payer perspectives on value-based contracting2014 life sciences industry forum payer perspectives on...

TRANSCRIPT

2014 Life Sciences Industry Forum

Payer Perspectives On

Value-based Contracting

Miles Snowden, MD, MPH, CEBS

Chief Medical Officer

1

2014 Life Sciences Industry Forum

Making the health system work better for everyone

A simple goal

2

2014 Life Sciences Industry Forum

60,000,000+ individuals

Statistics as of 6/30/13 except where noted; *as of 1/17/13

80,000 provider practices and other health care facilities

67,000 pharmacies*

5,000 hospitals

400 global life sciences organizations

300 health plans

150 state, federal and municipal agencies and departments

Optum serves

3

2014 Life Sciences Industry Forum

% Who Feel There are Significant Differences

in Quality of Care in Community

Majorities of physicians and, especially, hospital execs see significant differences in quality of care across the community.

Base: All Qualified Respondents: (Physicians n = 1,602, Consumers n = 3,400 / 3,398 / 3,397, Hospitals n = 400)

Q625/Q425/Q325 Are there, or are there not, significant differences in the quality of care provided by doctors and hospitals in your local area?

PHYSICIANS (A)

CONSUMERS (B)

HOSPITALS (C)

55%

37%

62%

4

2014 Life Sciences Industry Forum

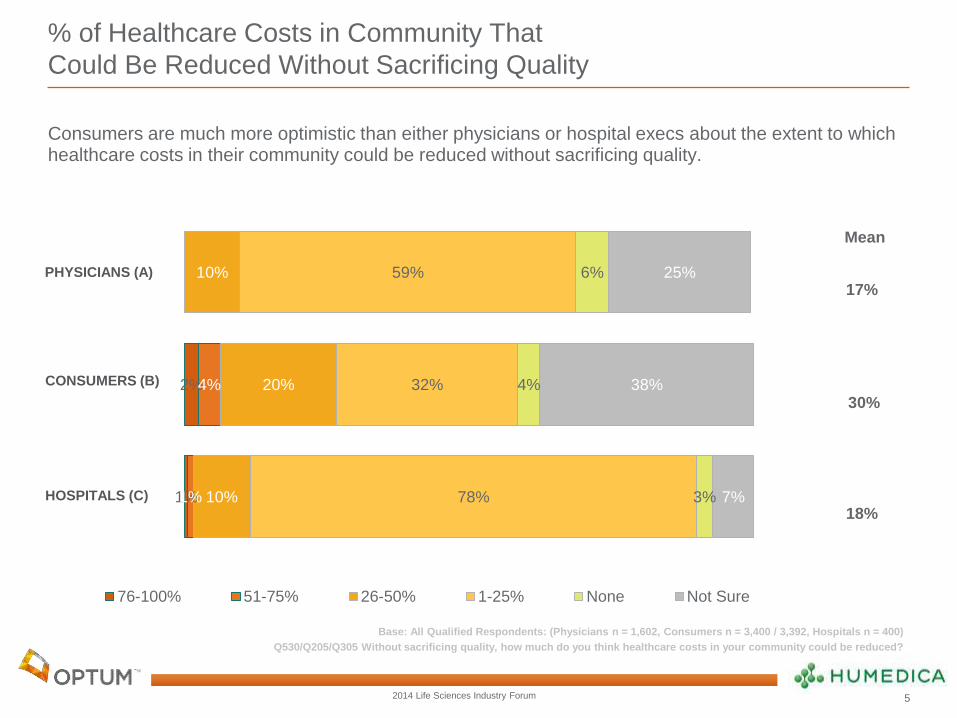

% of Healthcare Costs in Community That

Could Be Reduced Without Sacrificing Quality

Consumers are much more optimistic than either physicians or hospital execs about the extent to which healthcare costs in their community could be reduced without sacrificing quality.

Base: All Qualified Respondents: (Physicians n = 1,602, Consumers n = 3,400 / 3,392, Hospitals n = 400)

Q530/Q205/Q305 Without sacrificing quality, how much do you think healthcare costs in your community could be reduced?

2%

1%

4%

1%

10%

20%

10%

59%

32%

78%

6%

4%

3%

25%

38%

7%

76-100% 51-75% 26-50% 1-25% None Not Sure

PHYSICIANS (A)

CONSUMERS (B)

HOSPITALS (C)

