policy brief 15-13: korea and the tpp: the inevitable ... · (cjk) trilateral talks. meanwhile,...

TRANSCRIPT

N u m b e r P b 1 5 - 1 3 a u g u s t 2 0 1 5

1750 Massachusetts Avenue, NW Washington, DC 20036 Tel 202.328.9000 Fax 202.659.3225 www.piie.com

Policy Brief

trade and investment with TPP countries, although some of those benefits only will accrue if Korea implements politically sensitive reforms that open trade with Japan.

This Policy Brief begins by briefly examining why TPP participation is important for Korea. It then assesses the factors that could complicate Korea’s accession to the TPP, as well as possible scenarios for how it could negotiate its TPP entry. It concludes that Korea should join the TPP and the sooner the better. Unfortunately, Korea deferred its TPP decision for too long and probably cannot do so now as an original signatory. The timing of its participation will depend on when the TPP enters into force and how additional members are admitted to the pact.

W h y Ko r e a h a s B e e n C au t i o u s

Why did Korea delay its decision to join the TPP? The issue of TPP participation has been vetted by the Korean government for several years, long before Japan, the most recent entrant in the TPP talks, took a seat at the negotiating table in July 2013.

Korean officials cited several reasons for deferring a deci-sion on the TPP. First, after years of intensive FTA negotiations with the United States, European Union, and others, Korean officials were suffering from negotiation fatigue. Yet Korea did not retire from the FTA business. While the TPP was placed on the back burner, talks on a Korea-China FTA proceeded with the goal of concluding a deal by the end of 2014. The Korea-China deal was announced on November 17, 2014 and formally signed in June 2015. Unfortunately, efforts to expedite the pact’s conclusion resulted in a pared-down agreement that excluded coverage of key sectors of bilateral trade. Several other trade deals were also pursued, including FTAs with Australia, Canada, and New Zealand—all of which could be considered building blocks for future TPP membership.

Second, Korean officials were and remain worried that the same frictions with Japan that had stalled bilateral FTA efforts for the past decade would complicate TPP talks as well. Indeed, strained political relations with Japan may have been a decisive factor in deferring the TPP decision. Nonetheless, because of

Korea and the tPP: the Inevitable PartnershipJ e f f r e y J . s c h o t t

Jeffrey J. Schott is senior fellow at the Peterson Institute for International Economics. He is coauthor of Understanding the Trans-Pacific Partner-ship (2013).

Author’s Note: I thank Cathleen Cimino-Isaacs and Euijin Jung for research assistance. The Korea Institute for International Economic Policy provided funding for the research presented in this Policy Brief.

© Peterson Institute for International Economics. All rights reserved.

Negotiators of the Trans-Pacific Partnership (TPP) are close to finishing a comprehensive agreement that will liberalize trade and investment in goods and services among the 12 partici-pating countries. In a best-case scenario, the final deal could be signed before the end of 2015, once the text is publicly released and subject to a 60-day review period as mandated by the new US Trade Promotion Authority (TPA) legislation passed by Congress at the end of June 2015.

Korea is not currently participating in the TPP negotia-tions, although it has had ample opportunities to do so over the past few years. In November 2013, Korea announced its interest in participating and then held numerous rounds of consultations with TPP members regarding potential entry. In a previous Policy Brief, Cathleen Cimino-Isaacs and I argued that there was still a narrow window in late 2014 for Korea to ask to join the talks and be an original signatory to the TPP (see Schott and Cimino 2014). That window, however, is now closed.

That said, Korea is at the top of the list of countries that would like to join the TPP once the pact enters into force. It is largely ready to meet the TPP requirements, many of which are based on provisions of the Korea-US free trade agreement (KORUS FTA). Korea stands to reap large gains from increased

N u m b e r P b 1 5 - 1 3 a u g u s t 2 0 1 5

2

Japan’s entry into the TPP in 2013, these challenges will have to be confronted whenever Korea decides to join the pact.

Third, Korean deliberations to join were also fraught with concerns about reopening the sensitive issues that caused political problems during the Korea-US FTA negotiations and the subsequent ratification process, especially regarding agricul-

ture and rice and investor-state dispute settlement procedures. Ironically, as discussed shortly, Korean negotiators would have been better positioned to manage these problems and assuage domestic critics if they had joined the talks earlier. Now reforms in these areas are already baked into the TPP cake.

Because of the importance of Korea’s trade relations with countries in the Asia-Pacific, Korean officials and business leaders recognize that eventually they will need to participate in the TPP. Indeed, the TPP would upgrade and expand the scope of Korea’s trade and investment partnerships; moreover, it would facilitate Korea’s stated desire to play an active role in regional integration. I assume it is not a matter of whether Korea will join the TPP but when. However, for Korea the cost of entry in the TPP—in terms of liberalization commitments—will prob-ably be higher than had it joined as an original signatory.

