penta clo 9 dac

TRANSCRIPT

Presale:

Penta CLO 9 DACJuly 6, 2021

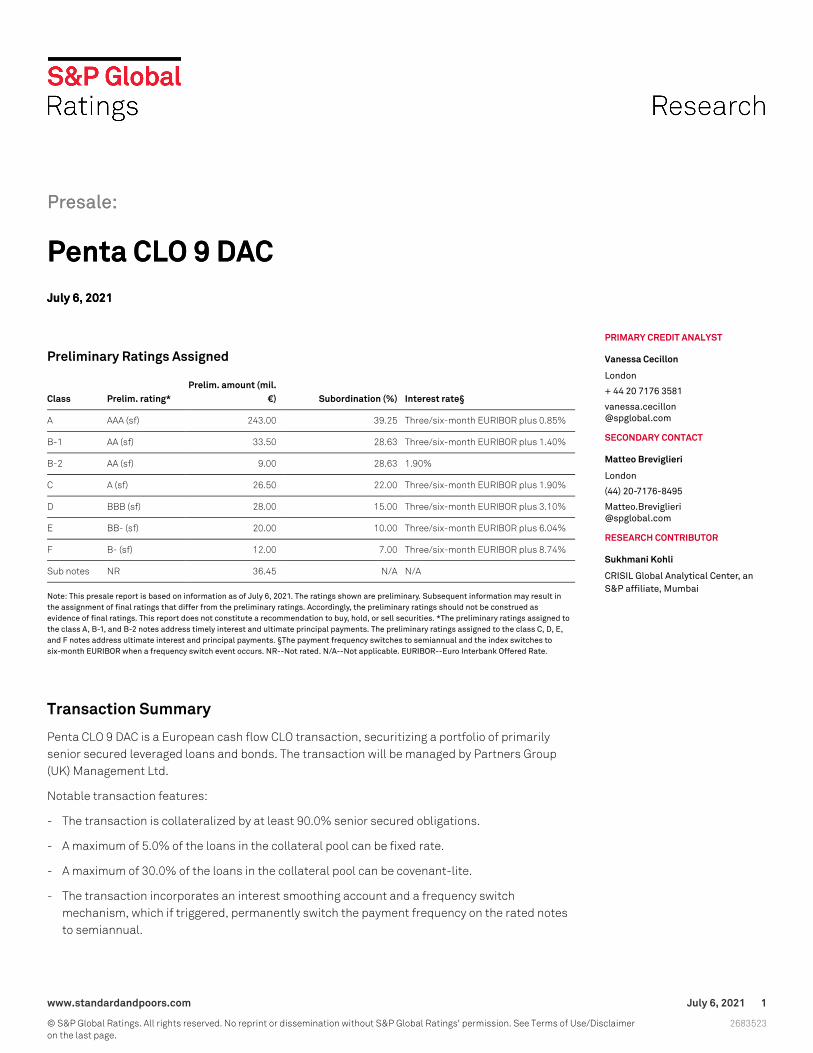

Preliminary Ratings Assigned

Class Prelim. rating*Prelim. amount (mil.

€) Subordination (%) Interest rate§

A AAA (sf) 243.00 39.25 Three/six-month EURIBOR plus 0.85%

B-1 AA (sf) 33.50 28.63 Three/six-month EURIBOR plus 1.40%

B-2 AA (sf) 9.00 28.63 1.90%

C A (sf) 26.50 22.00 Three/six-month EURIBOR plus 1.90%

D BBB (sf) 28.00 15.00 Three/six-month EURIBOR plus 3.10%

E BB- (sf) 20.00 10.00 Three/six-month EURIBOR plus 6.04%

F B- (sf) 12.00 7.00 Three/six-month EURIBOR plus 8.74%

Sub notes NR 36.45 N/A N/A

Note: This presale report is based on information as of July 6, 2021. The ratings shown are preliminary. Subsequent information may result inthe assignment of final ratings that differ from the preliminary ratings. Accordingly, the preliminary ratings should not be construed asevidence of final ratings. This report does not constitute a recommendation to buy, hold, or sell securities. *The preliminary ratings assigned tothe class A, B-1, and B-2 notes address timely interest and ultimate principal payments. The preliminary ratings assigned to the class C, D, E,and F notes address ultimate interest and principal payments. §The payment frequency switches to semiannual and the index switches tosix-month EURIBOR when a frequency switch event occurs. NR--Not rated. N/A--Not applicable. EURIBOR--Euro Interbank Offered Rate.

Transaction Summary

Penta CLO 9 DAC is a European cash flow CLO transaction, securitizing a portfolio of primarilysenior secured leveraged loans and bonds. The transaction will be managed by Partners Group(UK) Management Ltd.

Notable transaction features:

- The transaction is collateralized by at least 90.0% senior secured obligations.

- A maximum of 5.0% of the loans in the collateral pool can be fixed rate.

- A maximum of 30.0% of the loans in the collateral pool can be covenant-lite.

- The transaction incorporates an interest smoothing account and a frequency switchmechanism, which if triggered, permanently switch the payment frequency on the rated notesto semiannual.

Presale:

Penta CLO 9 DACJuly 6, 2021

PRIMARY CREDIT ANALYST

Vanessa Cecillon

London

+ 44 20 7176 3581

SECONDARY CONTACT

Matteo Breviglieri

London

(44) 20-7176-8495

RESEARCH CONTRIBUTOR

Sukhmani Kohli

CRISIL Global Analytical Center, anS&P affiliate, Mumbai

www.standardandpoors.com July 6, 2021 1

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Key Credit Metrics

Selected Credit Metrics

Total leverage (x)* 10.2

Weighted-average cost of debt (%)§ 1.70

Subordination ('AAA') (%) 39.25

Modeled WAS (%) 3.55

Modeled WAC (%) 4.00

Excess spread (%)† 1.87

SDR ('AAA') (%) 64.66

Modelled weighted-average portfolio recovery ('AAA') (%) 35.39

*Total debt/equity. §Spread over EURIBOR for all classes, excluding the subordinated notes. †WAS (calculated on the assumptions of 95.0% ofthe portfolio as floating-rate assets with 3.55% spread and 5.0% of the portfolio as fixed-rate assets with a coupon of 4.00%) minus theweighted-average cost of debt. WAS--Weighted-average spread. WAC--Weighted-average coupon. SDR--Scenario default rate.

Portfolio Credit Benchmarks

SPWARF* 2,758.01

'AAA' default rate dispersion 507.23

Obligor diversity measure§ 126.23

Industry diversity measure† 17.01

Regional diversity measure‡ 1.35

Weighted-average life 5.42

*The SPWARF is calculated by multiplying the par balance of each collateral obligation (with a rating from S&P Global Ratings of 'CCC-' orhigher) by S&P Global Ratings' rating factor, then summing the total for the portfolio, and then dividing this result by the aggregate principalbalance of all of the collateral obligations included in the calculation. The S&P Global Ratings' rating factor of an individual asset is the five-yeardefault rate given its S&P Global Ratings' credit rating and the default table in the corporate CDO criteria, multiplied by 10,000. §The effectivenumber of obligors in the underlying collateral, obtained by squaring the exposure for each obligor and taking the reciprocal of the sum of thesesquares [i.e., 1/sum()^2]. †The effective number of industry in the underlying collateral obtained the same way as the obligor diversity measure.‡The effective number of regions in the underlying collateral obtained the same way as obligor diversity measure. SPWARF--S&P Global Ratingsweighted-average rating factor.

