pbt1-12912 2002 annual reportpbt-permian.com/annual_quarterly/pbtannual2002.pdf · to unit holders...

TRANSCRIPT

P e r m i a n B a s i n R o y a l t y T r u s t A n n u a l R e p o r t & F o r m 1 0 - K 2 0 0 2

The Trust

The Permian Basin Royalty Trust’s (the “Trust”) principal assets are comprised of a 75% net overriding royalty interest carved

out by Southland Royalty Company (“Southland”) from its fee mineral interest in the Waddell Ranch properties in Crane

County, Texas (“Waddell Ranch properties”), and a 95% net overriding royalty interest carved out by Southland from its

major producing royalty properties in Texas (“Texas Royalty properties”). The interests out of which the Trust’s net overriding

royalty interests were carved were in all cases less than 100%. The Trust’s net overriding royalty interests represent burdens

against the properties in favor of the Trust without regard to ownership of the properties from which the overriding royalty

interests were carved. The net overriding royalties above are collectively referred to as the “Royalties.” The properties and

interests from which the Royalties were carved and which the Royalties now burden are collectively referred to as the

“Underlying Properties.”

The Trust has been advised that effective January 1, 1996, Southland was merged with and into Meridian Oil Inc.

(“Meridian”), a Delaware corporation, with Meridian being the surviving corporation. Meridian succeeded to the ownership

of all the assets, has the rights, powers and privileges, and assumed all of the liabilities and obligations of Southland.

Effective July 11, 1996, Meridian changed its name to Burlington Resources Oil & Gas Company (“BROG”). Any reference to

BROG hereafter for periods prior to the occurrence of the aforementioned name change or merger should, as applicable, be

construed to be a reference to Meridian or Southland. Further, BROG notified the Trust that, on February 14, 1997, the Texas

Royalty properties that are subject to the Net Overriding Royalty Conveyance dated November 1, 1980 (“Texas Royalty

Conveyance”), were sold to Riverhill Energy Corporation (“Riverhill Energy”) of Midland, Texas.

Units of Beneficial InterestUnits of Beneficial Interest (“Units”) of the Trust are traded on the New York Stock Exchange with the symbol PBT. Quarterly

high and low sales prices and the aggregate amount of monthly distributions paid each quarter during the Trust’s two most

recent years were as follows:

Distributions2002 High Low Paid

First Quarter ________________________________________ $5.650 $4.970 $.094796

Second Quarter ______________________________________ 5.950 5.000 .118491

Third Quarter ________________________________________ 5.350 4.500 .133892

Fourth Quarter ______________________________________ 6.400 5.070 .155203

Total for 2002 ___________________________________ $.502382

2001

First Quarter ________________________________________ $6.700 $5.625 $.256445

Second Quarter ______________________________________ 6.850 5.000 .256094

Third Quarter ________________________________________ 6.530 5.500 .179718

Fourth Quarter ______________________________________ 5.950 5.200 .154651

Total for 2001 ____________________________________ $.846908

Approximately 2,363 Unit holders of record held the 46,608,796 Units of the Trust at December 31, 2002.

Texas Royalty properties are located in 33 Texas counties.

Waddell Ranch properties are located in Crane County.

Andrews

Borden

Brazoria

Calhoun

Crane

Crockett

Ector

Gaines

Glasscock

Gray

Grayson

Gregg

Hale

Hockley

Howard

Hutchinson

Lubbock

Mitchell

Montgomery

Nueces

Pecos

Reagan

Scurry

Stonewall

Terry

Upshur

Upton

Van Zandt

Waller

Ward

Winkler

Wood

Yoakum

1

To Unit Holders

We are pleased to present the twenty-third Annual Report of

the Trust. The report includes a copy of the Trust’s Annual

Report on Form 10-K to the Securities and Exchange

Commission for the year ended December 31, 2002, without

exhibits. Both the report and accompanying Form 10-K

contain important information concerning the Trust’s properties,

including the oil and gas reserves attributable to the Royalties

owned by the Trust. Production figures, drilling activity and

certain other information included in this report have been

provided to the Trust by BROG (formerly Meridian and Southland).

As more particularly explained in the Notes to the

Financial Statements appearing in this report and in Item 1

of the accompanying Form 10-K, Bank of America, N.A., as

Trustee, has the primary function under the Trust Indenture

of collecting the monthly net proceeds attributable to the

Royalties and making monthly distributions to the Unit holders,

after deducting Trust administrative expenses and any amounts

necessary for cash reserves.

Royalty income received by the Trustee for the year

ended December 31, 2002, was $23,830,604 and interest

income earned for the same period was $17,140. General and

administrative expenses amounted to $432,338. A total of

$23,415,406 or $.502382 per Unit was distributed to Unit

holders during 2002. A discussion of factors affecting the

distributions for 2002 may be found in the Trustee’s Discussion

and Analysis section of this report and the accompanying

Form 10-K.

As of December 31, 2002, the Trust’s proved reserves were

estimated at 7,497,000 Bbls of oil and 28,506,000 Mcf of gas.

The estimated future net revenues from proved reserves at

December 31, 2002, amount to $294,576,000 or $6.32 per

Unit. The present value of estimated future net revenues

discounted at 10% at December 31, 2002, was $161,875,000

or $3.47 per Unit. The computation of future net revenues

is made following guidelines prescribed by the Financial

Accounting Standards Board (explained in Item 2 of the

accompanying Form 10-K) based on year-end prices and costs.

As has been previously reported, Southland advised the

Trust that it became operator of record of the Waddell Ranch

properties on May 1, 1991. Meridian, as successor by merger,

became the operator of record effective January 1, 1996.

Meridian changed its name to Burlington Resources Oil & Gas

Company in 1996. All field, technical and accounting

operations, however, have been carried out by Schlumberger

Technology Corporation (“STC”) and Riverhill Capital

Corporation (“Riverhill Capital”), but remain under the

direction of BROG.

As was previously reported, in February 1997, BROG sold

its interest in the Texas Royalty properties that are subject to

the Texas Royalty Conveyance to Riverhill Energy, which at the

time was a wholly-owned subsidiary of Riverhill Capital and an

affiliate of STC. Subsequently, the Trustee was advised that STC

acquired all of the shares of Riverhill Capital. The Trustee has

been advised that, as part of this transaction, ownership of

Riverhill Energy’s interests in the Texas Royalty properties

referenced above remain in Riverhill Energy, which was owned

by the former shareholders of Riverhill Capital. STC will continue

to perform all accounting operations pertaining to the Texas

Royalty properties under the direction of Riverhill Energy.

Percentage depletion is allowed on proven properties

acquired after October 11, 1990. For Units acquired after such

date, Unit holders would normally compute both percentage

depletion and cost depletion from each property, and claim the

larger amount as a deduction on their income tax returns. The

Trustee and its accountants have estimated the percentage

depletion for January through December 2002, and it appears

that cost depletion will exceed percentage depletion for all

Unit holders.

Royalty income is generally considered portfolio income

under the passive loss rules. Therefore, in general, it appears

that Unit holders should not consider the taxable income from

the Trust to be passive income in determining net passive

income or loss. Unit holders should consult their tax advisors

for further information.

Unit holders of record will continue to receive an

individualized tax information letter for each of the quarters

ending March 31, June 30 and September 30, 2003, and for

the year ending December 31, 2003. Unit holders owning Units

in nominee name may obtain monthly tax information from

the Trustee upon request.

Bank of America, N.A., Trustee

By:

Ron E. Hooper

Senior Vice President

2

Description of the Properties

The net overriding royalty interests held by the Trust are

carved out of high-quality producing oil and gas properties

located primarily in West Texas. A production index for oil and

gas properties is the number of years derived by dividing

remaining reserves by current production. The production index

for the Trust properties based on the reserve report prepared

by independent petroleum engineers as of December 31, 2002,

is approximately 6.26 years.

The net profits/overriding royalty interest in the Waddell

Ranch properties is the largest asset of the Trust. The mineral

interests in the Waddell Ranch, from which such net royalty

interests are carved, vary from 37.5% (Trust net interest) to

50% (Trust net interest) in 76,922 gross acres and 33,276 net

acres, containing 765 gross (339 net) productive oil wells,

184 gross (88 net) productive gas wells and 324 gross (141

net) injection wells.

Six major fields on the Waddell Ranch properties account

for more than 90% of the total production. In the six fields,

there are 12 producing zones ranging in depth from 2,800 to

10,600 feet. Most prolific of these zones are the Grayburg and

San Andres, which produce from depths between 2,800 and

3,400 feet. Productive from the San Andres are the Sand Hills

(Judkins) gas field and the Sand Hills (McKnight) oil field.

The Dune and Waddell oil fields are productive from both

the Grayburg and San Andres formations. The Sand Hills (Tubb)

oil fields produce from the Tubb formation at depths averaging

4,300 feet, and the University Waddell (Devonian) oil field is

productive from the Devonian formation between 8,400 and

9,200 feet.

All of the major oil fields on the Waddell Ranch properties

are currently being water flooded. Engineering studies and 3-D

seismic evaluations on these fields indicate the potential for

increased production through infill drilling, modifications of

existing water flood techniques, installation of larger capacity

pumping equipment and tertiary recovery projects. Capital

expenditures for remedial and maintenance activities during

2002 totaled approximately $9.9 million.

The Texas Royalty properties, out of which the other

net overriding royalty was carved, are located in 33 counties

across Texas. The Texas Royalty properties consist of

approximately 125 separate royalty interests containing

approximately 303,000 gross (51,000 net) producing acres.