W h y t h e t P P i s i m P o r ta n t f o r Ko r e a

A brief look at trade data offers insight into the importance of the TPP for Korea. Korean exports and imports to the TPP-12 countries constitute one-third of total Korean trade (see table 1). Thus, taken together, the TPP-12 are Korea’s largest trading partner, followed by China and the European Union; collec-tively they account for more than 60 percent of Korea’s total exports and imports. Much of Korea’s remaining trade is region-ally based: Key Asian trading partners, including Hong Kong, Taiwan, and India, are among Korea’s top export destinations, while energy supplies from trading partners in the Middle East account for the bulk of other imports.

From 2009 (the trough of the global financial crisis) to 2014, Korean exports to the TPP-12 increased by more than 80 percent (see table 2), and in 2014 they totaled $188 billion. The United States and Japan accounted for about 55 percent of Korean exports to the TPP. Over the same period, Korean

imports from the TPP countries grew by almost 40 percent, although imports fell by 8 percent after 2011, driven by the decline in the value of imports from Australia and Japan of more than 20 percent (see table 3). As a result, even though Japan is the leading supplier of goods to Korea among the TPP countries, Korean imports from Japan have not increased much over 2009 levels.

Interestingly, China has become Korea’s leading bilateral trading partner, accounting for 25 percent of total Korean exports and 17 percent of total Korean imports in 2014 (see table 4). Korean exports to China totaled $145 billion in 2014, more than double the value of shipments to the United States ($70 billion) and up 68 percent since 2009. But the growth of Korean exports to China has slowed considerably since 2011, and the same trend applies to Korean imports from China. This is one reason Korea gave priority to concluding an FTA with China in order to revitalize their important trade relationship. Unfortunately, the trade deal announced at the end of 2014 was rushed to conclusion for political reasons, and significant areas of trade, such as autos and certain agricultural goods, were excluded from FTA reforms.1 In the end, then, Korea squan-dered the chance to achieve a more comprehensive deal with China that could have provided a big boost to Korean exports and possibly helped to pave the way for China’s potential partic-ipation in the TPP in the medium term.

Despite this missed opportunity, Korea has remained an active player in the expanding network of bilateral and regional FTAs in the Asia-Pacific, including the Regional Comprehensive Economic Partnership (RCEP) and the China-Japan-Korea (CJK) trilateral talks. Meanwhile, Korea has completed bilateral FTAs with 10 of the current 12 TPP members.2 Even so, the TPP would be a substantial supplement to Korean trade policy for several reasons.

First, many of the FTAs that Korea has in force with the TPP countries are less comprehensive in coverage than the TPP and contain more exceptions to FTA reforms. The TPP would upgrade these pacts, including in some respects the KORUS FTA. Second, the TPP would facilitate the alignment of trading rules across the spectrum of Korea’s FTA partners, leading to lower transaction costs and strengthening global and regional value chain linkages. Third, the TPP would effectively yield an FTA with Japan and substitute for bilateral talks that stalled

1. The results of the Korea-China FTA will be assessed in a forthcoming Policy Brief.

2. Korea has also pursued trade talks with the two remaining TPP countries, Japan and Mexico, but bilateral negotiations stalled in 2004 and 2008, respec-tively, and have yet to resume.

For Korea the cost of entr y in the TPP—in

terms of l iberalization commitments—will

probably be higher than had it

joined as an original signator y.

N u m b e r P b 1 5 - 1 3 a u g u s t 2 0 1 5

3

more than a decade ago.3 To be sure, the problems—both economic and political—that plagued the bilateral effort still need to be resolved, but the TPP’s regional approach offers a better prospect for success, even though it is clear that Korea’s market access negotiations with Japan, in the context of its prospective TPP accession, will be difficult. Similarly, the TPP would constitute an FTA with Mexico, a country with which

3. For an overview of the estimated real income and export gains from Korea’s participation in the TPP, see Petri, Plummer, and Zhai (2013).

Korea has not been able to successfully conclude a bilateral free trade pact.

t h e Co n s e q u e n C e s o f D e l ay i n g Pa r t i C i Pat i o n

At first blush, the fact that Korea will not be a founding member of the TPP does not seem to be a major problem. The TPP draws heavily on precedents set in the KORUS FTA. Unlike other potential TPP entrants, Korea has its fingerprints on the

N U M B E R P B 1 5 - T B D M O N T H 2 0 1 5

1

Table 1 Korea’s top trading partners, 2014Korean exports

Top export destinationExports (billions

of US dollars)Percent of total Korean exports

1 TPP-12 188 33

2 China 145 25

3 European Union 52 9

4 Hong Kong 27 5

5 Taiwan 15 3

6 India 13 2

7 Indonesia 11 2

8 Russia 10 2

9 Philippines 10 2

10 Brazil 9 2

Subtotal 480 84

Rest of world 92 16

Global total 573 100

Korean imports

Top import sourceImports (billions

of US dollars)Percent of total Korean imports

1 TPP-12 168 32

2 China 90 17

3 European Union 62 12

4 Saudi Arabia 37 7

5 Qatar 26 5

6 Kuwait 17 3

7 United Arab Emirates 16 3

8 Taiwan 16 3

9 Russia 16 3

10 Indonesia 12 2

Subtotal 459 87

Rest of world 66 13

Global total 526 100

Note: TPP-12: Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, United States, and Vietnam.

