pilgrim bancorporation - dallasfed.org/media/documents/banking/nic/fry-6/2016/...title: pilgrim...

TRANSCRIPT

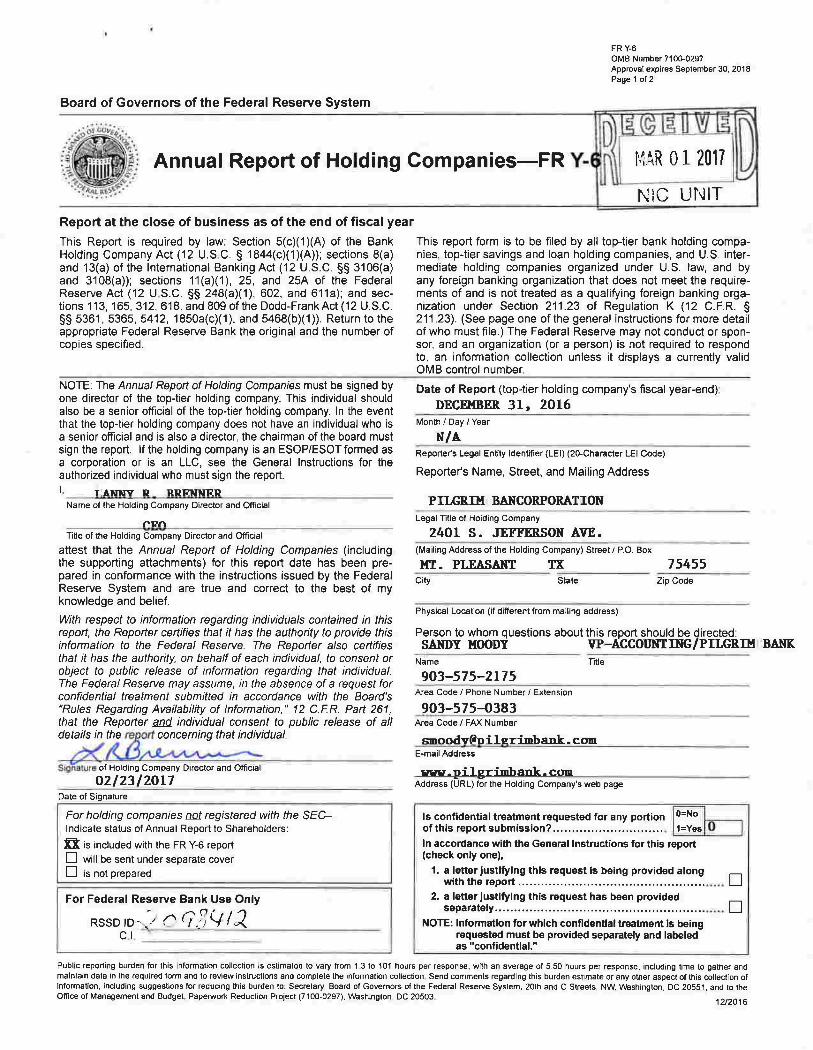

Board of Governors of the Federal Reserve System

Annual Report of Ho ding Companies-FR

Report at the close of business as of the end of fiscal year

This Report is required by law; Section 5(c)(1)(A) of the BankHolding Company Act (12 U.S C. S 1844(c)(1XA)); sections 8(a)and 13(a) of the lnternational Banking Act (12 U.S.C. SS 3106(a)and 3108(a)): sections 11(aX1), 25, and 25A of the FederalReserve Act (12 U S.C. SS 248(a)(1),602, and 611a); and sec-tions 113, 165, 312, 618, and 809 of the Dodd-FrankAct (12 U.S.C.

SS 5361, 5365, 5412, 1850a(cXl), and 5468(b)(1)). Return to theappropriate Federal Reserve Bank the original and the number ofcopies specified.

FR Y-6OMB Number 710G0297Approval expires September 30, 20 18

Page 1 ol 2

This report form is to be filed by all top-tier bank holding compa-nies, top-tier savings and loan holding companies, and U.S. inter-mediate holding companies organized under U.S. law, and byany foreign banking organization that does not meet the require-ments of and is not treated as a qualifying foreign banking orga-nization under Section 211.23 of Regulation K (12 C.F.R. S211 .23). (See page one of the general instructions for more detailof who must file.) The Federal Reserye may not conduct or spon-sor, and an organization (or a person) is not required to respondto, an information collection unless it displays a currently validOMB control number

I',l\R 0 1 2017

NIC UT{IT

NOTE: The Annual Repoft of Holding Companies must be signed byone director of the top-tier holding company. This individual shouldalso be a senior official of the top{ier holding company. ln the eventthat the top{ier holding company does not have an individual who isa senior ofiicial and is also a director, the chairman of the board mustsign the report. lf the holding company is an ESOP/ESOT formed asa corporation or is an LLC, see the General lnstructions for theauthorized individual who must sign the report.l, r-lrruv n RRENNF-R

Name oI the Holding Company Direclor and Official

rrEflTitle of the Holding Company Director and Official

attest that lhe Annual Repoft of Holding Companies (includingthe supporting attachments) for this report date has been pre-pared in conformance with the instructions issued by the FederalReserve System and are true and correct to the best of myknowledge and belief.

With respect to informalion regarding individuals contained in thisreport, the Repofter ceftifies that it has lhe authoity to provide thisinformation to the Federal Reserye. The Repofter also certifiesthat it has lhe authority, on behalf of each individual, to consent orobject to public release of information regarding that individual.The Federal Reserve may assume, in the absence of a reqLtest forconfidential treatment submitted in accordance with the Board's"Rules Regarding Availability of lnformation,' 12 C.F.R. Parl 261 ,

that the Repofter and individual consent to public release of all

Date of Report (top-tier holding company's fiscal year-end)

DECETAER 31, 2016Month/Oay/Year

N/AReporteis Legal Entity ldentifier (LEl) (2Gcharacter LEI Code)

Reporter's Name, Street, and Mailing Address

PII.GRI}T BAI{CORPORATIONLegal fitle of Holding Company

2401 S. JETFERSON AVE.(Mailing Address of the Holding Company) Street / PO. Box

IfT. PI.EASAIIT IX 75455City State Zip Code

Name 'lltle

903-575-2L75Area Code / Phone Number / Extension

903-575-0383Area Code / FAX Number

Physical Location (if different from mailing address)

Person to whom questions about this report should be Qirected:SANDY UOODY W-aCCOUt{TrItG/PrrCRrU BANK

details in the conce rn i ng th at i ndivid u al. smoodv@oilerimbank- coltrE-mail Address

of Holding Company Director and Official srs-oil.qrimbank.como2l23l2OL7 Address (URL) for the Holding Company's web page

Date of Signature

For holding companies not registered with the SEC-lndicate status of Annual Report to Shareholders:

fr is included with the FR Y-6 reportE will be sent under separate coverE i. not prepared

For Federal Reserve Bank Use Only

RSSD rD_ ,, r^ e:1,y1 I ecl

Oflie of Management and Budget. PapeMork Reduclion Proiect (7100-0297), Washington, DC 20503 :2tZO16

0=No

1=Yesls confidential trsatment requested for any portionof this report submission?...ln accordance with the General lnstructions for this report(check only one),

1. a letter iustlfylng this request ls being provided alongwith the report ..........

2. a letter Justifying this request has been providedseparately.,...

NOTE: lnformatlon for which confidential treatment ls beingrequested must be provided separately and labeledas "confidential."

trtr

E"(o

Eqlll -L citIEL6ro>erE=E$l.l.cl

'(U

Eo.C,

oc,

E-o=a

Eo-cooc.oo.Ncoo)Lo

LoEo-c0)oEoo.=oLoto-ooo--oo-J(uccOCE(I,ooE€gb(l)>agu, <)

Qofi .o() E;Fofi8oEECFtU

oTUaoEE==YoELoo,Loo-o)LooEo),:=qoL

oC.9.

O-d]oEF

trtooloE sEo O-s6x8EiE.C

f;3 EEb o'Bx io-=

-oNE(,=Eoo-o)t

oNEo=Eoo-otr

Egtafd..itrr

(Da

tlrEolJ-

3su)l'r)(U-Fa X

iE re P,

Ef ;ile,qE E EE-6* 8*c

+j-

zOro

Ee sI *P,t *.czOSoO2'-; *1< 6 hrxtr H E-.'SoroEr c

3E-o-

Hrep.6FUJ

fr.==6Eg'_(!:p,6ul= o-JEEu-(L-

Yz<rob==E(,

o-

logE fi-amP,CDx c7ro E O'-l

QEF-EY=fEE;x E E-

E# 8a-i c

=

a5EEc

;6

eEEo!

o

z

o

T

z

z

T

I

=g

z

=us

2

=o

E

z

Io

z

u

!I2

Ti

z

o

xIz

T

I

=g

z

z

=o

I

z

g

T

E

cz

T

I

z

dg

T:T

z

Ii

z

:g

I.!E

z

!r=i

z

o

IE

z

EI

Eo!

=I5zE6;'-)=z5cU

ts

c

=

FF

cc4

EoE2=

oEzl

YcE-=

E

oE2I

F

aEz=

ts

oEzl

E

Ezf

aEz=

F

oEzf

koEzf

atsz=

ts

cz

r3

Er9:

!a

EI

E2

E4:H

i9:E

I

g

-=

t

o

=gzfo

t,9:t

=cE

;o

Er

2cczE F

E;

F E

F

oTts

=a

t

!

E

-

E

fFs

E

d

=o

I

zcz

E

zoIz

=:

!a

Ea!:

F

I(tI9-

3ge

E

tsx I o

sF

I I

T

:

1Et

E!

3

:T I

:'E

,8

=

3F

tflI!i{

IIs

5I:

T

:

fitj

E

T

:

E

I:

I:

iod

n

2

EE

iq6qcb

E*i-qET

8E5E!fa,tJI;s-9

SFIgE=

E6

;:3:EEied*>ECEt;?!stp5ed

g>9E>t

Ei€9tiil hEi,EE

i-E.9=

EIet

!ra

iIrg!:tsi!E9d!EJ{ :-9

EE

Er's6lp

5ogE iEE E

8E Ed:4-dsH

Hss

x

co

s

-s

.*o

5T

E

P

cE

o

g'

aEz

ojz==9o

t3,!

r:.aEB

c.-9

o

I

!

siF

d

=loir

3.

3

a

t

E

g'

cI

Ea

E6:E

sg

EO92>6qiE:8E3#ED

6sEe,E!?EITEi ',5

cE S

;E b@

!6 5gi +rB I5E

=PFO E

t;1E;s-E€f;€s:acEg;itI6*<rra*E:!o o'8-95.PErEv- atsocxo

i 0.6 b o

E*';EE!I!sE!iIEE. E os F

EgEFfc*=gt? F: tsE9-!:!:--! ae5i5eET EETd E9 E S

Ei{Ei5:;b;;€:EtO E q d-

E€:ifE tei o

EIEiEHfEt;iS;€J=E

'ot!

.9t

o

EEf,g_EeErE

SEEEb.EEflEs-rTE E

ls E

5€r'H! EH= iEl : *

2

3iaaz-o.UE

!.ERflEE2ooB-troO!oE:E=iE!

EEIEEE!gEP

e8!:[:.ENT:!o

!fi

3E

PIoE.Do.;.=

L(J!-O:'u)=io)Ld,EE.F OE=,>l'aP?ts(D -'= (,-U)aONP6ER=<6.:o-" tr oYE.=OJ 69ro,PLairE:-E<oQ;:aE E 5E-L)F

Btb g do* F h 5

iP ET EO_ O .t/, O- O

?9s- S6 q.=5 e?

P T FE S;-Y*EU,!btv.E_oYs B qE E Fj

H q E EP*\LILE6'o - o).. cr)

x?*E=H!LJ-FL

.:z -9 ! z' '='-gt Hifl=cE€6;9I >! n' 6Eb:N F€E?PH!Eb I s? 5 BeHE#Ett33e€uECrtc\OoQF(0/^!-(1)+-RXE F"es r Afi

= E

2- - tf)!?i

EEEEE,i

Eobc=!* 3b(, o)s

J.=O,E5qF >(f)

bPbOEENc 6O r;l:fr5 E3ar J2 t-EA-

;E =

(ro..?p aL!!'+(UF O-'a c. VtO HEN d)- aoEi;XaE?E Od=EEE:*!-co ol-c cEoo-(o o}ioa6>- o t.ll-o(,EEgEcl-:z Q .b.Ea si,D j o)cESEFOFU)ooJ 0)oE-chF ovr (D

Er?e(Uv (,)

5S emO!i.i ot o(On-(f)n oN; (l).^ \-/ O-

rEu)E9!c E'=

gooE

. ob6 EsI o-o)E orc!F C(fJ

hE bOorES8ER EIo- c irjYE(o; EgEPc'_ (,, >F=6a- ^,

E BE:!oF+a

E2EI HEKr 3IorE=oq)i?;(Doj:=Sorgb5=5E:O raioo6BE'oauio_C,,?;- o-i-J o-Eo IirjocEEEFOtrU)EoJ oo(f-c=F o-u oEnE(Ev (,5S c-o!i..i el o(On#(f)n oN;i (1)

E; frE5 Y6E!c 6';

ED@EFERLlJ -E(,)IELo,o>f(E=

EHlI.O

9ooaEoEEoo+O-oEaaEboc-c>a6(O -o(O o\$o,OrqlOrNr

oN

a.f

.4Eaco).N.=()

o-cloo

riN

Nl<ooacoEEooo .o-o -c.EPoo-cca>OrO(O -o@o\.{ F-KocNO)

dN

a.f

.4EU'Co.N=ooDCloo

riN

=lzC)oacoEEoOoo_oEaaoq)SEa>OrO(O -o@o\^- f.-KoqNO,

oN

U)j.4-coEq).N/oo.cfoO

YooU)CoEEoC)

ooA'=Ebsb(,F<oX@_ss(oN r.-@- c.jr@

-:o

a.f

.4_caEo).N=oobcloO

--o

ciN

Lo

=oo-E

=oLoE

oslr)

oU'o).CEoELoEEoo1r)o_l5qbSc}Po.=-EEb=(U)vo=>\EE-a4:G

E9(,o)d-,.=

OE5eh9=ag

oBoo-E'=

EoEosro

oao).cootoEcooo-

!ao

=o

=o(DOlD-6?.CN0)rL

Eb2frco)E6=>rr O

U'ooo-cao)'=fooU)

c.j

Eo=Eoo-q)v.

trrooroE sEolt'g6x3Ei33 EEo o

E,N :o-=

(oI

tr.l!Eolr

@@(oEtr).= r..-

9x(LFvE9;><t_er

(o@g(O

(Dlocl-cg)xmFEP>=:m_sE

riN

xFAt,o_co-(o(Eu)/i (Ev()

9o-o;@>

(O@(o

trrO.= F-

9x(LF<E-o?=(h

_eE

(f,

dN

dN

ci

N

soocoz

€*sss=ooooxoooo:----€SleSSHEgEE

sooooz

@coz

oo60Be-bSz

oEoz

o0z

s*oooo{s Pxoo=sz

oJJ

o@

EY.ao

eo

=fEgo

EiE*qgo

E;? EJ!-6

e E,6Ppi5b.q6EaE*CPR_evtscov F.Q

H=lE t"*3;?: E

HE'g EEP83 E

=HEH EE

E,EE frEN60fooooro

Poz;i!!

