petrobras at glance - 2015

TRANSCRIPT

1

PETROBRAS

Update

May 2015

__

2 2

FORWARD-LOOKING STATEMENTS:

DISCLAIMER

The presentation may contain forward-looking statements about future events within the

meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of

the Securities Exchange Act of 1934, as amended, that are not based on historical facts

and are not assurances of future results. Such forward-looking statements merely reflect

the Company’s current views and estimates of future economic circumstances, industry

conditions, company performance and financial results. Such terms as "anticipate",

"believe", "expect", "forecast", "intend", "plan", "project", "seek", "should", along with

similar or analogous expressions, are used to identify such forward-looking statements.

Readers are cautioned that these statements are only projections and may differ

materially from actual future results or events. Readers are referred to the documents

filed by the Company with the SEC, specifically the Company’s most recent Annual

Report on Form 20-F, which identify important risk factors that could cause actual results

to differ from those contained in the forward-looking statements, including, among other

things, risks relating to general economic and business conditions, including crude oil and

other commodity prices, refining margins and prevailing exchange rates, uncertainties

inherent in making estimates of our oil and gas reserves including recently discovered oil

and gas reserves, international and Brazilian political, economic and social

developments, receipt of governmental approvals and licenses and our ability to obtain

financing.

We undertake no obligation to publicly update or revise any forward-looking

statements, whether as a result of new information or future events or for any

other reason. Figures for 2014 on are estimates or targets.

All forward-looking statements are expressly qualified in their entirety by this

cautionary statement, and you should not place reliance on any forward-looking

statement contained in this presentation.

NON-SEC COMPLIANT OIL AND GAS RESERVES:

CAUTIONARY STATEMENT FOR US INVESTORS

We present certain data in this presentation, such as oil and gas resources,

that we are not permitted to present in documents filed with the United States

Securities and Exchange Commission (SEC) under new Subpart 1200 to

Regulation S-K because such terms do not qualify as proved, probable or

possible reserves under Rule 4-10(a) of Regulation S-X.

DISCLAIMER

3 3

Competitive Advantages Uniquely positioned to integrate upstream and downstream operations

• Leader in deep-water production, with

access to abundant oil reserves

• New exploratory frontier, adjacent to

existing operations

• Dominant position in growing market, far

from other refining centers

• Balance and integration between

production, refining and demand

• Fully developed infrastructure for

processing and transfporting gas

• Integration accross full energy and

hydrocarbon chain in Brazil

Exploration & Production

Downstream

Gas & Power/ Biofuels/Petrochemicals

13

Abundant reserves

300 km away from

the market

4 4

New Systems Ensure Future Growth

1.937

3,2

4,2

2013 2014 2015 2016 2017 2018 2019 2020

2.034

Piloto Sapinhoá

(Cid. São Paulo)

Baúna

(Cid. Itajaí)

Piloto Lula NE

(Cid. Paraty)

Papa-Terra

(P-63)

Roncador III

(P-55)

Norte Pq. Baleias

(P-58)

Iracema Sul

(C. Mangaratiba)

Roncador IV

(P-62)

Sapinhoá Norte

(Cid. Ilhabela)

Papa-Terra

(P-61+TAD)

Itapu

Lula Alto

Lula Central

Júpiter Lula Sul

(P-66)

Búzios I

(P-74)

Lapa

Lula Norte

(P-67)

Búzios II

(P-75)

Lula Ext. Sul

e CO Sul de Lula

(P-68)

Lula Oeste

(P-69)

Búzios III

(P-76)

Tartaruga Verde e

Mestiça

Maromba I

Iara Horst

(P-70)

Búzios IV

(P-77)

Entorno de Iara

(P-73)

NE de Tupi

(P-72)

Iara NW

(P-71)

Sul Pq. Baleias

ES Águas

Profundas

Carcará

Espadarte III

SE Águas

Profundas I

Búzios V

Revitalização

Marlim I

SE Águas

Profundas II

Libra

Revitalização

Marlim II

Iracema Norte

(Cid. Itaguaí)

On Stream

On Location

Ordered

Under Bidding

+640kbpd +660kbpd +150kbpd +1000kbpd +900kbpd +1050kbpd Capacity added per year

3 MM bbl

Growth in 2015:

4.5% +/-1p.p.

Under Review

Growth in 2016:

2.8% +/-2p.p.

