performance-based long term incentive compensation and firm performance · ·...

TRANSCRIPT

Performance-Based Long Term Incentive Compensation

and Firm Performance∗

A Brief Prepared by the Institute for Compensation Studies

ILR School, Cornell University

Hassan Enayati, Kevin Hallock, and Linda Barrington

August 18, 2016

∗Funding for this study was provided by executive compensation consulting firm, Pearl Meyer, jointly

agreeing with the Institute for Compensation Studies (ICS) authors on the research question of interest.

This study builds upon our earlier work examining TSR, Executive Compensation, and Firm Performance.

Pearl Meyer obtained the underlying data from Equilar, Inc., a leading independent provider of executive

and board compensation data and analysis. Pearl Meyer provided these data to ICS for analysis, including

additional data on companies from Capital IQ, and “compensation plan existence and weight” variables that

they constructed. Pearl Meyer provided valuable insight on how executive compensation is structured in

the corporate landscape, which helped ICS ensure its models were valid in terms of real-world practice and

terminology. Independently, ICS conducted the statistical analyses herein. The views, opinions, findings

and conclusions or recommendations expressed in this paper are strictly those of the author(s). They do not

necessarily reflect the views of the ILR School at Cornell University.

For the complete set of analyses, please email Hassan Enayati at [email protected]. The authors wish to

thank Stephanie Thomas and the consultants at Pearl Meyer for their helpful comments.

1

1 Executive Summary

Awarding executives long-term incentive pay based on firm performance is often described

as a natural way to improve firm performance. This brief uses an analytical approach to

examine that proposed relationship. We first document the prevalence of performance-based

long-term incentive (PB LTI) measures and the trends in the relative size of these measures

compared to aggregate measures of compensation. We then compare the characteristics and

performance of firms that have implemented a PB LTI measure in the past to those that

have not. In order to understand the impact of PB LTI awards on firm performance, we

separately assess the roles of the existence of the PB LTI measures, the relative size of the

measures, and the type of PB LTI measure on firm performance.

Key Findings:

* In 2013, 88 percent of the 2014 S&P 500 firms offered PB LTI plans to one of their top

five named executive officers (NEO) - nearly a 40 percent increase from the level of 64

percent in 2006.

* There has been an increase in the weight of PB LTI awards relative to both all long-

term incentive pay and total direct compensation over the past eight years among NEOs.

Conditional upon having a PB LTI award, the average award has risen from 51 percent

of all LTI in 2006 to 56 percent in 2013.

* The increasing share of LTI that is performance-based is meaningful as LTI’s share of

TDC has jumped from 56 percent to 62 percent between 2006 and 2013.

* The inclusion of PB LTI plans is observed across all sectors, with particularly large uptake

in the Information Technology and Consumer Discretionary sectors.

* There are differences in the firms that include PB LTI awards in the compensation plans

of their executives compared to those that do not include PB LTI awards. Firms with PB

2

LTI awards tend to experience lower returns (as measured by 10 year compound annual

growth rates (CAGR) of Net Income, EBIT, EPS, ROA, and Free Cash Flow).

* Our models indicate a pattern of within-year increases of PB LTI on firm performance

followed by losses in subsequent years.

→ Contemporaneous estimates of the impact of a PB LTI plan on performance are positive

for one and three year TSR; however, we find a pattern of negative estimates for the

one and two year lags.

→ Results of the role of the relative weight of PB LTI plans on firm performance follow

a similar pattern of positive within year estimates followed by negative estimates in

lagged years when examining 1 year TSR and EPS growth. There is evidence of a

mostly positive impact on ROE and ROIC when increasing the weight of the plans.

* Comparing findings by level of analysis, i.e., top five NEOs, CEOs, and top five NEOs

excluding CEOs, across all subanalyses showed similar estimates and patterns.

3

2 Data

The firms studied in this brief were identified using the 2014 S&P 500 index. A rich longi-

tudinal dataset was constructed using compensation data and firm financial data covering

fiscal years 2006 through 2013.1 The information regarding compensation was derived from

Equilar’s executive compensation data. These data contain detailed records of the com-

pensation types and amounts for named executive officers from firms in our sample. For

example, we observe base salary, bonus payouts, stock awards, option awards, and several

types of incentive plan awards. Measures of firm performance include 1, 3 and 5-year TSR

as well as annual measures of return on equity (ROE), earning per share (EPS) growth, total

revenue growth, and return on invested capital (ROIC). Firm performance measures came

from Capital IQ.2

3 Methodology

To examine how the inclusion of PB LTI plans impacts firm performance, we used both

descriptive analysis and also regression analysis. The descriptive analysis compared the raw

patterns among groups of firms with and without PB LTI plans over time. The resulting

tables and figures are valuable in understanding the unconditional relationship between PB

LTI plans and firm performance. All analyses were conducted on three subsamples of ex-

ecutives: top five proxy-listed NEOs, CEOs only, and top five proxy-listed NEOs excluding

CEOs.

Regression analysis is used to as a way to control for other factors that might obscure

the role of PB LTI measures on firm performance. Our baseline model uses the following

1The analytical sample excluded firms due to extreme values: loses of 195 observations. Additionally,1,396 firm-year observations were removed from the sample when key data elements were missing. The finalbaseline sample consisted of 2,249 firm-year observations, which were associated with 367 firms.

2We would like to thank Pearl Meyer for providing us with the data used in this brief and also for con-structing the key measures of performance-based compensation, long-term incentive pay, total compensation,and others.

4

Ordinary Least Squares regression framework:

Yit = β1 + Zitβ2 + Sitβ3 + Ctβ4 + β5Xit + β6Xi,t−1 + β7Xi,t−2 + εit (1)

Yit represents a given performance measure for firm i in fiscal year t. The set of firm

performance measures studied in this brief are 1-year TSR, 3-year TSR, 5-year TSR, ROE,

EPS growth, total revenue growth, and ROIC. Zit is a set of control variables including

functions of market capitalization and an indicator for change in CEO. Our model also

accounts for sector performance and year fixed effects with Sit and Ct, respectively. The key

variables in this project are the PB LTI measures represented by Xit, which is an indicator

variable equal to one when a firm has any executive in the respective sample, i.e., top five

NEOs, CEOs, or top five NEOs excluding CEOs, with a PB LTI plan during the current

fiscal year. To analyze the role of weight on performance, Xit is set to the firm-level average,

given the respective sample, of the ratio of PB LTI award to either LTI or TDC. Our baseline

model includes two lags of Xit to account for a delay between PB LTI plan implementation

and impact on firm performance. Finally, the remaining error in the model is captured by

εit, which is clustered at the firm level.

Multiple extensions of the baseline model were investigated to assess the sensitivity of

our findings. One extension replaced the sector fixed effects with firm effects, which allows

the model to control for unobserved firm-specific and fixed attributes. We also considered

the impact of partitioning the sample across firm size and PB LTI plan history. Additional

sensitivity checks include removing the Financial sector from the analysis and running models

with a richer set of lag measures.

