perspectives on retail and supply chain trends in asia services limited- retail and... ·...

TRANSCRIPT

Perspectives on retail and supply chain trends in AsiaMay 2016

Fred Lemoine-Weave Services Limited

2

$10 trillion USD

by 2018

3

Asia pacific region is set to contribute to the highest retail income globally …

Source: pwchk.com.hk/webmedia/doc/635593364676310538_rc_outlook_201516.pdf

6 6.3 6.4 6.8 7.6 8.4 9.3 10.3

0

5

10

15

20

25Asia & Australasia Latin America Middle East , Nth Africa North America Western Europe World

2011 2012 2013 2014 2015 2016 2017 2018

Global retail sales by major geographies

USD-Trillions

4

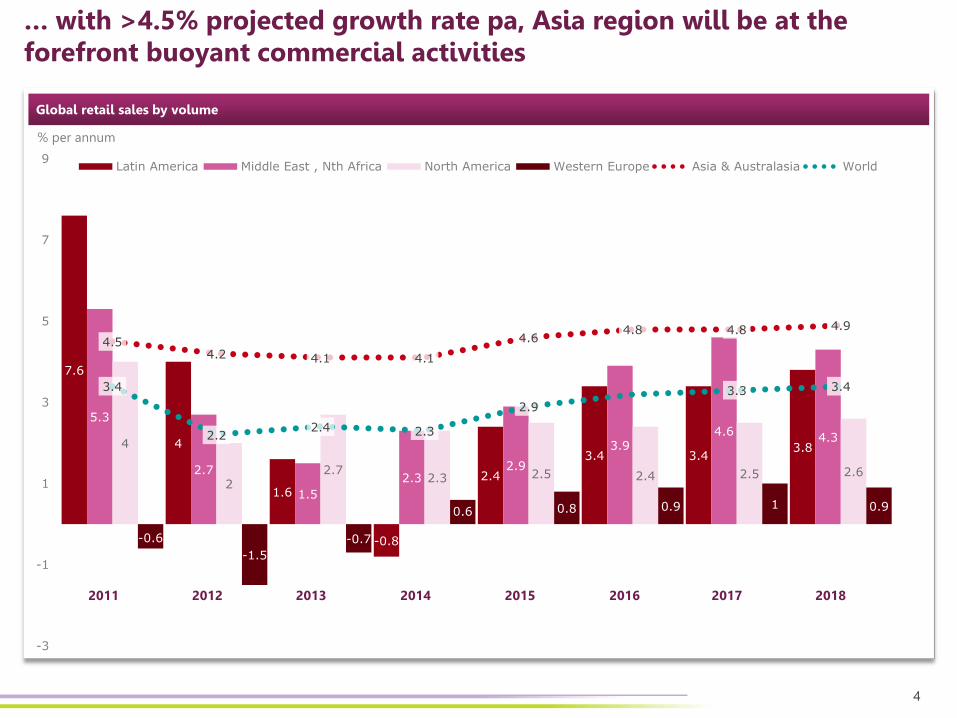

% per annum

7.6

4

1.6

-0.8

2.4

3.4 3.43.8

5.3

2.7

1.5

2.32.9

3.94.6

4.34

22.7

2.3 2.5 2.4 2.5 2.6

-0.6

-1.5

-0.7

0.6 0.8 0.9 1 0.9

4.54.2 4.1 4.1

4.64.8 4.8 4.9

3.4

2.22.4 2.3

2.9

3.3 3.4

-3

-1

1

3

5

7

9Latin America Middle East , Nth Africa North America Western Europe Asia & Australasia World

2011 2012 2013 2014 2015 2016 2017 2018

… with >4.5% projected growth rate pa, Asia region will be at the forefront buoyant commercial activities

Global retail sales by volume

5

4 major consumer-led trends are transforming the industry and supply chain strategies

Illustrations Major consumer-led trends

• Fast-fashion pushes a greater need for value-for-money goods delivered in record times

• Emerging manufacturing markets have flourishing consumer market of their own e.g. CN-4CN, India-4-India

• O2O is removing all physical barriers of the shopping experience

• Consumer behaviors are characterized by viral trends often set within virtual communities

