performance of danish banks during the financial crisis...

TRANSCRIPT

_____________________________________________________________________

_____________________________________________________________________

Performance of Danish Banks during the Financial Crisis - From a DEA Perspective

Author Charlotte Moeslund Madsen

CM87217

Supervisor Christian Schmaltz

Number of characters:

129.367

M.Sc. Finance and International Business Aarhus University

March 2015

Abstract The purpose of this study is to determine whether it possible to discriminate between failed and non-failed Danish banks before and during the financial crisis, and if it is possible to predict, which banks were to fail. The focus is solely on Danish banks in the years 2007 and 2010. The analysis was performed using a Slack-Based Measure of efficiency (SBM), which is a variant of the Data Envelopment Analysis (DEA). The model was composed of seven variables. Six of those were from the bank evaluation model CAMELS, which is an acronym for Capital adequacy, Asset quality, Management efficiency, Earnings, Liquidity, and Sensitivity to market risk. The last variable was the banks exposure to commercial real estate. The analysis follows and extends to the work of Avkiran and Cai (2014), who used the CAMELS variables to predict bankruptcy in US banks by performing a super-SBM model. The SMB model had an input-orientation, as the input variables were more discretionary than the output variables. For scaling method Variables Return to Scale (VRS) was chosen, to incorporate economies of scale into the model. This followed the preferred orientation and scaling of the existing DEA literature, despite the fact that the choice of variables in this study is untraditional compared to the existing literature. The SBM model yields efficiency scores for all the banks from 0 to 1, with 1 being the best. The analysis contained four methods for testing whether there was a significant difference between the efficiency score of the failed and of the non-failed banks and to learn if it was possible to predict, which banks would fail during the crisis. In the 2007 analysis the Mann-Whitney U-test found a significant difference between the failed and the non-failed, implying that the model was able to discriminate between the two groups. The Gini-coefficient was not as high as expected but at a fair level, implying that inequality was present in the sample, giving the model discriminative powers. The layer analysis showed predictive powers, as the non-failed banks were mainly in the upper layers of the analysis and the failed banks were in the lower levels. Lastly, the robustness test showed that the mean values did not differ much, when the sample was changed. Hence, the results were robust. In the 2010 analysis the Mann-Whitney U-test was only significant at a 10 percent significance level. Again the Gini-coefficient was at a fair level, implying that the model should be able to distinguish between the failed and the non-failed. Furthermore, the layer analysis showed no clear signs of predictive powers. However, it was better at identifying the critical failures in the lower layers of the Layer analysis. The robustness test further revealed lacking robustness in the analysis. These tests indicate that the model is capable of discriminating between failing and non-failing banks and predict, which banks will fail. However, during the crisis the model looses both discriminative and predictive powers. The decrease in powers might be

explained by the introduction of the Danish FSA’s Supervisory Diamond, which was a tool to prevent bank failure in Denmark. Furthermore, both analyses seemed to be affected greatly by the largest banks, which seemed to force the mean values up for the efficient banks, possibly due to their large sizes. Keywords: Data Envelopment Analysis, DEA, Danish Banks, Banking, Financial Crisis, Performance, Bank Failure

Content ______________________________________________________________________________________________________________________________________________________________________

i

Table of Contents

PART I 1. RESEARCH DESIGN ................................................................................................. 2

1.1. INTRODUCTION .......................................................................................................................... 2 1.2. PROBLEM STATEMENT ............................................................................................................... 3 1.3. DELIMITATION ........................................................................................................................... 3 1.4. METHOD AND STRUCTURE OF PAPER .................................................................................... 5

PART II 2. DATA ENVELOPMENT ANALYSIS ........................................................................ 8

2.1. TRADITIONAL DEA ................................................................................................................... 8 2.1.1. Notation .................................................................................................................................. 9 2.1.2. Assumptions ............................................................................................................................ 9 2.1.3. Choice of Scaling .................................................................................................................... 10 2.1.4. Inputs and outputs ................................................................................................................. 11 2.1.5. Graphical Explanation ......................................................................................................... 12 2.1.6. Calculating Efficiency Scores .................................................................................................. 14

3. SLACK-BASED MEASURE OF EFFICIENCY ....................................................... 17 3.1. ADVANTAGES OF SBM ............................................................................................................ 17 3.2. SBM EFFICIENCY ..................................................................................................................... 18 3.3. SBM NOTATION ....................................................................................................................... 18 3.4. CHOICE OF SCALING ................................................................................................................ 20

PART III 4. LITERATURE REVIEW ........................................................................................... 22

4.1. PERFORMANCE AND PREDICTING BANKRUPTCY .............................................................. 22 4.2. DEA AND BANKS ..................................................................................................................... 23

4.2.1. Development in DEA models ................................................................................................ 24 4.2.2. Return to scale ....................................................................................................................... 24 4.2.3. Selection of inputs and outputs ................................................................................................ 25 4.2.4. Orientation ............................................................................................................................ 26

4.3. CAMELS AND BANKS ............................................................................................................. 26

PART IV 5. VARIABLES ............................................................................................................... 29

5.1. THE CAMELS VARIABLES ...................................................................................................... 29 5.1.1. Capital Adequacy .................................................................................................................. 30 5.1.2. Asset Quality ........................................................................................................................ 30 5.1.3. Management Efficiency .......................................................................................................... 31 5.1.4. Earnings ............................................................................................................................... 31 5.1.5. Liquidity ............................................................................................................................... 32 5.1.6. Sensitivity to Market Risk ..................................................................................................... 33

5.2. EXPOSURE TO REAL ESTATE .................................................................................................. 33

6. CHOOSING INPUTS AND OUTPUTS .................................................................. 35 6.1. FULFILLING THE ASSUMPTIONS ............................................................................................. 36

Content ______________________________________________________________________________________________________________________________________________________________________

ii

7. DATA COLLECTION ............................................................................................... 38 7.1. BANKSCOPE ............................................................................................................................... 39

8. METHODS ................................................................................................................ 41 8.1. MANN-WHITNEY U-TEST ....................................................................................................... 41 8.2. GINI-COEFFICIENT .................................................................................................................. 42 8.3. LAYER ANALYSIS ...................................................................................................................... 43 8.4. ROBUSTNESS TEST ................................................................................................................... 44