Libra EWT

5 5

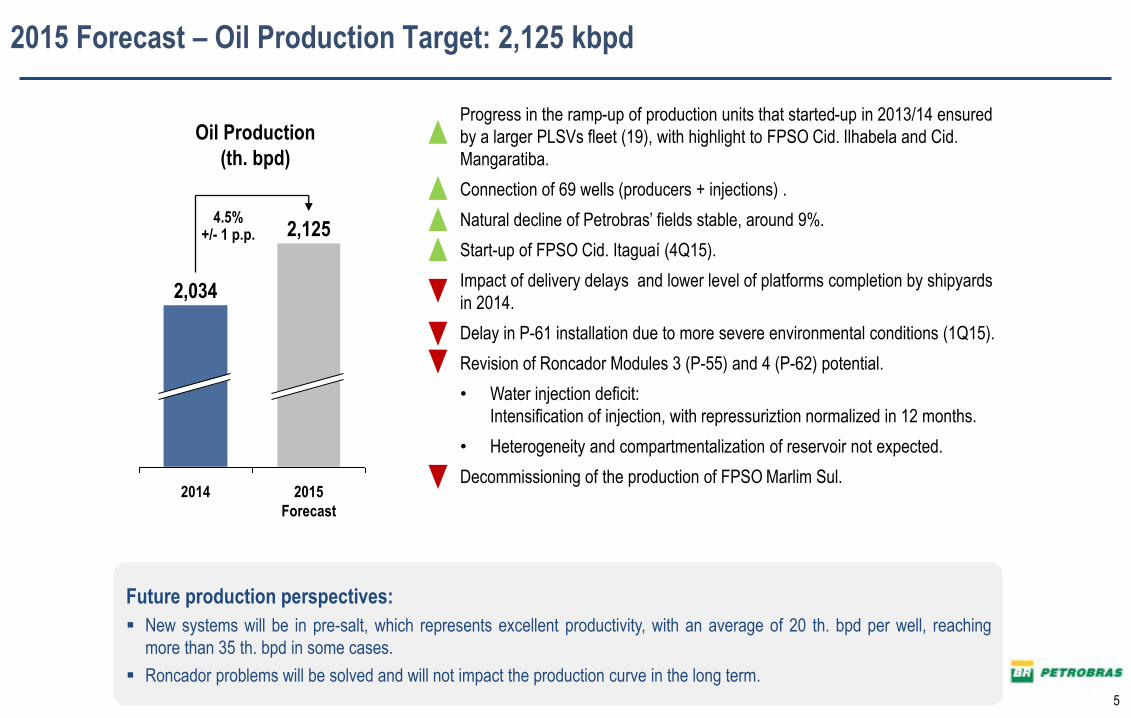

2015 Forecast – Oil Production Target: 2,125 kbpd

Future production perspectives:

New systems will be in pre-salt, which represents excellent productivity, with an average of 20 th. bpd per well, reaching

more than 35 th. bpd in some cases.

Roncador problems will be solved and will not impact the production curve in the long term.

Progress in the ramp-up of production units that started-up in 2013/14 ensured

by a larger PLSVs fleet (19), with highlight to FPSO Cid. Ilhabela and Cid.

Mangaratiba.

Connection of 69 wells (producers + injections) .

Natural decline of Petrobras’ fields stable, around 9%.

Start-up of FPSO Cid. Itaguaí (4Q15).

Impact of delivery delays and lower level of platforms completion by shipyards

in 2014.

Delay in P-61 installation due to more severe environmental conditions (1Q15).

Revision of Roncador Modules 3 (P-55) and 4 (P-62) potential.

• Water injection deficit:

Intensification of injection, with repressuriztion normalized in 12 months.

• Heterogeneity and compartmentalization of reservoir not expected.

Decommissioning of the production of FPSO Marlim Sul.

Oil Production

(th. bpd)

2015

Forecast

2,125

2014

2,034

4.5% +/- 1 p.p.

6 6

Oil and NGL Production in Brazil Petrobras Production in 2014 was 2,034 kpd, an increase of 103 kbpd over 2013

1.917 1.923 1.926

1.933

1.975

2.008

2.049

2.105 2.118 2.126 2.111

2.212 2.192

2.147

2.108

1.700

1.800

1.900

2.000

2.100

2.200

2.300

2.400

jan/

14

fev/

14

mar

/14

abr/

14

mai

/14

jun/

14

jul/1

4

ago/

14

set/1

4

out/1

4

nov/

14

dez/

14

jan/

15

fev/

15

mar

/15

2014: 2.034 mbpd (+5.3%)

1Q14: 1,922 2Q14: 1.972 3Q14: 2.090 4Q14: 2.150

kbpd

1Q15: 2.151

2015

Main factors that contributed to production growth:

Ramp up of 9 installed ( 2013 and 2014)

