performance measures: insights and challenges - · pdf fileperformance measures: insights and...

TRANSCRIPT

Performance Measures:Insights and ChallengesPerformance Measures:Insights and Challenges

David F. LarckerDavid F. Larcker

Management Accounting Research Group ConferenceMarch 25, 2004

Management Accounting Research Group ConferenceMarch 25, 2004

1

Traditional Approach to Performance Drivers ...Traditional Approach to Performance Drivers ...

DuPont ModelDuPont Model

Sales/Assets x Profit/Sales = Profit/Assets Future Cash Flows Stock Price

Residual Income ModelResidual Income Model

[Profit/Assets - Cost of Capital] Future Cash Flows Stock Price

2

Critiques of the Traditional Approach ...Critiques of the Traditional Approach ...

4Financial measures alone are inadequateToo narrowToo lateToo backward looking

4Drivers of financial performance are unknown

4Little insight into intangible assets

4Value-based management, balanced scorecards, and other related methods are now commonplace for selecting an expanded set of performance measures

4Financial measures alone are inadequateToo narrowToo lateToo backward looking

4Drivers of financial performance are unknown

4Little insight into intangible assets

4Value-based management, balanced scorecards, and other related methods are now commonplace for selecting an expanded set of performance measures

3

Internal and External

Communicationand Control

Translatestrategic goals into numerical objectives

Translatestrategic goals into numerical objectives

The Theory ...The Theory ...

Objectives8% increase in ROS10% asset turnover increase 7% EVA growth

Adjust objectives based onresults

Adjust objectives based onresults

Translate objectives into

actionable strategies

Translate objectives into

actionable strategies

StrategiesExpand global marketsProcess cost reductionIncrease new products

Translate strategies into measurements

Translate strategies into measurements

Success IndicatorsWorking capital levelsCustomer satisfactionTime-to-market

4

The Theory ...The Theory ...

4Develop an explicit causal business model describing how value drivers are linked to strategy

4 Identify specific value propositions or hypotheses

4Tabulate and integrate available data across functions (and identify what data are missing)

4Actually test the hypotheses (and determine whether your model and/or data is inadequate)

4Communicate and debate the results, develop new value propositions, and test again

4Develop an explicit causal business model describing how value drivers are linked to strategy

4 Identify specific value propositions or hypotheses

4Tabulate and integrate available data across functions (and identify what data are missing)

4Actually test the hypotheses (and determine whether your model and/or data is inadequate)

4Communicate and debate the results, develop new value propositions, and test again