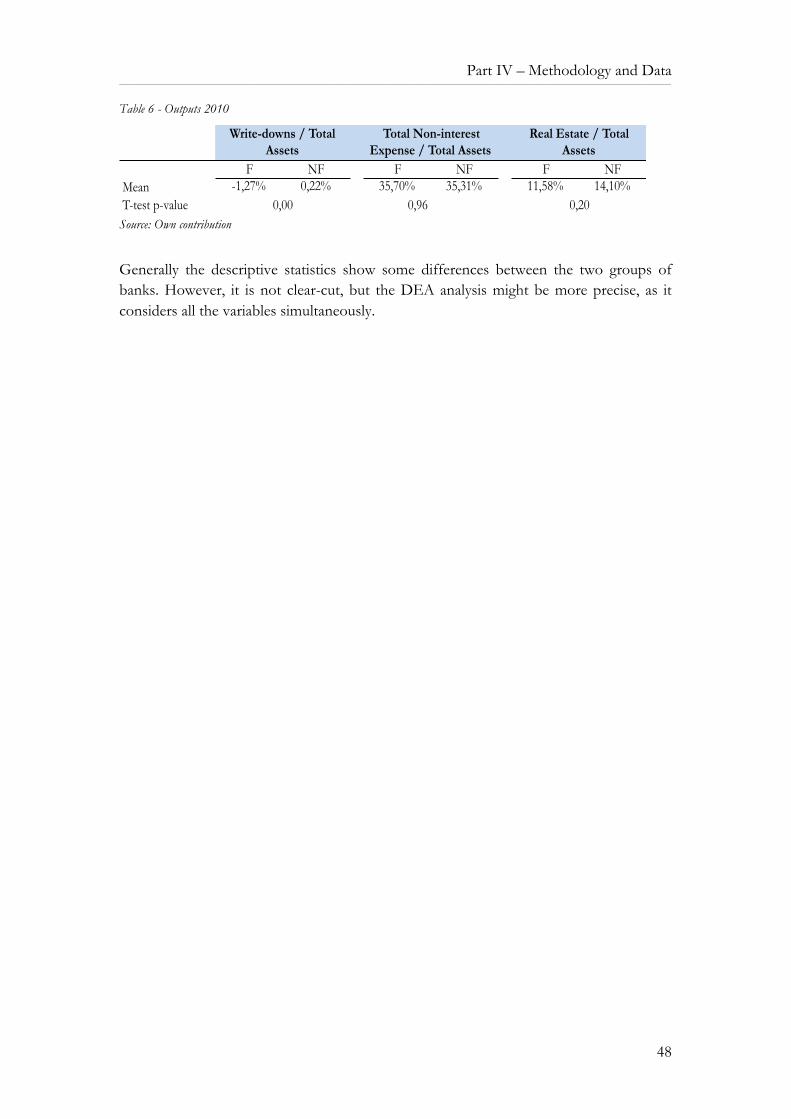

9. DESCRIPTIVE STATISTIC ..................................................................................... 46 9.1. DESCRIPTIVE STATISTICS 2007 .............................................................................................. 46 9.2. DESCRIPTIVE STATISTICS 2010 .............................................................................................. 47

PART V 10. ANALYSIS ................................................................................................................ 50

10.1. DEA ANALYSIS ....................................................................................................................... 50 10.1.1. Software .............................................................................................................................. 50 10.1.2. Complications for the Analysis ............................................................................................ 51

10.2. EMPIRICAL RESULTS .............................................................................................................. 52 10.2.1. Empirical Findings 2007 .................................................................................................... 53 10.2.2. Empirical Findings 2010 .................................................................................................... 56

PART VI 11. DISCUSSION .......................................................................................................... 61

11.1. FURTHER RESEARCH ............................................................................................................. 62

12. CONCLUSION ........................................................................................................ 63

13. REFERENCES ........................................................................................................ 65

APPENDIX ........................................................................................................................ 69

iii

List of figures Figure 1 - Structure of the paper .................................................................................................. 6 Figure 2 - Production Possibility Set ......................................................................................... 10 Figure 3 - Graphical Explanation .............................................................................................. 13 Figure 4 - DEA Solver Interface ................................................................................................ 50

List of tables Table 1 - 1 input and 2 outputs .................................................................................................. 11 Table 2 - CAMELS & Proxies ................................................................................................... 29 Table 3 - Inputs 2007 ................................................................................................................... 46 Table 4 - Outputs 2007 ............................................................................................................... 47 Table 5 - Inputs 2010 ................................................................................................................... 47 Table 6 - Outputs 2010 ............................................................................................................... 48 Table 7 - Empirical Findings 2007 ............................................................................................ 53 Table 8 - Layer Analysis 2007 ..................................................................................................... 54 Table 9 - Robustness Test 2007 ................................................................................................. 56 Table 10 - Empirical Findings 2010 .......................................................................................... 57 Table 11 - Layer Analysis 2010 .................................................................................................. 58 Table 12 - Robustness Test 2010 ............................................................................................... 59

iv

List of abbreviations and acronyms Abbreviation Explanation CRS Constant Return to Scale VRS Variable Return to Scale DMU Decision-Making Unit DEA Data Envelopment Analysis SBM Slack-Based Measure of efficiency CAMELS Bank rating model CCR Same as CRS BBC Same as VRS LP Linear Programming TE Technical Efficiency SE Scale Efficiency PTE Pure Technical Efficiency

______________________________________________________________________________________________________________________________________________________________________

1

Part I

Introduction

______________________________________________________________________________________________________________________________________________________________________

2

1. Research Design

1.1. Introduction Basically, a bank is a financial intermediary between a borrower and a saver. They simply establish the contact between the two, so it should be possible to manage without them. However, already as the financial crisis started the banks were blamed for causing the crisis from multiple sides, implying that the role of the banks is not as simple as just a financial intermediary (Udvalget om Finanskrisens Årsager, Erhvervs- og Vækstministeriet 2013). Banks are relevant for the public as they bring down transaction costs and risk for the borrower and the saver. Instead of searching for a counterpart the borrower and the saver can simply contact the bank and eliminate the time and challenges of finding a fitting counterpart (Baldvinsson 2011). Today banks are deeply involved in the society and their actions can imply severe consequences such as stagnating development, if they are reluctant to provide capital for businesses. Furthermore, they are connected to almost all parts of the society through loans, deposits, and bank accounts. Hence, when a bank fails it can have tremendous impact on the customers but also on all other stakeholders, such as the society and other banks. Because of this influence, the literature has attempted several routes to foresee the failure of banks to avoid crisis like the recent one, where a few bank failures started an avalanche of distressed banks (Iversen 2013). In this paper the multidimensional Data Envelopment Analysis (DEA) model will be used to measure the performance of the Danish banks before and during the financial crisis from 20081 to 20132, by using data from 2007 and 2010. The model will make a so-called efficient frontier consisting of a number of banks, which are best practice banks. This frontier will help divide the banks into groups, dependent on their performance, as it is assumed that the higher the efficiency score a bank achieves, the better it performs. Hence, it is expected that the failing banks will encounter low efficiency scores. This paper ceases to fill a gap in the literature. Not since the early 1990’s where Bukh used DEA models to examine Nordic and Danish banks, have any DEA research focused solely on Denmark (Bukh, Førsund & Berg 1995, Bukh 1994) . This is despite the fact that the Danish financial sector is quite interesting from a research perspective. Since the crisis the profitability of Danish banks has been half the

1 The sub-prime crisis in US started during 2007. However, it was not until 2008 that the first Danish bank, BankTrelleborg, were taken over by another bank, Sydbank, making this the starting point for this study. 2 In 2013 Denmark received the highest credit rating from the three largest credit rating agencies and were recognized for their stabile bank market (Iversen, 2013). Hence, 2013 will be the ending year in this study.

______________________________________________________________________________________________________________________________________________________________________

3

level of their peers3 mainly attributable to the five largest banks. The remaining banks have had poor profitability. Additionally, the asset quality in Danish banks is lower than for their peers. To compensate for the low quality the Danish banks had very large reserve coverage (IMF 2013). Furthermore, as the crisis hit Denmark the Government established Finansiel Stabilitet, an organization with the purpose of taking over distressed banks. A highly unique initiative (Udvalget om Finanskrisens Årsager, Erhvervs- og Vækstministeriet 2013). Despite these issues, Denmark and the Danish banks were among the first countries to receive the highest rating from the credit rating agencies and return to a stabile bank market. Hence, Denmark is a truly interesting country when considering banks. This study seeks to identify and distinguish between the failed and the non-failed Danish banks by performing the DEA analysis variant, the Slack-Based Measure of efficiency (SBM), with a set of untraditional variables.

1.2. Problem statement Using the Data Envelopment Analysis model with the variables from the CAMELS bank evaluation model and a commercial real estate loan variable, this paper seeks to discover which banks had the best and worst performance during the recent financial crisis. The main purpose of this thesis is to examine whether it is possible to predict which banks would fail during the financial crisis, by using the efficiency scores from a DEA analysis. It is also considered whether it is possible to identify the failing banks both before and during the financial crisis by using the DEA efficiency scores. Lastly, it is investigated if the discriminating and the predictive powers of the DEA model are significant. In other words, if the model will be able to distinguish between the two groups of banks and be able to predict, which banks are failing.

1.3. Delimitation The analysis will incorporate factors from the CAMELS model together with a real estate variable, as these have proven to be relevant in foreseeing bank failure (Cole, White 2012, Avkiran, Cai 2014). Besides these seven variables, other factors could have been relevant to incorporate. However, every time an extra variable is included, the model will be less discriminating. So it is important to choose the variables carefully to maintain discriminatory power while still choosing enough variables to explain the issue.

