people & organizational wellbeing strategy

TRANSCRIPT

U.S. Edition

2021 Workforce Trends Report Series

Findings and insights from the 2021 Benefits Strategy & Benchmarking Survey

PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

THIS REPORT IS JUST THE BEGINNING.

Access the complete 2021 Workforce Trends Report Series and confidently plan for your future success.

The Workforce Trends Report Series covers all aspects of employee and organizational wellbeing:• National benchmarking data from thousands of employers

• Up-to-date information and strategies for responding to current workforce challenges

• Insight into how other employers are responding to changing workforce needs

• Comprehensive views of the modern drivers of employee and organizational wellbeing

PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

Overview of current employer trends in total

rewards and operational priorities

PHYSICAL & EMOTIONAL WELLBEING

Insights into healthcare, people management

and competing for talent in an evolving market

CAREER WELLBEING

National review of salary strategies,

changing economic trends and

compensation practices

FINANCIAL WELLBEING

Strategies to help employees mitigate

financial stress and manage funds

ORGANIZATIONAL WELLBEING

Emerging HR tech, communications and

workforce management strategies

STATE OF THE SECTOR

See how the global pandemic continues to affect the way organizations approach internal communication and

employee experience. Informed by hundreds of responses from global communication and HR leaders, the State

of the Sector 2021 explores the key challenges and trends facing employers.

BEST-IN-CLASS BENCHMARKING ANALYSIS

Research into top-performing organizations in

cost control and workforce management

GET THE DATA YOU NEED TO CONFIDENTLY PLAN FOR YOUR FUTURE SUCCESS.Access the complete 2021 Workforce Trends Report series

for $650. Order now to see how you can sustainably balance

employee needs and expectations with your business goals.

PREVIEW REPORT DATA

ajg.com/2021-WFTRSeries

TABLE OF CONTENTS

The intent of this document is to provide general information regarding your potential interests and concerns related to employee compensation and benefits. It does not necessarily fully address all of your specific issues. It should not be construed as, and is not intended to provide, legal advice. Questions about specific issues should be addressed by your general counsel or an attorney who specializes in this practice area.

4 INTRODUCTION

8 PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

29 ENDNOTES

30 CONTRIBUTORS

31 ABOUT GALLAGHER

INTRODUCTION As the economy and labor market begin to rebound, the major changes to the way business was done in 2020 are defining the way forward in 2021. This period of great disruption has sparked a future of greater innovation that will indelibly remake organizational structures, workplace policies and total rewards.

5GALLAGHER AJG.COM

With expectations for growth and increasing competition for

talent, leaders have laser-focused their attention on compensation

approaches and retention strategies. Flexible workforce policies

and practices will remain essential, including a strong focus on

emotional wellbeing, because resiliency will continue to rely on

agility in adapting to change.

Constant change in society and its inevitable uncertainties create

challenges in the workplace, which make employee wellbeing an

employer’s greatest asset. This measure of whole health — physical,

emotional, career and financial — and the status of organizational

health are inseparable.

That’s why wellbeing is at the center of Gallagher Better Works℠,

our comprehensive approach to benefits, compensation,

retirement and employee communication that aligns your

people strategy with your overall business goals. It focuses on

the full spectrum of organizational wellbeing — taking a strategic

approach to investing in employee wellbeing at the right cost

structures to support diverse workforce needs.

To help you make the best decisions for the overall health and

wellbeing of your employees and organization, the pages that

follow set the stage for our Workforce Trends Report Series.

Here, we start where HR compensation and benefits planning

starts, with your people and organizational strategy, total rewards,

and healthcare cost considerations. The remaining installments

will focus specifically on one aspect of wellbeing, including

physical and emotional, career, financial and organizational.

Data and insights highlighted in the report series are compiled

from a variety of Gallagher benchmarking surveys, conducted

each year to capture current and emerging trends. In this

report, they’re based on an analysis of our Benefits Strategy &

Benchmarking Survey results, gathered from December 2020

to March 2021. A total of 3,996 organizations across the United

States participated.

Findings are broken out by region, organization size and

ownership structure for peer comparison. Each section features

core data highlights, contains tables with detailed results and

wraps up with key takeaways. From broad insights to specific

findings, you’ll gain a practical perspective on trends and best

practices to help you face your future with confidence.

To discuss your organization's people strategy, contact your local

Gallagher representative or one of the advisors listed in the back

of the report.

6 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

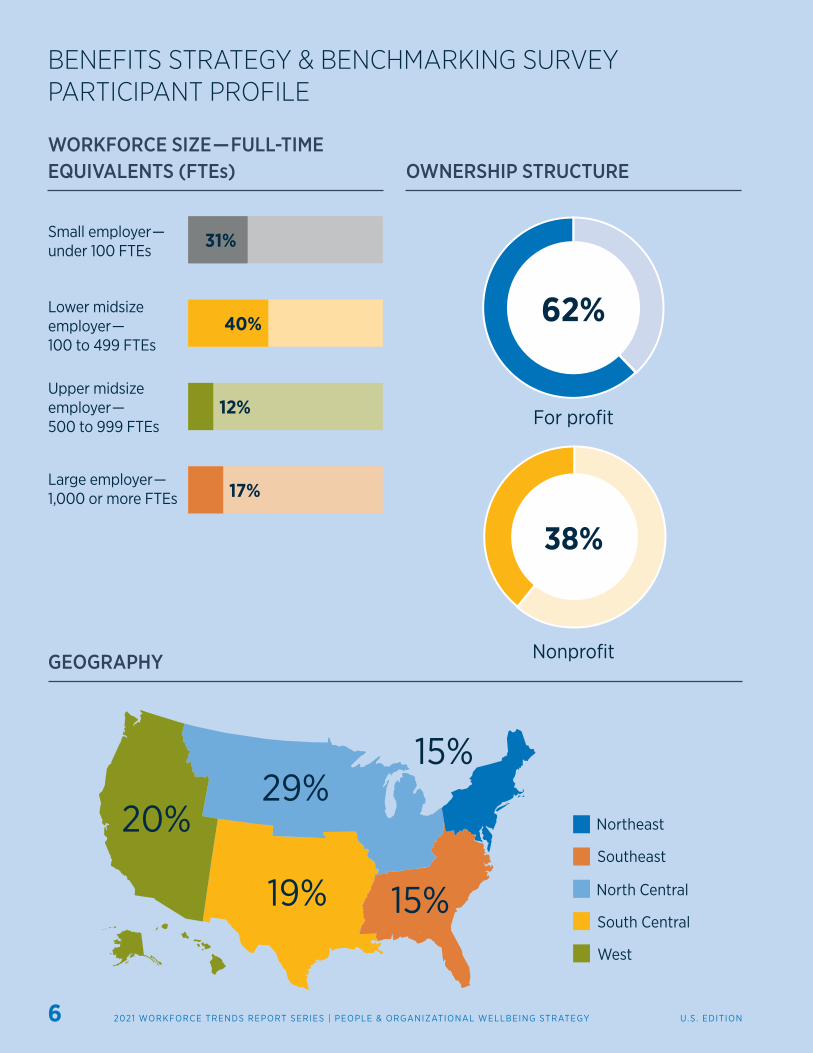

GEOGRAPHY

WORKFORCE SIZE — FULL-TIME EQUIVALENTS (FTEs)

BENEFITS STRATEGY & BENCHMARKING SURVEY PARTICIPANT PROFILE

OWNERSHIP STRUCTURE

Southeast

South Central

West

Northeast

North Central15%

29%20%

19%

15%

For profit

Nonprofit

Small employer — under 100 FTEs

Lower midsize employer — 100 to 499 FTEs

Upper midsize employer — 500 to 999 FTEs

Large employer — 1,000 or more FTEs

31%

40%

12%

17%

62%

38%

7GALLAGHER AJG.COM

NUMBER OF PARTICIPATING ORGANIZATIONS BY INDUSTRY

PUBLIC ENTITY

388MANUFACTURING

500

K–12 EDUCATION

208

HIGHER EDUCATION

74

FINANCIAL SERVICES

228TECHNOLOGY

256CONSTRUCTION

224

RELIGIOUS INSTITUTIONS

55

ENERGY

125

TRANSPORTATION

112

LIFE SCIENCES

57LAW

66

REAL ESTATE

67

PHARMACEUTICAL

33AGRICULTURE

42

HEALTHCARE

715

SOCIAL SERVICES

196

BUSINESS SERVICES

262

WHOLESALE-DISTRIBUTION

115

RETAIL

100

ASSOCIATIONS

64

HOSPITALITY/RESTAURANT/ ENTERTAINMENT

159

PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY Revenue disruption led to reduced compensation on a fairly broad scale in 2020, through measures such as cutting pay, and freezing or deferring wage increases and retiree contributions. For employers in most industries, a new challenge looms as the strengthening labor market increases pressure on compensation levels. They’re now tasked with optimizing employee relations in a competitive wage environment while managing their benefits spend.

9GALLAGHER AJG.COM

To help retain core talent, many employers are considering

formalized pay increases or delivery systems. Others are focused

on stability as they transition from survival mode — like those in

the retail and airline industries — so employee health and safety

remain top priorities. Although these employers are minimizing

unnecessary change, they’re also exploring sustainable reward

models, including variable compensation.

Transparent visibility into job openings and a vast amount of

readily available information on an organization's pay equity,

diversity and workplace culture makes it easier for employees to

evaluate options. Even geographic boundaries for employees have

diminished as virtual work has grown more prevalent, driving a

stronger focus on retention.

Workplace mobility gives employees in many industries more

power to dictate their locations and schedules. In response,

employers are looking to grant maximum flexibility while also

meeting compliance standards and keeping diligent records.

When employers consider the holistic value of their total rewards,

and make an effort to match these elements more closely to

workforce needs and interests, they can mitigate the potential

for turnover. Also important is recognizing and acting on cultural

opportunities for improving employee wellbeing.

Success in a new era of virtual and flexible work environments

will depend on the outcomes of investments and other decisions

driven by workforce preferences. In particular, keeping dispersed

employees interconnected, engaged in shared team goals and

working toward a common mission is likely to require some

time and tinkering — along with flexible thinking. Other core

considerations should include cultural impact, engagement,

inclusivity, communications transparency and change

management strategies. The right approach is one that’s just as

effective for the workforce as it is for the organization.

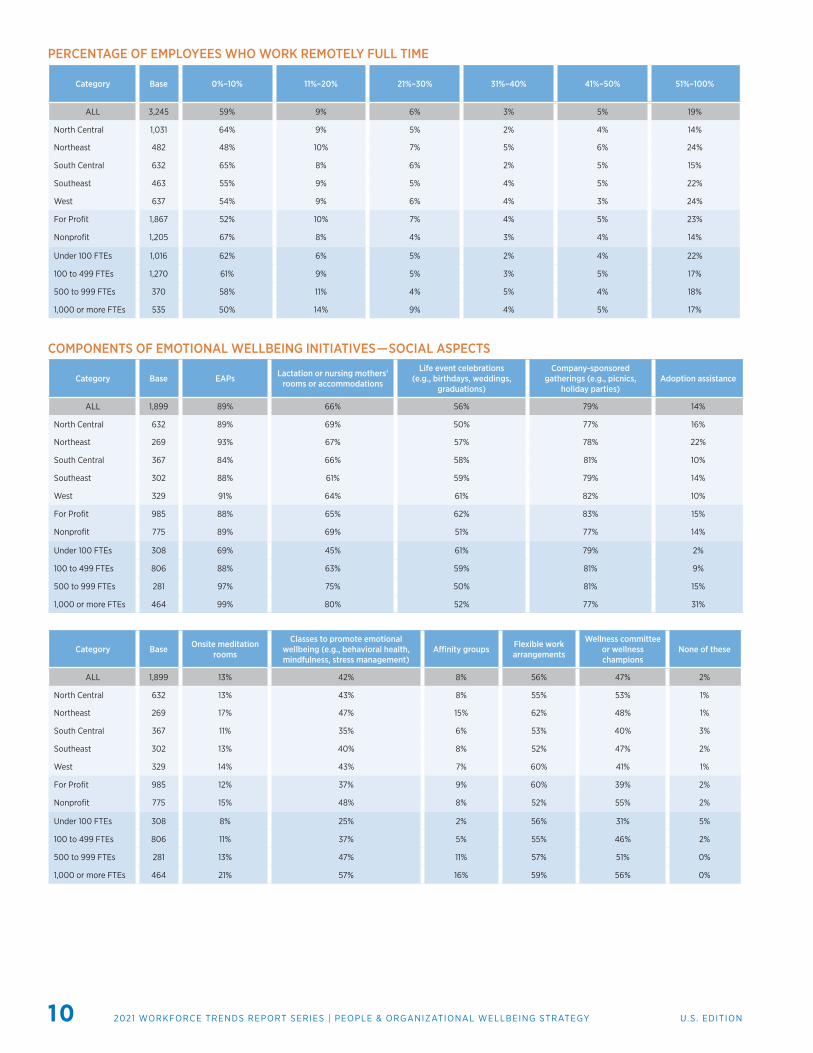

Full-time remote employees make up over 50% of the workforce for nearly 1 in 5 employers.

More than a year after massive change to business operations

brought a sudden upswing in remote work, 19% of organizations

have more than half of their employees located offsite full time.

And this population accounts for 21%–50% of the workforce at

another 14%. From a risk management standpoint, the upfront

benefits of shifting employees away from a group setting include

protection for their health and easier social distance scheduling

onsite. Factors such as virtual technology requirements, real

estate costs and cleaning expenses continue to be assessed, along

with the effect on employee engagement.

Considerations for returning remote employees to the

workplace include their comfort level with this change, onsite

productivity that compares favorably to remote productivity

and adequate social distancing protocols. Also important are

access to childcare or schooling and personal preferences. As

an underlying support mechanism, flexible work arrangements

(56%) help employees cope better with pandemic-altered

lifestyles — wherever they’re located.

While the physical health threat of COVID-19 has started to wane,

anxiety caused by coping with disrupted daily routines, financial

worries and other pandemic-related issues is slower to resolve.

Ensuring workplace safety not only helps reduce stress, but it

also provides an opportunity to advance a conversation with the

workforce about mental and emotional health, which has been a

growing concern for years.