Transaction Timeline

Transaction Timeline

Expected closing date July 8, 2021.

Effective date Jan. 11, 2022

Non-call period end date July 8, 2023.

Reinvestment period end date July 25, 2026.

Stated maturity date July 25, 2036.

Note payment frequency Quarterly, beginning Jan. 25, 2022. Semiannually after a frequency switch event.

www.standardandpoors.com July 6, 2021 2

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Transaction Timeline (cont.)

Participants

Collateral manager Partners Group (UK) Management Ltd.

Arranger Citigroup Global Markets Ltd.

Trustee U.S. Bank Trustees Ltd.

Rationale

Under the transaction documents, the rated notes will pay quarterly interest unless there is afrequency switch event. Following this, the notes will permanently switch to semiannual payment.

In our cash flow analysis, we used the €400 million target par amount, a weighted-average spreadof 3.55%, the reference weighted-average coupon (4.00%), and the weighted-average recoveryrates as calculated under our CLO criteria. We applied various cash flow stress scenarios, usingfour different default patterns, in conjunction with different interest rate stress scenarios for eachliability rating category.

Under our structured finance sovereign risk criteria, we consider that the transaction's exposureto country risk is sufficiently mitigated at the assigned preliminary ratings (see "IncorporatingSovereign Risk In Rating Structured Finance Securities: Methodology And Assumptions,"published on Jan. 30, 2019).

Our credit and cash flow analysis indicates that the available credit enhancement for the classB-1, B-2, C, and D notes could withstand stresses commensurate with higher ratings than thosewe have assigned. However, the CLO benefits from a reinvestment period until July 25, 2026,during which the transaction's credit risk profile could deteriorate, subject to CDO monitor results.We have therefore capped our preliminary ratings assigned to the notes.

Elavon Financial Services DAC is the bank account provider and custodian. At closing, we expectits documented replacement provisions to be in line with our counterparty criteria for liabilitiesrated up to 'AAA' (see "Counterparty Risk Framework: Methodology And Assumptions," publishedon March 8, 2019).

At closing, we expect the issuer to be bankruptcy remote, in accordance with our legal criteria (see"Structured Finance: Asset Isolation And Special-Purpose Entity Methodology," published onMarch 29, 2017).

Following our analysis of the credit, cash flow, counterparty, operational, and legal risks, webelieve our preliminary ratings are commensurate with the available credit enhancement for eachclass of notes.

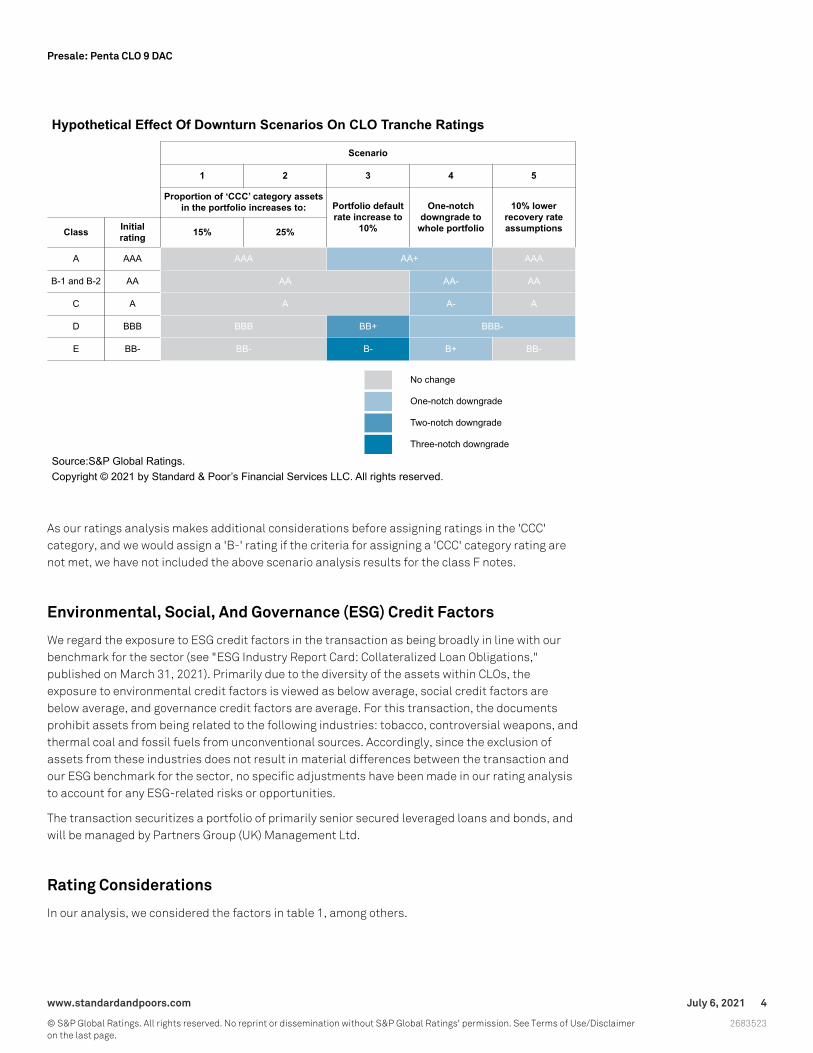

In addition to our standard analysis, to provide an indication of how rising pressures amongspeculative-grade corporates could affect our ratings on European CLO transactions, we have alsoincluded the sensitivity of the ratings on the class A to E notes to five of the 10 hypotheticalscenarios we looked at in our publication, "How Credit Distress Due To COVID-19 Could AffectEuropean CLO Ratings," published on April 2, 2020. The results are shown in the chart below.

www.standardandpoors.com July 6, 2021 3

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

As our ratings analysis makes additional considerations before assigning ratings in the 'CCC'category, and we would assign a 'B-' rating if the criteria for assigning a 'CCC' category rating arenot met, we have not included the above scenario analysis results for the class F notes.

Environmental, Social, And Governance (ESG) Credit Factors

We regard the exposure to ESG credit factors in the transaction as being broadly in line with ourbenchmark for the sector (see "ESG Industry Report Card: Collateralized Loan Obligations,"published on March 31, 2021). Primarily due to the diversity of the assets within CLOs, theexposure to environmental credit factors is viewed as below average, social credit factors arebelow average, and governance credit factors are average. For this transaction, the documentsprohibit assets from being related to the following industries: tobacco, controversial weapons, andthermal coal and fossil fuels from unconventional sources. Accordingly, since the exclusion ofassets from these industries does not result in material differences between the transaction andour ESG benchmark for the sector, no specific adjustments have been made in our rating analysisto account for any ESG-related risks or opportunities.

The transaction securitizes a portfolio of primarily senior secured leveraged loans and bonds, andwill be managed by Partners Group (UK) Management Ltd.

Rating Considerations

In our analysis, we considered the factors in table 1, among others.

www.standardandpoors.com July 6, 2021 4

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Table 1

Rating Considerations

Risk Risk description Mitigating factors

Reduction in cashflow

Defaults, adverse interest ratemovements, and low recoveries canreduce the cash flow generated by theunderlying portfolio and affect theissuer's ability to meet its obligationsin a timely manner.

Our quantitative analysis simulates various default patternsand interest rate movements, under various stressscenarios considering portfolio characteristics, paymentmechanics, covenants, collateral quality tests, and excessspread.

