chapter 5: spanning the internet divide to drive … 5: spanning the internet divide to drive...

TRANSCRIPT

Chapter 5: Spanning the Internet divide to drive development (ITU)

Vanessa GRAYHead of LDCs, SIDS &

Emergency Telecommunications DivisionTelecommunication Development Bureau

International Telecommunication Union (ITU)

Aid for Trade workshop2017 Aid‐for‐trade monitoring and evaluation exercise

30 May, 2017, OECD, Paris

Committed to Connecting the World

0

10

20

30

40

50

60

70

80

90

100

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Per 1

00 inhabitants/ho

useh

olds

Active mobile‐broadband subscriptions Fixed‐broadband subscriptionsFixed‐telephone subscriptions Households with a computerHouseholds with Internet access Individuals using the InternetMobile‐cellular telephone subscriptions

Note: * ITU estimates.Source: ITU .

A decade of strong growth in ICTs

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

Fixed‐telephonesubscriptions

Mobile‐cellularsubscriptions

Fixed‐broadbandsubscriptions

Mobile‐broadbandsubscriptions

Households with acomputer

Households withInternet access

Individuals usingthe Internet

Per 1

00 inhabitants/ho

useh

olds

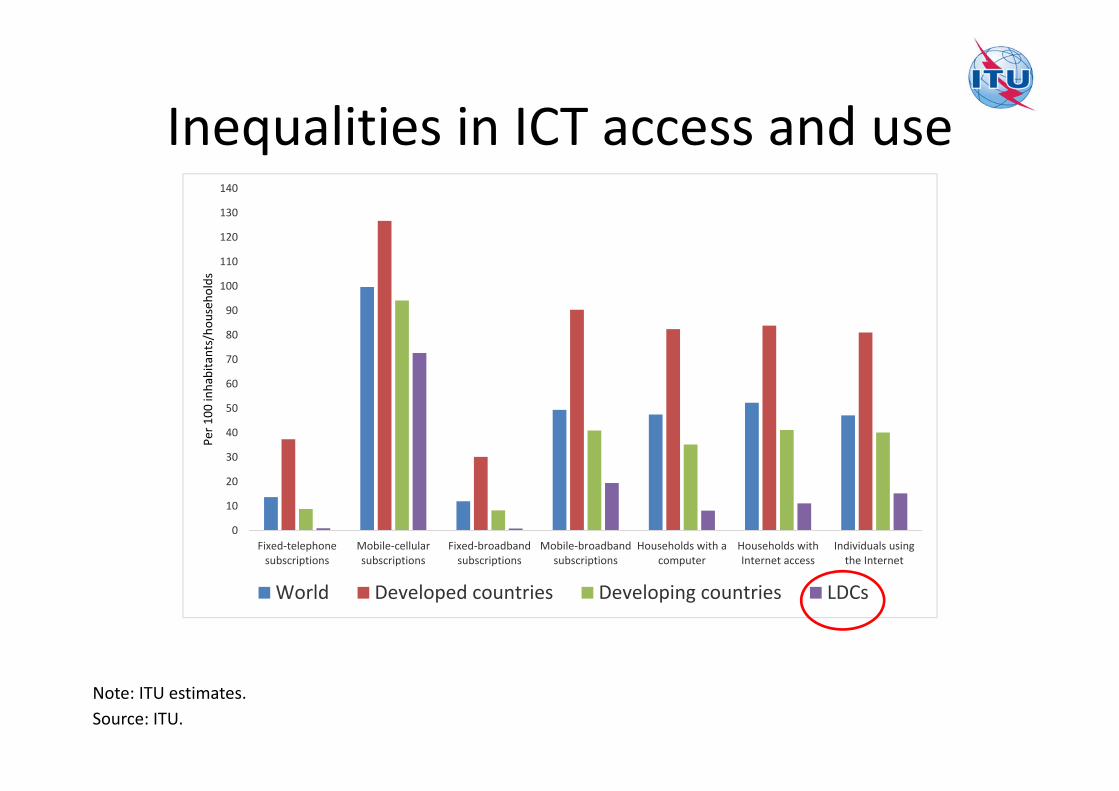

World Developed countries Developing countries LDCs

Note: ITU estimates.Source: ITU.