Most employers (89%) offer support through an employee

assistance program (EAP), but this benefit often needs to be more

actively managed to achieve the intended results. It’s critical to

both monitor utilization rates and modify the program as needed.

Manager education and training enables proactive intervention that

can help prevent burnout and promote employee wellbeing.

Have more than 50% of employees work remotely full time1 in 5

Almost

10 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

PERCENTAGE OF EMPLOYEES WHO WORK REMOTELY FULL TIME

Category Base 0%–10% 11%–20% 21%–30% 31%–40% 41%–50% 51%–100%

ALL 3,245 59% 9% 6% 3% 5% 19%

North Central 1,031 64% 9% 5% 2% 4% 14%

Northeast 482 48% 10% 7% 5% 6% 24%

South Central 632 65% 8% 6% 2% 5% 15%

Southeast 463 55% 9% 5% 4% 5% 22%

West 637 54% 9% 6% 4% 3% 24%

For Profit 1,867 52% 10% 7% 4% 5% 23%

Nonprofit 1,205 67% 8% 4% 3% 4% 14%

Under 100 FTEs 1,016 62% 6% 5% 2% 4% 22%

100 to 499 FTEs 1,270 61% 9% 5% 3% 5% 17%

500 to 999 FTEs 370 58% 11% 4% 5% 4% 18%

1,000 or more FTEs 535 50% 14% 9% 4% 5% 17%

COMPONENTS OF EMOTIONAL WELLBEING INITIATIVES — SOCIAL ASPECTS

Category Base EAPs Lactation or nursing mothers’ rooms or accommodations

Life event celebrations (e.g., birthdays, weddings,

graduations)

Company-sponsored gatherings (e.g., picnics,

holiday parties) Adoption assistance

ALL 1,899 89% 66% 56% 79% 14%

North Central 632 89% 69% 50% 77% 16%

Northeast 269 93% 67% 57% 78% 22%

South Central 367 84% 66% 58% 81% 10%

Southeast 302 88% 61% 59% 79% 14%

West 329 91% 64% 61% 82% 10%

For Profit 985 88% 65% 62% 83% 15%

Nonprofit 775 89% 69% 51% 77% 14%

Under 100 FTEs 308 69% 45% 61% 79% 2%

100 to 499 FTEs 806 88% 63% 59% 81% 9%

500 to 999 FTEs 281 97% 75% 50% 81% 15%

1,000 or more FTEs 464 99% 80% 52% 77% 31%

Category Base Onsite meditation rooms

Classes to promote emotional wellbeing (e.g., behavioral health, mindfulness, stress management)

Affinity groups Flexible work arrangements

Wellness committee or wellness champions

None of these

ALL 1,899 13% 42% 8% 56% 47% 2%

North Central 632 13% 43% 8% 55% 53% 1%

Northeast 269 17% 47% 15% 62% 48% 1%

South Central 367 11% 35% 6% 53% 40% 3%

Southeast 302 13% 40% 8% 52% 47% 2%

West 329 14% 43% 7% 60% 41% 1%

For Profit 985 12% 37% 9% 60% 39% 2%

Nonprofit 775 15% 48% 8% 52% 55% 2%

Under 100 FTEs 308 8% 25% 2% 56% 31% 5%

100 to 499 FTEs 806 11% 37% 5% 55% 46% 2%

500 to 999 FTEs 281 13% 47% 11% 57% 51% 0%

1,000 or more FTEs 464 21% 57% 16% 59% 56% 0%

11GALLAGHER AJG.COM

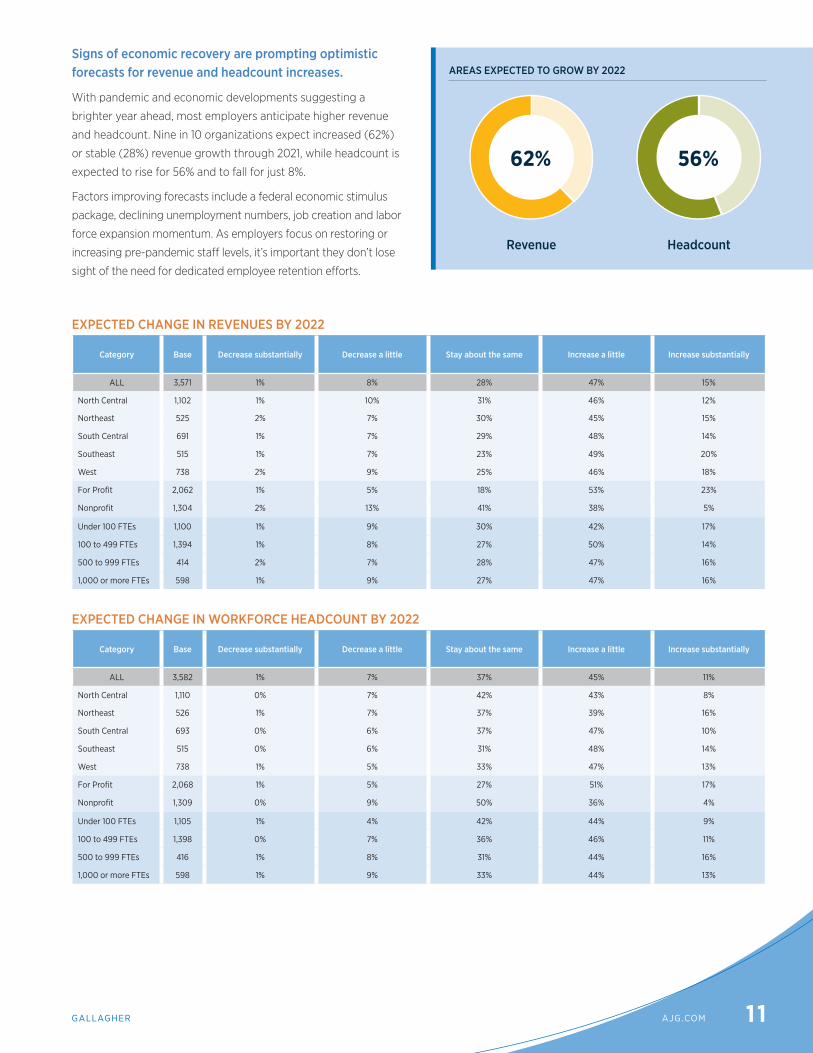

AREAS EXPECTED TO GROW BY 2022

EXPECTED CHANGE IN REVENUES BY 2022

Category Base Decrease substantially Decrease a little Stay about the same Increase a little Increase substantially

ALL 3,571 1% 8% 28% 47% 15%

North Central 1,102 1% 10% 31% 46% 12%

Northeast 525 2% 7% 30% 45% 15%

South Central 691 1% 7% 29% 48% 14%

Southeast 515 1% 7% 23% 49% 20%

West 738 2% 9% 25% 46% 18%

For Profit 2,062 1% 5% 18% 53% 23%

Nonprofit 1,304 2% 13% 41% 38% 5%

Under 100 FTEs 1,100 1% 9% 30% 42% 17%

100 to 499 FTEs 1,394 1% 8% 27% 50% 14%

500 to 999 FTEs 414 2% 7% 28% 47% 16%

1,000 or more FTEs 598 1% 9% 27% 47% 16%

EXPECTED CHANGE IN WORKFORCE HEADCOUNT BY 2022

Category Base Decrease substantially Decrease a little Stay about the same Increase a little Increase substantially

ALL 3,582 1% 7% 37% 45% 11%

North Central 1,110 0% 7% 42% 43% 8%

Northeast 526 1% 7% 37% 39% 16%

South Central 693 0% 6% 37% 47% 10%

Southeast 515 0% 6% 31% 48% 14%

West 738 1% 5% 33% 47% 13%

For Profit 2,068 1% 5% 27% 51% 17%

Nonprofit 1,309 0% 9% 50% 36% 4%

Under 100 FTEs 1,105 1% 4% 42% 44% 9%

100 to 499 FTEs 1,398 0% 7% 36% 46% 11%

500 to 999 FTEs 416 1% 8% 31% 44% 16%

1,000 or more FTEs 598 1% 9% 33% 44% 13%

Signs of economic recovery are prompting optimistic forecasts for revenue and headcount increases.

With pandemic and economic developments suggesting a

brighter year ahead, most employers anticipate higher revenue

and headcount. Nine in 10 organizations expect increased (62%)

or stable (28%) revenue growth through 2021, while headcount is

expected to rise for 56% and to fall for just 8%.

Factors improving forecasts include a federal economic stimulus

package, declining unemployment numbers, job creation and labor

force expansion momentum. As employers focus on restoring or

increasing pre-pandemic staff levels, it’s important they don’t lose

sight of the need for dedicated employee retention efforts.

Revenue Headcount

62% 56%

12 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

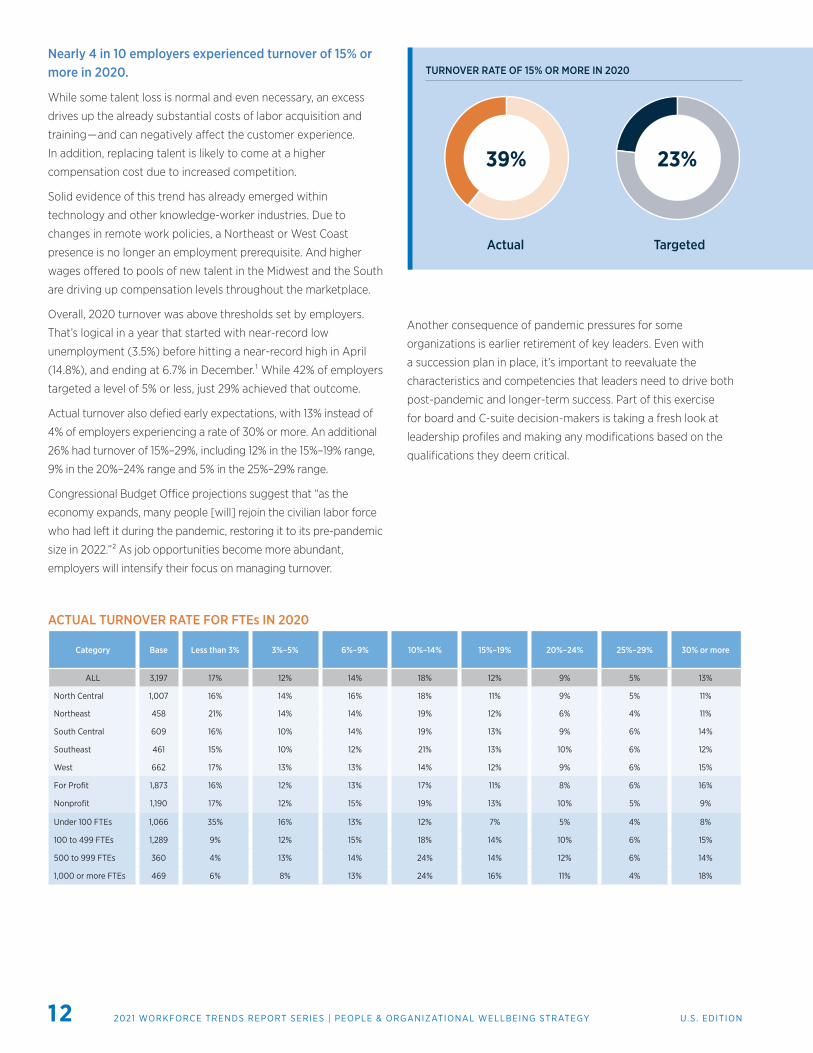

Nearly 4 in 10 employers experienced turnover of 15% or more in 2020.

While some talent loss is normal and even necessary, an excess

drives up the already substantial costs of labor acquisition and

training — and can negatively affect the customer experience.

In addition, replacing talent is likely to come at a higher

compensation cost due to increased competition.

Solid evidence of this trend has already emerged within

technology and other knowledge-worker industries. Due to

changes in remote work policies, a Northeast or West Coast

presence is no longer an employment prerequisite. And higher

wages offered to pools of new talent in the Midwest and the South

are driving up compensation levels throughout the marketplace.

Overall, 2020 turnover was above thresholds set by employers.

That’s logical in a year that started with near-record low

unemployment (3.5%) before hitting a near-record high in April

(14.8%), and ending at 6.7% in December.¹ While 42% of employers

targeted a level of 5% or less, just 29% achieved that outcome.

Actual turnover also defied early expectations, with 13% instead of

4% of employers experiencing a rate of 30% or more. An additional

26% had turnover of 15%–29%, including 12% in the 15%–19% range,

9% in the 20%–24% range and 5% in the 25%–29% range.

Congressional Budget Office projections suggest that “as the

economy expands, many people [will] rejoin the civilian labor force

who had left it during the pandemic, restoring it to its pre-pandemic

size in 2022.”² As job opportunities become more abundant,

employers will intensify their focus on managing turnover.

Another consequence of pandemic pressures for some

organizations is earlier retirement of key leaders. Even with

a succession plan in place, it’s important to reevaluate the

characteristics and competencies that leaders need to drive both

post-pandemic and longer-term success. Part of this exercise

for board and C-suite decision-makers is taking a fresh look at

leadership profiles and making any modifications based on the

qualifications they deem critical.