Excessconcentration incertain types ofcollateralobligations

The collateral manager's ability toinvest in certain types of collateral isoutlined by the indenture. Largerconcentrations in certain obligationscan introduce additional risks to therated notes.

Our cash flow analysis assumes the underlying portfoliocontains the maximum allowable amount of certain types ofcollateral obligations to stress test the transaction forconcentration risk. Examples include: 5.0% fixed rateassets. For more detail, please see table 11.

Collateral managertrading performance

During the reinvestment period, thecollateral manager can change theunderlying portfolio's composition,thus exposing the transaction topotential deterioration in creditenhancement.

The transaction documents require that any collateralobligation sold is replaced with another of equal or higherpar value (unless the collateral principal amount is greaterthan that of the target amount), or that the trade maintainsor increases the level of the transaction'sovercollateralization. Credit risk, defaulted, and equitysecurities are exempt from these restrictions. In addition,the indenture requires that each additional purchasesatisfy, maintain, or improve certain additional collateralquality tests.

Divergence ofeffective dateportfolio frompreliminaryassumptions

Most underlying portfolios are not fullypurchased by closing. Therefore, thereis a risk that the fully ramped-upportfolio at the transaction's effectivedate will be materially different thanthe one presented to us for itspreliminary analysis.

We offer collateral managers both a model andformula-based version of its CDO Monitor at closing. Thistool is intended to assist the collateral manager inmaintaining a similar credit risk and cash flow profile towhat was initially presented for our preliminary analysis.

Exposure tocovenant-lite loans

The collateral manager can purchasecovenant-lite loans (those that do notcontain incurrence or maintenancecovenants for the benefit of the lendingparty) for up to a certain percentage ofthe underlying portfolio (see table 11).Exposure to these types of loans mayreduce the transaction's recoveryprospects.

For covenant-lite loans that do not have an asset-specificrecovery rating, we apply reduced recovery rates in our cashflow analysis (41% under an 'AAA' level of stress versus 50%for a senior secured first-lien loan that is not covenant-lite(in a group "A" country).

Long-datedcollateral obligationcan introducemarket value risk

A portfolio containing long-datedcollateral obligations exposes atransaction to market value risk. Torepay the noteholders at thetransaction's maturity, the collateralmanager will be forced to sell suchobligations at the prevailing marketprice, which may be below par.

According to the transaction documents, the collateralmanager cannot purchase any long-dated collateralobligations, nor vote in favor of any waiver, modification, oramendment that would extend a collateral obligation'smaturity beyond the notes' stated maturity. Theweighted-average life test must be satisfied following anymaturity amendment.

Collateral Manager

Partners Group (UK) Management Ltd. is a subsidiary of Partners Group Holding AG. The group is aglobal private markets investment manager with over $109.1 billion in investment programs (as ofDec. 31, 2020) under management in private equity, private debt, private real estate, and private

www.standardandpoors.com July 6, 2021 5

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

infrastructure.

We reviewed Partners Group (UK) Management under our operational risk criteria (see "GlobalFramework For Assessing Operational Risk In Structured Finance Transactions," published on Oct.9, 2014). In our view, it is capable of managing this CLO, based on the extensive experience of itsportfolio managers.

Quantitative Analysis

In analyzing this transaction, we conducted a quantitative review consisting of two analyses: aportfolio analysis and a cash flow analysis.

Portfolio analysis

For the portfolio analysis, we ran the portfolio presented to us through the CDO Evaluator model,which defaults portions of the underlying collateral based on the default probability andcorrelation assumptions defined in our criteria. This resulted in a set of SDRs, which representexpected default levels for the portfolio under the different stress scenarios associated with eachrating level.

For unidentified assets in the collateral portfolio, we have relied on the information provided bythe portfolio manager for the asset characteristics (like ratings, industry, country, and notional ofthe asset).

Cash flow analysis

For the cash flow analysis, we input the transaction-specific structural features presented to usinto Standard & Poor's Cash Flow Evaluator model to generate a base-case set of cash flows. Wethen subjected these cash flows to various default timing and interest rate stress scenarios toarrive at a BDR for each rated class of notes.

For each class, the BDR represents the maximum amount of defaults that it can withstand whilestill being able to pay timely interest and ultimate principal to its noteholders. Classes with highersubordination typically have higher BDRs.

Because the transaction allows the manager to buy a maximum of 5.0% fixed paying assets, welooked at the BDRs considering this fixed bucket to be filled. Our base case is 5.0% fixed payingassets and 95.0% floating assets because it leads to the lowest BDRs on the 'AAA' rated notes. Inour analysis, we also modeled the weighted-average spread and coupon provided by the manager.

Connecting the portfolio and cash flow analyses

For a tranche to achieve a particular rating, it must be able to withstand the level of defaultsprojected by the CDO Evaluator and still pay timely interest and principal.

The results shown in table 2 indicate that the rated notes have sufficient credit enhancement towithstand our projected default levels. This scenario represents the scenario with the lowest BDRcushion at the 'AAA' level, in which we have modeled 95.0% of floating-rate assets and 5.0% offixed-rate assets.

www.standardandpoors.com July 6, 2021 6

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Table 2

Credit Enhancement

Class Subordination (%) BDR (%) SDR (%) BDR cushion (%)

A 39.25 67.97 64.66 3.32

B-1 28.63 65.07 56.81 8.26

B-2 28.63 65.07 56.81 8.26

C 22.00 58.83 50.76 8.07

D 15.00 50.28 44.96 5.33

E 10.00 39.86 33.67 6.19

F 7.00 28.85 27.59 1.26

BDR--Break-even default rate. SDR--Scenario default rate.

Supplemental tests

We also conduct a largest-industry default test, a largest-obligor default test, a largest sovereigndefault test, and a largest transfer and convertibility default test according to "GlobalMethodology And Assumptions For CLOs And Corporate CDOs," published on June 21, 2019, and"Incorporating Sovereign Risk In Rating Structured Finance Securities: Methodology AndAssumptions," published on Jan. 30, 2019. Under these assumptions, the notes can withstand theloss amounts indicated in table 3 at the assigned preliminary ratings.

Table 3

Supplemental Tests

ClassPreliminaryrating

Preliminaryamount (mil. €)

Largest industrydefault test loss

amount (mil. €)

Largest obligordefault test loss

amount (mil. €)

Largestsovereign test

amount (mil. €)

Largest sovereignT&C test amount

(mil. €)

A AAA (sf) 243.00 48.45 40.68 13.44 1.39

B-1 AA (sf) 33.50 48.45 33.13 13.44 0.00

B-2 AA (sf) 9.00 48.45 33.13 13.44 0.00

C A (sf) 26.50 N/A 25.49 0.00 0.00

D BBB (sf) 28.00 N/A 17.56 0.00 0.00

E BB- (sf) 20.00 N/A 13.53 0.00 0.00

F B- (sf) 12.00 N/A 9.28 0.00 0.00

N/A--Not applicable. T&C--Transfer and convertibility.

