phd course in corporate finance - graduate school of ... · phd course in corporate finance initial...

TRANSCRIPT

PhD Course in Corporate Finance

Initial Public O�erings

Ernst Maug1

Revised March 3, 2016

1Professor of Corporate Finance, University of Mannheim; Homepage:http://http://cf.bwl.uni-mannheim.de/de/people/maug/, Tel: +49 (621)181-1952, E-Mail: [email protected]. This note is made publiclyavailable subject to the condition that any user noti�es the author of its use.Please bring any errors and omissions to the attention of the author.

Ernst Maug PhD Course in Corporate Finance

The Model

Based on Rock (1986)

A company o�ers 1 share of its common stock for the �rst time in

an initial public o�ering (IPO). Value of company is uncertain:

V =

{V̄ with probability pV with probability 1− p

The share is o�ered at an initial o�ering price P0; the price cannot

be revised.

Ernst Maug PhD Course in Corporate Finance

There are two groups of investors:

Informed investors acquire information about the company.

They apply for 0 < QI ≤ 1 shares if and only if they expect to

break at least even, otherwise they do not apply for shares.

Uninformed investors do not acquire any information and only

know the probability distribution for �rm values. They apply

for QU ≥ 1 shares if and only if they expect to break at least

even, otherwise they do not apply for shares.

Note: If uninformed investors and informed investors apply for

shares, then demand exceeds supply. Assume also that the number

of shares cannot be increased in this case (no �Greenshoe option�).

Ernst Maug PhD Course in Corporate Finance

We also assume:

Investors cannot short sell the shares.

The information acquired by informed investors is of the form

of a binary signal σ ∈ {σ;σ} where:

Pr (σ = σ |V = V ) = Pr(σ = σ

∣∣V = V̄)

= 1− ε.

Hence ε is the error of the signal. Assume for now that ε = 0,

i. e. informed investors receive a perfect signal.

If demand exceeds supply, shares are rationed pro rata, i. e.

every investor receives a proportion 1

QU+QIper share ordered.

Ernst Maug PhD Course in Corporate Finance

From these assumptions it is easy to derive the decision rule of

informed investors:

Apply if P0 ≤ V ,Do not apply if P0 > V .

It is clear that the issuer will never issue shares below V , and no

investor will ever buy shares if P0 > V̄ . Hence P0 ∈[V , V̄

]and

the policy of the informed investor can be rewritten as:

Apply if V = V̄ ,Do not apply if V = V .

Ernst Maug PhD Course in Corporate Finance

Then we can write the incentive compatibility constraint for the

uninformed investors as follows:

pQU

QU + QI

(V̄ − P0

)+ (1− p) (V − P0) ≥ 0.

This implies that the o�ering price is bounded from above.

De�ne α ≡ QUQU+QI

. Then:

P0 ≤αpV̄ + (1− p)V

1− (1− α) p.

Uninformed investors will not participate if this constraint is

violated.

Ernst Maug PhD Course in Corporate Finance

This shows immediately that the o�er is underpriced. The average

price in secondary trading is:

P1 = pV̄ + (1− p)V .

Then the average IPO discount is:

∆IPO = P1 − P0 = pV̄

(1− α

1− (1− α) p

)+ (1− p)V

(1− 1

1− (1− α) p

)= p (1− p)

(V̄ − V

) 1− α1− (1− α) p

.

Ernst Maug PhD Course in Corporate Finance

Note that:

The variance of a Bernoulli random variable like �rm value is

p (1− p)(V̄ − V

)2, hence the IPO discount is closely related

to the uncertainty or volatility of the share price.

The IPO discount is zero only if α = 1 as long as volatility is

not zero. Hence, 1− α is a parameter for the degree of

adverse selection.

Exercise

Generalize the model above for the case where ε > 0 and informed

investors' information is only imperfect. Derive new expressions for

P0 and ∆IPO .

Ernst Maug PhD Course in Corporate Finance

Exercise

Extend the model of Rock (1986) to include underwriter price

support in the secondary market as follows. Assume the �rm hires

an underwriter who is committed to buy all shares from the �rm at

the price PF . The underwriter sells the shares in the IPO for P0

and agrees to buy shares back in the secondary market for some

support price P . Only investors who bought shares in the IPO can

sell them back at the support price.