4 Findings

One of the most striking features of PB LTI plans among Fortune 500 firms is how common

they have become. Table 1 shows that the share of firms offering their NEOs PB LTI plans

5

has increased from 64 percent of firms in 2006 to 88 percent of firms in 2013. Put another

way, only one in ten Fortune 500 firms does not offer a PB LTI award to their NEOs. This

high level of prevalence is not driven by PB LTI awards only being offered to CEOs as

evidenced by the comparable prevalence levels among CEOs and top five NEOs excluding

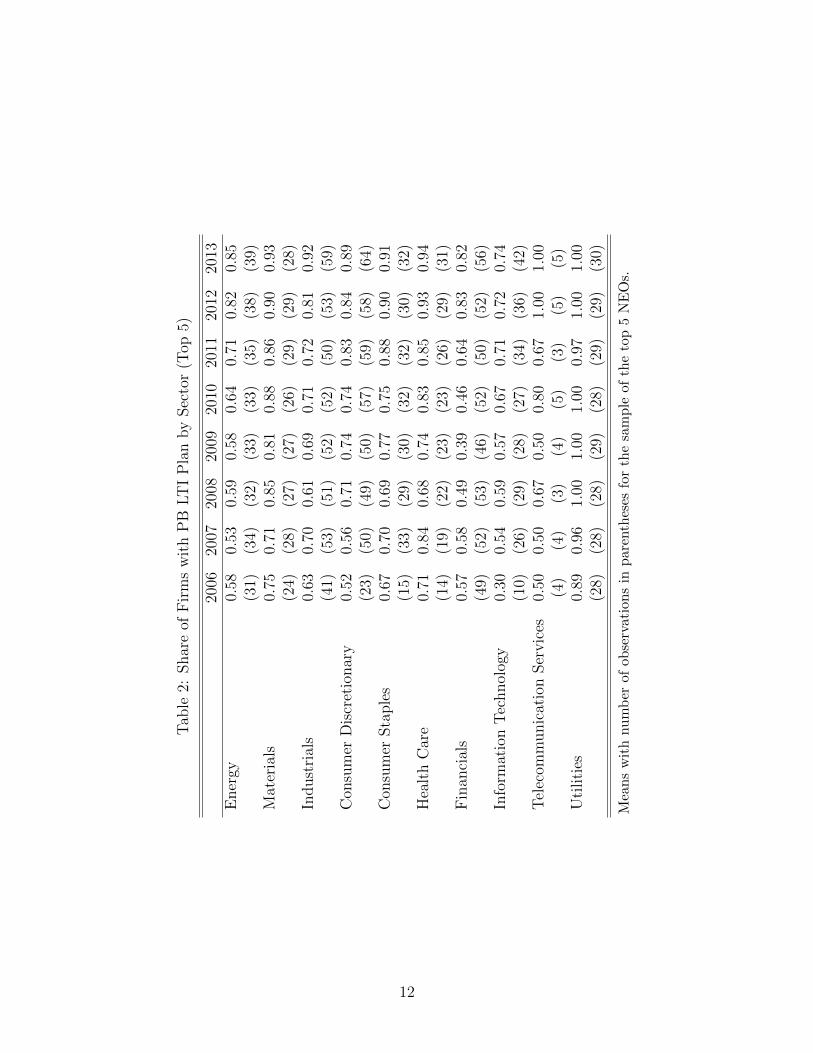

CEOs. Table 2 shows that firms in all sectors have increasingly included PB LTI plans in

the compensation of their executives.

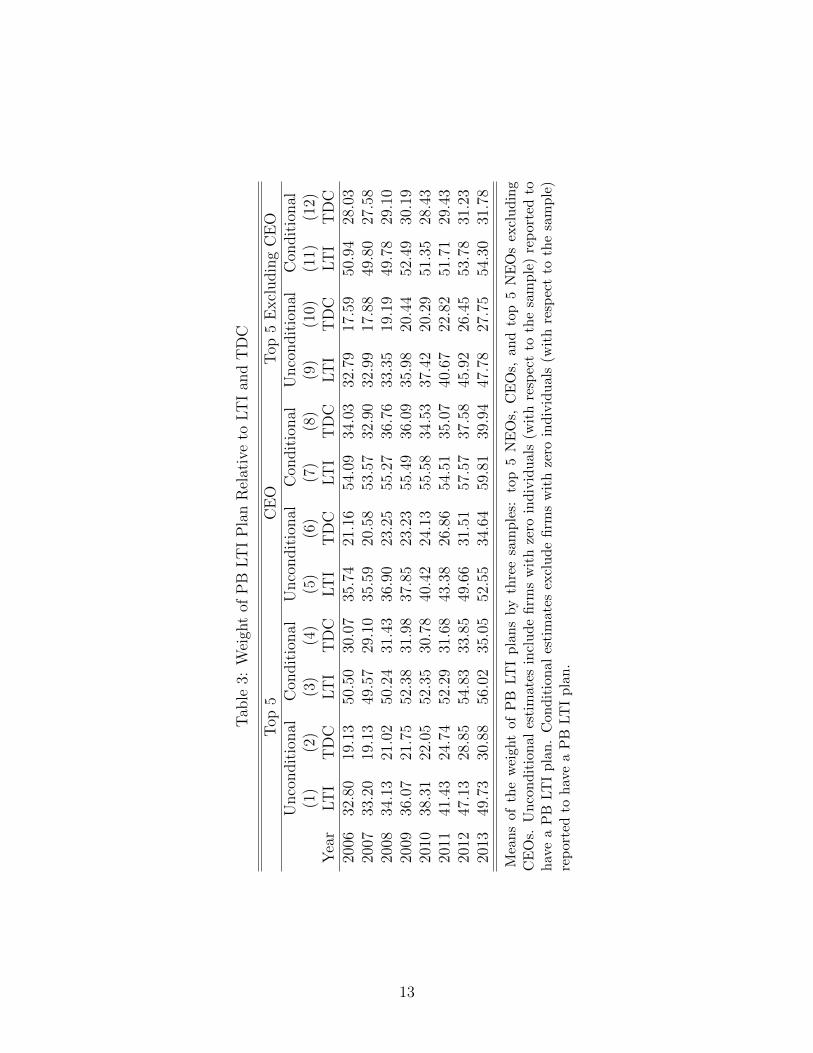

With an understanding of the pervasiveness of PB LTI awards, we next assessed the

relative size of the PB LTI awards. Table 3 examines how the weight of PB LTI relative

to LTI and TDC has changed over time. The average weight of PB LTI plans has been

increasing over time among all firms (the unconditional columns); though the fast growth

rate is influenced by the rapid increase in the prevalence of these awards. For the firms that

actually offer PB LTI plans (conditional columns), the weight of the plans has increased

more modestly over the sample time period, e.g., NEO PB LTI weight grew from 51 percent

of LTI to 56 percent. Given the growth of LTI during this same time period, the share of

total compensation coming from PB LTI increased from 28 percent to 35 percent.3

In an effort to understand the prevalence and impact of specific components of PB LTI

awards, we worked with the executive compensation consulting firm Pearl Meyer to categorize

the thirty-one individual incentive pay metrics reported within the Equilar data into six

strategically-aligned groups. The groups and individual metrics are reported in Table 4:

Cash Flow, Growth, Market-Based, Profitability, Returns, and Other.