Collateral Quality Tests And Credit Metrics

In addition to the quantitative framework, we produce and review other metrics to assess specificrisks inherent in a transaction. Results for the collateral quality tests based on the portfolioprovided to us are shown in table 4.

www.standardandpoors.com July 6, 2021 7

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Table 4

Collateral Quality Metrics – Performing Collateral

Test Weighted- average Covenant Margin

Modeled weighted-average life (years)* 5.42 9.1 3.58

Weighted-average spread including floors (%) 3.64 3.55 0.09

Weighted-average spread excluding floors (%) 3.63 3.55 0.08

Weighted-average fixed coupon (%) 3.33 4.00 (0.67)

*The modeled weighted-average life is the one used in our cash flow analysis and is quarterly. N/A--Not applicable.

Portfolio Characteristics

Metrics based on the portfolio presented to us and the level of ramp-up completion are shown intable 5.

Table 5

Target Collateral Obligations

Target par balance (mil. €) 400.00

Par balance of identified collateral (mil. €) 400.00

Par balance of collateral not yet identified (mil. €) 0.00

S&P Global Ratings' credit rating (% of identified collateral) 99.18

Obligors

Number of unique obligors 142

Number of identified obligors 142

Average obligor holding (%) 0.70

Largest-obligor holding (%) 1.28

Smallest-obligor holding (%) 0.12

N/A--Not applicable.

In the portfolio data referenced for this analysis, the issuer had identified almost all of theportfolio's collateral. As the portfolio composition changes, the information and results presentedin table 6 and charts 1-4 are also likely to change.

Obligor concentration

The underlying portfolio presented to us for our rating analysis consists of 142 distinct obligors.Table 6 below shows the respective industries of the 10 top obligors.

www.standardandpoors.com July 6, 2021 8

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Table 6

Top Obligor Holdings

Notional amount (mil.€) Notional amount (%)

Obligorreference Industry

S&P Global Ratings'credit rating Obligor Cumulative Obligor Cumulative

1 Media B+ 5.10 5.10 1.28 1.28

2 Chemicals B 4.67 9.77 1.17 2.44

3 Multiline retail B+ 4.47 14.24 1.12 3.56

4 Diversified telecommunicationservices

B 4.24 18.48 1.06 4.62

5 Personal products B 4.17 22.66 1.04 5.66

6 Chemicals B 4.17 26.83 1.04 6.71

7 Building products B 4.07 30.90 1.02 7.73

8 Healthcare providers andservices

B 3.97 34.87 0.99 8.72

9 Interactive media and services B 3.97 38.85 0.99 9.71

10 Diversified consumer services B 3.97 42.82 0.99 10.71

Industry distribution

Chart 1 shows the top 10 industry distribution in the portfolio. The portfolio is composed of 37distinct industries as per the Capital IQ industry - level 3 classification.

www.standardandpoors.com July 6, 2021 9

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Chart 1

Ratings distribution

Chart 2 shows the ratings distribution in the portfolio. All of the identified underlying collateralobligations have credit ratings assigned by us.

www.standardandpoors.com July 6, 2021 10

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Chart 2

Recovery rating distribution

Table 7 presents the recovery rates modeled to calculate BDRs and actual recovery rates of thetargeted portfolio. Chart 3 below presents our recovery rates distribution of the identifiedportfolio. Of the identified underlying collateral obligations, 98.84% have recovery ratings issuedby us.

Table 7

Collateral WARR

Liability rating Modeled WARR (%) Target pool WARR (%) Actual WARR on identified portfolio (%)

AAA (sf) 35.39 35.39 35.39

AA (sf) 45.17 45.17 45.17

A (sf) 51.22 51.22 51.22

BBB (sf) 57.99 57.99 57.99

BB- (sf) 62.89 62.89 62.89

B- (sf) 63.83 63.83 63.83

WARR--Weighted-average recovery rate. During the ramp-up period (generally six months from closing), the manager will buy assets to reachthe modeled WARR considered in our analysis.

www.standardandpoors.com July 6, 2021 11

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Chart 3

Deleveraging profile

Chart 4 shows the portfolio's deleveraging profile.

www.standardandpoors.com July 6, 2021 12

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Chart 4

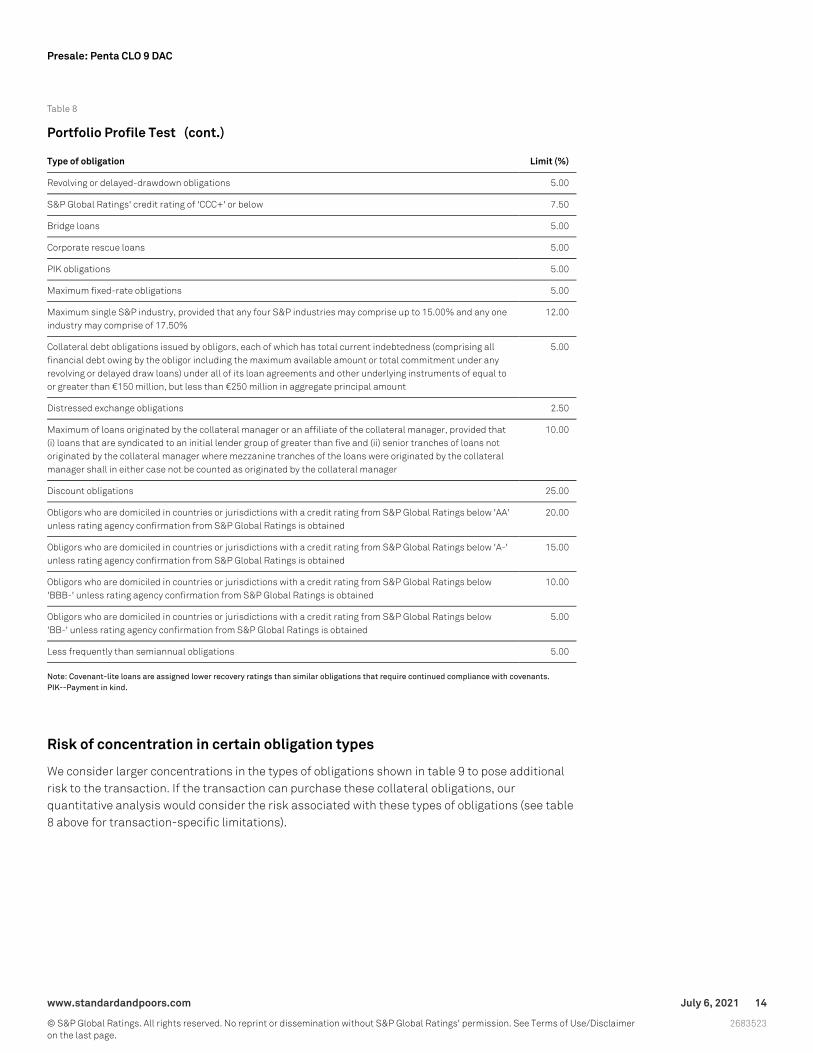

Portfolio Investment Guidelines

The underlying portfolio will primarily comprise euro denominated senior secured loans and bondsto broadly syndicated corporate borrowers. The collateral portfolio's effective date andreinvestment guidelines are expected to comply with the limitations shown in table 8.

Table 8

Portfolio Profile Test

Type of obligation Limit (%)

Secured senior loans or bonds 90.00

Maximum unsecured senior loans, second lien loans, mezzanine obligations, and high yield bonds in aggregate 10.00

Minimum senior secured loans 70.00

Maximum any single obligor, provided up to three obligors may each represent up to 3.00% of the aggregatecollateral balance

2.50

Maximum single obligor of for collateral other than senior secured obligations 1.50

Maximum currency hedge obligations 20.00

Covenant-lite loans 30.00

Participations 5.00

Current pay 5.00

www.standardandpoors.com July 6, 2021 13

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Table 8

Portfolio Profile Test (cont.)

