustainable growth that generates value for our stakeholders

PILLARS OF OUR CULTURE

Happiness

Excellence

STRATEGIC OBJECTIVES

Growth

Profitability

Sustainability

OUR VALUES

and the environment

Respectfor people

Opennessto change and innovation

Right option,Choose the

not the easiest one things

Makehappen

that inspiresan exceptional

Team

Createa work environment

/

10

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

INTRODUCTION

OUR OPERATIONS

INVESTMENT HIGHLIGHTS

FUTURE DEVELOPMENTS

/

11

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Colombia

Perú

Chile

Chilean Portfolio

Chile GLA (m2) % OwnershipOwned GLA

(m2)Occupancy

Year of incorporation

Parque Arauco Kennedy 112,500 100% 112,500 96.8% 1982

Arauco Maipú 74,000 100% 74,000 99.2% 1993

Arauco Chillán 32,000 100% 32,000 99.9% 2007

Arauco Estación 66,500 83% 55,195 97.1% 2008

Arauco San Antonio 28,500 65% 18,388 95.7% 2009

Arauco Express1 33,000 53% 17,602 82.2% 2012

Arauco Premium Outlets2 47,000 100% 47,000 92.7% 2012

Arauco Quilicura 32,000 100% 32,000 100.0% 2013

Arauco Coronel 30,000 100% 30,000 93.5% 2017

Total Chile 455,500 92% 418,685 95.9%

Source: Parque Arauco(1) Arauco Express has 14 Stripcenters in Chile: 11 strip centers in Santiago, 1 in Viña del Mar, 1 in Calama, and 1 in Antofagasta.(2) Arauco Premium Outlet has four outlets located in Santiago, Concepción, Coquimbo and Curauma.

In Chile Parque Arauco has 7 regional shopping centers, 4 outlets and 14 strip centers. The average age of the portfolio is 16 years.

/

11

/

12

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Colombia

Perú

Chile

Peruvian Portfolio

In Peru in the company has 6 regional shopping centers and 9 neighborhood shopping centers, 2 outlets and 2 strip centers. The average age of the portfolio is 6 years.

Peru GLA (m2) % OwnershipOwned GLA

(m2)Occupancy

Year of incorporation

MegaPlaza Norte 111,500 50% 55,750 98.2% 2006

MegaPlaza Express Villa

Chorrillos 8,000 50% 4,000 96.5% 2009

Larcomar 26,500 100% 26,500 92.8% 2010

Parque Lambramani 29,500 100% 29,500 88.2% 2010

MegaPlaza Chimbote 28,000 50% 14,000 94.3% 2012

MegaPlaza Express Villa El Salvador 9,500 50% 4,750 96.4% 2012

MegaPlaza Express Chincha 9,000 50% 4,500 76.8% 2013

InOutlet and Viamix(2) 23,000 100% 23,000 76.1% 2013

MegaPlaza Cañete 16,500 50% 8,250 97.9% 2013

MegaPlaza Express Barranca 10,000 50% 5,000 98.7% 2013

MegaPlaza Pisco 14,500 50% 7,250 97.3% 2015

El Quinde Cajamarca 31,000 100% 31,000 80.8% 2015

El Quinde Ica 36,500 100% 36,500 96.5% 2015

Plaza Jesús María 14,500 100% 14,500 47.7% 2016

MegaPlaza Jaén 14,500 50% 7,250 82.8% 2016

MegaPlaza Huaral 9,000 50% 4,500 65.6% 2017

Total Peru 391,500 71% 276,250 90.2%

Source: Parque Arauco(1) Only partner in peru is Grupo Wiese, which includes MegaPlaza formats (50%).(2) InOutlet and Viamix includes two premium outlets in Lima and two strip centers in Lima.

/

12

/

13

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Colombia

Perú

Chile

Colombian Portfolio

Parque Arauco has 3 regional shopping centers in Colombia and the average age of the portfolio is 3 years

Colombia GLA (m2) % OwnershipOwned GLA

(m2)Occupancy

Year of incorporation

Parque Arboleda 41,000 55% 22,550 95.3% 2010

Parque Caracoli 38,500 100% 38,500 87.8% 2013

Parque La Colina 63,000 100% 63,000 88.1% 2016

Total Colombia 142,500 87% 124,050 90.1%

Source: Parque Arauco

/

13

/

14

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

INTRODUCTION

OUR OPERATIONS

INVESTMENT HIGHLIGHTS

FUTURE DEVELOPMENTS

/

15

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Our operations

PortfolioParque Arauco has 3 regional shopping centers in Colombia and the average age of the portfolio is 3 years

1.Consistent results in a

challenging macroeconomic environment

2.Stable and

diversified revenues

4.Solid corporate governance and increased concern with

sustainability

6.Important growth

opportunities

3.Strong commercial

relationships with local and global businesses

5.Conservative debt

structure and outstanding financial performance

Investment Highlights

/

16

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Consistent results in a challenging macroeconomic environment

Parque Arauco is positioned in countries with strong macroeconomic prospects

Positive but weaker macroeconomic outlook and attractive industry dynamics

2015

2.3%

2016

1.6%

2017f

1.7%

2015

3.3%

2016

3.9%

2017f

3.5%

2015

3.1%

2016

1.9%

2017f

2.3%

2014

7.4%

2015

6.0%

2016

4.9%

2014

8.2%

2015

4.9%

2016

7.6%

2014

5.9%

2015

7. 1%

2016

7.2%

2015

18.0

2016

18.2

2017f

18.4

2015

31. 1

2016

31.5

2017f

31.8

2015

48.2

2016

48.8

2017f

49.3

2015

23,682

2016

24,113

2017f

24,797

2015

12,389

2016

12,903

2017f

13,501

2015

13,833

2016

14, 103

2017f

14,609Av. Latam:

15,078

Av. Latam:41.7

Source: GDP Growth, Population and GDP Per Capita: International Monetary Fund. Retail Sales: Euromonitor.

GDP GROWTH

POPULATION (MILLIONS) GDP PER CAPITA, PPP

RETAIL SALES GROWTH

Chile Peru Colombia

Chile Peru Colombia Chile Peru Colombia

Chile Peru Colombia

/

17

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

+8.3% +8.5% +9.9%+9.5%

Chile

Peru

Tenant sales1 Revenues1 NOI1,2

Colombia

(1) Chile in MMCLP, Peru in ThPEN and Colombia in MMCOP. (2) Not including overhead expenses (Corporate headquarters, regional Services Center, Chile Division, Peru Division and Colombia Division)

GLA1

983,814 1 ,077 , 18895,716 103,848 85,191 93,660

LTM 2Q16

420,500 455,500

LTM 2Q17 LTM 2Q16 LTM 2Q17 LTM 2Q16 LTM 2Q17 LTM 2Q16 LTM 2Q17

Consistent results in a challenging macroeconomic environment

Results have been positive in all three countries

+4.8% +3.9% +7.6% +12.3%

2,701 , 1072,807 ,789

230,717248,242

172,496193,714

373,500391 ,500

LTM 2Q16 LTM 2Q17 LTM 2Q16 LTM 2Q17 LTM 2Q16 LTM 2Q17 LTM 2Q16 LTM 2Q17

+80. 4% +49.9% +69.9% +89.3%

369,553554,027

42,68172,532

30,88658,468

79,000142,500

LTM 2Q16 LTM 2Q17 LTM 2Q16 LTM 2Q17 LTM 2Q16 LTM 2Q17 LTM 2Q16 LTM 2Q17

/

18

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Consistent Same Store Growth and a Healthy Occupancy Cost

2Q17

1 .7

4Q16

7 .2

3.7

2Q16 3Q16

4. 1

1Q17

2.6

2Q17

2.6

3Q16

6.2 7 .0

1Q172Q16

4.3

4Q16

2.7

2Q16

10.2%

2Q17

10.2%

58%Others

CHILE SAME STORE SALES / CHG. % CHILE SAME STORE RENT / CHG. % CHILE OCCUPANCY COST

42%Anchor Stores

1) Peru’s Same Store Sales and Same Store Rent in 4Q16 do not include Larcomar due to contingencies.

2Q17

0.2

4Q16

5.7

-2.4

2Q16 3Q16

9.2

1Q17

8.2

2Q17

-0.9

8.4

4Q16

5.5

2Q16 3Q16

5.3

1Q17

7 .6

70%Others

2Q16

11.8%

2Q17

13.9%

COLOMBIA SAME STORE SALES1 / CHG. % COLOMBIA SAME STORE RENT1 / CHG. % COLOMBIA OCCUPANCY COST

30%Anchor Stores

PERU SAME STORE SALES1 / CHG. % PERU SAME STORE RENT1 / CHG. % PERU OCCUPANCY COST

4. 2

2Q174Q16

2.0-1 . 1

2Q16 3Q16

1 .6

1Q17

0.4

2Q17

3.0

4Q16

5.8

-2.9

2Q16 3Q16

3.8

1Q17

4.641%Others

2Q16

7.6%

2Q17

7.5%

59%Anchor Stores

Consistent results in a challenging macroeconomic environment

/

19

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Stable and diversified revenues

Parque Arauco diversifies its market risks at a country, format, and socio-economic level

5043 7 100

Medium to HighIncome: Includes ABC1

and C2 in Chile, A and B in Peru and 6, 5 and 4

in Colombia

Medium Income:Includes C3 and D in

Chile, C and D in Peru and 3 in Colombia

Medium to LowIncome: Includes

E in Chile and Peru and 2 and 1 in

Colombia

10.3%

29.1%

85.6%

6.7%2.7%

5.0%

COUNTRY LEVEL DIVERSIFICATION (%REVENUES)

SOCIO-ECONOMIC LEVEL DIVERSIFICATION (% REVENUES)

FORMAT LEVEL DIVERSIFICATION (% REVENUES)

Chile Peru Colombia Regional Neighborhood Outlet Strip center

60.6%

/

20

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Stable and diversified revenues

With a 39% market share in Chile, Parque Arauco is the outlet market leader in the countries where we operateOutlets currently in our portfolio

Keys to the Premium Outlet Format >>1 >> Location

Located near main cities

2 >> Brands Premium name-brands

3 >> Discounts More than 30% discount

ARAUCO PREMIUM OUTLET BUENAVENTURA, CHILE ARAUCO PREMIUM OUTLET CONCEPCIÓN, CHILE

INOUTLET PREMIUM OUTLET LURIN, PERÚINOUTLET FAUCETT, PERÚ

ARAUCO PREMIUM OUTLET CURAUMA, CHILE

ARAUCO PREMIUM OUTLET CURAUMA, CHILE

/

21

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Strong commercial relationships with local and global brands

Consolidated commercial relationships with well-known tenants

Anchor Stores

Non AnchorStores

>>

>>

Malls

11

4

10

5

12

Years as a client

35

16

3512

9

Total GLA (m2)

96.554

33.011

74.54848.050

6.058

Country

CHILEPERU

COLOMBIA

CHILEPERU

CHILEPERU

CHILEPERU

CHILEPERU

COLOMBIA

18 117.316CHILEPERU

COLOMBIA

4 188.934CHILEPERU

COLOMBIA

14 142.307CHILEPERU

COLOMBIASource: Parque Arauco

/

22

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Strong commercial relationships with local and global brands

Parque Arauco is supporting the globalization of several brands entering the Andean region

Source: Parque Arauco

NEW TENANTS PARQUE ARAUCO KENNEDY IN THE LAST 5 YEARS:

80% of new GLA leased in Parque Arauco Kennedy over the last 5 years has been leased to international brands.