Approximately 41% of the future net revenues discounted

at 10% attributable to Texas Royalty properties are located

in the Wasson and Yates fields.

BROG has informed the Trustee that the 2003 capital

expenditures budget should total approximately $13.207 million

gross, of which $1.940 million gross is attributable to drilling,

$9.909 million gross to workovers and $1.358 million gross

to facilities.

COMPUTATION OF ROYALTY INCOME RECEIVED BY THE TRUST

The Trust’s royalty income is computed as a percentage of the

net profit from the operation of the properties in which the

Trust owns net overriding royalty interests. The percentages

of net profits are 75% and 95% in the cases of the Waddell

Ranch properties and the Texas Royalty properties, respectively.

Royalty income received by the Trust for the five years ended

December 31, 2002, was computed as shown in the table on

the next page.

3

(a) The Trust received funds in 1998 from BROG which represented the Trust’s portion of amounts that had been previously held in

suspense by BROG relating to the Texas Royalty properties. The Trustee was advised that these amounts relate to revenues received

by BROG prior to the conveyance of its interest in the Texas Royalty properties to Riverhill Energy in February 1997.

(b) In calculating Trust royalty income for the months of June through December 1998, costs exceeded revenues for the Waddell

Ranch properties underlying the Waddell Ranch Net Overriding Royalty Conveyance dated effective November 1, 1980 (“Waddell Ranch

Conveyance”), by $1,218,732. Pursuant to the Waddell Ranch Conveyance, excess costs plus accrued interest must be recovered from

future net proceeds relating to the underlying Waddell Ranch properties before the properties can again contribute to Trust royalty

income. Cumulative excess amounts were fully recovered in February 1999.

(c) In November 1998, the Trust received its portion of settlement proceeds totaling $766,051 from a class-action lawsuit.

Year Ended December 31,2002 2001 2000 1999 1998

Gross Proceeds Waddell Texas Waddell Texas Waddell Texas Waddell Texas Waddell Texasof Sales Ranch Royalty Ranch Royalty Ranch Royalty Ranch Royalty Ranch RoyaltyFrom the Underlying Properties Properties Properties Properties Properties Properties Properties Properties Properties PropertiesProperties:

Oil Proceeds $20,543,224 $ 7,785,749 $26,477,679 $ 9,524,586 $31,289,829 $ 9,770,732 $18,667,382 $ 5,261,863 $18,821,076 $ 5,404,598Gas Proceeds 14,861,094 2,245,648 26,068,379 3,771,184 18,342,926 2,701,298 12,794,695 1,760,499 13,769,872 1,880,571Other Payments (a) – – – – – – – – – 540,543

Total 35,404,318 10,031,397 52,546,058 13,295,770 49,632,755 12,472,030 31,462,077 7,022,362 32,590,948 7,825,712Less:

Severance TaxOil 863,299 302,665 1,108,968 374,204 1,288,522 373,643 726,944 186,846 725,100 196,770Gas 813,581 159,431 1,160,095 239,337 1,189,617 146,512 773,689 77,379 (1,299,730) 104,759Other 72,396 – – – 26,991 – 44,839 16,000 – –

Lease Operating Expense and Property Tax

Oil and Gas 9,424,724 933,646 9,086,468 605,125 9,318,915 442,523 9,687,476 525,035 14,096,881 790,246Other Payments – – 50,000 – – – 132,166 180,000 – –

Capital Expenditures 3,394,674 – 3,350,003 – 4,606,227 – 1,052,769 – 15,874,193 –Total 14,568,674 1,395,742 14,755,534 1,218,666 16,430,272 962,678 12,417,883 985,260 29,396,444 1,091,775

Net Profits 20,835,643 8,635,655 37,790,525 12,077,104 33,202,483 11,509,352 19,044,194 6,037,102 3,194,504 6,733,937Net OverridingRoyalty Interest 75% 95% 75% 95% 75% 95% 75% 95% 75% 95%

Royalty Income 15,626,732 8,203,852 28,342,893 11,473,248 24,901,862 10,933,884 14,284,146 5,735,247 2,395,878 6,397,240Negative Revenue (b) – – – – – – 1,218,732 – 1,218,732 –Litigation Settlement (c) – – – – – – – – 766,051 –Total Royalty Income for Distribution $15,626,732 $ 8,203,852 $28,342,893 $11,473,248 $24,901,862 $10,933,884 $13,064,414 $ 5,735,247 $ 4,380,661 $ 6,397,240

4

Discussion and Analysis

TRUSTEE’S DISCUSSION AND ANALYSIS FOR THE THREE-YEAR

PERIOD ENDED DECEMBER 31, 2002

Critical Accounting Policies and Estimates

The trust’s financial statements reflect the selection and

application of accounting policies that require the Trust to

make significant estimates and assumptions. The following are

some of the more critical judgment areas in the application

of accounting policies that currently affect the Trust’s financial

condition and results of operations.

1. Revenue Recognition

Revenues from Royalty Interests are recognized in the period

in which amounts are received by the Trust. Royalty income

received by the Trust in a given calendar year will generally

reflect the proceeds, on an entitlement basis, from natural

gas produced for the twelve-month period ended September

30th in that calendar year.

2. Reserve Recognition

Independent petroleum engineers estimate the net proved

reserves attributable to the Royalty Interest. In accordance with

Statement of Financial Standards No. 69, “Disclosures About Oil

and Gas Producing Activities,” estimates of future net revenues

from proved reserves have been prepared using year-end

contractual gas prices until additional information becomes

available. The reserves actually recovered and the timing of

production may be substantially different from the reserve

estimates and related costs. Numerous uncertainties are inherent

in estimating volumes and the value of proved reserves and

in projecting future production rates and the timing of

development of non-producing reserves.

3. Contingencies

Contingencies related to the Underlying Properties that are

unfavorably resolved would generally be reflected by the Trust

as reductions to future royalty income payments to the Trust

with corresponding reductions to cash distributions to

Unit holders.

4. New Accounting Pronouncements

Statement of Financial Accounting Standard (“SFAS”) No. 143,

“Accounting for Asset Retirement Obligations,” was issued by

the Financial Accounting Standards Board (“FASB”) in June

2001 and will be adopted by the Trust on January 1, 2003.

This Statement addresses financial accounting and reporting

for obligations associated with the retirement of tangible

long-lived assets and the associated asset retirement costs.

The effect of adopting SFAS No. 143 will not have a material

impact on the Trust’s financial statements.

SFAS No. 145, “Rescission of FASB Statements No. 4, 44,

and 64, Amendment of FASB Statement No. 13, and Technical

Corrections,” was issued in April 2002 and is effective for

fiscal years beginning after May 15, 2002. This Statement

includes the rescission of FASB Statement No. 4, “Reporting

Gains and Losses from Extinguishment of Debt,” and an

amendment to FASB Statement No. 13, “Accounting for

Leases,” to eliminate an inconsistency between the required

accounting for sale-leaseback transactions and the required

accounting for certain lease modifications that have economic

effects that are similar to sale-leaseback transactions. The

effect of adopting SFAS No. 145 will not have a material

impact on the Trust’s financial statements.

SFAS No. 146, “Accounting for Costs Associated with

Exit or Disposal Activities,” was issued in June 2002 and

will be effective for exit or disposal activities subsequent to

December 31, 2002. The Trust anticipates no material impact

on its financial statements from the adoption of this

accounting standard.

SFAS No. 148, “Accounting for Stock-Based Compensation

– Transition and Disclosure, an amendment of FASB Statement

No. 123,” was issued in December 2002 and provides new

transition methods if an entity adopts the fair value based

method of valuing stock-based compensation suggested in

SFAS No. 123, “Accounting for Stock-Based Compensation,”

as well as requiring additional disclosures in interim and

annual financial statements. The Trust has no options or other

stock-based instruments and accordingly, the impact of this

new Standard is not expected to be material to the financial

statements of the Trust.

5

Discussion and Analysis (continued)

FASB Interpretation (“FIN”) No. 45, “Guarantor’s

Accounting and Disclosure Requirements for Guarantees,

Including Indirect Guarantees of Indebtedness of Others,”

requires disclosures beginning with financial statements

ending after December 15, 2002, and requires liability

recognition beginning January 1, 2003. The Trust had no

such guarantees outstanding as of December 31, 2002.

FIN No. 46, “Consolidation of Variable Interest Entities,”

was issued in January 2003. This interpretation of Accounting

Research Bulletin No. 51, “Consolidated Financial Statements,”

applies immediately to variable interest entities created after

January 31, 2003, and applies to the first period beginning

after June 15, 2003, to entities acquired before February 1,

2003. This FIN does not affect the Trust as it has no

unconsolidated subsidiaries accounted for under the equity

method of accounting.

LIQUIDITY AND CAPITAL RESOURCES

As stipulated in the Trust Agreement, the Trust is intended to

be passive in nature and the Trustee does not have any control

over or any responsibility relating to the operation of the

Underlying Properties. The Trustee has powers to collect

and distribute proceeds received by the Trust and pay Trust

liabilities and expenses, and its actions have been limited to

those activities. The Trust is a passive entity, and other than

the Trust’s ability to periodically borrow money as necessary

to pay expenses, liabilities and obligations of the Trust that

cannot be paid out of cash held by the Trust, the Trust is

prohibited from engaging in borrowing transactions. As a

result, other than such borrowings, if any, the Trust has no

source of liquidity or capital resources other than the Royalties.