Type of obligation Limit (%)

Revolving or delayed-drawdown obligations 5.00

S&P Global Ratings' credit rating of 'CCC+' or below 7.50

Bridge loans 5.00

Corporate rescue loans 5.00

PIK obligations 5.00

Maximum fixed-rate obligations 5.00

Maximum single S&P industry, provided that any four S&P industries may comprise up to 15.00% and any oneindustry may comprise of 17.50%

12.00

Collateral debt obligations issued by obligors, each of which has total current indebtedness (comprising allfinancial debt owing by the obligor including the maximum available amount or total commitment under anyrevolving or delayed draw loans) under all of its loan agreements and other underlying instruments of equal toor greater than €150 million, but less than €250 million in aggregate principal amount

5.00

Distressed exchange obligations 2.50

Maximum of loans originated by the collateral manager or an affiliate of the collateral manager, provided that(i) loans that are syndicated to an initial lender group of greater than five and (ii) senior tranches of loans notoriginated by the collateral manager where mezzanine tranches of the loans were originated by the collateralmanager shall in either case not be counted as originated by the collateral manager

10.00

Discount obligations 25.00

Obligors who are domiciled in countries or jurisdictions with a credit rating from S&P Global Ratings below 'AA'unless rating agency confirmation from S&P Global Ratings is obtained

20.00

Obligors who are domiciled in countries or jurisdictions with a credit rating from S&P Global Ratings below 'A-'unless rating agency confirmation from S&P Global Ratings is obtained

15.00

Obligors who are domiciled in countries or jurisdictions with a credit rating from S&P Global Ratings below'BBB-' unless rating agency confirmation from S&P Global Ratings is obtained

10.00

Obligors who are domiciled in countries or jurisdictions with a credit rating from S&P Global Ratings below'BB-' unless rating agency confirmation from S&P Global Ratings is obtained

5.00

Less frequently than semiannual obligations 5.00

Note: Covenant-lite loans are assigned lower recovery ratings than similar obligations that require continued compliance with covenants.PIK--Payment in kind.

Risk of concentration in certain obligation types

We consider larger concentrations in the types of obligations shown in table 9 to pose additionalrisk to the transaction. If the transaction can purchase these collateral obligations, ourquantitative analysis would consider the risk associated with these types of obligations (see table8 above for transaction-specific limitations).

www.standardandpoors.com July 6, 2021 14

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Table 9

Risks Of Obligation Types

Obligation type Risk specific to the obligation

Fixed-rate obligations Because interest payments for all of the rated notes are tied to EURIBOR, obligations in theunderlying portfolio that pay a fixed rate create exposure to interest rate movements. Shouldmarket rates change significantly over the transaction's life, this may reduce excess spread. Toaccount for this risk, we consider the mix of fixed- and floating-rate assets at the minimum andmaximum levels. The results are captured in the BDRs generated by Cash Flow Evaluator.

Long-datedobligations

Collateral obligations scheduled to mature after the transaction's stated maturity date introducemarket value risk, as the collateral manager must sell the obligations at the prevailing market priceto pay the rated noteholders. To account for this risk, our cash flow analysis haircuts the paramount of these obligations (excess over 5% of the portfolio at 10% discount rate per year beyondthe legal final maturity date), which will lower the BDRs produced by Cash Flow Evaluator. Thisstress would also be considered for long-dated assets that the transaction can hold after anymaturity amendments.

Obligations that payinterest lessfrequently thanquarterly

Because transactions typically require quarterly interest payments to be made to the noteholders, aportfolio consisting of collateral obligations that pay interest less frequently creates a discrepancyin the timing of cash inflows and outflows. If this mismatch is significant, it may result in a shortfallin cash available to pay the rated noteholders. In order to mitigate the effects of these timingmismatches, the transaction incorporates an interest smoothing account and a frequency switchmechanism, which if triggered, will switch the payment frequency on the rated notes tosemi-annual.

S&P Global Ratingspreliminary ratings'credit rating of 'CCC+'or below

Transaction documents typically limit the amount of obligations rated 'CCC+' or below that thecollateral manager can purchase. A higher concentration of obligations rated 'CCC+' or lower willincrease the SDRs produced by CDO Evaluator.

BDR--Break-even default rate. SDR--Scenario default rate. EURIBOR--Euro Interbank Offered Rate. PIK--Payment in kind.

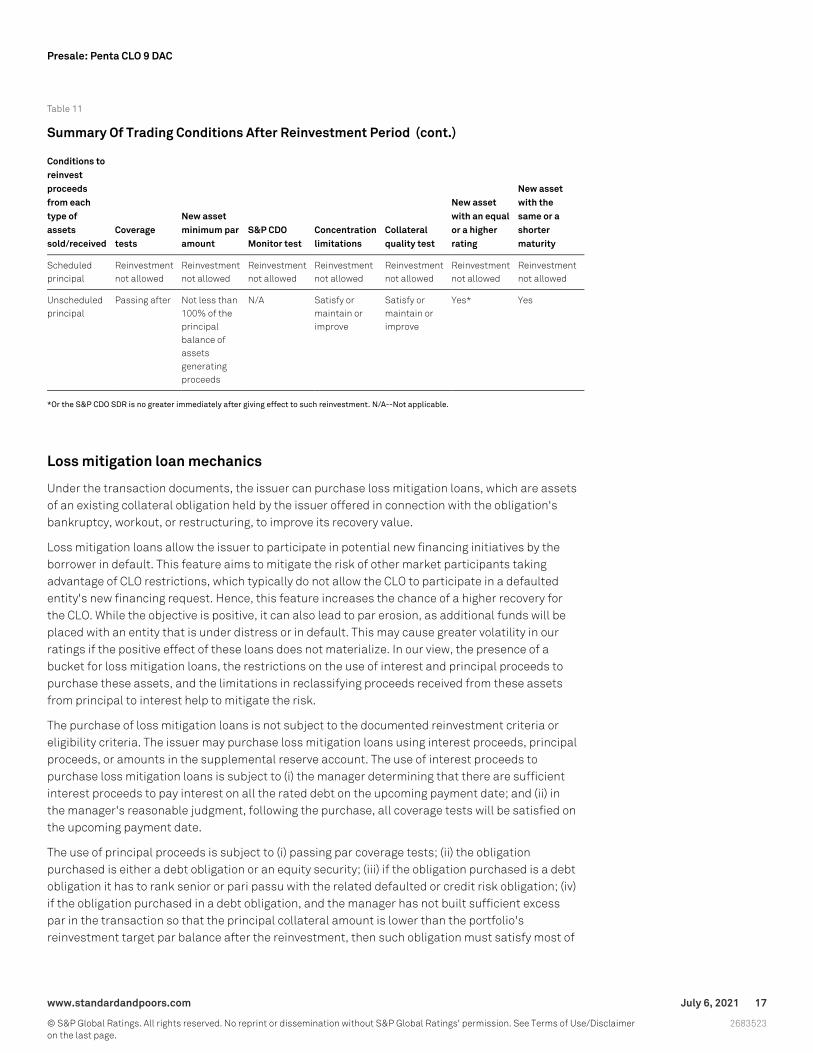

Under the transaction documents, certain conditions must be satisfied before collateral is boughtfor or sold from the portfolio (see tables 10 and 11).

