peter pénzeš pension funds regulatory department national bank of slovakia

DESCRIPTION

Peter Pénzeš Pension Funds Regulatory Department National Bank of Slovakia. Private pension system in Slovakia. CEIOPS OPC Meeting, Frankfurt am Main, 7 September 2007. Slovakia at a glance. Structure of the presentation. Pension reform 2004 – 2005 1 st pillar overview - PowerPoint PPT PresentationTRANSCRIPT

Peter PénzešPension Funds Regulatory Department

National Bank of Slovakia

Private pension system in Slovakia

CEIOPS OPC Meeting, Frankfurt am Main,

7 September 2007

2

Slovakia at a glanceEU Member: May 2004

Population: 5 393 637 (2006)

Working population:

2 301 400 (2006)i.e. 43 % of population

Retired population:

960 989 (2006)i.e. 17,8 % of population

Financial market supervisor and regulator:

National Bank of Slovakia (integrated authority)

Structure of the presentation

Pension reform 2004 – 2005 1st pillar

overview

2nd pillar and 3rd pillar overview contributions investments benefits

Final remarks

Pension reform 2004 – 2005

Source: OECD

The Slovak population pyramid

5

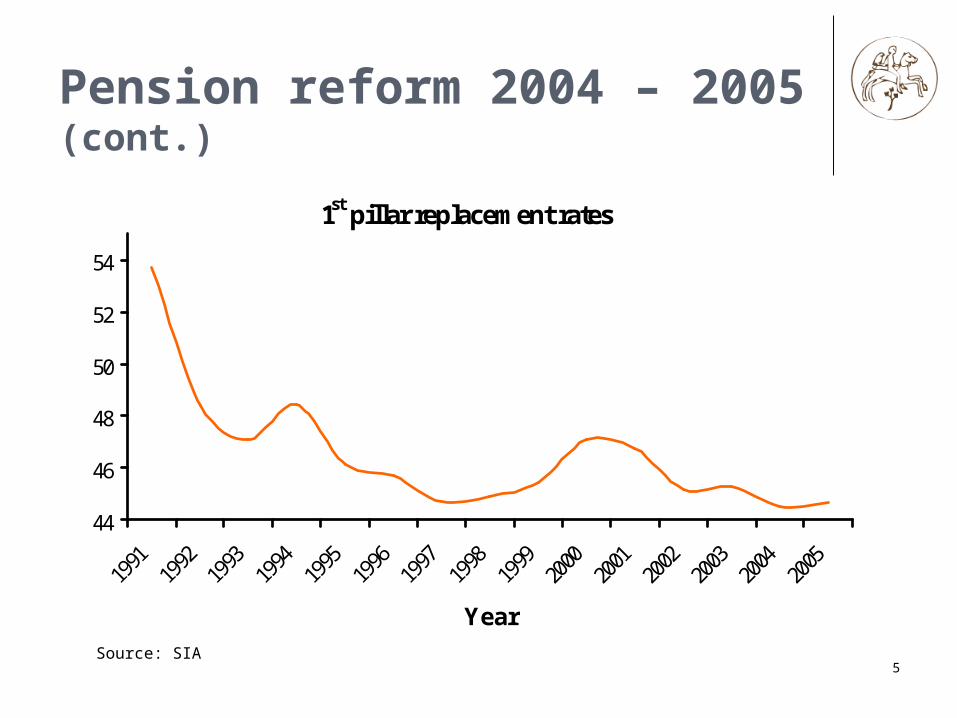

Pension reform 2004 – 2005 (cont.)

1st pillar replacement rates

44

46

48

50

52

54

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Year

Source: SIA

6

Changes in the 1st pillar (higher retirement age)

Introduction of the 2nd pillar

Transformation of the 3rd pillar

Pension reform 2004 – 2005 (cont.)