5

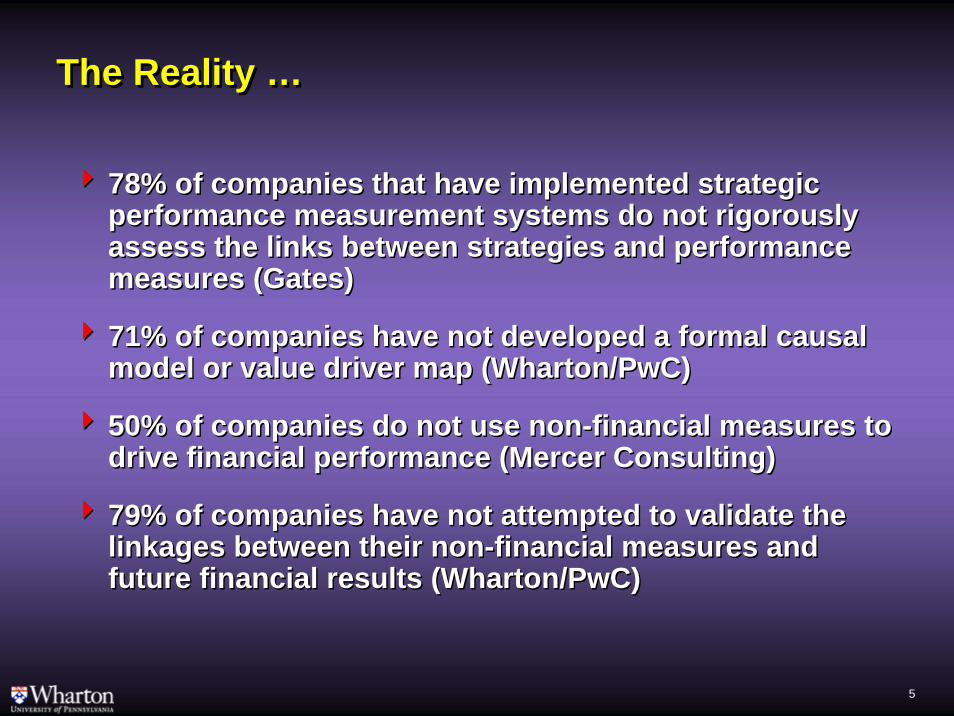

The Reality …The Reality …

4 78% of companies that have implemented strategic performance measurement systems do not rigorously assess the links between strategies and performance measures (Gates)

4 71% of companies have not developed a formal causal model or value driver map (Wharton/PwC)

4 50% of companies do not use non-financial measures to drive financial performance (Mercer Consulting)

4 79% of companies have not attempted to validate the linkages between their non-financial measures and future financial results (Wharton/PwC)

4 78% of companies that have implemented strategic performance measurement systems do not rigorously assess the links between strategies and performance measures (Gates)

4 71% of companies have not developed a formal causal model or value driver map (Wharton/PwC)

4 50% of companies do not use non-financial measures to drive financial performance (Mercer Consulting)

4 79% of companies have not attempted to validate the linkages between their non-financial measures and future financial results (Wharton/PwC)

6

The Reality ...The Reality ...

477% of organizations with a balanced scorecard place little or no reliance on business models (Ittner et al)

4There are relatively few cases where companies with a balanced scorecard test their hypotheses or value propositions even after they have several years of data

4When business models are developed, it is often a one-time event with little influence on ongoing measurement practices

477% of organizations with a balanced scorecard place little or no reliance on business models (Ittner et al)

4There are relatively few cases where companies with a balanced scorecard test their hypotheses or value propositions even after they have several years of data

4When business models are developed, it is often a one-time event with little influence on ongoing measurement practices

7

The Reality …The Reality …

445% of balanced scorecard users found the need to quantify qualitative results to be a major implementation problem (Towers Perrin)

455% of companies stated that the biggest implementation problem for strategic performance measurement systems is not measuring difficult-to-measure activities (Gates)

4Many companies simply ignore qualitative measures or exclude them from their performance reports

445% of balanced scorecard users found the need to quantify qualitative results to be a major implementation problem (Towers Perrin)

455% of companies stated that the biggest implementation problem for strategic performance measurement systems is not measuring difficult-to-measure activities (Gates)

4Many companies simply ignore qualitative measures or exclude them from their performance reports

8

Gaps Between Drivers and Measures …Gaps Between Drivers and Measures …

0

1

2

3

4

5

6

Custom

er

Quality

Operatio

nsS-T Finan

cial

Innovatio

nCom

munity

Employee

Ittner, Larcker, and Randall, 2003

Extremely Important asa Driver for Long-Term

Success

Extremely Important asa Driver for Long-Term

Success

Not at All ImportantNot at All Important

High QualityOf Measurement

High QualityOf Measurement

Extremely LowQuality of

Measurement

Extremely LowQuality of

Measurement

9

So What Are Companies Doing? ...So What Are Companies Doing? ...

