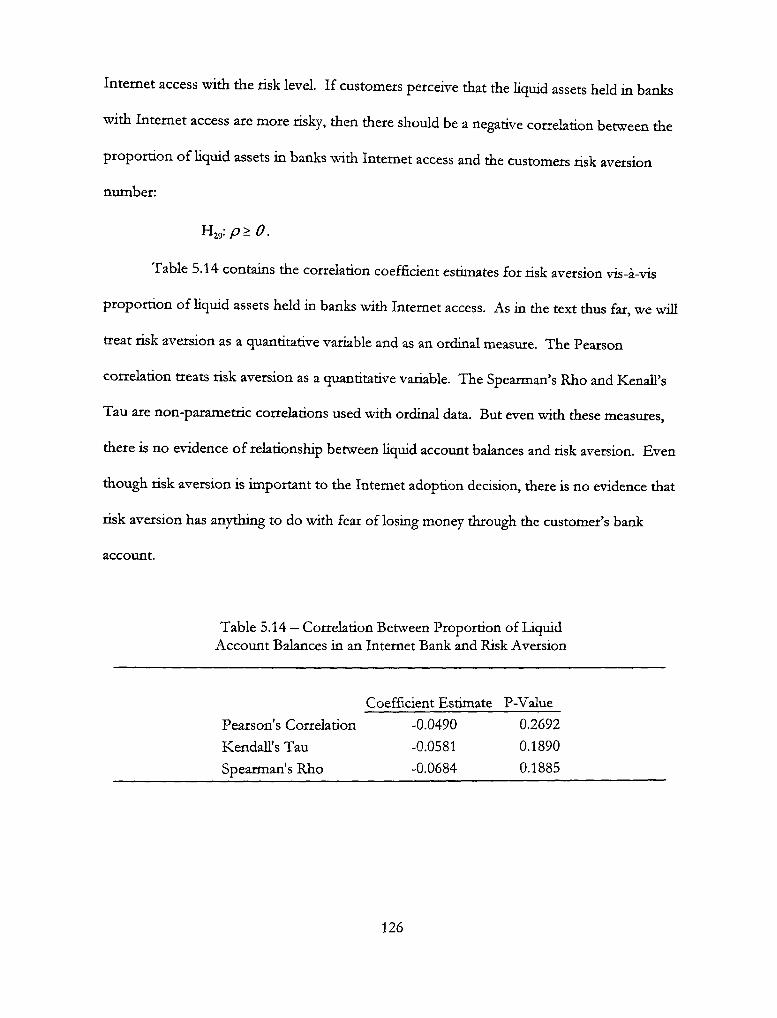

perceived risk and internet banking in business administration

TRANSCRIPT

PERCEIVED RISK AND INTERNET BANKING

by

KELDON J. BAUER, B.A., M.B.A.

A DISSERTATION

IN

BUSINESS ADMINISTRATION

Submitted to the Graduate Faculty of Texas Tech University in

Panial Fulfillment of the Requirements for

the Degree of

DOCTOR OF PHILOSOPHY

Approved

^^^ \ oil

Copyright 2002 Keldon J Bauer

AH Rights Reserved

ACKNOWLEDGMENTS

I would like to thank the members of my dissertation committee, not only for their

input along the way, but for their flexibility. I would like to thank Dr. Scott Hein for always

pushing this project to be better. The final thesis is so improved over the first drafts that

they appear to be completely different documents. I also would like to thank Dr. Peter

WestfaU for the insight he brought to this project. Through short visits to his office, new

analytical tecliniques were tried that shed a great deal of Hght on the subject of this thesis. I

would like to thank Dr. Philip English for sharpening the focus of the research and

encouraging me along the way. And I would like to thank Dr. Terry von Ende for having

the patience to teach me micro-economics in the first place, and then work with me to

understand it better two to three years later.

But my greatest source of strength, encouragement and support came from my

wonderful wife who endured years of stress and solitude while I worked long, frustrating

hours. Thank you, Sonia, for your love and ungrudging flexibility over the past years of

intense study.

u

TABLE OF CONTENTS

ACKNOWLEDGMENTS ii

ABSTRACT v

LIST OF TABLES vii

LIST OF FIGURES ix

CHAPTER

1 INTRODUCTION 1

2 LITERATURE REVIEW 13

2.1 Internet Market Overview 14 2.1.1 Empirical Evidence about the Internet Market 16 2.1.2 Empirical Evidence Regarding Internet Frictions 18

2.2 Internet Banking Overview 21 2.2.1 Price Competition and Elasticity 22 2.2.2 Motivations for Adopting Remote Banking 29

