permian basin - encana · permian basin *estimated inventory based on 450-660 ft spacing ... •...

TRANSCRIPT

ENCANA CORPORATION

Permian Basin

Jeff Balmer, PhDVice-President & General Manager, Southern Operations

2

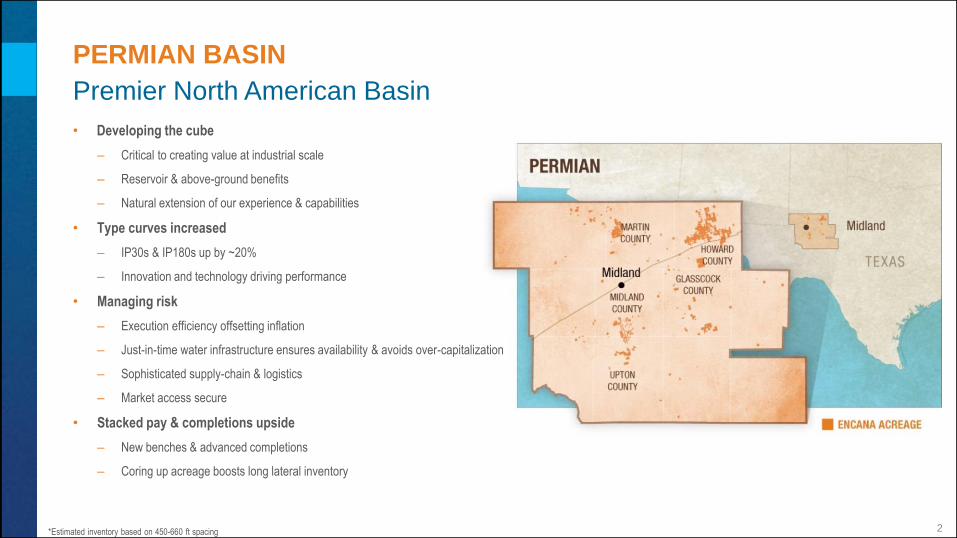

Premier North American Basin

PERMIAN BASIN

*Estimated inventory based on 450-660 ft spacing

• Developing the cube

– Critical to creating value at industrial scale

– Reservoir & above-ground benefits

– Natural extension of our experience & capabilities

• Type curves increased

– IP30s & IP180s up by ~20%

– Innovation and technology driving performance

• Managing risk

– Execution efficiency offsetting inflation

– Just-in-time water infrastructure ensures availability & avoids over-capitalization

– Sophisticated supply-chain & logistics

– Market access secure

• Stacked pay & completions upside

– New benches & advanced completions

– Coring up acreage boosts long lateral inventory

3

ENCANA’S PERMIAN ACREAGE

Core Position in Midland Basin

Martin

Midland

Howard

Glasscock

Upton Reagan

Active ECA Rigs

Encana Land

Basin Core

• In the Permian, execution efficiency at industrial

scale is going to be critical

• Industry leader in driving efficiency at scale

Cowden Pad Multi-Spread Operations

4

0

20,000

40,000

60,000

80,000

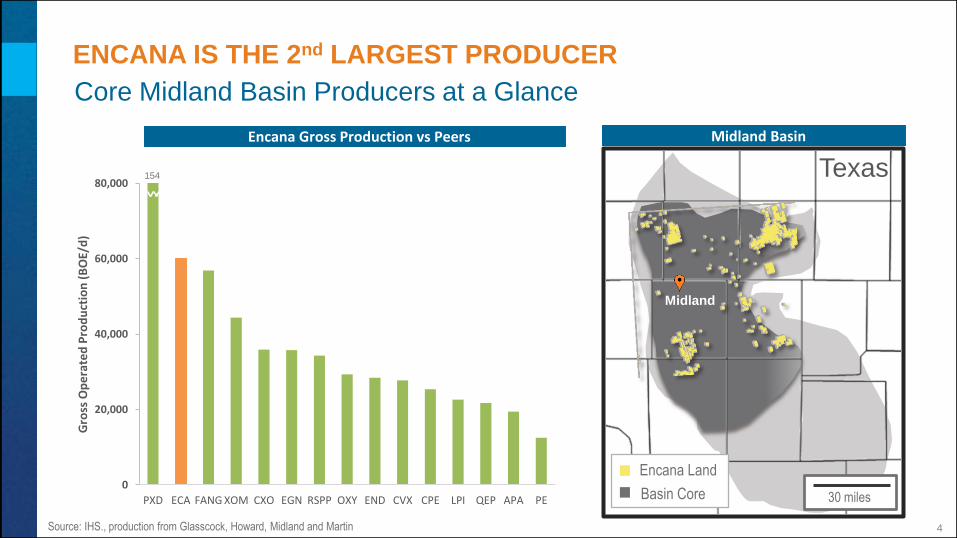

PXD ECA FANG XOM CXO EGN RSPP OXY END CVX CPE LPI QEP APA PE

Gro

ss O

pe

rate

d P

rod

uct

ion

(B

OE/

d)