ACTUAL TURNOVER RATE FOR FTEs IN 2020

Category Base Less than 3% 3%–5% 6%–9% 10%–14% 15%–19% 20%–24% 25%–29% 30% or more

ALL 3,197 17% 12% 14% 18% 12% 9% 5% 13%

North Central 1,007 16% 14% 16% 18% 11% 9% 5% 11%

Northeast 458 21% 14% 14% 19% 12% 6% 4% 11%

South Central 609 16% 10% 14% 19% 13% 9% 6% 14%

Southeast 461 15% 10% 12% 21% 13% 10% 6% 12%

West 662 17% 13% 13% 14% 12% 9% 6% 15%

For Profit 1,873 16% 12% 13% 17% 11% 8% 6% 16%

Nonprofit 1,190 17% 12% 15% 19% 13% 10% 5% 9%

Under 100 FTEs 1,066 35% 16% 13% 12% 7% 5% 4% 8%

100 to 499 FTEs 1,289 9% 12% 15% 18% 14% 10% 6% 15%

500 to 999 FTEs 360 4% 13% 14% 24% 14% 12% 6% 14%

1,000 or more FTEs 469 6% 8% 13% 24% 16% 11% 4% 18%

TURNOVER RATE OF 15% OR MORE IN 2020

Actual Targeted

39% 23%

13GALLAGHER AJG.COM

RANK ATTRACTING AND RETAINING A COMPETITIVE WORKFORCE NO. 1

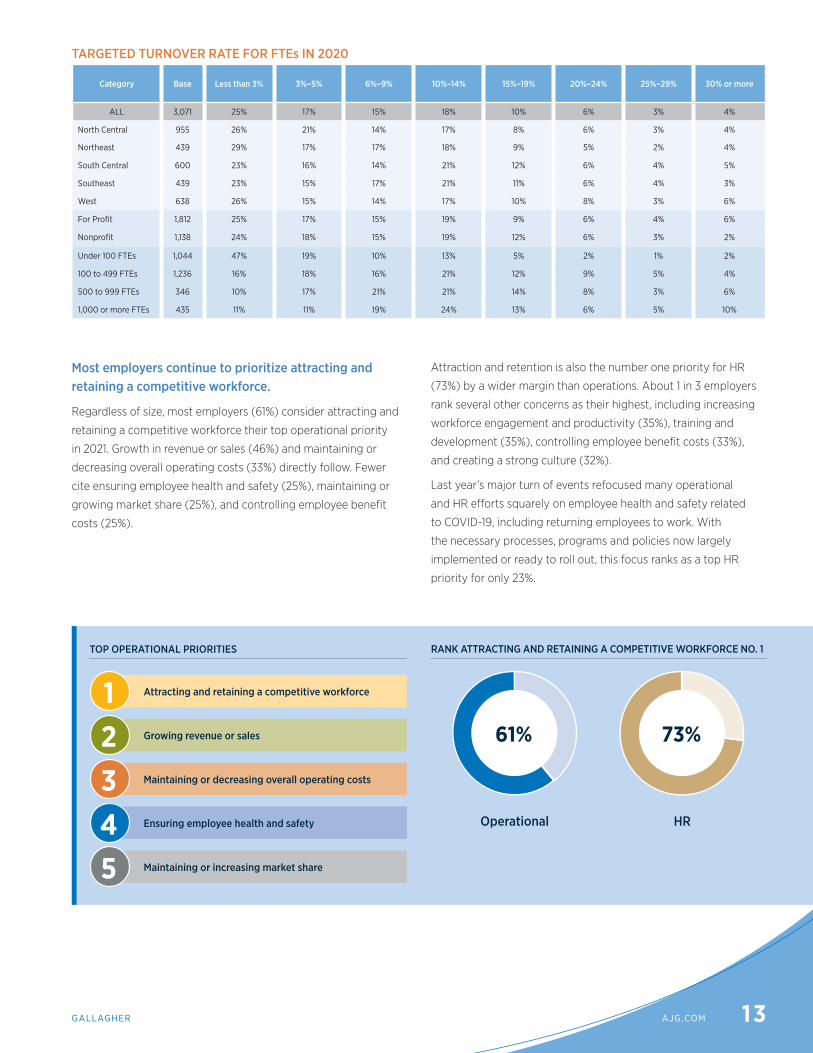

TARGETED TURNOVER RATE FOR FTEs IN 2020

Category Base Less than 3% 3%–5% 6%–9% 10%–14% 15%–19% 20%–24% 25%–29% 30% or more

ALL 3,071 25% 17% 15% 18% 10% 6% 3% 4%

North Central 955 26% 21% 14% 17% 8% 6% 3% 4%

Northeast 439 29% 17% 17% 18% 9% 5% 2% 4%

South Central 600 23% 16% 14% 21% 12% 6% 4% 5%

Southeast 439 23% 15% 17% 21% 11% 6% 4% 3%

West 638 26% 15% 14% 17% 10% 8% 3% 6%

For Profit 1,812 25% 17% 15% 19% 9% 6% 4% 6%

Nonprofit 1,138 24% 18% 15% 19% 12% 6% 3% 2%

Under 100 FTEs 1,044 47% 19% 10% 13% 5% 2% 1% 2%

100 to 499 FTEs 1,236 16% 18% 16% 21% 12% 9% 5% 4%

500 to 999 FTEs 346 10% 17% 21% 21% 14% 8% 3% 6%

1,000 or more FTEs 435 11% 11% 19% 24% 13% 6% 5% 10%

Most employers continue to prioritize attracting and retaining a competitive workforce.

Regardless of size, most employers (61%) consider attracting and

retaining a competitive workforce their top operational priority

in 2021. Growth in revenue or sales (46%) and maintaining or

decreasing overall operating costs (33%) directly follow. Fewer

cite ensuring employee health and safety (25%), maintaining or

growing market share (25%), and controlling employee benefit

costs (25%).

Attraction and retention is also the number one priority for HR

(73%) by a wider margin than operations. About 1 in 3 employers

rank several other concerns as their highest, including increasing

workforce engagement and productivity (35%), training and

development (35%), controlling employee benefit costs (33%),

and creating a strong culture (32%).

Last year’s major turn of events refocused many operational

and HR efforts squarely on employee health and safety related

to COVID-19, including returning employees to work. With

the necessary processes, programs and policies now largely

implemented or ready to roll out, this focus ranks as a top HR

priority for only 23%.

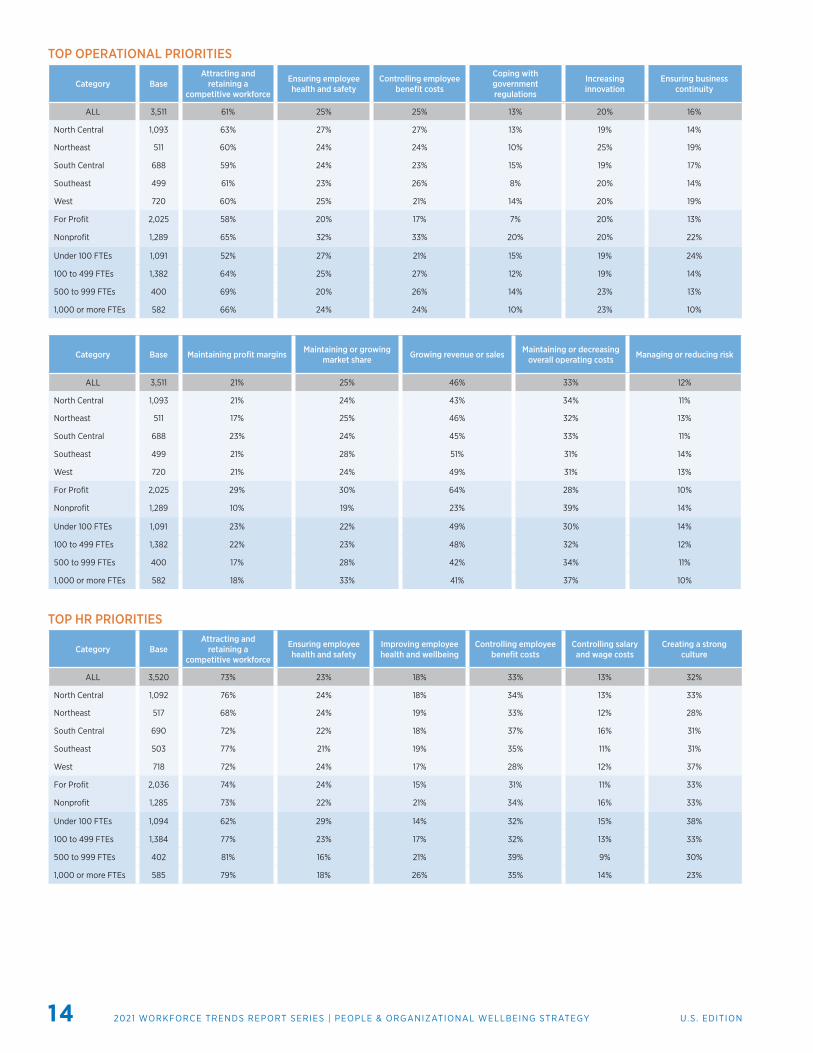

TOP OPERATIONAL PRIORITIES

Operational HR

Attracting and retaining a competitive workforce

Growing revenue or sales

Maintaining or decreasing overall operating costs

Ensuring employee health and safety

Maintaining or increasing market share

12345

61% 73%

14 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

TOP OPERATIONAL PRIORITIES

Category BaseAttracting and

retaining a competitive workforce

Ensuring employee health and safety

Controlling employee benefit costs

Coping with government regulations

Increasing innovation

Ensuring business continuity

ALL 3,511 61% 25% 25% 13% 20% 16%

North Central 1,093 63% 27% 27% 13% 19% 14%

Northeast 511 60% 24% 24% 10% 25% 19%

South Central 688 59% 24% 23% 15% 19% 17%

Southeast 499 61% 23% 26% 8% 20% 14%

West 720 60% 25% 21% 14% 20% 19%

For Profit 2,025 58% 20% 17% 7% 20% 13%

Nonprofit 1,289 65% 32% 33% 20% 20% 22%

Under 100 FTEs 1,091 52% 27% 21% 15% 19% 24%

100 to 499 FTEs 1,382 64% 25% 27% 12% 19% 14%

500 to 999 FTEs 400 69% 20% 26% 14% 23% 13%

1,000 or more FTEs 582 66% 24% 24% 10% 23% 10%

Category Base Maintaining profit margins Maintaining or growing market share Growing revenue or sales Maintaining or decreasing

overall operating costs Managing or reducing risk

ALL 3,511 21% 25% 46% 33% 12%

North Central 1,093 21% 24% 43% 34% 11%

Northeast 511 17% 25% 46% 32% 13%

South Central 688 23% 24% 45% 33% 11%

Southeast 499 21% 28% 51% 31% 14%

West 720 21% 24% 49% 31% 13%

For Profit 2,025 29% 30% 64% 28% 10%

Nonprofit 1,289 10% 19% 23% 39% 14%

Under 100 FTEs 1,091 23% 22% 49% 30% 14%

100 to 499 FTEs 1,382 22% 23% 48% 32% 12%

500 to 999 FTEs 400 17% 28% 42% 34% 11%

1,000 or more FTEs 582 18% 33% 41% 37% 10%

TOP HR PRIORITIES

Category BaseAttracting and

retaining a competitive workforce

Ensuring employee health and safety

Improving employee health and wellbeing

Controlling employee benefit costs

Controlling salary and wage costs

Creating a strong culture

ALL 3,520 73% 23% 18% 33% 13% 32%

North Central 1,092 76% 24% 18% 34% 13% 33%

Northeast 517 68% 24% 19% 33% 12% 28%

South Central 690 72% 22% 18% 37% 16% 31%

Southeast 503 77% 21% 19% 35% 11% 31%

West 718 72% 24% 17% 28% 12% 37%

For Profit 2,036 74% 24% 15% 31% 11% 33%

Nonprofit 1,285 73% 22% 21% 34% 16% 33%

Under 100 FTEs 1,094 62% 29% 14% 32% 15% 38%

100 to 499 FTEs 1,384 77% 23% 17% 32% 13% 33%

500 to 999 FTEs 402 81% 16% 21% 39% 9% 30%

1,000 or more FTEs 585 79% 18% 26% 35% 14% 23%

15GALLAGHER AJG.COM

TOTAL REWARDSEnhanced compensation and medical benefits are the most common total rewards boosters.

No matter how their relationship to organizational success is

perceived, compensation and benefits should form a solid core of

dependable resources for achieving recruitment, engagement and

retention goals. While 1 in 4 employers see them as a necessary

operating cost (25%), almost half (47%) consider them useful

tools for attracting and retaining talent. The rest (28%) value these

total rewards as strategic investments in maximizing workforce

performance to achieve operational outcomes. Increasingly, an

optimized return requires more than just competitive pay and

healthcare benefits.

Expecting and preparing to compete in a relatively tight labor

market, many employers advanced their efforts to enhance

total rewards in 2020 — before the pandemic altered plans or

put progress on hold. As prospects for an economic recovery

strengthen, they’re gearing up again to retain and attract key

talent. However, growing competition is increasing attention on

compensation, with 72% of employers enhancing base salary and

39% enhancing variable pay or bonus programs.

Medical is the top benefits category for enhancement, targeted

by over half of employers (55%). About 4 in 10 upgraded leave

policies (43%), voluntary or supplemental benefits (41%), and

retirement options (38%). And at least 3 in 10 enhanced wellbeing

initiatives (33%), dental benefits (31%) or life insurance (30%).

TOP HR PRIORITIES (CONT.)