Inequalities in ICT access and use

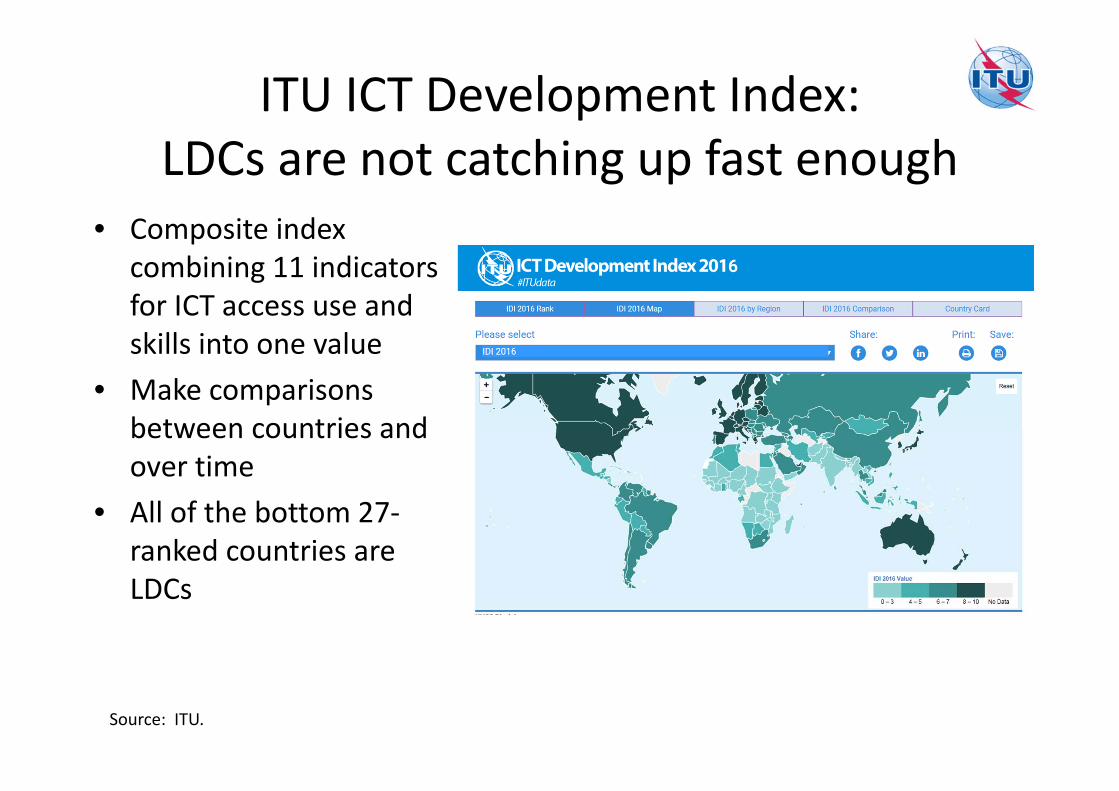

ITU ICT Development Index: LDCs are not catching up fast enough

• Composite index combining 11 indicators for ICT access use and skills into one value

• Make comparisons between countries and over time

• All of the bottom 27‐ranked countries are LDCs

Source: ITU.