New 61 production wells connected in 2014

High productivity of Santos Basin pre-salt wells

7 7

Pre-Salt Province Production Highlights

8 8

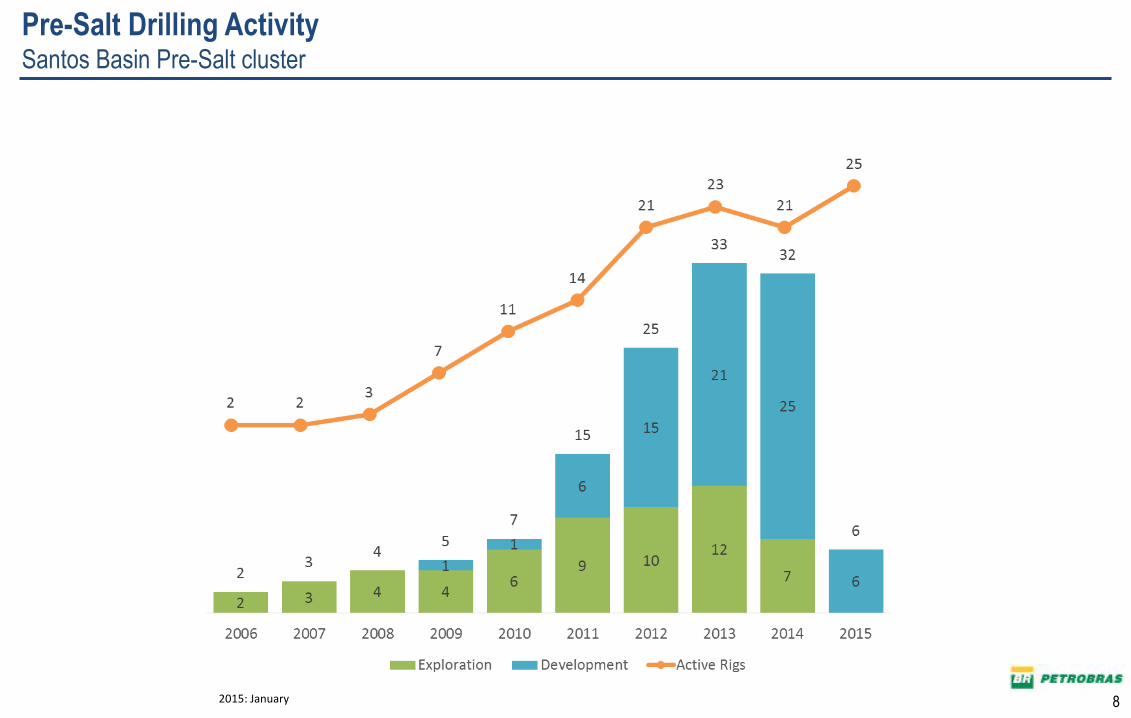

Pre-Salt Drilling Activity Santos Basin Pre-Salt cluster

2015: January

9 9

Wells Construction in Santos Pre-Salt Total Duration

Drilling (days/well)

Completion (days/well)

Source: January 2015

158

102 89 86

66 54

Until2010

2011 2012 2013 2014 2015

152

126

101 99 85 84

Until2010

2011 2012 2013 2014 2015

10

Well Connection in Brazil

4030 34

61

13

1217

26

2014

87

+70.6%

2013

51

2012

42

2011

53

Injectors

Producers

11 11

Pre-Salt Results Are Competitive to Deepwater Peers

150

120

90

60

30

0

Other

Heavy oil/oil sands/shale oil/tight liquids

Deep/ultradeep (>450 m)

Conventional

1. Range of predicted global oil demand according to the New Policies Scenario (91.7 Mboed) and the Current Policy Scenario (93.5 Mboed) in 2020, already subtracting 2.5 MBoed of processing gains – IEA Source: Rystad Energy UCUBE, IEA WEO 2012 (Nov-2012)

60

60

120

150

0

100 80 40 20 0

30

90

Break-even commercial ($/bbl)

(Mbpd)

OPEC conventional

Other conventional

Global forecasted production and break-even prices by types of oil and projects (*)