Many brands have opened their first store in Chile in Parque Arauco Kennedy during the last five years including Tiffany & Co., Dolce & Gabbana, Forever 21, Bath & Body Works, Tory Burch, Victoria’s Secret, Omega, Versace Collection, Vince Camuto, and BCBG.

International Local

NOMBRE GLA

FOREVER 21 1,639

TOP SHOP 464

UNDER ARMOUR 445

LOUIS VUITTON 420

GUCCI 406

BANANA REPUBLIC 363

AMERICAN EAGLE 351

AEROPOSTALE 342

DOLCE & GABBANA 316

BURBERRY 276

EMPORIO ARMANI 247

SALVATORE FERRAGAMO 241

TIFFANY & CO 219

EL VOLCAN 218

BOLD 214

NOMBRE GLA

ETIQUETA NEGRA 209

MICHAEL KORS 208

RALPH LAUREN 207

TORY BURCH 201

ERMENEGILDO ZEGNA 197

ENTEL 190

ARTE ISABEL ANINAT 161

VICTORIA´S SECRET 129

ETAM 123

MILK 117

CANELA HOME & DECOR 105

METRO CUADRADO 114

JUSTICE 104

BATH & BODY WORKS 103

OCTOBER 102

OTHERS 3,020

TOTAL 14,956

>>

INTERNATIONAL LOCAL

/

23

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Solid corporate governance and increased concern with sustainability

Parque Arauco has received important recognitions from local and international organizations

Workplace Recognition

Investor Relations Recognition

Management Recognition

Sustainability Recognition

Best Capital Markets Strategy:

Andes in 2016.

In 2016, Parque Arauco is part of the Dow Jones

Emerging Market Sustainability Index. We are the

first Latin American real estate company to be part

of this prestigious index.

Best Investor Relations

Department for Mid-Size

companies according to Santander

and Revista Capital in 2016.

Parque Arauco was recognized by

Great Place to Work in Chile and

Peru in 2016.

Source: Parque Arauco

/

24

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Solid corporate governance and increased concern with sustainability

In the last years we have continued advancing our sustainability strategy

Source: Parque Arauco

Environmental Management1.We established the baseline for energy, water, greenhouse gases (GHG) and residual consumption in Chile, Peru and Colombia. 2.We developed an environmental management model, which will be implemented in 2017. 3.We continued sustainably building projects in Colombia (Parque La Colina) and Peru (InOutlet Premium Lurin). 4.We began a study to identify and prioritize climate change risks in some of our assets and projects.

Social Management5.We worked on designing a community relationship strategy and policy applicable to all of operations. 6.We approved and implemented a corporate donation policy.7.More than 20 foundations or social organization had access to free space in our assets. 8.Our intellectual disability intern program had more than 40 participants. 9.We supported more than 340 small entrepreneurs, with more than 20 local and emerging entrepreneur fairs.

Corporate Governance10. We evaluated our corporate governance practices with an expert consultant in this matter. 11. We redefined our values, purpose, mision and long term strategy. 12.We strengthened our risk management team, which performed an exhaustive examination of this matter.13.We initiated a diagnostic with international experts in safety and security standards in our assets. 14.We continued being one of the best places to work, according to the ranking Great Place to Work.

Other Highlights15.We adhere to the United Nations Global Compact.16. We are the first Latin American Real Estate Company to enter into the Dow Jones Sustainability Emerging Markets Index.

2016 Highlights

/

25

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Conservative debt structure and outstanding financial performance

Parque Arauco's policy is to finance projects with 50% debt and 50% equity, and is comfortably within all its covenantsLIABILITIES / EQUITY

EBITDA/FINANCIAL EXPENSES NET FINANCIAL DEBT/EBITDA

|NET FINANCIAL DEBT / EQUITY

2012 2013 2014 20162015 2Q17

3.42x3.89x

3.37x 3.33x3.04x 3.12x

2012

2012

2013

2013

2014

2014

2016

2016

2015

2015

2Q17

2Q17

0.43x

3.85x

0.59x

5.00x

0.47x

4.25x

0.76x

5.87x

0.72xx

5.88x

0.79x

6.06x

> 2.50x

< 1.40x < 1.50x

2012 2013 2014 20162015 2Q17

0.78x0.89x 0.81x

1.14x 1.18x 1.16x

/

26

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

JUNE 2017

Conservative debt structure and outstanding financial performance

The Company has a conservative debt structure

JUNE 2014

175

938

6498

3311

77

188

25-36months

13-24months

0-3months

49-60months

7-12months

11-20years

37-48months

4-6months

6-10years

21-35years

0

150

4

80

156300134

735

158

25-36months

13-24months

0-3months

49-60months

7-12months

11-20years

37-48months

4-6months

6-10years

21-35years

181

333

IMPROVEMENT IN LOCAL DEBT RATINGFitch: AA- Feller: AA- ICR:AA-

BBB- BBB BBB+ A- AA-A AAA+ AA+

Source: Parque Arauco(1) Does not include accrued interests and the exchange rate is at the close of June 30, 2017.

55% UF

66% UF

12% CLP 7% CLP

13% PEN 16% PEN

1 1% USD 10% COP

9% COP

7% Variable79%

Fixed 93% Fixed

21% Variable

DEC. 2016

SUMMARY OF DEBT BY CURRENCY

LIABILITY AMORTIZATION PROFILE AND DURATION1

SUMMARY OF DEBT RATES

JUNE 2017JUNE 2014

June 2014 (US$MM)Average Duration: 4.1 Years

June 2017 (US$MM)Average Duration: 7.0 Years

/

27

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Conservative debt structure and outstanding financial performance

The cost of debt has decreased importantly in the past 5 years

The cost of debt of Parque Arauco has decreased 160 points from 4.1% to 2.5%The spread five years ago had collateral agreements, while the current spread is

unsecured with no collateral.

Date: 12-12-2014Base: 1.66%Spread: 1.74%Duration: 14.3

Date: 04-17-2015Base: 1.62%Spread: 1.68%Duration: 14.77

Date: 10-12-2016Base: 1.46%Spread: 1.02%Duration: 12.71

Generic long-term bond issued by Parque Arauco in Chile

Source: Risk America

/

28

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Important growth opportunities

Parque Arauco has 0.9 million m2 and a 2% market participation in Latin American and a 8% market participation in the Andean Region.

Source: Prepared using information published by the International Council of Shopping Centers (ICSC)., Peruvian Shopping Center Council (ACCEP) and Parque Arauco analysis

BrazilGLA: 14.7 million de m2

32% of total

Latin AmericaGLA: 46.1 million m2 Andean Region

GLA: 11.9 million m2

25% of total

MexicoGLA: 17.4 million m2

38% of total

ArgentinaGLA: 2.1 million m2

5% of total

Indicator CHILE PERU COLOMBIA

Total GLA (th) 3,600 2,700 5,600

GLA Parque Arauco (th) 454 382 142

Market Share 13% 14% 3%

Rank #3 #3 #5

/

29

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Parque Arauco participates in markets with a growing retail market

2,500

2,000

1,500

1,000

500

-

OPENING PEAKING MATURING CLOSING

Chile

Mexico

Brazil

PeruColombia

(1) Source: International Council of Shopping Centers, World Bank, Parque Arauco analysis(2) Source: AT Kearney Global Retail Development Index 2016(3) Source: CBRE- How Global is the business of retail?. This report did not include Colombia.

Important growth opportunities

RETAIL SALES PER CAPITA AND GLA PER 1,000 INHABITANTS1

AT KEARNEY GRDI WINDOW OF OPPORTUNITY2

GLA

per

1,0

00

hab

itant

s

Middle class is growing; consumers are willing to explores organized

formats; government is relaxing restrictions

Consumers seek organized formats and

greater exposure to global brands; retail

shopping districts are being developed; real

estate is affordable and available

Consumer spending has expanded significantly; desirable real estate is

more difficult to secure; local competition has

become more sofisticated

Consumes are more used to modern retail; discretionary spending is higher; competition

is fierce both from local and foreign retailers;

real estate is expensive and not readily available

RETAIL PRESENCE BY COUNTRY3 (% OF GLOBAL BRANDS IN COUNTRY)

39.5%

Mexico

21.0%

Chile Brazil

20.7%

Argentina

11.7%

Venezuela

10.2%

Peru

9.9%

United States

16,000

12,000

8,000

4000

Canada Australia UK Chile Mexico Colombia Peru Brazil Argentina

Reta

il Sa

les

Per

Capi

ta

51.5%

United States

57.5%

UK

Retail sales per capitaGLA per 1,000 habitants

/

30

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Parque Arauco's growth has come from greenfield projects and M&A