7

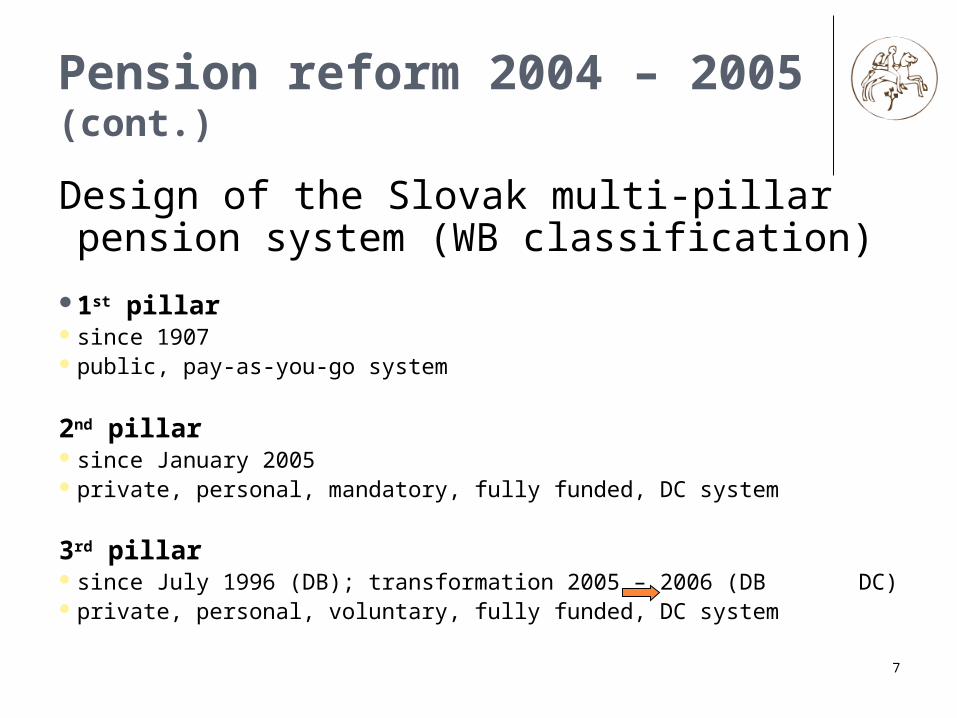

Design of the Slovak multi-pillar pension system (WB classification)

1st pillarsince 1907public, pay-as-you-go system

2nd pillar since January 2005private, personal, mandatory, fully funded, DC system

3rd pillar since July 1996 (DB); transformation 2005 – 2006 (DB DC)private, personal, voluntary, fully funded, DC system

Pension reform 2004 – 2005 (cont.)

8

Legal framework of the Slovak pension system

1st pillarSocial Insurance Act (No. 461/2003 Coll.)

2nd pillarOld-Age Pension Savings Act (No. 43/2004 Coll.)

3rd pillarSupplementary Pension Savings Act (No. 650/2004 Coll.)

Pension reform 2004 – 2005 (cont.)

9

1st pillar(since 1907)

10

administered by the state owned institution - the Social Insurance Agency (SIA)

supervised by the Ministry of Labour automatic enrolment of all workers and mandatory

participation for self-employed with income over a certain level prescribed by law ; anyone can join voluntary

contributions: 14% employer, 4% employee assets are deposited on the 0% interest rate account in the

State Treasury benefits: old-age pensions, early old-age pensions,

survivors’ benefits; automatic indexation of benefits on yearly basis

current replacement rate: 44,65%

1st pillar – overview

11

2nd pillar(since 2005)

12

separation of 2nd pillar institution’s assets from assets of its members (pension fund)

member’s contributions go to its individual pension account

account balance is inheritable

January 2005 – June 2006 opened for all workers and self-employed individuals

since January 2005 automatic enrolment (default option – conservative fund) for new labour market entrants

2nd pillar – overview

2nd pillar – overview (cont.)

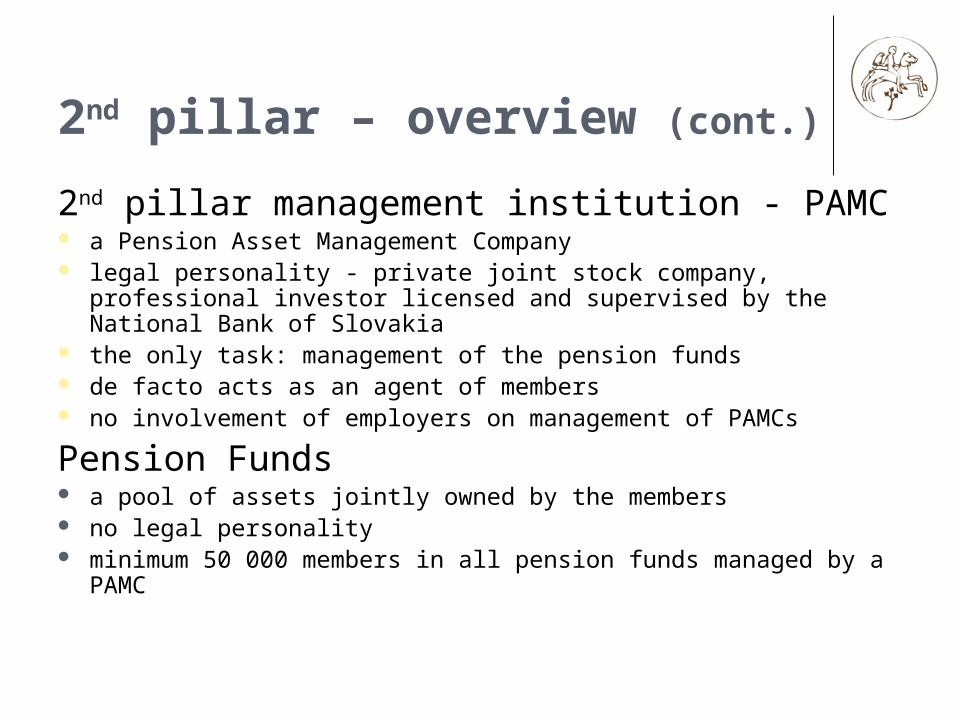

2nd pillar management institution - PAMC a Pension Asset Management Company legal personality - private joint stock company, professional

investor licensed and supervised by the National Bank of Slovakia

the only task: management of the pension funds de facto acts as an agent of members no involvement of employers on management of PAMCs

Pension Funds a pool of assets jointly owned by the members no legal personality minimum 50 000 members in all pension funds managed by

a PAMC

14

6 PAMCs

18 pension funds

1 545 916 members (as of June 2007)

42 bln. Sk / € 1,2 bln. of assets (as of June 2007) (approx. 2,4% of GDP)

2nd pillar – overview (cont.)

