pemex hr a- (g) - mexican stock exchange · pemex transformación industrial, pemex perforación y...

TRANSCRIPT

A NRSRO Rating*

Hoja 1 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

Twitter: @HRRATINGS

PEMEX Euro-denominated Notes

HR A- (G)

Corporates February 21, 2017

Ratings 4.875% Note due 2028 HR A- (G) 3.750% Note due 2024 HR A- (G) 2.500% Note due 2021 HR A- (G) Outlook Negative Contacts

José Luis Cano Vice-president Corporates / ABS [email protected]

Mariela Moreno Associate [email protected]

Luis Roberto Quintero Executive Director Corporates / ABS [email protected]

Definition The long term global rating assigned to the 4.875% Note due 2028, 3.750% Note due 2024 and 2.500% Note due 2021 is HR A- (G). This indicates that the issuer or issue with this rating offers acceptable safety for timely payment of debt obligations and maintains low credit risk on a global scale basis. The negative sign means a relative weakness into the assigned rate.

HR Ratings assigns the rating of HR A- (G) with negative outlook to three euro-denominated notes issued by PEMEX1 for a total amount of €4,250m.

The senior unsecured notes (Euro Notes), listed at the Luxembourg Stock Exchange, will have maturities of 4.5, 7 and 11 years. Each will pay annual interest at a predefined date and an obligatory full amortization upon maturity. The issued notes are part of PEMEX’s 2017 financing program. With this transaction, along with the pre-funding transaction of US$5.5Mm2 carried out in December 2016, the Company reported that it has achieved its minimum financing needs for 2017, however, it kept open the possibility to look for alternative debt sources in international markets. The rating assigned the Euro Notes is based on PEMEX’s long term global corporate rating of HR A- (G) with Negative Outlook, and is aligned with our sovereign rating for Mexico3. HR Ratings assumes that PEMEX’s debt enjoys a sovereign de facto status given its strategic importance for the Federal Government and the Mexican economy. The Federal Government has demonstrated its support for PEMEX by transferring to it funds for a total of P$73.5Mm in 20164. In addition, the Federal Government issued an IOU to Pemex for an additional P$134.2Mm to be amortized in favor of the Company as its pension obligations require. This support was used by PEMEX to provide liquidity and reduce financial obligations with its suppliers. We believe that PEMEX enjoys an adequate debt structure as 88.8% of its total debt at 3Q16 is long term vs. 86.6% a year earlier. Nevertheless, we expect net debt to grow as its Free Cash Flow (FCF5) continues to decline as a result of a lower EBITDA due to a falling but still substantially heavy tax burden, rising employee benefits, inefficiencies presented in PEMEX’s refineries and a persistent reduction in terms of oil production. This situation has been exacerbated due to a slower recovery in international crude oil prices; coupled with higher working capital requirements as a result of payments to suppliers and an increase in accounts receivables and inventories mainly due to higher export volumes. On the other hand, we estimate that over time PEMEX can strengthen its balance sheet by monetizing the value of alliances and associations with third parties made possible by the Energy Reform. In this context we note the increasing success of the auctions in recent months to obtain the rights to explore and develop oil fields. The Company should also benefit by changes in tax rules that should allow for a lower tax burden as well as Pemex’s efforts to improve its refinery operations. Although we expect Pemex’s tax burden to decline as a result of changes made by the Federal Government for this purpose, we estimate that the Company will continue to provide substantial revenues to the public sector. The notes are guaranteed by the following PEMEX subsidiaries: PEMEX Exploración y Producción, PEMEX Transformación Industrial, PEMEX Perforación y Servicios, PEMEX Logística and PEMEX Cogeneración y Servicios. The Company reported that the proceeds of the three issuances will be used to finance investment projects and for refinancing part of its debt. The main characteristics of the notes are shown in the below table.

1 Petróleos Mexicanos and/or PEMEX and/or the Company. 2 Mm= Thousands of Millions. 3 As per our report of December 22, 2016 ratifying the rating of A-(G) and changing the outlook from Stable to Negative. For more details please refer to the report published in www.hrratings.com. 4 The P$73.5Mm included amortization of a similar IOU issued for Pemex in 2015 originally for P$50Mm. 5 FCF = Cash generated by operating activities - Maintenance CAPEX + difference in FX accounts.

A NRSRO Rating*

Hoja 2 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

The factors that justify the assigned rating are:

Status of Sovereign Debt. PEMEX’s debt enjoys a sovereign status de facto because we consider that is a relevant income generator for the Mexican Federal Government and due to its importance to Mexico’s economy. The foregoing was confirmed by the contribution of P$73.5Mm made by the Federal Government to support the Company’s liquidity. Our rating is based on the assumption that the government will continue supporting the Company through capital injection or policies that will contribute to improve its financial and operative results.