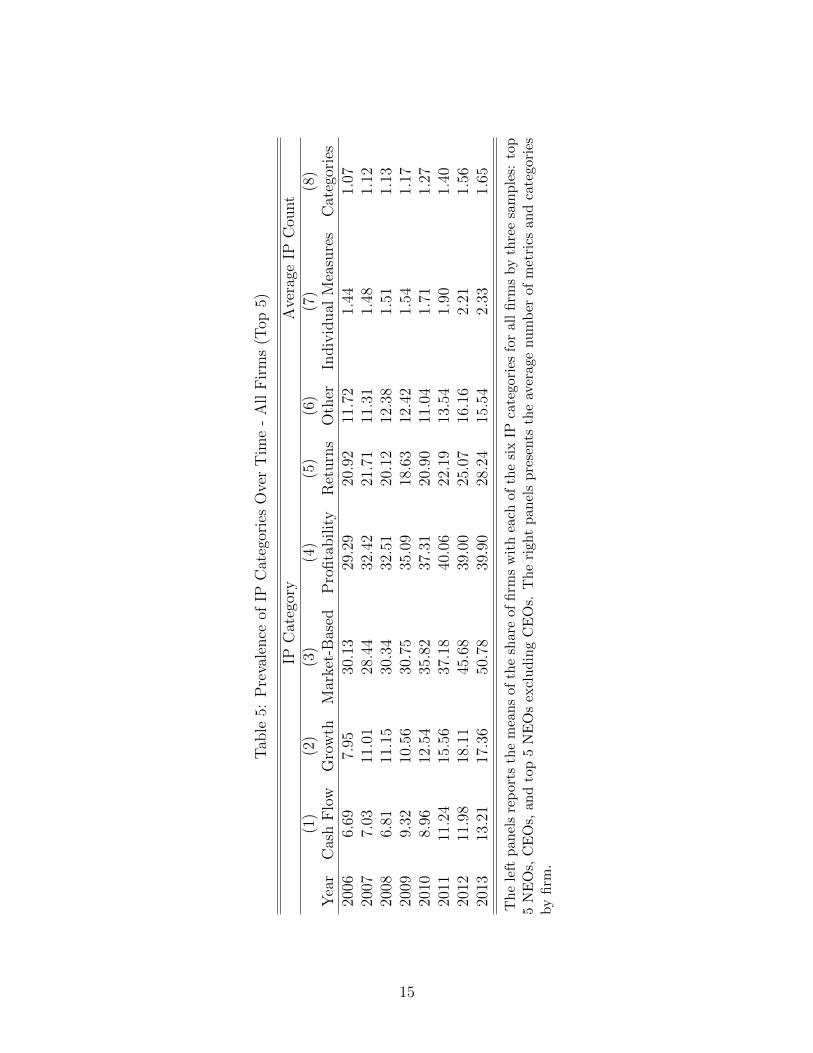

The trends in the prevalence of the IP categories among all firms are described in Table

5. We find that each of the six categories became more common over time. For example,

30 percent of firms offered Market-Based metrics to their NEOs in 2006 while 51 percent

offered Market-Based metrics in 2013. Table 6 reports the same prevalency rates but only

considers firms that offer at least one of their top five NEOs a PB LTI award. Conditioning

on PB LTI award changes the patterns observed in Table 5. Here we find that only Cash

3The share of total direct compensation attributed to LTI increased from 56 percent in 2006 to 62 percentin 2013.

6

Flow, Growth, and Market-Based metrics are becoming more common with the other three

groups becoming slightly less prevalent. Columns 7 and 8 report the number of individual

metrics and categories, respectively, in the NEOs plans. The average number of individual

measures among NEOs with a PB LTI award has increased by 17 percent from 2.36 to 2.75

metrics. At the same time, the number of unique categories only increased by 11 percent

(1.75 to 1.94). The slower growth rate of categories and higher value in individual measures

describe a situation where firms are offering NEOs multiple metrics from within the same

incentive pay category.

We next compared the performance of firms based on their prior history of offering PB

LTI awards to their NEOs. Table 7 shows the results of an analysis that separated firms

into one of three groups: those that always offered a PB LTI awards to their NEOs, those

that never offered the awards, and those that changed between offering and not. Results

indicate the firms that change or always had a PB LTI award have lower returns in terms

of Net Income, EBIT, EPS, and ROA. While Table 7 provides evidence of differences in

performance being related to a firm’s history offering PB LTI awards, these estimates may

be influenced by other factors associated to the firm.

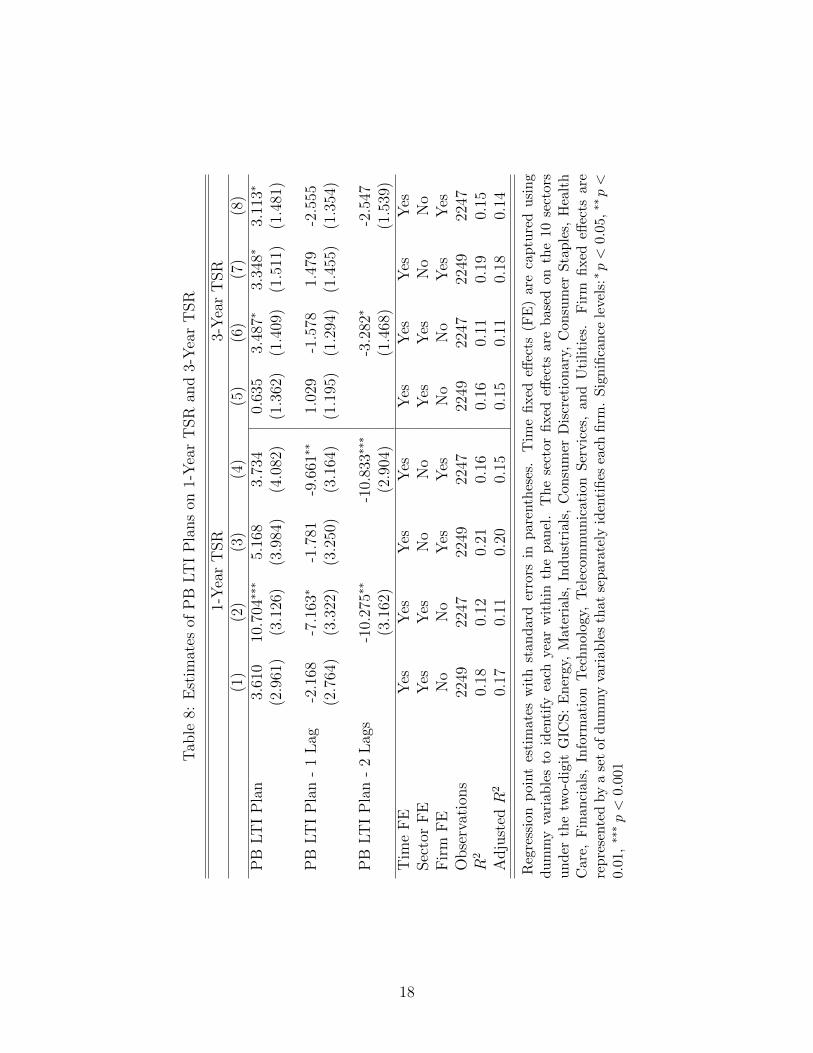

A series of regression analyses were implemented in an attempt to isolate the role of

PB LTI awards on firm performance. Tables 8 through 11 report the estimates from our

baseline model, described in Equation 1, of the relationship between the inclusion of PB

LTI awards and performance. The tables reveal a pattern of positive within year increases

followed by negative estimates in lagged years. For example, column 2 of Table 8 indicates

that including a PB LTI plan in the current year predicts a 10.7 percentage point jump in

1-year TSR. At the same time, we also find that having a PB LTI plan last year (two years

ago) predicts a 7.2 (10.3) percentage point decline in 1-year TSR. Looking at our preferred

specifications in the four columns reported for each dependent variable, we find evidence

of positive contemporaneous estimates on 1-year TSR, 3-year TSR, and ROE but negative

lagged estimates for 1-year TSR, 3-year TSR, and 5-year TSR.