Category BaseIncreasing workforce

engagement and productivity

Keeping remote employees connected

Increasing workforce inclusion and diversity

Training and developing employees

Complying with state and federal employee

regulations

ALL 3,520 35% 7% 17% 35% 11%

North Central 1,092 35% 6% 17% 33% 9%

Northeast 517 37% 11% 24% 33% 10%

South Central 690 35% 6% 10% 37% 13%

Southeast 503 35% 7% 20% 34% 10%

West 718 35% 8% 15% 38% 12%

For Profit 2,036 37% 8% 15% 39% 10%

Nonprofit 1,285 33% 7% 20% 29% 11%

Under 100 FTEs 1,094 36% 11% 11% 37% 13%

100 to 499 FTEs 1,384 35% 6% 16% 38% 9%

500 to 999 FTEs 402 34% 6% 19% 32% 10%

1,000 or more FTEs 585 36% 5% 27% 24% 11%

ORGANIZATION’S PERSPECTIVE ON COMPENSATION AND BENEFITS

Category Base Necessary operational costs Tools to attract and retain talent Investments in maximizing workforce performance to achieve operational outcomes

ALL 3,528 25% 47% 28%

North Central 1,112 23% 49% 28%

Northeast 504 26% 48% 26%

South Central 680 27% 44% 29%

Southeast 511 21% 50% 28%

West 721 27% 43% 30%

For Profit 2,042 23% 46% 31%

Nonprofit 1,289 27% 48% 25%

Under 100 FTEs 1,087 29% 40% 31%

100 to 499 FTEs 1,387 26% 47% 28%

500 to 999 FTEs 402 23% 51% 26%

1,000 or more FTEs 594 18% 56% 26%

16 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

COMPENSATION AND BENEFITS PLANNING HORIZON

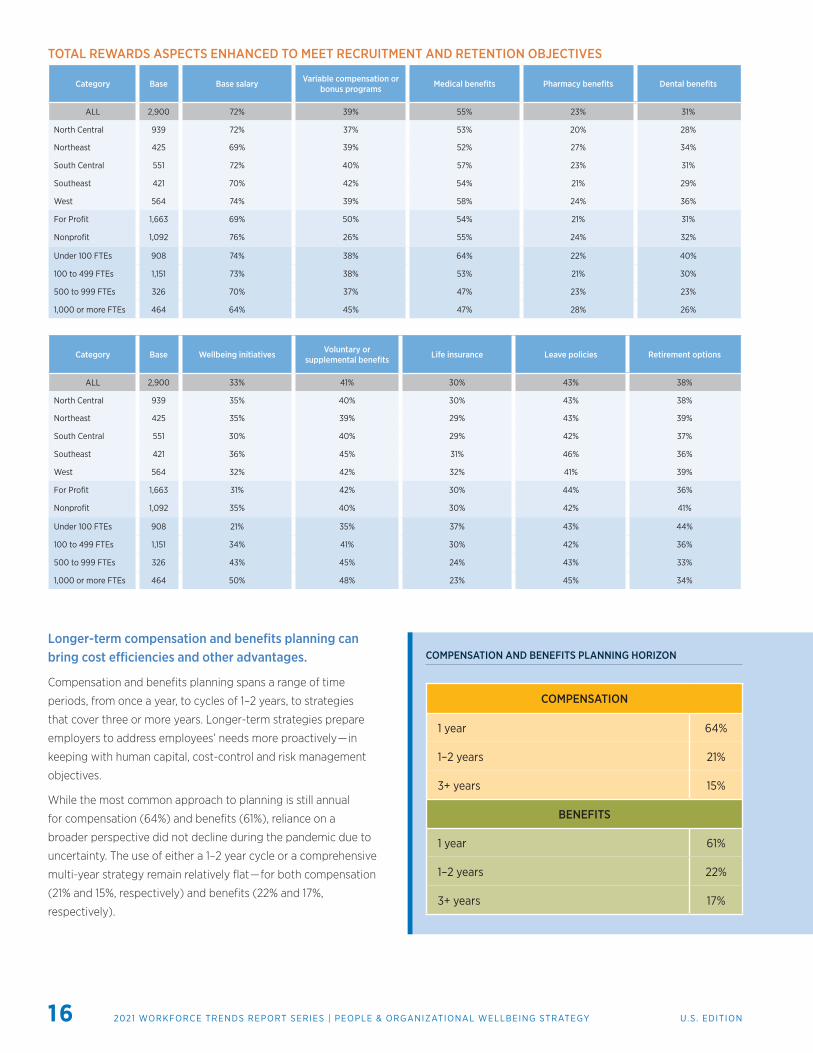

TOTAL REWARDS ASPECTS ENHANCED TO MEET RECRUITMENT AND RETENTION OBJECTIVES

Category Base Base salary Variable compensation or bonus programs Medical benefits Pharmacy benefits Dental benefits

ALL 2,900 72% 39% 55% 23% 31%

North Central 939 72% 37% 53% 20% 28%

Northeast 425 69% 39% 52% 27% 34%

South Central 551 72% 40% 57% 23% 31%

Southeast 421 70% 42% 54% 21% 29%

West 564 74% 39% 58% 24% 36%

For Profit 1,663 69% 50% 54% 21% 31%

Nonprofit 1,092 76% 26% 55% 24% 32%

Under 100 FTEs 908 74% 38% 64% 22% 40%

100 to 499 FTEs 1,151 73% 38% 53% 21% 30%

500 to 999 FTEs 326 70% 37% 47% 23% 23%

1,000 or more FTEs 464 64% 45% 47% 28% 26%

Category Base Wellbeing initiatives Voluntary or supplemental benefits Life insurance Leave policies Retirement options

ALL 2,900 33% 41% 30% 43% 38%

North Central 939 35% 40% 30% 43% 38%

Northeast 425 35% 39% 29% 43% 39%

South Central 551 30% 40% 29% 42% 37%

Southeast 421 36% 45% 31% 46% 36%

West 564 32% 42% 32% 41% 39%

For Profit 1,663 31% 42% 30% 44% 36%

Nonprofit 1,092 35% 40% 30% 42% 41%

Under 100 FTEs 908 21% 35% 37% 43% 44%

100 to 499 FTEs 1,151 34% 41% 30% 42% 36%

500 to 999 FTEs 326 43% 45% 24% 43% 33%

1,000 or more FTEs 464 50% 48% 23% 45% 34%

Longer-term compensation and benefits planning can bring cost efficiencies and other advantages.

Compensation and benefits planning spans a range of time

periods, from once a year, to cycles of 1–2 years, to strategies

that cover three or more years. Longer-term strategies prepare

employers to address employees’ needs more proactively — in

keeping with human capital, cost-control and risk management

objectives.

While the most common approach to planning is still annual

for compensation (64%) and benefits (61%), reliance on a

broader perspective did not decline during the pandemic due to

uncertainty. The use of either a 1–2 year cycle or a comprehensive

multi-year strategy remain relatively flat — for both compensation

(21% and 15%, respectively) and benefits (22% and 17%,

respectively).

COMPENSATION

1 year 64%

1–2 years 21%

3+ years 15%

BENEFITS

1 year 61%

1–2 years 22%

3+ years 17%

17GALLAGHER AJG.COM

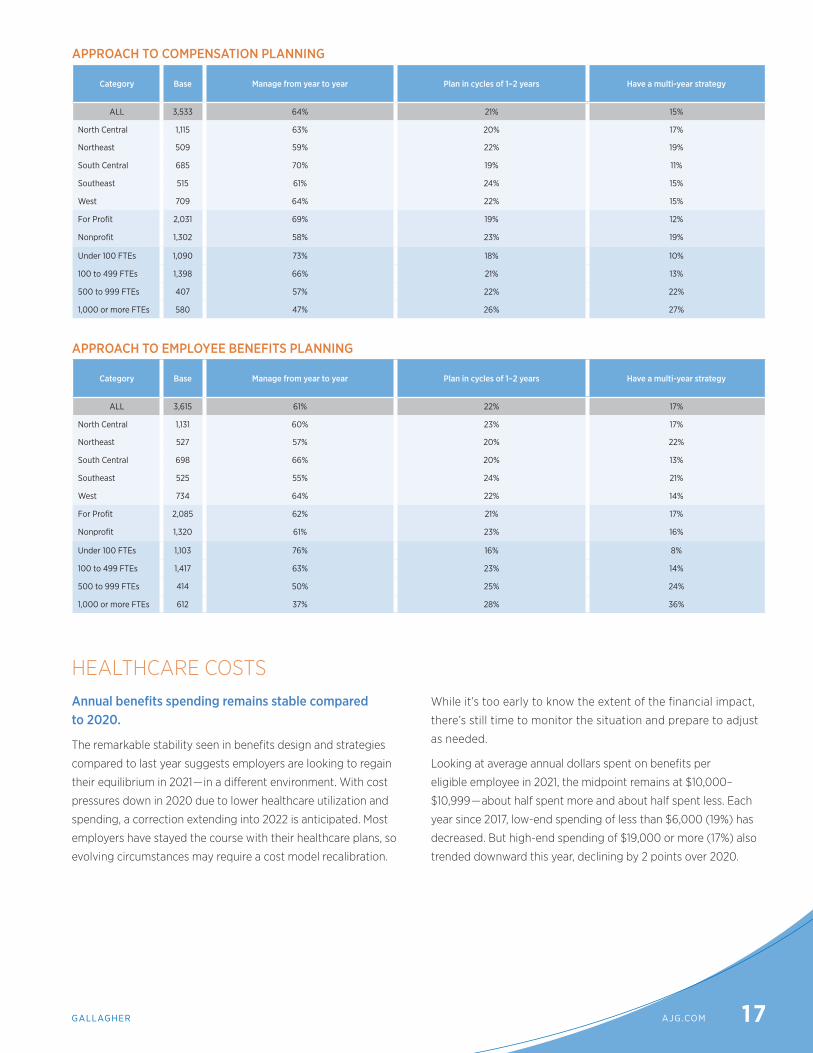

HEALTHCARE COSTSAnnual benefits spending remains stable compared to 2020.

The remarkable stability seen in benefits design and strategies

compared to last year suggests employers are looking to regain

their equilibrium in 2021 — in a different environment. With cost

pressures down in 2020 due to lower healthcare utilization and

spending, a correction extending into 2022 is anticipated. Most

employers have stayed the course with their healthcare plans, so

evolving circumstances may require a cost model recalibration.

While it’s too early to know the extent of the financial impact,

there’s still time to monitor the situation and prepare to adjust

as needed.

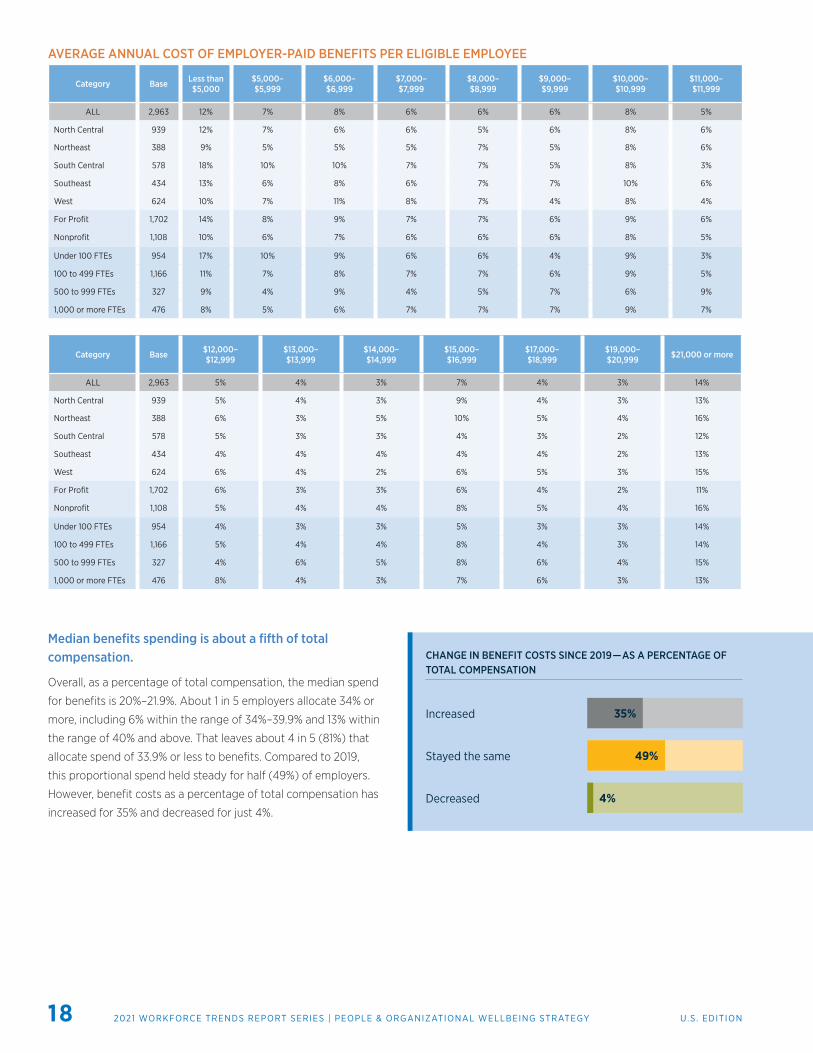

Looking at average annual dollars spent on benefits per

eligible employee in 2021, the midpoint remains at $10,000–

$10,999 — about half spent more and about half spent less. Each

year since 2017, low-end spending of less than $6,000 (19%) has

decreased. But high-end spending of $19,000 or more (17%) also

trended downward this year, declining by 2 points over 2020.

APPROACH TO COMPENSATION PLANNING

Category Base Manage from year to year Plan in cycles of 1–2 years Have a multi-year strategy

ALL 3,533 64% 21% 15%

North Central 1,115 63% 20% 17%

Northeast 509 59% 22% 19%

South Central 685 70% 19% 11%

Southeast 515 61% 24% 15%

West 709 64% 22% 15%

For Profit 2,031 69% 19% 12%

Nonprofit 1,302 58% 23% 19%

Under 100 FTEs 1,090 73% 18% 10%

100 to 499 FTEs 1,398 66% 21% 13%

500 to 999 FTEs 407 57% 22% 22%

1,000 or more FTEs 580 47% 26% 27%

APPROACH TO EMPLOYEE BENEFITS PLANNING

Category Base Manage from year to year Plan in cycles of 1–2 years Have a multi-year strategy

ALL 3,615 61% 22% 17%

North Central 1,131 60% 23% 17%

Northeast 527 57% 20% 22%

South Central 698 66% 20% 13%

Southeast 525 55% 24% 21%

West 734 64% 22% 14%

For Profit 2,085 62% 21% 17%

Nonprofit 1,320 61% 23% 16%

Under 100 FTEs 1,103 76% 16% 8%

100 to 499 FTEs 1,417 63% 23% 14%

500 to 999 FTEs 414 50% 25% 24%

1,000 or more FTEs 612 37% 28% 36%

18 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

AVERAGE ANNUAL COST OF EMPLOYER-PAID BENEFITS PER ELIGIBLE EMPLOYEE

Category Base Less than $5,000

$5,000–$5,999

$6,000–$6,999

$7,000–$7,999

$8,000–$8,999

$9,000–$9,999

$10,000–$10,999

$11,000–$11,999

ALL 2,963 12% 7% 8% 6% 6% 6% 8% 5%

North Central 939 12% 7% 6% 6% 5% 6% 8% 6%

Northeast 388 9% 5% 5% 5% 7% 5% 8% 6%

South Central 578 18% 10% 10% 7% 7% 5% 8% 3%

Southeast 434 13% 6% 8% 6% 7% 7% 10% 6%

West 624 10% 7% 11% 8% 7% 4% 8% 4%

For Profit 1,702 14% 8% 9% 7% 7% 6% 9% 6%

Nonprofit 1,108 10% 6% 7% 6% 6% 6% 8% 5%

Under 100 FTEs 954 17% 10% 9% 6% 6% 4% 9% 3%

100 to 499 FTEs 1,166 11% 7% 8% 7% 7% 6% 9% 5%

500 to 999 FTEs 327 9% 4% 9% 4% 5% 7% 6% 9%

1,000 or more FTEs 476 8% 5% 6% 7% 7% 7% 9% 7%

Category Base $12,000– $12,999

$13,000– $13,999

$14,000– $14,999

$15,000– $16,999

$17,000– $18,999

$19,000– $20,999 $21,000 or more

ALL 2,963 5% 4% 3% 7% 4% 3% 14%

North Central 939 5% 4% 3% 9% 4% 3% 13%

Northeast 388 6% 3% 5% 10% 5% 4% 16%

South Central 578 5% 3% 3% 4% 3% 2% 12%

Southeast 434 4% 4% 4% 4% 4% 2% 13%

West 624 6% 4% 2% 6% 5% 3% 15%

For Profit 1,702 6% 3% 3% 6% 4% 2% 11%

Nonprofit 1,108 5% 4% 4% 8% 5% 4% 16%

Under 100 FTEs 954 4% 3% 3% 5% 3% 3% 14%

100 to 499 FTEs 1,166 5% 4% 4% 8% 4% 3% 14%

500 to 999 FTEs 327 4% 6% 5% 8% 6% 4% 15%

1,000 or more FTEs 476 8% 4% 3% 7% 6% 3% 13%

Median benefits spending is about a fifth of total compensation.