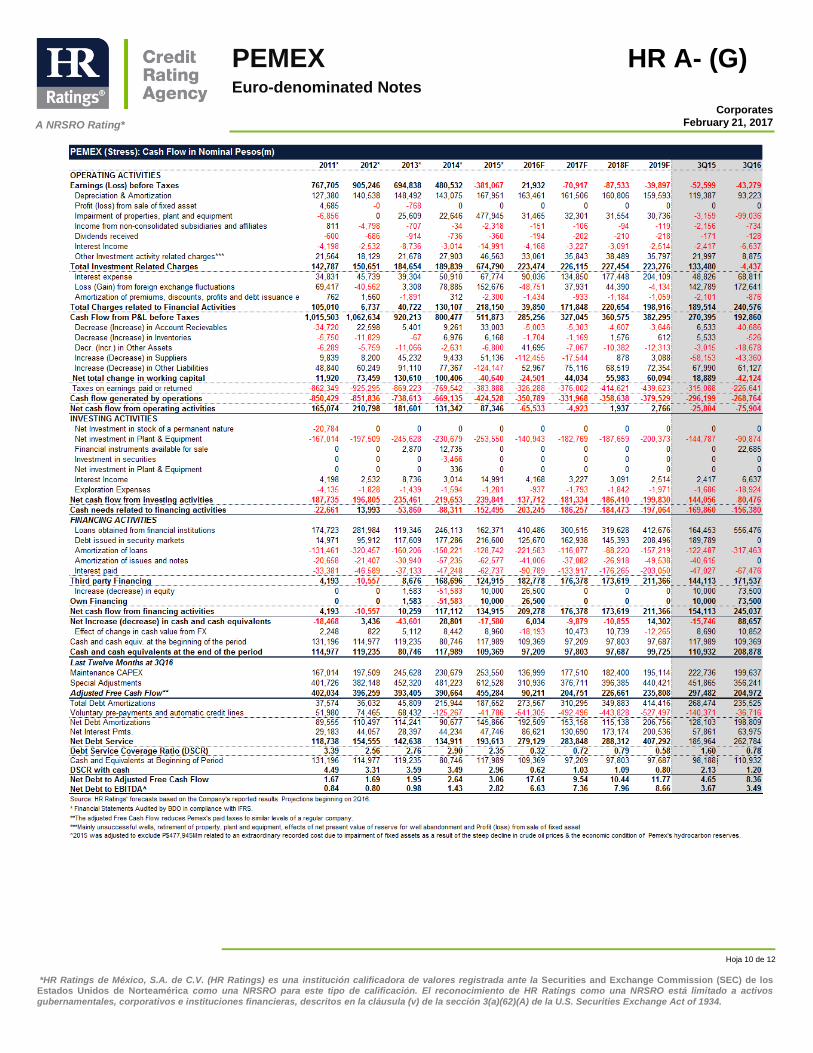

Healthy debt structure. Although the Company’s net debt increased by 23.0% by 3Q16, 88.6% of its total debt is long term (vs. 87.1% in 2015). This has helped reduce pressure on the Company’s liquidity, allowing it to cover its short term financial obligations and align its debt service to PEMEX’s business model.