17%

Mean

30%

18%

17%

Mean

30%

18%

5

2014 Life Sciences Industry Forum

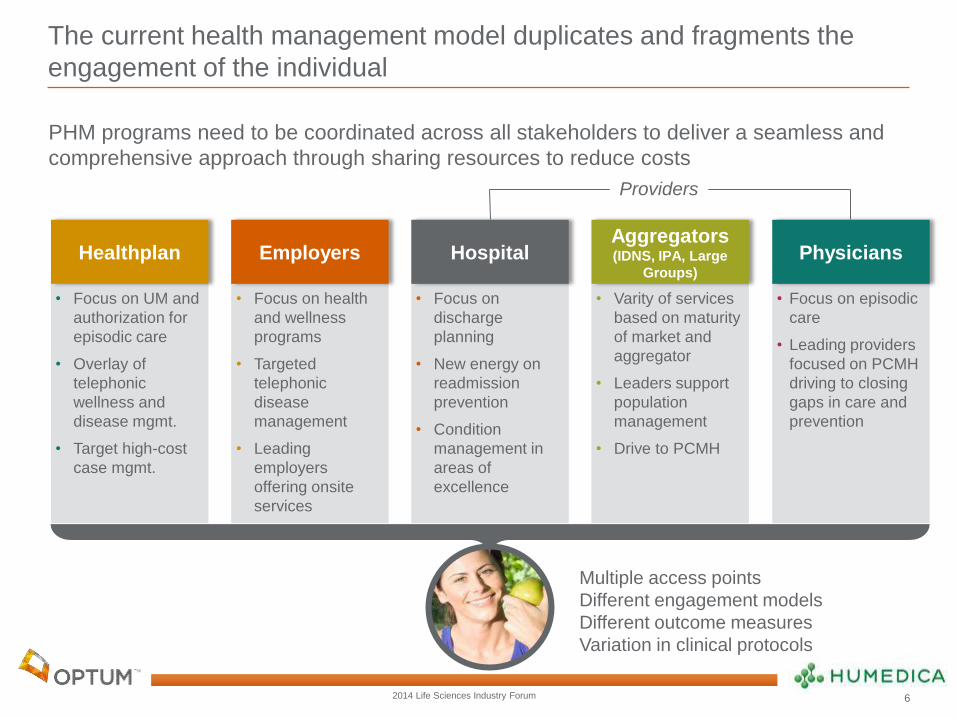

The current health management model duplicates and fragments the

engagement of the individual

• Focus on UM and

authorization for

episodic care

• Overlay of

telephonic

wellness and

disease mgmt.

• Target high-cost

case mgmt.

Healthplan

• Focus on health

and wellness

programs

• Targeted

telephonic

disease

management

• Leading

employers

offering onsite

services

Employers

• Focus on

discharge

planning

• New energy on

readmission

prevention

• Condition

management in

areas of

excellence

Hospital

• Varity of services

based on maturity

of market and

aggregator

• Leaders support

population

management

• Drive to PCMH

Aggregators (IDNS, IPA, Large

Groups)

• Focus on episodic

care

• Leading providers

focused on PCMH

driving to closing

gaps in care and

prevention

Physicians

Providers

Multiple access points

Different engagement models

Different outcome measures

Variation in clinical protocols

PHM programs need to be coordinated across all stakeholders to deliver a seamless and

comprehensive approach through sharing resources to reduce costs

6

2014 Life Sciences Industry Forum

We begin by understanding the market trends

Trends Implications

1. Need to focus on clinical and

operational improvement to achieve

value beyond market share

2. Market is defining new

reimbursement models focused on

population management

3. Market is defining new incentives

and penalties in physician

compensation models

4. New primary care models are

being deployed

5. New capabilities needed to

measure and deliver value-based

care

Continued focus on gaining market leverage with

payer community

Consolidation of

Provider

Community

System

Affordability

Consumers are faced with a health care affordability

crisis

Value-Based

Care Models

Aligned economic and practice incentives between

providers and payers

Population Care

Management

Focus on managing populations and individuals

across the system of care

Industry Defined

Performance

Measurements

New patient satisfaction, outcomes and quality

measurements are tied to reimbursement and

compensation models

7

2014 Life Sciences Industry Forum

There are many new partnership models occurring to engage

stakeholders in many different ways

Private Exchanges/Defined Contribution Direct to Employer

Three-Prong Partnership Traditional

8

Payer

Provider

Employer

Employer

Provider

Payer

Individual

Employer

Provider

Individual

Employer

Payer

Payer Provider

Ind

ivid

ua

l

Payer Provider

Exchange

8

2014 Life Sciences Industry Forum

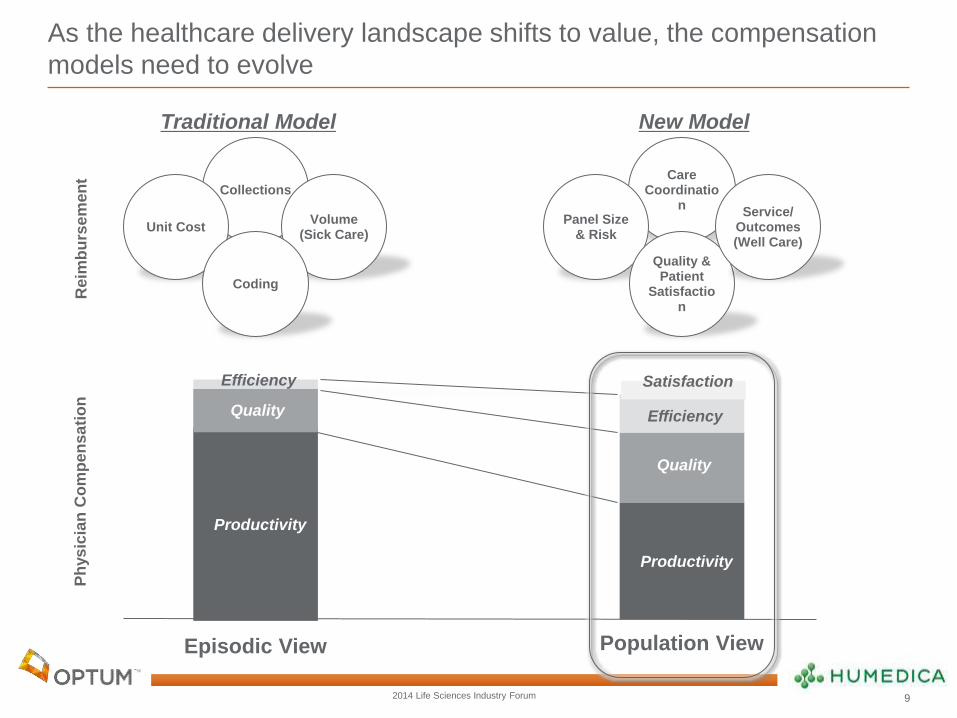

As the healthcare delivery landscape shifts to value, the compensation

models need to evolve

Collections Care

Coordination

Panel Size & Risk

Quality & Patient

Satisfaction

Service/ Outcomes (Well Care)

Productivity

Quality

Efficiency

Ph

ys

icia

n C

om

pe

nsa

tio

n

Unit Cost Volume

(Sick Care)

