< picture to go here > - lloyd's of london · pdf filepicture to go here > ......

TRANSCRIPT

© Lloyd’s 2012

< Picture to go here >

Colombia Insurance day 6 June 2013

© Lloyd’s 2012

<

Picture

to

go here

>

agenda

08.30 Welcome & opening remarks

John Nelson

08.45 The Critical role of insurance in Colombia

Roberto Junguito

09.00 Panel - Colombian insurance market: Experiences, perspectives

and lesson learned

10.05 Coffee & networking break

10.20 Panel - British perspective of Colombian market, Reinsurance

11.00 Panel - Bridging the two markets – exsisting practice and

challenges for the future

11.40 Closing remarks

Nigel Luson

11.45 Networking & Coffee

© Lloyd’s 2012

< Picture to

go here > John Nelson Chairman, lloyd’s

© Lloyd’s 2012

< Picture to

go here >

The Critical role of insurance in colombia Roberto Junguito, president, colombian insurance association

© Lloyd’s 2012

< Picture to

go here >

Colombian insurance market: experiences, perspectives and lessons learned Chair: Roberto Juanguito President, FASECOLDA

© Lloyd’s 2012

< Picture to

go here >

Regulation and supervision issues Jorge enrique uribe President, Seguras Bolivar

COLOMBIA INSURANCE DAY AT LLOYDS

REGULATION AND SUPERVISION ISSUES

Jorge Enrique Uribe

June 6, 2013

London

I. Colombia and its Development

II. Regulation and Supervition Issues

AGENDA

COLOMBIA AND ITS DEVELOPMENT

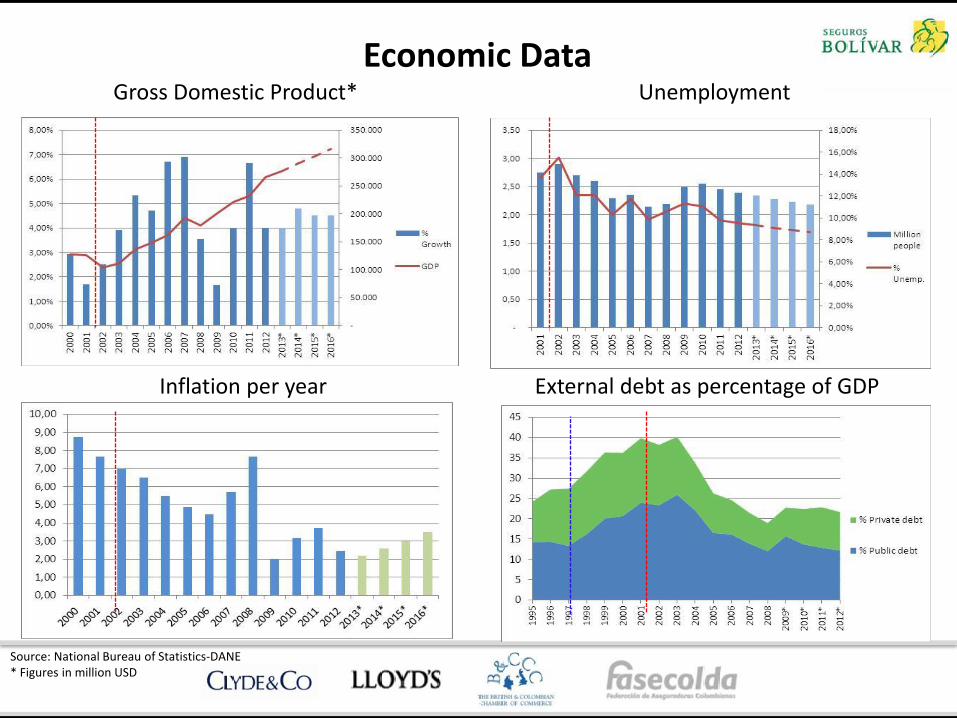

Economic Data

Source: National Bureau of Statistics-DANE * Figures in million USD

External debt as percentage of GDP

Gross Domestic Product*

Inflation per year

Unemployment

Economic Data

Per capita Gross Domestic Product*

Evolution of middle class in Colombia

Pessimistic scenario Optimistic scenario

Adjusted to USD dollars of 2011

Middle class: People who belongs to families with monthly income between 1 And 5 thousand dollars in 2010.

