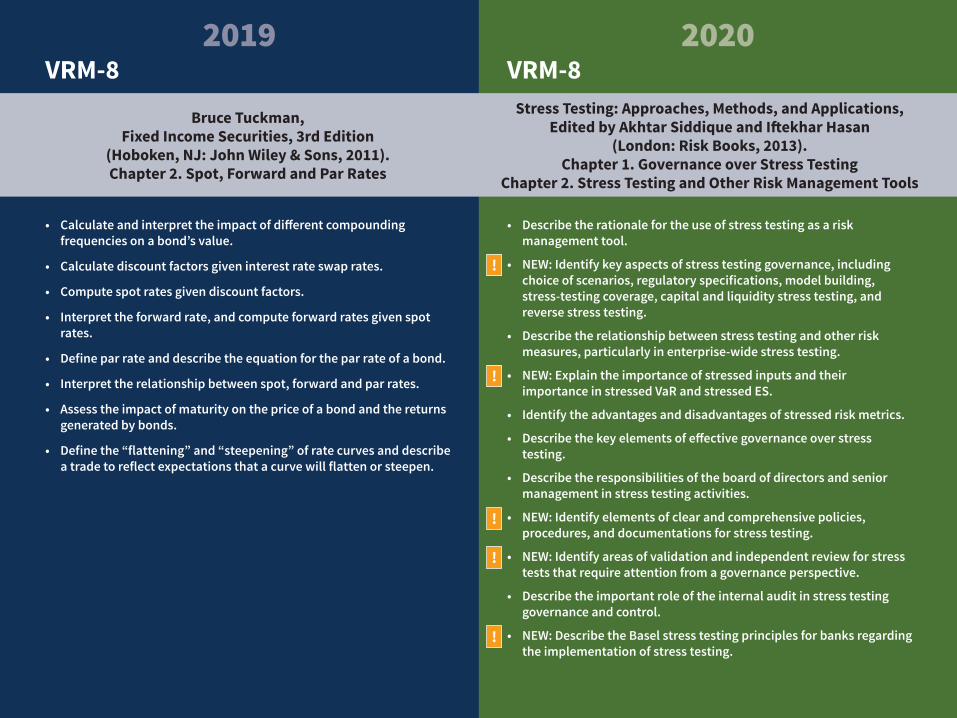

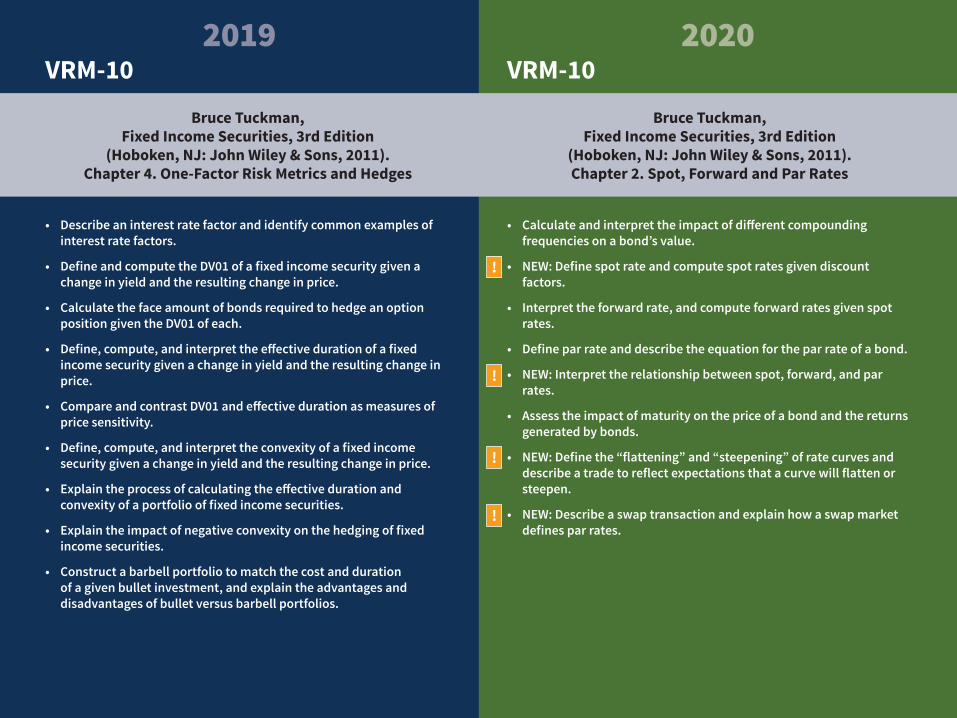

part i frm - efficientlearning.com · journal of economic perspectives 23:1, 77—100 frm-7 frm-7...

TRANSCRIPT

PART I FRM2020 CURRICULUM UPDATES

See updates to the 2020 PART I FRM program curriculum.

GARP updates the program curriculum every year to ensure study materials and exams refl ect the most up-to-date knowledge and skills required to be successful as a risk professional.

2019 2020

Michel Crouhy, Dan Galai, and Robert Mark, The Essentials of Risk Management, 2nd Edition (New

York: McGraw-Hill, 2014). Chapter 1. Risk Management: A Helicopter View (Including Appendix 1.1)

Michel Crouhy, Dan Galai, and Robert Mark, The Essentials of Risk Management, 2nd Edition (New

York: McGraw-Hill, 2014). Chapter 1. Risk Management: A Helicopter View (Including Appendix 1.1)

FRM-1 FRM-1

• Explaintheconceptofriskandcompareriskmanagementwithrisktaking.

• Describetheriskmanagementprocessandidentifyproblemsandchallengesthatcanariseintheriskmanagementprocess.

• Evaluateandapplytoolsandproceduresusedtomeasureandmanagerisk,includingquantitativemeasures,qualitativeassessment,andenterpriseriskmanagement.

• Distinguishbetweenexpectedlossandunexpectedloss,andprovideexamplesofeach.

• Interprettherelationshipbetweenriskandrewardandexplainhowconflictsofinterestcanimpactriskmanagement.

• Describeanddifferentiatebetweenthekeyclassesofrisks,explainhoweachtypeofriskcanarise,andassessthepotentialimpactofeachtypeofriskonanorganization.

• Explaintheconceptofriskandcompareriskmanagementwithrisktaking.

• NEW:Describeelements,orbuildingblocks,oftheriskmanagementprocessandidentifyproblemsandchallengesthatcanariseintheriskmanagementprocess.

• Evaluateandapplytoolsandproceduresusedtomeasureandmanagerisk,includingquantitativemeasures,qualitativeassessment,andenterpriseriskmanagement.

• Distinguishbetweenexpectedlossandunexpectedloss,andprovideexamplesofeach.

• Interprettherelationshipbetweenriskandrewardandexplainhowconflictsofinterestcanimpactriskmanagement.

• Describeanddifferentiatebetweenthekeyclassesofrisks,explainhoweachtypeofriskcanarise,andassessthepotentialimpactofeachtypeofriskonanorganization.

• NEW:Explainhowriskfactorscaninteractwitheachotheranddescribechallengesinaggregatingriskexposures.

!

!

2019 2020

Michel Crouhy, Dan Galai, and Robert Mark, The Essentials of Risk Management,

2nd Edition (New York: McGraw-Hill, 2014). Chapter 2. Corporate Risk Management: A Primer

Michel Crouhy, Dan Galai, and Robert Mark, The Essentials of Risk Management,

2nd Edition (New York: McGraw-Hill, 2014). Chapter 2. Corporate Risk Management: A Primer

FRM-2 FRM-2

• Evaluatesomeadvantagesanddisadvantagesofhedgingriskexposures.

• Explainconsiderationsandproceduresindeterminingafirm’sriskappetiteanditsbusinessobjectives.

• Explainhowacompanycandeterminewhethertohedgespecificriskfactors,includingtheroleoftheboardofdirectorsandtheprocessofmappingrisks.

• Applyappropriatemethodstohedgeoperationalandfinancialrisks,includingpricing,foreigncurrencyandinterestraterisk.

• Assesstheimpactofriskmanagementinstruments.

• NEW:Comparedifferentstrategiesafirmcanusetomanageitsriskexposuresandexplainsituationsinwhichafirmwouldwanttouseeachstrategy.

• NEW:Explaintherelationshipbetweenriskappetiteandafirm’sriskmanagementdecisions.

• NEW:Evaluatesomeadvantagesanddisadvantagesofhedgingriskexposures,andexplainchallengesthatcanarisewhenimplementingahedgingstrategy.

• Applyappropriatemethodstohedgeoperationalandfinancialrisks,includingpricing,foreigncurrency,andinterestraterisk.

• NEW:Assesstheimpactofriskmanagementtoolsandinstruments,includingrisklimitsandderivatives.

!

!

!

!

2019 2020

Michel Crouhy, Dan Galai, and Robert Mark, The Essentials of Risk Management, 2nd Edition

(New York: McGraw-Hill, 2014). Chapter 4. Corporate Governance and Risk Management

Michel Crouhy, Dan Galai, and Robert Mark, The Essentials of Risk Management, 2nd Edition

(New York: McGraw-Hill, 2014). Chapter 4. Corporate Governance and Risk Management

FRM-3 FRM-3

• Compareandcontrastbestpracticesincorporategovernancewiththoseofriskmanagement.

• Assesstheroleandresponsibilitiesoftheboardofdirectorsinriskgovernance.

• Evaluatetherelationshipbetweenafirm’sriskappetiteanditsbusinessstrategy,includingtheroleofincentives.

• Distinguishthedifferentmechanismsfortransmittingriskgovernancethroughoutanorganization.

• Illustratetheinterdependenceoffunctionalunitswithinafirmasitrelatestoriskmanagement.

• Assesstheroleandresponsibilitiesofafirm’sauditcommittee.

• NEW:Explainchangesincorporateriskgovernancethatoccurredasaresultofthe2007—2009financialcrisis.

• Compareandcontrastbestpracticesincorporategovernancewiththoseofriskmanagement.

• Assesstheroleandresponsibilitiesoftheboardofdirectorsinriskgovernance.

• Evaluatetherelationshipbetweenafirm’sriskappetiteanditsbusinessstrategy,includingtheroleofincentives.

• Illustratetheinterdependenceoffunctionalunitswithinafirmasitrelatestoriskmanagement.

• Assesstheroleandresponsibilitiesofafirm’sauditcommittee.

!

2019 2020

James Lam, Enterprise Risk Management: From Incentives to Controls, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2014).

Chapter 4. What is ERM?

James Lam, Enterprise Risk Management: From Incentives to Controls, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2014).

Chapter 4. What is ERM?

FRM-4 FRM-4

• Describeenterpriseriskmanagement(ERM)andcompareandcontrastdifferingdefinitionsofERM.

• ComparethebenefitsandcostsofERManddescribethemotivationsforafirmtoadoptanERMinitiative.

• Describetheroleandresponsibilitiesofachiefriskofficer(CRO)andassesshowtheCROshouldinteractwithotherseniormanagement.

• DistinguishbetweencomponentsofanERMprogram

• NEW:Comparedifferenttypesofcreditderivatives,explainhoweachonetransferscreditrisk,anddescribetheiradvantagesanddisadvantages.

• NEW:Explaindifferenttraditionalapproachesormechanismsthatfirmscanusetohelpmitigatecreditrisk.

• NEW:Evaluatetheroleofcreditderivativesinthe2007—2009financialcrisis,andexplainchangesinthecreditderivativemarketthatoccurredasaresultofthecrisis.

• NEW:Explaintheprocessofsecuritization,describeaspecialpurposevehicle(SPV),andassesstheriskofdifferentbusinessmodelsthatbankscanuseforsecuritizedproducts.

!

!

!

!

2019 2020

Elton, Gruber, Brown and Goetzmann, Modern Portfolio Theory and Investment Analysis,

9th Edition, Chapter 13. Amenc and Le Sourd,

Portfolio Theory and Performance Analysis. Chapter 4.

René Stulz, Risk Management, Governance, Culture and Risk Taking in Banks,

FRBNY Economic Policy Review, (August 2016): 43-59.

FRM-5 FRM-5

• Assessmethodsthatbankscanusetodeterminetheiroptimallevelofriskexposure,andexplainhowtheoptimallevelofriskcandifferacrossbanks

• Describeimplicationsforabankifittakestoolittleortoomuchriskcomparedtoitsoptimallevel

• Explainwaysinwhichriskmanagementcanaddordestroyvalueforabank

• Describestructuralchallengesandlimitationstoeffectiveriskmanagement,includingtheuseofVaRinsettinglimits.

• Assessthepotentialimpactofabank’sgovernance,incentivestructureandriskcultureonitsriskprofileanditsperformance

• NEW:ExplainmodernportfoliotheoryandinterprettheMarkowitzefficientfrontier.

• UnderstandthederivationandcomponentsoftheCAPM.

• DescribetheassumptionsunderlyingtheCAPM.

• Interpretthecapitalmarketline.

• ApplytheCAPMincalculatingtheexpectedreturnonanasset.

• Interpretbetaandcalculatethebetaofasingleassetorportfolio.

• Calculate,compare,andinterpretthefollowingperformancemeasures:theSharpeperformanceindex,theTreynorperformanceindex,theJensenperformanceindex,thetrackingerror,informationratio,andSortinoratio.

!

2019 2020

Zvi Bodie, Alex Kane, and Alan J. Marcus, Investments, 10th Edition (New York: McGraw-Hill, 2013).