. 5go -9E

*u 6hQuBi€ E,H E

E^aa$9e S-€o ELOe >!D

3=EtBp.'-o & .E

}FEpE6EEE:383E=8es;F

E EE E 91gd 8d-.3<!o! o 69 0 d oE :,660foooooro!

oooEc

e€

d.6cO.Ed=Eoo=o

ofcoB,EoEfa

c@

EosYo.

_qEe@ciE8o--EEg-eE<cOU?rUL

o6g

3gAE:iD- -g E

u5rE^ E.Ei'Eoyoccc

o

oFf

o99.4td,cO

EE e306o=o

olEo3o66l

o6o 'do

o >EEo tgO C = [ .\

€iE e=AL= >E

Eo;o

E€!o@I=vaEtrE 3o-

-'=o >o-Y 6 0

SEfEo

6

.sGeo-EoL-ror.9<

, E.;bXE<EOud

.t!>6

of96o or= o!leEZo60>oo!

t6

_ Ea g

E IE Eg

e EEeefe !u-r=Eheeie+EEFEPEE>cIcccF

EoEooE}oOE€uBooE(J

otozoo@oogcccaooooozzzzz

so@

ocoz

Doo

sssssoQoo@ooooooooo

ocoz

Noo

ocoz

soo

s3o

ocozoEoz

oEoz

s8o

s@Nri@

oJJoOio

;--c

6kdazob.FEEE i(,co

pE6 ).,oFp;Eg*Do-6 h-

. e89No()o6=o6,=FFU6uzd

co6E.Ego

EIGxCFo,YEol

-98

E,EFg9aBEE

8xOF6.oz=$E9fr;

EETa'

E:YL

.9x]Fo-->3ci g8da-6-

cXIF

=o=;=EEC

EEx6-8E=;-qEoo

E6XCFf.

6gdD99id

tsoEEra--c33troEE.9-n=

xGtr63EEEao=

Ea

EH<gECOJli=

EE.9vdlj<0of

-i.s

IogeHFts6OEp.E90ta*

o6pi5c@poo

@!6ECL

66

opi5

tr@EE

-9E

bE,Hr€E9d!D603E EE

oco2

o66

ecom

Egi5g

dodE>oq -@: z.=HOaLOC

?coobEHE5d_

.5oJoct;EEGO

IE66

ob

EgET

o

eo

a9ii o-p66E65B6

I.E9^UJEE9EE'Es-c

eoEUcG

.EEE()

oop

aoUo

oco6

Pxo-.6bEO>gcdc_9=

c6EoGo

?co6

5Ened -E)

5E*

cdmF-c

Ir

cdoE

-eir

bE6

?cGE

OEficEgi5g

o6o

ooooooooooPEEEEi56666o.qo

Eoq

o

tocd

o

66

oot

@

EoEo

coE

@

=ooeoa

oUto6Ep@E.

ri

,IB=oI!ooE.

[email protected]!-lll -GL60>Ea6.ErrO

!!@Ee85LO

ERc-

EQeh6E8Eo@

!'g soFi}

coE(J

8*6S

Gesol= l

.63ooEE

^6O-z<

EEEzo6^883:8EE

oPooEBe

:F€E

E'5aEtsEEbP

asE

€ sIi€:638Eb o=-E tE=

-EoEoaoE

Id.LEoL

-oCTe6o!

8;oo

.8Eoic=

dro?

F-fi

*

Io2

'sEo

E5EE.tG,ct,0,E.,E,

.E.o-E.6,

:i.EoE.

E&.

IeEtEoE

x,E.,oo.E

EI

.1.EI

BE3E.EhoI

Er$EE8Ar e,

ErgEgo

.6: ()

EGI

E",F;EE,r

3E*

c8EP

^.58iz<

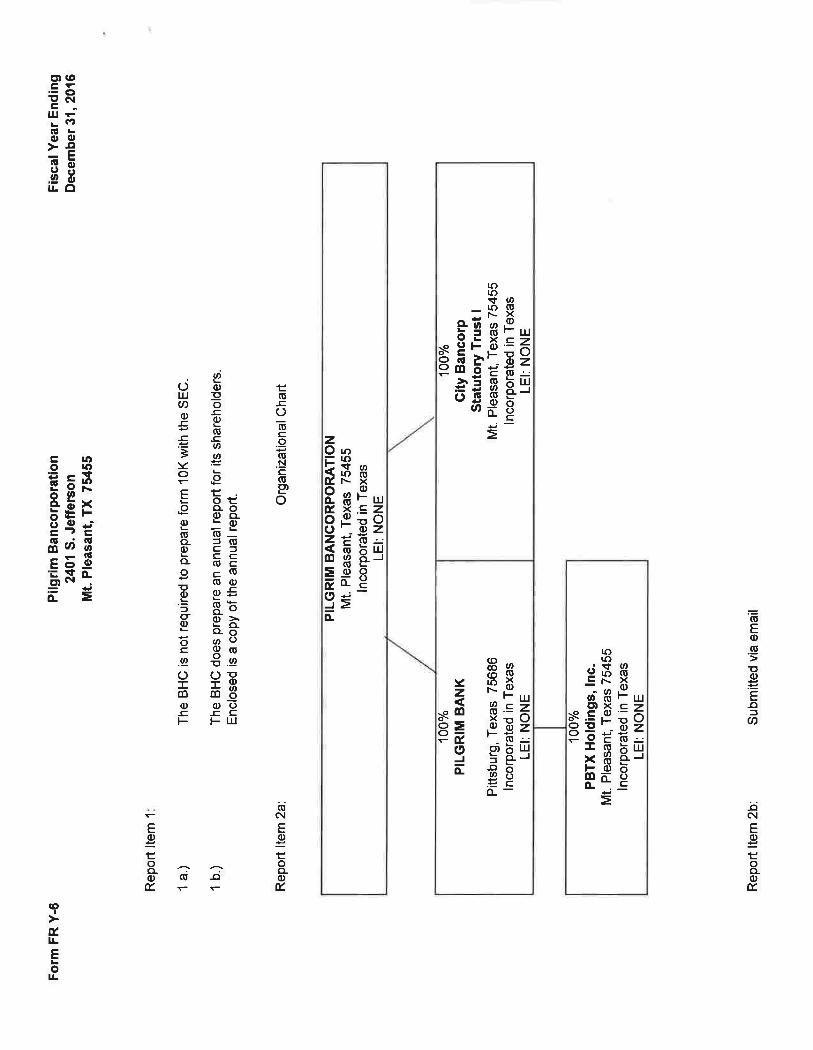

PILG RIM B ANCORPO RATIO NATVD SUBSIDIARIES

CO,VSOITDA TED Fl N ANCIAL STATEMENTS

December 31,2016 AND 2015

I

TABLE OF CONTENTS

lndependent Auditor's Report........

Consolidated Balance Sheets........

Consol idated Sfafements of I ncome and Comprehe nsive I ncome.........

Consolidated Statemenfs of Changes in Stockholders' Equity..

Consolidated Stafements of Cash Flows..........

Nofes to Consolidated Financial Sfatements

lndependent Auditols Report on Additional lnformation

Addition al I nformation

Consolidating Balance Sheets

Consolidating Sfatements of lncome and Comprehensive lncome

Page

1

,2-3

.4

tr

.6-7

.8-24

.26

27-28

29-s0

judd thomascertified public accountants & advisors

I N DEP EN D ENT AU DITOR'S REPORT

To the Board of Directors and Stockholdersof Pilgrim Bancorporation and Subsidiaries

We have audited the accompanying consolidated financial sfatements of Pilgrim Bancorporation andSubsrdraries (a Texas corporation), which compise the consolidated balance sheets as of December 31, 2016and 2015, and the related consolidated statements of income and comprehensive income, changes instockholders' equity, and cash flows for the years then ended, and the related nofes to the consolidatedfinancial stafements.

M a nag e m ent's Respon si bi I ity to r the F i n a n c i al StatementsManagement is responsib le for the preparation and fair presentation of these consolidated financial statementsin accordance with accounting principles generally accepted in the United Stafes ofAmeica; this includes thedesign, implementation, and maintenance of internal control relevant to the preparation and fair presentation ofconsolidated financialstatemenfs that are free from material misstatement, whether due to fraud or error.

Au dito r's Respon si bil ityOur responsibility is to express an opinion on these consolidated financial statements based on our audits, Weconducted our audits in accordance with auditing standards generally accepted in the United Stales ofAmerica. Ihose standards require that we plan and pertorm the audit to obtain reasonable assurance aboutwhether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disc/osu res in theconsolidated financialsfatements. The procedures se/ected depend on the auditofs judgment, including theassessment of the risks of material misstatement of the consolidated financialstafemenfs, whether due tofraud or error. ln making fhose risk assessments, the auditor consrders internal control relevant to the entity'spreparation and fair presentation of the consolidated financialstatements in orderto design audit proceduresthat are appropriate in the circumstances, but not for the purpose of expressing an opinion on theeffectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includesevaluating the appropriateness of accounting policies used and the reasonableness of significant accountingestimafes made by management, as well as evaluating the overall presentation of the consolidated financialsfafemenfs.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for ouraudit opinion.

Opinionln our opinion, the consolidated financial statements referred to above present fairly, in all material respecfs,the financial position of Pilgrim Bancorporation and Subsidianes as of December 31, 2016 and 2015, and theresu/fs of its operations andits cash flows for the years then ended in accordance with accounting principlesgenerally accepted in the United Sfafes of America.

Dallas, TexasJanuary 27,2017

II

+-

judd thomas.com12222MeritDriveSuite 1900Dallas, TX 75251-3209

214.296.0900 Main800.304.4887 Toll Frce972.651.3651 Fax

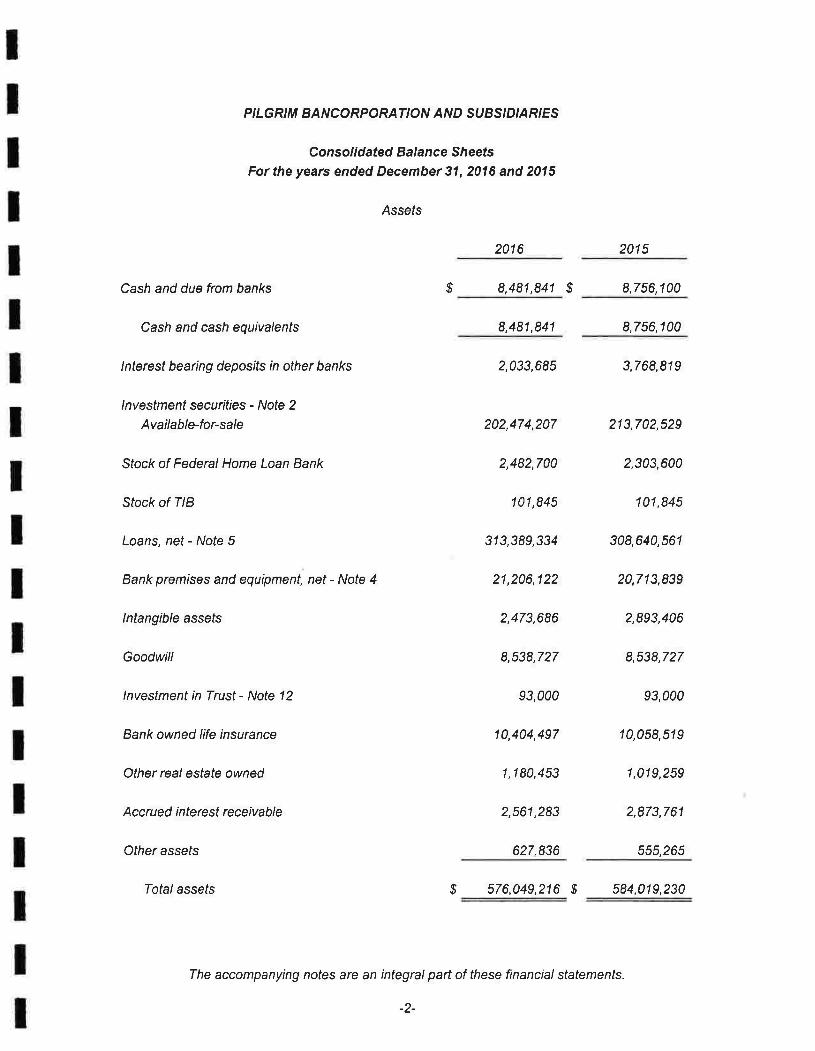

PILG RIM BAN CO RPO RATI O N AIVD SUBS I DIARI ES

Consolidated Balance SheefsFor the years ended December 31 , 201 6 and 201 5

Assets

201 6

Cash and due from banks

Cash and cash equivalents

lnterest bearing deposifs in other banks

lnvestment securities - Note 2

Available-for-sale

Stock of Federal Home Loan Bank

Stock of TIB

Loans, net - Nofe 5

Bank premises and equipment, net - Note 4

lntangible assets

Goodwill

lnvestment in Trust - Note 12

Bank owned life insurance

Other realesfafe owned

Accrued interest receivable

Ofher assets

Iotal assefs

201 5

$ 8,481,841 $ 8,756,100

8,481,841 8,756,100

2,033,685 3,768,819

202,474,207 213,702,529

2,482,700 2,303,600

101,84s 101,84s

313,389,334 308,640,561

21,206,122 20,713,839

2,473,686 2,893,406

8,538,727 8,538,727

93,000 93,000

10,404,497 10,058,519

1,180,453 1,019,259

2,561,283 2,873,761

627.836 555,265

$ 576,049,216 $ 584,019,230

The accompanying notes are an integral paft of these financial statements.

-2-

PILGRIM BANCORPORATION AND SUES'D'AR'ES

Co nsolidated Bala n c e SheefsFor the years ended December 31, 2016 and 2015

Liabilities

2016 201 5

Deposrts;

Noninterest-beaing demand

I nterest-beaing demand

Money market and savings

Time, $100,000 and over

Iime, /ess than $100,000

$

Iotal deposits

Notes payable - Note 3

Trust prefened payable

Accrued i nterest payable

Other liabilities

Total liabilities

Stockholders' Equity

Common stock - $1 par value; authorized

4,000,000 shares in 2016 and 201 5,

respectively; 2,237,967 shares lssued

and outstanding in 2016 and 2015, respectively

Additional p aid-in capital

Retained earnings

Unrealized garns (/osses) on investment securitres

considered available-for-sale - Note 2

Total stockholders' equity

Total liabilities and stockholders' equity

456,257,196 472,148,788

53,400,000 47,325,000

3,093,000 3,093,000

167,412 152,050

715,684 450,407

513,633,292 523,169,245

2,237,967 2,237,967

27,562,785 27,562,785

36,068,507 33,005,411

(3,453,335) (1,956,178)

29,985,825 $9,506,811

281,387,4E3

84,496,797

50,880,280

30,667,234

11,048,050

289,926,382

85,663,429

54,843,693

62,415,924 60,849,985

s 576,049,216 $ 584,019,230

The accompanying notes are an integral paft of these financialstatemenls.

