política de dividendos y estructura de

TRANSCRIPT

i

1

Política de dividendos y estructura de propiedad en Latinoamérica

Dividend policy and ownership structure in Latin America

Maximiliano González*Carlos Molina Eduardo Pablo

Abstract

This paper analyzes the relationship between dividend payout and ownership structure in Latin American firms, using a comprehensive sample covering five countries. We find a U-shaped relationship between dividends and ownership: When firms are relatively less controlled by the management group or by strong shareholders, dividends tend to be a negative function of ownership; as ownership increases, dividends tend to be lower. The compelling finding, however, is the nonlinear relationship between dividends and ow-nership levels. We show that when control is already strong enough, the relationship between dividends and ownership concentration turns positive.

JEL Classification Codes: G32, G35

Keywords

Dividend policy, ownership structure, emerging mar-kets, Latin America.

Resumen

* Universidad de los Andes, Bogotá, Colombia. [email protected]

En este trabajo se analiza la relación entre el pago de dividendos y la estructura de propiedad en empresas en Latinoamérica, usando un base de datos que cubre cinco países. Encontramos una relación en forma de U: cuando las firmas están relativamente menos controla-das por el grupo gerencial o por un accionista fuerte, los dividendos tienden a ser una función negativa de la propiedad; a medida que la concentración de propiedad aumenta, los dividendos tienden a ser menores. Lo más importante de los hallazgos, sin embargo, es la relación no lineal entre dividendos y concentración de propie-dad. Se muestra que, cuando el control sobre la firma es suficientemente fuerte, la relación entre dividendos y concentración de propiedad cambia de signo y se transforma en positiva.

Palabras claves

Política de dividendos, estructura de propiedad, mer-cados emergentes y Latinoamérica.

2 Internet-Based Corporate Disclosure and Market Value: Evidence from Latin America

Introduction

Agency theory provides a strong link between dividend policy and ownership structure (Rozeff, 1982; Easter-brook, 1984; Jensen, 1986): managers acting in favor of the controlling shareholders increase dividends to reduce agency cost, especially when external finan-cing is needed. Empirically, Moh’d, Perry and Rimbey (1995) show for the U.S. market that, in fact, managers tend to adjust dividends in response to their agency cost/transaction cost tradeoff.

The role of controlling shareholders is a key issue in the agency/dividend relationship. Grossman and Hart (1980) and Shleifer and Vishny (1986) argue that large shareholders have stronger incentives to monitor ma-nagement, thereby reducing owner/manager agency cost. However, large shareholders’ blocks increase the tension between controlling and minority shareholders. Morck, Shleifer, and Vishny (1988) address this am-biguity, showing that for low levels of ownership the presence of large shareholders has a positive effect on firm value, what they called the “incentive effect.” As ownership concentration increases, however, the im-pact of large shareholders on firm value turns negative, what they called the “entrenchment effect.”

A large shareholder is not necessarily a controlling sha-reholder. Eckbo and Verma (1994) and Jensen, Solberg, and Zorn (1992) show a negative relation between inside ownership and dividend payout, yielding cash dividends of almost zero when owner-managers have full control of the firm. However, recent studies in the U.S. show that institutional investors tend to have a positive influence on dividends (Short, Zhang, and Keasey, 2002), although among dividend-paying firms they prefer those with fewer dividends (Grinstein and Michaely, 2005). In the case of individual large share-holders, Pérez-González (2002) show that dividend payouts increase in years when dividend income is less tax-disadvantaged relative to capital gains and decrease

if there is a relative increase in dividend taxes. These results show that large, not necessarily controlling shareholders, influence dividend decisions in the U.S.

The agency link between dividends and ownership is even more interesting outside the U.S. La Porta, López-de-Silanes and Shleifer (1999) show that the typical firms in the world have high ownership concentration levels and in most cases the largest shareholders are highly involved in management duties. Moreover, La Porta, et al. (1998) point out that ownership is more concentrated in countries with inferior shareholder protection (French civil law countries). In this scena-rio, La Porta, et al. (2000) tested two agency models of dividends: the “outcome” model in which dividends are paid because of the pressure of minority shareholder for dividends, and the “substitute” model in which insiders interested in issuing equity in the future pay dividends to establish a good reputation. Their results after examining 4,000 firms in 33 countries tend to support the first model: strong shareholders’ rights are associated with higher dividend payments.