Important growth opportunities

Total GLA

in 2006

194,74555,651

83,708 24,59591,625 27,676

80,242

132,85837,400

90,000

989,500

Total GLA

in 2007

Total GLA

in 2010

Total GLA

in 2014

Total GLA

in 2008

Total GLA

in 2011

Total GLA

in 2015

Total GLA

in 2009

Total GLA

in 2013

Total GLA

in 2012

New GLA

in 2016

Greenfields663,143 m2

M&A326,357 m2

Greenfield M&A

67%

33%

Total GLA

2Q2017

126,500

New GLA

in 2017

44,500

Source: Parque Arauco

/

31

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

INTRODUCTION

OUR OPERATIONS

INVESTMENT HIGHLIGHTS

FUTURE DEVELOPMENTS

/

32

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

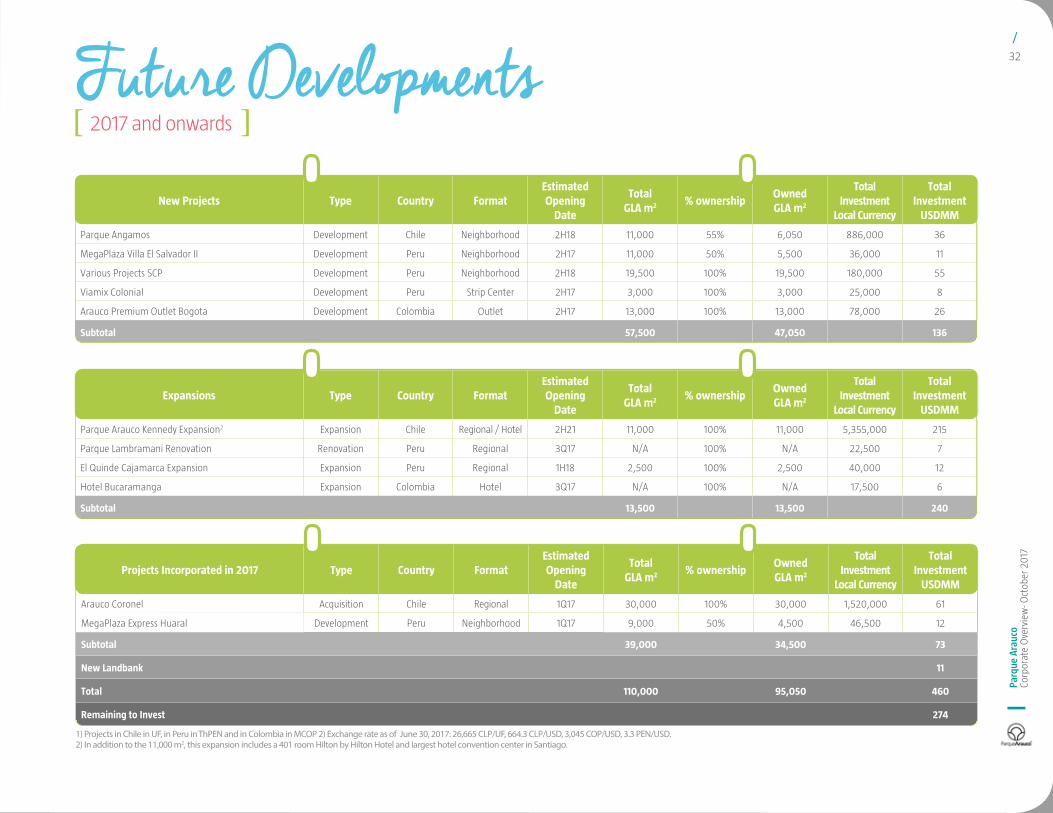

Future Developments2017 and onwards

New Projects Type Country FormatEstimated Opening

Date

Total GLA m2 % ownership

Owned GLA m2

Total Investment

Local Currency

Total Investment

USDMM

Parque Angamos Development Chile Neighborhood 2H18 11,000 55% 6,050 886,000 36

MegaPlaza Villa El Salvador II Development Peru Neighborhood 2H17 11,000 50% 5,500 36,000 11

Various Projects SCP Development Peru Neighborhood 2H18 19,500 100% 19,500 180,000 55

Viamix Colonial Development Peru Strip Center 2H17 3,000 100% 3,000 25,000 8

Arauco Premium Outlet Bogota Development Colombia Outlet 2H17 13,000 100% 13,000 78,000 26

Subtotal 57,500 47,050 136

Expansions Type Country FormatEstimated Opening

Date

Total GLA m2 % ownership

Owned GLA m2

Total Investment

Local Currency

Total Investment

USDMM

Parque Arauco Kennedy Expansion2 Expansion Chile Regional / Hotel 2H21 11,000 100% 11,000 5,355,000 215

Parque Lambramani Renovation Renovation Peru Regional 3Q17 N/A 100% N/A 22,500 7

El Quinde Cajamarca Expansion Expansion Peru Regional 1H18 2,500 100% 2,500 40,000 12

Hotel Bucaramanga Expansion Colombia Hotel 3Q17 N/A 100% N/A 17,500 6

Subtotal 13,500 13,500 240

Projects Incorporated in 2017 Type Country FormatEstimated Opening

Date

Total GLA m2 % ownership

Owned GLA m2

Total Investment

Local Currency

Total Investment

USDMM

Arauco Coronel Acquisition Chile Regional 1Q17 30,000 100% 30,000 1,520,000 61

MegaPlaza Express Huaral Development Peru Neighborhood 1Q17 9,000 50% 4,500 46,500 12

Subtotal 39,000 34,500 73

New Landbank 11

Total 110,000 95,050 460

Remaining to Invest 274

1) Projects in Chile in UF, in Peru in ThPEN and in Colombia in MCOP 2) Exchange rate as of June 30, 2017: 26,665 CLP/UF, 664.3 CLP/USD, 3,045 COP/USD, 3.3 PEN/USD.2) In addition to the 11,000 m2, this expansion includes a 401 room Hilton by Hilton Hotel and largest hotel convention center in Santiago.

/

33

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

OPENING DATE: The shopping center opened on December 6, 2016.

COMMERCIALIZATION STATE: 88.1% of the GLA is open. H&M opened on May 6, 2017.

BRANDS:

Parque La Colina was inaugurated in December 2016

/

34

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

We announced a new expansion of Parque Arauco Kennedy

PROJECT DETAILS:

Investment: 5,355,000 UF5-star hotel: Hilton by HiltonRooms: 401Convention center: 3,000 m2

Parking spots: 700Additional GLA: 11,000 m2

- The project will have the first five star Hilton Hotel in Chile, a convention center, as well as theincorporation of new stores and more parking.

- The five star Hilton hotel will have 401 rooms, two restaurants, three bars, two pools, a gym and an executive lounge. It will have the largest hotel convention center in the country, with the possibility of hosting over 2,800 people.

- The expansion will include a new flagship Falabella store with almost 25,000 m2 of GLA. This store will occupy the first four floors of the

HOTEL OPERATOR:

/

35

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

LandbankName m2 % Ownership Total Cost (local currency) Total Cost (USD MM)

Quilicura 25,486 100% 78,000 3

Buenaventura 115,864 100% 455,000 18

Chicureo 47,614 100% 206,000 8

Los Andes 39,254 100% 117,000 5

Others in Chile 67,550 92% 522,000 21

Total Chile 295,768 98% 1,378,000 55

Parque El Golf - San Isidro 16,350 68% 127,590 40

Chimbote 42,657 100% 18,000 6

Talara 30,675 100% 9,400 3

Ica 12,643 100% 13,500 4

Chiclayo 6,609 100% 6,300 2

Pomalca Chiclayo 45,042 100% 6,565 2

Lambayeque- MegaPlaza 25,260 50% 18,900 6

San Juan de Lurigancho- MegaPlaza 80,000 50% 10,415 3

Others MegaPlaza 106,157 50% 85,685 26

Total Peru 365,393 70% 296,355 92

Neiva 49,537 100% 18,000 6

Valledupar 46,000 100% 30,000 10

Barranquilla 56,166 100% 76,000 26

Total Colombia 151,703 100% 124,000 42

Total 812,864 86% 189

1) Landbank in Chile in UF, in Peru in ThPEN and in Colombia in MCOP 2) Exchange rate as of June 30, 2017: 26,665 CLP/UF, 664.3 CLP/USD, 3,045 COP/USD, 3.3 PEN/USD.

/

36

Parq

ue A

rauc

oCo

rpor

ate

Ove

rvie

w- O

ctob

er 2

017

Glossary»Adjusted FFO Margin - AFFO / revenues

»AFFO -Adjusted Funds From Operations: Net Profit - Depreciation & Amortization - Other Income/expenses - Share of Profit (Loss) of Associates Accounted - Foreign Exchange Differences - Income (Loss) for indexed assets and liabilities - Gains (losses) from the difference between the previous book value and the fair value of financial assets - Deferred tax+ Associates accounted Adjusted FFO

»Controlling Adjusted FFO -AFFO attributable to the shareholders of the company

»Controlling FFO -FFO attributable to the shareholders of the company

»EBITDA - Earnings Before Income Tax Depreciation and Amortization: Revenues + Cost of Sales + Administration Expenses - Depreciation and Amortization EBITDA margin -EBITDA divided by revenues

»EPS -Earnings Per Share: Net income attributable to the equity holders of the company/weighted average number of shares outstanding

»FFO -Funds From Operations: Net Profit - Depreciation & Amortization - Share of Profit (Loss) of Associates Accounted + Associates Accounted FFO

»GLA -Gross Leasable Area. Equivalent to the sum of all

the areas available for lease

»Greenfield Projects - Organic development of new shopping centers

»Landbank -Land held by the company for future development

»LTM -Refers to information from the last twelve months

»Monthly Revenues/m2 -Monthly revenues divided by the occupied GLA for the period

»Monthly Sales/m2 -Monthly tenant sales divided by the occupied GLA for the period

»Neighborhood Mall -A shopping mall with a GLA between 6,000 and 20,000 m2

» Net income margin -Net profit / revenues

»NOI -Net Operating Income: Revenues + Cost of Sales + Administration Expenses - Depreciation & Amortization + Associates accounted NOI

»Occupancy -GLA paying rent divided by total GLA

»Occupancy cost -Minimum rent, plus variable rent, plus common expenses, plus a promotion fund that the

tenants pay Parque Arauco divided by the sales of the tenant.

»Owned GLA -Total GLA weighted by Parque Arauco’s interest in the mall

»Pipeline -Greenfield and expansion projects under development

»Premium Outlet - Shopping center located outside of the city offering name brand clothing and goods for a reduced price

»Regional Mall - A shopping mall with a GLA over 20,000 m2.

»SSR -Same Store Rent: Percentage change in rent collected from tenants that paid rent in both of the periods compared

»SSS -Same Store Sales: Percentage change in sales from tenants that reported sales in both of the periods compared

»Strip Center -A shopping center with a GLA less than 6,000 m2 Tenant Sales Tenant sales of the consolidated assets

»UF -Unidad de Fomento: A chilean currency unit indexed according to inflation on a daily basis.