3 IMF uses Austria, Finland, France, Germany, the Netherlands, Norway, Sweden, Switzerland, and the United Kingdom as peers.

______________________________________________________________________________________________________________________________________________________________________

4

The model has some restrictions, which means that the variables included have to have the same format such as volume, index, and percentage. Of these, volume variables are mostly preferred in the literature (Thanassoulis 2003). This issue implies that some factors, which would have been relevant to this study, cannot be included due to their format. An example is the lending growth. A high lending growth has proved to be correlated with the risk of failure, so this could have been an insightful variable. However, as this factor is measured in percentage, it is not possible to include it in the model. The same goes for the sum of large exposures and the funding-ratio, which are both variables from the Supervisory Diamond4 that could have been relevant to incorporate (The Danish FSA 2010). Another issue is the format of the analysis, which implies that the banks will be evaluated solely on one year’s performance. This might seem narrow if considering a bank, which is otherwise healthy but have had a weak year that particular year. However, the model consists of seven different variables, so a single bad year might make some of the numbers seem poor but ceteris paribus not all of them, unless the bank is distressed and therefore potentially a failing bank. Another material delimitation is caused by the use of accounting data. The balance is a snapshot of the current situation in the bank and not an average of the past year. Hence, it is possible to make the bank look better at the end of the year, than what would have been the case if the balance had been an average view. On the other hand, a bank may also encounter a loss just before formulating the balance, which will make it look like it is in a worse position than what is actually the case (Baldvinsson 2011). However, as the annual report is generally used to valuate banks, and other companies, the author believes it to be a suitable tool for this analysis too. One large challenge for the analysis is the classification of the banks. When identifying the distressed banks all banks, which either went bankrupt, ceased activity or got acquired by another bank, is classified as failed banks in the analysis. This has two consequences. First of all, it is impossible to know whether any of the banks that got overtaken during the crisis could have survived on its own and therefore should not have been classified as a failed bank. Second, as the financial crisis started rolling it got very clear that Danske Bank was in great danger of failing but got saved by the government, as it was ‘too big to fail’. Under normal circumstances the bank would probably have failed, but as the consequences of letting it fail were too big with regards to the financial market, the investors, and the customers, the bank was rescued. This implies that Danske Bank, might look like a bank, which is about to fail. As it did not fail, their figures and the figures of other banks, which where rescued or got helped by a bank package, might skew the result (Iversen 2013).

4 The variables of the Supervisory Diamond are based on learnings and experiences from the recent financial crisis regarding the distressed and failed banks. By 2012 all Danish banks had to fulfill the limits of the diamond as an attempt to limit the number of bank failures in the future (The Danish FSA 2010).

______________________________________________________________________________________________________________________________________________________________________

5

As the bank market has a great influence on other markets and the society in general, many accords and compliances are imposed on the banks. Even though these are relevant for the market and have great influences, most of these accords and compliances will not be dealt with due to the scope and focus of this paper.

1.4. Method and Structure of paper This study is based on Avkiran & Cai’s article Identifying distress among banks prior to a major crisis using non-oriented super-SBM. Especially, Avkiran is well-known within the field of DEA and their article has been published in the Annals of Operations Research, which is a journal published by Springer that engages in key aspects in operations research, including DEA. The author of this paper therefore believes the article to be reliable and trustworthy. The remainder of the empirical material is mainly consisting of articles, which have been published in other well-established and professional journals and books written by contributors to the DEA theory. The author feels, that this paper builds on a strong empirical background. Furthermore, it is assumed that as the paper only focuses on the banking sector, articles and research from other parts of the world than Denmark still have a high transferability to this study. The data used in the analysis is solely stemming from the annual reports of the banks and the database Bankscope. The annual reports have been approved by an auditor and must be considered trustworthy, even though some of the banks may wish to conceal and postpone issues such as large amount of impaired loans. This will be elaborated later in the paper (Finanstilsynet 2012). However, as the annual reports are the most direct way of getting large amounts of information about the banks, these are used in the analysis without further adjustments. Furthermore, the data from Bankscope have been reviewed to ensure that it is consistent with the data in the annual reports. Below Figure 1 displays the structure of the paper.

______________________________________________________________________________________________________________________________________________________________________

6

Figure 1 - Structure of the paper

Source: Own contribution

Each part of the paper covers different relevant areas of the study. Part I – The research design of the study and introduction is presented. Part II – The DEA approach used in this paper will be presented to ensure that the reader has an understanding of the concept and the terminology. Part III – The Literature Review sets out the conceptual framework of the paper and goes through relevant literature, hereunder performance and bankruptcy, the rating model CAMELS, and DEA and banks. Part IV – The methodology and data used in this paper will be examined. Chapter 5 gives a comprehensive explanation to the variables included in the model. Chapter 6 will go through the selection of inputs and outputs from a DEA perspective and Chapter 7 will describe the process of collecting the data for the paper. Chapter 8 presents the four methods used for examining the results of the DEA analyses and Chapter 9 provides the descriptive statistics. Part V – The results of the DEA analysis will be processed and tested using the four methods introduced in Chapter 8. Part VI – Chapter 11 is a discussion on how to use the results and if the current interventions towards banks are enough. Further research areas are also suggested. Finally, chapter 12 is a conclusion on the study.

Chapter 1 Research Design

Chapter 2 Data Envelopment Analysis

Chapter 3 Slack-based Measure of Efficiency

Chapter 4 Literature Review

Chapter 5 Variables

Chapter 6 Choosing Inputs and Outputs

Chapter 7 Data Collection

Chapter 8 Methods

Chapter 9 Descriptive Statistics

Chapter 10 Analysis

Chapter 11 Discussion

Chapter 12 ConclusionPart

VI

Part

IV

Part

IPa

rt I

IPa

rt I

IIPa

rt V

______________________________________________________________________________________________________________________________________________________________________

7

Part II

Data Envelopment Analysis

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

8

2. Data Envelopment Analysis

In 1978 Charnes, Cooper and Rhodes proposed a model for Measuring the efficiency of decision making units, where they used linear programming to measure efficiency while considering multiple inputs and outputs simultaneously (Charnes et al, 1978, p. 1). Today this model is known as Data Envelopment Analysis (DEA) with constant return to scale (CSR). The model is also known as the CCR model after the authors. In 1984 Banker, Charnes and Cooper extended the DEA model with variable return to scale (VRS), which also got known as the BCC model. The model is basically the same as the original model besides the different scaling choice (Banker, Charnes & Cooper 1984) . Since 1978 the DEA model has been extended with many different variations but all with basis in one of the two original models (Cooper, Seiford & Tone 2000) .

2.1. Traditional DEA Traditionally DEA is a method of performance measurement used to assess the comparative efficiency of homogenous units or observations. In the DEA terminology these units are called Decision Making Units or DMUs. As DEA is a multidimensional model it can consider multiple inputs and outputs at the same time, and hereby identify the most efficient DMUs. Performance measurement in a DEA context is the efficiency of resource utilization. In other words, how well a certain DMU transforms the inputs it gets into outputs. Naturally, the idea is to identify those DMUs, which use the fewest inputs to produce the most outputs. Hence, in most cases the method will be used in an operational setting, like a production, where there is a clear connection between the inputs used and the outputs produced. Over the years, the model has been expanded to areas where the connection is a little less profound but where the general idea of identifying best performance is still relevant (Thanassoulis 2003). As the DEA model is non-parametric, it does not require a functional form to be determined before the analysis. This implies that it is not possible to specify a ‘wrong’ functional form. Compared to other analysis methods this is a great advantage, as most real data does not fit a certain functional form and therefore often will skew the results. However, the model is also deterministic. This means that everything lower than the efficient frontier is considered inefficient. This makes the model sensitive to outliers, as an outlier risk forcing up the efficient frontier, making efficient DMUs seem inefficient. This will be elaborated later in Part II.

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

9

2.1.1. Notation As DEA is capable of handling multiple inputs and outputs and several DMUs, vector notation is used to keep it simple and clear. Consider

-‐ n observed DMUs (j = 1,…, n) -‐ all using m different inputs (i = 1, … , m) -‐ to produce s different outputs (r = 1, …, s)

This means that DMU j is defined by -‐ the input vector 𝑥! ∈ ℜ!