7

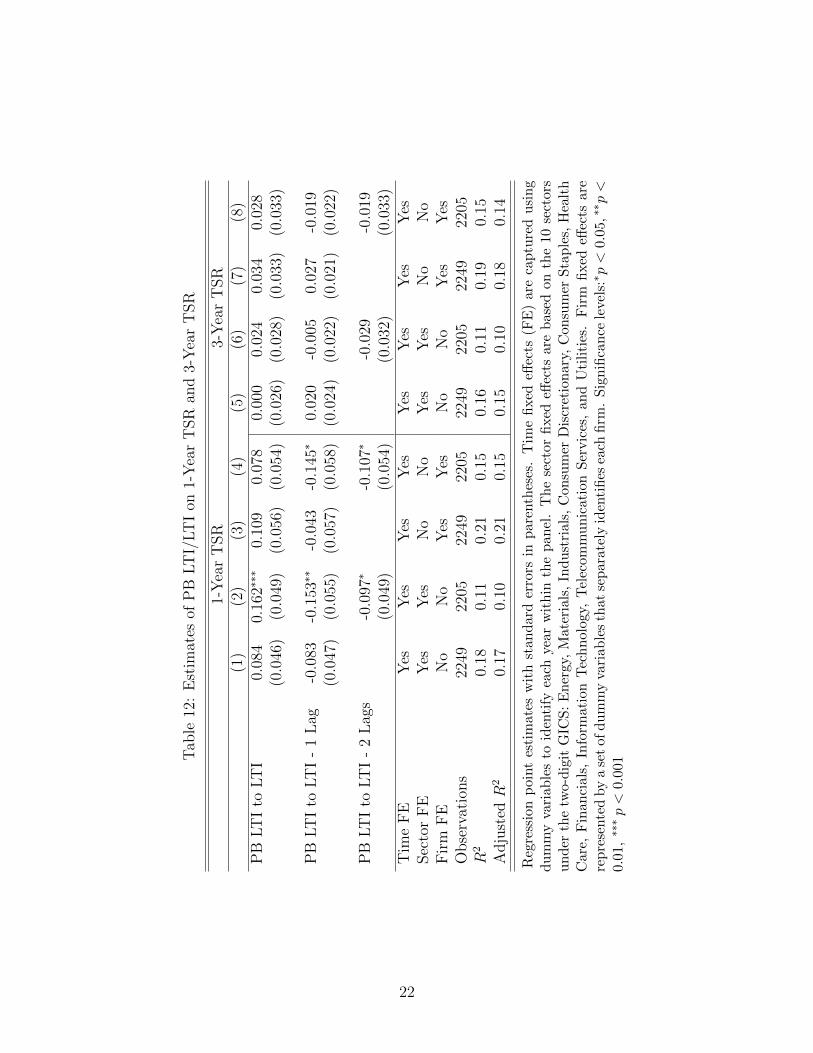

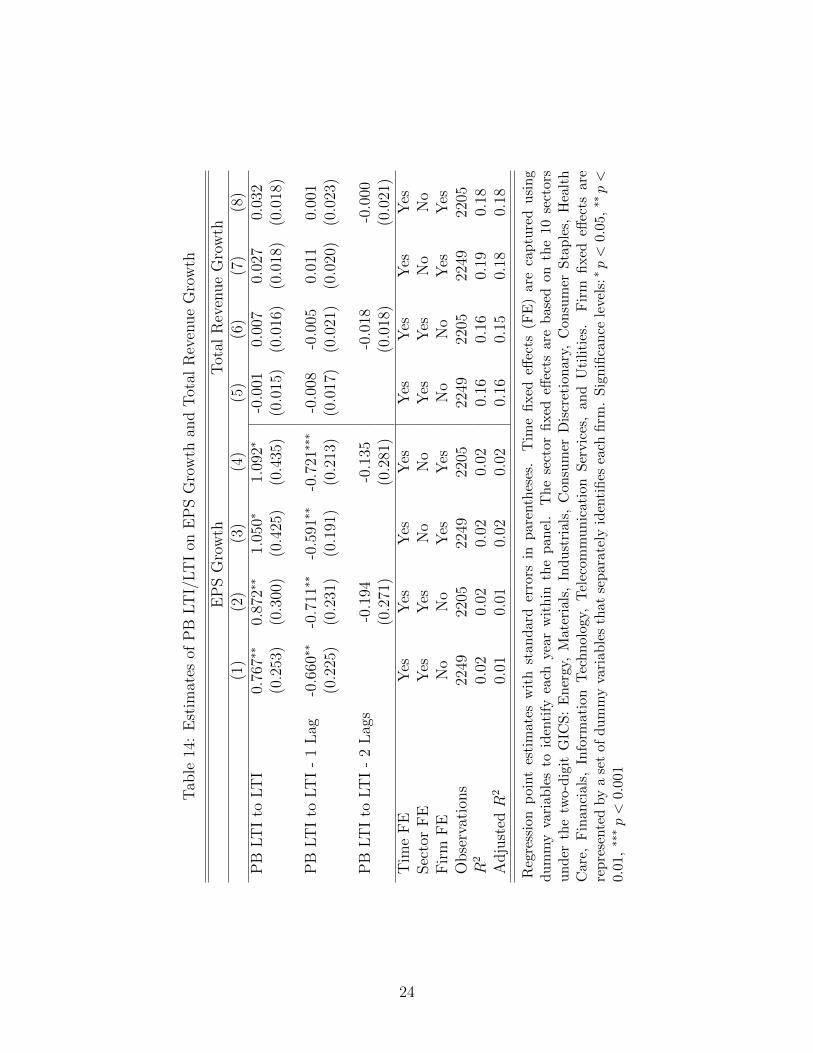

Estimates of the relative size of PB LTI to LTI on firm performance, reported in Tables

12 through 15, continue to present evidence of a short-term bump followed by a decline in

firm performance. Notably, a different set of firm performance measures are impacted by

changes in the weight compared to the introduction or removal of a PB LTI plan. Here we

find that the weight of PB LTI to LTI most directly predicts ROE, EPS Growth, and ROIC.

In fact, increasing the weight of PB LTI plans predicts only a positive increase in ROE and

ROIC with no subsequent decline, i.e., increasing the share of LTI that is performance based

by 1 percentage point is associated with between a 0.020 and 0.026 percentage point increase

in ROIC.

In addition to the baseline analysis, we performed a series of sensitivity checks, examining

the relative impact of market capitalization, financial sector, PB LTI offering pattern, and

richer five year lag structure. The positive relationship between contemporaneous PB LTI

plans is only present in Fortune 500 firms with lower market capitalization. Excluding firms

from the Financial sector weakens the evidence of the positive contemporaneous relationships

with PB LTI plans. Neither restricting the analysis to only those firms with changing PB

LTI policy nor extending the model to include five lags change the baseline findings other

than attenuating the results. Additionally, we explored the relationship between specific

incentive pay categories on firm performance but found most estimates to be insignificant.

Thus, these findings do not point to a particular category as driving the broader PB LTI

impact found earlier.

5 Discussion and Future Direction

Currently, almost ninety percent of the 2014 S&P 500 firms offer PB LTI plans to their named

executive officers - a forty percent increase between 2006 and 2013. The relative value of

these PB LTI plans has also increased over time, even among those firms that offer the plans,

with PB LTI awards now representing just over one third of the total direct compensation

8

for NEOs. Breaking all PB LTI into six major categories reveals that half of those categories

have growth while the other half remain stable or have slightly decreased.

Differences are observable in the firms that include PB LTI awards into the compensation

plans of their NEOs compared to those that do not. Firms with PB LTI plans experience

poorer performance in key areas. That said, the decision to use PB LTI awards may actually

have been a response by the board to improve poor performance among those firms with

any PB LTI history. In a similar vein, firms that have been performing well may not feel

the need to change their compensation structure. Thus, the usage of PB LTI awards may

be endogenous to observed firm performance, so care should be used when drawing causal

implications from descriptive statistics.

Our baseline models examined the impact of the inclusion and size of PB LTI awards on

firm performance. Evidence suggests that the inclusion of these plans results in short-term

increases in performance followed by later declines. Alternatively, increasing the weight

of the plans has a more positive impact overall, though there was still some evidence of

later losses. While these models provide a clearer understanding of the impact of PB LTI

awards on firm performance than the purely descriptive analyses, they still only describe the

statistical relationship and are not causal.