2.3 Professional Literature 33

2.4 Summary of Literature 37

3 THEORETICAL FRAMEWORK 39

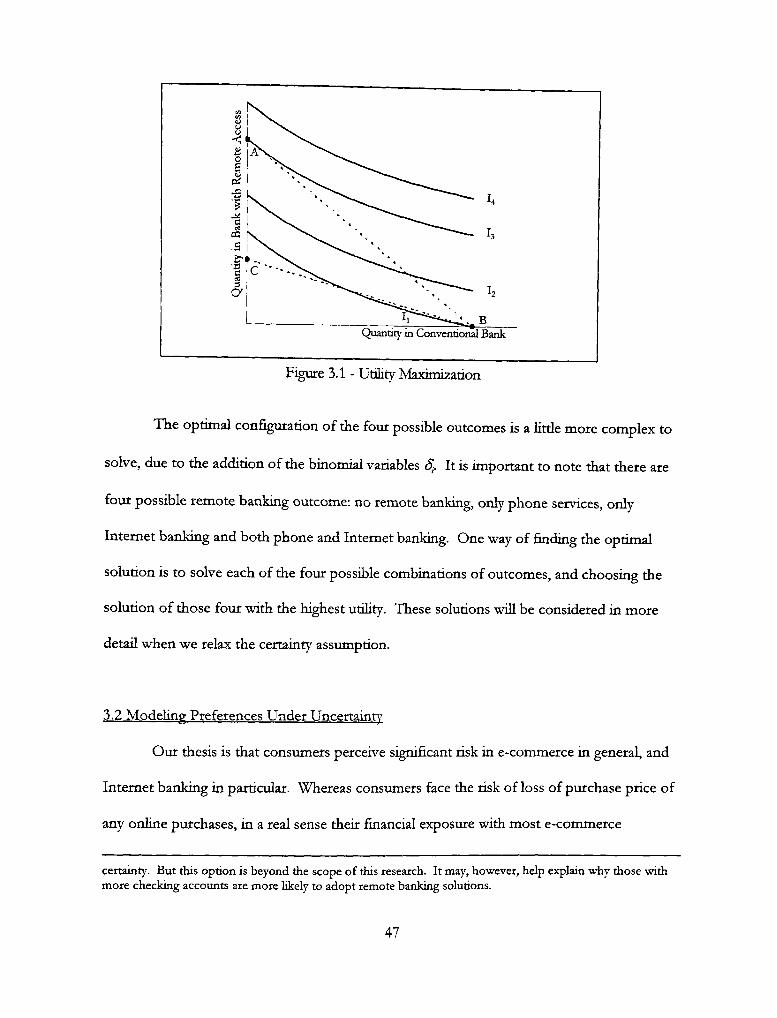

3.1 Base Model Under Certainty 41

3.2 Modeling Preferences Under Uncertainty 47

3.3 The Role of Risk Aversion on Adoption Decisions 50

3.4 Theoretical Summary 55

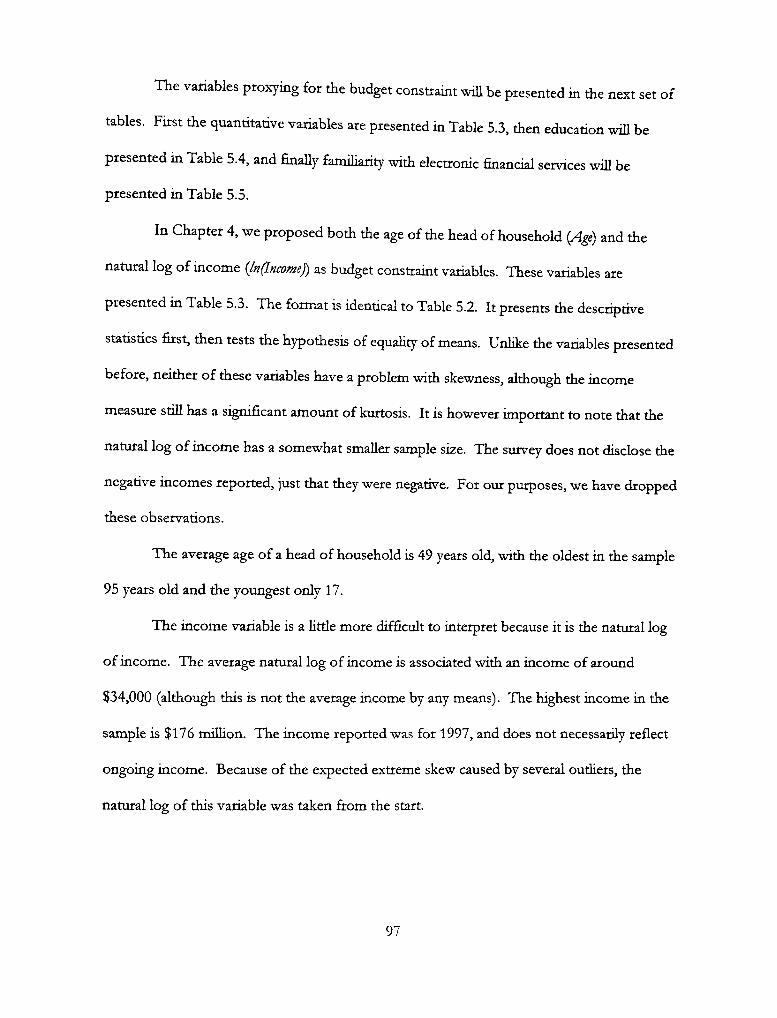

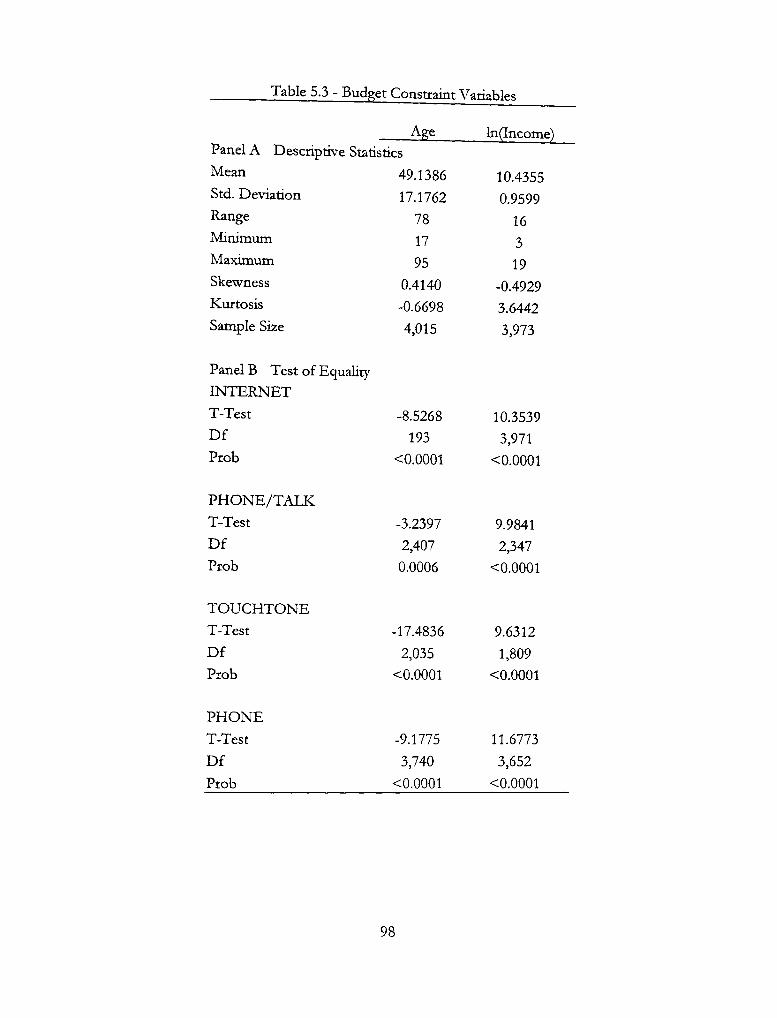

4 DATA AND METHODOLOGY 57

4.1 Variable Description 66 4.1,1 Differing Degrees of Risk Aversion 69

m

4.2 Base Model Development 70

4.3 Functional Forms Test of the Base Model 79

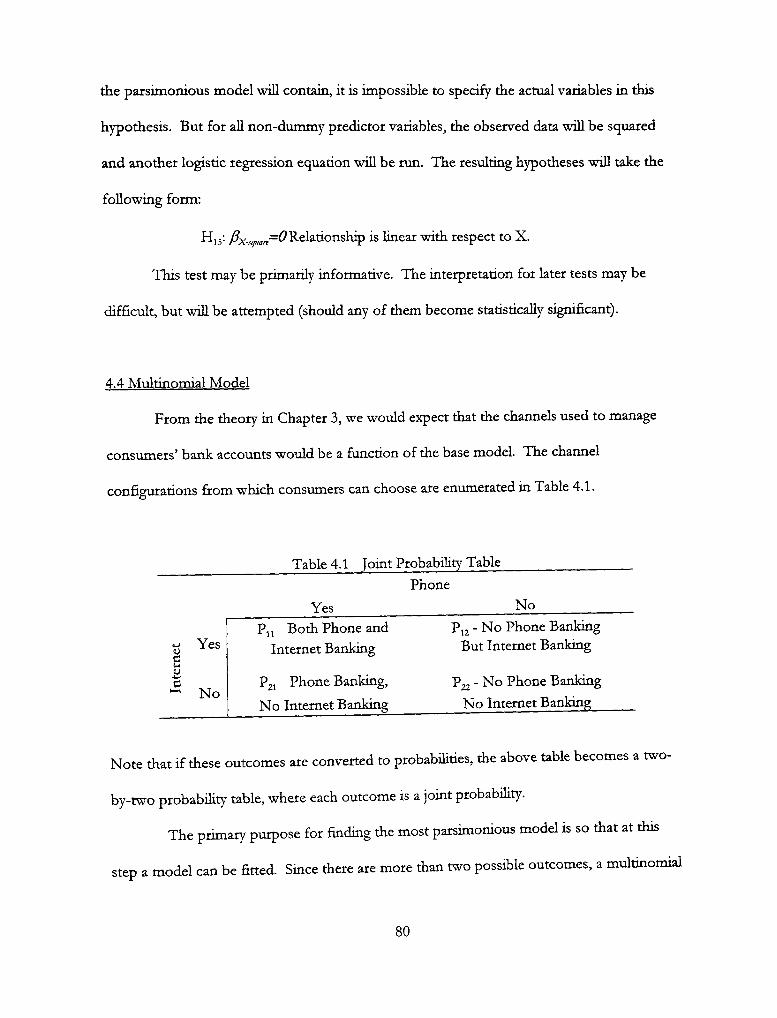

4.4 Multinomial Model 80

4.5 Modeling the Marginal Propensity to Adopt 82

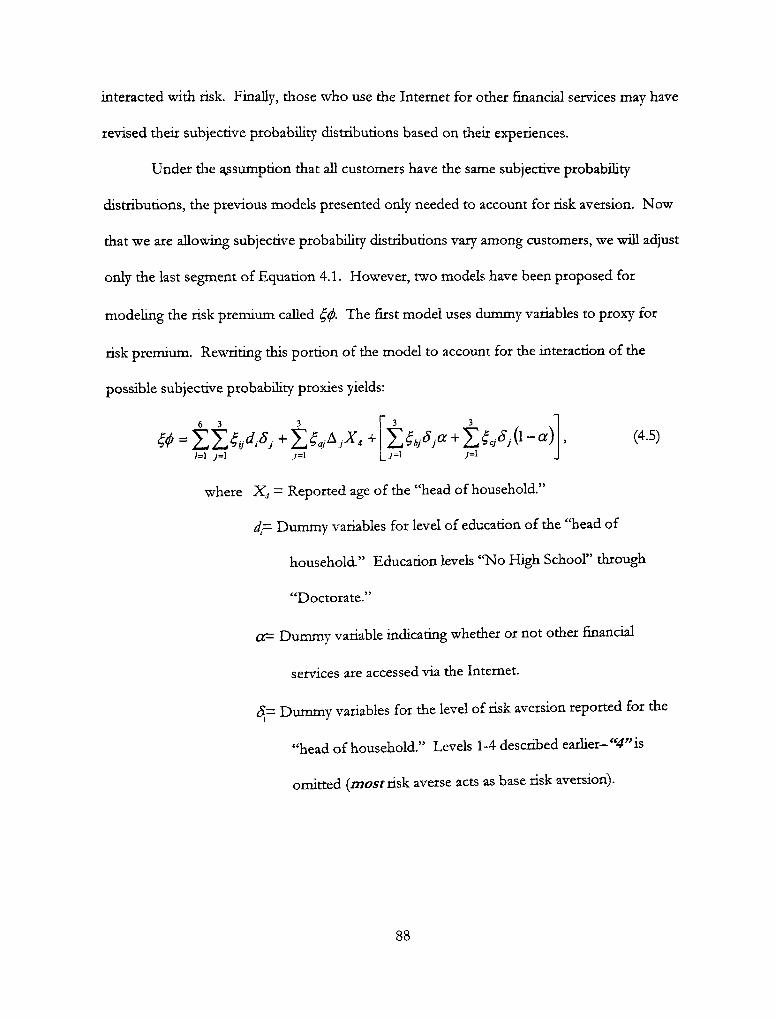

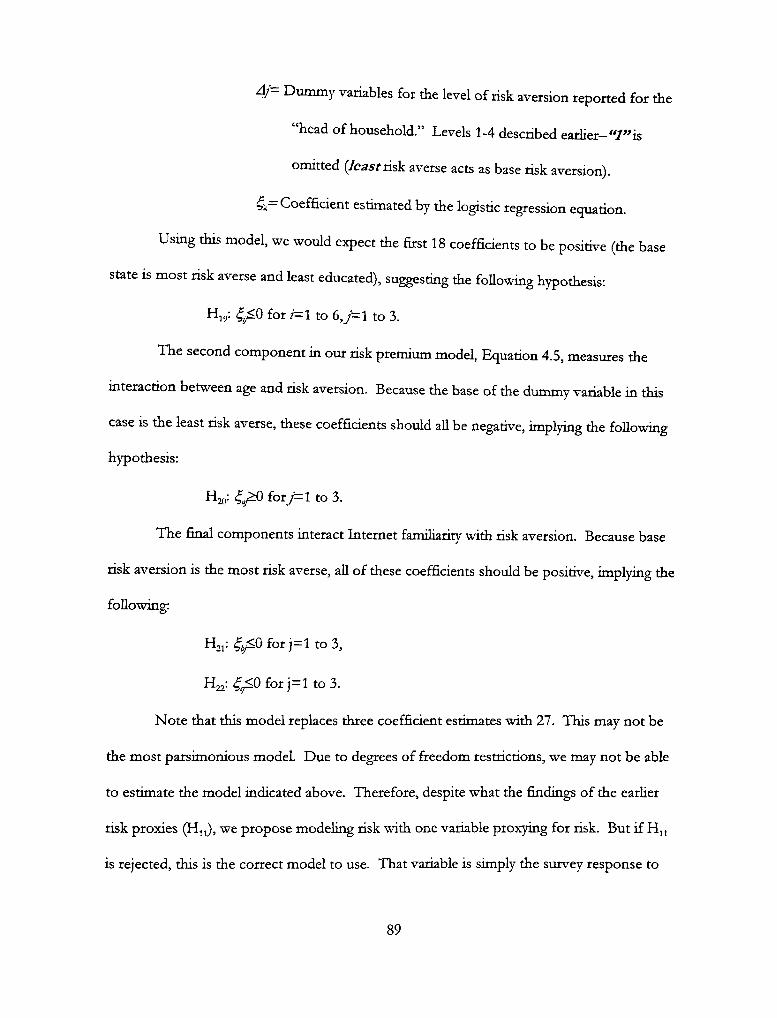

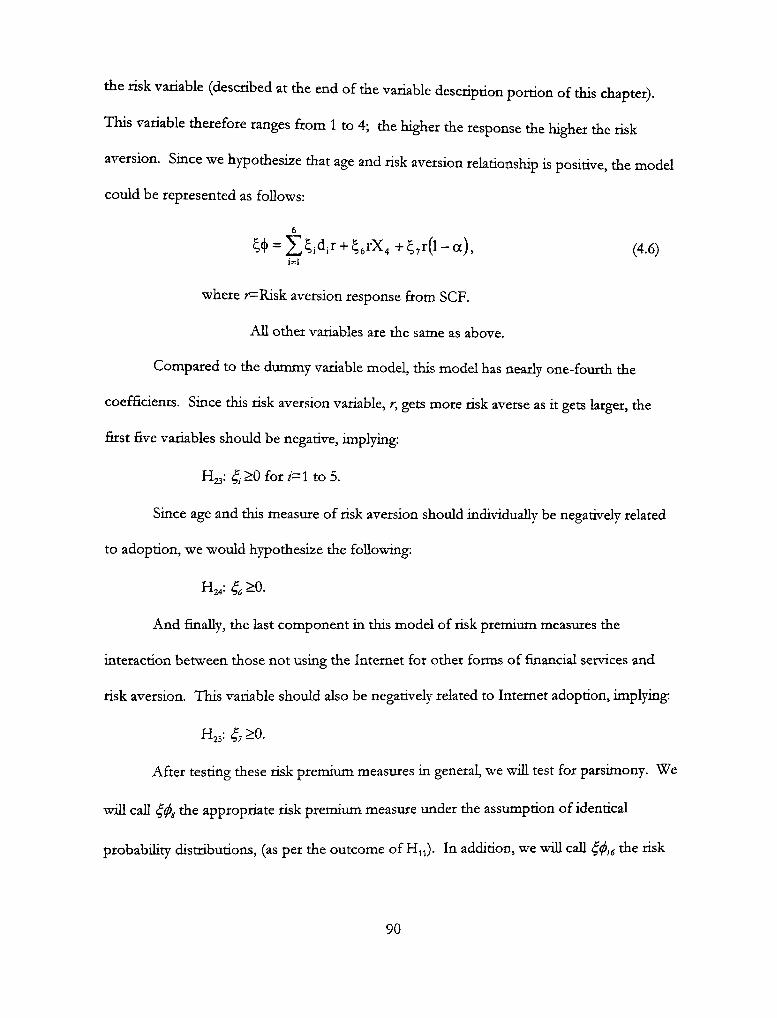

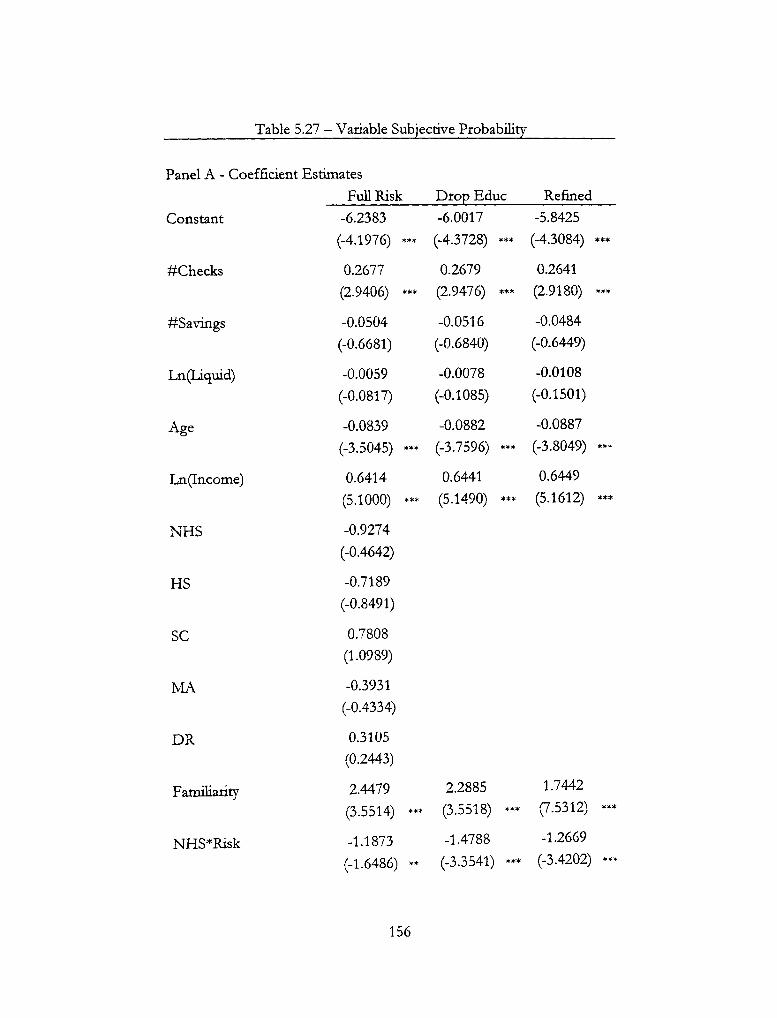

4.6 Allowing Subjective Probability to Vary 87

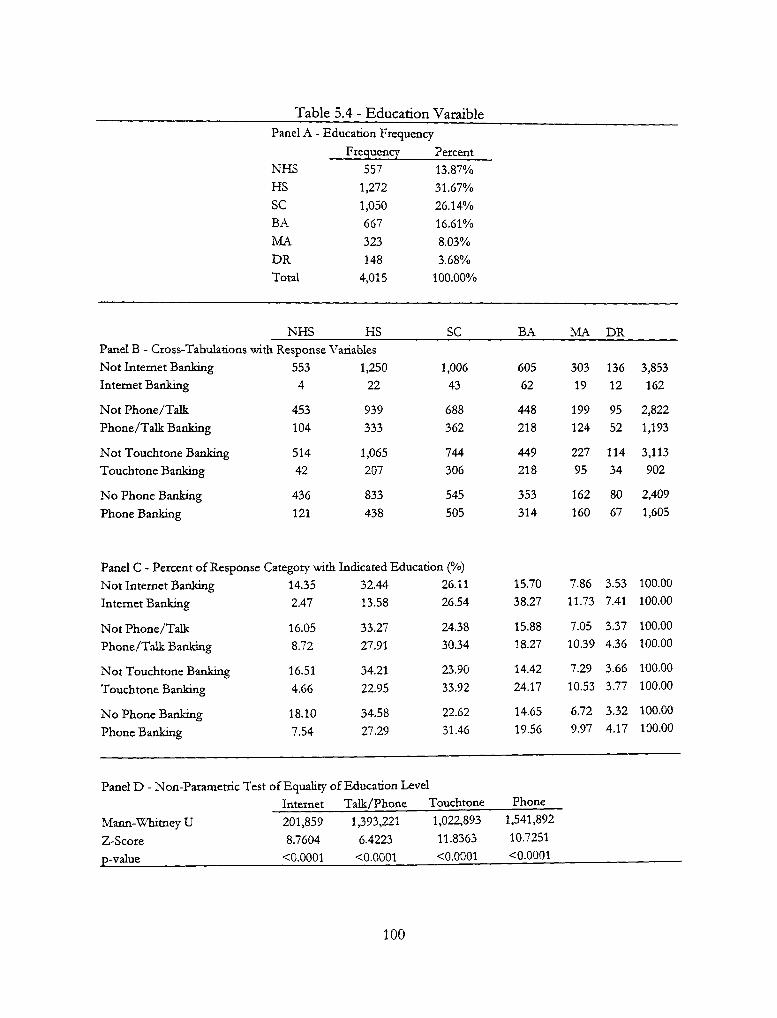

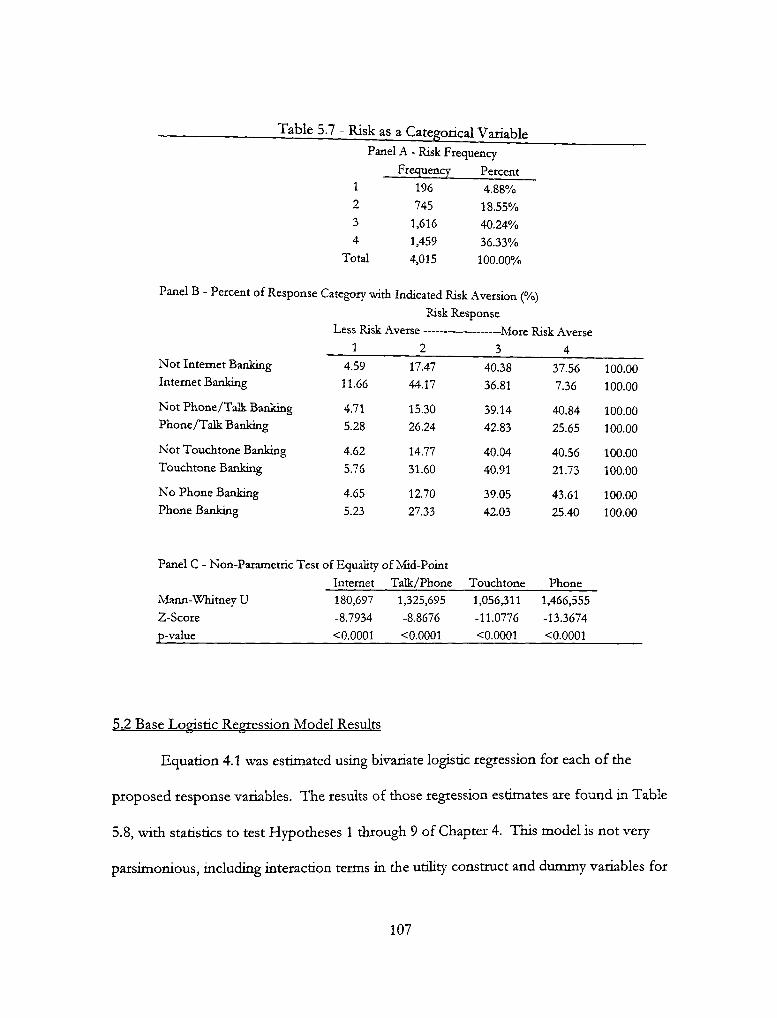

5 EMPIRICAL RESULTS 92

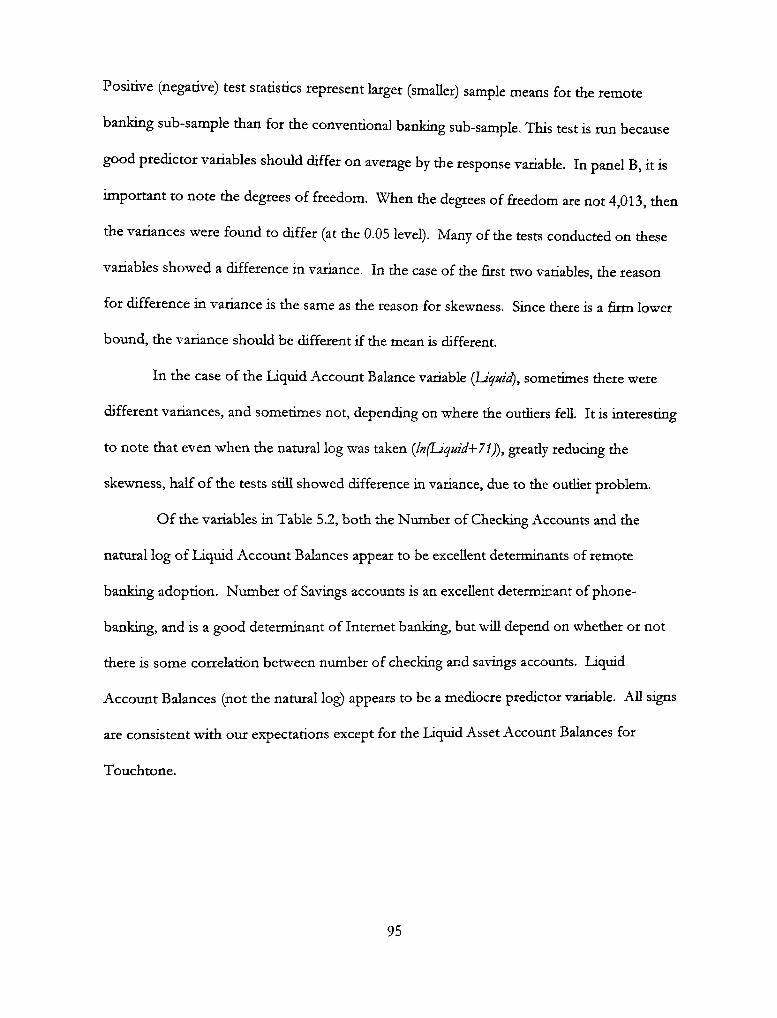

5.1 Descriptive Statistics 92

5.2 Base Logistic Regression Model Resvilts 107

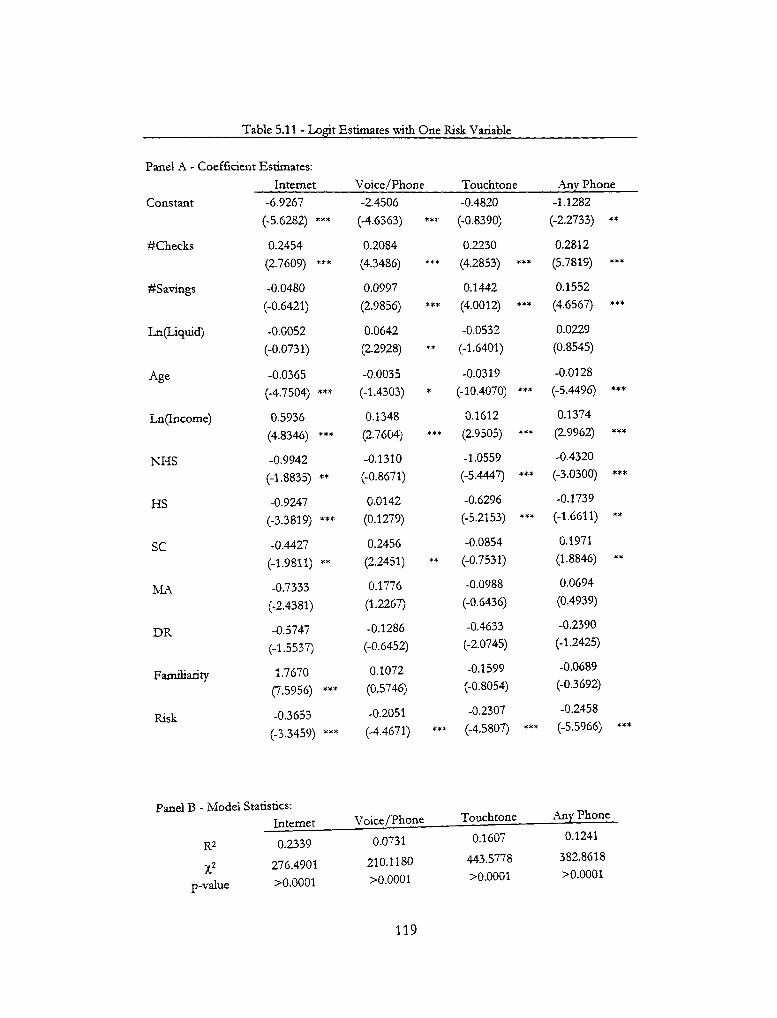

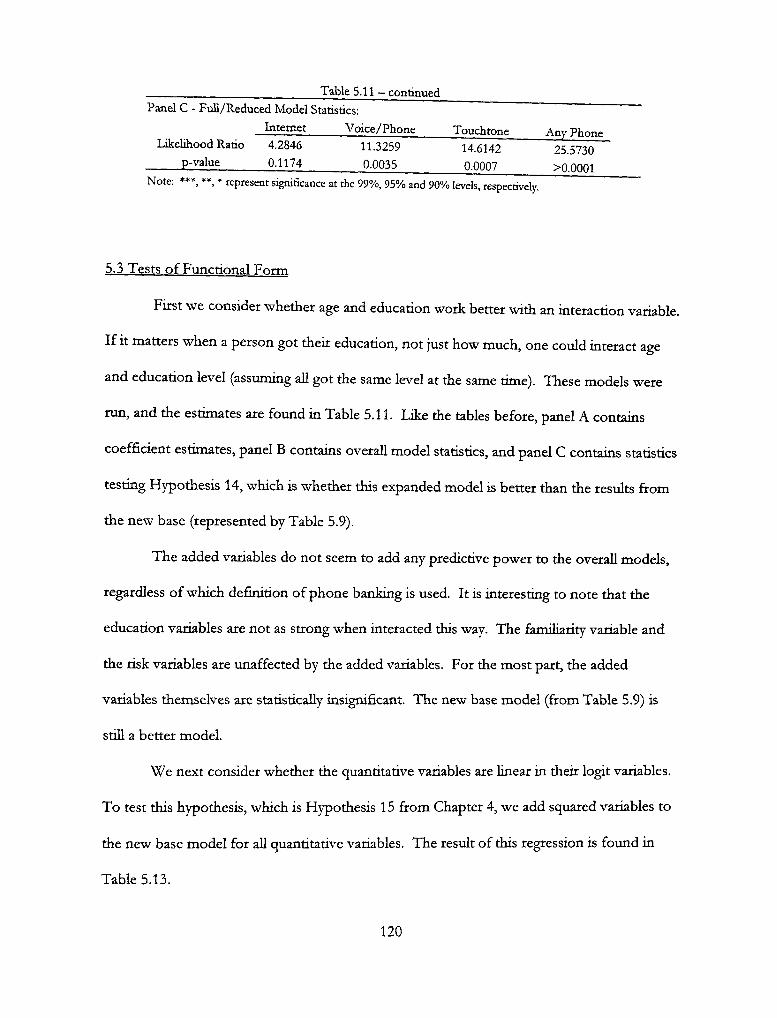

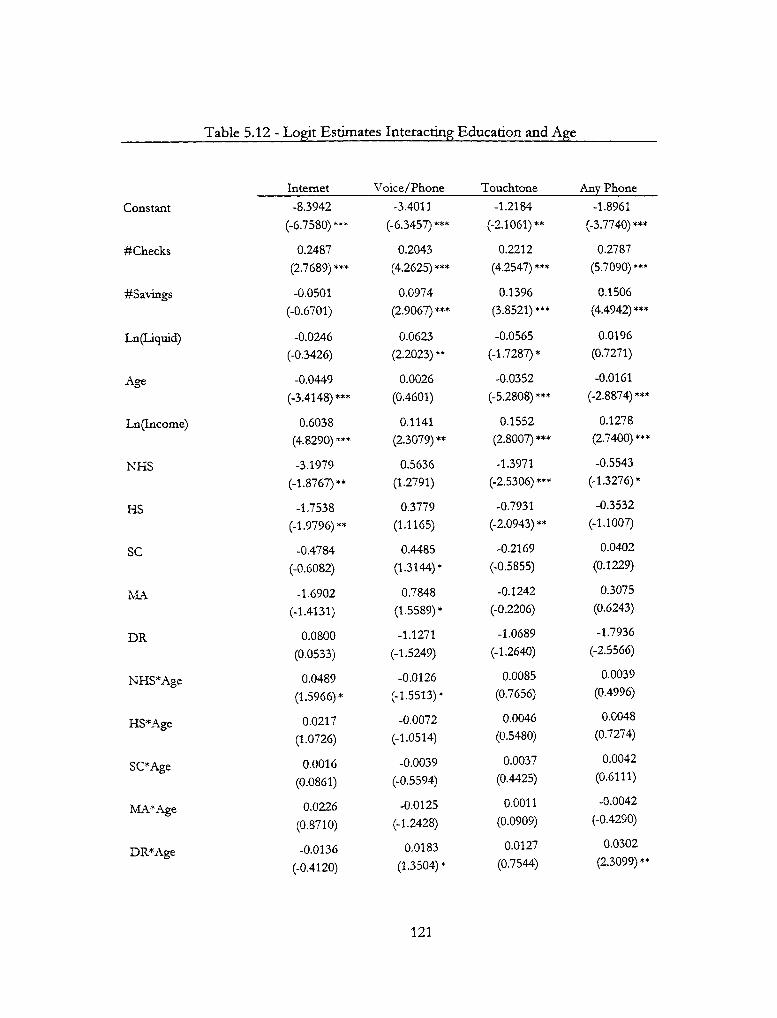

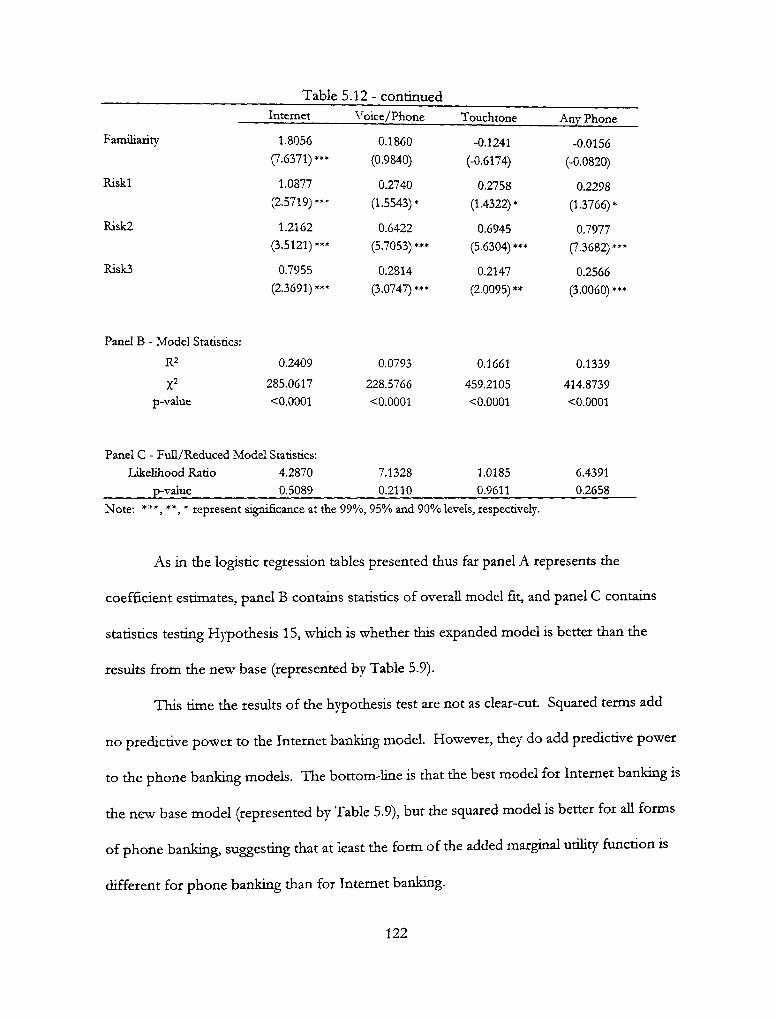

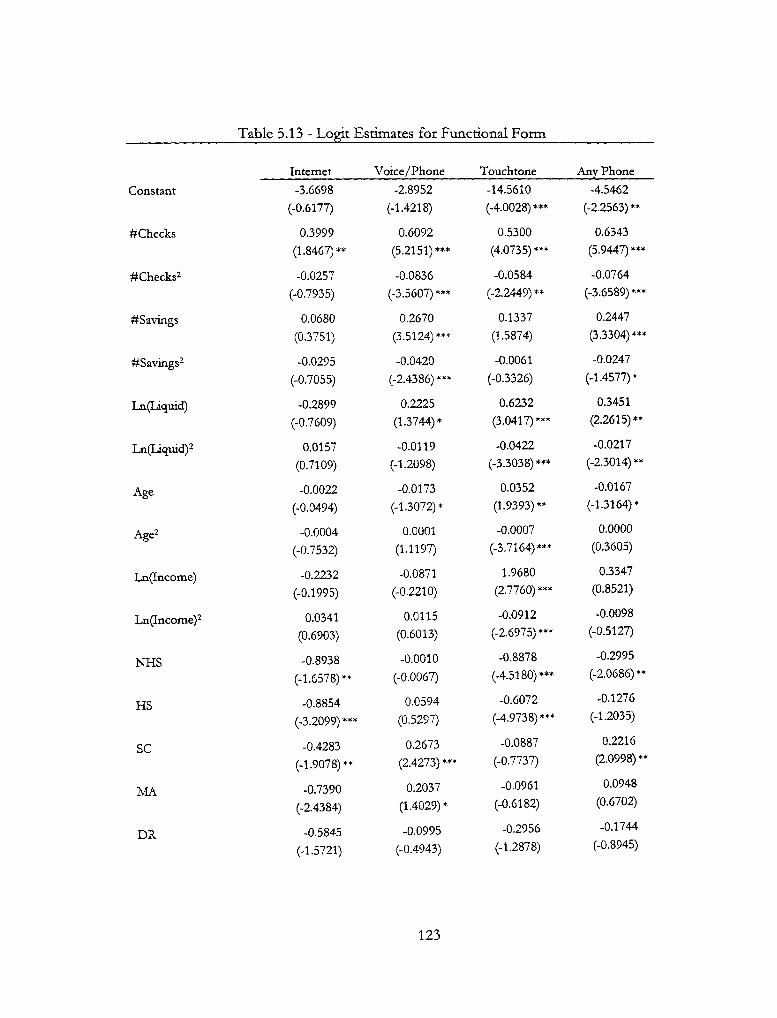

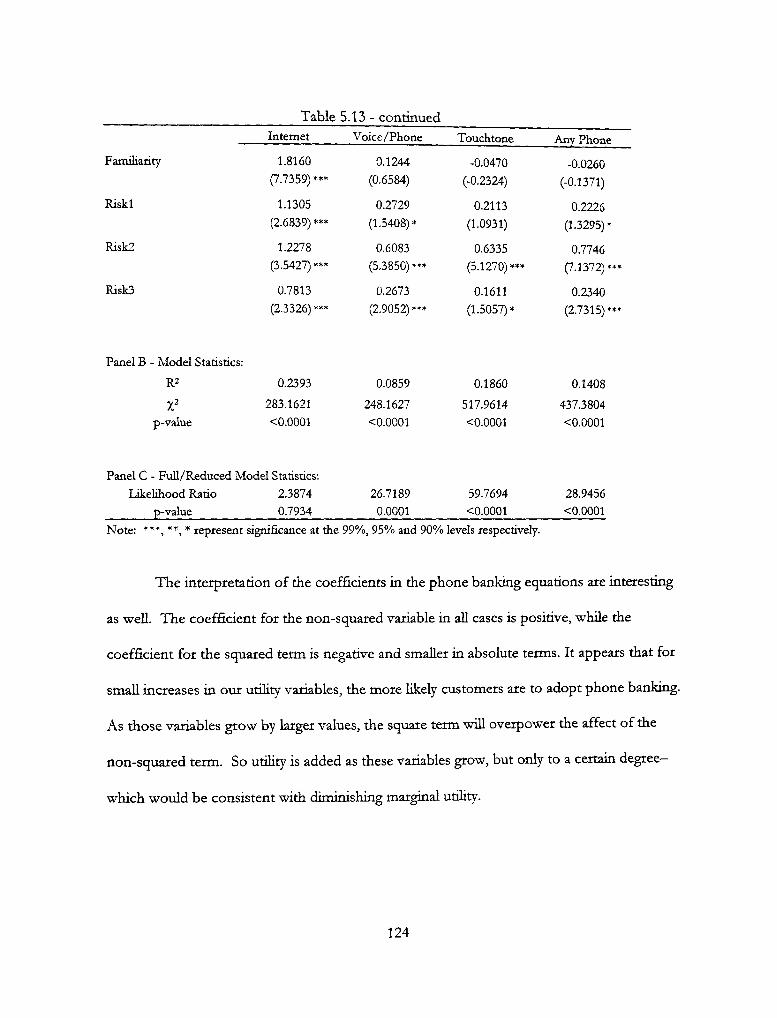

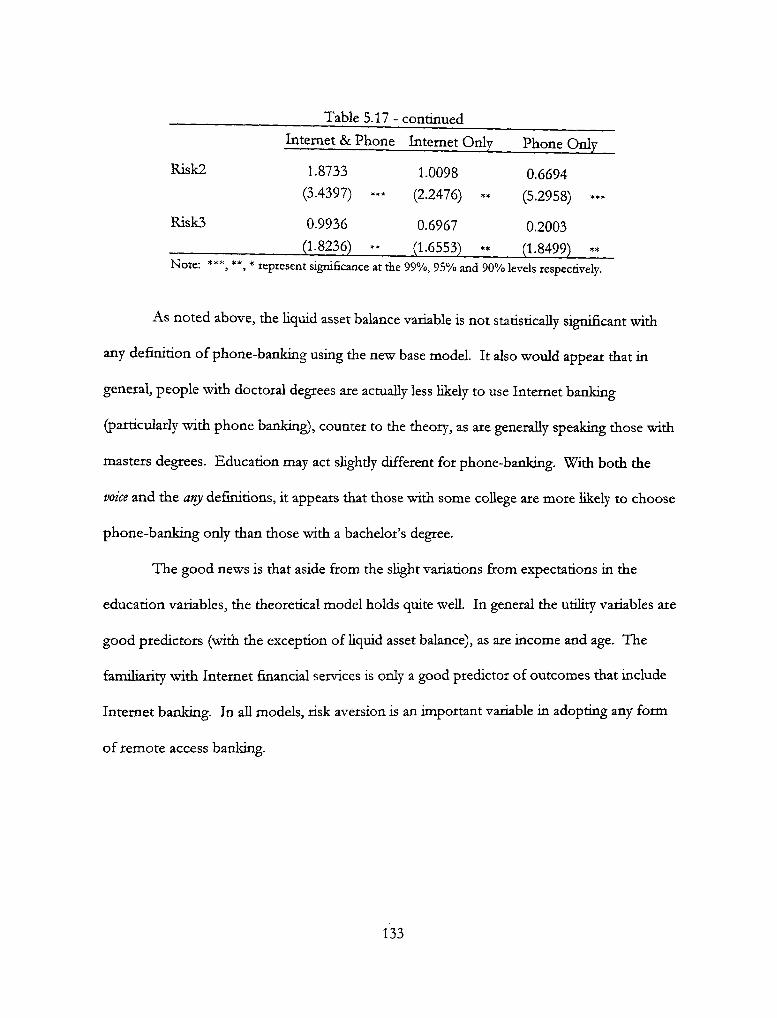

5.3 Tests of Functional Form 120 5.3.1 Comment on Risk Aversion 125