Year Ended December 31,

Royalties 2002 2001 2000Total Revenue $23,830,604 $39,816,141 $35,835,746

100% 100% 100%

Oil Revenue 15,013,280 22,466,757 24,901,862

63% 56% 70%

Gas Revenue 8,817,324 17,349,384 10,933,884

37% 44% 32%

Total Revenue/Unit $ .511289 $ .854327 $ .768862

RESULTS OF OPERATIONS

Royalty income received by the Trust for the three-year period ended December 31, 2002, is reported in the following table:

6

Royalty income of the Trust for the calendar year is associated with actual oil and gas production for the period November of

the prior year through October of the current year. Oil and gas sales for 2002, 2001 and 2000 for the Royalties and the Underlying

Properties, excluding portions attributable to the adjustments discussed hereafter, are presented in the following table:

Year Ended December 31,

Royalties 2002 2001 2000Oil Sales (Bbls) 728,313 941,202 919,429

Gas Sales (Mcf) 3,192,175 3,875,586 3,346,445

Underlying Properties

Oil

Total Oil Sales (Bbls) 1,272,923 1,434,983 1,486,110

Average Per Day (Bbls) 3,489 3,931 4,072

Average Price/Bbl $22.31 $24.88 $27.66

Gas

Total Gas Sales (Mcf) 6,189,015 6,441,298 5,890,023

Average Per Day (Mcf) 16,956 17,593 16,137

Average Price/Mcf $2.74 $4.70 $3.63

The average price of oil decreased to $22.21 per barrel in

2002, down from $24.88 per barrel in 2001. In addition, the

average price of gas declined from $4.70 per Mcf in 2001 to

$2.76 per Mcf in 2002.

Since the oil and gas sales attributable to the Royalties

are based on an allocation formula that is dependent on such

factors as price and cost (including capital expenditures),

production amounts do not necessarily provide a meaningful

comparison. Total oil production decreased approximately 11%

from 2002 to 2001 primarily due to lower capital expenditures

in previous years. Total gas sales decreased approximately 4%

from 2002 to 2001 primarily due to a decrease in capital

expenditures for gas wells.

Total capital expenditures in 2002 used in the net

overriding royalty calculation were approximately $9.9 million

compared to $3.4 million in 2001 and $4.6 million in 2000.

During 2002, there were 4 gross (1.75 net) wells drilled

and completed on the Waddell Ranch properties. At

December 31, 2002, there were no wells in progress on

the Waddell Ranch properties.

In 2002, lease operating expense and property taxes

on the Waddell Ranch properties amounted to approximately

$9.4 million, which amount was approximately the same as

in 2001.

The Trustee has been advised by BROG that for the

period August 1, 1993, through June 30, 2003, the oil from

the Waddell Ranch was sold under a competitive bid to a

third party.

During 2002, the monthly royalty receipts were invested

by the Trustee in U.S. Treasury securities until the monthly

distribution date, and earned interest totaled $17,140.

Interest income for 2001 and 2000 was $77,977 and $85,348,

respectively.

General and administrative expenses in 2002 were $432,338

compared to $420,723 in 2001 and $375,953 in 2000.

Distributable income for 2002 was $23,415,406, or

$.502382 per Unit. Distributable income for 2001 was

$39,473,395 or $.846908 per Unit. Distributable income

for 2000 was $35,545,141 or $.762627 per Unit.

7

Results of the Fourth Quarters of 2002 and 2001

the fourth quarter of 2002 compared to $49,388 for the fourth

quarter of 2001.

Royalty income for the Trust for the fourth quarter is

associated with actual oil and gas production during August

through October from the Underlying Properties. Oil and

gas sales attributable to the Royalties and the Underlying

Properties for the quarter and the comparable period for

2001 are as follows:

Fourth Quarter 2002 2001

RoyaltiesOil Sales (Bbls) 185,131 226,307

Gas Sales (Mcf) 874,957 943,738

Fourth Quarter 2002 2001

Underlying PropertiesTotal Oil Sales (Bbls) 309,368 350,921

Average Per Day (Bbls) 3,363 3,814

Average Price/Bbls $26.53 $22.52

Total Gas Sales (Mcf) 1,593,780 1,610,652

Average Per Day (Mcf) 17,324 17,507

Average Price/Mcf $3.13 $2.63

The posted price of oil increased for the fourth quarter of

2002 compared to the fourth quarter of 2001, resulting in an

average price per barrel of $26.53 compared to $22.52 in the

same period of 2001. The average price of gas increased for

the fourth quarter of 2002 compared to the same period in

2001, resulting in an average price per Mcf of $3.13 compared

to $2.63 in the fourth quarter of 2001.

The Trustee has been advised that oil sales decreased in

2002 compared to the same period in 2001 primarily due to

decreased capital expenditures in prior periods and natural

production declines. Gas sales from the Underlying Properties

decreased in the fourth quarter of 2002 compared to the same

period in 2001 due to the same factors.The Trust has been

advised that no wells were drilled and completed during the

three months ended December 31, 2002, and there were no

wells in progress.

Royalty income received by the Trust for the fourth quarter of

2002 amounted to $7,296,142 or $.155203 per Unit. For the

fourth quarter of 2001, the Trust received royalty income of

$7,247,490 or $.154651 per Unit. Interest income for the

fourth quarter of 2002 amounted to $4,929 compared to

$9,925 for the fourth quarter of 2001. The decrease in interest

income can be attributed primarily to a decrease in interest

rates. General and administrative expenses totaled $67,256 for

8

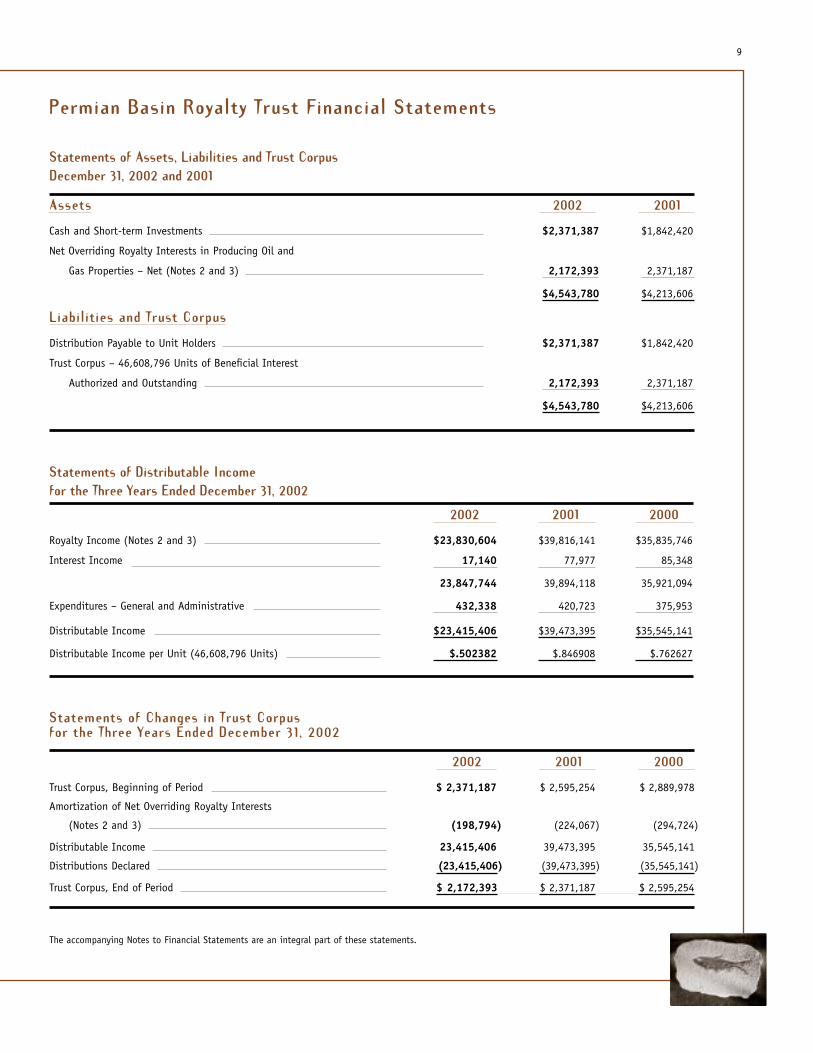

Permian Basin Royalty Trust Financial Statements

Assets 2002 2001

Cash and Short-term Investments $2,371,387 $1,842,420

Net Overriding Royalty Interests in Producing Oil and

Gas Properties – Net (Notes 2 and 3) 2,172,393 2,371,187

$4,543,780 $4,213,606

Liabilities and Trust Corpus

Distribution Payable to Unit Holders $2,371,387 $1,842,420

Trust Corpus – 46,608,796 Units of Beneficial Interest

Authorized and Outstanding 2,172,393 2,371,187

$4,543,780 $4,213,606

2002 2001 2000

Royalty Income (Notes 2 and 3) $23,830,604 $39,816,141 $35,835,746

Interest Income 17,140 77,977 85,348

23,847,744 39,894,118 35,921,094

Expenditures – General and Administrative 432,338 420,723 375,953

Distributable Income $23,415,406 $39,473,395 $35,545,141

Distributable Income per Unit (46,608,796 Units) $.502382 $.846908 $.762627

Statements of Assets, Liabilities and Trust CorpusDecember 31, 2002 and 2001

2002 2001 2000

Trust Corpus, Beginning of Period $ 2,371,187 $ 2,595,254 $ 2,889,978

Amortization of Net Overriding Royalty Interests

(Notes 2 and 3) (198,794) (224,067) (294,724)

Distributable Income 23,415,406 39,473,395 35,545,141

Distributions Declared (23,415,406) (39,473,395) (35,545,141)

Trust Corpus, End of Period $ 2,172,393 $ 2,371,187 $ 2,595,254

The accompanying Notes to Financial Statements are an integral part of these statements.