6

3 emerging trends are dominating the boardrooms

“Low hanging

fruits” offered by

classic

procurement

strategies are fast

running out |of

steam

0 20 40 60

Reducing operating costs

Reducing overall inventory levels

Improving the quality of products or services

Improving customer service

Getting products or services to market faster

Reducing capital costs

Reducing risk

Reducing carbon footprint/creating greener supply chain

% of respondents, n=639

Challenges ahead for supply chains-Industry survey

-21

-18

+4

+15

+13

-7

+2

+13

Last 3 years Next 5 years New trends

Source: mckinsey.com/business-functions/operations/our-insights/the-challenges-ahead-for-supply-chains-mckinsey-global-survey-results

7

Cost optimization

Speed to market

Connected devises

Social Corporate responsibilities

Supply chain strategy-core pillars

As a result, CEO/COO should consider 4 major strategic pillars to support their retail and manufacturing play

8

UK

US

France

Germany

Italy

Japan

Indonesia

Brazil Mexico

Nicaragua

Ethiopia Vietnam

China

0

20

40

60

80

100

120

0 5 10 15 20 25

Labo

rpr

oduc

tivity

Capital intensity

2013 cross country productivity analysis – World Bank

Thousand USD/worker (2015 Exchange Rate)

Asia is lagging behind in terms of relative productivity

Source: World Bank Data, Weave analysis

9

The soft goods industry has been dormant in the past few years and new trends are now emerging

Brands and manufacturers are stuck in a chicken-and-egg situation New trends are emerging

• Industry is suffering from lack of investment in lean initiatives and machinery

• Large MNC’s behaving like SME’s with shortermism and lack of strategic transformation mindset

• SME’s are lacking capabilities to drive fundamental change within their organizations

• Retailers/brands are deepening their production capabilities

• Industry 4.0 is fuelling investments and new manufacturing models are emerging

• SCM collaboration frameworkbecome very relevant to both retailers and manufacturers

10

23%

41%

52%

-8.5%

Brands are fast growing their manufacturing capabilities to bridge gaps current players cannot fill

Own factories External suppliers Hybrid model

• Manufacturing best practice

• Product-specific expertise

• Capacity flexibility

• Industry-specific expertise

Combined benefits

• Cutting

• Sewing

• Finishing

• Defects

VF obtained tangible benefits on it’s Third Way strategy

1st level benefits 2nd level benefits

Third WaySecond WayFirst Way

Source: Weave analysis

11

Supply chain strategy-core pillars

4 pillars should be at the heart of today’s retail supply chain strategies

Cost optimization

Speed to market

Connected devises

Social Corporate responsibilities

12

0

200

400

600

800

1000

1200

1400

1600

TimeTimeTime

Fashion-driven products fell short (25%) of stock within the season start

Sales units

Potential sales Actual salesPotential Sales can be captured

End of fashion season

Start of fashion season Replenishment

Impacts:

Sales Index*

*Sales Index represents the relative sales amount

0.100.25

1.35

1

Actualsales

Potentialsales canbe captured

Potentialsales cannotbe captured

Total Potential

25%

20-30% sales opportunity by reducing out of stocks

Source: Client example

13

100% 12%

35%

25%

10%

14%

4%

0

20

40

60

80

100

Causes of OOS Store Ordering StoreForecasting

Store Stocking Warehousing PlanningManagement

Others

72% of Out-Of-Stock can be linked to replenishment practices

Linked to replenishment practices

Source: http://itsoutofstock.com/wp-content/uploads/2013/04/GMA_2002_-Worldwide_OOS_Study.pdf

Root cause of Out-Of-Stock (OOS)

Percentage %

14

Out-of-stock root causes “Read and React” model allows the gain of speed through 3 key levers

“Read and React” programs mitigate out of stock issues

• Infrequent replenishments

• Short supply of raw materials from suppliers

• Production issues

Buy Smart!• Gather POS data • Formulate demand forecast • Evaluate risk

Engage with suppliers!

• Develop collaboration model with suppliers

Start planning from materials!