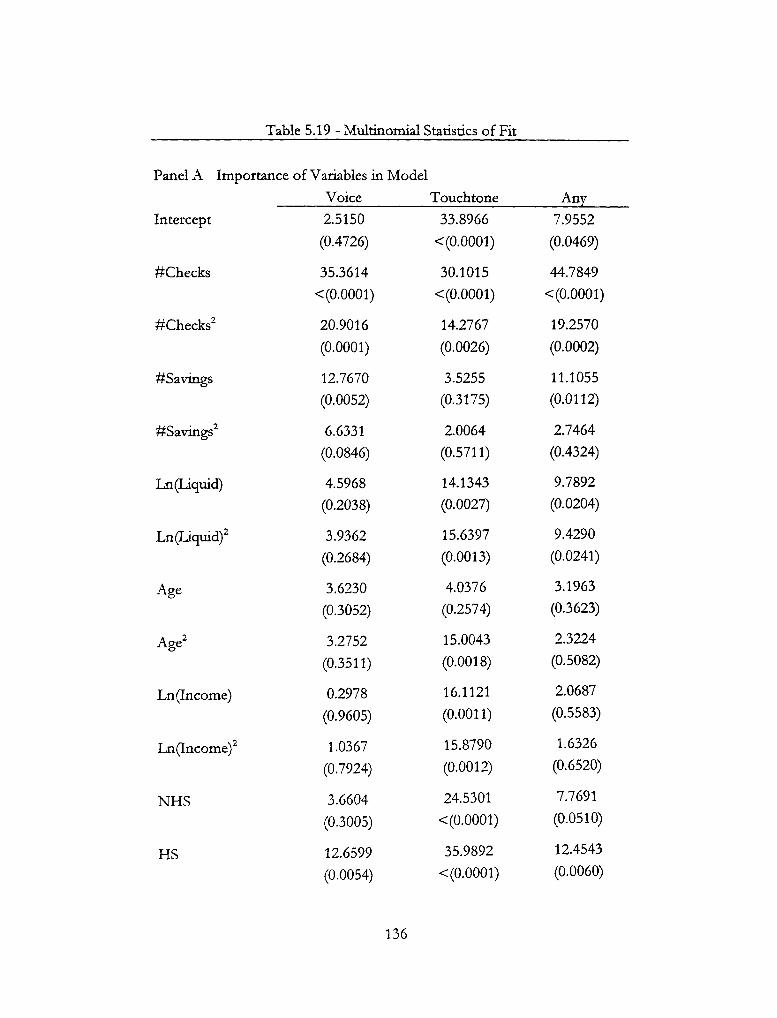

5.4 Multinomial Model 127

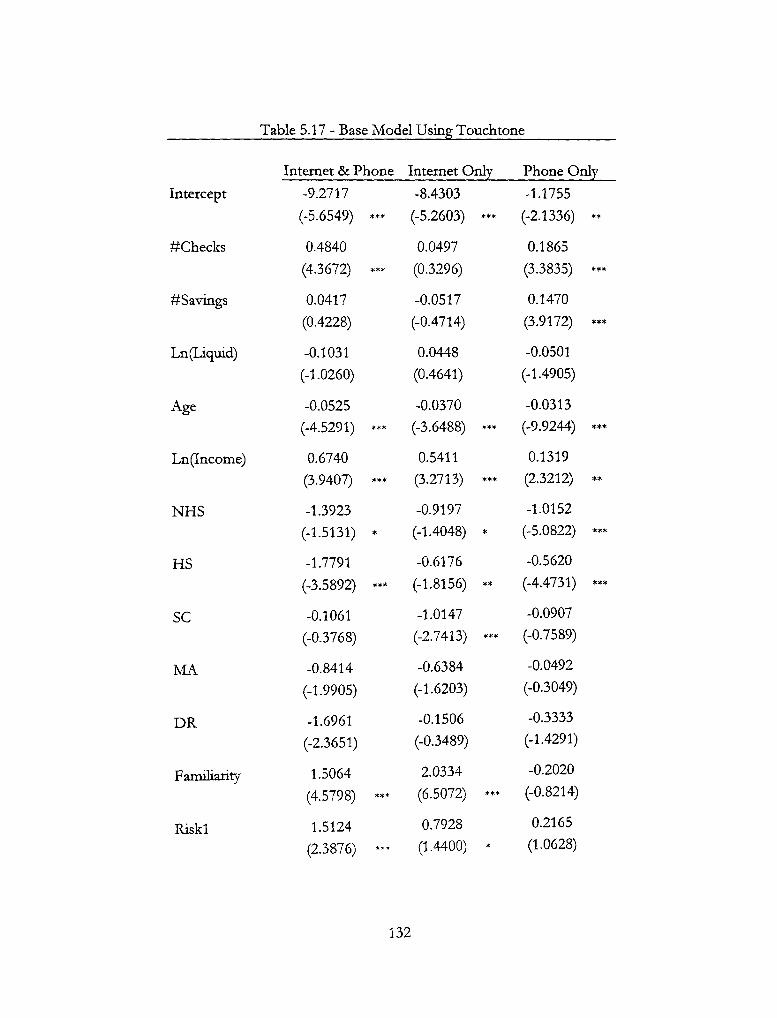

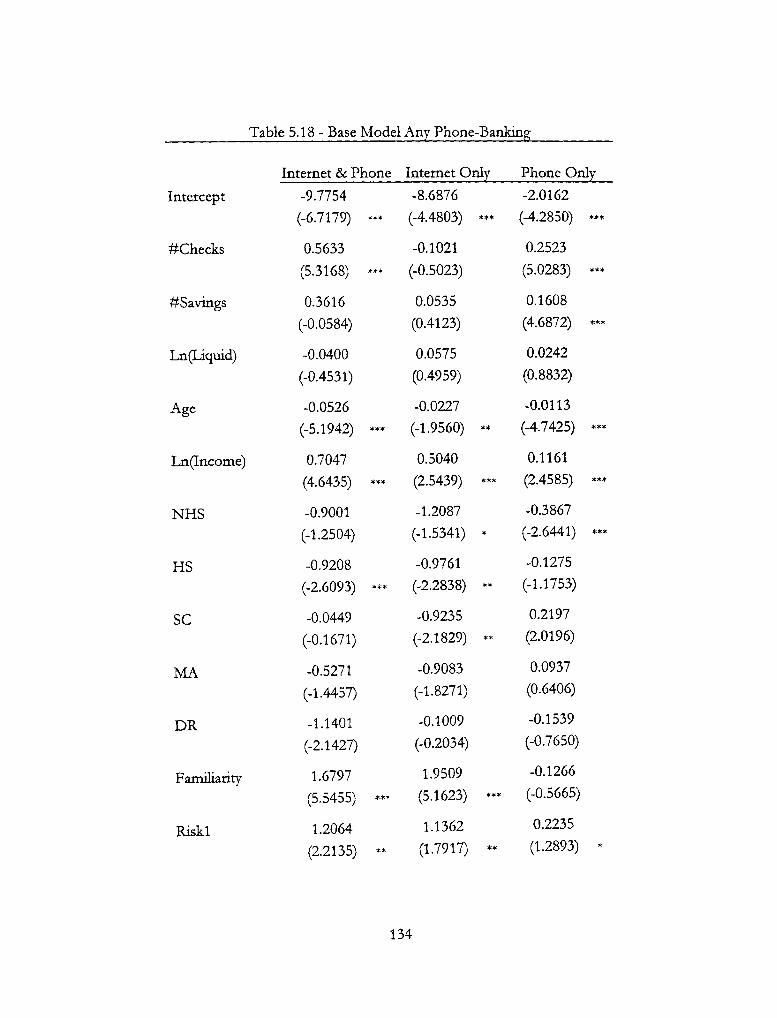

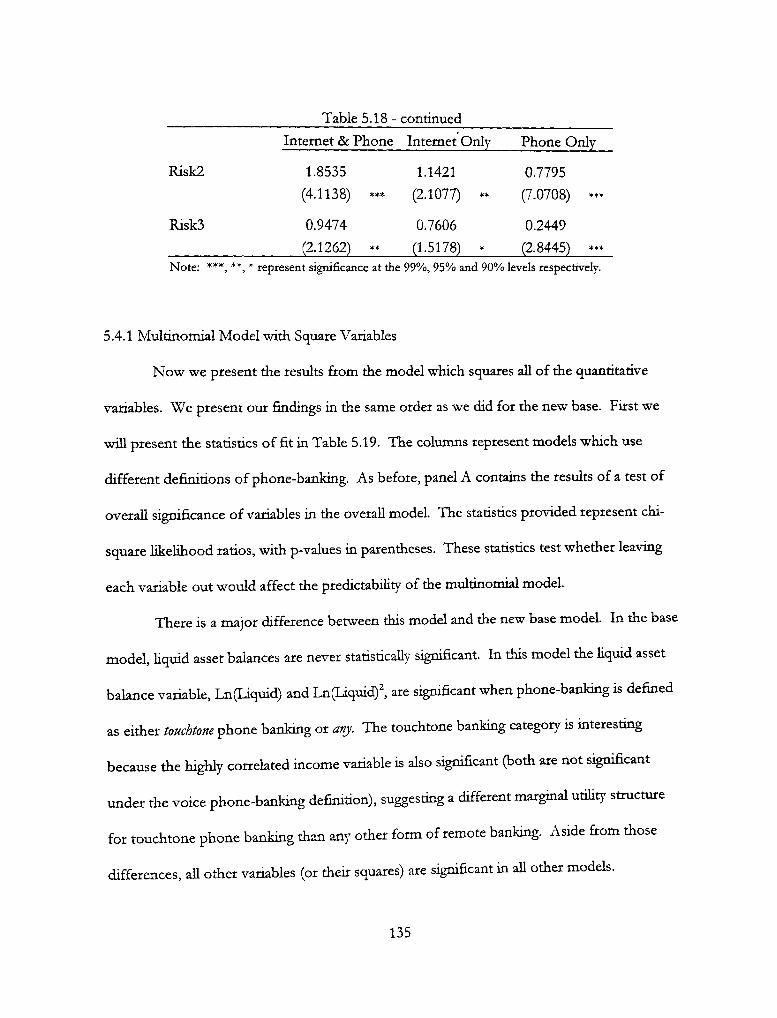

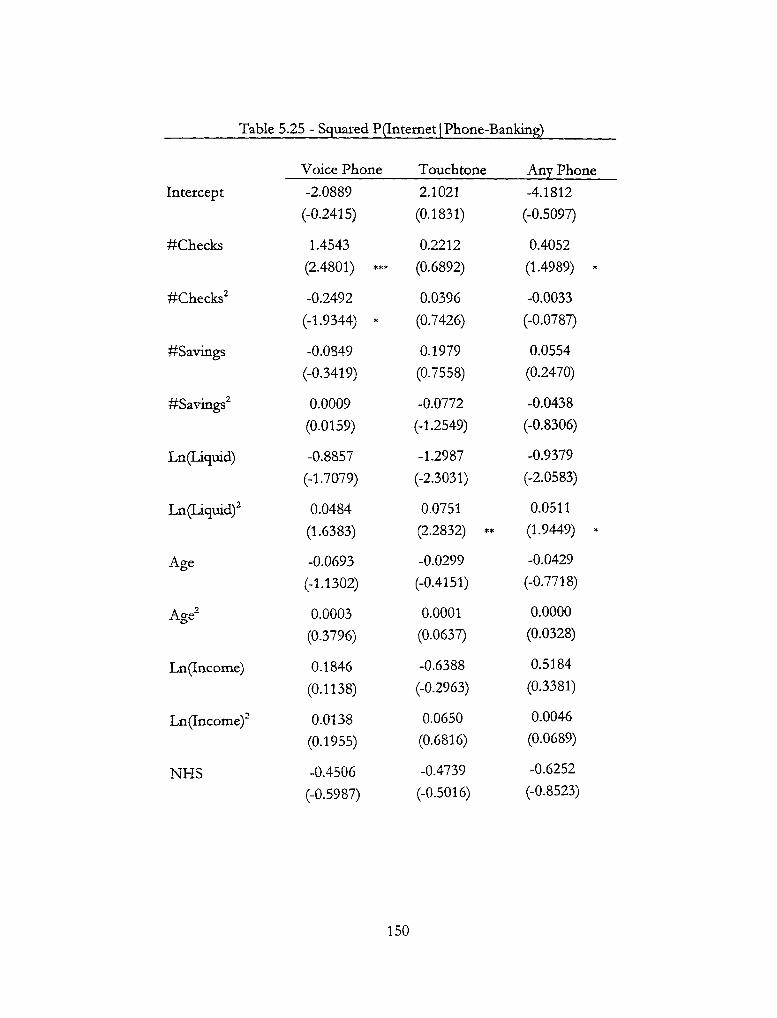

5.4.1 Multinomial Model with Square Variables 135

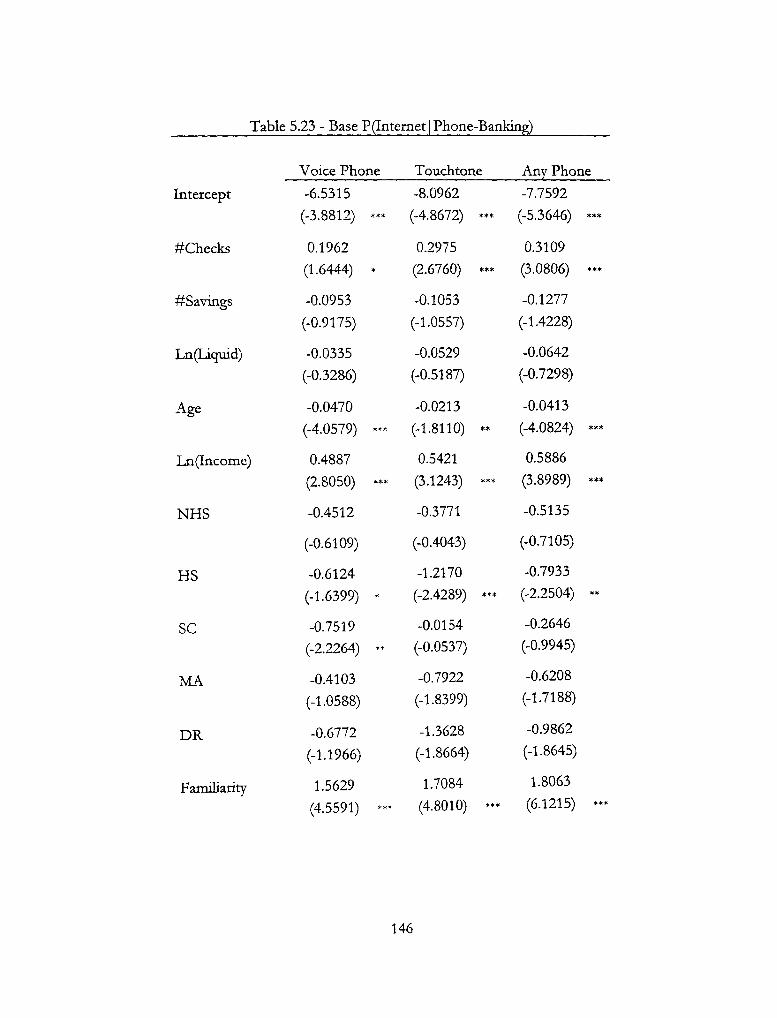

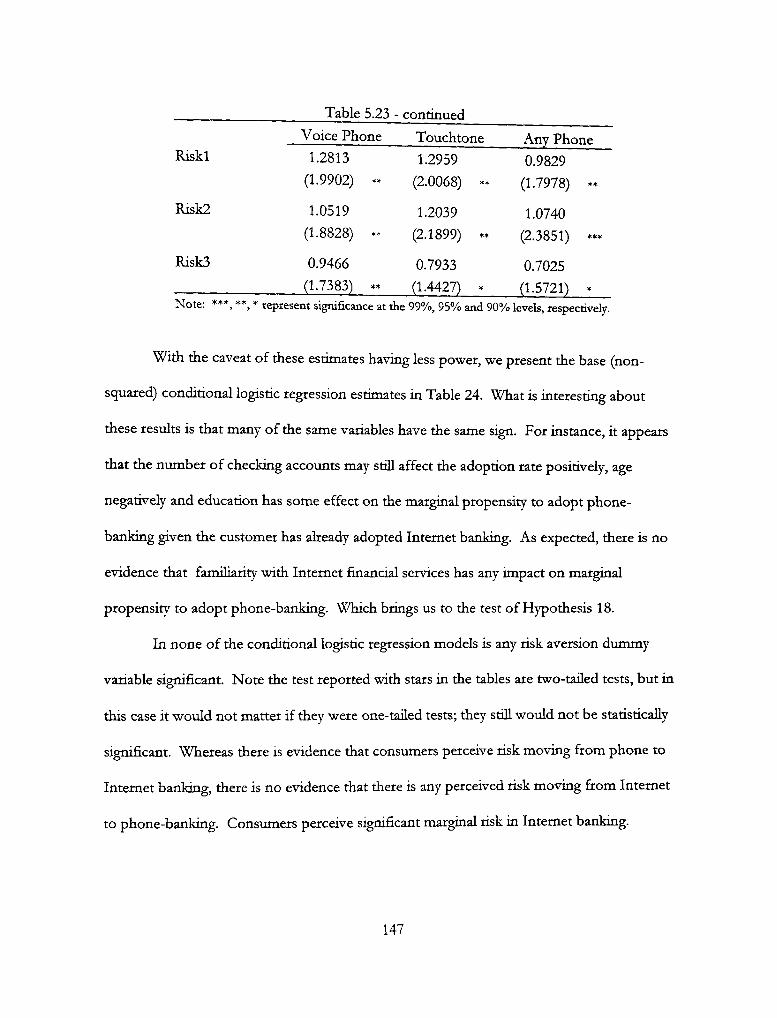

5.5 Modeling Marginal Propensity to Adopt 144

5.6 Allowing Subjective Probability to Vary 153

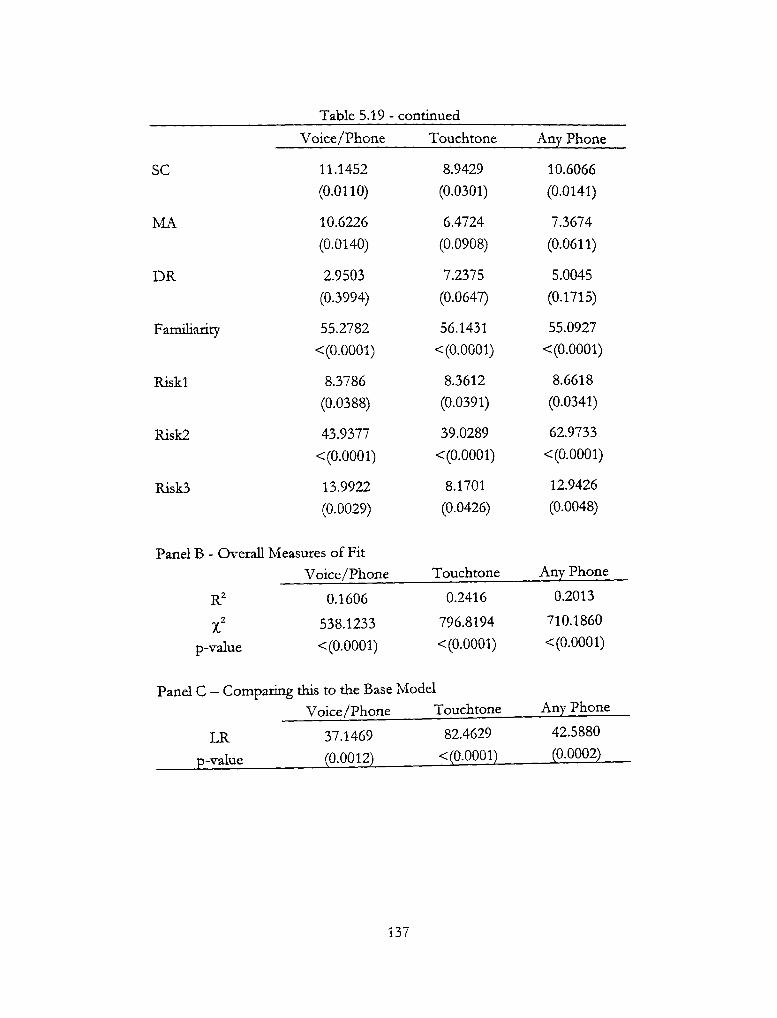

6 CONCLUSIONS AND CONTRIBUTIONS 190

6.1 Conclusions 190

6.2 Contributions 196 6.2.1 Practical Contributions 197 6.2.2 Shortcomings and Future Research 200

REFERENCES 201

IV

ABSTRACT

Bankers and consumers are both interested in the potential for Internet banking.

Individuals have been adopting die Internet in large numbers, with more than half of all

American households having some form of Internet access by 2000. Banks too have been

developing their infrastructure to address what they perceive as a growing demand for online

services, with 84% of all accounts offering some form of Internet banking by 1999.

However, the adoption rate has not followed the hype. By 2000, the proportion of

households using Internet banking was less than 10%. This research looks at the critical

factors needed to promote banking adoption from the consumer's perspective. We use a

consumer utiHty maximization framework, and include in the consumption bundle the

possibihty of using conventional, phone-banking and/or Internet banking. Phone-banking

is added because it could be seen as a substitute for Internet banking. Many of the same

services are available on both, and many of die restrictions are the same, i.e., no cash can be

withdrawn from either.

Using the utihty maximization approach, we are able to conclude that adoption

depends on marginal utiHty gain, marginal cost and a risk premium; where risk premium is

the product of subjective probability of adverse outcomes from the technology and the

utility of each adverse outcome. We use logistic regression to explore what factors are

important to consumers adopting Internet banking in general. A conditional logit model is

used to estimate the sensitivity of different decision factors to the marginal propensity of

phone-bank customers adopting Internet banking and vice-versa.

The overall utility maximization model is consistent with our results from these

logistic regressions. The results presented in this research also support the hypothesis that

the subjective probability of security problems experienced by Internet bank customers is

not the same for all customers, and that it depends on their level of education. Varying

subjective probability means that the risk premixim can be affected by exogenous factors, in

this case education. In other words, banks could affect the risk premium of their customers,

thereby affecting adoption rates.