Statements of Distributable Incomefor the Three Years Ended December 31, 2002

Statements of Changes in Trust Corpusfor the Three Years Ended December 31, 2002

9

Notes to Financial Statements

1. Trust Organization and Provisions

The Permian Basin Royalty Trust (“Trust”) was established

as of November 1, 1980. Bank of America, N.A. (“Trustee”)

is Trustee for the Trust. Southland Royalty Company

(“Southland”) conveyed to the Trust (1) a 75% net overriding

royalty in Southland’s fee mineral interest in the Waddell

Ranch in Crane County, Texas (“Waddell Ranch properties”) and

(2) a 95% net overriding royalty carved out of Southland’s

major producing royalty properties in Texas (“Texas Royalty

properties”). The net overriding royalties above are collectively

referred to as the “Royalties.”

On November 3, 1980, Units of Beneficial Interest

(“Units”) in the Trust were distributed to the Trustee for the

benefit of Southland shareholders of record as of November 3,

1980, who received one Unit in the Trust for each share of

Southland common stock held. The Units are traded on the

New York Stock Exchange.

The terms of the Trust Indenture provide, among other

things, that:

■ the Trust shall not engage in any business or commercial

activity of any kind or acquire any assets other than those

initially conveyed to the Trust;

■ the Trustee may not sell all or any part of the Royalties

unless approved by holders of 75% of all Units outstanding

in which case the sale must be for cash and the proceeds

promptly distributed;

■ the Trustee may establish a cash reserve for the payment

of any liability which is contingent or uncertain in amount;

■ the Trustee is authorized to borrow funds to pay liabilities

of the Trust; and

■ the Trustee will make monthly cash distributions to Unit

holders (see Note 2).

2. Net Overriding Royalty Interests and Distribution to

Unit Holders

The amounts to be distributed to Unit holders (“Monthly

Distribution Amounts”) are determined on a monthly basis.

The Monthly Distribution Amount is an amount equal to the

sum of cash received by the Trustee during a calendar month

attributable to the Royalties, any reduction in cash reserves

and any other cash receipts of the Trust, including interest,

reduced by the sum of liabilities paid and any increase in cash

reserves. If the Monthly Distribution Amount for any monthly

period is a negative number, then the distribution will be

zero for such month. To the extent the distribution amount

is a negative number, that amount will be carried forward

and deducted from future monthly distributions until the

cumulative distribution calculation becomes a positive number,

at which time a distribution will be made. Unit holders of

record will be entitled to receive the calculated Monthly

Distribution Amount for each month on or before 10 business

days after the monthly record date, which is generally the last

business day of each calendar month.

The cash received by the Trustee consists of the amounts

received by owners of the interest burdened by the Royalties

from the sale of production less the sum of applicable taxes,

accrued production costs, development and drilling costs,

operating charges and other costs and deductions, multiplied

by 75% in the case of the Waddell Ranch properties and 95%

in the case of the Texas Royalty properties.

The initial carrying value of the Royalties ($10,975,216)

represented Southland’s historical net book value at the date

of the transfer to the Trust. Accumulated amortization as of

December 31, 2002 and 2001, aggregated $8,802,823 and

$8,604,029, respectively.

3. Basis of Accounting

The financial statements of the Trust are prepared on the

following basis:

■ Royalty income recorded is the amount computed and

paid by the working interest owner to the Trustee on behalf

of the Trust.

■ Trust expenses recorded are based on liabilities paid and

cash reserves established out of cash received or borrowed

funds for liabilities and contingencies.

■ Distributions to Unit holders are recorded when declared

by the Trustee.

The financial statements of the Trust differ from financial

statements prepared in accordance with accounting principles

generally accepted in the United States of America because

revenues are not accrued in the month of production and

certain cash reserves may be established for contingencies

10

which would not be accrued in financial statements prepared

in accordance with accounting principles generally accepted

in the United States of America. Amortization of the Royalties

calculated on a unit-of-production basis is charged directly to

trust corpus.

4. New Accounting Pronouncements

Statement of Financial Accounting Standard (“SFAS”) No. 143,

“Accounting for Asset Retirement Obligations,” was issued

by the Financial Accounting Standards Board (“FASB”) in

June 2001 and will be adopted by the Trust on January 1,

2003. This Statement addresses financial accounting and

reporting for obligations associated with the retirement of

tangible long-lived assets and the associated asset retirement

costs. The effect of adopting SFAS No. 143 will not have a

material impact on the Trust’s financial statements.

SFAS No. 145, “Rescission of FASB Statements No. 4, 44,

and 64, Amendment of FASB Statement No. 13, and Technical

Corrections,” was issued in April 2002 and is effective for

fiscal years beginning after May 15, 2002. This Statement

includes the rescission of FASB Statement No. 4, “Reporting

Gains and Losses from Extinguishment of Debt,” and an

amendment to FASB Statement No. 13, “Accounting for

Leases,” to eliminate an inconsistency between the required

accounting for sale-leaseback transactions and the required

accounting for certain lease modifications that have economic

effects that are similar to sale-leaseback transactions. The

effect of adopting SFAS No. 145 will not have a material

impact on the Trust’s financial statements.

SFAS No. 146, “Accounting for Costs Associated with

Exit or Disposal Activities,” was issued in June 2002 and

will be effective for exit or disposal activities subsequent to

December 31, 2002. The Trust anticipates no material impact

on its financial statements from the adoption of this

accounting standard.

SFAS No. 148, “Accounting for Stock-Based Compensation

– Transition and Disclosure, an amendment of FASB Statement

No. 123,” was issued in December 2002 and provides new

transition methods if an entity adopts the fair value based

method of valuing stock-based compensation suggested in

SFAS No. 123, “Accounting for Stock-Based Compensation,”

as well as requiring additional disclosures in interim and

annual financial statements. The Trust has no options or other

stock-based instruments and accordingly, the impact of this

new Standard is not expected to be material to the financial

statements of the Trust.

FASB Interpretation (“FIN”) No. 45, “Guarantor’s

Accounting and Disclosure Requirements for Guarantees,

Including Indirect Guarantees of Indebtedness of Others,”

requires disclosures beginning with financial statements ending

after December 15, 2002, and requires liability recognition

beginning January 1, 2003. The Trust had no such guarantees

outstanding as of December 31, 2002.

FIN No. 46, “Consolidation of Variable Interest Entities,”

was issued in January 2003. This interpretation of Accounting

Research Bulletin No. 51, “Consolidated Financial Statements,”

applies immediately to variable interest entities created after

January 31, 2003, and applies to the first period beginning

after June 15, 2003, to entities acquired before February 1,

2003. This FIN does not affect the Trust as it has no

unconsolidated subsidiaries accounted for under the equity

method of accounting.

5. Federal Income Tax

For federal income tax purposes, the Trust constitutes a fixed

investment trust which is taxed as a grantor trust. A grantor

trust is not subject to tax at the trust level. The Unit holders

are considered to own the Trust’s income and principal as

though no trust were in existence. The income of the Trust is

deemed to have been received or accrued by each Unit holder

at the time such income is received or accrued by the Trust

rather than when distributed by the Trust.

The Royalties constitute “economic interests” in oil and

gas properties for federal income tax purposes. Unit holders

must report their share of the revenues of the Trust as ordinary

income from oil and gas royalties and are entitled to claim

depletion with respect to such income.

The Trust has on file technical advice memoranda

confirming the tax treatment described above.

The classification of the Trust’s income for purposes of

the passive loss rules may be important to a Unit holder.

Royalty income generally is treated as portfolio income and

does not offset passive losses.

Unit holders should consult their tax advisors for further

information.

11

DistributableIncome

DistributableIncome andDistribution

Per UnitRoyaltyIncome2002

First Quarter $ 4,574 $ 4,418 $.094796

Second Quarter 5,654 5,523 .118491

Third Quarter 6,306 6,241 .133892

Fourth Quarter 7,297 7,233 .155203

Total $23,831 $23,415 $.502382

2001

First Quarter $12,092 $11,953 $.256445

Second Quarter 12,043 11,936 .256094

Third Quarter 8,433 8,376 .179718

Fourth Quarter 7,247 7,208 .154651

Total $39,816 $39,473 $.846908

6. Significant Customers

Information as to significant purchasers of oil and gas

production attributable to the Trust’s economic interests is

included in Item 2 of the Trust’s Annual Report on Form 10-K

which is included in this report.

7. Proved Oil and Gas Reserves (Unaudited)

Proved oil and gas reserve information is included in Item 2

of the Trust’s Annual Report on Form 10-K which is included

in this report.

8. Quarterly Schedule of Distributable Income (Unaudited)

The following is a summary of the unaudited quarterly schedule

of distributable income for the two years ended December 31,

2002 (in thousands, except per Unit amounts):

BANK OF AMERICA, N.A., AS TRUSTEE FOR THE PERMIAN

BASIN ROYALTY TRUST:

We have audited the accompanying statements of assets,

liabilities and trust corpus of the Permian Basin Royalty Trust

(the “Trust”) as of December 31, 2002 and 2001, and the

related statements of distributable income and changes in

trust corpus for each of the three years in the period ended

December 31, 2002. These financial statements are the

responsibility of the Trustee. Our responsibility is to express

an opinion on these financial statements based on our audits.

We conducted our audits in accordance with auditing

standards generally accepted in the United States of America.