Overall, as a percentage of total compensation, the median spend

for benefits is 20%–21.9%. About 1 in 5 employers allocate 34% or

more, including 6% within the range of 34%–39.9% and 13% within

the range of 40% and above. That leaves about 4 in 5 (81%) that

allocate spend of 33.9% or less to benefits. Compared to 2019,

this proportional spend held steady for half (49%) of employers.

However, benefit costs as a percentage of total compensation has

increased for 35% and decreased for just 4%.

CHANGE IN BENEFIT COSTS SINCE 2019 — AS A PERCENTAGE OF TOTAL COMPENSATION

Increased

Stayed the same

Decreased

35%

49%

4%

19GALLAGHER AJG.COM

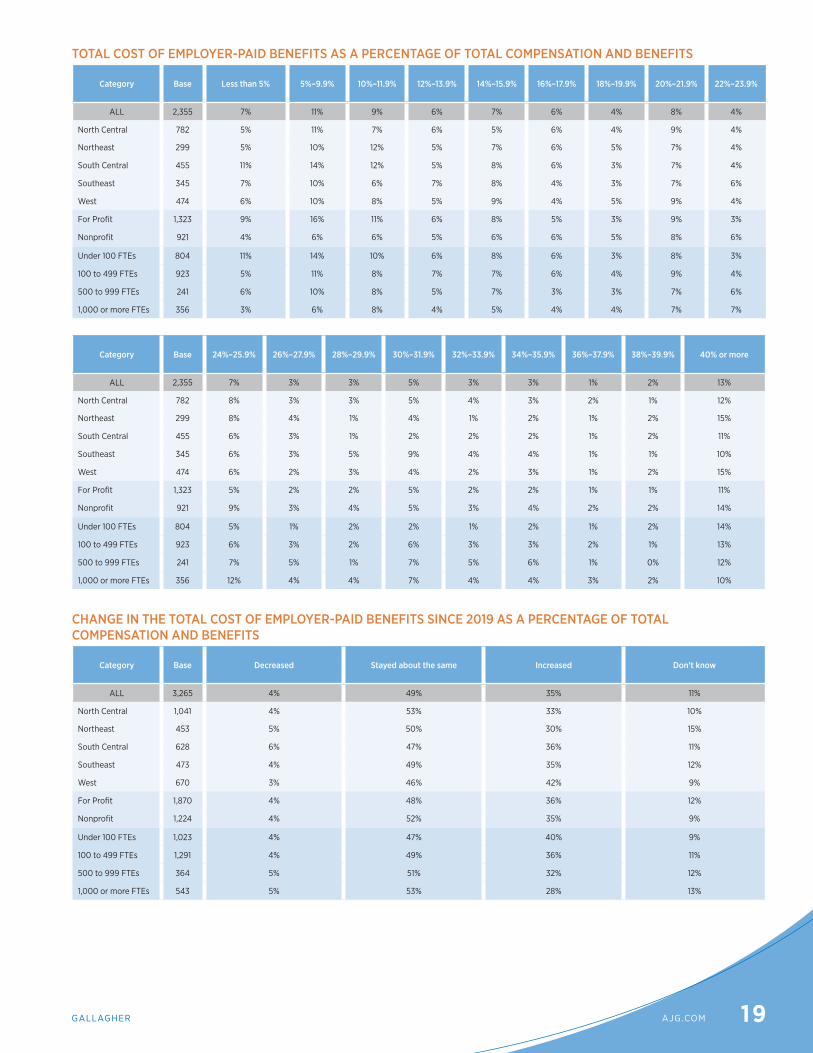

TOTAL COST OF EMPLOYER-PAID BENEFITS AS A PERCENTAGE OF TOTAL COMPENSATION AND BENEFITS

Category Base Less than 5% 5%–9.9% 10%–11.9% 12%–13.9% 14%–15.9% 16%–17.9% 18%–19.9% 20%–21.9% 22%–23.9%

ALL 2,355 7% 11% 9% 6% 7% 6% 4% 8% 4%

North Central 782 5% 11% 7% 6% 5% 6% 4% 9% 4%

Northeast 299 5% 10% 12% 5% 7% 6% 5% 7% 4%

South Central 455 11% 14% 12% 5% 8% 6% 3% 7% 4%

Southeast 345 7% 10% 6% 7% 8% 4% 3% 7% 6%

West 474 6% 10% 8% 5% 9% 4% 5% 9% 4%

For Profit 1,323 9% 16% 11% 6% 8% 5% 3% 9% 3%

Nonprofit 921 4% 6% 6% 5% 6% 6% 5% 8% 6%

Under 100 FTEs 804 11% 14% 10% 6% 8% 6% 3% 8% 3%

100 to 499 FTEs 923 5% 11% 8% 7% 7% 6% 4% 9% 4%

500 to 999 FTEs 241 6% 10% 8% 5% 7% 3% 3% 7% 6%

1,000 or more FTEs 356 3% 6% 8% 4% 5% 4% 4% 7% 7%

Category Base 24%–25.9% 26%–27.9% 28%–29.9% 30%–31.9% 32%–33.9% 34%–35.9% 36%–37.9% 38%–39.9% 40% or more

ALL 2,355 7% 3% 3% 5% 3% 3% 1% 2% 13%

North Central 782 8% 3% 3% 5% 4% 3% 2% 1% 12%

Northeast 299 8% 4% 1% 4% 1% 2% 1% 2% 15%

South Central 455 6% 3% 1% 2% 2% 2% 1% 2% 11%

Southeast 345 6% 3% 5% 9% 4% 4% 1% 1% 10%

West 474 6% 2% 3% 4% 2% 3% 1% 2% 15%

For Profit 1,323 5% 2% 2% 5% 2% 2% 1% 1% 11%

Nonprofit 921 9% 3% 4% 5% 3% 4% 2% 2% 14%

Under 100 FTEs 804 5% 1% 2% 2% 1% 2% 1% 2% 14%

100 to 499 FTEs 923 6% 3% 2% 6% 3% 3% 2% 1% 13%

500 to 999 FTEs 241 7% 5% 1% 7% 5% 6% 1% 0% 12%

1,000 or more FTEs 356 12% 4% 4% 7% 4% 4% 3% 2% 10%

CHANGE IN THE TOTAL COST OF EMPLOYER-PAID BENEFITS SINCE 2019 AS A PERCENTAGE OF TOTAL COMPENSATION AND BENEFITS

Category Base Decreased Stayed about the same Increased Don’t know

ALL 3,265 4% 49% 35% 11%

North Central 1,041 4% 53% 33% 10%

Northeast 453 5% 50% 30% 15%

South Central 628 6% 47% 36% 11%

Southeast 473 4% 49% 35% 12%

West 670 3% 46% 42% 9%

For Profit 1,870 4% 48% 36% 12%

Nonprofit 1,224 4% 52% 35% 9%

Under 100 FTEs 1,023 4% 47% 40% 9%

100 to 499 FTEs 1,291 4% 49% 36% 11%

500 to 999 FTEs 364 5% 51% 32% 12%

1,000 or more FTEs 543 5% 53% 28% 13%

20 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

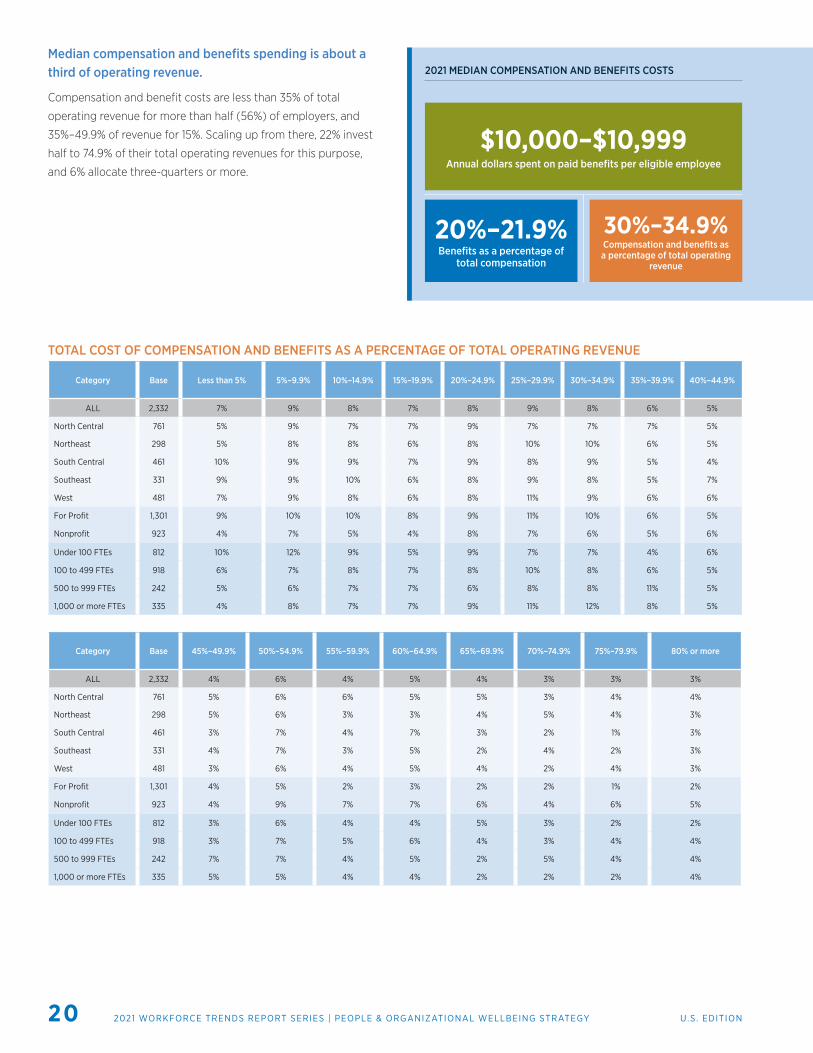

Median compensation and benefits spending is about a third of operating revenue.

Compensation and benefit costs are less than 35% of total

operating revenue for more than half (56%) of employers, and

35%–49.9% of revenue for 15%. Scaling up from there, 22% invest

half to 74.9% of their total operating revenues for this purpose,

and 6% allocate three-quarters or more.

TOTAL COST OF COMPENSATION AND BENEFITS AS A PERCENTAGE OF TOTAL OPERATING REVENUE

Category Base Less than 5% 5%–9.9% 10%–14.9% 15%–19.9% 20%–24.9% 25%–29.9% 30%–34.9% 35%–39.9% 40%–44.9%

ALL 2,332 7% 9% 8% 7% 8% 9% 8% 6% 5%

North Central 761 5% 9% 7% 7% 9% 7% 7% 7% 5%

Northeast 298 5% 8% 8% 6% 8% 10% 10% 6% 5%

South Central 461 10% 9% 9% 7% 9% 8% 9% 5% 4%

Southeast 331 9% 9% 10% 6% 8% 9% 8% 5% 7%

West 481 7% 9% 8% 6% 8% 11% 9% 6% 6%

For Profit 1,301 9% 10% 10% 8% 9% 11% 10% 6% 5%

Nonprofit 923 4% 7% 5% 4% 8% 7% 6% 5% 6%

Under 100 FTEs 812 10% 12% 9% 5% 9% 7% 7% 4% 6%

100 to 499 FTEs 918 6% 7% 8% 7% 8% 10% 8% 6% 5%

500 to 999 FTEs 242 5% 6% 7% 7% 6% 8% 8% 11% 5%

1,000 or more FTEs 335 4% 8% 7% 7% 9% 11% 12% 8% 5%

Category Base 45%–49.9% 50%–54.9% 55%–59.9% 60%–64.9% 65%–69.9% 70%–74.9% 75%–79.9% 80% or more

ALL 2,332 4% 6% 4% 5% 4% 3% 3% 3%

North Central 761 5% 6% 6% 5% 5% 3% 4% 4%

Northeast 298 5% 6% 3% 3% 4% 5% 4% 3%

South Central 461 3% 7% 4% 7% 3% 2% 1% 3%

Southeast 331 4% 7% 3% 5% 2% 4% 2% 3%

West 481 3% 6% 4% 5% 4% 2% 4% 3%

For Profit 1,301 4% 5% 2% 3% 2% 2% 1% 2%

Nonprofit 923 4% 9% 7% 7% 6% 4% 6% 5%

Under 100 FTEs 812 3% 6% 4% 4% 5% 3% 2% 2%

100 to 499 FTEs 918 3% 7% 5% 6% 4% 3% 4% 4%

500 to 999 FTEs 242 7% 7% 4% 5% 2% 5% 4% 4%

1,000 or more FTEs 335 5% 5% 4% 4% 2% 2% 2% 4%

2021 MEDIAN COMPENSATION AND BENEFITS COSTS

20%–21.9%Benefits as a percentage of

total compensation

$10,000–$10,999Annual dollars spent on paid benefits per eligible employee

30%–34.9%Compensation and benefits as a percentage of total operating

revenue

21GALLAGHER AJG.COM

Most employers expect moderate healthcare cost increases in 2021.