Source: Trade Statistics, Korea International Trade Association (KITA).

N u m b e r P b 1 5 - 1 3 a u g u s t 2 0 1 5

4

original text in many areas, suggesting Korean participation could be more seamless because of reforms already undertaken via Korea’s trade pacts with the United States and European Union.4

That said, there is a difference between negotiating the terms of the original deal among a dozen countries and nego-tiating access to an existing pact. Korean negotiators will have less leverage and could face heightened demands in at least five specific areas.

First, Korea will have less leverage in negotiating TPP entry because Japan will be able to delay Korean accession until it is satisfied with Korea’s market access offers. That would have been true as well if Korea were already participating in the TPP talks, but there probably would have been more group pressure to compromise in the initial endgame TPP negotiations.

Second, as a result of the intensive bilateral market access talks between the United States and Japan in the TPP, several sticking points will be ironed out in politically sensitive issues in the agriculture and auto sectors without Korea at the negoti-ating table. This means Korea will be expected to substantially meet benchmarks set by both of those countries.

4. The TPP does, however, seek to expand in some areas that would be KORUS-plus, such as placing disciplines on state-owned enterprises, which will require new rounds of domestic debate (and undoubtedly renewed debate over old issues as well).

Third, Korea will have less leverage in avoiding additional agricultural liberalization, especially if Japan agrees to an increased rice quota.5 Current Korean imports basically cover Korea’s minimum access quota of 409,000 tons as established under the World Trade Organization (WTO), subject to a 5 percent tariff—the over-quota tariff is set at a highly restrictive 513 percent. Depending on the results of the market access deal struck in the TPP, Korea may have to agree to a larger tariff-rate quota (TRQ) as well. Both domestic production and consump-tion of rice in Korea have been on a downward trend over the past decade (see table 5). Declining consumption, coupled with oversupply in Korea, has prompted concerns that protection of Korea’s domestic production is unsustainable. Current Korean rice imports account for 9 percent of rice consumption. That figure used to be some 4 percent based on Korea’s previous quota agreement with the WTO in the early 1990s, but the terms expanded when renegotiated in 2004, continuing an agreement that Korea would expand its import quota if it was allowed to insulate its market from full liberalization (this agreement finally expired in late 2014). According to the WTO (2012), the costs of the quantitative restrictions have included higher prices for Korean consumers—nearly double international prices. The

5. It is interesting to speculate whether, if they had been in the current talks, Korea and Japan would have been able to exempt rice from the TPP.

N U M B E R P B 1 5 - T B D M O N T H 2 0 1 5

2

Table 2 Korean merchandise exports to TPP-12, 2001−14 (billions of US dollars)TPP trading partner 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Australia 2.2 2.3 3.3 3.4 3.8 4.7 4.7 5.2 5.2 6.6 8.2 9.3 9.6 10.3

Brunei 0.0 0.0 0.0 0.0 0.1 0.0 0.0 0.1 0.1 0.1 0.6 0.1 0.1 0.3

Canada 2.0 2.3 2.7 3.4 3.4 3.6 3.5 4.1 3.4 4.1 4.9 4.8 5.2 4.9

Chile 0.6 0.5 0.5 0.7 1.2 1.6 3.1 3.0 2.2 2.9 2.4 2.5 2.5 2.1

Japan 16.5 15.1 17.3 21.7 24.0 26.5 26.4 28.3 21.8 28.2 39.7 38.8 34.7 32.2

Malaysia 2.6 3.2 3.9 4.5 4.6 5.2 5.7 5.8 4.3 6.1 6.3 7.7 8.6 7.6

Mexico 2.1 2.2 2.5 3.0 3.8 6.3 7.5 9.1 7.1 8.8 9.7 9.0 9.7 10.8

New Zealand 0.3 0.3 0.4 0.6 0.7 0.7 0.7 0.8 0.9 0.9 1.1 1.5 1.5 1.7

Peru 0.2 0.2 0.2 0.2 0.3 0.4 0.5 0.7 0.6 0.9 1.4 1.5 1.4 1.4

Singapore 4.1 4.2 4.6 5.7 7.4 9.5 11.9 16.3 13.6 15.2 20.8 22.9 22.3 23.7

Vietnam 1.7 2.2 2.6 3.3 3.4 3.9 5.8 7.8 7.1 9.7 13.5 15.9 21.1 22.4

United States 31.2 32.8 34.2 42.8 41.3 43.2 45.8 46.4 37.6 49.8 56.2 58.5 62.1 70.3

Subtotal, TPP-12 64 66 72 89 94 106 116 127 104 133 165 173 179 188

Total Korean global exports

150 162 194 254 284 325 371 422 364 466 555 548 560 573

TPP-12 as percent of Korean global exports

42 40 37 35 33 32 31 30 29 29 30 31 32 33

TPP = Trans-Pacific Partnership

Source: Trade Statistics, Korea International Trade Association (KITA).