This work builds upon our prior work exploring the role of TSR awards on firm per-

formance. In this project, we aimed to understand how the role of the broader category

of PB LTI is related to firm performance and which subcomponents may be driving that

relationship. Future steps may include examining the role of compensation complexity on

the relationship between incentive pay and firm performance.

9

6 Appendix

This appendix provides variable definitions for key measures used in this study.

• TSR outcome measures, where the closing price is adjusted for dividends

– 1-Year TSR: (Fiscal year end stock price/previous fiscal year end stock price)-1

– 3-Year TSR: {(Fiscal year end stock price/three fiscal year priors end stock

price)(̂1/3)}-1

– 5-Year TSR: {(Fiscal year end stock price/five fiscal year priors end stock price)(̂1/5)}-

1

• TDC measure

– TDC = Long-Term Incentives + Base Salary + Short-Term Portion of NEIP

Compensation + Bonus

• LTI measure

– LTI = Grant Date Present Value of Securities + Grant Date Present Value of

Option (FAS 123(R)) + Grant Date Present Value of Target Award

10

7 Tables

Table 1: Percent of Firms with PB LTIPlans

Top 5 CEO Top 5Excluding CEO

2006 63.60 62.18 62.762007 65.75 62.35 64.832008 66.87 63.04 65.942009 68.01 64.38 67.702010 71.64 69.88 71.342011 78.10 76.59 77.522012 85.24 83.84 84.682013 88.08 86.49 87.31

Means of the share of firms with PB LTIplans by three samples: top 5 NEOs, CEOs,and top 5 NEOs excluding CEOs.

11

Tab

le2:

Shar

eof

Fir

ms

wit

hP

BLT

IP

lan

by

Sec

tor

(Top

5)

2006

2007

2008

2009

2010

2011

2012

2013

Ener

gy0.

580.

530.

590.

580.

640.

710.

820.

85(3

1)(3

4)(3

2)(3

3)(3

3)(3

5)(3

8)(3

9)M

ater

ials

0.75

0.71

0.85

0.81

0.88

0.86

0.90

0.93

(24)

(28)

(27)

(27)

(26)

(29)

(29)

(28)

Indust

rial

s0.

630.

700.

610.

690.

710.

720.

810.

92(4

1)(5

3)(5

1)(5

2)(5

2)(5

0)(5

3)(5

9)C

onsu

mer

Dis

cret

ionar

y0.

520.

560.

710.

740.

740.

830.

840.

89(2

3)(5

0)(4

9)(5

0)(5

7)(5

9)(5

8)(6

4)C

onsu

mer

Sta

ple

s0.

670.

700.

690.

770.

750.

880.

900.

91(1

5)(3

3)(2

9)(3

0)(3

2)(3

2)(3

0)(3

2)H

ealt

hC

are

0.71

0.84

0.68

0.74

0.83

0.85

0.93

0.94

(14)

(19)

(22)

(23)

(23)

(26)

(29)

(31)

Fin

anci

als

0.57

0.58

0.49

0.39

0.46

0.64

0.83

0.82

(49)

(52)

(53)

(46)

(52)

(50)

(52)

(56)

Info

rmat

ion

Tec

hnol

ogy

0.30

0.54

0.59

0.57

0.67

0.71

0.72

0.74

(10)

(26)

(29)

(28)

(27)

(34)

(36)

(42)

Tel

ecom

munic

atio

nSer

vic

es0.

500.

500.

670.

500.

800.

671.

001.

00(4

)(4

)(3

)(4

)(5

)(3

)(5

)(5

)U

tiliti

es0.

890.

961.

001.

001.

000.

971.

001.

00(2

8)(2

8)(2

8)(2

9)(2

8)(2

9)(2

9)(3

0)

Mea

ns

wit

hnu

mb

erof

obse

rvat

ion

sin

par

enth

eses

for

the

sam

ple

ofth

eto

p5

NE

Os.

12

Tab

le3:

Wei

ght

ofP

BLT

IP

lan

Rel

ativ

eto

LT

Ian

dT

DC

Top

5C

EO

Top

5E

xcl

udin

gC

EO

Unco

ndit

ional

Con

dit

ional

Unco

ndit

ional

Con

dit

ional

Unco

ndit

ional

Con

dit

ional

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

(12)

Yea

rLT

IT

DC

LT

IT

DC

LT

IT

DC

LT

IT

DC

LT

IT

DC

LT

IT

DC

2006

32.8

019

.13

50.5

030

.07

35.7

421

.16

54.0

934

.03

32.7

917

.59

50.9

428

.03

2007

33.2

019

.13

49.5

729

.10

35.5

920

.58

53.5

732

.90

32.9

917

.88

49.8

027

.58

2008

34.1

321

.02

50.2

431

.43

36.9

023

.25

55.2

736

.76

33.3

519

.19

49.7

829

.10

2009

36.0

721

.75

52.3

831

.98

37.8

523

.23

55.4

936

.09

35.9

820

.44

52.4

930

.19

2010

38.3

122

.05

52.3

530

.78

40.4

224

.13

55.5

834

.53

37.4

220

.29

51.3

528

.43

2011

41.4

324

.74

52.2

931

.68

43.3

826

.86

54.5

135

.07

40.6

722

.82

51.7

129

.43

2012

47.1

328

.85

54.8

333

.85

49.6

631

.51

57.5

737

.58

45.9

226

.45

53.7

831

.23

2013

49.7

330

.88

56.0

235

.05

52.5

534

.64

59.8

139

.94

47.7

827

.75

54.3

031

.78

Mea

ns

of

the

wei

ght

ofP

BLT

Ip

lan

sby

thre

esa

mp

les:

top

5N

EO

s,C

EO

s,an

dto

p5

NE

Os

excl

udin

gC

EO

s.U

nco

nd

itio

nal

esti

mat

esin

clu

de

firm

sw

ith

zero

ind

ivid

ual

s(w

ith

resp

ect

toth

esa

mp

le)

rep

orte

dto

hav

ea

PB

LT

Ip

lan

.C

ond

itio

nal

esti

mat

esex

clu

de

firm

sw

ith

zero

ind

ivid

ual

s(w

ith

resp

ect

toth

esa

mp

le)

rep

ort

edto

hav

ea

PB

LT

Ip

lan

.

13

7.1 Trends in IP Categories

Table 4: Separating IP Metrics in Strategically-Aligned Cat-egories

IP Award Bin IP Award MetricCash Flow Cash Flow

EBITDAGrowth (Top Line) Market Share

RevenueMarket-Based Absolute TSR

Market CapitalizationRelative TSRStock PriceTotal TSR (Relative and Absolute)

Profitability EPSEPS / Net IncomeGross Profit / MarginNet IncomeOperating Income / MarginROS

Returns EVAROC / ROICROEROA

Other Asset/Asset RatioCost/Cost RatioCustomer SatisfactionDebt Leverage/Debt RatiosDivision PerformanceEnvironmentalIndustry SpecificN/AOther FinancialOther Non-FinancialOther RatiosSafety

The ICS thanks Pearl Meyer for categorizing the individual met-rics into the above six groups.

14

Tab

le5:

Pre

vale

nce

ofIP

Cat

egor

ies

Ove

rT

ime

-A

llF

irm

s(T

op5)

IPC

ateg

ory

Ave

rage

IPC

ount

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Yea

rC

ash

Flo

wG

row

thM

arke

t-B

ased

Pro

fita

bilit

yR

eturn

sO

ther

Indiv

idual

Mea

sure

sC

ateg

orie

s20

066.

