paycheck protection program loans · 2020-05-05 · certification language •develop a written...

TRANSCRIPT

fisherphillips.com

Paycheck Protection Program Loans:Latest Updates & Forgiveness Issues

TIM SCOTT

(504) 529-3834

fisherphillips.com

Paycheck Protection Program Loans:Latest Updates & Forgiveness Issues

(504) 529-3834

netchex.com

fisherphillips.com

Reminders

• This is being recorded

• Please hold questions until the end!• Submit through the Q & A box

• Separate session for Netchex-specific updates

netchex.com

fisherphillips.com

Paycheck Protection ProgramTimeline

• Enacted into law on March 27, 2020• Loan applications started April 3, 2020• By April 16, initial $349B exhausted• Second round of funding ($60B) approved on April 24, 2020• Loans can be applied for from April 27 until money runs out (or June 30)• Since April 3, very little guidance (most information so far focuses on

eligibility rules and lender protocols)• Mostly silent on loan forgiveness and permissive uses of loan money

netchex.com

fisherphillips.com

Paycheck Protection ProgramCertifications

• Required certifications in loan application:(1) “Current economic uncertainty makes this loan request necessary to

support the ongoing operations of the Applicant.”

(2) “Loan forgiveness will be provided for the sum of documentedpayroll costs, covered mortgage interest payments, covered rentpayments, and covered utilities, and not more than 25% of theforgiven amount may be of non-payroll purposes.”