-3-

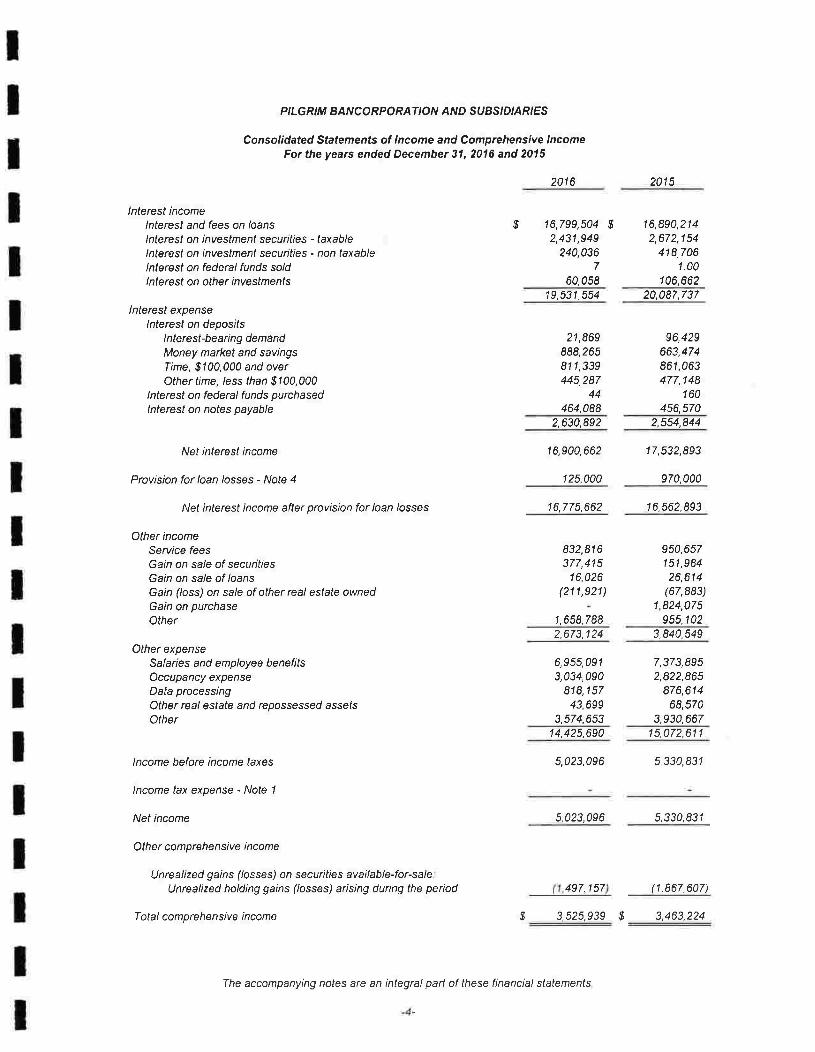

PILGRIM BANCORPORATION AND SUBS'D'ARIES

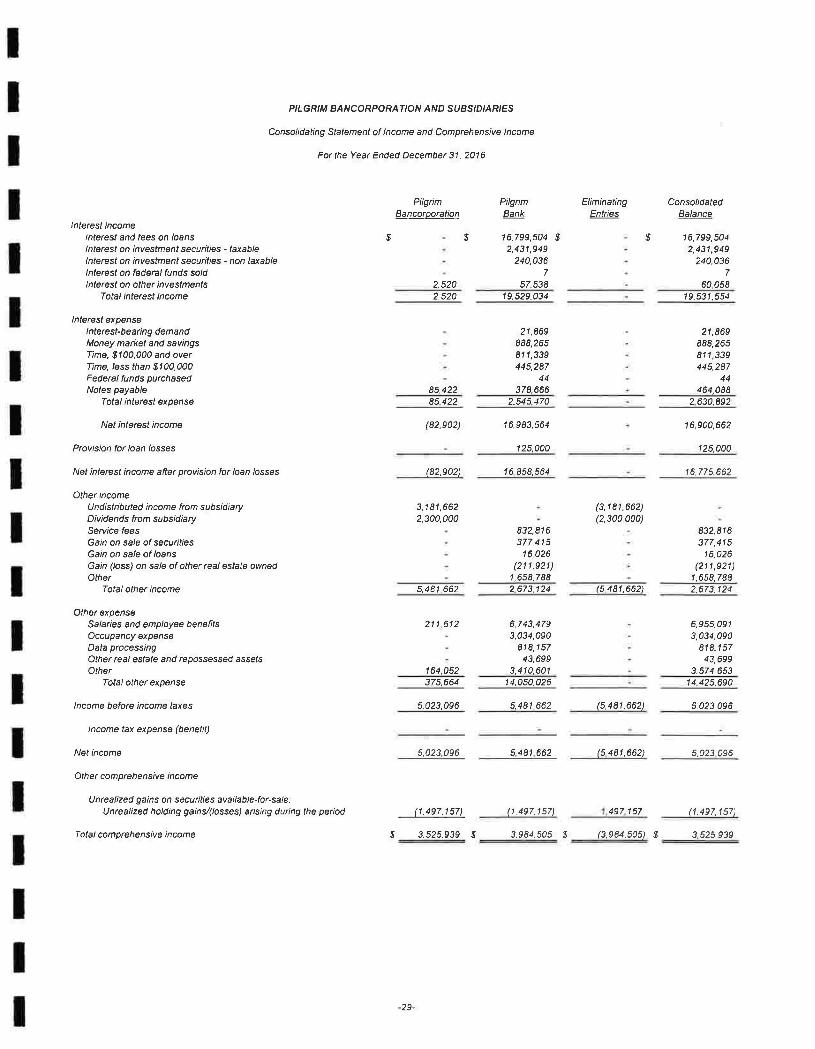

Consolidated Statements of lncome and Comprehensive lncomeFor the years ended December 31 , 201 6 and 201 5

201 6 2015

lnterest incomelnteresl and fees on loanslnlerest on investment securilles - taxablelnterest on investment securities - non taxablelnterest on federal funds soldlnterest on other inveslments

lnterest expenselnterest on deposfis

I nterest-be aring demandMoney market and savingsTine, $100,000 and overOther time, /ess than 5100,000

lnterest on federal funds purchasedlnterest on notes payable

Net interesl income

Provision for loan /osses - Nole 4

Nel rnterest income after provision for loan losses

Other incomeService feesGain on sa/e of securitiesGain on sale of loansGain (loss) on sale of other real estate ownedGain on purchaseOther

Other expenseSa/aries and employee benefitsOccupancy expenseData processingOther real estate and repossessed asselsOther

lncome before income taxes

lncome tax expense - Note 1

Net income

Other comprehensive income

U nrealized g ains (/osses) on secu rities avai I able-for-sal eUnrealized holding garns (/osses) arising during the period

Total comprehen sive income

14,425,690 15,072,611

5,023,096 5,330,831

5,023,096 5,330,831

497.1 57 (1,867,607)

s 3,525,939 $ 3,463,224

$ 16,799,504 $2,431,949

240,0367

60,058

16,890,2142,672,154

418,7061.00

106,66220,087,73719,531,554

21,869888,265811,339445,287

44464,048

2,630,892

16,900,662

125,000

96,429663,474861,063477,148

160456,570

2,554,844

17,532,893

970,000

16,775,662 16,562,893

8s2,816377,415

16,026(211,921)

950,657151,98426,614

(67,883)1,824,075

955,1021,658,7882,673,124 3,840,549

6,955,0913,034,090

818,15743,699

3,574,653

7,373,8952,822,865

876,61468,570

3,930,667

The accompanying notes are an integral parl of these financial slatemenls

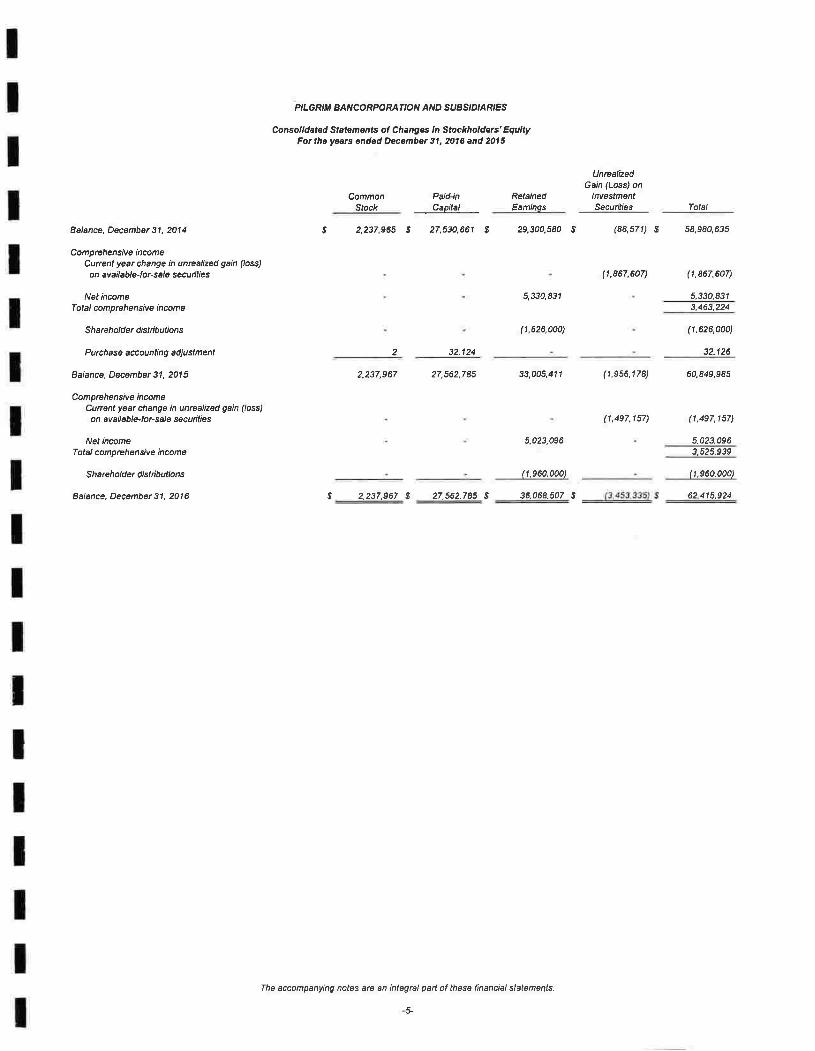

PILGRIM BANCORPORATION AND SUAS'D'AR'ES

Consolldated Stelements of Changes ln Stockholdets' EqullyFot the yeats ended Decembet 31, zua and 2015

ComfionStock

Paid-inCapital

RetainedEdminos

UnrcalizedGarn fLoss) on

lnvestmentSecunf,'es

Ealance, December 31, 2014

Comprehensive incomeCurrenl year ahanga in unrealized gain (loss)

on av ail able-t o r- sare secunlies

Net incomeTotal com p reh en siv e incom e

S h areholder clistib u uons

Pu rch a se accounting adju slmen I

Balance, Oecembet 31, 2015

Comprghensive incomeCuftant year change in unrealizecl gain (loss)

o n ava il abl*lo r- sa,B secunlies

Net inameTotal co m p reh e n siv e income

Sh a reholder di stribution s

Balance, Oecembet 31, 2o16

Tolal

$ 2,237,965 8 27,530,661 I 29,3OO,58O $ (88,571) S 58,980,635

(1,867,607) (1,867,607)

5,330,8i1 5,330.8313,463,224

(1,626,000) (1.626,000)

32,124

27,562,7E5

32,126

2,237,967 33,005.41 1 (1,956,178) 60,849,985

(1,497,157) (1,497,1 57)

5.023,0965.023,0563,525,939

(1,960,000) (1,960.000)

$ 2,237,967 $ 27,562.785 I 36.068.507 $ a2 415.9?4

The accompanying notes are an integral pad ot |l,ese linencial slatemenls.

2

F

P ILG RIM B AN C O RP O R ATIO N A'VD SUES'DIAR'ES

Consolidated Stalements of Cash FlowsFor the years ended December 31, 2016 and 2015

Cash flows from operating activities:Net incomeAdjustments to reconcile net income to net

cash provided by operating activities:Depreciation and amortizationAmoilization and accretion of secuitiesAmoftization of intangible assefsProvision for loan /ossesLoss on sale and witedowns of other real estateLoss on sale of premises and equipmentLoss on sale of softwareGain on sa/e of secuntiesGain on sale of loansGain on purchase of bankStock dividend from FHLBChange in:

Ac c ru e d i nte re st rece iv abl eOfher assetsAccrued interest payableOther liabilities

Net cash provided by (used in) operating activities

Cash flows from investing activities:Net change in interest bearing deposits in other banksPurchase of available-for-sale investment secuitiesProceeds from principal payments and matuities

of available-for-sale investment secuitiesPurchase of Federal Home Loan Bank stockSale of Federal Home Loan Bank stockNet proceeds from sales of other real estate ownedNet change in loansPurchase of bankProceeds from sale of premises and equipmentPurchase of premises and equipmentPurchase of bank owned insurancePurchase of other intanglble assets

Net cash provided by (used in) investing activities

2016 201 5

$ 5,023.096 $ 5,3s0,831

1,212,7012,642,647

470,569125,000211,921

(377,415)(16,026)

(20,100)

312,478(87,525)15,362

265,277

1,178,0952,529,256

471,485970,000

67,883401,380

402(151 ,e84)

(26,614)(1,824,075)

(6,000)

(1,1s6,E46)1,156,829

(33,535)(1,190,355)

9,777 985 7,736,752

1,735,134(1s7,2s2,658)

144,718,592(1se,000)

130,553(5,361,415)

136,633,110(210,897,333)

136,081,301(es3,700)345,100230,324

(5,424,890)(24,000,000)

66,907(1,008,042)

(10,0s8,519)(1,705,043)

(345,978)(3s,837) (103, 850)

1 724 348 20,930,408

The accompanying notes are an integral paft of these financial statemenls

-6-

PI LG RI M B ANCO RPO RATIO N A ND SUBS I DIARI ES

Consolidated Sfatements of Cash FlowsFor the years ended December 31, 2016 and 2015

201 6 201 5

Cash flows from financing activities:Net change in demand and savings deposrtsNet change in time deposrtsProceeds from notes payable and FHLB advancesD istrib ution s to sh areholders/ssuance of stock

Net cash provided by (used in) financing activities

Net increase (decrease) in cash and cash equivalents

Cash and cash equivalents at beginning of year

Cash and cash equivalents at end of year

Supplementaldisclosure of cash flow information -Cash paid during the year for:

lnterest

lncome taxes

Supplemental schedule of noncash investingand fi n a nci ng activities :

Rea/ esfafe acquired in foreclosure or settlement of loans

32 126

(11,776,592) (23,894,899)

$ (10,761,547) $(5,130,045)6,075,000

(1,960,000)

(8,315,737)(32,685,288)18,700,000(1,626,000)

(274,259)

8,756,100

4,772,261

3,983,839

$

$ 8,481,841 $ 8,756,100

$ 2,615,530 $ 2,s88,379

$

503,668 $ 304.520

$ 242,699,092

$ (216,87s,017)

Assets acquired in bank acquisition

Liabilities acquired in bank acquisition

The accompanying notes are an integral part of these financial statements.

