the london stock exchange aim market - k&l gates london stock exchange aim market: securing...

TRANSCRIPT

The London Stock Exchange AIM Market: Securing Capital through an Initial Public Listing or Dual Listing

Breakfast Briefing and Web Cast October 4, 2007

Contents Tab Number

The London Stock Exchange AIM Market: Securing Capital through an Initial Public Listing or Dual Listing .............. 1

Presentation Slides Speaker and Company Profiles .................................................. 2 Introduction to AIM Guide to AIM AIM–NASDAQ Comparison ........................................................ 3

Speaker and Company Profiles Speakers:

Richard Webster-Smith, London Stock Exchange

Jeremy Landau and Alex Gibson, K&L Gates

Steve Smith, Ernst & Young UK

Nigel Daly, Piper Jaffray & Co.

Heather Salmond, Abchurch Communications

Alex Munro, London Bridge Capital

Series Host: Stephan Coonrod, K&L Gates

1

The London Stock Exchange AIM Market:

Securing Capital Through an Initial Public Listing or Dual Listing

Presentation Topics

AIM: Supporting the Growth of Small and Midcap CompaniesRichard Webster-Smith, London Stock Exchange

Introduction to AIM – the Legal ProcessJeremy Landau and Alex Gibson, K&L Gates

Key Accounting Issues for an AIM IPOSteve Smith, Ernst & Young UK

The Nomad's Point of View - Securing Capital and Who Should Look to List on AIMNigel Daly, Piper Jaffray London

How to Communicate an IPOHeather Salmond, Abchruch Communications

Preparing Companies Before the AIM Admission ProcessAlex Munro, London Bridge Capital

2

Supporting the growth

of small and midcap

companies

October 2007

UK Companies

Total companiesDomestic: 3,281International: 666

Market capitalisationMain Market:UK listed: US$3,794bnInternational listed: US$5,061bnAIM: US$208bn

Equity turnover (Jan-July 2007)Main Market:Domestic: US$5,586 bnInternational: US$6,840bnAIM: US$103bn

Source: London Stock Exchange statistics – August 2007

London Stock Exchange - key statistics

3

UK Companies

Total number of IPOs on the LSE, Nasdaq and NYSE 2000-2007

0

50

100

150

200

250

300

350

400

450

2000 2001 2002 2003 2004 2005 2006 2007

Lon Stock ExchangeNasdaqNYSE

The platform of choice for international companies

In 2006: • London Stock Exchange - 367 new companies joined in 2006. NYSE, Nasdaq & Hong Kong Stock Exchange had 332

IPOs in 2006.• $104bn were raised on the London Stock Exchange, $40bn on NYSE, and $29bn on Nasdaq

• First half of 2007 - $26bn were raised on the London Stock Exchange. NYSE and Nasdaq raised $21bn combined.

Source: London Stock Exchange and Exchanges website – August 2007

UK CompaniesThe widest choice of proven global markets

A choice of globally respected markets supported by a wide range of institutional & retail investors

Supports more established companies seeking further

growth.1,596 issuers

Supports earlier stage companies in their initial growth period.

1,685 issuers

Main Market

Sponsor

UK Listing AuthorityNominated Adviser (Nomad)

Source: London Stock Exchange statistics – August 2007

4

UK Companies

The world’s most successful growth market

UK Companies

• AIM companies: 1,685

• Overseas AIM companies: 329

• IPOs on AIM in 2006: 341• 232 UK • 109 overseas

• IPOs on AIM in 2007: 134

• Capital raised (new & further) since 1995: US$104bn

• Capital raised (new & further) in 2006: US$31bn• $US 21bn UK companies• $US 10bn overseas companies

Key Statistics

Source: London Stock Exchange trade statistics – August 2007

5

UK CompaniesAIM – critical mass to support growth

Source: London Stock Exchange trade statistics – August 2007

Number of admission 1995 to 2007

123145

107

75102

277

177160 162

355

519

462

201

0

100

200

300

400

500

600

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Num

ber

of a

dmis

sion

s

UK Companies

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007

Fund

s ra

ised

($b

n)

Further money raised ($bn)

Money raised at admission ($bn)

Raising new and further capital on AIM

More money was raised on AIM in 2006 ($31bn) as on NASDAQ ($29bn).

If AIM were an independent stock exchange it would be the sixth largest in the world (by money raised).

Source: London Stock Exchange trade statistics – August 2007

6

UK Companies

Flexible regulation

Admission Rules

• No minimum size to be admitted

• No minimum financial history required

• No minimum amount of shares to be in public hands

• In most cases, no prior shareholder approval required for transactions

• Admission documents not pre-vetted by Exchange or UKLA but by nominated adviser

• Nominated adviser (Nomad) required at all times

Appropriate regulation and oversight

UK Companies

Continuing obligations

AIM companies are subject to the AIM Rules which outline the continuing obligations ofbeing on a public market. Some of the key continuing obligations are:

• AIM companies must have a Nomad at all times, otherwise they will be suspended from the market

• AIM companies must disclose all price sensitive information in a timely manner including substantial transactions, related party transaction, reverse takeovers and other miscellaneous transactions

• Half yearly and annual report and accounts required in adherence with deadlines

• All directors accept full responsibility, collectively and individually for the AIM Rules

• Restrictions on deals for directors and applicable employees on AIM securities during close periods

• UK Corporate Governance standards

Appropriate regulation and oversight

7

UK CompaniesAIM: a market for companies of all sizes

Source: London Stock Exchange trade statistics – August 2007

Distribution of AIM Companies by Market Value August 2006 vs August 07

0

50

100

150

200

250

300

350

400

Less than$3.9m

$3.9m - $9.9m $9.9m -$19.8m

$19.8m -$49.5m

$49.5m -$99m

$99m - $198m $198m -$495m

$495m -$990m

$990m -$1980m

over £1980m

Market Value (US$)

No

of C

ompa

nies

No of companies August-06

No of companies August-07

UK CompaniesA diverse market

Source: London Stock Exchange trade statistics – August 2007

Top AIM sectors by market capitalisation and no. of companies Aug 07

-

5,000

10,000

15,000

20,000

25,000

30,000

Real Estate Mining SupportServices

GeneralFinancial

Oil & GasProducers

Softw are &ComputerServices

Media EquityInvestmentIntruments

Travel & Leisure

Pharmaceuticals& Biotechnology

Mkt

Val

ue (U

S$m

)

0

50

100

150

200

250

Num

ber o

f com

pani

es

Latest Market Value USD$Number of Companies

8

UK CompaniesUS companies - sectors

Sector distribution of US companies by number August 07

Other24%

Oil & Gas Producers12%

Electronic & Electrical Equipment

12%Software & Computer

Services11%

Pharmaceuticals & Biotechnology

9%

Support Services5%

General Financial5%

Health4%

Media4%

Speciality & Other Finance4%

Automobiles & Parts5%

Chemicals5%

UK CompaniesUS companies – size distribution

Distribution of US companies by market value August 07

0

2

4

6

8

10

12

14

16

18

20

22

Less than $9.9m

$9.9m - $19.8m

$19.8m - $49.5m

$49.5m -$99m

$99m - $198m

$198m - $495m

$495m - $990m

over $990m

Market Value (US $)

No.

of C

ompa

nies

9

UK CompaniesInstitutional investors understand AIM

All of the main UK institutions invest in AIM.

151413

12111098

7654321

Rank

692.1778RAB Capital719.85120F & C Asset Management

750.2054CSFB

725.0027Lansdowne Partners

750.7459UBS

1,077.3290Gartmore993.7057Schroders886.1172Goldman Sachs

1,115.16118AXA1,178.105Cede & Co1,179.3167Merrill Lynch1,290.3184AMVESCAP1,297.9750New Star Asset Management1,341.29130Artemis Investment Bank2,052.41160Fidelity

Value of Investments (US$m)No of InvestmentsMost active Institutions by value of investment

Source: London Stock Exchange trade statistics – December 2006

UK Companies

Better value than NYSE or NASDAQ

Admission fees for Non-domestic Equities US$8,980

Annual fees for Non-domestic Equities US$8,980

Source: London Stock Exchange – August 2007

Simple, cost-effective

10

UK CompaniesCase study – Clipper Windpower Plc

Core business activitiesThe Clipper Group designs wind turbines and is a developer and owner of wind development projects. Since it was founded in 2001, the group has focused on developing advanced wind turbine technology embodied in its new Liberty 2.5MW turbine. The Liberty turbine has been designed to provide a machine that is more efficient, more reliable, easier to erect and maintain and offers a significantly longer life than conventional wind turbines in the market. Through these advances, the company believes the Liberty turbine offers a lower cost of energy over a full range of wind classes than thatoffered by competitors’ turbines in the market.

ObjectivesThe net proceeds were used to fund the tooling, manufacture and assembly of the Liberty turbine and for continuing project development and construction. In addition, the Directors used a portion of the net proceeds to expand and strengthen the management and engineering team and for further development and commercialisation of its technology. Initially, the proceeds will provide funding for the manufacture of turbines for installation into Clipper’s most advanced power projects, located in Maryland, and Iowa, USA as well as providing funding for infrastructure costs of these projects.

“The AIM market has enabled our company efficiently to move to the next level of its development and build out a production platform for our industry leading turbine

technology. Clipper Windpower achieved its principal goals in the AIM offering as well as

broadening our exposure to European investors and increasing our global profile.”

Jim Dehlsen - Chairman and CEO

Transaction Synopsis

Date of Admission : 15 September 2005Market: AIMTransaction: PlacingMarket Cap. admission: $358mCapital raised initially: $149mFTSE Classification: Utilities - ElectricityCountry of Incorporation: UK re-incorporation (USA)Nominated Adviser: Lehman BrothersBrokers: Lehman Brothers

UK Companies

Overview of Clipper IPO

Clipper was admitted to AIM on 15 September 2005

July 06, Clipper Windpower and BP announce a strategic turbine supply and joint development agreement.