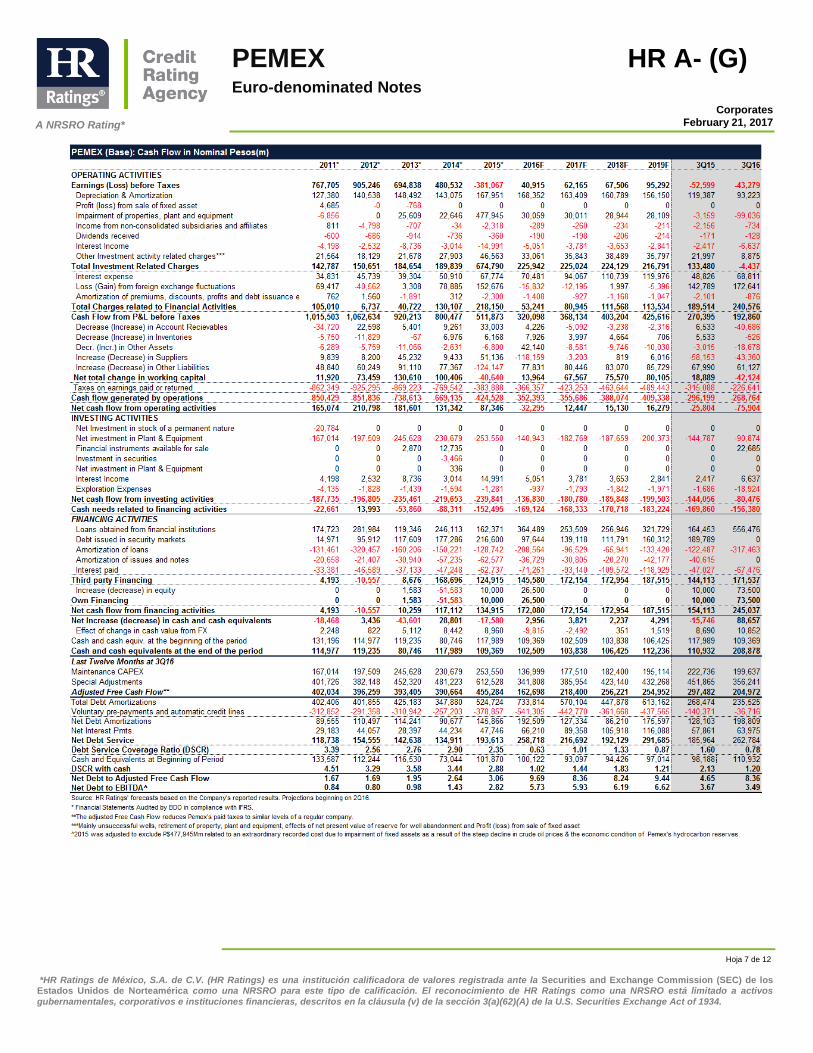

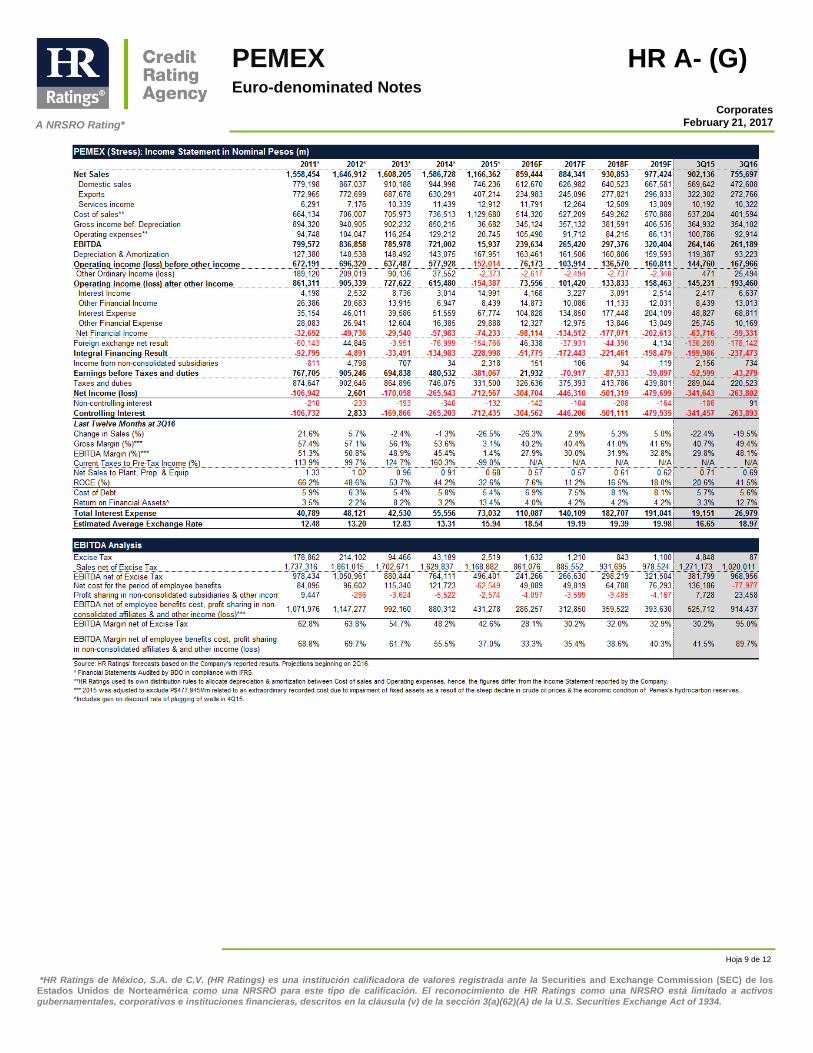

Reduction of Adjusted Free Cash Flow (AFCF6). During the LTM7 through 3Q16 we estimate that the Company generated an AFCF of P$205Mm, below our estimate for the same period through 3Q15 of P$298Mm. This is due to a lower EBITDA and a smaller generation of working capital. We are expecting this trend to continue in the medium term, but it could be reversed if the Company implements several of the initiatives it has announced: joint ventures, focusing on profitable segments, outsourcing its non-value added operations and the benefits derived from the reform of the mechanism to determine gasolines prices. This reform will allow domestic prices in Mexico to immediately reflect international prices.