netchex.com

fisherphillips.com

Paycheck Protection ProgramUncertainty vs. Necessity

netchex.com

fisherphillips.com

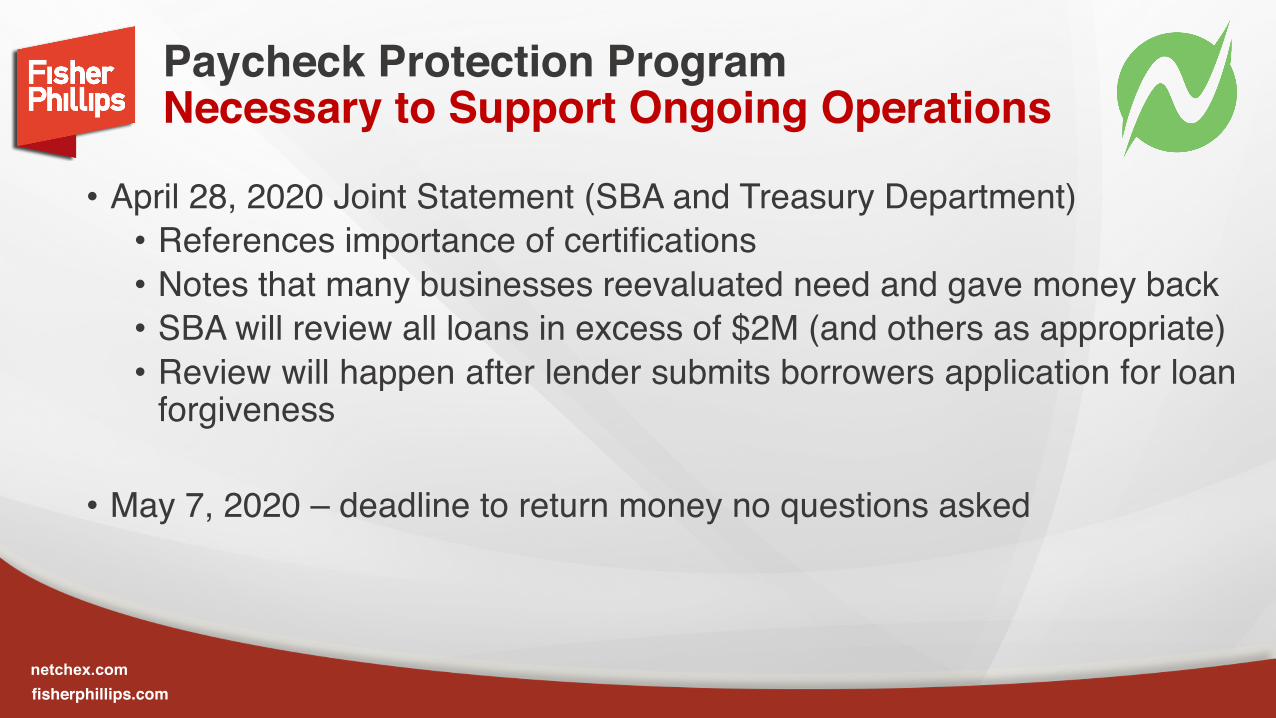

Paycheck Protection ProgramNecessary to Support Ongoing Operations

• April 28, 2020 Joint Statement (SBA and Treasury Department)• References importance of certifications• Notes that many businesses reevaluated need and gave money back• SBA will review all loans in excess of $2M (and others as appropriate)• Review will happen after lender submits borrowers application for loan

forgiveness

• May 7, 2020 – deadline to return money no questions asked

netchex.com

fisherphillips.com

Paycheck Protection ProgramNecessary to Support Ongoing Operations

SBA FAQ Publications• Question No. 31: what about small businesses owned by large companies with access

to liquidity to support ongoing operations?• Question No. 37: what about small businesses owned by private companies with

access to liquidity to support ongoing operations?• Short answer:

• Must assess “economic need” for PPP loan at the time of the loan application• Focus on certification that PPP proceeds are “necessary”• Access to other sources of liquidity is relevant• Not on the lender• May 7 payback deadline• Penalties?

netchex.com

fisherphillips.com

Paycheck Protection ProgramWhat Should Borrowers Do Before May 7, 2020?

• Reevaluate need for loan under certification language • Develop a written list of reasons why PPP

loan proceeds are necessary for your business’s continued operations• Find out from your lender if others in your

industry or in similar financial circumstances are giving money back

netchex.com

fisherphillips.com

Paycheck Protection ProgramWhat Can Loans Be Used For?

Loans may be used for “Payroll Costs”, defined as:• Salary, wages, commission of similar compensation• Cash tips or equivalent• Payments for vacation, parental, family, medical or sick leave• Group health care benefits

• Including insurance premiums• Retirement benefits• State or local tax assessed on the compensation of employees (not

