polyolefins overview - fpa · nick vafiadis, senior director – global polyolefins and plastics...

TRANSCRIPT

Nick Vafiadis, Senior Director – Global Polyolefins and Plastics

1(281)752-3206

FPA: September 2013

Polyolefins Overview

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

•Ethylene

•Polyethylene

•Propylene

•Polypropylene

2

Agenda

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

•Feedstock Cost Advantage

− Relationship of crude/natural gas …. & coal

• Shale based NGL’s in North America

• Abundant feedstock in Middle East

• Coal in China

•Proximity to Derivative Demand− Adding capacity to supply domestic demand (China)

3

Ethylene Capacity Drivers

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Ethylene Nameplate Capacity

By Major Region

Ethylene Production

By Feedstock

Global Ethylene Capacity = 154 MM tons2013 Production = 133 MM tons; 86% Utilization

North America

23%South

America4%

Europe20%

Africa/Middle East21%

Asia Pacific32%

Ethane36%

Propane9%

Butane4%

Naphtha47%

Gas Oil3%

Coal to

Olefins0.2%

Others1%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Ethylene Cost Curve: A Feedstock Story….

MDE Avg

NAM Avg

NEA Avg

SAM AvgSEA Avg

WEP Avg

0

300

600

900

1,200

1,500

1,800

0.0 20.0 40.0 60.0 80.0 100.0 120.0 140.0

2012 World: Ethylene Cost Curve

Cumulative Production - Million Metric Tons

Dollars Per Metric Ton

Brazil Avg

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 6

Ethylene Capacity vs. Demand

-10

-5

0

5

10

15

20

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Million Metric Tons

North America Middle East Asia Pacific West Europe

Other South America Demand Change

AAGR 13-18

Total Demand = 4.3%

Total Capacity = 4.0%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0%

20%

40%

60%

80%

100%

120%

0

3

6

9

12

15

18

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Natural Gas Crude (WTI) Gas as % of Crude

Gas as % of Crude $US per Million Btu

Key to North American AdvantageCrude to Natural Gas Ratio

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Feedstocks & Cracker Economics The Range for NGL Prices has Expanded

0

5

10

15

20

25

1995 2000 2005 2010 2015

USGC Light NaphthaBrent CrudeWTI CrudeHenry Hub GasPropaneEthaneButane

Constant 2012 Dollars Per MMBtu

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Feedstocks & Cracker EconomicsUS Feedslates Will Continue Trending Lighter

0%

20%

40%

60%

80%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Ethane Propane Butane Naphtha Gas Oil

Weight Produced From Feedstock

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

65%

70%

75%

80%

85%

90%

95%

100%

9

10

11

12

13

14

15

16

07 08 09 10 11 12 13 14

Operating RateBillion Pounds

Total Demand Effective Operating Rate Nameplate Operating Rate

Ethylene Market ViewU.S. Supply/Demand Balance Remains Tight

UPDATE FROM AUGUST 2013

Company LocationEthylene

Capacity

Propylene

CapacityStatus From Period

Equistar Clinton, IA 1049 CG: 152 Maintenance Outage Early - Aug 8-9 Weeks

Williams/SABIC Geismar, LA 1578 - Accident/Maintenance OutageJune 2013- April

20149 Months

A detailed steam cracker operating schedule can be found in the

North America Light Olefins Market Report Data Supplement or online at www.ihs.com/chemical