VI

LIST OF TABLES

4.1 - Joint Probability Table 80

5.1 — Internet and Phone Banking Utilization 93

5.2 — Variables Proxying for Utility Construct 96

5.3 - Budget Constraint Variables 98

5.4 - Education Variable 100

5.5 — Familiarity E-Financial Services 103

5.6 — Risk Treated as a Continuous Variable 105

5.7 — Risk as a Quahtative Variable 107

5.8 — Base Logit Estimates 111

5.9 — More Parsimonious Logit Estimates 114

5.10 - Testing Hypotheses 10-12 117

5.11 - Logit Estimates with One Risk Variable 119

5.12 — Logit Estimates Interacting Education and Age 121

5.13 — Logit Estimates for Functional Form 123

5.14 — Correlation Between Proportion of Liquid Account Balances in an

Internet Band and Risk Aversion 126

5.15 - Base Model Statistics of Fit 128

5.16 -Base Model Using Voice Phone-Banking 130

5.17 - Base Model Using Touchtone 132

5.18 - Base Model Any Phone-Banking 134

5.19 - Multinomial Statistics of Fit 136

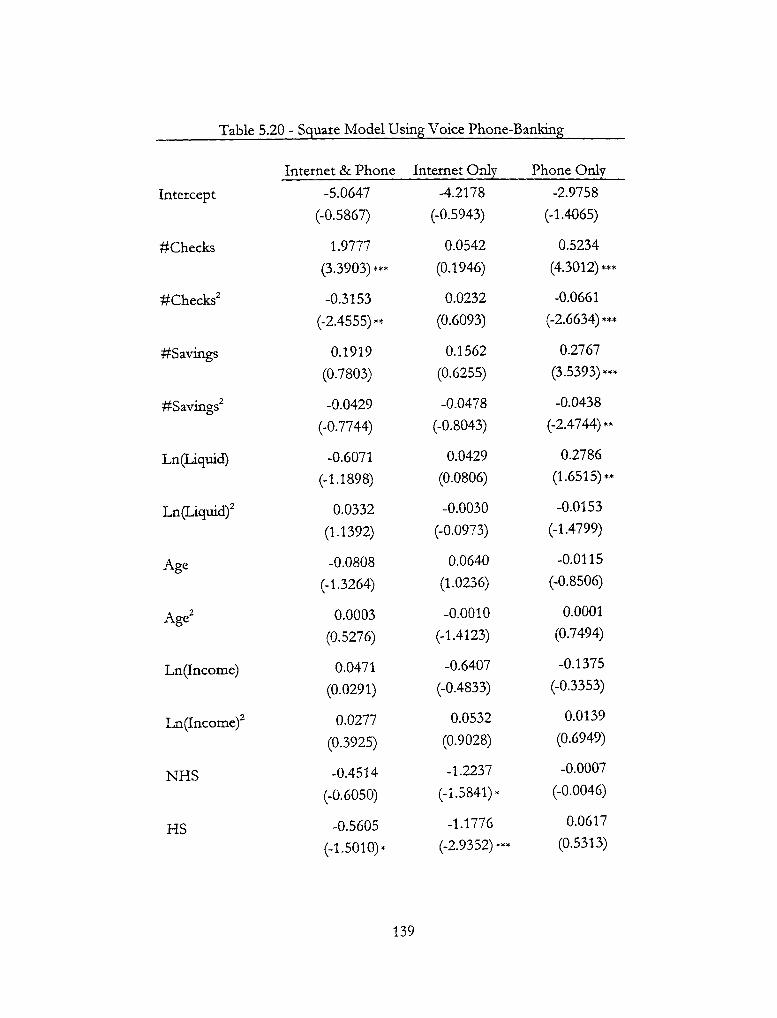

5.20 - Squared Model using Voice Phone-Banking 139

vii

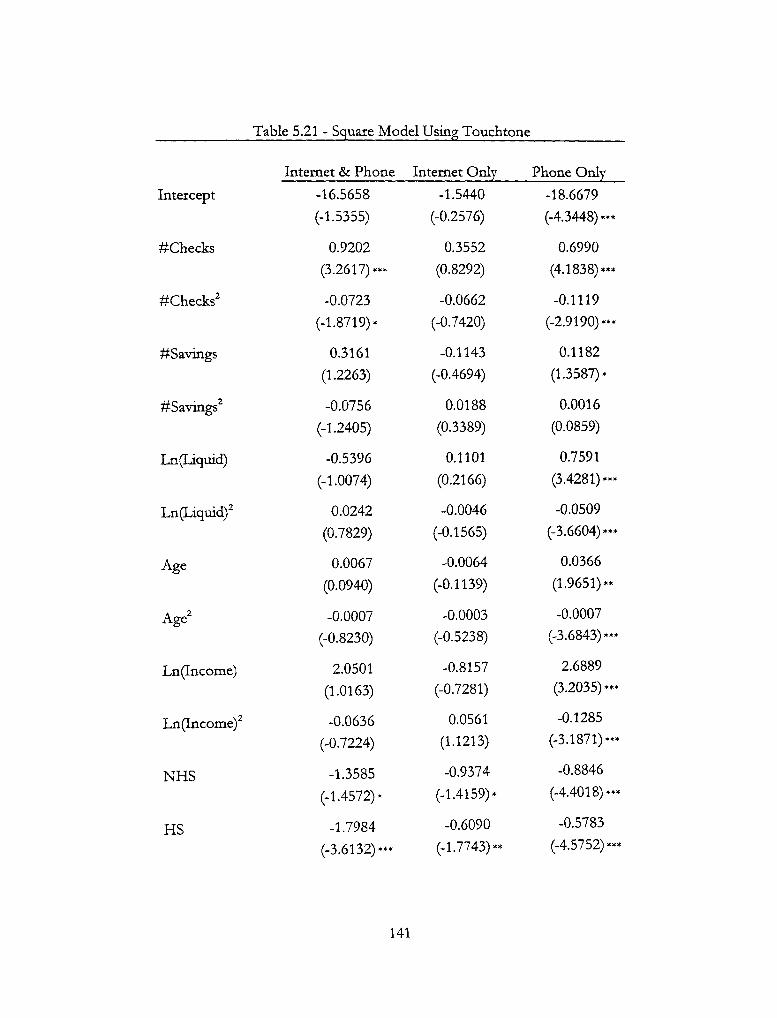

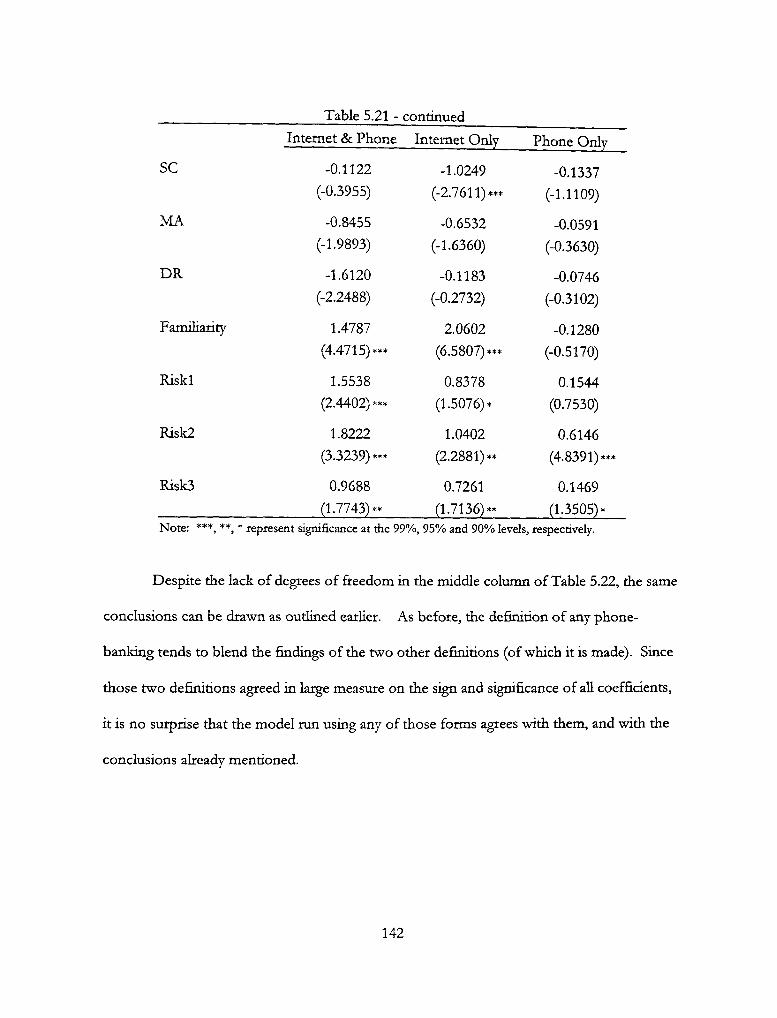

5.21 - Squared Model Using Touchtone 141

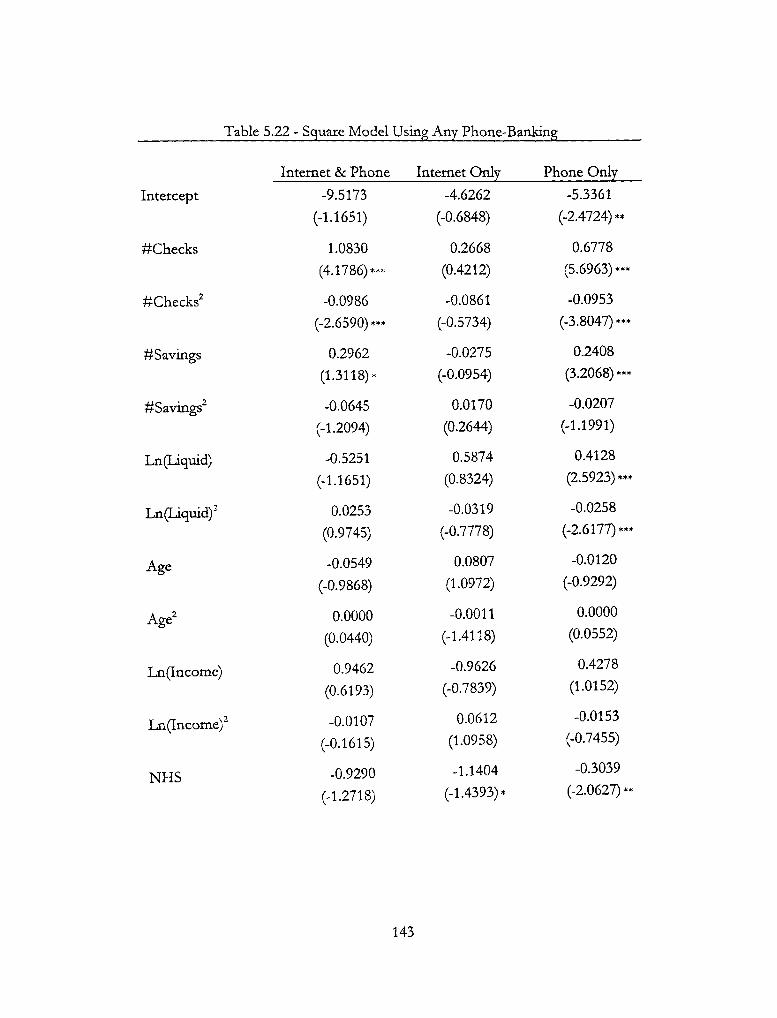

5.22 - Squared Model Using Any Phone-Banking 143

5.23 - Base P(Internet | Phone-Banking) 146

5.24-Base P(Phone-Banking|Internet) 148

5.25 - Squared P(Intemet | Phone-Banking) 150

5.26 - Squared P(Phone-Banking| Internet) 152

5.27 -Variable Subjective Probability 156

5.28 - Statistics of Fit 160

5.29 - Coefficient Estimates (\''oice) 163

5.30 - Coefficient Estimates (Touchtone) 164

5.31 -Coefficient Estimates (Any) 165

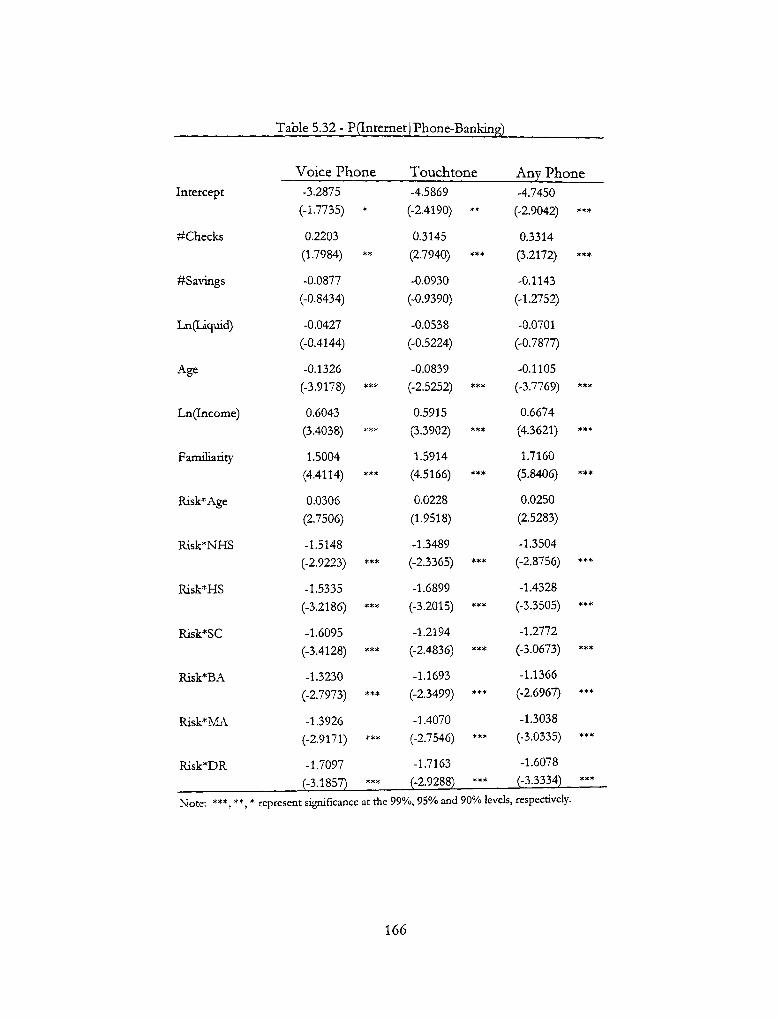

5.32 - P([ntemet | Phone-Banking) 166

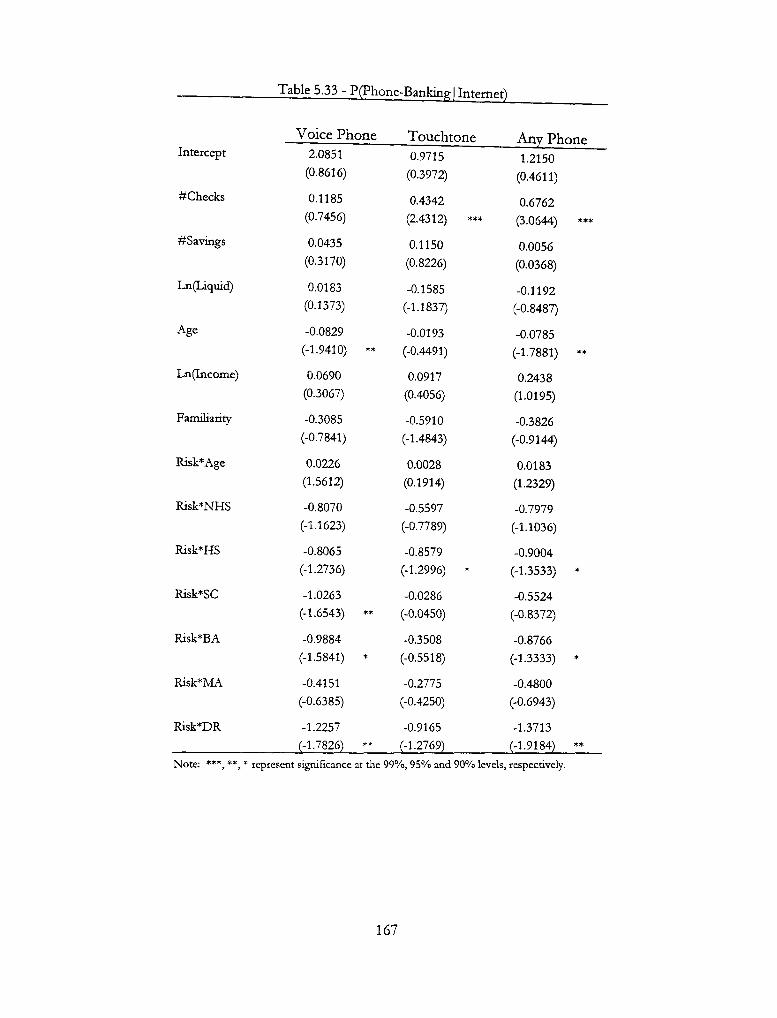

5.33 - P(Phone-Banking | Internet) 167

5.34 - Squared Model Statistics of Fit 173

5.35 - Squared Coefficient Estimates (Voice) 177

5.36 - Squared Coefficient Estimates (Touchtone) 179

5.37 - Squared Coefficient Estimates (Any) 181

5.38 - Squared P(Internet | Phone-Banking) 183

5.39 - Squared P(Phone-Banking | Internet) 185

vm

LIST OF FIGURES

1.1 — Internet Usage 1

1.2- Bank Internet Infirastructure 5

3.1 - Utility Maximization 47

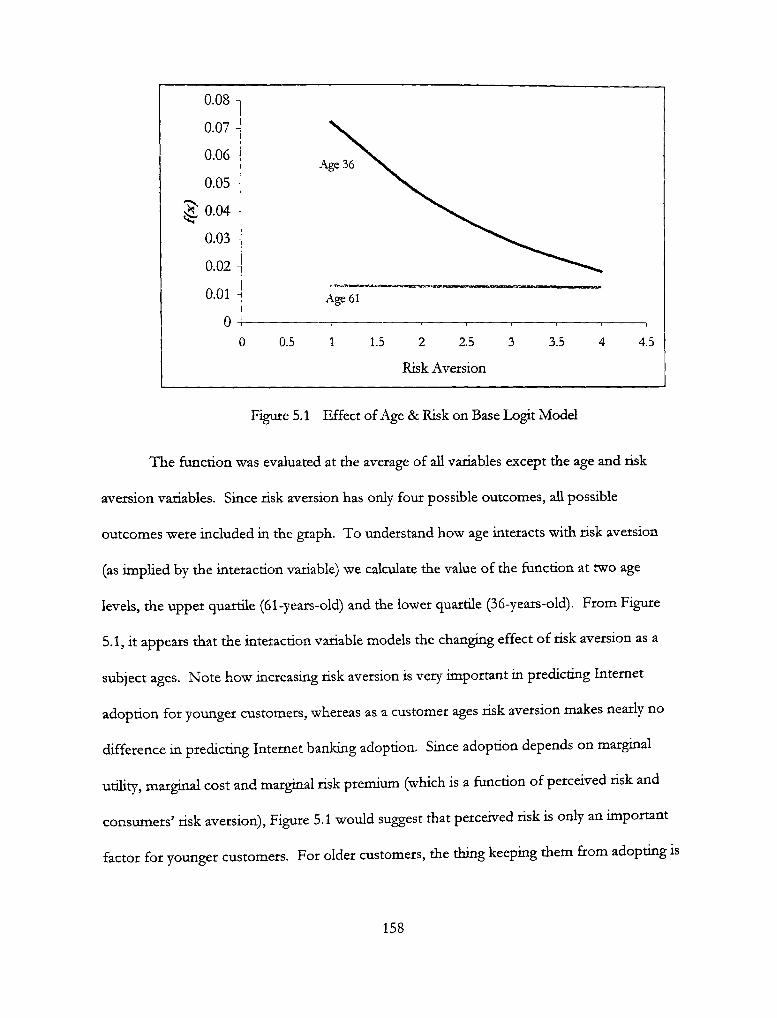

5.1 - Effect of Age and Risk on Base Logit Model 158

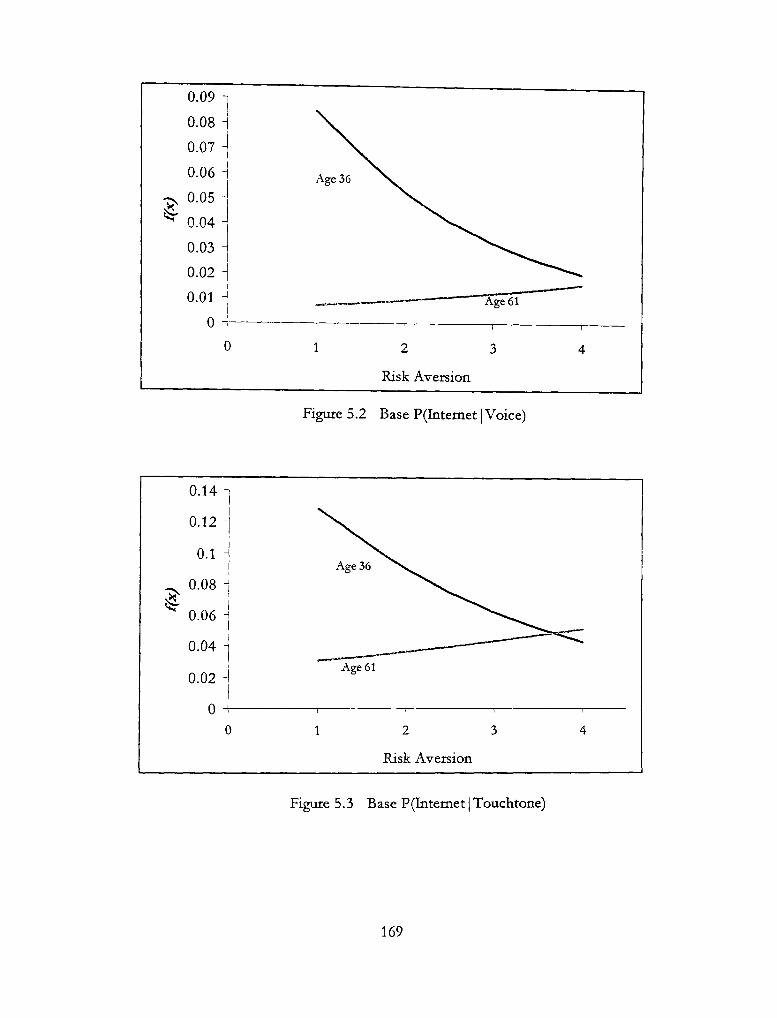

5.2 -Base P(Internet] Voice) 169

5.3 - Base P(Internet | Touchtone) 169

5.4 - Base P(Internet | Any) 170

5.5 -Base P(Voice|Internet) 170

5.6 — Base P(rouchtone | Internet) 171

5.7 -Base P(Any| Internet) 171

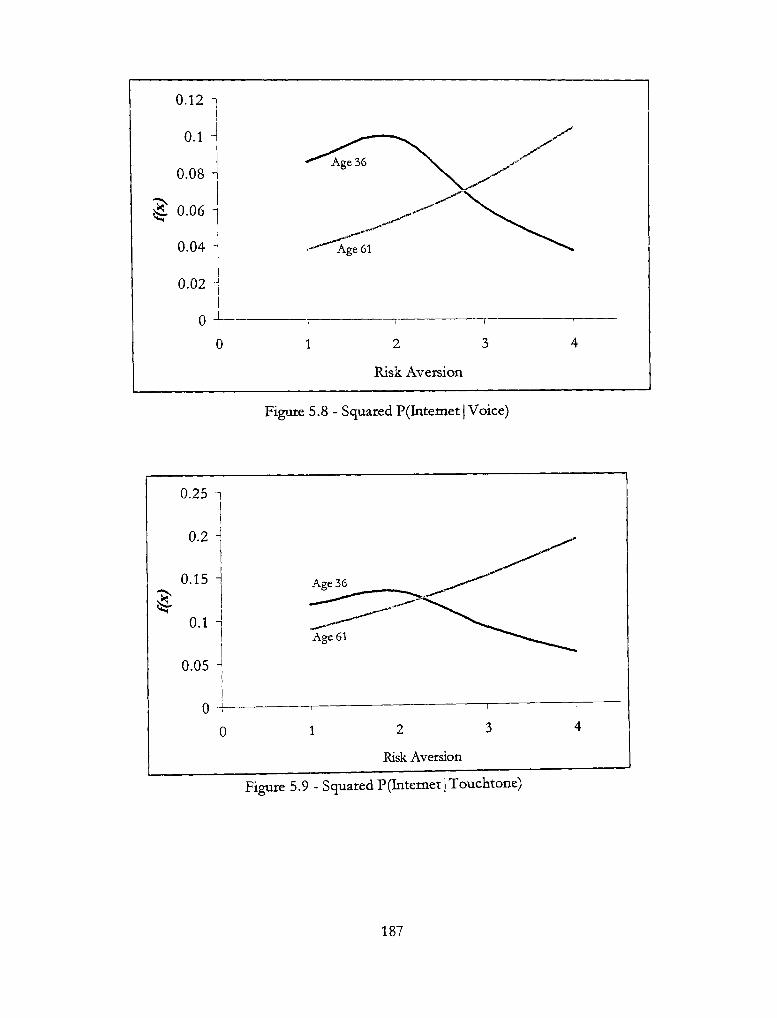

5.8 - Squared P(Intemet| Voice) 187

5.9 - Squared P(Internet ] Touchtone) 187

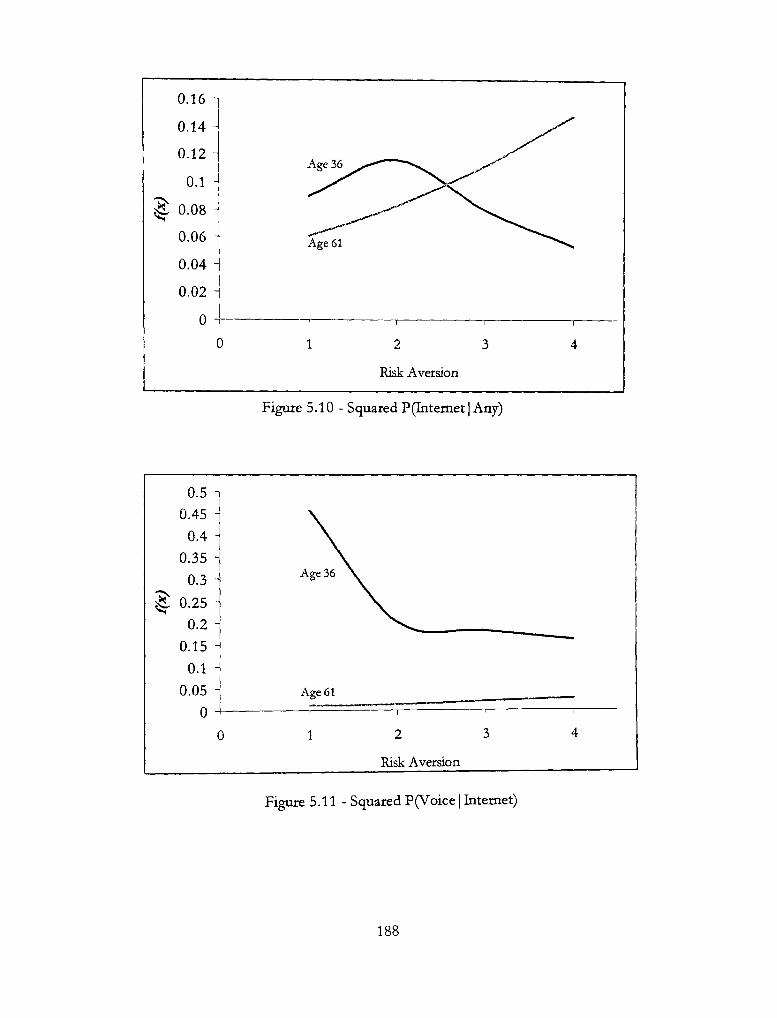

5.10 - Squared P(Intemet| Any) 188

5.11 - Squared P(Voice | Internet) 188

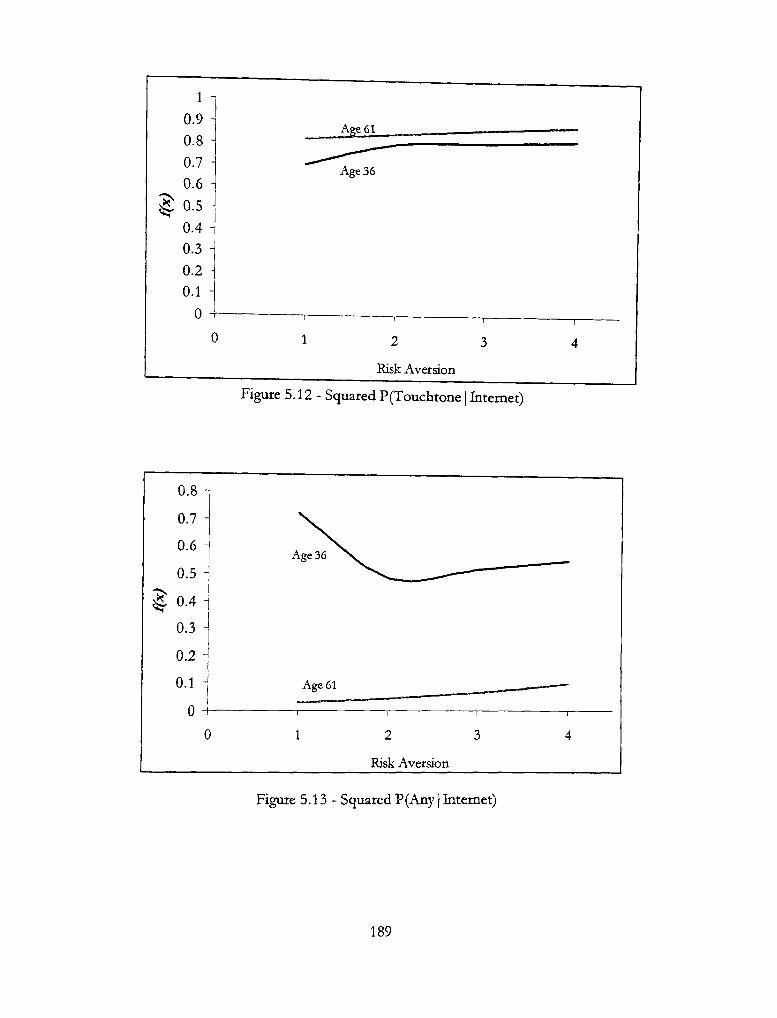

5.12 - Squared P(Touchtone | Internet) 189

5.13 - Squared P(Any | Internet) 189

IX

CHAPTER 1

INTRODUCTION

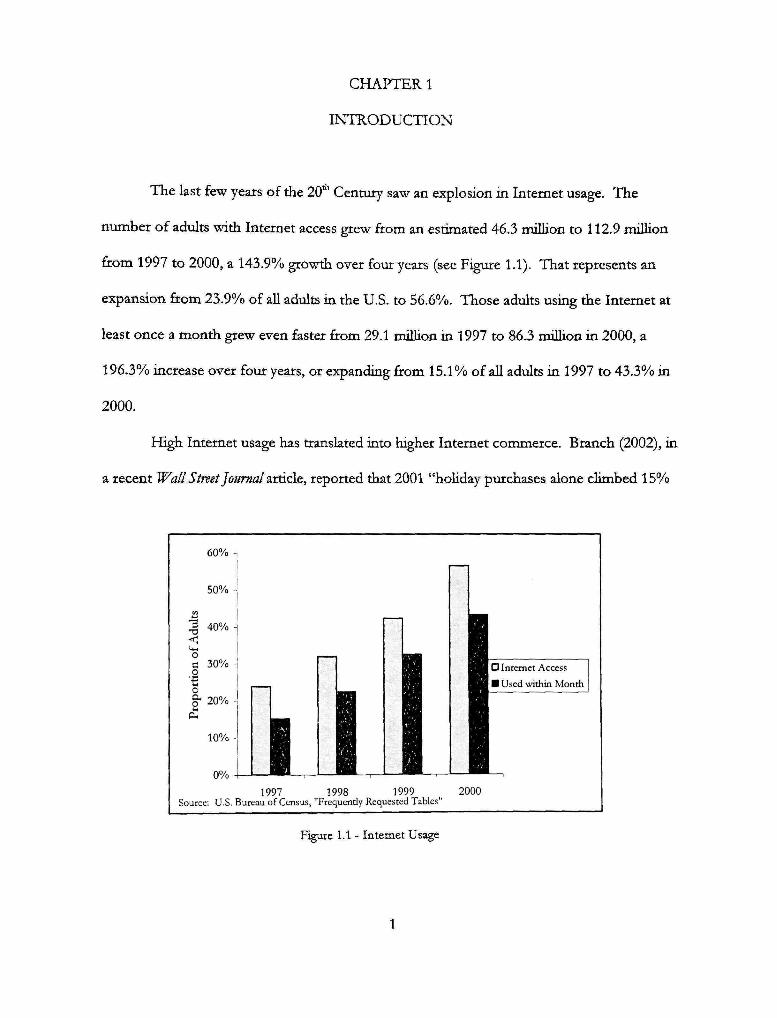

The last few years of the 20* Century saw an explosion in Internet usage. The

number of adults with Internet access grew firom an estimated 46.3 million to 112.9 million

from 1997 to 2000, a 143.9% growth over four years (see Figure 1.1). That represents an

expansion from 23.9% of all adults in the U.S. to 56.6%. Those adults using the Internet at

least once a month grew even faster from 29.1 million in 1997 to 86.3 million in 2000, a

196.3% increase over four years, or expanding from 15.1% of aU adults in 1997 to 43.3% in

2000.

High Internet usage has translated into higher Internet commerce. Branch (2002), in

a recent Wa/I Sireet Journal ntdcle, reported that 2001 "hoUday purchases alone climbed 15%

60% -1

50% -

Ad

ult

s 1

G 30% 0 •ci u O §- 20% -

10% J • 1 1

1997 Source; U.S. Bureau of Census,'

D Internet Access

• U.sed within Month

1998 1999 ^ 2000 Frequendy Requested Tables"

Figure 1.1 - Internet Usage

to nearly $14 bilhon from $12 billion in 2000." Included in this growth are industries long

thought to be poorly sviited for die Internet. In another Wall Street Journal 2irtid&, Totty and

Grimes (2002) show how adjusting the services of grocery, fiamiture and wine e-tailers has

allowed even these industries to succeed on the Internet. From a marketing standpoint, it

would seem that creating a product with the right mix leads to success. For most retailers,

customer risk sensitivity is only a passing concern.

As the popularity of the Internet grew, many expected it to fundamentally change the

way business is conducted. Electronic commerce appeared to eliminate many fiictions

hindering efficient price discovery in conventional retailing. With the Internet, consvimers

should be able to screen more alternatives in less time. It also is a medium where

information on different goods and services can more easily be exchanged. With this ease of

collecting and analyzing information, many expected intense price competition. Consumers

were to enforce price competition through extreme price elasticity.

But consumers were not the only hypothesized beneficiaries. Businesses operating

on the Internet were supposed to have seen lower costs because they would have to hire

fewer salespeople (or none at aU), since the same product descriptions could be given to an

unlimited number of potential customers at a marginal cost approaching zero. They would

also not need as many physical locations, reducing overhead. Many electronic retailers

would save on working capital since they would not necessarily need to have inventory until

a sale was made, and they would be paid as soon as it was sold. Market research would be

cheaper, and if the business were large enough could be another source of income. And

margins would be easier to manage because menu costs would be lower.

Since consumers were expected to cause intense price competition and suppliers

would be able to reduce dieir costs, most of the margin squeeze would, over the long run,

benefit the consumer. The margin squeeze was expected to be enforced by low barriers to

entry (i.e., low start-up costs). Therefore, to compete in the "new economy" businesses

were beginning to believe they had to have an online presence, and most saw theoretical

reasons to believe a margin squeeze was imminent.

Banking traditionally has been very labor intensive. One main hypothetical benefit

to Internet banking adoption has been the reduced cost. Whether giving the customer

information, transferring funds between accounts, or applying for a loan, aU traditional

banking activities include interaction with bank employees, and require a convenient branch

location, paper forms, and a receipt. A transaction as simple as caslnng a check can cost a

bank $1.10\ If customers used the Internet to interact with the bank, the costs would faU

dramatically, even when compared to other forms of remote bank access. Humphreys

(1999) estimates tliat Internet transactions cost less than $0.01 per transaction, compared to

ATM of $0.27, telephone of $0.54, mail of $0.73 and in-person of $1.50. These figures are

almost identical to those quoted by the Department of Commerce^.

But Internet banking supposedly had one other tremendous advantage, pent-up

customer demand. Humphreys (1999) describes demand as follows:

It took nearly 30 years for technology like ATMs to be widely accepted by the public, and screen phone technology never really took off Even the furst attempts at ditect-dial PC home phone banking by some of the larger banks in the middle 1980s met witii Kttle success. Internet banking is

' Robinson, Ten (2000). "Internet banking: Still not a perfect marnage," Informationweek. (782): p. 104, (April 17, 2000).

2 See U.S. Department of Commerce, "The Emerging Digital Economy," Washington D.C., April 1998, p. 29. littp://www.ecotnmcrce.gov/EmcrgingDig,pdf.

different-this is tlie first time customers have led the technology and encouraged banks to move forward rather than the banks pushing the technology on the customer. Consumers want Internet banking because they have the necessary technology-a computer and Internet access-and they are aheady using it to conduct electronic transactions, (p. 8-1)

The implication in this statement is that demand is so high, if you build the

infrastructure, they will come.

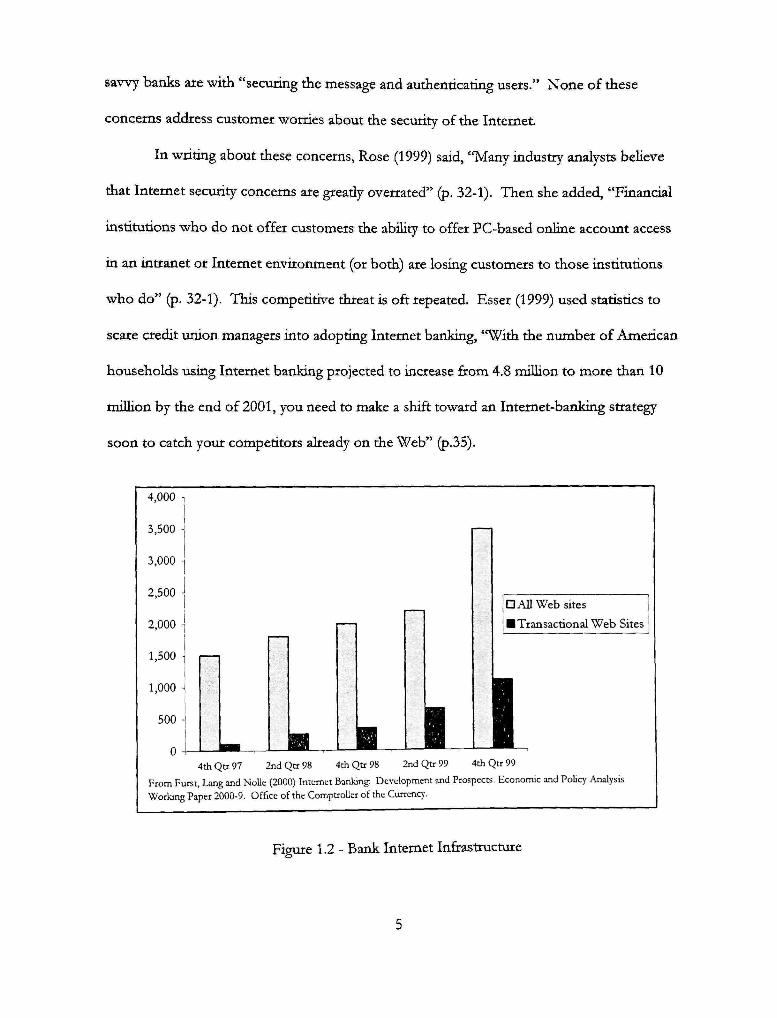

No wonder tiie e-banldng infrastructure has been a major priority at most banks.