! and -‐ the output vector 𝑦! ∈ ℜ!

! The production possibility set (PPS) is defined as:

-‐ 𝑃𝑃𝑆 = (𝑥,𝑦) 𝑥 ∈ ℜ!! 𝑐𝑎𝑛 𝑝𝑟𝑜𝑑𝑢𝑐𝑒 𝑦 ∈ ℜ!

! This means that in a DEA model every DMU has the same m input variables and s output variables. When the analysis is performed the most efficient ones, meaning the ones that use the lowest level of inputs to produce the highest level of outputs, will compose the so-called efficient frontier. The area below this efficient frontier is called the Production Possibility Set (PPS) and all the inefficient DMUs are enveloped in this area. This notation is adopted from Thanassoulis (2003) and will be used throughout the paper. Unfortunately, as this is not unique DEA notation different sources may use other notations.

2.1.2. Assumptions When performing a DEA analysis a number of conditions must be assumed to construct the PPS. These conditions are:

1. Inefficient production is possible. This has two consequences a. Strong free disposability of input: It is always possible to use more input

without increasing the output level. This also implies that it is possible to use less input without decreasing the outputs as long as the DMU is inefficient.

b. Strong free disposability of output: It is always possible to produce less output without decreasing the level of inputs and vice versa as long as the DMU is inefficient.

2. No output can be produced without some input: This is also known as the ‘no free lunch’ assumption. This means that no positive output can be produced without a positive input. Hence, 𝑥!, 0 ∈ 𝑃𝑃𝑆 but if y’ > 0 then (0,𝑦!) ∉ 𝑃𝑃𝑆. This is very logical when considering an operational model, where physical inputs are used to produce physical outputs. However, in a situation where the

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

10

production is more theoretical it can cause some problems if the model includes variables like net income or other variables, which easily can have value of zero or even a negative value. As this is an issue for some of the variables in this study, this assumption will be dealt with later.

3. Minimum extrapolation: This means that all DMUs are part of the PPS and that the PPS is the smallest set that fulfills the above conditions.

4. Constant return to scale: If x’, y’ ∈ 𝑃𝑃𝑆 then for all 𝜆 > 0 we have 𝜆𝑥!, 𝜆𝑦! ∈ 𝑃𝑃𝑆 - This means that the model will identify the most efficient

DMU(s) and create the efficient frontier as a straight tangent on this or these DMU(s). This last assumption can be omitted and in that case the model will have variable return to scale (VRS). This is also the difference between the two original models, the CRS and the VRS model.

2.1.3. Choice of Scaling When creating a DEA model the choice of scaling is an important subject. There are two options; Constant return to scale (CRS) and Variable return to scale (VRS). Figure 2 shows an example of the two scaling methods. The green line is CRS and the blue line is VRS. Figure 2 - Production Possibility Set

Source: Own contribution

When using CRS the model will identify the most efficient DMU5 in the sample. In the simplest model with a single input and a single output the model will make a straight line from the origin and through the efficient DMU. This straight line is the efficient frontier and the positive area below it, is the PPS. All the remaining DMUs will be enveloped by

5 Or DMUs if two or more DMUs are equally efficient.

VRS

CRS

PPS

0

5

10

15

20

25

30

0 1 2 3 4 5 6

Output

Input

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

11

the efficient frontier in this area. Their efficiency is dependent on their distance from the frontier. The more efficient they are, the closer they will be to the frontier. When using the CRS model the fourth condition is effective, which implies that it is possible to multiply the input/output-combination of an efficient DMU with a factor and receive another larger or smaller efficient DMU, which will be placed further up or down the frontier. In reality, a production facility will often experience economies of scale, when they increase their production and if they get too large, they will experience diminishing economies of scale. This implies that it is often difficult for small and large-sized DMUs to be deemed efficient under CRS (Thanassoulis 2003). The VRS has a slightly different approach. In Figure 2, it is easy to see that the model incorporates economies of scale and encounters both increasing and decreasing economies of scale on the efficient frontier. Instead of just creating a straight line, the model finds the best performing DMUs at different sizes and creates the frontier along those DMUs. Both scaling choices have some pros and cons. When applying VRS the efficiency measures are more robust compared to those calculated with CRS. However, some DMUs might seem efficient without being it, solely because there is no better alternative at that size. Hence, when using VRS any DMUs with either very large outputs or very small inputs compared to the other DMUs, will most likely become efficient due to their extreme values. On the other hand, using CRS requires that the DMUs are able replicate combinations from efficient banks, which in reality often is impossible due to advantages such as economies of scale (Bukh 1995).

2.1.4. Inputs and outputs When choosing inputs and outputs for a DEA model several things should be considered. One thing to keep in mind is the format of the inputs and outputs. In general, the values are preferred to be volume measures, however it is possible to use e.g. indices, as long as two or more formats are not combined. If volume measures and indices are combined, it can result in some DMUs becoming inefficient even though they are efficient. See the Table 1 below for an example.

Table 1 - 1 input and 2 outputs

Input 1 Output 1 Output 2 DMU 1 5 20 2,5 DMU2 10 40 2,5

Source: Own contribution

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

12

Imagine DMU 1 and 2 as two factories that produce furniture; chairs and tables. The input is wood, output 1 is total number of chairs and output 2 is number of tables per machine. When looking at input 1 and output 1 for DMU 1 and 2 it is clear, that the two DMUs are equally efficient, but that DMU 2 has a larger production than DMU 1. Now, imagine that DMU 1 produces five tables on two machines and DMU 2 produces ten tables on four machines. Hence, the production is still twice as big for DMU 2 but output 2, the tables per machine, is now 2,5 for both. DMU 1 will now seem more efficient than DMU 2 even though that is not the case. For the model to make the two DMUs equally efficient output 2 should have been five for DMU 2, implying that DMU 2 should have produced twenty tables on the four machines. However, as the index is standardized and therefore independent of size, the two DMUs will have the same output. As this example clearly illustrates the inputs and outputs of a DEA model should be kept in volume measures or alternatively, all in indices. However, using only indices also implies that only CSR can be applied to the model, as the sizes of the DMUs, which the VRS is based on, will be standardized.

2.1.5. Graphical Explanation Figure 3 is an example of the simplest version of a DEA model with a single-input and a single-output. In practice, this model will never be used, as the advantage of DEA is its ability to handle multiple inputs and outputs simultaneously. However, it is a good graphical explanation of how DEA works. Under the VRS method DMU F, A, D, and E define the so-called efficient frontier, which is shown as the blue dotted line in Figure 3. These four DMUs are considered best practice. Below the efficient frontier is the production possibility set (PPS), where the remaining DMUs are located. The PPS contains all feasible combinations of inputs and outputs. The green dotted line is the efficient frontier under CRS. It is clear that under CRS only DMU A is deemed efficient, as it has the highest slope of the DMUs and hence the highest efficiency, as it only needs two inputs to produce 12 outputs. From Figure 3 it is clear to see, that the DMUs with the lowest levels of inputs and the highest levels of outputs easily are deemed efficient under VRS but not necessarily under CRS.

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

13

Figure 3 - Graphical Explanation

Source: Own contribution

Looking at the DMUs in Figure 3 it is clear how an outlier easily could skew the results. Imagine if DMU A, by mistake, had been entered into the model with 21 outputs instead of the current 12 outputs. This would shift the CRS frontier to a much steeper slope, which none of the other DMUs would be able to conform with. Further, all of the other DMUs would get very low efficiency scores compared to DMU A. As an example, DMU D, which is almost

efficient under CRS, would suddenly have an efficiency score of !"!",!

= 0,54.

The outlier would also cause problems under VRS. DMU F would due to its lower levels of input compared to DMU A, still be deemed efficient as the only one. However, none of the other DMUs would now be efficient, as their outputs were smaller than DMU A’s outputs. The difference would not be as severe as under CRS, but DMU D would now,

instead of being efficient, have an efficiency score of !"!"

