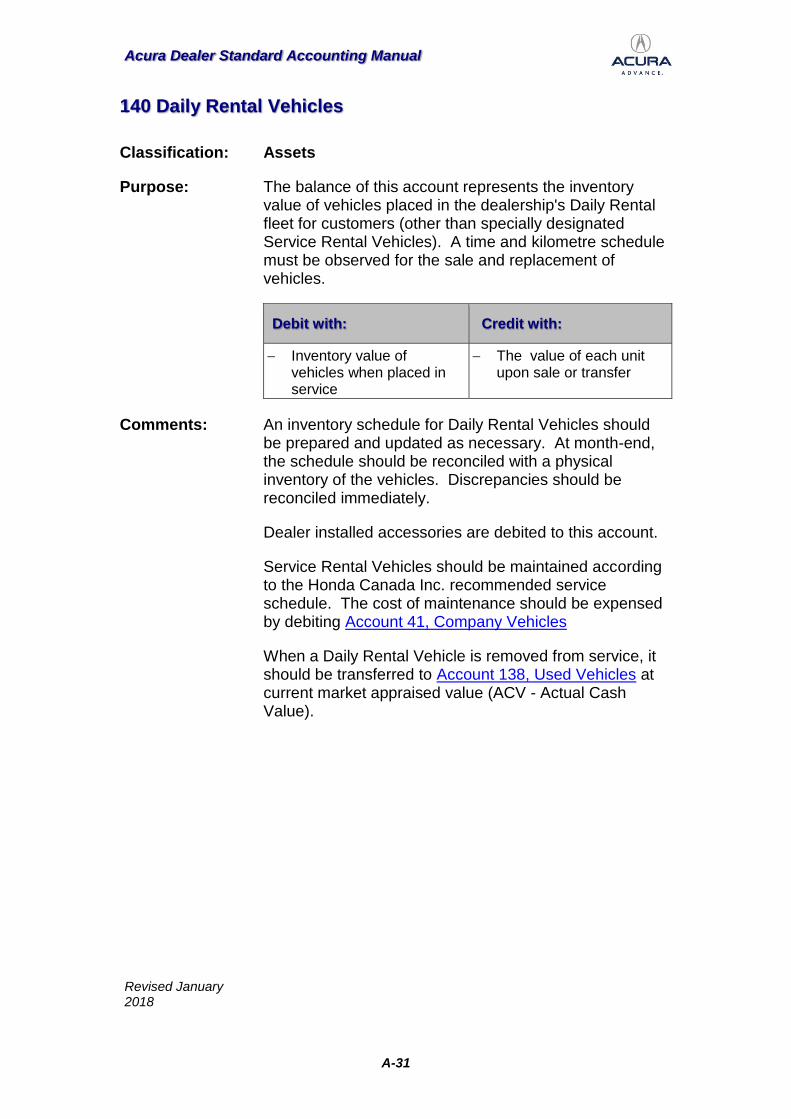

acura dealer standard accounting manual dealer standard accounting manual revised january 2018...

TRANSCRIPT

Acura Dealer Standard Accounting Manual

Revised January 2018

Introduction ................................................................................ 1

Monthly Routine ......................................................................... 2

Management Operating Information ......................................... 3

Dealership Receivables ........................................................................ 3 Distribution of Personnel (Dealership personnel count) ........................ 3

New, Used Vehicle Inventory Analysis .................................................. 3 Parts & Accessories Inventory Analysis ................................................ 4 Service Department Data ...................................................................... 4 Absorption & Breakeven analysis .......................................................... 5

Chart of Accounts Summary – Acura ....................................... 8

Assets ................................................................................................... 8 Liabilities ............................................................................................... 8 Net Worth .............................................................................................. 8 Operating Accounts ............................................................................... 9

Expense Accounts ................................................................................ 9 Other Income ...................................................................................... 10

Other Deductions ................................................................................ 10

Chart of Accounts – Detail by Account ................................ A-1

A- ASSETS ............................................................................................ A-1

101 Petty Cash .................................................................................. A-2 102 Cash on Hand ............................................................................ A-3

104 Bank Accounts ........................................................................... A-4 105 Trust Account ............................................................................. A-5 107 Finance Contracts in Transit ...................................................... A-6

108 Marketable Securities ................................................................. A-7 109 Cash Sales Clearing................................................................... A-8

110 Vehicle Licenses Clearing .......................................................... A-9 115 Accounts Receivable - Customer Service, Parts, Body Shop .. A-10

116 Accounts Receivable - Vehicles ............................................... A-12 117 Accounts Receivable - Factory ................................................. A-13 119 Lease Receivables ................................................................... A-14

120 Warranty Claims ....................................................................... A-15 121 Marketing Allowance Receivable ............................................. A-16

122 Goods and Services Tax Receivable ....................................... A-18 123 Finance and Insurance Commissions ...................................... A-20 125 Allowance for Doubtful Accounts .............................................. A-21

130 New Vehicles ........................................................................... A-22 136 Demonstrators .......................................................................... A-25

138 Used Vehicles .......................................................................... A-27 139 Courtesy Vehicles – Inventory .................................................. A-28

140 Daily Rental Vehicles ............................................................... A-31 141 Other Inventories ...................................................................... A-32 142 Parts – Acura ........................................................................... A-33 144 Accessories – Acura................................................................. A-34 145 Parts – Other ............................................................................ A-35

146 Accessories - Other .................................................................. A-36 148 Tires ......................................................................................... A-37

Acura Dealer Standard Accounting Manual

Revised January 2018

149 Sublet Repairs .......................................................................... A-38

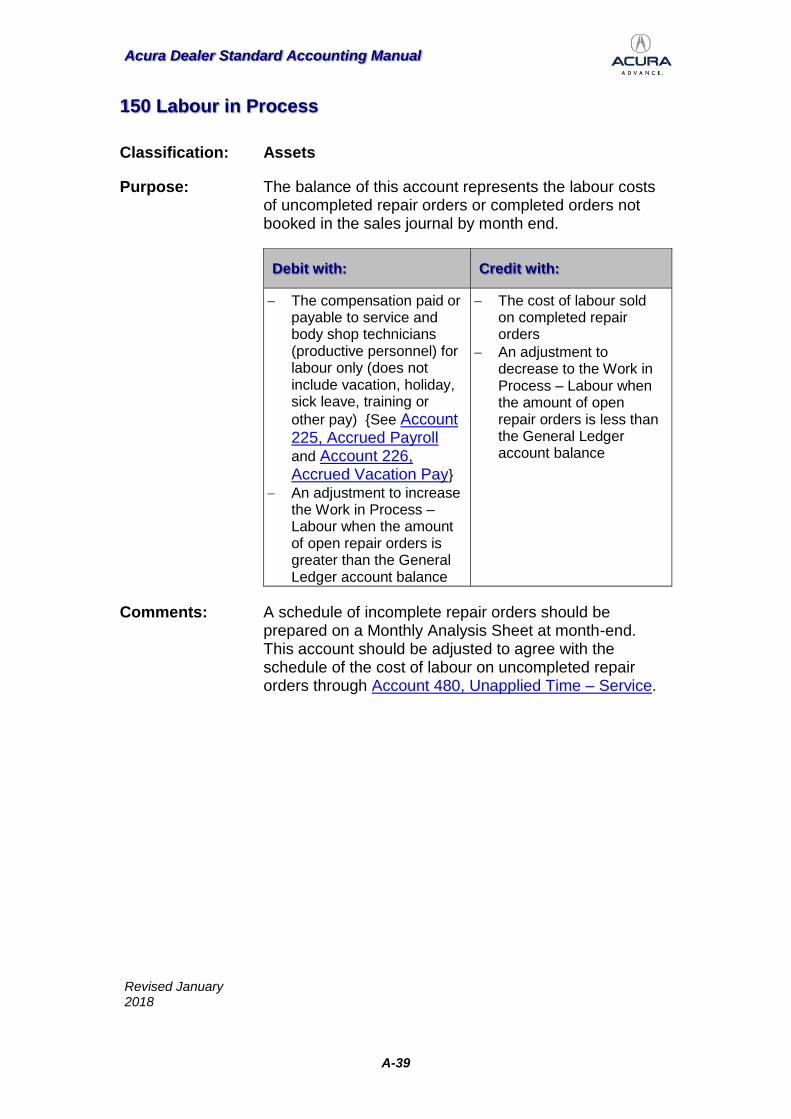

150 Labour in Process .................................................................... A-39 151 Gasoline (fuel), Oil and Grease ................................................ A-40

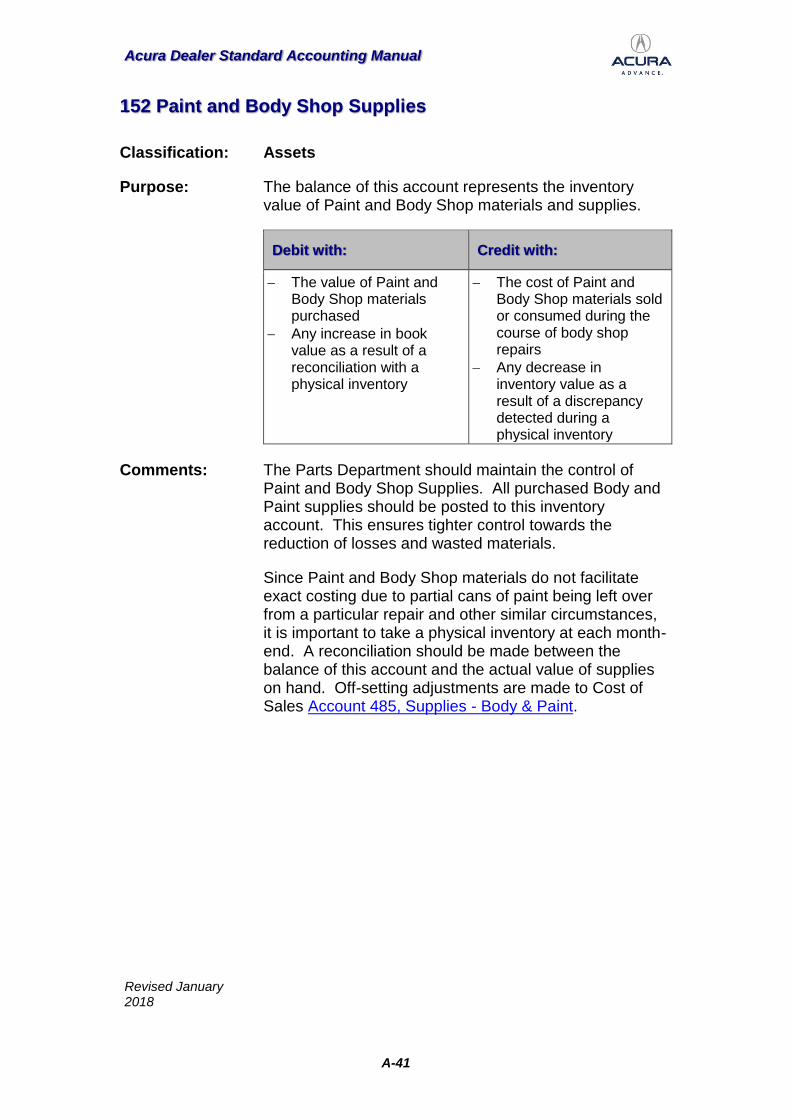

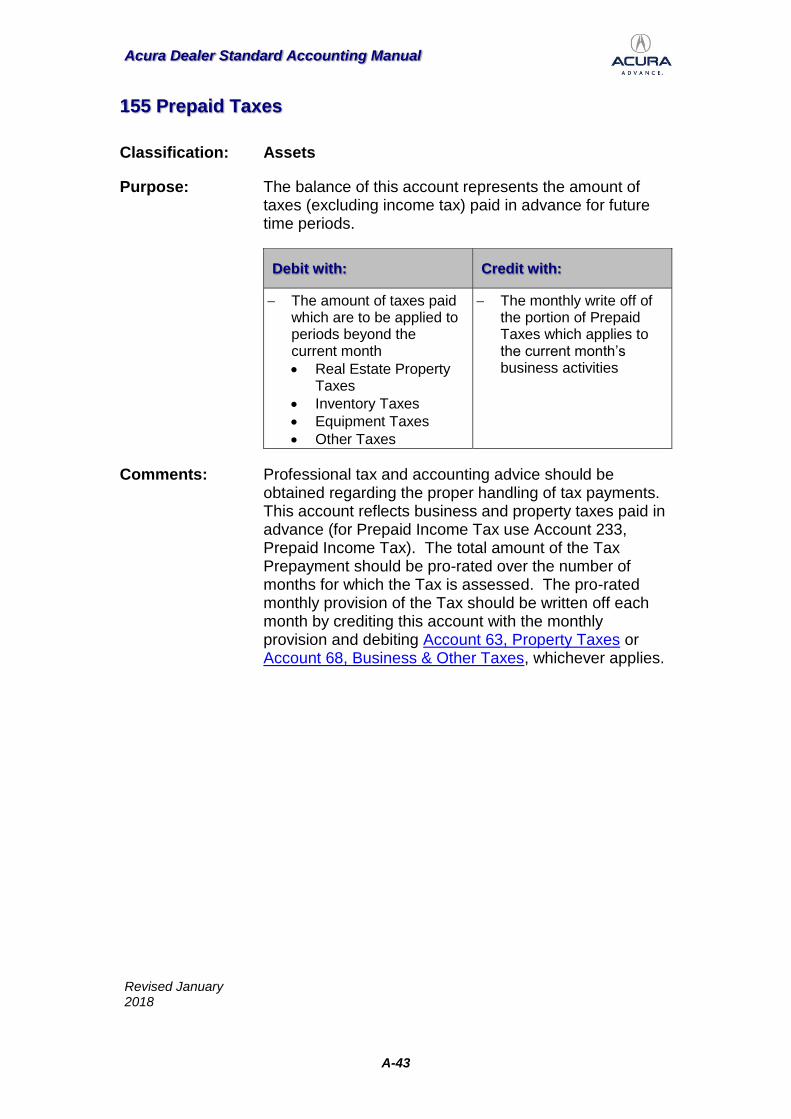

152 Paint and Body Shop Supplies ................................................. A-41 154 Prepaid Rent ............................................................................ A-42 155 Prepaid Taxes .......................................................................... A-43 156 Prepaid Insurance .................................................................... A-44 157 Other Prepaid Expenses .......................................................... A-45