Shareholder % Dehlson Associated LLc 14.6

Energy Spectrum Partners II and III L.P

8.5

Hare & Co 8.0

Trustees of the Dehlson Family Trust

6.2

Lucas Energy Total Return Master Fund L.P.

3.2

Montecito Bank and Trust 4.4

Pioneer Asset Management SA

4.0

Lansdowne Partners Ltd 3.2

Threadneedle Asset Management

3.2

Fidelity Investments 2.5

Shell Pension 1.9

Shareholder £m $m % Market Cap, on admission 181 334

Fund Raised 75 138 – Primary 67 120 87

– Secondary 10 18.5 13

Placing price per share 190p

Free Float 65%

Case study – Clipper Windpower Plc

11

UK Companies

As companies mature and grow, the Main Market offers a migrationpath

FIRST QUANTUM MINERALS joined AIM in April 2001. Their market cap is now over C$4.5 billion, and in March 2007 they announced they will migrate to the Main Market

AIM is a platform for growth

UK Companies

To summarise… why choose AIM

• The world’s most successful growth market

• An internationally focused, professional investor base

• Comprehensive research coverage for international companies

• A more flexible approach to regulation

• Better value than NYSE or NASDAQ

The Exchange of choice for companies wishing to access the international capital markets

12

AIMTAKING YOUR COMPANY PUBLIC ON THE

LONDON STOCK EXCHANGE

INTRODUCTION

Preparing for IPOCorporate structureRegulationHow to IPO

13

KEY PREPARATIONSAppointment of advisers

Plan and prepareSpeak to your lawyers at an early stage

KEY PREPARATIONSOrganisation of company’s management

Agree a timetableSet up working groupsGet the right non-executive directors

14

CORPORATE STRUCTURERoutes for US Companies

Three main routesTax considerationsUS company admitted to AIM directly

Regulation SElectronic trading – CREST and SISIncreased liquidity

CORPORATE STRUCTURERoutes for US Companies

US company admitted via UK PLC holding company

pre-admission reorganisationshare for share exchange

US company admitted via off-shore holding company

tax considerations

15

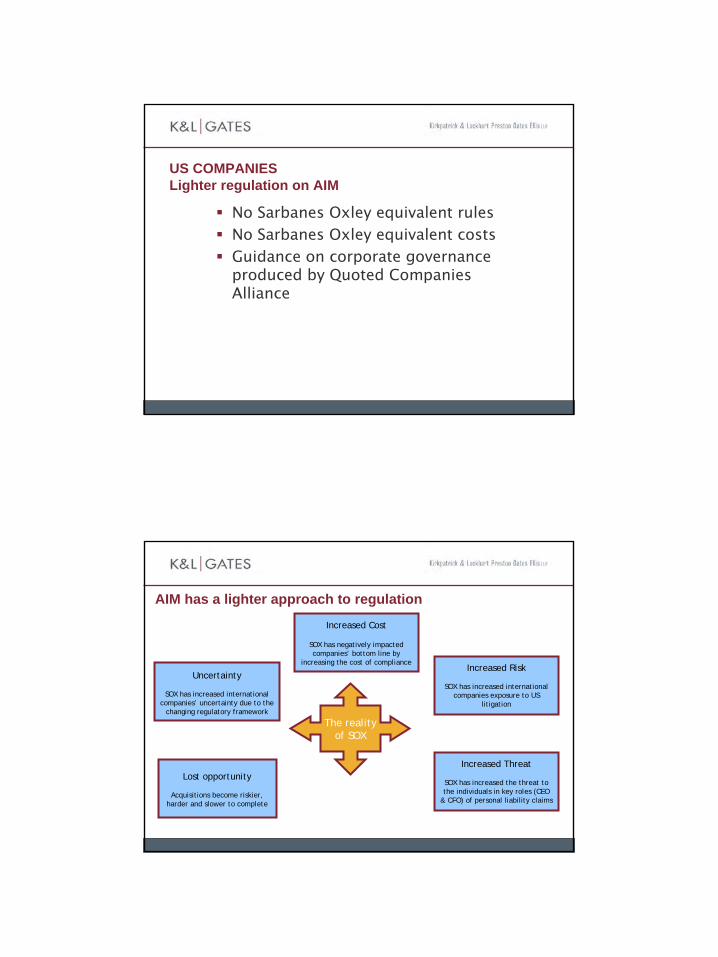

US COMPANIESLighter regulation on AIM

No Sarbanes Oxley equivalent rulesNo Sarbanes Oxley equivalent costsGuidance on corporate governance produced by Quoted Companies Alliance

AIM has a lighter approach to regulation

The reality of SOX

Increased Cost

SOX has negatively impacted companies’ bottom line by

increasing the cost of compliance

Uncertainty

SOX has increased international companies’ uncertainty due to the

changing regulatory framework

Increased Risk

SOX has increased international companies exposure to US

litigation

Increased Threat

SOX has increased the threat to the individuals in key roles (CEO

& CFO) of personal liability claims

Lost opportunity

Acquisitions become riskier, harder and slower to complete

16

CASE STUDY – DAWSON HOLDINGS PLC

First company on AIM in 1995Printed media distributorShare price $8.25 to $15.40 in 1 yearSpringboard to full listShares as acquisition currencyTurnover up from $122m in 1990 to $1.3bn in 1999

The AIM Market of the London Stock Exchange

1. AIM in context2. Basic requirements for an AIM Listing3. AIM Admission Process

17

AIM in context

Over $30 billion funds raised by AIM companies in 2006 (c.f. $16 billion in 2005)Over 1650 companies now on AIM – combined market cap of circa £110 billionMore companies on AIM than Official ListAIM’s popularity on international stageOther secondary markets can’t competeAIM – the only credible market for SMEs

HOW TO IPO

Basic requirementsAdvisersProcess

18

HOW TO IPOBasic requirements

Requirementsno trading record neededno minimum market capno minimum public float

Only 45 AIM rulesLess stringent continuing obligations

HOW TO IPOBasic requirements

AIM Rules:Shares capable of being offered to publicAppoint and retain Nomad and BrokerNo restrictions on transfer of sharesEligibility for electronic settlement All securities of class to be listed“Lock in” requirements

19

HOW TO IPOYour Advisers!

LEGAL

CompanyBoard ofDirectors

Nominated adviser/Broker

PR PrintersRegistrar

Company'sLawyers

(UK + US)

NOMAD'sLawyers

(UK)

Auditors

ReportingAccountants

ACCOUNTING

HOW TO IPOOverview of process

Admission document draftedLegal due diligenceFinancial due diligenceVerification – protecting directorsLondon Stock Exchange formal dealing notice10-14 week timetable

20

K&L Gates: A Few FactsOver the last 2 years:

1st Spin out of businesses from NASDAQ onto AIM (life sciences)

1st Greek based company to IPO on AIM (technology)

1st Japanese company to IPO on AIM (technology)

1st Share for share takeout offer for an AIM company using Japanese paper (natural resources)

1st Fundraising to use a prospectus under the new UK Prospective Regime (financial services)

1st Spin out of a subsidiary of a JASDAQ listed Japanese company onto AIM (manufacturing)

1st US company to utilise SIS System for trading restricted US Reg. S stock

Advised on more than 40 AIM IPO’s over last two years

Advised on more than 200 IPO’s over last eight years

IPO Services

The Financial Aspects of an IPOHelping you to understand the challenges that you may face in listing your company on the Alternative Investment Market

Steve SmithIPO Leader UK NorthTransaction Advisory ServicesErnst & Young LLP+44 161 333 [email protected]

Seattle4 October 2007

21

Ernst & Young in the IPO Space

Number of dealsEY

14%

DT14%

KPMG11%

PwC12%

Other49%

Total capital raised

EY29%

DT18%

KPMG15%

PwC23%

Other15%

Source: Dealogic, Thomson Financial

Globally 2006UK IPOs (>£200m) 2006 (% of proceeds raised)

UK IPOs 2006 (% of proceeds raised)

D T10%

EY46%

KP M G3%

P WC30%

Other9%

Unkno wn2% D T

11%

EY38%

KP M G6%

P WC28%

Other11%

Unkno wn6%

Source: Dealogic, Thomson Financial

• Short form report

• Working capital report

• Long form report

• Comfort letters

Reporting Accountant

AIM Candidate

Parties involved in an IPO

• Issue audit opinion on financial statements

• Comfort letters

Auditor

• Analysis and optimization of key business processes, KPIs

• Development of IFRS compliant reporting policy & procedures

• Definition of internal controls framework

• IT Audit & Security

• Tax structuring & transfer pricing

• Management incentive schemes, Non-executive directors system

• Environmental DD

• Legal DD

Other Advisors

• Test marketing

• Identify investors

• Valuation benchmarking

• Marketing roadshow

• Book-building and pricing

Broker

Lawyers

Financial PR

Registrars

NOMAD

• Ensure that the directors of the Company have received satisfactory advice and guidance as to the nature of their obligations

• Coordinate the work of other professionals – such as accountants and lawyers who are involved in preparing a Company for the market

• Issue an opinion that it is satisfied that the Company applying to AIM is appropriate to be admitted.