Lower production of hydrocarbons. As a consequence of continued low international crude oil prices, limitations on investment spending and the presence of fractional water flow within productive fields, the Company’s LTM daily average production of crude fell 5.6%, reaching 2,138mbd vs. 2,266mbd LTM through 3T15. We expect that this situation will continue as a consequence of PEMEX’s still constrained financial situation. The declining trend could be reversed should the Company’s strategy be effectively executed and international oil prices recover.

Decrease of P$100Mm to achieve the established financial balance. As result of the decrease of the international crude oil prices, the Board of Directors of Petróleos Mexicanos and the Congress approved a reduction in expenditures of P$100Mm to PEMEX 2016 budget. At the moment of this report, the company has indicated that it has surpassed the requested reduction achieving a cut of P$106Mm. Although the reached decrease on costs, we expect that PEMEX will continue experiencing pressures on its financial results mainly due to current crude oil prices, investment restrictions, inefficiencies in its Industrial Transformation segment and its current high tax burden.

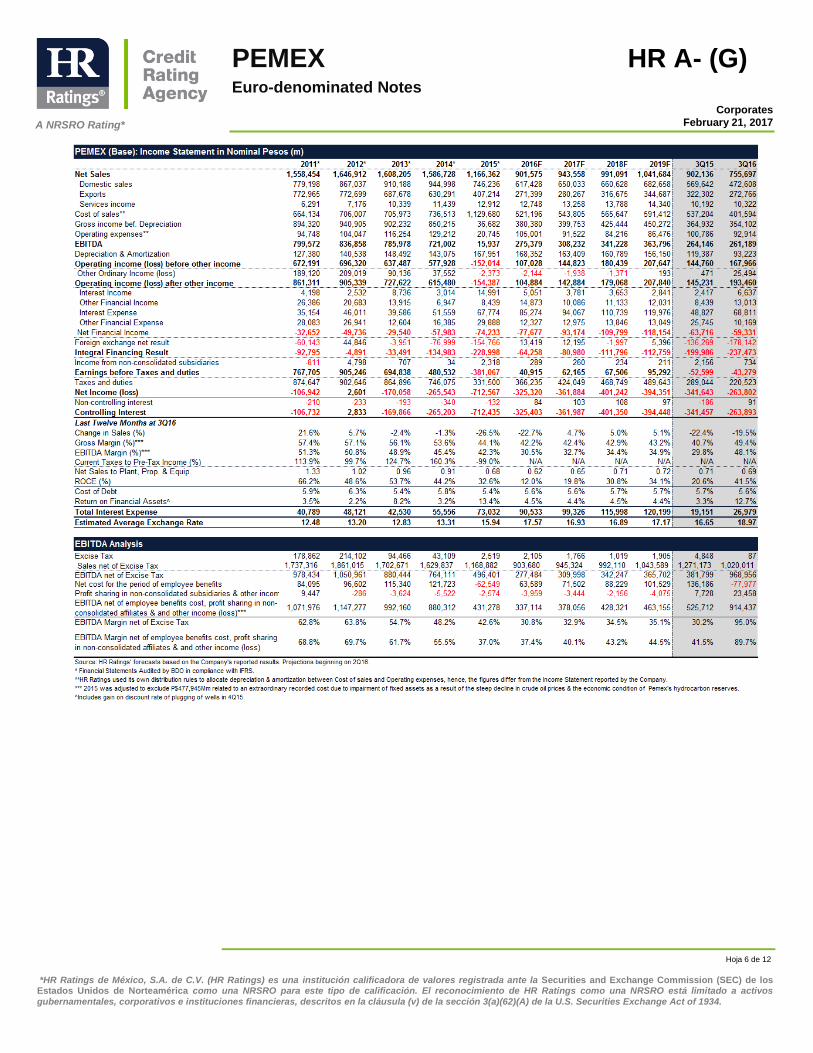

Despite a reduction in production levels by OPEC8, international crude oil prices continue depressed negatively impacting PEMEX’s revenues and EBITDA. During the first three quarters of 2016 EBITDA declined 1.1% in peso terms, reaching P$261Mm compared to P$264Mm at 3Q15. On the positive side, this shows Pemex’s ability to control costs as revenues fell a substantial 16.2% during the same three quarter period. The limited decline in EBITDA was also due to PEMEX’s stronger focus on profitable activities. Furthermore, observed EBITDA is 24.7% higher than our base scenario of P$210Mm