165 Land ......................................................................................... A-46 167 Buildings ................................................................................... A-47 168 Accumulated Amortization - Buildings ...................................... A-48 1690 EDP Equipment ...................................................................... A-49 1691 Accumulated Amortization - EDP Equipment ......................... A-50

170 Building Fixtures ....................................................................... A-51 171 Accumulated Amortization - Building Fixtures .......................... A-52

172 Leasehold Improvements ......................................................... A-53

173 Accumulated Amortization - Leasehold Improvements ............ A-54 174 Office Equipment ...................................................................... A-55 175 Accumulated Amortization - Office Equipment ......................... A-56 176 Parts Department Equipment ................................................... A-57

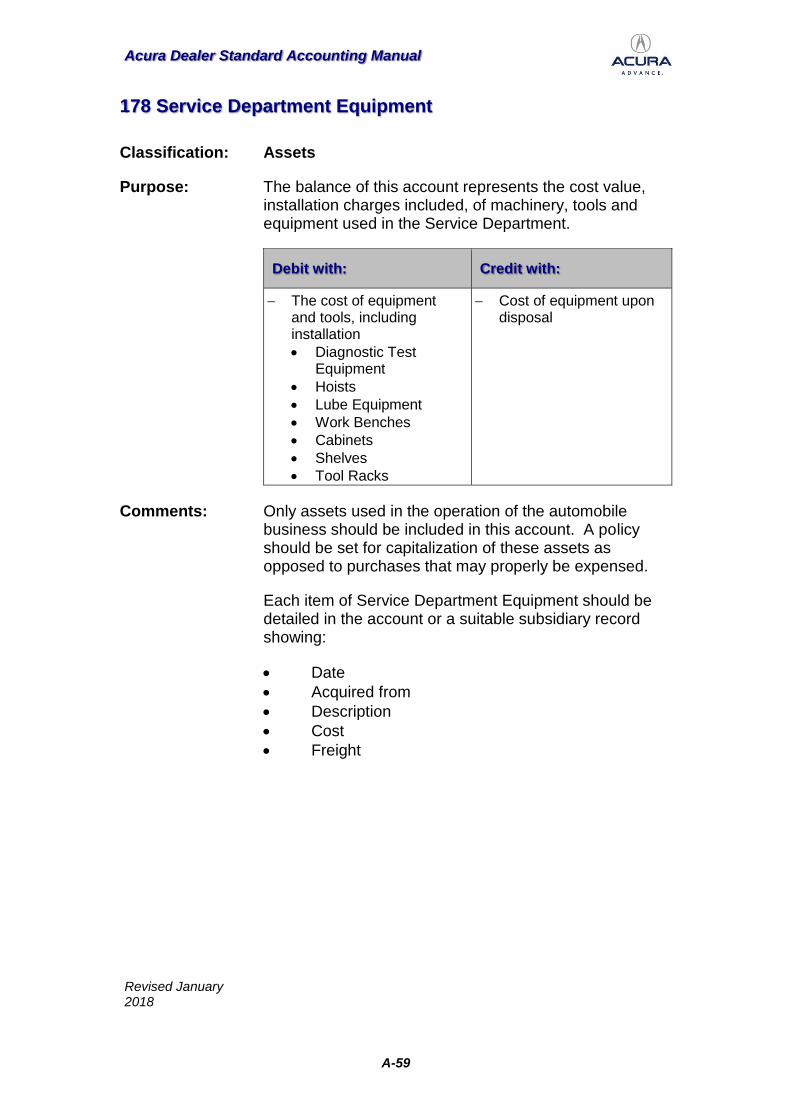

177 Accumulated Amortization - Parts Department Equipment ...... A-58 178 Service Department Equipment ............................................... A-59

179 Accumulated Amortization - Service Department Equipment ... A-60 181 Signs ........................................................................................ A-61 182 Accumulated Amortization - Signs ........................................... A-62

183 Company Vehicles ................................................................... A-63 184 Accumulated Amortization - Company Vehicles ....................... A-65

185 Leased Vehicles ....................................................................... A-66 186 Accumulated Amortization - Leased Vehicles .......................... A-68

188 Refundable Deposits ................................................................ A-69 189 Investments .............................................................................. A-70

190 Organization Expense .............................................................. A-71 191 Life Insurance - Cash Values ................................................... A-72

192 Advances - Officers and Employees ........................................ A-73 193 Notes / Long-Term Accounts Receivable ................................. A-74 195 Goodwill ................................................................................... A-75

196 Finance Company Participation ............................................... A-76

B- LIABILITIES ...................................................................................... B-1

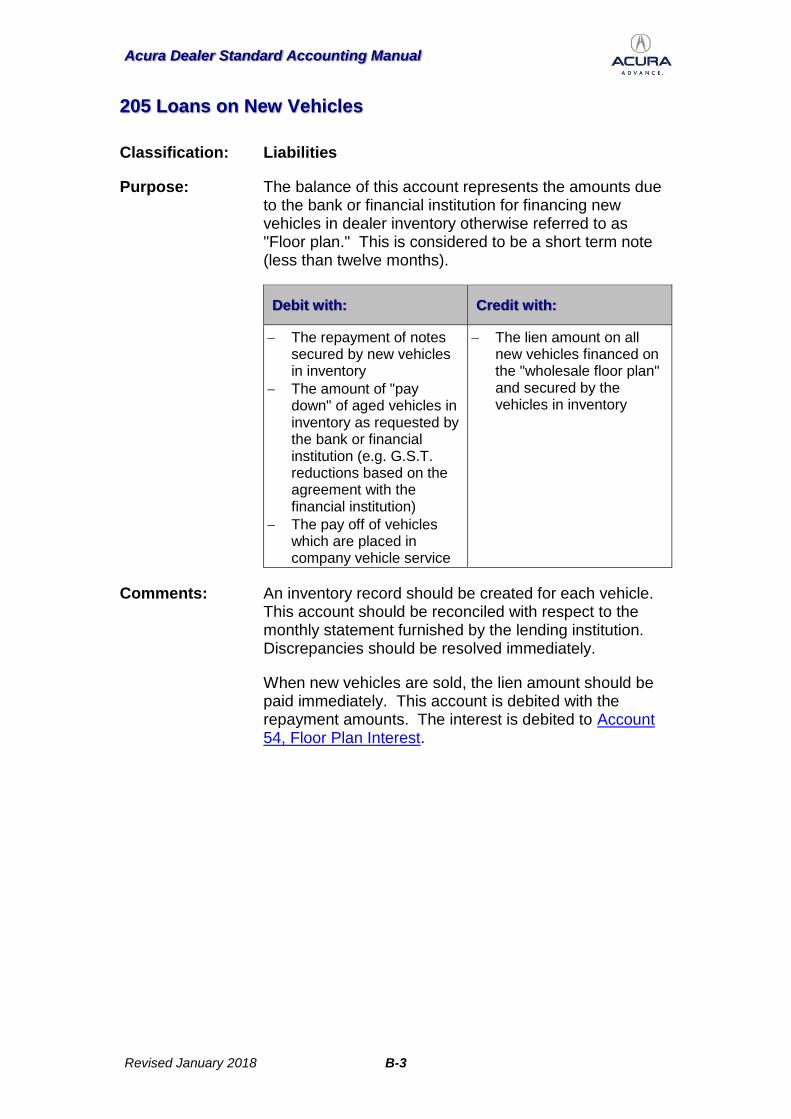

201 Bank Loan .................................................................................. B-2 205 Loans on New Vehicles .............................................................. B-3 206 Loans On Rental Vehicles .......................................................... B-4

207 Loans on Used Vehicles............................................................. B-5 208 Loans on Demonstrators / Courtesy vehicles ............................. B-6 209 Loans on Other Inventories ........................................................ B-7 210 Car Encumbrances .................................................................... B-8

212 Due on Repossession ................................................................ B-9 213 Current Portion - Long Term Debt ............................................ B-10 214 Customer Payments ................................................................. B-11

215 Trade Accounts Payable .......................................................... B-12

Acura Dealer Standard Accounting Manual

Revised January 2018

217 Payroll Deductions (To Include All Payroll Deductions)............ B-13

218 Factory Payable ....................................................................... B-14 219A Goods and Services Tax (Input Tax Credit) ........................... B-15

219B Goods and Service Tax (Payable) ......................................... B-18 220 Provincial Sales Tax ................................................................. B-21 221 Vehicle Sales Personnel Compensation .................................. B-22 222 Customer Deposits ................................................................... B-23 225 Accrued Payroll ........................................................................ B-24

226 Accrued Vacation Pay .............................................................. B-25 227 Accrued Interest ....................................................................... B-26 228 Bonuses ................................................................................... B-27 230 Deferred Marketing Allowance ................................................. B-28 231 Provision for Income Tax - Current Year .................................. B-30

232 Federal & Provincial Taxes - Prior Period ................................ B-31 233 Prepaid Income Tax ................................................................. B-32

234 Estimated Income Tax.............................................................. B-33

240 Notes Payable .......................................................................... B-34 246 Mortgage - Real Estate ............................................................ B-35 247 Deferred Taxes ........................................................................ B-36 248 Financing Leased Vehicles ...................................................... B-37

249 Chattel Mortgage ...................................................................... B-38 255 Other Long Term Debt ............................................................. B-39

256 Provision for Repossession ...................................................... B-40 260 Directors' or Shareholders' Loans ............................................ B-41

C- NET WORTH .................................................................................... C-1

280 Capital Stock Issued - Common ................................................. C-2 282 Capital Stock Issued - Preferred ................................................ C-3

285 Retained Earnings - Prior Years ................................................. C-4

286 Dividends ................................................................................... C-5

287 Investment - Proprietor or Partners ............................................ C-6 290 Withdrawals - Proprietor or Partners .......................................... C-7

299 Profit (Loss) Clearing.................................................................. C-8

D- SALES AND COST OF SALES ........................................................ D-1

301-315, New Vehicles ..................................................................... D-2 401-415 New Vehicles .................................................................... D-2

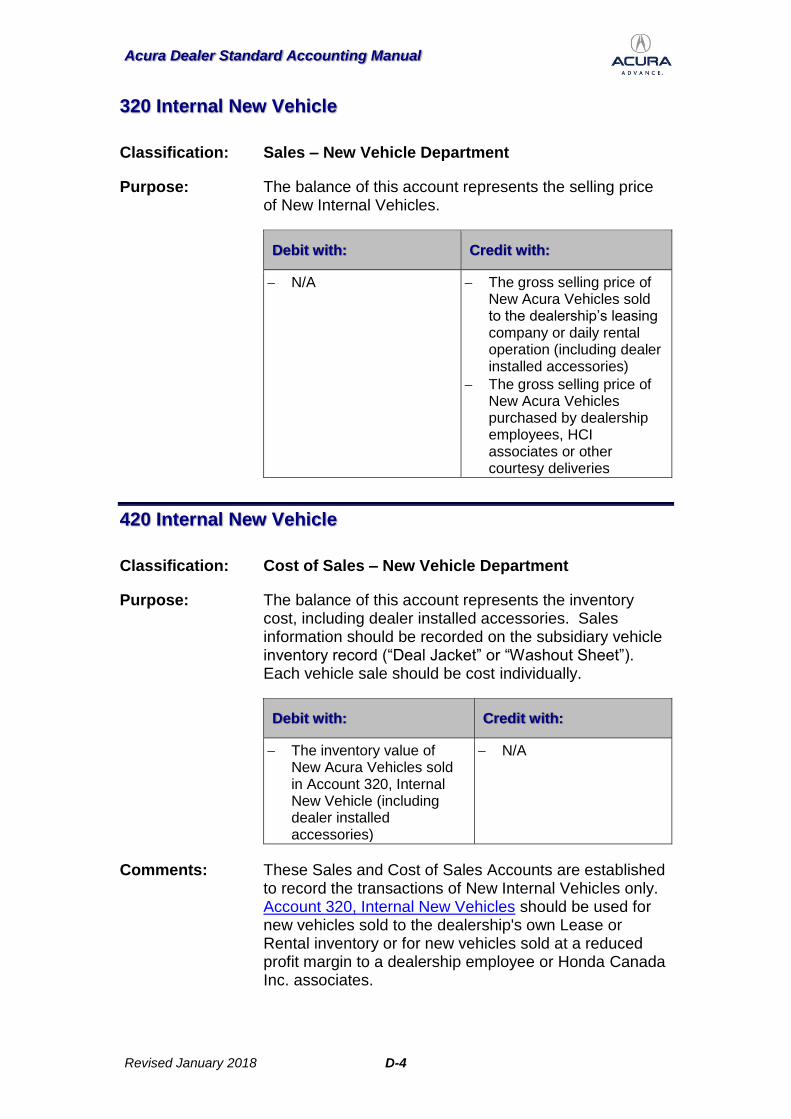

320 Internal New Vehicle .................................................................. D-4 420 Internal New Vehicle ................................................................ D-4

321 Fleet Sales ................................................................................. D-6

421 Fleet Sales ............................................................................... D-6 323 Certified Pre-Owned Acura – Retail ........................................... D-7

423 Certified Pre-Owned Acura – Retail ......................................... D-7

325 Non-Certified, Pre-Owned Acura - Retail ................................... D-9 425 Non-Certified Pre-Owned Acura – Retail ................................. D-9

327 Used Other – Retail .................................................................. D-11 427 Used Other – Retail ................................................................ D-11

332 Used Vehicle Wholesale .......................................................... D-12 432 Used Vehicle Wholesale ........................................................ D-12