15

2nd pillar – overview (cont.)

Allianz – Slovenská DSS, a.s.

Aegon, d. s. s., a. s.

Axa d. s. s., a. s.

ČSOB d. s. s., a. s.

ING d.s.s., a. s.

VÚB Generali d.s.s., a. s.

2 takeovers in 2005 - 2006:Prvá dôchodková sporiteľňa, d. s. s., a. s. AllianzSympatia – Pohoda, d. s. s., a. s. ING

PAMCs:

16

2nd pillar – overview (cont.)

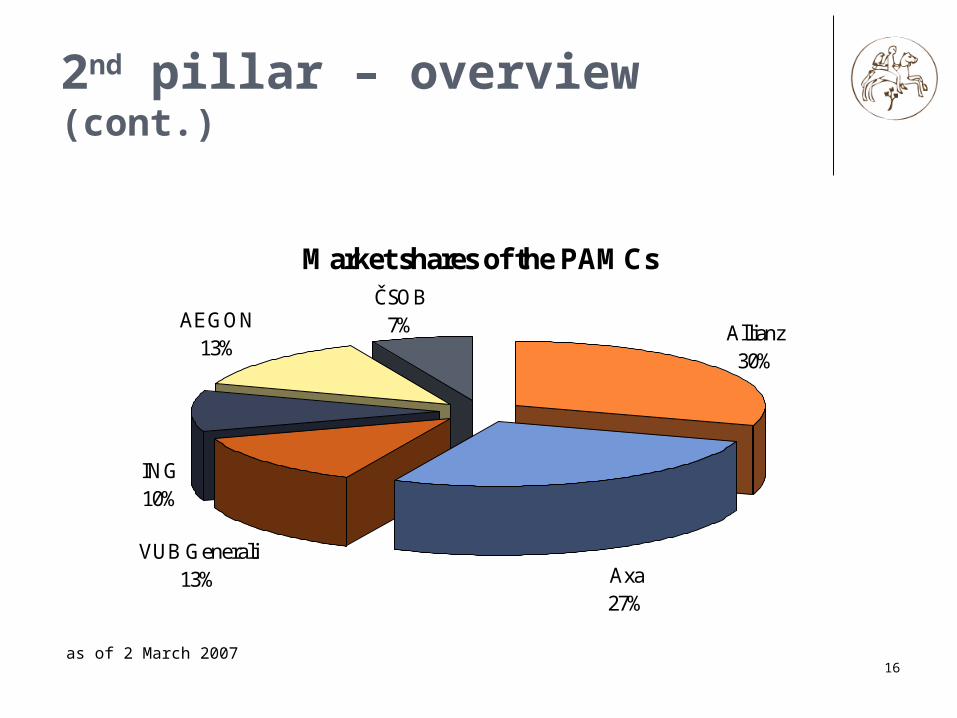

Market shares of the PAMCs

Allianz30%

Axa27%

VUB Generali13%

ING10%

AEGON13%

ČSOB7%

as of 2 March 2007

17

Each PAMC is obliged to establish 3 types of pension funds with different risk-return relationship:

conservative pension fund

balanced pension fund

growth pension fund

2nd pillar – overview (cont.)

18

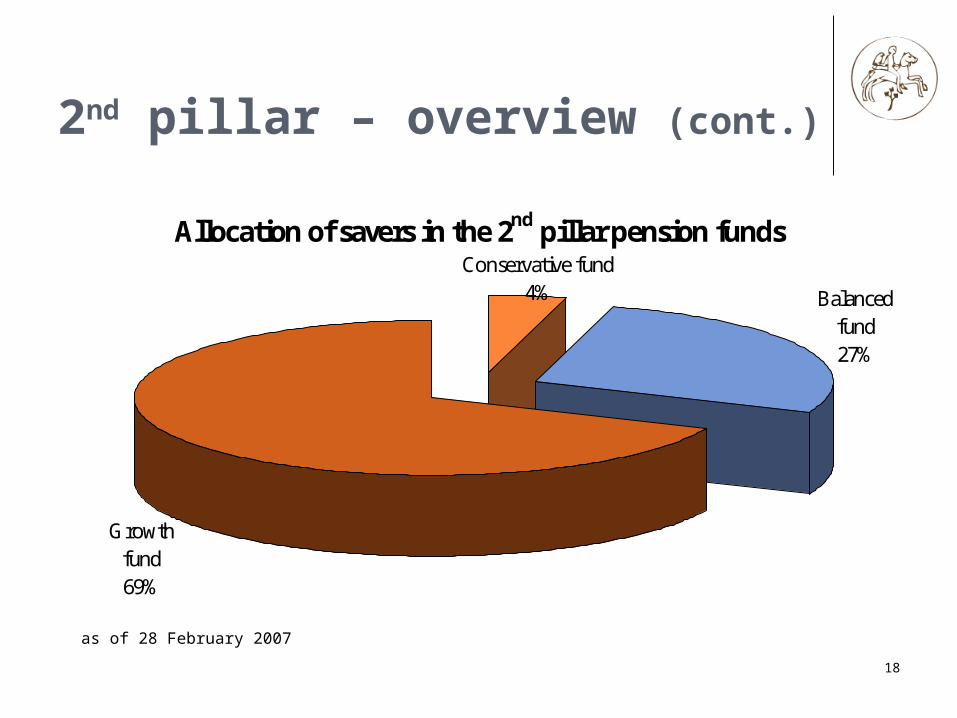

Allocation of savers in the 2nd pillar pension fundsConservative fund

4% Balanced fund27%

Growth fund69%

2nd pillar – overview (cont.)

as of 28 February 2007

2nd pillar – overview (cont.)

