running musharakah - riphah international...

TRANSCRIPT

Running Musharakah

Ahmed Ali Siddiqui

Director, IBA CEIF

&

Exec. Vice President & Head,

Product Development & Shariah Compliance, Meezan Bank

• Introduction

• Key Features

• Portfolio at Meezan Bank Limited

• Running Musharakah Facility Limit

• Musharakah Total Investment

o Adjusted Cost of Goods

o Calculation of Musharakah Total Investment

• Bank’s Investment in Musharakah

• Customer’s investment in Musharakah

• Musharakah Profit Sharing Mechanism

• Loss Sharing and Termination of Musharakah

• Risk Mitigation in Running Musharakah

Presentation Outline

The Bank and the Customer will enter into Musharakah, based on Shirkat-ul-

Aqd

The Bank and the Customer will invest in the identified primary Operating

Activities (or any identifiable segment thereof) of the Customer’s business

Running Musharakah will be used to finance Customer’s Operating Activities

only.

Bank and customer will participate in the profits/(loss) generated by the

Musharakah in proportion to their respective Profit sharing Ratios.

Introduction

Offers a Shariah Compliant alternative to Running Finance.

Minimal documentation required.

Running Musharakah enables the Customer to draw and deposit funds

against a Running Musharakah finance limit offered by MBL

The Running Musharakah facility may be offered for a period of one year, or

any agreed term, starting from the day the facility is sanctioned.

Payment by the client is done provisionally at the end of each Musharakah

Period which is subject to final settlement.

Key Features

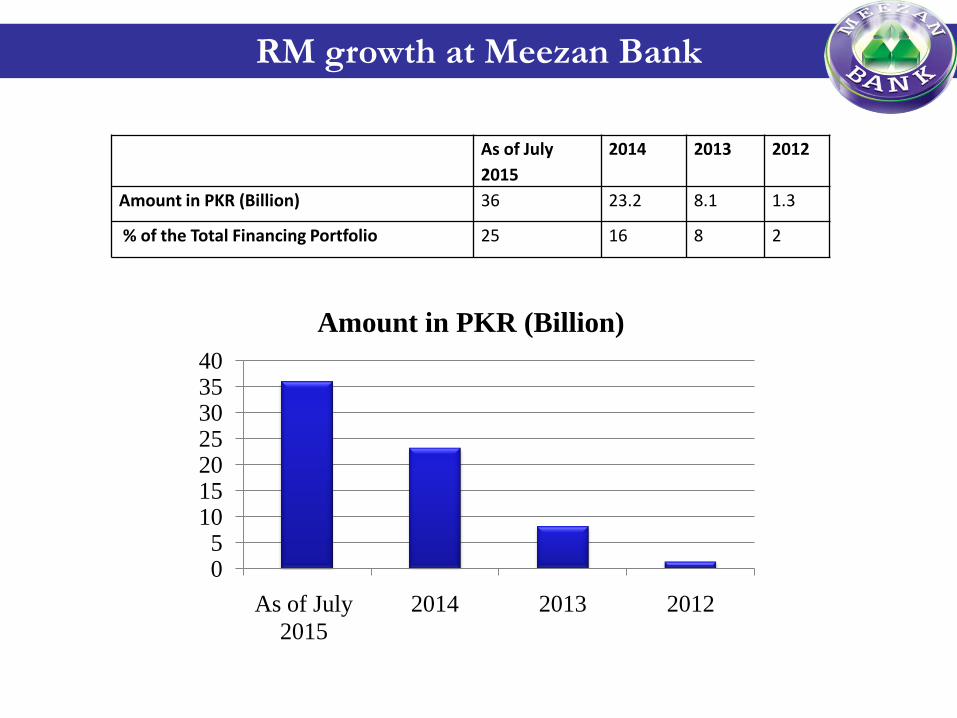

As of July

2015

2014 2013 2012

Amount in PKR (Billion) 36 23.2 8.1 1.3

% of the Total Financing Portfolio 25 16 8 2

05

10152025303540

As of July

2015

2014 2013 2012

Amount in PKR (Billion)

RM growth at Meezan Bank

Understanding the concept

• In order to calculate Total Investment a simple working example of Musharakah with

a retailer who purchases and sells the goods on the same day on cash is taken, thus

having nil inventory turnover and average collection periods.