= 0,81 with an output-

orientation. Usually not is possible to draw the model due to the multidimensional form, so the outliers must be identified using other methods. This could be through simple calculation, where the different variables are standardized and compared, to see if any of them stands out. The software used in this paper provides another option. The results calculated by the software contain a reference set for reach DMU, which can give an indication of potential outliers. A reference set shows for each the inefficient DMUs, which efficient DMUs it should try to replicate. If one of the efficient DMUs is referred to constantly in the reference sets, it could be an indication of an outlier. A thorough explanation of the reference set and an example of how the solution to a DEA model with more than three variables is calculated, are found in the appendix.

A B

C D E

F

G

0

5

10

15

20

25

30

0 1 2 3 4 5 6

Output

Input

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

14

2.1.6. Calculating Efficiency Scores When calculating the efficiency scores the formulation of the calculation is dependent on the orientation of the model. In an input-oriented model the inputs are examined for possible reductions while the outputs are held constant. In an output-orientation the inputs are constant, while the model looks to increase the outputs. Under VRS the choice of orientation is important, as the efficiency scores can change if the orientation is changed. Imagine in Figure 3 on page 13 a new DMU with 1 input and 2 outputs. It would be situated just below DMU F. If an input-orientation were used, the new DMU would be deemed efficient, as it were not possible to find a lower level of inputs, while keeping the outputs constant. However, if an output-orientation were used, the DMU would be deemed inefficient, as the DMU should be able to maintain the input level, but produce the same outputs as DMU F. This is also known as mix-efficiency (Thanassoulis 2003). Under CRS the efficiency scores will be the same independent of the orientation of the model. When calculating the efficiency, each of the DMUs will by turns be the unit of assessment. In the model the DMU of assessment is called DMU0. The formulation for the input-oriented model is: 𝑀𝑖𝑛 𝜃 Subject to

𝜆!𝑥!" ≤ 𝜃𝑥!!, 𝑖 = 1,… ,𝑚!

!!!

𝜆!𝑦!" ≥ 𝑦!!, 𝑟 = 1, . . , 𝑠!

!!!

𝜆! = 1 𝑉𝑅𝑆!

!!!

𝜆! ≥ 0, 𝑗 = 1, . . ,𝑁 Where theta, 𝜃, is the objective function and the efficiency score, which for the input-oriented model should be minimized. The right-hand side of the first two constraints attempts to minimize the input level of DMU0, while keeping the output level constant. The purpose is to find the lambdas, which will fulfill both sides of the constraints while minimizing theta. The third constraint is only relevant for VRS models. This constraint forces the efficient frontier to follow the most efficient DMUs at different sizes making the line piecewise. If this constraint is removed, the model will identify the most efficient DMU(s) and scale the combination of inputs and outputs to form the efficient frontier (Thanassoulis 2003).

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

15

When minimizing the efficiency scores under input orientation the model will compare DMU0 to the remaining DMUs and the PPS. If the DMU is efficient, it will be located on the efficient frontier, implying that it is not possible to decrease the level of inputs without detriment to the outputs. The efficiency score symbolize the percentage to which the DMU can decrease its level of input while keeping the level of output constant. Hence, an efficiency score of 0,8 means that the DMU can decrease the inputs to 80 % of the current level (Thanassoulis 2003). Instead of an input-orientation, an output-orientation can also be used. The formulation for the output-oriented model is: 𝑀𝑎𝑥 𝜑 Subject to

𝜆!𝑥!" ≤ 𝑥!!, 𝑖 = 1,… ,𝑚!

!!!

𝜆!𝑦!" ≥ 𝜑𝑦!!, 𝑟 = 1, . . , 𝑠!

!!!

𝜆! = 1 𝑉𝑅𝑆!

!!!

𝜆! ≥ 0, 𝑗 = 1, . . ,𝑁 The output-oriented model is almost similar to the input-oriented but with a few differences. As this model is focusing on the output level of DMU0 the purpose is to maximize phi. The phi is therefore affected by the outputs of the DMUs, while the inputs are kept constant. The phi is therefore multiplied to the output vector, where theta was multiplied to the input vector. As phi is maximized it will yield a result, which is equal or larger than one, which means that the efficiency score instead is the inverse of phi (Thanassoulis 2003). To illustrate output-orientation, see Figure 3 on page 13. It is clear that DMU D is dominating DMU B. DMU D produces 17 outputs with 3 inputs, where DMU B uses 3 inputs and only produces 12 outputs. This means that the phi for DMU B is 17/12 = 1,4167. Hence, the output efficiency of DMU B is 1/1,4167 = 0,706, implying that DMU B is only producing 70,6 % of its potential. When modeling in DEA it is important to keep in mind that the efficiencies found are relative efficiencies. For the efficiencies to be absolute, it would demand an assumption stating that the DMUs, which comprise the efficient frontier, were fully and absolutely efficient and covered all possible combinations. However, in reality it is possible that some of the DMUs, which are deemed efficient, in fact are capable of becoming more

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

16

efficient. Hence, the efficiencies in DEA cannot be more than relative efficiencies based on the included DMUs. The efficiency score is more complex than what is seen at first sight. Hence, a DMU can be deemed efficient in different ways. Technical efficiency (TE) is full efficiency in a CRS model, while efficiency in a VRS model is called pure technical efficiency (PTE). The difference between the two efficiencies is called scale efficiency (Cooper, Seiford & Tone 2000) . Scale efficiency (SE) shows how much the choice of scale impacts the efficiency score. Imagine a DMU with the following efficiency scores, 𝜃!"#! and 𝜃!"#! , under CRS and VRS, respectively. Using these scores the SE is measured as:

SE = !!"#!

!!"#!

The SE can never be larger than one, as the VRS efficiency score always will be larger or equal to the CRS efficiency score, due to the nature of the scaling methods. In order to find the TE for a DMU in a VRS-model the relationship between the different efficiencies can be used. Hence, TE = PTE * SE Using this decomposition makes it possible to depict the source of inefficiency for a DMU, whether it is caused by inefficient operations, represented by PTE, or disadvantageous conditions, represented by the SE, or both (Cooper, Seiford & Tone 2000) . In the appendix a more thorough graphical example is included. As mentioned earlier, the literature has undergone a great development since the introduction of the two original models. Many variations and improvements have been presented and the next section will examine one of these extensions to the original models.

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

17

3. Slack-based Measure of Efficiency

For this study the original DEA model, hereafter known as DEA, is not sufficient. As mentioned above the DEA model cannot handle negative values and values of 0. As the model in this study will contain variables, which can obtain negative values, another model must be considered. What DEA lacks is translation invariance, the ability to handle negative values. One translation invariant model is the Additive model. However, as this model has serious imperfections regarding the efficiency scores and the calculation hereof, this model is hardly ever used. Instead it is often replaced by the Slack-based Measure of efficiency (SBM). The SBM provides almost the same advantages as the Additive model, but offers a more useful result.

3.1. Advantages of SBM The SBM model has several favorable characteristics. Even though it is not fully translation invariant like the Additive model, it allows for input values to be semi-positive, which means it can handle values of 0. Additionally, the output values are ‘free’ meaning it permits all values (Cooper, Seiford & Tone 2000) . The efficiency score is also unit invariant. This means that the results will be the same independent of the scale of the variables. As an example, the efficiency scores would be the same if the net income variable were changed from one currency to another. This is not the case with the DEA model (Cooper, Seiford & Tone 2000) . This is a great advantage when using data from an annual report, which consist of both accumulated and static data. By using the SBM model, the difference in the format of the figures is irrelevant and will not skew the results (Cooper, Seiford & Tone 2000) . Another important quality for the SBM model is that the DMUs are monotone decreasing in each of the slacks. This means that if just one of the input or output values is changed, it will affect the efficiency score. In DEA the efficiency scores are found with radial projection, where the model put weights on the different inputs and outputs when comparing them. This implies that it is possible to change an input or output value in the model and still get the same result. However, as the SBM accumulates all the slacks, any changes will be detected and affect the efficiency score (Cooper, Seiford & Tone 2000) .