Ernst Maug PhD Course in Corporate Finance

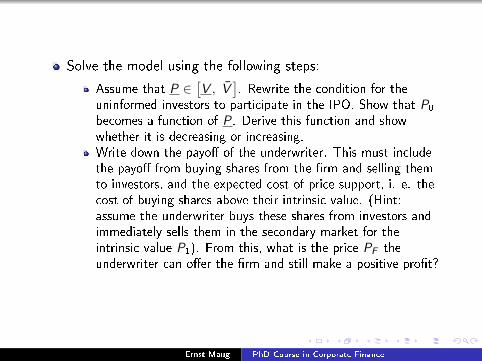

Solve the model using the following steps:

Assume that P ∈[V , V̄

]. Rewrite the condition for the

uninformed investors to participate in the IPO. Show that P0

becomes a function of P. Derive this function and showwhether it is decreasing or increasing.Write down the payo� of the underwriter. This must includethe payo� from buying shares from the �rm and selling themto investors, and the expected cost of price support, i. e. thecost of buying shares above their intrinsic value. (Hint:assume the underwriter buys these shares from investors andimmediately sells them in the secondary market for theintrinsic value P1). From this, what is the price PF theunderwriter can o�er the �rm and still make a positive pro�t?

Ernst Maug PhD Course in Corporate Finance

Assume many banks compete for underwriting the issue, so

the underwriter makes zero pro�ts in equilibrium and the

underwriter who buys the shares from the �rm at the highest

price PF conducts the o�ering. Which level of price support Pis o�ered in equilibrium? Verify the initial assumption that

P ∈[V , V̄

]. Hence, what is the equilibrium solution for P0

and PF ?

Show that the equilibrium has the following properties: (1) the

adverse selection problem is eliminated completely, and the

�rm receives a fair price of the stock, and (2) the IPO is

overpriced. Comment on this solution.

Note: Models of IPO price support were published by Chowdhry

and Nanda (1996) and Benveniste, BuSaba and Wilhelm (1996).

Ernst Maug PhD Course in Corporate Finance

Based on Benveniste and Wilhelm (1990)

Entrepreneur wants to take his �rm public and sell one share

to two investors. Each investor observes a signal that is either

good (g) with probability p or bad (b) with probability 1− p.

Once listed, shares are trading at a price Ps where

s ∈ {0, 1, 2}, the number of good signals:

Ps = P̄ − (2− s)α .

Ernst Maug PhD Course in Corporate Finance

The entrepreneur hires an investment bank that sells the

shares at o�ering prices PsO to the public and elicits the

information of the two investors by way of a mechanism

through direct revelation (the revelation principle applies).

The investment bank can choose the allocation qsg , qsb as a

function of the information investors reveal to the bank during

bookbuilding.

Let φ ≤ 1 be the minimum number of shares the entrepreneur

wishes to sell in the issue.

Let f ≥ φ/2 be the maximum each investor is willing to buy.

Ernst Maug PhD Course in Corporate Finance

The objective of the bank and the entrepreneur is to choose an

allocation and o�ering prices to maximize expected proceeds.

Shares not sold in the IPO will be sold in an SEO later:

Π = E (Ps)− p2(P2 − P2

O

)2q2g

−2p (1− p)(P1 − P1

O

) (q1g + q1b

)− (1− p)2

(P0 − P0

O

)2q0b

subject to the following constraints.