DaysTotal Daily

Purchases

Bank

Investment

Balance

Customer

InvestmentTotal Sales Profit

(A) (B) (C=A-B) (D) (E=D-A)

1 100 50 50 115 15

2 100 70 30 115 15

3 200 40 160 230 30

4 200 60 140 230 30

5 150 30 120 173 23

6 200 60 140 230 30

Total 950 1,093 143

Average 158 52 107

Total Investment

Since investment period in Musharakah would not be limited to the

purchase/production and sale of goods on cash the same day,

therefore the results of the following formulae will be used to arrive at

Musharakah Total Average Investment:

Adjusted COGS multiplied by Inventory Turnover in Days and

divided by Musharakah tenor.

+

Adjusted COGS multiplied by Average Collection Period in Days and

divided by Musharakah tenor.

=

Musharakah Total Average Investment

• The Inventory & Accounts Receivable will be based on average of the

preceding three quarterly financial statement immediately preceding

Musharakah Tenor, normalized for extraordinary changes (if any) in

customer business model.

Total Investment

Days COGS FG Acc Rec Customer Bank

1 3,000 3,000 2,000 1,000

2 3,000 2,000 1,000

3 3,000 2,000 1,000

4 3,000 2,000 1,000

5 3,000 2,000 1,000

6 3,000 2,000 1,000

7 3,000 2,000 1,000

8 3,000 2,000 1,000

9 3,000 2,000 1,000

10 3,000 2,000 1,000

11 3,000 2,000 1,000

12 3,000 2,000 1,000

13 3,000 2,500 500

14 3,000 2,500 500

15 3,000 2,500 500

16 3,000 2,500 500

17 3,000 2,500 500

18 3,000 2,500 500

19 3,000 2,500 500

20 3,000 2,500 500

21 3,000 2,500 500

22

23

24

25

26

27

28

29

30

Total 3,000 46,500 16,500

Avg 100 1,550 550

Inventory Turnover 10

11

COGS*Inve Turnover /No of Days 1,000

COGS*Ac. Rec Turnover/No of Days 1,100

Musharakah Investment 2,100

1,550Customer Investment

Ac. Rec Turnover

Adjusted Cost of Goods Sold

• COGS is an income statement item, it relates to the whole period of

the business and gives a more accurate picture compared to the

Current Asset figures, which are balance sheet items and portray only

the end of period information.

• Normally COGS is calculated as follows:

Opening Stock + (Direct Labor + Direct Raw Material + Direct

Overheads) – Closing Stock

• For the purpose of Musharakah the COGS will have to be adjusted to

exclude expenses such as Repair & maintenance, Stores & Spares,

Plant Depreciation, Plant Insurance, etc from Direct Overheads,

which are not related to the activities of the Musharakah.

Running Musharakah Facility Limit

• The Facility Limit can be calculated as % of the average value of

Stock-in-Trade and Trade Receivables appearing in the preceding four

financial years statement of the company. E.g. Calculation of Facility

Limit for ABC Cement for the year 2016.