Deep and Ultradeep

Brownfield Canada oil sands and heavy oil

Greenfield Canada oil sands and heavy oil

Other oil sands and heavy oil

Tight liquids

Arctic

Oil shale

Shale oil

Break-even price range

for Brazil Pre-Salt

sanctioned projects

Next wave of new

technologies can

further decrease break-

even pre-salt price

(*) Concession Model

12 12

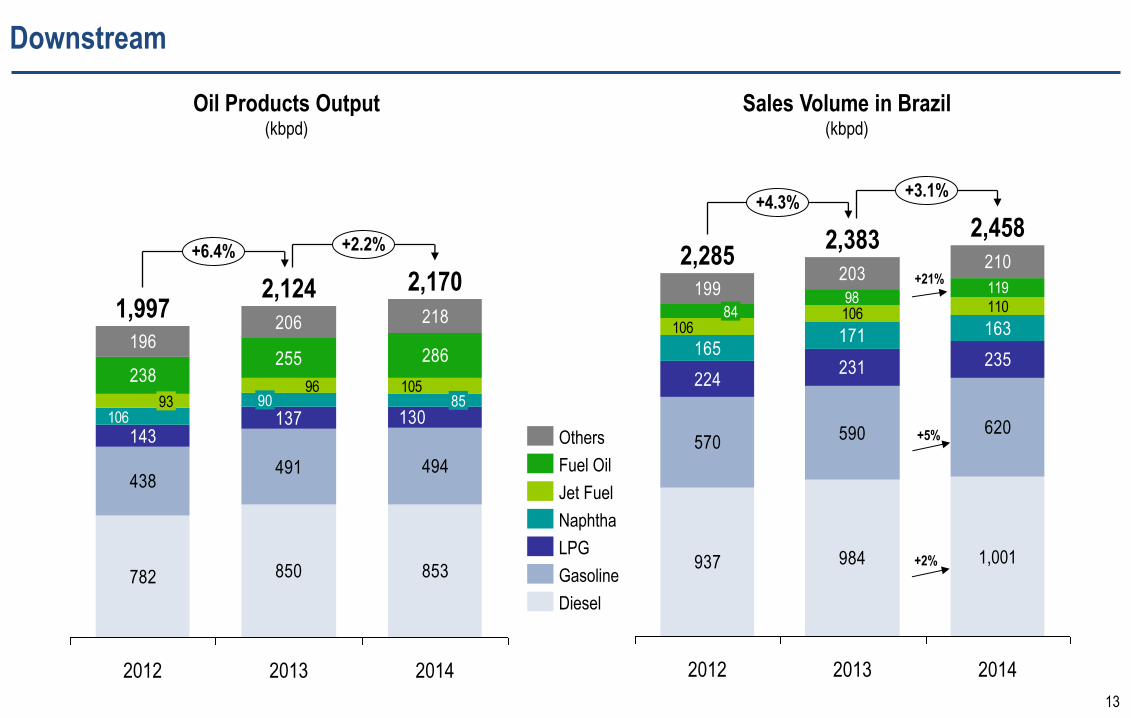

Oil Products Output Record in Brazil: 13 Refineries New HDT´s and conversion units, logistics and process optimization lead to higher output

1,850

1,800

1,750

1,700

1,650

1,550

1,600

1,950

2,200

2,150

2,100

2,050

2,000

1,900

1,588

2,074

1,944

2011

1,862

2010

1,798

2009

1,799

2008

1,779

2006

1,746

+226 th. Bpd +12%

2014

2,170

2013

1,765

2007 2012 2005

1,727

2004

1,704

2003

kbpd

13

Downstream

782 850 853

438491 494

238255 286

196206 218

130137143

106

10596

+6.4% +2.2%

2013

2,124

90

2012

1,997

93

2014

2,170

85

Oil Products Output (kbpd)

937 984

570590 620

224231 235

165171 163

110199

203210

106106

98119

+4.3% +3.1%

2014

2,458

1,001

2013

2,383

2012

2,285

84

+5%

+2%

+21%

Sales Volume in Brazil (kbpd)

Diesel

Gasoline

LPG

Naphtha

Jet Fuel

Fuel Oil

Others

14 14

338 394 489 570 590 620

0

100

200

300

400

500

600

700

2009 2010 2011 2012 2013 2014

740 809 880 937 984 1001

0

200

400

600

800

1000

1200

2009 2010 2011 2012 2013 2014

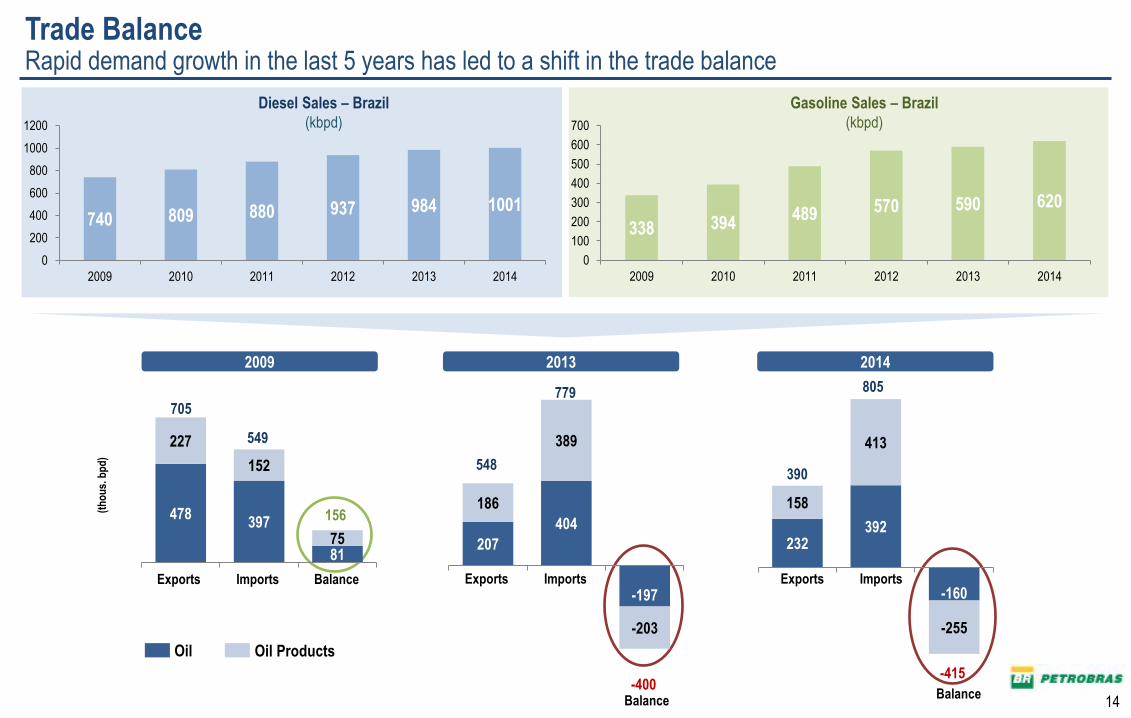

Trade Balance Rapid demand growth in the last 5 years has led to a shift in the trade balance

Gasoline Sales – Brazil

(kbpd)

Diesel Sales – Brazil

(kbpd)