Parque Arauco ColombiaOctober 2017

[2]

I. Introduction to Colombia

II. Parque Arauco Colombia

Agenda

Versión 16-10-2017 20:30

[3]

I. Introduction to Colombia

II. Parque Arauco Colombia

Agenda

4

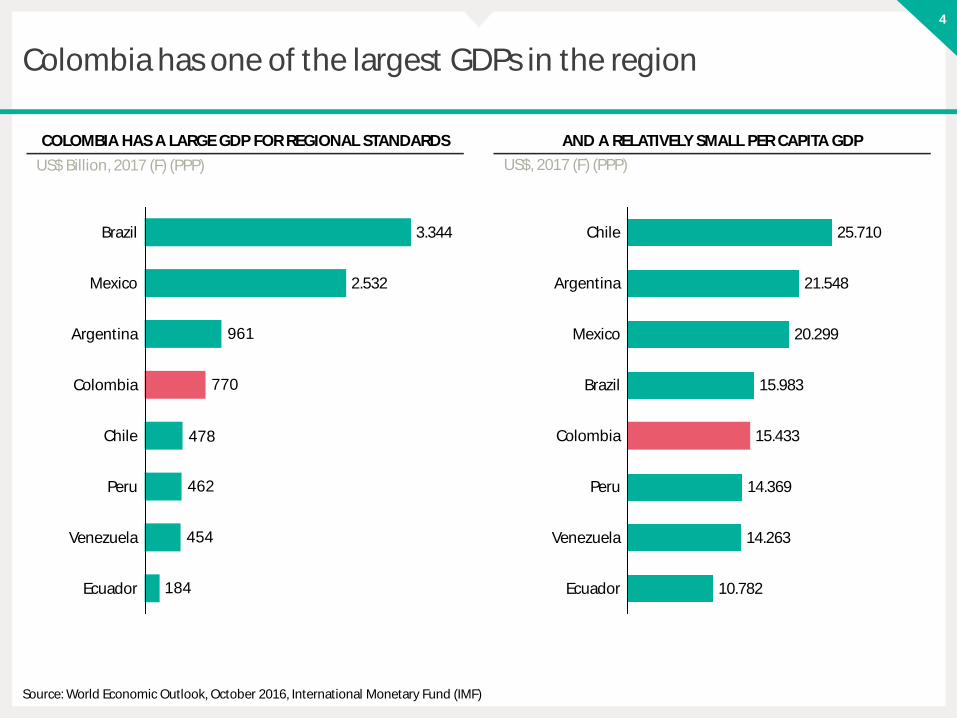

Colombia has one of the largest GDPs in the region

US$, 2017 (F) (PPP)US$ Billion, 2017 (F) (PPP)

184

454

462

478

770

961

Venezuela

Colombia

Ecuador

Peru

Chile

Brazil 3.344

Argentina

2.532Mexico

Venezuela

10.782

14.263

Ecuador

Colombia 15.433

14.369

15.983Brazil

20.299

Argentina

Peru

Mexico

Chile

21.548

25.710

COLOMBIA HAS A LARGE GDP FOR REGIONAL STANDARDS AND A RELATIVELY SMALL PER CAPITA GDP

Source: World Economic Outlook, October 2016, International Monetary Fund (IMF)

5

Colombia will continue to have a leading growth in the region

Colombia

Mexico

Ecuador

Argentina

0,3

3,2

3,7

2,6

Chile 2,5

Brazil

2,4

1,6

Peru

20192017

2,3

3,6

3,0

2018

3,63,6

20212020

Source:, World Economic Outlook, April, 2017, International Monetary Fund (IMF)

Real GDP% Change ForecaseRead GDP% Change, Average 2017-2012

COLOMBIA HAS STRONG GROWTH GOING FORWARD COLOMBIA GDP GROWTH EXPECTATION

6

Colombia has a diversified economy

17,1%

23,1%

Transport and communicationsAgricultureElectricity, gas and water

Commerce

7,9%

Financial intermediation

Social and personal services

Manufacturing

6,7%

13,5%

Construction

Mining

8,2%

7,1%

12,4%

3,8%

Source: Colombian Central Bank

2016 GDP BREAKDOWN BY ECONOMIC ACTIVITY

7

diversified exports and imports

TOP 2016 EXPORTS (% OF TOTAL) TOP 2016 IMPORTS BY USE (% OF TOTAL)

Source: Central Bank of Colombia

Ferronickel

Petroleum and derivtives1,0%

7,7%

Coffee

14,8%

Carbon

33,2%

Mining

Industrial

5,8%

8,9%

Farming

28,5%

11,2%

Farming

Industrial

Non-durable goods

8,5%

13,3%7,8%

Transportation

3,9%

Durable Goods

Combustibles

32,9%

Industrial (Raw material)

3,1%Construction

18,9%

8

There are 5 cities in Colombia with over 1,000,000 people

Bucaramanga

City Population

1. Bogotá 8,000,000+

2. Medellín 2,500,000 +

3. Calí 2,400,000+

4. Barranquilla 1,200,000+

5. Cartagena 1,000,000+

6. Cúcuta 650,000+

7. Soledad 600,000+

8. Ibagué 550,000+

9. Soacha 525,000+

10. Bucaramanga 500,000+

11. Villavicencio 500,000+

12. Santa Marta 490,000+

13. Pereira 470,000+

BogotáPereira

Cartagena

Calí

Barranquilla

Cúcuta

Soledad

Ibagué

Soacha

Source: DANE

Medellín

9

Macroeconomic indicators are sending mixed signals

-40

-30

-20

-10

0

10

20

30

40

20152013 20172014 20162012 2018

CHALLENGING CONSUMER CONFIDENCE

Consumer confidence levels (DANE)

STABLE UNEMPLOYMENT RATES

Unemployment rates(DANE)

10,5

11,0

10,0

20182017

9,0

20162015201420132012

0,0

9,5

DECREASING INFLATION

Inflation % (DANE)

4

6

0

7

5

3

2017201420132012 20162015

DECREASING LONG TERM RATES

Colombia generic 10 year bond (Bloomberg)

7

0

6

8

9

20152013 20142012 20172016

10

Some consumption indicators are improving

DECREASING POVERTY RATES

Poverty headcount (% of population)

2015

28%

20142009

34%

2008

33% 31%

20132010 2012

37%42%

29%

40%

2011

IMPROVED BANKING PENETRATION

%Population with at least one financial product

64,9%62,2%71,5%67,2%

75,0%72,5%

20152010 2012 2013 20142011

A STEADY POPULATION GROWTH

1,0%

1,2%

0,9%1,1%

2010

1,1%

20142012 2013

1,0%

2011

1,1%0,9%

20092008 2015

Population growth %

GROWING URBAN POPULATION

2015

1,4%

2011

1,4%1,5%

201320102008

1,3%1,6% 1,5%

2009 2014

1,3%

2012

1,3%

Urban population growth %

Source: World Bank for poverty rates, population growth rates and Asobancaria for banking penetration.

11

CHILE

PERÚ

COLOMBIA

improving institutional frameworks

EASE OF DOING BUSINESS RANK (2016)

Mexico 47

Colombia 53

Peru 54

Chile 57

Argentina 116

Brazil 123

WEF GLOBAL COMPETITIVENESS DETAIL FOR COLOMBIA

01234567

Institutions

Infrastructure

Macroeconom

Health and

Higher

Goods marketefficiency

Labor marketefficiency

Financial

Technologicalreadiness

Market size

Businesssophistication

Innovation

WEF GLOBAL COMPETITIVENESS RANK (2016)

Chile 33

Mexico 51

Colombia 61

Peru 67

Brazil 81

Argentina 104

Score 1 (low) to 7 (high)

Source: Ease of Business, World Economic Forum

12

Shopping center sales have outpaced sector dynamics in Colombia

10.000

0

5.000

15.000

20142013

+11,6%

201620152011 2012

SHOPPING CENTER SALES (RADDAR/ ACE COLOMBIA) (THUSD)

50.000

40.000

30.000

20.000

10.000

0

70.000

60.000

20162013

+6,1%

20122011 20152014

RETAIL SALES (EUROMONITOR) (THUSD)

200.000

100.000

150.000

50.000

0

+3,9%

201520132011 201620142012

FINAL CONSUMPTION (COLOMBIAN CENTRAL BANK) (THUSD)

RETAIL AND MALL SALES AS % OF TOTAL FINAL CONSUMPTION

60,6% 60,3%

7,3%6,1%

33,3% 32,3%

2012

32,8%

2011

6,9%

59,8%

33,0% 33,6%

8,0%

60,4% 58,4%

2013

7,3%

2014 2016

35,0%

8,7%

56,3%

2015

Retail (ex mall)Mall OthersSource: Colombian Central Bank, Euromonitor, Raddar, ACE Colombia

13

Distribution of Colombian spend

HOW 100 COLOMBIAN PESOS ARE SPENT IN A SHOPPING CENTER

4,5% 5,2%

27,7%28,6%

7,5%8,6%

EducationHousing

7,3%

Eating outside

of the home

Entertainment& culture

Transport. & Comm.

Health

6,5%

38,4%

Clothing and shoes

OthersAnchor stores

39,0%

7,2%6,6%

0,1%

2,6% 3,0%3,7%

0,0%

3,6%

2017

2016

Source: Raddar

14

Colombian elections

• Presidential elections take place in May 2018• Latest Datexco voting intention survey results:

4,1%

20,1%

Germán Vargas Lleras

5,9%

16,5%

7,6%

12,1%

Gustavo Petro

Sergio Fajardo

11,2%

Juan Manuel Galan

Clara Lopez know

No Response

WHO WOULD YOU VOTE FOR IF THE ELECTIONS WERETOMORROW?

Simón Gaviria

4,3%

18,6%

13,1%

2,4%

Germán Vargas Lleras

3,3% 2,6%

Gustavo Petro

Francisco Santos

13,7%

Alejandro Ordoñez

Roy Barreras

Piedad Córdoba

WHICH CANDIDATE WOULD YOU NEVER VOTE FOR?

52,9%

Unemploy.

41,0%

Political corruption

Common crimes

Health National safety

Educational coverage

15,4% 12,8%

Education quality

11,5% 9,8%

EconomySafety Health coverage

39,4%

11,6% 10,1%20,0%

WHAT ARE THE THREE PROBLEMS THE NEXT PRESIDENTSHOULD SOLVE?

Source: Datexco

15

Peace agreement

• The agreement is to end the civil war with the FARC and create a stable and during peace for Colombia. The agreements are summarized as:

1. A new Colombian countryside: Comprehensive rural reform2. Political participation: A democratic opportunity to build peace3. End of the conflict: Agreement on the bilateral and definitive

ceasefire and cessation of hostilities and laying down of arms4. Solution to the problems of illicit drugs5. Agreement regarding the victims of the conflict:

Comprehensive system from truth, justice, reparation and non-repetition

6. Implementation and verification mechanisms

Source: Colombia Peace Organization

[16]

I. Introduction to Colombia

II. Parque Arauco Colombia

Agenda

17

CHILE

PERÚ

COLOMBIA

Purchase of Barranquilla

land

Purchase of

minority stake

Parque Caracolí opens in

Bucaramanga

History of Parque Arauco in Colombia

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Parque Arauco opens

office in Colombia

Parque Arboleda opens in Pereira

Parque La Colina opens in Bogotá

Agreementsigned with

Bancolombia

Purchase of Valledupar land

Purchase of La Colina

land

Purchase of Bucaramanga

land

Agreementsigned withMerheg´sfamily to developParque

Arboleda

Source: Parque Arauco

18

Legal Structure

INVERSIONES INMOBILIARIASARAUCO ALAMEDA S.A.S.

INVERSIONES COLOMBIANASARAUCO S.A.S.

INMOBILIARIA LA COLINA ARAUCO S.A.S

INVERSIONES INMOBILIARIAS BUCARAMANGA ARAUCO S.A.S

EJE CONSTRUCCIONES S.A.S

100% 100%

6,0001632%

48,9998878%100%100%

PARQUE ARAUCO INTERNACIONAL S.A. PARQUE ARAUCO S.A.