Coding

Reim

bu

rse

men

t

Traditional Model New Model

Population View

Productivity

Quality

Efficiency

Episodic View

9

Satisfaction

2014 Life Sciences Industry Forum

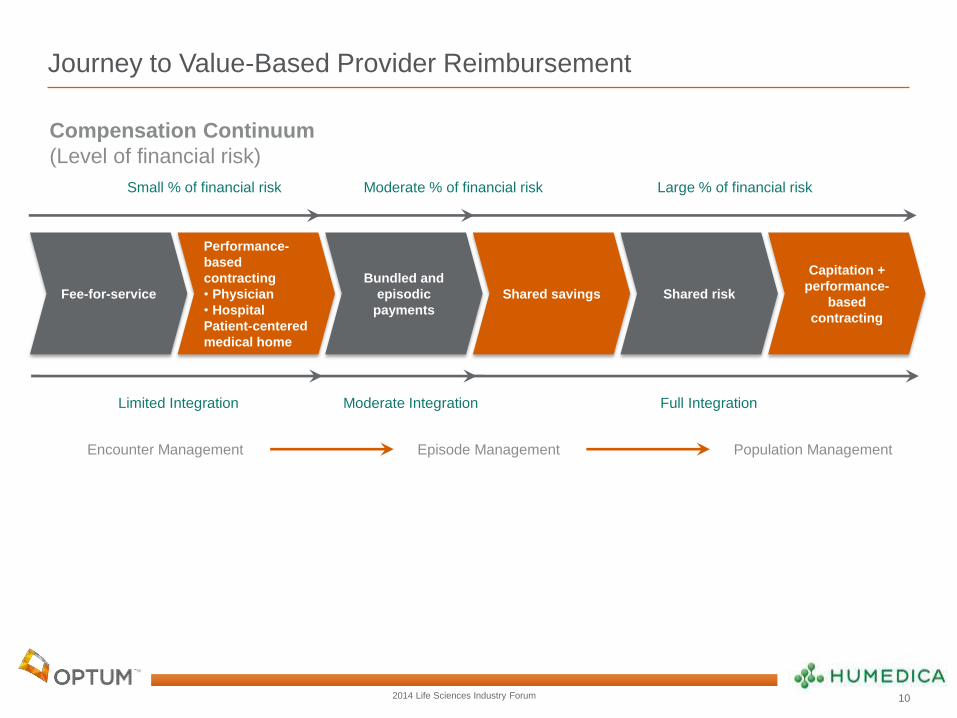

Journey to Value-Based Provider Reimbursement

Fee-for-service

Performance-

based

contracting

• Physician

• Hospital

Patient-centered

medical home

Bundled and

episodic

payments

Shared savings Shared risk

Capitation +

performance-

based

contracting

Episode Management Encounter Management Population Management

Moderate Integration Full Integration Limited Integration

Small % of financial risk Moderate % of financial risk Large % of financial risk

Compensation Continuum

(Level of financial risk)

10

2014 Life Sciences Industry Forum

87%

13%

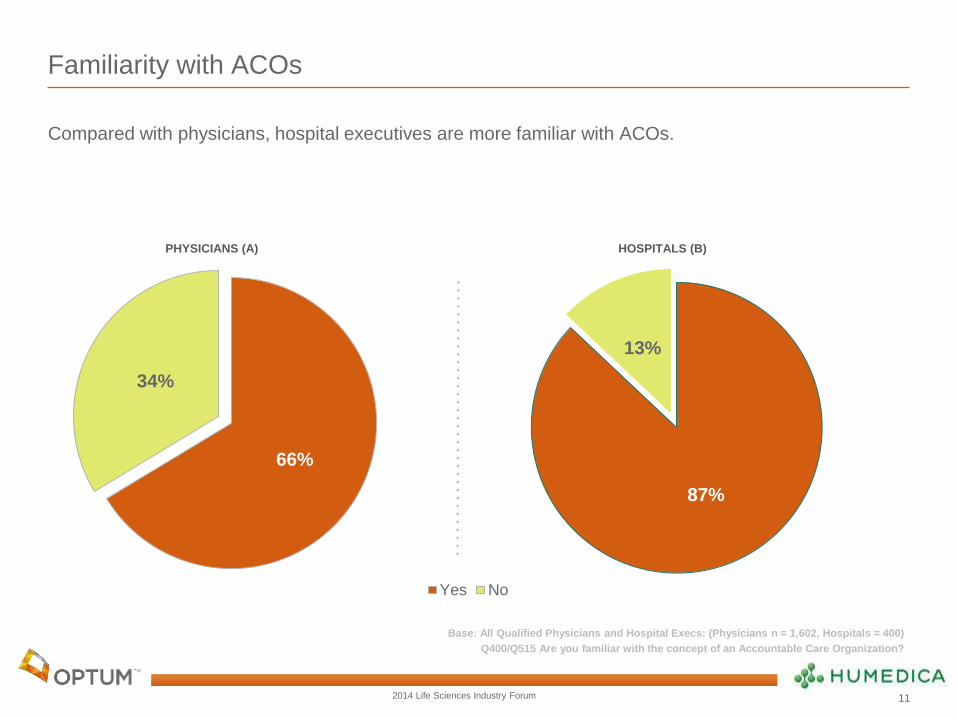

Familiarity with ACOs

Compared with physicians, hospital executives are more familiar with ACOs.

Base: All Qualified Physicians and Hospital Execs: (Physicians n = 1,602, Hospitals = 400)

Q400/Q515 Are you familiar with the concept of an Accountable Care Organization?