1 Sell at least φ and at most one share:

1 ≥ 2q2g ≥ φ1 ≥ q1g + q1b ≥ φ (1)

1 ≥ 2q0b ≥ φ

Ernst Maug PhD Course in Corporate Finance

2 Investors are willing to buy at most f shares each:

0 ≤ qsg , qsb ≤ f s = 0, 1, 2. (2)

3 It must be incentive compatible for the investor with good

information to reveal her information truthfully:

p(P2 − P2

O

)q2g + (1− p)

(P1 − P1

O

)q1g (3)

≥ p(P2 − P1

O

)q1b + (1− p)

(P1 − P0

O

)q0b (4)

= p(P1 + α− P1

O

)q1b + (1− p)

(P0 + α− P0

O

)q0b .(5)

Ernst Maug PhD Course in Corporate Finance

4 It must be incentive compatible for the investor with bad

information to reveal her information truthfully:

p(P1 − P1

O

)q1b + (1− p)

(P0 − P0

O

)q0b

≥ p(P1 − P2

O

)q2g + (1− p)

(P0 − P1

O

)q1g (6)

= p(P2 − α− P2

O

)q1b + (1− p)

(P1 − α− P1

O

)q0b .

5 Investors are not willing to pay more for shares than they are

worth (participation constraint):

Ps ≥ Ps0 s = 0, 1, 2. (7)

Ernst Maug PhD Course in Corporate Finance

Analysis

Rewrite Π as:

Π = E (Ps)− 2p[p(P2 − P2

O

)q2g + (1− p)

(P1 − P1

O

)q1g]

−2 (1− p)[p(P1 − P1

O

)q1b + (1− p)

(P0 − P0

O

)q0b]

Assume that only (4) is binding and that (6) is not binding. Then

substitute (4) into the �rst square brackets:

Π = E (Ps)− 2p[p(P1 + α− P1

O

)q1b + (1− p)

(P0 + α− P0

O

)q0b]

−2 (1− p)[p(P1 − P1

O

)q1b + (1− p)

(P0 − P0

O

)q0b]

= E (Ps)− 2[p(P1 − P1

O

)q1b + (1− p)

(P0 − P0

O

)q0b]

−2pα[pq1b + (1− p) q0b

].

Ernst Maug PhD Course in Corporate Finance

Now choose the allocation and prices as follows:

1 Π is increasing in P1

O and P0

O . Hence, choose P1

O = P1 and

P0

O = P0, so (7) is binding for s = 0, 1. Then the �rst term in

square bracket vanishes.

2 Π is decreasing in q0b and q1b, so choose these as small as

possible, so from (1), q0b = φ/2, q1b = f and q1g = φ− f .

Ernst Maug PhD Course in Corporate Finance

3 Rewrite (4) and choose(P2 − P2

O

)q2g so that (4) is just

satis�ed:

p(P2 − P2

O

)q2g = α (pf + (1− p)φ/2) .

Solving for P2

0gives:

P2

O = P2 − α[f

q2g+

(1− p)φ

2pq2g

]Clearly, an admissable solution is q2g = f and

P2

O = P2 − α[1 +

(1− p)φ

2pf

]. (8)

Note that

P2 − α− P2

O =α (1− p)φ

2pf> 0 . (9)

Ernst Maug PhD Course in Corporate Finance

4 With this, P2

O < P1 = P2 − α. Note that the left hand side of

(6) equals zero because the o�ering prices equal the

aftermarket prices from the �rst step. The right hand side of

(6) can be rewritten using (9):

0 ≥ p

(α (1− p)φ

2pf

)f + (1− p) (−α) q

φ

2= 0 ,

where we have used that P1

O = P1, q0b = φ/2, and q1b = f ,hence (6) is also satis�ed.

Ernst Maug PhD Course in Corporate Finance

Discussion

Underpricing is the expected di�erence between market price and

o�ering price:

E (Ps − PsO) = p2

(P2 − P2

O

)= p2α

[1 +

(1− p)φ

pf

].

Underpricing is therefore:

Increasing in α,

Increasing in φ,

Decreasing in f .

Ernst Maug PhD Course in Corporate Finance

Expected proceeds are:

E (Ps)− 2pα [pf + (1− p)φ/2]

The second expression represents the rents extracted by informed

investors.

The o�ering price is not monotonic (P2

O < P1

O = P1). If that would

be required, then choose P1

O < P1 and underpricing increases.

Ernst Maug PhD Course in Corporate Finance

Regular investors

Assume the bank can extract some of the rents of regular investors

and induce them to accept a loss L > 0. Then (7) becomes

Ps + L ≥ Ps0 s = 0, 1, 2. (10)

Clearly, the bank will then overprice some IPOs and increase the

o�ering amount.