Competent Person

• Resource companies

22

The AIM Admission Document

The Public Document – similar to a Prospectus

Description of the business

− A balanced appraisal of the business and its prospects

− The risk factors

− Details of the offer and the use of funds

Financial information

− Includes historical financial track record – 3 years possibly with recent stub period

› Accountant’s report

› Previously audited financial information with audit reports

Legal disclosures

− Includes working capital statement and significant change in financial position disclosure

The role of the accountant in an IPOReporting accountant

• Preparation of accountant’s (short form) report(s)

• Preparation of long form report

• Preparation of working capital report

• Other comfort letters

Tax advisor

• Structuring advice

• Independent tax diligence

• Tax clearances

• Review tax section of the prospectus/admission document

23

Short form Public report, included in document

Reports on the financial information supplied on the Company

• Typically 3 years

• US GAAP is acceptable

Gives an opinion similar to audit opinion – “true and fair view”

• Review audit files for a period of up to three years to the date of the latest audited accounts

• Perform additional audit work (if necessary) to ascertain that the report gives a true and fair view

• Reporting Accountant ensures there is adequate reliable evidence to support the opinion

Need to watch the 135 day rule (under US rule144a) for age of financial information if shares are offered in the US as well

Long form report Private document – addressed to the Nomad and the Company

Full scope due diligence report prepared to assist in the drafting of the admission document, to determine the suitability of the Company for admission and covering:

• History, development and strategy of the business

• Management, employees and organisation structure

• Financial reporting procedures and accounting policies

• Historical financial information

• Taxation

Significant amount of information required from Company

Substantial management time commitment

24

Working capital report Private document – addressed to the Nomad and the Company

Directors are required to make a statement in admission document concerning sufficiency of working capital for 12 months

Company prepares financial projections model for valuation purposes but also to support this statement

Accountant’s report on this in order to give comfort on the statement

• Detailed review of model

• Sensitivity analysis

Significant management time – taken in preparation of model and accountant’s review

Other comfort letters Pro forma financial information

• In admission document to illustrate changes due to IPO

• Reporting accountant reports on this (private report)

Profit forecast

• Try to avoid making profit forecasts in admission document

• If made, must be reported on by accountant’s

• Significant piece of work

Review of admission document

• General assistance in drafting process

• Comfort on certain financial/tax matters

US share offering would require separate ‘SAS 72’ comfort letter

25

Roles of reporting accountant vs auditorThe role of the Reporting Accountant and Auditor are different and will be conducted by different teams whether the Reporting Accountant is from the same firm or a different firm.

Based on the future structure of the Group, prepare a pro forma balance sheet and income statement that supports the marketing process

NonePro forma

Comfort on selected financial information disclosed in the ProspectusNoneProspectus

Review and report on the forecast cash flows and funding position of the Group to be listed

NoneWorking Capital Report

Formal sign off on the appropriateness of the Group’s financial reporting procedures and controls

NoneFinancial Reporting Procedures

Review and report on the affairs of the Group to be listed to enable the Sponsor to approve the IPO

NoneLong Form Report

To give a fresh, audit style, opinion on the financial informationAudit the financials of the legal entities which will eventually form part of the Group

Short Form Report

Role of the reporting accountantRole of the auditorDeliverable

In effect, the Sponsor requires support from the Reporting Accountant to meet its regulatory responsibility

Issues that may be encounteredOur experience in performing IPOs indicates that the Reporting Accountant may need to deal with issues in the following areas

The evolving nature of tax legislation of many countries may mean that changes are required to meet Nomad and market expectationsTaxation

Local historical audit evidence available may not be sufficient to enable sign-off. This may require significant reworkDocumentation

The historical accounting policies may not be in line with your peer group and may need to be amendedAccounting policies

There will be a series of related party transactions and balances that need to be appropriately disclosedRelated party disclosures

Demonstrable unencumbered title to assets (throughout their operating life) needs to be demonstratedAsset title

Public companies have additional disclosure obligationsHigher burden oftransparency and disclosure

Our approach and early issues review is designed to identify these potential issues, enabling us to design solutions which can then be implemented without disruption to the timetable.

26

To conclude

In our experience AIM is open for US companies

• It will take longer than you expect

• Plan as early as you can

Choose advisors carefully

• Knowledge

• Experience

• Reputation

ERNST & YOUNG LLP www.ey.com

Disclaimer: Information in this presentation is intended to provide only a general outline of the subjects covered.

It should neither be regarded as comprehensive nor sufficient for making decisions, nor should it be used in place

of professional advice. Ernst & Young accepts no responsibility for any loss arising from any action taken or not taken

by anyone using this material.

The UK firm Ernst & Young LLP is a limited liability partnership registered in England and Wales with

registered number OC300001 and is a member practice of Ernst & Young Global.

27

The NOMAD’s Point of View Securing Capital and Who Should Look to List on AiM?

Palo AltoSan FranciscoLondon Minneapolis New YorkChicagoHong KongShanghaiBeijing

Table of Contents

Section I Securing Capital

Section II Who Should Look to List on AiM?

Appendix A IPO Process

Appendix B Liquidity case study

Appendix C Overview of Piper Jaffray

28

SECTION ISecuring Capital

Possible reasons for considering AiM

• Access development capital

• Secure future funding rounds

• Remove inefficient financing

• Provide an exit for existing shareholders

• Achieve greater liquidity

• Gain an international shareholder base

• Facilitate expansion into Europe

• Enhance the Company’s profile and status – increase press coverage and transparency of public reporting

• Provide currency to make acquisitions

• Provide currency to incentivise staff and encourage employee share ownership

• Achieve a dual listing

• Avoid costly U.S. regulatory environment

There are several good

reasons to consider an

AiM IPO, but for smaller

U.S. companies the key

driver has often been to

avoid the costly U.S.

regulatory environment

accompanying a listing

in the U.S.

Regulatory arbitrage is

not well received by

institutional investors

“WHY AiM?” – the first question from institutional investors

29

Successful listing characteristics - generally

• Realistic valuation expectations

• Experienced management team – professional, dynamic, communicative and open

• Strong track record of delivery

• Growth potential

• Visibility of future earnings

- recurrent revenue

- company newsflow

• Well positioned in a significant and well defined market

• Clearly defined strategy and robust business plan

• Competitive advantage - innovative products/services/technology

• Protected market position

- barriers to entry

- IP

• Size of free float

- greater liquidity and free-float is valued highly by investors

- 25%+ of outstanding shares

- at least $20-25m in absolute terms

• Quality of NOMAD

The quality threshold for companies seeking an IPO is not lower on AiM

Institutional investors

are increasingly focused

on high quality

companies as the

market softens, a

situation which is

exacerbated for foreign

companies

Successful listing characteristics – U.S. companies

• Clear rationale for AiM listing

– international revenues

– international operations, preferably with a European presence

– defined international expansion plans

• Adoption of, or readiness to adopt, UK plc practices

– Board structureChairman and CEO separate

independent non-executives – at least two

regular re-election

audit, remuneration and nomination committees

– investor protectionspre-emption rights

disclosure of substantial share interests

mandatory take-over provisions

– non-U.S. holding companymay be beneficial to avoid SEC registration obligations

but consider tax implications

– preferred stock converted into ordinary shares

U.S. companies can increase the warmth of welcome by investors by articulating clear business reasons to list on AiM and by adopting certain corporate governance good practices

30

Other key issuesPrimary vs. Secondary• Primary preferred by investors but must be clear rationale and justification• Partial exit possible

– small proportion of overall offering size: more than 50% exceptional– small proportion of holders’ shares sold – shares being sold by longer term shareholders, though wary of founders cashing-out– but positive effect on offering size and liquidity– often through Greenshoe

Board presence• Remote in distance and time zones

– executive management regularly required to be in UK – recommend one director to be based in the UK

Share option schemes• Needs justification to price at less than the IPO price• The longer between award and IPO the better if priced at a discount, even if priced at ‘fair

value’• Performance hurdles

Other key issues (cont’d)Accounting standards and financial history• U.S. GAAP is permissible• A three year track record will not be required

Company lock-up

• 6 – 12 months– with 6 - 12 month orderly market agreement

Shareholder lock-ups• For companies whose main business activity has not been independent and revenue earning

for two years prior to Admission, 12 months lock-up for Directors, Substantial Shareholders (≥10%) and their Associates and Applicable Employees (≥0.5%) (Rule 7 of the AiM Rules for Companies)

• Otherwise,– 12 month lock-up for senior management– with 6 - 12 month orderly market agreement– may be longer if selling stock on IPO

• Limited exceptions – take-over offer, death or court order or, if not Rule 7, with agreement of NOMAD

31

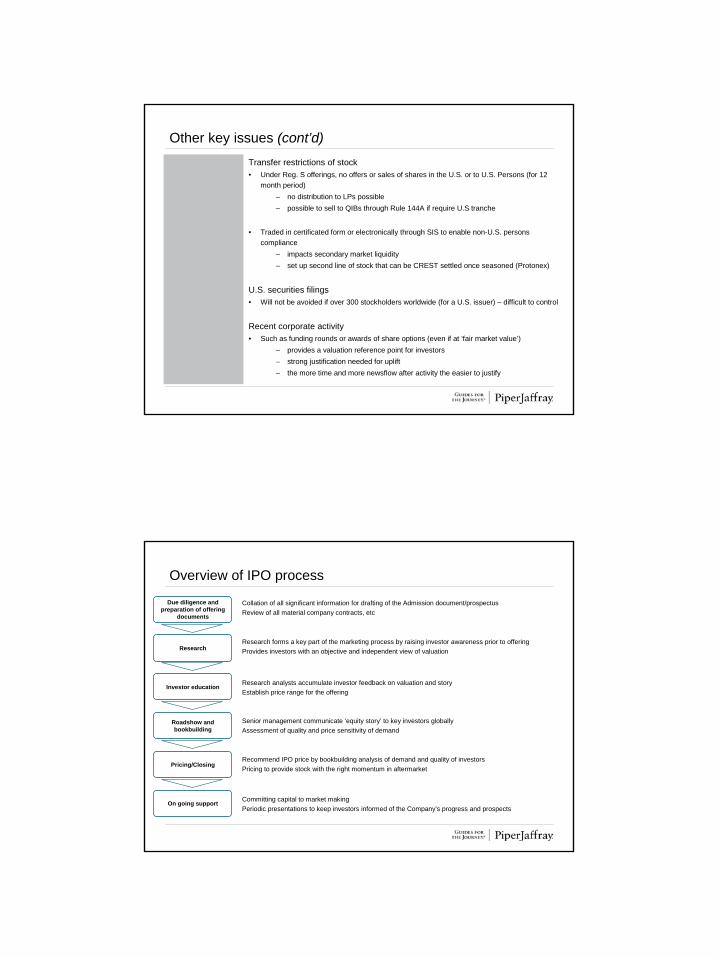

Other key issues (cont’d)Transfer restrictions of stock• Under Reg. S offerings, no offers or sales of shares in the U.S. or to U.S. Persons (for 12

month period)– no distribution to LPs possible– possible to sell to QIBs through Rule 144A if require U.S tranche