6 AFCF = the adjusted Free Cash Flow reduces Pemex's paid taxes to similar levels of a regular company. 7 LTM = Last Twelve Months 8 Organization of the Petroleum Exporting Countries

A NRSRO Rating*

Hoja 3 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

incorporated into our previous report, hence, we expect that the company could achieve our full year 2016 projections. Regardless of several cost control initiatives and efficiencies implemented by PEMEX in the past months, we consider that PEMEX will continue increasing its financial requirements since its adjusted free cash flow has continued to decline. This is due to a heavy tax burden and employees’ benefits, along with a natural decline of Cantarell’s production coupled with an increase in the fractional water flow of well and the austerity program implemented by PEMEX, which has diminished the investments in productive fields which are not profitable at current prices. Because of PEMEX’s deteriorated AFCF they have needed to fund their investment needs through debt. This explains a growth of 23.0% in its net debt reaching P$1,714Mm at 3Q16 vs. P$1,393Mm in 2015. Adjusting for the currency impact, we estimate that net debt increased 16.0%. It’s important to recall that EBITDA was impacted by lower domestic revenues, as a result of negative price variations over gasoline and diesel prices. Also, its operational inefficiencies presented at PEMEX´s refineries have impacted their EBITDA generation. Another reason why the AFCF has been impacted is due to an increase in accounts receivables and inventories mainly due to higher export volumes and the appreciation of the U.S. dollar against the Mexican peso and a partial payment of existing liabilities with suppliers. This reduction of liabilities with suppliers is in part due to an economic policy by the Federal Government aiming to reduce PEMEX’s impact over the Mexican Economy. Because of PEMEX’s elevated revenue contributions to the Federal Government, the Company has continued to adjust its operating expenses and investments to compensate its heavy tax burden. Due to PEMEX’s financial constraints they have delayed investments in exploration and production, as well as the revamping of its refineries. We estimate that the Company will improve its AFCF as the several actions and strategies based on the Energy Reform are enacted and as soon as it advances through the different Bids and Rounds of the Energy Reform, which will help them to source some of its projects with the integration of third party investors sharing the cost and the risk. Due to low international prices for crude oil, PEMEX has decided to work on specific fields based on their costs of extraction. Since current prices have been low, the Company has showed a declining trend in production averaging 2,138 MBPD in the 3Q16, representing a 5.6% decline vs. 2,266 MBPD in the 3Q15. Another factor that has impacted production is a higher presence of fractional flow of wells along with a reduction in Cantarell’s production. Due to a lower replacement rate of reservoirs PEMEX has experienced a reduction of years of proven reserves from 10.0 to 8.1 years. Despite the observed production levels, we consider that PEMEX continues having a solid presence in the global oil market maintaining the 8th position9 among the main crude producers worldwide. Because of low crude oil prices, PEMEX has focused on improving the balance between domestic sales and exports, pursuing a more profitable mix. Due to the current situation, the Company has increased its proportion of exports from its total revenues representing 36.1% at 3Q16, vs. 35.7% at 3Q15. Based on the changes that the mix between exports and domestic consumption experienced, exports represented P$273Mm at 3Q16 (vs. P$473Mm domestic revenues.