* Source. Fedesarrollo (Local economical studies organization)

Economic Data

REGULATION AND SUPERVISION ISSUES

Regulation and surveillance of insurance companies is being strenghthened

Consumer Protection

Information - Transparency

Financial soundness of

insurance companies

Competition

Financial Education

Supervision Risk Management & Solvency Assesment

LIQUIDITY

RETENTION

RI & POLICY CONDITIONS

SECURITY

RISK TRANSFER

DEFAULT RISK

MATERIAL RISKS

SUPPORT PROCESSES

TRANSFER OF KNOW-HOW & INFORMATION

PILAR I CAPITAL

REQUIREMENTS

PILAR II SUPERVISION, CONTROL & RISK MNG.

OPERATIONAL RISK

REPUTATIONAL RISK

STRATEGIC RISK

CLAIMS MANAGEMENT

UNDERWRITING

PRICING

RESERVING ACCOUNTING

ASSET LIABILITY MANAGEMENT

BALANCE SHEET

PILAR III DISCLOSURE & TRANSPARENCY.

Adapted from a

MUNICH RE Chart

TECHNICAL RISK

ISSUES

OF INTEREST

FOR YEARS

2013-2014

Regulation and Supervision

• Regulation, surveillance and adoption of international standards will determine the path that the insurance industry will follow.

• Consumer protection regulations, financial literacy obligations and more adequate information requirements will be in the order of the day.

• The risk based supervision scheme is also being used by the Financial Superintendence, in line with the Canadian experience.

• The Colombian government is currently working on the adoption of a modern technical provisions regime, as well as of international accounting standards (IFRS).

Solvency Regime Evolution

• Before 1990, regulated tariffs implied the sufficiency of them to cover risks. There were minimum capital requirements to operate by line of business.

• With the Colombian financial liberalization of 1990, free competition and pricing implied the adoption of a Solvency I regime, with capital requirements depending on technical risks.

• During 2010, Colombia’s insurance market updated its regulatory architecture in terms of solvency and investment regimes, introducing additional capital requirements to face market and credit risk.

Non Life Insurance Companies Solvency

• Regulatory capital requirement: Whole set of requirements set by the solvency regime (Technical risk + asset risk + market risk)

• Available capital: Available capital resources to accredit capital requirements.

0,0

0,5

1,0

1,5

2,0

2,5

3,0

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

Dic

Ma

r

Jun

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Patrimonio Adecuado Patrimonio Técnico Decreto 2954/10 CoberturaRegulatory capital requirement

