payment systems

TRANSCRIPT

PAYMENT SYSTEMS IN BANKING

• SUSHIL KAMBLE PRN NO.10020242034• VARUN PATNI PRN NO.10020242031• VIMAL PANJWANI PRN NO.10020242032• VISHAL RATAN PRN NO.10020242033

PAYMENT SYSTEM:Under bank of international settlement(BIS) definition, a payment system consist of instruments, banking procedures and typically interbank funds transfer that ensures and facilitate the circulation of money. In essence, it facilitates corporation, businesses and consumers to transfer funds to one other.

History OF PAYMENT SYSTems

Earliest instruments used:- CoinsPreviously loan deed forms used, these contains:- Rate of interest Condition of repayment Time of repaymentMost important class of credit instrument is hundis, used as: A remmitance instrument(to transfer funds from one place to other) Credit instrument(to borrow money) Trade transactions(as bills of exchange)

Moving forward to paper money.

Origin in 18th century: Earlier issued by private banks and semi government banks,earliest of

them were:- General bank in Bengal Bengal banks Later 3 presidency banks established. Paper currency act 1961, gives monopoly to government to issue notes,

end to issue notes by private and presidency banks. Other payment instruments include cheques(introduced by bank of

Hindustan, estb. 1770) In 1883,cash credit account added to bank of bengal’s array of credit

instruments(includes granting loans against security of company’s paper, bullion, jewels etc.

CONTINUED… Buying and selling bills of exchange become one of

items of business to be conducted by bank of Bengal from 1839.

In 1881, the negotiable instrument act(NI). Formalizing usage of instruments like cheque, bills of exchange, promissory notes, provide legal framework for non-cash paper payment instrument.

MILESTONES OF EVOLUTION OF PAYMENT SYSTEMS IN INDIA:

• The CLEARING SYSTEM in India provides a convenient and well established institutional mechanism to take care of the problem of physical delivery of instruments as well as funds transfer between different banks.

• Computerization of clearing operations was the first major step towards modernization of the payments system. The next important milestone was mechanization of the clearing operations with the introduction of Magnetic Ink Character Recognition (MICR) based cheque processing technology (in 1986) using High Speed Reader Sorter Systems (HSRS).

CONTINUED..• The Computerized Cheque Clearing Process has been

further consolidated through the introduction of magnetic media based input settlement as an Electronic Banking and Payment System – Reading Material 31 intermediate step towards complete automation of cheque clearing through MICR processing especially to facilitate the high-value and inter-bank clearing.

• Greyscale Imaging Technology has been introduced (in 2000) as a value added service to the members of the Clearing Houses in some cities which will serve as a forerunner for the introduction of electronic presentment and cheque truncation.

CONTINUED…• The Electronic Clearing Service (ECS) was introduced (in

1994) whereby a series of electronic payment instructions are generated to replace paper instruments to meet the requirement of a cost-effective system which would serve as an alternate method of effecting bulk, low value, recurring payment transactions, thereby obviating the need to issue and handle paper instruments.

• Another development that took place in the payments system scenario was the introduction of the Electronic Funds Transfer Scheme (in 1998) which is a retail funds transfer system and enables an account holder of a bank to transfer funds to another person having an account with any of the participating banks, without any physical movement of instruments from one center to another.

CONTINUED…

• Centralised Funds Management System (CFMS) – was introduced (in 2002) to facilitate better funds management by account holders with RBI byproviding on-line consolidated information about their transactions / balances across accounts maintained with Deposit Accounts Departments in different offices.

• Negotiated Dealing System / Securities Settlement System - NDS/SSS – was developed (in 2002) as a system to provide an electronic platform for trading and reporting of transactions in government securities market and to facilitate settlement of these transactions through the delivery versus payment mechanism.