ENCANA IS THE 2nd LARGEST PRODUCER

Core Midland Basin Producers at a Glance

Source: IHS., production from Glasscock, Howard, Midland and Martin

Midland BasinEncana Gross Production vs Peers

154

30 miles

Midland

Texas

Encana Land

Basin Core

5

CUBE DEVELOPMENT ABOVE-GROUND BENEFITS

Development at Industrial Scale

• Highly efficient, agile development

• Multi-well pads

– Higher utilization of services & infrastructure

• Multiple drilling rigs and frac spreads on a pad

– Rapid cycle times

– Accelerated learnings

• Integrated supply chain

– Leveraging economies of scale

– Centralized planning and logistics

Cube Development

Above Ground Benefits

Multi-well Pads

Multi-rig, Multi-

spread

Integrated Supply Chain

Re-occupied facilities

Reliable market access

Water Manage-

ment

6

• Re-occupied infrastructure

– Multiple wells sharing infrastructure yields

scale efficiency

– Continued high utilization of wellsite

facilities through re-occupation

• Reliable market access

– Pipe based gathering through Medallion

– Provides access diversity of markets

CUBE DEVELOPMENT ABOVE-GROUND BENEFITS

Practical Infrastructure Solutions

RAB Davidson Re-occupied Facilities

7

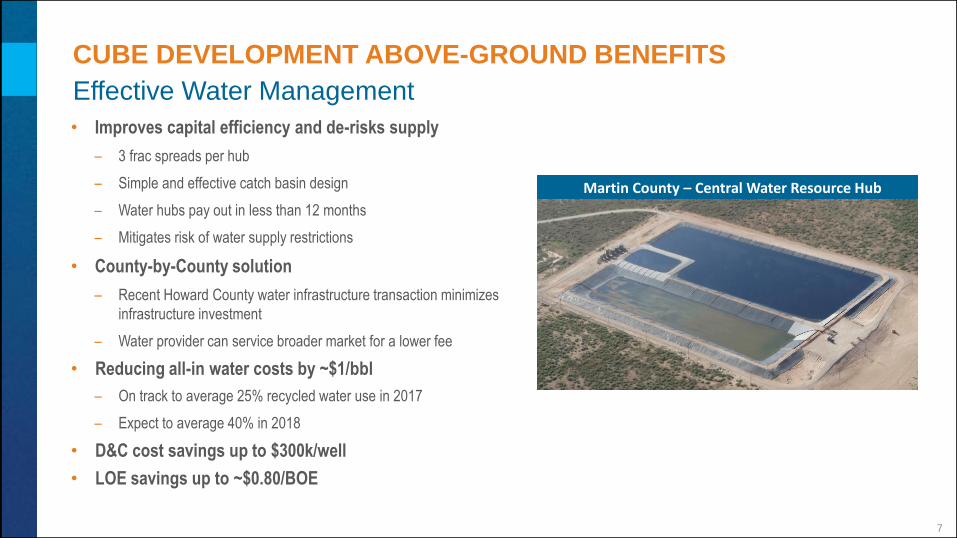

• Improves capital efficiency and de-risks supply

– 3 frac spreads per hub

– Simple and effective catch basin design

– Water hubs pay out in less than 12 months

– Mitigates risk of water supply restrictions

• County-by-County solution

– Recent Howard County water infrastructure transaction minimizes

infrastructure investment

– Water provider can service broader market for a lower fee

• Reducing all-in water costs by ~$1/bbl

– On track to average 25% recycled water use in 2017

– Expect to average 40% in 2018

• D&C cost savings up to $300k/well

• LOE savings up to ~$0.80/BOE

CUBE DEVELOPMENT ABOVE-GROUND BENEFITS

Effective Water Management

Martin County – Central Water Resource Hub

8

INNOVATION SUCCESS

Identifying Optimal Completion Design and Geometry

• Applying advanced completions to high-

density, stacked development

• Key principles:

– Tight cluster spacing and optimal hydraulics

maximize fracture surface area

– Clean, non-guar based fluids lead to better

fracture conductivity

– Fine grained proppant maximizes fracture

complexity

• Improved recovery from stacked pay reservoir

– Effective draw-down within cube

• Continued evolution and data-driven refinement

9

CUBE DEVELOPMENT RESULTS

• Accelerated learning

– Each pad producing stronger wells

– Abbie Laine outperforming RAB Davidson Phase 1 by 22% after

180 days

– RAB Davidson 2 outperforming RAB Davidson Phase 1 by 28%

after 170 days

• 45 ECA cube wells on production

– Abbie Laine and RAB Davidson Phase 2 continue to lead industry

– RAB Davidson Phase 1 among the best results

– 20 additional cube wells scheduled to be on production early Q4

• Industry dataset is all wells at >10 total wells per

section

– ~930 wells, 17 operators, 7 counties

Boosting Permian Productivity

*Well results normalized to 7500' lateral

Large Scale Development Performance Comparison

Abbie Laine RAB Davidson Phase 1

RAB Davidson Phase 2Peer Large Pads

ECA leading performance in

large scale development

0

20

40

60

80

100

120

140

0 30 60 90 120 150 180 210 240 270

Ave

rag

e C

um

ula

tive

Pro

du

cti

on

/we

ll (

MB

OE

)*

Days

10

0

25

50

75

Peer 1 Peer 2 ECA Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 Peer 12 Peer 13 Peer 14 Peer 15 Peer 16