federal)• Certain sole proprietor and independent contractor compensation

netchex.com

fisherphillips.com

Paycheck Protection ProgramOther Recent Guidance – Payroll Costs

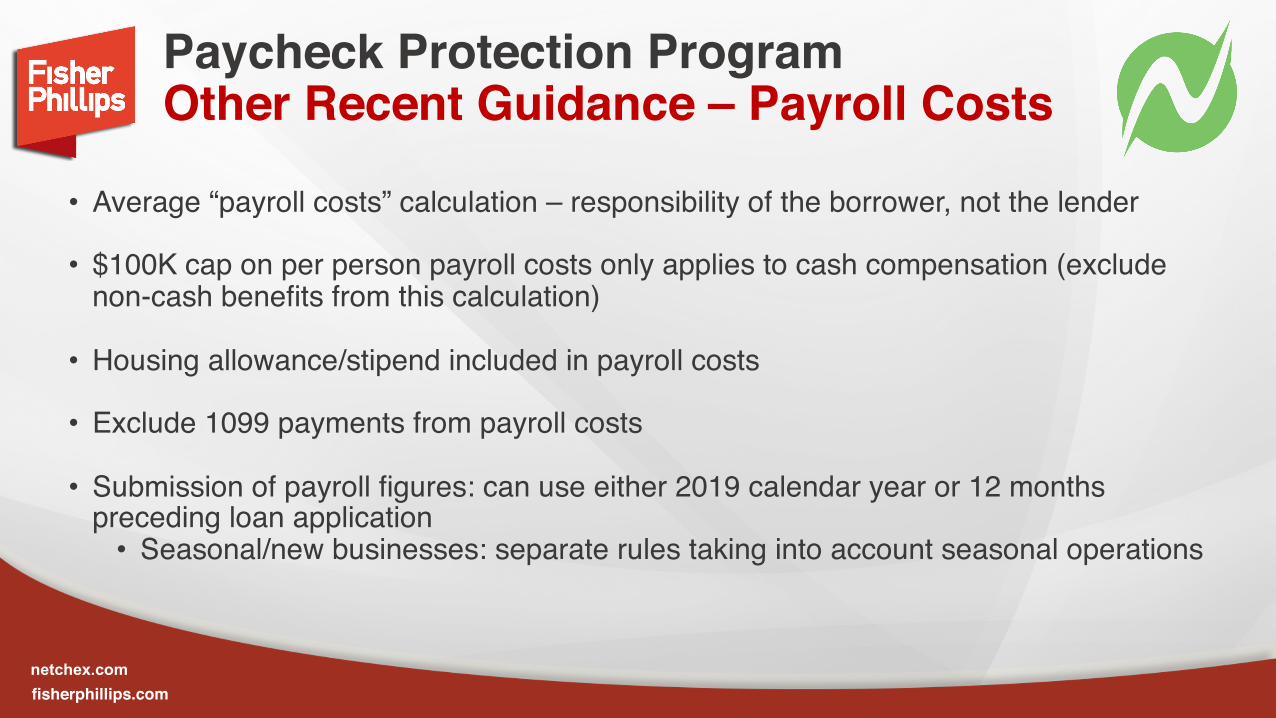

• Average “payroll costs” calculation – responsibility of the borrower, not the lender

• $100K cap on per person payroll costs only applies to cash compensation (exclude non-cash benefits from this calculation)

• Housing allowance/stipend included in payroll costs

• Exclude 1099 payments from payroll costs

• Submission of payroll figures: can use either 2019 calendar year or 12 months preceding loan application • Seasonal/new businesses: separate rules taking into account seasonal operations