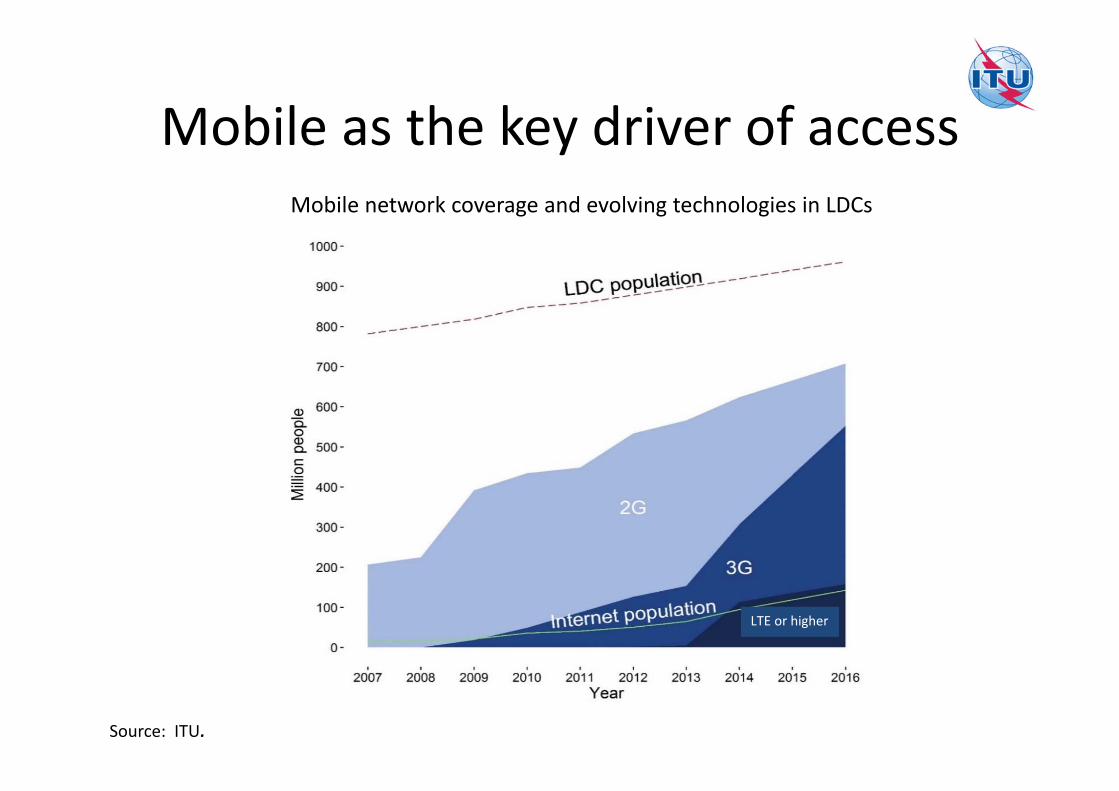

Mobile as the key driver of accessMobile network coverage and evolving technologies in LDCs

Source: ITU.

LTE or higher

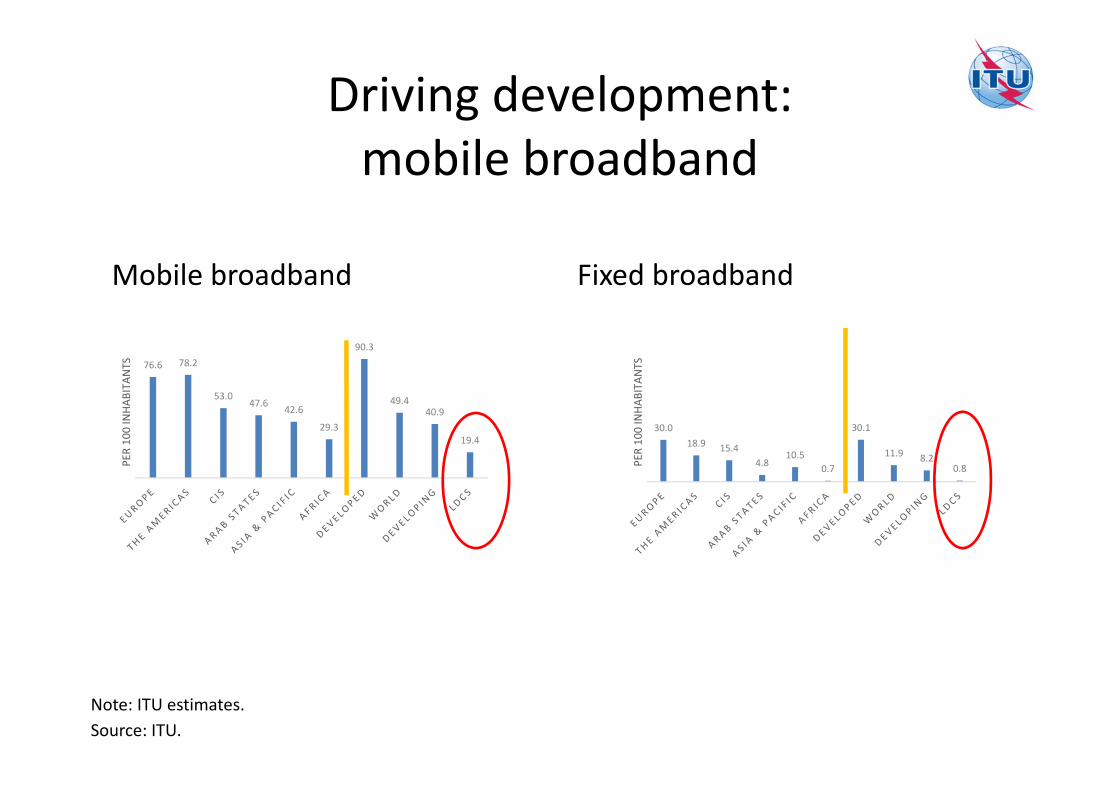

Driving development: mobile broadband

Mobile broadband Fixed broadband

30.018.9 15.4

4.810.5

0.7

30.1

11.9 8.20.8PE

R 100 INHA

BITA

NTS76.6 78.2

53.047.6 42.6

29.3

90.3

49.440.9

19.4

PER 100 INHA

BITA

NTS

Note: ITU estimates.Source: ITU.