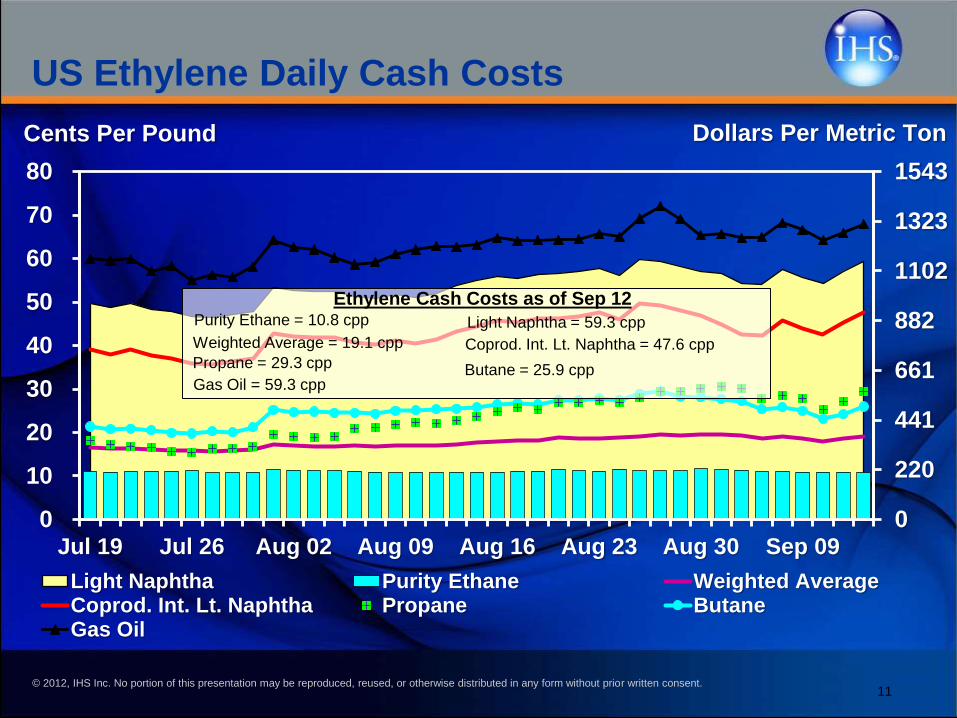

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.11

0

220

441

661

882

1102

1323

1543

0

10

20

30

40

50

60

70

80

Jul 19 Jul 26 Aug 02 Aug 09 Aug 16 Aug 23 Aug 30 Sep 09

Light Naphtha Purity Ethane Weighted AverageCoprod. Int. Lt. Naphtha Propane ButaneGas Oil

Dollars Per Metric Ton

Ethylene Cash Costs as of Sep 12 Purity Ethane = 10.8 cpp

Weighted Average = 19.1 cpp

Propane = 29.3 cpp

Light Naphtha = 59.3 cpp

Coprod. Int. Lt. Naphtha = 47.6 cpp

Butane = 25.9 cppGas Oil = 59.3 cpp

Cents Per Pound

US Ethylene Daily Cash Costs

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

0

10

20

30

40

50

60

70

10 11 12 13 14

Cents Per Pound

Weight Avg. Cash Cost Net Contract Price Avg. Spot Price

Ethylene Market ViewU.S. Spot Price Forecast to Remain Elevated versus Net Transaction

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

-200

0

200

400

600

800

1,000

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Dollars Per Ton

U.S. Ethane U.S. Integrated Lt. NaphthaWEP Naphtha Discounted Price SEA NaphthaU.S. Weighted Average

Ethylene Market ViewGlobal Annual Cash Margins…a stunning turn of events.

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Announced (-000- MT) 2012-2014 2016-2020

BASF/Total (Port Arthur) 180

Chevron Phillips (Cedar Bayou) 1500

Dow (Taft / Freeport) 386 1500

Eastman 90

Equistar (All locations) 521

Exxon (Baytown) 1500

Formosa (Point Comfort) 800

Ineos (Chocolate Bayou) 107

Oxy (Ingleside) 550*

Sasol (Lake Charles) 1400

Shell (Northeast) 1000*

Westlake (Lake Charles/Calvert City) 310

Williams (Geismar) 300

Nova (Sarnia) 250*

Braskem/Idesa (Mexico) 1000

Total 1,894 9,500

Cumulative Total 11,394* Shell, NOVA, and Oxy capacity additions shown are IHS estimates

Ethylene Market View

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Polyethylene

15

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Polyethylene: Global Momentum