Those standards require that we plan and perform the audit

to obtain reasonable assurance about whether the financial

statements are free of material misstatement. An audit

includes examining, on a test basis, evidence supporting the

amounts and disclosures in the financial statements. An audit

also includes assessing the accounting principles used and

significant estimates made by management, as well as

evaluating the overall financial statement presentation.

We believe that our audits provide a reasonable basis for

our opinion.

As described in Note 3 to the financial statements,

these statements were prepared on a modified cash basis

of accounting, which is a comprehensive basis of accounting

other than accounting principles generally accepted in the

United States of America.

In our opinion, such financial statements present fairly,

in all material respects, the assets, liabilities and trust

corpus of the Trust at December 31, 2002 and 2001, and the

distributable income and changes in trust corpus for each of

the three years in the period ended December 31, 2002, on

the basis of accounting described in Note 3.

Deloitte & Touche LLP

Dallas, Texas

March 25, 2003

Independent Auditors’ Report

12

UNITED STATES SECURITIES AND EXCHANGE COMMISSIONWashington, D.C. 20549

Form 10-K(Mark One)

¥ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)OF THE SECURITIES EXCHANGE ACT OF 1934

For the Ñscal year ended December 31, 2002

or

n TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)OF THE SECURITIES EXCHANGE ACT OF 1934

Commission Ñle number 1-8033

Permian Basin Royalty Trust(Exact name of registrant as speciÑed in the Permian Basin Royalty Trust Indenture)

Texas 75-6280532(State or Other Jurisdiction of (I.R.S. EmployerIncorporation or Organization) IdentiÑcation No.)

Bank of America, N.A.Trust DepartmentP.O. Box 830650

Dallas, Texas 75202(Address of Principal Executive OÇces; Zip Code)

(214) 209-2400(Registrant's Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:Title of Each Class Name of Each Exchange on Which Registered

Units of BeneÑcial Interest New York Stock Exchange

Securities Registered Pursuant to Section 12(g) of the Act:None

Indicate by check mark whether the registrant: (1) has Ñled all reports required to be Ñled by Section 13or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter periodthat the registrant was required to Ñle such reports), and (2) has been subject to such Ñling requirements forthe past 90 days. Yes ¥ No n

Indicate by check mark if disclosure of delinquent Ñlers pursuant to Item 405 of Regulation S-K is notcontained herein, and will not be contained, to the best of registrant's knowledge, in deÑnitive proxy orinformation statements incorporated by reference in Part III of this Form 10-K or any amendment to thisForm 10-K. ¥

Indicate by check mark whether the registrant is an accelerated Ñled (as deÑned in Rule 12b-2 of theSecurities Exchange Act of 1934). Yes n No ¥

The aggregate market value of the registrant's units of beneÑcial interest outstanding (based on theclosing sale price on the New York Stock Exchange) held by non-aÇliates of the registrant as of the lastbusiness day of the registrant's most recently completed second Ñscal quarter was approximately$73,943,659.85.

At March 21, 2003, there were 46,608,796 Units of BeneÑcial Interest of the Trust outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

""Units of BeneÑcial Interest'' at page 1; ""Trustee's Discussion and Analysis for the Three-Year PeriodEnded December 31, 2002'' at pages 7 through 10; ""Results of the 4th Quarters of 2002 and 2001'' at page 9;and ""Statements of Assets, Liabilities and Trust Corpus,'' ""Statements of Distributable Income,'' ""State-ments of Changes in Trust Corpus,'' ""Notes to Financial Statements'' and ""Independent Auditors' Report'' atpage 11 et seq., in registrant's Annual Report to security holders for Ñscal year ended December 31, 2002 areincorporated herein by reference for Item 5, Item 7 and Item 8 of Part II of this Report.

TABLE OF CONTENTS

Page

PART I

Item 1. Business ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 2

Website/SEC Filings ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 4

Item 2. Properties ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 4

PRODUCING ACREAGE, WELLS AND DRILLINGÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 4

OIL AND GAS PRODUCTIONÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 5

PRODUCTION COST ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 6

PRICING INFORMATION ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 6

OIL AND GAS RESERVESÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 6

REGULATION ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 9

Federal Natural Gas Regulation ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 10

State Regulation ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 10

Other Regulation ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 10

Item 3. Legal Proceedings ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 10

Item 4. Submission of Matters to a Vote of Security HoldersÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 11

PART II

Item 5. Market for Units of the Trust and Related Security Holder Matters ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 11

Item 6. Selected Financial Data ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 11

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operation 11

Item 7A. Quantitative and Qualitative Disclosures About Market Risk ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 11

Item 8. Financial Statements and Supplementary Data ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 11

Item 9. Changes in and Disagreements With Accountants on Accounting and FinancialDisclosure ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 11

PART III

Item 10. Directors and Executive OÇcers of the Registrant ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 12

Item 11. Executive CompensationÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 12

Item 12. Security Ownership of Certain BeneÑcial Owners and Management ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 12

Item 13. Certain Relationships and Related Transactions ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 13

Item 14. Controls and Procedures ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 13

PART IV

Item 15. Exhibits, Financial Statement Schedules and Reports on Form 8-K ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 13

1

FORWARD LOOKING INFORMATION

Certain information included in this report contains, and other materials Ñled or to be Ñled by the Trustwith the Securities and Exchange Commission (as well as information included in oral statements or otherwritten statements made or to be made by the Trust) may contain or include, forward looking statementswithin the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and Section 27A ofthe Securities Act of 1933, as amended. Such forward looking statements may be or may concern, amongother things, capital expenditures, drilling activity, development activities, production eÅorts and volumes,hydrocarbon prices and the results thereof, and regulatory matters. Although the Trustee believes that theexpectations reÖected in such forward looking statements are reasonable, such expectations are subject tonumerous risks and uncertainties and the Trustee can give no assurance that they will prove correct. There aremany factors, none of which is within the Trustee's control, that may cause such expectations not to berealized, including, among other things, factors such as actual oil and gas prices and the recoverability ofreserves, capital expenditures, general economic conditions, actions and policies of petroleum-producingnations and other changes in the domestic and international energy markets. Such forward looking statementsgenerally are accompanied by words such as ""estimate,'' ""expect,'' ""anticipate,'' ""goal,'' ""should,'' ""assume,''""believe,'' or other words that convey the uncertainty of future events or outcomes.

PART I

Item 1. Business

The Permian Basin Royalty Trust (the ""Trust'') is an express trust created under the laws of the state ofTexas by the Permian Basin Royalty Trust Indenture (the ""Trust Indenture'') entered into on November 3,1980, between Southland Royalty Company (""Southland Royalty'') and The First National Bank ofFort Worth, as Trustee. Bank of America, N.A., a banking association organized under the laws of the UnitedStates, as the successor of The First National Bank of Fort Worth, is now the Trustee of the Trust. Theprincipal oÇce of the Trust (sometimes referred to herein as the ""Registrant'') is located at 901 Main Street,Dallas, Texas (telephone number 214/209-2400).

On October 23, 1980, the stockholders of Southland Royalty approved and authorized that company'sconveyance of net overriding royalty interests (equivalent to net proÑts interests) to the Trust for the beneÑt ofthe stockholders of Southland Royalty of record at the close of business on the date of the conveyanceconsisting of a 75% net overriding royalty interest carved out of that company's fee mineral interests in theWaddell Ranch properties in Crane County, Texas and a 95% net overriding royalty interest carved out of thatcompany's major producing royalty properties in Texas. The conveyance of these interests (the ""Royalties'')was made on November 3, 1980, eÅective as to production from and after November 1, 1980 at 7:00 a.m. Theproperties and interests from which the Royalties were carved and which the Royalties now burden arecollectively referred to herein as the ""Underlying Properties.'' The Underlying Properties are more particularlydescribed under ""Item 2. Properties'' herein.

The function of the Trustee is to collect the income attributable to the Royalties, to pay all expenses andcharges of the Trust, and then distribute the remaining available income to the Unit holders. The Trust is notempowered to carry on any business activity and has no employees, all administrative functions beingperformed by the Trustee.

The Royalties constitute the principal asset of the Trust and the beneÑcial interests in the Royalties aredivided into that number of Units of BeneÑcial Interest (the ""Units'') of the Trust equal to the number ofshares of the common stock of Southland Royalty outstanding as of the close of business on November 3,1980. Each stockholder of Southland Royalty of record at the close of business on November 3, 1980, receivedone Unit for each share of the common stock of Southland Royalty then held.

In 1985, Southland Royalty became a wholly-owned subsidiary of Burlington Northern Inc. (""BNI''). In1988, BNI transferred its natural resource operations to Burlington Resources Inc. (""BRI'') as a result ofwhich Southland Royalty became a wholly-owned indirect subsidiary of BRI. As a result of these transactions,

2

El Paso Natural Gas Company (""El Paso'') also became an indirect subsidiary of BRI. In March 1992,El Paso completed an initial public oÅering of 5,750,000 newly issued shares of El Paso common stock,thereby decreasing BRI's ownership of El Paso to approximately eighty-Ñve percent (85%). On June 30, 1992,BRI distributed all of the shares of El Paso common stock owned by BRI to BRI's stockholders of record as ofJune 15, 1992. See ""Pricing Information'' under ""ITEM 2. Properties'' herein.

EÅective January 1, 1996, Southland Royalty, a wholly-owned subsidiary of Meridian Oil Inc. (""MOI'')was merged with and into MOI, by which action the separate corporate existence of Southland Royalty ceasedand MOI survived and succeeded to the ownership of all of the assets of Southland Royalty and has assumedall of its rights, powers and privileges, and all of its liabilities and obligations. In 1996, MOI changed its nameto Burlington Resources Oil & Gas Company (""BROG'').