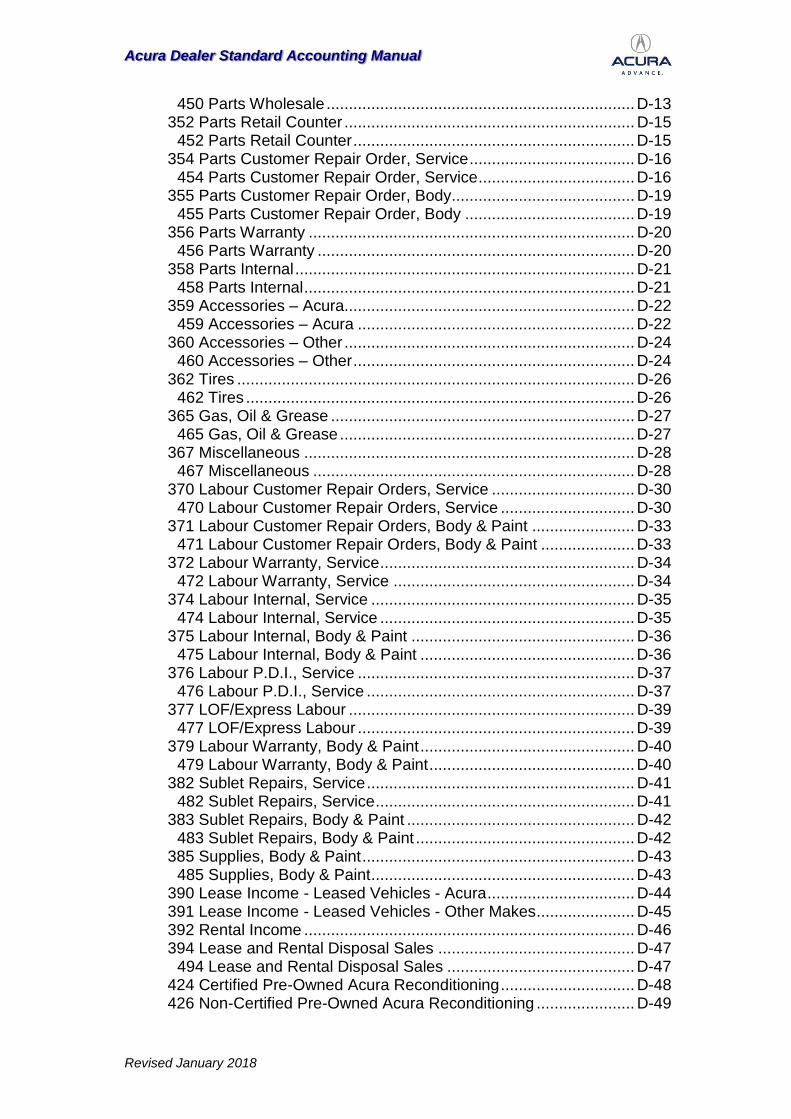

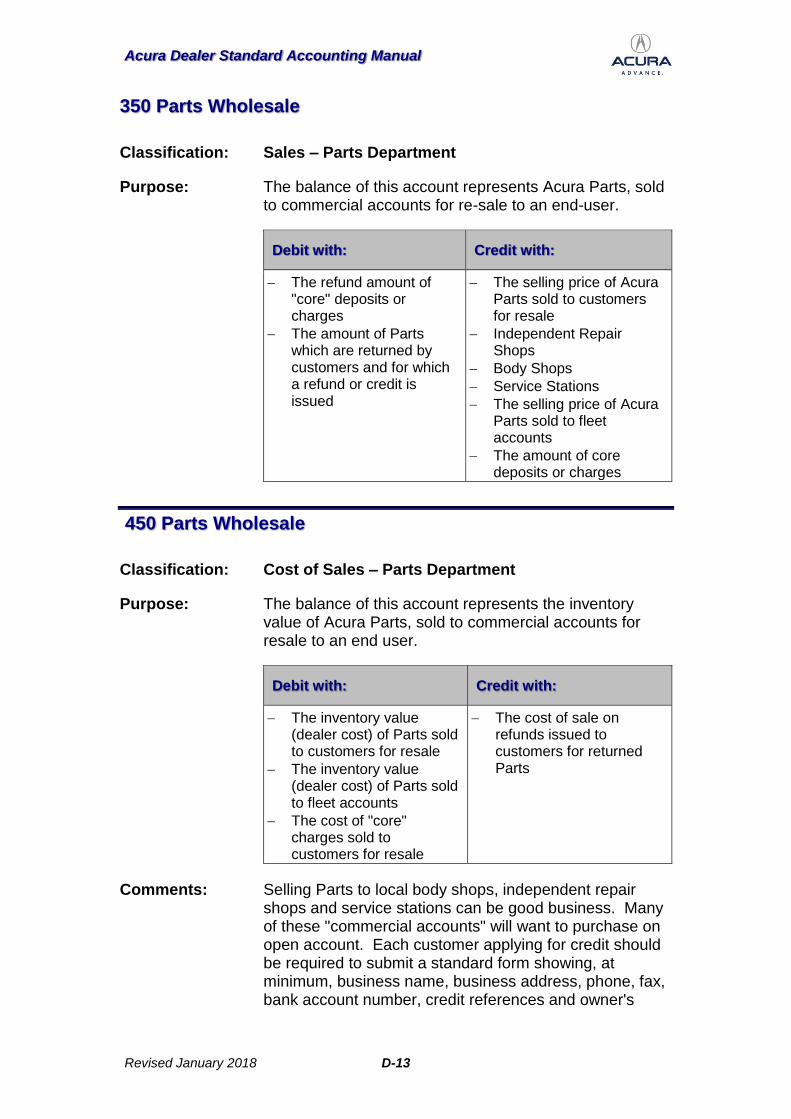

350 Parts Wholesale ....................................................................... D-13

Acura Dealer Standard Accounting Manual

Revised January 2018

450 Parts Wholesale ..................................................................... D-13

352 Parts Retail Counter ................................................................. D-15 452 Parts Retail Counter ............................................................... D-15

354 Parts Customer Repair Order, Service ..................................... D-16 454 Parts Customer Repair Order, Service ................................... D-16

355 Parts Customer Repair Order, Body......................................... D-19 455 Parts Customer Repair Order, Body ...................................... D-19

356 Parts Warranty ......................................................................... D-20

456 Parts Warranty ....................................................................... D-20 358 Parts Internal ............................................................................ D-21

458 Parts Internal .......................................................................... D-21 359 Accessories – Acura................................................................. D-22

459 Accessories – Acura .............................................................. D-22

360 Accessories – Other ................................................................. D-24 460 Accessories – Other ............................................................... D-24

362 Tires ......................................................................................... D-26

462 Tires ....................................................................................... D-26 365 Gas, Oil & Grease .................................................................... D-27

465 Gas, Oil & Grease .................................................................. D-27 367 Miscellaneous .......................................................................... D-28

467 Miscellaneous ........................................................................ D-28 370 Labour Customer Repair Orders, Service ................................ D-30

470 Labour Customer Repair Orders, Service .............................. D-30 371 Labour Customer Repair Orders, Body & Paint ....................... D-33

471 Labour Customer Repair Orders, Body & Paint ..................... D-33

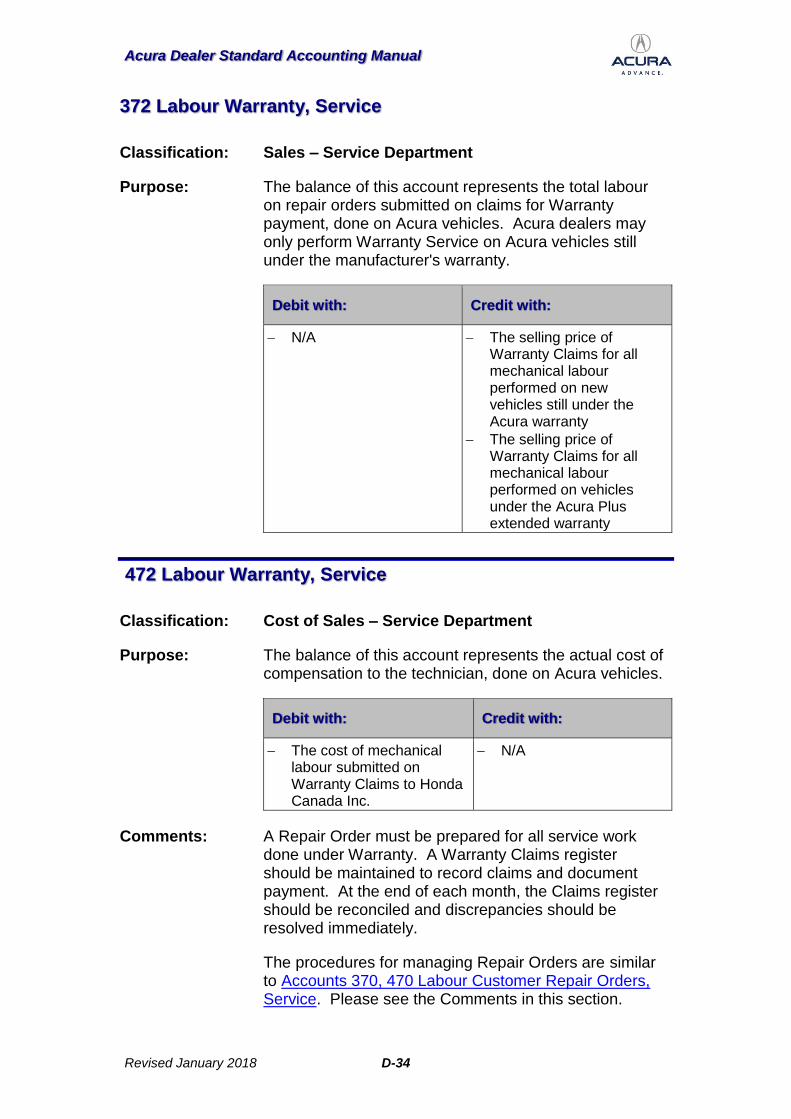

372 Labour Warranty, Service ......................................................... D-34 472 Labour Warranty, Service ...................................................... D-34

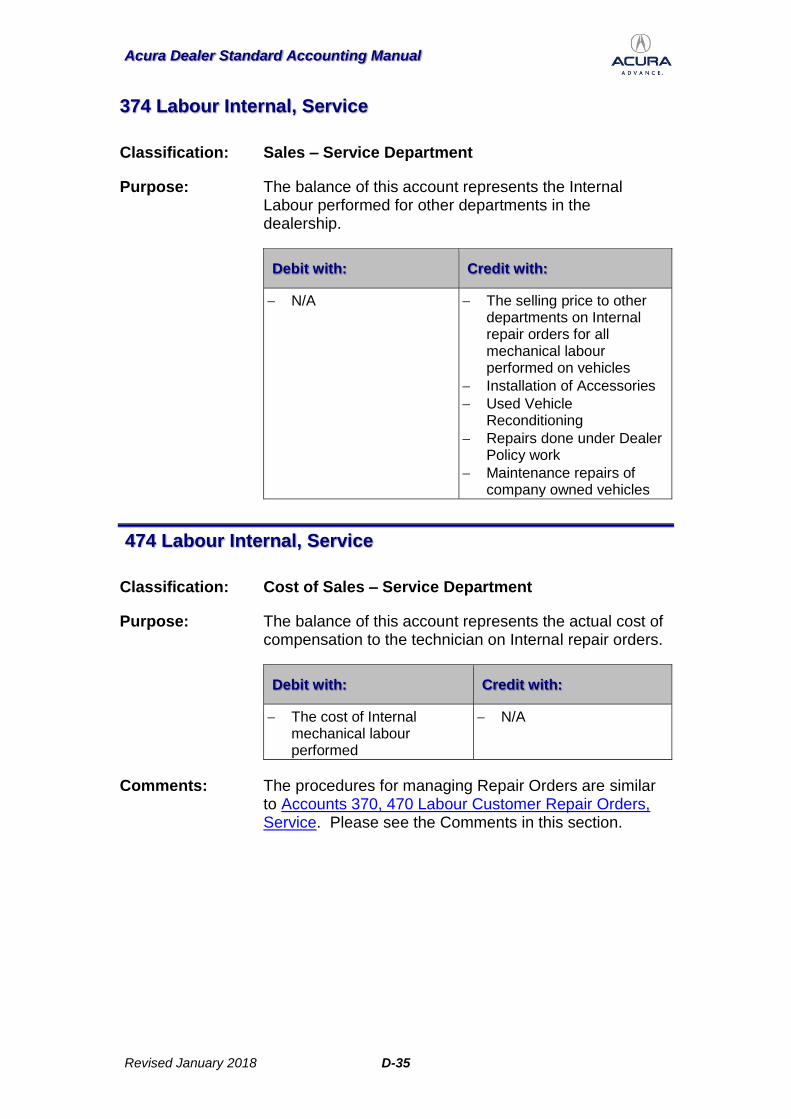

374 Labour Internal, Service ........................................................... D-35 474 Labour Internal, Service ......................................................... D-35

375 Labour Internal, Body & Paint .................................................. D-36 475 Labour Internal, Body & Paint ................................................ D-36

376 Labour P.D.I., Service .............................................................. D-37 476 Labour P.D.I., Service ............................................................ D-37

377 LOF/Express Labour ................................................................ D-39 477 LOF/Express Labour .............................................................. D-39

379 Labour Warranty, Body & Paint ................................................ D-40

479 Labour Warranty, Body & Paint .............................................. D-40 382 Sublet Repairs, Service ............................................................ D-41

482 Sublet Repairs, Service .......................................................... D-41 383 Sublet Repairs, Body & Paint ................................................... D-42

483 Sublet Repairs, Body & Paint ................................................. D-42 385 Supplies, Body & Paint ............................................................. D-43

485 Supplies, Body & Paint ........................................................... D-43 390 Lease Income - Leased Vehicles - Acura ................................. D-44 391 Lease Income - Leased Vehicles - Other Makes ...................... D-45

392 Rental Income .......................................................................... D-46 394 Lease and Rental Disposal Sales ............................................ D-47

494 Lease and Rental Disposal Sales .......................................... D-47 424 Certified Pre-Owned Acura Reconditioning .............................. D-48 426 Non-Certified Pre-Owned Acura Reconditioning ...................... D-49

Acura Dealer Standard Accounting Manual

Revised January 2018

428 Used Other Reconditioning ...................................................... D-50

435 Inventory Revaluation............................................................... D-51 463 Parts Discount Earned ............................................................. D-52

464 Parts Inventory Adjustment ...................................................... D-53 480 Unapplied Time, Service .......................................................... D-54 481 Unapplied Time, Body & Paint ................................................. D-55 490 Amortization, Interest, Maintenance, Leased Vehicles, Acura . D-56 491 Amortization, Interest, Maintenance, Leased Vehicles, Other Make ............................................................................................... D-57 492 Amortization, Interest and Vehicle Maintenance ...................... D-58

E- EXPENSES ....................................................................................... E-1

Expense Distribution ............................................................................ E-2 01 Compensation - Vehicles Sales Personnel .................................. E-8

02 Compensation - Finance & Insurance ........................................ E-10

03 Pre - Delivery ............................................................................. E-11 05 Policy Inspection ........................................................................ E-12

20 Salaries - Managers ................................................................... E-13 21 Salaries - Owners ....................................................................... E-14 22 Salaries - Others ........................................................................ E-15 23 Absentee And Vacation Pay ....................................................... E-16

24 Employee Benefits ..................................................................... E-17 30 Office Supplies ........................................................................... E-18