66%

34%

Yes No

HOSPITALS (B) PHYSICIANS (A)

11

2014 Life Sciences Industry Forum

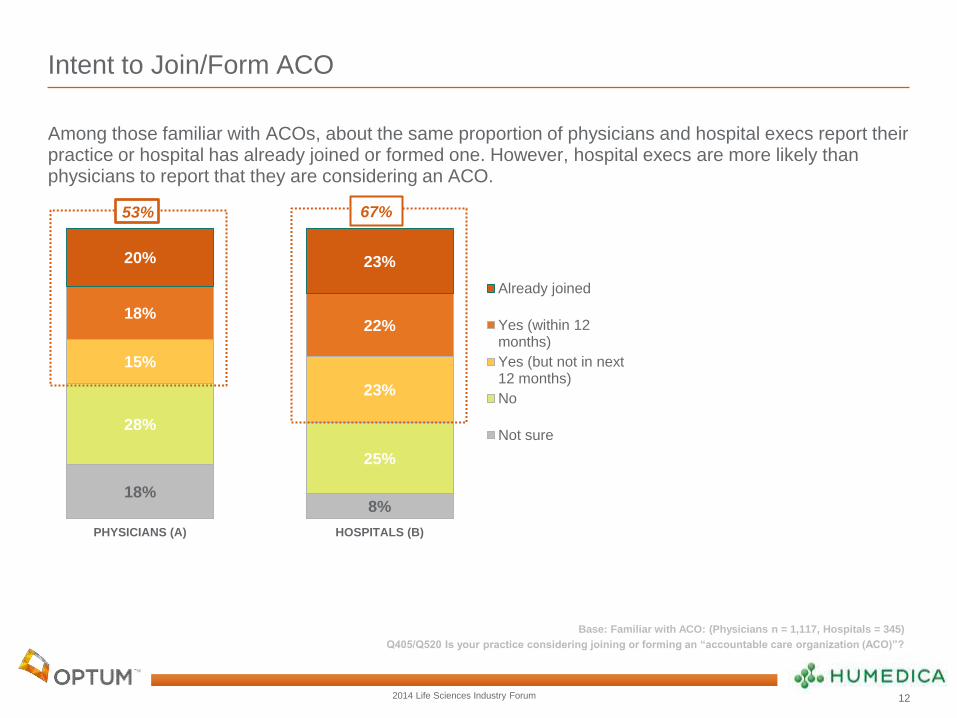

8% 18%

25%

28%

23%

15%

22% 18%

23% 20%

HOSPITALS (B)PHYSICIANS (A)

Already joined

Yes (within 12months)

Yes (but not in next12 months)

No

Not sure

Intent to Join/Form ACO

Among those familiar with ACOs, about the same proportion of physicians and hospital execs report their practice or hospital has already joined or formed one. However, hospital execs are more likely than physicians to report that they are considering an ACO.

Base: Familiar with ACO: (Physicians n = 1,117, Hospitals = 345)

Q405/Q520 Is your practice considering joining or forming an “accountable care organization (ACO)”?