9 Petroleum Intelligence Weekly (PIW) 2015, The World’s Top 50 Oil Companies.

A NRSRO Rating*

Hoja 4 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

Since September of 2016 crude oil prices have experienced a slight recovery moving from US$37.76 per barrel September 2016 to US$45.34 in February 2017. If this trend were to prevail in the following quarters, we estimate that PEMEX’s situation will improve if they are able to adequately control costs of sales. Another factor to consider in the future is the fact that the Company will face further competition due to the liberalization of gasoline and gas prices through the arrival of other companies. The manner in which PEMEX is able to balance this changing environment will prove fundamental for its AFCF generation. As a consequence of the observed AFCF the Company required further financial resources, therefore increasing its years of payment to Adjusted Free Cash Flow to 8.4 years vs. 4.7 years at 3Q15. However, PEMEX’s adequate debt structure has allowed them to reach DSCR levels with cash above 1.0x. These ratios have kept falling due to PEMEX’s overall situation which has translated into lower levels of AFCF. Despite, this, the Company has reported that it has already achieved its minimum financing needs for 2017, however, it expressed the possibility to access again international debt markets looking for alternatives to source its monetary requirements, maintain its credit lines available, stay present in key markets, develop financing sources or to partially pre-fund its 2018 needs. HR Ratings will continue to monitor the Company’s operations in the future in order to verify if they are capable to achieve higher EBITDA levels based on higher crude oil prices, while improving their years of payment and DSCR levels. The present notes also received the following long term ratings: BBB+ by Standard & Poors Global Rating Services, BBB+ by Fitch Ratings and Baa3 by Moody’s Investors Service. Additionally, the issuer (PEMEX) has a Negative Outlook assigned by each of the three above mentioned Rating Companies.