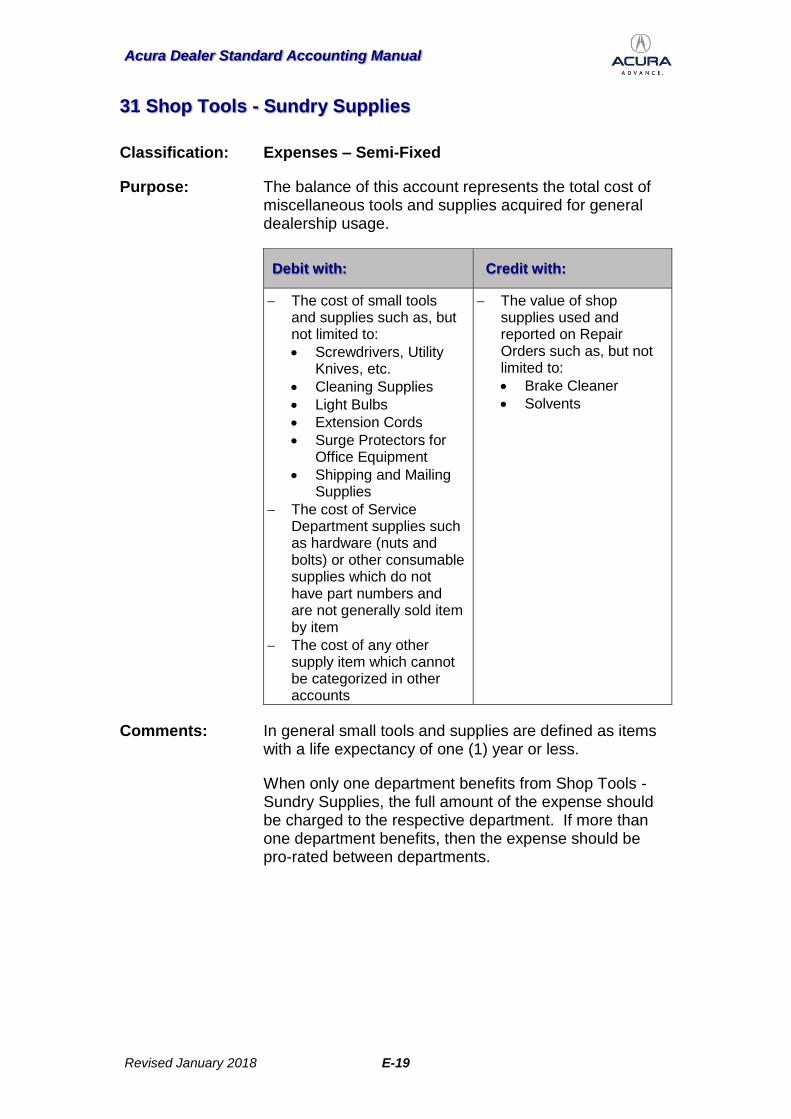

31 Shop Tools - Sundry Supplies .................................................... E-19 32 Courtesy Vehicles ...................................................................... E-20 34 Laundry - Uniforms ..................................................................... E-24

35 Janitor Services - Cleaning ........................................................ E-25 36 Postage ...................................................................................... E-26

37 Policy Adjustments ..................................................................... E-27

38 Advertising ................................................................................. E-28

39 Donations ................................................................................... E-31 41 Company Vehicles ..................................................................... E-32

42 Inventory Maintenance - Vehicle Department ............................ E-33 44 Data Processing ......................................................................... E-34

45 Training ...................................................................................... E-35 46 Travel - Entertainment ................................................................ E-36 47 Telephone - Fax ......................................................................... E-37 48 Membership Dues & Subscriptions ............................................ E-38 49 Freight - Express ........................................................................ E-39

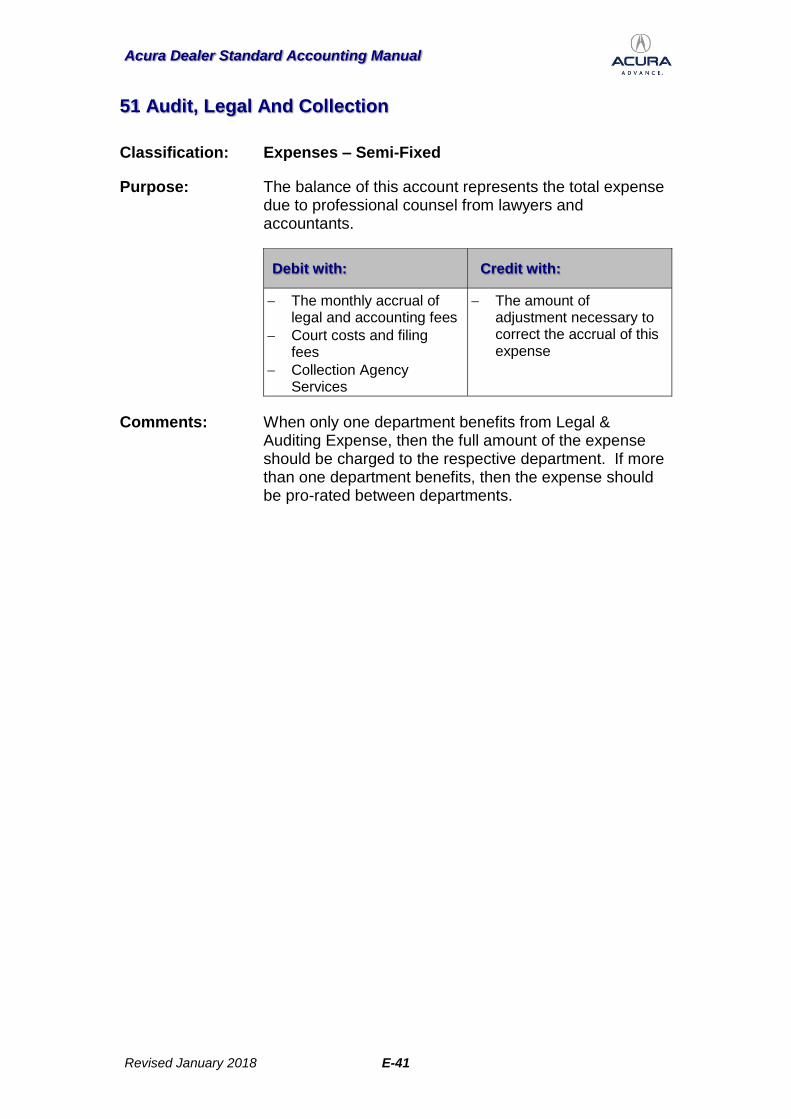

50 Outside Services ........................................................................ E-40 51 Audit, Legal And Collection ........................................................ E-41 52 Miscellaneous ............................................................................ E-42

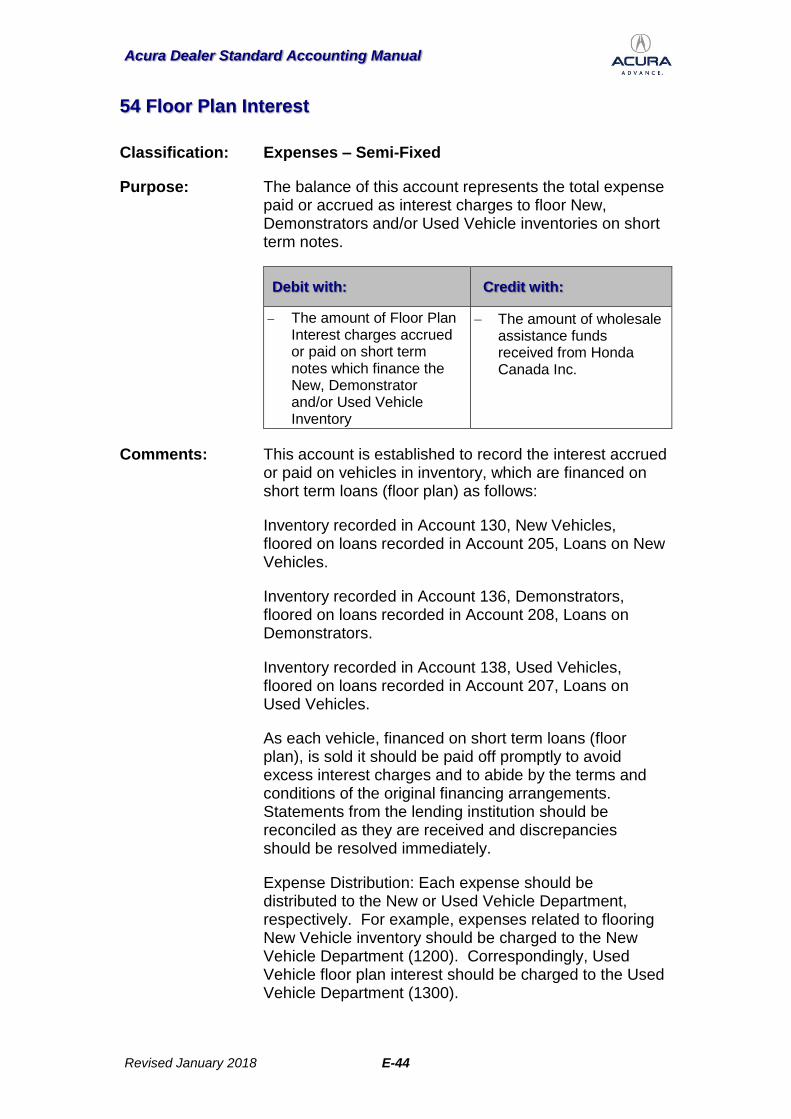

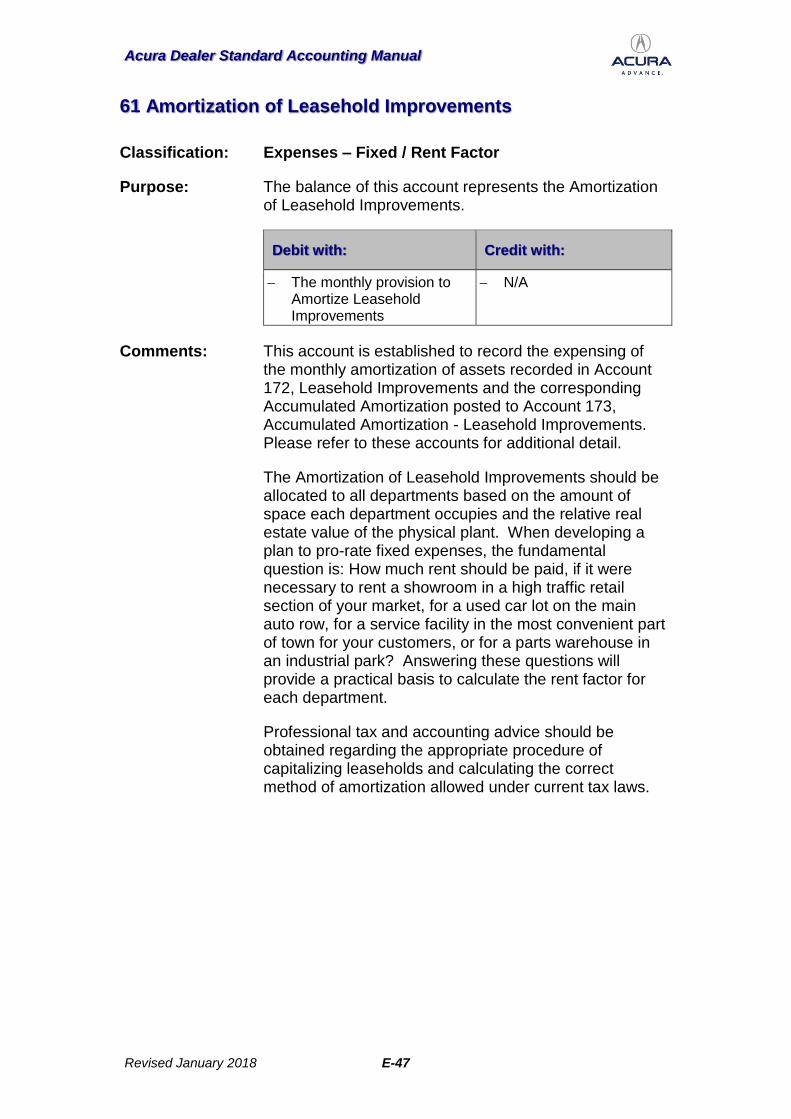

53 Interest & Bank Charges ............................................................ E-43 54 Floor Plan Interest ...................................................................... E-44 60 Rent And/Or Mortgage Interest .................................................. E-46 61 Amortization of Leasehold Improvements .................................. E-47

62 Property Maintenance ................................................................ E-48 63 Property Taxes ........................................................................... E-49 64 Building Insurance ...................................................................... E-50

65 Building Amortization ................................................................. E-51

Acura Dealer Standard Accounting Manual

Revised January 2018

68 Business And Other Taxes ......................................................... E-52

69 Amortization - Equipment and Fixtures ...................................... E-53 70 General Insurance ...................................................................... E-54

73 Maintenance of Equipment ......................................................... E-55 74 Heat, Light, Power And Water .................................................... E-56 75 Equipment Rental ....................................................................... E-57 78 Amortization of Deferred Charges and Intangibles ..................... E-58 80 Licenses (Company Only) .......................................................... E-59

90 Marketing Allowance for New Vehicles Sold .............................. E-60 91 Acura Concierge / AAFP Fund ................................................... E-62 99 Bonuses - Owners ...................................................................... E-63

F- OTHER INCOME AND DEDUCTIONS ............................................. F-1

701 Contract Reserves- New ............................................................ F-2

702 Extended Warranty Income- New .............................................. F-3

752 Extended Warranty Income- New .............................................. F-4 703 – Acura Product Including Insurance ......................................... F-5

753 –Acura Product Inc. Insurance ................................................... F-6 704 – Non-Acura Product Including insurance .................................. F-7 754 – Non-Acura Product Including insurance .................................. F-8 705 Repossession Losses and Charge Backs - New ........................ F-9

706 Finance Income - Used ............................................................ F-11 707 Protection Plan Income - Used ................................................. F-12

757 Protection Plan Income - Used ................................................. F-13 708 Other Merchandise – Used ...................................................... F-14 758 Other Merchandise – Used ...................................................... F-15

709 Repossession Losses and Charge Backs - Used .................... F-16 801 Cash Discount Earned ............................................................. F-18