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

18

3.2. SBM Efficiency One of the biggest differences between the DEA and the SBM model is the introduction of 𝑠!!and 𝑠!!, which is input excess and output shortfall, respectively, or in other words; slack. By inserting the two slack variables, the model becomes capable of detecting any slack present in all the inputs and outputs for each DMU.

3.3. SBM Notation In this section the efficiency score and the constraints of an SBM model will be examined and compared to DEA.

𝜌 = 1− 1𝑚

𝑠!!𝑥!!

!!!!

1+ 1𝑠𝑠!!𝑦!!

!!!!

Subject to:

𝜆!𝑥!" + 𝑠! = 𝑥!!, 𝑖 = 1,… ,𝑚!

!!!

𝜆!𝑦!" − 𝑠! = 𝑦!!, 𝑟 = 1, . . , 𝑠!

!!!

𝜆! , 𝑠!, 𝑠! ≥ 0, 𝑗 = 1, . . ,𝑁 At first sight, the formulation is seemingly similar to DEA. However, the objective function is more comprehensive, as the slack variables have been incorporated (Cooper, Seiford & Tone 2000) . The last part of the numerator of the efficiency score calculation is the slack for each input (𝑠!!) divided by the value of the input (𝑥!!) it refers to. By dividing with the input value the slacks get standardized. Hence, the size of the DMU will not influence the size of the slack, as slacks from large banks are divided with large input values and vice versa for small banks. The sum of the all the standardized input slacks is then divided by the number of inputs (m) to get the average slack per input. If there is no input slack, meaning the DMU is efficient, this part of the numerator will be 0 and the total numerator will be 1. If the DMU does experience input slack the numerator will yield a value below 1. The same is valid for the denominator of the efficiency score but with opposite sign. If the DMU does not experience output slack the denominator will be 1, but if there is slack in just one of the outputs, the value of the denominator will be above 1. Hence, in the SBM model a DMU can only become efficient if both the inputs and the outputs are efficient.

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

19

The first two constraints seem similar to DEA asides the inclusion of the slack variables, and that the ‘less than’- and ‘greater than’-signs are replaced by equal signs. The equal signs are due to the slack variables, as they catch any difference between the right-hand side and the left-hand side, resulting in the two sides becoming equal. Finally, the lambdas and the slack variables all have to be positive or 0. As the software used in this paper does not allow for a standard SBM but only for an input- or output-oriented SBM, the objective has to be revised to reflect one of the two orientations. If the standard SBM were to be used, the software should yield results for both input and output variables simultaneously, but this is not an option in the software used in this study. Additionally, it is important to consider whether all the variables are discretionary. If this is not the case, it might be more accurate to focus on either the input or output-orientation, to ensure that the result is found from variables, which are under managerial control (Thanassoulis 2003). Hence, the SBM formulation is revisited. For an input-oriented SBM-model the following notation is used.

𝜌!" = 1− 1𝑚

𝑠!!

𝑥!!

!

!!!

Subject to:

𝜆!𝑥!" + 𝑠! = 𝑥!!, 𝑖 = 1,… ,𝑚!

!!!

𝜆!𝑦!" − 𝑠! = 𝑦!!, 𝑟 = 1, . . , 𝑠!

!!!

𝜆! , 𝑠!, 𝑠! ≥ 0, 𝑗 = 1, . . ,𝑁 For an output-oriented SBM-model the following notation is used.

𝜌!"# = 1+ 1𝑠

𝑠!!

𝑦!!

!

!!!

Subject to:

𝜆!𝑥!" + 𝑠! = 𝑥!!, 𝑖 = 1,… ,𝑚!

!!!

𝜆!𝑦!" − 𝑠! = 𝑦!!, 𝑟 = 1, . . , 𝑠!

!!!

𝜆! , 𝑠!, 𝑠! ≥ 0, 𝑗 = 1, . . ,𝑁

Part II – Data Envelopment Analysis ______________________________________________________________________________________________________________________________________________________________________

20

The new objective functions are now a modified version of the original SBM objective function, focusing on either input slacks or output slacks. The models have many of the same advantages as the original SBM model but give the analyst an opportunity to choose an orientation for the model.

3.4. Choice of scaling As with the orientation, the software also requires a choice of scaling. The different pros and cons mentioned in the section 2.1.3 Choice of Scaling are also present when using a SBM model. Hence, using the CRS method implies that all banks have to achieve the same level of efficiency, but at different activity levels. Economies of scale is not present in this model, meaning that small banks should be able to obtain the same efficiency as larger banks, that operate under economies of scale. Hence, a bank, which operates fully efficiently, might not be efficient in the model, because another bank has better conditions for efficiency. In return, economies of scale is present with the VRS method. However, if the VRS method is used, the risk of deeming an inefficient DMU efficient increases. Especially, DMUs with extremely low or high values are likely to be deemed efficient, solely based on the extreme values. Hence, it is important to clarify what scaling method is used and to be fully aware of the consequences the chosen method can have.

______________________________________________________________________________________________________________________________________________________________________

21

Part III

Literature Review

Part III – Literature Review ______________________________________________________________________________________________________________________________________________________________________

22

4. Literature Review

The Literature Review will go through performance and bankruptcy both regarding regular companies and banks. Next, an overview of how DEA has been used in predicting bank failure is presented. Finally, the CAMELS model and how it has been used in the banking literature is examined. The appendix holds an overview of the Danish bank and the financial crisis with a focus on the Danish bank packages.

4.1. Performance and Predicting Bankruptcy When discussing corporate performance in finance theory, one concept is predominating. Good performance is equal to maximization of shareholder’s wealth, hence the market value of the company (Berk, DeMarzo 2011). Normally, the job of predicting good performance and bankruptcy is reserved to credit rating agencies such as Moody’s Investors Service (Moody’s) and Standard and Poor’s (S&P). The rating agencies assess and rate the risk and quality of companies, debt securities and countries, and assign them with a rating from AAA to CCC dependent on, the risk and quality. If a company receives a CCC rating it is in severe danger of going bankrupt (Casu, Girardone & Molyneux 2006) . When analyzing banks, it is easy to just consider them as any other company. However, it is important to be aware of the differences between a bank and an ordinary company, as this has a great influence on how to view concepts such as stakeholders, risk, and not least performance. Normally, a company will supply a service or a product to its customers. However, a bank is instead a financial intermediary between borrowers and savers. Basically, a bank deposits money for savers and lend them to borrowers. This intermediary role requires a well-performing institution as deposits will often have a short-term horizon and should be available instantly or within a short period to the saver. However, the deposits are simultaneously used to supply loans for the borrowers. These loans will often have a medium to long-term horizon, which creates a mismatch between the incoming and the outgoing funds. If this mismatch is not handled carefully, it will increase the liquidity risk, which means that the bank might not be able to fulfill its liabilities (Casu, Girardone & Molyneux 2006) . The idea of foreseeing bankruptcy is a common goal both for the corporate world and the banking world. In 1968, Altman published his work on the Z-score formula for predicting bankruptcy. This Z-score consisted of five ratios; working capital to total assets, retained earnings to total assets, EBIT to total assets, market value of equity to total book value of liabilities, and sales to total assets. Each of the ratios are positively

Part III – Literature Review ______________________________________________________________________________________________________________________________________________________________________

23

correlated to the Z-score and the higher the score the lower the risk of bankruptcy (Altman 1968). Ever since Altman published his Z-score the academic world has been trying to come up with an even better prediction method, using various kinds analysis techniques (Demyanyk, Hasan 2010, Altman 1968). Canbas, Cabuk, and Kilic (2005) used a principal component analysis to built an integrated early warning system, which can identify banks with serious problems. Fiordelisi, Marques-Ibanez and Molyneux (2011) used Granger-causality techniques to measure the relationship between risk, capital and bank efficiency in European banks. Cox and Wang (2014) used discriminant analysis to identify the main predictors of bank failure to use these indicators in an early warning system. Kolari, Glennon, Shin, and Caputo (2002) used a parametric logit analysis and a non-parametric trait recognition approach in the attempt of predicting failures in large US commercial banks. Generally, there are many approaches to predicting bank failures both in terms of model choices and variables to be included.