• Traded in certificated form or electronically through SIS to enable non-U.S. persons compliance

– impacts secondary market liquidity– set up second line of stock that can be CREST settled once seasoned (Protonex)

U.S. securities filings• Will not be avoided if over 300 stockholders worldwide (for a U.S. issuer) – difficult to control

Recent corporate activity• Such as funding rounds or awards of share options (even if at ‘fair market value’)

– provides a valuation reference point for investors– strong justification needed for uplift– the more time and more newsflow after activity the easier to justify

Collation of all significant information for drafting of the Admission document/prospectus Review of all material company contracts, etc

Due diligence and preparation of offering

documents

Research forms a key part of the marketing process by raising investor awareness prior to offeringProvides investors with an objective and independent view of valuation

Research analysts accumulate investor feedback on valuation and story Establish price range for the offering

Senior management communicate ‘equity story’ to key investors globallyAssessment of quality and price sensitivity of demand

Recommend IPO price by bookbuilding analysis of demand and quality of investorsPricing to provide stock with the right momentum in aftermarket

Committing capital to market makingPeriodic presentations to keep investors informed of the Company’s progress and prospects

Research

Investor education

Roadshow and bookbuilding

Pricing/Closing

On going support

Overview of IPO process

32

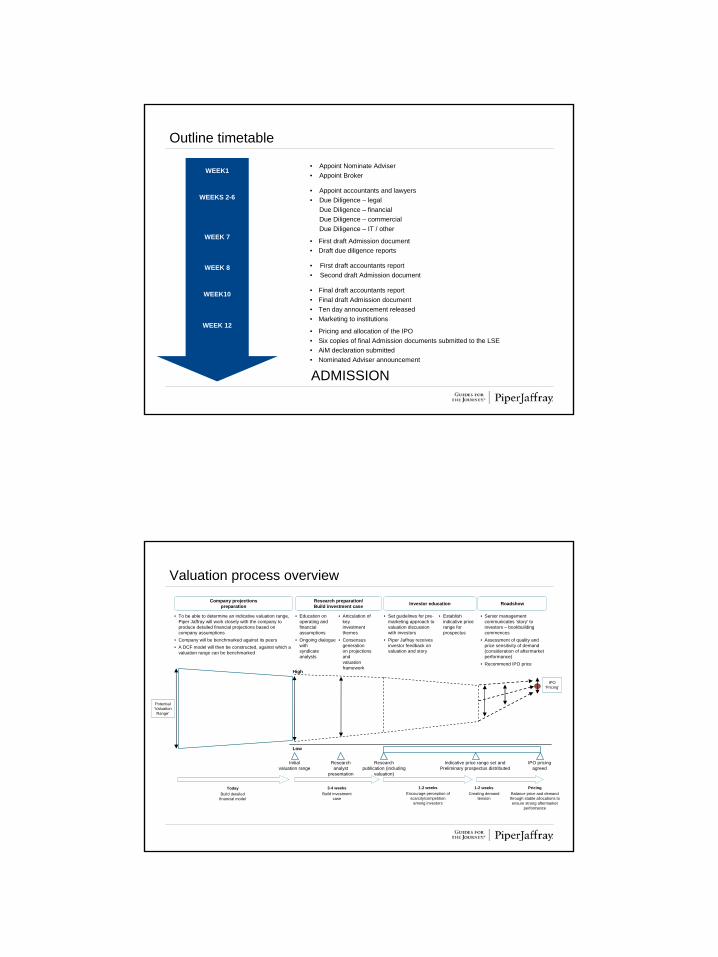

Indicative timetable

ADMISSION

WEEK 12

WEEK10

WEEK 8

WEEK 7

WEEKS 2-6

WEEK1

• Pricing and allocation of the IPO• Six copies of final Admission documents submitted to the LSE• AiM declaration submitted • Nominated Adviser announcement

• Final draft accountants report• Final draft Admission document• Ten day announcement released• Marketing to institutions

• First draft accountants report• Second draft Admission document

• First draft Admission document• Draft due diligence reports

• Appoint accountants and lawyers• Due Diligence – legal• Due Diligence – financial• Due Diligence – commercial• Due Diligence – IT / other

• Appoint Nominate Adviser• Appoint Broker

Outline timetable

Valuation process overview

Investor educationResearch preparation/ Build investment case Roadshow

PricingBalance price and demand

through stable allocations to ensure strong aftermarket

performance

• Set guidelines for pre-marketing approach to valuation discussion with investors

• Piper Jaffray receives investor feedback on valuation and story

• Establish indicative price range for prospectus

• Education on operating and financialassumptions

• Ongoing dialogue withsyndicate analysts

• Articulation of keyinvestment themes

• Consensus generationon projections andvaluation framework

• Senior management communicates ‘story’ to investors – bookbuilding commences

• Assessment of quality and price sensitivity of demand (consideration of aftermarket performance)

• Recommend IPO price

Company projectionspreparation

• To be able to determine an indicative valuation range, Piper Jaffray will work closely with the company to produce detailed financial projections based on company assumptions

• Company will be benchmarked against its peers• A DCF model will then be constructed, against which a

valuation range can be benchmarked

IPO ‘Pricing’

Initialvaluation range

Research analyst

presentation

Indicative price range set and Preliminary prospectus distributed

IPO pricingagreed

3-4 weeksBuild investment

case

1-2 weeksEncourage perception of

scarcity/competition among investors

1-2 weeksCreating demand

tension

Researchpublication (including

valuation)

Low

High

Potential‘Valuation

Range’

TodayBuild detailed

financial model

33

SECTION IIWho Should Look to List on AiM?

A market for companies of all sizes

Distribution of AIM Companies by M arket Value August 2006 vs August 07

123

178

222

367

233

199

145

2310 6

104

171

227

359

274

242

183

68

204

0

50

100

150

200

250

300

350

400

Less than$3.9m

$3.9m - $9.9m $9.9m - $19.8m $19.8m -$49.5m

$49.5m - $99m $99m - $198m $198m -$495m

$495m -$990m

$990m -$1980m

over $1980m

M arket Value (US$)

No.

of C

ompa

nies

The majority of AiM

companies have a

market cap below

$200m – a striking

contrast to NASDAQ

and the LSE Official List

– although sizes are

growing

60% of AiM companies

by value now have a

market cap. greater than

$200m

U.S. companies on AiM

tend to be larger than

the market as a whole

No. of companies August-06

No. of companies August-07

Distribution of US companies by Market alue August 07

6 6

14

16

21

65

2

0

2

4

6

8

10

12

14

16

18

20

22

Less than $9.9m

$9.9m - $19.8m

$19.8m - $49.5m

$49.5m -$99m

$99m - $198m

$198m - $495m

$495m - $990m

over $990m

Market Value (US $)

No.

of C

ompa

nies

Source: London Stock ExchangeData through Aug 31, 2007

34

A market for companies of all sectors

Sector distribution of US companies by number August 07

9 9

8

7

4 4 4 4

3 3 3

0

1

2

3

4

5

6

7

8

9

10

Electronic &Electrical

Equipment

Oil & GasProducers

Software &ComputerServices

Pharmaceuticals&

Biotechnology

Automobiles &Parts

Chemicals GeneralFinancial

SupportServices

Health Media Speciality &Other Finance

No.

of C

ompa

nies

While real estate,

natural resources,

support services and

financials lead the pack,

AiM is a market open to

all sectors

For U.S. companies,

Technology, Healthcare

and Oil & Gas

companies dominate

Top AIM sectors by market capitalisation and no. of companies August 07

106179

146 193102

143 116 66 8876

-

5,000

10,000

15,000

20,000

25,000

30,000

Real Estate Mining SupportServices

GeneralFinancial

Oil & GasProducers

Softw are &ComputerServices

Media EquityInvestmentIntruments

Travel & Leisure

Pharmaceuticals& Biotechnology

Mkt

Val

ue (

US$

m)

0

50

100

150

200

250

Num

ber o

f com

pani

esMarket Value USD$Number of Companies

Source: London Stock ExchangeData through Aug 31, 2007

A market for companies seeking to secure capital

Number of admissions 1995 to 2007

123145

107

75102

277

177160 162

355

519

462

201

0

100

200

300

400

500

600

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Num

ber o

f adm

issi

ons

AiM is maturing as a

market – the average

amount raised by

companies floating on

AiM is now c. $95m*

and growing

However, the climate for

IPOs on AiM, and

foreign companies in

particular, has cooled

recently

* Excluding IPOs <$5m; 2007 YTD

Note: Includes transfer and relistings

3.51.2 1.0 2.2

5.5

12.8

19.7

10.62.6

1.1 1.02.0

3.7

4.9

11.4

15.3

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2000 2001 2002 2003 2004 2005 2006 2007

Fund

s ra

ised

($b

n)

Further money raised ($bn)

Money raised at admission ($bn)

35

A market for high quality growth companies

• No minimum capitalisation, free float or shareholder requirements– allows earlier stage, smaller companies to float– attracts investors seeking high growth opportunities– ‘Bigger fish in a smaller pond’

• No operating history and trading record required (if no offer to the public and prospectus)– companies can be admitted to AiM before they are old enough to list on the Main

Market in London or on NASDAQ

• Internationally orientated institutional investors hungry for high quality, high growth stories, regardless of country of incorporation

– companies that meet the standards discussed earlier will attract strong investor interest

AiM allows high quality

companies with a strong

equity story to achieve a

public market quotation

sooner than on the full

Official List in London or

on NASDAQ

APPENDIX AIPO Process

36

Preparation: due diligence and documentation

Regulatory and legal requirements and market practice oblige Piper Jaffray and transaction counsel to undertake extensive due diligence

Due diligence process:

• Piper Jaffray and lawyers meet with Issuer’s management, board and auditors• The Admission document/prospectus must fully and accurately portray the issuer’s affairs with no material omissions• Key selling messages developed

– position the Issuer– address potential concerns

Admission document/Prospectus:Admission document/prospectus serves two functions – a disclosure document (approved by, and filed with, the UKLA if a prospectus) and a marketing document to sell the offer. The Admission document/prospectus contains:

• business activities• trading history • management structure• future direction

Research report – prepared by the senior syndicate managers’ research analysts (who give their independent view), distributed before the offering and used as the managers’ principal marketing tool, guiding investors towards the appropriate valuation. One-on-one and roadshow presentations – used to market the Issuer and its investment case to investors.