-7-

$

$

$

PILGRIM BANCORPORATION AND SUBSIDIARIES

Notes to Financial Statements

1. Summary of Significant Accounting Policies

Nature of Operations

The accounting and reporting policies of Pilgrim Bancorporation (the Company) and subsidiaries conform toU.S. generally accepted accounting principles and to general practices within the banking industry. Theconsolidated financial sfatemenfs include the accounts of the Company, the Company's wholly-ownedsubsidiaries, Pilgrim Bank and PBTX Holding, lnc., collectively referred to as "the Bank". lntercompanyaccounts, transactions and earnings have been eliminated in consolidation.

The Bank generates commercial, mortgage, and consumer loans and receives deposifs from customerslocated primarily in Nofth East and North West Texas and the surrounding areas. The Bank operates under astate bank charter and proyides full banking seryices. As a state bank, the Bank is subject to regulation by theIexas Department of Banking and the Federal Deposit lnsurance Corporation.

Effective January 8, 2015, the Bank purchased North Central Texas Bancshares, lnc and subsidiary,State Natlon al Bank of Texas. State Nation al Bank of Texas operates nine community banks,predominately in the West fexas regrcn.

Use of Estlmates

The preparation of financialstatements in conformity with U.S. generally accepted accounting principlesrequires management to make estimates and assumptions that affect the reported amounts of assets andliabilities and disclosure of contingent assefs and liabilities at the date of the financialsfatemenfs and therepofted amounts of revenue and expenses during the repofting period. Actualresults could differfrom thoseestimafes.

The determination of the adequacy of the allowance for loan /osses is based on estimafes that are pafticuladysuscepflb/e to significant changes in the economic environment and market conditions. ln connection with thedetermination of the estimated /osses on loans, management obtains independent appraisals for significantcollateral.

The Bank's loans are generally secured by specific items of collateral including real property, consumerassefs, and business assets. Although the Bank has a diversified loan portfolio, a substantial portion of itsdebtors' ability to honor their contracts is dependent on local economic conditions.

While management uses available information to recognize /osses on loans, further reductions in the carryingamounts of loans may be necessaty based on changes in local economic conditions. ln addition, regulatoryagencies,asanintegralpartoftheirexaminationprocess, periodicallyreviewtheestimatedlossesonloans.Such agencies may require the Bank to recognize additional /osses based on their judgments aboutinformation available to them at the time of their examination. Because of fhese factors, it is reasonablypossib/e that the estimated losses on loans may change materially in the near term. However, the amount ofthe change that is reasonably posslb/e cannot be estimated.

lnvestment Securities

Debt securities are c/assrfied as held-to-maturity when the Bank has the positive intent and ability to hold thesecuritles to maturity. Securifies held-to-maturity are carried at amortized cost. The amortization of premiumsand accretion of discounts are recognized in interest income using methods approximating the interest methodover the period to maturity.

Debt securities nof c/assified as held-to-maturity are classified as available-for-sale. Securities c/assifled asavailable-for-sale are carried at fair value with unrealized gains and /osses reported in other comprehensivetncome.

I

PILGRIM BANCORPORATION AAlD SUBSIDIARIES

Nofes to Financial Statements

1. Summary of Significant Accounting Policies, continued

Realized garns (/osses) on securities available for sale are included in other income (expense) and, whenapplicable, are reported as a reclassification adjustment, in other comprehensive income. Gains and /osseson sa/es of securities are determined on the specific-identification method.

Declines in the fair value of individual held-to-maturity and available for sale securities, below their cost thatareotherthantemporary,resultinwrite-downsoftheindividualsecuritiestotheirfairvalue. Therelatedwrite-downs are included in earnings as realized /osses. ln estimating other-than-temporary impairment /osses,management considers (1) the length of time and the extent to which the fair value has been /ess than cost,(2) the financial condition and near-term prospects of the issuer, and (3) the intent and ability of the Bank toretain its investment in the issuer for a period of time sufficient to allow for any anticipated recovery in fairvalue.

Loans

The Bank grants mortgage, commercial, and consumer loans to customers. A substantial porlion of the loanportfolio is represented by mortgage loans throughout East and North West fexas. The ability of the Bank'sdebtors to honor their contracts is dependent upon the realesfate and general economic conditions in thisarea.

Loans are stated at unpaid principal balances, /ess the allowance for loan /osses and deferred loan fees. Loanfee income and costs associafed with originating loans have been recognized in the period in which the feeswere received and the cosfs were incurred.

lnterest on loans is calculated by using the simple interest method on daily balances of the principal amountoutstanding.

The accrual of interest on mortgage and commercial loans is discontinued at the time the loan is 90 days pastdue unless the credit is well-secured and in process of collection. Personal loans are typically charged off nolater than 180 days past due. Past due status is based on contractual terms of the loan ln all cases, loansare placed on nonaccrual or charged off at an earlier date if collection of principal or interestis consldereddoubtful.

All interest accrued but not collected for loans that are placed on nonaccrualorcharged off is reversed againstinterestincome. Theinterestontheseloansisaccountedforonthecash-basisorcost-recoverymethod,untilqualifying for return to accrual. Loans are returned to accrual stafus when all the principal and interestamounts contractually due are brought current and future payments are reasonably assured.

Allowance for Loan Losses

The allowance for loan /osses is esfab/ished as /osses are estimated to have occurred through a provision for/oan /osses charged to earnings. Loan /osses are charged against the allowance when management believesthe uncollectability of a loan balance is confirmed. Subsequent recoveries, if any, are credited to theallowance

The allowance for /oan /osses is evaluated on a regular basis by management and is based uponmanagement's periodic review of the collectability of the loans in light of historical experience, the nature andvolume of the loan portfolio, adverse sifuafions that may affect the borrower's ability to repay, estimated valueof any underlying collateral, and prevailing economic conditions. This evaluation is inherently subjective as itrequires esfimafes that are susceptible to significant revision as more information becomes available

9

PI LG RIM BAN CO RPORATI ON AA'D SUBS I DIARIES

Notes to Financial Statemenfs

1. Summary of Significant Accounting Policies, continued

The allowance consrsts of specific, general, and unallocated components. The specific component relafes toloans that are c/assified as doubtful, substandard, or special mention. For such loans that are also c/assifiedas impaired, an allowance is esfab/rshed when the discounted cash flows (or collateral value or observablemarket price) of the impaired loan is lower than the carrying value of that loan. The general component coversnon-classified loans and rs based on historical/oss experie nce adjusted for qualitative factors. An unallocatedcomponent is maintained to cover uncerlainties that could affect management's estimate of probable /osses.The unallocated component of the allowance reflects the margin of imprecision inherent in the underlyingassumptions used in the methodologles for estimating specific and generallosses in the portfolio.

A loan is considered impaired when, based on current information and events, it is probable that the Bank willbe unable to collect the scheduled payments of principal or interest when due according to the contractualterms of the loan agreement. Factors considered by management in determining impairment include paymentstatus, collateral value, and the probability of collecting scheduled principal and interest payments when due.Loans that experience insignificant payment delays and payment shortfalls generally are not c/assffied asimpaired. Management determines the significance of payment delays and payment shortfalls on a case-by-case basis, taking into consideration all of the circumstances surrounding the loan and the borrower, includingthe length of the delay, the reasons for the delay, the borrower's prior payment record, and the amount of theshortfall in relation to the principal and interest owed. lmpairment is measured on a loan-by-loan basis forcommercial and construction loans by either the present value of expected future cash f/ows discounted at theloan's effective interest rate, the loan's obtainable market price, or the fair value of the collateral if the loan iscollateral dependent.

Large groups of smaller balance homogeneous /oans are collectively evaluated for impairment. Accordingly,the Bank does not separately identify individual consumer and residential loans for impairment dlsc/osures,unless such loans are the subject of a restructuring agreement.

Premises and Equipment

Premlses and equipment are carried at cost net of accumulated depreciation. Depreciation is computed usingthe straight-line method based principally on the estimated useful lives of the assets ranging from three to fortyyears. Maintenance and repairs are expensed as incurred while major additions and improvements arecapitalized. Gains and /osses on dispositions are included in current operations.

Other RealEsfafe Owned

Real estate properties acquired through or in lieu of loan foreclosure are initially recorded at fair value lessestimated selling cosf at the date of foreclosure, Any write-downs based on the assef s fair value at the dateof acquisition are charged to the allowance of loan /osses. After foreclosure, valuations are periodicallyperformed by management and property held for sale is carried at the lower of the new cost basis or fair value/ess cosl to sell. lmpairment /osses on property to be held and used are measured as the amount which thecarrying amount of a property exceeds its fair value Cosfs of slgnificant property improvements, if any, arecapitalized whereas costs relating to holding property are expensed. The portion of interest costs relatrng todevelopment of realesfate is capitalized. Valuations are periodically performed by management, and anysubsequent write-downs are recorded as a charge to operations, lf necessa ry, to reduce the carrying value ofa property to the lower of ifs cosf or fair value less cost to se//.

Goodwill

The Bank had $285,000 of goodwill on the books as a result of a branch purchase in 1997. Goodwill had beenfully amortized using the straightline method.

-10-

PILGRIM BANCORPORATION AND SUESIDIARIES

Notes to Financial Sfafemenfs

1. Summary of Significant Accounting Policies, continued

The Bank has $8,538,727 of goodwill on the books as a resu/t of the purchase of Community Bank inNovember 2007. Financial Accounting Standards Board Accounting Standard codification (FASB ASC) 350-20-35, "Goodwill and Other lntangible Assefs', stafes that goodwill shall not be amortized. Goodwill should betested for impairment annually, or more frequently if circumstances warrant.

The bargain purchase of North Central fexas Bancshares , lnc and subsidiary, State Nation al Bank of Texas,resulted in negative goodwill of $1,824,075, ln accordance with FAS 805-30, the negative goodwill wasrecognized as a gain in the current year. The Company paid $24,000,000 for the acquisition of assefs wtfh afair market value of $242,699,092 and liabilities of $216,875,017.

Additionally, core deposit intangibles totaling $4,278,000 were booked at the date of the purchases. Ihe coredeposit intangibles are amoftized over ten years and are included in other assets, net of amortization, at a netvalue of $2,473,686 and $2,893,406 at December 31, 2016 and 2015, respectively.

lncome Iaxes

Effective January 1, 2012 the Company elected S corporation sfafus, as of December 31 , 2011 alldeferred taxasset and liability balances have been eliminated. Earnings and /osses are included in the personal incometax returns of the stockho/ders and taxed depending on their personal fax strafegies. Accordingly, theCompany will not incur Federal income tax obligations, and the financial statements will not include a provisionfor Federal income taxes.

The Company is subject to routine audits by taxing jurisdictions; however, there are currently no audits for anytax periods in progress. Management believes it is no longer subject to income tax examinations for yearsprior to 2013.

Statemenfs of Cash Flows

The Bank considers all cash and amounts due from depository institutions to be cash equivalents for purposesof the statemenfs of cash flows. The Bank maintains balances at financial institutions rn excess of federallyinsured limits.

Fair Values of Financial lnstruments

FASB ASC 825-10-50, 'Disclosures about Fair Value of Financial lnstruments," requires disclosure of fairvalue information about financial instruments, whether or not recognized in the statement of financial condition./n cases where quoted market prices are not available, fair values are based on esfimates using presentvalue or other valuation techniques. Ihose techniques are significantly affected by the assumpfions used,includingthediscountrateand estimafes of future cashf/ows. lnthatregard,thederivedfairvalue estimatescannot be substantiated by comparison to independent markets and, in many cases, could not be realized inimmediate settlement of the instruments. FASB ASC 825-10-50 excludes cedain financial instruments and allnonfinancial instruments from its dlsc/osure requirements. Accordingly, the aggregate fair value amountspresented do not represent the underlying value of the Bank.

The following methods and assumptions were used by the Bank tn estimating its fair value disclosures forfi n anci al i nstru m e nts :

Cash and cash equivalenfs: Ihe carrying amounts reported for cash and cash equivalents approximate thoseassefs' fair values.

-1 1-

PILGRIM BANCORPORATION A'VD SUESIDIARIES

IVotes to Financia, Sfatements

1. Summary of Significant Accounting Policies, continued

Time deposits: Fair values for time deposlts are estimated using a discounted cash flow analysis that appliesinterest rates currently being offered on certificates to a schedule of aggregated contractual matuities on suchtime deposifs.

lnvestment secudtles: Fair values for investment securities are based on quoted market prices, whereavailable. lf quoted market prices are not available, fair values are based on quoted market prices ofco m p arable in stru me nts.

Loans: For variable-rate loans that re-price frequently and with no significant change in credit risk, fair valuesare based on carrying amounts. The fair values for other loans (for example, fixed rate commercial real estateand rental property moftgage loans and commercialand industrialloans) are estimated using discounted cashflow analysis, based on interest rates currently being offered for loans with similar terms to borrowers of similarcredit equity. Loan fair value estimates include judgments regarding future expected /oss experience and riskcharacteristics. The carrying amount of accrued interest receivable approximates its fair value.

Deposits: Thefairvaluesdlsclosedfordemanddeposits(forexample,interestbearingcheckingaccountsandsavtngs accounts) are, by definition, equal to the amount payable on demand at the repofting date (that is,their carrying amounts). The fair values for certificates of deposit are estimated using a discounted cash flowcalculation that applies interest rates currently being offered on ceftificates to a schedule of aggregatedcontractual maturities on such time deposits. The carrying amount of accrued interest payable approximatesfair value.

Shoftlerm borrowings and notes payable: The carrying amounts of short-term borrowings and notes payableapproximate their fair values.

Other liabilities: Commitments to extend credit were evaluated and fair value was estimated using the feescurrently charged to enter into similar agreements, taking into account the remaining terms of the agreementsand the present credilworthlness of the counterpafties

Classification of Prior Year AmountsCeftain prior period amounts have been reclassified to conform to current year presentation.

Date of Manaoement's Review of Subsequent EventsManagement has evaluated subsequent events through January 27, 2017, the date which the financialstatements were available to be issued.