Available capital Decree 2954/10 Available / required capital

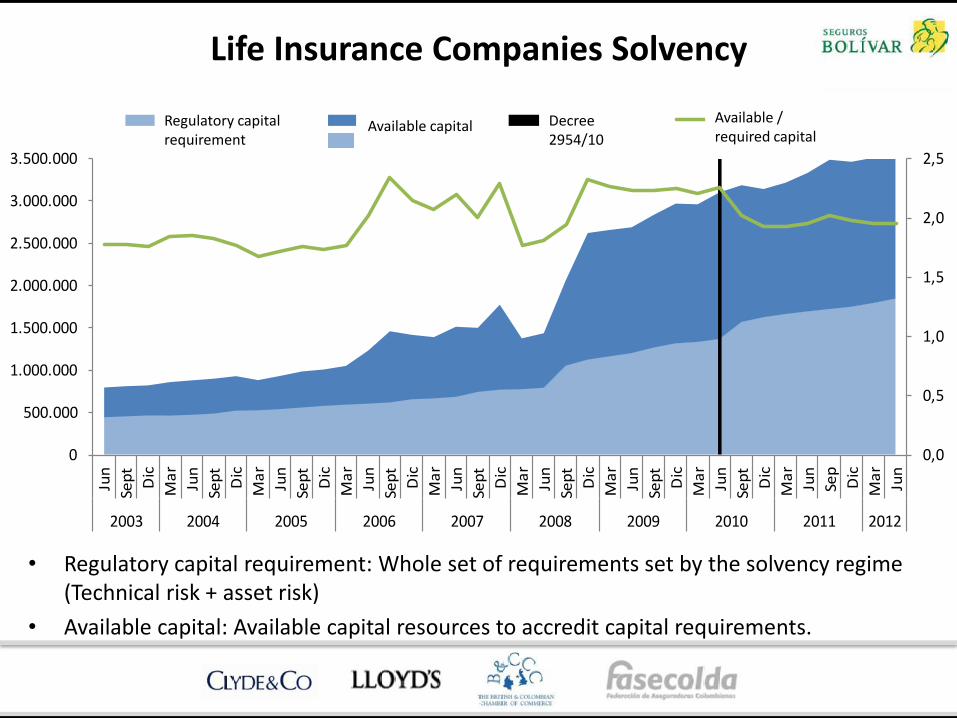

Life Insurance Companies Solvency

• Regulatory capital requirement: Whole set of requirements set by the solvency regime (Technical risk + asset risk)

• Available capital: Available capital resources to accredit capital requirements.

0,0

0,5

1,0

1,5

2,0

2,5

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000

3.500.000

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

t

Dic

Ma

r

Jun

Sep

Dic

Ma

r

Jun

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Patrimonio Adecuado Patrimonio Técnico Decreto 2954/10 CoberturaRegulatory capital requirement

Available capital Decree 2954/10

Available / required capital

Reserving 2013 Colombia’s Ministry of Finance Decree Project

• Premium Reserves

– Unearned Premium Reserve

– Premium Deficiency Reserve

• Benefit Reserve

• Asset Adequacy Reserve

• Outstanding Claims Reserves – Case Reserve

– IBNR/IBNER

• Adverse Deviation Reserve

• Catastrophic Risk Reserve

• New Reserve

• Important

changes in

Methodology

Current status: Third draft being discussed.Industry is performing impact on reserves’ tests. Government is expecting to issue This decree on 2nd semester of 2013.

THANK YOU

© Lloyd’s 2012

< Picture to

go here >

Liberalisation of the Colombian market act 1328, 2009 Fernando Quintero arturo President seguros colpatria

7 de Junio de 2013

• Background

• Legal Framework

• Considerations / Impact

• Future steps

Contents

7 de Junio de 2013 Background

Worldwide 1986 : Creation of WTO

1994 : Signing of NAFTA ( México, United States and Canada.)

1995: WTO GATS. Protection framework and promotion of services world trade. 4 modes of service supply: Cross-border trade, consumption overseas, commercial presence and movement of businessmen. Concept of Most Favored Nation Treatment

2001 – 2005 : DOHA Round with the Financial Leaders Working Groups ( FLWG ) and independent insurers - Model Time Schedule to Liberate Insurance Services.

In Colombia

1990: Economic Opening Environment ( Act 45 ) 100% foreign capital, regulated rates and commissions release, strengthening supervision 1994 : Act 170 – Joining to WTO