Furst, Lang, and Nolle (2000) report that by die thicd quarter of 1999, only 20 percent of

national banks offered Internet banking, which represents 84 percent of all small deposit

accounts. This capabihty was built qiiickly. In the fourth quarter of 1997, only 103 national

banks were reported as offering transactional Internet banking, but by the second quarter of

1998 (six months later), 258 banks were offering Internet banking services (see Figure 1.2).

By the third quarter of 1999, tliis figure had grown to 541. In a study of 3000 banks, MarHn

(2000) reports planned e-banldng investments to grow from $500 million in 2000 to $2.1

biUion in 2005. The ABA Banking Journal estimates that by 2003, 86% of all banks, savings

and loans and credit unions wiU have adopted transactional e-banking technology .

But only 20% of banks had adopted transactional Internet banking in 1999. The

biggest reason for low bank adoption seems to be concerns with security. Their security

concerns are not customer-oriented, but a concern for risk management on the banks' part.

Koonce (1998) quotes libby Ghekiere, chair of NACHA's Internet Council and senior vice

president of electronic commerce with Bank of America's Interactive Banldng Division as

placing traditional banks concerns with "accountability and hability," but those of Internet

^ Bielski, Lauren (2000). Online banking yet to deliver, ABA Bankingjournal, vol. 92 Issue 9

(September), pp. 6,12+.

savvy banks are with "securing the message and audienticating users." None of these

concerns address customer worries about the security of the Internet.

In writing about these concerns, Rose (1999) said, "Many industry analysts beheve

that Internet security concerns are gready overrated" (p. 32-1). Then she added, "Financial

institutions who do not offer customers the ability to offer PC-based online accovmt access

in an intranet or Internet environment (or both) are losing customers to those institutions

who do" (p. 32-1). This competitive threat is oft repeated. Esser (1999) used statistics to

scare credit union managers into adopting Internet banking, "With the number of American

households using Internet banking projected to increase firom 4.8 million to more than 10

miUion by the end of 2001, you need to make a shift toward an Internet-banking strategy

soon to catch yoxir competitors already on the Web" (p.35).

4,000 1

3,500

3,000 -

2,500 J

2,000 \

1,500

1,000

500 -

0 -

From Ft Working

n H 1

OAU Web sites

j • Transactional Web Sites

1 1 4thQtr97 2ndQtr98 4thQtr98 2ndQtr99 4thQtr99

rst, Lting and Nolle (2000) Internet Banking-. Development and Prospects. Economic and Pobcy Analysis

Paper 2000-9. Office of the Comptroller of the Currenq.

Figure 1.2 - Bank Internet Infiastructure

Security concerns in nearly all of die professional literature deal with why banks are

slow to supply Internet banking. Totty (1999) started his article on online security by saying,

"Three years ago, most consumers harbored doubts about online security, especially when it

came to financial transactions or e-commerce. But consumers seem to be getting over their

fears if miUions of online credit card transactions are any indication" (p. 70). He then

insinuated diat customers now place tiieir trust in the due-diiigence of financial institutions

in building secure Internet facilities. But note diat die statistics he quotes are for credit card

transactions. The growth of Internet banking is not as rosy.

By third quarter 1999, 20% of all national banks offered transactional Internet

banking services, according to Furst et al. (2000). Although that may not sound hke many, it

represented 90% of all banking assets and 84% of all small deposit accovints. Despite the

availabihty of Internet banking services, only 5-7% of all households actually used it in 1999.

And although the infrastructure has seen rapid development over the past several years, the

growth in the number of households using e-banking has been almost flat.

Academic research into electronic commerce in general has tested the fricrionless

commerce claims stated earher. Although it appears that prices are lower than at

conventional retailers, as are menu costs, Internet commerce introduces its own fiictions

including what most researchers thus far have called trust. Trust simply means if I order

sometiiing via the Internet, do I get it, in other words, the customers' trust in the firm. But

there is much we still do not know. Research thus far has focused almost exclusively on the

differences between Internet only retailers versus conventional retailer. Due to sales tax

laws, retailers need to choose whether they will offer electronic or conventional services.

Large companies can rarely do both. Few have addressed services offered over the Internet.

Fewer yet have examined electronic financial services. And none have addressed the

demand for Internet services.

Consumer demand for Internet banking services is the main topic of this paper. We

approach demand using a traditional utility optimization framework. In order to compare

our results with other remote banking services, we also examine phone-banking usage using

a similar model. Phone banking was used as a comparison because it allows similar access

(after hours and remote access, without cash access available to ATM users), but enjoys a

much higher adoption rate than that experienced by Internet banking. The model impHes

that consumers configuring access channels to their accounts wiU analyze the expected added

utihty to their account, the expected disutility due to potential security breaches, and any

added cost. Most of the additional cost is computer hardware (in the case of e-banking) or

computer hteracy.

In a static world, rational consumers would assess the marginal benefit of a remote

banking solution with its marginal cost. If the marginal benefit outweighs the marginal cost,

they should adopt it. However, in realitjf, the outcomes are not known in advance.

Therefore, there is an element of risk. Using a subjective set of probabilities for all potential

outcomes, the consumer can assess the expected marginal benefit and compare it to the

expected marginal cost. The difference between the static marginal cost/benefit analysis

under certainty and the dynamic cost/benefit analysis imder uncertainty is called the risk

premium. The theoretical chapter of this research demonstrates that if the risk premium

were eliminated, aU people would adopt all forms of remote banking (or would be indifferent

to adopting it).

Based on the theoretical model, several empirical models are developed to compare

and contrast die Internet banking adoption components mentioned above with those of

phone banking. Fkst, logit models are proposed diat model individual remote banking

decisions over conventional banking. Logit (logistic regression) models estimate die

probabihty of an outcome; we use this technique to estimate the probability of Internet

banking adoption. These models test whether phone banking adoption (or Internet banking

adoption) is a fiinction of the components described in the theoretical model A multiple

dimensional version of this model is then proposed, estimating joint probabihties of

adoption (Internet banking and phone banking).

We consider the outcome space of phone-, Internet and conventional banldng

solutions. If banking consumers are truly rational, they wiU choose the configuration of

conventional, Internet and phone-banking that maximizes expected utility. Philosophically,

consumers would adopt a remote banking solution as long as the expected increase in utility

is larger than the expected cost. The fact that more than two outcomes are possible suggests

that a multinomial empirical approach to this solution would be the most appropriate. Using

this outcome space, we can assess the conditional probability of adopting Internet banking

given the consumer has adopted phone-banking (and vice versa).

This conditional probability wiU help us assess the marginal propensity to adopt

Internet banking given phone-banking (or vice versa). Factors affecting Internet banking

can then be compared with those of phone banking. This comparison will yield information

on what makes phone banking much more widely accepted than Internet banking-greater

benefit, lower cost, less risk, or a combination.