Chapter 10. Arbitrage Pricing Theory and Multifactor Models of Risk and Return

Steve Allen, Financial Risk Management: A Practitioner’s Guide to Managing Market and Credit

Risk, 2nd Edition (New York: John Wiley & Sons, 2013). Chapter 4. Financial Disasters

FRM-6 FRM-6

• Analyzethekeyfactorsthatledtoandderivethelessonslearnedfromthefollowingriskmanagementcasestudies:ChaseManhattanandtheirinvolvementwithDrysdaleSecurities,KidderPeabody,Barings,AlliedIrishBank,UnionBankofSwitzerland,SociétéGénérale,LongTermCapitalManagement,Metallgesellschaft,BankersTrust,JPMorgan,Citigroup,andEnron

• NEW:Explainthearbitragepricingtheory(APT),describeitsassumptions,andcomparetheAPTtotheCAPM.

• Describetheinputs(includingfactorbetas)toamultifactormodel.

• Calculatetheexpectedreturnofanassetusingasingle-factorandamultifactormodel.

• NEW:Explainmodelsthataccountforcorrelationsbetweenassetreturnsinamulti-assetportfolio.

• Explainhowtoconstructaportfoliotohedgeexposuretomultiplefactors.

• DescribeandapplytheFama-Frenchthreefactormodelinestimatingassetreturns.

!

!

2019 2020

Principles for Effective Data Aggregation and Risk Reporting,

(Basel Committee on Banking Supervision Publication, January 2013).

Markus K. Brunnermeir, 2009. Deciphering the Liquidity and Credit Crunch 2007—2008,

Journal of Economic Perspectives 23:1, 77—100

FRM-7 FRM-7

• Explainthepotentialbenefitsofhavingeffectiveriskdataaggregationandreporting.

• NEW:Describetheimpactofdataqualityonmodelriskandthemodeldevelopmentprocess.

• Describekeygovernanceprinciplesrelatedtoriskdataaggregationandriskreportingpractices.

• NEW:Identifythegovernanceframework,riskdataarchitectureandITinfrastructurefeaturesthatcancontributetoeffectiveriskdataaggregationandriskreportingpractices.

• Describecharacteristicsofastrongriskdataaggregationcapabilityanddemonstratehowthesecharacteristicsinteractwithoneanother.

• Describecharacteristicsofeffectiveriskreportingpractices.

• Describetherolethatsupervisorsplayinthemonitoringandimplementationoftheriskdataaggregationandreportingpractices.

• Describethekeyfactorstheledtothehousingbubble.

• Explainthebankingindustrytrendsleadinguptotheliquiditysqueezeandassessthetriggersfortheliquiditycrisis.

• Explainthepurposesandusesofcreditdefaultswaps.

• Describehowsecuritizedandstructuredproductswereusedbyinvestorgroupsanddescribetheconsequencesoftheirincreaseduse.

• Describehowthefinancialcrisistriggeredaseriesofworldwidefinancialandeconomicconsequences.

• Distinguishbetweenfundingliquidityandmarketliquidityandexplainhowtheevaporationofliquiditycanleadtoafinancialcrisis.

• Analyzehowanincreaseincounterpartycreditriskcangenerateadditionalfundingneedsandpossiblesystemicrisk

!

!

2019 2020

James Lam, Enterprise Risk Management: From Incentives to Controls, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2014).

Chapter 4. What is ERM?

Gary Gorton and Andrew Metrick, 2012. Getting Up to Speed on the Financial Crisis:

A One-Weekend-Reader’s Guide, Journal of Economic Literature 50:1, 128—150.

FRM-8 FRM-8

• Distinguishbetweentriggersandvulnerabilitiesthatledtothefinancialcrisisandtheircontributionstothecrisis.

• Describethemainvulnerabilitiesofshort-termdebtespeciallyrepoagreementsandcommercialpaper.

• AssesstheconsequencesoftheLehmanfailureontheglobalfinancialmarkets.

• Describethehistoricalbackgroundleadingtotherecentfinancialcrisis.

• Distinguishbetweenthetwomainpanicperiodsofthefinancialcrisisanddescribethestateofthemarketsduringeach.

• Assessthegovernmentalpolicyresponsestothefinancialcrisisandreviewtheirshort-termimpact.

• Describetheglobaleffectsofthefinancialcrisisonfirmsandtherealeconomy

• NEW:DescribeEnterpriseRiskManagement(ERM)andcompareanERMprogramwithatraditionalsilo-basedriskmanagementprogram.

• ComparethebenefitsandcostsofERManddescribethemotivationsforafirmtoadoptanERMinitiative.

• NEW:ExplainbestpracticesforthegovernanceandimplementationofanERMprogram.

• NEW:DescribeimportantdimensionsofanERMprogramandrelateERMtostrategicplanning.

• NEW:Describeriskculture,explaincharacteristicsofastrongcorporateriskculture,anddescribechallengestotheestablishmentofastrongriskcultureatafirm.

• NEW:ExplaintheroleofscenarioanalysisintheimplementationofanERMprogramanddescribeitsadvantagesanddisadvantages.

• NEW:Explaintheuseofscenarioanalysisinstresstestingprogramsandincapitalplanning.

!

!

!

!

!

!

2019 2020

René Stulz, Risk Management Failures: What are They and When Do They Happen?

Fisher College of Business Working Paper Series, October 2008.

René Stulz, Risk Management Failures: What are They and When Do They Happen?

Fisher College of Business Working Paper Series, October 2008.

FRM-9 FRM-9

• Explainhowalargefinanciallossmaynotnecessarilybeevidenceofariskmanagementfailure.

• Analyzeandidentifyinstancesofriskmanagementfailure.

• Explainhowriskmanagementfailurescanariseinthefollowingareas:measurementofknownriskexposures,identificationofriskexposures,communicationofrisks,andmonitoringofrisks.

• Evaluatetheroleofriskmetricsandanalyzetheshortcomingsofexistingriskmetrics.

• NEW:Analyzethekeyfactorsthatledtoandderivethelessonslearnedfromcasestudiesinvolvingthefollowingriskfactor:Interestraterisk,includingthe1980ssavingsandloancrisisintheUS

• NEW:Analyzethekeyfactorsthatledtoandderivethelessonslearnedfromcasestudiesinvolvingthefollowingriskfactor:Fundingliquidityrisk,includingLehmanBrothers,ContinentalIllinois,andNorthernRock

• NEW:Analyzethekeyfactorsthatledtoandderivethelessonslearnedfromcasestudiesinvolvingthefollowingriskfactor:Implementinghedgingstrategies,includingtheMetallgesellschaftcase

• NEW:Analyzethekeyfactorsthatledtoandderivethelessonslearnedfromcasestudiesinvolvingthefollowingriskfactor:Modelrisk,includingtheNiederhoffercase,LongTermCapitalManagement,andtheLondonWhalecase

• NEW:Analyzethekeyfactorsthatledtoandderivethelessonslearnedfromcasestudiesinvolvingthefollowingriskfactor:Roguetradingandmisleadingreporting,includingtheBaringscase

• NEW:Analyzethekeyfactorsthatledtoandderivethelessonslearnedfromcasestudiesinvolvingthefollowingriskfactor:Financialengineeringandcomplexderivatives,includingBankersTrust,theOrangeCountycase,andSachsenLandesbank

• NEW:Analyzethekeyfactorsthatledtoandderivethelessonslearnedfromcasestudiesinvolvingthefollowingriskfactor:Reputationalrisk,includingtheVolkswagencase

• NEW:Analyzethekeyfactorsthatledtoandderivethelessonslearnedfromcasestudiesinvolvingthefollowingriskfactor:Corporategovernance,includingtheEnroncase

• NEW:Analyzethekeyfactorsthatledtoandderivethelessonslearnedfromcasestudiesinvolvingthefollowingriskfactor:Cyberrisk,includingtheSWIFTcase

!

!

!

!

!

!

!

!

!

2019 2020

Edwin J. Elton, Martin J. Gruber, Stephen J. Brown and William N. Goetzmann,

Modern Portfolio Theory and Investment Analysis, 9th Edition (Hoboken, NJ: John Wiley & Sons, 2014).

Chapter 13. The Standard Capital Asset Pricing Model

Edwin J. Elton, Martin J. Gruber, Stephen J. Brown and William N. Goetzmann,

Modern Portfolio Theory and Investment Analysis, 9th Edition (Hoboken, NJ: John Wiley & Sons, 2014).

Chapter 13. The Standard Capital Asset Pricing Model

FRM-10 FRM-10

• UnderstandthederivationandcomponentsoftheCAPM.

• DescribetheassumptionsunderlyingtheCAPM.

• Interpretthecapitalmarketline.

• ApplytheCAPMincalculatingtheexpectedreturnonanasset.

• Interpretbetaandcalculatethebetaofasingleassetorportfolio.

• NEW:Describethehistoricalbackgroundandprovideanoverviewofthe2007—2009financialcrisis.

• NEW:Describethebuild-uptothefinancialcrisisandthefactorsthatplayedanimportantrole.

• NEW:Explaintheroleofsubprimemortgagesandcollateralizeddebtobligations(CDOs)inthecrisis.

• NEW:Comparetherolesofdifferenttypesofinstitutionsinthefinancialcrisis,includingbanks,financialintermediaries,mortgagebrokersandlenders,andratingagencies.

• NEW:Describetrendsintheshort-termwholesalefundingmarketsthatcontributedtothefinancialcrisis,includingtheirimpactonsystemicrisk.

• NEW:Describeresponsestakenbycentralbanksinresponsetothecrisis.

!

!

!

!

!

!

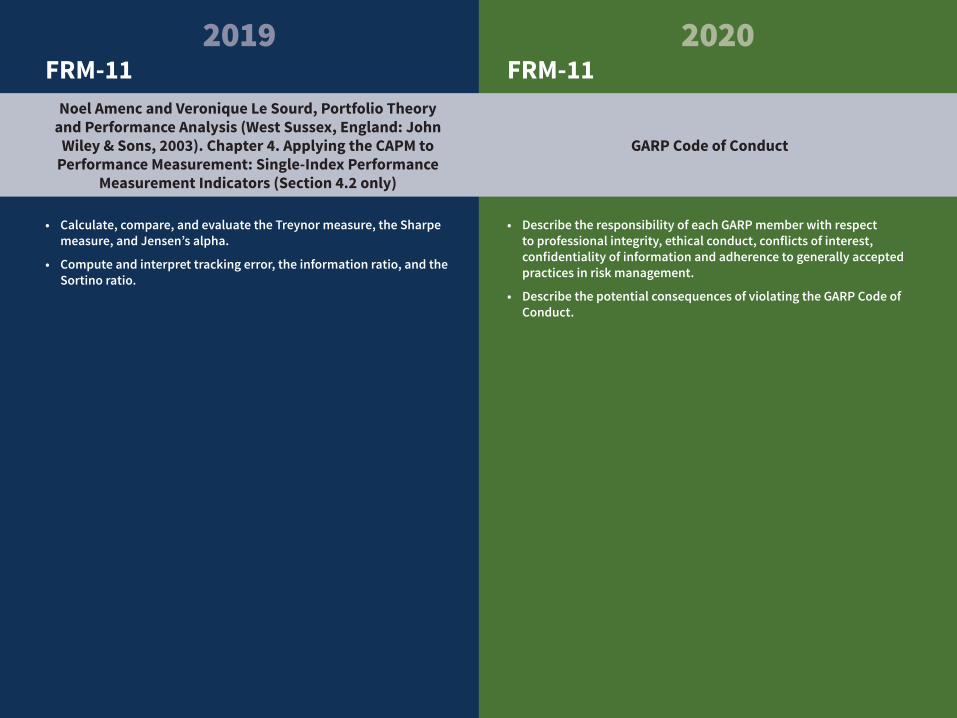

2019 2020

GARP Code of Conduct

Noel Amenc and Veronique Le Sourd, Portfolio Theory and Performance Analysis (West Sussex, England: John

Wiley & Sons, 2003). Chapter 4. Applying the CAPM to Performance Measurement: Single-Index Performance

Measurement Indicators (Section 4.2 only)

FRM-11 FRM-11

• Calculate,compare,andevaluatetheTreynormeasure,theSharpemeasure,andJensen’salpha.

• Computeandinterprettrackingerror,theinformationratio,andtheSortinoratio.

• DescribetheresponsibilityofeachGARPmemberwithrespecttoprofessionalintegrity,ethicalconduct,conflictsofinterest,confidentialityofinformationandadherencetogenerallyacceptedpracticesinriskmanagement.

• DescribethepotentialconsequencesofviolatingtheGARPCodeofConduct.

2019 2020

Michael Miller, Mathematics and Statistics for Financial Risk Management, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2013).

Chapter 2. Probabilities

Michael Miller, Mathematics and Statistics for Financial Risk Management, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2013).

Chapter 2. Probabilities

QA-1 QA-1

• Describeanddistinguishbetweencontinuousanddiscreterandomvariables.

• Defineanddistinguishbetweentheprobabilitydensityfunction,thecumulativedistributionfunction,andtheinversecumulativedistributionfunction.

• Calculatetheprobabilityofaneventgivenadiscreteprobabilityfunction.

• Distinguishbetweenindependentandmutuallyexclusiveevents.

• Definejointprobability,describeaprobabilitymatrix,andcalculatejointprobabilitiesusingprobabilitymatrices.

• Defineandcalculateaconditionalprobability,anddistinguishbetweenconditionalandunconditionalprobabilities.

• NEW:Describeaneventandaneventspace.

• Describeindependenteventsandmutuallyexclusiveevents.

• NEW:Explainthedifferencebetweenindependenteventsandconditionallyindependentevents.