June 7, 2013

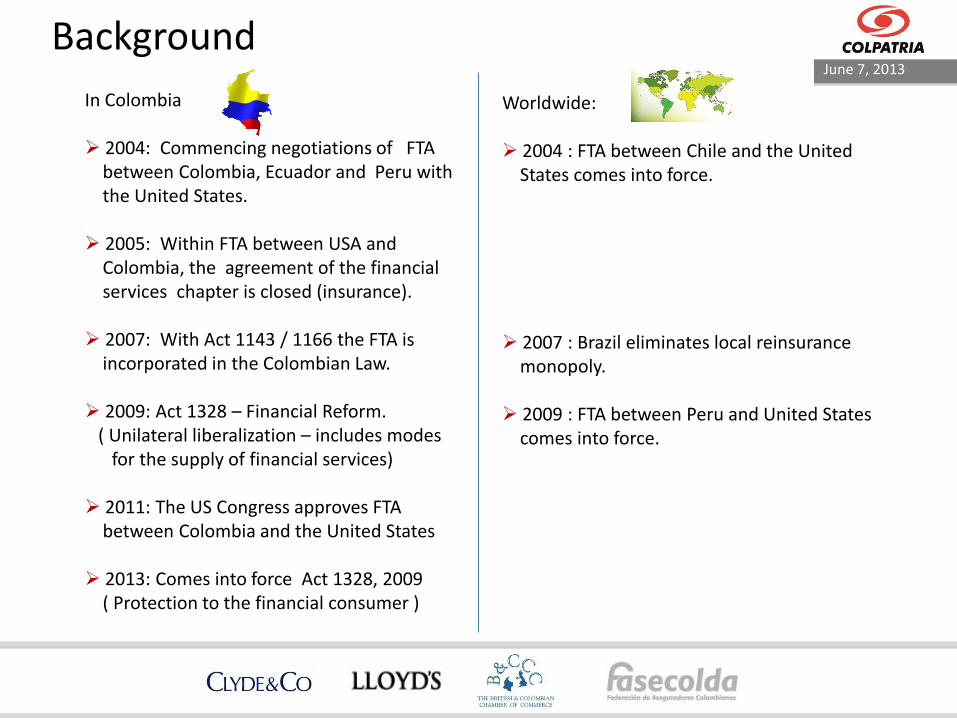

Background

Worldwide:

2004 : FTA between Chile and the United States comes into force.

2007 : Brazil eliminates local reinsurance monopoly.

2009 : FTA between Peru and United States comes into force.

In Colombia 2004: Commencing negotiations of FTA between Colombia, Ecuador and Peru with the United States.

2005: Within FTA between USA and Colombia, the agreement of the financial services chapter is closed (insurance). 2007: With Act 1143 / 1166 the FTA is incorporated in the Colombian Law. 2009: Act 1328 – Financial Reform. ( Unilateral liberalization – includes modes for the supply of financial services) 2011: The US Congress approves FTA between Colombia and the United States

2013: Comes into force Act 1328, 2009 ( Protection to the financial consumer )