99,9956392%

Source: Parque Arauco

19

Organizational chart

Gerencia Legal

Gerencia de Administración y

Finanzas

Gerencia Inmobiliaria

Country ManagerJuan Pablo Romero

Subgerencia de Personas

Gerencia de Centros Comerciales

Gerencia Comercial

Source: Parque Arauco

20

CHILE

PERÚ

COLOMBIA

Parque Arauco has three shopping centers in Colombia

BogotáPereira

Bucaramanga

Colombia GLA (m2) % OwnershipOwned GLA

(m2) OccupancyYear of incorporation

Parque Arboleda 41,000 55% 22,550 95.3% 2010

Parque Caracoli 38,500 100% 38,500 87.8% 2013

Parque La Colina 63,000 100% 63,000 88.1% 2016

Total Colombia 142,500 87% 124,050 90.1%

Source: Parque Arauco

21

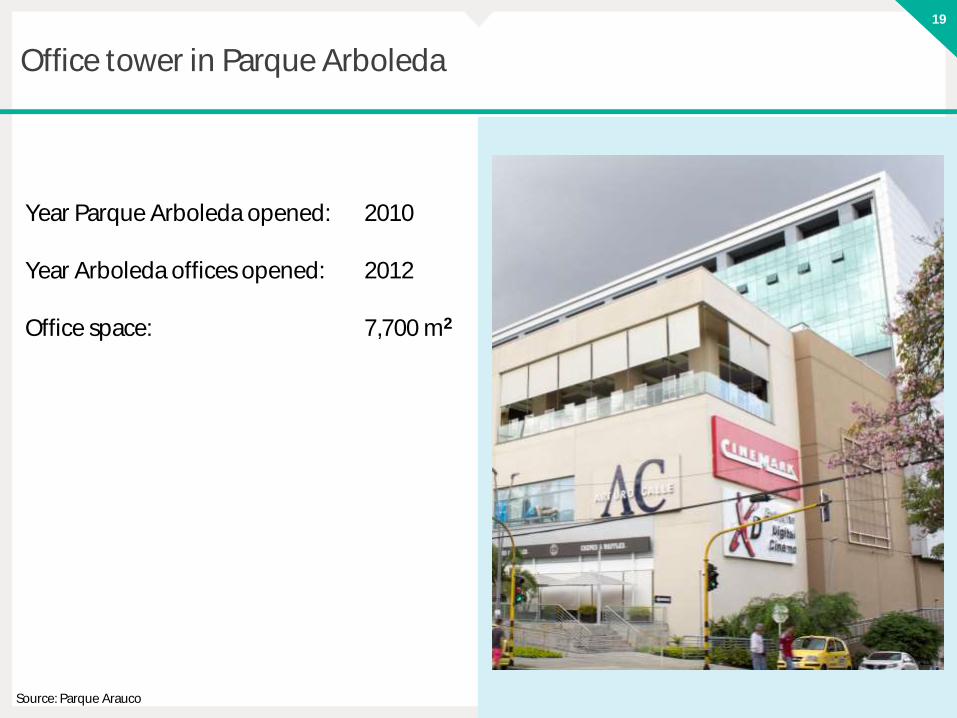

Parque Arboleda - Pereira

TENANTS SALES (MMCOP)REVENUES WITHOUTOVERHEAD (MMCOP)

NOI WITHOUT OVERHEAD(MMCOP)

GLA (M2) AND OCCUPANCY (%)

LTM 2Q16

33.000

LTM 2Q17

40.500 41.000

2016

40.500

2015 LTM 2Q17

218.743

2016

198.348 215.055

+10,3%

2015

+3,8%

LTM 2Q16

210.655 25.07924.373

20162015

21.636

LTM 2Q17

+15,9% +9,2%

22.959

LTM 2Q16

+23,0%

LTM 2Q17

16.27920.01919.436

2015 2016

+14,4%

LTM 2Q16

17.501

92,9%94,6% 95,3%95,6%

KEY METRICS

PARQUE ARBOLEDA

Opening: 2010

Location: Cra. 14 #5-20, Pereira

Anchor: Falabella

Type of mall: Regional

Total GLA: 41,000 m²

Owner: Parque Arauco (55%) and

Merheg´s family (45%)

Pereira

Source: Parque Arauco

22

Parque Caracolí - Bucaramanga

TENANTS SALES (MMCOP)REVENUES WITHOUTOVERHEAD (MMCOP)

NOI WITHOUT OVERHEAD(MMCOP)

GLA (M2) AND OCCUPANCY (%)

38.500

LTM 2Q16

38.500

LTM 2Q17

20162015

38.500 38.500

158.898 158.129

LTM 2Q17

-0,5%

LTM 2Q16

+4,5%

2016

161.384

2015

151.378

LTM 2Q16

19.723

-0,3%

20.073

LTM 2Q17

2015

18.978 19.656

+3,6%

2016

12.801 13.385

LTM 2Q16

+1,5%+6,2%

LTM 2Q17

13.591

2016

13.909

2015

KEY METRICS

100,0%

87,8%88,4%87,3%

PARQUE CARACOLÍ

Opening: 2013

Location: Carrera 27 #29 145

Bucaramanga

Anchor: Falabella

Type of mall: Regional

Total GLA: 38,500 m²

Owner: Parque Arauco (100%)

Bucaramanga

Source: Parque Arauco

23

Parque La Colina - Bogotá

SALES / M2 (MMCOP)REVENUES / M2 WITHOUT

OVERHEAD (MMCOP) NOI MARGINGLA (M2) AND

OCCUPANCY (%)

63.00063.000

2017 E

63.000

2Q171Q17 1Q17

663.194

2Q17

505.343

2Q17

94.093

1Q17

89.97590,8%

1Q17 2Q17

87,9%

KEY METRICS

90,0%88,1%77,7%

PARQUE LA COLINA

Opening: 2016

Location: Cra. 58d #146-51,

Bogotá

Anchor: Falabella

Type of mall: Regional

Total GLA: 63,000 m²

Owner: Parque Arauco (100%)

Bogotá

Source: Parque Arauco

24

Revenue type and contract duration

16%

84%

Other Revenues

Rental Revenues

Fixed Revenues

Variable Revenues

97%

3%

47

9

21

23

< 2 years >4 years3-4 years2-3 years

FIXED VS VARIABLE RENTAL REVENUES COLOMBIA

As of June 30, 2017

CONTRACT LENGTH IN COLOMBIA

Based on % of revenues

Source: Parque Arauco

25

CHILE

PERÚ

COLOMBIA

Parque GLA in Colombia has tripled since 2010

142.500

20172015

71.500

2014 20162013

143.000

71.500

+331,8%

33.000 33.000

20122011

33.000

71.500

2010

Parque Arboleda

Parque Caracolí

Parque La Colina

Total GLA

Source: Parque Arauco

26

CHILE

PERÚ

COLOMBIA

The owned GLA has increased over 12x

Parque Caracolí

Parque Arboleda

Parque La Colina

Own GLA

0,2

0,1

140.000

120.000

100.000

0,9

0,0

60.000

0

80.000

0,4

0,8

0,7

0,6

0,5

0,340.000

20.000 9.999

2012

31.174

2013

31.174

2010

9.999

20162015

9.999

123.775

2011 2017

56.650

124.050

2014

Ownership %

We increased our ownership when we purchased minority participationin 2015

27

The GLA of Parque Arauco Colombia has increased fourfoldin the last five years

GLA (M²) TENANT SALES (MUSD)2

REVENUES (MUSD)1,2 NOI¹ (MMCOP)

(1) Not including overhead expenses (Corporate headquarters, regional Services Center and Colombia Division)(2) 1 USD= 2,921.72 COPSource: Parque Arauco

79.000

+80,4%

20162015 LTM 2Q2017

141.500

+331,8%

142.500

71.500

33.000

2013

33.000

71.500

20122011

71.500

2014 LTM 2Q16

190

113129120

10578

4943

LTM 2Q16

2012 2015

346%

LTM 2Q17

2016201420132011

+68,1%

25

1515141210

54

+69,9%

2016 LTM 2Q17

20122011 2013 2014

544%

2015 LTM 2Q16

20

1111109

84

3

+89,3%

LTM 2Q17

568%

20162015201420132011 2012 LTM 2Q16

28

The company has stable management indicators in Colombia

2Q16

90%

1Q15 3Q152Q15 1Q16

90% 93%93%

4Q15

89% 90% 90%

3Q16

92% 92%

2Q171Q17

85%

4Q16

OCCUPANCY (%)

0,2%

1Q16 4Q16

-1,1%

2Q16

1,6%

11,5%

4Q15

8,6%

5,3%

1Q173Q151Q15

4,5%

0,9%

2Q15

2,0%

3Q16

-0,5%

2Q17

SAME STORE SALES (CHG. %)

-0,9%

2Q17

5,3%

8,4%

4Q16 1Q17

7,6%

3Q16

11,2%

4Q15

5,5%

2Q161Q16

12,5%

1Q15

1,1%

3Q15

5,5%

2Q15

1,5%

SAME STORE RENT (CHG. %)

3Q16

12%

9%

1Q16 2Q16

15%

12%

1Q174Q162Q151Q15 3Q15

10%

12%14% 13%

12%

4Q15 2Q17

14%

OCCUPANCY COST (%)

Source: Parque Arauco

29

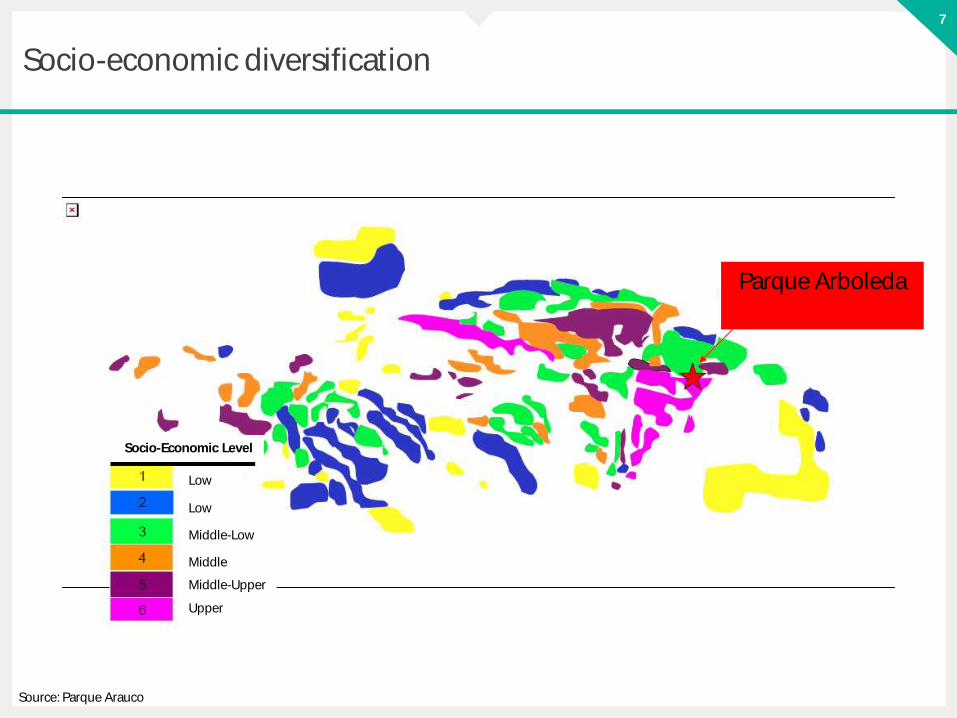

Diversified assets and revenues

57

100

29

14

TotalMedium Income: 4 and 3 in Colombia

Medium to Low Income: 2 and 1 in Colombia

Medium to High Income: 6 and 5 in Colombia

Source: Parque Arauco. Based on socio-economic composition of community in which malls are located.