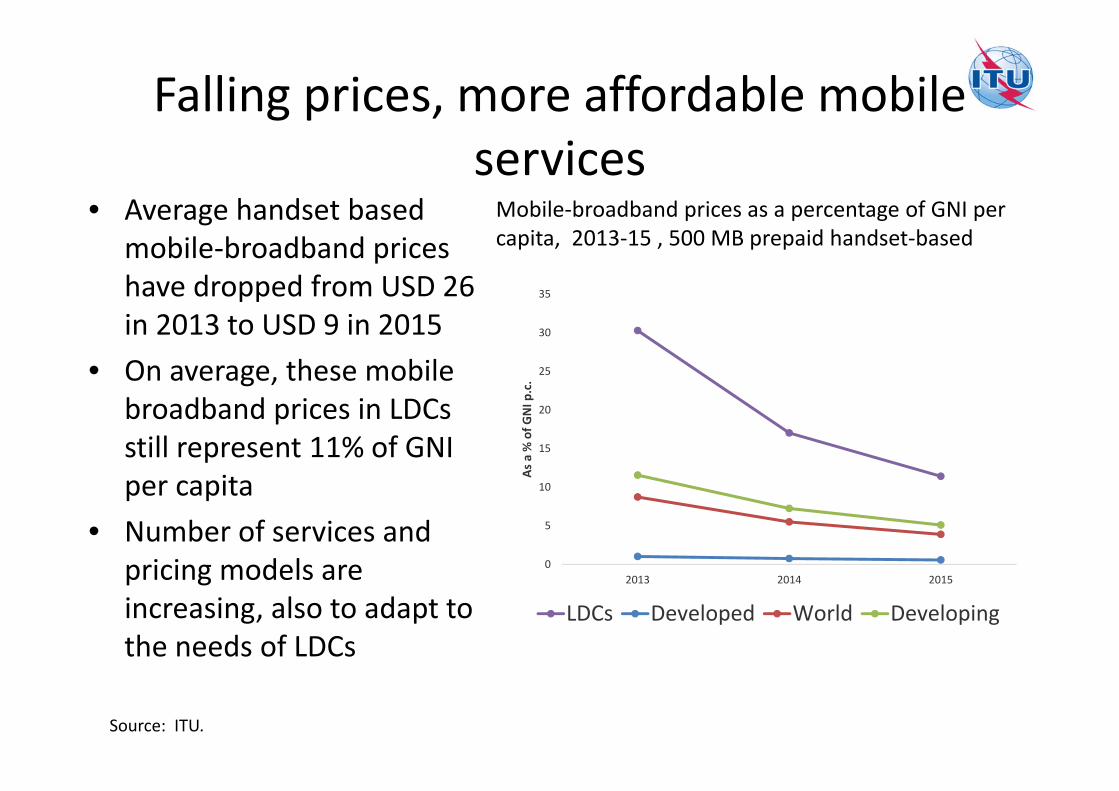

Falling prices, more affordable mobile services

• Average handset based mobile‐broadband prices have dropped from USD 26 in 2013 to USD 9 in 2015

• On average, these mobile broadband prices in LDCs still represent 11% of GNI per capita

• Number of services and pricing models are increasing, also to adapt to the needs of LDCs

0

5

10

15

20

25

30

35

2013 2014 2015

As a % of G

NI p

.c.

LDCs Developed World Developing

Mobile‐broadband prices as a percentage of GNI per capita, 2013‐15 , 500 MB prepaid handset‐based

Source: ITU.

Fixed versus mobile networks

• Mobile‐broadband remains inferior in terms of speed, latency, and capacity

• IMT‐2020 (5G) networks promise to address some of the challenges but backbone infrastructure is critical

• Key policy implications:– Governments must foster investments in the latest generation of mobile networks

– Countries must invest in fixed‐broadband infrastructure: national backbones and international connectivity