4Heavy reliance on management intuition, “organizational folklore”, and unsophisticated guesses

4Fixation on the “four buckets” of the balanced scorecard (with the belief that these categories are all encompassing)

4Attempting to apply a seemingly endless set of measurement frameworks, models, and laundry lists of measures being pushed by consultants

4Measuring an ever-increasing number of measures to avoid missing anything important

4Heavy reliance on management intuition, “organizational folklore”, and unsophisticated guesses

4Fixation on the “four buckets” of the balanced scorecard (with the belief that these categories are all encompassing)

4Attempting to apply a seemingly endless set of measurement frameworks, models, and laundry lists of measures being pushed by consultants

4Measuring an ever-increasing number of measures to avoid missing anything important

10

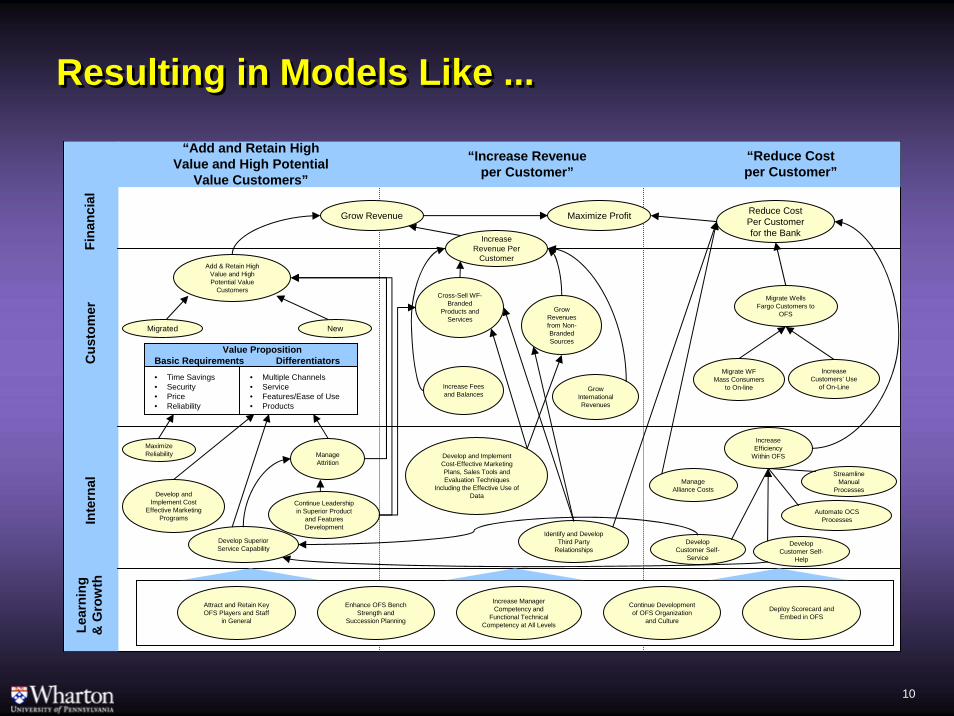

Resulting in Models Like ...Resulting in Models Like ...

Add & Retain High Value and High Potential Value

Customers

Migrated New

• Time Savings• Security• Price• Reliability

• Multiple Channels• Service• Features/Ease of Use• Products

Value PropositionBasic Requirements Differentiators

Maximize Reliability Manage

Attrition

Develop and Implement Cost

Effective Marketing Programs

Continue Leadership in Superior Product

and Features Development

Develop Superior Service Capability

Attract and Retain Key OFS Players and Staff

in General

Enhance OFS Bench Strength and

Succession Planning

Increase Manager Competency and

Functional Technical Competency at All Levels

Continue Development of OFS Organization

and Culture

Deploy Scorecard and Embed in OFS

Grow Revenue Maximize Profit Reduce Cost Per Customer for the Bank

Increase Revenue Per

Customer

Cross-Sell WF-Branded

Products and Services

Grow Revenues from Non-Branded Sources

Increase Fees and Balances

Grow International Revenues

Develop and Implement Cost-Effective Marketing Plans, Sales Tools and Evaluation Techniques

Including the Effective Use of Data

Identify and Develop Third Party

Relationships

Migrate Wells Fargo Customers to

OFS

Migrate WF Mass Consumers

to On-line

Increase Customers’ Use

of On-Line

Increase Efficiency

Within OFS

Manage Alliance Costs

Develop Customer Self-

Service

Develop Customer Self-

Help

Automate OCS Processes

Streamline Manual

Processes

Lear

ning

&

Gro

wth

Fina

ncia

lC

usto

mer

Inte

rnal

“Add and Retain High Value and High Potential

Value Customers”

“Increase Revenue per Customer”

“Reduce Cost per Customer”

11

Some of the Fundamental Questions …Some of the Fundamental Questions …

4How confident are you that business model incorporates the right drivers of financial success?