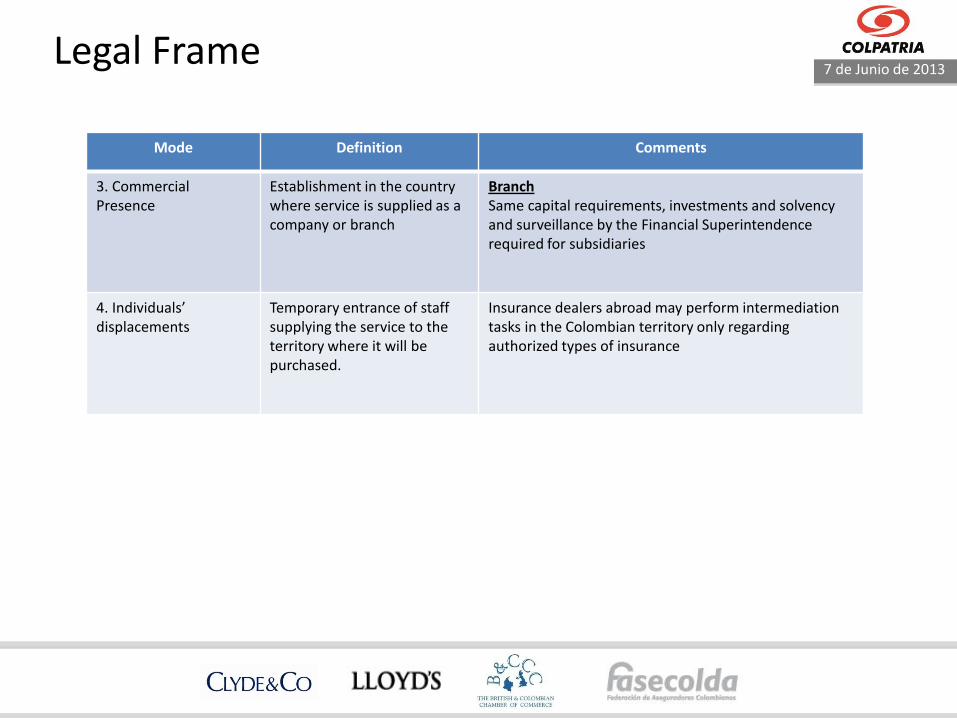

7 de Junio de 2013 Legal Frame

Mode Definition Comments

1-Cross-border trade Services provided from one territory to the other without the parties being displaced

Authorized lines : International marine transportation, international commercial aviation and space transportation. Risks covered: those related to the goods subject to international transportation, vehicle transporting the goods and general liability arising them, insurance covering goods in international transit

2. Consumption abroad Consumer is displaced and consumes services abroad

All individuals or companies residents in the country may acquire abroad any type of insurance. Exceptions: Related to social security Those requiring previous mandatory insurance Mandatory insurance When the Government is the Insured, Police

holder or beneficiary Except for MAT, prohibition to sell, offer, promote and advertise insurance policies issued by foreign companies

7 de Junio de 2013 Legal Frame

Mode Definition Comments

3. Commercial Presence

Establishment in the country where service is supplied as a company or branch

Branch Same capital requirements, investments and solvency and surveillance by the Financial Superintendence required for subsidiaries

4. Individuals’ displacements

Temporary entrance of staff supplying the service to the territory where it will be purchased.

Insurance dealers abroad may perform intermediation tasks in the Colombian territory only regarding authorized types of insurance

7 de Junio de 2013 Considerations/ Impact

• Emphasis in the protection to the consumer – Creation of a Foreign Companies Register. (Cross-border trade)

• Except for MAT, clarity in the scope of the prohibition to offer in Colombia insurance from foreign companies.

• Except for the exceptions, allowance to acquire insurance overseas by means of displacement.

• Individuals displacement (intermediaries) allowed only for MAT insurance.

• Branches as an innovation in the presence model.

• Environment of higher requirement levels for service and products.

• Greater competition for major risks (medium size and major companies / global)

• Approximately 50% of the Colombian market is exposed to risk.

7 de Junio de 2013 Next steps

• Creation of a secondary regulation / guidance (Registration of Foreign companies MAT insurance, report of insurance operations with foreign insurance companies, regulations in order to enforce prohibitions, control of money laundering).

• Continuous search for higher levels of education to the consumer (regulator, government, universities, schools, etc.)

• Avoidance of fiscal asymmetries.

• Agreements between supervisors from different countries

© Lloyd’s 2012

< Picture to

go here >

Internationalisation EXPERIENCE OF Grupo Sura as a transnational company in emerging markets David Bojanini President, Grupo Sura