“000”

2013 2014 2015 TOTAL

Avg of Stock in Trade 144,026 273,594.5 553,837 323,819

Avg of Trade Recievables 19,582 60,598.5 287,528 107,940

431,759BANK'S MAXIMUM LIMIT

(at 70%) 302,231

Profit & Loss Sharing

• The Profit Sharing Ratio between the Bank and the Customer will be

in proportion to their respective Investment ratios in the Running

Musharakah up to an agreed profit Ceiling

• Profit amount over the Profit Ceiling can be mutually agreed to a

lower amount like 2% for bank and 98% for customer

• The Running Musharakah Loss will be shared between the Bank and the

Customer in proportion to their respective Investment ratio

Running Musharakah Step by Step

Step 1: The Bank and the Customer will enter into Musharakah for the operating

activities of the business; which will be the Gross Profit level of thecustomer’s business. Activities limited to production and sales

For this the Bank and the Customer will agree on the items which are to beincluded in the Adjusted Cost of Goods sold for the purpose ofMusharakah.

Adjustments for various Direct and Indirect expense components need to bedetermined.

The COGS would have to be adjusted to exclude expenses such as Rents, Rates & Taxes Insurance Travel & Conveyance Repair & Maintenance Depreciation Etc.

Running Musharakah

Cost of Sales "000" Audited Accounts For Musharaka

Raw material consumed 15,518,409 15,518,409

Packaging material 470,472 470,472

Fuel and power 1,990,504 1,990,504

Chemicals & Supplies 158,370 158,370

Salaries, wages and benefits 1,074,527 1,074,527

Rent Rates & Taxes 28,359 -

Insurance(Split b/w stocks & plant) 69,671 -

Travel and conveyance 55,145 -

Repair and maintenance 979,294 -

Depreciation 1,212,073 -

Provision for inventory obsolence 56,263 -

Opening Stock - work in progress 3,602 3,602

closing stock - work in progress (5,140) (5,140)

subsidiary on DAP fertilizer from GoP 0

Cost of Goods manufactured 21,611,549 19,210,744

Opening Stock - own manufactured fertilizer 5,583,460 5,583,460

Less: closing stock - own manufactured fertilizer (170,926) (170,926)

Cost of Sales '000' 27,024,083 24,623,278

Adjusted Cost of SalesABC Limited

Running Musharakah

Step 2: The Bank and the Customer will then agree on the items of the Musharakah

Income.

Adjusted Cost of Goods Sold will be deducted from Net Sales, which will

then be adjusted for other Direct Expenses related to the operating business.

For Musharaka

Net Sales xxxxxxxx

Adjusted Cost of Sales '000' xxxxxxxx

Gross Profit xxxxxxxx

Freight xxxxxxxx

Musharakah Profit xxxxxxxx

Running Musharakah Income Statement

Running Musharakah

Step 3: The Bank and the Customer sign the Musharakah Agreement.

The Customer starts using the facility.

Running Musharakah product will enable the Customer to draw and depositfunds against a Running Musharakah finance limit offered by MBL.

Amount drawn by the Customer will be Bank’s investment in Customer’sbusiness or Musharakah.

Hence Bank’s investment in this business will vary from time to time subject

to a maximum Running Musharakah Facility Limit (“facility Limit).

Running Musharakah

Step 4 (At the end of the Musharakah Tenor):

Bank’s Running Musharakah Investment will be calculated.

This will be equivalent to the average balance of the Running Musharakah

Account maintained in the name of the Customer calculated on daily product

basis over the Musharakah Facility Tenor.

Suppose a Customer has a limit of Rs1,568,656/= for the purpose of this

example we assume that the Customer availed this limit fully on each day of

the year and hence Bank’s Musharakah Investment for the quarter based on

Daily Product basis is Rs1,568,656/=.

Running Musharakah

Step 5 (Calculation of Total Musharakah Investment):

The total Musharakah Investment will be calculated based on the actual

quarterly accounts of the Customer.

Adjusted Cost of Goods Sold (ACOGS) of the Musharakah Period would

be used to calculate Total Musharakah investment since it directly relates to

the operating activity of the business for which Musharakah is being done

and not to the whole enterprise of the business.

Since COGS is an income statement item, it relates to the whole period of

the business and gives a more accurate picture compared to the Current Asset

figures, which are balance sheet items and portray only the end of period

information.