A NRSRO Rating*

Hoja 5 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

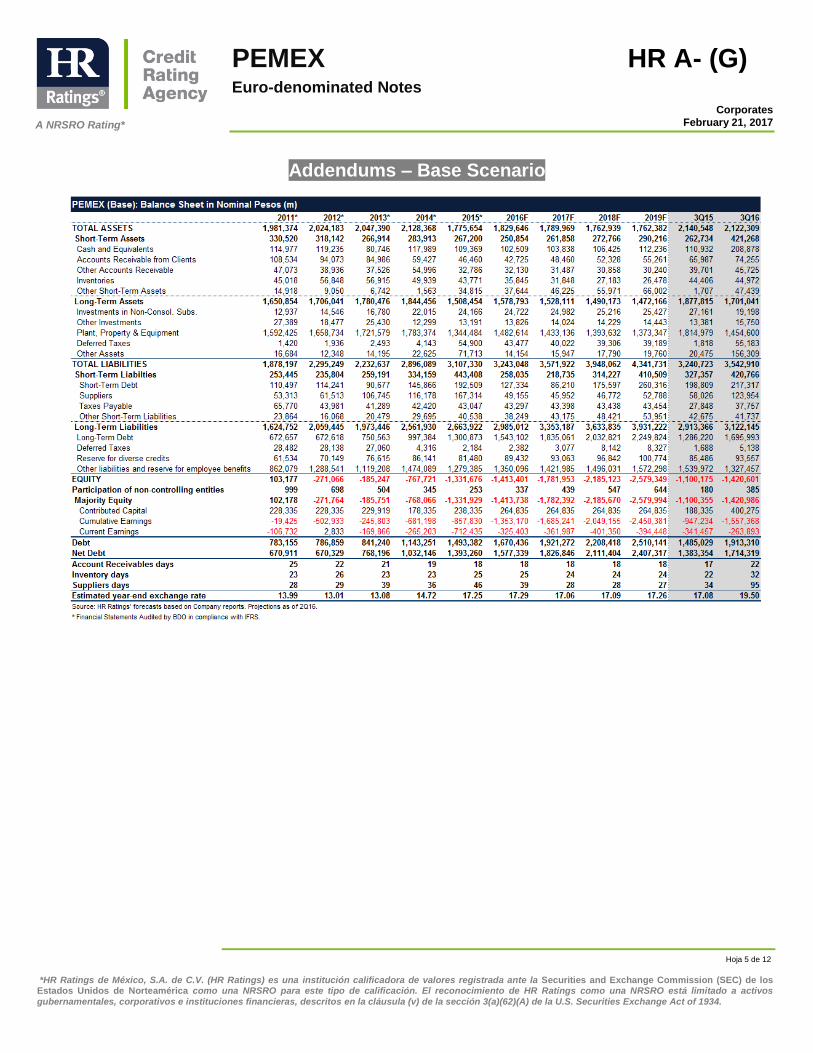

Addendums – Base Scenario

A NRSRO Rating*

Hoja 6 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

A NRSRO Rating*

Hoja 7 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

A NRSRO Rating*

Hoja 8 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

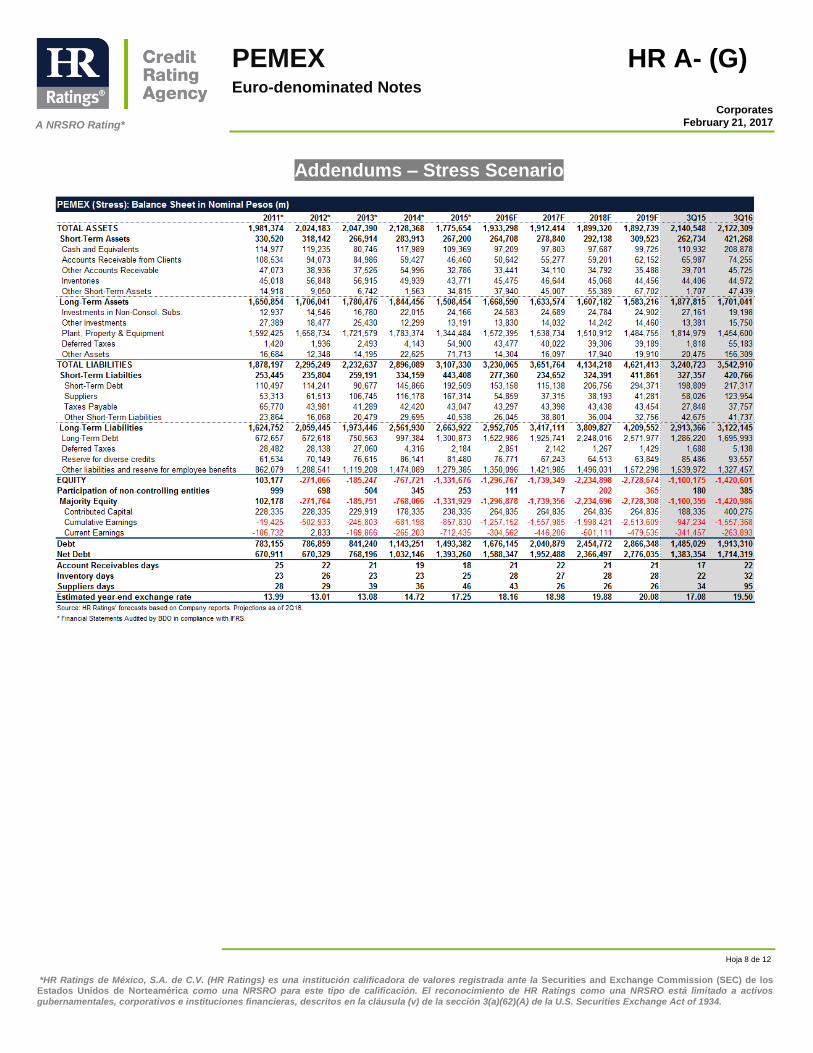

Addendums – Stress Scenario

A NRSRO Rating*

Hoja 9 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

A NRSRO Rating*

Hoja 10 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

A NRSRO Rating*

Hoja 11 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

HR Ratings Senior Management

Management

Chairman of the Board

Vice- President

Alberto I. Ramos +52 55 1500 3130 Aníbal Habeica +52 55 1500 3130

[email protected] [email protected]

Chief Executive Officer

Fernando Montes de Oca +52 55 1500 3130

Analysis

Chief Credit Officer

Chief Operating Officer

Felix Boni +52 55 1500 3133 Álvaro Rangel +52 55 8647 3835

Public Finance / Infrastructure Financial Institutions / ABS

Ricardo Gallegos +52 55 1500 3139 Fernando Sandoval +52 55 1253 6546

Roberto Ballinez +52 55 1500 3143 [email protected]

Corporates / ABS

Methodologies

Luis Quintero +52 55 1500 3146 Karla Rivas +52 55 1500 0762

[email protected] [email protected]

José Luis Cano +52 55 1500 0763

Regulation

Chief Risk Officer

Head Compliance Officer

Rogelio Argüelles +52 181 8187 9309 Laura Mariscal +52 55 1500 0761

[email protected] [email protected]

Rafael Colado +52 55 1500 3817

Business Development

Business Development

Francisco Valle +52 55 1500 3134

A NRSRO Rating*

Hoja 12 de 12

*HR Ratings de México, S.A. de C.V. (HR Ratings) es una institución calificadora de valores registrada ante la Securities and Exchange Commission (SEC) de los Estados Unidos de Norteamérica como una NRSRO para este tipo de calificación. El reconocimiento de HR Ratings como una NRSRO está limitado a activos

gubernamentales, corporativos e instituciones financieras, descritos en la cláusula (v) de la sección 3(a)(62)(A) de la U.S. Securities Exchange Act of 1934.

PEMEX Euro-denominated Notes

HR A- (G)

Corporates

February 21, 2017

Mexico: Avenida Prolongación Paseo de la Reforma #1015 torre A, piso 3, Col. Santa Fe, México, D.F., CP 01210, Tel 52 (55) 1500 3130. United States: One World Trade Center, Suite 8500, New York, New York, ZIP Code 10007, Tel +1 (212) 220 5735.