The term ""net proceeds'' as used in the above described conveyance means the excess of ""grossproceeds'' received by BROG during a particular period over ""production costs'' for such period. ""Grossproceeds'' means the amount received by BROG (or any subsequent owner of the Underlying Properties)from the sale of the production attributable to the Underlying Properties, subject to certain adjustments.""Production costs'' means, generally, costs incurred on an accrual basis in operating the Underlying Properties,including both capital and non-capital costs; for example, development drilling, production and processingcosts, applicable taxes, and operating charges. If production costs exceed gross proceeds in any month, theexcess is recovered out of future gross proceeds prior to the making of further payment to the Trust, but theTrust is not liable for any production costs or liabilities attributable to these properties and interests or theminerals produced therefrom. If at any time the Trust receives more than the amount due from the Royalties,it shall not be obligated to return such overpayment, but the amounts payable to it for any subsequent periodshall be reduced by such overpaid amount, plus interest, at a rate speciÑed in the conveyance.

To the extent it has the legal right to do so, BROG is responsible for marketing the production from suchproperties and interests, either under existing sales contracts or under future arrangements at the best pricesand on the best terms it shall deem reasonably obtainable in the circumstances. BROG also has the obligationto maintain books and records suÇcient to determine the amounts payable to the Trustee. BROG, however,can sell its interests in the Underlying Properties.

Proceeds from production in the Ñrst month are generally received by BROG in the second month, thenet proceeds attributable to the Royalties are paid by BROG to the Trustee in the third month anddistribution by the Trustee to the Unit holders is made in the fourth month. The identity of Unit holdersentitled to a distribution will generally be determined as of the last business day of each calendar month (the""monthly record date''). The amount of each monthly distribution will generally be determined andannounced ten days before the monthly record date. Unit holders of record as of the monthly record date willbe entitled to receive the calculated monthly distribution amount for each month on or before ten businessdays after the monthly record date. The aggregate monthly distribution amount is the excess of (i) netrevenues from the Trust properties, plus any decrease in cash reserves previously established for contingentliabilities and any other cash receipts of the Trust over (ii) the expenses and payments of liabilities of theTrust plus any net increase in cash reserves for contingent liabilities.

Cash held by the Trustee as a reserve for liabilities or contingencies (which reserves may be establishedby the Trustee in its discretion) or pending distribution is placed, at the Trustee's discretion, in obligationsissued by (or unconditionally guaranteed by) the United States or any agency thereof, repurchase agreementssecured by obligations issued by the United States or any agency thereof, or certiÑcates of deposit of bankshaving a capital surplus and undivided proÑts in excess of $50,000,000, subject, in each case, to certain otherqualifying conditions.

The income to the Trust attributable to the Royalties is not subject in material respects to seasonalfactors nor in any manner related to or dependent upon patents, licenses, franchises or concessions. The Trustconducts no research activities. The Trust has no employees since all administrative functions are performedby the Trustee.

3

BROG has advised the Trustee that it believes that comparable revenues could be obtained in the eventof a change in purchasers of production.

Website/SEC Filings

Our Internet address is http://www.pbt-permianbasintrust.com. You can review the Ñlings the Trust hasmade with respect to its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports onForm 8-K and amendments to those reports Ñled or furnished pursuant to Section 13(a) or 15(d) of theSecurities Exchange Act of 1934. We shall post these reports as soon as reasonably practicable after weelectronically Ñle them with, or furnish them to the SEC.

Item 2. Properties

The net overriding royalties conveyed to the Trust include: (1) a 75% net overriding royalty carved out ofBROG's (as successor to Southland Royalty) fee mineral interests in the Waddell Ranch in Crane County,Texas (the ""Waddell Ranch properties''); and (2) a 95% net overriding royalty carved out of BROG's (assuccessor to Southland Royalty) major producing royalty interests in Texas (the ""Texas Royalty properties'').The net overriding royalty for the Texas Royalty properties is subject to the provisions of the lease agreementsunder which such royalties were created. References below to ""net'' wells and acres are to the interests ofBROG (from which the Royalties were carved) in the ""gross'' wells and acres.

The following information under this ITEM 2 is based upon data and information furnished to theTrustee by BROG.

PRODUCING ACREAGE, WELLS AND DRILLING

Waddell Ranch Properties. The Waddell Ranch properties consist of 78,175 gross (34,205 net)producing acres. A majority of the proved reserves are attributable to six Ñelds: Dune, Sand Hills (Judkins),Sand Hills (McKnight), Sand Hills (Tubb), University-Waddell (Devonian) and Waddell. At December 31,2002, the Waddell Ranch properties contained 765 gross (339 net) productive oil wells, 184 gross (88 net)productive gas wells and 324 gross (141 net) injection wells.

BROG is operator of record of the Waddell Ranch properties. All Ñeld, technical and accountingoperations have been contracted by an agreement between the working interest owners and CoastalManagement Corporation (""CMC'') but remain under the direction of BROG.

The Waddell Ranch properties are mature producing properties, and all of the major oil Ñelds arecurrently being waterÖooded for the purpose of facilitating enhanced recovery. Proved reserves and estimatedfuture net revenues attributable to the properties are included in the reserve reports summarized below.BROG does not own the full working interest in any of the tracts constituting the Waddell Ranch propertiesand, therefore, implementation of any development programs will require approvals of other working interestholders as well as BROG. In addition, implementation of any development programs will be dependent uponoil and gas prices currently being received and anticipated to be received in the future. There were 4 gross(1.75 net) wells drilled and completed on the Waddell Ranch properties during 2002. At December 31, 2002there were no wells in progress on the Waddell Ranch properties. During 2001 there were 11 gross (.76 net)wells drilled and completed on the Waddell Ranch properties. At December 31, 2001 there were 8 gross(3.75 net) wells in progress on the Waddell Ranch properties. During 2000 there were no wells drilled on theWaddell Ranch properties. At December 31, 2000 there were 10 gross (4.88 net) wells in progress on theWaddell Ranch properties.

BROG has advised the Trustee that the total amount of capital expenditures for 2002 with regard to theWaddell Ranch properties totalled $9.9 million. Capital expenditures include the cost of remedial andmaintenance activities. This amount spent is approximately $.1 million less than the budgeted amountprojected by BROG for 2002. BROG has advised the Trustee that the capital expenditures budget for 2003totals approximately $10.0 million, of which approximately $1.1 is attributable to the 2003 drilling program,

4

and $8.9 million to workovers and recompletions. Accordingly, there is a minor increase in capitalexpenditures for 2003 as compared with the 2002 capital expenditures.

Texas Royalty Properties. The Texas Royalty properties consist of royalty interests in mature producingoil Ñelds, such as Yates, Wasson, Sand Hills, East Texas, Kelly-Snyder, Panhandle Regular, N. Cowden,Todd, Keystone, Kermit, McElroy, Howard-Glasscock, Seminole and others. The Texas Royalty propertiescontain approximately 303,000 gross (approximately 51,000 net) producing acres. Detailed informationconcerning the number of wells on royalty properties is not generally available to the owners of royaltyinterests. Consequently, an accurate count of the number of wells located on the Texas Royalty propertiescannot readily be obtained.

In February 1997, BROG sold its interests in the Texas Royalty properties that are subject to the NetOverriding Royalty Conveyance to the Trust dated eÅective November 1, 1980 (""Texas Royalty Convey-ance'') to Riverhill Energy Corporation (""Riverhill Energy''), which was then a wholly-owned subsidiary ofRiverhill Capital Corporation (""Riverhill Capital'') and an aÇliate of CMC. At the time of such sale,Riverhill Capital was a privately owned Texas corporation with oÇces in Bryan and Midland, Texas. TheTrustee was informed by BROG that, as required by the Texas Royalty Conveyance, Riverhill Energysucceeded to all of the requirements upon and the responsibilities of BROG under the Texas RoyaltyConveyance with regard to the Texas Royalty properties. BROG and Riverhill Energy further advised theTrustee that all accounting operations pertaining to the Texas Royalty properties were being performed byCMC under the direction of Riverhill Energy. BROG indicated to the Trustee that BROG will work togetherwith CMC and Riverhill Energy in an eÅort to assure that various administrative functions and reportingrequirements assumed by Riverhill Energy are met. The Trustee has been advised that independent auditorsrepresenting Riverhill Energy and CMC are PriceWaterhouseCoopers.

The Trustee has been advised that in the Ñrst quarter of 1998 Schlumberger Technology Corporation(""Schlumberger''), acquired all of the shares of stock of Riverhill Capital. Prior to such acquisition bySchlumberger, CMC and Riverhill Energy were wholly-owned subsidiaries of Riverhill Capital. The Trusteehas further been advised that in connection with Schlumberger's acquisition of Riverhill Capital, theshareholders of Riverhill Capital acquired ownership of all of the shares of stock of Riverhill Energy. Thus, theownership in the Texas Royalty properties referenced above remained in Riverhill Energy, the stock ownershipof which was acquired by the former shareholders of Riverhill Capital. Accounting operations pertaining to theTexas Royalty properties are being performed by CMC under the direction of Riverhill Energy. CMC alsocurrently conducts all Ñeld, technical and accounting operations on behalf of BROG with regard to theWaddell Ranch properties.

Well Count and Acreage Summary. The following table shows as of December 31, 2002, the gross andnet producing wells and acres for the Company Interests. The net wells and acres are determined bymultiplying the gross wells or acres by the Company Interests Owner's working interest in the wells or acres.There is very little undeveloped Acreage held by the Trust, and all this is held by production.