In the same vein but analyzing only Asian and European firms, Faccio, Lang and Young (2001) find that when firms have more expropriation possibilities (e.g. when they are associated to a business group), firms tend to pay larger dividends in order to get cheaper capital. On the other hand, firms unaffiliated with a business group pay fewer dividends because outside investors perceive lower expropriation risk. Most recent papers find similar results: Truong and Heaney (2007) study the interaction between the largest shareholder and dividend policy in a sample of 8,279 listed firms in 37 countries. They find that dividends are negatively related to ownership concentration, and Brockman and Unlu (2009) find for 52 countries that the probability of paying dividends and their levels are significantly lower in countries with poor creditors’ rights1.

1 Country studies also find an inverse relation between ownership concentration and dividend payments. See Gugler (2003) for Austria, Correia, Da Silva, Goergen and Renneboog (2004) for Germany, and Khan (2006) for England. 2 There are few country studies that relate ownership structure and dividend policy with corporate governance and firm valuation. See for example Bebczuk (2007) for Argentina, Leal and Carvalhal-da-Silva (2007) for Brazil and Chile, Lefort and Walker (2007) also for Chile, Arce and Robles (2005) for Costa Rica, and Chong and Lopez-de-Silanes (2006) for Mexico. These country studies usually show that dividend payment is positively related with good governance practices.

3

The abundance of empirical literature studying the di-vidend/ownership relationship around the world con-trasts with the scarcity of academic research for Latin America2. Lefort (2008) studies how agency conflicts affect firms’ dividend policy in Chile. He found that the closer that cash flow rights correspond with con-trol rights (after considering among other things, such pyramidal structures and business groups), the more dividends firms pay. He also found abnormally high returns for firms that announce dividend payments and are subject to relatively high agency conflicts.

All countries in this region have the same legal origin, which is French Civil Law. Chong and Lopez-de-Silanes (2007) show that in Latin America, whose countries offer less investor protection than average French Civil Law countries, investors’ expropriation risk is more severe, the cost of capital is higher, firms pay less in dividends, and, in general, the level of financial deve-lopment is relatively very low. In addition, as shown in the reference given in footnote 2, the typical CEO is either one of the firm’s largest controlling shareholders or related to one of them, exacerbating the agency con-flict between different types of shareholders. According to Johnston (2004), only two shareholders typically hold more than 50% of a firm’s equity in the region3.

The predicted dividend/ownership relation in Latin America is far from obvious. On the one hand, the latent agency tension between controlling and mi-nority shareholders could suggest a negative relation where controlling shareholders extract firm value for their own benefits (e.g. high firm’s perquisites, related parties’ transaction). This negative relation will be con-

sistent with the previous empirical findings around the world. However, consistent with Easterbrook (1984), Gomes (2000), and La Porta et al. (2000) a firm with high ownership concentration could pay dividends to establish a good reputation, which is an important “as-set” especially in countries with weak legal protection of minority shareholders such as those in Latin America.

In this setting, we empirically examine the relation between dividend policy and ownership concentra-tion for firms based in five Latin American countries: Brazil, Chile, Colombia, Peru and Venezuela, for the years 2000-2006. We find a U-shaped relation between dividends and ownership. Results show that when firms exhibit relatively less control by management or strong shareholders, dividends tend to be negatively related to ownership. However, as ownership control increases sufficiently, the relationship between dividends and ownership levels turns positive.

Our paper contributes to the finance literature by showing that ownership structure has a statistically significant effect on dividend policy for Latin American firms. We also contribute to the incipient corporate governance literature in the Latin American region showing the importance of dividends in the latent agency conflict, not only between managers and share-holders, but also between large and small shareholders.

The rest of the paper proceeds as follows: section two describes the data and the variables used in the paper, section three presents the econometric results, and section four presents conclusions.