• details of offering

• current shareholders

• risk factors

• other financial and legal information

Pre-marketing

Roadshow

Bookbuilding

Pricing/Allocation/

ClosingStabilisationDue

Diligence

Preparation of offering materials

Research

Legal documentation

• Regulates the offering and placement of shares• Partly based on letter of engagement, but also includes representations and warranties by the

Issuer and selling shareholdersUnderwriting Agreement

• General agreement between the Issuer and Piper Jaffray • Regulates rights and obligations in the course of preparation of the issue, including

commission and reimbursement of costsEngagement Letter

• Auditors’s confirmation regarding accuracy of financial data published in the prospectus• Negative assurance of no material change since last auditLetter of Comfort

• Submitted by lawyers• 10b5 opinion not required if no selling into the USLegal Opinion

• Company, directors, selling shareholders• Designed to protect investorsLock up

Pre-marketing

Roadshow

Bookbuilding

Pricing/Allocation/

ClosingStabilisationDue

Diligence

Preparation of offering materials

Research

37

Importance of research

It is important for the Issuer to appoint a Lead Manager whose investment research is highly regarded

Piper Jaffray would produce comprehensive research and co-ordinate research production by any other syndicate members

Institutional investors rely heavily on research in making investment decisions

Research forms a key part of the marketing process for any new issue

• raises investor awareness prior to offering

• explains valuation

• provides investors with an objective and independent view

• induces investors to alter portfolio allocationsInvestor education enables the indicated size and price range to be based on accurate feed-back

Approximately two weeks prior to launch, specific investor education of the issue would commence

From this pre-marketing a picture of the likely level of investor demand will emerge. Based on this feedback, the Issuer and Piper Jaffray set the expected size and the anticipated price range of the offering. This allows extensive but directed ‘price talk’with institutions during the building of the book of demand, creating price tension

Pre-marketing

Roadshow

Bookbuilding

Pricing/Allocation/Closing

StabilisationDueDiligence

Preparation of offering materials

Research

Germany

ActivestAllianz/DIT Bayern Invest Cominvest DWS DeutscheDGZ-DekaBankFrankfurt TrustInvesco Kapital

Lupus AlphaNordinvestOppenheimDeutsche Postbank SEBUnion InvestWest AM

France

Spain

Scandinavia

AP3BankInvestCarnegie AMDanske Capital

Den Danske Bank NordeaUnibank

Netherlands

ABN AmroASWDelta LloydDe MelloDSM PFGo Capital

INGInsingerMacCapitalProgress (Unilever) Robeco

Belgium/Luxembourg

Banque de LuxembourgBGL InvesmentCorluyDexiaEthiasFortisGIMV

KBCINGPetercamPuilaetcoQuest for GrowthSERCAM

Italy

SwitzerlandAdamantBank Julius Baer & Co.Bank ThalerBank LeuBellevue Asset ManagementClariden BankCompania Intl FinancieraCredit Suisse Asset Mgmt.EFG International

Lombard Odier Darier MicroValue AGPictet & CieSuvaSwissca Portfolio Mgmt.Swissfirst Bank (Zurich)UBS GAMUnion Bancaire Privee

Aletti Gestielle AM.Anima S.G.R.p.AAntonveneta ABN AmroArcaAzimutBNL Gestioni Bipiemme Gestioni S.G.R.S.p.A

CapitalgestCAAM IMErselEuromobiliare AMGenerali AM.Julius BaerMonte Paschi AMRAS AMSanpaolo IMI AM

Roadshows

UK Jupiter LansdowneLegal & General LiontrustM & G MarlboroughMarathon AM Merrill Lynch IMMilleniumMKM LongboatMorgan Stanley AM Morley New Star AM Newton IMOdey Old Mutual AMPolar Capital PolygonPutnamRAB CapitalRCM (U.K.) LtdReabourne LtdRothschild AMRoyal London AMSarasin IM.Schroder IMScottish WidowsSoc Gen AM. UKStandard LifeThreadneedle AMTT InternationalUniversities Superannuation UBS Walter Capital Axa

BNP Paribas CCRCDCCGU Victoire AM

Credit LyonnaisLCF RothschildFortisMeeschaertOptigestionSGAM

Banco Popular Barclays FondosBBVABSCH

CaixagestCaixa CatalunyaGesbetaGesmadridSantander

AberforthAbingworthABN Amro AdelphiAegon IMAlliance Trust ArtemisAxa FramlingtonBaring AMBlackrockBlueCrest BradshawCanada lifeCapital InternationalCCLACheyne CloseCQSFidelity Findlay Park First State F&CGartmoreGLG PartnersHealthcorHenderson Herald IMHermesInsight IMINVESCO Perpetual JO HambroJP Morgan AM

Pre-marketing

Roadshow

Bookbuilding

Pricing/Allocation/ Closing

StabilisationDueDiligence

Preparation of offering materials

Research

38

Bookbuilding

Offer launched on indicative pricing termsOffer price fixed after marketing/roadshows completedUnderwriting occurs after bookbuilding completeAllocation to investors

The bookbuilding process is designed to identify sources of highest demand and create ‘competitive tension’ among investors

Build book of demand

Sizing and pricing

Indicative valuation

Pre-marketing

Pricerange

Determine demand at different prices

Provide feedback to investors

Bookbuilding is designed to achieve the optimum price for the offering• pricing which reflects genuine demand in the marketplace and offers transparency of investor demand, allowing

assessment of investor quality and the effect of changes in price upon demand

Pre-marketing

Roadshow

Bookbuilding

Pricing/Allocation/

ClosingStabilisationDue

Diligence

Preparation of offering materials

Research

Setting the price

Price range

• Attractive value proposition to investors within range

• Large enough range around fair price to allow for market adjustments

• Ensure price range creates pricing discussion

• High level of confidence in achieving forecasts underpinning valuation

• Flexibility to move price range if required

+

Roadshow• Management convincing investment

community of strategy (vision) and business plan

• Broader introduction to financial markets

Market• General market sentiment• Share price movements in direct

comparables • Newsflow on sector

- earnings- industry trends

Investor interest• Anchor investors, setting trend and

building momentum in the book• General level of oversubscription of

quality accounts• Price limits• Indications on aftermarket interest

+

Offer price

• Maximise value for selling shareholders whilst

• Giving stock right momentum in aftermarket

• Offering fair value for balanced investor group

• Giving management opportunity to deliver and provide medium-term impetus to stock

Pre-marketing

Roadshow

Bookbuilding

Pricing/Allocation/

ClosingStabilisationDue

Diligence

Preparation of offering materials

Research

39

Allocation criteria

• Price leadership; price limits• Size of order (relative to average holding size)• Timing of order• Stability of order (demand increase; limit changes)• Seriousness of order - record in similar investments; level of analysis completed• Participation in one-on-one, roadshow and research call• Anticipated aftermarket behaviour (previous experience of aftermarket holding/buying/selling• Behaviour in previous offerings

Allocation

Pre-marketing

Roadshow

Bookbuilding

Pricing/Allocation/

ClosingStabilisationDue

Diligence

Preparation of offering materials

Research

Time

Pric

e

Stabilisation supports aftermarket, if requiredObjective is to stabilise aftermarket performance of the IPO and to ensure an orderly market for investors with sufficient trading liquidity and demand to absorb any selling pressure if required

The Lead Manager is given a ‘Greenshoe’ over-allotment option by the issuer/selling shareholder to facilitate stabilisation – usually 15% of offering

The existence of the option provides investors with confidence when bidding, maximising proceeds, that there will be stabilisation

As a successful offering will be oversubscribed, the Greenshoe will be allocated, thus creating a short position for the syndicate

• if the share price falls in initial trading, Piper Jaffray will place a bid in the market at issue price to absorb any shares offered, thus reducing the short position

• if share price rises in initial trading, Piper Jaffray will exercise the Greenshoe to prevent losses that syndicate would incur in covering short position above issue price

Stabilisation

Pre-marketing

Roadshow

Bookbuilding

Pricing/Allocation/

ClosingStabilisationDue

Diligence

Preparation of offering materials

Research

40

Aftermarket support

• Aftermarket support is provided at Piper Jaffray by the Corporate Broking team• Continuing research coverage

– regular reports– ad hoc reports on newsflow

Roadshow management and investor targeting

Co-ordination of institutional company visits/meetings undertaken to build and maintain investor relationships, including for• Results• Site visits• Lunches• Corporate activity

Selective investor targeting for effective use of management timeFeedback exercise undertaken and provided to client