Reduced healthcare costs took many self-insured employers by

surprise last year. Major factors underlying this anomaly include

a substantial number of canceled or deferred doctor visits, for

both routine care and elective procedures. Favorable cash flow

was the unanticipated outcome of lower healthcare system

utilization — which outweighed any increased burden of direct

claims related to COVID-19.

However, the trade-off for the diminished pandemic threat and

healthier economy anticipated in 2021 is likely to be higher health

costs. More than 7 in 10 employers expect a significant (7%) or

moderate (65%) rise, while less than 1 in 10 foresee a moderate

(8%) or significant (1%) decline. Just 14% think costs will stay

about the same. Besides a return to preventive and elective care

by health plan participants, a probable contributor to an upswing

in costs is treatment for health issues that went undetected due to

avoidance of medical services.³

Responses to emotional wellbeing and mental health are a core

employer focus this year, including communicating effectively with

employees about related needs. The attention on vaccinations

creates an opening to bring this concern, exacerbated by the

pandemic, to the forefront.

Going beyond the basics of informing the workforce about

benefits and enrollment, a more comprehensive and cohesive

communication approach drives more appropriate use. By

encouraging and enabling employees to manage their wellbeing

better, healthcare costs are mitigated.

EXPECTED DIFFERENCE IN HEALTHCARE COSTS FOR 2021 COMPARED TO 2020

Category Base Significantly higher Somewhat higher No difference Somewhat lower Significantly lower Don’t know

ALL 3,234 7% 65% 14% 8% 1% 6%

North Central 1,052 6% 66% 13% 8% 1% 6%

Northeast 466 7% 62% 14% 10% 2% 6%

South Central 618 7% 62% 14% 9% 1% 6%

Southeast 471 7% 63% 15% 8% 0% 6%

West 627 7% 70% 12% 6% 1% 4%

For Profit 1,849 7% 65% 14% 7% 1% 5%

Nonprofit 1,212 6% 66% 14% 8% 1% 6%

Under 100 FTEs 997 10% 62% 14% 8% 2% 5%

100 to 499 FTEs 1,262 6% 64% 14% 8% 1% 7%

500 to 999 FTEs 381 4% 68% 15% 8% 1% 4%

1,000 or more FTEs 540 6% 71% 11% 6% 1% 4%

EXPECTED CHANGE IN HEALTHCARE COSTS — 2021 VS. 2020

Higher

No change

Lower

72%

14%

9%

22 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

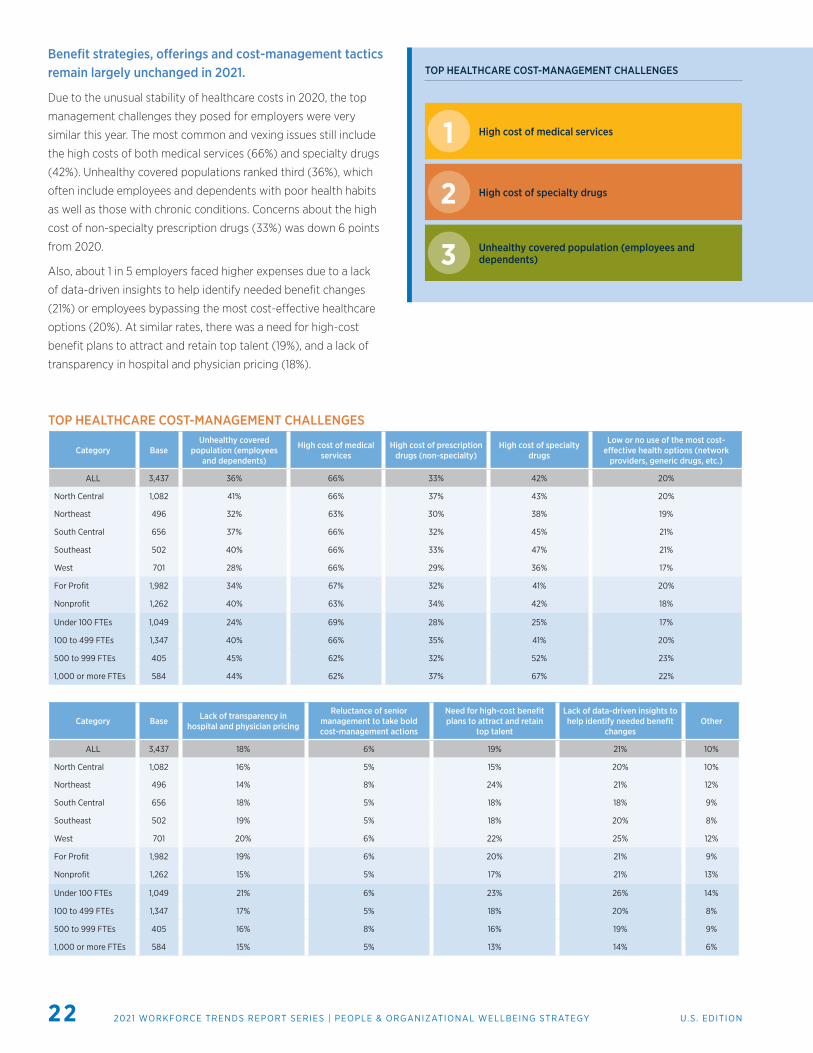

TOP HEALTHCARE COST-MANAGEMENT CHALLENGESBenefit strategies, offerings and cost-management tactics remain largely unchanged in 2021.

Due to the unusual stability of healthcare costs in 2020, the top

management challenges they posed for employers were very

similar this year. The most common and vexing issues still include

the high costs of both medical services (66%) and specialty drugs

(42%). Unhealthy covered populations ranked third (36%), which

often include employees and dependents with poor health habits

as well as those with chronic conditions. Concerns about the high

cost of non-specialty prescription drugs (33%) was down 6 points

from 2020.

Also, about 1 in 5 employers faced higher expenses due to a lack

of data-driven insights to help identify needed benefit changes

(21%) or employees bypassing the most cost-effective healthcare

options (20%). At similar rates, there was a need for high-cost

benefit plans to attract and retain top talent (19%), and a lack of

transparency in hospital and physician pricing (18%).

High cost of medical services

High cost of specialty drugs

Unhealthy covered population (employees and dependents)

1

2

3

TOP HEALTHCARE COST-MANAGEMENT CHALLENGES

Category BaseUnhealthy covered

population (employees and dependents)

High cost of medical services

High cost of prescription drugs (non-specialty)

High cost of specialty drugs

Low or no use of the most cost-effective health options (network

providers, generic drugs, etc.)

ALL 3,437 36% 66% 33% 42% 20%

North Central 1,082 41% 66% 37% 43% 20%

Northeast 496 32% 63% 30% 38% 19%

South Central 656 37% 66% 32% 45% 21%

Southeast 502 40% 66% 33% 47% 21%

West 701 28% 66% 29% 36% 17%

For Profit 1,982 34% 67% 32% 41% 20%

Nonprofit 1,262 40% 63% 34% 42% 18%

Under 100 FTEs 1,049 24% 69% 28% 25% 17%

100 to 499 FTEs 1,347 40% 66% 35% 41% 20%

500 to 999 FTEs 405 45% 62% 32% 52% 23%

1,000 or more FTEs 584 44% 62% 37% 67% 22%

Category Base Lack of transparency in hospital and physician pricing

Reluctance of senior management to take bold cost-management actions

Need for high-cost benefit plans to attract and retain

top talent

Lack of data-driven insights to help identify needed benefit

changes Other

ALL 3,437 18% 6% 19% 21% 10%

North Central 1,082 16% 5% 15% 20% 10%

Northeast 496 14% 8% 24% 21% 12%

South Central 656 18% 5% 18% 18% 9%

Southeast 502 19% 5% 18% 20% 8%

West 701 20% 6% 22% 25% 12%

For Profit 1,982 19% 6% 20% 21% 9%

Nonprofit 1,262 15% 5% 17% 21% 13%

Under 100 FTEs 1,049 21% 6% 23% 26% 14%

100 to 499 FTEs 1,347 17% 5% 18% 20% 8%

500 to 999 FTEs 405 16% 8% 16% 19% 9%

1,000 or more FTEs 584 15% 5% 13% 14% 6%

23GALLAGHER AJG.COM

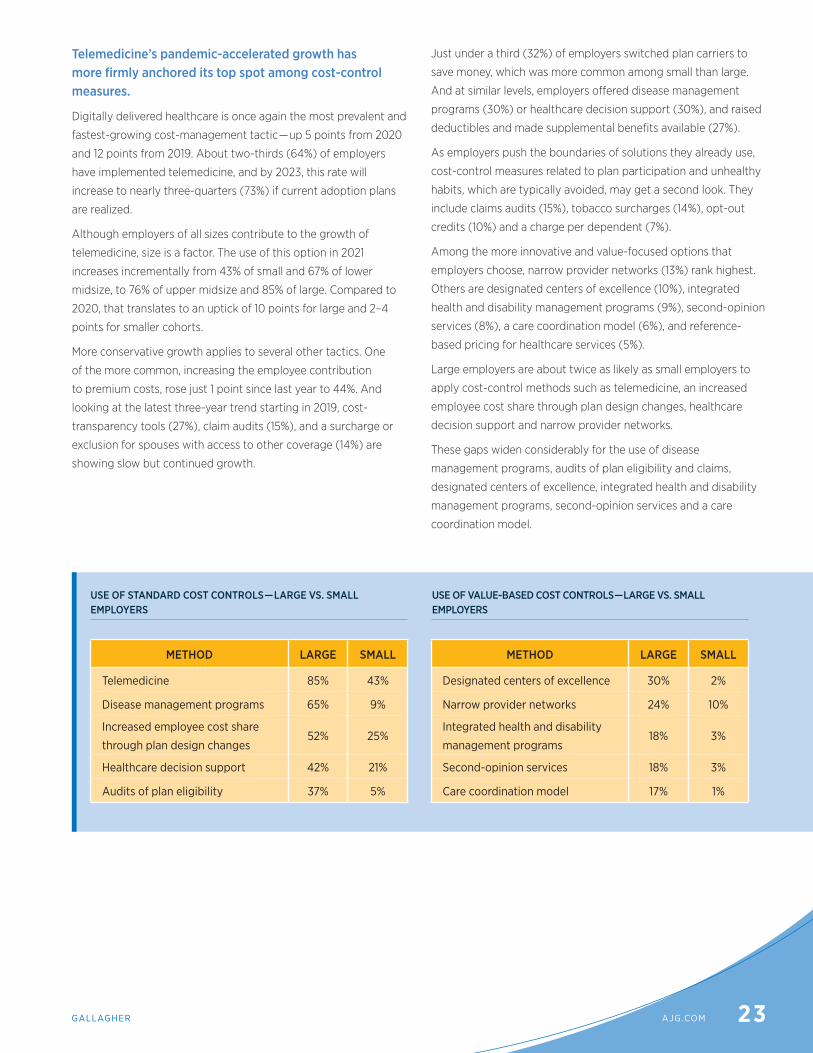

Telemedicine’s pandemic-accelerated growth has more firmly anchored its top spot among cost-control measures.

Digitally delivered healthcare is once again the most prevalent and

fastest-growing cost-management tactic — up 5 points from 2020

and 12 points from 2019. About two-thirds (64%) of employers

have implemented telemedicine, and by 2023, this rate will

increase to nearly three-quarters (73%) if current adoption plans

are realized.

Although employers of all sizes contribute to the growth of

telemedicine, size is a factor. The use of this option in 2021

increases incrementally from 43% of small and 67% of lower

midsize, to 76% of upper midsize and 85% of large. Compared to

2020, that translates to an uptick of 10 points for large and 2–4

points for smaller cohorts.

More conservative growth applies to several other tactics. One

of the more common, increasing the employee contribution

to premium costs, rose just 1 point since last year to 44%. And

looking at the latest three-year trend starting in 2019, cost-

transparency tools (27%), claim audits (15%), and a surcharge or

exclusion for spouses with access to other coverage (14%) are

showing slow but continued growth.

Just under a third (32%) of employers switched plan carriers to

save money, which was more common among small than large.

And at similar levels, employers offered disease management

programs (30%) or healthcare decision support (30%), and raised

deductibles and made supplemental benefits available (27%).

As employers push the boundaries of solutions they already use,

cost-control measures related to plan participation and unhealthy

habits, which are typically avoided, may get a second look. They

include claims audits (15%), tobacco surcharges (14%), opt-out

credits (10%) and a charge per dependent (7%).

Among the more innovative and value-focused options that

employers choose, narrow provider networks (13%) rank highest.

Others are designated centers of excellence (10%), integrated

health and disability management programs (9%), second-opinion

services (8%), a care coordination model (6%), and reference-

based pricing for healthcare services (5%).

Large employers are about twice as likely as small employers to

apply cost-control methods such as telemedicine, an increased

employee cost share through plan design changes, healthcare

decision support and narrow provider networks.

These gaps widen considerably for the use of disease

management programs, audits of plan eligibility and claims,

designated centers of excellence, integrated health and disability

management programs, second-opinion services and a care

coordination model.