Data and variables

3 In a sample of Latin American large firms, Johnston (2004) finds that the first two stockholders hold between 54% and 69% of total ownership, and the first five stockholders hold between 65% and 87% of total ownership.4 Economatica is among the largest databases of financial information for Latin American firms. It includes quarterly company financial statements and shareholder information, as well as financial and market data. The data can be displayed in U.S. dollars or the local currency.

The sample includes all Latin American firms with data available in the Economatica database from 1996 to 20084. Economatica has financial data for firms in se-ven Latin American countries: Argentina, Brazil, Chile, Colombia, Mexico, Peru, and Venezuela. The database

includes firms that report their financial statements to local regulatory agencies. Ownership-concentration data is collected from Economatica only for Brazil, Chile, Colombia, Peru, and Venezuela.

4 Internet-Based Corporate Disclosure and Market Value: Evidence from Latin America

The initial sample includes 1,664 Latin American firms. This study uses fiscal year-end consolidated financial statements measured in U.S. dollars. Stock prices are for the end of the calendar year. We exclude firms without ownership information (all Argentinean and Mexican firms), with ownership information for less than two years, and firms that do not have direct operations and that are used only as vehicles for other investments. Hadi’s (1992, 1994) Outliers Method is also applied to the control variables5.

The final sample varies year by year as shown in Table 1.1, panel A. For the year 2008 (the year with the most

observations) we have 1,142 firms with ownership information. For the entire sample our unbalanced panel has 6,732 firm-year observations after excluding outliers6. In term of countries, Brazilian firms are the most representative with around half of the sample and Venezuelan firms the least with 2% as shown in Table 1.1, panel B. Finally, in terms of industrial sec-tors Economatica classified each firm in 21 different categories; we reclassified them in five macro sectors: commerce, financial, manufacture, service, and other (oil and gas, agriculture, and construction) as shown in Table 1.1, panel C7.

Table 1.1 Description of the sample

In this table we describe the sample in terms of the country and year (panel A), in terms of business sector (panel B) for the year 2008, and in terms of business sector, also for the year 2008.

Panel A: By country and by year.

5 Hadi (1992, 1994) proposes a multivariate outlier method based on the observation distance to a central cluster based on the multiva-riate covariance matrix. The exclusion of these outliers does not affect the results.6 To control for potential survivorship bias, a subset of firms was constructed with all firms present for the entire sample period. The main results were similar to those reported here.7 We decided to include financial firms such as banks, insurance companies and funds in order to maximize the number of firm-year observations; however, the main results remained if we exclude them.

5

Panel B: By country for the year 2008

Panel C: By sector for the year 2008

Source: Economatica.

Following the dividend literature, we use as the de-pendent variable:

DIV: Stock cash dividend, measured as the quotient between total cash dividend and stocks outstanding.

We also use other measures of dividends for robustness, however, such as cash dividend to sales, cash dividend to assets, total cash dividend to EBITDA, and dividend yield. In each case we calculated the cash dividend in excess of the amount the firm must pay to common shareholders as dividends. For Brazil there is a 25% of required dividend over net earnings, Chile 30%, Colombia 25%, Peru 50%, and Venezuela 25%. The security laws in each of these countries establish the minimum dividend as a compensatory measure to protect minority shareholders.

Our independent variable is ownership concentration, defined as:

OWN: Ownership concentration using the Herfin-dahl index. We calculate this index as the sum of the squares of the fractions of equity held by each individual shareholder (as reported by Economatica):

2

1_

n

ii

herf ind s=

=∑, where s

i is the percentage owner-

ship of shareholder i and n is the number of total shareholders in the firm, as reported by Economati-ca8. High levels of herf_ind represent high ownership concentration9.