CONTINUED…

• Clearing of Forex transactions – was instituted (in 2002) as a system to provide net settlement arrangement for forex transactions between members /entities in the foreign exchange market in the country. The process of settling only net obligations reduced the liquidity requirements of foreign currency, sought to reduce transaction costs (SWIFT related) and also take care of settlement related risks since the mechanism was facilitated by guaranteed settlement through central counter party arrangement of the Clearing Corporation of India.

CONTINUED…

• Real Time Gross Settlement (RTGS) System – was introduced (in 2004) to facilitate predominantly the settlement of inter-bank payments on a real-time and gross basis so as to reduce the incidence of risks in the payment systems.

ROLE OF RBI IN PAYMENT SYSTEMS:• The Reserve Bank of India participates in the

payment systems as a user of the system, as the service provider for various components of the systems and is also the regulator of the systems in many instances.

CONTINUED…

• As a user, the RBI submits instruments for clearing in the cheque-based clearing operations.

• RBI also participates as an user in the ECS and EFT systems for making its own internal payments to its employees, vendor payments etc.

• Similarly, RBI transactions in Repo / Reverse Repo under LAF, Open Market Operations etc.,would also be settled through the respective components of payment systems.

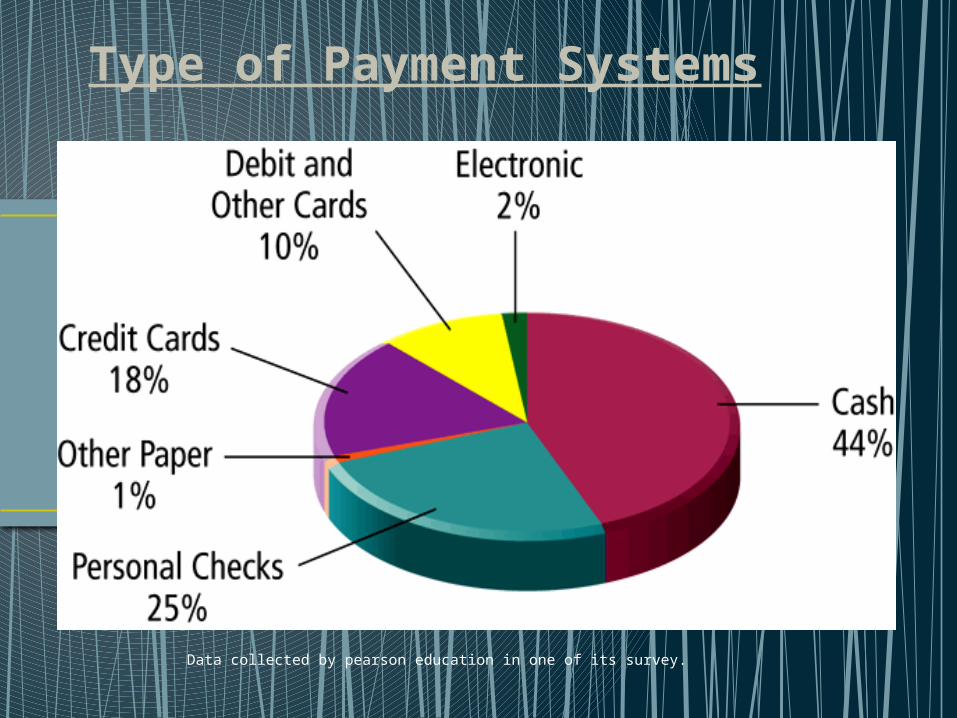

Type of Payment Systems

Data collected by pearson education in one of its survey.

Cash

Legal tender defined by a national authority to

represent value Most common form of payment in terms of number of

transactions Instantly convertible into other forms of value without

intermediation of any kind Portable, requires no authentication, and provides

instant purchasing power “Free” (no transaction fee), anonymous, low cognitive

demands Limitations: easily stolen, limited to smaller

transaction, does not provide any float (the period of

time between a purchase and actual payment for the purchase.