APPENDIX BLiquidity Case Study

41

0

20

40

60

80

100

120

140

Jul-0

4

Aug

-04

Sep-

04

Oct

-04

Nov

-04

Dec

-04

Jan-

05

Feb-

05

Mar

-05

Apr

-05

May

-05

Jun-

05

Jul-0

5

Aug

-05

Sep-

05

Oct

-05

Nov

-05

Dec

-05

Jan-

06

Feb-

06

Mar

-06

Apr

-06

May

-06

Jun-

06

Jul-0

6

Aug

-06

Six month lock-upexpiry

Market cap onadmission of £60m,

£20m raised

First development phase of Gyrohaler completed

Interim results to30 Sep-04 announced

$375m licensing agreementsigned with Novartis forAD237, $15m up front

Final results to 31 Mar-05

Interim results to 30 Sep-05 announced

Collaborative agreement signed for VR315,

EUR23m in milestones anddevelopment funding

Collaboration agreementsigned with Boehringer

Ingelheim to developbranded DPI, €15m

investment in cash andshares

Final results toMarch 2006

£45m fundraising announced

11m VC shares placed

2m VC shares placed

3m VC shares placed

3m VC shares placed

6m VC shares placed

Sha

re p

rice

(pen

ce)

Liquidity case study: Vectura Group Plc

25m+ VC shares placed

Liquidity case study: Vectura Group Plc (cont’d)

• UK emerging pharmaceutical company developing a range of inhaled drugs for the treatment of lung diseases and other conditions where delivery via the lungs can provide significant benefits

• Raised £20m ($38m) new money through an AiM IPO in June 2004 - £60m ($114m) market cap

• Immediately after IPO, pre-IPO shareholders comprised approximately 55% of the share register–- locked-up (hard) for 6 months with a further 6 month orderly market agreement

• Diverse group of key pre-IPO shareholders, including a number of “classic” VC investors, founding shareholders (several private individuals and a university) and former directors

• Imperative that the placing of VC stock in the market is carried out in a co-ordinated way to capitalise fully on liquidity opportunities

• As each pre-IPO shareholder had different intentions and exit strategies following the IPO, essential that close proactive contact was maintained by the NOMAD with each party in the lead-up to, and throughout, the sell-down process

–- allow fast reaction to liquidity opportunities –- ensure all pre-IPO shareholders are treated on an equitable basis –- avoid “breaking of ranks”

• Since IPO lock-up expiry, over 25 million Vectura shares have been placed in the market by the Piper Jaffray teamon behalf of pre-IPO shareholders

42

Liquidity case study: Vectura Group Plc (cont’d)

• Shares placed in a co-ordinated fashion, to capitalise on positive company news flow and successful investor road shows

• Larger blocks of VC stock targeted at particularly liquid and receptive periods in the market, generally on the back of positive company news flow - ensure such large stock placements did not negatively impact the share price

• From 55% at IPO in June 2004, Vectura’s VC shareholding was below 10% by April 2006 with those VCs remaining shareholders doing so through choice

• In June 2006, Piper Jaffray lead-managed a £45 million ($86m) fundraising for Vectura, the largest secondaryfundraising ever for an AiM-listed biotechnology company

• Conclusion: Liquidity is not a function of AiM vs. LSE or NASDAQ but instead a function of:– quality of company– quality of management team– company newsflow & delivery on expectations– business plan and track record– size of free float– quality of NOMAD

• AiM now represents a highly credible option for VCs seeking timely liquidity opportunities from high growth, quality newsflow-rich companies

APPENDIX COverview of Piper Jaffray

43

- leading sector focused middle market investment bank

Key factsKey facts

• 10 offices worldwide• More than 1,000 employees• Publicly listed in New York• $1.0bn market capitalisation• Over 350 growth companies covered • Focus on 6 core sectors

• 10 offices worldwide• More than 1,000 employees• Publicly listed in New York• $1.0bn market capitalisation• Over 350 growth companies covered • Focus on 6 core sectors

*Securities and products are offered in the United Kingdom through Piper Jaffray Ltd., which is authorized and regulated by the Financial Services Authority

• Client-focused, independent, publicly held securities firm founded in 1895

• Leading growth-oriented, middle market investment bank

• Top ranked middle market M&A adviser

• Ranked No.1 in IPOs completed in our focus sectors

• Lead manager on the top performing IPOs in the industry in recent years

• NOMAD and broker to leading growth companies

• Full service capabilities and unparalleled transaction execution

• Client-focused, independent, publicly held securities firm founded in 1895

• Leading growth-oriented, middle market investment bank

• Top ranked middle market M&A adviser

• Ranked No.1 in IPOs completed in our focus sectors

• Lead manager on the top performing IPOs in the industry in recent years

• NOMAD and broker to leading growth companies

• Full service capabilities and unparalleled transaction execution

Piper JaffrayPiper Jaffray

Minneapolis (HQ)

Chicago BostonNew York

London*

Shanghai

San Francisco

Palo Alto

Hong Kong

Beijing

70+ employees in Europe focussed on Technology, CleanTech, Healthcare and ConsumerAcquisition of Goldbond Capital holdings, Hong Kong based investment bank with 70 employee

Growth sector focus, integrated approach

TechnologyTechnology

Clean TechClean Tech

ConsumerConsumer

Financial InstitutionsFinancial Institutions

HealthcareHealthcare

Industrial GrowthIndustrial Growth

Investment Banking

Institutional Equity Sales

Equity Trading

Equity & Debt

Capital Markets

Convertible Securities

High-Yield &

AcquisitionFinance

Equity & Fixed

Income Research

Piper Jaffray offers the advantage of scale without sacrificing impartiality of advice or client focus

Sectors Global presence Products

Inte

grat

ed a

ppro

ach

44

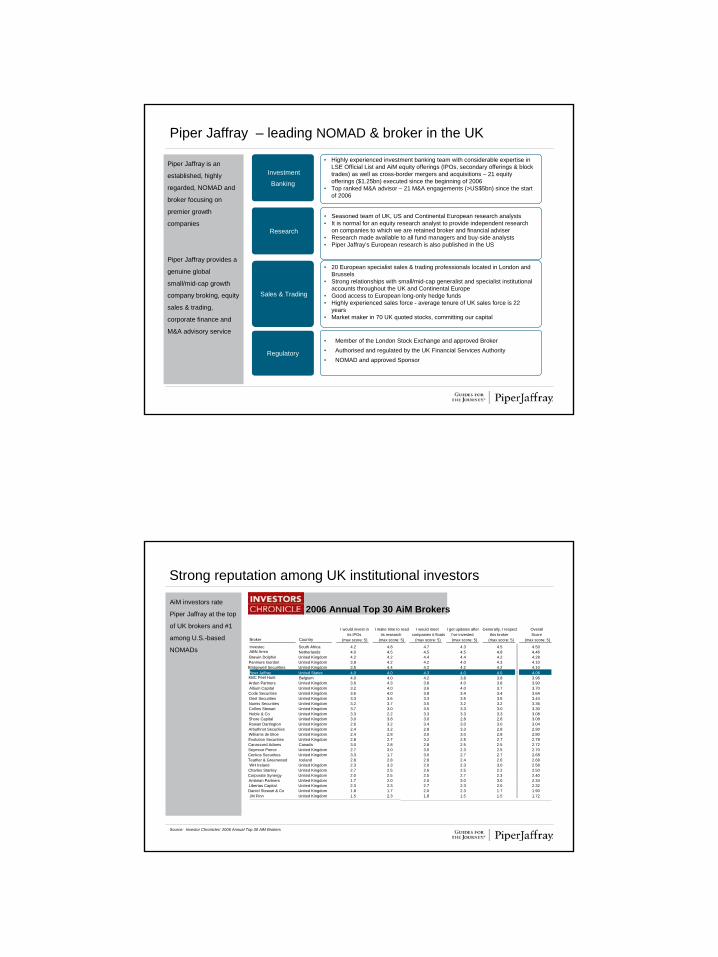

• Highly experienced investment banking team with considerable expertise in LSE Official List and AiM equity offerings (IPOs, secondary offerings & block trades) as well as cross-border mergers and acquisitions – 21 equity offerings ($1.25bn) executed since the beginning of 2006

• Top ranked M&A advisor – 21 M&A engagements (>US$5bn) since the start of 2006

Piper Jaffray – leading NOMAD & broker in the UK

Piper Jaffray is an

established, highly

regarded, NOMAD and

broker focusing on

premier growth

companies

Piper Jaffray provides a

genuine global

small/mid-cap growth

company broking, equity

sales & trading,

corporate finance and

M&A advisory service

Investment

Banking

Regulatory

• Member of the London Stock Exchange and approved Broker• Authorised and regulated by the UK Financial Services Authority• NOMAD and approved Sponsor

Sales & Trading

Research

• 20 European specialist sales & trading professionals located in London and Brussels

• Strong relationships with small/mid-cap generalist and specialist institutional accounts throughout the UK and Continental Europe

• Good access to European long-only hedge funds• Highly experienced sales force - average tenure of UK sales force is 22

years • Market maker in 70 UK quoted stocks, committing our capital

• Seasoned team of UK, US and Continental European research analysts• It is normal for an equity research analyst to provide independent research

on companies to which we are retained broker and financial adviser• Research made available to all fund managers and buy-side analysts• Piper Jaffray’s European research is also published in the US