Ernst Maug PhD Course in Corporate Finance

Motivation

Based on Khanna, Noe and Sonti (2008)

Puzzling observations about IPOs:

Hot issue markets: why do many �rms suddenly decide to go

public? What is the �window of opportunity�?

Underpricing is higher in hot markets than in cold markets.

Why do �rms not shift to markets where they have to leave

less money on the table?

Why does competition not eliminate banks' rents in hot

markets?

Why are �rms during hot markets younger, less pro�table, and

with less insider ownership?

Ernst Maug PhD Course in Corporate Finance

The Model

Economy has N entrepreneurs who may go public. Each is matched

with one of a continuum of underwriters:

A fraction ρ of projects is good (�G�) with payo� X = 1, 1− ρis bad (�B�) with payo� X = 0.

Going public has an opportunity cost w .

Each �rm bargains with the underwriter it is matched with

who sets the o�er price ps . Firms capture a fraction β of the

issue price, underwriters 1− β.Underwriters' bene�t from higher prices through higher fees;

they are penalized for overpricing IPOs.

Underwriters hire a quantity η ∈ [0, 1] of bankers who cost θand screen projects. With probability 1− η they receive an

uninformed signal U. With probability η they become perfectly

informed so that Pr (H |1) = Pr (L |0) = η.

Ernst Maug PhD Course in Corporate Finance

Timing of Events

Ernst Maug PhD Course in Corporate Finance

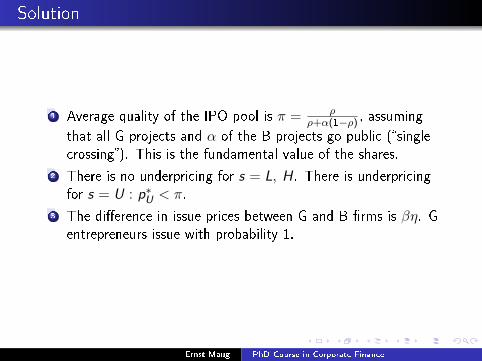

Solution

1 Average quality of the IPO pool is π = ρρ+α(1−ρ) , assuming

that all G projects and α of the B projects go public (�single

crossing�). This is the fundamental value of the shares.

2 There is no underpricing for s = L, H. There is underpricing

for s = U : p∗U < π.

3 The di�erence in issue prices between G and B �rms is βη. Gentrepreneurs issue with probability 1.

Ernst Maug PhD Course in Corporate Finance

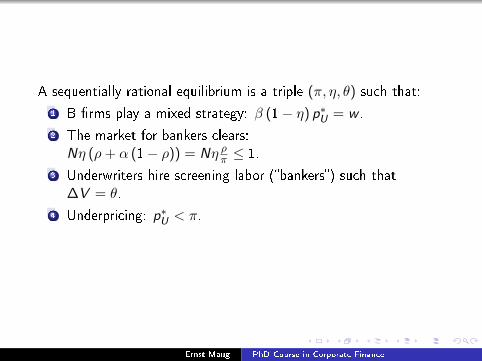

A sequentially rational equilibrium is a triple (π, η, θ) such that:

1 B �rms play a mixed strategy: β (1− η) p∗U = w .

2 The market for bankers clears:

Nη (ρ+ α (1− ρ)) = Nη ρπ ≤ 1.

3 Underwriters hire screening labor (�bankers�) such that

∆V = θ.

4 Underpricing: p∗U < π.

Ernst Maug PhD Course in Corporate Finance

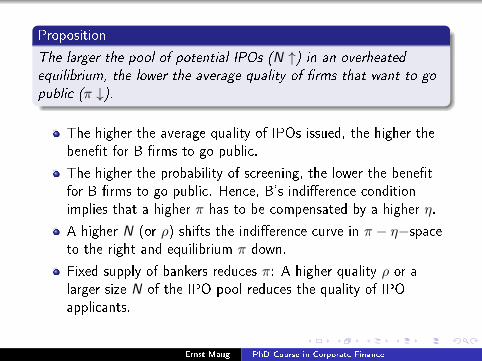

Proposition

The larger the pool of potential IPOs (N ↑) in an overheated

equilibrium, the lower the average quality of �rms that want to go

public (π ↓).