Checking Transfer

Funds transferred directly via a signed draft or check

from a consumer’s checking account to a merchant

or other individual

Most common form of payment in terms of amount

spend

Can be used for both small and large transactions

Some float

Not anonymous, require third-party intervention

(banks)

Introduce security risks for merchants (forgeries,

stopped payments), so authentication typically required.

Credit Card Represents an account that extends credit to

consumers, permitting consumers to purchase items

while deferring payment, and allows consumers to

make payments to multiple vendors at one time

Credit card associations – Nonprofit associations

(Visa, MasterCard) that set standards for issuing

banks

Issuing banks – Issue cards and process transactions

Processing centers (clearinghouses) – Handle

verification of accounts and balances.

Stored Value

Accounts created by depositing funds into an

account and from which funds are paid out or

withdrawn as needed

Examples: Debit cards, gift certificates,

prepaid cards, smart cards

Debit cards: Immediately debit a checking or

other demand-deposit account

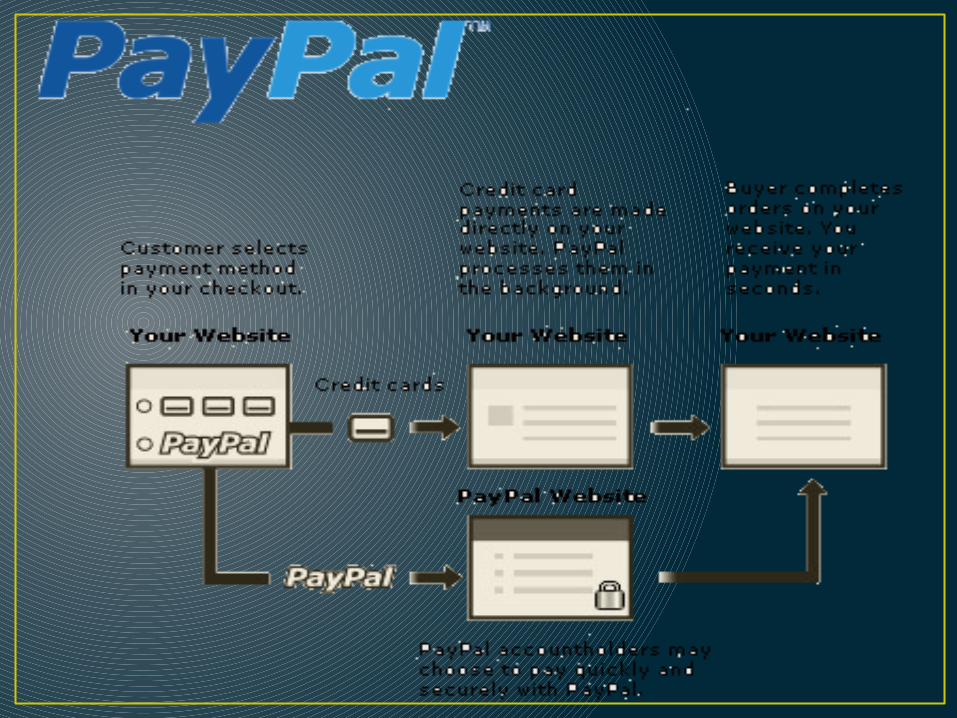

Peer-to-peer payment systems such as

PayPal a variation

Accumulating Balance

Accounts that accumulate expenditures and

to which consumers make period payments Examples: utility, phone, American Express

accounts

Current Online Payment Systems

Credit cards are dominant form of online payment,

accounting for around 80% of online payments in

2002

New forms of electronic payment include:

Digital cash

Online stored value systems

Digital accumulating balance payment systems

Digital credit accounts

Digital checking

• E-commerce payment system facilitates the acceptance of ELECTRONIC PAAY MENT for ONLINE TRANSACTIONS.

• Also known as ELECTRONIC DATA INTERCHANGE(EDI), e-commerce payment systems have become increasingly popular due to the widespread use of the internet-based shopping and banking.

FACTS AND EXAPMLES:• In the early years of B2C transactions, many

consumers were apprehensive of using their credit and debit cards over the internet because of the perceived increased risk of fraud.