N u m b e r P b 1 5 - 1 3 a u g u s t 2 0 1 5

5

relative importance of a possible TRQ increase of something like 100,000 to 200,000 tons would represent roughly 2.5 to 5 percent of Korean rice production and consumption.

Fourth, Korea’s delayed participation could mean more congressional demands for additional Korean commitments beyond those in the KORUS FTA when the time comes for passing Korea-TPP implementing legislation. This concern goes beyond the immediate ones about the KORUS FTA implementation issues cited in Schott and Cimino (2014). To summarize briefly, those concerns focused on (1) the proce-dures implemented by Korean officials to determine the rules of origin qualifications of US goods; (2) whether Korea was in compliance with commitments on financial services and alleged restrictions on the cross-border transfer of financial data; (3) Korea’s use of an incentive-penalty system in conjunction with auto emission measures; and (4) lack of mutual recognition in the organic certification of US agricultural products. It seems unlikely that Korea could gain an endorsement from the United States to join the TPP if there were major residual concerns about FTA implementation. For that reason, many of these issues have been fully or partially resolved over the past year.6

6. See “South Korea Kicks Off New Round of Consultations on TPP Entry,” Inside US Trade, April 2, 2015, www.insidetrade.com (accessed on May 25, 2015).

To be sure, the KORUS FTA itself would not be insulated from further congressional scrutiny. Such was the case during the KORUS FTA ratification debate, when, after much delay, addi-tional deals were made on politically contentious issues—autos, pharmaceutical patents, pork, and US visas—in order to see the final deal through (for details, see Schott 2010).

Fifth, provisions on currency policies added to the new TPA and complementary trade legislation likely to be approved by Congress in 2015 could focus attention on Korean exchange rate policies and complicate US support for Korean accession to the TPP. During the TPA debate, members of Congress from both parties voiced concern about concluding trade deals with countries that manipulate their currencies to gain commercial advantage. In the new TPA, deterring currency manipulation is among the US priority negotiating objectives for the TPP and subsequent US FTAs—although the TPA does not explic-itly require that an FTA include obligations to proscribe such practices.7 Both the Obama administration and the majority of members of Congress prefer to strengthen current US Treasury efforts—both bilateral and in the G-20—to deter currency

7. That said, Congress is also considering separate legislation that would authorize countervailing duties against imports that are allegedly subsidized by currency manipulation.

N U M B E R P B 1 5 - T B D M O N T H 2 0 1 5

2

Table 2 Korean merchandise exports to TPP-12, 2001−14 (billions of US dollars)TPP trading partner 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Australia 2.2 2.3 3.3 3.4 3.8 4.7 4.7 5.2 5.2 6.6 8.2 9.3 9.6 10.3

Brunei 0.0 0.0 0.0 0.0 0.1 0.0 0.0 0.1 0.1 0.1 0.6 0.1 0.1 0.3

Canada 2.0 2.3 2.7 3.4 3.4 3.6 3.5 4.1 3.4 4.1 4.9 4.8 5.2 4.9

Chile 0.6 0.5 0.5 0.7 1.2 1.6 3.1 3.0 2.2 2.9 2.4 2.5 2.5 2.1

Japan 16.5 15.1 17.3 21.7 24.0 26.5 26.4 28.3 21.8 28.2 39.7 38.8 34.7 32.2

Malaysia 2.6 3.2 3.9 4.5 4.6 5.2 5.7 5.8 4.3 6.1 6.3 7.7 8.6 7.6

Mexico 2.1 2.2 2.5 3.0 3.8 6.3 7.5 9.1 7.1 8.8 9.7 9.0 9.7 10.8

New Zealand 0.3 0.3 0.4 0.6 0.7 0.7 0.7 0.8 0.9 0.9 1.1 1.5 1.5 1.7

Peru 0.2 0.2 0.2 0.2 0.3 0.4 0.5 0.7 0.6 0.9 1.4 1.5 1.4 1.4

Singapore 4.1 4.2 4.6 5.7 7.4 9.5 11.9 16.3 13.6 15.2 20.8 22.9 22.3 23.7

Vietnam 1.7 2.2 2.6 3.3 3.4 3.9 5.8 7.8 7.1 9.7 13.5 15.9 21.1 22.4

United States 31.2 32.8 34.2 42.8 41.3 43.2 45.8 46.4 37.6 49.8 56.2 58.5 62.1 70.3

Subtotal, TPP-12 64 66 72 89 94 106 116 127 104 133 165 173 179 188

Total Korean global exports

150 162 194 254 284 325 371 422 364 466 555 548 560 573

TPP-12 as percent of Korean global exports

42 40 37 35 33 32 31 30 29 29 30 31 32 33

TPP = Trans-Pacific Partnership

Source: Trade Statistics, Korea International Trade Association (KITA).