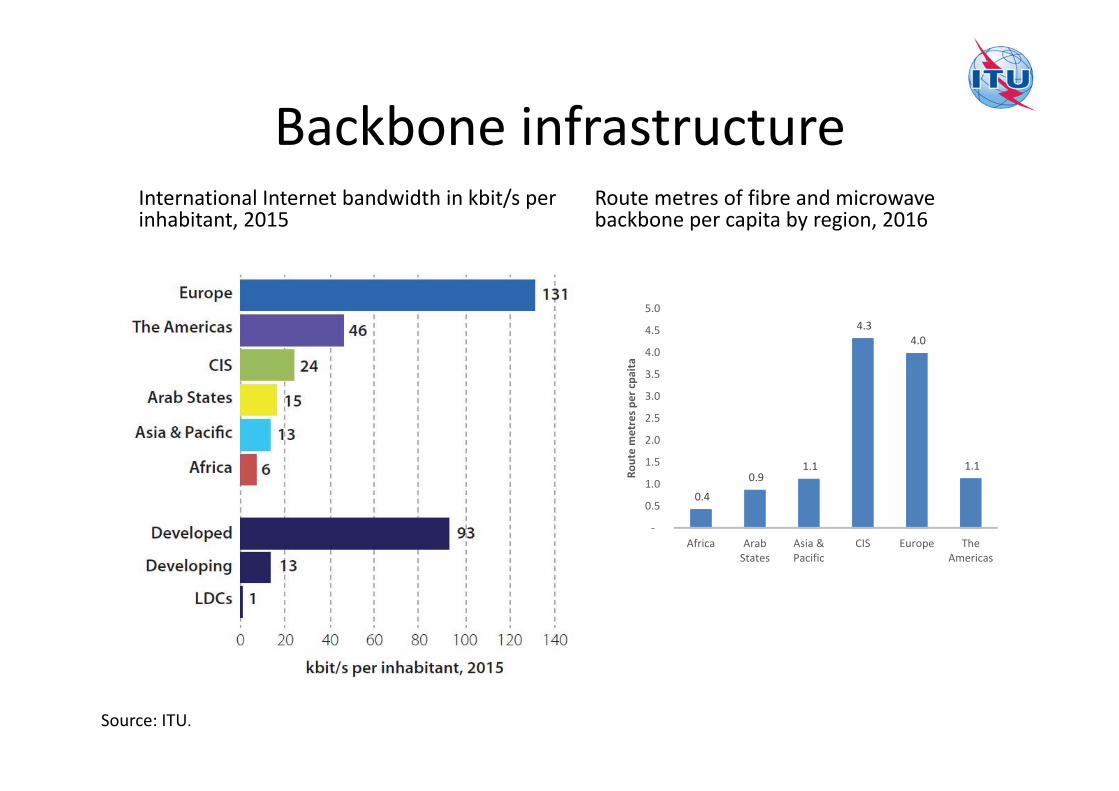

Backbone infrastructureInternational Internet bandwidth in kbit/s per inhabitant, 2015

Source: ITU.

0.4

0.9 1.1

4.3 4.0

1.1

‐

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Africa ArabStates

Asia &Pacific

CIS Europe TheAmericas

Route metres p

er cpa

ita

Route metres of fibre and microwave backbone per capita by region, 2016

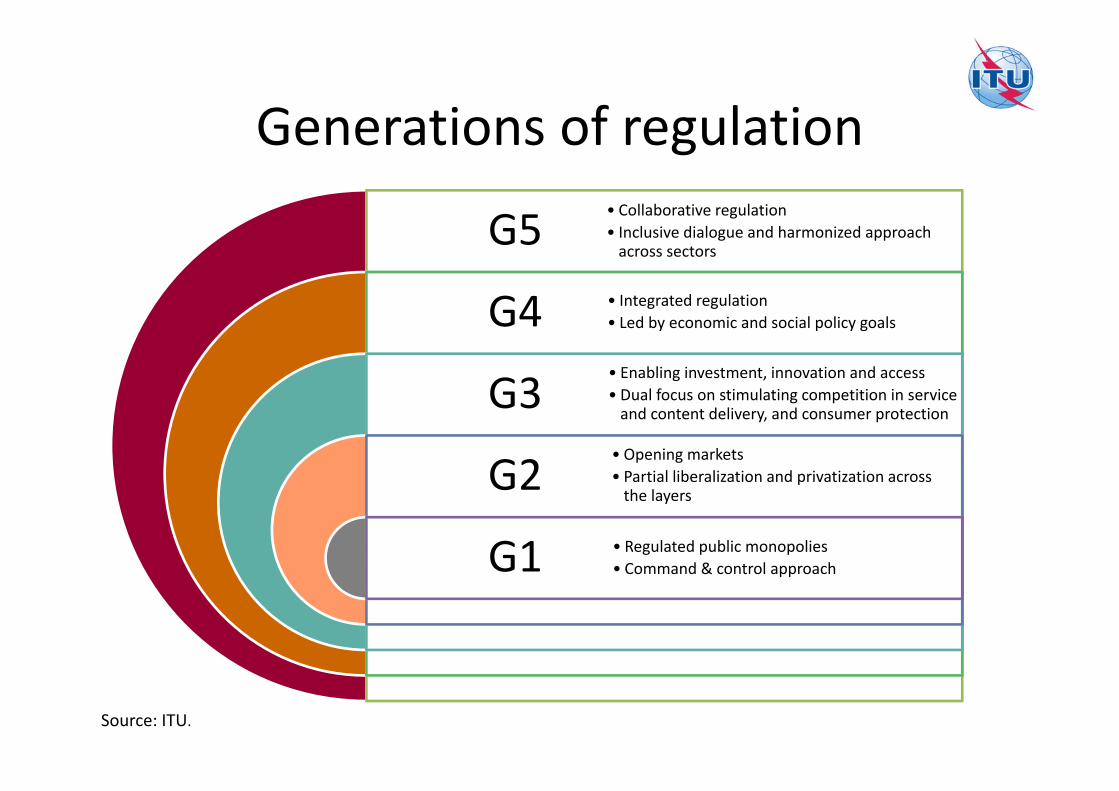

G5

G4

G3

G2

G1

•Collaborative regulation• Inclusive dialogue and harmonized approach across sectors

• Integrated regulation• Led by economic and social policy goals

• Enabling investment, innovation and access • Dual focus on stimulating competition in service and content delivery, and consumer protection

• Opening markets• Partial liberalization and privatization across the layers

• Regulated public monopolies• Command & control approach

Generations of regulation

Source: ITU.