A

53% 67%

12

2014 Life Sciences Industry Forum

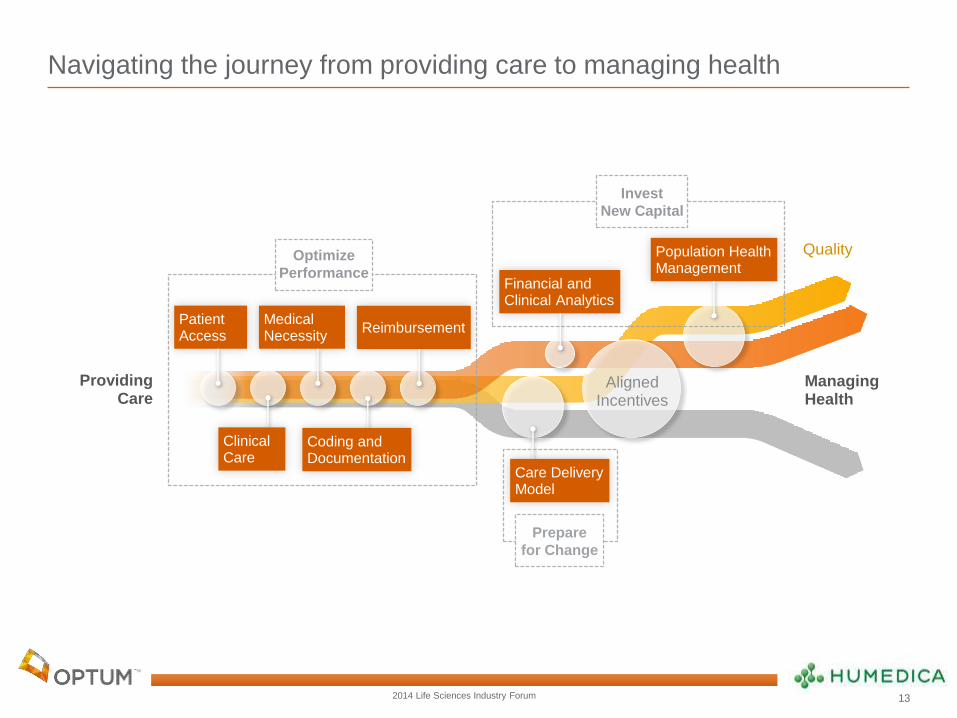

Navigating the journey from providing care to managing health

Quality

Patient Access

Medical Necessity

Reimbursement

Financial and Clinical Analytics

Population Health Management

Aligned Incentives

Providing Care

Clinical Care

Coding and Documentation

Care Delivery Model

Managing Health

Prepare

for Change

Optimize

Performance

Invest

New Capital

13

2014 Life Sciences Industry Forum

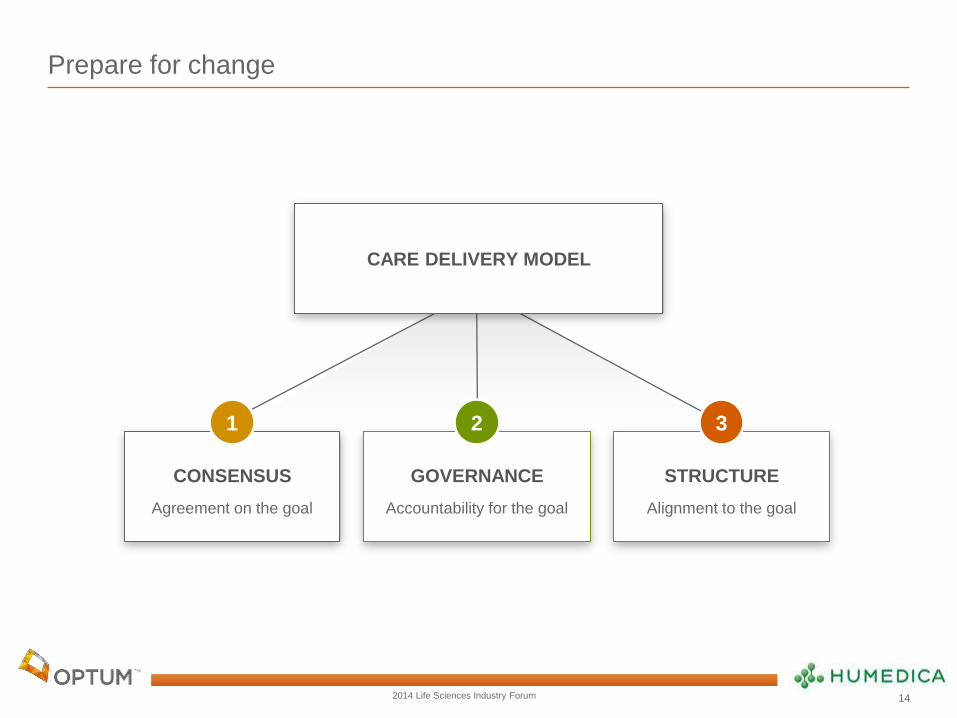

Prepare for change

CONSENSUS

Agreement on the goal

1

STRUCTURE

Alignment to the goal

3

Care delivery model

GOVERNANCE

Accountability for the goal

2

CARE DELIVERY MODEL

14

2014 Life Sciences Industry Forum

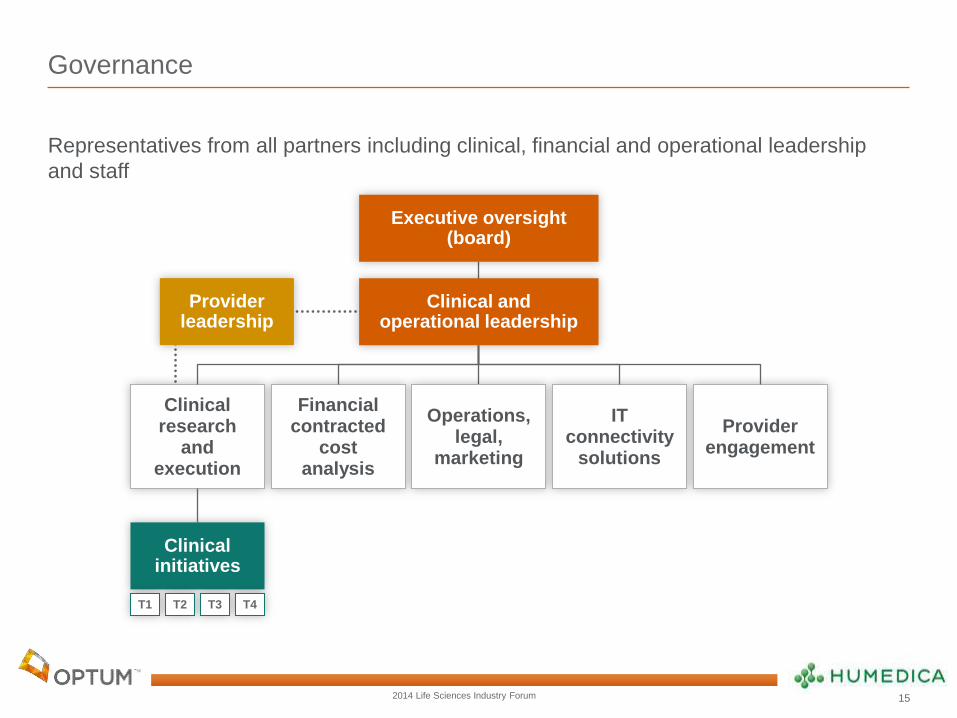

Governance

Representatives from all partners including clinical, financial and operational leadership

and staff

Executive oversight (board)