• Calculatetheprobabilityofaneventforadiscreteprobabilityfunction.

• NEW:Defineandcalculateaconditionalprobability.

• NEW:Distinguishbetweenconditionalandunconditionalprobabilities.

• NEW:ExplainandapplyBayes’rule.

!

!

!!

!

2019 2020

Michael Miller, Mathematics and Statistics for Financial Risk Management, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2013).

Chapter 3. Basic Statistics

Michael Miller, Mathematics and Statistics for Financial Risk Management, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2013).

Chapter 3. Basic Statistics

QA-2 QA-2

• Interpretandapplythemean,standarddeviation,andvarianceofarandomvariable.

• Calculatethemean,standarddeviation,andvarianceofadiscreterandomvariable

• Interpretandcalculatetheexpectedvalueofadiscreterandomvariable.

• Calculateandinterpretthecovarianceandcorrelationbetweentworandomvariables.

• Calculatethemeanandvarianceofsumsofvariables.

• Describethefourcentralmomentsofastatisticalvariableordistribution:mean,variance,skewnessandkurtosis.

• Interprettheskewnessandkurtosisofastatisticaldistribution,andinterprettheconceptsofcoskewnessandcokurtosis.

• Describeandinterpretthebestlinearunbiasedestimator.

• NEW:Describeanddistinguishaprobabilitymassfunctionfromacumulativedistributionfunction,andexplaintherelationshipbetweenthesetwo.

• NEW:Understandandapplytheconceptofamathematicalexpectationofarandomvariable.

• NEW:Describethefourcommonpopulationmoments.

• NEW:Explainthedifferencesbetweenaprobabilitymassfunctionandaprobabilitydensityfunction.

• NEW:Characterizethequantilefunctionandquantile-basedestimators.

• NEW:Explaintheeffectofalineartransformationofarandomvariableonthemean,variance,standarddeviation,skewness,kurtosis,median,andinterquartilerange.

!

!

!!

!

!

2019 2020

Michael Miller, Mathematics and Statistics for Financial Risk Management, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2013).

Chapter 4. Distributions

Michael Miller, Mathematics and Statistics for Financial Risk Management, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2013).

Chapter 4. Distributions

QA-3 QA-3

• Distinguishthekeypropertiesamongthefollowingdistributions:uniformdistribution,Bernoullidistribution,Binomialdistribution,Poissondistribution,normaldistribution,lognormaldistribution,Chisquareddistribution,Student’st,andF-distributions,andidentifycommonoccurrencesofeachdistribution.

• Describethecentrallimittheoremandtheimplicationsithaswhencombiningi.i.d.randomvariables.

• Describeindependentandidenticallydistributed(i.i.d)randomvariablesandtheimplicationsofthei.i.d.assumptionwhencombiningrandomvariables.

• Describeamixturedistributionandexplainthecreationandcharacteristicsofmixturedistributions.

• Distinguishthekeypropertiesandidentifythecommonoccurrencesofthefollowingdistributions:uniformdistribution,Bernoullidistribution,binomialdistribution,Poissondistribution,normaldistribution,lognormaldistribution,Chi-squareddistribution,Student’st,andF-distributions.

• Describeamixturedistributionandexplainthecreationandcharacteristicsofmixturedistributions.

2019 2020

Michael Miller, Mathematics and Statistics for Financial Risk Management, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2013).

Chapter 6. Bayesian Analysis (pp. 113-124 only)

Michael Miller, Mathematics and Statistics for Financial Risk Management, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2013).

Chapter 6. Bayesian Analysis (pp. 113-124 only)

QA-4 QA-4

• DescribeBayes’theoremandapplythistheoreminthecalculationofconditionalprobabilities.

• ComparetheBayesianapproachtothefrequentistapproach.

• ApplyBayes’theoremtoscenarioswithmorethantwopossibleoutcomesandcalculateposteriorprobabilities.

• NEW:Explainhowaprobabilitymatrixcanbeusedtoexpressaprobabilitymassfunction.

• NEW:Computethemarginalandconditionaldistributionsofadiscretebivariaterandomvariable.

• NEW:Explainhowtheexpectationofafunctioniscomputedforabivariatediscreterandomvariable.

• NEW:Definecovarianceandexplainwhatitmeasures.

• NEW:Explaintherelationshipbetweenthecovarianceandcorrelationoftworandomvariables,andhowthesearerelatedtotheindependenceofthetwovariables.

• NEW:Explaintheeffectsofapplyinglineartransformationsonthecovarianceandcorrelationbetweentworandomvariables.

• NEW:Computethevarianceofaweightedsumoftworandomvariables.

• NEW:Computetheconditionalexpectationofacomponentofabivariaterandomvariable.

• NEW:Describethefeaturesofaniidsequenceofrandomvariables.

• NEW:Explainhowtheiidpropertyishelpfulincomputingthemeanandvarianceofasumofiidrandomvariables.

!

!

!

!

!

!

!

!

!

!

2019 2020

Michael Miller, Mathematics and Statistics for Financial Risk Management, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2013).

Chapter 7. Hypothesis Testing and Confidence Intervals

Michael Miller, Mathematics and Statistics for Financial Risk Management, 2nd Edition (Hoboken, NJ: John Wiley & Sons, 2013).

Chapter 7. Hypothesis Testing and Confidence Intervals

QA-5 QA-5

• Calculateandinterpretthesamplemeanandsamplevariance.

• Constructandinterpretaconfidenceinterval.

• Constructanappropriatenullandalternativehypothesis,andcalculateanappropriateteststatistic.

• Differentiatebetweenaone-tailedandatwo-tailedtestandidentifywhentouseeachtest.

• Interprettheresultsofhypothesistestswithaspecificlevelofconfidence.

• DemonstratetheprocessofbacktestingVaRbycalculatingthenumberofexceedances.

• NEW:Estimatethemean,variance,andstandarddeviationusingsampledata.

• NEW:Explainthedifferencebetweenapopulationmomentandasamplemoment.

• NEW:Distinguishbetweenanestimatorandanestimate.

• NEW:Describethebiasofanestimatorandexplainwhatthebiasmeasures.

• NEW:ExplainwhatismeantbythestatementthatthemeanestimatorisBLUE.

• NEW:Describetheconsistencyofanestimatorandexplaintheusefulnessofthisconcept.

• NEW:ExplainhowtheLawofLargeNumbers(LLN)andCentralLimitTheorem(CLT)applytothesamplemean.

• NEW:Estimateandinterprettheskewnessandkurtosisofarandomvariable.

• NEW:Usesampledatatoestimatequantiles,includingthemedian.

• NEW:EstimatethemeanoftwovariablesandapplytheCLT.

• NEW:Estimatethecovarianceandcorrelationbetweentworandomvariables.

• NEW:Explainhowcoskewnessandcokurtosisarerelatedtoskewnessandkurtosis.

!

!

!

!

!

!

!!

!

!

!!

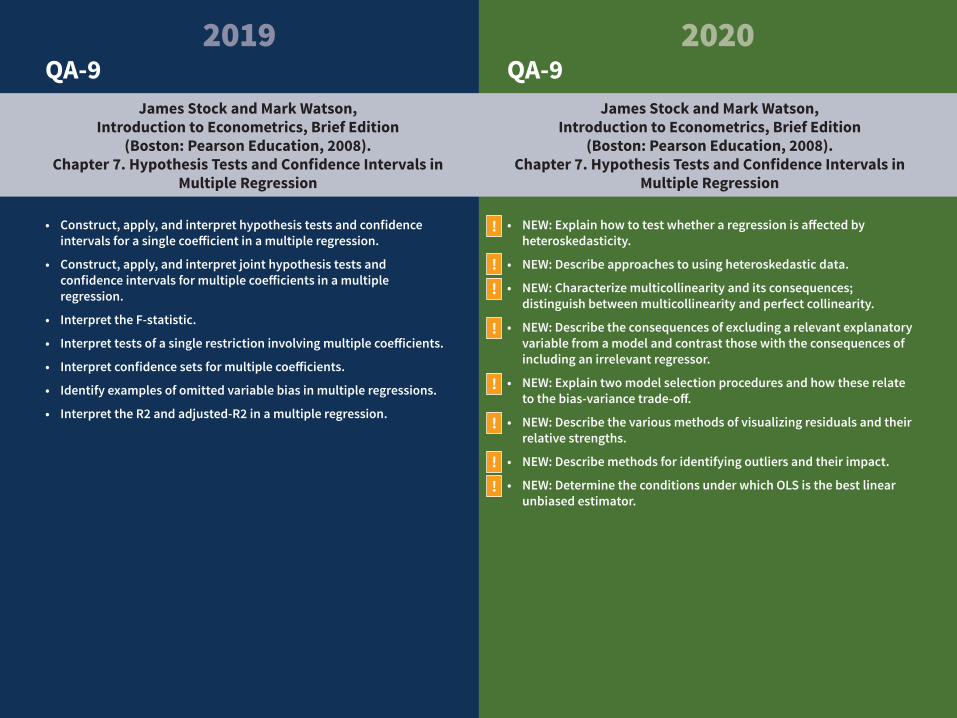

2019 2020

James Stock and Mark Watson, Introduction to Econometrics, Brief Edition (Boston: Pearson, 2008).

Chapter 4. Linear Regression with One Regressor

James Stock and Mark Watson, Introduction to Econometrics, Brief Edition (Boston: Pearson, 2008).

Chapter 4. Linear Regression with One Regressor

QA-6 QA-6

• Explainhowregressionanalysisineconometricsmeasurestherelationshipbetweendependentandindependentvariables.

• Interpretapopulationregressionfunction,regressioncoefficients,parameters,slope,intercept,andtheerrorterm.

• Interpretasampleregressionfunction,regressioncoefficients,parameters,slope,intercept,andtheerrorterm.

• Describethekeypropertiesofalinearregression

• Defineanordinaryleastsquares(OLS)regressionandcalculatetheinterceptandslopeoftheregression.

• DescribethemethodandthreekeyassumptionsofOLSforestimationofparameters.

• SummarizethebenefitsofusingOLSestimators

• DescribethepropertiesofOLSestimatorsandtheirsamplingdistributions,andexplainthepropertiesofconsistentestimatorsingeneral.

• Interprettheexplainedsumofsquares,thetotalsumofsquares,theresidualsumofsquares,thestandarderroroftheregression,andtheregressionR2.

• InterprettheresultsofanOLSregression

• NEW:Constructanappropriatenullhypothesisandalternativehypothesisanddistinguishbetweenthetwo.

• NEW:Differentiatebetweenaone-sidedandatwo-sidedtestandidentifywhentouseeachtest.

• NEW:ExplainthedifferencebetweenTypeIandTypeIIerrorsandhowtheserelatetothesizeandpowerofatest.

• NEW:Understandhowahypothesistestandaconfidenceintervalarerelated.

• NEW:Explainwhatthep-valueofahypothesistestmeasures.

• NEW:Interprettheresultsofhypothesistestswithaspecificlevelofconfidence.

• NEW:Identifythestepstotestahypothesisaboutthedifferencebetweentwopopulationmeans.

• NEW:Explaintheproblemofmultipletestingandhowitcanbiasresults.

!

!

!

!

!

!!

!

2019 2020

James Stock and Mark Watson, Introduction to Econometrics, Brief Edition

(Boston: Pearson Education, 2008). Chapter 5. Regression with a Single Regressor

James Stock and Mark Watson, Introduction to Econometrics, Brief Edition

(Boston: Pearson Education, 2008). Chapter 5. Regression with a Single Regressor

QA-7 QA-7

• Calculate,andinterpretconfidenceintervalsforregressioncoefficients.

• Interpretthep-value.

• Interprethypothesistestsaboutregressioncoefficients.

• Evaluatetheimplicationsofhomoskedasticityandheteroskedasticity.

• DeterminetheconditionsunderwhichtheOLSisthebestlinearconditionallyunbiasedestimator.

• ExplaintheGauss-MarkovTheoremanditslimitations,andalternativestotheOLS.

• Applyandinterpretthet-statisticwhenthesamplesizeissmall.

• Describethemodelswhichcanbeestimatedusinglinearregressionanddifferentiatethemfromthosewhichcannot.

• InterprettheresultsofanOLSregressionwithasingleexplanatoryvariable.

• DescribethekeyassumptionsofOLSparameterestimation.

• CharacterizethepropertiesofOLSestimatorsandtheirsamplingdistributions.

• Construct,apply,andinterprethypothesistestsandconfidenceintervalsforasingleregressioncoefficientinaregression.

• Explainthestepsneededtoperformahypothesistestinalinearregression.

• Describetherelationshipbetweenat-statistic,it’sp-value,andaconfidenceinterval.

!

!

!

!

!!

!

2019 2020

James Stock and Mark Watson, Introduction to Econometrics, Brief Edition

(Boston: Pearson Education, 2008). Chapter 6. Linear Regression with Multiple Regressors

James Stock and Mark Watson, Introduction to Econometrics, Brief Edition

(Boston: Pearson Education, 2008). Chapter 6. Linear Regression with Multiple Regressors

QA-8 QA-8

• Defineandinterpretomittedvariablebias,anddescribethemethodsforaddressingthisbias.

• Distinguishbetweensingleandmultipleregression.

• Interprettheslopecoefficientinamultipleregression.

• Describehomoskedasticityandheterosckedasticityinamultipleregression.

• DescribetheOLSestimatorinamultipleregression.

• Calculateandinterpretmeasuresoffitinmultipleregression.

• Explaintheassumptionsofthemultiplelinearregressionmodel.