Complementary information in accordance with section V, paragraph A) of Annex 1 of the General Provisions applicable to Credit Rating Agencies.

Previous Rating. Initial

Date of the last Rating Action. Initial

Period of the financial information used by HR Ratings for the assignment of the current rating.

1st Quarter 2011 to 3rd Quarter 2016

Main sources of information used, including third parties. Internal financial and operational report published by the Company, final term sheet of the notes, presentations issued by the Company and Audited financial of BOD.

Ratings assigned by other rating agencies that were used by HR Ratings (if so). NA

HR Ratings considered at the moment of assigning or reviewing the rating, the existence of mechanisms designed to align the incentives between the originator, servicer and guarantor and the possible buyers of the rated instrument (where it applies).

NA

HR Ratings de México, S.A. de C.V. (HR Ratings), is a Credit Rating Agency authorized by the National Banking and Securities Commission (CNBV), registered by the Securities and Exchange Commission (SEC) as a Nationally Recognized Statistical Rating Organization (NRSRO) for the assets of government securities, corporates and financial institutions, as described in clause (v) of section 3(a)(62)(A) of the US Securities Exchange Act of 1934 and certified as Credit Rating Agency (CRA) by the European Securities and Markets Authority (ESMA).

The rating was solicited by the entity or issuer, or on its behalf, and therefore, HR Ratings has received the corresponding fees for the rating services provided. The following information can be found on our website at www.hrratings.com: (i) The internal procedures for the monitoring and surveillance of our ratings and the periodicity with which they are formally updated, (ii) the criteria used by HR Ratings for the withdrawal or suspension of the maintenance of a rating, and (iii) the procedure and process of voting on our Analysis Committee. HR Ratings de México SA de CV (HR Ratings) ratings and/or opinions are opinions of credit quality and/or regarding the ability of management to administer assets; or opinions regarding the efficacy of activities to meet the nature or purpose of the business on the part of issuers, other entities or sectors, and are based exclusively on the characteristics of the entity, issuer or operation, independent of any activity or business that exists between HR Ratings and the entity or issuer. The ratings and/or opinions assigned are issued on behalf of HR Ratings, not of its management or technical staff, and do not constitute an investment recommendation to buy, sell, or hold any instrument nor to perform any business, investment or other operation. The assigned ratings and/or opinions issued may be subject to updates at any time, in accordance with HR Ratings’ methodologies. HR Ratings bases its ratings and/or opinions on information obtained from sources that are believed to be accurate and reliable. HR Ratings, however, does not validate, guarantee or certify the accuracy, correctness or completeness of any information and is not responsible for any errors or omissions or for results obtained from the use of such information. Most issuers of debt securities rated by HR Ratings have paid a fee for the credit rating based on the amount and type of debt issued. The degree of creditworthiness of an issue or issuer, opinions regarding asset manager quality or ratings related to an entity’s performance of its business purpose are subject to change, which can produce a rating upgrade or downgrade, without implying any responsibility for HR Ratings. The ratings issued by HR Ratings are assigned in an ethical manner, in accordance with healthy market practices and in compliance with applicable regulations found on the www.hrratings.com rating agency webpage. There Code of Conduct, HR Ratings’ rating methodologies, rating criteria and current ratings can also be found on the website. Ratings and/or opinions assigned by HR Ratings are based on an analysis of the creditworthiness of an entity, issue or issuer, and do not necessarily imply a statistical likelihood of default, HR Ratings defines as the inability or unwillingness to satisfy the contractually stipulated payment terms of an obligation, such that creditors and/or bondholders are forced to take action in order to recover their investment or to restructure the debt due to a situation of stress faced by the debtor. Without disregard to the aforementioned point, in order to validate our ratings, our methodologies consider stress scenarios as a complement to the analysis derived from a base case scenario. The rating fee that HR Ratings receives from issuers generally ranges from US$1,000 to US$1,000,000 (or the foreign currency equivalent) per issue. In some instances, HR Ratings will rate all or some of the issues of a particular issuer for an annual fee. It is estimated that the annual fees range from US$5,000 to US$2,000,00 (or the foreign currency equivalent).

The rating assigned by HR Ratings de México, S.A. de C.V. to the entity, issuer and/or issue is based upon the analysis performed under a base case and stress case scenario, in accordance with the following methodology(ies) established by the rating agency: Corporate Debt Credit Risk Evaluation, May 2014 General Methodological Criteria, January 2017 For more information with respect to this (these) methodology (ies), please consult the website:

www.hrratings.com/en/methodology