N U M B E R P B 1 5 - T B D M O N T H 2 0 1 5

3

Table 3 Korean merchandise imports from TPP-12, 2001−14 (billions of US dollars)TPP trading partner 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Australia 5.5 6.0 5.9 7.4 9.9 11.3 13.2 18.0 14.8 20.5 26.3 23.0 20.8 20.4

Brunei 0.5 0.5 0.5 0.7 0.8 1.2 0.9 1.7 1.0 1.5 2.0 2.0 1.9 1.3

Canada 1.8 1.8 1.9 2.2 2.6 3.1 3.3 4.4 3.5 4.4 6.6 5.2 4.7 5.4

Chile 0.7 0.8 1.1 1.9 2.3 3.8 4.2 4.1 3.1 4.2 4.9 4.7 4.7 4.8

Japan 26.6 29.9 36.3 46.1 48.4 51.9 56.3 61.0 49.4 64.3 68.3 64.4 60.0 53.8

Malaysia 4.1 4.0 4.2 5.7 6.0 7.2 8.4 9.9 7.6 9.5 10.5 9.8 11.1 11.1

Mexico 0.3 0.3 0.3 0.4 0.5 0.8 1.0 1.0 1.0 1.5 2.3 2.6 2.3 3.3

New Zealand 0.7 0.8 0.7 0.9 0.9 1.0 1.2 1.1 0.9 1.2 1.5 1.3 1.4 1.5

Peru 0.1 0.2 0.2 0.3 0.2 0.7 1.0 0.9 0.9 1.0 2.0 1.6 2.0 1.4

Singapore 3.0 3.4 4.1 4.5 5.3 5.9 6.9 8.4 7.9 7.8 9.0 9.7 10.4 11.3

Vietnam 0.4 0.5 0.5 0.7 0.7 0.9 1.4 2.0 2.4 3.3 5.1 5.7 7.2 8.0

United States 22.4 23.0 24.8 28.8 30.6 33.7 37.2 38.4 29.0 40.4 44.6 43.3 41.5 45.3

Subtotal, TPP-12 66 71 81 100 108 121 135 151 121 160 183 173 168 168

Total Korean global imports

141 152 179 224 261 309 357 435 323 425 524 520 516 526

TPP-12 as percent of Korean global imports, 2001−14

47 47 45 44 41 39 38 35 38 38 35 33 33 32

TPP = Trans-Pacific Partnership

Source: Trade Statistics, Korea International Trade Association (KITA).

N u m b e r P b 1 5 - 1 3 a u g u s t 2 0 1 5

6

manipulation through financial diplomacy.8 The TPA legisla-tion largely supports that policy and puts forward construc-tive guidelines for Treasury’s ongoing currency consultations that should improve the effectiveness of diplomatic efforts to counter competitive depreciation policies.

To a large extent, congressional concerns have focused on China and its currency policies of a decade ago when China maintained an undervalued currency to drive export-led growth and ran current account surpluses in excess of 10 percent of GDP. Today, the International Monetary Fund (IMF) and the US Treasury do not consider the renminbi to be undervalued to any significant extent, but some politicians and academics fear a revival of past practices. In early August, the devaluation of China’s exchange rate set off alarm bells, although experts perceived the move as part of market-driven reforms rather than signaling a new wave of currency manipulation.9

8. In addition, finance ministers of the TPP countries are considering the establishment of a new consultative mechanism to discuss and monitor exchange rate policies. This forum would include all TPP countries but would not be linked to the TPP obligations. See “TPP Countries Mull U.S. Proposal For Currency Committee Side Deal,” Inside US Trade, July 30, 2015, www.insidetrade.com (accessed on August 18, 2015).

9. See Nicholas R. Lardy, “China’s Latest Currency Actions Are Market Driven,” China Economic Watch, August 11, 2015, http://blogs.piie.com/china/?p=4465 (accessed on August 18, 2015).