Balance -400

Balance

156

Oil Oil Products

Imports Exports

-415

Imports Exports Imports Exports

2009 2013 2014

(th

ou

s. b

pd

)

705

549

548

779

390

805

Balance

478 397

81

227

152

75 207

404

-197

186

389

-203

232 392

-160

158

413

-255

15 15

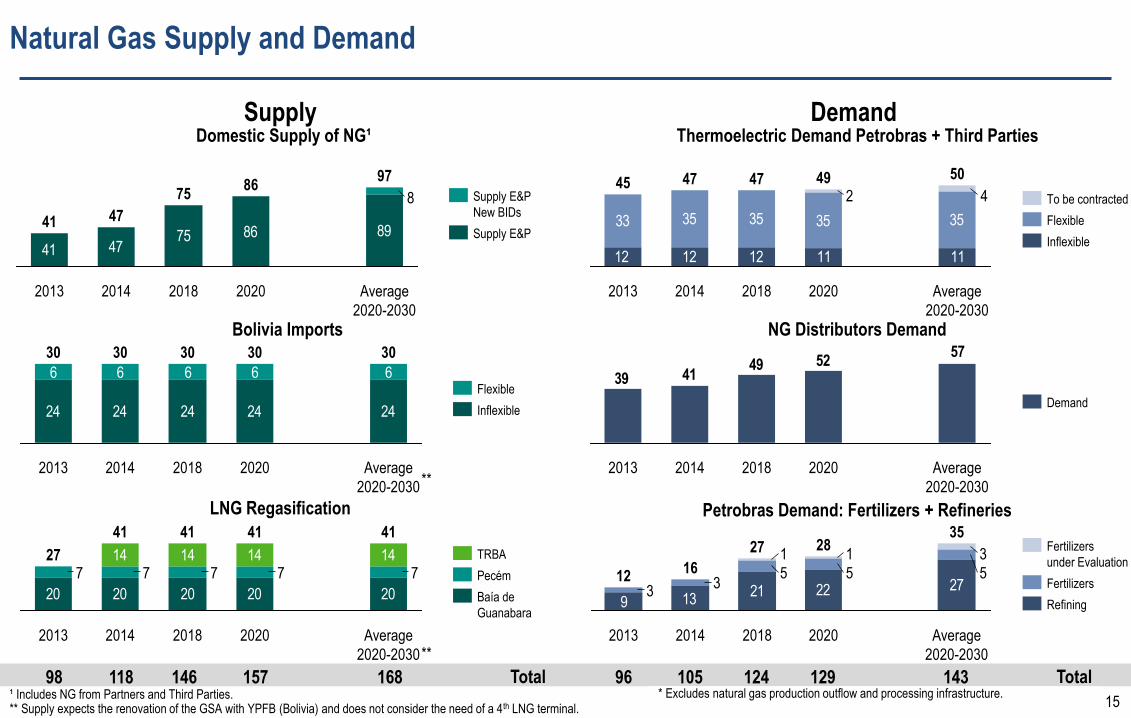

Supply Demand

LNG Regasification

Thermoelectric Demand Petrobras + Third Parties

33 35 35 35 35

1111121212

42

Average

2020-2030

50

2020

49

2018

47

2014

47

2013

45

Inflexible

Flexible

To be contracted

NG Distributors Demand 57

52494139

Average

2020-2030

2020 2018 2014 2013

Demand

Petrobras Demand: Fertilizers + Refineries

921 22 27

13

5553

3

311

Average

2020-2030

35

2020

28

2018

27

2014

16

2013

12

Refining

Fertilizers

Fertilizers

under Evaluation

96 124 129 143 98 146 157 168 118 105 Total

20 20 20 20 20

14 14 14 1477777

2013

27

2014

41

2018

41

Average

2020-2030

41

2020

41

Baía de

Guanabara

Pecém

TRBA

Bolivia Imports

24 24 24 24 24

6 6 6 6 6

2020

30

Average

2020-2030

30

2018

30

2014

30

2013

30

Inflexible

Flexible

Domestic Supply of NG¹

41 4775 86 89

8

2014

47

2013

41

Average

2020-2030

97

2020

86

2018

75 Supply E&P

New BIDs

Supply E&P

Total ¹ Includes NG from Partners and Third Parties. ** Supply expects the renovation of the GSA with YPFB (Bolivia) and does not consider the need of a 4th LNG terminal.

**

**

* Excludes natural gas production outflow and processing infrastructure.

Natural Gas Supply and Demand

16 16

37,3

27,6 29,4

25,0

2011 2012 2013 2014

EBITDA Price increases contributed to higher cash flow, but additional adjustments still needed

43,4 42,0 37,4

32,4

-6,9

-15,6 -9,8

-6,0

3,6 2,0

1,6

0,5

1,3 1,6

1,5

0,9

3,0 3,2

3,5

2,3

E&P RTM G&P Distribution International

2011 2012 2013 2014

(*) Adjusted according average exchange rate. Excludes Corporate and Elimination. 3Q14: unaudited numbers

Adjusted EBITDA Adjusted EBITDA Breakdown per Segment *

17 17

CAPEX EVOLUTION IN BUSINESS AND MANAGEMENT PLANS Total planned investments declining, E&P share increasing in each of last five Plans