USE OF VALUE-BASED COST CONTROLS — LARGE VS. SMALL EMPLOYERS

USE OF STANDARD COST CONTROLS — LARGE VS. SMALL EMPLOYERS

METHOD LARGE SMALL

Telemedicine 85% 43%

Disease management programs 65% 9%

Increased employee cost share

through plan design changes52% 25%

Healthcare decision support 42% 21%

Audits of plan eligibility 37% 5%

METHOD LARGE SMALL

Designated centers of excellence 30% 2%

Narrow provider networks 24% 10%

Integrated health and disability

management programs18% 3%

Second-opinion services 18% 3%

Care coordination model 17% 1%

24 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

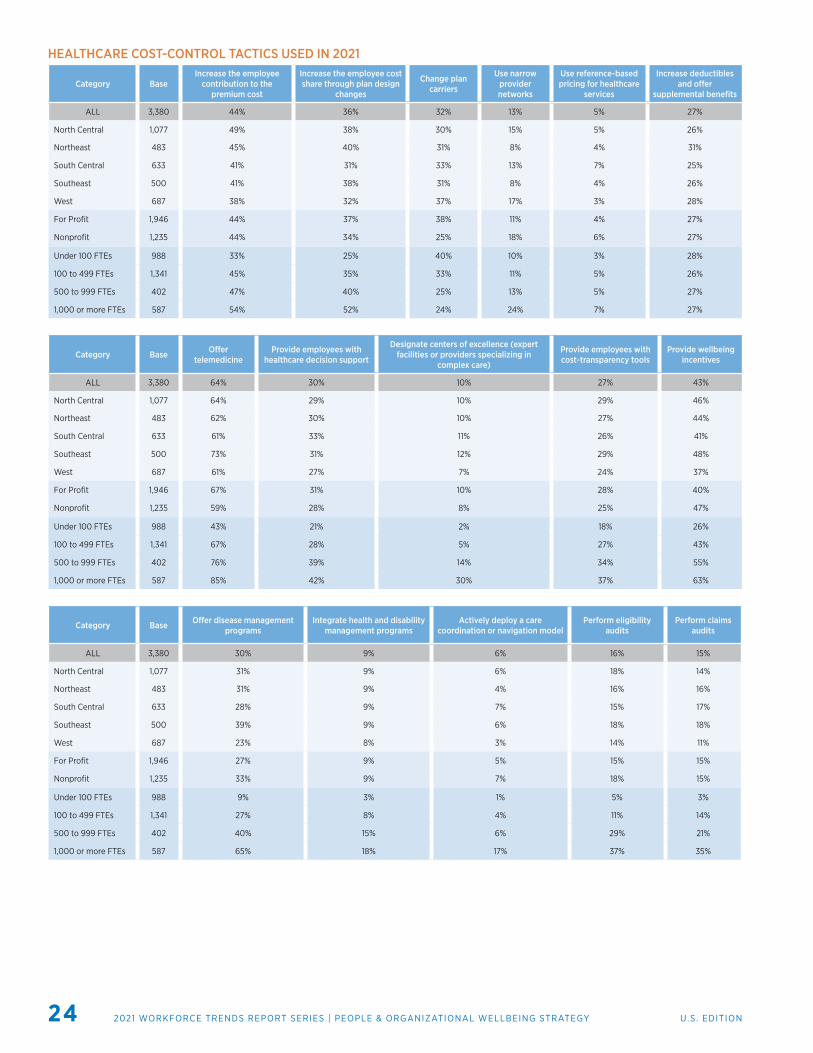

HEALTHCARE COST-CONTROL TACTICS USED IN 2021

Category BaseIncrease the employee

contribution to the premium cost

Increase the employee cost share through plan design

changes

Change plan carriers

Use narrow provider networks

Use reference-based pricing for healthcare

services

Increase deductibles and offer

supplemental benefits

ALL 3,380 44% 36% 32% 13% 5% 27%

North Central 1,077 49% 38% 30% 15% 5% 26%

Northeast 483 45% 40% 31% 8% 4% 31%

South Central 633 41% 31% 33% 13% 7% 25%

Southeast 500 41% 38% 31% 8% 4% 26%

West 687 38% 32% 37% 17% 3% 28%

For Profit 1,946 44% 37% 38% 11% 4% 27%

Nonprofit 1,235 44% 34% 25% 18% 6% 27%

Under 100 FTEs 988 33% 25% 40% 10% 3% 28%

100 to 499 FTEs 1,341 45% 35% 33% 11% 5% 26%

500 to 999 FTEs 402 47% 40% 25% 13% 5% 27%

1,000 or more FTEs 587 54% 52% 24% 24% 7% 27%

Category Base Offer telemedicine

Provide employees with healthcare decision support

Designate centers of excellence (expert facilities or providers specializing in

complex care)

Provide employees with cost-transparency tools

Provide wellbeing incentives

ALL 3,380 64% 30% 10% 27% 43%

North Central 1,077 64% 29% 10% 29% 46%

Northeast 483 62% 30% 10% 27% 44%

South Central 633 61% 33% 11% 26% 41%

Southeast 500 73% 31% 12% 29% 48%

West 687 61% 27% 7% 24% 37%

For Profit 1,946 67% 31% 10% 28% 40%

Nonprofit 1,235 59% 28% 8% 25% 47%

Under 100 FTEs 988 43% 21% 2% 18% 26%

100 to 499 FTEs 1,341 67% 28% 5% 27% 43%

500 to 999 FTEs 402 76% 39% 14% 34% 55%

1,000 or more FTEs 587 85% 42% 30% 37% 63%

Category Base Offer disease management programs

Integrate health and disability management programs

Actively deploy a care coordination or navigation model

Perform eligibility audits

Perform claims audits

ALL 3,380 30% 9% 6% 16% 15%

North Central 1,077 31% 9% 6% 18% 14%

Northeast 483 31% 9% 4% 16% 16%

South Central 633 28% 9% 7% 15% 17%

Southeast 500 39% 9% 6% 18% 18%

West 687 23% 8% 3% 14% 11%

For Profit 1,946 27% 9% 5% 15% 15%

Nonprofit 1,235 33% 9% 7% 18% 15%

Under 100 FTEs 988 9% 3% 1% 5% 3%

100 to 499 FTEs 1,341 27% 8% 4% 11% 14%

500 to 999 FTEs 402 40% 15% 6% 29% 21%

1,000 or more FTEs 587 65% 18% 17% 37% 35%

25GALLAGHER AJG.COM

USE OF COST-MANAGEMENT TACTICS — PROJECTED INCREASE OF 20% OR MORE BY 2023

HEALTHCARE COST-CONTROL TACTICS EXPECTED TO BE IMPLEMENTED BY 2023

Category BaseIncrease the employee

contribution to the premium cost

Increase the employee cost share through plan design

changes

Change plan carriers

Use narrow provider networks

Use reference-based pricing for healthcare

services

Increase deductibles and offer

supplemental benefits

ALL 1,555 19% 24% 15% 6% 7% 16%

North Central 501 18% 26% 14% 5% 7% 17%

Northeast 239 18% 23% 18% 6% 11% 17%

South Central 318 21% 25% 14% 4% 5% 16%

Southeast 202 20% 19% 15% 5% 7% 15%

West 295 22% 22% 13% 9% 7% 14%

For Profit 906 19% 23% 15% 5% 7% 17%

Nonprofit 594 21% 24% 14% 6% 8% 15%

Under 100 FTEs 519 19% 24% 16% 5% 6% 14%

100 to 499 FTEs 605 19% 24% 16% 5% 8% 15%

500 to 999 FTEs 163 27% 26% 10% 6% 7% 21%

1,000 or more FTEs 226 15% 19% 12% 9% 11% 19%

Adoption of cost-management tactics is expected to pick up over the next two years.

By 2023, the use of several popular cost-management tactics is

expected to rise by 20% or more, including cost sharing through

plan design changes (24%), wellbeing incentives (22%), cost-

transparency tools (22%) and healthcare decision support (20%).

Nearly as many employers, 19%, plan to increase employee

contributions to the cost of premiums, while 16% plan to increase

deductibles and offer employee-paid supplemental benefits. At

declining rates, forecasts also include changing plan carriers (15%),

adding disease management programs (11%), and performing

eligibility (10%) and claims audits (10%). Planned adoption of

other cost-control tactics stands at 9% or less.

Cost sharing through plan design changes

Wellbeing incentives

Healthcare decision support

Cost-transparency tools

24%

22%

22%

20%

HEALTHCARE COST-CONTROL TACTICS USED IN 2021 (CONT.)

Category Base Offer second-opinion services

Provide nonsmokers a discount on premiums (smoker or

tobacco surcharge)

Apply a separate charge per dependent

Apply a surcharge or exclusion for spouses with access to other coverage

Offer an opt-out credit to employees who waive

coverage

ALL 3,380 8% 14% 7% 14% 10%

North Central 1,077 7% 16% 7% 22% 12%

Northeast 483 9% 11% 4% 13% 15%

South Central 633 9% 14% 7% 12% 4%

Southeast 500 7% 19% 7% 15% 8%

West 687 7% 7% 9% 5% 12%

For Profit 1,946 8% 16% 7% 15% 8%

Nonprofit 1,235 7% 10% 7% 14% 13%

Under 100 FTEs 988 3% 4% 12% 6% 10%

100 to 499 FTEs 1,341 6% 13% 5% 12% 12%

500 to 999 FTEs 402 8% 17% 5% 19% 12%

1,000 or more FTEs 587 18% 30% 3% 29% 7%

26 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

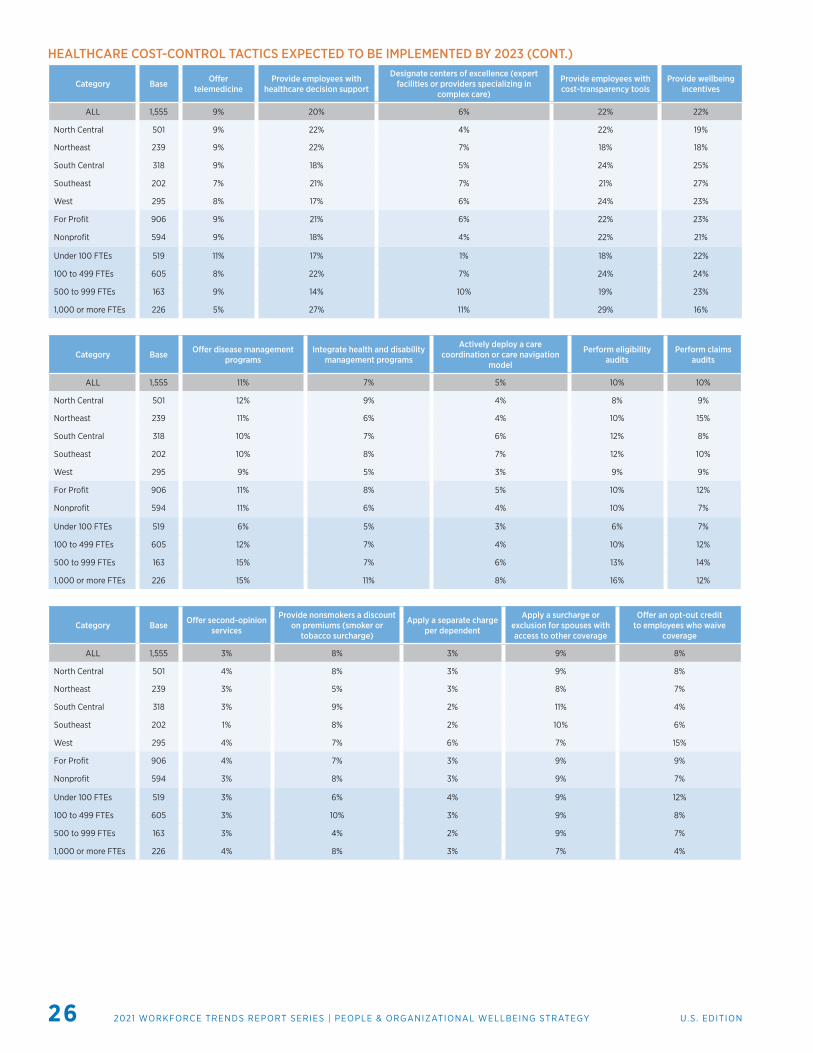

HEALTHCARE COST-CONTROL TACTICS EXPECTED TO BE IMPLEMENTED BY 2023 (CONT.)

Category Base Offer telemedicine

Provide employees with healthcare decision support

Designate centers of excellence (expert facilities or providers specializing in

complex care)

Provide employees with cost-transparency tools

Provide wellbeing incentives

ALL 1,555 9% 20% 6% 22% 22%

North Central 501 9% 22% 4% 22% 19%

Northeast 239 9% 22% 7% 18% 18%

South Central 318 9% 18% 5% 24% 25%

Southeast 202 7% 21% 7% 21% 27%

West 295 8% 17% 6% 24% 23%

For Profit 906 9% 21% 6% 22% 23%

Nonprofit 594 9% 18% 4% 22% 21%

Under 100 FTEs 519 11% 17% 1% 18% 22%

100 to 499 FTEs 605 8% 22% 7% 24% 24%

500 to 999 FTEs 163 9% 14% 10% 19% 23%

1,000 or more FTEs 226 5% 27% 11% 29% 16%

Category Base Offer disease management programs

Integrate health and disability management programs

Actively deploy a care coordination or care navigation

model

Perform eligibility audits

Perform claims audits

ALL 1,555 11% 7% 5% 10% 10%

North Central 501 12% 9% 4% 8% 9%

Northeast 239 11% 6% 4% 10% 15%

South Central 318 10% 7% 6% 12% 8%

Southeast 202 10% 8% 7% 12% 10%

West 295 9% 5% 3% 9% 9%

For Profit 906 11% 8% 5% 10% 12%

Nonprofit 594 11% 6% 4% 10% 7%

Under 100 FTEs 519 6% 5% 3% 6% 7%

100 to 499 FTEs 605 12% 7% 4% 10% 12%

500 to 999 FTEs 163 15% 7% 6% 13% 14%

1,000 or more FTEs 226 15% 11% 8% 16% 12%

Category Base Offer second-opinion services

Provide nonsmokers a discount on premiums (smoker or

tobacco surcharge)