ASSET LEVEL DIVERSIFICATION (º/º REVENUES 2017E) REVENUE TYPE DIVERSIFICATION (º/º REVENUES)

SOCIO-ECONOMIC LEVEL DIVERSIFICATION (º/º REVENUES)

Variable Revenues

Fixed Revenues

Other Revenues

12%

Parking Revenues

3%2%

84%

Parque Arboleda

Parque Caracoli19%

Parque La Colina

22%

58%

30

Future growth will come from pipeline and landbank

Project Type Format Estimatedopening

date

Total GLA m2

% ownership

OwnedGLA m2

Total investment

local currency

Total investment

USDMM

Arauco Premium Outlet Bogotá

Develop. Outlet 2H17 13,000 100% 13,000 78,000 26

Hotel Bucaramanga

Expansion Hotel 3Q17 N/A 100% N/A 17,500 6

Total 13,000 100% 13,000 95,500 32

NEW PROJECTS

LANDBANK

Name M2 % ownership Total cost (local currency)

Total Cost (USDMM)

Neiva 49,537 100% 18,000 6

Valledupar 46,000 100% 30,000 10

Barranquilla 56,166 100% 76,000 26

Total Colombia 151,703 100% 124,000 42

Source: Parque Arauco

31

CHILE

PERÚ

COLOMBIA

Project Arauco Premium Outlet Bogotá - Bogotá

Opening: 2H2017

Location: Sopó, Bogotá

Type of mall: Outlet

Total GLA: 13,000 m²

Total Investment: US$ 26 millones

Owner: Parque Arauco (100%)

Commercial %: 25% of contracts signed, 50% in negotiation

Bogotá

ARAUCO PREMIUM OUTLET BOGOTÁ

Source: Parque Arauco

32

Brands signed in Arauco Premium Outlet Bogotá

33

CHILE

PERÚ

COLOMBIA

Bucaramanga Hotel Project

Opening: 3Q2017

Location: Bucaramanga

Type of project: Hotel

N° of rooms: 104

Hotel Brand: Sonesta

Total Investment: US$ 6 millones

Owner: Parque Arauco (100%)

PARQUE CARACOLÍBucaramanga

Source: Parque Arauco

34

Bucaramanga Hotel

Source: Parque Arauco

35

Landbank

Barranquilla

Neiva

Name: NeivaM2: 49,537% Ownership: 100%Total Cost: 6(MMUS$)

Valledupar

Name: ValleduparM2: 46,000% Ownership: 100%Total Cost: 10(MMUS$)

Name: BarranquillaM2: 56,166% Ownership: 100%Total Cost: 26(MMUS$)

Source: Parque Arauco

[36]

Colombia’s Shopping Center IndustryOctober 2017

[2]

I. Competitive landscape

II. Sector dynamics

III. Rental vs. condominium

IV. eCommerce in Colombia

V. Globalization of Brands

Agenda

[3]

I. Competitive landscape

II. Sector dynamics

III. Rental vs. condominium

IV. eCommerce in Colombia

V. Globalization of Brands

Agenda

4

Parque Arauco has almost one million m², a 2% market participation in Latin America and a 8% market participation in the Andean Region

#5

456 392 143

5

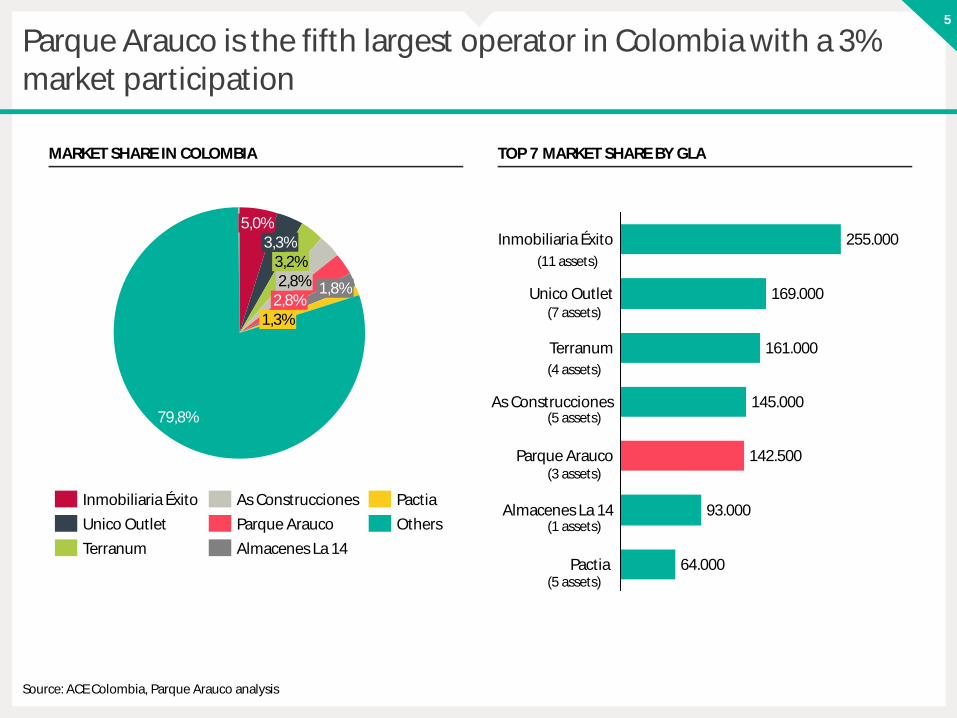

Parque Arauco is the fifth largest operator in Colombia with a 3% market participation

3,2%

2,8%2,8%

3,3%5,0%

79,8%

1,8%

1,3%

Parque Arauco

As ConstruccionesInmobiliaria Éxito

Terranum

Unico Outlet

Almacenes La 14

Others

Pactia

MARKET SHARE IN COLOMBIA

Terranum

Unico Outlet 169.000

145.000

161.000

Parque Arauco

255.000

142.500

As Construcciones

Inmobiliaria Éxito

Almacenes La 14

Pactia 64.000

93.000

TOP 7 MARKET SHARE BY GLA

Source: ACE Colombia, Parque Arauco analysis

(11 assets)

(7 assets)

(4 assets)

(5 assets)

(3 assets)

(1 assets)

(5 assets)

6

Parque Arauco has improved its market share in a fragmented market

2010 2011 2012 2013 2014 2015 2016

0,5

0,0

4,5

4,0

3,5

3,0

5,0

1,0

2,0

2,5

1,5

As Construcciones Pactia

Parque Arauco

Terranum

Unico Outlet Almacenes La 14

Inmobiliaria Éxito

HISTORICAL MARKET SHARE

Source: ACE Colombia, Parque Arauco analysis

7

In Colombia market share is diversified by type of mall

57,9%

14,5%

27,6%

36,7%

33,5%

29,8%

Medium ( 20,000-39,999)

Large (>40,000)

Small (5,000-19,999)

Source: ACE Colombia

NUMBER OF SHOPPING MALLS BY SIZE GLA BY TYPE OF MALL

Total # of shopping malls: 214

Total m2: 4,942,791

8

Colombia has international developers

Owner Parque Arauco Falabella Spectrum Grupo Roble

Country Chile Chile Guatemala El Salvador

Assets Parque Arboleda (Pereira)Parque Caracolí (Bucaramanga)Parque La Colina (Bogotá)

El Castillo (Cartagena)

Fontanar (Bogotá) MultiPlaza (Bogotá)

Projects Arauco PremiumOutlet Bogotá

ManizalesBarranquillaCalí

Medellín

GLA (m2)¹ 142,500 40,000 57,000 65,000

(1) Rental Model GLASource: ACE Colombia

Brand

9

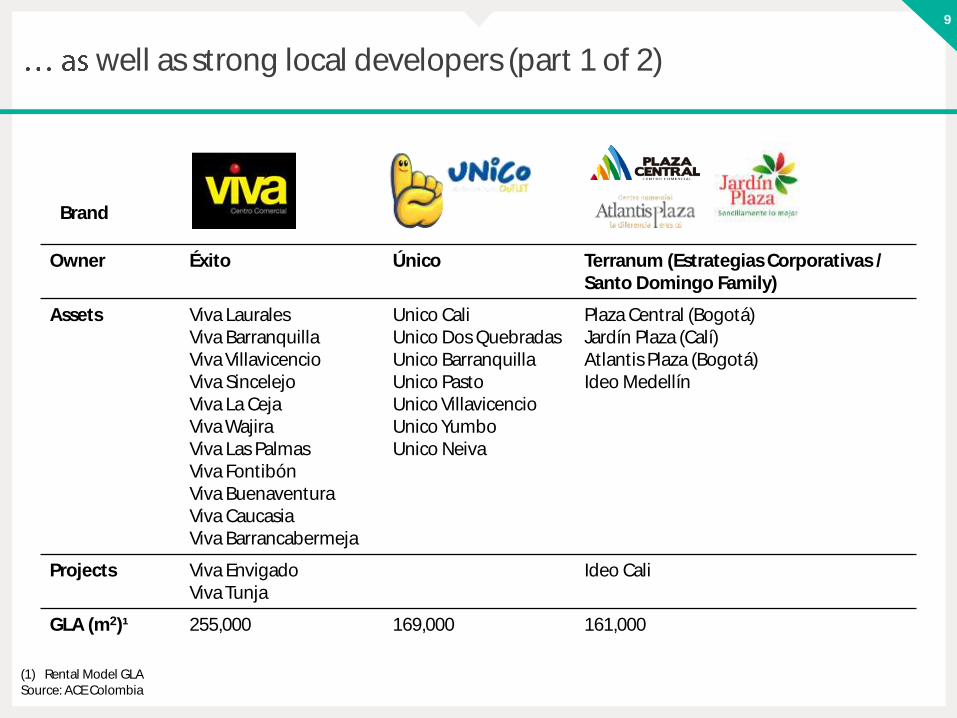

well as strong local developers (part 1 of 2)