802 Interest Earned ......................................................................... F-19

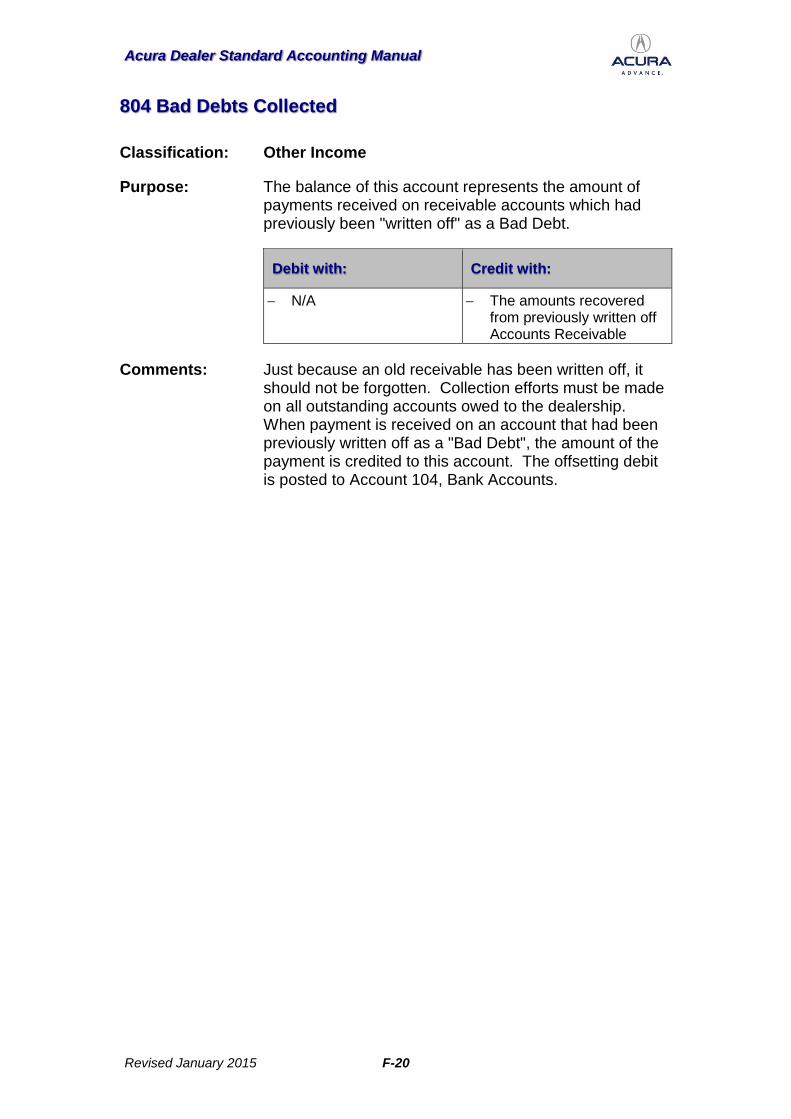

804 Bad Debts Collected................................................................. F-20

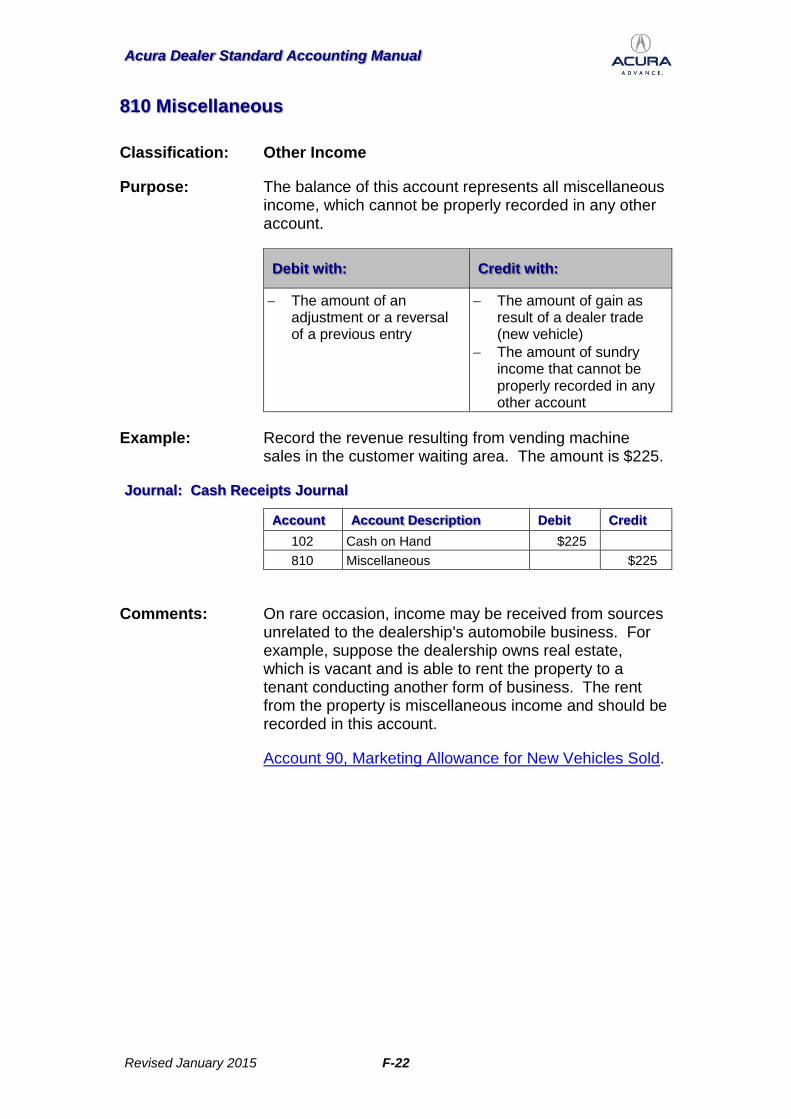

806 Compensation Earned - Sales Tax .......................................... F-21 810 Miscellaneous .......................................................................... F-22

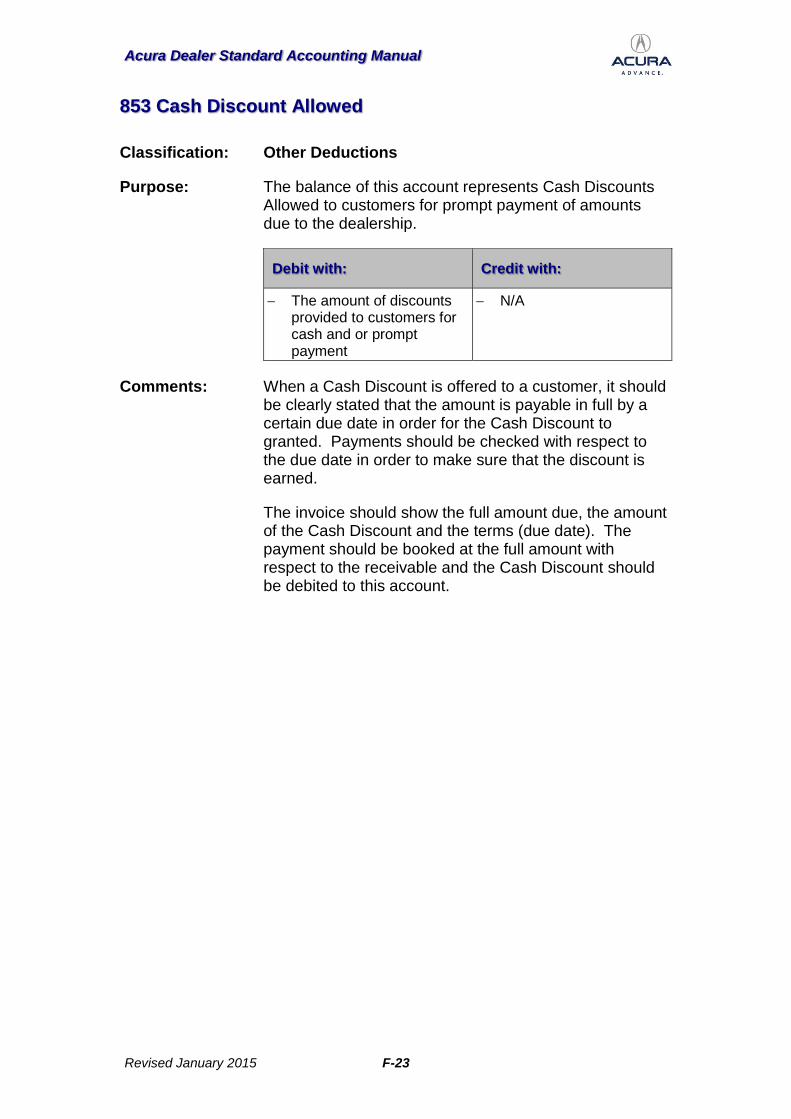

853 Cash Discount Allowed ............................................................ F-23 854 Bad Debt Expense ................................................................... F-24

856 Director's Fees ......................................................................... F-25 860 Miscellaneous .......................................................................... F-26

Index .......................................................................................... F-i

Acura Dealer Standard Accounting Manual

Revised January 2018 1

Introduction Honda Canada Inc. is pleased to present this revised Standard Accounting Manual in a web-based format. We have expanded the manual to provide precise account definitions, clear accounting instructions and comments about proper utilization and guidelines for interpreting the account balance. We hope that this Manual will be helpful in setting up your internal accounting procedures. We also hope that the individual pages will serve as a training aid for new employees. By adhering to Standard Acura accounting procedures, your monthly Financial Statements will become a better management tool. You will be able to apply Acura guidelines in order to improve operational efficiency and get the most from your dealership. We ask that you keep good records, prepare and submit your monthly Financial Statements on time. By doing so, we will be able to provide feedback that will benefit your dealership directly. Your Financial Statements are your scorecards to let you know when you are improving and by how much. Our Acura guidelines will provide benchmarks that will help you set objectives for your managers and make adjustments to produce more profit.

With respect to issues relating to taxation, we strongly recommend that you seek professional tax and accounting advice. Due to the complexity of tax laws, we cannot provide individual counsel in this area. Matters relating to taxes are beyond the scope of this Manual.

We sincerely hope that our efforts in this area provide additional value to being an Acura dealer. It is one example of our intention to support you, your dealership and your employees. We look forward to working with you in the years to come and to see your progress each month along the way. Sincerely, Dealer Development Honda Canada Inc.

Acura Dealer Standard Accounting Manual

Revised January 2018 2

Monthly Routine

Prepare the Monthly Financial Statement to the nearest dollar (no cents). The accounting staff should arrange to have the financial statement completed by the 10th of the following month for submission to Honda Canada Inc. no later than the 15th of that month, via the HONDACOM system.

At the end of each month, several steps should be taken to facilitate the preparation of the Financial Statement.

1. The Petty Cash Fund should be replenished. 2. Review Payables and process for payment by stipulated deadlines in

order to avoid late payment penalties and interest. Verify that Purchase Orders have been properly prepared for all invoices received.

3. All bank balances should be reconciled with bank statements. 4. Prepare a schedule of finance contracts receivable. 5. Receivables should be aged and reconciled - Doubtful Accounts

should be reserved against and expensed as Bad Debts. 6. Prepare various inventory schedules for New Vehicles, Used Vehicles,

Rental Vehicles, Other Inventories, Sublet Repairs, Tires, Labour in Process, Paint & Body Shop Supplies, Gas, Oil & Grease, and miscellaneous assets. Reconcile with actual physical inventory on hand. Adjust account balances in the General Journal as necessary.

7. Make necessary adjustments to Prepaid Expenses. 8. Record the monthly Amortization of Fixed Assets. 9. Reconcile balances of Car Encumbrances, Customer Payments Trade

Accounts Payable, Payroll Deductions, Factory Payable, G.S.T. & P.S.T. Payable, Vehicle Sales Personnel Compensation, and Customer Deposits.

10. Set up accruals for Payroll, Vacation Pay, Accrued Interest, Accrued Bonuses, and Taxes and any other expense that has not been recorded through normal processes, yet which applies to that month.

11. Estimate and post Income Tax Liability. 12. Balance all Journals and post summaries to the General Ledger

(manual bookkeeping). 13. Post adjusting entries to the General Ledger as necessary. 14. Prepare and review the Trial Balance for accuracy. 15. Prepare the Financial Statement.

Acura Dealer Standard Accounting Manual

Revised January 2018 3

Management Operating Information

This section, on page 5 of the Financial Statement, is intended to provide information which is useful in assessing productivity. It covers:

Dealership Receivables Service Department Data Distribution of Personnel (Dealership Personnel Count) New and Used Vehicle Inventory Analysis Absorption and Break-Even Analysis

Dealership Receivables

This section summarizes the following accounts and provides an aging summary detailing the Receivables which are Current, 31 – 60 days past due, 61 – 90 days past due and over 90 days past due.

Account 115, Accounts Receivable – Customer Service, Parts, Body Shop

Account 116, Accounts Receivable – Vehicles

Account 118, Notes Receivable

Account 119, Lease Receivables

Account 125, Allowance for Doubtful Accounts

Account 117, Factory Receivables

Account 120, Warranty Receivables

Account 123, Finance & Insurance Commissions

Account 122, Miscellaneous Receivables

Total Receivables should agree with page 1, line 20.

Distribution of Personnel (Dealership personnel count)

Please provide number of employees by category and department. Use only whole numbers to report the Personnel Count. For employees that support more than one department such as administrative staff, assign each respective employee to the department that receives the majority of the service. Dealer Principals and General Managers may be assigned to the New Vehicle Department. Do not assign employees to the Body Shop if the dealership does not have a Body Shop. The same applies to the "Other" Department.

New, Used Vehicle Inventory Analysis

Please provide an aged analysis of new and used vehicles in inventory by both units and dollars. The total in units and dollars of both new and used vehicles should agree with the respective inventory statistics on page 1 of the Financial Statement.

Acura Dealer Standard Accounting Manual

Revised January 2018 4

Parts & Accessories Inventory Analysis

The Parts and Accessories Inventory Analysis is designed to provide ageing of dealerships’ Acura Parts and Accessories Inventories. This section includes columns for both units and dollar values.

Units refer to the number of pieces in the dealership’s parts inventory at the end of the period and dollars refer to the cost value of this inventory. These details should be available on the Parts management report from your dealership’s management system (i.e., DMS – ADP, Reynolds and Reynolds, PBS, SERTI, DIS, etc.). Please note that this inventory analysis is for Acura Parts and Accessories inventory and specifically excludes tire inventory as well as parts and accessories inventory other than Acura.

Service Department Data

Available Time is the actual time technicians were available for work (i.e. 5 technicians @7 hrs/day = 35 hrs/day total Available Time). It does not include holidays, sick leave, etc.)