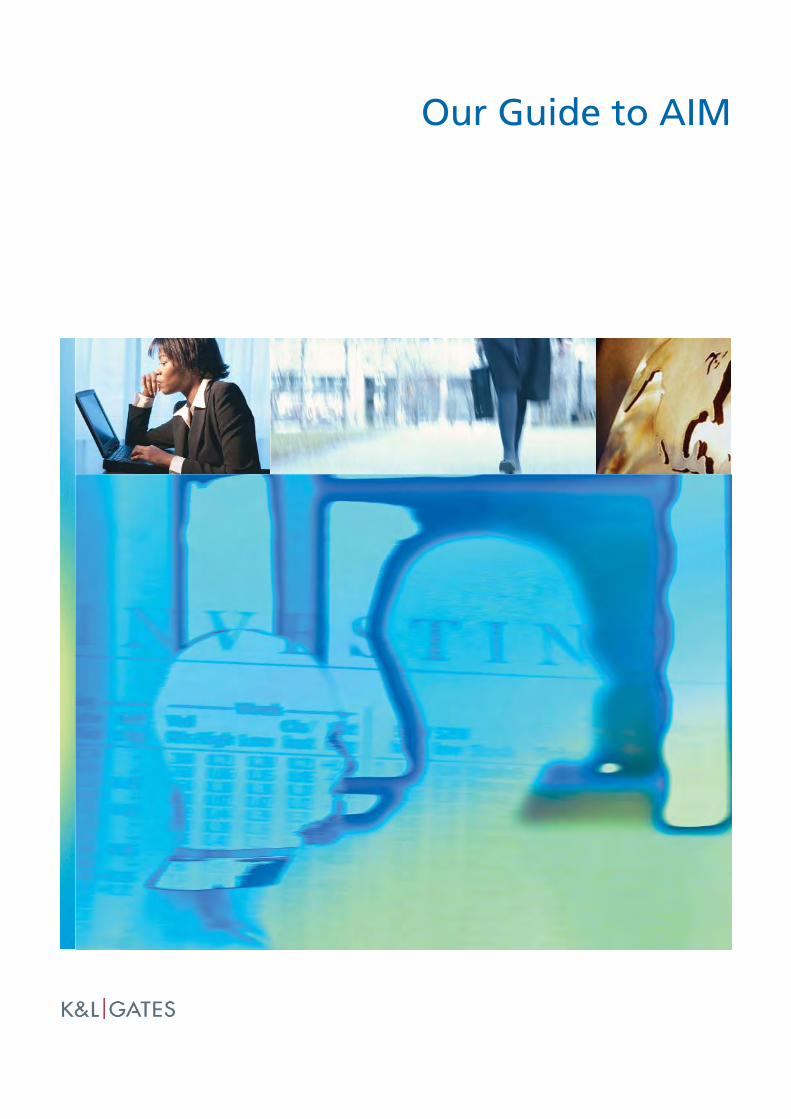

AiM investors rate

Piper Jaffray at the top

of UK brokers and #1

among U.S.-based

NOMADs

Strong reputation among UK institutional investors

Source: Investor Chronicles’ 2006 Annual Top 30 AiM Brokers

I would invest in I make time to read I would meet I get updates after Generally, I respect Overallits IPOs its research companies it floats I've invested this broker Score

Broker Country (max score: 5) (max score: 5) (max score: 5) (max score: 5) (max score: 5) (max score: 5)

Investec South Africa 4.2 4.8 4.7 4.3 4.5 4.50ABN Amro Netherlands 4.0 4.5 4.5 4.5 4.8 4.46Brewin Dolphin United Kingdom 4.2 4.2 4.4 4.4 4.2 4.28Panmure Gordon United Kingdom 3.8 4.2 4.2 4.0 4.3 4.10Bridgewell Securities United Kingdom 3.5 4.4 4.2 4.2 4.2 4.10Piper Jaffray United States 4.0 4.0 4.3 4.0 4.0 4.06KBC Peel Hunt Belgium 4.0 4.0 4.2 3.8 3.8 3.96Arden Partners United Kingdom 3.6 4.3 3.8 4.0 3.8 3.90Altium Capital United Kingdom 3.2 4.0 3.6 4.0 3.7 3.70Code Securities United Kingdom 3.6 4.0 3.8 3.4 3.4 3.64Oriel Securities United Kingdom 3.3 3.6 3.3 3.5 3.5 3.44Numis Securities United Kingdom 3.2 3.7 3.5 3.2 3.2 3.36Collins Stewart United Kingdom 3.7 3.0 3.5 3.3 3.0 3.30Noble & Co United Kingdom 3.3 2.2 3.3 3.3 3.3 3.08Shore Capital 3.0 3.8 3.0 2.8 2.8 3.08Rowan Dartington United Kingdom 2.6 3.2 3.4 3.0 3.0 3.04Arbuthnot Securities United Kingdom 2.4 3.2 2.8 3.3 2.8 2.90Williams de Broe United Kingdom 2.4 2.8 3.0 3.0 2.8 2.80Evolution Securities United Kingdom 2.8 2.7 3.2 2.5 2.7 2.78Canaccord Adams Canada 3.0 2.8 2.8 2.5 2.5 2.72Seymour Pierce United Kingdom 2.7 3.0 3.0 2.3 2.5 2.70Cenkos Securities United Kingdom 3.3 1.7 3.0 2.7 2.7 2.68Teather & Greenwood Iceland 2.8 2.8 2.8 2.4 2.6 2.68WH Ireland United Kingdom 2.3 3.3 2.0 2.3 3.0 2.58

Charles Stanley United Kingdom 2.7 2.5 2.6 2.5 2.2 2.50Corporate Synergy United Kingdom 2.0 2.5 2.5 2.7 2.3 2.40Ambrian Partners United Kingdom 1.7 2.0 2.0 3.0 3.0 2.34Libertas Capital United Kingdom 2.3 2.3 2.7 2.3 2.0 2.32Daniel Stewart & Co United Kingdom 1.8 1.7 2.0 2.3 1.7 1.90JM Finn United Kingdom 1.5 2.3 1.8 1.5 1.5 1.72

2006 Annual Top 30 AiM Brokers

United Kingdom

45

Retained corporate advisory/broking clients

*As of 26 Sept, 2007

Company Listing Mkt. Cap*

AGI Therapeutics AIM £103m

Alizyme Full £155m

Antisoma Full £155m

Ardana Full £60m

Ark Therapeutics Full £198m

Axis-Shield Full £136m

Biocompatibles Full £66m

BTG Full £150m

Corin Group Full £258m

Genetix Group AIM £42m

Inion Full £30m

Intercytex Group AIM £44m

Macro 4 Full £44m

ProStrakan Group Full £136m

Protherics Full £159m

Sinclair Pharma Full £78m

SkyePharma Full £143m

Spacelabs AIM £53m

Vectura Group Full £224m

Vernalis Full £134m

xG Technology AiM £1,010m

Leading execution capabilities in Europe*

US $25,800,000

acquired Applied Imaging Corp.

November 2006

US $9,000,000

has acquiredproducts from

Cellegy Pharma

November 2006

£11,000,000

Vendor Placing &Open Offer

September 2006

CHF 88,500,000

Initial Public Offering

November 2006

US $25,000,000

has acquiredMacroMed

December 2006

CHF 370,000,000

Rights Issue

March 2007

£12,000,000

Vendor Placing

May 2007

£120,000,000

Transfer to Full List

April 2007

CHF 136,875,000

Initial Public Offering

May 2007

£14,500,000

Vendor Placing

December 2006

£26,300,000

Vendor Placing

December 2006

£38,200,000

Vendor Placing &Open Offer

December 2006

Undisclosed

has soldmajority stake to

January 2007

€129,700,000

Rights Issue

February 2007

EUR 40,000,000

Initial Public Offering

March 2007

£131,000,000

has acquired

January 2007

DKK 64,000,000

Cash Placing

February 2007

NOMAD and Financial Advisor

Sept 2007

€655,000,000Value N/D

Disposable of it Subsidiary

February 2006

£231,000,000

April 2006

Recommended offer by Golden Gate Capital

Management buy out and sale to Carlyle Group

May 2006

Acquisition Of

Value N/D

January 2006

£11,300,000

Vendor Placing

July 2006

£11,300,000

Vendor Placing

July 2006

£11,300,000

Vendor Placing

July 2006

£11,300,000

Vendor Placing

July 2006

£11,300,000

Vendor Placing

July 2006

Since the start of

2006, we have

completed 21 capital

raisings, amounting

to over US$1.25bn

In the same period,

our European team

has also been

engaged in executing

21 M&A deals,

amounting to c.$5bn

* Based on deals completed by European Investment Banking team members

46

www.abchurch-group.com100 Cannon Street, London, EC4N 6EU Tel: 020 7398 7700 Fax: 020 7398 7799

West One, Wellington Street, Leeds LS1 1BA Tel: 0113 203 1340 Fax: 0870 762 7015

Heather Salmond, Director

An IPO is a one-off opportunity to raise significant funds and also to

really put your business on the map

47

Recent IPOs & Placings

IPO1 June 2007£25m Placing

£110m mkt cap

IPO13 Dec 2006

US$40m PlacingUS$120m mkt cap

IPO30 March 2006£120m Placing£321m mkt cap

IPO06 Aug 2007

£7.5m Placing£27.6m mkt cap

IPO07 Sept 2006£3.8m Placing£20m mkt cap

IPO26 Oct 2006£7m Placing

£29.5m mkt cap

IPO05 Dec 2006

£1.5m Placing£13.55m mkt cap

IPO06 Dec 2006

£0.5m Placing£25m mkt cap

IPO28 March 2007£7.5m Placing

£17.6m mkt cap

IPO21 June 2007£32m Placing

£171m mkt cap

IPO13 Aug 2007£75m Placing

£204m mkt cap

10 May 2007£279m Placing

N.B. Market caps shown are at time of Listing

IPO01 Nov 2006

£2.5m Placing£31.7m mkt cap

4 April 2007£43.7m Placing

IPO12 Dec 2006

£600,000 Placing£10m mkt cap

48

Communication objective

Investment in PR / IR & marketing

Retail & institutional

demand

Greater awareness

More partners & customers

Share price reflects true

value

Investor interest

Commercial benefits

Increased revenues

Your target audiences

Analysts

Media

Customers

Employees

Trade partners

RetailInvestors

InstitutionalInvestors

Private ClientBrokers

Company

49

Photo shoot Website content

Presentation preparation

IPO communications process

Comms tool kit

Announcement weekend

Monday media coverage

Release and Pathfinder prospectus

Follow up in trade and B2B

Marketing

Information infrastructure

Analyst meetings

10 day announcement

(AIM only)