4How do you use the business model to allocate resources?

4How do you set targets for the measures?

4How can the business model be used to design an effective compensation?

4How confident are you that business model incorporates the right drivers of financial success?

4How do you use the business model to allocate resources?

4How do you set targets for the measures?

4How can the business model be used to design an effective compensation?

12

Identifying the Right Drivers ...Identifying the Right Drivers ...

4Develop a causal business model thatIs linked to organizational strategyArticulates the key, hypothesized drivers of financial performance

4Construct reliable and valid measures for the key drivers

4Verify the linkages in the business model

4Develop a causal business model thatIs linked to organizational strategyArticulates the key, hypothesized drivers of financial performance

4Construct reliable and valid measures for the key drivers

4Verify the linkages in the business model

13

A Major Fast Food Chain …A Major Fast Food Chain …

4Company operates or franchises 6,000+ stores

4Overall profitability was not growing enough to meet either internal or external expectations

4A series of meetings involving senior-level executives from all functional areas produced a consensus business model

4The consensus business model was developed using only management intuition (i.e., without any real data analysis)

4Company operates or franchises 6,000+ stores

4Overall profitability was not growing enough to meet either internal or external expectations

4A series of meetings involving senior-level executives from all functional areas produced a consensus business model

4The consensus business model was developed using only management intuition (i.e., without any real data analysis)

14

A Major Fast Food Chain …A Major Fast Food Chain …

SelectionAnd

Staffing

Employee-AddedValue

EmployeeSatisfaction

•Enablement•Alignment•Accountability

•Enablement•Alignment•Accountability

•Supervision•Support•Fairness

•Supervision•Support•Fairness

•Quantity•Education•Work Experience

•Quantity•Education•Work Experience

CustomerBuying

Behavior

CustomerSatisfaction

•Quality•Shopping Experience•Timeliness

•Quality•Shopping Experience•Timeliness

•Frequency•Retention•Referral

•Frequency•Retention•Referral

SustainedGrowth

ShareholderValue

•Each outlet•Over time•Better than competition

•Each outlet•Over time•Better than competition

•Growth•Earnings•Free Cash Flow

•Growth•Earnings•Free Cash Flow

Consensus Business ModelConsensus Business Model

15

A Major Fast Food Chain …A Major Fast Food Chain …

4Employee turnover became the primary measure used for decision-making and performance evaluation (“we just know this is the key driver”)

4Expensive human resource programs (retention bonuses) were put into place to reduce turnover

4However, subsequent statistical analysis revealed:Stores with same overall turnover, but very different financial performanceMore profitable stores had higher employee turnoverOnly turnover among supervisory personnel had any relation to store financial performance

4Employee turnover became the primary measure used for decision-making and performance evaluation (“we just know this is the key driver”)

4Expensive human resource programs (retention bonuses) were put into place to reduce turnover

4However, subsequent statistical analysis revealed:Stores with same overall turnover, but very different financial performanceMore profitable stores had higher employee turnoverOnly turnover among supervisory personnel had any relation to store financial performance

16

A Major Fast Food Chain …A Major Fast Food Chain …

4Management intuition was only partially correct

4The turnover measure was changed from overall turnover to turnover by employee category

4Further analysis provided an estimate for the financial cost of turnover (and an upper bound for the size of the retention bonus)

4Presently analyzing the relation between employee measures, customer measures, and store profitability

4Management intuition was only partially correct

4The turnover measure was changed from overall turnover to turnover by employee category

4Further analysis provided an estimate for the financial cost of turnover (and an upper bound for the size of the retention bonus)