Number ofWells Acres

Gross Net Gross Net

Company Interests ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 1,273 568 76,992 33,276

OIL AND GAS PRODUCTION

The Trust recognizes production during the month in which the related distribution is received.Production of oil and gas attributable to the Royalties and the Underlying Properties and the related average

5

sales prices attributable to the Underlying Properties for the three years ended December 31, 2002, excludingportions attributable to the adjustments discussed below, were as follows:

Waddell Ranch Properties Texas Royalty Properties Total

2002 2001 2000 2002 2001 2000 2002 2001 2000

Royalties:

Production

Oil (barrels) ÏÏÏÏÏ 426,719 577,243 584,269 301,594 363,959 335,160 728,313 941,202 919,429

Gas (Mcf)ÏÏÏÏÏÏÏ 2,440,678 3,109,734 2,654,731 751,497 765,852 691,714 3,192,175 3,875,586 3,346,445

Underlying Properties:

Production

Oil (barrels) ÏÏÏÏÏ 922,766 1,032,678 1,119,835 350,157 402,305 366,275 1,272,923 1,434,983 1,486,110

Gas (Mcf)ÏÏÏÏÏÏÏ 5,310,364 5,572,143 5,134,829 878,651 869,155 755,194 6,189,015 6,441,298 5,890,023

Average Price

Oil/barrelÏÏÏÏÏÏÏÏ $ 22.44 $ 25.64 $ 28.28 $ 22.12 $ 23.68 $ 26.58 $ 22.31 $ 24.88 $ 27.66

Gas/Mcf ÏÏÏÏÏÏÏÏ $ 2.80 $ 4.68 $ 3.65 $ 2.55 $ 4.34 $ 3.58 $ 2.74 $ 4.70 $ 3.63

Since the oil and gas sales attributable to the Royalties are based on an allocation formula that isdependent on such factors as price and cost (including capital expenditures), production amounts do notnecessarily provide a meaningful comparison.

PRODUCTION COST

Waddell Ranch total lease operating expense for 2002 was $22.318 million gross and $7.703 million net.The lease operating expense increased 5% from 2001 to 2002 primarily because of the increase in wellmaintenance operations and abandonment of shut in non-economic wellbores. Waddell Ranch lifting cost on abarrel of oil equivalent (BOE) basis was $5.20/bbl. The lifting cost on a barrel of total Öuid produced(BTF) basis was $.41/bbl.

PRICING INFORMATION

Reference is made to ""Regulation'' for information as to federal regulation of prices of natural gas. Thefollowing paragraphs provide information regarding sales of oil and gas from the Waddell Ranch properties. Asa royalty owner, BROG is not furnished detailed information regarding sales of oil and gas from the TexasRoyalty properties.

Oil. The Trustee has been advised by BROG that for the period August 1, 1993 through June 30, 2003,the oil from the Waddell Ranch properties is being sold under a competitive bid to independent third parties.

Gas. The gas produced from the Waddell Ranch properties is processed through a natural gasprocessing plant and sold at the tailgate of the plant. Plant products are marketed by Burlington ResourcesHydrocarbons Inc., an indirect subsidiary of BRI. The processor of the gas (Warren Petroleum Company,L.P.) receives 15% of the liquids and residue gas as a fee for gathering, compression, treating and processingthe gas.

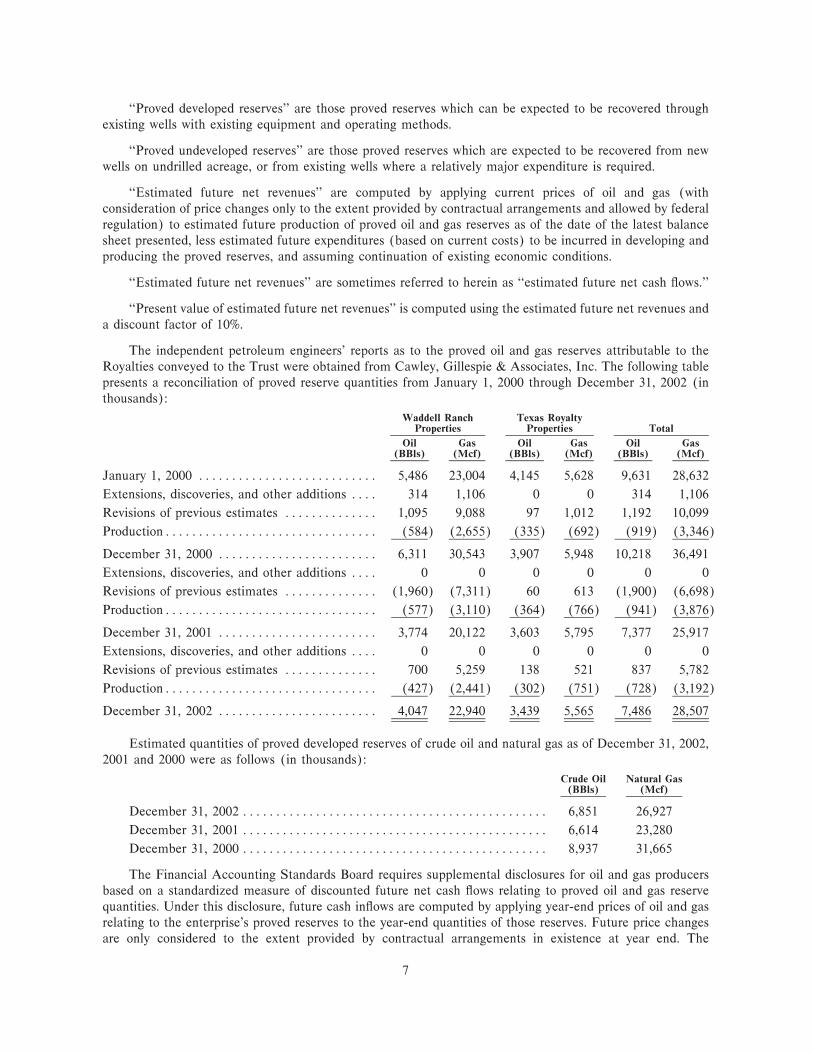

OIL AND GAS RESERVES

The following are deÑnitions adopted by the Securities and Exchange Commission (""SEC'') and theFinancial Accounting Standards Board which are applicable to terms used within this Item:

""Proved reserves'' are those estimated quantities of crude oil, natural gas and natural gas liquids, which,upon analysis of geological and engineering data, appear with reasonable certainty to be recoverable in thefuture from known oil and gas reservoirs under existing economic and operating conditions.

6

""Proved developed reserves'' are those proved reserves which can be expected to be recovered throughexisting wells with existing equipment and operating methods.

""Proved undeveloped reserves'' are those proved reserves which are expected to be recovered from newwells on undrilled acreage, or from existing wells where a relatively major expenditure is required.

""Estimated future net revenues'' are computed by applying current prices of oil and gas (withconsideration of price changes only to the extent provided by contractual arrangements and allowed by federalregulation) to estimated future production of proved oil and gas reserves as of the date of the latest balancesheet presented, less estimated future expenditures (based on current costs) to be incurred in developing andproducing the proved reserves, and assuming continuation of existing economic conditions.

""Estimated future net revenues'' are sometimes referred to herein as ""estimated future net cash Öows.''

""Present value of estimated future net revenues'' is computed using the estimated future net revenues anda discount factor of 10%.

The independent petroleum engineers' reports as to the proved oil and gas reserves attributable to theRoyalties conveyed to the Trust were obtained from Cawley, Gillespie & Associates, Inc. The following tablepresents a reconciliation of proved reserve quantities from January 1, 2000 through December 31, 2002 (inthousands):

Waddell Ranch Texas RoyaltyProperties Properties Total

Oil Gas Oil Gas Oil Gas(BBls) (Mcf) (BBls) (Mcf) (BBls) (Mcf)

January 1, 2000 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 5,486 23,004 4,145 5,628 9,631 28,632

Extensions, discoveries, and other additions ÏÏÏÏ 314 1,106 0 0 314 1,106

Revisions of previous estimates ÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 1,095 9,088 97 1,012 1,192 10,099

ProductionÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (584) (2,655) (335) (692) (919) (3,346)

December 31, 2000 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 6,311 30,543 3,907 5,948 10,218 36,491

Extensions, discoveries, and other additions ÏÏÏÏ 0 0 0 0 0 0

Revisions of previous estimates ÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (1,960) (7,311) 60 613 (1,900) (6,698)

ProductionÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (577) (3,110) (364) (766) (941) (3,876)

December 31, 2001 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 3,774 20,122 3,603 5,795 7,377 25,917

Extensions, discoveries, and other additions ÏÏÏÏ 0 0 0 0 0 0

Revisions of previous estimates ÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 700 5,259 138 521 837 5,782

ProductionÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ (427) (2,441) (302) (751) (728) (3,192)

December 31, 2002 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 4,047 22,940 3,439 5,565 7,486 28,507

Estimated quantities of proved developed reserves of crude oil and natural gas as of December 31, 2002,2001 and 2000 were as follows (in thousands):

Crude Oil Natural Gas(BBls) (Mcf)

December 31, 2002 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 6,851 26,927

December 31, 2001 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 6,614 23,280

December 31, 2000 ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 8,937 31,665

The Financial Accounting Standards Board requires supplemental disclosures for oil and gas producersbased on a standardized measure of discounted future net cash Öows relating to proved oil and gas reservequantities. Under this disclosure, future cash inÖows are computed by applying year-end prices of oil and gasrelating to the enterprise's proved reserves to the year-end quantities of those reserves. Future price changesare only considered to the extent provided by contractual arrangements in existence at year end. The

7

standardized measure of discounted future net cash Öows is achieved by using a discount rate of 10% a year toreÖect the timing of future cash Öows relating to proved oil and gas reserves.