• Explaintheconceptofimperfectandperfectmulticollinearityandtheirimplications.

• NEW:Distinguishbetweentherelativeassumptionsofsingleandmultipleregression.

• NEW:Interpretregressioncoefficientsinamultipleregression.

• NEW:Interpretgoodnessoffitmeasuresforsingleandmultipleregressions,includingR2andadjusted-R2.

• NEW:Construct,apply,andinterpretjointhypothesistestsandconfidenceintervalsformultiplecoefficientsinaregression.

!

!

!!

2019 2020

James Stock and Mark Watson, Introduction to Econometrics, Brief Edition

(Boston: Pearson Education, 2008). Chapter 7. Hypothesis Tests and Confidence Intervals in

Multiple Regression

James Stock and Mark Watson, Introduction to Econometrics, Brief Edition

(Boston: Pearson Education, 2008). Chapter 7. Hypothesis Tests and Confidence Intervals in

Multiple Regression

QA-9 QA-9

• Construct,apply,andinterprethypothesistestsandconfidenceintervalsforasinglecoefficientinamultipleregression.

• Construct,apply,andinterpretjointhypothesistestsandconfidenceintervalsformultiplecoefficientsinamultipleregression.

• InterprettheF-statistic.

• Interprettestsofasinglerestrictioninvolvingmultiplecoefficients.

• Interpretconfidencesetsformultiplecoefficients.

• Identifyexamplesofomittedvariablebiasinmultipleregressions.

• InterprettheR2andadjusted-R2inamultipleregression.

• NEW:Explainhowtotestwhetheraregressionisaffectedbyheteroskedasticity.

• NEW:Describeapproachestousingheteroskedasticdata.

• NEW:Characterizemulticollinearityanditsconsequences;distinguishbetweenmulticollinearityandperfectcollinearity.

• NEW:Describetheconsequencesofexcludingarelevantexplanatoryvariablefromamodelandcontrastthosewiththeconsequencesofincludinganirrelevantregressor.

• NEW:Explaintwomodelselectionproceduresandhowtheserelatetothebias-variancetrade-off.

• NEW:Describethevariousmethodsofvisualizingresidualsandtheirrelativestrengths.

• NEW:Describemethodsforidentifyingoutliersandtheirimpact.

• NEW:DeterminetheconditionsunderwhichOLSisthebestlinearunbiasedestimator.

!

!

!

!

!!

!!

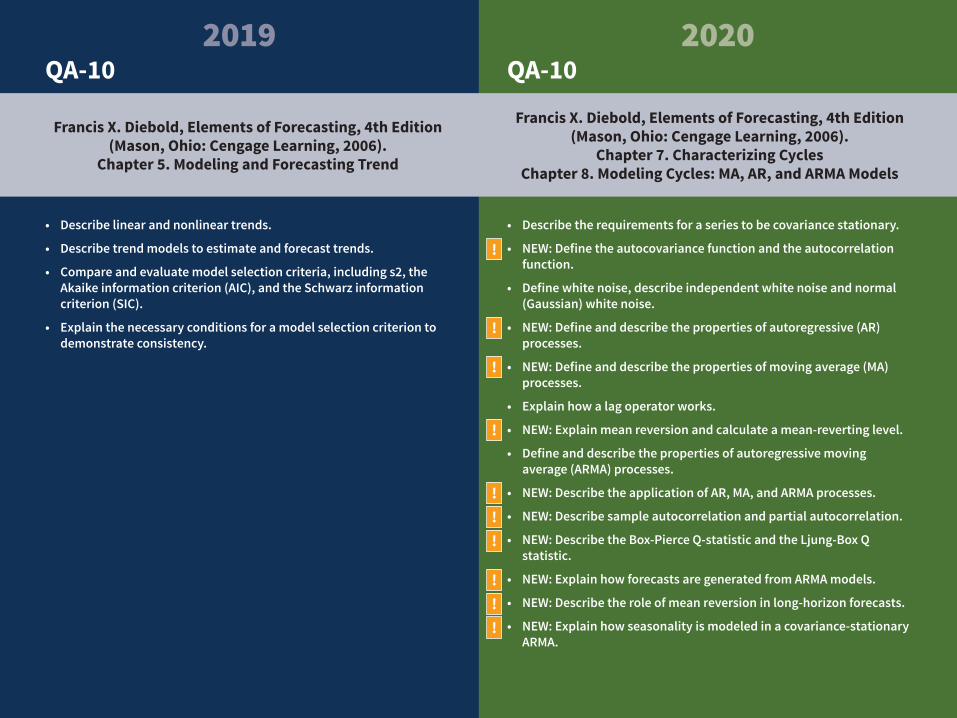

2019 2020

Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006).

Chapter 7. Characterizing CyclesChapter 8. Modeling Cycles: MA, AR, and ARMA Models

Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006).

Chapter 5. Modeling and Forecasting Trend

QA-10 QA-10

• Describelinearandnonlineartrends.

• Describetrendmodelstoestimateandforecasttrends.

• Compareandevaluatemodelselectioncriteria,includings2,theAkaikeinformationcriterion(AIC),andtheSchwarzinformationcriterion(SIC).

• Explainthenecessaryconditionsforamodelselectioncriteriontodemonstrateconsistency.

• Describetherequirementsforaseriestobecovariancestationary.

• NEW:Definetheautocovariancefunctionandtheautocorrelationfunction.

• Definewhitenoise,describeindependentwhitenoiseandnormal(Gaussian)whitenoise.

• NEW:Defineanddescribethepropertiesofautoregressive(AR)processes.

• NEW:Defineanddescribethepropertiesofmovingaverage(MA)processes.

• Explainhowalagoperatorworks.

• NEW:Explainmeanreversionandcalculateamean-revertinglevel.

• Defineanddescribethepropertiesofautoregressivemovingaverage(ARMA)processes.

• NEW:DescribetheapplicationofAR,MA,andARMAprocesses.

• NEW:Describesampleautocorrelationandpartialautocorrelation.

• NEW:DescribetheBox-PierceQ-statisticandtheLjung-BoxQstatistic.

• NEW:ExplainhowforecastsaregeneratedfromARMAmodels.

• NEW:Describetheroleofmeanreversioninlong-horizonforecasts.

• NEW:Explainhowseasonalityismodeledinacovariance-stationaryARMA.

!

!

!!

!

!!

!

!

!

2019 2020

Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006).

Chapter 5. Modeling and Forecasting TrendChapter 6. Modeling and Forecasting Seasonality

Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006).

Chapter 6. Modeling and Forecasting Seasonality

QA-11 QA-11

• Describethesourcesofseasonalityandhowtodealwithitintimeseriesanalysis

• Explainhowtouseregressionanalysistomodelseasonality

• Explainhowtoconstructanh-step-aheadpointforecast

• Describelinearandnonlineartimetrends.

• Explainhowtouseregressionanalysistomodelseasonality.

• NEW:Describearandomwalkandaunitroot.

• NEW:Explainthechallengesofmodelingtimeseriescontainingunitroots.

• NEW:Describehowtotestifatimeseriescontainsaunitroot.

• NEW:Explainhowtoconstructanh-step-aheadpointforecastforatimeserieswithseasonality.

• NEW:Calculatetheestimatedtrendvalueandformanintervalforecastforatimeseries.

!!

!!

!

2019 2020

John C. Hull, Risk Management and Financial Institutions, 4th Edition

(Hoboken, NJ: John Wiley & Sons, 2015). Chapter 10. Volatility

Chapter 11. Correlations and Copulas

Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006).

Chapter 7. Characterizing Cycles

QA-12 QA-12

• Definecovariancestationary,autocovariancefunction,autocorrelationfunction,partialautocorrelationfunctionandautoregression.

• Describetherequirementsforaseriestobecovariancestationary.

• Explaintheimplicationsofworkingwithmodelsthatarenotcovariancestationary.

• Definewhitenoise,describeindependentwhitenoiseandnormal(Gaussian)whitenoise.

• Explainthecharacteristicsofthedynamicstructureofwhitenoise.

• Explainhowalagoperatorworks.

• DescribeWold’stheorem.

• Defineagenerallinearprocess.

• RelaterationaldistributedlagstoWold’stheorem.

• Calculatethesamplemeanandsampleautocorrelation,anddescribetheBox-PierceQ-statisticandtheLjung-BoxQ-statistic.

• Describesamplepartialautocorrelation.

• NEW:Calculate,distinguish,andconvertbetweensimpleandcontinuouslycompoundedreturns.

• Defineanddistinguishbetweenvolatility,variancerate,andimpliedvolatility.

• NEW:Describehowthefirsttwomomentsmaybeinsufficienttodescribenon-normaldistributions.

• NEW:ExplainhowtheJarque-Beratestisusedtodeterminewhetherreturnsarenormallydistributed.

• NEW:Describethepowerlawanditsusefornon-normaldistributions.

• Definecorrelationandcovarianceanddifferentiatebetweencorrelationanddependence.

• NEW:Describepropertiesofcorrelationsbetweennormallydistributedvariableswhenusingaone-factormodel.

!

!

!

!

!

2019 2020

Chris Brooks, Introductory Econometrics for Finance, 3rd Edition

(Cambridge, UK: Cambridge University Press, 2014). Chapter 3.

Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006).

Chapter 8. Modeling Cycles: MA, AR, and ARMA Models

QA-13 QA-13

• Describethepropertiesofthefirst-ordermovingaverage(MA(1))process,anddistinguishbetweenautoregressiverepresentationandmovingaveragerepresentation.

• Describethepropertiesofageneralfinite-orderprocessoforderq(MA(q))process.

• Describethepropertiesofthefirst-orderautoregressive(AR(1))process,anddefineandexplaintheYule-Walkerequation.

• Describethepropertiesofageneralpthorderautoregressive(AR(p))process.

• Defineanddescribethepropertiesoftheautoregressivemovingaverage(ARMA)process.

• DescribetheapplicationofARandARMAprocesses.

• DescribethebasicstepstoconductaMonteCarlosimulation.

• DescribewaystoreduceMonteCarlosamplingerror.

• NEW:ExplaintheuseofantitheticandcontrolvariatesinreducingMonteCarlosamplingerror.

• NEW:DescribethebootstrappingmethodanditsadvantageoverMonteCarlosimulation.

• Describepseudo-randomnumbergenerationandhowagoodsimulationdesignalleviatestheeffectsthechoiceoftheseedhasonthepropertiesofthegeneratedseries.

• Describesituationswherethebootstrappingmethodisineffective.

• Describethedisadvantagesofthesimulationapproachtofinancialproblemsolving.

!

!

2019 2020

John C. Hull, Risk Management and Financial Institutions, 4th edition

(Hoboken, New Jersey: John Wiley & Sons, 2015). Chapter 2. Banks

John C. Hull, Risk Management and Financial Institutions, 4th edition

(Hoboken, New Jersey: John Wiley & Sons, 2015). Chapter 2. Banks

FMP-1 FMP-1

• Identifythemajorrisksfacedbyabank.

• Evaluatethecapitalrequirementsforbanks.

• Distinguishbetweeneconomiccapitalandregulatorycapital.

• Explainhowdepositinsurancegivesrisetoamoralhazardproblem.

• Describeinvestmentbankingfinancingarrangementsincludingprivateplacement,publicoffering,bestefforts,firmcommitment,andDutchauctionapproaches.

• Describethepotentialconflictsofinterestamongcommercialbanking,securitiesservices,andinvestmentbankingdivisionsofabankandrecommendsolutionstotheconflictofinterestproblems.”

• Describethedistinctionsbetweenthe“bankingbook”andthe“tradingbook”ofabank.

• Explaintheoriginate-to-distributemodelofabankanddiscussitsbenefitsanddrawbacks.

• NEW:Identifythemajorrisksfacedbyabank,andexplainwaysinwhichtheseriskscanarise.

• Distinguishbetweeneconomiccapitalandregulatorycapital.

• NEW:SummarizeBaselCommitteeregulationsforregulatorycapitalandtheirmotivations.

• Explainhowdepositinsurancegivesrisetoamoralhazardproblem.

• NEW:Describeinvestmentbankingfinancingarrangementsincludingprivateplacement,publicoffering,bestefforts,firmcommitment,andDutchauctionapproaches.

• NEW:Describethepotentialconflictsofinterestamongcommercialbanking,securitiesservices,andinvestmentbankingdivisionsofabankandrecommendsolutionstotheconflictofinterestproblems.

• Describethedistinctionsbetweenthe“bankingbook”andthe“tradingbook”ofabank.

• Explaintheoriginate-to-distributemodelofabankanddiscussitsbenefitsanddrawbacks.

!

!

!

!

2019 2020

John C. Hull, Risk Management and Financial Institutions, 4th edition

(Hoboken, New Jersey: John Wiley & Sons, 2015). Chapter 3. Insurance Companies and Pension Plans

John C. Hull, Risk Management and Financial Institutions, 4th edition

(Hoboken, New Jersey: John Wiley & Sons, 2015). Chapter 3. Insurance Companies and Pension Plans

FMP-2 FMP-2

• Describethekeyfeaturesofthevariouscategoriesofinsurancecompaniesandidentifytherisksfacinginsurancecompanies.

• Describetheuseofmortalitytableandcalculatepremiumpaymentforapolicyholder.

• Calculateandinterpretlossratio,expenseratio,combinedratio,andoperatingratioforaproperty-casualtyinsurancecompany.

• Describemoralhazardandadverseselectionrisksfacinginsurancecompanies,provideexamplesofeach,anddescribehowtoovercometheproblems.