Owner Éxito Único Terranum (Estrategias Corporativas / Santo Domingo Family)

Assets Viva LauralesViva BarranquillaViva VillavicencioViva SincelejoViva La CejaViva WajiraViva Las PalmasViva FontibónViva BuenaventuraViva CaucasiaViva Barrancabermeja

Unico CaliUnico Dos QuebradasUnico BarranquillaUnico PastoUnico VillavicencioUnico YumboUnico Neiva

Plaza Central (Bogotá)Jardín Plaza (Calí)Atlantis Plaza (Bogotá)Ideo Medellín

Projects Viva EnvigadoViva Tunja

Ideo Cali

GLA (m2)¹ 255,000 169,000 161,000

(1) Rental Model GLASource: ACE Colombia

Brand

10

well as strong local developers (part 2 of 2)

Owner As Construcciones Almacenes La 14 Pactia (Conconcreto / Grupo Argos)

Assets Buenavista BarranquillaBuenavista MonteriaBuenavista Santa MartaPanorama (Barranquilla)Americano (Barranquilla)

Calima Bogotá Gran Plaza SoledadGran Plaza PitalitoGran Plaza FlorenciaGran Plaza IpialesGran Plaza AntaresGran Plaza AlcaravánGran Plaza San AntonioGran Plaza del SolSan Pedro Plaza (Neiva)Guatapurí Plaza (Valledupar)

Projects Gran Plaza BosaGran Plaza El Ensueño

GLA (m2)¹ 145,000 93,000 64,000

(1) Rental Model GLASource: ACE Colombia

Brand

[11]

I. Competitive landscape

II. Sector dynamics

III. Rental vs. condominium

IV. eCommerce in Colombia

V. Globalization of Brands

Agenda

12

GLA in Colombia has been growing on average at 7% in the last 5 years

4.000

5.000

2.000

1.000

3.000

0

2013

+7%

201620152014

+7%

2011200920082007 20122010

214204198188166158152139133121

20162014

+7%

201220112010 2015

+6%

2013200920082007

Source: ACE Colombia

161.500199.030

20142012

437.779

20132010

168.680

322.482

2016

216.372

2011 2015

383.599

2009

318.622

95.666

268.965

2007 2008 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

12%

8%

4%5%

6%5%

11%10%

13%

3%

EVOLUTION OF GLA IN COLOMBIA(TH M2)

NUMBERS OF SHOPPING CENTERS IN COLOMBIA(#)

ANNUAL VARIATION OF GLA (M2)

ANNUAL GROWTH RATE (% CHANGE)

13

Shopping center sales have outpaced retail sales in Colombia

10.000

0

15.000

5.000

2013 2015 20162014

+11,6%

20122011

2011 2012 2013 2014 2015 2016

10,8%

18,9%19,8%

11,5%13,9%

3,6%

80.000

60.000

20.000

0

40.000

2015 2016

+6,1%

20142011 20132012

2011 2012 2013 2014 2015 2016

5,6%7,1%

16,9%

7,2%5,9%4,6%

Source: ACE Colombia / Raddar- Shopping Centerr Sales, Euromonitor- Retail Sales

RETAIL SALES (EUROMONITOR) (THUSD)

SHOPPING CENTER SALES (RADDAR/ACE COLOMBIA) (THUSD)

RETAIL SALES GROWTH (% CHANGE)

SHOPPING CENTER SALES GROWTH (% CHANGE)

14

Rental model malls are gaining market share in Colombia

75 73 69 68 67 65 61

11 11 13 13 13 1313

14 17 18 19 20 22 26

2013 20162011 2015201420122010

Mixed Model

Rental Model

Condominium

Source: ACE Colombia

Rental 553,321 698,015 778,021 910,887 1,007,585 1,145,744 1,469,668

Mixed 434,752 451,656 561,904 623,238 654,931 677,031 734,834

Condo. 2,964,218 2,997,357 2,982,415 3,260,016 3,375,411 3,385,153 3,448,067

Total 3,952,290 4,147,028 4,322,340 4,794,141 5,037,927 5,207,927 5,652,569

% OF GLA BY PROPERTY TYPE IN COLOMBIA

15

New malls opening are predominately rental model

6,0%

New development GLA

60,6%

33,4%

Rental Model

Mixed Model

Condominium

Source: ACE Colombia

% NEW GLA IN COLOMBIA BY PROPERTY TYPE (% OF TOTAL GLA)

[16]

I. Competitive landscape

II. Sector dynamics

III. Rental vs. condominium

IV. eCommerce in Colombia

V. Globalization of Brands

Agenda

17

Colombian shopping center industry is unique

• Sometimes operational standard (i.e. marketing efforts, cleaning and security, window display standard, etc.) is lower

• Operational standard (i.e. marketing efforts, cleaning and security, window display standard, etc.) is higher

Condominium Malls Rental Model Malls

Owner

Financing

Construction quality

Layout

Commercial Mix

Operational standard

Capex

Several owners buy stores; most of them are retailers, some of them are investors that sublease the store

• Single owner lease stores

• Construction is financed by pre-selling stores

• Construction is financed by issuing debt

• Sometimes construction materials and equipment are acquired thinking about short term

• Construction materials and equipment are acquired thinking about long term

• Sometimes layout is not optimum since construction companies minimize common areas in order to maximize area to be sold

• Layout is defined by single owner that think about the customer experience afterwards

• Sometimes commercial mix is not optimum since it is defined by maximizing money collected in selling process

• Commercial mix is defined by criteria of maximizing long term sales and revenues and tends to be optimum

• Sometimes agreeing on capex between 200 tenants can be challenging because of

Free Riders

• Single owner define capex (growth and/or maintenance capex) thinking about the long term

Source: Parque Arauco

18

Case Study Pereira: Rental Sales vs. Condominium Sales

0

10

20

30

40

50

60

70

80

2008 2009 2010 2011 2012 2013 2014 2015 2016

Condo. Mall 3

Condo. Mall 2Parque Arboleda

Condo. Mall 1

PEREIRA MALL SALES (USDMM)

Source: Raddar / Parque Arauco

[19]

I. Competitive landscape

II. Sector dynamics

III. Rental vs. condominium

IV. eCommerce in Colombia

V. Globalization of Brands

Agenda

20

Colombia has one of the lowest ecommerce penetrationsin the region

4,7%

Argentina

1,6%

4,0%

2,5%

United States

2,6%

United Kingdom

Mexico ChileBrazil PeruColombia

10,5%

14,9%

1,1%

Source: ICSC, Euromonitor

INTERNET RETAIL AS % OF TOTAL RETAIL IN 2016

21

CHILE

PERÚ

COLOMBIA

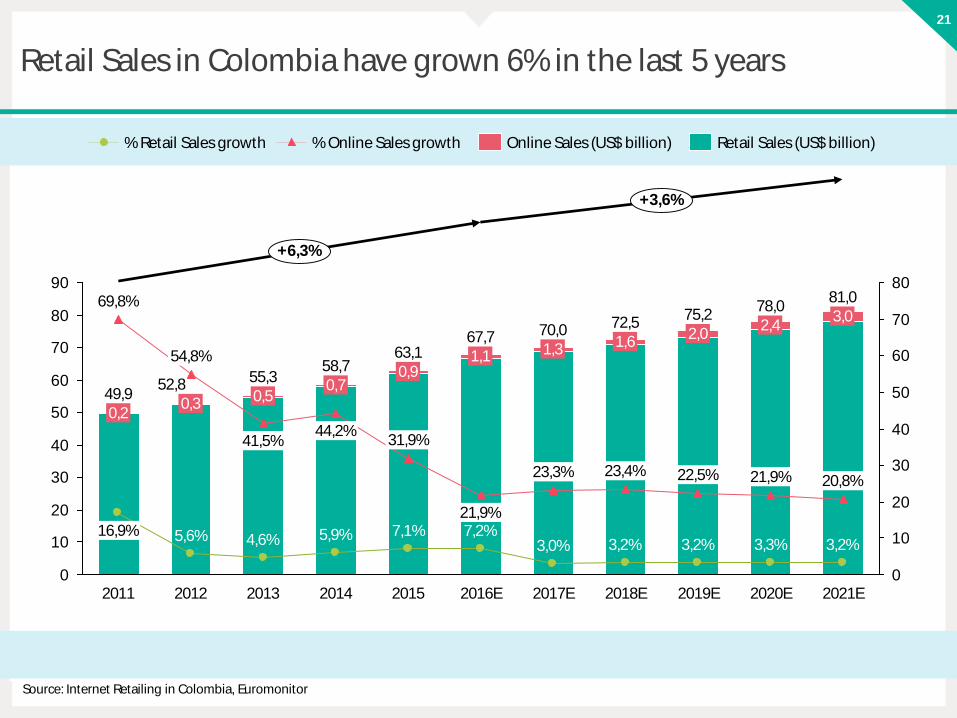

Retail Sales in Colombia have grown 6% in the last 5 years

0

10

20

30

40

50

60

70

80

90

0

10

20

30

40

50

60

70

80

22,5%

3,2%

20,8%

3,2%

2018E

78,02,4

21,9%

+6,3%

3,3%

2020E2019E

1,3

7,2%

44,2%

2013

63,1

23,3%

1,1

2015

7,1%3,0%

2014

21,9%

72,51,6

2017E

31,9%

67,7

58,7

23,4%

0,9

3,2%

70,0

2016E

0,7

5,9%

55,30,5

69,8%

41,5%

52,849,9

2012

4,6%

0,3

54,8%

2011

0,2

5,6%16,9%

2021E

75,22,0

+3,6%

81,03,0

% Online Sales growth% Retail Sales growth Retail Sales (US$ billion)Online Sales (US$ billion)

Source: Internet Retailing in Colombia, Euromonitor

22

Retail eCommerce concentration in Colombia is low

0,4%

Online Retail

Retail

99,6%

Online Retail

Retail

98,4%

1,6%

96,4%

Online Retail

3,6%

Retail

2011 2016E 2021E

Source: Internet Retailing in Colombia, Euromonitor

RETAIL SALES IN COLOMBIA

[23]

I. Competitive landscape

II. Sector dynamics

III. Rental vs. condominium

IV. eCommerce in Colombia

V. Globalization of Brands

Agenda

24

Colombia is still an underpenetrated market by global retailers

9%

Me

xico

19%

8%

Ch

ile

10%

14%

Pe

ru

Co

lom

bia

8%

Arg

en

tin

a

Bra

zil

Can

ada

UK

27%

32%

46%

USA

Source: Parque Arauco analysis Powers of Retailing by Deloitte

% OF TOP 100 LARGEST GLOBAL RETAILERS IN COUNTRY GLOBAL RETAILERS PRESENT IN COLOMBIA

25

La Colina has a higher penetration of global brandsthan its competitors in Bogotá