4Presently analyzing the relation between employee measures, customer measures, and store profitability

17

A Large Operator of Convenience Stores …A Large Operator of Convenience Stores …

4Company owns and operates thousands of convenience stores across the country

4Stores sell gasoline and various food products

4Management intuition:“Gasoline sales are unrelated to food sales”

Managed using two different profit centerSeparate P&L’s

“Only beer and cigarette sales explain profits from food sales”“Employee and customer measures have no impact on profits from food sales”

4Company owns and operates thousands of convenience stores across the country

4Stores sell gasoline and various food products

4Management intuition:“Gasoline sales are unrelated to food sales”

Managed using two different profit centerSeparate P&L’s

“Only beer and cigarette sales explain profits from food sales”“Employee and customer measures have no impact on profits from food sales”

18

Drivers of Store Financial Performance …Drivers of Store Financial Performance …

Employee Turnover Customer Satisfaction Food Profit/Sq Foot

Notation: +/- refers to a strong statistical positive/negative link(precise numbers are not reported due to company request)

Gasoline Gallons Sold

# of Workplace Injuries

Beer Sales/Food Sales

Cigarette Sales/Food Sales

- +

+ +

+ -

+

Food Profit/Sq Foot

19

A Large Operator of Convenience Stores …A Large Operator of Convenience Stores …

4Management intuition was not very insightful

4Combined the food and gasoline profit centers

4Began an internal dialog concerning reducing gasoline prices (with a low margin) to increase food sales (with a high margin)

4Started tracking employee satisfaction, customer satisfaction, and workplace injuries

4 Incorporated these non-financial measures into the quarterly bonus plan

4Management intuition was not very insightful

4Combined the food and gasoline profit centers

4Began an internal dialog concerning reducing gasoline prices (with a low margin) to increase food sales (with a high margin)

4Started tracking employee satisfaction, customer satisfaction, and workplace injuries

4 Incorporated these non-financial measures into the quarterly bonus plan

20

Allocating Resources ...Allocating Resources ...

4Even if you have identified and validated the key drivers, you still need to determine how to allocation resources to improve these factors

4 It is necessary to determine root causes

4Ultimately, you need to estimate the financial consequences of non-financial improvements

4Even if you have identified and validated the key drivers, you still need to determine how to allocation resources to improve these factors

4 It is necessary to determine root causes

4Ultimately, you need to estimate the financial consequences of non-financial improvements

21

Computer Hardware Manufacturer …Computer Hardware Manufacturer …

4Company is a major supplier of computer equipment to consumers and businesses

4Senior-level management desired a model to explain customer behavior

4Model results to be used for justifying and evaluating expenditures on customer initiatives

4Company is a major supplier of computer equipment to consumers and businesses

4Senior-level management desired a model to explain customer behavior

4Model results to be used for justifying and evaluating expenditures on customer initiatives

22

Linking Drivers, Satisfaction, and Outcomes ...Linking Drivers, Satisfaction, and Outcomes ...

Customer Satisfaction75

.7

1.0

1.0

.4

.9

1.0

Relationship

Trust

Set Up

Physical

Troubleshooting

Shopping

Value

61

80

86

80

72

67

78

Retention

Recommendation

Share of Budget

Up Price Tolerance

Down Price Tolerance

Buy Additional

74

76

78

48

73

35

.2

.1

.5

.3

.8

.3

.1

23

Driver Priority Matrix …Driver Priority Matrix …

ImpactImpact

ScoreScore

Physical

TrustSet UpValue

ShoppingRelationship

Troubleshooting

HighHigh

HighHighLowLow

Low

24

Linking Perceptions and Behavior ...Linking Perceptions and Behavior ...

