partnership with telenor, easypaisa - mefin 2nd ppd-2017...partnership with telenor, easypaisa...

TRANSCRIPT

PARTNERSHIP WITH TELENOR, Easypaisa

MOBILE NETWORK OPERATOR & BRANCHLESS BANK

MEFIN PPD2, 14-16 March 2017

Hanoi, Vietnam

I’m Mohammed Ali Ahmed

Chief Strategy Office, Executive Director EFU Life Assurance Ltd

You can call me Ali

I am here to share my experience of working on a micro life product with the Largest Branchless Banking

Platform and second Largest Mobile Operator in Pakistan

INSURANCE FOR MASSES Creating a wide ranging social impact

1

“ New Digital Technologies are irrevocably changing the way

companies engage and interact with consumers.

It’s time for Insurers to re-evaluate their business objectives and see where does

mass market/inclusive/microinsurance fit in their model.

Transformation

Shift to the middle of the Pyramid: - Change in mindset. - Focus attention on the much

larger middle segment of the pyramid.

- Understanding of the market which was unexplored previously.

- Use of technology , relaxed underwriting and revisiting the existing processes.

Stated vision for financial inclusion in Pakistan is that: “Individuals and firms can access and use a range of quality payments, savings, credit and insurance services which meet their needs with dignity and fairness” ⊡Insurance ⊡Awareness, trust, reach, affordability ⊡Social impact for underprivileged segment ⊡Telco's/Branchless banking have a major role in this strategy

National Financial Inclusion Strategy

Pakistan – Micro lives insured - 2015

10.5 million lives insured (Criteria: Max Annual Premium of USD 50)

Predominantly credit life, and also includes term life, living benefits

• Enable all-inclusive micro and mass market solutions to be financially sustainable and

commercially viable for the Company

• Develop and market financial solutions for life and health meeting the needs of the target

market with a keen focus on affordability. The solutions will include protection as well as savings.

• Collaboration with diverse intermediaries with country level and concentrated geographical

presence and reach. These include MicroFinance Institutions, MicroFinance Banks, Branchless Banks,

Non-Governmental Organizations, Telecommunication companies and any other intermediary.

• Technology to act as a catalyst for optimizing all aspects of the business model such as

customer acquisition, claims, awareness creation as well as enhancing the customer experience.

• Leveraging on the intermediary setup for creating mass level awareness for insurance benefits.

• Have close alignment with regulator on their efforts for development of this sector and regular

engagement to have a relevant contribution in charting the direction of the regulatory framework

EFU Life’s key pillars for Financial Inclusion strategy

Easypaisa Kamyab Mustakbil

(Successful Future)

Launched in November 2016

A successful strategy will meet the essential requirements/objectives of the 3 stakeholders:

Telenor

• Stickiness

• Increase in awareness.

• New customers

• Self Sufficiency.

EFU Life

• Insurer visibility

• Insurance Penetration

• Opportunities for upselling

• More Lives

Customer

• Protection

• Simple product

• Minimal exclusions

The 3 parties

Product details Kamyab Mustakbil Plan

Term 1 year

Annual

contribution USD 5 for USD 1,000 insurance cover; can go up to USD 50

Benefit amount

Minimum death benefit amount (1 unit): USD 1,000; can

go up to USD 10,000

On death of the covered member, the beneficiary has the

option of taking the lump sum amount, OR 12 equal

monthly instalments, in which case EFU Life will pay one

extra monthly instalment to the beneficiary.

Key exclusion Only one exclusion:

Suicide and self-inflicted injury

Waiting period For policies sold through Telesales: None

For policies sold through Retailers: 30 days

Free look period 30 days from date of enrolment

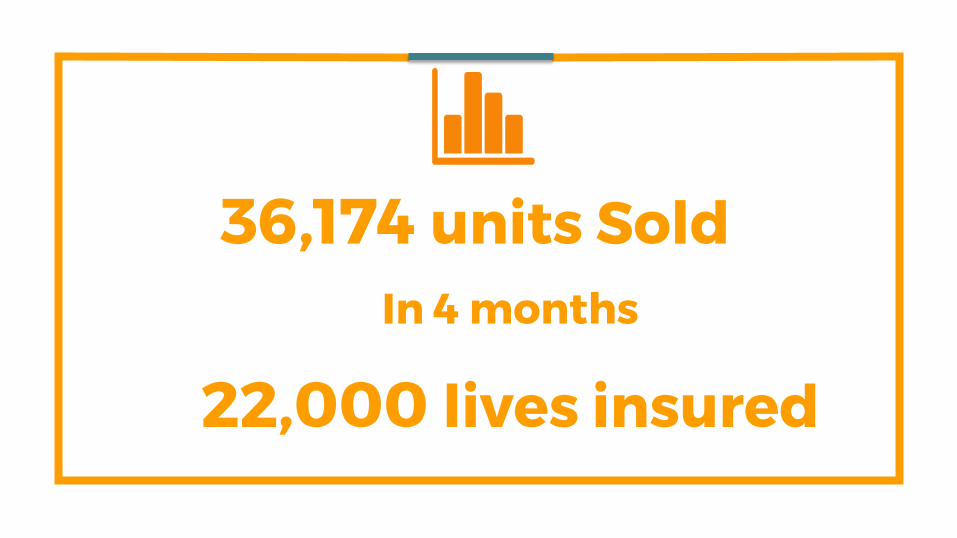

Nano-Term Takaful

36,174 units Sold In 4 months

22,000 lives insured

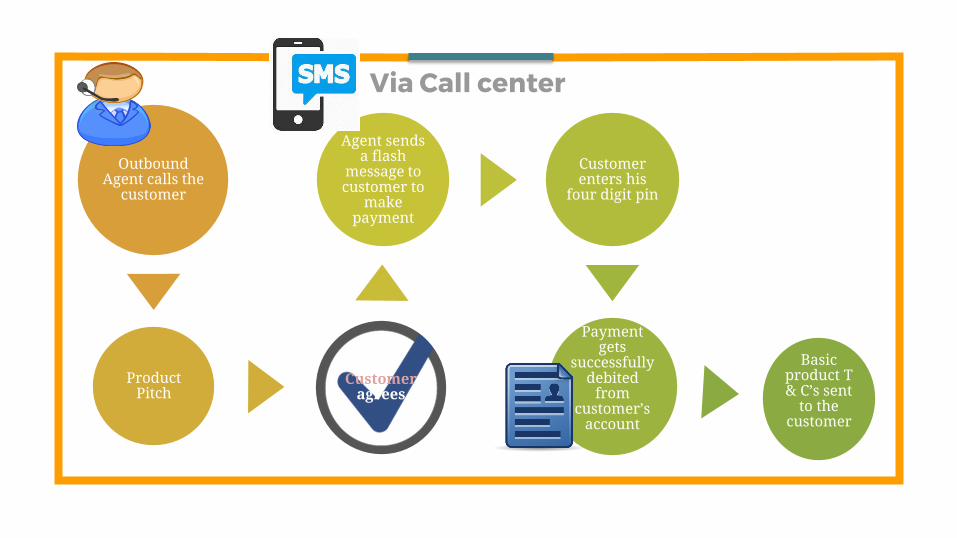

Enrollment Process

Current 1. Via Outbound Sales Channel

To be launched 1. Blast SMS 2. Other network service providers 3. Retailers

Enrollment

Outbound Agent calls the

customer

Product Pitch

Customer agrees

Agent sends a flash

message to customer to

make payment

Customer enters his

four digit pin

Payment gets

successfully debited

from customer’s

account

Basic product T & C’s sent

to the customer

Via Call center

By Easypaisa:

SMS 2: Easypaisa Kamyab Mustaqbil takaful is valid for one year from date of premium payment. Customer can request the cancellation of the product within 30 days of premium payment. For More details please visit www.easypaisa.com.pk. For any queries related to claims please dial 3737

Detailed T&C’s can be viewed on the website or a printed hard copy can be collected from sales centers of Telenor.

Product communication via SMS

SMS 1: Easypaisa Kamyab Mustaqbil is life Bema Takaful plan, where beneficiary will be paid coverage amount in case of customer's death. Death in case of suicide is not covered. Waiting period of 30 Days will apply only in case of self-registration

By EFUL:

Dear Customer, Your contribution payment for Easypaisa Kamyab Mustaqbil has been received, You are now covered up to Rs. Xxx during the member ship year from the date of subscription. For further information please dial 3737 or logon to www.easypaisa.com.pk

Product communication via SMS

Detailed T&C’s can be viewed on the website or a printed hard copy can be collected from sales centers of Telenor.

Select:

1. Insurance Type

2. Plan

Enter Beneficiary details

Select

1.Premium

2. Payment Method

On completion of premium

payment customer receives

gratification message

along with product

basic T&C

*786

#

Customer

Dials

Via Mobile USSD (self & retailers)

Selects

1. Get Insured

2.Insurance Type

3. Plan

Enter Beneficiary details

Select

1. Premium

2. Payment Method

On completion of premium payment customer receives

gratification message along with product basic

T&C

Via mobile app

Product & Processes approved by our Shariah Advisor.

Shariah Certificate available on website and can be emailed or posted to customer whenever requested.

Shariah Certificate

Claims Process

Beneficiary/Customer intimates the claim to EFUL through

•Helpline --021-111-EFU-111 (111-338-111) •Email •Postal Mail

Beneficiary/ Customer send the required documents to EFUL via

•E-mail •Postal Mail •Whatsapp •Courier •Google Docs, etc.

Claim is examined

within 48 Hours

Claim amount is disbursed into

customer/beneficiary’s account ,

or is paid via cheque.

Claims process

1 claim has been received - it’s early days for the product. To increase the claim awareness we are planning to carry out the following activities: 1. Blast SMS to all the policy holders to increase the awareness of claims

2. Sample customer satisfaction and claims awareness call to all the

clients.

Claims awareness

There is a great sense of urgency in Telcos

Buying Insurance should be as easy as buying a

mobile package.

Higher Management believe in the product at

both sides.

Insurance does not sell by itself.

Start with a radically simple product

Use of Technology & Process simplicity

Lessons learnt

⊡Change is inevitable

⊡There will always be an alternative that will cross the boundary into the mainstream

⊡Success - to adapt across the organization when this happens

Change…

“The secret of change is to focus all of your energy, not on fighting the old, but on building the new.”

- Socrates

Thank you for being a wonderful audience!