Clinical and operational leadership

Provider leadership

Clinical initiatives

Clinical research

and execution

IT connectivity

solutions

Operations, legal,

marketing

Financial contracted

cost analysis

Provider engagement

T1 T2 T3 T4

15

2014 Life Sciences Industry Forum 16

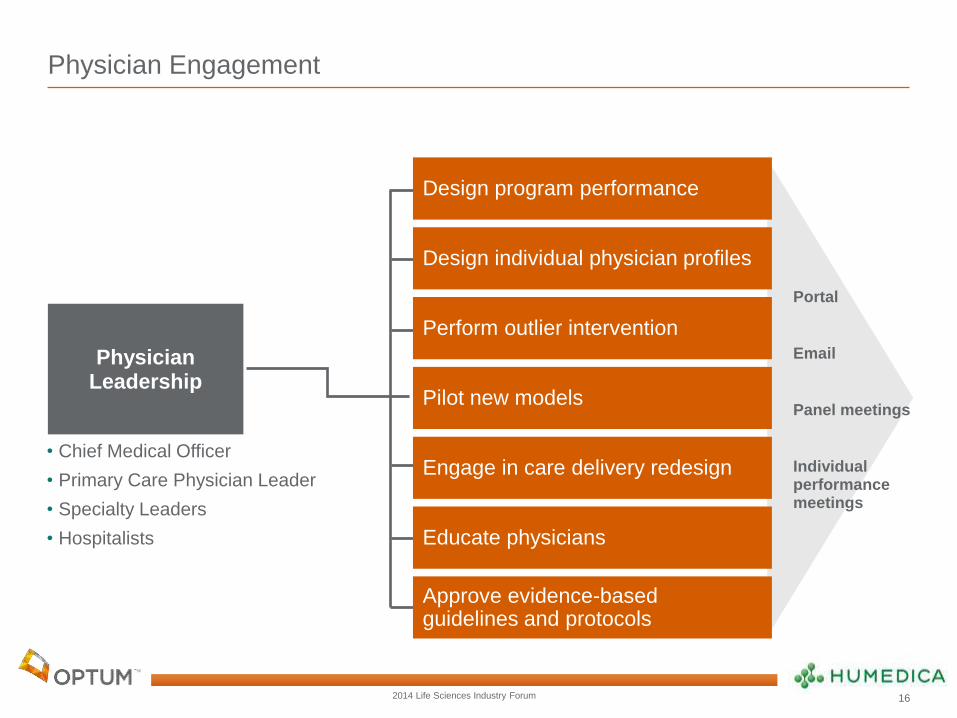

Physician Engagement

Portal

Panel meetings

Individual performance meetings

Design program performance

Design individual physician profiles

Perform outlier intervention

Pilot new models

Engage in care delivery redesign

Educate physicians

Approve evidence-based guidelines and protocols

Physician Leadership

• Chief Medical Officer

• Primary Care Physician Leader

• Specialty Leaders

• Hospitalists

2014 Life Sciences Industry Forum

Key opportunities in population health management

2012 medical claims cost distribution among 5.5 million commercial members using

Optum for Population Health Management services

Population medical costs are largely from treatment of chronic conditions in the

ambulatory setting.

17

2014 Life Sciences Industry Forum

Invest new capital

With expert financial and clinical predictive analytics as your enabler, patient risk now

becomes an opportunity to manage health and drive down costs.