• Develop Time & Action calendar with reorder timeline

• Low forecast accuracy

• Long replenishment leadtime

• Low forecast accuracy

• Long replenishment leadtime

Focusing on ordering POSDCTier 1Tier 2

Planning

15

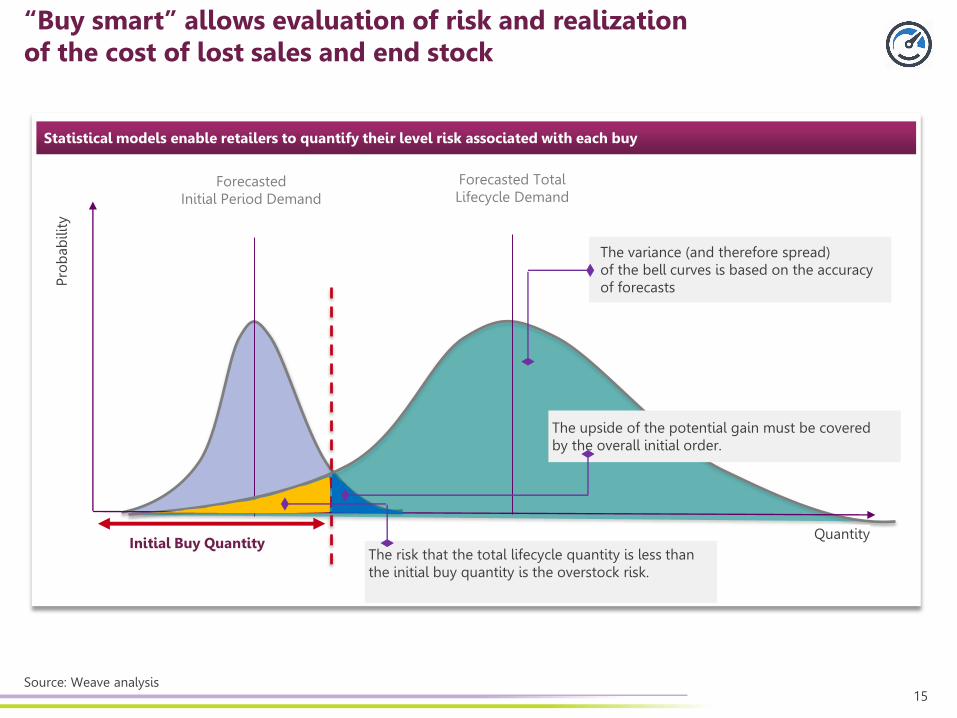

Forecasted Initial Period Demand

Forecasted Total Lifecycle Demand

“Buy smart” allows evaluation of risk and realization of the cost of lost sales and end stock

Statistical models enable retailers to quantify their level risk associated with each buy

Prob

abili

ty

QuantityInitial Buy Quantity

The variance (and therefore spread) of the bell curves is based on the accuracy of forecasts

The upside of the potential gain must be covered by the overall initial order.

The risk that the total lifecycle quantity is less than the initial buy quantity is the overstock risk.

Source: Weave analysis

16

Business are developing disruptive technologies to capture emerging fashions trends

WGSN, Edited, Stylumia, SnapFashion, ASAP54 & Thread

Trend forecasting and anticipatory analytics Speed factories: Glocal & Robotized

• “Robots” deployed online scanning publically available information

• In-street mass-photo shooting by country

• Trend analytics drawn at 2 years horizon

• 1st Speedfactory built in Germany, closer to geographical markets

• >90% robotized and emergence of mass-usage of 3D printing

• Configured to support high customization trends and “batch size 1” model

Source: Weave analysis, www.adidas-group.com/en/magazine/stories/specialty/adidas-future-manufacturing/

17

Supply chain strategy-core pillars

4 pillars should be at the heart of today’s retail supply chain strategies

Cost optimization

Speed to market

Connected devises

Social Corporate responsibilities

18

… by 2020, 38 billionsdevises will be part of our day-

to-day life

In 2015 connected devises

x2 the size of human population …

19

Consumer will demand it soon, but Wall Street wants it now!