• Distinguishbetweenmortalityriskandlongevityriskanddescribehowtohedgetheserisks.

• Evaluatethecapitalrequirementsforlifeinsuranceandproperty-casualtyinsurancecompanies.

• Comparetheguarantysystemandtheregulatoryrequirementsforinsurancecompanieswiththoseforbanks.

• Describeadefinedbenefitplanandadefinedcontributionplanforapensionfundandexplainthedifferencesbetweenthem.

• Describethekeyfeaturesofthevariouscategoriesofinsurancecompaniesandidentifytherisksfacinginsurancecompanies.

• Describetheuseofmortalitytablesandcalculatethepremiumpaymentforapolicyholder.

• Distinguishbetweenmortalityriskandlongevityriskanddescribehowtohedgetheserisks

• Describeadefinedbenefitplanandadefinedcontributionplanforapensionfundandexplainthedifferencesbetweenthem.

• NEW:Calculateandinterpretlossratio,expenseratio,combinedratio,andoperatingratioforaproperty-casualtyinsurancecompany.

• NEW:Describemoralhazardandadverseselectionrisksfacinginsurancecompanies,provideexamplesofeach,anddescribehowtoovercometheproblems.

• Evaluatethecapitalrequirementsforlifeinsuranceandproperty-casualtyinsurancecompanies.

• Comparetheguarantysystemandtheregulatoryrequirementsforinsurancecompanieswiththoseforbanks.

!

!

2019 2020

John C. Hull, Risk Management and Financial Institutions, 4th edition

(Hoboken, New Jersey: John Wiley & Sons, 2015). Chapter 4. Mutual Funds and Hedge Funds

John C. Hull, Risk Management and Financial Institutions, 4th edition

(Hoboken, New Jersey: John Wiley & Sons, 2015). Chapter 4. Mutual Funds and Hedge Funds

FMP-3 FMP-3

• Differentiateamongopen-endmutualfunds,closed-endmutualfunds,andexchange-tradedfunds(ETFs).

• Calculatethenetassetvalue(NAV)ofanopen-endmutualfund.

• Distinguishbetweenactiveandpassivemanagementanddefinealpha.

• Explainthekeydifferencesbetweenhedgefundsandmutualfunds.

• Calculatethereturnonahedgefundinvestmentandexplaintheincentivefeestructureofahedgefundincludingthetermshurdlerate,high-watermark,andclawback.

• Describevarioushedgefundstrategies,includinglong/shortequity,dedicatedshort,distressedsecurities,mergerarbitrage,convertiblearbitrage,fixedincomearbitrage,emergingmarkets,globalmacro,andmanagedfutures,andidentifytherisksfacedbyhedgefunds.

• Describehedgefundperformanceandexplaintheeffectofmeasurementbiasesonperformancemeasurement.

• Differentiateamongopen-endmutualfunds,closed-endmutualfunds,andexchange-tradedfunds(ETFs).

• NEW:Identifyanddescribepotentialundesirabletradingbehaviorsatmutualfunds.

• Calculatethenetassetvalue(NAV)ofanopen-endmutualfund.

• Explainthekeydifferencesbetweenhedgefundsandmutualfunds.

• Calculatethereturnonahedgefundinvestmentandexplaintheincentivefeestructureofahedgefundincludingthetermshurdlerate,high-watermark,andclawback.

• Describevarioushedgefundstrategies,includinglong/shortequity,dedicatedshort,distressedsecurities,mergerarbitrage,convertiblearbitrage,fixedincomearbitrage,emergingmarkets,globalmacro,andmanagedfutures,andidentifytherisksfacedbyhedgefunds.

• NEW:Describecharacteristicsofmutualfundandhedgefundperformanceandexplaintheeffectofmeasurementbiasesonperformancemeasurement.

!

!

2019 2020

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 1. Introduction

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 1. Introduction

FMP-4 FMP-4

• NEW:Definederivatives,describefeaturesandusesofderivatives,andcomparelinearandnon-linearderivatives.

• NEW:Describetheover-the-countermarket,distinguishitfromtradingonanexchange,andevaluateitsadvantagesanddisadvantages.

• Differentiatebetweenoptions,forwards,andfuturescontracts.

• Identifyandcalculateoptionandforwardcontractpayoffs.

• Differentiateamongthebroadcategoriesoftraders:hedgers,speculators,andarbitrageurs.

• Calculateandcomparethepayoffsfromhedgingstrategiesinvolvingforwardcontractsandoptions.

• Calculateandcomparethepayoffsfromspeculativestrategiesinvolvingfuturesandoptions.

• Calculateanarbitragepayoffanddescribehowarbitrageopportunitiesaretemporary.

• Describesomeoftherisksthatcanarisefromtheuseofderivatives.

• Describetheover-the-countermarket,distinguishitfromtradingonanexchange,andevaluateitsadvantagesanddisadvantages.

• Differentiatebetweenoptions,forwards,andfuturescontracts.

• Identifyandcalculateoptionandforwardcontractpayoffs.

• Calculateandcomparethepayoffsfromhedgingstrategiesinvolvingforwardcontractsandoptions.

• Calculateandcomparethepayoffsfromspeculativestrategiesinvolvingfuturesandoptions.

• Calculateanarbitragepayoffanddescribehowarbitrageopportunitiesaretemporary.

• Describesomeoftherisksthatcanarisefromtheuseofderivatives.

• Differentiateamongthebroadcategoriesoftraders:hedgers,speculators,andarbitrageurs.

!

!

2019 2020

!!

!

!

!

!

Jon Gregory, Central Counterparties: Mandatory Clearing and Bilateral Margin Requirements for OTC Derivatives

(West Sussex, UK: John Wiley & Sons, 2014). Chapter 2. Exchanges, OTC Derivatives, DPCs and SPVs

John Hull, Options, Futures, and Other Derivatives, 9th Edition

(New York: Pearson, 2014). Chapter 2. Mechanics of Futures Markets

FMP-5 FMP-5

• Describehowexchangescanbeusedtoalleviatecounterpartyrisk.

• Explainthedevelopmentsinclearingthatreducerisk.

• NEW:Describenettinganddescribeanettingprocess.

• NEW:Describetheimplementationofamarginingprocessandexplainthedeterminantsofinitialandvariationmarginrequirements.

• NEW:Compareexchange-tradedandOTCmarketsanddescribetheiruses.

• NEW:Identifytheclassesofderivativesecuritiesandexplaintheriskassociatedwiththem.

• IdentifyrisksassociatedwithOTCmarketsandexplainhowtheseriskscanbemitigated.

• NEW:Describetheroleofcollateralizationintheover-the-countermarketandcompareittothemarginingsystem.

• NEW:Explaintheuseofspecialpurposevehicles(SPVs)intheOTCderivativesmarket.

• Defineanddescribethekeyfeaturesofafuturescontract,includingtheasset,thecontractpriceandsize,delivery,andlimits.

• Explaintheconvergenceoffuturesandspotprices.

• Describetherationaleformarginrequirementsandexplainhowtheywork.

• Describetheroleofaclearinghouseinfuturesandover-the-countermarkettransactions.

• Describetheroleofcentralcounterparties(CCPs)anddistinguishbetweenbilateralandcentralizedclearing.

• Describetheroleofcollateralizationintheover-the-countermarketandcompareittothemarginingsystem.

• Identifythedifferencesbetweenanormalandinvertedfuturesmarket.

• Describethemechanicsofthedeliveryprocessandcontrastitwithcashsettlement.

• Explainthedifferentmarketquotes.

• Evaluatetheimpactofdifferenttradingordertypes.

• Compareandcontrastforwardandfuturescontracts.

2019 2020

Jon Gregory, Central Counterparties: Mandatory Clearing and Bilateral Margin Requirements for OTC Derivatives

(West Sussex, UK: John Wiley & Sons, 2014). Chapter 3. Basic Principles of Central Clearing

Chapter 14. Risks Caused by CCPs: Risks Faced by CCPs

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 4. Interest Rates

FMP-6 FMP-6

• Defineanddifferentiatebetweenshortandlonghedgesandidentifytheirappropriateuses.

• Describetheargumentsforandagainsthedgingandthepotentialimpactofhedgingonfirmprofitability.

• Definethebasisandexplainthevarioussourcesofbasisrisk,andexplainhowbasisrisksarisewhenhedgingwithfutures.

• Definecrosshedging,andcomputeandinterprettheminimumvariancehedgeratioandhedgeeffectiveness.

• Computetheoptimalnumberoffuturescontractsneededtohedgeanexposure,andexplainandcalculatethe“tailingthehedge”adjustment.

• Explainhowtousestockindexfuturescontractstochangeastockportfolio’sbeta.

• Explaintheterm“rollingthehedgeforward”anddescribesomeoftherisksthatarisefromthisstrategy.

• Provideexamplesofthemechanicsofacentralcounterparty(CCP).

• NEW:DescribetheroleofCCPsanddistinguishbetweenbilateralandcentralizedclearing.

• DescribeadvantagesanddisadvantagesofcentralclearingofOTCderivatives.

• NEW:ExplainregulatoryinitiativesfortheOTCderivativesmarketandtheirimpactoncentralclearing.

• Comparemarginrequirementsincentrallyclearedandbilateralmarkets,andexplainhowmargincanmitigaterisk.

• Compareandcontrastbilateralmarketstotheuseofnovationandnetting.

• Assesstheimpactofcentralclearingonthebroaderfinancialmarkets.

• IdentifyandexplainthetypesofrisksfacedbyCCPs.

• NEW:Identifyanddistinguishbetweentheriskstoclearingmembersaswellasnon-members.

!

!

!

2019 2020

John C. Hull, Risk Management and Financial Institutions, 4th edition

(Hoboken, New Jersey: John Wiley & Sons, 2015). Chapter 2. Banks

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 4. Interest Rates

FMP-7 FMP-7

• DescribeTreasuryrates,LIBOR,andreporates,andexplainwhatismeantbythe“risk-free”rate.

• Calculatethevalueofaninvestmentusingdifferentcompoundingfrequencies.

• Convertinterestratesbasedondifferentcompoundingfrequencies.

• Calculatethetheoreticalpriceofabondusingspotrates.

• Deriveforwardinterestratesfromasetofspotrates.

• Derivethevalueofthecashflowsfromaforwardrateagreement(FRA).

• Calculatetheduration,modifieddurationanddollardurationofabond.

• Evaluatethelimitationsofdurationandexplainhowconvexityaddressessomeofthem.

• Calculatethechangeinabond’spricegivenitsduration,itsconvexity,andachangeininterestrates.

• Compareandcontrastthemajortheoriesofthetermstructureofinterestrates.

• NEW:Defineanddescribethekeyfeaturesofafuturescontract,includingtheunderlyingasset,thecontractpriceandsize,tradingvolume,openinterest,delivery,andlimits.

• Explaintheconvergenceoffuturesandspotprices.

• Describetherationaleformarginrequirementsandexplainhowtheywork.

• NEW:Describetheroleofanexchangeinfuturesandover-the-countermarkettransactions.

• Identifythedifferencesbetweenanormalandinvertedfuturesmarket.

• Explainthedifferentmarketquotes.

• Describethemechanicsofthedeliveryprocessandcontrastitwithcashsettlement.

• Evaluatetheimpactofdifferenttradingordertypes.

• NEW:Describetheapplicationofmarkingtomarketandhedgeaccountingforfutures.

• Compareandcontrastforwardandfuturescontracts.

!

!

!

2019 2020

John C. Hull, Risk Management and Financial Institutions, 4th edition

(Hoboken, New Jersey: John Wiley & Sons, 2015). Chapter 3. Insurance Companies and Pension Plans

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 5. Determination of Forward and Futures Prices

FMP-8 FMP-8

• Differentiatebetweeninvestmentandconsumptionassets.• Defineshort-sellingandcalculatethenetprofitofashortsaleofa

dividend-payingstock.• Describethedifferencesbetweenforwardandfuturescontractsand

explaintherelationshipbetweenforwardandspotprices.• Calculatetheforwardpricegiventheunderlyingasset’sspotprice,

anddescribeanarbitrageargumentbetweenspotandforwardprices.

• Explaintherelationshipbetweenforwardandfuturesprices.• Calculateaforwardforeignexchangerateusingtheinterestrate

parityrelationship.• Defineincome,storagecosts,andconvenienceyield.• Calculatethefuturespriceoncommoditiesincorporatingincome/

storagecostsand/orconvenienceyields.• Calculate,usingthecost-of-carrymodel,forwardpriceswherethe

underlyingasseteitherdoesordoesnothaveinterimcashflows.• Describethevariousdeliveryoptionsavailableinthefuturesmarkets

andhowtheycaninfluencefuturesprices.• Explaintherelationshipbetweencurrentfuturespricesand

expectedfuturespotprices,includingtheimpactofsystematicandnonsystematicrisk.

• Defineandinterpretcontangoandbackwardation,andexplainhowtheyrelatetothecost-of-carrymodel.

• Defineanddifferentiatebetweenshortandlonghedgesandidentifytheirappropriateuses.

• Describetheargumentsforandagainsthedgingandthepotentialimpactofhedgingonfirmprofitability.

• Definethebasisandexplainthevarioussourcesofbasisrisk,andexplainhowbasisrisksarisewhenhedgingwithfutures.

• Definecrosshedging,andcomputeandinterprettheminimumvariancehedgeratioandhedgeeffectiveness.

• Computetheoptimalnumberoffuturescontractsneededtohedgeanexposure,andexplainandcalculatethe“tailingthehedge”adjustment.