4.2. DEA and banks Since the late 1980’s, DEA analyst have been absorbed with finding the best way to measure performance and efficiency in banks using DEA models. Consequently, banking is one of the most used keywords in DEA articles (Emrouznejad, Thanassoulis 1996). A survey, which covered the last 30 years of DEA practice, found that ‘bank or banking’, were the 12th most used keyword in DEA articles and more used than keywords such as production, optimization, and benchmarking (Emrouznejad, Parker & Tavares 2008) . In 1992, Siems presented what is thought to be the first article, which used a DEA model to distinguish between failed and non-failed US banks, focusing on management quality (Siems 1992, Avkiran, Cai 2014). Since then, many have tried to improve and extend the DEA analysis for bank failure prediction. Despite the high interest and the many published DEA articles on the subject, there is no clear-cut way on how to predict failures or measure performance in banks. Therefore, the literature opens up for a large degree of freedom when analyzing banks. However, this freedom implies that it can be very difficult to compare analyses and get an overview of the literature and the methods used. The following sections will go through some of the issues in the literature and how the many methods differ.

Part III – Literature Review ______________________________________________________________________________________________________________________________________________________________________

24

4.2.1. Development in DEA models When Charnes, Cooper and Rhodes (1978) introduced the CCR model in 1978, the purpose was to measure efficiency in public ‘programs’ such as schools and other non-profit entities. The focus on the public sector was due to a lack of prices and profits in the model, which implies that the inputs and outputs are independent of cost and price. This cause that the model is not suitable for private sector, as the competition would force prices to be involved in the analysis (Charnes, Cooper & Rhodes 1978) . In 1984 Banker, Charnes, and Cooper (1984) extended the work from the CCR models by including a convexity constraint. The extension builds on the economic theory of production, as the concept of constant return to scale might be too theoretical. In reality a production will often experience both increasing return to scale, constant return to scale and decreasing return to scale, as the production increases in size. Hence, the BCC model incorporated these scaling differences with the convexity constraint (Banker, Charnes & Cooper 1984, Cook, Seiford 2009) . Both the CCR model and the BCC model builds on radial projection, which means that it requires an orientation. As it in some cases might be an issue that only the inputs or the outputs are in question, Charnes et al (1985) introduced the Additive model. The Additive model combines both orientations, as it incorporates slacks in the constraints. The objective function in this model is to maximize the sum of the input and the output slacks. This has some consequences; the efficiency scores can now obtain any value instead of a value in the interval 0: 1 , making the efficiency scores difficult to interpret and compare. Another issue is that the inputs and outputs might be measured in non-commensurate units, making the sum of the slacks an unsuitable measure. In other words, the Additive model is not unit invariant, which in a worst-case scenario can make the efficiency score useless (Cook, Seiford 2009). Since 1985, many different attempts to fix the issues with the Additive model have been published and one solution is Tone’s (2001) Slack-Based Measure of efficiency (SBM). The SBM model has many of the same advantages as the Additive model. Additionally, it has one advantage compared to the Additive model, as it provides comparable efficiency scores in the interval 0: 1 , just like DEA (Cooper, Seiford & Tone 2000) . Many other model variances, both radial and non-radial, have been published through the years, but this paper only focuses on some of the more popular and relevant models for this study.

4.2.2. Return to scale The choice between CRS and VRS can have a great effect on the results of the DEA analysis and it is therefore important to consider both pros and cons of both scaling methods. The VRS method seems to be preferred by most authors in recent time, to

Part III – Literature Review ______________________________________________________________________________________________________________________________________________________________________

25

avoid the strict scaling of the CRS method, even if it might imply an advantage for some of the DMUs (Pasiouras, Fethi 2010). In their study on efficiency in European banks, Altunbas et al (2001) found, that in most countries, including Denmark, small banks experienced constant return to scale. This implies that for some countries it might be more appropriate to use a mix of VRS and CRS such as the non-increasing return to scale. This is easily done by changing the constraint for VRS from 𝜆! = 1 !

!!! to 𝜆! ≤ 1 !!!! (Thanassoulis 2003).

However, as most software packages only allow the user to choose between CRS and VRS, this is often not an option. Due to the complexity in the choice of the return of scale, many authors choose to use both scaling methods in their publications and therefore report two results; one result for CRS and one for VRS. Using both scaling methods allow the author to identify scale efficiency as well and hence get a better understanding of the efficiency score (Zuzana 2014, Seiford, Zhu 1999).

4.2.3. Selection of inputs and outputs There have been almost as many assumptions of inputs and outputs as there have been applications of DEA (Bergendahl 1998, p. 235). Bergendahl’s quote on the choice of inputs and outputs in a DEA bank analysis is still, 17 years later, valid. Each bank analysis seems to have its own set of inputs and outputs. An explanation to this variance is most likely that the literature still lacks to identify a set of inputs and outputs, which catch the entire complexity of a bank (Berger, Humphrey 1997, Pasiouras, Fethi 2010). The selection of inputs and outputs can often cause trouble due to the literature’s inconsistent concerning the variables to be included. Obviously, the variables will be dependent on the purpose of the analysis but even analyses with the same purpose can have very differing inputs and outputs (Pasiouras, Fethi 2010). An example is the classification of deposits. Some see deposit as an input, others as an output. Some even divided the deposits into subsections and use some as inputs and others as outputs. Hence, dependent on the approach and the purpose of the analysis, the deposits can be used very different (Pasiouras, Fethi 2010). Historically, the bank analyses have, despite the variety, been very true to the idea of the input and output linkage; the inputs are used to produce the output and an increase in input should increase the outputs as well. Hence, the input variables were often factors like labor, number of branches, capital and other factors, which the bank needed to ‘produce’ the output variables, such as loans, interest income, and total income (Bergendahl 1998, Pasiouras, Fethi 2010). Compared to other methods of predicting bank failure, this approach often makes DEA stand out. Whereas other methods usually

Part III – Literature Review ______________________________________________________________________________________________________________________________________________________________________

26

focus on more financial figures such as financial ratios, risky assets, and market value of the bank, DEA analysis has held on to the production idea (Altman 1968, Canbas, Cabuk & Kilic 2005, Demyanyk, Hasan 2010) . In recent years, some DEA papers have challenged the traditional approach to bank studies, perhaps inspired by some of the other research fields in banking. Avkiran is one of the leading advocates for a more financially based DEA model. He finds that traditional DEA, despite the idea of linkage, often has an ill-explained selection of inputs and outputs, with an unclear link to theory. Moreover, he concluded that the, in a financial setting, untraditional choice of variables in the DEA literature, makes it difficult to compare the results to other methods (Avkiran 2006). Instead he introduced traditional finance and banking theory to his DEA models (Avkiran 2009, 2006, Avkiran, Cai 2014).

4.2.4. Orientation As touched upon earlier, the choice of orientation can have a great influence on the efficiency scores and on how the results are interpreted. In the literature, most authors choose the input-orientation, as the inputs are often discretionary factors, which are easier to change for the management, compared to the outputs. This could be inputs such as labor, expenses, and capital and outputs such as loans, number of transactions, and income. Hence, it is ceteris paribus easier for the management to hire more labor than to double the number of transactions. Even though most studies use input-orientation, some analysts use the output-orientation while others use models without orientation6 (Pasiouras, Fethi 2010).

4.3. CAMELS and banks In November 1979, the Uniform Financial Institutions Rating System was introduced by the Federal Financial Institutions Examination Council (FFIEC) in the USA. The purpose of the rating system was to evaluate financial institutions and identify those that was in distress and needed more attention. Originally, the system was known as CAMEL, which was an acronym for the five variables; Capital adequacy, Asset quality, Management efficiency, Earnings, and Liquidity. However, as the banking industry incurred some changes, the original model was no longer sufficient. So in 1997 the sixth variable, Sensitivity to market risk, was added to the model and the name was extended to CAMELS. Despite the American origin, various bank sectors around the world are now evaluated with the CAMELS model (Federal Deposit Insurance Corporation 1997, Barr et al. 2002, Sayed, Sayed 2013).