* Gas and Energy, International, BR Distribuidora, PBio , Engineering Technology and Materials (ETM) and Corporate and Services Area

2014-2018 BMP Total Capex

2012-2016 BMP Total Capex

2013-2017 BMP Total Capex

2010-2014 BMP 2011-2015 BMP

E&P

Downstream

Other Areas*

Po

rtfo

lio o

f P

roje

cts

for

Fin

anci

abili

ty E

valu

atio

n

US$ 224.0 Billion Investment US$ 224.7 Billion US$ 236.5 Billion US$ 236.7 Billion US$ 220.6 Billion

48%

35%

17%

52%

33%

11% 15%

18%

27%

62%

14%

30%

56%

70%

12%

18 18

CAPEX Exploration & Production and Downstream

19 20

22

28 24

0

5

10

15

20

25

30

2010 2011 2012 2013 2014

Exploration & Production US$ Billion

16 16 15 14

8

0

5

10

15

20

25

30

2010 2011 2012 2013 2014

Downstream US$ Billion

19

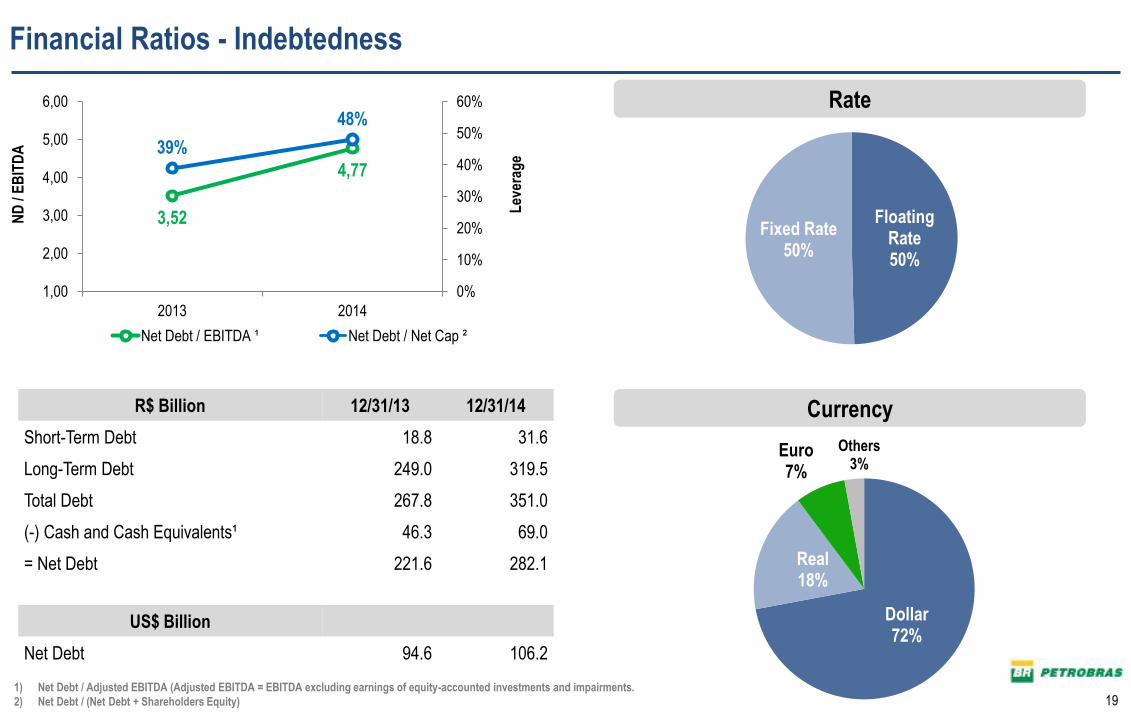

Financial Ratios - Indebtedness

Lev

erag

e

ND

/ E

BIT

DA

1) Net Debt / Adjusted EBITDA (Adjusted EBITDA = EBITDA excluding earnings of equity-accounted investments and impairments.

2) Net Debt / (Net Debt + Shareholders Equity)

3,52

4,77

39%

48%

0%

10%

20%

30%

40%

50%

60%

1,00

2,00

3,00

4,00

5,00

6,00

2013 2014

Net Debt / EBITDA ¹ Net Debt / Net Cap ²

R$ Billion 12/31/13 12/31/14

Short-Term Debt 18.8 31.6

Long-Term Debt 249.0 319.5

Total Debt 267.8 351.0

(-) Cash and Cash Equivalents¹ 46.3 69.0

= Net Debt 221.6 282.1

US$ Billion

Net Debt 94.6 106.2

Rate

Floating Rate 50%

Fixed Rate 50%

Currency

Dollar 72%

Real 18%

Euro 7%

Others 3%

20

Nominal flow (not discounted) of principal and interest, by maturity

42.6

2015

73.1

2017 2018

44.7 49.1 59.4

2020 +

208.4

2019 2016

R$ Billion

21

2015 Cash Flow

US$ Billion

US$ 60 /bbl (average)

R$ 3.10 /US$ (average)