Table 10

Summary Of Trading Conditions During Reinvestment Period

Conditions toreinvest proceedsfrom each type ofassetssold/received

Coveragetests

New assetminimumpar amount

S&P CDOMonitortest

Concentrationlimitations

Collateralquality test

Condition fornew assetwith anequal or ahigherrating?

Condition fornew assetwith thesame or ashortermaturity?

Discretionary Satisfy ormaintain orimprove

Not less than100% of theprincipalbalance ofassets sold*

Satisfy ormaintainor improve

Satisfy ormaintain orimprove

Satisfy ormaintain orimprove

No No

Credit risk Satisfy ormaintain orimprove

Not less than100% of thesaleproceeds ofassets sold*

Satisfy ormaintainor improve

Satisfy ormaintain orimprove

Notrequired

No No

Credit improved Satisfy ormaintain orimprove

Not less than100% of theprincipalbalance ofassets sold*

Satisfy ormaintainor improve

Satisfy ormaintain orimprove

Satisfy ormaintain orimprove

No No

www.standardandpoors.com July 6, 2021 15

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Table 10

Summary Of Trading Conditions During Reinvestment Period (cont.)

Conditions toreinvest proceedsfrom each type ofassetssold/received

Coveragetests

New assetminimumpar amount

S&P CDOMonitortest

Concentrationlimitations

Collateralquality test

Condition fornew assetwith anequal or ahigherrating?

Condition fornew assetwith thesame or ashortermaturity?

Defaulted(includingrecovery ondefaulted assets)

Notrequired

Not less than100% of thesaleproceeds ofassets sold*

Notrequired

Not required Notrequired

No No

Unscheduledprincipal(includingrecoveries)

Satisfy ormaintain orimprove

Not less than100% of theprincipalbalance ofassets sold*

Satisfy ormaintainor improve

Satisfy ormaintain orimprove

Satisfy ormaintain orimprove

No No

Scheduledprincipal

Satisfy ormaintain orimprove

Not less than100% of theprincipalbalance ofassets sold*

Satisfy ormaintainor improve

Satisfy ormaintain orimprove

Satisfy ormaintain orimprove

No No

*Alternatively, if the aggregate collateral balance of the portfolio is greater than the reinvestment target par balance. CDO--Collateral debtobligation.

Table 11

Summary Of Trading Conditions After Reinvestment Period

Conditions toreinvestproceedsfrom eachtype ofassetssold/received

Coveragetests

New assetminimum paramount

S&P CDOMonitor test

Concentrationlimitations

Collateralquality test

New assetwith an equalor a higherrating

New assetwith thesame or ashortermaturity

Discretionary Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Credit risk Passing after Not less than100% of thesale proceedsof assets sold

N/A Satisfy ormaintain orimprove

Satisfy ormaintain orimprove

Yes* Yes

Creditimproved

Passing after Not less than100% of theprincipalbalance ofassetsgeneratingproceeds

N/A Satisfy ormaintain orimprove

Satisfy ormaintain orimprove

Yes* Yes

Defaulted(includingrecovery ondefaultedassets)

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

www.standardandpoors.com July 6, 2021 16

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Table 11

Summary Of Trading Conditions After Reinvestment Period (cont.)

Conditions toreinvestproceedsfrom eachtype ofassetssold/received

Coveragetests

New assetminimum paramount

S&P CDOMonitor test

Concentrationlimitations

Collateralquality test

New assetwith an equalor a higherrating

New assetwith thesame or ashortermaturity

Scheduledprincipal

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Reinvestmentnot allowed

Unscheduledprincipal

Passing after Not less than100% of theprincipalbalance ofassetsgeneratingproceeds

N/A Satisfy ormaintain orimprove

Satisfy ormaintain orimprove

Yes* Yes

*Or the S&P CDO SDR is no greater immediately after giving effect to such reinvestment. N/A--Not applicable.

Loss mitigation loan mechanics

Under the transaction documents, the issuer can purchase loss mitigation loans, which are assetsof an existing collateral obligation held by the issuer offered in connection with the obligation'sbankruptcy, workout, or restructuring, to improve its recovery value.

Loss mitigation loans allow the issuer to participate in potential new financing initiatives by theborrower in default. This feature aims to mitigate the risk of other market participants takingadvantage of CLO restrictions, which typically do not allow the CLO to participate in a defaultedentity's new financing request. Hence, this feature increases the chance of a higher recovery forthe CLO. While the objective is positive, it can also lead to par erosion, as additional funds will beplaced with an entity that is under distress or in default. This may cause greater volatility in ourratings if the positive effect of these loans does not materialize. In our view, the presence of abucket for loss mitigation loans, the restrictions on the use of interest and principal proceeds topurchase these assets, and the limitations in reclassifying proceeds received from these assetsfrom principal to interest help to mitigate the risk.

The purchase of loss mitigation loans is not subject to the documented reinvestment criteria oreligibility criteria. The issuer may purchase loss mitigation loans using interest proceeds, principalproceeds, or amounts in the supplemental reserve account. The use of interest proceeds topurchase loss mitigation loans is subject to (i) the manager determining that there are sufficientinterest proceeds to pay interest on all the rated debt on the upcoming payment date; and (ii) inthe manager's reasonable judgment, following the purchase, all coverage tests will be satisfied onthe upcoming payment date.

The use of principal proceeds is subject to (i) passing par coverage tests; (ii) the obligationpurchased is either a debt obligation or an equity security; (iii) if the obligation purchased is a debtobligation it has to rank senior or pari passu with the related defaulted or credit risk obligation; (iv)if the obligation purchased in a debt obligation, and the manager has not built sufficient excesspar in the transaction so that the principal collateral amount is lower than the portfolio'sreinvestment target par balance after the reinvestment, then such obligation must satisfy most of

www.standardandpoors.com July 6, 2021 17

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

the eligibility criteria; (v) if the obligation purchased is an equity security, the manager having builtsufficient excess par in the transaction so that the principal collateral amount is greater than theportfolio's reinvestment target par balance after the reinvestment; and (vi) the obligationpurchases has a par value greater than its purchase price

Loss mitigation loans that are purchased with principal proceeds and have limited deviation fromthe eligibility criteria will receive defaulted treatment in the adjusted collateral principal amount.To protect the transaction from par erosion, any distributions received from loss mitigation loanspurchased with the use of principal proceeds will form part of the issuer's principal accountproceeds and cannot be recharacterized as interest.

Loss mitigation loans that are purchased with interest will receive zero credit in the principalbalance determination, and the proceeds received will form part of the issuer's interest accountproceeds. The manager can elect to give collateral value credit to loss mitigation loans, purchasedwith interest proceeds, subject to them meeting the same limited deviation from eligibility criteriaconditions. The proceeds from any loss mitigations reclassified in this way are credited to theprincipal account, subject to meeting the reinvestment provision and the manager having builtsufficient excess par in the transaction so that the principal collateral amount is greater than theportfolio's reinvestment target par balance after the transfer to the interest account.

The cumulative exposure to loss mitigation loans purchased with principal is limited to 5% of thetarget par balance. The cumulative exposure to loss mitigation loans purchased with principal andinterest is limited to 10% of the target par balance.