8 This index tends to underestimate ownership concentration given that some shareholders could be related (i.e., have family ties). Grouping the ownership concentration if shareholder i has the same last name as shareholder j does not change the main results. Mo-reover, the sample includes just the main 10 shareholders, so the Herfindahl index has a downward bias. However, the sample includes more than 70 percent of the ownership (Σsi>0,70) for more than 2/3 of the firms included. Luckily this situation, if anything, works in the study’s favor because it tends to bias the t-values toward zero. 9 If the firm has, for instance, only two shareholders who each own 50% of the company, the herf_ind will be 0.5 (=sq(0.5)+sq(0.5)). On the other hand, if the firm has 5 shareholders with 20% ownership each, the herf_ind will be 0.2, indicating less ownership concentration. See Curry and George (1983) for a discussion on concentration proxies.

6 Internet-Based Corporate Disclosure and Market Value: Evidence from Latin America

To test the existence of nonlinearities between divi-dends and ownership concentration we also used the squared valued of our ownership proxy:

OWN2: The squared value of OWN.

Following the literature, we control for profitability (lag and actual), growth (lag and actual), risk, size, and leverage, using the following proxies:

ROA: Return on assets, measured as operating earnings (EBITDA) divided by total assets.

LROS: Lagged value of return on sales, measured as the lagged value of EBITDA divided by sales.

GROW1: Growth, measured as the moving average of the percentage change in firm’s assets for the years t-2,t-1 and t.

LGROW2: Lagged growth, measured as the moving average of the percentage change in firm’s sales for the years t-2,t-1 and t.

RISK: Risk, measured as the moving average of the per-centage change in firm’s ROA for the years t-2,t-1 and t.

SIZE: Firm size, measured as the natural logarithm of firm assets.

LLEV: Lagged leverage, measured as the lagged valued of the quotient between total debt and total assets.

To complete our set of control variables we also include in our regressions country and industry dummies. In

addition, we test different measures for each variable without significant changes in the main results.