netchex.com

fisherphillips.com

Paycheck Protection ProgramAdditional Permitted Usage

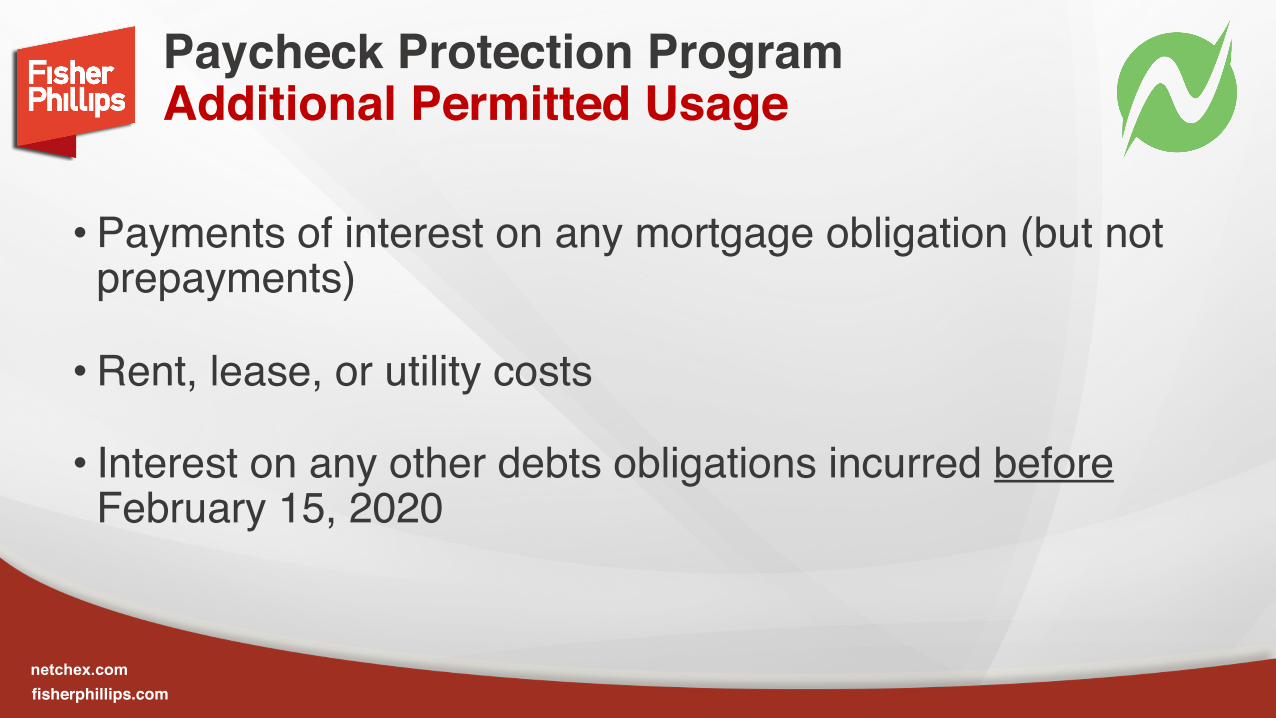

• Payments of interest on any mortgage obligation (but not prepayments)

•Rent, lease, or utility costs

• Interest on any other debts obligations incurred beforeFebruary 15, 2020

netchex.com

fisherphillips.com

Paycheck Protection ProgramLoan Forgiveness – Step 1

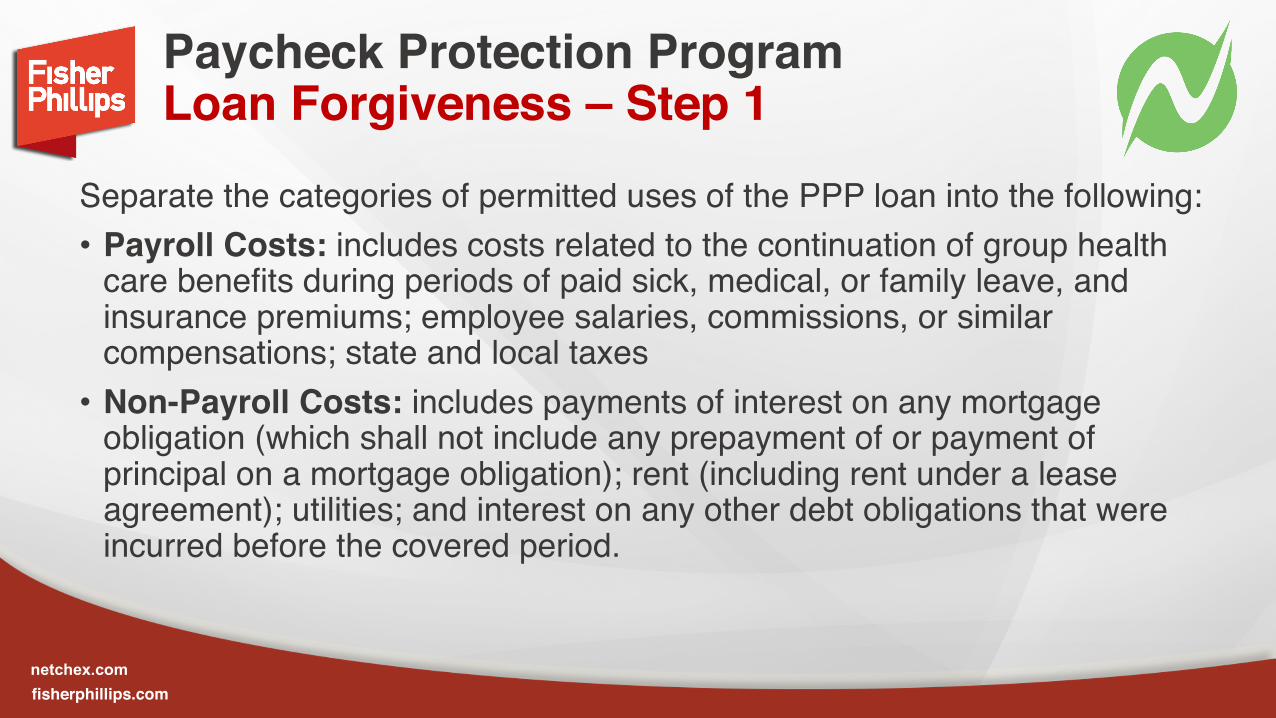

Separate the categories of permitted uses of the PPP loan into the following:• Payroll Costs: includes costs related to the continuation of group health

care benefits during periods of paid sick, medical, or family leave, and insurance premiums; employee salaries, commissions, or similar compensations; state and local taxes• Non-Payroll Costs: includes payments of interest on any mortgage

obligation (which shall not include any prepayment of or payment of principal on a mortgage obligation); rent (including rent under a lease agreement); utilities; and interest on any other debt obligations that were incurred before the covered period.