• Development of connected cars

• Acquisition of Misfit

• Development of smart home and smart body apps

-1000 4000 9000 14000 19000 24000

2013 2014 2015 2020

Genericbusinesses

VerticallyIntegrated

Consumer

Automotive

High number of initiatives launched in recent years

42% CARG to 2020 projection supports investments from industrialists

CARG

53%

39%

82%

29%

Source: Weave analysis, Gartner November 2014

20

Fundamental changes will transform the industry

“Do-or-Die” moment for manufacturers

Revolution for replenishment specialists

• Increased data points for predetermining demand trends i.e. anticipatory optimization

• New channels available conduct demand shaping

• Greater vertical integration of data through the use of smart tags and smart appliances

• New procurement strategies

• Transformation of assembly and production line arrangements

• Added complexity in managing product life cycle

21

Connected devises will create an eco-system of integrated data that will transform supply chains

Benefits

Examples

New features

Raw materialsManufacturing

Assembly Finished goodsIn-boundLogistics

Last Mile logisticsShops/ platforms Natural environment

• Smart tracking-RFID

• Smart tagging e.g. disposable watermarking

• Cloud logistics • Online-off-line • On-demand delivery e.g. crowd based parcel delivery

• Traceability of RM and components

• Connected devises

• Part of day to day activities from home, work, gym, travels

• Enable nimble reaction to crisis

• Safeguard brand image

• Real time calculation of WIP and productivity

• Increased traceability beyond POS

• Increased predictability e.gexpiration date

• Scalability of IT logistic services via one integrated platform from consolidation to billing

• Offer modular services e.g. pay per use

• Reduction of inventory in store

• Increase range to customers

• Improved demand shaping

• Reduction of assets

• Reach to low density locations

• C2C consumer experience

• Anticipatory optimization

• Increase ability to perform demand shaping

• Data available to manufactures

22

Supply chain strategy-core pillars

4 pillars should be at the heart of today’s retail supply chain strategies

Cost optimization

Speed to market

Connected devises

Social Corporate responsibilities

23

Social Corporate Responsibility cannot be ignored

24

Those who ignore it, are impacting their market reach and sales potential

“We recognize that the frequent use of short term, fixed duration contracts, in the Cambodian garment industry constitutes an illegal breach of workers’ rights”

“The outrage over the disaster threatened to tarnish permanently the names of top High Street firms and spurred the drive among many to cut their dependence on Third World factories and bring manufacturing back to Britain.

25

Case study of Patagonia shows industry best practice

https://www.youtube.com/watch?v=WexueycQgmY

Best practices observed at PatagoniaVideo- case study of Patagonia

• Independent and frequent audits i.e. internal or/and external parties

• 4 decision factors with equal veto rights i.e. sourcing, quality, social and environmental

• Cover the End-2-End supply chain with robust traceability tools

• Maintain database of key metrics and drive continuous improvement programs

26

Root causes

Solutions

3 major roadblocks to embedding SCR into your supply chain strategy

Liability of investment Un-unified world standards

Roles and Responsibilities

• Manufacturers are reluctant to invest without long term commitment

• Retailers cannotoften translate investments into tangible ROI

• Multiple initiatives led by large soft goods organization and global association

• Retail organization often do not know how to integratethis function in a way that drives impact

• Integrate to your vendor balance score card e.g. Nike

• PE firms founding SCR friendly factories

• Align to the highest standards e.g. many retailers see the Higgs index as best in class

• Bring SCR at the board level

• Integrate to your supply chain strategy

27

Supply chain strategy-core pillars

Managing the integration of these 4 pillars is essential to supporting a retail growth strategy in 2016 and beyond

Cost optimization

Speed to market

Connected devises

Social Corporate responsibilities

28

• Resurgence of M&A: Investments in manufacturing across APAC by PE firms and investment founds

• 4CP for MNC’s: Large corporation behaving like SME’s slow down change management

• Technologies and analytics dominate the conversations. More mathematically based decision making processes and tools are yet to be embedded

Cost optimization

Speed to market

Connected devises

Social Corporate responsibilities

So what does that mean for the service industry?

29

Fast Fashion demystified April 16 Future of manufacturing in Vietnam March 2016

Innovation in the apparel industryMarch16

Future of manufacturing in ChinaFebruary 2016

Tap into the Weave’s library for more information