4RetentionIf the retention score was 90 or above (below 90), the customer bought the same brand again 56.76% (30.77%) of the time -- a change of 25.99%

4RecommendationIf the recommendation score was 90 or above (below 90), the customer recommendation resulted in 1.52 (0.87) purchases of the same brand -- a change of 0.65

4RetentionIf the retention score was 90 or above (below 90), the customer bought the same brand again 56.76% (30.77%) of the time -- a change of 25.99%

4RecommendationIf the recommendation score was 90 or above (below 90), the customer recommendation resulted in 1.52 (0.87) purchases of the same brand -- a change of 0.65

25

Computer Hardware Manufacturer …Computer Hardware Manufacturer …

4Based on this model, capital resources were allocated to:

Improving Relationship and Troubleshooting (e.g., improving technical service and quickly providing upgrade notices)Maintaining Trust, Set up, and Value (e.g., improving setup procedures and providing inexpensive migration and data backup services)

4Developed a NPV model for valuing customer initiatives using

Customer marginsEstimated impacts Linkages between perceptions and customer behavior

4Based on this model, capital resources were allocated to:

Improving Relationship and Troubleshooting (e.g., improving technical service and quickly providing upgrade notices)Maintaining Trust, Set up, and Value (e.g., improving setup procedures and providing inexpensive migration and data backup services)

4Developed a NPV model for valuing customer initiatives using

Customer marginsEstimated impacts Linkages between perceptions and customer behavior

26

Target Setting …Target Setting …

4Common intuition: “More is better”; “100% need to be 100% satisfied”

4Considerable difficulty setting goals for any non-financial performance measure

4Difficult to set targets for different measures when no common denominator exists (Is a 10% decrease in customer complaints equivalent to a 3% reduction in defect rates?)

4Non-linear functional relations and tradeoffs among financial and non-financial measures complicate goal setting

4Common intuition: “More is better”; “100% need to be 100% satisfied”

4Considerable difficulty setting goals for any non-financial performance measure

4Difficult to set targets for different measures when no common denominator exists (Is a 10% decrease in customer complaints equivalent to a 3% reduction in defect rates?)

4Non-linear functional relations and tradeoffs among financial and non-financial measures complicate goal setting

27

Manufacturer Study …Manufacturer Study …

0

0.2

0.4

0.6

0.8

1

Mea

n Po

sitiv

e R

ecom

men

datio

n

1 2 3 4 5Prior Wave Self-Reported Customer Satisfaction

0

0.2

0.4

0.6

0.8

1

Mea

n N

egat

ive

Rec

omm

enda

tion

1 2 3 4 5Prior Wave Self-Reported Customer Satisfaction

28

Customer Satisfaction and Financial Results ...Customer Satisfaction and Financial Results ...Major U.S. Telecommunications Firm (n = 2,156 customers)Major U.S. Telecommunications Firm (n = 2,156 customers)

1.221.24

0 20 40 60 80 1001.041.061.08

1.11.121.141.161.18

1.2

Customer Satisfaction in Year 1

Year

2 Re

venu

e / Y

ear 1

Rev

enue

Ittner and Larcker, 1998

29

Investor Advisor Rating and Assets Invested ...Investor Advisor Rating and Assets Invested ...

Assets Invested

Index

Assets Invested

Index

Customer Satisfaction with Investment AdvisorCustomer Satisfaction with Investment Advisor

Note: Assets invested is measured as a composite index that reflected the dollar amount invested, profitability of the products selected by the customer, etc.

0

20

40

60

80

100

120

140

1 2 3 4 5 6 7

30

Target Setting …Target Setting …

4 In some cases there are diminishing returns from increases in non-financial measures, but other situations require very high performance

4Notable thresholds are commonly observed

4Sophisticated analysis is required to identify appropriate targets for non-financial measures

4 In some cases there are diminishing returns from increases in non-financial measures, but other situations require very high performance

4Notable thresholds are commonly observed

4Sophisticated analysis is required to identify appropriate targets for non-financial measures

31

Compensation Plan Design …Compensation Plan Design …

4Most companies use their balanced scorecard or non-financial measures in their reward systems (i.e., If you know the value drivers, why not use them in the bonus plan?)