2nd pillar security mechanisms

Licensing Prior approvals (fit and proper requirements) Supervision by the NBS Prudent person rules Internal control External audit Depositary bank Risk management (from January 2008)

19

2nd pillar – overview (cont.)

Guarantees in the 2nd pillar

The Minimum Return Guarantee (MRG) obligation of a PAMC to pay from its own assets to the

assets of the pension fund in case of underperformance to avoid major discrepancies among returns of pension

funds

Social Insurance Agency in case of fraud

20

21

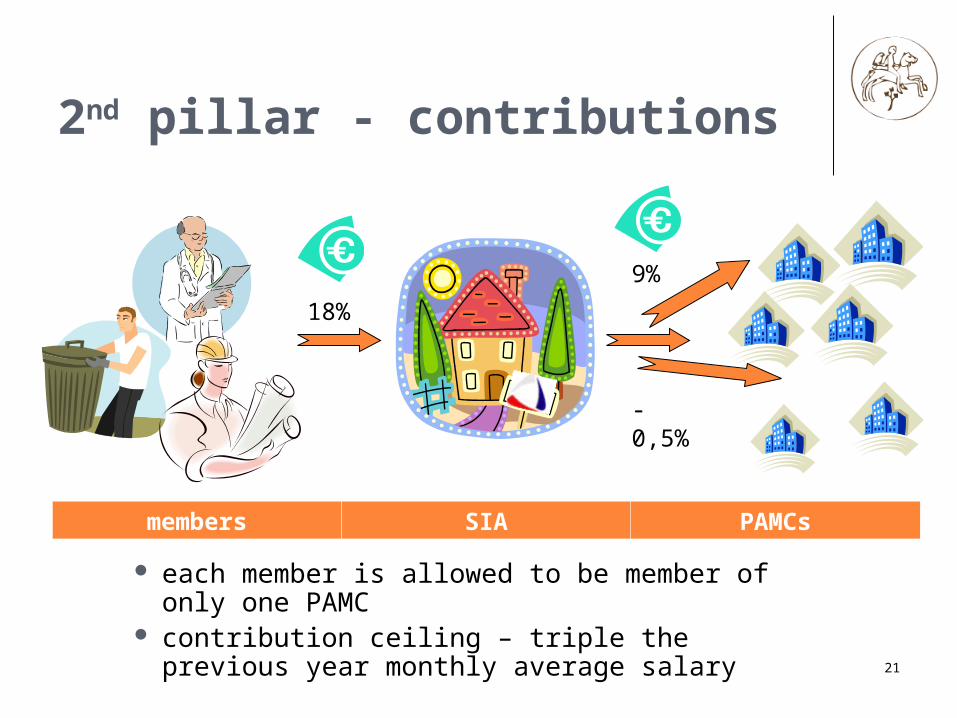

2nd pillar - contributions

each member is allowed to be member of only one PAMC

contribution ceiling – triple the previous year monthly average salary

18%

9%

-0,5%

members SIA PAMCs

22

2nd pillar – contributions (cont.)

Proportion of the 2nd pillar assets to the GDP

0

4

8

12

16

20

24

2005

2007

2009

2011

2013

2015

2017

Year

% G

DP

Source: NBS, own calculations

23

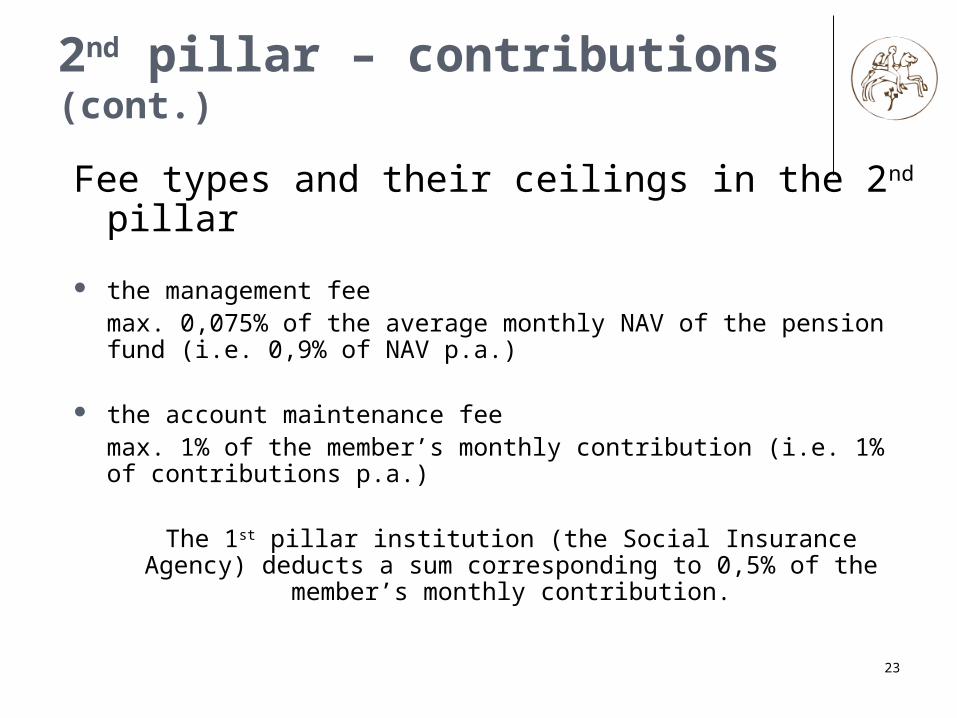

2nd pillar – contributions (cont.)