697.

9530

.13

29.2

920

.92

11.7

21.

441.

0720

077.

0311

.01

28.4

432

.42

21.7

111

.31

1.48

1.12

2008

6.81

11.1

530

.34

32.5

120

.12

12.3

81.

511.

1320

099.

3210

.56

30.7

535

.09

18.6

312

.42

1.54

1.17

2010

8.96

12.5

435

.82

37.3

120

.90

11.0

41.

711.

2720

1111

.24

15.5

637

.18

40.0

622

.19

13.5

41.

901.

4020

1211

.98

18.1

145

.68

39.0

025

.07

16.1

62.

211.

5620

1313

.21

17.3

650

.78

39.9

028

.24

15.5

42.

331.

65

Th

ele

ftp

anel

sre

por

tsth

em

ean

sof

the

shar

eof

firm

sw

ith

each

ofth

esi

xIP

cate

gori

esfo

ral

lfi

rms

by

thre

esa

mp

les:

top

5N

EO

s,C

EO

s,an

dto

p5

NE

Os

excl

ud

ing

CE

Os.

Th

eri

ght

pan

els

pre

sents

the

aver

age

nu

mb

erof

met

rics

and

cate

gori

esby

firm

.

15

Tab

le6:

Pre

vale

nce

ofIP

Cat

egor

ies

Ove

rT

ime

-F

irm

sW

ith

PB

LT

I(T

op5)

IPC

ateg

ory

Ave

rage

IPC

ount

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

Yea

rC

ash

Flo

wG

row

thM

arke

t-B

ased

Pro

fita

bilit

yR

eturn

sO

ther

Indiv

idual

Mea

sure

sC

ateg

orie

s20

0610

.96

13.0

149

.32

47.9

534

.25

19.1

82.

361.

7520

0711

.39

17.8

246

.04

52.4

835

.15

18.3

22.

391.

8120

0810

.84

17.7

348

.28

51.7

232

.02

19.7

02.

401.

8020

0914

.08

15.9

646

.48

53.0

528

.17

18.7

82.

331.

7720

1012

.71

17.8

050

.85

52.9

729

.66

15.6

82.

421.

8020

1115

.00

20.7

749

.62

53.4

629

.62

18.0

82.

531.

8720

1214

.83

22.4

156

.55

48.2

831

.03

20.0

02.

731.

9320

1315

.55

20.4

359

.76

46.9

533

.23

18.2

92.

751.

94

Th

ele

ftp

an

els

rep

ort

sth

em

ean

sof

the

shar

eof

firm

sw

ith

each

ofth

esi

xIP

cate

gori

esfo

rfi

rms

offer

ing

PB

LT

Iaw

ard

sby

thre

esa

mp

les:

top

5N

EO

s,C

EO

s,an

dto

p5

NE

Os

excl

ud

ing

CE

Os.

Th

eri

ght

pan

els

pre

sents

the

aver

age

nu

mb

erof

met

rics

an

dca

tego

ries

by

firm

.

16

Table 7: Firm Characteristics by PB LTI Plan Pattern (Top 5)

Always PB LTI Change PB LTI Never PB LTIMarket Cap - Avg 23690.79 25687.94 26379.44

(0.72) (0.94)Total Revenue - Avg 20476.85 17960.63 22355.41

(0.78) (0.55)10 Yr Net Inc CAGR 7.10 7.12 14.64

(0.00) (0.00)10 Yr ROIC CAGR 0.69 0.48 3.76

(0.07) (0.06)10 Yr EBIT CAGR 7.26 6.92 15.62

(0.00) (0.00)10 Yr EPS CAGR 7.00 6.33 13.38

(0.00) (0.00)10 Yr ROA CAGR 0.06 0.06 0.08

(0.01) (0.03)10 Yr ROE CAGR 0.16 0.15 0.26

(0.51) (0.02)10 Yr FCF CAGR 6.65 7.23 13.25

(0.03) (0.02)Observations 210 122 35

Means with p-values in parentheses for the sample of the top five NEOs. Firmsare grouped into three groups based on the sample period: those that always hada PB LTI plan, those that never had a PB LTI plan, and those that changed theirPB LTI plans by either introducing or removing them.

17

Tab

le8:

Est

imat

esof

PB

LT

IP

lans

on1-

Yea

rT

SR

and

3-Y

ear

TSR

1-Y

ear

TSR

3-Y

ear

TSR

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

PB

LT

IP

lan

3.61

010

.704

∗∗∗

5.16

83.

734

0.63

53.

487∗

3.34

8∗3.

113∗

(2.9

61)

(3.1

26)

(3.9

84)

(4.0

82)

(1.3

62)

(1.4

09)

(1.5

11)

(1.4

81)

PB

LT

IP

lan

-1

Lag

-2.1

68-7

.163

∗-1

.781

-9.6

61∗∗

1.02

9-1

.578

1.47

9-2

.555

(2.7

64)

(3.3

22)

(3.2

50)

(3.1

64)

(1.1

95)

(1.2

94)

(1.4

55)

(1.3

54)

PB

LT

IP

lan

-2

Lag

s-1

0.27

5∗∗

-10.

833∗

∗∗-3

.282

∗-2

.547

(3.1

62)

(2.9

04)

(1.4

68)

(1.5

39)

Tim

eF

EY

esY

esY

esY

esY

esY

esY

esY

esSec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

2249

2247

2249

2247

2249

2247

2249

2247

R2

0.18

0.12

0.21

0.16

0.16

0.11

0.19

0.15

Adju

sted

R2

0.17

0.11

0.20

0.15

0.15

0.11

0.18

0.14

Reg

ress

ion

poin

tes

tim

ate

sw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

ab

les

toid

enti

fyea

chye

arw

ith

inth

ep

anel

.T

he

sect

orfi

xed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-d

igit

GIC

S:

En

ergy

,M

ater

ials

,In

du

stri

als,

Con

sum

erD

iscr

etio

nar

y,C

onsu

mer

Sta

ple

s,H

ealt

hC

are

,F

inan

cials

,In

form

atio

nT

ech

nol

ogy,

Tel

ecom

mu

nic

atio

nS

ervic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsar

ere

pre

sente

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.0

5,∗∗p<

0.01,

∗∗∗p<

0.0

01

18

Tab

le9:

Est

imat

esof

PB

LT

IP

lans

on5-

Yea

rT

SR

and

RO

E

5-Y

ear

TSR

RO

E(1

)(2

)(3

)(4

)(5

)(6

)(7

)(8

)P

BLT

IP

lan

-2.2

49∗

-0.5

15-0

.283

-0.4

251.

552

1.80

11.

120

1.16

3(1

.073

)(1

.089

)(1

.084

)(1

.098

)(1

.177

)(1

.171

)(0

.852

)(0

.877

)

PB

LT

IP

lan

-1

Lag

2.11

9∗∗

0.27

72.

103∗

-0.2

781.

088

0.46

40.

581

0.18

8(0

.791

)(0

.830

)(0

.855

)(0

.794

)(0

.862

)(0

.729

)(0

.714

)(0

.661

)

PB

LT

IP

lan

-2

Lag

s-1

.669

-1.4

990.

206

0.16

1(0

.858

)(0

.937

)(0

.928

)(0

.909

)T

ime

FE

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Sec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

2249

2247

2249

2247

2249

2247

2249

2247

R2

0.22

0.18

0.27

0.23

0.13

0.13

0.05

0.05

Adju

sted

R2

0.21

0.17

0.27

0.23

0.12

0.12

0.05

0.04

Reg

ress

ion

poi

nt

esti

mat

esw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

able

sto

iden

tify

each

year

wit

hin

the

pan

el.