netchex.com

fisherphillips.com

Paycheck Protection ProgramLoan Forgiveness – Step 2

Ex. 1: Total Non-Payroll Costs Exceed 25%

Type of Cost Expense AmountPayroll Cost Wages $300,000Payroll Cost Health Care Premiums $10,000Payroll Cost State and Local Taxes $5,000

Total Payroll Costs $315,000

Non Payroll Cost Rent $90,000Non Payroll Cost Internet, Phone, Electric $2,000Non Payroll Cost Mortgage Interest $40,000

Total Non-Payroll Costs $132,000

Calculate the total amount of your PPP loan spent in the 8-weekperiod following disbursement of your loan for each category.

Type of Cost Expense AmountPayroll Cost Wages $300,000Payroll Cost Health Care Premiums $10,000Payroll Cost State and Local Taxes $5,000

Total Payroll Costs $315,000

Non Payroll Cost Rent $90,000Non Payroll Cost Internet, Phone, Electric $2,000Non Payroll Cost Mortgage Interest $10,000

Total Non-Payroll Costs $102,000

Ex. 2: Total Non-Payroll Costs Do Not Exceed 25%

netchex.com

fisherphillips.com

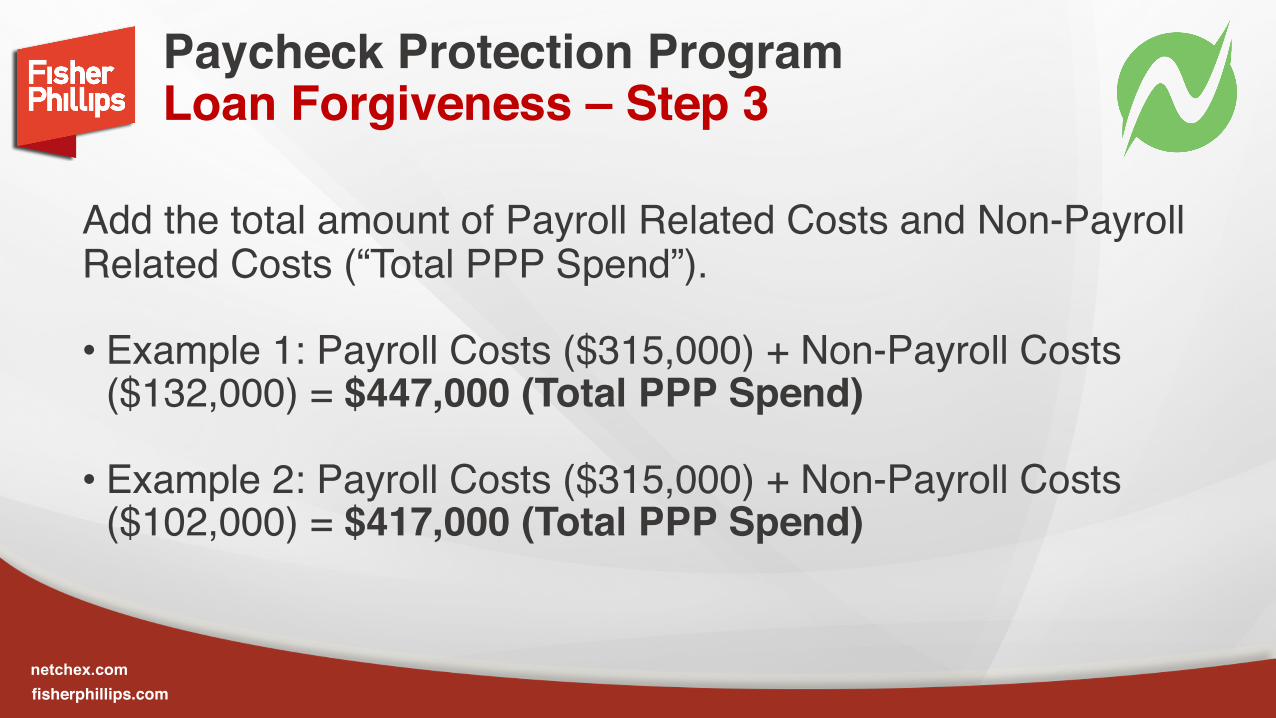

Paycheck Protection ProgramLoan Forgiveness – Step 3

Add the total amount of Payroll Related Costs and Non-Payroll Related Costs (“Total PPP Spend”).

• Example 1: Payroll Costs ($315,000) + Non-Payroll Costs ($132,000) = $447,000 (Total PPP Spend)

• Example 2: Payroll Costs ($315,000) + Non-Payroll Costs ($102,000) = $417,000 (Total PPP Spend)

netchex.com

fisherphillips.com

Paycheck Protection ProgramLoan Forgiveness – Step 4

Multiply the Total PPP Spend by 25% to get the limit of the Total Potential Forgivable Non-Payroll Related Costs. Any monies spent on Non-Payroll Related Costs above and beyond the Total Potential Forgivable Non-Payroll Related Costs are not eligible for forgiveness.

• Example 1: $447,000 x .25 = $111,750 (Total Potential Forgivable Non-Payroll Related Costs)

• Example 2: $417,000 x .25 = $104,250 (Total Potential Forgivable Non-Payroll Related Costs)

fisherphillips.com

Paycheck Protection ProgramLoan Forgiveness – Step 5

Determine if Non-Payroll Related Costs are greater than Total Potential Forgivable Non-Payroll Related Costs. If so, add Payroll Related Costs and Total Potential Forgivable Non-Payroll Related Costs to get the Total Potentially Eligible for PPP Loan Forgiveness. If not, use the Total PPP Spend as the Total Potentially Eligible for PPP Loan Forgiveness. • Ex. 1: $315,000 + $111,750 = $426,750 (Total Potentially Eligible for PPP Loan

Forgiveness)• Ex. 2: Non-Payroll Costs ($102,000) < Total Potential Forgivable Non-Payroll

Related Costs ($104,250) so $417,000 (Total Potentially Eligible for PPP Loan Forgiveness)

fisherphillips.com

Paycheck Protection ProgramLoan Forgiveness – Step 6

Divide the average number of Full Time Equivalent Employees (“FTEEs”) during the covered period by the average number of FTEEs during 2/15/19-6/30/19 or 1/1/20-2/29/20 (at your choice – use the lower figure).

• Average Monthly FTEEs during 8-weeks following disbursement of loan: 40• Option 1 - Average Monthly FTEEs during 2/15/19 – 6/30/19: 52• Option 2 - Average Monthly FTEEs during 1/1/20 – 2/29/20: 48• Option 2 is the lowest FTEE count, so divide 40/48 = .8333

netchex.com

fisherphillips.com

Paycheck Protection ProgramLoan Forgiveness – Step 7

Multiply the Total Potentially Eligible for PPP Loan Forgiveness by the percentage from Step 6.