Financial & Clinical Analytics

To predict the future medical

experience of individual health

consumers and defined populations

Population Health Management

To identify, engage, and impact

every individual with a health need

within a defined population

18

2014 Life Sciences Industry Forum

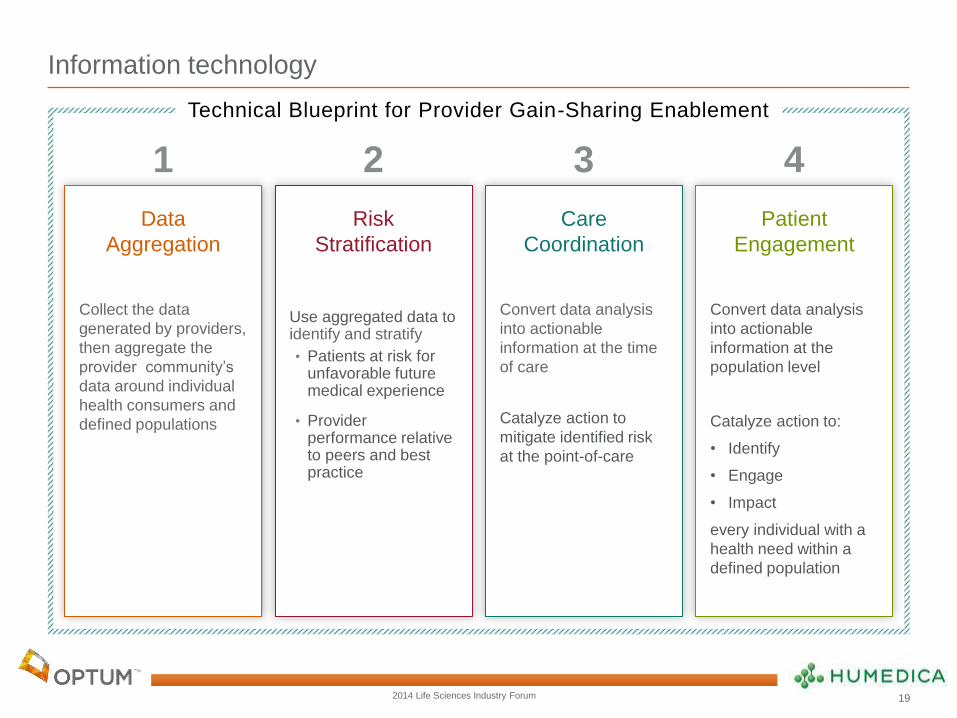

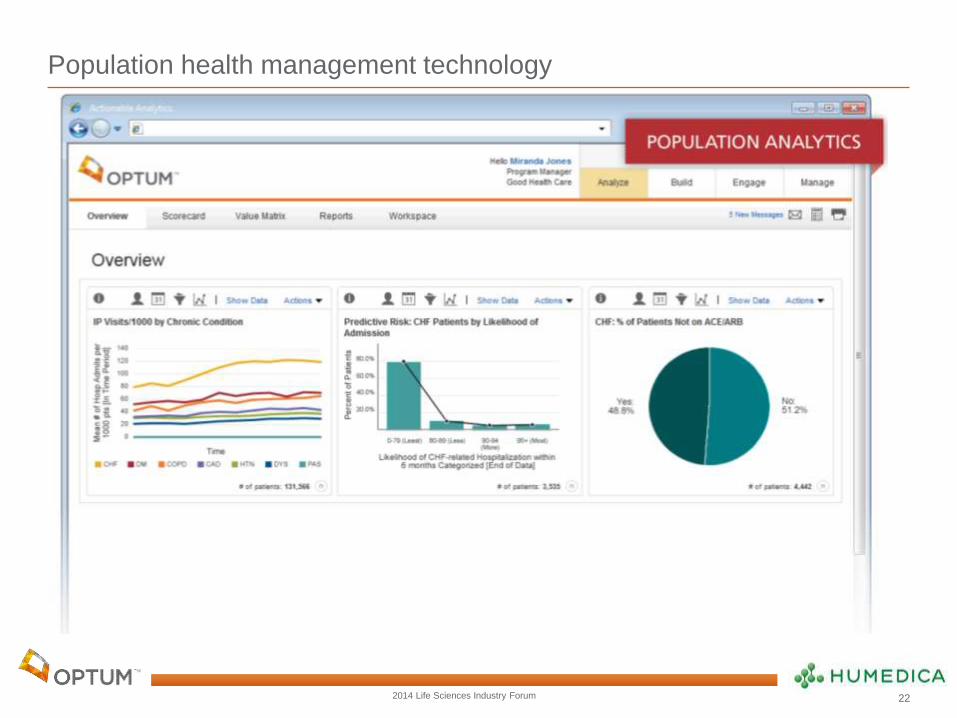

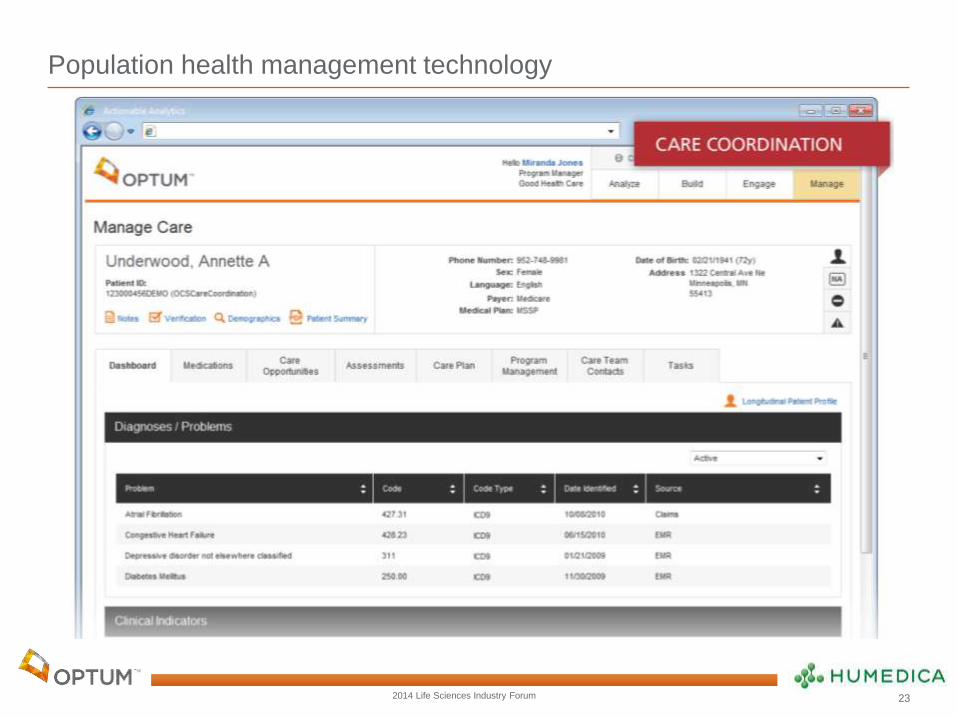

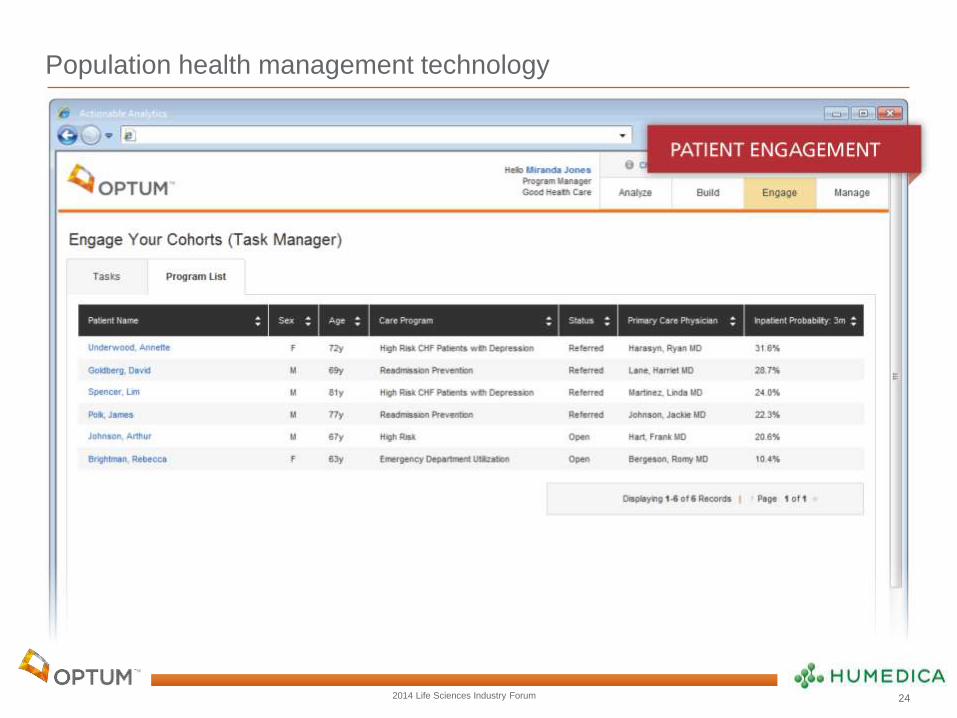

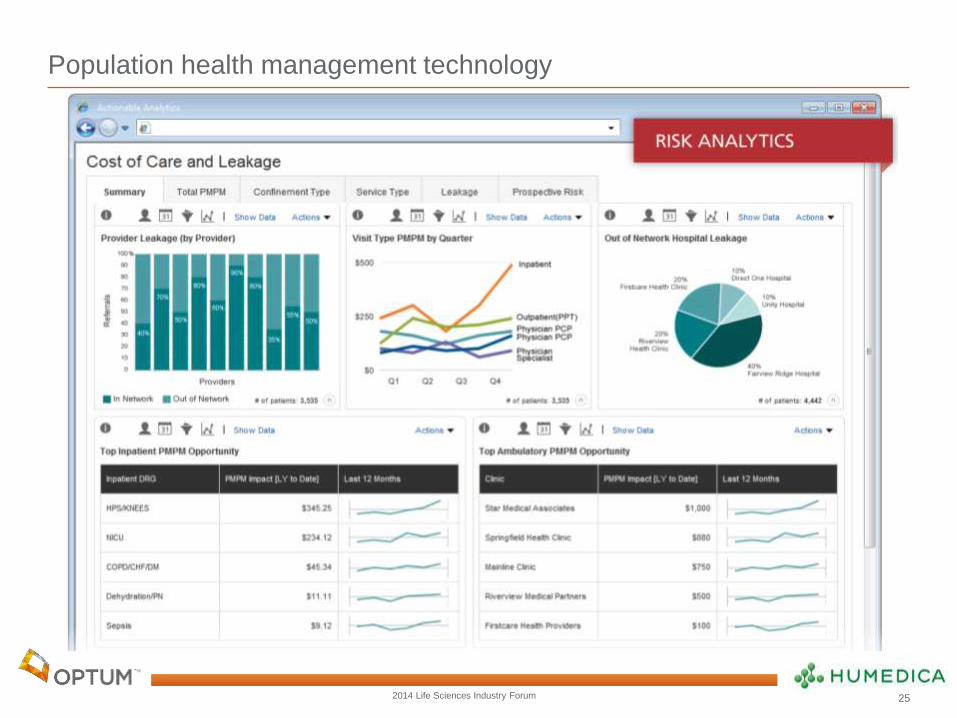

Information technology

Technical Blueprint for Provider Gain-Sharing Enablement

Data

Aggregation

Collect the data

generated by providers,

then aggregate the

provider community’s

data around individual

health consumers and

defined populations

Risk

Stratification

Use aggregated data to identify and stratify

• Patients at risk for unfavorable future medical experience

• Provider performance relative to peers and best practice

Care

Coordination

Convert data analysis

into actionable

information at the time

of care

Catalyze action to

mitigate identified risk

at the point-of-care

Patient

Engagement

Convert data analysis

into actionable

information at the

population level

Catalyze action to:

• Identify

• Engage

• Impact

every individual with a

health need within a

defined population

1 2 3 4

19

2014 Life Sciences Industry Forum

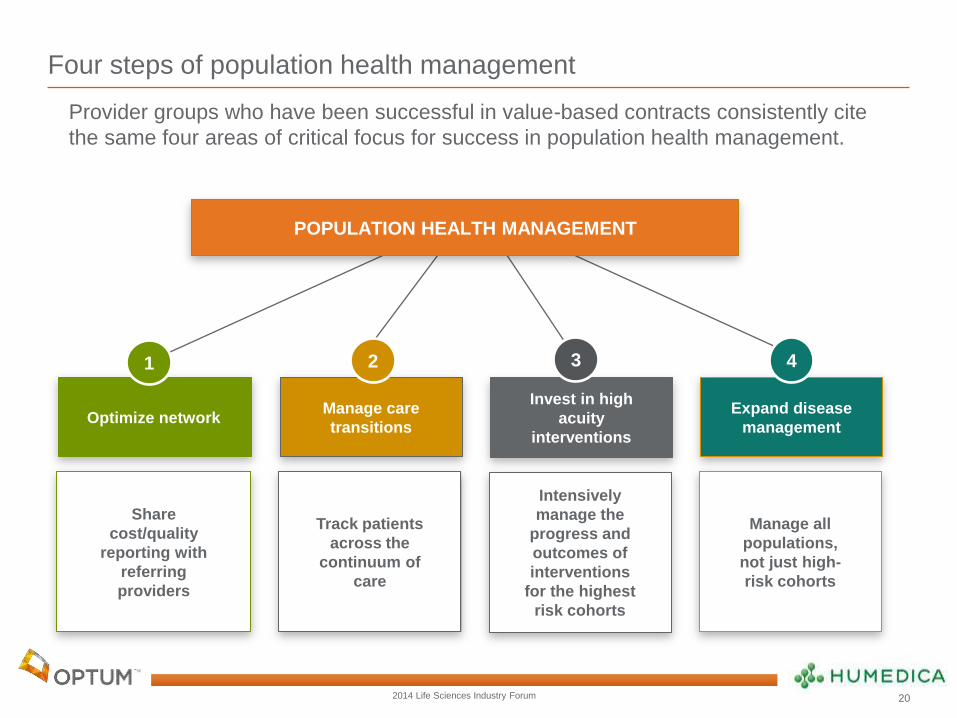

Four steps of population health management

Optimize network

Invest in high

acuity

interventions

Manage care

transitions

Expand disease

management

POPULATION HEALTH MANAGEMENT

1 2 3 4

Share

cost/quality

reporting with

referring

providers

Intensively

manage the

progress and

outcomes of

interventions

for the highest

risk cohorts

Track patients

across the

continuum of

care

Manage all

populations,

not just high-

risk cohorts

Provider groups who have been successful in value-based contracts consistently cite

the same four areas of critical focus for success in population health management.

20

2014 Life Sciences Industry Forum

Actionable information begins with the right data

Analytics to predict future medical costs of individuals and populations are limited by the characteristics of the types of available data:

Claims data Clinical data

Socio-demographic

and Care

Management data

– insensitive

– non-specific

– untimely

+ always available

+ sensitive

+ specific

+ timely

– variably available (may be

incomplete or

unstructured

in EMR, or unavailable

from non-EMR users)

+ sensitive

– non-specific

+ timely

+ generally available

21

2014 Life Sciences Industry Forum

Population health management technology

22

2014 Life Sciences Industry Forum

Population health management technology

23

2014 Life Sciences Industry Forum

Population health management technology

24

2014 Life Sciences Industry Forum

Population health management technology

25