Th

ese

ctor

fixed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Ind

ust

rial

s,C

onsu

mer

Dis

cret

ionar

y,C

onsu

mer

Sta

ple

s,H

ealt

hC

are,

Fin

an

cial

s,In

form

atio

nT

ech

nol

ogy,

Tel

ecom

mu

nic

atio

nS

ervic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsare

rep

rese

nte

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.0

5,∗∗

p<

0.0

1,∗∗

∗p<

0.00

1

19

Tab

le10

:E

stim

ates

ofP

BLT

IP

lans

onE

PS

Gro

wth

and

Tot

alR

even

ue

Gro

wth

EP

SG

row

thT

otal

Rev

enue

Gro

wth

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

PB

LT

IP

lan

9.80

719

.286

32.8

9830

.231

-1.8

84-1

.450

0.29

60.

280

(13.

081)

(10.

589)

(21.

099)

(24.

286)

(0.9

60)

(0.9

97)

(1.1

17)

(1.1

22)

PB

LT

IP

lan

-1

Lag

-15.

031

-13.

884

-9.1

42-1

7.24

70.

323

0.41

21.

575

1.08

7(1

3.98

2)(1

4.62

4)(1

7.11

1)(1

6.08

0)(0

.882

)(0

.979

)(1

.059

)(1

.031

)

PB

LT

IP

lan

-2

Lag

s-2

4.67

6-1

7.60

5-1

.165

-0.2

68(2

0.67

6)(2

6.02

4)(0

.987

)(1

.152

)T

ime

FE

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Sec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

2249

2247

2249

2247

2249

2247

2249

2247

R2

0.02

0.02

0.02

0.02

0.17

0.16

0.19

0.19

Adju

sted

R2

0.01

0.01

0.01

0.01

0.16

0.16

0.18

0.18

Reg

ress

ion

poi

nt

esti

mate

sw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

able

sto

iden

tify

each

year

wit

hin

the

pan

el.

Th

ese

ctor

fixed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Ind

ust

rial

s,C

onsu

mer

Dis

cret

ion

ary,

Con

sum

erS

tap

les,

Hea

lth

Car

e,F

inan

cials

,In

form

ati

on

Tec

hn

olog

y,T

elec

omm

un

icat

ion

Ser

vic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsar

ere

pre

sente

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.0

5,∗∗p<

0.01,∗∗

∗p<

0.0

01

20

Tab

le11

:E

stim

ates

ofP

BLT

IP

lans

onR

OIC

RO

IC(1

)(2

)(3

)(4

)P

BLT

IP

lan

0.28

50.

468

0.62

10.

642

(0.8

33)

(0.8

45)

(0.5

28)

(0.5

30)

PB

LT

IP

lan

-1

Lag

-0.0

08-0

.201

-0.1

04-0

.425

(0.5

95)

(0.4

37)

(0.4

11)

(0.3

94)

PB

LT

IP

lan

-2

Lag

s-0

.175

0.02

7(0

.625

)(0

.475

)T

ime

FE

Yes

Yes

Yes

Yes

Sec

tor

FE

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esO

bse

rvat

ions

2249

2247

2249

2247

R2

0.17

0.17

0.08

0.07

Adju

sted

R2

0.16

0.16

0.07

0.07

Reg

ress

ion

poi

nt

esti

mat

esw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gdu

mm

yva

riab

les

toid

enti

fyea

chye

arw

ith

inth

ep

anel

.T

he

sect

orfi

xed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Ma-

teri

als

,In

du

stri

als,

Con

sum

erD

iscr

etio

nar

y,C

onsu

mer

Sta

ple

s,H

ealt

hC

are,

Fin

anci

als,

Info

rmat

ion

Tec

hn

olog

y,T

elec

omm

un

i-ca

tion

Ser

vic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsar

ere

pre

sente

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.0

5,∗∗

p<

0.0

1,∗∗

∗p<

0.0

01

21

Tab

le12

:E

stim

ates

ofP

BLT

I/LT

Ion

1-Y

ear

TSR

and

3-Y

ear

TSR

1-Y

ear

TSR

3-Y

ear

TSR

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

PB

LT

Ito

LT

I0.

084

0.16

2∗∗∗

0.10

90.

078

0.00

00.

024

0.03

40.

028

(0.0

46)

(0.0

49)

(0.0

56)

(0.0

54)

(0.0

26)

(0.0

28)

(0.0

33)

(0.0

33)

PB

LT

Ito

LT

I-

1L

ag-0

.083

-0.1

53∗∗

-0.0

43-0

.145

∗0.

020

-0.0

050.

027

-0.0

19(0

.047

)(0

.055

)(0

.057

)(0

.058

)(0

.024

)(0

.022

)(0

.021

)(0

.022

)

PB

LT

Ito

LT

I-

2L

ags

-0.0

97∗

-0.1

07∗

-0.0

29-0

.019

(0.0

49)

(0.0

54)

(0.0

32)

(0.0

33)

Tim

eF

EY

esY

esY

esY

esY

esY

esY

esY

esSec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

2249

2205

2249

2205

2249

2205

2249

2205

R2

0.18

0.11

0.21

0.15

0.16

0.11

0.19

0.15

Adju

sted

R2

0.17

0.10

0.21

0.15

0.15

0.10

0.18

0.14

Reg

ress

ion

poi

nt

esti

mat

esw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

able

sto

iden

tify

each

year

wit

hin

the

pan

el.

Th

ese

ctor

fixed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Ind

ust

rial

s,C

onsu

mer

Dis

cret

ion

ary,

Con

sum

erS

tap

les,

Hea

lth

Car

e,F

inan

cial

s,In

form

atio

nT

ech

nol

ogy,

Tel

ecom

mu

nic

atio

nS

ervic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsar

ere

pre

sente

dby

ase

tofd

um

my

vari

able

sth

atse

par

atel

yid

enti

fies

each

firm

.S

ignifi

can

cele

vels

:∗p<

0.05

,∗∗ p

<0.0

1,∗∗

∗p<

0.001

22

Tab

le13

:E

stim

ates

ofP

BLT

I/LT

Ion

5-Y

ear

TSR

and

RO

E

5-Y

ear

TSR

RO

E(1

)(2

)(3

)(4

)(5

)(6

)(7

)(8

)P

BLT

Ito

LT

I-0

.022

-0.0

040.

017

0.01

60.

041∗

0.04

0∗0.

036∗

0.03

7∗

(0.0

15)

(0.0

15)

(0.0

16)

(0.0

17)

(0.0

17)

(0.0

17)

(0.0

14)

(0.0

15)

PB

LT

Ito

LT

I-

1L

ag0.

022

0.00

70.

042∗

0.01

5-0

.005

-0.0

06-0

.006

-0.0

13(0

.014

)(0

.015

)(0

.016

)(0

.015

)(0

.014

)(0

.013

)(0

.013

)(0

.013

)

PB

LT

Ito

LT

I-

2L

ags

-0.0

26-0

.016

-0.0

010.