LDPEHDPE

LLDPE

Total Global Demand = 81.5

Million Metric Tons

2013 Global Demand

LDPE

LLDPEHDPE

Total Global Demand = 102.9

Million Metric Tons

2018 Global Demand

AAGR 13-18 = 4.8%

Growth Forecast = 1.3 x GDP of 3.6%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Asia/Pacific Africa/ Middle East North America

South America Central Europe/ CIS West Europe

Global Demand Change

Million Metric Tons

2013 – 2018 AAGR

Total Capacity = 4.6%

Total Demand = 4.8%

Polyethylene Capacity Changes

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Shale Drives North America PE Projects

Company Location Country LDPE LLDPE HDPE Resin Type TBA Startup

2012-2013

Equistar LaPorte, TX United States 23 Q4 2012

Equistar Morris, IL United States 45 Q4 2012

2014

Equistar Bay City United States 91 Q4 2014

2015-2016

Ineos Sasol Deer Park, TX United States 475 Q2-Q3 2015

Braskem Idesa Coatzacoalcos Mexico 300 750 Q3-Q4 2015

Nova Joffre Canada 450 Q4 2015

ExxonMobil Mont Belvieu, TX United States 650 710 Q3 2016

Equistar * Corpus Christi, TX United States 500 2016

Formosa Point Comfort, TX United States 300 Q4 2016

2017

Dow Freeport, TX United States 400 650 2017

CPChem Sweeny, TX United States 500 500 Q3 2017

2018-2019

Sasol Lake Charles, LA United States 420 450 Q3 2018

Nova* Sarnia Canada 430 Q3 2018

Shell* Marcellus United States 500 500 Q3 2019

Totals, 000's MT 1420 3698 3026 500 8644

*Reported projects not fully verified or approved and not included in IHS capacity database.

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

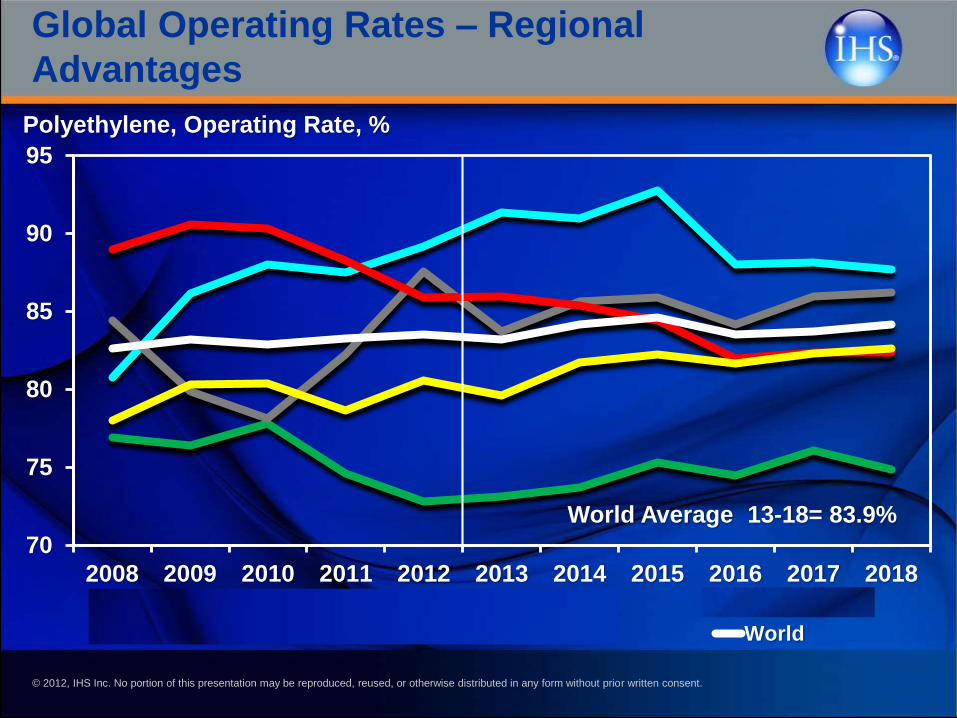

70

75

80

85

90

95

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

North America West Europe Middle East

Northeast Asia South America World

Polyethylene, Operating Rate, %

Global Operating Rates – Regional

Advantages

World Average 13-18= 83.9%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 20