Clocked R.O. Time is the time which the technician(s) actually used to perform the repair(s).

Charged Out Time is the time that was charged to the Customers on the repair order, and mostly reflects flat rate times or menu priced items.

Customer Pay Time is the time that was charged to Customers on the repair orders, and mostly reflects flat rate times or menu priced items.

Warranty Time is the time that was charged to Warranty on repair orders, and mostly reflects flat rate times or menu priced items.

Internal Time is the time that was charged to Internal departments on repair orders, and mostly reflects flat rate times or menu priced items.

Customer R.O.'s summarizes the number of Customer repair orders written for that month and year to date (do not include Warranty or Internal repair orders).

Total R.O.'s is the number of all repair orders written, including Internal, Warranty P.D. I. and Express Labour.

Acura Dealer Standard Accounting Manual

Revised January 2018 5

Average Technician Hourly Wage

is the average hourly compensation for all technicians. In the case of straight time operation, total the hourly wages for all the technicians and divide by the number of billed hours. In the case of flat rate operation, divide total wages paid by total available time ($ + hrs.).

Customer Labour Rate is the hourly rate charged to Customers during the period of the Financial Report.

Warranty Labour Rate is the hourly rate paid by Honda Canada for repairs performed under warranty, for the period of time of the Financial Report.

Internal Labour Rate is the hourly rate charged by the Service Department to other Departments, such as sales, etc.

Bays is the number of available productive work stalls contained inside the Service and Body Shop areas.

Active Customers in File is the number of Customers that have visited the dealer during the last 12 months at least twice for service or maintenance.

Service Potential is the number of Units In Operation (U.I.O)

Absorption & Breakeven analysis

Absorption and breakeven analysis provides information on gross profit generation and its coverage of fixed overhead. This is represented in terms of absorption and new unit break-even.

VARIABLE GROSS PROFIT (L)

is the sum of the gross profits for both "New and Used Vehicle Department, from page 4.

VARIABLE SELLING EXPENSES (M)

is the sum of the New and Used Vehicle Selling Expenses, from page 2.

VARIABLE SALES PROFIT (N)

is the Variable Gross Profit less the Variable Selling Expenses.

(L – M)

CONTRIBUTION PNVS (O) is the Variable Sales Profit (N) divided by the number of New Vehicles Sold.

Acura Dealer Standard Accounting Manual

Revised January 2018 6

N / PNVS

FIXED GROSS PROFIT (P) is the gross profit from all departments excluding New and Used Vehicle Departments.

TOTAL FIXED OVERHEAD (Q)

is the total of Semi-Fixed and Fixed Expenses from page 2.

MARKETING ALLOWANCE + AAFP FUND + OTHER INCOME AND DEDUCTIONS (R)

is the total of marketing allowance, AAFP Fund, and the net of Other Income and Deductions from page 2.

UNABSORBED OVERHEAD (S)

is the Total Fixed Overhead not absorbed by Fixed Gross Profit and Other Income.

Q - (P + R)

ABSORPTION (T) is the percentage of Total Fixed Overhead, which is covered by the Fixed Gross Profit.

P x 100 / Q

UNIT BREAKEVEN (U) is the unabsorbed overhead divided by the Contribution PNVS. If your break-even figure was 19, for example, this would indicate that the dealership would have to sell 19 new units to break-even.

S / O

Acura Dealer Standard Accounting Manual

Revised January 2018 7

Acura Dealer Standard Accounting Manual

Revised January 2018 8

Chart of Accounts Summary – Acura Assets

Cash & Equivalent 101 Petty Cash 102 Cash on Hand 104 Bank Accounts 105 Trust Account 107 Finance Contracts In Transit 108 Marketable Securities 109 Cash Sales Clearing 110 Vehicle Licenses Clearing

Receivables 115 Accounts Receivable - Cust. Service, Parts, Body Shop 116 Accounts Receivable - Vehicles 117 Accounts Receivable - Factory 119 Lease Receivables 120 Warranty Claims 121 Marketing Allowance Receivable 122 G.S.T. Receivable 123 Finance & Insurance Commissions 125 Allowance For Doubtful Accounts

Inventories 130 New Vehicles 136 Demonstrators 138 Used Vehicles 139 Courtesy Vehicles - Inventory 140 Daily Rental Vehicles 141 Other Inventories 142 Parts – Acura 144 Accessories - Acura 145 Parts - Other 146 Accessories – Other 148 Tires 149 Sublet Repairs 150 Labour In Process 151 Gasoline (Fuel), Oil & Grease 152 Paint & Body Shop Supplies

Prepaid Expenses 154 Prepaid Rent 155 Prepaid Taxes 156 Prepaid Insurance 157 Other Prepaid Expenses

Fixed Assets 165 Land 167 Buildings 168 Accumulated Amortization - Buildings 1690 EDP Equipment 1691 Accumulated Amortization - EDP Equipment 170 Building Fixtures 171 Accumulated Amortization - Building Fixtures 172 Leasehold Improvements 173 Accumulated Amortization - Leasehold Imp. 174 Office Equipment 175 Accumulated Amortization - Office Equipment 176 Parts Department Equipment 177 Accumulated Amortization - Parts Dept. Equip. 178 Service Department Equipment 179 Accumulated Amortization - Service Dept. Equip. 181 Signs 182 Accumulated Amortization - Signs 183 Company Vehicle 184 Accumulated Amortization - Company Vehicles 185 Leased Vehicles 186 Accumulated Amortization - Leased Vehicles

Other Assets 188 Refundable Deposits 189 Investments 190 Organization Expense 191 Life Insurance - Cash Values 192 Advances - Officers & Employees 193 Notes / Long Term Accounts Receivable 195 Goodwill

Liabilities Bank & Finance Company

201 Bank Loan 205 Loans On New Vehicles 206 Loans On Rental Vehicles 207 Loans On Used Vehicles 208 Loans On Demonstrators / Courtesy Vehicles 209 Loans On Other Inventories 210 Car Encumbrances 212 Due On Repossession 213 Current Portion - Long Term Debt 214 Customer Payments

Accounts Payable 215 Trade Accounts Payable 217 Payroll Deductions 218 Factory Payable 219A Goods And Service Tax (Input Tax Credit) 219B Goods And Services Tax (Payable) 220 Provincial Sales Tax 221 Vehicle Sales Personnel Compensation 222 Customer Deposits

Accrued Liabilities 225 Accrued Payroll 226 Accrued Vacation Pay 227 Accrued Interest 228 Accrued Bonuses 230 Deferred Marketing Allowance 231 Provision For Income Tax - Current Year 232 Federal & Provincial Taxes - Prior Period 233 Prepaid Income Tax

Long Term Liabilities 240 Notes Payable 246 Mortgage - Real Estate 247 Deferred Taxes 248 Financing Leased Vehicles 249 Chattel Mortgage 255 Other Long Term Debt 256 Provision For Repossessions 260 Directors' Or Shareholders' Loans

Net Worth 280 Capital Stock Issued - Common 282 Capital Stock Issued - Preferred 285 Retained Earnings - Prior Years 286 Dividends 287 Investment - Proprietor Or Partners 290 Withdrawals - Proprietor Or Partners 234 Estimated Income Tax 299 Profit And Loss Clearing

Acura Dealer Standard Accounting Manual

Revised January 2018 9

196 Finance Company Participation

Operating Accounts

New Vehicle

Acura Sales COS 304 404 ILX 308 408 TLX 309 409 RLX 310 410 RLX Hybrid 312 412 RDX 313 413 MDX 315 415 NSX 320 420 Internal - New Vehicle 321 421 Fleet Sales

Used Vehicles Sales COS 323 423 Certified Used Acura - Retail

424 Certified Used Acura - Reconditioning 325 425 Non-Certified Used Acura - Retail

426 Non-Certified Used Acura - Reconditioning 327 427 Used Other - Retail

428 Used Other Reconditioning 332 432 Used Vehicle Wholesale

435 Inventory Revaluation

Parts 350 450 Parts - Wholesale 352 452 Parts - Retail Counter 354 454 Parts - Customer Repair Order, Service 355 455 Parts - Customer Repair Order, Body Shop 356 456 Parts - Warranty 358 458 Parts - Internal 359 459 Accessories - Acura 360 460 Accessories – Other 362 462 Tires

463 Parts Discount Earned 464 Parts Inventory Adjustment

365 465 Gas (Fuel), Oil & Grease 367 467 Miscellaneous

Service 370 470 Labour - Customer Repair Orders, Service 372 472 Labour - Warranty, Service 374 474 Labour - Internal, Service 376 476 Labour - P.D.I., Service 377 477 Express Labour

480 Unapplied Time - Service 382 482 Sublet Repairs - Service

Body Shop 371 471 Labour - Customer Repair Orders, Body &

Paint 375 475 Labour - Internal, Body & Paint 379 479 Labour - Warranty, Body & Paint

481 Unapplied Time, Body & Paint 383 483 Sublet Repairs - Body & Paint 385 485 Supplies - Body & Paint

Lease & Rental 390 Lease Income - Leased Vehicles - Acura

490 Amortization, Interest, Maintenance - Leased Vehicles - Acura

391 Lease Income - Leased Vehicles - Other Makes 491 Amortization, Interest, Maint. - Leased Vehicles - Other Makes

392 Rental Income 492 Amortization, Interest, & Vehicle Maintenance - Rental Vehicles

394 494 Lease & Rental Disposal Sales

Finance & Insurance Income 701 Contract Reserves - New 702 752 Extended Warranty Income - New 703 753 Acura Product Inc. Insurance 704 754 Non –Acura Prod Inc. Insurance 705 Repossession Losses & Chargebacks - New 706 Finance Income - Used 707 757 Extended Warranty Income - Used 708 758 Other Merchandise - Used 709 Repossession Losses & Chargebacks -

Used

Expense Accounts The Expense Accounts consist of four (4) digits. Expenses for each department are organized by the following account ranges:

New Vehicle 1200 – 1280

Used Vehicle 1300 – 1380

Parts 1400 – 1480

Service 1500 – 1580

Body Shop 1600 – 1680

Leasing 1800 – 1880

Other 2800 – 2880

Each Expense Account number is formed by using the department range above and appending the two (2) digits identifying code below. For example, New Vehicle Compensation - Vehicle Sales Personnel is Account Number 1201; Used Vehicle Compensation - Vehicle Sales Personnel is 1301. This pattern is to be applied to all Expense Accounts in order to charge the correct amount to each department. Please refer to the Accounting Manual for a complete discussion of Expense Distribution.

Acura Dealer Standard Accounting Manual

Revised January 2018 10

Variable Selling Expenses 01 Compensation - Vehicle Sales Personnel 02 Compensation - Finance & Insurance 03 Pre-Delivery 05 Policy Inspection

Employment Expenses 20 Salaries -Department Managers 21 Salaries - Owners 22 Salaries - Others 23 Absentee & Vacation Pay 24 Employee Benefits

Semi-Fixed Expenses 30 Office Supplies 31 Shop Tools - Sundry Supplies 32 Courtesy Vehicle 34 Laundry - Uniforms 35 Janitor Services - Cleaning 36 Postage 37 Policy Adjustments 38 Advertising 39 Donations 41 Company Vehicles 42 Inventory Maintenance - Vehicle Department 44 Data Processing 45 Training 46 Travel - Entertainment 47 Telephone - Fax 48 Membership Dues & Subscriptions 49 Freight - Express 50 Outside Services 51 Audit, Legal & Collection 52 Miscellaneous 53 Interest & Bank Charges 54 Floor Plan Interest

Fixed Expenses

Rent Factor 60 Rent And/or Mortgage Interest 61 Amortization Of Leasehold Improvements 62 Property Maintenance 63 Property Taxes 64 Building Insurance 65 Amortization of Building

Other Fixed Expenses 68 Business & Other Taxes 69 Amortization of Equipment & Fixtures 70 General Insurance 73 Maintenance Of Equipment 74 Heat, Light. Power & Water 75 Equipment Rental 80 Licenses (Company Only)

Adjustments 90 Marketing Allowance (for New Vehicles Sold) 91 Acura Concierge / AAFP Fund 99 Bonuses - Owners

Other Income 801 Cash Discount Earned 802 Interest Earned 804 Bad Debts Collected 806 Compensation Earned - Sales Tax 810 Miscellaneous

Other Deductions 853 Cash Discount Allowed 854 Bad Debt Expense 856 Directors' Fees 860 Miscellaneous

Acura Dealer Standard Accounting Manual

Revised January 2018 A-1

Chart of Accounts – Detail by Account

A- ASSETS

Acura Dealer Standard Accounting Manual

Revised January 2018 A-2

101 Petty Cash

Classification: Assets

Purpose: This account reflects a fund set up for the payment of small bills and provision for change for cash registers. It is recommended that items of $25.00 or over be paid by cheque. Every payment from this fund must be supported by a Petty Cash voucher stating the purpose of the payment shown and signed by the person receiving the money. Any invoices involved should be attached to the voucher.

The balance of the actual cash on hand plus the total voucher amount should always equal the original amount of this fund.

Whenever necessary, and always at month-end, diminishing cash may be replenished by issuing a cheque for the total of the vouchers, summarizing the vouchers on a Petty Cash Summary envelope.

Instructions:

Debit with: Credit with:

The amount originally set aside to establish the Petty Cash Fund

Any amount to increase the Petty Cash Fund

The amount which will reduce the Petty Cash Fund to a new level

The amount equal to the remaining balance if the Petty Cash Fund is eliminated

Comments: Each disbursement from the fund should be recorded and explained on a Petty Cash Voucher. The Petty Cash Voucher should indicate the department(s) to which the expense is charged (Please see additional comments in the Expense section). This serves also as a receipt from the person receiving the money. Each Petty Cash Voucher should be summarized on a Petty Cash Summary. A cheque should be issued reimbursing the fund as often as necessary and always at the month-end.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-3

102 Cash on Hand

Classification: Assets

Purpose: This account reflects all receipts from daily business transactions, which have been taken in but, not yet deposited in the bank. This does NOT include Petty Cash, cash deposits, NOR down payments for vehicles. Deposits on vehicles (depending on Provincial rules) may need to be recorded in Account 105, Trust Account.

Debit with: Credit with:

Total of cash received from all sources

Bank deposits

Comments: A receipt should be prepared for all funds taken in during the course of each day's business. No cash disbursements should be made from this account. All cash received should be properly recorded in the cash receipts journal and deposited intact daily.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-4

104 Bank Accounts

Classification: Assets

Purpose: This account reflects the amount on deposit and must be reconciled with the bank statement at month-end, taking into consideration all outstanding cheques, deposits and bank charges.