Fee types and their ceilings in the 2nd pillar

the management feemax. 0,075% of the average monthly NAV of the pension fund (i.e. 0,9% of NAV p.a.)

the account maintenance fee max. 1% of the member’s monthly contribution (i.e. 1% of contributions p.a.)

The 1st pillar institution (the Social Insurance Agency) deducts a sum corresponding to 0,5% of the member’s

monthly contribution.

2nd pillar - investments

Allocation of pension funds’ investments Bank deposits

Bonds Shares and mutual funds

Conservative funds

38% - 55% 38% - 62% 0%

Balanced funds 17% - 41% 21% - 68% 11% - 16%

Growth funds 18% - 43% 22% - 63% 14% - 20%

24

Problem: too conservativePossible solution: charging based on performance?as of 30 June 2007

2nd pillar - investments

25

2,00%

3,00%

4,00%

5,00%

Conservative funds Balanced funds Growth funds

Returns of the 2nd pillar pension funds

20062007

26

Investment limits quantitative qualitative

Basic investment limits conservative pension fund - only bonds and money market

instruments in portfolio balanced pension fund - bonds and money market

instruments, max. 50% of equity in portfolio

growth pension fund - bonds and money market

instruments, max. 80% of equity in portfolio)

2nd pillar – investments (cont.)

27

Other investment limits

min. 30% of assets to be invested domestically derivatives allowed only for hedging purpose – problem:

sometimes hard to distinguish the purpose of the instrument

only indirect investment into real-estates allowed totally 17 investment limits, all stipulated in law

Problem: not very flexibleSolution: more qualitative investment rules, risk based

investment rules

2nd pillar – investments (cont.)

2nd pillar - benefits Programmed withdrawal + Life annuity Life annuity Survivors benefits (paid for the period of one year after the

members’ death)

Conditions for payment of the life annuity: min. 10 years of membership attainment of the retirement age

Programmed withdrawal paid by the PAMC Life annuity paid by an Insurance Company Survivors benefits paid by the PAMC/IC

28

29

3rd pillar(since 1996)

30

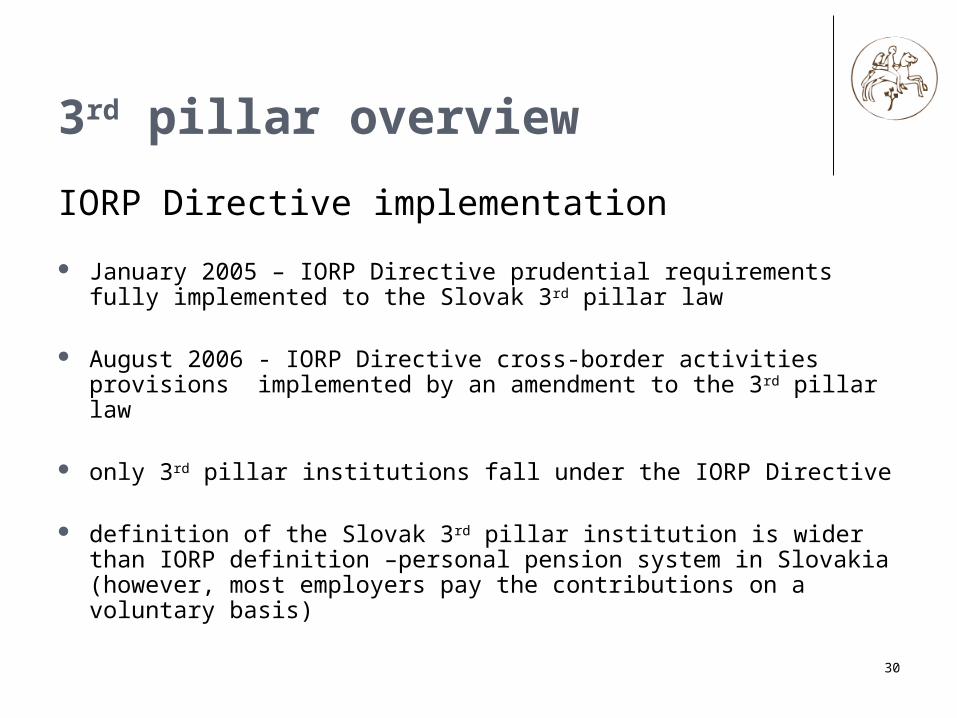

3rd pillar overview

IORP Directive implementation

January 2005 – IORP Directive prudential requirements fully implemented to the Slovak 3rd pillar law