-12-

PILGRIM BANCORPORATION AND SUBSIDIARIES

IVotes to Financial Sfafemenfs

2. lnvestmentSecurifies

The amortized cost of secudties and their approximate fair values are as follows:

Secunfies Available for SaleGross

UnrealizedGain

December 31, 2016Morlgage backed secunfiesMunicipal bondsTaxable municial bondsSBAsCorporate stock

AmortizedCosf

GrossUnrealized

Loss

EstimatedFair

Value

$ $ (3,5e8,000) $144,867

50,198(62,461)

12 061

$ 205,927,542 $ 207 126$ (3,660,461)$ 202,474,207

196,042,866 $5,176,686

500,0004,193,351

14,639

192,444,8665,321,553

550,1984,130,890

26,700

AmoftizedCosf

GrossUnrealized

Gain

GrossUnrealized

Loss

EstimatedFair

ValueDecember 31, 201 5Mortgage backed secuntiesMunicipal bondsTaxable municial bondsSBAsCorporate stock

191,383,222 $18,599,606

535,0005,126,239

14,639

$ (2,625,090) $667,586

69,394(80,207)

12,140$ 215,658,706 $ 749,120 $ (2,705,297) $ 213,702,529

The amortized cosf and estimated fair value of securities, by contractual maturity, at December 31, 2016are as follows:

Securitles Available for Sale

$ 188,758,13219,267,192

604,3945,046,032

26,779

AmoftizedCost

FairValue

Amounts maturing in:One year or /essAfter one year to five yearsAfter five years to ten yearsAfter ten years

$ 23,030,524 $61,211,34533,691,28187,994,392

22,567,68160,172,72033,051,75886,682,048

$ 205,927,542 $ 202,474,207

The maturities of the Mortgage backed securifles may differ from contractual maturities because borrowershave the right to prepay obligations without penalties.

Securities with carrying values of $91,326,407 and $87,385,714 at December 31,2016 and 2015,respectively, were pledged to secure a line of credit and other public funds as required or permitted by law.

Net unrealized gains (/osses) on available for sale securities amounted to $(3,453,335) and $(1,956,178) atDecember 31 , 201 6 and 2015, respectively, and were recognized as a decrease to stockh olders' equity.

-13-

PI LG RIM BANCO RPORATI ON AA'D SUBS I DIARIES

IVofes to Financial Sfatements

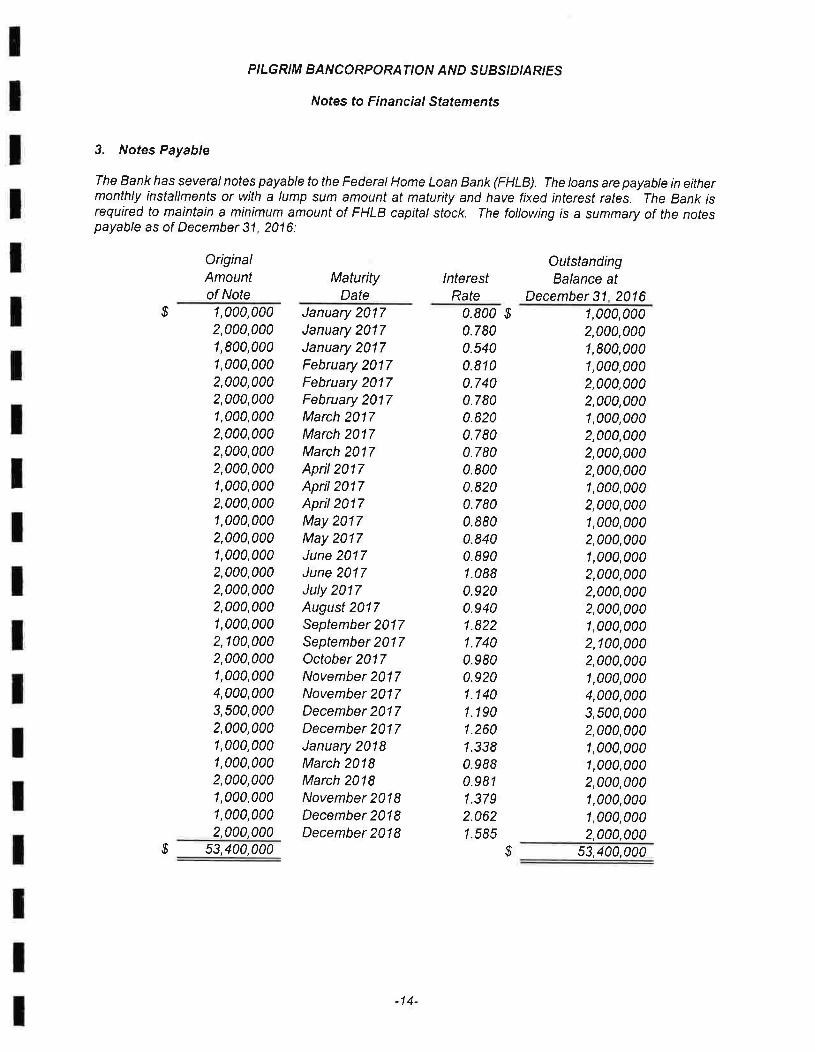

3. Notes Payable

The Bank has several notes payable to the Federal Home Loan Bank (FHLB) The loans are payable in eithermonthly installments or with a lump sum amount at maturity and have fixed interesf rafes. The Bank isrequired to maintain a minimum amount of FHLB capital stock. The following is a summary of the notespayable as of December 31 , 2016:

1,000,0002,000,0001,800,0001,000,0002,000,0002,000,0001,000,0002,000,0002,000,0002,000,0001,000,0002,000,0001,000,0002,000,0001,000,0002,000,0002,000,0002,000,0001,000,0002,100,0002,000,0001,000,0004,000,0003,500,0002,000,0001,000,0001,000,0002,000,0001,000,0001,000,0002,000,000

January 2017January 2017January 2017February 2017February 2017February 2017March 2017March 2017March 2017April2017April2017April2017May 2017May 2017June 2017June 2017July 2017August 2017September 2017September 2017October 2017November 2017November 2017December 2017December 2017January 2018March 2018March 2018November 201 IDecember 2018December 201 I

OutstandingBalance at

December 31 20161,000,0002,000,0001,800,0001,000,0002,000,0002,000,0001,000,0002,000,0002,000,0002,000,0001,000,0002,000,0001,000,0002,000,0001,000,0002,000,0002,000,0002,000,0001,000,0002,100,0002,000,0001,000,0004,000,0003,500,0002,000,0001,000,0001,000,0002,000,0001,000,0001,000,0002,000,000

OriginalAmountof Note

MaturityDate

lnterestRate

$ 0.800 $0.7800.5400.8100.7400.7800.8200.7800.7800.8000.8200.7800.8800.8400.8901.0880.9200.9401.8221.7400.9800.9201 .1401.1901.2601.3380.9880.9811.3792.0621.585

$.$ 5s,400,000

-1 4-

53,400,000

PILGRIM BANCORPORATION AND SUESIDIARIES

Notes to Financial Sfatements

3. Notes Payable, continued

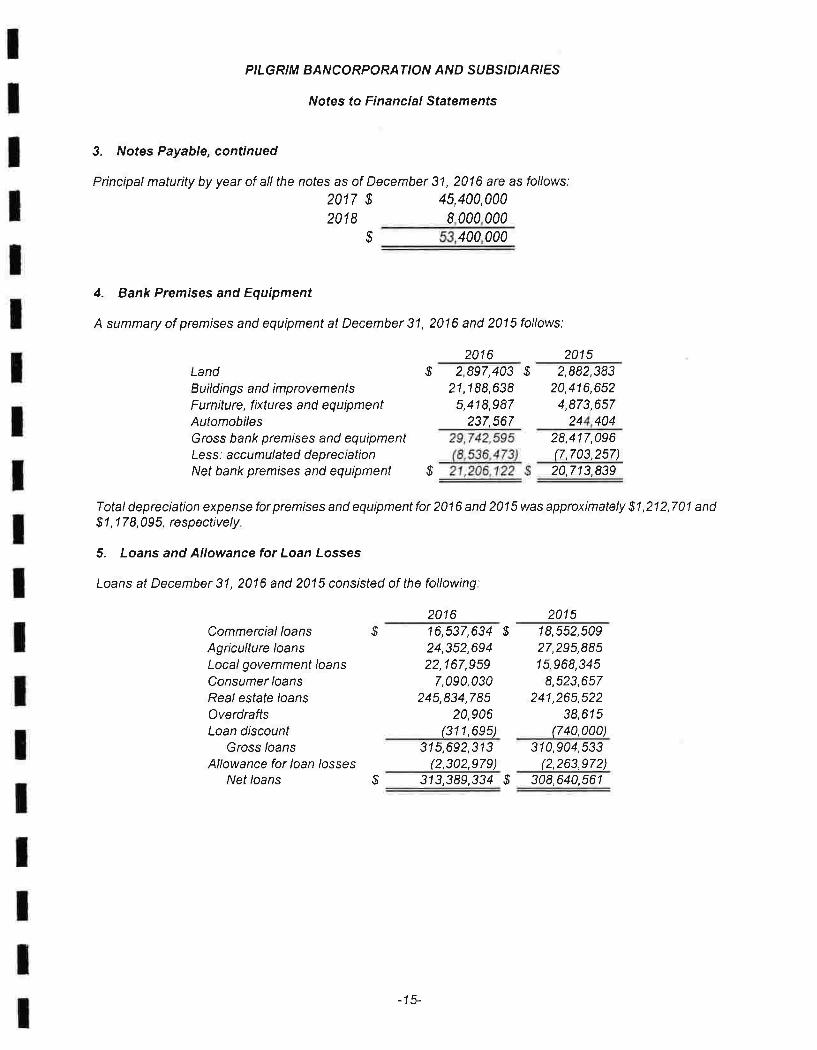

Principal maturity by year of all the notes as of December 31, 2016 are as follows:

2017 $ 45,400,0002018 I 000 000

$ 400 000

4. Bank Premises and Equipment

A summary of premises and equipment at December 31, 2016 and 2015 follows:

2016 2015LandB uild i ng s and improv e m e ntsFurniture, fixtures and equipmentAutomobilesGross bank premises and equipmentLess. accumulated depreciationNet bank premises and equipment

CommercialloansAgriculture loansLocalgovernment loansConsumer loansRealestate loansOverdraftsLoan discount

Gross /oansAllowance for loan /osses

Net /oans $ 313,389,334 $ 308,640,561

$ 2,897,403 $21 ,188,638

5,418,987237,567

2,882,38320,416,6524,873,657

24 40428,417,096(7,703,257)20,713,839$

Total depreciation expense for premises and equipment for 2016 and 2015 was approximately $1 ,212,701 and$1, 1 7 8,09 5, respectively

5. Loans and Allowance for Loan Losses

Loans at December 31 , 2016 and 2015 consisfed of the following:

2016 2015.9 16,537,634 $

24,352,69422,167,959

7,090,030245,834,785

20,906(311 ,695)

18,552,50927,295,88515,968,345

8,523,657241,265,522

38,615(740,000)

315,692,313(2,302,979)

310,904,533(2,263,972)

-1 5-

PILGRIM BANCORPORATION AND SUBSIDIARIES

IVofes to Financial Stafemenfs

5. Loans and Allowancefor Loan Losses, continued

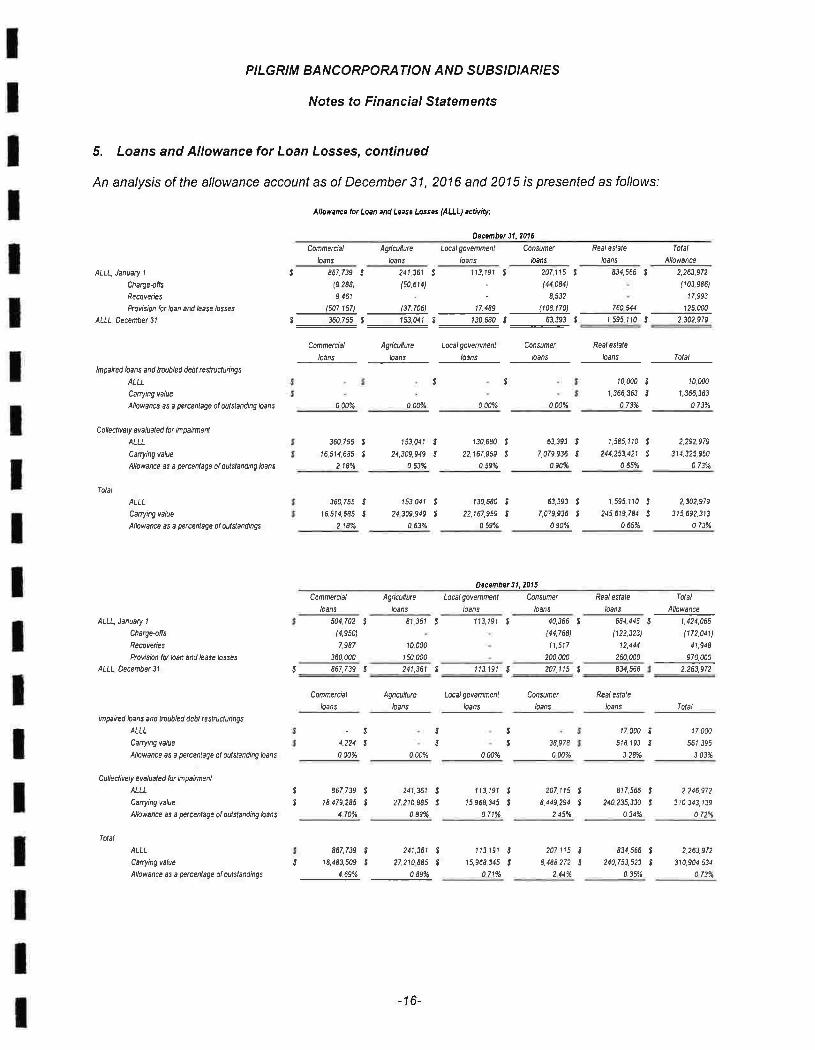

An analysis of the allowance account as of December 31, 2016 and 2015 is presented as fol/ows:

Allowance hrLoan and Leeso Lossos rALLL) activry:

Daconbet 31,2015

Consur'etConnercial

loans

Agncullwe

loans

Local govefimenl

loans

0.00%

/oans

Reai eslale

loars

834,566 J

760 544

1,595,110 5

10,0a0 t1,366,363 5

0 73%

Tolal

Allowance

2,263.9t2

(103.986)

t7,993

125.040

2,302,979

t0,N0

,,360363

0 73y.

