pce.ppt

TRANSCRIPT

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 1/16

SME Rating Agency of India Ltd

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 2/16

Minimise lending risk thru ratings 2

SME Expectations for growth

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 3/16

Minimise lending risk thru ratings 3

Challenges faced by lenders

NumerousSMEs

Geographically

Dispersed

Lack of

Reliable InformationMultiple segment –

Multiple Needs

Limited skills in

understanding &

evaluating

Lending

Institutions

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 4/16

Minimise lending risk thru ratings 4

Relevance for a rating Agency dedicated for SMEs

• Focused approach towards SMEs

• Strong data & knowledge-base about SMEs

• Different evaluation approach based on size and industry

• Ability to analyze in limited and lesser reliable information• Emphasis on non-financial parameters

TO BRIDGE THE GAP BETWEEN FINANCIERS AND SMEs

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 5/16

Minimise lending risk thru ratings 5

SMERA – An Introduction

• Only rating agency dedicated to the SME segment offeringqualitative services at competitive prices.

• Joint initiative of SIDBI, Dun & Bradstreet and 11 leading banksoperating in SME segment.

• Launched on the 5th September 2005 by the Hon. Finance Minister,Shri P Chidambaram.

• Completed around 4800 ratings till date.

• Greater acceptability in banks (MOU with 22 leading banks). 14Banks offer interest rate and security concessions for well ratedSMERA customers.

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 6/16

Minimise lending risk thru ratings 6

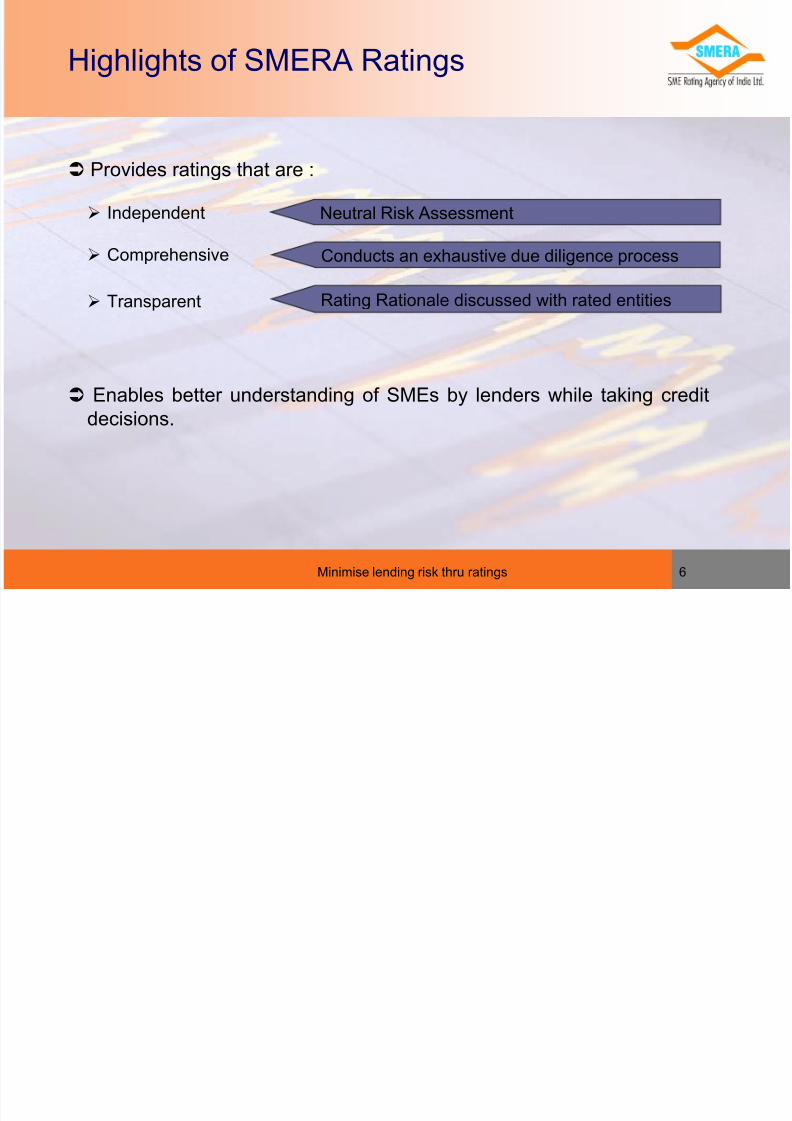

Highlights of SMERA Ratings

Provides ratings that are :

Independent

Comprehensive

Transparent

Enables better understanding of SMEs by lenders while taking credit

decisions.