• Explainhowtousestockindexfuturescontractstochangeastockportfolio’sbeta.

• NEW:Explainhowtocreatealong-termhedgeusinga“stackandroll”strategyanddescribesomeoftherisksthatarisefromthisstrategy.

!

2019 2020

Anthony Saunders and Marcia Millon Cornett, Financial Institutions Management:

A Risk Management Approach, 8th Edition (New York: McGraw-Hill, 2014).

Chapter 13. Foreign Exchange Risk

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 6. Interest Rate Futures

FMP-9 FMP-9

• Identifythemostcommonlyuseddaycountconventions,describethemarketsthateachoneistypicallyusedin,andapplyeachtoaninterestcalculation.

• CalculatetheconversionofadiscountratetoapriceforaUSTreasurybill.

• DifferentiatebetweenthecleananddirtypriceforaUSTreasurybond;calculatetheaccruedinterestanddirtypriceonaUSTreasurybond.

• ExplainandcalculateaUSTreasurybondfuturescontractconversionfactor.

• CalculatethecostofdeliveringabondintoaTreasurybondfuturescontract.

• Describetheimpactofthelevelandshapeoftheyieldcurveonthecheapest-to-deliverTreasurybonddecision.

• CalculatethetheoreticalfuturespriceforaTreasurybondfuturescontract.

• CalculatethefinalcontractpriceonaEurodollarfuturescontract.

• DescribeandcomputetheEurodollarfuturescontractconvexityadjustment.

• ExplainhowEurodollarfuturescanbeusedtoextendtheLIBORzerocurve.

• Calculatetheduration-basedhedgeratioandcreateaduration-basedhedgingstrategyusinginterestratefutures.

• Explainthelimitationsofusingaduration-basedhedgingstrategy.

• NEW:Explainanddescribethemechanicsofspotquotes,forwardquotes,andfuturesquotesintheforeignexchangemarkets,anddistinguishbetweenbidandaskexchangerates.

• NEW:Calculatebid-askspreadandexplainwhythebid-askspreadforspotquotesmaybedifferentfromthebid-askspreadforforwardquotes.

• NEW:Compareoutright(forward)andswaptransactions.

• NEW:Define,compare,andcontrasttransactionrisk,translationrisk,andeconomicrisk.

• NEW:Describeexamplesoftransaction,translation,andeconomicrisks,andexplainhowtohedgetheserisks.

• NEW:Describetherationaleformulti-currencyhedgingusingoptions.

• NEW:Identifyandexplainthefactorsthatdetermineexchangerates.

• Calculateandexplaintheeffectofanappreciation/depreciationofacurrencyrelativetoaforeigncurrency.

• Explainthepurchasingpowerparitytheoremandusethistheoremtocalculatetheappreciationordepreciationofaforeigncurrency.

• Describetherelationshipbetweennominalandrealinterestrates.

• Describehowanon-arbitrageassumptionintheforeignexchangemarketsleadstotheinterestrateparitytheorem,andusethistheoremtocalculateforwardforeignexchangerates.

• NEW:Distinguishbetweencoveredanduncoveredinterestrateparityconditions.

!

!

!

!

!

!

!

!

2019 2020

New Edition: John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 5. Determination of Forward and Futures Prices

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 7. Swaps

FMP-10 FMP-10

• Explainthemechanicsofaplainvanillainterestrateswapandcomputeitscashflows.

• Explainhowaplainvanillainterestrateswapcanbeusedtotransformanassetoraliabilityandcalculatetheresultingcashflows.

• Explaintheroleoffinancialintermediariesintheswapsmarket.• Describetheroleoftheconfirmationinaswaptransaction.• Describethecomparativeadvantageargumentfortheexistence

ofinterestrateswapsandevaluatesomeofthecriticismsofthisargument.

• Explainhowthediscountratesinaplainvanillainterestrateswaparecomputed.

• Calculatethevalueofaplainvanillainterestrateswapbasedontwosimultaneousbondpositions.

• Calculatethevalueofaplainvanillainterestrateswapfromasequenceofforwardrateagreements(FRAs).

• Explainthemechanicsofacurrencyswapandcomputeitscashflows.

• Explainhowacurrencyswapcanbeusedtotransformanassetorliabilityandcalculatetheresultingcashflows.

• Calculatethevalueofacurrencyswapbasedontwosimultaneousbondpositions.

• CalculatethevalueofacurrencyswapbasedonasequenceofFRAs.• Describethecreditriskexposureinaswapposition.• Identifyanddescribeothertypesofswaps,includingcommodity,

volatilityandexoticswaps.

• Differentiatebetweeninvestmentandconsumptionassets.• NEW:Defineshort-sellingandcalculatethenetprofitofashortsale

ofadividend-payingstock.• Describethedifferencesbetweenforwardandfuturescontractsand

explaintherelationshipbetweenforwardandspotprices.• Calculatetheforwardpricegiventheunderlyingasset’sspotprice,

anddescribeanarbitrageargumentbetweenspotandforwardprices.

• NEW:Distinguishbetweentheforwardpriceandthevalueofaforwardcontract.

• NEW:Calculatethevalueofaforwardcontractonafinancialassetthatdoesordoesnotprovideincomeoryield.

• Explaintherelationshipbetweenforwardandfuturesprices.• Calculateaforwardforeignexchangerateusingtheinterestrate

parityrelationship.• NEW:Calculatethevalueofastockindexfuturescontractand

explaintheconceptofindexarbitrage.

!

!

!

!

2019 2020

Robert McDonald, Derivatives Markets, 3rd Ed. Chapter 6. Commodity Forwards and Futures

John C. Hull, Options, Futures, and Other Derivatives, 10th Ed.Chapter 5. Determination of Forward and Futures Prices

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 10. Mechanics of Options Markets

FMP-11 FMP-11

• Describethetypes,positionvariations,andtypicalunderlyingassetsofoptions.

• Explainthespecificationofexchange-tradedstockoptioncontracts,includingthatofnonstandardproducts.

• Describehowtrading,commissions,marginrequirements,andexercisetypicallyworkforexchange-tradedoptions.

• NEW:Explainthekeydifferencesbetweencommoditiesandfinancialassets.

• NEW:Defineandapplycommodityconceptssuchasstoragecosts,carrymarkets,leaserate,andconvenienceyield.

• NEW:Identifyfactorsthatimpactpricesonagriculturalcommodities,metals,energy,andweatherderivatives.

• Explainthebasicequilibriumformulaforpricingcommodityforwards.

• Describeanarbitragetransactionincommodityforwards,andcomputethepotentialarbitrageprofit.

• NEW:Definetheleaserateandexplainhowitdeterminestheno-arbitragevaluesforcommodityforwardsandfutures.

• NEW:Describethecostofcarrymodelandillustratetheimpactofstoragecostsandconvenienceyieldsoncommodityforwardpricesandno-arbitragebounds.

• Computetheforwardpriceofacommoditywithstoragecosts.

• Comparetheleaseratewiththeconvenienceyield.

• Explainhowtocreateasyntheticcommodityposition,anduseittoexplaintherelationshipbetweentheforwardpriceandtheexpectedfuturespotprice.

• Explaintherelationshipbetweencurrentfuturespricesandexpectedfuturespotprices,includingtheimpactofsystematicandnonsystematicrisk.

• NEW:Defineandinterpretnormalbackwardationandcontango.

!

!

!

!

!

!

2019 2020

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 11. Properties of Stock Options

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 11. Properties of Stock Options

FMP-12 FMP-12

• Identifythesixfactorsthataffectanoption’spriceanddescribehowthesesixfactorsaffectthepriceforbothEuropeanandAmericanoptions.

• Identifyandcomputeupperandlowerboundsforoptionpricesonnon-dividendanddividendpayingstocks.

• Explainput-callparityandapplyittothevaluationofEuropeanandAmericanstockoptions.

• ExplaintheearlyexercisefeaturesofAmericancallandputoptions.

• NEW:Describethetypes,positionvariations,payoffsandprofits,andtypicalunderlyingassetsofoptions.

• NEW:Explainthespecificationofexchange-tradedstockoptioncontracts,includingthatofnonstandardproducts.

• NEW:Explainhowdividendsandstocksplitscanimpactthetermsofastockoption.

• NEW:Describehowtrading,commissions,marginrequirements,andexercisetypicallyworkforexchange-tradedoptions.

• NEW:Defineanddescribewarrants,convertiblebonds,andemployeestockoptions.

!

!

!

!

!

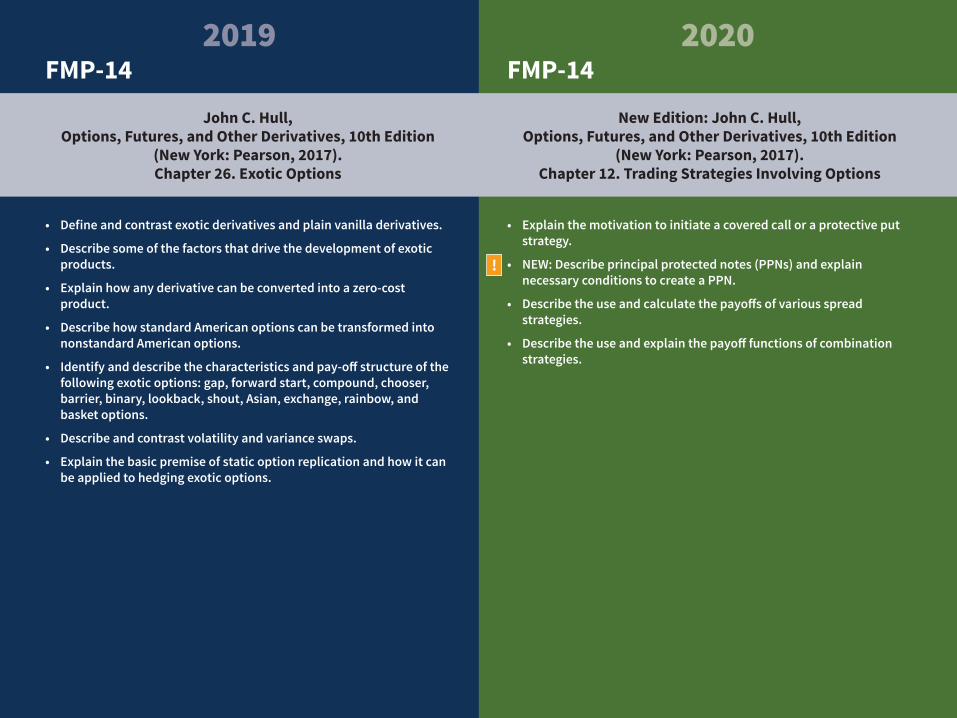

2019 2020

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 12. Trading Strategies Involving Options

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 12. Trading Strategies Involving Options

FMP-13 FMP-13

• Explainthemotivationtoinitiateacoveredcalloraprotectiveputstrategy.

• Describetheuseandcalculatethepayoffsofvariousspreadstrategies.

• Describetheuseandexplainthepayofffunctionsofcombinationstrategies.

• NEW:Identifythesixfactorsthataffectanoption’sprice.

• NEW:Identifyandcomputeupperandlowerboundsforoptionpricesonnon-dividendanddividendpayingstocks.

• NEW:Explainput-callparityandapplyittothevaluationofEuropeanandAmericanstockoptions,withdividendsandwithoutdividends,andexpressitintermsofforwardprices.

• NEW:ExplainandassesspotentialrationalesforusingtheearlyexercisefeaturesofAmericancallandputoptions.

!!

!

!

2019 2020

New Edition: John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 12. Trading Strategies Involving Options

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 26. Exotic Options

FMP-14 FMP-14

• Defineandcontrastexoticderivativesandplainvanilladerivatives.

• Describesomeofthefactorsthatdrivethedevelopmentofexoticproducts.

• Explainhowanyderivativecanbeconvertedintoazero-costproduct.

• DescribehowstandardAmericanoptionscanbetransformedintononstandardAmericanoptions.

• Identifyanddescribethecharacteristicsandpay-offstructureofthefollowingexoticoptions:gap,forwardstart,compound,chooser,barrier,binary,lookback,shout,Asian,exchange,rainbow,andbasketoptions.

• Describeandcontrastvolatilityandvarianceswaps.

• Explainthebasicpremiseofstaticoptionreplicationandhowitcanbeappliedtohedgingexoticoptions.

• Explainthemotivationtoinitiateacoveredcalloraprotectiveputstrategy.

• NEW:Describeprincipalprotectednotes(PPNs)andexplainnecessaryconditionstocreateaPPN.

• Describetheuseandcalculatethepayoffsofvariousspreadstrategies.

• Describetheuseandexplainthepayofffunctionsofcombinationstrategies.

!