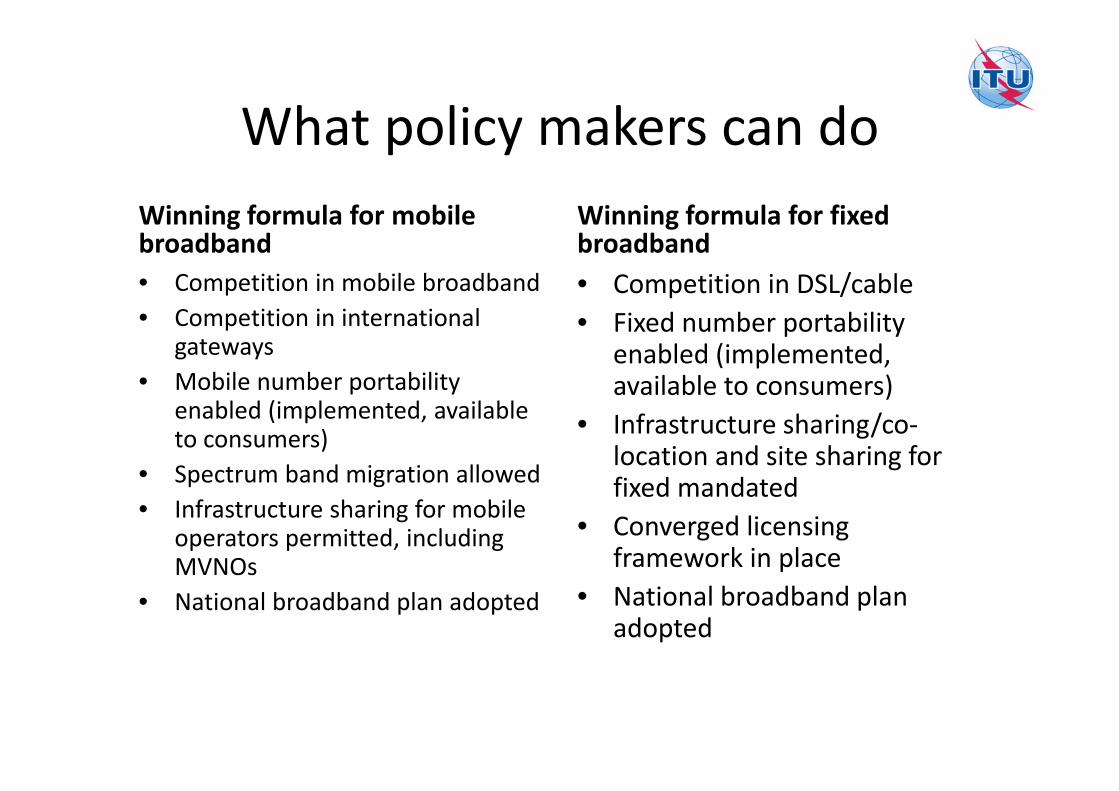

Adressing connectivity bottlenecks• Develop National ICT/Broadband Plans, set targets and track and monitor implementation

• Liberalization, privatization and inter and intra platform competition

• Creating an enabling environment, removing entry barriers, allow foreign ownership and investment

• When private investment is not sufficient– Direct government investment – Public private partnerships (PPPs) – Use of universal service funds and obligations– State aid, tax incentives

What policy makers can doWinning formula for mobile broadband• Competition in mobile broadband• Competition in international

gateways• Mobile number portability

enabled (implemented, available to consumers)

• Spectrum band migration allowed• Infrastructure sharing for mobile

operators permitted, including MVNOs

• National broadband plan adopted

Winning formula for fixed broadband• Competition in DSL/cable• Fixed number portability

enabled (implemented, available to consumers)