Neutral Risk Assessment

Conducts an exhaustive due diligence process

Rating Rationale discussed with rated entities

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 7/16

Rating Scales

• NSIC

• SMERA

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 8/16

NSIC Rating Scale

RATING INDICATOR

Financial Strength

High Moderate Low

Performance

Capability

Highest SE1A SE1B SE1C

High SE2A SE2B SE2C

Moderate SE3A SE3B SE3C

Weak SE4A SE4B SE4C

Poor SE5A SE5B SE5C

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 9/16

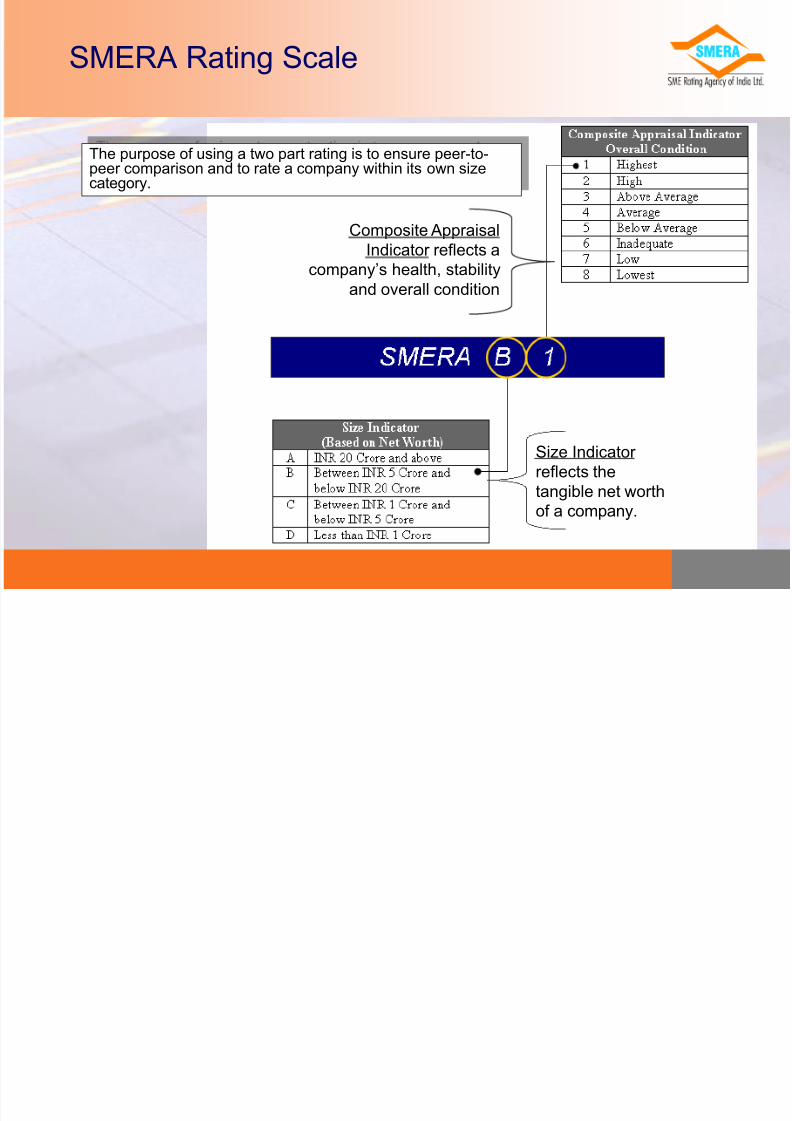

SMERA Rating Scale

The purpose of using a two part rating is to ensure peer-to-peer comparison and to rate a company within its own sizecategory.

Composite Appraisal

Indicator reflects a

company’s health, stabilityand overall condition

Size Indicator

reflects the

tangible net worth

of a company.

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 10/16Minimise lending risk thru ratings 10

Rating Process Flow

Request forInterview and

site visit

Rating Request SMERA Site visit Enterprise

Questionnaire

Documents,

audited results

& certified

projections

Site Visit

Assessment

Report

ROC

Information

Rating

Model

Industry Assessment

and Cluster

data

Rating Analyst

Peer Review

Third PartyData – e.g.

Litigation

Information

Conducts site

visit and

interviews

Management

Documents Obtained

External Data

SMERA

Database

Entity RatingFinal Rating

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 11/16Minimise lending risk thru ratings 11

Factors considered while rating

Parameters of Rating

Financial Non-Financial

Solvency

Ratios

Liquidity

Ratios

Profitability

Ratios

Activity

Ratio

Management Quality

Location Advantage

Marketing Network

Legal Issues

Industry and Macro-Economic Assessment

e.g. Debt-Equity Current Ratio RONW Asset-

turnover

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 12/16Minimise lending risk thru ratings 12

Non-Financial Parameters

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 13/16Minimise lending risk thru ratings 14

Benefits of SMERA Rating

• Third party credit rating helps in extending additional comfort for

internal decision making.

• Validation of the internal ratings.

• Intrinsic Strengths of SME units captured as model also considers

qualitative parameters in addition to financial results.

• Strengthening of Credit Portfolio thru rating/review ratings – early

warning signals.

• Impact of industry related cyclical trend considered in rating.

• Cluster centric approach.

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 14/16

Minimise lending risk thru ratings 15

Above fees is inclusive of service tax @ 10.3%

NSIC - D&B - SMERA Rating Fee

Category Fees Service Tax Total

Turnover Rs. Rs. Rs.

< 50 Lacs 7,500 772.5 8,272

50 to 200 Lacs 9,000 927 9927

> 200 Lacs 12,000 1,236 13,236

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 15/16

Minimise lending risk thru ratings 16

SMERA Rating Fee

Category Fees Service Tax Total

Turnover Rs. Rs. Rs.

< 50 Lacs 30,000 3,090 33,090

50 to 200 Lacs 36,000 3708 39,708

> 200 Lacs 48,000 4,944 52,944

8/14/2019 pce.ppt

http://slidepdf.com/reader/full/pceppt 16/16

Thank YouContact Details

Virendra Goyal-National Sales Manager