August 2006 - IORP Directive cross-border activities provisions implemented by an amendment to the 3rd pillar law

only 3rd pillar institutions fall under the IORP Directive

definition of the Slovak 3rd pillar institution is wider than IORP definition –personal pension system in Slovakia (however, most employers pay the contributions on a voluntary basis)

31

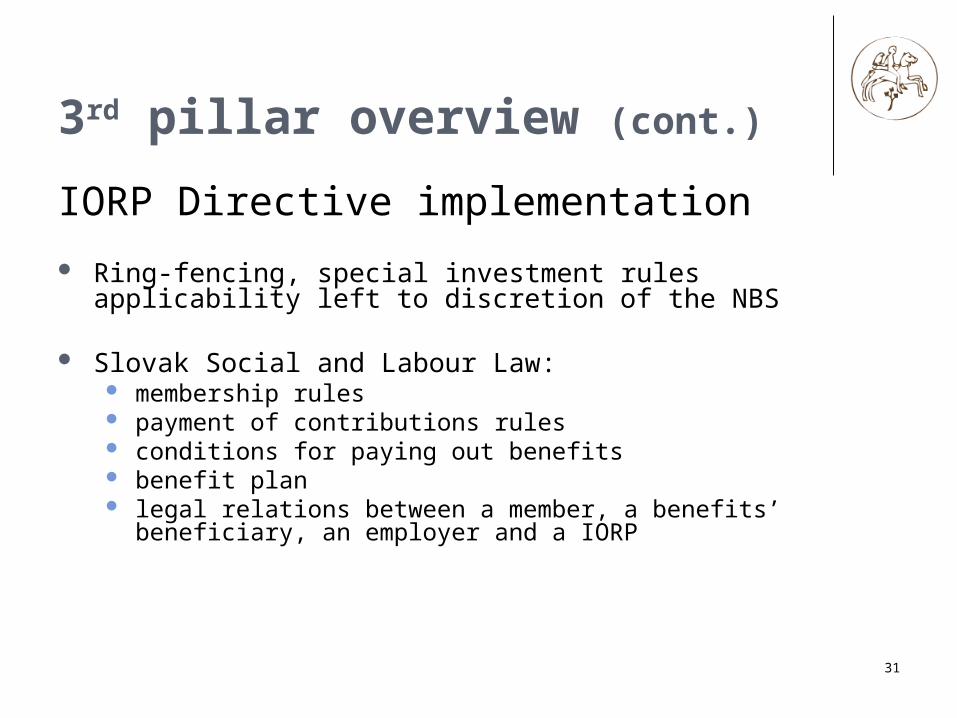

3rd pillar overview (cont.)

IORP Directive implementation

Ring-fencing, special investment rules applicability left to discretion of the NBS

Slovak Social and Labour Law: membership rules payment of contributions rules conditions for paying out benefits benefit plan legal relations between a member, a benefits’ beneficiary, an

employer and a IORP

32

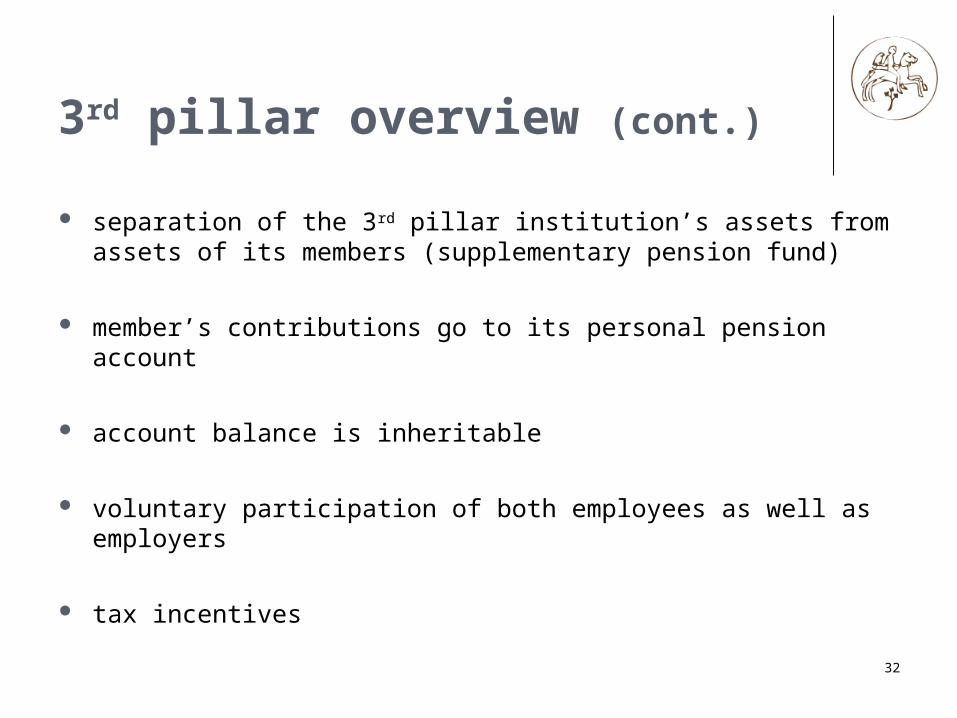

separation of the 3rd pillar institution’s assets from assets of its members (supplementary pension fund)

member’s contributions go to its personal pension account

account balance is inheritable

voluntary participation of both employees as well as employers

tax incentives

3rd pillar overview (cont.)