4Difficulties in using multiple performance measures in formula-based bonus plans:

Assigning weights to each measure“Gaming” associated with a formula-based planBonuses may paid even when performance is “unbalanced”

4One suggested solution for these problems is greater use of subjectivity and discretion in compensation plans

4Most companies use their balanced scorecard or non-financial measures in their reward systems (i.e., If you know the value drivers, why not use them in the bonus plan?)

4Difficulties in using multiple performance measures in formula-based bonus plans:

Assigning weights to each measure“Gaming” associated with a formula-based planBonuses may paid even when performance is “unbalanced”

4One suggested solution for these problems is greater use of subjectivity and discretion in compensation plans

32

Formula-Based Bonus Plan at Citibank …Formula-Based Bonus Plan at Citibank …

4Hurdles or targets (must meet to obtain bonus):Customer satisfaction at or above region meanOperations control audit must be satisfactory

4Potential bonus as a % of salary:Margin growth – 3%Growth in large customers – 1.5%Checking balance growth – 3%Revenue growth – 3%Liability/asset growth – 1.5%Expenses/revenues – 0.5%Total balance/household – 0.5%

4Hurdles or targets (must meet to obtain bonus):Customer satisfaction at or above region meanOperations control audit must be satisfactory

4Potential bonus as a % of salary:Margin growth – 3%Growth in large customers – 1.5%Checking balance growth – 3%Revenue growth – 3%Liability/asset growth – 1.5%Expenses/revenues – 0.5%Total balance/household – 0.5%

33

Balanced Scorecard Bonus Plan at Citibank … Balanced Scorecard Bonus Plan at Citibank …

Manager Bonus

Overall Par Score

FinancialPar

Score

StrategyPar

Score

CustomerPar

Score

ControlPar

Score

PeoplePar

Score

3 Measures 7 - 18 Measures 2 Measures 3 AuditJudgements

StandardsPar

Score

5 QualitativeAssessments

5 QualitativeAssessments

LaborGradeLaborGrade SalarySalary

34

Outcomes at Citibank …Outcomes at Citibank …

4Performance evaluations were primarily influenced by financial results, despite the corporate strategy of emphasizing all of the balanced scorecard categories

4Little weight was placed on “softer,” qualitative measures (after the initial quarters)

4Some of the non-financial measures emphasized in the performance evaluations had no ability to predict future financial performance, whereas some that were ignored were highly predictive

4Performance evaluations were primarily influenced by financial results, despite the corporate strategy of emphasizing all of the balanced scorecard categories

4Little weight was placed on “softer,” qualitative measures (after the initial quarters)

4Some of the non-financial measures emphasized in the performance evaluations had no ability to predict future financial performance, whereas some that were ignored were highly predictive

35

Citibank Branch Manager Survey …Citibank Branch Manager Survey …

45%45%23%23%32%32%Overall, I am satisfied with the scorecard processOverall, I am satisfied with the scorecard process

25%25%20%20%55%55%When it comes to scorecard bonuses, I have no idea who gets what and why

When it comes to scorecard bonuses, I have no idea who gets what and why

40%40%21%21%39%39%My scorecard goals cover all the important parts of my jobMy scorecard goals cover all the important parts of my job

31%31%28%28%41%41%With scorecard, it is easy to see the connection between individual and branch performance

With scorecard, it is easy to see the connection between individual and branch performance

21%21%18%18%61%61%I have a good understanding of the scorecard processI have a good understanding of the scorecard process

DisagreeDisagreeNeutralNeutralAgreeAgree

36

Explicit Statements by Citibank Managers …Explicit Statements by Citibank Managers …

4“Eliminate the scorecards! Promotions and bonuses are still given to those who kiss-up to their supervisors, with little regard to performance, educational background, and experience”

4“I hate this new process. Favoritism comes too much into play”

4“Scorecards only reflect certain parts of your job”

4“This is a black box process, no one knows anything”

4“I would have liked to have known what my evaluation was going to be based on before the quarter began”