0

5

10

15

20

25

30

35

40

45

50 48%

Mall 5 Mall 6

12%

28%

23%

Mall 2

30%

Mall 1

12%

Mall 4

33%

Mall 3Parque La Colina

International Brand %

Source: Parque Arauco analysis of tenants in each mall

Parque La Colinadirect competitor

PENETRATION OF GLOBAL BRANDS IN BOGOTÁ MALLS (% OF TOTAL STORES)

26

Parque Arboleda has a higher penetration of global brandsthan its competitors

0

2

4

6

8

10

12

14

16

18

20

22

24

Mall 3

6%

Mall 2

9%

Mall 1

10%

23%

Parque Arboleda

International Brand %

Source: Parque Arauco analysis of tenants in each mall

PENETRATION OF GLOBAL BRANDS IN BOGOTÁ MALLS (% OF TOTAL STORES)

27

Parque Caracolí has a higher penetration of global brandsthan its competitors

0

5

10

15

20

25

Mall 2

8%

15%

Mall 3

18%

Mall 1Parque Caracolí

25% International Brand %

Source: Parque Arauco analysis of tenants in each mall

PENETRATION OF GLOBAL BRANDS IN BOGOTÁ MALLS (% OF TOTAL STORES)

[28]

Managing Parque La ColinaOctober 2017

[2]

I. Introduction Parque La Colina

II. Commercial mix

III. Parque La Colina teamresponsibilities

V. Parque La Colina marketing activities

VI. Sustainability at Parque La Colina

Agenda

Versión 16-10-2017 20:32

[3]

I. Introduction Parque La Colina

II. Commercial mix

III. Parque La Colina teamresponsibilities

V. Parque La Colina marketing activities

VI. Sustainability at Parque La Colina

Agenda

[4]

Parque La Colina

Source: Parque Arauco

PARQUE LA COLINA

• Total investment of US$ 221 million

• 63,000 m2 of GLA

• 199 stores

• Opening date: December 2016

• 13,262 m2 of park

• 2,900 m2 of vertical gardens

• 3,000 parking spots

• 235 bicycle parking spots

• First openings of H&M, Crate & Barrel and Purificación García in Colombia

5

Mall is located by Avenida Boyacá, an important transportation road in Bogotá

Source: Parque Arauco

6

Location and influence area

Source: Parque Arauco

7

Influence area

41%

38%

3

4

5

18%

6

3%

6

2.584

5

1.803

1.195

43

2.133

Socio Economic Class Population HomesAverage Household

Income (USD)Clothing Spend

(USD)Recreational Spend

(USD)

3 197,027 62,999 1,195 251 117

4 117,720 50,707 1,803 481 187

5 62,857 25,853 2,133 563 223

6 13,022 4,113 2,584 721 299

HOMES BY SOCIOECONOMIC LEVEL AVERAGE INCOME BY HOME (USD)

Source: Parque Arauco

8

Consumer profile

HOME SIZE

1 2 3 49.11% 17.3% 29.46% 28.8%

5+15.33%

SEX OF

HEAD OF HOUSEHOLD

M F40.97% 59.03%

SEX OF MAIN

SHOPPERM F

6.15% 93.85%

Soure: EGM Ola III 2016 M +25 NSE 456 Bogotá

9

Consumer profile

Soure: EGM Ola III 2016 M +25 NSE 456 Bogotá

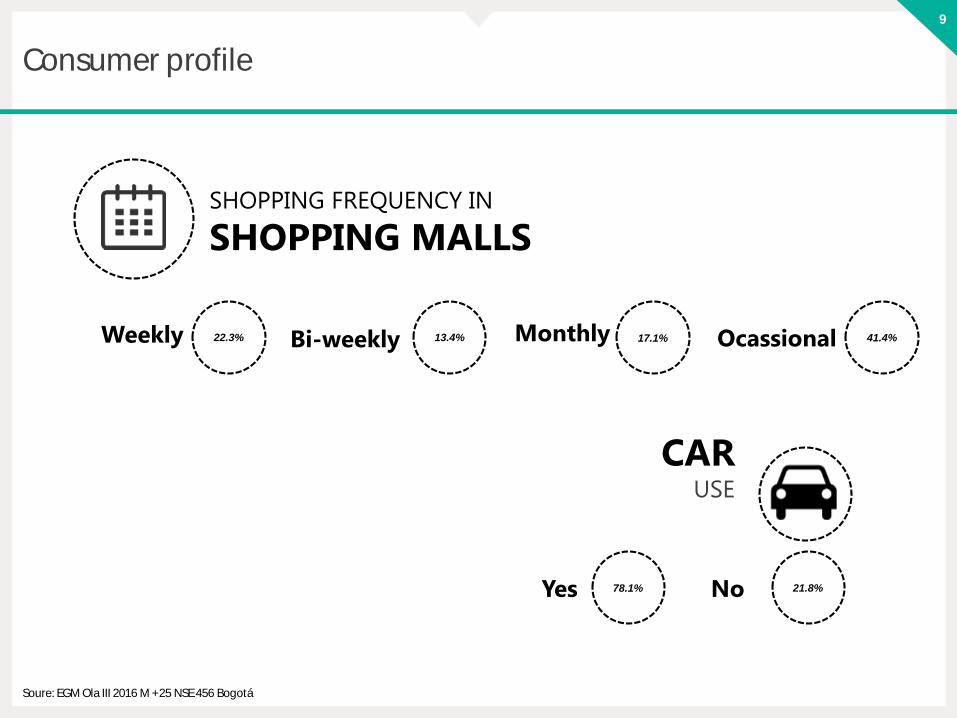

SHOPPING FREQUENCY IN

SHOPPING MALLS

OcassionalWeekly MonthlyBi-weekly 41.4%22.3% 17.1%13.4%

Yes No78.1% 21.8%

CARUSE

10

Consumer profile

Soure: EGM Ola III 2016 M +25 NSE 456 Bogotá

Women’s

ClothesLingerie

Women’s

ShoesBooks

Men’s

Clothes

Children’s

Clothes

Children’s

Shoes

Men’s

Shoes

Technology Bathing

Suits

81.2% 56.8% 54.6% 51.7%

48.3%

21.4%

35.6%

16.8%

34.9%30.0%

PURCHASES IN THE

LAST

3 MONTHS

11

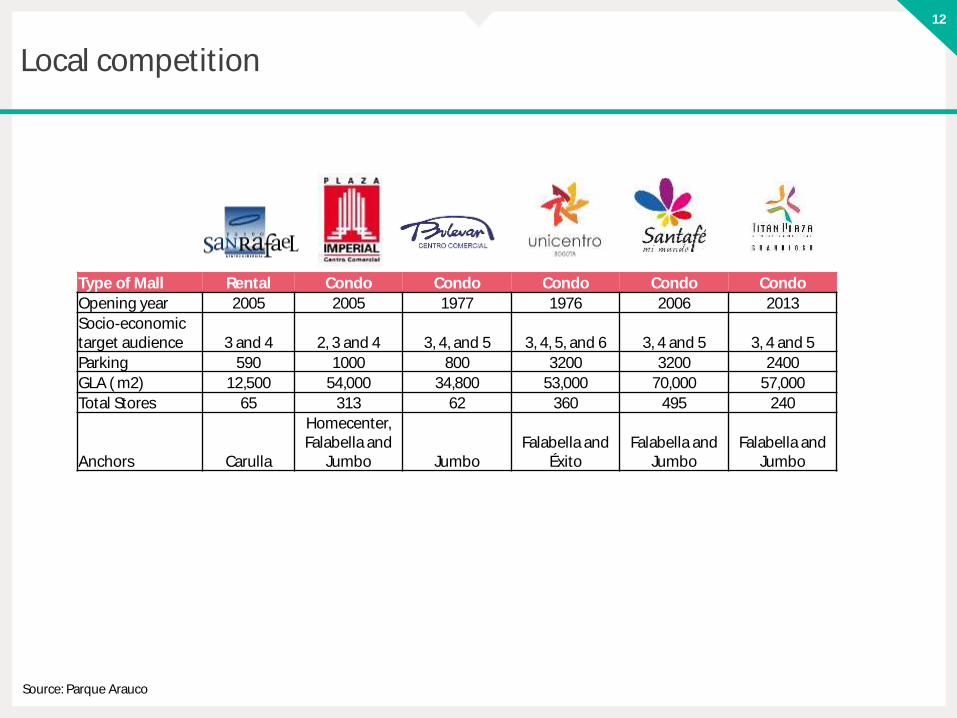

Local competition

• Local competition: 6 shopping centers are located in the North of Bogotá. Only three are within 4 km of Parque La Colina

Source: Parque Arauco

12

Local competition

Type of Mall Rental Condo Condo Condo Condo Condo

Opening year 2005 2005 1977 1976 2006 2013

Socio-economictarget audience 3 and 4 2, 3 and 4 3, 4, and 5 3, 4, 5, and 6 3, 4 and 5 3, 4 and 5

Parking 590 1000 800 3200 3200 2400

GLA ( m2) 12,500 54,000 34,800 53,000 70,000 57,000

Total Stores 65 313 62 360 495 240

Anchors Carulla

Homecenter, Falabella and

Jumbo JumboFalabella and

ÉxitoFalabella and

JumboFalabella and

Jumbo

Source: Parque Arauco

[13]

I. Introduction Parque La Colina

II. Commercial mix

III. Parque La Colina teamresponsibilities

V. Parque La Colina marketing activities

VI. Sustainability at Parque La Colina

Agenda

14

Commercial mix

1

2

5

5

16

17

25

28

Movie Theatre

Medium Sized Stores

Department Stores

Minor Stores

Small Sized Stores

Games

Restaurants

Food Court

GLA M² BY TYPE OF STORE BRANDS OPENING IN COLOMBIA IN PARQUE LA COLINA

Source: Parque Arauco

15

First floor layout

Source: Parque Arauco

16

Second floor layout

Source: Parque Arauco

17

Third floor layout

Source: Parque Arauco

18

La Colina has a higher penetration of global brands than itscompetitors in Bogotá

0

5

10

15

20

25

30

35

40

45

50 48%

Mall 5 Mall 6

12%

28%

23%

Mall 2

30%

Mall 1

12%

Mall 4

33%

Mall 3Parque La Colina

International Brand %

PENETRATION OF GLOBAL BRANDS IN BOGOTÁ MALLS (% OF TOTAL STORES)

Source: Parque Arauco analysis of tenants in each mall

Direct competition

19

Brands in Parque La Colina

Source: Parque Arauco

20

Brands in Parque La Colina

Source: Parque Arauco

21

I. Introduction Parque La Colina

II. Commercial mix

III. Parque La Colina teamresponsibilities

V. Parque La Colina marketing activities

VI. Sustainability at Parque La Colina

Agenda

22

Strategic Plan Parque La Colina

• Parque La Colina is the meeting placefor women and their circle of friends andfamily in the North of Bogota, with aninnovative and modern construction. The