Economics by Region: Price Forecast

0

20

40

60

80

100

120

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14NAM Cash Cost, Integrated NAM LLDPEWEP LLDPE CHINA LLDPE (Spot)SAM LLDPE

Cents Per Pound

Saudi ethane based

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

-5%

5%

15%

25%

-5.0

0.0

5.0

10.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

South America Net TradeNorth America Net TradeNAM Exports - SAM ImportsNAM Exports - SAM Imports as % of NAM Prod

Net Trade, Million Metric Tons Trade as a % of Production

America’s Trade Balance

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Polyethylene: Price Momentum

Equilibrates

1102

1323

1543

1764

1984

50

60

70

80

90

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

North America Discounted West Europe DiscountedCFR China Spot

Price, Dollars Per Metric TonPrice, Cents Per Pound

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Distribution of Margin

-10

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Wtd. Avg. PE Margin - Contract Non-Int. Including Discounts

Ethylene Margin - Average Acquisition Ethylene Price Minus Ethane Cracking Costs

Cents Per Pound Polyethylene

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

PE: North America Current Situation

• Domestic demand: is positive by 0.1% through August

• Export volumes: are positive by 8.3% YTD.

• Total demand: is higher versus 2012 YTD by 1.9%

• Domestic & total: demand has been trending higher since

July: August = strongest demand month of 2013.

• Export volumes: averaging about 790 million pounds per

month = 24% of total sales through August.

• We expect: demand to continue on current path and 2013

domestic demand will approximate 2012 levels. 2014 growth

slightly below GDP levels

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

PE: North America: Current + Forecast

• Contract PE prices: HDPE +11cpp ytd (only 2 cpp since Feb).

LLDPE / LDPE + 9 cpp ytd (flat since April).

• Price Increase Announcements. 5 -10 cpp for Sept / Oct

(supply/demand driven). 5 cents likely: particularly for HDPE

• Margins: YTD integrated margins avg approx. 40 cpp. 2013

will be a record. Reference: 2012 = 28.5 cpp, 2011 = 14.6 cpp

2000 – 2010 = 13.6

• Forecast: Sellers market conditions continue to keep prices

high and margins strong until new capacity drives competition

and pressures pricing and margins.

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 26

Polyethylene End Use Demand Segments

LLDPE Film 2.6%

Food Packaging 4.6%

Non-Food Packaging 3.6%

LDPE Film -1.3%

Food Packaging -6.5%

Non-Food Packaging 13.9%

HDPE Film -3.8%

Food Packaging 6.0%

Non-Food Packaging -19.2%

% Change 12 to 13 YTD Jul

Source: ACC

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

North America: New Momentum

65%

70%

75%

80%

85%

90%

95%

0.0

5.0

10.0

15.0

20.0

25.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Domestic Demand Exports Total Capacity Imports Operating Rate

Million Metric Tons Operating Rate

2013 - 2018 AAGR

Total Capacity = 5.0%

Domestic Demand = 2.3%

Exports = 6%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 28

US PE: Strong Growth Projected

-15.0

-10.0

-5.0

0.0

5.0

10.0

0.0

5.0

10.0

15.0

20.0

25.0

2008 2010 2012 2014 2016 2018 2020 2022

US Domestic Demand US Exports US Demand Change US GDP

Total Demand, Million Metric Tons % Change, Year over Year

2013 - 2018 AAGR

Total Capacity = 5.8%

Domestic Demand = 1.9%

Exports = 7.6%

2018 - 2023 AAGR

Total Capacity = 3.7%

Domestic Demand = 2.7%

Exports = 3.8%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

• Global demand growth: continues to exceed GDP

• Production capacity growth: located in low cost or

high demand regions

• Commoditization: of specialty products ex.