© Lloyd’s 2012

< Picture to

go here >

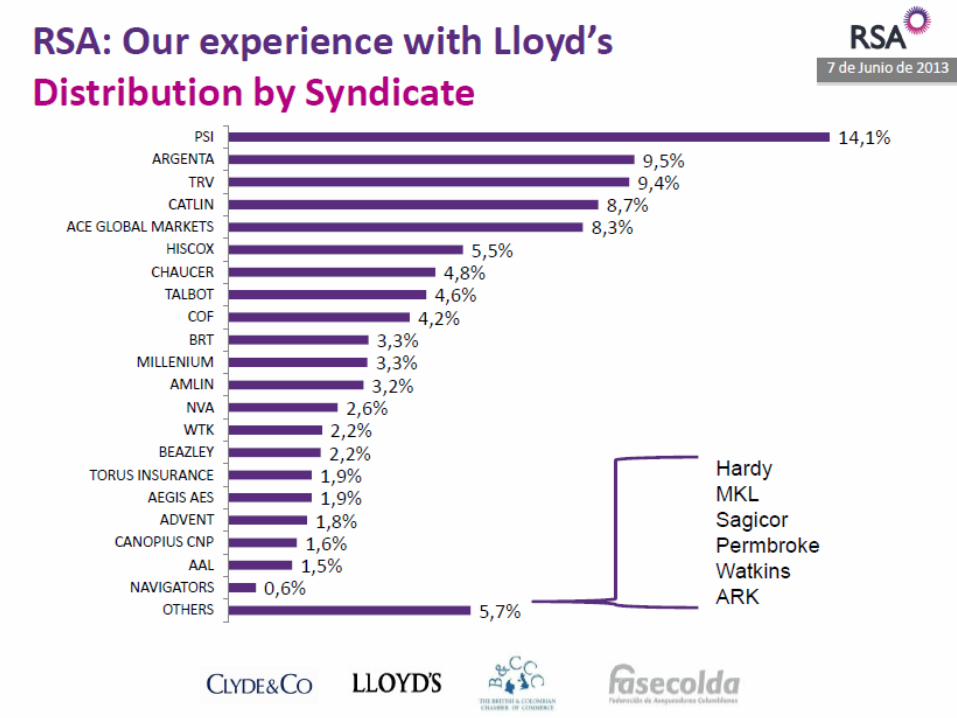

Experience of a british company in the Colombian market LILIAN PEREA President, RSA

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

© Lloyd’s 2012

< Picture to

go here >

Experience of a foreign insurance company in Colombia: Lessons and challenges Juan Carlos Realphe Vice President, Mapfre colombia

7 de Junio de 2013 Our History

1984

1993

1995

1999

2003

Seguros Caribe receives first investment

from MAPFRE INTERNACIONAL.

MAPFRE INTERNACIONAL becomes

the main Shareholder of Seguros Caribe.

Seguros Caribe changes its name to

MAPFRE SEGUROS GENERALES DE

COLOMBIA

MAPFRE COLOMBIA VIDA SEGUROS

S.A. begins operations.

Integration Process of MAPFRE

GENERALES and MAPFRE VIDA.

7 de Junio de 2013 MAPFRE COLOMBIA |

Written Premiums: 2012 USD750 million

Pre-tax Profits: USD21,2 million

Equity MAPFRE Life: USD83,2 million

Equity MAPFRE Non Life: USD55,8 million

ROE: 12,12%

Employees: 787

National Network: 173 branches

Retail Business Brokers : 2.130

7 de Junio de 2013 Lessons……

• Corporate Culture, Values, Core Business

• Market Knowledge

• Colombia: Professional Insurance Market

• Local Team Operation

• Empowerment, Autonomy, Delegation

• Reliability and Trust – Brokers

• Close Relationship with Insured (Clients)

• Specialized Corporate Clients

7 de Junio de 2013 Opportunities and Challenges……

• Low Penetration 2,48% of GDP (10% Family Housing,

5% Life, 28% Vehicles)

• Economic Growth – High Demand

• Financial Incursion, Microinsurance

• Infrastructure Projects Insurance

• Agricultural Development – Climate Change

• Market Liberalization

• Legal Environment - Requirements

• Sustainability: Information, Financial Education,

Financial Consumer Protection

7 de Junio de 2013

Thank You

7 de Junio de 2013 Colombia Infraestructura…..

7 de Junio de 2013 Colombian Agriculture…….

© Lloyd’s 2012

< Picture to

go here >

Role and responsibility of a broker with the british market Humberto Caberra President, Aon benfield colombia

© Lloyd’s 2012

< Picture to

go here > Coffee Break

© Lloyd’s 2012

< Picture to

go here >

British Perspective of colombian market, reinsurance Chair: GABRIEL ANGUIANO, LLOYD’S

© Lloyd’s 2012

< Picture to

go here >

Bridging the two markets, existing practice and challenges for the future Chair: Peter Hirst, Clyde & Co

© Lloyd’s 2012

< Picture to

go here >

Closing remarks nigel luson, chairman, british & colombian chamber of commerce in london

© Lloyd’s 2012