Instructions:

Debit with: Credit with:

All amounts deposited in the bank

All withdrawals, by cheque or otherwise

Comments: If more than one bank is used, a separate ledger account should be established for each, following the same procedure for each bank.

The bank statement should be given, unopened, to the dealer principal for review prior to routing it to the accounting department. Any discrepancies should be resolved immediately.

*NOTE: A Credit balance reflects a liability, to be recorded as such on balance sheet.

A Debit balance reflects an asset, to be recorded as such on balance sheet.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-5

105 Trust Account

Classification: Assets

Purpose: In certain provinces, there is a legal requirement to keep a separate account of all deposits made by customers on New and Used vehicle transactions. Even if not required by law, this procedure is recommended to protect these deposits from all contingencies.

Debit with: Credit with:

Deposits made by customers on future deliveries of all New and Used vehicles.

Transfers to current bank account on delivery of vehicle or completion of obligation

Refund to customer if delivery of vehicle cannot be finalized

Comments: Because of the legal and tax implications related to customer deposits, professional tax and legal advice should be obtained regarding the proper usage of this account with regard to the laws of each respective province.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-6

107 Finance Contracts in Transit

Classification: Assets

Purpose: The balance represents the amount due from finance institutions on customer finance contracts. A period of time may elapse between the forwarding of retail contracts to the finance company and receipt of the proceeds cheque. The total of all outstanding contracts should agree with the balance in this account at month-end.

Debit with: Credit with:

The net amount (not including interest) of a customer finance contract submitted to a financial institution for payment to the dealership

The amount received from a financial institution on a customer finance contract

Comments: The activity in this account should be reviewed daily. A follow-up with the financial institution must be made if payment is not received promptly. Payments from the financial institutions must be verified to make sure that the amounts are correct. Any under or overpayment must be reconciled immediately. At month-end, a list of the notes for which payment has not been received should be prepared on a Monthly Analysis Sheet. This account must be reconciled at the end of each month.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-7

108 Marketable Securities

Classification: Assets

Purpose: This account reflects investments by the dealership in Marketable Securities or bonds which may be quickly converted into cash within thirty (30) days.

Debit with: Credit with:

The purchase price of securities

The selling or liquidation amount of securities

Comments: If the dealership has a surplus of cash, it may be prudent to invest these funds in liquid investments that may provide a higher yield than ordinary bank interest.

Interest or dividends will be credited to Interest Earned - Account 802.

Profits on the sale of securities should be credited to Miscellaneous Income - Account 810, and any losses should be debited to Miscellaneous Deductions - Account 860.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-8

109 Cash Sales Clearing

Classification: Assets

Purpose: The balance represents cash receipts not yet deposited. Whenever practical, bank deposits should be made daily. This is a control account which should carry no balance at month-end.

Debit with: Credit with:

Cash sales covering new vehicles (excluding customer deposits and down payments)

Cash sales covering used vehicles (excluding customer deposits and down payments)

Cash sales for customer repair orders prepared by the Service or Body Shop Departments

Cash sales for parts and accessories sold on counter tickets

The amount of cash received for depositing in the bank by the New Vehicle Department

The amount of cash received for depositing in the bank by the Used Vehicle Department

The amount of cash received for service or body shop labour completed (and parts sold) on customer repair orders

The amount of cash received for parts and accessories sold on counter tickets

Comments: No money should be paid out of the Cash Clearing account. Disbursements should be made by cheque or from the Petty Cash Fund. Cash receipts, regardless of the source, should pass through the hands of the cashier or person responsible for the cash so that they may be properly recorded and deposited intact.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-9

110 Vehicle Licenses Clearing

Classification: Assets

Purpose: When the dealership is required to apply for a vehicle license to register a sold vehicle on the customer's behalf, the application may be submitted prior to the payment by the customer. The balance in this account reflects all license plates purchased (except Dealer plates - Expense Account 80) and permit transfers paid in advance.

Debit with: Credit with:

The amount of all charges for license plates and transfers

All payments from customers received through the Vehicle Sales Journal for vehicle licenses

Comments: This is a control account to monitor the activity of vehicle licenses purchased on behalf of customers. The activity in this account should be reviewed at month-end. This account should be reconciled monthly. Outstanding amounts for licenses on delivered vehicles which have not been paid should be subject to collection procedures from the customer.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-10

115 Accounts Receivable - Customer Service, Parts, Body

Shop

Classification: Assets

Purpose: The balance represents the unpaid balances of charges made to open accounts for Service, Parts and Body Shop sales. This is a control account and supporting details should be contained in a subsidiary ledger recording the status of all charge sales to customers.

Debit with: Credit with:

The amount of sales charged on open account for Service, Parts ad Body Shop sales (includes open accounts for employees)

The amount of C.O.D. shipments of parts to customers

Customer cheques returned as uncollectible

Payments received which are to be applied to Service, Parts and Body Shop open accounts

Cash discounts offered for early payment of accounts

Credit memos issued to customers for Service, Parts or Body Shop adjustments

Write-offs of uncollectible ac-counts

Comments: Credit should only be extended to customers with a manager's approval. The manager authorizing the charge must be responsible for collecting payment. A subsidiary ledger should be set up for each open account. At the end of each month, all accounts should be aged and efforts must be made to collect the amounts due. Past due accounts should be reviewed by the dealer principal. After sixty (60) days, any amounts deemed, by the dealer principal, to be uncollectible should be set up as a "doubtful account" by crediting the past due amount to Account 125, Allowance for Doubtful Accounts and debiting Account 854, Bad Debt Expense. This complies with accounting procedures prescribed by most lending institutions for proper evaluation of Working Capital.

Subsequently, if a past due account is not paid, the dealer principal should direct the accounting staff to relieve the past due amount from this account by crediting this account and debiting Account 125, Allowance for Doubtful Accounts. Professional tax and

Acura Dealer Standard Accounting Manual

Revised January 2018 A-11

legal advice should be obtained regarding the proper procedures for writing off bad debts. Further, professional tax and legal advice should also be obtained regarding Provincial Sales Tax and/or G.S.T. that may have been included in the amounts in the doubtful accounts.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-12

116 Accounts Receivable - Vehicles

Classification: Assets

Purpose: The balance of this account represents the amount due from customers for sales of vehicles on open account. It does NOT include amounts due on unpaid finance contracts. Unpaid finance contracts should be recorded in Account 107 - Finance Contracts in Transit.

Debit with: Credit with:

The face value of promissory (one pay) notes from customers for vehicle sales (new or used)

The amount owed by customers on open account for vehicles purchased

Cheques returned by the bank as uncollectible for vehicles bought by customers

Payments (excluding interest) received for vehicle accounts

Unpaid balance of an account when the vehicle is repossessed from the customer

Write–offs of uncollectible amounts

Comments: Occasionally, customers will take delivery of vehicles pending funding of approved car loans from the customer's own bank, credit union or other private financing source. When this is the case, the down payment should be collected before delivery and a promissory note should be signed by the customer. This account is a control account which is used to keep track of money owed to the dealership for the purchase of new or used vehicles. Any outstanding amounts should be collected on or before the agreed upon date.

Payments received should be recorded immediately and deposited in the bank on a daily basis. Timeliness of balancing this account is vital.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-13

117 Accounts Receivable - Factory

Classification: Assets

Purpose: The balance of this account represents the amount due to the dealership from Honda Canada Inc. This is a control account and supporting details should be contained in a subsidiary ledger recording charges to Honda Canada Inc.

Debit with: Credit with:

The amount of all charges which have been billed to Honda Canada Inc.

• Program Payments

• Fleet Trading Assistance

• Service Co-op

• Wholesale Assistance

• Transportation Claims

• No Charge Maintenance Programs

The amount of other charges billed

Payments received or adjustments made by Honda Canada Inc.

Comments: In order to facilitate record keeping, it may be convenient to establish sub-accounts for each of the categories shown above.

This account should be reconciled at month-end and any discrepancies should be resolved immediately.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-14

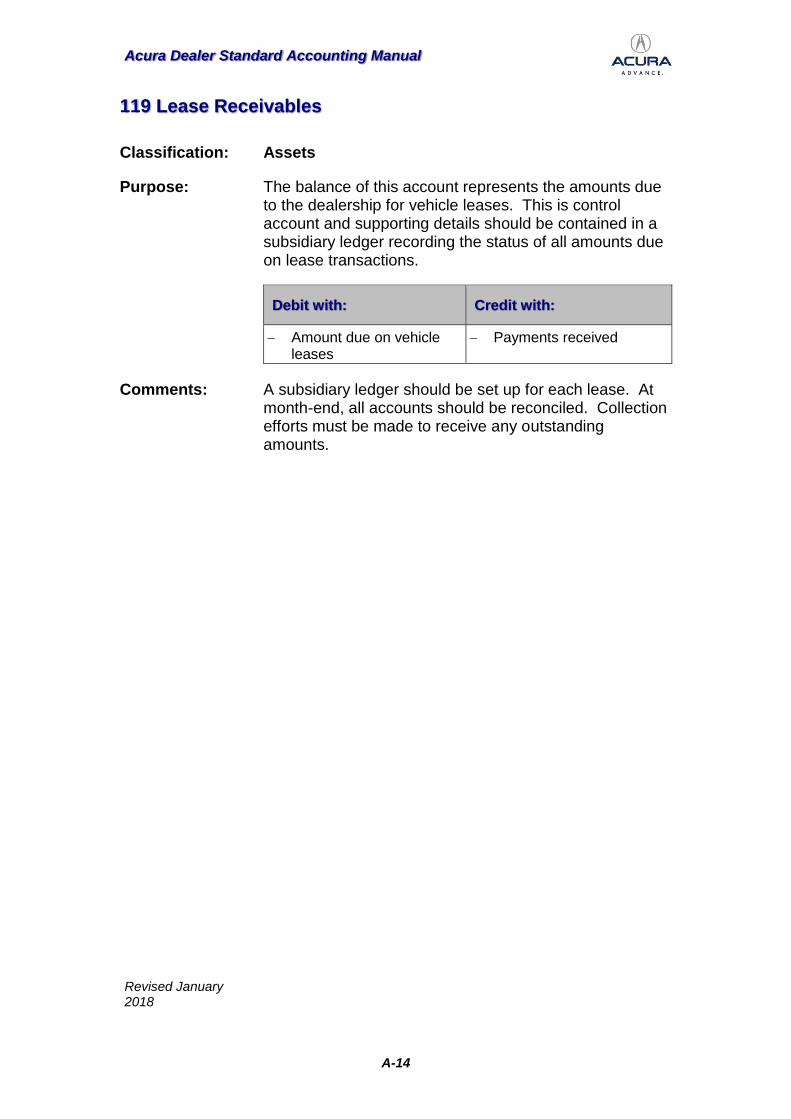

119 Lease Receivables

Classification: Assets

Purpose: The balance of this account represents the amounts due to the dealership for vehicle leases. This is control account and supporting details should be contained in a subsidiary ledger recording the status of all amounts due on lease transactions.

Debit with: Credit with:

Amount due on vehicle leases

Payments received

Comments: A subsidiary ledger should be set up for each lease. At month-end, all accounts should be reconciled. Collection efforts must be made to receive any outstanding amounts.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-15

120 Warranty Claims

Classification: Assets

Purpose: The balance of this account represents the amount due from Honda Canada Inc. for warranty service performed by the dealership at the agreed rates and on the conditions set out in the warranty procedure manual.

Debit with: Credit with:

The amount allowed by Honda Canada Inc. for warranty work performed on customer vehicles still under the manufacturer’s warranty

The amount received as credit or cash in payment of Warranty Claims

Comments: Each claim should be recorded in the Warranty Claims Register.

A month-end schedule should be prepared on a Monthly Analysis Sheet showing the amount of each unpaid claim. Any difference between the total of this schedule and the account balance should be reconciled and adjusted through Account 05, Policy Inspection or Account 37, Policy Adjustments - Parts & Services. If there is an error in billing, then consideration should be made to adjusting the applicable warranty sales account.

Claims which are denied payment in its entirety should be investigated to determine the reason of ineligibility for payment. After determination is made that the claim cannot be paid, it should be written off by debiting Account 37, Policy Adjustments - Parts & Services.

Past due amounts must be shown in the designated place on the Financial Statement.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-16

121 Marketing Allowance Receivable

Classification: Assets

Purpose: As a matter of policy, Honda Canada Inc. (HCI) will return a portion of each new vehicle invoice amount to assist the dealers to sell new vehicles. This amount is called the Marketing Allowance or Marketing Support and HCI reserves the right to adjust the amount from time to time. The balance represents the amount of Marketing Allowance due to the dealership as a result of new vehicles purchased from HCI.

Debit with: Credit with:

The amount of Marketing Allowance or Marketing Support receivable on each new vehicle purchased

The amount of payment received from HCI for Marketing Allowance or Marketing Support

Example 1: Record the purchase of a new vehicle directly from HCI, which has an invoice of $20,000 (including freight, air tax, advertising and Dealer Council), a Marketing Allowance of $300, Wholesale Assistance of $35 and a G.S.T. charge of $1,400.

Journal: New Vehicle Purchase Journal

Account Account Description Debit Credit

121 Marketing Allowance Receivable $300

230 Deferred Marketing Allowance $300

117 Accounts Receivable - Factory (Wholesale Assistance)

$35

1254 Floor Plan Interest $35

130 New Vehicles (Inventory) $20,000

219A Goods and Services Tax (Input Credit)

$1,400

205 Loans on New Vehicles (Floor plan)

$21,400

Example 2: Record the sale of the new vehicle above for $21,000, the G.S.T. is $1,470, the Provincial Sales Tax is $1,680, and the Vehicle License is $100. There is no trade and the customer has previously paid $6,000 as a cash down payment and finances $18,150. The Finance reserve is $350.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-17

Journal: New Vehicle Purchase Journal

Account Account Description Debit Credit

304 New Vehicle (Sales) $21,000

404 New Vehicle (Cost of Sales) $20,000

130 New Vehicles (Inventory) $20,000

1238 Advertising (New Vehicles) $150

404 New Vehicle (Cost of Sales) $150

230 Deferred Marketing Allowance (reversal of Marketing Allowance credit)

$300

90 Marketing Allowance on New Vehicles Sold

$300

219B Goods and Services Tax (Payable)

$1,470

220 Provincial Sales Tax $1,680

109 Cash Sales Clearing $100

110 Vehicle Licenses Clearing $100

222 Customer Deposits $6,000

107 Finance Contracts in Transit $18,150

701 Contract Reserves-New $350

123 Finance and Insurance Commissions (Receivable)

$350

Comments: This account is established to record the Marketing Allowance or Marketing Support only.