For the consumers' Internet banking risk premium to be interesting to most bankers,

it must be a variable over which they have some influence. Most academic papers assume

that all consumers have identical subjective probability distributions, in essence assuming

that all market participants interpret publicly available information the same way. Identical

subjective probabilities are much easier to model. From a utihty maximization framework,

theories tend to focus on the risk premium assessed by consumers. The risk premium is a

compound construct, made up of both perceived risk and the consumer's risk aversion. To

be consistent with most academic research, we also model the adoption decision by

assvmung identical subjective probability sets.

If we can hypothesize what variables might be important in revising probabihties, we

can model the adoption decision under a varying subjective probability set framework, which

is proposed in this thesis. Most of the variables in the budget constraint (i.e., age, education

and famiHarity with the electronic financial services) are proposed as possible variables

affecting the subjective risk assessment.

This paper adds to the current body of knowledge in several ways. First, the focus

of this paper is on the demand. This is the first research diat empirically models the

consumer adoption of e-banking (or phone banldng for that matter). This is the first paper

that models overall consumption demand for Internet products or services (others have

looked at branding, price elasticity, and other issues, but not overall demand).

Second, this paper examines the role of perceived risk in the Internet commerce

decision. One component in the adoption model is the expected disutihty associated with

adoption. This measure allows us to analyze and hopefully compare the subjective

probability of outcomes leading to disutihty. Because most Internet banking is offered by

banks that also offer conventional banking services, we can model the decision to adopt

Internet banking using variables that measure different components of risk premium.

Initially, we will assume that all consumers have an identical set of subjective probabilities.

Then we will examine what might explain differences in subjective probabihties.

The paper wiU proceed as follows. Chapter 2 reviews academic hterature exploring

the economics of electronic commerce. This review starts with all electronic commerce and

narrows to cover just the electronic banking. Although no pubhshed paper has used

financial economic models to analyze either the characteristics of the demand for Internet

banking or its effect on the bottom-line of the institution, there are relevant papers in related

fields. First, there is a growing hterature focused on the developing e-commerce field.

Second, there are some important financial economic papers exploring the motivation of

banks adopting remote access technologies (focusing on ATMs and phone-banking). Finally,

there is an extensive hterature that examines the financial impact of improved technology in

banking.

The Hterature review also contains a brief review of current articles in the

professional press. Since there is no academic Hterature in the field, the "conventional

wisdom" in die field, among practitioners is also used to develop our understanding theory.

Most of the Hterature in the e-commerce field is either descriptive in its analysis or

broader (considering all industries) in scope than this paper. As such, they tend to miss

important issues relevant to the demand for financial services, such as subjective probabihty.

Most papers analyzing e-commerce are written by management or marketing researchers.

The closest they come to perceived risk is the concept of trust-describing whether one

beheves one wiU receive what one buys over the Internet.

10

Chapter 3 presents the models and the hypotheses impHed by the theory. As

mentioned above, this model is based on the classical optimization of consumer utihty.

Models under certainty and uncertainty are compared to show the impact of risk on the

adoption decision; in short if the outcome were certain, adoption rates of Internet banking

would be significantiy higher. The ultimate outcome of the theoretical model is that

adoption depends on potential utiHty gains by adopting, the consumer's risk premium and

the added cost of the service, including htiman capital cost for computer Hteracy. But the

most interesting outcome is that if Internet banking were offered in an environment of

complete security, all bank customers with the requisite stank costs would use the service.

That finding makes perceived risk the driving force of Internet banking adoption.

Chapter 4 describes the data used as weU as the methodologies proposed to test

those hypotheses. The data used in this paper comes from the Svuvey of Consumer Finance

for 1998 and 1995. This data is compiled by the University of Chicago for the Board of

Governors of the Federal Reserve, and is used more in economics papers than finance

papers. These papers are briefly re^tiewed to determine how the data have been treated in

the past, and the reputation the dataset has in the academic press. The chapter also

proposes several logit models consistent with die theory of Chapter 3 to measure the vaHdity

of the theory and the importance of individual components in the remote banking adoption

decision.

Chapter 5 presents the empkical results of die tests described in Chapter 4. For die

most part, the sections in this chapter correspond widi diose in die mediodology chapter.

The descriptive statistics are presented. Since many of die variables are quahtative, we

present not only firequencies, but critical cross-tabulations. The descriptive statistics section

11

also contains relevant univariate statistical tests. After presenting these descriptive statistics,

the logistic regressions presented in the methodology chapter are presented, supplemented

by follow-up tests to refine the analysis set fordi in Chapter 4.

Chapter 6 synthesizes the findings, tying the theory to the methodology and

empirical findings and interpreting what it all means to the current state of the theory of

electronic commerce in general and the demand for electronic financial services in particular.

It closes by noting the major contributions of this research and the unanswered questions

left by this thesis.

12

CHAPTER 2

LITERATURE REVIEW

There are no papers that look at demand for Internet banking from a micro-

economic perspective. However, diere are odier researchers who have looked at markets for

electronic commerce. Some papers also exist tiiat analyze aspects of the Internet banking

market. There are many claims made by electronic business proponents that the Internet

will significantiy change the retailing landscape, the same can be said in the professional

banking hterature. Some of these claims are based on economic models. Section 2.1

presents these claims as a coherent theory of frictionless economy and reviews academic

papers that describe how well the impHed claims of that theory are supported by empirical

evidence.

A similar coherent "theory" could be developed for Internet banking. Some have

made similar claims, but very Htde research has been done on the subject of Internet

banking, only some theoretical claims and basic empirical evidence. The empirical evidence

includes cost reduction as well as motivations for banks adopting the service. With only one

exception, this Hterature is not aimed at Internet Banking. Some research has been done on

banks' motivation for offering remote access innovations, such as ATMs and phone-

banking. As with the electronic commerce Hterature, these papers focus on the supply of

remote banking services. These papers are briefly summarized in section 2.2 Remote Banking

and compared to the findings of the general electronic commerce Hterature.

Because this research area is so new, die Hterature review is supplemented by a brief

overview of the coverage of Internet banking in the professional press. Unlike the academic

13

press, diere are many articles on this subject in die professional banking journals. Section

2.3 only briefly discusses die current state of conventional wisdom in diis area.

Taken togedier diese areas, electronic commerce and remote banking, form a

foundation upon which die demand for diese services can be analyzed. The findings of

these papers are then summarized in Section 2.4.

2.1 Internet Market Overview"

From a customer perspective, the Internet would be used as a channel for products

and services only if the added utihty outweighed die added cost. Alba et al. (1997) analyzed

the many benefits that interactive home shopping was thought to have over conventional

retailing. OnHne customers have greater alternatives, and can screen them faster and more

efficientiy. In addition, the Internet is a medium through which customers can gain added

information about the good/service. InformaUy using a traditional utiHty maximization

firamework. Alba et al. (1997) talk theoretically about what kinds of goods would seem to

have a competitive advantage online. The analysis uses what the authors consider to be

utiHties versus what they consider costs. None of this analysis considers the subjective

probabihty distribution of possible outcomes, and therefore, does not address the role of

perceived risk of the dehvery system.

Many of the early e-commerce pundits, along with Alba et al. saw the Internet as a

way of overcoming some market frictions. It was assumed that the nature of Internet

shopping would allow customers to search ah sellers and find the products that they wanted

at the cheapest price. Search costs, until now a market friction, would nearly be eliminated

'• Most of the introduction to this section comes from Israilevich (2000).

14

in many industries, which would force the price of goods offered through the Internet closer

to thek margmal costs. It was hoped that the Internet would gready reduce (or eliminate)

much of the frictions involved in the price discovery process.

But consumers were not the only beneficiaries of the new distribution channel,

suppHers would also benefit from the change in business channels. They would be able to

sell products cheaper because they would not have to hire as many salespeople, nor build as

many facihties. As mentioned above, customers would be able to gather information about

products without salespeople. Internet companies could even save on the working capital

needed because they are paid closer to the time when the goods are exchanged, and in some

instances the inventory is not ordered until after a sale is made. In addition, if information is

managed efficiendy, the Internet can save money in marketing research, and customer

information itself may become a profitable by-product of normal business transactions.

Finally, Internet companies are more easily able to manage their margins because the menu

costs are far less than a conventional store.

Unfortunately, there is a downside to the lower operating costs. There are lower

entry costs, lowering the barrier to entry for most industries, worsening the margin squeeze

explained above. This margin squeeze pre-supposes infinite price elasticity, assuming that

price is the only relevant variable to the online shopper.

In short, the Internet was to provide a shopper's Utopia, the ultimate beneficiaries of

the this styHzed model would be the consumers. Normal economic frictions were to

disappear as shoppers, armed with improved information, forced the market to a higher level

of efficiency. Because aU fitrms are seen in this model as operating under perfect

competition, ah benefits of this added efficiency would be captured by the consumer.

15

Section 2.1.1 reviews die tests of most of diese hypotiieses, finding that the styHzed worid

exists primarily on paper. Section 2.1.2 focuses on die frictions tiiat tend to differentiate the

actual Internet market from the theorized Internet market.

2.1.1 Emphical Evidence about the Internet Market

Research has begun to paint a different cyber-landscape than that portrayed by the

Utopian theorists. Brynjolfsson and Smith (2000) tested many of the central hypotheses of

the model described in the previous section, using over 8,500 price observations of

homogeneous books and CDs over a 15-month period. They compared 41 Internet retailers

with conventional retail outiets. The books and CDs chosen were spHt between very

popular items (best-seUers) and more obscure tides (aldiough aU tides had to be held by all

oudets in the study). Prices quoted on the Internet were, on average, 16% lower than in

conventional stores. When adjusting for taxes, shipping and shopping costs the Internet

averaged 9% lower costs, supporting the lowering price hypothesis. Online price

adjustments (a measure of menu costs) were 100 times smaUer than conventional stores,

supporting the lower menu costs hypothesized. Both of those findings support the Utopian

view of the Internet.

However, price dispersion did not necessarily comply with the theory. The raw

price data show that there is more dispersion in Internet prices than among conventional

retailers. The authors re-weight their findings according to market share, and find that

dispersion is now lower among Internet retailers, which raises another problem. The lowest

prices do not have the highest market share, which suggests that consumers are not as price

16

sensitive as die Utopian models would suggest. This is a senous problem for die overall

model, since extreme price elasticity drives much of die findings of die dieorized model.

But diat IS not to say diat price is unimportant to cyber retailers. Price sensitivity

does exist. Goolsbee (2000) tested to see whedier high sales taxes can induce customers to

make more purchases via. die Internet. He used a proprietary survey conducted by Forrester

Research, a market research company m Cambridge, Massachusetts, in December 1997.

They surveyed 110,000 households and asked questions about onhne purchase of 13 types of

goods onhne, as well as consumer demographic data. ControlHng for income, education,

age, and computer access (botii at work and at home), he found that Internet purchases were

higher given high local sales tax rates. These results suggest that there is some price

sensitivity regarding online purchases.

Degeratu, Rangaswamy, and Wu (2000) examined prices of groceries. They

compared sales and price data from sales of 300 subscribers of Peapod, Inc., an online

grocery subscription service, and conventional retailers in the Chicago area between May

1996 and July 1997. The conventional shoppers were interviewed by IRI and consisted of

1,039 shoppers. They found that brand named goods were demanded more by onHne than

conventional customers, but only on certain types of items. They further found that factual

information was more important to online shopper than sensory (appearance) information.

They concluded that evaluating products online could lead to missing information pertinent

to the purchase decision. Wlien there is missing relevant information, customers use the

price as a signal of quahty, and therefore, they do not appear to be as price sensitive as

conventional shoppers.

17

In short, prices seem to be lower for online goods than conventional retail goods,

and menu costs appear to be lower, but Internet consumers do not appear to be as price

sensitive as was hypothesized. The frictionless economy appears to merely be an economy

with different frictions. One of die fictions was identified by Degeratu et al. was that the

information set was different for online shoppers than traditional shoppers.

2.1.2 Empirical E-stidence Regarding Internet Frictions

These conclusions about information were strengthened by Lynch and Ariely (2000)

who investigated price sensitivity in a simulated electronic wine market. They found that as

the cost of information on the quahty of the goods increased, the price sensitivity decreased.

In other words, goods became less price-sensitive as more characteristics are used in the

purchase decision. However, as aU information costs, including price information, become

less expensive, customers become more price-sensitive. Therefore, price-sensitivity can be

used by retailers to their advantage, and if information about a good is withheld from the

market, it may actuahy increase the demand for that good (if its expensive) causing a market

friction.

These general conclusions were supported by demons, Hann, and Hitt (1999), who

found one more friction. They investigated the price competition between ordine travel

agents. They examined tickets written for five corporate cHents for April 1997, and

compared them with other onhne travel agents. Some of thek findings were clearly

damaging to the Utopian cyber-market presented at the beginning of this section. Prices

differed by as much as 18% for the same flight. They found diat some price dispersion is

18

caused by the same company. Bodi the highest and lowest priced onhne travel agents m

thek study were owned by die same parent company. The only difference between the two

agents was that one (die less-expensive) offered a less user-friendly web-design, suggesting

that if shoppers were willing to spend more time, even on the Internet, they could have

gotten better deals on travel in 1997. These findings are consistent with the cost of

mformation argument forwarded by Lynch and Ariely, but would also be consistent with the

hypothesis that the higher the consumer's human capital investment, the more benefit one

gains from Internet shopping.

Another theoretical prediction about the Internet marketplace that does not seem to

be as accurate as it once appeared is that of barriers to entry. Prices of goods on the Internet

were expected to fall close to marginal costs due to the low cost of starting an e-business.

Although it is relatively inexpensive to start an Internet based business, there are economies

to running some types of electronic businesses that may not exist elsewhere. Bakos and

Brynjolfsson (2000) showed that for information based companies on the Internet where

marginal costs are very low, there exists an economy of aggregation, where the company can

simply offer more and more information content to make a more attractive offer. They

show that larger bundlers (usuaUy larger companies) have an advantage in outbidding smaUer

ones. Further, they show that larger bundlers (companies that bundle many information

products together) can make a tougher competitor than smaUer, single-product companies.

They find that in some instances simply adding one information product to thek line, they

can enter and dominate a new market; which is easier to do if you have many such products

that can be added at low marginal costs. Because of the strategic advantages discussed thus

19

far, small information companies may have Httie incentive to create new informational

content (although larger bundlers may have more incentive to iimovate).

Bakos and Brynjolfsson's conclusions only are appHcable to informational goods.

Physical goods with larger marginal costs do not tend to foUow these principles, although

bundling goods and services have long been seen as adding value to the customers. It is

unclear from thek research whether this economy of aggregation holds for financial services,

and would probably depend on the marginal cost of those services. If financial services tend

to have lower marginal costs, thek findings could mean that larger financial companies have

a competitive edge in electronic commerce. As wiU be discussed later, (account) aggregation

is a hot topic in the professional Internet banking Hterature, and has much the same

arguments at it root as informational product aggregation.

The final friction fotind in the empirical work on Internet commerce is typicahy

described as trust, since it is usuaUy covered in the marketing Hterature. Israelevich identifies

it as risk aversion, but as used in the Hterature, it is whoUy insufficient for financial assets.

Trust refers to whether the customer beheves that the product wiU Hve up to promises made

about it. Trust can refer to product quahty, as weh as the retailer's service after the sale (or

whether the goods are ever shipped to the customer). Examples ki the Hterature include

Internet customers brand loyalty in the Shankar Rangaswamy and Pustateri (1999). This

loyalty was further tested with onhne retailers that have been used before. If the customer

had a good experience the first time, they are likely to return.

These conclusions are supported by Brynjolfsson and Smith (2000), who found that

retailers with an estabhshed name and reputation in conventional retailing could command

between 8-9% higher prices than die competition, just because they feh more confident that

20

they would get what they purchased, and that problems could be resolved with a real person

in a convenient location. This is one of very few papers in this genre that

Urban, Sultan, and QuaHs (1999) used a cHnical experiment to examine the effect

that an imbiased onhne "advisor" had on the purchase of products. The "advisors" in

essence provided information about the product or the retailer, and were in no way

associated with the retailer. They found that more subjects were willing to purchase the

product recommended by the unbiased advisor than those without the "trusted" advisor.

Since this was a cHnical experiment, not involving a real company or real money, there had

to have been some halo effect in the results.

2.2 Internet Banking Overview

Many of the expectations of e-commerce were shared by those theorizing the impact

of the Internet on distributing financial services in general and banking in particular through

this new medium. l ike Alba et al., Mols (1998) also saw consumers maxknizing utiHty

subject to budget constraints. He also expected price competition, suggesting that those

banks wanting to participate in this channel wiU have to offer better rates, because Internet

customers are sophisticated and extremely price-conscious. Mol sees a world where banks

focus thek development in eitiier branch banking or Internet banking. This hnpHes that die

overall cost structure will depend on the dominant channel chosen.

The hnpHcation of tins e-banking vision is extreme price elasticity. If the theories of

e-commerce are consistent across channels (from electronic retaihng to electronic financial

services) then we would expect a lower cost strucmre, and higher price elasticity, which

would lead margms to be squeezed to approximately marginal costs. In addition, barriers to

21

entrance wiU be low, enhancing competition and reducing costs to consumers. These are

essentially the same assumptions made of e-commerce in general.

Few empirical papers in this genre look specificaUy at Internet banking. Although

many of these papers look at adoption of technology, some of thek knphcations can be

apphed to e-banking. Section 2.2.1 will review empirical findings regarding price

competition and elasticity. Section 2.2.2 wiU review empirical findings regarding motivations

for adopting remote banking services.

2.2.1 Price Competition and Elasticity

Price competition suggests that the production function of banks participating in

Internet banking wiU shift. In addition the empirical efficiency of the industry, how close

banks appear to be operating to the most efficient expansion path, would deteriorate as long

as aU banks do not adopt these technologies simultaneously. Mol would expect that not aU

will adopt them at aU, so the efficient expansion path would permanendy deteriorate.

Cost efficiency with lower overhead could be interpreted as increased scale

economies. One of die earhest investigations into the effect of technology on the scale

economies of banking was conducted by Daniel, Longbrake, and Murphy (1973). They

looked at differences in scale economies brought about by adoption of computer technology

to service demand deposits. Thek proposed model was rather simple. They assumed the

following Cobb-Douglas production function:

C = p,X,^^X^'e" (2.1)

where X,=Number of demand deposit accounts

22

X^=Wage rate

u=Disturbance term.

To estimate die function, Daniel et al. took die log of bodi sides and ran a Hnear

regression. However, in order to be able to test whether die production fiinction was

different for banks using computers to service thek demand deposits they ran one regression

to estimate three cost functions, one for conventional servicing, one for banks who had

adopted computer servicing widiin a year, and another for those banks that had had thek

computer servicing for more than a year. They segmented thek predictor variable matrix to

include all of those models so they could conduct F-tests to show that the production

function was positively impacted by the adoption of computers. They found that larger

banks demonstrated greater scale efficiencies than smaUer firms.

The data used by Daniel et al. were coUected from a study conducted by the Federal

Reserve. A cross-section of 967 banks was surveyed in 1967. Banks voluntarily submitted

data on when they adopted a computer system and the cost of running it.

Hunter and Tknme (1991) investigated how large banks' economies of scale are

affected by technology. In the context of this paper, technology has an economic

interpretation (not necessarily involving just computer technology). They modeled total

bank costs as a function of outputs, input prices and time (the latter variable proxied as a

technology index). Thek model used a truncated thkd-order translog approximation of thek

hypothesized cost function. Outputs were total loans and produced deposits (measured by

doUar volume). Input prices included labor, capital and interest price of funds. Time was

indexed 0 through 6 for the seven years of the study.

23

Hunter and Timme used data primarily from the year-end caU reports for 1980-86.

They only consider the 400 largest banks, and farther restrict thek sample to banks in states

that aUow branching, as were money center banks. Thek final sample included 219 banks,

which they subdivided kito smaUer (110) and larger banks (109).