• Infrastructure sharing/co‐location and site sharing for fixed mandated

• Converged licensing framework in place

• National broadband plan adopted

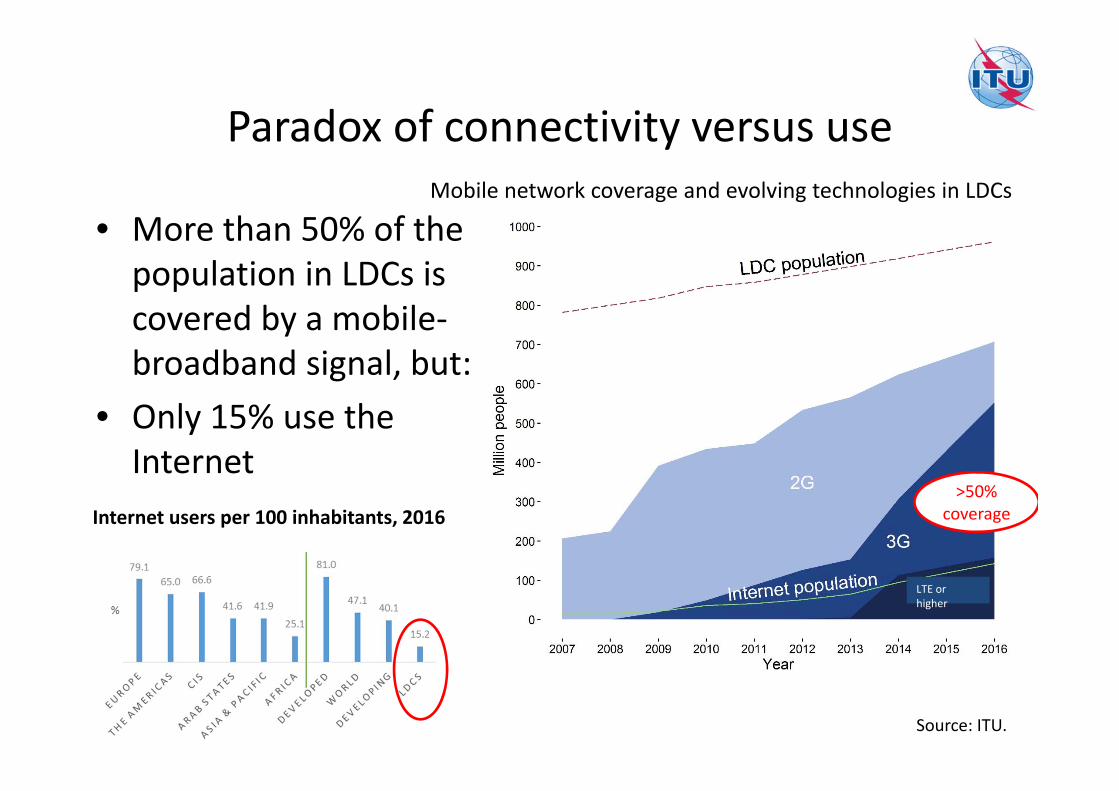

Paradox of connectivity versus use

• More than 50% of the population in LDCs is covered by a mobile‐broadband signal, but:

• Only 15% use the Internet

Source: ITU.