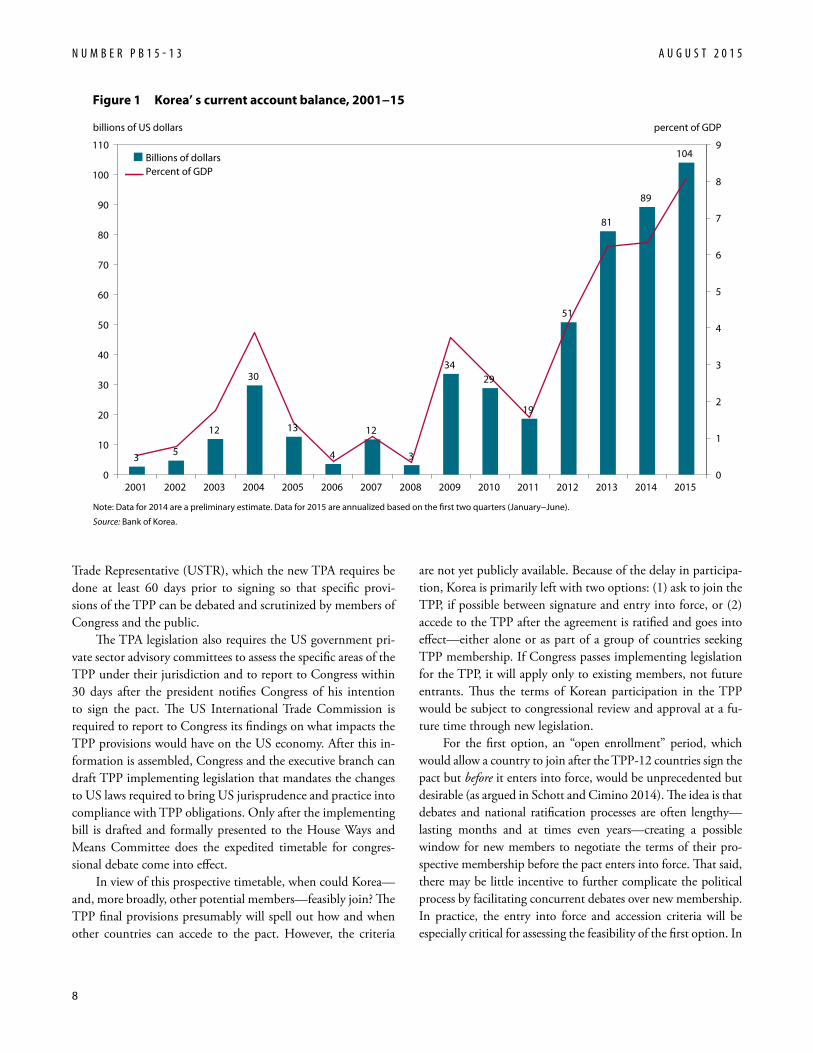

The currency issue focused on China in the TPA debate, but it is likely to refocus on Korea in the TPP context because of Korea’s current policies and interventions in foreign exchange markets to forestall appreciation of the won. The most recent US Treasury Report to Congress on International Economic and Exchange Rate Policies, issued on April 9, 2015, noted that “Korean authorities have intervened to resist won appreciation in the context of a large and growing current account surplus” (US Department of Treasury 2015, 4). In 2013 and 2014, Korea’s current account surplus exceeded 6 percent of GDP; in the first half of 2015 the surplus soared above 8 percent of GDP (see figure 1).10 Although Treasury did not conclude that Korea was “preventing effective balance of payments adjust-ments or gaining unfair competitive advantage in international trade”—the standard set by US law to cite a country as a currency manipulator—it did recommend that Korea refrain from currency intervention (except to address disorderly market conditions) and “allow the won to appreciate further” (US Department of Treasury 2015, 4).

To be sure, Korea’s particular situation with regard to the ongoing threat from North Korea suggests that its level of

10. Korea’s oil import bill is down 40 percent in 2015 compared with 2014 because of lower prices. The decrease has boosted the current account surplus by around 2.5 percent of GDP. Even excluding this windfall, the Korean surplus seems high.

N U M B E R P B 1 5 - T B D M O N T H 2 0 1 5

4

Table 4 Korean merchandise trade with China compared with TPP-12, 2001−14Korean exports Korean imports

Exports to China Exports to TPP-12 Imports from China Imports from TPP-12

YearBillions of US dollars

Percent of Korean

global exports

Billions of US dollars

Percent of Korean

global exports

Billions of US dollars

Percent of Korean

global imports

Billions of US dollars

Percent of Korean

global imports

2001 18 12 64 42 13 9 66 47

2002 24 15 66 40 17 11 71 47

2003 35 18 72 37 22 12 81 45

2004 50 20 89 35 30 13 100 44

2005 62 22 94 33 39 15 108 41

2006 69 21 106 32 49 16 121 39

2007 82 22 116 31 63 18 135 38

2008 91 22 127 30 77 18 151 35

2009 87 24 104 29 54 17 121 38

2010 117 25 133 29 72 17 160 38

2011 134 24 165 30 86 16 183 35

2012 134 25 173 31 81 16 173 33

2013 146 26 179 32 83 16 168 33

2014 145 25 188 33 90 17 168 32

Source: Trade Statistics, Korea International Trade Association (KITA).

N u m b e r P b 1 5 - 1 3 a u g u s t 2 0 1 5

7

foreign exchange reserves should be larger than that considered adequate for other countries as a defense against politically induced market disruptions and as a hedge against contingen-cies that might arise in the event of the collapse of North Korea. However, Korea’s foreign exchange reserves are already substan-tial, and running large current account surpluses does not seem to be required for precautionary purposes at this time.

The April 2015 Treasury report will be cited and exchange rate policies will be closely followed in the forthcoming congres-sional deliberations on the TPP and in the decision by Congress on whether to approve the participation of additional countries in the TPP after the pact enters into force. In that regard, the Bennet-Carper amendment to the customs and enforcement bill that proceeded in parallel with the TPA legislation in the summer of 2015 requires US officials to consider currency poli-cies when choosing future FTA partners; this provision has not yet been finalized but is likely to become law in the near future. Because of the intensity of the congressional debate on this topic, Korean policies are likely to be put in a spotlight when Korean officials ask to join the TPP.

t P P t i m e ta B l e a n D Ko r e a’s e n t r y o P t i o n s

After passage of the TPA in June 2015, trade officials accelerated efforts to complete the TPP negotiations. Efforts to conclude the deal at the meeting of TPP trade ministers in Maui at the end of July fell a little short, however. The final sticking points in areas such as agriculture, autos, and intellectual property rights were teed up for resolution by trade ministers in the near future.11 In an optimistic scenario, the TPP could be finalized in September and then signed before Christmas.