4“Eliminate the scorecards! Promotions and bonuses are still given to those who kiss-up to their supervisors, with little regard to performance, educational background, and experience”

4“I hate this new process. Favoritism comes too much into play”

4“Scorecards only reflect certain parts of your job”

4“This is a black box process, no one knows anything”

4“I would have liked to have known what my evaluation was going to be based on before the quarter began”

37

Compensation Plan Design …Compensation Plan Design …

4Many companies have experienced serious problems after incorporating non-financial measures into their bonus plan

4One explanation is that subjectivity helps to combine disparate measures, but is very difficult to use in practice

4Another explanation is that companies do not have a validated causal business model and they use unreliable and invalid measures in the bonus plan

4Many companies have experienced serious problems after incorporating non-financial measures into their bonus plan

4One explanation is that subjectivity helps to combine disparate measures, but is very difficult to use in practice

4Another explanation is that companies do not have a validated causal business model and they use unreliable and invalid measures in the bonus plan

38

Financial Benefits of Using Causal Models …Financial Benefits of Using Causal Models …

Broad Industry Survey of CFOs (n = 157)Broad Industry Survey of CFOs (n = 157)

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Raw ROA Raw ROE Ind Adj ROA Ind Adj ROE

Little Attempt to Use Causal Models and Link Non-Financial Performance to Future Financial PerformanceExtensive Effort to Use Causal Models and Link Non-Financial Performance to Future Financial Performance

39

Why is This So Hard?...Why is This So Hard?...

4 Insufficient model development (e.g., simply relying on generic measurement frameworks or “best practice” is unlikely to work)

4Difficult to determine which measures are useful without sophisticated analysis

Measurement proliferation and disintegrationMeasurement choice becomes more political

4 Inadequate existing measuresPoor reliability and validityInconsistent definitions, units of analysis, and time framesNo common identifier to link data across functions

4 Insufficient model development (e.g., simply relying on generic measurement frameworks or “best practice” is unlikely to work)

4Difficult to determine which measures are useful without sophisticated analysis

Measurement proliferation and disintegrationMeasurement choice becomes more political

4 Inadequate existing measuresPoor reliability and validityInconsistent definitions, units of analysis, and time framesNo common identifier to link data across functions

40

Why is This So Hard? …Why is This So Hard? …

4Organizational barriers stop the sharing data across functions (“data fiefdoms” and “islands of analysis”)

4Some managers do not want to know the results

4 Inadequate analysis skills and resources inside organizations

4Technology (CRM, ERP, etc.) alone is not the answer

4Organizational barriers stop the sharing data across functions (“data fiefdoms” and “islands of analysis”)

4Some managers do not want to know the results

4 Inadequate analysis skills and resources inside organizations

4Technology (CRM, ERP, etc.) alone is not the answer

41

Research Opportunities …Research Opportunities …

4How much emphasis should be placed on intuition versus sophisticated analysis when selecting performance measures?

4How should companies select and combine performance measures that are defined in different dimensions (e.g., money, time, survey scores, etc.)

4How much subjectivity should be used in compensation systems?

4How useful are “soft” or qualitative measures for directing managerial actions?

4How much emphasis should be placed on intuition versus sophisticated analysis when selecting performance measures?

4How should companies select and combine performance measures that are defined in different dimensions (e.g., money, time, survey scores, etc.)

4How much subjectivity should be used in compensation systems?

4How useful are “soft” or qualitative measures for directing managerial actions?

42

Research Opportunities …Research Opportunities …

4How should targets be set for non-financial (and financial) performance measures?

4What are the financial consequences of changing performance measurement systems?

4Are observed financial consequences simply the “Hawthorne Effect?”

4When should non-financial measures be disclosed to external analysts and shareholders?

4How should targets be set for non-financial (and financial) performance measures?

4What are the financial consequences of changing performance measurement systems?

4Are observed financial consequences simply the “Hawthorne Effect?”

4When should non-financial measures be disclosed to external analysts and shareholders?