ALLL, January 1

Charge{fis

Recoyenes

ftovision lor loan and /ease losses

ALLL oecenbet 31

lnpaired loans and hEUDied deol reslrucluahgs

ALLL

Carrying value

Allowance as a percenlage al aulslanding hans

Colleclively eveluated lo( inpatnent

ALLL

Catryingvalue

Nlowance as a Frcenlage ol outslanding laant

Tolal

ALLL

Carrying value

Nlowance as a percenlage ol oulstandings

ALLI- January 1

Charge4fls

Recoveres

Provision lot loan and lease losses

ALLL. Decenbet 31

lnpated bans and lroubled debl reslruclunngs

ALLL

Carrying value

Nlowance as a pcrcentage ol outdanding loans

Colleclively evalualed hr inpairnenl

ALU

Catrying value

Nlowance as a percenlage ol oulslanding loans

Tolal

ALLL

Catrying value

Allowance as a percentage ol ottslaodings

$ 867,739 S 241,361 3 113,191 $ 207115 t(e288) (s0,614) - (44084)

9,461 8,532

(s07.157) (37.706) 17.489 (108.170)

t 360,755 S 153,U1 S '30,6A0

S 6J,393 t

Comnetcial Agricufrure Localgovemnenl Consumer Realeslate

/oans loars ,oans /oars loars Total

5 s

000% 000y, 0 000,(

2 18vo

360.755 S

,6,5t4,685 '/18%

153,U1 S

24,3N,949 I0.63% 0 59yo

130,680 S

22,167,959 $

130.680 I22,1619s9 5

0 s9%

63,393 t7,079,936 I

09a%

1,585.t10 t244,253,421 S

0 65/o

2,292,979

3t1,325,950

073%

2,302,979

3r5.692,3.,3

0.73%

360,755 g

,6,5'4,685 5

153,041 t24 3A9,949 t

0 63%

63,393 E

7,079,936 .t

090%

,,595,r'0 S

245,6t9.1U $

0 6594

Dscenbet 31,2015

Commercial

ioans

504,702 S

(4,950)

7,987

360.000

Connercial

loars

-t4.224 $

0 000,6

g 867.739 $

5 18.479.285 5

4 fe/L

Local govemmenl

ioans

,13, '91 '

Local govemnenl

loars

113,191 S

15,968,345 8

Consuner

/oars

Real eslale

loans

Total

Allawance

t.424,065

1172.U1)

41,940

970,0a0

2,263,972

fotal

17,000

561,J95

3 03%

2,246,972

310,343, r39

0 t2%

2,26i,9f2

310,904,534

Agicultue

loans

81,J5' $

10,000

150.000

40,366 I(44,768)

11,517

6A4,445 S

(122,323)

12,444

2C0,@0 260.000

$ 867,739 I 241,361 8 fi3,191 8 207,t15 '

834.566

Agricullure

loans

Consuner

loans

Real eslale

ioans

3

.t

t5 38.978

0 00%

207.fi5 S

8.419,294 5

17,000 g

518,193 '3 28yo

8'7.566 $

240,235,330 $

0 00%

241,36t t2t,210.885 $

00e,6

089% 071% 245% 034%

867,739 $

18,483,509 t241,361 $

27,210 885 $

,13 191 S

15,968,345 5

071%

207,11s t8,488,272 I

834566 5

240,753,523 S

0 35%4.69% 089%

t

-16-

2 44% 0 t3%

5. Loans and Allowance for Loan Losses, continued

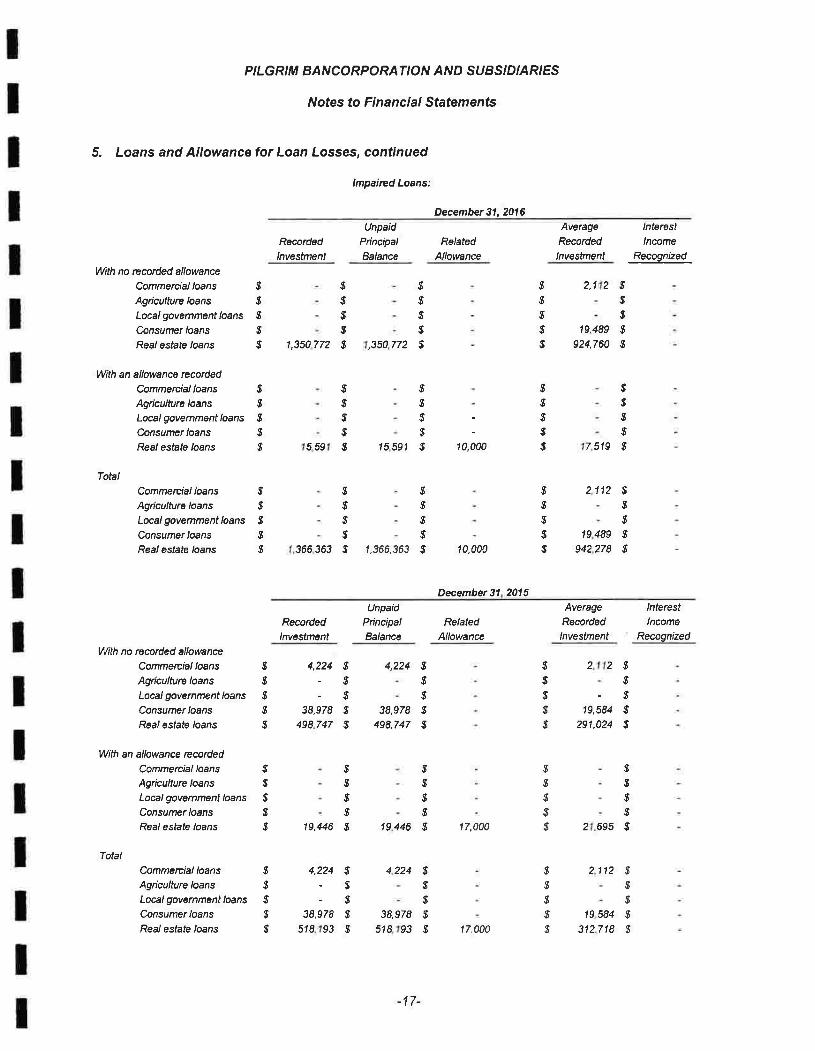

lmpaired Loans:

P I LG RI M B AN CO RPO RATI O N AA'D SUBS I DI ARIES

IVofes to Financial Stafemenfs

December 31,2016

Recordedlnvestment

UnpaidPrincipalBalance

Related

Allowance

Average

Recorded

lnvestment

/nterest

lncomeRecognized

With no rccorded allowance

Commercial loans $Agiculture loans $

Local govemment loans $

Consumer loans $Real estate loans $

With an allowanco recorded

Commercial loans $Agiculture loans $

Local govemment loans $

Consumer loans $

Rea/ estale /oans $

TohlCommercial loans $

Agriculture loans $

Local govemment loans $

Consumer loans $

Real estab loans $

With no recorded allowance

Commercial loans $

Agriculture loans ,S

Local govemment loans $

Consumer loans $

Real estate /oans $

With an allowance recorded

Commercial loans $Agriculture loans $Local govemment loans $

Consumer loans $

Real estate loans S

Commercial loans $

Agriculture loans $

Local government loans $Consumer loans $

Real estate loans $

363 1,366,363 10,000

$

$$$

$

$$$

$.9

$

$

$$$

s$.$

$

$

$

$

$$.,

$

$

$

$

$

12, 2 $

$

s$

$

$

$

$

$

$

$.$

$

.s

$

1 772,350772,350

19.489

924,760

$.s($

$

$$

$

$

$

559 1 519

112

7

2

10,0005975

$

$$$.$

19 489278942366

6952

12

December 31 2015

Recordedlnvestment

Unpaid

PrincipalBalance

RelatedAllowance

17.000

Average

Recordedlnvestment

lnterest

lncome

Recognized

224

74

4,

49E,

38,978

4,224

38,97874498 77

$

$

$,$

.$

.,

$s$

$

$$

$

$

$

$

.$

$

s$

$$

$

$$

$

$

$

$

$

.s

$

$

$$

$

$

$

$

$

.$

$

$.$

$

2

n,iat291,024

2

19 446

224

38,978

4

19,446

4,224

34,978

$

$

$

$

$

12

$

E

$

$

$

$

$

$

$

$

19 584

312 7 1893II

Total

51 93 51

- I t-

17.000

PILGRIM BANCORPORATION AND SUBSIDIARIES

Notes to Financial Sfatements

5. Loans and Allowance for Loan Losses, continued

Loa n Cl a ssific ation Statusi

December 31 2016

Commercialloans

Agicullure,oans

Local govemment

/oans

Consumerloans

Real eslate

loans Total

Pass

Special Mention

SubstandardDoublful

LossTotal

16,163,737 $

208,9s7142,011

21,673,758 $2,375,328

260,863

22,167,959 $ 7,022,693 $54.034

3,209

237,475,807 S

3,148,9164,995,061

304,503.954

5,787.2155,401,1 41

.'

$ 16,514,68s S 24,309.949 $ 22,162959 $ 7,079,936$ 245,619,7845 315,692,313

December 31 2015

Commercialloens

Agiculture Local govemment

loans loansConsumer

loansReal eslale

loans Total

Pass

Special Mention

SubstandardDoubttulLoss

Total

18,295,312 $

183,973

4,224

25.987,765 $2,68s

1,220,435

15.968,345 $ 8,377,904 $

68,017

42,3s1

231,755,518 $

2,965,9056,032,099

300,384,844

3,220,5807,299,109

$

$ 18,483,509 S 27,210,885 $ 15,968,34s $ 8.488,272 $ 240,753,522 S 310,904,533

Nonaccrual Loans

Nonaccrual Loans

Accruing Past Due

90 Days or More

December 31 December 31

2016 201 5 201 6 201 5

Commercialloans $

Agriculture loans

Local government loans

Consumer loans

Rea/ esfafe /oans

Total loans $

$ 4,224

1,366,363

38,978

518,193

1,366,363 $ 561,395

$

$

$

$

-1 8-

PILGRIM BANCORPORATION A/VD SUBSIDIARIES

IVofes to Financial Sfatements

5. Loans and Allowance for Loan Losses, continued

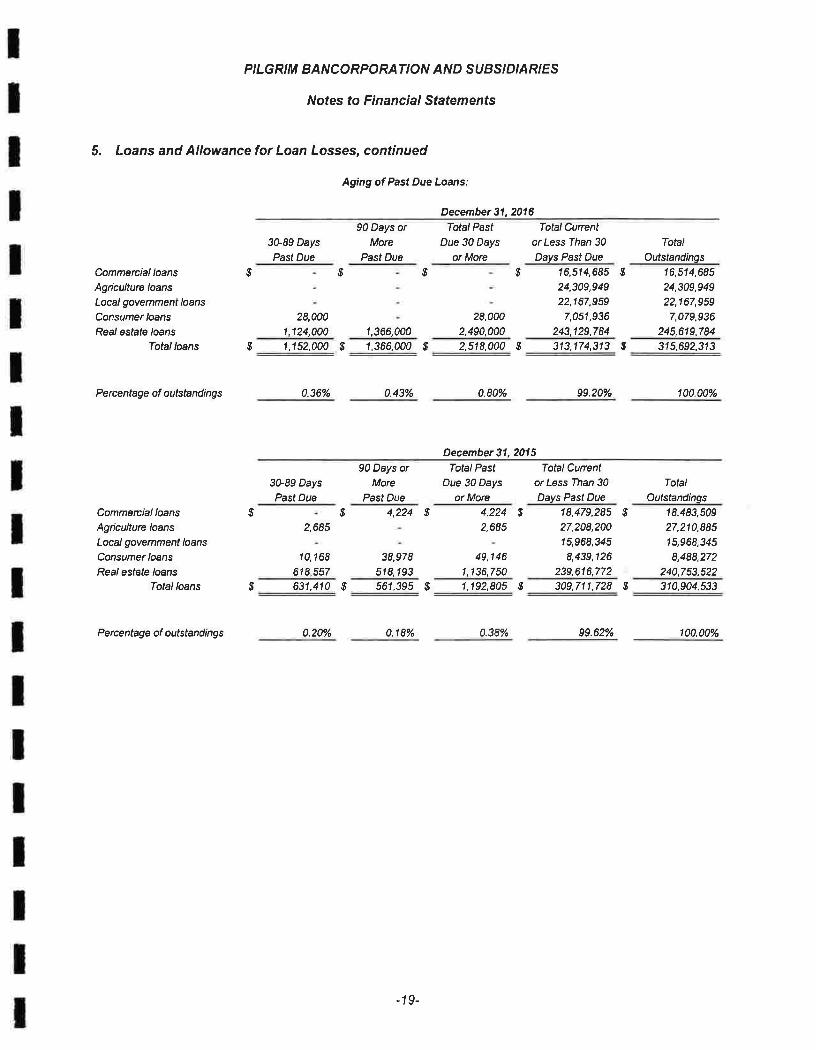

Aging ol Past Due Loans:

December 31,2016

3G89 Days

Pasl Due

90 Days orMore

Past Due

Total Past

Due 30 Days

or More

Total Cunenlor Less Than 30

Days Past Due

Total

Outstandings

Commercial loans

Agiculture loans

Local govemment loansConsumer loans

Rea/ eslale loansTotal loans

P e rce ntage of outstand i ng s

Commercial loans

Agiculture loans

Local govemment loans

Consumer loans

Real estate loansTotal loans

P erce ntag e of o utstan di ng s

$ $ $ $

2E,000

2,490,000

16,514,685 $24,309,949

22,167,959

7,051,936

243,129,784

16,514,685

24,309,949

22,167,959

7,079,936

245,619.784

28,0001,124,000 1,366,000

$ 1,152,000 $ 1,366,000 $ 2,518,000 $ 313,174,313 I 31s,692,313

0.36% 0.43% 0.80% 99.20% 100.00%

December 31,2015

3G89 Days

Past Due

90 Days orMore

Past Due

Total Past

Due 30 Days

or More

Total Curentor Less Than 30

Days Past Due

Total

Outstandinqs

$2,68s

10,16E

618,557

$ 631,410

.s 4,224 $

38,978

518,193

4,224 $

2,685

49,146

1,1s6,750

18,479,285 I27,208,200

15,968,345

8,439,126

239,616,772

18,483,509

27,210,885

15,968,345

8,488,272

240,753,522

$ 567,395 $ 1,192,805 I 309,711,728 $ 310,904,533

0.20% 0.18% 0.3E% 99.62% 100.00%

-19-

5. Loans and Allowance for Loan Losses, continued

T roubled Debt Restruclu i ngs :

2016

PE-Modificatton PoslModficalion

Numbet ot

Cortracls

Oulslanding Recorded Oulstanding

lnveslment Recoded lnvestmenl

Connercial loans

Agicultwe loans

Locel govemment loans

Consumer loans

Rea/ eslate ,oans

t 135,000 $ 114,918

1,401,756 1,350,n2Tolal loans ,,536,756 3 1.465.690

Troubled Debt Restfl clurlngs ahat Subsequenaly Delaulted :

2016

PI LG RI M B AN CO RP O RATI O N A IVD SUBS I D I ARI ES

Nofes to Financial Sfafemenfs

Nunber olCont|acls

2015

s

Pre-Modilicalion

Outslanding Recoded

lnveslmenl

Posl-Modilicalion

Oulstandtng

Recgded lnvestmenl

J-

4.137 376 4.017 187

5s 4.137.376 g 4,017.187

2015

Nunbet olContracls

Recodied

lnvestment

Nunber olContracls

Recoded

lnvestnent

Conmercial loans

Agticutlure loans

Local govemment loans

Consumer loans

Real estate ,oans

Total loans

Loan pafticipations sold and seNiced by the Bank totaled approximately $835,265 and $917,005 as ofDecember 31 , 2016 and 2015, respectively.