Descriptive statistics and correlation matrix

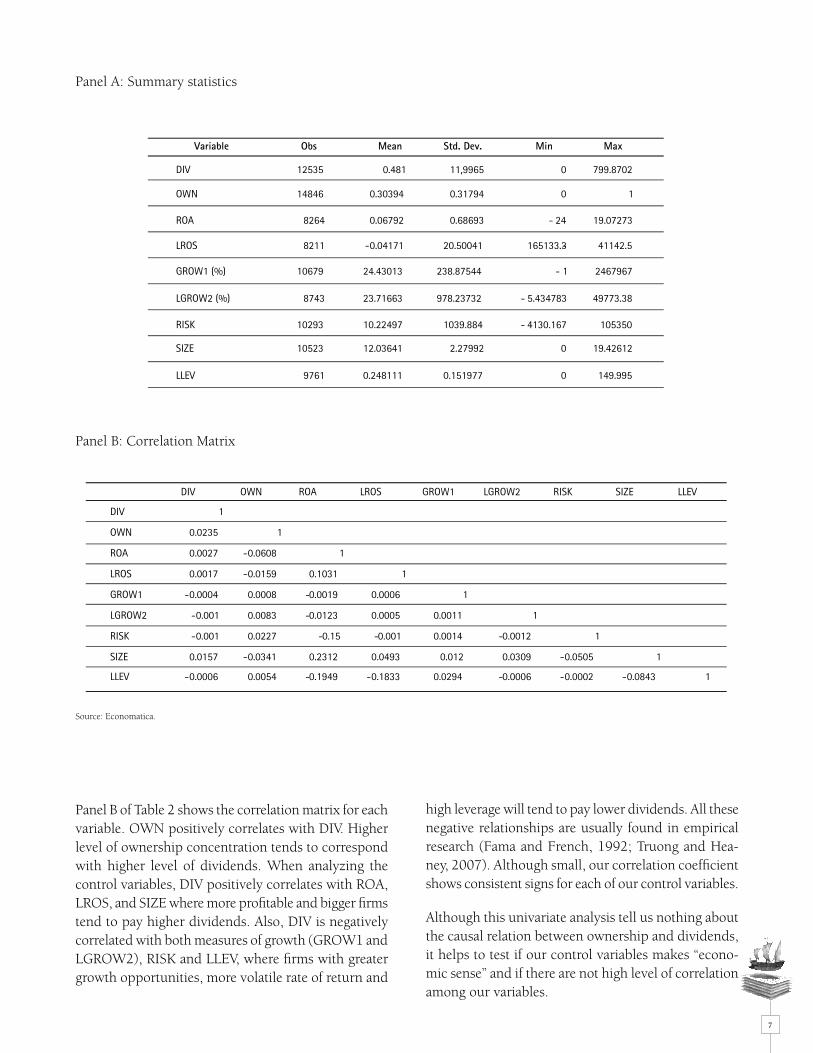

In panel A of table 1.2, we present the descriptive statistics for each variable in our pooled sample. The average stock dividend is 0.48 dollars with a standard deviation of 12 dollars approximately. The average ownership concentration, measured by the Herfindahl index is 0.30394 which is consistent with the finding of Céspedes, González and Molina (2009) for a Latin American sample. In terms of profitability, our pooled sample shows an average ROA of 6.7 percent, and a lagged ROS of -4.17 percent.

Average growth is 24.43 percent when measured as the three-year moving average of the change in assets (GROW1) and a 23.72 percent when measured as the lagged value of the three-year moving average of the change in sales. In both cases the standard deviation is very high, which is consistent with the high volatility in this region, as also shown in the RISK variable (Chong and Lopez-de-Silanes, 2007).

Finally, the average firm size in the sample is $169 million USD in total assets (=exp(12,03641)*1000) and an average leverage of approximately 25 percent. All these values must be treated with caution given the pooled nature of the sample to calculate these statistics. Summary statistics for each country and each year are available from the authors.

Table 1.2. Summary statistics and correlation matrix

In this table we present the summary statistics of the variables that will be used in the regression analysis for the pooled sample (panel A), and the correlation matrix (panel B). DIV: Stock cash dividend, measured as the quotient between total cash dividend and stocks outstanding. OWN: Ownership concentration using the Herfindahl index. OWN2: The squared value of OWN. ROA: Return on assets, measured as the operating earnings (EBITDA) divided by total assets. LROS: Lagged value of return on sales, measured as the lagged value of EBITDA divided by sales. GROW1: Growth, measured as the moving average of the percentage change in firm’s assets for the years t-2,t-1 and t. LGROW2: Lagged growth, measured as the moving average of the percentage change in firm’s sales for the years t-2,t-1 and t. RISK: Risk, measured as the moving average of the percentage change in firm’s ROA for the years t-2,t-1 and t. SIZE: Firm size, measured as the natural logarithm of firm assets. LLEV: Lagged leverage, measured as the lagged valued of the quotient between total debt and total assets.

7

Panel A: Summary statistics

high leverage will tend to pay lower dividends. All these negative relationships are usually found in empirical research (Fama and French, 1992; Truong and Hea-ney, 2007). Although small, our correlation coefficient shows consistent signs for each of our control variables.

Although this univariate analysis tell us nothing about the causal relation between ownership and dividends, it helps to test if our control variables makes “econo-mic sense” and if there are not high level of correlation among our variables.

Panel B: Correlation Matrix

Source: Economatica.

Panel B of Table 2 shows the correlation matrix for each variable. OWN positively correlates with DIV. Higher level of ownership concentration tends to correspond with higher level of dividends. When analyzing the control variables, DIV positively correlates with ROA, LROS, and SIZE where more profitable and bigger firms tend to pay higher dividends. Also, DIV is negatively correlated with both measures of growth (GROW1 and LGROW2), RISK and LLEV, where firms with greater growth opportunities, more volatile rate of return and