Note Payment Considerations

Overcollateralization, interest coverage, and interest diversion tests

The rated notes benefit from certain structural features that require sequential mandatoryredemption upon a breach of any overcollateralization or interest coverage test. Additionally,during the reinvestment period, the rated notes benefit from the reinvestment of up to a certainamount of the excess interest proceeds, captured upon breach of the transaction's interestdiversion test (see table 12).

Table 12

Overcollateralization, Interest Coverage, And Interest Diversion Tests

Class Actual O/C (%) Min. O/C required (%) Min. I/C required (%)

A/B 140.11 130.11 120.00

C 128.21 120.21 110.00

D 117.65 111.65 105.00

E 111.11 106.61 N/A

F 107.53 103.53 N/A

Interest diversion test 107.53 103.53 N/A

O/C--Overcollateralization. I/C--Interest coverage. N/A--Not applicable.

www.standardandpoors.com July 6, 2021 18

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Payment priorities

Under the transaction documents, the collateral's interest and principal collections are payableaccording to separate payment priorities. On each payment date during and after thereinvestment period, unless at the stated maturity or an acceleration following an event of defaultoccurs, proceeds will be distributed in the priority outlined in table 13.

Table 13

Waterfall Payment Priority

Priority Interest waterfall Principal waterfall

A Taxes and issuer profit amount Payment of A through I ofinterest waterfall if previouslyunpaid

B Accrued and unpaid trustee fees and expenses, up to the cap If class C is controlling class,any unpaid interest

C Trustee fees and administrative expenses, up to the cap If class C is controlling class,unpaid deferred interest

D Transfers to expense reserve account Cure class C coverage test(s)

E (i)Senior collateral management fees, some of which may be deferred topurchase additional collateral or waived (such as deferred senior collateralmanagement amounts)*; (ii)Catch up on previously due and unpaid (notdeferred senior collateral management amounts) senior collateralmanagement fees

If class D is controlling class,any unpaid interest

F (i)Scheduled periodic hedge issuer payments, and any hedge terminationpayments; (ii)Hedge replacement payments

If class D is controlling class,unpaid deferred interest

G Class A interest Cure class D coverage test(s)

H Class B-1 and B-2 notes interest pro rata pari passu If class E is controlling class,any unpaid interest

I Cure class A/B notes' coverage tests If class E is controlling class,unpaid deferred interest

J Class C notes' interest, current period Cure class E par value test

K Class C notes' deferred interest If class F is controlling class,any unpaid interest

L Cure Class C notes' coverage tests If class F is controlling class,unpaid deferred interest

M Class D notes' interest, current period Cure the class F notes' parvalue test (following the expiryof the reinvestment period)

N Class D notes' deferred interest Make payments under aneffective date rating event

O Cure class D notes' coverage tests Make payments under aspecial redemption event

P Class E notes' interest, current period Purchase collateral in line withreinvestment criteria

Q Class E notes' deferred interest Note redemption in line withpriority

R Cure class E notes' par value test Purchase collateral in line withreinvestment criteria

www.standardandpoors.com July 6, 2021 19

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Table 13

Waterfall Payment Priority (cont.)

Priority Interest waterfall Principal waterfall

S Class F notes' interest, current period Payment of X through AA ofinterest waterfall if previouslyunpaid

T Class F notes' deferred interest Residual payments to equityand, where appropriate,collateral manager

U Cure the class F notes' par value test (following the expiry of thereinvestment period)

V Redemption following an effective date rating event

W Reinvestment overcollateralization test, minimum of cure amount or 50% ofremaining proceeds to either redeem notes or purchase additional collateral

X Deferred senior collateral manager amounts and repayment of seniorcollateral manager advances

Y Any remaining trustee fees and expenses not paid under the cap§

Z Any remaining administrative expenses under the cap

AA Any payments in relation to a defaulted hedge counterparty

BB Transfer to supplemental reserve account

CC Investment management fee incentive and VAT

DD Residual payments to equity and, where appropriate, collateral manager

*0.20% per year. §0.025% per year. Note: The note payment sequence is: First, the class A loan and notes at the applicable redemption priceuntil they fully redeem, followed by the class B-1 and B-2 notes pro rata pari passu in the same manner. Then, the class C notes includingunpaid interest and deferred interest at the applicable redemption price until they fully redeem, followed by the class D to F notes in the samemanner.

Note redemption circumstances

Under the transaction documents, the notes can be redeemed before the stated maturity date ofthe transaction in the circumstances outlined below (see table 14).

Table 14

Note Redemption

Redemption events Redemption terms

Final redemption Each class of notes will be redeemed at their redemption price in accordancewith the notes payment of sequence on the maturity date.

Optional redemption in whole -subordinated noteholders/collateralmanager

After expiry of the non-call period or in case of a collateral tax event, at thedirection of the subordinated noteholders, subject to consent from themanager or at the direction of the manager, any class of notes may beredeemed, in whole but not in part, from sale proceeds or refinancingproceeds.

Optional redemption in part – subordinatednoteholders or collateral manager

After expiry of the non-call period, at the direction of the subordinatednoteholders, subject to consent from the manager or at the direction of themanager, any the notes of any class may be redeemed, in part, fromrefinancing proceeds.

www.standardandpoors.com July 6, 2021 20

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Table 14

Note Redemption (cont.)

Redemption events Redemption terms

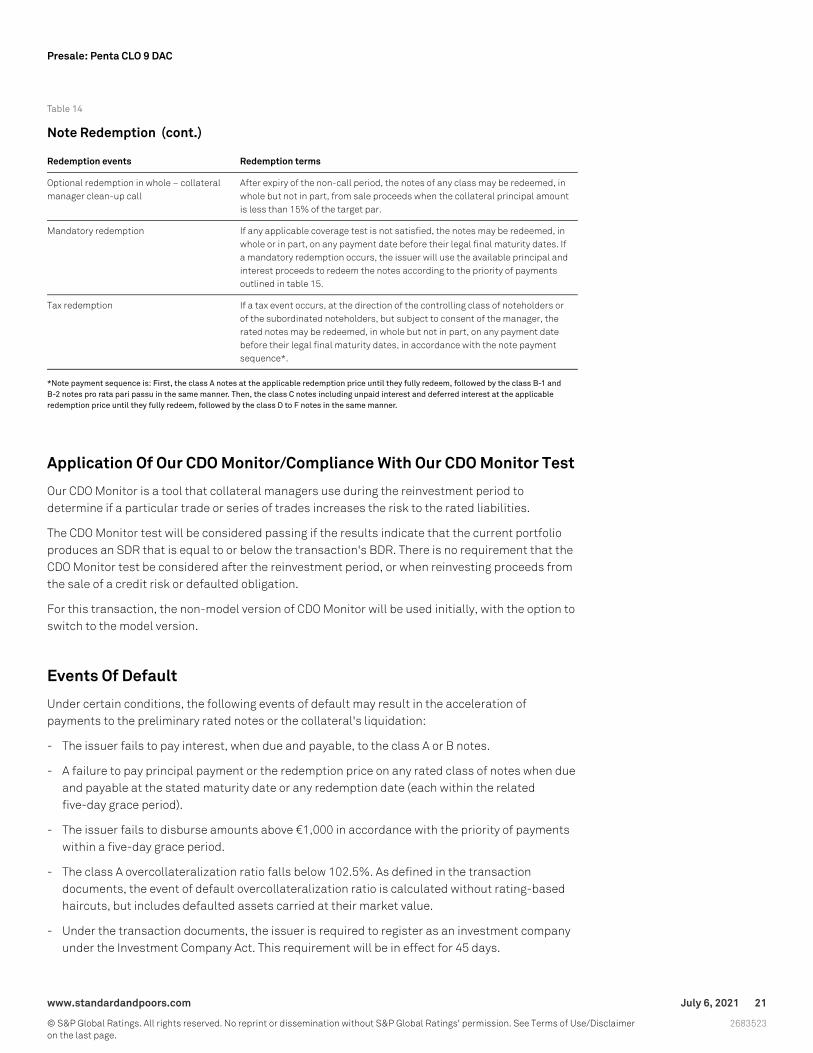

Optional redemption in whole – collateralmanager clean-up call

After expiry of the non-call period, the notes of any class may be redeemed, inwhole but not in part, from sale proceeds when the collateral principal amountis less than 15% of the target par.