6 An example of a model without orientation is the SBM model. However, it can be used with orientations as well, as is seen in this paper.

Part III – Literature Review ______________________________________________________________________________________________________________________________________________________________________

27

When the FFIEC evaluates financial institutions with the CAMELS model, they assign a number between 1 and 5 to the financial institution based on how well they perform on the six variables. The best rating is 1 and this group includes sound financial institutions with no need for supervisory concern. The worst rating is 5 and the institutions in this group have unsafe and unsound practices or conditions, which require ongoing supervisory attention, as failure is highly likely (Federal Deposit Insurance Corporation 1997). The CAMELS model has always been shrouded in a little mystery, as the public does not know exactly what the six different factors cover. Despite that obvious challenge, numerous analyses have been published using the CAMEL or the CAMELS model to evaluate banks. Cole and White (2012) use proxies for the six CAMELS variables in combination with other variables in their multivariate logistic regression, where the dependent variable is a binary variable with the two outcomes; fail or survive. They find that the CAMELS variables are capable of explaining bank failures both in the recent crisis and in the American bank crisis in 1985-1992. Barr el al (2002) has another approach to the CAMELS model than most studies. Instead of finding proxies for the six CAMELS variables, they use the actual CAMELS scores that each bank has received, in a DEA model to evaluate the productive efficiency in US banks. Based on their results they recommend using CAMELS as a monitoring tool. Hence, the CAMELS variables have been used in different approaches and seem to be a good predictor of bank failure.

______________________________________________________________________________________________________________________________________________________________________

28

Part IV

Methodology and Data

Part IV – Methodology and Data ______________________________________________________________________________________________________________________________________________________________________

29

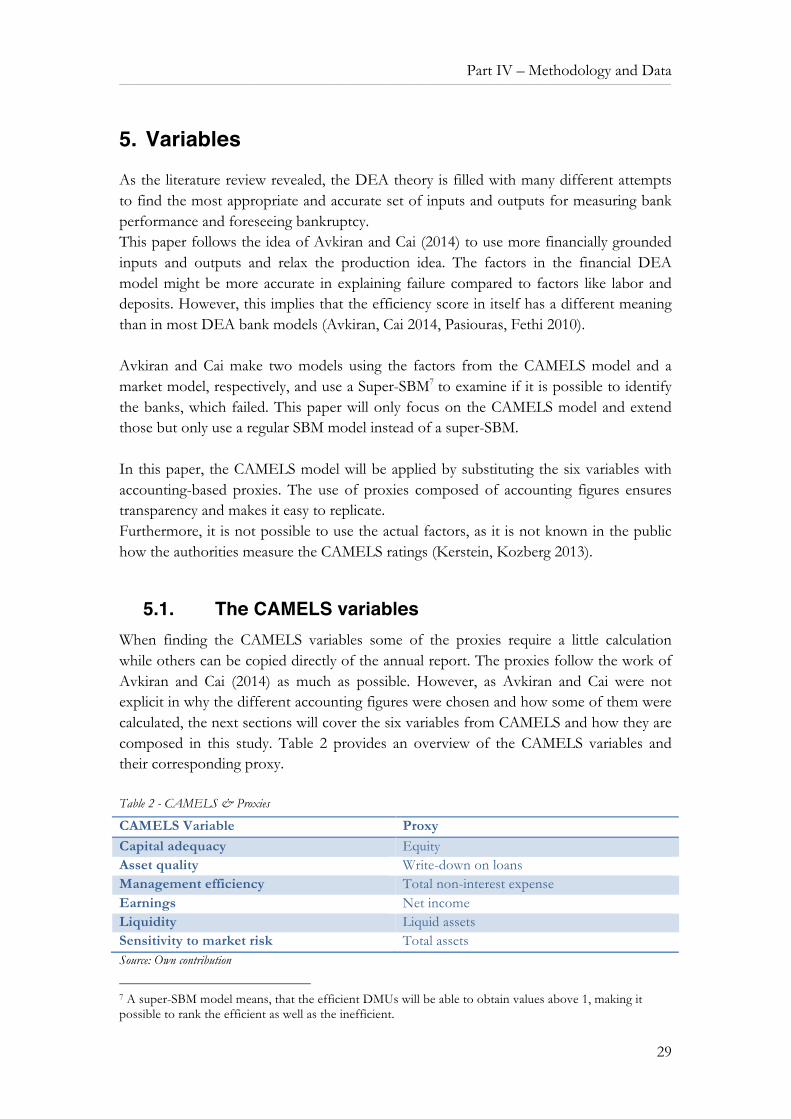

5. Variables

As the literature review revealed, the DEA theory is filled with many different attempts to find the most appropriate and accurate set of inputs and outputs for measuring bank performance and foreseeing bankruptcy. This paper follows the idea of Avkiran and Cai (2014) to use more financially grounded inputs and outputs and relax the production idea. The factors in the financial DEA model might be more accurate in explaining failure compared to factors like labor and deposits. However, this implies that the efficiency score in itself has a different meaning than in most DEA bank models (Avkiran, Cai 2014, Pasiouras, Fethi 2010). Avkiran and Cai make two models using the factors from the CAMELS model and a market model, respectively, and use a Super-SBM7 to examine if it is possible to identify the banks, which failed. This paper will only focus on the CAMELS model and extend those but only use a regular SBM model instead of a super-SBM. In this paper, the CAMELS model will be applied by substituting the six variables with accounting-based proxies. The use of proxies composed of accounting figures ensures transparency and makes it easy to replicate. Furthermore, it is not possible to use the actual factors, as it is not known in the public how the authorities measure the CAMELS ratings (Kerstein, Kozberg 2013).

5.1. The CAMELS variables When finding the CAMELS variables some of the proxies require a little calculation while others can be copied directly of the annual report. The proxies follow the work of Avkiran and Cai (2014) as much as possible. However, as Avkiran and Cai were not explicit in why the different accounting figures were chosen and how some of them were calculated, the next sections will cover the six variables from CAMELS and how they are composed in this study. Table 2 provides an overview of the CAMELS variables and their corresponding proxy. Table 2 - CAMELS & Proxies

CAMELS Variable Proxy Capital adequacy Equity Asset quality Write-down on loans Management efficiency Total non-interest expense Earnings Net income Liquidity Liquid assets Sensitivity to market risk Total assets Source: Own contribution

7 A super-SBM model means, that the efficient DMUs will be able to obtain values above 1, making it possible to rank the efficient as well as the inefficient.

Part IV – Methodology and Data ______________________________________________________________________________________________________________________________________________________________________

30

5.1.1. Capital Adequacy Capital adequacy is a term introduced with the Basel Accords, and states how much capital a bank should hold in relation to the riskiness of the business activities, meaning both assets and off-balance activities. Hence, the more risky a bank is, the more capital it needs to hold (Casu, Molyneux 2003). This is obviously not possible to calculate with accounting numbers, as it also concerns off-balance sheet risks. Instead Equity is used as a substitute, as this posting is an indication on how solid the bank is. The Equity can be seen as a capital cushion, which the bank can be forced to use if the loans they have provided, are not paid back. Hence, Equity is not an immaterial figure. Compared to a normal company, a bank will often have a higher leverage. A manufacturing firm will often have debt-to-equity ratio just above 1, whereas a bank can have a debt-to-equity ratio as high as 11,5. Despite this high leverage Equity is crucial for the bank, as it risks becoming technically insolvent, if the Equity is not large enough to cover the loss from loans that are not paid (Casu, Girardone & Molyneux 2006) . As the Equity consists of prior years profit, and also is a measure of the banks’ risk appetite, it is expected that distressed banks will have a lower level of Equity and vice versa for the well-performing banks. Hence, Capital Adequacy, represented by Equity, is an output variable in the model.