Mobile network coverage and evolving technologies in LDCs

LTE or higher

Internet users per 100 inhabitants, 2016>50%

coverage

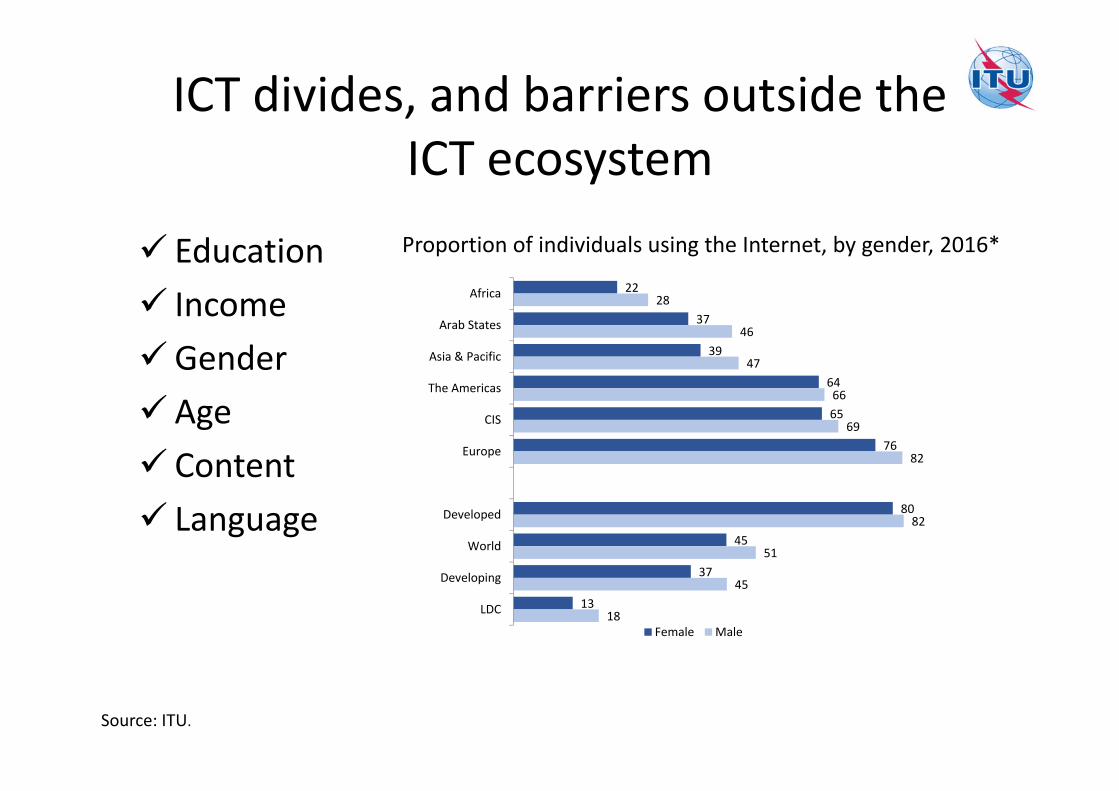

ICT divides, and barriers outside the ICT ecosystem

Education IncomeGender Age Content Language

22

37

39

64

65

76

80

45

37

13

28

46

47

66

69

82

82

51

45

18

Africa

Arab States

Asia & Pacific

The Americas

CIS

Europe

Developed

World

Developing

LDC

Female Male

Proportion of individuals using the Internet, by gender, 2016*

Source: ITU.

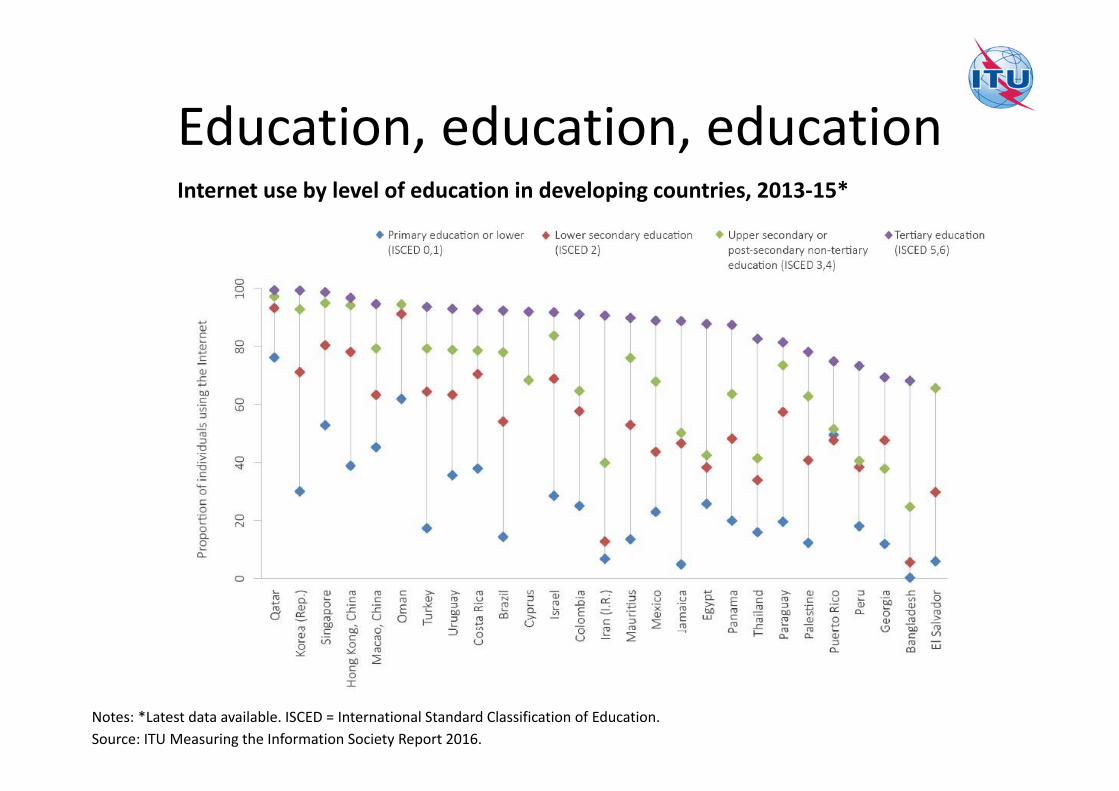

Education, education, education

Notes: *Latest data available. ISCED = International Standard Classification of Education.Source: ITU Measuring the Information Society Report 2016.

Internet use by level of education in developing countries, 2013‐15*

Highlights

• Growth in ICT infrastructure, connectivity, access and use promise great development opportunities

• ICTs are key building blocks of the digital economy, to facilitate trade and drive e‐commerce

• Internet divide remains a key barrier to the global information society, particularly for LDCs

• Governments have an important role to play in creating an enabling environment, to make ICTs affordable, and to address key barriers

• Broader socio‐economic barriers and inequalities outside the ICT ecosystem also need to be addressed