Mandatory redemption If any applicable coverage test is not satisfied, the notes may be redeemed, inwhole or in part, on any payment date before their legal final maturity dates. Ifa mandatory redemption occurs, the issuer will use the available principal andinterest proceeds to redeem the notes according to the priority of paymentsoutlined in table 15.

Tax redemption If a tax event occurs, at the direction of the controlling class of noteholders orof the subordinated noteholders, but subject to consent of the manager, therated notes may be redeemed, in whole but not in part, on any payment datebefore their legal final maturity dates, in accordance with the note paymentsequence*.

*Note payment sequence is: First, the class A notes at the applicable redemption price until they fully redeem, followed by the class B-1 andB-2 notes pro rata pari passu in the same manner. Then, the class C notes including unpaid interest and deferred interest at the applicableredemption price until they fully redeem, followed by the class D to F notes in the same manner.

Application Of Our CDO Monitor/Compliance With Our CDO Monitor Test

Our CDO Monitor is a tool that collateral managers use during the reinvestment period todetermine if a particular trade or series of trades increases the risk to the rated liabilities.

The CDO Monitor test will be considered passing if the results indicate that the current portfolioproduces an SDR that is equal to or below the transaction's BDR. There is no requirement that theCDO Monitor test be considered after the reinvestment period, or when reinvesting proceeds fromthe sale of a credit risk or defaulted obligation.

For this transaction, the non-model version of CDO Monitor will be used initially, with the option toswitch to the model version.

Events Of Default

Under certain conditions, the following events of default may result in the acceleration ofpayments to the preliminary rated notes or the collateral's liquidation:

- The issuer fails to pay interest, when due and payable, to the class A or B notes.

- A failure to pay principal payment or the redemption price on any rated class of notes when dueand payable at the stated maturity date or any redemption date (each within the relatedfive-day grace period).

- The issuer fails to disburse amounts above €1,000 in accordance with the priority of paymentswithin a five-day grace period.

- The class A overcollateralization ratio falls below 102.5%. As defined in the transactiondocuments, the event of default overcollateralization ratio is calculated without rating-basedhaircuts, but includes defaulted assets carried at their market value.

- Under the transaction documents, the issuer is required to register as an investment companyunder the Investment Company Act. This requirement will be in effect for 45 days.

www.standardandpoors.com July 6, 2021 21

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

- A material default in the performance or material breach of any covenant, or other issueragreement that is not cured within the 30-day cure period.

- The issuer's voluntary or involuntary bankruptcy.

- It becomes unlawful for the issuer to perform or comply with one or more of its obligations.

Structural Overview

Penta 9 CLO, the issuer, is a special-purpose entity (SPE) that was incorporated as an exemptedcompany with limited liability under the laws of Ireland. The issuer's only purposes are to acquirethe collateral portfolio, issue the notes, enter into transaction documents, and engage in certainrelated transactions. We expect the issuer's SPE provisions to be consistent with our bankruptcyremoteness criteria outlined in our latest legal criteria. In rating this transaction, we will review thelegal matters that we consider to be relevant to our analysis, as outlined in our criteria.

Surveillance

We will maintain active surveillance on the rated notes until the notes mature or are retired, oruntil our credit ratings on the transaction have been withdrawn. The purpose of surveillance is toassess whether the rated notes are performing within the initial parameters and assumptionsapplied to each rating category. The issuer is required under the terms of the transactiondocuments to supply periodic reports and notices to us to maintain continuous surveillance on therated notes.

Related Criteria

- Criteria | Structured Finance | General: Global Framework For Payment Structure And CashFlow Analysis Of Structured Finance Securities, Dec. 22, 2020

- Criteria | Structured Finance | General: Methodology To Derive Stressed Interest Rates InStructured Finance, Oct. 18, 2019

- Criteria | Structured Finance | CDOs: Global Methodology And Assumptions For CLOs AndCorporate CDOs, June 21, 2019

- Criteria | Structured Finance | General: Counterparty Risk Framework: Methodology AndAssumptions, March 8, 2019

- Criteria | Structured Finance | General: Incorporating Sovereign Risk In Rating StructuredFinance Securities: Methodology And Assumptions, Jan. 30, 2019

- Legal Criteria: Structured Finance: Asset Isolation And Special-Purpose Entity Methodology,March 29, 2017

- Criteria | Structured Finance | General: Global Framework For Assessing Operational Risk InStructured Finance Transactions, Oct. 9, 2014

- General Criteria: Methodology Applied To Bank Branch-Supported Transactions, Oct. 14, 2013

- Criteria | Structured Finance | General: Global Derivative Agreement Criteria, June 24, 2013

- General Criteria: Criteria For Assigning 'CCC+', 'CCC', 'CCC-', And 'CC' Ratings, Oct. 1, 2012

- General Criteria: Global Investment Criteria For Temporary Investments In Transaction

www.standardandpoors.com July 6, 2021 22

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

Accounts, May 31, 2012

- General Criteria: Principles Of Credit Ratings, Feb. 16, 2011

Related Research

- ESG Industry Report Card: Collateralized Loan Obligations, March 31, 2021

- How Credit Distress Due To COVID-19 Could Affect European CLO Ratings, April 2, 2020

- Scenario and Sensitivity Analysis: 2017 EMEA Structured Credit Scenario And SensitivityAnalysis, July 6, 2017

- Global Structured Finance Scenario And Sensitivity Analysis 2016: The Effects Of The Top FiveMacroeconomic Factors, Dec. 16, 2016

- European Structured Finance Scenario And Sensitivity Analysis 2016: The Effects Of The TopFive Macroeconomic Factors, Dec. 16, 2016

www.standardandpoors.com July 6, 2021 23

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2683523

Presale: Penta CLO 9 DAC

S&P may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of securities or from obligors.S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributedthrough other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available atwww.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respectiveactivities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has establishedpolicies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed andnot statements of fact. S&P's opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase,hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation toupdate the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment andexperience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not actas a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable,S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. Rating-relatedpublications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not limitedto, the publication of a periodic update on a credit rating and related analyses.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certainregulatory purposes, S&P reserves the right to assign, withdraw or suspend such acknowledgment at any time and in its sole discretion. S&P Partiesdisclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damagealleged to have been suffered on account thereof.

Copyright © 2021 Standard & Poor's Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any partthereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrievalsystem, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not beused for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees oragents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are notresponsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or forthe security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESSOR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE ORUSE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THECONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct,indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, withoutlimitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advisedof the possibility of such damages.

Standard & Poor’s | Research | July 6, 2021 24

2683523

Presale: Penta CLO 9 DAC