Running Musharakah

Calculation of Total Musharakah Investment

Since investment period in Musharakah would not be limited to the

purchase/production and sale of goods on cash the same day, the

considerable time period during which investment remains tied up in

inventory and receivables would have to be accounted for.

Due to this fact the results of the following formulae would be used to

arrive at Musharkah’s Total Investment:

Musharkah’s Total Investment

=Adjusted COGS multiplied by Inventory Turnover in Days and divided by

Musharakah tenor

+

Adjusted COGS multiplied by Average Collection Period in Days and

divided by Musharakah tenor

Running Musharakah

Calculation of Total Musharakah Investment

Cost of Goods Sold (2015-16) 27,059,566

Net Sales (2015-16)36,724,920

Musharakah Tenor365

Starting Jul 01, 2015 – June 30, 2016

Adjusted COGS 24,715,024

Average Inventory (2012-15)2,073,058

Average of Trade Recievables (2012-

15) 309,301

Inventory Turnover in Days 27.96

Average Collection Period in Days 3.07

Musharaka Total Investment2,101,593

Running Musharakah

Step 6 (Calculation of Customer’s Musharakah Investment):

Subtracting Bank’s Musharakah Investment from Total Musharakah

Investment would give us Customer’s Musharakah Investment for the

Tenor:

Customer’s Musharakah Investment = 2,101,593 – 1,568,656

= Rs. 532,937/=

Running Musharakah

Step 7 (Calculation of Actual Musharakah Profit):

PKR as on 30/06/2016 ABC Limited

Audited Accounts For Musharaka

Net Sales 36,724,920 36,724,920

Cost of Sales '000' 27,059,566 24,715,024

Gross Profit 9,665,354 12,009,896

Freight

Musharakah Profit 12,009,896

Running Musharakah Profit

Running Musharakah

Step 8 (Distribution of Profit):

Calculation of Profit Ceiling = Desired Rate x Total MusharakahInvestment

Profit Ceiling = Desired Rate x Total Musharakah Investment= 14.40% x 2,101,593,336= 302,629,440

Running Musharakah Profit upto the Profit Ceiling will be shared between theBank and the Customer in the proportion to their respective Investment ratiosin the Running Musharakah.

Bank’s Profit Share =Bank’s Musharakah Investment/ Total Musharakah Investment x Profit CeilingAmount= (1,568,656,625 / 2,101,593,336) x 302,629,440= 225,886,122/=

Bank’s profit as a %age of Bank’s Musharakah Investment= 225,886,122 / 1,568,656,625.= 14.40% (Same as the required rate outlined earlier)

Running Musharakah

Distribution of Profit above Ceiling amount:

For profit above ceiling amount Bank generally keep a small ratio of profit. Thisis required to fulfill the Shariah requirements of Musharakah

Running Musharakah

Customer Name: ABC Limited

Running Musharaka Sub-Tenor: July 01, 2008 to June 30, 2009

Customer's Running Musharaka Finance Limit 1,568,653,625

Desired Profit Rate (% p.a.)

- Relevant KIBOR 13.40%

- Margin 1.00%

Profit Ceiling Rate (% p.a.) 14.40%

Number of Days in relevant Sub-Tenor 365

Total MBL Customer

Running Musharaka Investment for the relevant Sub-Tenor (PKR) 2,101,593,336 1,568,653,625 532,939,711

Investment & Profit/(Loss) Sharing Ratio

(for profit amount BELOW Profit Ceiling Amount)74.64% 25.36%

Sharing Ratio above ceiling amount 1.000% 99.000%

Actual Running Musharaka Profit 12,009,896,000

Running Musharaka Profit Ceiling 302,629,440

Running Musharaka Profit BELOW the Profit Ceiling Amount 302,629,440 225,886,122 76,743,318

Running Musharaka Profit ABOVE the Profit Ceiling Amount 11,707,266,560 117,072,666 11,590,193,894

Running Musharaka Profit Computation