• Example 1: $426,750 x .8333 = $355,610.78

• Example 2: $417,000 x .8333 = $347,486.10

netchex.com

fisherphillips.com

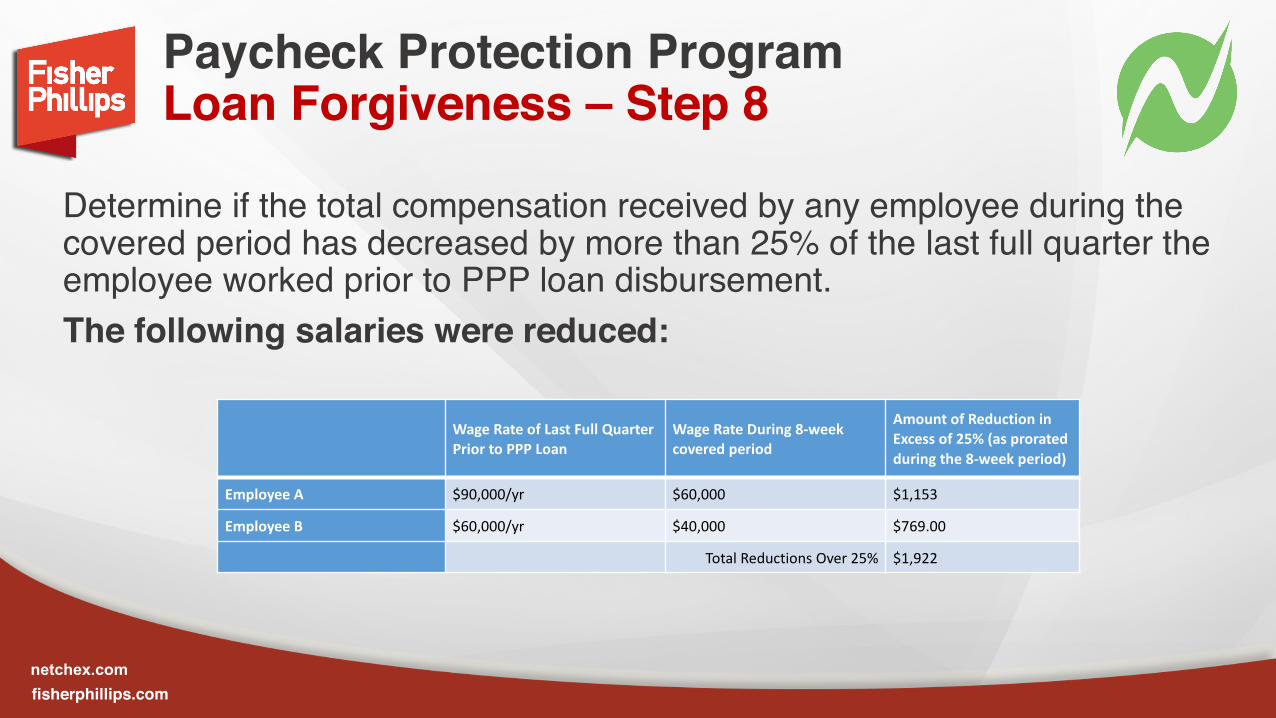

Paycheck Protection ProgramLoan Forgiveness – Step 8

Determine if the total compensation received by any employee during the covered period has decreased by more than 25% of the last full quarter the employee worked prior to PPP loan disbursement.The following salaries were reduced:

Wage Rate of Last Full Quarter Prior to PPP Loan

Wage Rate During 8-week covered period

Amount of Reduction in Excess of 25% (as prorated during the 8-week period)

Employee A $90,000/yr $60,000 $1,153

Employee B $60,000/yr $40,000 $769.00

Total Reductions Over 25% $1,922

netchex.com

fisherphillips.com

Paycheck Protection ProgramLoan Forgiveness – Step 9

Reduce the number from Step 7 by the percentage decrease in salary beyond a 25% reduction obtained in Step 8 to obtain Total Eligible Forgiveness.

• Example 1: $355,610.78 - $1,922 = $353,688.78 Total Eligible Forgiveness

• Example 2: $347,486.10 - $1,922 = $345,564.10 Total Eligible Forgiveness

netchex.com

fisherphillips.com

Paycheck Protection programLoan Forgiveness – Safe Harbor

FAQ 40 (May 3):

PPP loan forgiveness will be reduced if a borrower laid off anemployee, offered to rehire the same employee, but the employeedeclined the offer.

• Must occur prior to June 30, 2020• Must make a good faith offer of reemployment (in writing)• Must document the rejection of the offer• Key provision given issued with enhanced unemployment benefits

netchex.com

fisherphillips.com

QUESTIONS?PRESENTED BY:

TIM SCOTT

netchex.com