They found that technology had increased the efficient bank size by shifting the cost

curve downward and outward. And Hke Daniel et al., they found that larger banks had

benefited more from technological change than smaUer banks. The shift in the cost function

had changed the optimal mix among smaUer institutions.

Another paper germane to the topic of improved cost structure is Hancock,

Humphrey, and Wilcox (1999) who investigated the economies of scale experienced by

consoHdation of Fedwke electronic fimds transfer operations. Previous research had shown

Httie evidence of scale economies, attributing most cost savings to technical advances.

But this investigation used a longer time period, discounted transition costs, and

used indexed input prices. Using a translog function to estimate the production function,

they concluded that there were significant economies of scale realized in the consoHdation,

but fakly Htde teclinical improvement. The biggest reason for the difference in conclusion

was probably the time interval. The shorter time interval was still picking up cost noise due

to the transition.

Domowitz (2001) investigated the relationship between technology implementation

and its effect on trading costs and intermediation in the securities trading hidustry. Using

regression analysis, he found evidence of cost reduction.

In short, the economies of scale Hterature tends to agree that technology improves

the cost structure for banks and other financial services providers and tends to favor larger

24

banks. The larger the bank, the more savings are possible once some of the more routine

tasks are automated. In die context of Internet banking, the adoption of technology has

always reduced bank cost structures. Therefore, it is consistent with evidence from earher

technology adoption that die cost stmcture would improve by adoption of Internet banking.

Much of the recent work in bank cost determinants biulds on the foundation of

production functions developed above. But in addition to estimating the production

function, they examine the dispersion within the production possibihty frontier. If Mols'

(1998) theory of strategic bank channel specialization is correct, banks wUl not adopt

uniformly, creating greater dispersion from the overaU banking efficiency frontier. The

distance from that frontier is a measure of efficiency of individual banks. Taken together,

these efficiency measures can assess the overaU efficiency of the banking industry. The

measure of efficiency depends on which variables are taken into account. The papers

reviewed here are just some of the more recent examples in this genre, and do not represent

an extensive Hst, but these are the most important exploring the role of technology and

confounding variables. The earher papers in this genre agree that there is a large dispersion

in efficiency between banks. In addition, there is an extensive Hst of working papers that

further explore bank efficiency (in some cases thek definitions of efficiency differ gready

from that described here and may not be germane to this topic).

Rogers (1998) examined whether nontraditional activities can explain a portion of

the observed inefficiency. In addition to cost efficiency, he considered revenue and profit

efficiency. Three functions were estimated using translog models. One fiinction was

estimated for cost, another for revenue and yet another for profit using a distribution free

25

approach. The input consisted of panel data on some 2,000 banks over five years. The data

were separated into banks operating in states with limited or statewide branching.

To test whether nontraditional activities affect the efficiency, Rogers separates these

models ushig a restricted-unrestricted model methodology. Then efficiency measures were

calculated for each observation, and mean and standard deviations were estimated. FinaUy,

t-statistics were calculated on the differences between the mean efficiency calculations using

die restricted versus utuestricted models. He found a statisricaUy significant cost efficiency,

and profit efficiency improvement among those with more nontraditional activities. In

short, part of the observed inefficiency is explained by the bank's dependence on non-

traditional activities. Not including these activities in models in earher studies has overstated

the inefficiency in the industry.

WTieelock and Wilson (1999) investigated productivity, efficiency and the role of

technical progress in both productivity and efficiency. They begin by developing a model of

change in efficiency over time. The model is designed to extract the components of the

efficiency change into pure efficiency changes, changes in scale economies and changes in

technology. The underiying concept is that if a bank does nothing over time, it wiU look less

efficient because scale economies, technologies and other forces change the industry

production function over time. If enough banks do nothing while other banks irmovate and

improve thek production technology, the industry wUl look inefficient because a few banks

have become more efficient. This paper attempts to identifjr how much of die kiefficiency

of banks over trnie are due to each of these individual component.

Wheelock and WUson used a data envelopment analysis (DEA) and derived

Mahnquist indices of productivity changes for die components in question. They used data

26

firom die CaU Report for die fkst quarter of each year 1984-93. They made estimates on aU

banks, and just those surviving for the entire time period (with the same quahtative results).

They assumed that the technology used in production was continuous across aU banks.

They conclude that over the time period smdied, banks have experienced large

advances in technology. This improvement is attributed to technological change, which has

moved the production function, coming closer to constant returns to scale. However,

technical efficiency has decHned over time. Wheelock and WUson explain the decline in

technical efficiency as unequal adoption of technology. They argue that a minority of banks

in each size class has been successfuUy implementing technological advancements. One area

of technological innovation cited by these authors is Internet banking. These findings are

consistent with Mols' contention that some banks wiU make a strategic choice not to adopt

Internet banking. If Internet banking is more efficient, then the technical efficiency

deterioration would be explained by the tendency for banks to specialize into Internet

banking institutions versus non-Internet banking institutions.

Furst et al. (2000) are the only researchers who have looked specificaUy at the affect

of adoption of Internet banking to thek cost structure. They test the cost structure of banks

with Internet banking capability versus those without, and find the production function to

be different. But because they do not account for the cost structure before adoption, it is

unclear whether the difference in costs is due to the adoption of Internet banking or

whether Internet bankkig is due to the fact that these banks had lower costs, and could

therefore afford to invest in this new technology.

There are no pubhshed research addressmg price elasticity. Mols (1998) cites one of

his unpubhshed papers to conclude that those customers who use home-banking are "more

27

satisfied with thek bank, have higher intentions of repurchasing, provide more positive

word-of-mouth communication and are less likely to switch to another bank." AU of these

findings suggest higher loyalty, which is counter to Mol's own contention that these

customers are more price-sensitive. A recent article by Schwaiger and Locarek-Junge (1998)

also suggested that electronic banking could be used to retain bank customers.

The research investigating the types of barriers to entry do not have a comparative

empirical echo among finance researchers. It does appear from descriptive data in Furst et

al. (2000) that early adoption of Internet technology has been concentrated among the

largest banks first,^ suggesting that at least originaUy, there may have been a barrier to entry

in this market, probably due in large measure to buUding the necessary security protocols. If

bundling has the same impact on financial assets as described earher by Bakos and

Brynjolfsson (1999), then these larger banks wiU have an advantage, in that they have

developed more financial services offered via the Internet. Mols (1998) would suggest that

smaUer banks might want to focus on branch operations due to thek strategic disadvantage.

In short, there is some sketchy evidence that Internet banking does reduce the cost

structure of banks. Unlike the e-commerce Hterature no researcher has looked at interest

rates offered by banks for onhne products to see if better deals for the customers are

offered. But since the majority of banks offering onhne services are traditional banks, it is

unlikely that the interest rates offered online customers differ from conventional banking

products. This is verj^ different fiom the findmgs of the e-commerce Hterature. It suggests

5 Tliis statement appears to be true also in the U.K. from the findings reported in Jayawardhena and

Foley (2000).

28

diat onhne bank customers are not overly price sensitive, which is what Mol says he found ki

a survey of onhne bank customers.

2.2.2 Motivations for Adopting Remote Banking

The reasons why the styHzed model of electronic commerce does not hold have not

been investigated. In that context, these fiictions are not explained. However one research

topic unique to the finance Hterature is why banks decide to adopt technology, aside from

concerns about lowering costs. This may be a different kind of friction in this market, since

it would affect the overaU technical efficiency of the industry. Mol would suggest that the

decision were made based on whether smaUer banks felt they could compete. Few

researchers have addressed this issue as it relates to Internet banking.

However, Hannan and McDoweU (1984) investigated the economic determinants of

ATM adoption. They found evidence that large banks that were operating in a bank holding

company, and in states where branching was aUowed were more likely to offer ATM

services. Thek conclusions tended to focus on the banks' size and organization. However,

they also controUed for wages and demand deposits, which may reflect something about the

ultimate user of the service. They also found that areas with higher wage rates, and high

levels of demand deposits to total deposits were also more likely to offer ATMs.

Three years later, Hannan and McDoweU (1987) explored the connection between

adoption of ATMs and the previous employment of ATMs by competitors, hypothesizing

that adoption of new technology may foUow a diffusion process. In this study, no economic

data on consumers was used, tiiey only considered individual bank data, finding support for

29

diek hypothesis that there is a relationship between supply structure of the market and bank

adoption of ATMs.

In 1990, Hannan and McDoweU explored the effect of technology adoption on

market structure, as described by concentration. Again the technology adoption tested is

ATM adoption. Although banking firms did use ATM access to attract customers,

concentration did not tend to change drasticaUy because smaU and large banks tended to add

the capabUity at roughly the same time. In short, Hannan and McDoweU contend that

ATMs were used originaUy by large banks to lure away customers fiom other banks. SmaUer

banks then combined into networks to batde these competitive forces to protect thek

current customer base. Although large banks used ATMs to attract customers away from

larger banks, the concentration did not change much, because smaUer banks began offering

the same services.

The reason banks adopted the technology at roughly the same time, regardless of

size may be explained by game theory, which is another approach used to analyze this issue.

Bouckaert and Degryse (1995) studied the phone-banking adoption decision. As in Degryse

(1996), which studied remote banking in general, they apply game theory to bank

management's decision to initiate remote banldng services. These papers model the decision

of adopting remote banking through strategic games, where cost of gaining or maintaining

marketshare is the object.

Matutes and PadUla (1994) used a skmlar approach to explain under what conditions

banks would share an ATM network and when diey would use a stand-alone ATM system.

They pokit out that die customer benefits from a shared network in two-ways. Fkst, a

shared system offers better access to deposits (die network effect) and k forces diek bank to

30

be more competitive in rates offered, because they can not compete on location (the

substitution effect). In investigating the trade-off between the network effect and the

substitution effect, they conclude that only two states wUl obtain a possible equUibrium,

either a subset of banks share thek network (what they caU partial compatibiHty) or aU banks

go it alone (total incompatibihty). In thek model fuU compatibiHty does not ever obtain

unless withdrawal or interchange fees are charged for use of an ATM that is not owned by

your bank. It is not clear whether the model would be observed in the United States. One

reason for partial compatibiHty is that banks in the network can use the network as a weapon

to keep other banks out of thek market.

By contrast, Byers and Lederer (2001) use an operations research approach to

finding the optimal mix of remote banking channels offered by a bank. The configuration

can include branch banking, home PC banking, owned ATMs, ATMs owned by others, or

any combination of these. This paper uses economic modeHng as weU as operations

research to analyze the distribution chaimel configuration from the bank management's

perspective. Marketwide shifts in configuration and avaUabihty of service are modeled and

predicted using sensitivit)' analysis whUe adjusting level of consumer demand for electronic

versus branch access, or the cost structure of electronic banking. They are optimizing profit

to the bank given certain input parameters. One of the more interesting Byers and Lederer's

findings in Hght of the focus of this paper is that changes in consumer behavior and attitudes

have a proformd effect on the distribution strategy. Thek model suggests that pure

electronic banks are only viable when die electronic-preferring segment is nearly twice the

size of the branch-preferring segment. One major drawback to this model is that it treats

31

many issues as static variables. Even the response of the customer to bank offers of Internet

banking is treated as a known, which it clearly is not.

In Mols (2000), the adoption of Danish Internet banking is modeled as dependent

on managers' characteristics. Do managers feel threatened by being replaced? How

comfortable are the managers with computers? Again, survey data were used. He found

that banks where managers did not feel threatened were more likely to adopt this

distribution technology.

The findings of these "marketabUity papers" is that one reason banks choose to

adopt remote banking is to gain customers through offering them a service that thek current

bank does not offer. Another reason for adopting onhne banking is to guard against other

banks stealing your customers. They model why banks adopt new technology, as weU as

why not aU banks adopt the technology. One assumption made in aU of these models is that

the probabihty of consumer adoption is known and constant. But even these have a friction.

Mols showed that this propensity is tempered by how threatened bank managers may feel.

In short, the frictions in the financial services industry appear to be different than

those in general e-commerce. But the participants are also different, since they are usuaUy

conventional financial services firms offering thek cHents one more distribution channel.

One of the biggest "frictions" in this context is why they chose to offer Internet banking at

aU. These films tend to offer Internet banking services because they seek a competitive

advantage, seek to guard agakist incursions on thek customer base, because that mix

maximizes profits, or because managers are in favor of it.

32

2.3 Professional Literature

Much of the professional press has echoed in large measure the findings of the

academic press. Bank Marketing (2001") claims, "purely onhne banks ought to have an

insurmountable advantage over brick-and-mortar institutions." They cite then lower

overhead, higher interest-rates on product offerings, more convenient hours and locations as

these unmatchable advantages. But despite conventional wisdom, a new report from

Meridien Research claims that if consumers can choose between a website with higher

interest-rates on products and a banker with a website and a physical location, the bank with

the physical location wiU win. Only 2% of the increase in onhne banking was captured by

pure online banks, the rest was captured by traditional banks with a web presence.

These findings were recendy reaffirmed by Mearian (2001). Citing a report by

Jupiter Media Metrix, he reports that traffic increased 110.5% fiom July 2000 to July 2001 at

banks with both a physical and cyber branches. Over that same time period traffic at purely

cyber-banks feU 8.1%. Although the onhne only banks seemed to have such tremendous

advantages, for most bank customers, the benefits of a physical location outweigh the

disadvantages in sHghtiy higher interest. The advantages entimerated contain physical access

to money, customer service and perceived longevity. These finding suggest that there are

barriers to entry, and that price sensitivity is not as strong as hypothesized.

But simply starting a transactional cyber-branch does not ensure profits. To profit hi

this market, banks must first "crack tiie code on customer priorities," clahns Slywotzky

(2001). Only then, should a bank digitize. Aldiough he gives European examples of banks

that have successfiiUy implemented an onhne presence, most American financial mstitutions

are on thek own fittkig financial offerings to customer deskes. Key Corp., for kistance.

33

seems to dimk diat most potential cHents do not know how convenient onhne bankkig is.

According to a Bank Marketing (2001'') article, tiie bank is maUmg 118,000 bags of popcorn

to customers widi checkkig accounts and an ATM or debit card, teUkig diem diat ki die time

k takes to pop die com in die bag, tiiey could have estabhshed an onhne account.

For most banks, the strategy to increase onhne banldng is to kicrease consumers'

utiHty with the service. One of die biggest bankkig catch-phrases auned at knproving utiHty

is account aggregation. As described in the academic section of this chapter, aggregation

refers to bringing many related information products together. In banking, it is bringing

together many different financial services. Since the beginning of the onhne banking

movement, banks have seen this as a way of increasing the value to the customer. For banks

that had an in-house investment and/or insurance department, aggregation meant simply

cross-selHng. To those institutions without in-house resources, they would simply bring

together partners to a cyber maU, usuaUy run by a thkd-party vendor. Moss (2001) saw these

a^regator sites as die wave of the future. She predicts that in the future customers wUl be

able to transfer funds, purchase financial products, and obtain financial planning advice.

However, Bruno (2001) clakned that the current aggregation solutions are too

primitive to Hve up to thek expectations. In addition, the pay-off to the financial institutions

is unclear as far as thek abUity to cross-seU products from one financial product to another.

The primary objective of aggregation is to retain current customers and cross-seU products,

and it is nearly impossible to demonstrate how weU it has accompHshed this objective. In

fact, Bruno suggested that current trends ki the industry will make thkd-party aggregators

more responsible for demonstrating the value they are adding, which he thinks is not what

34

tiiey are charging. Over the long mn, he expects any aggregating to be done by a lead

financial institution, cutting out the thkd party vendor.

This reahty check is not restiicted to aggregators. The entire onhne banking service

is beginning to be evaluated as to whether it is worth the current investment Unfortimately,

not everyone is in agreement on the answer. Orr (2001) says that over five years, if a

"typical" bank has 50,000 onhne customers, offering a "fuU plate" of e-banldng services, they

should be able to realize a net present value of $5 per customer, or an IRR of 60%. Of

course, that rosy figure is contradicted by Matthew Lawler, an e-bankuig consultant

interviewed by Kingson (2001), who claims that a bank must achieve an adoption rate of at

least 10-15% of thek customer base before thek onhne banking services are profitable.

Benaroch and Kaufmaim (2000) beheve that the analysis used by both of these "experts" is

inappropriate. They show how an option framework and the Black-Scholes model could be

used to analyze the bank's electronic banking decision.

But aU of these analysts focus the institution's attention on the benefits of the

technology to the bank. Which is why when security risk is discussed, the institution

typicaUy thinks about what the ramifications of these risks are to themselves and thek

shareholders. Many articles discuss security issues, but rarely is the effect on the customer

mentioned other than ki passing. For kistance, even though Schacklett (2000) says, "[Credit

union] members need to know they're protected." But she starts out by saying that half of

Internet shoppers are concerned about security, and half of Americans not yet on Internet

are also concerned with security. With that kind of an introduction, it soimds Hke concern

about security does not affect adoption of Internet banking. The rest of die article does not

refer to die needs of customers at aU.

35

However, Rob Lee, Executive Vice President of ALLTEL RLS, in a speech to die

Mortgage Bankers Association of America (2001) showed die real power of perceived risk of

the Internet. After explainkig that mortgage appHcations can currentiy be made online, with

many of die fields of die appHcation being "pre-populated" widi mformation from the

kistitution's files or the customer's credit report, making the form much easier to complete,

he explained diat few customers are using it. Citing a recent Fannie Mae survey, he says that

56% of recent home buyers used the Internet to get mortgage information, 4% of recent

purchasers apphed onhne, and only 2% completed the entire mortgage onhne. He

continued, "Why are so many people holding back? WeU, Fannie Mae foimd that answer,

too. They're afraid ... afraid to give out so much personal information online. ... Thek

fears are focused on die Internet itself Sixty percent of the people surveyed said the

Internet is not a secure place to conduct personal finances."

And if that source is not enough, even potential customers are Hsting security as a

major issue in deciding whether to go ordine. In a recent Association Management (2001)

article questioning whether electronic banking was right "for you," the three factors most

important to making that decision were Hsted as first - security, second — cost, and thkd -

overaU fit. Note that security, risk of losing resources or information, was Hsted as the first

factor.

In short, the professional press has also assumed that online bankkig would reduce

thek costs, improve thek profit margins and kitensify competition. The realization has been

different from the perceived model. Ahnost aU practitioners have assumed the key to

Internet adoption was improving the benefit to the customer. But there seems to be some

36

evidence tiiat one of die biggest drawbacks firom die consumer's standpoint is die perceived

risk of exchanging personal financial kiformation over die Internet.

2.4 Summary of Literature

The Internet was originaUy seen as creating a world much closer to the fiictionless

world hypodiesized m Utopian economic models. It was seen as a medium tiiat could reduce

information asymmetries among customers durough search engkies and "shop-bots." And

since the information set would be closer to uniform among shoppers, it was assumed that

the Internet would enhance price competition, sknpHfy the price discovery process and that

price elasticity would kicrease. In the case of financial services largely the same expectations

were made.

Empirical evidence shows that although e-taUer costs in this medium are lower, and

economic pressure forces thek prices lower, frictions stiU remain. AU bundles offered by

compaiues and received by consumers are not homogeneous. Each retaUer offers different

levels of service and information along with products. These services include ease of use of

the interface, customer support after the sale, abihty to talk to representatives in person

should things go wrong, and trust engendered in the business and product being offered,

which may explain the observed preference of traditional banks offering Internet banking

over purely onHne banks.

In short, although Internet commerce does reduce some frictions experienced in the

conventional economy, it does not eliminate them, and may have created some of its own.

Businesses are beginning to use those "fiictions" to differentiate thek products and erect

competitive barriers to entry in this developing market for goods and services.

37

Aldiough tills Hterature explains some tilings about the Internet marketplace, nearly

aU of the Internet research considered only those firms that conducted aU of thek buskiess

electronicaUy. The demand for banking services is a different question in most cases.

Traditional banks are offering conventional financial services via an Internet channel. Thek

customers can either choose to kiteract with the bank in person or via the Internet. This

paper explores what factors affect the decision to adopt the Internet chaimel. It adds to the