013

(0.0

15)

(0.0

16)

(0.0

16)

(0.0

15)

Tim

eF

EY

esY

esY

esY

esY

esY

esY

esY

esSec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

2249

2205

2249

2205

2249

2205

2249

2205

R2

0.22

0.18

0.27

0.23

0.13

0.13

0.05

0.05

Adju

sted

R2

0.21

0.17

0.27

0.23

0.12

0.12

0.05

0.05

Reg

ress

ion

poin

tes

tim

ates

wit

hst

and

ard

erro

rsin

par

enth

eses

.T

ime

fixed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

ab

les

toid

enti

fyea

chye

arw

ith

inth

ep

anel

.T

he

sect

orfi

xed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Ind

ust

rial

s,C

onsu

mer

Dis

cret

ion

ary,

Con

sum

erS

tap

les,

Hea

lth

Car

e,F

inan

cials

,In

form

atio

nT

ech

nol

ogy,

Tel

ecom

mu

nic

atio

nS

ervic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsar

ere

pre

sente

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p

<0.0

5,∗∗

p<

0.01,∗∗

∗p<

0.0

01

23

Tab

le14

:E

stim

ates

ofP

BLT

I/LT

Ion

EP

SG

row

than

dT

otal

Rev

enue

Gro

wth

EP

SG

row

thT

otal

Rev

enue

Gro

wth

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

PB

LT

Ito

LT

I0.

767∗

∗0.

872∗

∗1.

050∗

1.09

2∗-0

.001

0.00

70.

027

0.03

2(0

.253

)(0

.300

)(0

.425

)(0

.435

)(0

.015

)(0

.016

)(0

.018

)(0

.018

)

PB

LT

Ito

LT

I-

1L

ag-0

.660

∗∗-0

.711

∗∗-0

.591

∗∗-0

.721

∗∗∗

-0.0

08-0

.005

0.01

10.

001

(0.2

25)

(0.2

31)

(0.1

91)

(0.2

13)

(0.0

17)

(0.0

21)

(0.0

20)

(0.0

23)

PB

LT

Ito

LT

I-

2L

ags

-0.1

94-0

.135

-0.0

18-0

.000

(0.2

71)

(0.2

81)

(0.0

18)

(0.0

21)

Tim

eF

EY

esY

esY

esY

esY

esY

esY

esY

esSec

tor

FE

Yes

Yes

No

No

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esN

oN

oY

esY

esO

bse

rvat

ions

2249

2205

2249

2205

2249

2205

2249

2205

R2

0.02

0.02

0.02

0.02

0.16

0.16

0.19

0.18

Adju

sted

R2

0.01

0.01

0.02

0.02

0.16

0.15

0.18

0.18

Reg

ress

ion

poin

tes

tim

ate

sw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gd

um

my

vari

able

sto

iden

tify

each

year

wit

hin

the

pan

el.

Th

ese

ctor

fixed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Mat

eria

ls,

Ind

ust

rial

s,C

onsu

mer

Dis

cret

ion

ary,

Con

sum

erS

tap

les,

Hea

lth

Care

,F

inan

cials

,In

form

ati

on

Tec

hn

olog

y,T

elec

omm

un

icat

ion

Ser

vic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsar

ere

pre

sente

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifies

each

firm

.S

ign

ifica

nce

level

s:∗p<

0.0

5,∗∗p<

0.01

,∗∗

∗p<

0.0

01

24

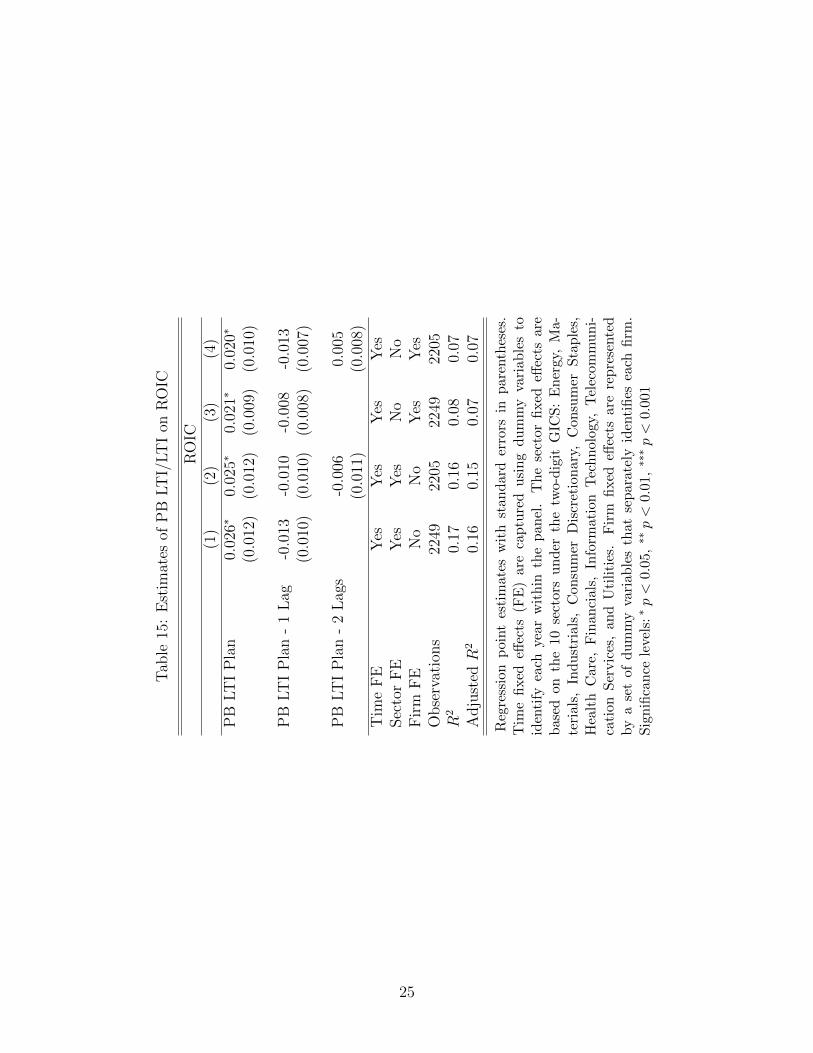

Tab

le15

:E

stim

ates

ofP

BLT

I/LT

Ion

RO

IC

RO

IC(1

)(2

)(3

)(4

)P

BLT

IP

lan

0.02

6∗0.

025∗

0.02

1∗0.

020∗

(0.0

12)

(0.0

12)

(0.0

09)

(0.0

10)

PB

LT

IP

lan

-1

Lag

-0.0

13-0

.010

-0.0

08-0

.013

(0.0

10)

(0.0

10)

(0.0

08)

(0.0

07)

PB

LT

IP

lan

-2

Lag

s-0

.006

0.00

5(0

.011

)(0

.008

)T

ime

FE

Yes

Yes

Yes

Yes

Sec

tor

FE

Yes

Yes

No

No

Fir

mF

EN

oN

oY

esY

esO

bse

rvat

ions

2249

2205

2249

2205

R2

0.17

0.16

0.08

0.07

Adju

sted

R2

0.16

0.15

0.07

0.07

Reg

ress

ion

poi

nt

esti

mat

esw

ith

stan

dar

der

rors

inp

aren

thes

es.

Tim

efi

xed

effec

ts(F

E)

are

cap

ture

du

sin

gdu

mm

yva

riab

les

toid

enti

fyea

chye

arw

ith

inth

ep

anel

.T

he

sect

orfi

xed

effec

tsar

eb

ased

onth

e10

sect

ors

un

der

the

two-

dig

itG

ICS

:E

ner

gy,

Ma-

teri

als

,In

du

stri

als,

Con

sum

erD

iscr

etio

nar

y,C

onsu

mer

Sta

ple

s,H

ealt

hC

are,

Fin

anci

als,

Info

rmat

ion

Tec

hn

olog

y,T

elec

omm

un

i-ca

tion

Ser

vic

es,

and

Uti

liti

es.

Fir

mfi

xed

effec

tsar

ere

pre

sente

dby

ase

tof

du

mm

yva

riab

les

that

sep

arat

ely

iden

tifi

esea

chfi

rm.

Sig

nifi

can

cele

vels

:∗p<

0.0

5,∗∗

p<

0.0

1,∗∗

∗p<

0.0

01

25