3rd pillar overview (cont.)

3rd pillar management institution - SPAMC a Supplementary Pension Asset Management Company legal personality - private joint stock company, professional

investor licensed and supervised by the National Bank of Slovakia

the same principles apply as in case of 2nd pillar PAMC

Supplementary Pension Funds the same principles as in the 2nd pillar except for minimum

number of members

34

5 SPAMCs

13 supplementary pension funds

716 383 members (as of December 2006)

21,5 bln. Sk / € 637 mil. of assets (as of December 2006) (approx. 1,3% of GDP)

3rd pillar overview (cont.)

35

3rd pillar – overview (cont.)

Aegon d. d. s., a. s.

Axa d. d. s., a. s.

DDS Tatra banky, a. s.

ING Tatry – Sympatia, d. d. s., a. s.

Stabilita, d. d. s., a. s.

SPAMCs:

36

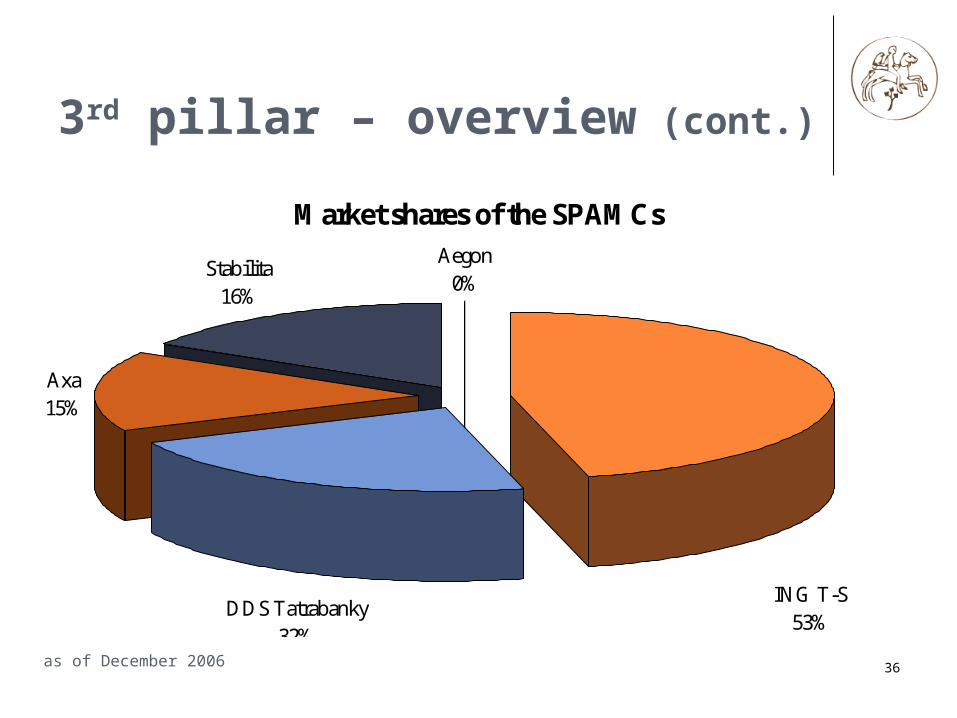

Market shares of the SPAMCs

Stabilita16%

Aegon0%

Axa15%

DDS Tatrabanky32%

ING T-S53%

3rd pillar – overview (cont.)

as of December 2006

3rd pillar – overview (cont.)

3rd pillar security mechanisms the same as in the 2nd pillar

Guarantees in the 3rd pillar no guarantees

37

38

The SPC is obliged to establish two types of funds:

at least one Contributory pension fund an investment strategy is entirely up to the 3rd pillar

institution; however, quite strict investments limits and one Paying-out pension fund

very strict investment limits (high liquidity) when a member asks for payment of benefits that are

paid by the SPAMC, the 3rd pillar institution is obliged to transfer member’s account balance from the Contributory pension fund to the Paying-out pension fund.

3rd pillar – overview (cont.)

39

3rd pillar - contributions

each individual is allowed to be member of several SPAMCs;

no contribution ceiling

members PAMCs

40

3rd pillar - contributions (cont.)

Fee types and their ceilings in the 3rd pillar

the management feemax. 3% a year of the average yearly NAV of the pension fund

the SPAMC switching fee max. 5% of the member’s account balance in the first five years after concluding a contract with the member and max 1% thereafter

the termination settlement feemax. 20% of the member’s account balance

3rd pillar - investments

41

Problem: too conservative, the same picture as in the 2nd pillarPossible solution: charging based on performance?as of 30 June 2007

Allocation of the supplementary pension funds’ investments

Bank deposits

BondsShares and

mutual funds

37,11% 56,23% 7%

42

Investment limits quantitative qualitative

Investment limits linked to those in the 2nd pillar with the few exceptions (no 30% limit on domestic investments, etc.)

Problem: too restrictive for the system with voluntary participation

Solution: more qualitative investment limits, risk based investment limits

3rd pillar – investments (cont.)