8 Internet-Based Corporate Disclosure and Market Value: Evidence from Latin America

Results

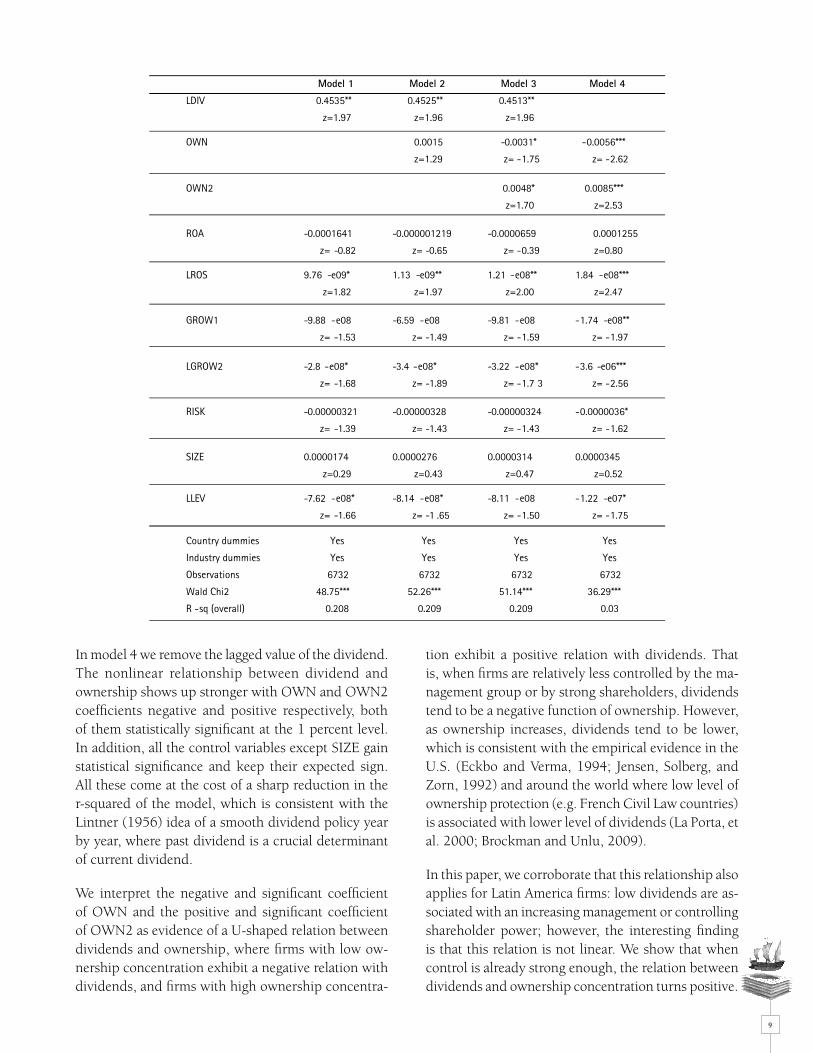

We performed an OLS panel data analysis to test the empirical relation between dividends and ownership concentration in our sample of Latin American firms. Model 1 in Table 3 shows OLS panel regression co-efficients for the theoretical determinants of dividend payout plus dummy variables to control for country and industry without including ownership concentra-tion. First, the lagged value of dividend is significant at the 5 percent level, showing as expected that corporate dividend policy aims to smooth the level of dividends over time (Litner, 1956). Second, profitability and size have a predicted positive relationship with dividend payment. In this model, the lagged value of return on sales (LROS) is positive and statistically significant at the 10 percent level. Although SIZE is positively rela-ted to dividends, it is not significant. Third, dividend theory predicts a negative relationship between divi-dends and growth, dividends and risk, and dividends and leverage. Our results show that our growth proxies (GROW1 and LGROW2) have a negative relationship

with dividends that is statistically significant at the 10 percent level, (GROW1 is significant at the 12,5 percent), the risk proxy (RISK) is negatively related as predicted but not significant, and leverage is, as pre-dicted by theory, negatively related to dividends and is significant at 10 percent. Overall, model 1 confirms that our proxies for dividend payment determinants “make economic sense” even though their statistical significance is low.

In model 2, table 2.1 we include our ownership con-centration variable and show a positive but insignificant coefficient (z=1,29; p=0.198). The rest of the variables remained basically unchanged from model 1. In model 3 we include the squared value of OWN to test for a nonlinear relationship between dividends and owner-ship. In this case OWN’s coefficient turns negative and significant at the 10 percent level (z=1,75; p=0.081) and OWN2’s coefficient is positive and statistically sig-nificant also at the 10 percent level (z=1,70; p=0,089).