As each new vehicle is received from H.C.I. and placed into the dealership's inventory, the Marketing Allowance amount is debited to Account 121, Marketing Allowance Receivable

(Note: The Advertising charges are debited to Account 1238, Advertising, at the time the vehicle is sold).

When the Marketing Allowance "payment" is received (via credit to the Parts statement) from HCI, the amount is credited to Account 121, Marketing Allowance Receivable (to relieve the account), Account 219B, Goods and Services Tax (payable), is credited and the sum debited to Account 218, Factory Payable.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-18

122 Goods and Services Tax Receivable

Classification: Assets

Purpose: The balance represents the Goods and Services Tax refunds owed to the dealership for any month in which the Input Tax Credits exceed the liability.

Debit with: Credit with:

The amount of G.S.T. to be recovered from a prior month

The amount of G.S.T. refunds received

Example 1: When reviewing the month-end trial balance, it is determined that a debit balance of $4,000 exists (G.S.T. due to the dealership as a refund). Record the G.S.T. Receivable which is transferred from Account 219A, Goods and Services Tax (Input Tax Credit), where the balance is $225,000 and Account 219B, Goods and Services Tax (Payable) with a balance of $221,000.

Journal: General Journal

Account Account Description Debit Credit

122 G.S.T. Receivable $4,000

219B Goods and Services Tax (Payable)

$221,000

219A Goods and Services Tax (Input Tax Credit)

$225,000

Note: This entry should be processed prior to preparing the monthly financial statement.

Example 2: Record the receipt of the G.S.T. refund cheque of $4,000.

Journal: Cash Receipts Journal

Account Account Description Debit Credit

122 G.S.T. Receivable $4,000

104 Bank Accounts $4,000

Comments: In most cases, the amount of G.S.T. payable (see Account 219B, Goods and Services Tax (Payable)) will be more than the G.S.T. (Input Tax Credit). However, if a refund is due to the dealership, the amount of the refund is credited to Account 219A, Goods and Services

Acura Dealer Standard Accounting Manual

Revised January 2018 A-19

Tax (Input Tax Credit) and debited to Account 122, G.S.T. Receivable.

As G.S.T. refunds are received and reconciled at the dealership, the amount of the refund cheque is credited to Account 122, G.S.T. Receivable (to relieve the account) and debited to Account 104, Bank Accounts as the deposit is made.

Any interest received on the G.S.T. refund is recorded in Account 802, Interest Earned.

A properly completed G.S.T. Return must be prepared and filed before the deadline in order to avoid penalties and interest.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-20

123 Finance and Insurance Commissions

Classification: Assets

Purpose: The balance of this account represents the outstanding amounts of funds owed to the dealership by financial institutions and insurance companies. This is a control account and supporting details should be contained in a subsidiary ledger recording the amount of all F&I Commissions receivable.

Debit with: Credit with:

The amount of commissions due

The amount of payments received

Comments: Each bank and insurance company should be recorded in a subsidiary ledger. A review of outstanding amounts due to the dealership should be conducted at month-end and reconciled. All over and underpayments should be followed up on a timely basis. If a pattern of discrepancies emerges, steps need to be taken to ensure that proper F & I receivables are setup when processing the transaction. Caution needs to be exercised when short payments are received. Collection efforts must be initiated regarding any amounts that have not been paid.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-21

125 Allowance for Doubtful Accounts

Classification: Assets

Purpose: The balance of this account reflects a reserve for potential losses incurred due to the possible non collection of customers' accounts. Even though this account is classified as an Asset, it is a contra account (i.e. credit balance).

Debit with: Credit with:

The amounts recovered for receivables previously allowed for as uncollectible

The amount of monthly adjustment to decrease the balance of the account

The amount of all receivables classified as Bad Debts and for which a provision should be set up

The amount of the monthly adjustment to increase the balance of the account

Comments: Professional tax and accounting advice should be obtained regarding the proper handling of Bad Debts and the subsequent write off. When Bad Debts are written off, they should be removed from the subsidiary ledger and retained in a Bad Debts file. Even after an account has been written off, collection efforts should continue.

As Bad Debts are provided for, the amount is credited to this account. The offsetting debit is posted to Account 854, Bad Debt Expense.

This account should be reconciled with the Accounts Receivable subsidiary ledgers.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-22

130 New Vehicles

Classification: Assets

Purpose: This account reflects the value of New Vehicles on hand including the invoice cost (including advertising association and SYST / MKTG Support fees) and cost of dealer-installed equipment. Each vehicle's particular record should be carried in the inventory (Washout) Record.

Debit with: Credit with:

The inventory cost of New Vehicles received directly from Honda Canada Inc. (HCI)

The price of a New Vehicle received as a trade from another Acura dealer

The cost of parts and labour for accessories installed on the vehicles

The inventory value of New Vehicles sold to end users or traded to another Acura dealer

The inventory value of New Vehicles transferred to demonstrator service, lease or rental vehicle inventory, driver training inventory, company vehicle service, or courtesy vehicle service

The cost of accessories removed from New Vehicles while still in inventory

Recommended Procedure

Example 1: Record the purchase of a new vehicle directly from HCI, which has an invoice of $20,000 (including freight, air tax, advertising and Dealer Council), a Marketing Allowance of $300, Wholesale Assistance of $35 and a G.S.T. charge of $1,400.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-23

Journal: New Vehicle Purchase Journal

Account Account Description Debit Credit

121 Marketing Allowance Receivable $300

230 Deferred Marketing Allowance $300

117 Accounts Receivable - Factory (Wholesale Assistance)

$35

1254 Floor Plan Interest $35

130 New Vehicles (Inventory) $20,000

219A Goods and Services Tax (Input Credit)

$1,400

205 Loans on New Vehicles (Floor plan)

$21,400

Example 2: Record the sale of the new vehicle above for $21,000, the G.S.T. is $1,470, the Provincial Sales Tax is $1,680, and the Vehicle License is $100. There is no trade and the customer has previously paid $6,000 as a cash down payment and finances $18,150. The Finance reserve is $350.

Journal: New Vehicle Purchase Journal

Account Account Description Debit Credit

304 New Vehicle (Sales) $21,000

404 New Vehicle (Cost of Sales) $20,000

130 New Vehicles (Inventory) $20,000

1238 Advertising (New Vehicles) $150

404 New Vehicle (Cost of Sales) $150

230 Deferred Marketing Allowance (reversal of Marketing Allowance credit)

$300

90 Marketing Allowance on New Vehicles Sold

$300

219B Goods and Services Tax (Payable)

$1,470

220 Provincial Sales Tax $1,680

109 Cash Sales Clearing $100

110 Vehicle Licenses Clearing $100

222 Customer Deposits $6,000

107 Finance Contracts in Transit $18,150

701 Contract Reserves-New $350

123 Finance and Insurance Commissions (Receivable)

$350

Comments: New vehicle purchases should be posted to this account as soon as they are received.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-24

The amount of the Marketing Allowance should be identified and debited to Account 121, Marketing Allowance Receivable. The offsetting credit is posted to Account 230, Deferred Marketing Allowance.

When the vehicle is sold, the respective amount of the Marketing Allowance is debited - reversing the credit above and relieving the account. The offsetting credit is applied to Account 90, Marketing Allowance for New Vehicles Sold.

The amount of Advertising Association Fees should be kept with the inventory value of the vehicle until the vehicle is sold. At the time of sale, the Advertising Association fees should be identified and debited to Account 38, Advertising (New Vehicle Department). This preserves the "timing and matching" of the advertising expense with the sale of the vehicle and provides a better framework for analysing the performance of the New Vehicle Department.

Vehicles that are placed in demonstrator service, leased to customers, out in rental car service, loaned to driver training schools, or used as company vehicles should be removed from the New Vehicle inventory and posted to the proper account.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-25

136 Demonstrators

Classification: Assets

Purpose: The balance represents the cost of new Acura vehicles set aside for use as Demonstrators. This account reflects all Demonstrators transferred from the New Vehicle inventory accounts.

Debit with: Credit with:

The inventory value of the new vehicle placed in demonstrator service

Parts and labour for dealer installed accessories added to Demonstrators

The inventory value of Demonstrators removed from demonstrator service

The cost of “take off” equipment or accessories removed from a demonstrator while the vehicle is still in service (e.g. Ski rack)

Example 1: Record the transfer of a new vehicle placed in demonstrator service. The vehicle has an inventory value (formerly in Account 130, New Vehicles) of $20,000.

Journal: General Journal

Account Account Description Debit Credit

136 Demonstrators $20,000

130 New Vehicles (Inventory) $20,000

Example 2: Record the installation of an engine block heater on the demonstrator above. The Internal Parts sale is $125, with an inventory cost value of $100. The labour to install the block heater is $80 and the compensation paid to the technician is $20. The total transaction is $205.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-26

Journal: Internal Sales or Service Sales Journal

Account Account Description Debit Credit

136 Demonstrators (Inventory) $205

358 Parts Internal (Sales) $125

458 Parts Internal (Cost of Sales) $100

144 Parts & Accessories - Acura (Inventory)

$100

374 Labour - Internal, Service (Sales)

$80

474 Labour - Internal, Service (Cost of Sales)

$20

150 Labour in Process (Inventory) $20

Comments: When a new unit is placed in demonstrator service, a notation should be made on the Vehicle Inventory Record. Dealer installed accessories are debited to this account.

Demonstrators should be maintained according to the Honda Canada Inc. recommended service schedule. The cost of routine maintenance is expensed by debiting Account 41, Company Vehicles.

Note: Please consult your accounting and tax professional(s) regarding the applicable provincial or local usage taxes, which are assessed on Demonstrators in Inventory.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-27

138 Used Vehicles

Classification: Assets

Purpose: The balance of this account reflects the inventory value of all Used Vehicles purchased or accepted as trade-ins. The recommended inventory value is the Actual Cash Value (ACV) or "wholesale price."

Debit with: Credit with:

The purchase price of Used Vehicles acquired as trade-ins, at auctions, from wholesalers or purchased directly from an owner

The amount of reconditioning costs (including safety checks, emission tests, and dealer installed accessories) performed on Used Vehicles while in inventory

Expenses incurred to acquire a Used Vehicle including auction fees, buyer’s fees, travel & transportation expenses and other miscellaneous expenses

The inventory value of Used Vehicles when sold at retail or wholesale

The inventory value of Used Vehicles which are transferred to company vehicle service, scrapped, junked, or disposed of through normal business transactions

The amount of any month-end inventory adjustment (“write-down”)

Comments: An inventory schedule should be prepared at the end of each month and reconciled with a physical inventory. Discrepancies should be reconciled immediately. Each Used Vehicle should be aged and compared to current market value. Adjustments to the value should be credited to this account.

Acura Dealer Standard Accounting Manual

Revised January 2018 A-28

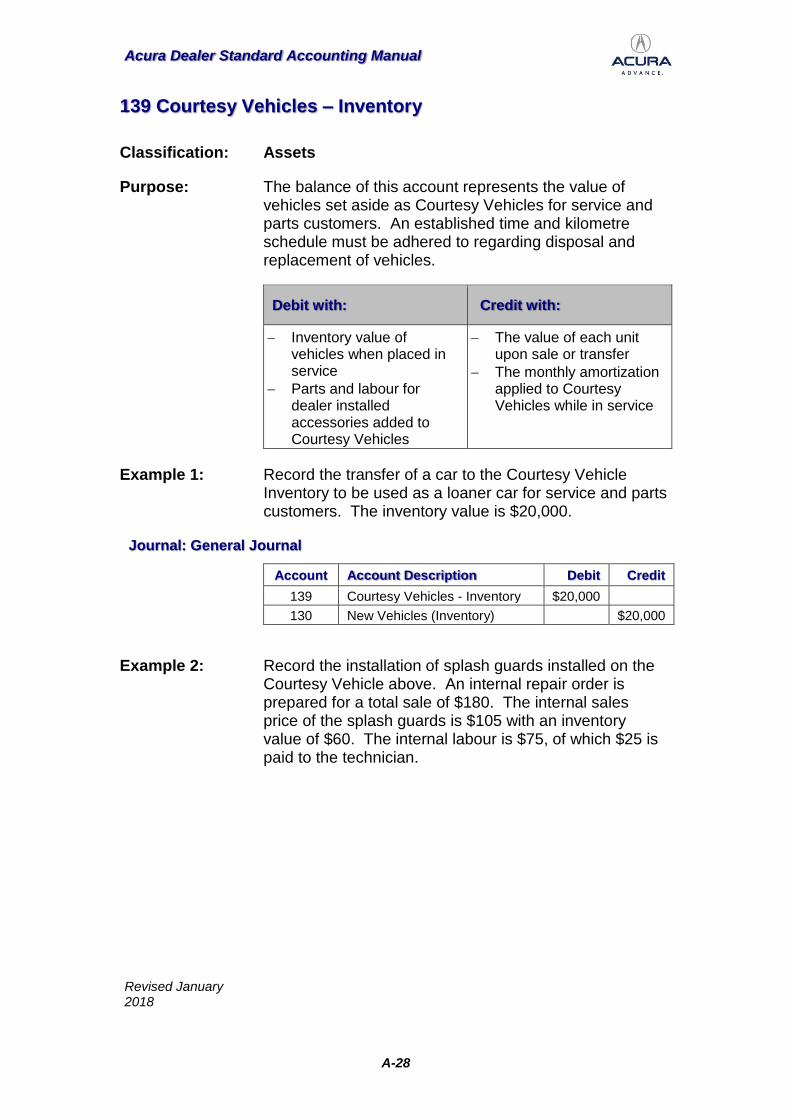

139 Courtesy Vehicles – Inventory

Classification: Assets

Purpose: The balance of this account represents the value of vehicles set aside as Courtesy Vehicles for service and parts customers. An established time and kilometre schedule must be adhered to regarding disposal and replacement of vehicles.

Debit with: Credit with:

Inventory value of vehicles when placed in service

Parts and labour for dealer installed accessories added to Courtesy Vehicles

The value of each unit upon sale or transfer

The monthly amortization applied to Courtesy Vehicles while in service

Example 1: Record the transfer of a car to the Courtesy Vehicle Inventory to be used as a loaner car for service and parts customers. The inventory value is $20,000.

Journal: General Journal

Account Account Description Debit Credit

139 Courtesy Vehicles - Inventory $20,000

130 New Vehicles (Inventory) $20,000