The higher the average quality of IPOs issued, the higher the

bene�t for B �rms to go public.

The higher the probability of screening, the lower the bene�t

for B �rms to go public. Hence, B's indi�erence condition

implies that a higher π has to be compensated by a higher η.

A higher N (or ρ) shifts the indi�erence curve in π − η−spaceto the right and equilibrium π down.

Fixed supply of bankers reduces π: A higher quality ρ or a

larger size N of the IPO pool reduces the quality of IPO

applicants.

Ernst Maug PhD Course in Corporate Finance

Ernst Maug PhD Course in Corporate Finance

Hot and Cold Markets

Proposition

If the number of good projects ρN is below ββ−w , there exists an

equilibrium in which only good projects try to obtain funding. If ρNis above this cut-o�, some bad �rms apply for funding.

Implications:

There is a discontinuous shift at some point such that above

the threshold, there are more �rms apply for funds.

Such a shock is more likely to come from market-wide shocks

than from industry-speci�c IPO waves.

Ernst Maug PhD Course in Corporate Finance

Discussion

The story in a nutshell:

Hot markets are ignited for neoclassical reasons: The number

of good �rms that want to go public crosses a critical

threshold.

Once su�ciently many investment bankers are too busy

screening projects, the quality of screening declines, which

opens a �window of opportunity� for bad �rms.

Bad �rms are drawn into the market, which becomes even

more crowded, deteriorating the quality of screening further.

The quality of IPOs declines and the uncertainty about quality

increases, leading to more underpricing.

Ernst Maug PhD Course in Corporate Finance

Motivation

Based on Schultz (2008)

Question: Why do IPOs underperform in the long run?

Potential explanation:

behavioral e�ects: companies issue equity when the market isovervaluedproblem: violates market e�ciency

Alternative: Pseudo-market timing: companies issue more

equity at higher stock market levels

Then IPOs cluster at ex post peaks

Ernst Maug PhD Course in Corporate Finance

Idea

The argument in �ve steps:

1 More companies are taken public when stock market values are

higher than when they are lower.

2 If stock prices decline, then the number of IPOs goes down

subsequently.

3 Then the ex post peak of the stock market also becomes the

ex post peak of IPO activity.

4 Event studies weight returns by the number of IPOs at the

beginning of the period, hence they give more weight to these

ex post peaks followed by negative returns.

5 Event study returns are lower than calendar returns.

Ernst Maug PhD Course in Corporate Finance

Example

Two periods

In each period, the excess return on the stock market is either

+10% or -10%.

The current level of the IPO price is equal to 100.

IPO activity depends on the price level

if P<95: no IPOsif 95<P<105: 1 IPOif P>105: 3 IPOs

With two periods and two states there are four equally likely

scenarios.

Ernst Maug PhD Course in Corporate Finance

Pseudo market timing in a two-period model

Ernst Maug PhD Course in Corporate Finance

Two-period model: Calculations

Period 0 Period 1 Total X Return

Scen. Price # X Ret Price # X Ret IPOs Cal. Event

1 100 1 0.10 110 3 0.10 4 0.10 0.10

2 100 1 0.10 110 3 -0.10 4 0.00 -0.05

3 100 1 -0.10 90 0 0.10 1 0.00 -0.10

4 100 1 -0.10 90 0 -0.10 1 -0.10 -0.10

Avg. 0.00 0.00 -0.04

Consider scenario 2:

Calendar day return = (XRet0 + XRet1) /2 = (0.10− 0.10) /2 = 0.00

Event day return = (1× XRet0 + 3× XRet2) /4

= (1× 0.10 + 3×−0.10) /4 = −0.05.

Ernst Maug PhD Course in Corporate Finance

A general restatement

CAARs in long-term event studies are calculated as:

CAAR =t=T∑t=1

1

N

[i=N∑i=1

(ri ,t − rm,t)

].