Table 2.1. OLS Panel regression

In this table we present the results of a random effect OLE panel regression of DIV and OWN using different mo-del specifications. Table 1.2 specifies the variables. The regressions include an intercept and country and industry dummy variables whose coefficient are unreported. Robust t-values are in parenthesis. * = significant at 10%; ** = significant at 5%; *** = significant at 1%.

9

In model 4 we remove the lagged value of the dividend. The nonlinear relationship between dividend and ownership shows up stronger with OWN and OWN2 coefficients negative and positive respectively, both of them statistically significant at the 1 percent level. In addition, all the control variables except SIZE gain statistical significance and keep their expected sign. All these come at the cost of a sharp reduction in the r-squared of the model, which is consistent with the Lintner (1956) idea of a smooth dividend policy year by year, where past dividend is a crucial determinant of current dividend.

We interpret the negative and significant coefficient of OWN and the positive and significant coefficient of OWN2 as evidence of a U-shaped relation between dividends and ownership, where firms with low ow-nership concentration exhibit a negative relation with dividends, and firms with high ownership concentra-

tion exhibit a positive relation with dividends. That is, when firms are relatively less controlled by the ma-nagement group or by strong shareholders, dividends tend to be a negative function of ownership. However, as ownership increases, dividends tend to be lower, which is consistent with the empirical evidence in the U.S. (Eckbo and Verma, 1994; Jensen, Solberg, and Zorn, 1992) and around the world where low level of ownership protection (e.g. French Civil Law countries) is associated with lower level of dividends (La Porta, et al. 2000; Brockman and Unlu, 2009).

In this paper, we corroborate that this relationship also applies for Latin America firms: low dividends are as-sociated with an increasing management or controlling shareholder power; however, the interesting finding is that this relation is not linear. We show that when control is already strong enough, the relation between dividends and ownership concentration turns positive.

10 Internet-Based Corporate Disclosure and Market Value: Evidence from Latin America

Reference

Arce, G. and E. Robles (2005), Corporate governance in Costa Rica, Inter-American Development Bank, Research Working Paper # R-519.

Bebczuk (2007), Corporate Governance, Ownership, and dividend policies in Argentina, in Investor Protection and corporate governance: Firm level evidence across Latin America, Chong and Lópes-de-Silanes Eds.

Brockman, P. and E. Unlu (2009), Dividend policy, creditors rights, and agency cost of debt, Journal of Financial Economics 92, 267-299.

Cespedes, J., M. González y C. Molina (2009), Ownership and capital structure in Latin America, Journal of Business Research, in press. doi: 10.1016/j.jbusres.2009.03.010

Chong, A. and López-de-Silanes, F. (2007), Investor protection and corporate governance: Firm level evidence across Latin America, Stanford University Press: New York.

Chong, A. and López-de-Silanes, F. (2006), Corporate Governance and Firm Value in Mexico, Inter-American Development Bank Working Paper, #564.

Correia D., M. Goergen and L. Renneboog (2004), Divi-dend policy and corporate governance, Oxford University Press: New York.

Curry, B. and K. George (1983), Industrial concen-tration: a survey. Journal of Industrial Economics 31, 203-255.

Easterbrook, F. (1984), Two agency-cost explanations of dividends, American Economic Review 74, 650-659.

Eckbo, B. and S. Verma (1994), Managerial share ownership, voting power, and cash dividend policy, Journal of Corporate Finance 1, 33-62.

Fama, E. and K. French (1992), Testing trade-off and pecking order predictions about dividends and debt, Review of Financial Studies 15, 1-33.

Faccio, M., L. Lang, and L. Young (2001), Dividends and expropriation, American Economic Review 91, 54-78.

Gomes, A. (2000), Going public without governance: Managerial reputation effect, Journal of Finance 55, 615-646.

Conclusions

We find a U-shaped relation between dividend pay-ments and ownership structure for a sample of firms operating in five Latin American countries. Our result relates to Morck, Shleifer, and Vishny (1988) who also show a U-shaped relation between management ow-nership and firm value in the U.S. and with Céspedes, González, and Molina (2009) who show a U-shaped relation between leverage and ownership in Latin Ame-rica. Our paper contributes to the finance literature by showing the importance of ownership structure as a

determinant of dividend policy in Latin America, We also contribute to the corporate governance literature in the region showing that dividend policy moderates the latent agency conflict not only between managers and shareholders but also between large and small shareholders. The nonlinear relationship found in this paper between dividends and ownership could prove useful in further studying dividend policy in Latin Ame-rica where high ownership concentration is the norm.