In part, the TPP timetable has been driven by progress on TPA legislation and notification and other TPA requirements that US officials must fulfill before signing the trade pact. Once the deal is substantially complete, President Barack Obama is required to give Congress 90 days’ notice before formally entering into the agreement. During this period, US officials will post the text of the agreement on the website of the US

11. See Jeffrey J. Schott, “The TPP Deal: Not Closed but Close to Closure,” Trade and Investment Policy Watch, Peterson Institute for International Economics, August 3, 2015, http://blogs.piie.com/trade/?p=384 (accessed on August 11, 2015).

N U M B E R P B 1 5 - T B D M O N T H 2 0 1 5

4

Table 4 Korean merchandise trade with China compared with TPP-12, 2001−14Korean exports Korean imports

Exports to China Exports to TPP-12 Imports from China Imports from TPP-12

YearBillions of US dollars

Percent of Korean

global exports

Billions of US dollars

Percent of Korean

global exports

Billions of US dollars

Percent of Korean

global imports

Billions of US dollars

Percent of Korean

global imports

2001 18 12 64 42 13 9 66 47

2002 24 15 66 40 17 11 71 47

2003 35 18 72 37 22 12 81 45

2004 50 20 89 35 30 13 100 44

2005 62 22 94 33 39 15 108 41

2006 69 21 106 32 49 16 121 39

2007 82 22 116 31 63 18 135 38

2008 91 22 127 30 77 18 151 35

2009 87 24 104 29 54 17 121 38

2010 117 25 133 29 72 17 160 38

2011 134 24 165 30 86 16 183 35

2012 134 25 173 31 81 16 173 33

2013 146 26 179 32 83 16 168 33

2014 145 25 188 33 90 17 168 32

Source: Trade Statistics, Korea International Trade Association (KITA).

N U M B E R P B 1 5 - T B D M O N T H 2 0 1 5

5

Table 5 Korean rice production, consumption, and imports, 2001−14Production Consumption Importsa Rice farming households

YearBillions of US dollars

Million tons

Million tons

Per capita consumption

(kilograms)Billions of US dollars

Million tons Millions

Percent of total

households

2001 8.3 5.3 5.5 89 0.03 0.2 0.77 5.2

2002 7.7 5.5 5.6 87 0.04 0.2 0.71 4.6

2003 7.4 4.9 5.6 83 0.05 0.2 0.66 4.3

2004 8.7 4.5 4.7 82 0.08 0.2 0.64 4.1

2005 8.4 5.0 5.2 81 0.05 0.2 0.65 4.1

2006 8.8 4.8 5.0 79 0.12 0.2 0.64 3.9

2007 8.5 4.7 5.1 77 0.14 0.2 0.61 3.7

2008 8.5 4.4 4.7 76 0.19 0.3 0.60 3.6

2009 6.9 4.8 4.8 74 0.25 0.3 0.57 3.4

2010 5.9 4.9 4.7 73 0.25 0.3 0.52 3.0

2011 7.2 4.3 5.2 71 0.44 0.4 0.51 2.9

2012 7.2 4.2 4.9 70 0.17 0.4 0.49 2.8

2013 7.8 4.0 4.5 67 0.49 0.5 0.48 2.6

2014b 7.8 4.2 4.5 65 0.30 0.4 0.47 2.6

a. Korea imposes a 5 percent tariff rate on its rice import quota of up to 409,000 tons. All imports above this quota are subject to a 513 percent tariff. b. Rice production and consumption data for 2014 are preliminary estimates.

Sources: Trade data: Korean Statistical Information Services, Korea International Trade Association (KITA); rice production, consumption, and household data: Korean Ministry of Agriculture, Food and Rural Affairs.

N u m b e r P b 1 5 - 1 3 a u g u s t 2 0 1 5

8

are not yet publicly available. Because of the delay in participa-tion, Korea is primarily left with two options: (1) ask to join the TPP, if possible between signature and entry into force, or (2) accede to the TPP after the agreement is ratified and goes into effect—either alone or as part of a group of countries seeking TPP membership. If Congress passes implementing legislation for the TPP, it will apply only to existing members, not future entrants. Thus the terms of Korean participation in the TPP would be subject to congressional review and approval at a fu-ture time through new legislation.