Here:

r = returnt = event month (usually runs from 1 to 36 or 60)i = stock of IPO �rm (runs from 1 to number of IPOs)m = market or matching stock

Ernst Maug PhD Course in Corporate Finance

Why average CAR-estimates are biased

Standard assumption: N is �xed.

Assumption here: N is a random variable

E (CAAR) = E

(1

N

)E

(t=T∑t=1

i=N∑i=1

(ri ,t − rm,t)

)

+ Cov

(1

N,

t=T∑t=1

i=N∑i=1

(ri ,t − rm,t)

).

N is positively correlated with returns

Covariance in second line is negative (correlation with 1/N)

Estimate of CAAR is biased downward

Ernst Maug PhD Course in Corporate Finance

How big is this e�ect?

Need to calibrate magnitude of this e�ect and compare it to

returns from statistical studies

Research design:

1 Measure empirical sensitivity of number of IPOs to value ofstock market and to value of �rms that recently went public

2 Simulate economy with realistic parameters for returns to themarket, IPO-portfolio, and issuance activity

3 Calibrate model so that markets in the simulated economy aree�cient and no real market timing is possible

4 Measure e�ect of pseudo market timing using usualbuy-and-hold returns (BHAR)

Ernst Maug PhD Course in Corporate Finance

Step 1: Measure sensitivity of IPOs to returns

Research design:

Construct IPO-index from �rms that went public in 60 monthsprior, calculate returnIndex value is 100 in February 1973, subsequently index valueis IPO-Index(t)=IPO-Index(t-1)*(1+mean return to IPO �rms)Regress IPO activity from 1973 to 1997 on IPO-index, stockmarket index, and time

#IPOs = −1.974− 0.144t − 0.057Markett(−11.66)

+ 0.153IPOt(19.43)

.

The R-squared of this regression is 77.8%.

Ernst Maug PhD Course in Corporate Finance

Steps 2-4: Run Monte Carlo simulations

Step 2: Estimate statistics of returns

Mean monthly return is 1.12% with standard deviation of4.52%Regress return to IPO-portfolio on market return: is 1.31 timeshigher with residual variance of 4.27%

Step 3: Calibrate economy and run 5,000 times

Generate returns from normal distribution with parameters asestimated in step 2 for market returnsFor IPO-portfolio, use slope coe�cient and variance ofdisturbance term from regression, but use intercept to equateexpected IPO returns with expected market returnsGenerate returns for 300 months (25 years)

Step 4: Calculate BHARs, average across 5,000 runs

Ernst Maug PhD Course in Corporate Finance

Simulated excess returns and wealth relatives

BHARs

1-12 1-24 1-36 1-60

Median -5.29% -10.97% -17.06% -31.75%

Mean -5.26% -10.18% -15.18% -26.50%

Std. error 0.10% 0.19% 0.29% 0.55%

t-statistic -54.77 -54.35 -52.74 -47.94

Percent<0 81.80% 82.10% 82.70% 82.80%

Wealth relatives

1-36 1-60

Median 85.29% 77.81%

Mean 86.43% 80.82%

Std. error 0.20% 0.29%

Ernst Maug PhD Course in Corporate Finance

Comparison to other theories

Behav. Inad. Psd.

market risk market

timing adj. timing

1 Underperformance after o�erings " " "

2 Poor operating perf. after o�erings " "

3 Underperf.: Other countries, other times ? ? "

4 O�ering clustering at market peaks " "

5 Perf. is worse in event-time " "

6 Perf. is worst after heavy issuance " "

7 Perf. is poor after debt issues ? "

8 Managers do not appear to pro�t "

Ernst Maug PhD Course in Corporate Finance

Conclusions

It is better to measure returns in calendar time, not in event

time, to account for the endogeneity (dependence on stock

market valuation) of the event itself.

Benchmark against index that not only has the same expected

return under the null, but is also highly correlated with the

event itself.

More detailed discussion of econometric issues: Baker,

Taliaferro, Wurgler, JF 2006; Viswanathan & Wei, RFS 2008.

Ernst Maug PhD Course in Corporate Finance