Oil Prices

Exchange Rate

2013

23

25

26

-21

Interest,

Amortization

s and Others

-29

Investments Opearting

Cash

Flow

2015 Initial

Cash

Position

2015 Final Cash

Position

Funding Needs Rollovers Divestments

2,796 kboed Total Production

22

Assumptions for 2016

New Production Units (FPSO):

Cidade de Itaguaí (4Q15)

Cidade de Maricá (1Q16)

Cidade de Saquarema (2Q16)

Cidade de Caraguatatuba (3Q16)

Extended Well Test - Libra (4Q16)

Oil and Natural Gas

Production

(Brazil and Abroad)

US$ 10 billion Divestments

Approximately US$ 25 billion (82% in E&P)

37% below 2016 CAPEX (US$ 39.5 billion), in the 2014-2018 Business Plan Investments

2,886 kboed

+/- 2%

US$ 70 / bbl Oil Price

(Brent average) R$ 3,30 /US$

Exchange Rate (Average)

2,185 kbpd Oil Production

(Only Brazil)

23 23

Petrobras Ratings

Petrobras

Ba2

Brazil

Baa2

“The confirmation of Petrobras' rating reflects Moody's belief that the provision of audited financial statements eliminates the near term prospect of debt acceleration resulting from violation of covenants in indentures and loan agreements.

Future positive rating actions are likely to depend upon the company's ability to demonstrate improved operating performance that will support a stronger financial profile. Negative rating actions could result from significant deterioration in operating performance, major new negative developments from the corruption investigations, or the reappearance of significant liquidity pressures.”

Petrobras

BBB-

Brazil

BBB-

“Our negative outlook on Petrobras continues to reflect our intermediate-term uncertainties about the company's ability to boost production and, as a consequence, deleverage its balance sheet.

Our ratings on Petrobras continue to reflect our view that there is a "very high" likelihood that the company would receive timely extraordinary support from the Brazilian government under financial stress scenarios. Absent any sovereign rating action and change in our assessment about the likelihood of extraordinary government support, a downgrade would occur if the company's stand-alone credit profile (SACP) were to fall to 'b' Our current SACP assessment on Petrobras is 'b+'.

Petrobras

BBB-

Brazil

BBB

“The rating action reflects the publication of year-end 2014 audited financial statements, which averted violating indebtedness covenants that would have allowed creditors to start an acceleration process.

The rating action also reflects the company's improved liquidity position as a result of the recently announced USD13 billion of new financings facilities.

The Negative Outlook reflects the uncertainties surrounding the company's ability to deleverage its balance sheet in the medium term.

Petrobras' 'BBB-' and 'AAA (bra)' ratings continue to reflect its close linkage with the sovereign rating of Brazil due to the government's control of the company and its strategic importance to Brazil as its near monopoly supplier of liquid fuels.

24 24

Dividend Policy

According to Brazilian Corporate Law, companies with two classes of shares must pay a minimum amount equal to

25% of net income

Regarding Petrobras By-Laws, minimum payable to non-voting shares (PN/PBR.A) is the higher of:

25% of Adjusted Net Income

3% of the PN’s proportional book value of shareholder’s equity

5% of the PN’s proportional paid-in capital

Non-voting shares have priority rights to distribution of dividends

Petrobras By-Laws Consistent with Brazilian Corporate Law

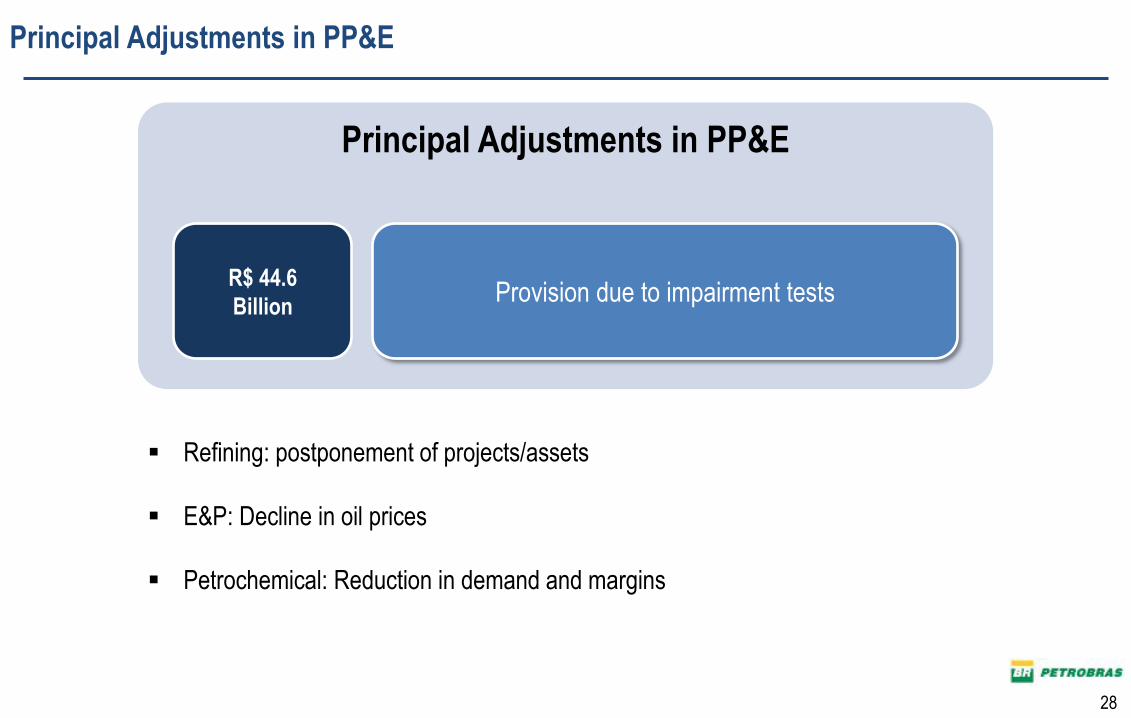

Principal Adjustments in PP&E

25

Principal Adjustments in PP&E R$ 50.8 billion

R$ 6.2

Billion

Write-off related to overpayment incorrectly

capitalized, as a consequence of the “Car Wash

Operation”

Provision due to impairment tests R$ 44.6

Billion

PP&E in 12/31/14: R$ 581 billion

26

Principal Adjustments in PP&E

R$ 6.2

Billion

Write-off related to overpayment incorrectly

capitalized, as a consequence of the “Car Wash

Operation”

Amount of 3% over contracts with 27 companies members of the cartel between

2004 and 2012

For companies outside the cartel, specific values mentioned in the depositions

Principal Adjustments in PP&E

Methodology based on the contents of the Prosecutor’s Office investigations

Depositions consistent with relation to: the existence of the cartel; time period; percentages and values

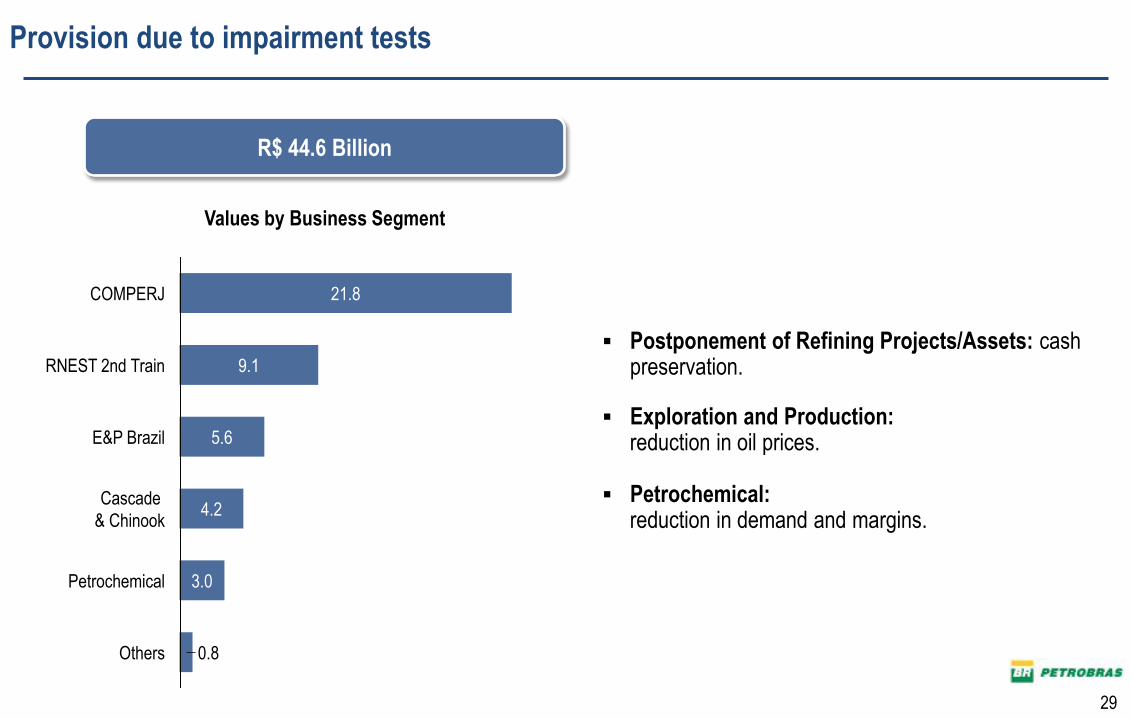

Values by Business Segment

0.1

0.7 G&P

2.0

Others

E&P

Downstream 3.4

27

R$ 6.2 Billion

Write-off related to overpayment incorrectly capitalized, as a consequence of the “Car

Wash Operation”

28

Principal Adjustments in PP&E

R$ 44.6

Billion Provision due to impairment tests

Refining: postponement of projects/assets

E&P: Decline in oil prices

Petrochemical: Reduction in demand and margins

Principal Adjustments in PP&E

Postponement of Refining Projects/Assets: cash preservation.

Exploration and Production: reduction in oil prices.

Petrochemical:

reduction in demand and margins.

Others 0.8

Petrochemical 3.0

Cascade

& Chinook 4.2

E&P Brazil 5.6

RNEST 2nd Train 9.1

COMPERJ 21.8

29

Values by Business Segment

R$ 44.6 Billion

Provision due to impairment tests