• Recent research shows that 30% of people in the United Kingdom still do not shop online because they do not trust online payment systems.

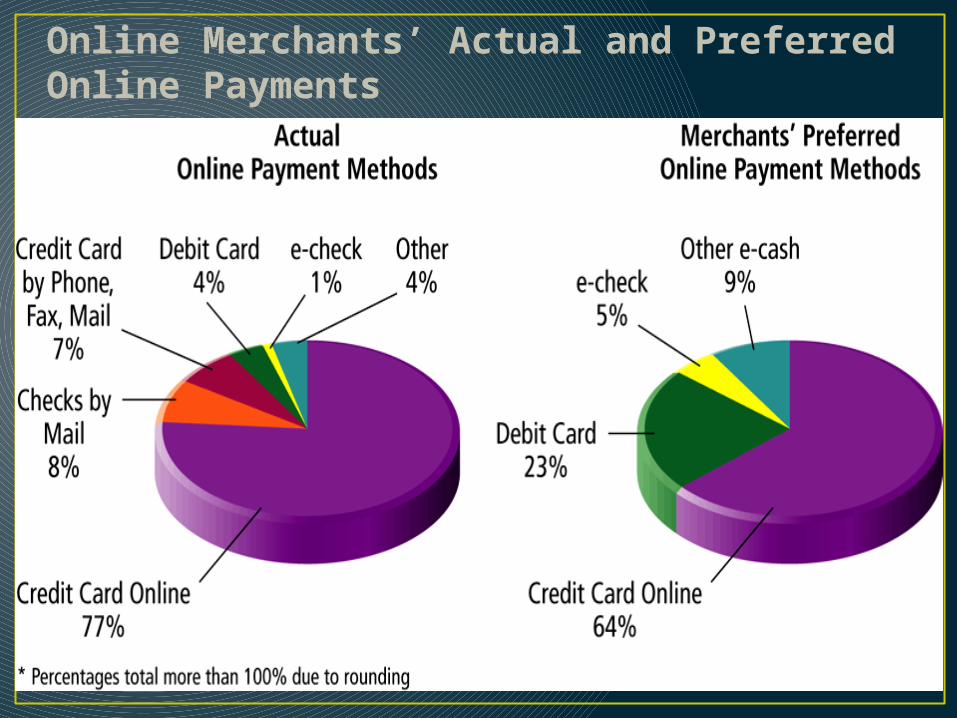

Online Merchants’ Actual and Preferred Online Payments

ORGANISATION STRUCTURE:• In order to usher in and establish a modern,

robust payments and settlement system consistent with international best practices, the Reserve Bank has adopted a three-pronged strategy of Consolidation of existing Payment Systems, Development of Payment Systems and Integration of the Payment and Settlement System. In order to drive this Payment System reform process an institutional framework and structure has been created within the Reserve Bank.

PAYMENT SYSTEMS GROUP:• The base layer of this structure consisted of the

Payment Systems Group, which included an exclusive team of inter-disciplinary professionals representing IT, Banking Operations, Supervision, Legal, Economics, Government & Bank Accounts, and Foreign Exchange operations.

PAYMENT SYSTEMS ADVISORY COMMITTEE:• The next tier in the institutional framework is the

Payment Systems Advisory Committee which is a permanent body and oversees the operations of the Payment Systems Group and reviews the developments in the area of Payment Systems.

NATIONAL PAYMENTS COUNCIL:• The apex layer in the institutional structure is the

National Payments Council. The council lays down the broad policy framework and guidelines for the implementation of a sound and efficient payments and settlement system for the country.

OVERSIGHT ARRANGEMENTS:• Continuous efforts are being made by the Bank to

ensure that the systems operated by it are complying with the requirements of the core principles – both in case of already existing payments systems and the ones being introduced newly. Broadly, the RBI derives its regulatory and supervisory powers over the banking system through the provisions of Banking Regulation Act, 1949.