For the first option, an “open enrollment” period, which would allow a country to join after the TPP-12 countries sign the pact but before it enters into force, would be unprecedented but desirable (as argued in Schott and Cimino 2014). The idea is that debates and national ratification processes are often lengthy—lasting months and at times even years—creating a possible window for new members to negotiate the terms of their pro-spective membership before the pact enters into force. That said, there may be little incentive to further complicate the political process by facilitating concurrent debates over new membership. In practice, the entry into force and accession criteria will be especially critical for assessing the feasibility of the first option. In

Trade Representative (USTR), which the new TPA requires be done at least 60 days prior to signing so that specific provi-sions of the TPP can be debated and scrutinized by members of Congress and the public.

The TPA legislation also requires the US government pri-vate sector advisory committees to assess the specific areas of the TPP under their jurisdiction and to report to Congress within 30 days after the president notifies Congress of his intention to sign the pact. The US International Trade Commission is required to report to Congress its findings on what impacts the TPP provisions would have on the US economy. After this in-formation is assembled, Congress and the executive branch can draft TPP implementing legislation that mandates the changes to US laws required to bring US jurisprudence and practice into compliance with TPP obligations. Only after the implementing bill is drafted and formally presented to the House Ways and Means Committee does the expedited timetable for congres-sional debate come into effect.

In view of this prospective timetable, when could Korea—and, more broadly, other potential members—feasibly join? The TPP final provisions presumably will spell out how and when other countries can accede to the pact. However, the criteria

3 5

12

30

13

4

12

3

34 29

19

51

81

89

104

0

1

2

3

4

5

6

7

8

9

0

10

20

30

40

50

60

70

80

90

100

110

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Figure 1 Korea’ s current account balance, 2001−15

billions of US dollars percent of GDP

Note: Data for 2014 are a preliminary estimate. Data for 2015 are annualized based on the �rst two quarters (January−June).

Source: Bank of Korea.

Billions of dollarsPercent of GDP

N u m b e r P b 1 5 - 1 3 a u g u s t 2 0 1 5

9

membership is a distinct possibility in the coming years. In that case, Korea could not control the content or timing of joining the joint TPP membership negotiations.

In summary, Korea’s decision to delay a request to join the talks was a tactical mistake. Korea still has good options for joining the TPP in the next few years, but it will be in a less favorable position in negotiating the terms of its entry. As a major trading nation, Korea should opt to join the TPP as soon as the window for entry reopens.

r e f e r e n C e s

Petri, Peter A., Michael G. Plummer, and Fan Zhai. 2013. Adding Japan and Korea to the TPP. March 7. Available at http://asiapacific-trade.org/wp-content/uploads/2013/05/Adding-Japan-and-Korea-to-TPP.pdf.

Schott, Jeffrey J. 2010. KORUS FTA 2.0: Assessing the Changes. Policy Brief 10-28 (December). Washington: Peterson Institute for International Economics.

Schott, Jeffrey J., and Cathleen Cimino. 2014. Should Korea Join the Trans-Pacific Partnership? Policy Brief 14-22 (September). Washington: Peterson Institute for International Economics.

US Department of Treasury. 2015. Report to Congress on International Economic and Exchange Rates Policies. Washington. Available at http://1.usa.gov/1arAWv2.

WTO (World Trade Organization). 2012. Trade Policy Review: Republic of Korea. WT/TPR/S/268. Geneva. Available at www.wto.org/english/tratop_e/tpr_e/tp368_e.htm.

all likelihood, Korea will have to wait until the TPP enters into force (perhaps as early as January 2017 or possibly later).

The second option has been the more common course for adding members to FTAs under accession procedures set out in the trade pact. Interestingly, the United States has almost never invoked such provisions in US FTAs. But the 12-member TPP

is different from other US FTAs in terms of both the size of its initial membership and its ambition to expand to many other countries in the Asia-Pacific region. As such, the TPP accession clause probably will be used, although TPP countries will still require each new member to negotiate the specific terms of its market access commitments in goods and services.

Under the second scenario, Korea could join the TPP either alone or with other prospective members. Because of the number of countries that already have expressed interest in joining the TPP (e.g., the Philippines, Taiwan, and Thailand) or are undertaking due diligence to decide whether to join (e.g., China and Indonesia), the negotiation of a second tranche of

Korea sti l l has good options for joining

the TPP in the next few years, but it

wil l be in a less favorable position in

negotiating the terms of its entr y.

This publication has been subjected to a prepublication peer review intended to ensure analytical quality. The views expressed are those of the author. This publication is part of the overall program of the Peterson Institute for International Economics, as endorsed by its

Board of Directors, but it does not necessarily reflect the views of individual members of the Board or of the Institute’s staff or management. The Peterson Institute for International Economics is a private nonpartisan, nonprofit institution for rigorous, intel-

lectually open, and indepth study and discussion of international economic policy. Its purpose is to identify and analyze important issues to make globalization beneficial and sustainable for the people of the United States and the world, and then to develop and communicate practical new approaches for dealing with them. Its work is funded by a highly diverse

group of philanthropic foundations, private corporations, and interested individuals, as well as income on its capital fund. About 35 percent of the Institute’s resources in its latest fiscal year were provided by contributors from outside the United

States. A list of all financial supporters for the preceding four years is posted at http://piie.com/supporters.cfm.