2019 2020

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 26. Exotic Options

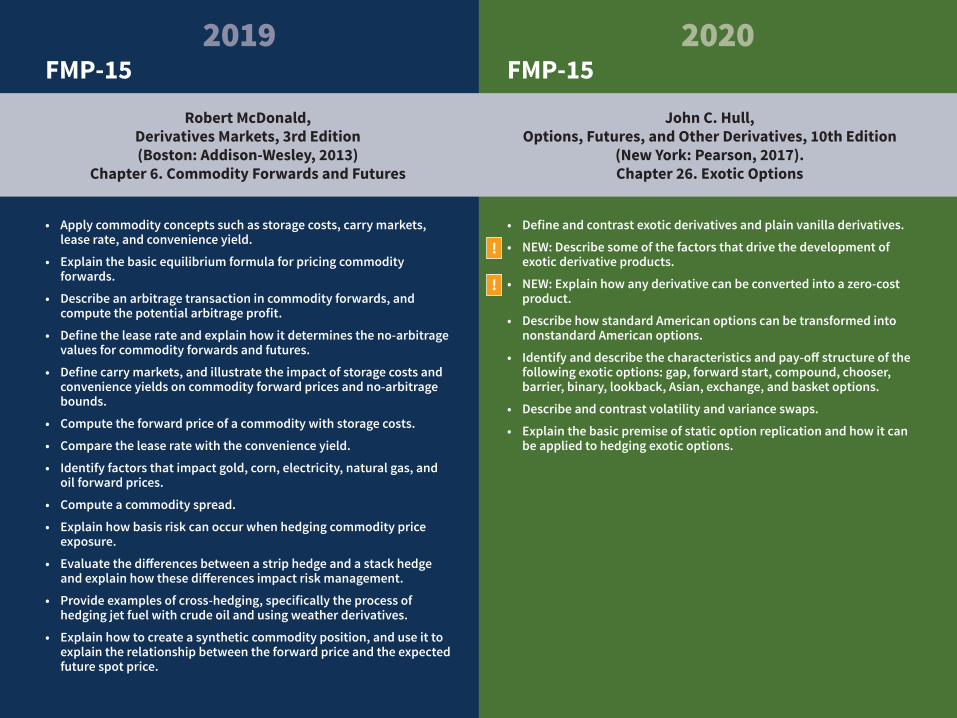

Robert McDonald, Derivatives Markets, 3rd Edition (Boston: Addison-Wesley, 2013)

Chapter 6. Commodity Forwards and Futures

FMP-15 FMP-15

• Applycommodityconceptssuchasstoragecosts,carrymarkets,leaserate,andconvenienceyield.

• Explainthebasicequilibriumformulaforpricingcommodityforwards.

• Describeanarbitragetransactionincommodityforwards,andcomputethepotentialarbitrageprofit.

• Definetheleaserateandexplainhowitdeterminestheno-arbitragevaluesforcommodityforwardsandfutures.

• Definecarrymarkets,andillustratetheimpactofstoragecostsandconvenienceyieldsoncommodityforwardpricesandno-arbitragebounds.

• Computetheforwardpriceofacommoditywithstoragecosts.

• Comparetheleaseratewiththeconvenienceyield.

• Identifyfactorsthatimpactgold,corn,electricity,naturalgas,andoilforwardprices.

• Computeacommodityspread.

• Explainhowbasisriskcanoccurwhenhedgingcommoditypriceexposure.

• Evaluatethedifferencesbetweenastriphedgeandastackhedgeandexplainhowthesedifferencesimpactriskmanagement.

• Provideexamplesofcross-hedging,specificallytheprocessofhedgingjetfuelwithcrudeoilandusingweatherderivatives.

• Explainhowtocreateasyntheticcommodityposition,anduseittoexplaintherelationshipbetweentheforwardpriceandtheexpectedfuturespotprice.

• Defineandcontrastexoticderivativesandplainvanilladerivatives.

• NEW:Describesomeofthefactorsthatdrivethedevelopmentofexoticderivativeproducts.

• NEW:Explainhowanyderivativecanbeconvertedintoazero-costproduct.

• DescribehowstandardAmericanoptionscanbetransformedintononstandardAmericanoptions.

• Identifyanddescribethecharacteristicsandpay-offstructureofthefollowingexoticoptions:gap,forwardstart,compound,chooser,barrier,binary,lookback,Asian,exchange,andbasketoptions.

• Describeandcontrastvolatilityandvarianceswaps.

• Explainthebasicpremiseofstaticoptionreplicationandhowitcanbeappliedtohedgingexoticoptions.

!

!

2019 2020

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 4. Interest Rates

Jon Gregory, Central Counterparties: Mandatory Clearing and Bilateral Margin Requirements for OTC Derivatives

(West Sussex, UK: John Wiley & Sons, 2014). Chapter 2. Exchanges, OTC Derivatives, DPCs and SPVs

FMP-16 FMP-16

• Describehowexchangescanbeusedtoalleviatecounterpartyrisk.• Explainthedevelopmentsinclearingthatreducerisk.• Compareexchange-tradedandOTCmarketsanddescribetheiruses.• Identifytheclassesofderivativessecuritiesandexplaintherisk

associatedwiththem.• IdentifyrisksassociatedwithOTCmarketsandexplainhowthese

riskscanbemitigated.

• NEW:DescribeTreasuryrates,LIBOR,SecuredOvernightFinancingRate(SOFR),andreporatesandexplainwhatismeantbythe“risk-free”rate.

• Calculatethevalueofaninvestmentusingdifferentcompoundingfrequencies.

• Convertinterestratesbasedondifferentcompoundingfrequencies.

• Calculatethetheoreticalpriceofabondusingspotrates.

• NEW:Calculatetheduration,modifiedduration,anddollardurationofabond.

• Evaluatethelimitationsofdurationandexplainhowconvexityaddressessomeofthem.

• Calculatethechangeinabond’spricegivenitsduration,itsconvexity,andachangeininterestrates.

• Deriveforwardinterestratesfromasetofspotrates.

• Derivethevalueofthecashflowsfromaforwardrateagreement(FRA).

• NEW:Calculatezero-couponratesusingthebootstrapmethod.

• NEW:Compareandcontrastthemajortheoriesofthetermstructureofinterestrates.

!

!

!!

2019 2020

Frank Fabozzi (editor), Steve Mann, and Adam Cohen, The Handbook of Fixed Income Securities, 8th Edition

(New York: McGraw-Hill, 2012). Chapter 12. Corporate Bonds

Jon Gregory, Central Counterparties: Mandatory Clearing and Bilateral Margin Requirements for OTC Derivatives

(West Sussex, UK: John Wiley & Sons, 2014). Chapter 3. Basic Principles of Central Clearing

FMP-17 FMP-17

• Provideexamplesofthemechanicsofacentralcounterparty(CCP).• DescribeadvantagesanddisadvantagesofcentralclearingofOTC

derivatives.• Comparemarginrequirementsincentrallyclearedandbilateral

markets,andexplainhowmargincanmitigaterisk.• Compareandcontrastbilateralmarketstotheuseofnovationand

netting.• Assesstheimpactofcentralclearingonthebroaderfinancial

markets.

• NEW:Describefeaturesofbondtrading,andexplainthebehaviorofbondyield.

• Describeabondindentureandexplaintheroleofthecorporatetrusteeinabondindenture.

• NEW:Definehigh-yieldbonds,anddescribetypesofhigh-yieldbondissuersandsomeofthepaymentfeaturesuniquetohighyieldbonds.

• Differentiatebetweencreditdefaultriskandcreditspreadrisk.

• Describeeventriskandexplainwhatmaycauseitincorporatebonds.

• NEW:Describethedifferentclassificationsofbondscharacterizedbyissuer,maturity,interestrate,andcollateral.

• Describethemechanismsbywhichcorporatebondscanberetiredbeforematurity.

• NEW:Definerecoveryrateanddefaultrate,differentiatebetweenanissuedefaultrateandadollardefaultrate,anddescribetherelationshipbetweenrecoveryratesandseniority.

• Evaluatetheexpectedreturnfromabondinvestmentandidentifythecomponentsofthebond’sexpectedreturn.

!

!

!

!

2019 2020

Bruce Tuckman, Angel Serrat, Fixed Income Securities: Tools for Today’s Markets, 3rd Edition

(Hoboken, NJ: John Wiley & Sons, 2011). Chapter 20. Mortgages and Mortgage-Backed Securities

Jon Gregory, Central Counterparties: Mandatory Clearing and Bilateral Margin Requirements for OTC Derivatives

(West Sussex, UK: John Wiley & Sons, 2014). Chapter 14 (section 14.4 only).

Risks Caused by CCPs: Risks Faced by CCPs

FMP-18 FMP-18

• IdentifyandexplainthetypesofrisksfacedbyCCPs.

• Identifyanddistinguishbetweentheriskstoclearingmembersaswellasnon-members.

• IdentifyandevaluatelessonslearnedfrompriorCCPfailures.

• Describethevarioustypesofresidentialmortgageproducts.

• Calculateafixedratemortgagepayment,anditsprincipalandinterestcomponents.

• Describethemortgageprepaymentoptionandthefactorsthatinfluenceprepayments.

• NEW:Summarizethesecuritizationprocessofmortgagebackedsecurities(MBS),particularlyformationofmortgagepoolsincludingspecificpoolsandto-be-announceds(TBAs).

• NEW:Calculateweightedaveragecoupon,weightedaveragematurity,singlemonthlymortalityrate(SMM),andconditionalprepaymentrate(CPR)foramortgagepool.

• NEW:Describetheprocessoftradingofpass-throughagencyMBS.

• NEW:ExplainthemechanicsofdifferenttypesofagencyMBSproducts,includingcollateralizedmortgageobligations(CMOs),interest-onlysecurities(IOs),andprincipal-onlysecurities(POs).

• Describeadollarrolltransactionandhowtovalueadollarroll.

• Explainprepaymentmodelinganditsfourcomponents:refinancing,turnover,defaults,andcurtailments.

• DescribethestepsinvaluinganMBSusingMonteCarlosimulation.

• DefineOptionAdjustedSpread(OAS),andexplainitschallengesanditsuses.

!

!

!!

2019 2020

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 6. Interest Rate Futures

Anthony Saunders and Marcia Millon Cornett, Financial Institutions Management:

A Risk Management Approach, 8th Edition (New York: McGraw-Hill, 2014).

Chapter 13. Foreign Exchange Risk

FMP-19FMP-19

• Identifythemostcommonlyuseddaycountconventions,describethemarketsthateachoneistypicallyusedin,andapplyeachtoaninterestcalculation.

• CalculatetheconversionofadiscountratetoapriceforaUSTreasurybill.

• DifferentiatebetweenthecleananddirtypriceforaUSTreasurybond;calculatetheaccruedinterestanddirtypriceonaUSTreasurybond.

• ExplainandcalculateaUSTreasurybondfuturescontractconversionfactor.

• CalculatethecostofdeliveringabondintoaTreasurybondfuturescontract.

• NEW:Describetheimpactofthelevelandshapeoftheyieldcurveonthecheapest-to-deliverTreasurybonddecision.

• CalculatethetheoreticalfuturespriceforaTreasurybondfuturescontract.

• NEW:CalculatethefinalcontractpriceonaEurodollarfuturescontract,andcompareEurodollarfuturestoFRAs.

• DescribeandcomputetheEurodollarfuturescontractconvexityadjustment.

• ExplainhowEurodollarfuturescanbeusedtoextendtheLIBORzerocurve.

• NEW:Calculatetheduration-basedhedgeratioandcreateaduration-basedhedgingstrategyusinginterestratefutures.

• NEW:Explainthelimitationsofusingaduration-basedhedgingstrategy.

• Calculateafinancialinstitution’soverallforeignexchangeexposure.

• Explainhowafinancialinstitutioncouldalteritsnetpositionexposuretoreduceforeignexchangerisk.

• Calculateandexplaintheeffectofanappreciation/depreciationofacurrencyrelativetoaforeigncurrency.

• Calculateafinancialinstitution’spotentialdollargainorlossexposuretoaparticularcurrency.

• Identifyanddescribethedifferenttypesofforeignexchangetradingactivities.

• Identifythesourcesofforeignexchangetradinggainsandlosses.

• Calculatethepotentialgainorlossfromaforeigncurrencydenominatedinvestment.

• Explainbalance-sheethedgingwithforwards.

• Describehowanon-arbitrageassumptionintheforeignexchangemarketsleadstotheinterestrateparitytheorem,andusethistheoremtocalculateforwardforeignexchangerates.

• Explainthepurchasingpowerparitytheoremandusethistheoremtocalculatetheappreciationordepreciationofaforeigncurrency.

• Explainwhydiversificationinmulticurrencyasset-liabilitypositionscouldreduceportfoliorisk.

• Describetherelationshipbetweennominalandrealinterestrates.

!

!

!

!

2019 2020

John C. Hull, Options, Futures, and Other Derivatives, 10th Edition

(New York: Pearson, 2017). Chapter 7. Swaps

Frank Fabozzi (editor), Steve Mann, and Adam Cohen, The Handbook of Fixed Income Securities, 8th Edition

(New York: McGraw-Hill, 2012). Chapter 12. Corporate Bonds

FMP-20 FMP-20

• Describeabondindentureandexplaintheroleofthecorporatetrusteeinabondindenture.

• Explainabond’smaturitydateandhowitimpactsbondretirements.

• Describethemaintypesofinterestpaymentclassifications.

• Describezero-couponbondsandexplaintherelationshipbetweenoriginal-issuediscountandreinvestmentrisk.

• Distinguishamongthefollowingsecuritytypesrelevantforcorporatebonds:mortgagebonds,collateraltrustbonds,equipmenttrustcertificates,subordinatedandconvertibledebenturebonds,andguaranteedbonds.

• Describethemechanismsbywhichcorporatebondscanberetiredbeforematurity.

• Differentiatebetweencreditdefaultriskandcreditspreadrisk.

• Describeeventriskandexplainwhatmaycauseitincorporatebonds.

• Definehigh-yieldbonds,anddescribetypesofhigh-yieldbondissuersandsomeofthepaymentfeaturesuniquetohighyieldbonds.

• Defineanddifferentiatebetweenanissuerdefaultrateandadollardefaultrate.

• Definerecoveryratesanddescribetherelationshipbetweenrecoveryratesandseniority.