Oil P

rod

ucti

on

IP

180/1

,000ft

(b

bls

/d)

WELL PRODUCTIVITY

Encana Wells Outpacing Peer Results

Data sourced from IHS, includes Midland Basin data from 2014 onward. Peers include APA, AREX, CPE, CVX, CXO, EGN, END, EPE, FANG, LPI, OXY, PXD, QEP, RSPP, SM and XOM

Producers with high density stack development

11

• D&C well costs held flat countering inflation

– 20% increase in service cost offset with efficiencies

– Performing amongst the top operators on days and cost

– Managing shallow flow zones with 3 string design

• 52% reduction in drilling days

– Limiter approach to maximize footage per day

– High performance water based mud

– Advanced survey tools and mud motors

PERMIAN CAPITAL EFFICIENCY

Leading Operator

Normalized D&C Cost/1,000’ vs Peers**

Drilling Days vs Depth

*Normalized to 7,500’. **Data sourced from latest peer IR presentations. Peers include APA, CPE, FANG, LPI, OXY, PE, PXD, QEP, and SM

0

5,000

10,000

15,000

20,000

0 5 10 15 20 25 30

Measu

red

Dep

th (

ft)

Days

2014 Average

2015 Average

2016 Average

2017 Average YTD

Pacesetter

0.0

0.2

0.4

0.6

0.8

1.0

Peer 1 ECA Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9

MM

$/1

000’

12

0

25

50

75

100

0 30 60 90

Cu

mu

lati

ve P

rod

ucti

on

(M

BO

E)

Producing Days

Advanced Completion Pad Average

Pre-2017 Wells

2017 Wells

2017 UPDATED Type Curve

2017 ORIGINAL Type Curve

WOLFCAMP

Midland/Upton County

Midland/Upton WCA/WCB Type Curve

IP180 = 800 BOE/d

EUR = 1,100 MBOE

D&C = $5.6 MM (incl. advanced completions scope)

Lateral Length = 7,500’

All metrics based on $50/bbl WTI, $3.00/MMBtu NYMEX

Type Well Metrics – ECA Net

Atax IRR (%) 35-47%

Operating Margin ($/BOE) $30

WCA

ECA Leases

WCBWCC

13

0

20

40

60

80

100

120

140

160

180

0 30 60 90 120 150 180

Cu

mm

ula

tive P

rod

ucti

on

(M

BO

E)

Producing Days

2017 Average Well 2017 UPDATED Type Curve

LOWER SPRABERRY

Martin, Midland/Upton, Glasscock

Martin Lower Spraberry Type Curve

IP180 = 650 BOE/d

EUR = 1,020 MBOE

D&C = $5.4 MM (incl. advanced completions scope)

Lateral Length = 7,500 ft

Type Well Metrics – ECA Net

Atax IRR (%) 39-54%

Operating Margin ($/BOE) $30

All metrics based on $50/bbl WTI, $3.00/MMBtu NYMEX

14

EXPANDING MARGINS

Reducing Operating Costs

• Improving efficiencies

– Company-wide effort

– Accountability at the operator level

• Working smarter

– >80% of produced water on pipe

– >70% of production on remote monitoring and control

• Negotiating the best price

~30%Improvement in

operating costs

Permian Direct Operating Cost Reductions

$/BOE

$0

$2

$4

$6

$8

$10

$12

2015 2016 2017F

15

Permian

MIDSTREAM AND MARKETING OVERVIEW

Gathering system links production to

pipeline hubs

Permian

• Majority of oil production gathered via

pipeline with access to multiple physical

markets

• Firm gas gathering and NGL processing

with access to Waha and Mt. Bellvieu

markets

• Secured firm, low-cost pipeline capacity

to Gulf Coast refining/export markets

(Enterprise Echo Pipeline 2018)

• No take or pay commitments

Colorado

City

Midland

Crane

Pipelines connect to

Cushing and Gulf Coast

Permian: Proximity to market and environment

of responsive infrastructure development

Secured capacity on Enterprise (Echo

Pipeline) adds market diversity and reduces physical risk

(2018)

16

PERMIAN

5 Year Growth Profile

-

40

80

120

160

200

240

2017F 2018F 2019F 2020F 2021F 2022FM

BO

E/d

• >50% of Encana’s capital directed to the

Permian in 2018

• Permian production expected to grow 3x

‒ 5 year CAGR 25%

• Quality inventory with scale

• No infrastructure or midstream limitations

• Minimal vertical program

Five Year Production Profile