Apply a separate charge per dependent

Apply a surcharge or exclusion for spouses with access to other coverage

Offer an opt-out credit to employees who waive

coverage

ALL 1,555 3% 8% 3% 9% 8%

North Central 501 4% 8% 3% 9% 8%

Northeast 239 3% 5% 3% 8% 7%

South Central 318 3% 9% 2% 11% 4%

Southeast 202 1% 8% 2% 10% 6%

West 295 4% 7% 6% 7% 15%

For Profit 906 4% 7% 3% 9% 9%

Nonprofit 594 3% 8% 3% 9% 7%

Under 100 FTEs 519 3% 6% 4% 9% 12%

100 to 499 FTEs 605 3% 10% 3% 9% 8%

500 to 999 FTEs 163 3% 4% 2% 9% 7%

1,000 or more FTEs 226 4% 8% 3% 7% 4%

27GALLAGHER AJG.COM

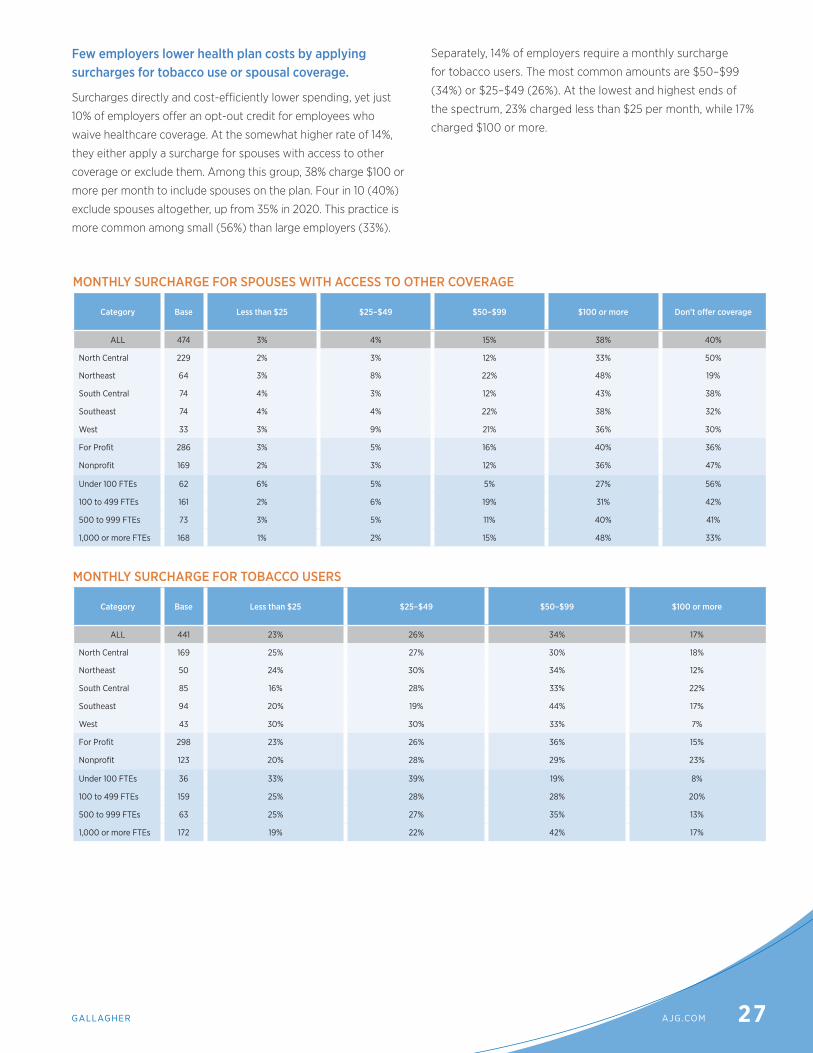

Few employers lower health plan costs by applying surcharges for tobacco use or spousal coverage.

Surcharges directly and cost-efficiently lower spending, yet just

10% of employers offer an opt-out credit for employees who

waive healthcare coverage. At the somewhat higher rate of 14%,

they either apply a surcharge for spouses with access to other

coverage or exclude them. Among this group, 38% charge $100 or

more per month to include spouses on the plan. Four in 10 (40%)

exclude spouses altogether, up from 35% in 2020. This practice is

more common among small (56%) than large employers (33%).

Separately, 14% of employers require a monthly surcharge

for tobacco users. The most common amounts are $50–$99

(34%) or $25–$49 (26%). At the lowest and highest ends of

the spectrum, 23% charged less than $25 per month, while 17%

charged $100 or more.

MONTHLY SURCHARGE FOR SPOUSES WITH ACCESS TO OTHER COVERAGE

Category Base Less than $25 $25–$49 $50–$99 $100 or more Don’t offer coverage

ALL 474 3% 4% 15% 38% 40%

North Central 229 2% 3% 12% 33% 50%

Northeast 64 3% 8% 22% 48% 19%

South Central 74 4% 3% 12% 43% 38%

Southeast 74 4% 4% 22% 38% 32%

West 33 3% 9% 21% 36% 30%

For Profit 286 3% 5% 16% 40% 36%

Nonprofit 169 2% 3% 12% 36% 47%

Under 100 FTEs 62 6% 5% 5% 27% 56%

100 to 499 FTEs 161 2% 6% 19% 31% 42%

500 to 999 FTEs 73 3% 5% 11% 40% 41%

1,000 or more FTEs 168 1% 2% 15% 48% 33%

MONTHLY SURCHARGE FOR TOBACCO USERS

Category Base Less than $25 $25–$49 $50–$99 $100 or more

ALL 441 23% 26% 34% 17%

North Central 169 25% 27% 30% 18%

Northeast 50 24% 30% 34% 12%

South Central 85 16% 28% 33% 22%

Southeast 94 20% 19% 44% 17%

West 43 30% 30% 33% 7%

For Profit 298 23% 26% 36% 15%

Nonprofit 123 20% 28% 29% 23%

Under 100 FTEs 36 33% 39% 19% 8%

100 to 499 FTEs 159 25% 28% 28% 20%

500 to 999 FTEs 63 25% 27% 35% 13%

1,000 or more FTEs 172 19% 22% 42% 17%

28 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

KEY TAKEAWAYSVirtual permanence — the transition to virtual workplaces as part of a standard operational structure — is creating broad access to non-local talent pools. As the economic recovery takes hold, organizations also see these fading geographic boundaries as new opportunities for engaging clients and increasing revenues. This reconfiguration also encompasses workforce strategies, which now include a focus on retaining and attracting key talent with the competencies required to lead in this new environment.

A hiatus in the growth of healthcare costs has required fewer adjustments to benefits strategy, design and selection for 2021. And even if costs go up as expected when the utilization of provider services normalizes, many employers are well positioned to keep them in check.

The past three years have been marked by increases in telemedicine adoption; higher employee contributions to health plan premium costs; and greater use of cost-transparency tools, claims audits, and a surcharge or exclusion for spouses with access to other coverage. By 2023, more than 20% of employers plan to fortify their cost-management efforts and outcomes through plan design changes and the addition of wellbeing incentives, cost-transparency tools and healthcare decision support.

The pressure to endure long-term unpredictability and to manage not-so-new everyday stresses has increased burnout and decreased emotional wellbeing among employees. With remote work now commonplace for many businesses, managers who schedule check-ins and maintain regular contact with their team members will be more attuned to the need for additional support. Keeping everyone aware of resources like EAPs, mental health self-assessment tools, coaching and counseling programs, or other available options is key to connecting them to better health and wellbeing.

For many employee roles, allowing flexibility in how and when work gets done, as well as where, is essential to both productivity and profitability. Long before the pandemic, accelerating advances in communication technology not only laid the groundwork for this shift, but also made it inevitable. Success in a society that’s constantly connected insists on negotiable work arrangements and hours, wherever practical.

Evaluating the specific needs of employee groups allows employers to more effectively identify and develop supportive workplace policies that discourage turnover. Caregiver burdens and high attrition among female employees with school-age children are two high-priority retention risks. Diversity will continue to set the course for organizational success, making it critical to address the stressors underlying an exodus of women from the workforce — through policies such as paid and unpaid leave policies, job sharing or reduced hours.

Tasked with keeping a competitive workforce during an unparalleled rise in labor market mobility, sustainability requires a firm foundation for pay equity and employee performance. Policy adjustments, targeted training and individualized support resources are also needed to help people adapt to a flexible environment.

This eventful decade that’s barely even started has already brought a much deeper understanding about the meaning of resilience in the near and distant future. For retaining and attracting new talent, proactively managing constant change is about keeping pace with the present — by evolving the employee value proposition through an integrated approach to total rewards, workplace culture and employee wellbeing.

29GALLAGHER AJG.COM

ENDNOTES

PEOPLE & ORGANIZATIONAL STRATEGY¹U.S. Bureau of Labor Statistics, “Graphics for Economic News Releases: Civilian unemployment rate,” accessed March 2021

²Congressional Budget Office, “An Overview of the Economic Outlook: 2021 to 2031,” February 2021

³Gallagher, “The impact of COVID-19: Self-funded employers should experience a reduction in healthcare costs — Yes, a reduction,” May 2020

30 U.S. EDITION2021 WORKFORCE TRENDS REPORT SERIES | PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

CONTRIBUTORS

PEOPLE & ORGANIZATIONAL WELLBEING STRATEGY

Scott Hamilton [email protected]

Joe Milano [email protected]

PRODUCTION

Stacy [email protected]

Cindy [email protected]

RESEARCH & REPORTING

Stephanie [email protected]

Sarah Daley [email protected]

SURVEY DEVELOPMENT

Michelle [email protected]

Thomas [email protected]

PREVIEW REPORT DATA

ajg.com/2021-WFTRSeries

LIKE THE DATA IN THIS REPORT?

Get the full employee and organizational wellbeing story with the complete 2021 Workforce Trends Report Series. Access all the data and insights in the complete 2021 series for

only $650.

This series includes employer insights and analysis from

Gallagher's biggest benefits and workforce strategy surveys.

31GALLAGHER AJG.COM

ABOUT GALLAGHER

The pursuit of “better” is ongoing. And the process involved requires recognizing and acting on unforeseen risks, while keeping a mindset that turns the toughest challenges into opportunities.

People are an organization’s greatest asset in any challenge. And the connection between employee wellbeing and organizational wellbeing

has never been more apparent — or more important.

Employees have multifaceted needs that extend beyond their work commitments. That’s why their wellbeing is at the center of Gallagher

Better Works℠, a comprehensive approach that engages them in their work and drives your organization’s success. By strategically investing

in benefits, compensation, retirement and employee communication, you’re able to support the health, financial security and career growth

of your people at the right cost structures.

From evaluating the demographics of your workforce to surveying and analyzing competitor trends, Gallagher helps you gather new insights

and apply best practices that promote productivity and growth. A data-driven focus allows you to continually improve and make changes for

better outcomes.

As you develop new business operating models, support employees working remotely, and ensure equity and inclusion within a diverse

workplace culture, your people can perform at a higher level. When this happens, you optimize your annual talent investment and mitigate

organizational risk to maximize your profitability.

A strategy rooted in the wellbeing of your people is one that allows organizational wellbeing to thrive — even in times of uncertainty.

Arthur J. Gallagher & Co. (NYSE: AJG), an international insurance brokerage and risk management services firm, is headquartered in

Rolling Meadows, Illinois; has operations in 56 countries; and offers client-service capabilities in more than 150 countries around the

world through a network of correspondent brokers and consultants.

TERMS OF USE

The intent of this Survey is to provide you with general information regarding current practice within the employee benefits environment. The data does not constitute recommendations or other advice regarding employee benefit programs, and the user is in no way obligated to accept or implement any information for use within their organization(s). The decision to utilize any information provided rests solely with the user, and application of the data contained does not guarantee compliance with applicable laws or regulations regarding employee benefits. Information provided by the Survey, even if generally applicable, cannot possibly take into account all of the various factors that may affect a specific individual or situation. Additionally, practices described within the Survey should not be construed as, nor are they intended to provide, legal advice.

The Web Site and the Content do not constitute accounting, consulting, investment, insurance, legal, tax or any other type of professional advice, and should be used only in conjunction with the services of a Gallagher consultant and any other appropriate professional advisors who have full knowledge of the user’s situation.

Gallagher does not represent or warrant that the Content will be correct, accurate, timely or otherwise reliable. Gallagher may make changes to the Content at any time. Gallagher assumes no responsibility of any kind, oral or written, express or implied, including but not limited to fitness for a particular purpose, accuracy, omissions and completeness of information. Gallagher shall in no event whatsoever be liable to licensee or any other party for any indirect, special, consequential, incidental, or similar damages, including damages for lost data or economic loss, even if Gallagher has been notified of the possibility of such loss. For the purposes of this section the term “Gallagher” shall be construed so as to include Gallagher Surveys as a marketing division and/or Gallagher Benefit Services, Inc. and its affiliates.

Consulting and insurance brokerage services to be provided by Gallagher Benefit Services, Inc. and/or its affiliate Gallagher Benefit Services (Canada) Group Inc. Gallagher Benefit Services, Inc., a non-investment firm and subsidiary of Arthur J. Gallagher & Co., is a licensed insurance agency that does business in California as “Gallagher Benefit Services of California Insurance Services” and in Massachusetts as “Gallagher Benefit Insurance Services.” Certain appropriately licensed individuals of Arthur J. Gallagher & Co. subsidiaries or affiliates offer securities through Kestra Investment Services, LLC (Kestra IS), member FINRA/SIPC and or investment advisory services through Kestra Advisory Services, LLC (Kestra AS), an affiliate of Kestra IS. Neither Kestra IS nor Kestra AS is affiliated with Arthur J. Gallagher & Co., or Gallagher Benefit Services, Inc. Neither Kestra AS, Kestra IS, Arthur J. Gallagher & Co., nor their affiliates provide accounting, legal, or tax advice. GBS/Kestra-CD(3582630)(exp052022).

Investor disclosures https://bit.ly/KF-Disclosures

For institutional use only. Not for public distribution. All rights reserved. No part of this book, including the text, data, graphics, interior design and cover design may be reproduced or transmitted in any form, without explicit consent from Arthur J. Gallagher & Co.

“World’s Most Ethical Companies” and “Ethisphere” names and marks are registered trademarks of Ethisphere LLC.

© 2021 Arthur J. Gallagher & Co. | 40116

ajg.com The Gallagher Way. Since 1927.