11

Grossman S. and O. Hart (1980), Takeover bids, the free raider problem, and the theory of the corporation, Bell Journal of Economics 11, 42-64.

Grinstein, Y. and R. Michaely (2005), Institutional holdings and payout policy, Journal of Finance 60, 1389-1426.

Gugler, K. (2003), Corporate governance, dividend payout policy, and the interrelation between dividends, R&D, and capital investment, Journal of Banking and Finance 27, 1297-1321.

Hadi, S. (1992), Identifying multiple outliers in multi-variate data, Journal of the Royal Statistical Society, Series B 54: 761-771.

Hadi, S. (1994), A modification of a method for the detection of outliers in multivariate samples, Journal of the Royal Statistical Society, Series B 56: 393-396.

Jensen, G., D. Solberg and T. Zorn (1992), Simulta-neous determination of insider ownership, debt, and dividend policies, Journal of Finance and Quantitative Analysis 27, 247-263.

Jensen, M. (1986), Agency cost of free cash flow, corporate finance and takeovers, American Economic Review 76, 323-329.

Johnston, D. (2004), White paper on corporate governan-ce in Latin America, OECD, Paris, France.

Khan, T. (2006), Company dividends and ownership structure: Evidence from UK panel data, Economic Journal 116, C172-C189.

La Porta, R., F. Lopez-de-Silanes, A. Shleifer and R. Vishny (1998), Journal of Political Economy 106, 1113-1155.

La Porta, R., F. Lopez-de-Silanes and A. Shleifer (1999) Corporate ownership around the world, Journal of Finance 54, 471-517.

La Porta, R., F. Lopez-de-Silanes, F., A. Shleifer, R. Vis-hny (2000), Agency problems and dividend policies around the world, Journal of Finance 55, 1131-1150.

Leal, R. and A. Carvalhal-da-Silva (2007), Corporate governance and value in Brazil (and in Chile), in Investor Protection and corporate governance: Firm level evidence across Latin America, Chong and Lópes-de-Silanes Eds.

Lefort, F. (2008), El efecto de los conflictos de agencia en la política de dividendos a los accionistas: El caso chileno, El Trimestre Económico 75, 597-639.

Lefort, F. and E. Walker (2007), Corporate governance, market valuation, and payout policy in Chile, in Investor Protection and corporate governance: Firm level evidence across Latin America, Chong and Lópes-de-Silanes Eds.

Lintner, J. (1956), Distribution of income of corpora-tions among dividends, retained earnings, and taxes, American Economic Review 46, 97-113.

Moh’d, M., L. Perry and J. Rimbey (1995), An investiga-tion of the dynamic relationship between agency theory and dividend policy, Financial Review 30, 367-385.

Morck, R, A. Shleifer and R. Vishny (1988), Manage-ment ownership and market valuation: An empirical analysis, Journal of Financial Economics 20, 293-315.

Pérez-González, F. (2002), Large shareholders and di-vidends: Evidence from U.S. tax reforms, unpublished manuscript: Columbia University.

Rozeff, M. (1982), Growth, beta and agency costs as determinants of dividend payout ratios, Journal of Fi-nancial Research 5, 249-259.

Shleifer, A. and R. Vishny (1986), Large shareholders and corporate control, Journal of Political Economy 94, 461-488.

Short, H., H. Zhang and K. Keasey (2002), The link between dividend policy and institutional ownership, Journal of Corporate Finance 8, 105-122.

Truong, T. and R. Heaney (2007), Largest shareholder and dividend policy around the world, Quarterly Review of Economics and Finance 47, 667-687.

12 Internet-Based Corporate Disclosure and Market Value: Evidence from Latin America

14 Internet-Based Corporate Disclosure and Market Value: Evidence from Latin America