• Explainthemechanicsofaplainvanillainterestrateswapandcomputeitscashflows.

• Explainhowaplainvanillainterestrateswapcanbeusedtotransformanassetoraliabilityandcalculatetheresultingcashflows.

• Explaintheroleoffinancialintermediariesintheswapsmarket.

• Describetheroleoftheconfirmationinaswaptransaction.

• Describethecomparativeadvantageargumentfortheexistenceofinterestrateswapsandevaluatesomeofthecriticismsofthisargument.

• Explainhowthediscountratesinaplainvanillainterestrateswaparecomputed.

• Calculatethevalueofaplainvanillainterestrateswapbasedontwosimultaneousbondpositions.

• Calculatethevalueofaplainvanillainterestrateswapfromasequenceofforwardrateagreements(FRAs).

• Explainthemechanicsofacurrencyswapandcomputeitscashflows.

• Explainhowacurrencyswapcanbeusedtotransformanassetorliabilityandcalculatetheresultingcashflows.

• Calculatethevalueofacurrencyswapbasedontwosimultaneousbondpositions.

• NEW:Calculatethevalueofacurrencyswapbasedonasequenceofforwardexchangerates.

• NEW:Identifyanddescribeothertypesofswaps,includingcommodity,volatility,creditdefault,andexoticswaps.

• Describethecreditriskexposureinaswapposition.

!

!

2019 2020

Kevin Dowd, Measuring Market Risk, 2nd Edition

(West Sussex, England: John Wiley & Sons, 2005).Chapter 2. Measures of Financial Risk

Linda Allen, Jacob Boudoukh and Anthony Saunders, Understanding Market, Credit and Operational Risk:

The Value at Risk Approach (Oxford: Blackwell Publishing, 2004).

Chapter 2. Quantifying Volatility in VaR Models

VRM-1 VRM-1

• Explainhowassetreturndistributionstendtodeviatefromthenormaldistribution.

• Explainreasonsforfattailsinareturndistributionanddescribetheirimplications.

• Distinguishbetweenconditionalandunconditionaldistributions.

• Describetheimplicationsofregimeswitchingonquantifyingvolatility.

• EvaluatethevariousapproachesforestimatingVaR.

• Compareandcontrastdifferentparametricandnon-parametricapproachesforestimatingconditionalvolatility.

• Calculateconditionalvolatilityusingparametricandnon-parametricapproaches.

• Explaintheprocessofreturnaggregationinthecontextofvolatilityforecastingmethods.

• Evaluateimpliedvolatilityasapredictoroffuturevolatilityanditsshortcomings.

• Explainlonghorizonvolatility/VaRandtheprocessofmeanreversionaccordingtoanAR(1)model.

• Calculateconditionalvolatilitywithandwithoutmeanreversion.

• Describetheimpactofmeanreversiononlonghorizonconditionalvolatilityestimation

• NEW:Describethemean-varianceframeworkandtheefficientfrontier.

• NEW:Explainthelimitationsofthemean-varianceframeworkwithrespecttoassumptionsaboutreturndistributions.

• NEW:Comparethenormaldistributionwiththetypicaldistributionofreturnsofriskyfinancialassetssuchasequities.

• NEW:DefinetheVaRmeasureofrisk,describeassumptionsaboutreturndistributionsandholdingperiod,andexplainthelimitationsofVaR.

• ExplainandcalculateExpectedShortfall(ES),andcompareandcontrastVaRandES.

• Definethepropertiesofacoherentriskmeasureandexplainthemeaningofeachproperty.

• ExplainwhyVaRisnotacoherentriskmeasure.

• Describespectralriskmeasures,andexplainhowVaRandESarespecialcasesofspectralriskmeasures.

!

!

!

!

2019 2020

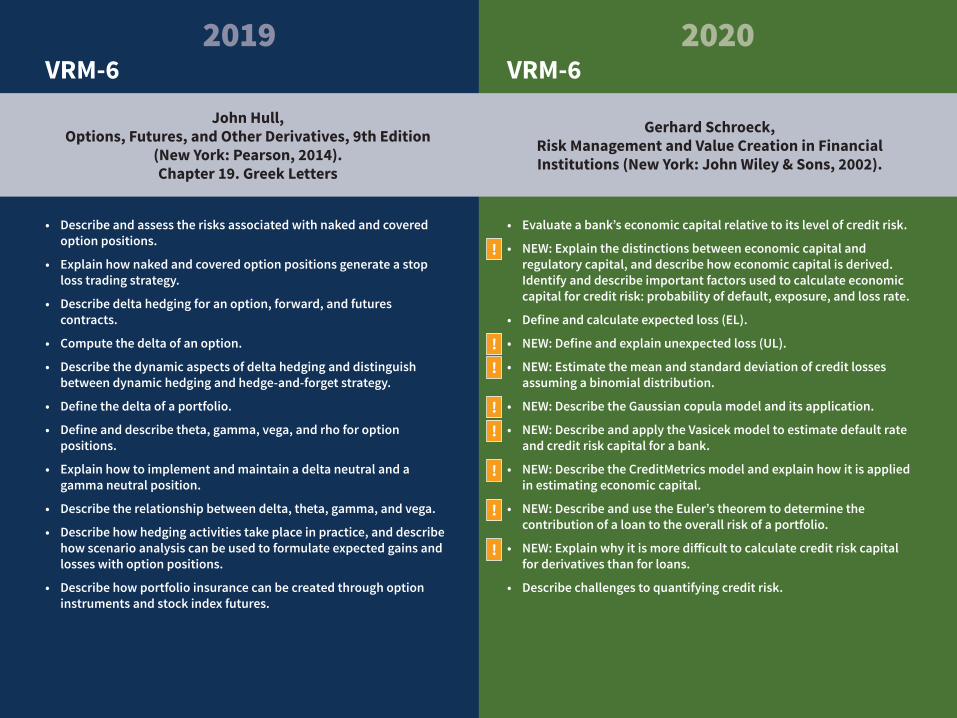

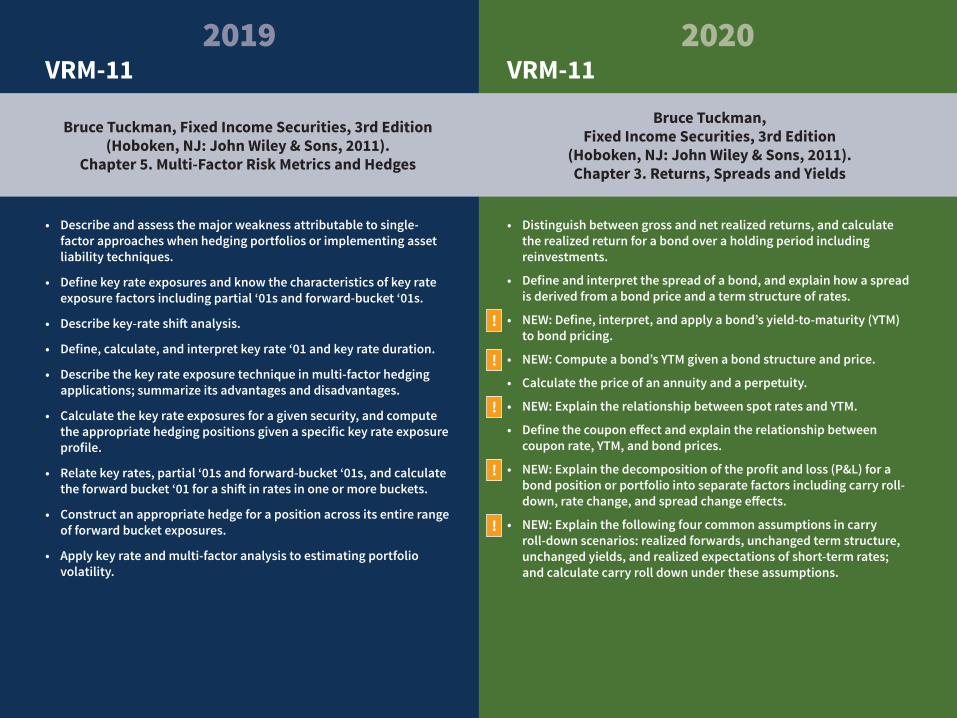

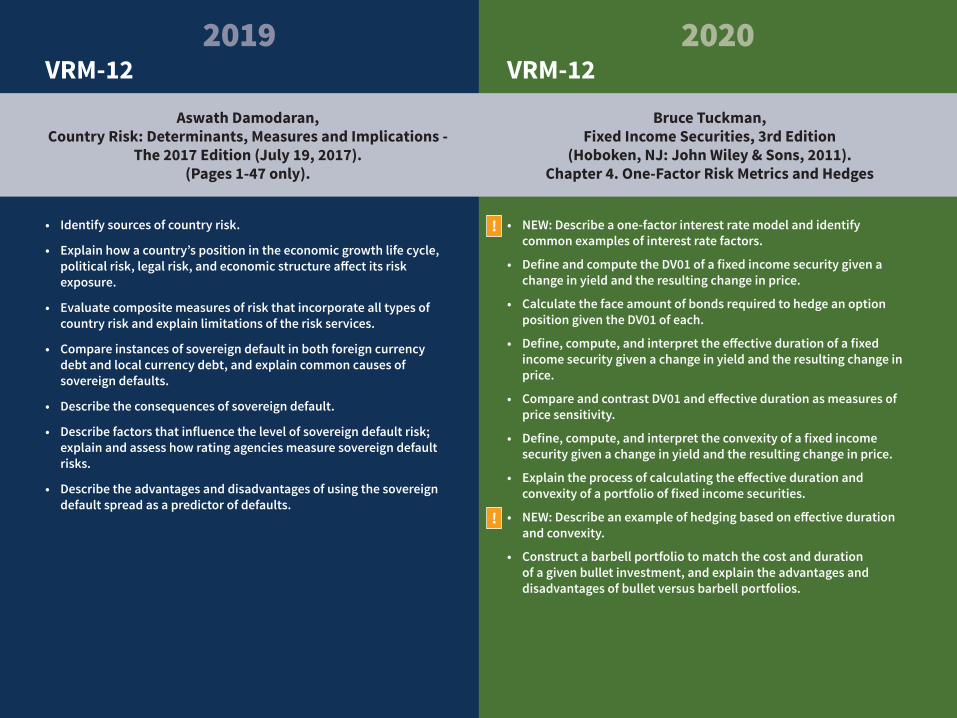

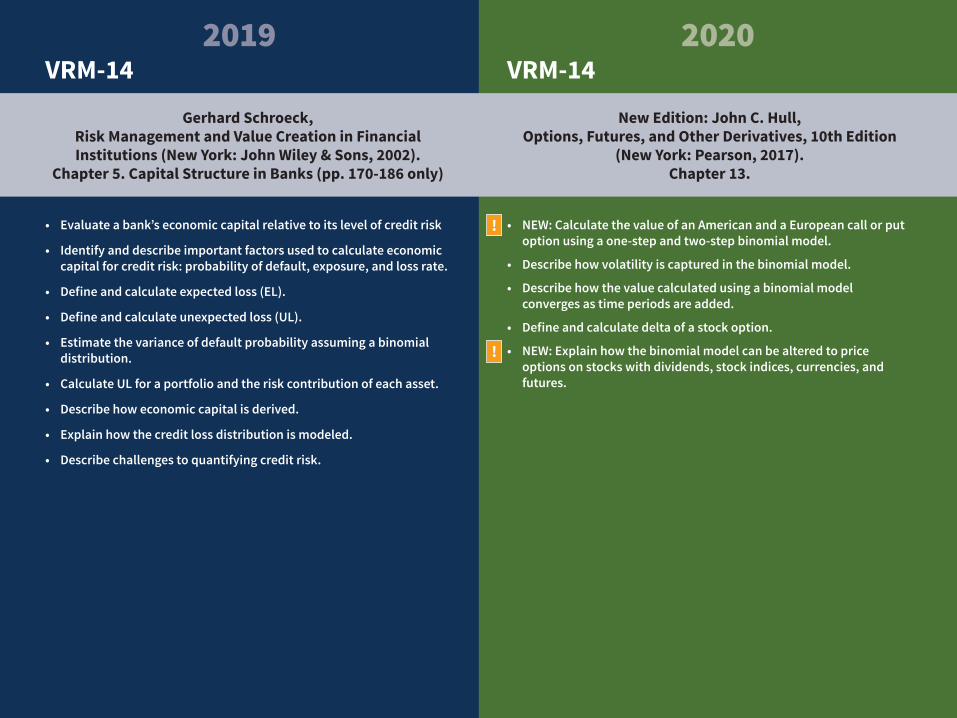

Linda Allen, Jacob Boudoukh and Anthony Saunders, Understanding Market, Credit and Operational Risk:

The Value at Risk Approach (Oxford: Blackwell Publishing, 2004).

Chapter 3. Putting VaR to Work

Linda Allen, Jacob Boudoukh and Anthony Saunders, Understanding Market, Credit and Operational Risk:

The Value at Risk Approach (Oxford: Blackwell Publishing, 2004).

Chapter 3. Putting VaR to Work

VRM-2 VRM-2

• Explainandgiveexamplesoflinearandnon-linearderivatives.

• DescribeandcalculateVaRforlinearderivatives.

• Describethedelta-normalapproachtocalculatingVaRfornon-linearderivatives.

• Describethelimitationsofthedelta-normalmethod.

• ExplainthefullrevaluationmethodforcomputingVaR.

• Comparedelta-normalandfullrevaluationapproachesforcomputingVaR.