Estimates of proved oil and gas reserves are by their very nature imprecise. Estimates of future netrevenue attributable to proved reserves are sensitive to the unpredictable prices of oil and gas and othervariables.

The 2002, 2001 and 2000 change in the standardized measure of discounted future net cash Öows relatedto future royalty income from proved reserves discounted at 10% is as follows (in thousands):

Waddell Ranch Properties Texas Royalty Properties Total

2002 2001 2000 2002 2001 2000 2002 2001 2000

January 1 ÏÏÏÏÏÏÏÏÏÏ $ 59,283 $ 214,029 $102,088 $34,519 $ 65,784 $ 52,126 $ 93,802 $ 279,813 $154,214

Extensions,discoveries, andother additions ÏÏÏÏ 0 0 10,281 0 0 0 0 0 10,281

Accretion of discount 5,928 21,403 10,209 3,452 6,578 5,213 9,380 27,981 15,422

Revisions of previousestimates and other 67,650 (147,806) 116,353 26,205 (26,370) 19,379 93,855 (174,176) 135,732

Royalty income ÏÏÏÏÏ (15,627) (28,343) (24,902) (8,204) (11,473) (10,934) (23,831) (39,816) (35,836)

December 31 ÏÏÏÏÏÏÏ $117,234 $ 59,283 $214,029 $55,972 $ 34,519 $ 65,784 $173,206 $ 93,802 $279,813

Oil and gas prices of $31.88 and $28.95 per barrel and $3.80 and $3.79 per Mcf were used to determinethe estimated future net revenues from the Waddell Ranch properties and the Texas Royalty properties,respectively, at December 31, 2002. The upward revisions of both reserves and discounted future net cashÖows for the Waddell Ranch properties and the Texas Royalty properties are due to increase in oil and gasprices from 2001 to 2002.

Oil and gas prices of $17.05 and $17.62 per barrel and $2.15 and $1.93 per Mcf, respectively, were used todetermine the estimated future net revenues from the Waddell Ranch properties and the Texas Royaltyproperties, respectively, at December 31, 2001. The extension, discoveries and other additions for the WaddellRanch properties are proved reserves related to the Waddell (Greyburg) and Running WN (Wolfcamp)Ñelds. The upward revisions of both reserves and discounted future net cash Öows for the Waddell Ranchproperties and the Texas Royalty properties are due to increases in oil and gas prices from 2000 to 2001.

Oil and gas prices of $24.65 and $26.46 per barrel and $8.98 and $7.03 per Mcf, respectively, were used todetermine the estimated future net revenues from the Waddell Ranch properties and the Texas Royaltyproperties at December 31, 2000. The extension, discoveries and other additions for the Waddell Ranchproperties are proved developed producing reserves related to the RM (Clearfork) Ñeld. The upward revisionsof both reserves and discounted future net cash Öows for the Waddell Ranch properties and the Texas Royaltyproperties were due to increases in oil and gas prices from 1999 to 2000.

8

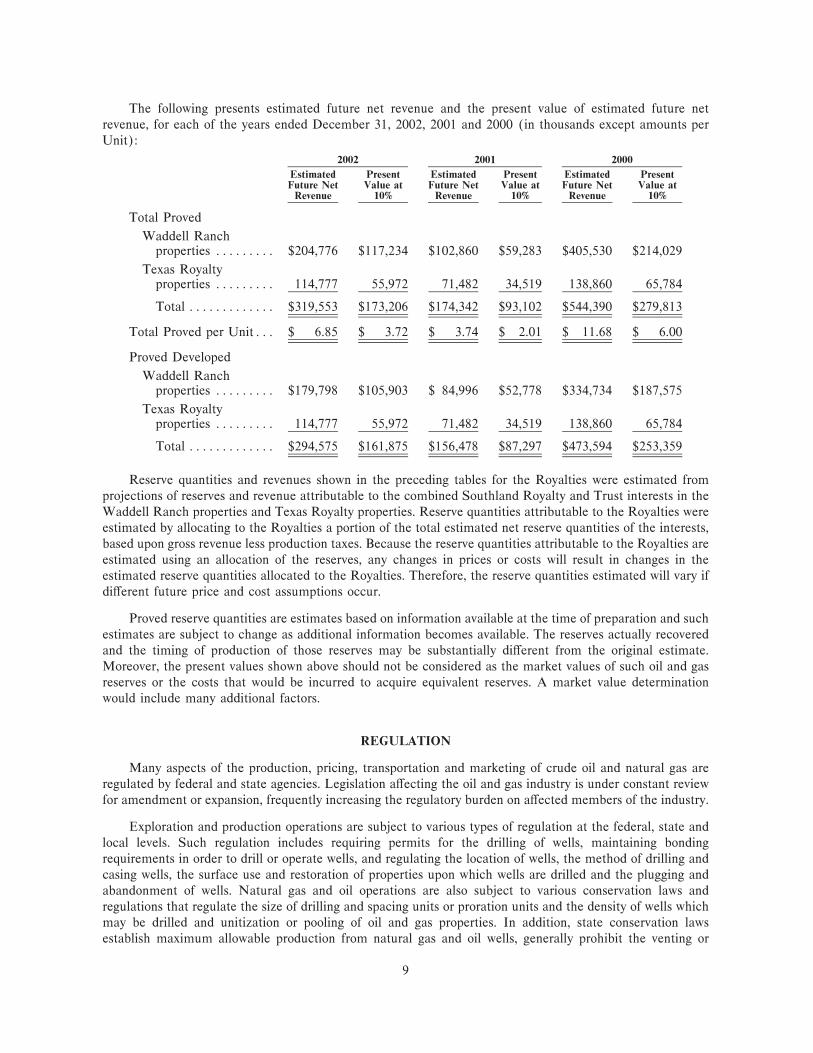

The following presents estimated future net revenue and the present value of estimated future netrevenue, for each of the years ended December 31, 2002, 2001 and 2000 (in thousands except amounts perUnit):

2002 2001 2000

Estimated Present Estimated Present Estimated PresentFuture Net Value at Future Net Value at Future Net Value atRevenue 10% Revenue 10% Revenue 10%

Total Proved

Waddell Ranchproperties ÏÏÏÏÏÏÏÏÏ $204,776 $117,234 $102,860 $59,283 $405,530 $214,029

Texas Royaltyproperties ÏÏÏÏÏÏÏÏÏ 114,777 55,972 71,482 34,519 138,860 65,784

Total ÏÏÏÏÏÏÏÏÏÏÏÏÏ $319,553 $173,206 $174,342 $93,102 $544,390 $279,813

Total Proved per UnitÏÏÏ $ 6.85 $ 3.72 $ 3.74 $ 2.01 $ 11.68 $ 6.00

Proved Developed

Waddell Ranchproperties ÏÏÏÏÏÏÏÏÏ $179,798 $105,903 $ 84,996 $52,778 $334,734 $187,575

Texas Royaltyproperties ÏÏÏÏÏÏÏÏÏ 114,777 55,972 71,482 34,519 138,860 65,784

Total ÏÏÏÏÏÏÏÏÏÏÏÏÏ $294,575 $161,875 $156,478 $87,297 $473,594 $253,359

Reserve quantities and revenues shown in the preceding tables for the Royalties were estimated fromprojections of reserves and revenue attributable to the combined Southland Royalty and Trust interests in theWaddell Ranch properties and Texas Royalty properties. Reserve quantities attributable to the Royalties wereestimated by allocating to the Royalties a portion of the total estimated net reserve quantities of the interests,based upon gross revenue less production taxes. Because the reserve quantities attributable to the Royalties areestimated using an allocation of the reserves, any changes in prices or costs will result in changes in theestimated reserve quantities allocated to the Royalties. Therefore, the reserve quantities estimated will vary ifdiÅerent future price and cost assumptions occur.

Proved reserve quantities are estimates based on information available at the time of preparation and suchestimates are subject to change as additional information becomes available. The reserves actually recoveredand the timing of production of those reserves may be substantially diÅerent from the original estimate.Moreover, the present values shown above should not be considered as the market values of such oil and gasreserves or the costs that would be incurred to acquire equivalent reserves. A market value determinationwould include many additional factors.

REGULATION

Many aspects of the production, pricing, transportation and marketing of crude oil and natural gas areregulated by federal and state agencies. Legislation aÅecting the oil and gas industry is under constant reviewfor amendment or expansion, frequently increasing the regulatory burden on aÅected members of the industry.

Exploration and production operations are subject to various types of regulation at the federal, state andlocal levels. Such regulation includes requiring permits for the drilling of wells, maintaining bondingrequirements in order to drill or operate wells, and regulating the location of wells, the method of drilling andcasing wells, the surface use and restoration of properties upon which wells are drilled and the plugging andabandonment of wells. Natural gas and oil operations are also subject to various conservation laws andregulations that regulate the size of drilling and spacing units or proration units and the density of wells whichmay be drilled and unitization or pooling of oil and gas properties. In addition, state conservation lawsestablish maximum allowable production from natural gas and oil wells, generally prohibit the venting or

9

Öaring of natural gas and impose certain requirements regarding the ratability of production. The eÅect ofthese regulations is to limit the amounts of natural gas and oil that can be produced, potentially raise prices,and to limit the number of wells or the locations which can be drilled.