6. Deposits

Year-end deposlts consisfed of the following:

201 6 201 5

,$

ss

Noninterest bearingI nte rest-b e a ri ng demandMoney market and savingsTime, $100,000 and overIime, /ess than $100,000

$ 29,985,825 $9,506,811

281,387,48384,496,797

30,667,23411,048,050

289,926,38285,663,429

Certificates mature in the years following as of December 31 , 2016

50 880 280 54. 843,693$ 456,257,196 $ 472,148,788

$ 70,201,07155,698,8609,477,146

One year or /essOne year to three yearsOver three years

-20-

$ 135,377,077

PILGRIM BANCORPORATION AND SUBSIDIARIES

A/otes to Financial Stafements

7. Related Party Transactions

ln the ordinary course of busrness, the Bank has and expects to continue to have transactions, includingborrowings, with its employees, officers, directors, shareholders, and their affiliates. ln the opinion ofmanagement, such transactions are on the same ferms as comparable transactionswith unaffiliatedpersons.

Loans to related pafties totaled $7,506,279 and $9,824,625 at December 31 , 2016 and 201 5, respectively.During 2016, new loans made fo such related parties amounted to $848,546 and payments amounted to$3,166,892.

The Bank held related pafty deposits of approximately $15,776,921 and $12,932,464 at December 31, 2016and 201 5, respectively.

8. Financial lnstruments with Off-Balance-Sheet Rrsk

The Bank is a pafty to financial instruments with off-balance-sheet risk in the normal course of business fomeet the financing needs of ifs customers. Ihese financial instruments include commitments to extend credit,standby letters of credit, and financial guarantees. Ihese instruments involve, to varying degrees, elements ofcredit and interest rate risk rn excess of the amount recognized in the balance sheet The contract amount ofthose rnstru ments reflects the extent of involvement the Bank has in particular classes of f,na ncial instruments.The Bank uses the same credit policies in making such commitments as it does for instruments that areincluded in the statements of financial condition.

Financial instruments whose contract amount represents credit risk were as follows201 6 201 5

Commitments to extend credit on unfunded loans $ 25,998,969 $Standby /etters of credit and financial guarantees written $ 1 ,464,180 $

22,087,5501,293,220

Commitments to extend credit are agreements to lend to a customer if there is no violation of any conditionestab/ished in the contract. Commitments generally have fixed expiration dates or other termination c/ausesand may require payment of a fee. Since many of the commitments are expected to expire without beingdrawn upon, the totalcommitment amounts do not necessarily representfuture cash requirements. The Bankevaluates each customer's credit worthiness on a case-by-case basrs. The amount of the collateral obtained, ifdeemed necessary by the Bank upon extension of credit, is based on management's credit evaluation of thecounter-pafty. Collateral held varies but may include customer deposits, accounts receivable, inventory,property, plant, and equipment, and income-producing commercial properties.

Standby letters of credit and financial guarantees written are conditional commitments issued b y the Bank toguarantee the performance of a customer to a third party. Those guarantees are primarilyissued to supportpublic and private borrowing arrangements, including commercial paper, bond financing, and similartransactions. The credit risk involved in issuing letters of credit is essentia//y the same as thal involved inextending loan facilities fo customers.

The Bank obtained a line-of-credit with the Federal Home Loan Bank in the amount of $128,988,200 and$89,472,725 at December 31, 2016 and 2015, respectively. The agreement allows the Bankto draw securedadvances based upon 75% of one to four single family loans, 75%o of multifamily loans, 60% of sma// buslnessloans and 40% of small farms loans. As paft of the agreement, the Bank is required to own stock of theFederal Home Loan Bank. The Bank held $2,482,700 and $2,303,600 of stock in 2016 and 2015,respectively. The Bank a/so has an unsecured line-of-credit with TIB in the amount of $17,500,000.

-21-

PILGRIM BANCORPORATION AND SUBSIDIARIES

lVofes to Financial Statemenfs

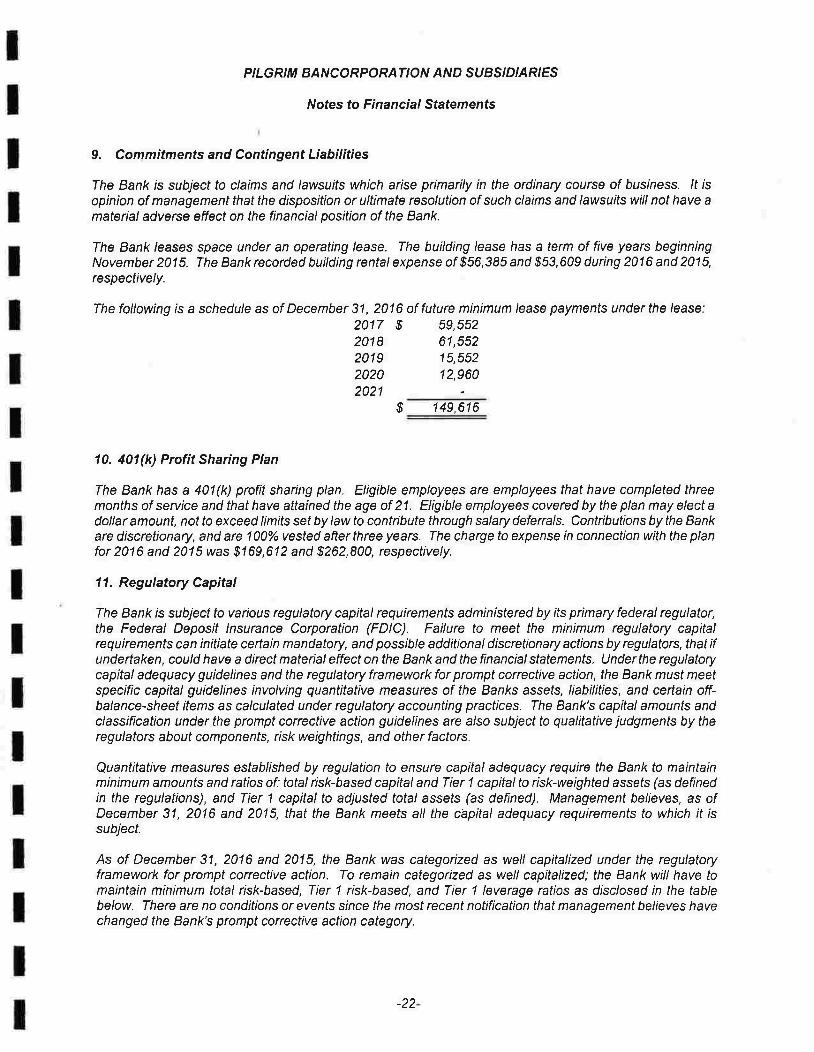

9. Commitments and Contingent Liabilities

The Bank rs subT'ect to claims and lawsuits which arise primarily in the ordinary course of busrness. /t lsopinion of management that fhe dlsposition or ultimate resolution of such claims and lawsuits will not have amaterial adverse effect on the financial position of the Bank.

The Bank /eases space under an operating /ease. The building /ease has a term of five years beginningNovember2015. TheBankrecordedbuildingrentalexpenseof$56,385and$53,609durin72016and2015,respectively.

The following is a schedule as of December 31 , 2016 of future minimum lease payments under the /ease:2017 $ 59,5522018 61,5522019 15,5522020 12,9602021

$ 149,616

10. 401(k) Profit Sharing Plan

The Bank has a 401(k) profit sharing plan. Eligible employees are employees that have completed threemonths of seruice and that have attained the age of 21. Eligible employees covered by the plan may elect adollar amount, notto exceed limits set by law to contribute through salary deferrals. Contributions by the Bankare discretionary, and are 100% vested afterthree years. The charge to expense in connection with the planfor 2016 and 2015 was $169,612 and $262,800, respectively.

11. Regulatory Capital

The Bankis sub1'ect to various regulatory capital requirements administered by its primary federal regulator,the Federal Deposit lnsurance Corporation (FDIC). Failure to meet the minimum regulatory capitalrequirements can initiate ceftain mandatory, and possib/e additional discretionary actions by regulators, that ifundertaken, could have a direct material effect on the Bank and the financial statements. Under the regulatorycapital adequacy guidelines and the regulatory framework for prompt corrective action, the Bank must meetspecific capital guidelines involving quantitative measures of the Banks assefs, liabilities, and certain off-balance-sheet items as calculated under regulatory accounting practices. The Bank's capital amounts andclassification under the prompt corrective action guidelines are also subject to qualitative judgments by theregulators about components, risk weightings, and other factors.

Quantitative measures estab/rshed by regulation to ensure capital adequacy require the Bank to maintainminimum amounts and ratios of: total risk-based capitaland Tier 1 capitalto risk-weighted assefs (as definedin the regulations), and Tier 1 capital to adjusted tofal assets (as defined). Management believes, as ofDecember 31, 2016 and 2015, that the Bank meets all the cbpital adequacy requirements to which it issubject.

As of December 31,2016 and 2015, the Bank was categorized as well capitalized under the regulatoryframework for prompt corrective action. To remain categorized as well capitalized; the Bank will have tomaintain minimum total risk-based, Tier 1 risk-based, and Tier 1 leverage ratios as dlsc/osed in the tablebelow. There are no conditions orevenfs since the most recent notification that management believes havechanged the Bank's prompt corrective action category.

-22

PILGRIM BANCORPORATION AiVD SUBSIDIARIES

Notes to Financial Sfatements

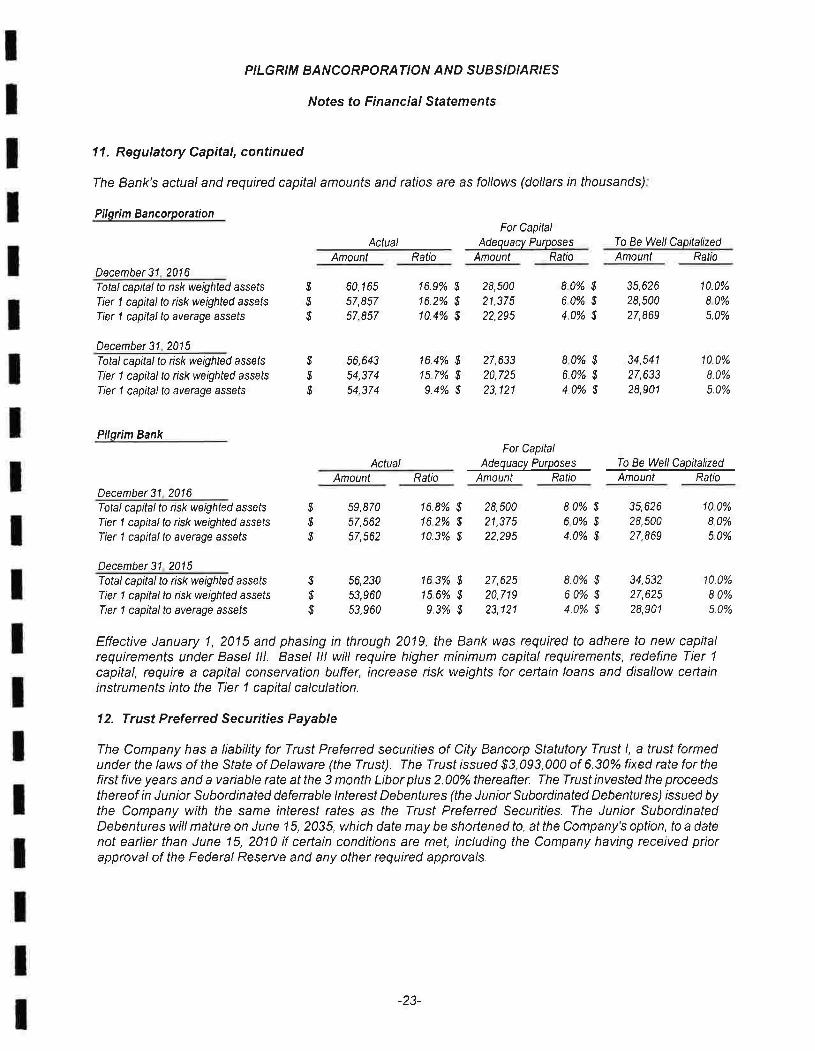

11. Regulatory Capital, continued

The Bank's actual and required capital amounts and ratios are as follows (dollars in thousands)

Pilgri m BancorporationFor Capital

Adequacy PurposesActual To Be WellCapitalizedAmount Ratio Amount Ratio Amount Ratio

December 31 201 6

Total capital fo nsk weighled assets

Tier 1 capital to risk weighted asselsTier 1 capitallo average assets

December 31 2015

Total capital to isk weighted assefs

Tier 1 capital to risk weighted asselsTier 1 capital to average assefs

Pilgrim Bank

December 31 2016

Total capital to risk weighted asselsTier 1 capital to risk weighted assets

Tier 1 capital lo average assets

December 31 2015

Total capital to risk werghted assets

Tier 1 capital to risk weighted assets

Tier 1 capital to average assels

Amount Ratio

59,870

57,562

57,562

$,$

$

60,16557,85757.857

56,643

54,37454.374

16.9% $

16.2% S

10.4% $

16j% S

157% $

94% $

28,500

21,37522,295

27,63320,725

23,121

28,50021,37522,295

80% $

60% $

4.0% $

80% $

6.0% $

4.0% $

8.0% $

60% $

4.0% $

8.0% $6.0% $4.0% $

35,62628,500

27,869

34,541

27,63328,901

35,626

28,50027.869

34,53227,62528,901

10.0%

80%5.0%

10.0%

8.0%

s.0%

10 0%

80%50%

10.0%

8.0%

5.0%

a

$

$

$.$

$

$

$

$

AcIualFor Capital

Adequacy Purposes

Amount RalioTo Be Well CapitalizedAmount Ratio

16.8% $162% $10.3% $

56,230 16 3% $ 27,625

53,960 15 6% $ 20,719

53,960 9.3% $ 23,121

Effective January 1, 2015 and phasing in through 2019, the Bankwas required to adhere to new capitalrequirements under Basel lll. Basel lll will require higher minimum capital requirements, redefine Tier 1

capital, require a capital conservation buffer, increase risk weights for ceftain loans and disallow ceftaininstruments into the Tier 1 capitalcalculation.

12. Trust Preferred Securities Payable

The Company has a liability for Trust Preferred securities of City Bancorp Statutory Trust l, a trust formedunder the laws of the State of Delaware (the Trust). The Trustissued $3,093,000 of 6.30% fixed rate for thefirst five years and a variable rate at the 3 month Libor plus 2.00% thereafter. The Trust invesfed the proceedsthereof in Junior Subordinated deferrable lnterest Debentures (the Junior Subordinated Debentures) issued bythe Company with the same interest rates as the Trust Preferred Securities The Junior SubordinatedDebentures will mature on June 15, 2035, which date may be shoftened to, at the Company's option, to a datenot earlier than June 15, 2010 if ceftain conditions are met, including the Company having received priorapproval of the Federal Reserve and any other required approvals.