Pricing / impact day release (Official List only)

First day of dealings

LSE Welcome

After market

Target profiling

Market columns

Private client broker meetings

Corporate and financial PR

IR

B2B and trade PR

Q&As FAQs

spokes-persons

notes to editors

photojournalism

commstraining

issues-management

key messages descriptor

define audiences

Preparation

50

Photojournalism

Quality CoverageCity AM

Daily Express

Independent

Daily Telegraph

Shares

51

Photo shoot Website content

Presentation preparation

IPO communications process

Comms tool kit

Announcement weekend

Monday media coverage

Release and Pathfinder prospectus

Follow up in trade and B2B

Marketing

Information infrastructure

Analyst meetings

10 day announcement

(AIM only)

Pricing / impact day release (Official List only)

First day of dealings

LSE Welcome

After market

Target profiling

Market columns

Private client broker meetings

Corporate and financial PR

IR

B2B and trade PR

Business broadcast

52

An IPO is just the beginning…

Maintain momentum

Refresh Communications Tool KitUpdate Report Medicsight/Abchurch meeting

Media interviews surrounding announcement

One-on-one analyst meetings (w/c 3 December)

Shareholder register analysis report

Trading update

December

Update Report

Medicsight/Abchurch meeting

Media site vistShareholder register analysis report

Website reviewNovember

Medicsight at China CCR annual (Oct)

Medicsight/ Toshiba CTC training day at JDDW (Oct)

Medicsight ColonCAD/ clinical presentation at Boston (Oct)

Update Report Medicsight/Abchurch meeting

Media interviews surrounding announcement

Shareholder register analysis report

Peer Group analysis

Ongoing updates to IR website

Private Client Broker meeting

Contract announcement

Q3 Results

October

Update Report

Medicsight/Abchurch meeting

Analyst feedback report

Analyst site visit

Analyst feedback reportSeptember

Features:•Pharma – Medical DevicesEvents:•National Pharmacist Day - USA

Update Report

Medicsight/Abchurch meeting

Results preparation

Results evaluation report

Media briefings at results

Shareholder register analysis report

Website Review

Notice of results

Interim results

August

CPR / Speaking OpsClient managementFinancial PR/ Media Relations

Investor RelationsFinancial Calendar / RNS

53

Ongoing PR

£15M contract win

SharesInvestors Chronicle

Shares

Interims

Shares and Investors Chronicle

£50M

contract win

Bloomberg: stocks towatch in

2005

IPO of the Year

Award

Samsung contract win

DailyMail

£8M contract win

£25M contract win

AGM

AIM & Ofex

Investing for Growth

Hyundai contract win

£29M, two contracts

Interims

Site Visit£20M contract win DSME

Share price performance for Hamworthy

£13M contract win

£15M contract win

Acquisition of Serck

£15M contract win

Interims

Issuesmanagement

Comprehensive investor relations offering

B2B & T&T PR

Contribution to full

marketing mix

Major transaction/ M&A capability

Value add

International reach, IPREX

/ Northern region

Core corporate

& financial

programme

54

www.abchurch-group.com100 Cannon Street, London, EC4N 6EU Tel: 020 7398 7700 Fax: 020 7398 7799

West One, Wellington Street, Leeds LS1 1BA Tel: 0113 203 1340 Fax: 0870 762 7015

4 October 2007 London Bridge Capital

London Bridge Capital

Corporate Finance AdvisoryFund managementTrading / Brokerage servicesNot a NomAd / Broker

4 October 2007 London Bridge Capital 108

We exclusively offer financial and strategic advice to companies operating in the cleantech sector.

Our Advisers have brought 5 major West Coast companies to market:Gatekeeper (CA)HaloSource (WA)Libra Natural Resources (WA)Prometheus Energy (WA)Solar Integrated Technologies (CA)

55

4 October 2007 London Bridge Capital4 October 2007 London Bridge Capital 109

The London Edge - a ‘cluster’

London / UK plc – the place to do business

Government and trade body support for your business, whether UK-based planning to go global, or outside the UK wanting to invest here

World’s leading capital markets

The London Stock Exchange markets –providing the financial platform that supports your strategic ambitions

A specialist financial network

Corporate finance, lawyers, fund managers, investor & public relations, accountancy

London continues to hold the deepest pool of Europe’s capital.

4 October 2007 London Bridge Capital4 October 2007 London Bridge Capital 110

The London IPO: Money and Study

In 2006:541 companies joined our markets raising £28bn

Main Market £20bn; AIM £8bn346 IPOs took place

More than all of Western Europe combinedMore than NASDAQ, NYSE and Hong Kong combined

The overall cost of Capital on London’s Public markets is considerably less than in the US

33% more efficient IPO pricing (less discounting)

Underwriting fees are some 50% less

56

4 October 2007 London Bridge Capital4 October 2007 London Bridge Capital 111

Your IPO

The directors of the issuer

Major shareholders

Sponsor / Nominated Adviser

Broker

Research Analyst

Lawyers – for company and

underwriters

Experts

Reporting accountants

Public relations adviser

With all that’s going on for your IPO, it can seem pretty daunting...

Our US/Canadian clientele want someone to manage, to negotiate, and to facilitate the process on site and in situ.

4 October 2007 London Bridge Capital4 October 2007 London Bridge Capital 112

Determining your valueBottom-up: business fundamentalsMarket characteristics (size, growth, etc)Risk factors

Discounted Cash FlowApplication

Combine assumptions with well known valuation tools:

Peer GroupEV/Sales, EV/EBITDA, P/ELast VC round Invested capital to date

Valuation Remember…Be realistic Have a contingency

plan

57

4 October 2007 London Bridge Capital4 October 2007 London Bridge Capital 113

Current Market ConditionsInvestors are:

More selectiveSome are closed off to early -stage companies

What you need:Revenues, contracts – an order bookAttractive valuation (risk/return)Market cap and liquidity cannot be overstated enough

This has raised the bar for IPOs

But deals are still getting doneGreen IPOs so far in 2007 raising at least £20m of new money

Applied Intellectual Capital Modern WaterPlanticTechnologiesPV CrystaloxSolarVECTRIX

Success for unique or establishedbusiness models at realisticvaluations

4 October 2007 London Bridge Capital

Corporate Finance

Contacts:

Peter Greensmith, CEO; [email protected] Finston, MD; [email protected] Munro, Senior VP; [email protected]

London Bridge CapitalLevel 2 - City Tower40 Basinghall StreetLondon, UKEC2V 5DE+44 (0) 207 877 5040

4 October 2007 London Bridge Capital 114

58

4 October 2007 London Bridge Capital4 October 2007 London Bridge Capital 115

APPENDIX 1: Environmental industries - the energy case

£ Millions raised at IPO combined AiM & Main for Alternative Energy Companies.

Questions and Answers

Richard Webster-Smith is responsible for the London Stock Exchange’s International Business Development activities in the USA and Canada. He plays an integral role in building and maintaining the Exchange’s profile and presence in the adviser communities in London and the finance centres of North America, focusing on attracting international companies to the London markets. Richard was previously in charge of media relations for the Exchange’s AIM market, and has also worked in the Exchange’s Public Affairs team where he worked on both UK and EU public policy issues. He joined the Exchange in 2000. +44 (0)20 7797 1058 [email protected] The London Stock Exchange is one of the world’s oldest stock exchanges and can trace its history back more than 300 years. Starting life in the coffee houses of 17th century London, the Exchange quickly grew to become the City’s most important financial institution. Today, The London Stock Exchange is at the heart of global financial markets and is home to some of the best companies in the world. The aim of the exchange is to compete in the global market for financial transaction services to become the supplier of choice – providing customers with the most efficient, trusted and reliable services, and shareholders with the most successful exchange business.

Jeremy Landau is a partner in the firm’s Corporate, Private Equity, AIM, and Telecom, Media and Technology practice groups. He has particular experience in advising both public and private companies on their corporate and commercial transactions and requirements in a broad range of sectors, with particular emphasis on the Technology and Telecommunications, Life Sciences, Leisure and Retail sectors, including dealing with domestic and cross border mergers & acquisitions, disposals, private equity and corporate finance transactions. In particular, Mr. Landau has a wealth of experience of advising companies (both domestic and international), as well as investment banks on IPOs and fundraisings on the London Stock Exchanges' Full List and AIM markets. Mr. Landau is also listed in Chambers Guide to the Legal Profession as a leading lawyer in relation to Technology/Telecoms transactions. +44 (0)20 7360 8114 [email protected] K&L Gates comprises approximately 1,400 lawyers located in 22 offices on three continents. The firm represents capital markets participants and leading global corporations, growth and middle-market companies, and entrepreneurs in every major industry group as well as public sector entities, educational institutions and philanthropic organizations. The firm’s practice is at once regional, national and international in scope, cutting edge, complex, and dynamic. K&L Gates lawyers are experienced in serving clients’ corporate legal needs, from general business planning to highly specialized and critical emergency matters. The firm serves as general or special legal advisors to many public and privately-held companies, as well as partnerships, formal and informal strategic alliances and joint ventures. In providing a full range of corporate services, K&L Gates is focused on working with clients to solve problems and achieve their objectives in the most efficient, effective and time-sensitive manner. The firm’s practice expertise includes corporate governance, transactions, with all of the ancillary practice capabilities, finance, real estate, bankruptcy and restructuring, securities and private equity and venture capital.