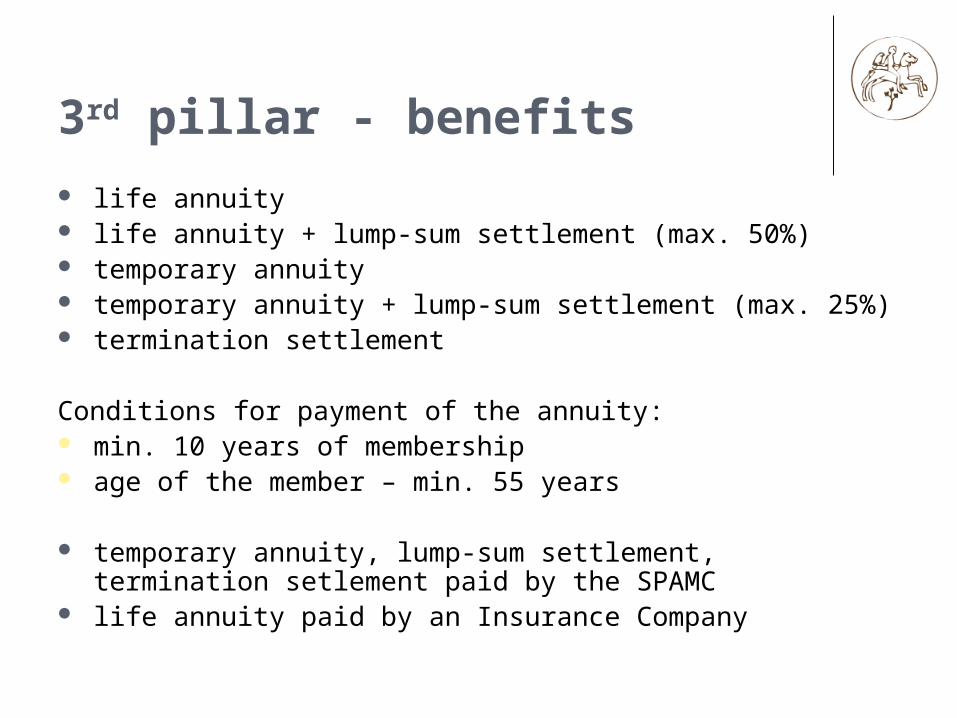

3rd pillar - benefits life annuity life annuity + lump-sum settlement (max. 50%) temporary annuity temporary annuity + lump-sum settlement (max. 25%) termination settlement

Conditions for payment of the annuity: min. 10 years of membership age of the member – min. 55 years

temporary annuity, lump-sum settlement, termination setlement paid by the SPAMC

life annuity paid by an Insurance Company

44

Final remarks

45

Final remarks

Tax issues

2nd pillar – ETE: contributions tax free investment returns taxed benefits tax free

3rd pillar – ETT: employee’s contributions tax deductible up to 12.000 Sk

a year, employers’ contributions tax deductible up to 6% of employees’ salary

investment returns taxed benefits taxed

46

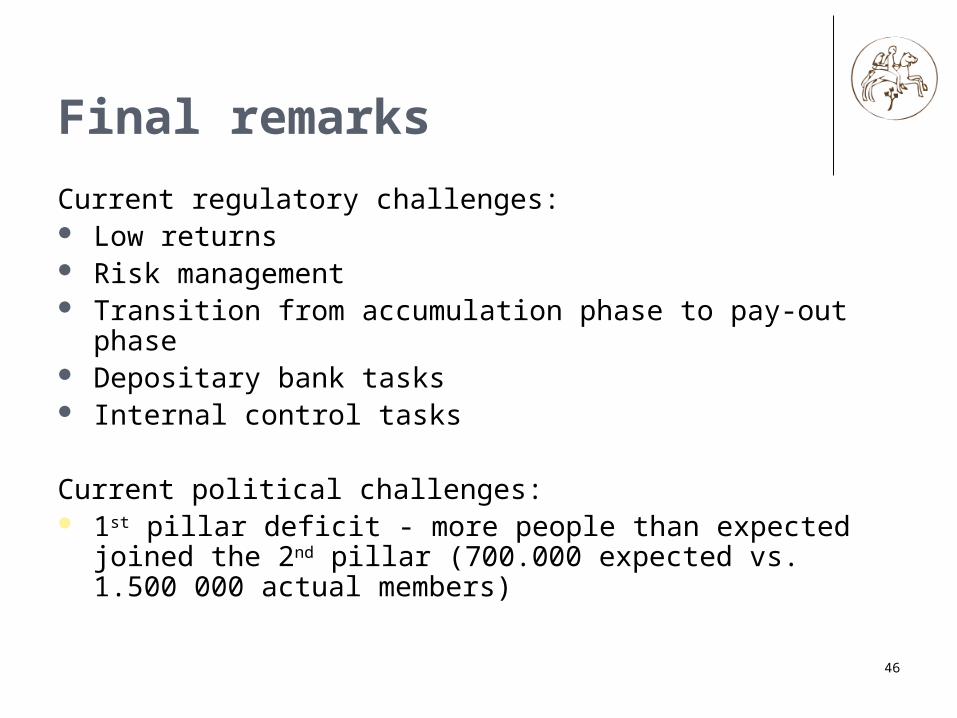

Final remarks

Current regulatory challenges: Low returns Risk management Transition from accumulation phase to pay-out phase Depositary bank tasks Internal control tasks

Current political challenges: 1st pillar deficit - more people than expected joined the

2nd pillar (700.000 expected vs. 1.500 000 actual members)