-23-

PILGRIM BANCORPORATION AND SUESIDIARIES

Notes to Financial Stafemenfs

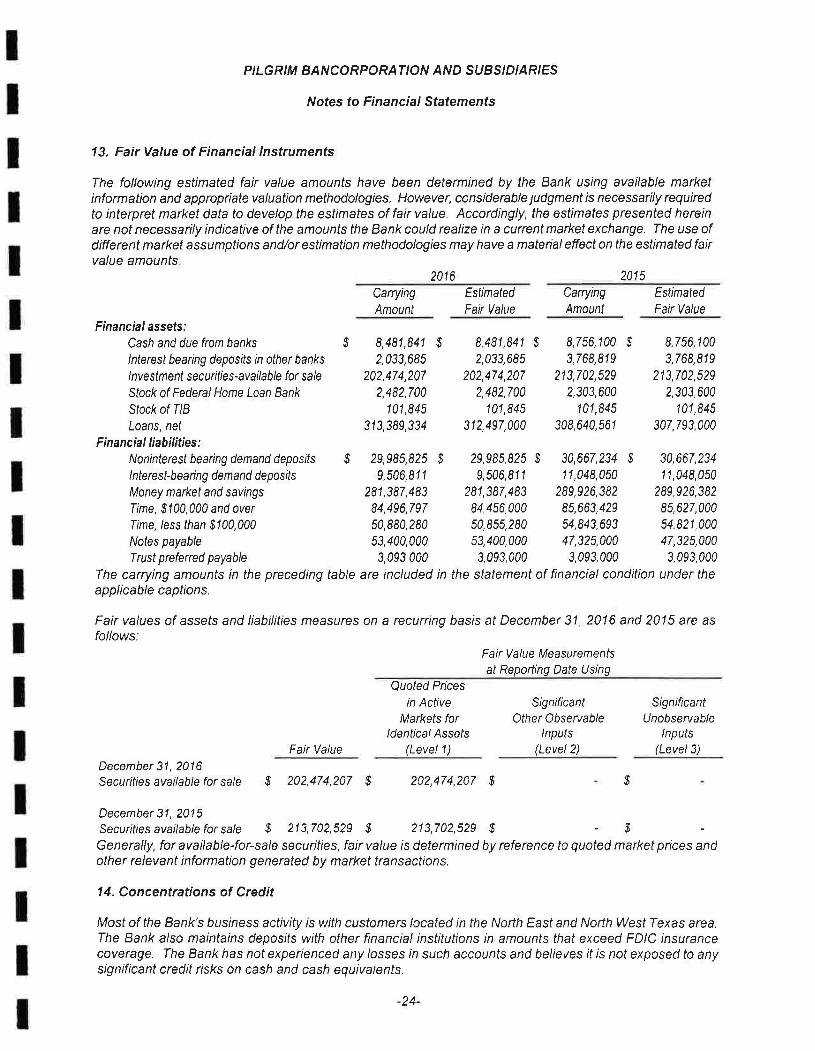

13. Fair Value of Financial lnstruments

The following estimated fair value amounts have been determined by the Bank using available marketinformation and appropriate valuation methodologies. However, considerable judgment is necessarily requiredto interpret market data to develop the estimates of fair value. Accordingly, the estimates presented hereinare not necessar/y indicative of the amounts the Bank could realize in a current market exchange. The use ofdifferent market assumptions and/or estimation methodologies may have a mateial effect on the estimated fairvalue amounts

2016 2015

Carrying

Amount

Estimated

Fair Value

Carrying

Amount

Estimated

Fair Value

Financial assets:Cash and due from banks $ 8,481,841 $ 8,481,841 $ 8,756,100 $ 8,756,100

lnterest bearing deposits in other banks 2,033,685 2,033,685 3,768,819 3,768,819

lnvestment securities-available for sale 202,474,207 202,474,207 213,702,529 213,702,529

Stock of Federal Home Loan Bank 2,482,700 2,482.700 2,303,600 2,303,600

Stock of r/B 101,845 101,845 101,845 101,845

Loans, net 313,389,334 312,497,000 308,640,561 307,793,000

F inancial liabilities :Noninteresl bearing demand deposits $ 29,985,825 $ 29,985,825 $ 30,667,234 $ 30,667,234

lnterest-bearing demand deposits 9,506,811 9,506,81 1 11 ,048,050 1 1 ,048,050Money market and savings 281 ,387 ,483 281 ,387 ,483 289,926,382 289 ,926,382Time, $100,000 and over 84,496,797 84,456,000 85,663,429 85,627,000

Iime, /ess than $100,000 50,880,280 50,855,280 54,843,693 54,821,000

Notes payable 53,400,000 53,400,000 47,325,000 47,325,000

Trust preferred payable 3,093,000 3,093,000 3,093,000 3,093,000

The carrying amounts in the preceding table are included in the statement of financial condition under theapplicable captions.

Fair values of assets and liabilities rneasures on a recurring basis at December 31 , 2016 and 2015 are asfollows:

F ai r V al ue Me asu rem entsat Reporling Date Using

Quoted Prices

in Active Significant SignificantMarkets for Other Obseruable Unobseruable

ldenticalAssels lnputs lnputsFair Value (Level 1) (Level 2) (Level 3)

December 31, 201 6

Securilies available for sale $ 202,474,207 $ 202,474,207 $

December 31, 201 5

Securifies avaitable for sale $ 213,702,529 $ 213,702,529 $ $

Generally, for available-for-sale securlties, fair value is determined by reference to quoted market prices andother relevant information generated by market transactions.

14. Concentrations of Credit

Most of the Bank's busrness activity is with customers located in the North East and North West Texas area.The Bank also maintains deposlts with other financial institutions in amounts that exceed FDIC insurancecoverage. The Bank has not experienced any /osses in such accounts and believes it is not exposed to anysignificant credit risks on cash and cash equivalents.

$

24-

ADD ITI @.NAL,fNFOB,}'AT' OM

judd thomas

{rr,,lL,{,brun-, Swtl + C,.Wf, / CDallas,Iexas

I certified public accountants & advisors

I N D EP EN DENT AU D ITO R'S REPORTO N ADDITIO N AL I N FO RMATIO N

To the Board of Directors and Stockholdersof Pilgrim Bancorporation and Subsidiaries

We have audited the consolidated financial statemenfs of Pilgrim Bancorporation and Subsidlaries as of andfor the years ended December 31, 2016 and 2015, and our repoft thereon dated January 27, 2017, whichexpressed an unmodified opinion on those financial sfatements, appears on page 1. Our audits wereconducted for the purpose of forming an opinion on the consolidated financialsfatements as a whole. Theconsolidating information is presented for purposes of additional analysis of the consolidated financialsfalemenfs rather than to present the financial position, results of operations, and cash flows of the individualcompanies, and it is not a required part of the consolidated financialstatemenfs. Such information is theresponsibility of management and was derived from and relates directly to the underlying accounting and otherrecords used to prepare the consolidated financial sfatements. The consolidating information has beensubjected to the auditing procedures applied in the audit of the consolidated financial statements and certainadditional procedures, including comparing and reconciling such information directly to the underlyingaccounting and other records used to prepare the consolidated financial statements or to the consolidatedfinancialstatemenfs themselves, and other additional procedures in accordance with auditing standardsgenerally accepted in the United Sfafes of America. ln ouropinion, the consolidating information isfairly statedin all material respecfs in relation to the consolidated financialstafemenfs as a whole.

January 27,2017

12222 Meril DtiveSuite 1900

214.296.0900 Main800.304.4887 Toll Free972.661.3651 FaxDallas, TX 75251 -3209

-26-judd$omas.com

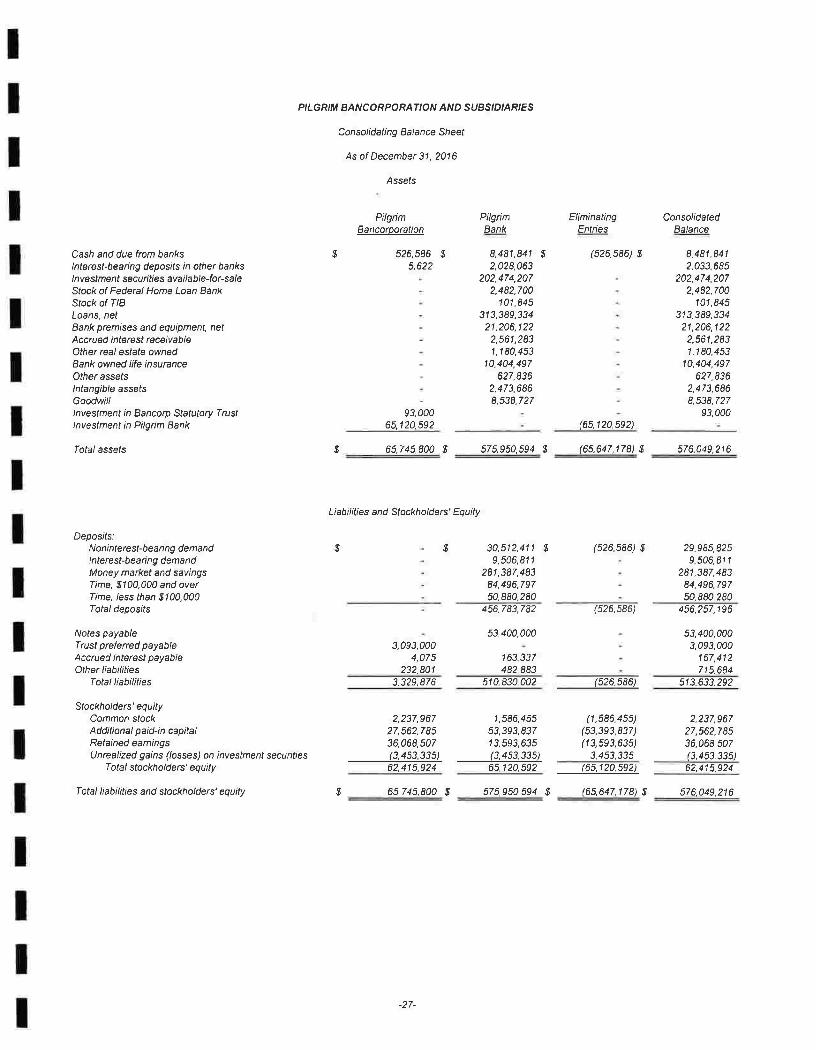

P' LG RIM BA N C O R PO RAT IO N AN D SUBS'D'AR'ES

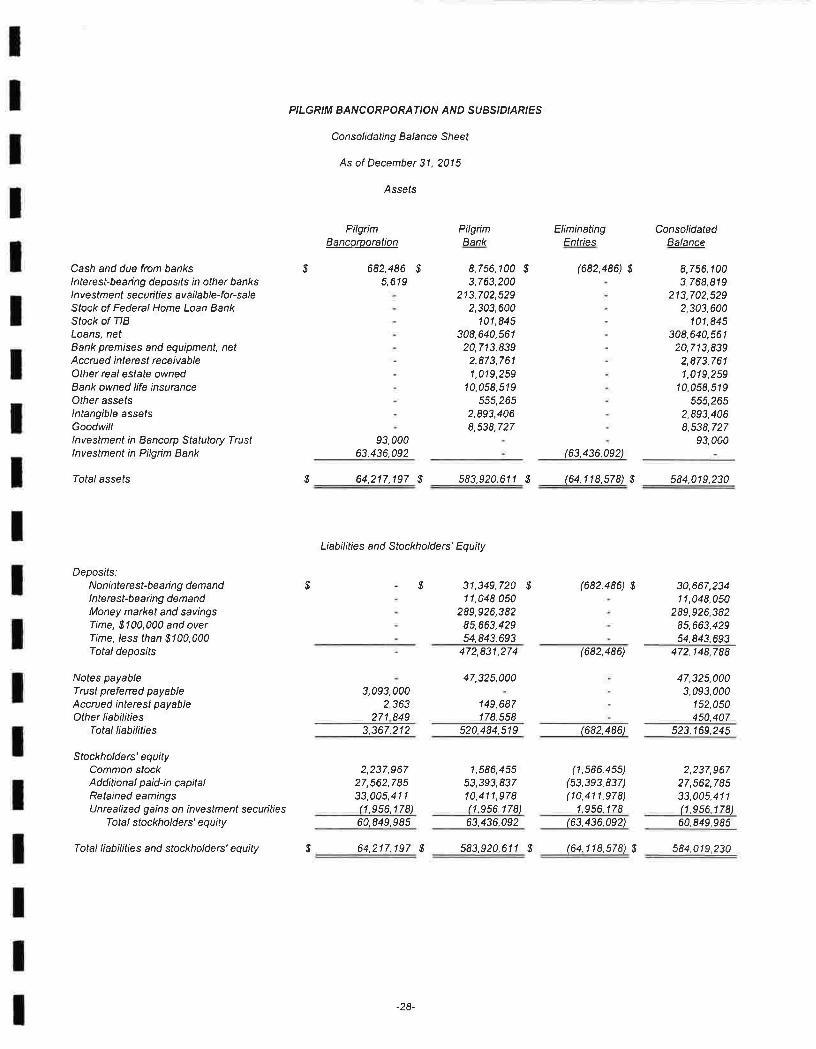

Con solid ati ng Bal ance Sheet

As of December 31 , 201 6

Assels

PilgimBancorooration

PilgrimBank

EliminatingEntries

ConsolidatedBalance

Cash and due from bankslnteresl-beaing deposr?s ln other bankslnvestment secuities available-for-saleStock ol Federal Home Loan BankStock of TIBLoans, netBank premises and equipment, netAccrued interest receivableOther real estate ownedBank owned life insuranceOfher assets/nlangible assetsGoodwilllnvestment in Bancorp Statutory Trustlnvestment in Pilgrim Bank

fotal assels

Deposrls:N o n i n te re sl-b e a ri n g d e m a ndlnterest-beaing demandMoney market and savingsTine, $100,000 and overIime, /ess than $100,000Iotal deposits

Notes payableTrust preferred payableAccrued interest payableOther liabilities

Total liabilities

Stockholders' equityCommon stockAdditional paid-in capilalRelained eamingsUnrealized gains (/osses) on investment secunties

Total stockholders' equily

Total liabilities and stockholders' equity

120,592)

65,745,800 $ 575,950,594 $ (65,647,17il$ 576,049,216

Liabilities and Stockholders' Equity

$ 30,512,411 $9,506,811

241,387,48384,496,79750,880,280

(526,586) $ 29,985,8259,506,811

281,387,48384,496,79750,880,280

456,783,782 (526,s86) 456,257,1 96

53,400,0003,093,000

4,07 5232.801

3.329,876 510,830,002 (526,586)

$ 526,586 $5,622

8,481,841 $2,028,063

202,474,2072,482,700

101,845313,389,334

21 ,206,1222,561,2831 ,180,453

10,404,497627,836

2,473,6868,538,727

(526,586) $ 8,481,8412,033,685

202,474,2072,482,700

101,845313,389,3i421,206,122

2,561,2831.180,453

10,404,497627,836

2,473,6868,538,727

93.00093,00065,120,592 (6s,

$

$

$