MLLDPE

• Trade: US to increase exports of PE resins and

finished goods as producer and processor

capacity increases

• Demand: China drives global demand growth

• Threats:

• Economy, energy price surge, legislation

(bag bans, shale gas)

29

Polyethylene Take Aways

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Propylene / Polypropylene

30

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

North America13%

South America 5%

Europe18%

Asia Pacific53%

Africa/Middle East10%

2013-2018 AAGR

Europe = 1.8%

North America = 2.3%

South America = 5.1%

Asia Pacific = 5.9%

Africa/Middle East = 5.3%

2013 Total Global Demand = 56.0 Million Metric Tons

2018 Total Global Demand = 71.6 Million Metric Tons

Global Polypropylene Demand Today

Demand Growth

2013-2018 = 28%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

2013 – 2018 AAGR

Total Capacity = 4.9%

Total Demand = 5.0%-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

North America South America Europe

Africa/Middle East Indian Sub. Northeast Asia

Southeast Asia Global Demand Growth

Million Metric Tons

PP Capacity Builds in Middle East and China

Leads to Over-Capacity

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Propylene Market ViewUS PDH Margins Attracting New Investment – 2012 cash costs

0

9

18

27

36

45

54

63

73

82

0

200

400

600

800

1000

1200

1400

1600

U.S. PDH MDE PDH China CTO West EuropeNaphtha

U.S. Splitter NortheastAsia Naphtha

NortheastAsia PDH

U.S.Metathesis

US Dollars Per Metric Ton US.Cents Per Pound

U.S. RG Price

U.S. PG Price

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

• PP supply constrained since June due to unplanned

disruptions in both monomer and PP production.

• Phillips 66 has been preparing for a 45 day outage in

October, resulting in sales allocation and an exit from spot

sales.

• PP op. rates since April have been above 90% in May, July,

and August.

• PP producers are pushing for margin improvement on the

back of very tight supply and demand fundamentals. IHS

has forecasted at least one cent of margin improvement

effective 1 January 2014.

Short Term Price Outlook: N. AmericaThe Price Spike Pattern Continues as propylene is structurally tight

34

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

• Prices fcst. to erode in Nov. and Dec in line with C3

before moving up in Q14 (refinery ta’s) peaking in April.

• Post April: prices forecast to moderate through the

remainder of the year.

• Demand destruction in PP is likely to be the main lever

to impact propylene price spikes until on-purpose

propylene production comes on stream in 2015.

35

Short Term Price Outlook Continued

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Global Demand Slowdown & Overcapacity

Centered in Asia

661

882

1,102

1,323

1,543

1,764

1,984

2,205

2,425

30

40

50

60

70

80

90

100

110

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

North America Discounted West Europe DiscountedNorth America Spot Export China Spot

Price, Dollars Per Metric TonPrice, Cents Per Pound

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Regional Polypropylene Prices

881

1,101

1,322

1,542

1,763

1,983

2,204

2,424

2,645

40

50

60

70

80

90

100

110

120

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

North America Discounted West Europe Discounted

SAM Domestic Delivered China spot (cfr China)

Price, Dollars Per Metric TonPrice, Cents Per Pound

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Polypropylene Price vs. HDPE

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

2007 2008 2009 2010 2011 2012 2013 2014

PP/HDPE North America PP/HDPE West Europe

PP/HDPE China PP/HDPE South America

Price Ratio

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 39

N. America: Propylene Market ViewFuture North America Propylene Production

• Steam cracker propylene production will trend slightly lower

as additional ethane comes to market and is preferentially

processed versus other feedstocks

• FCC (refinery grade propylene supply) operating rates are

down as refiners optimize diesel production - decreasing

refinery grade propylene supplies.

• IHS view: six new PDH units being added through the 2018

timeframe in North America….Dow (2), Enterprise, Formosa,

Williams (Canada), and Ascend.

• Enterprise and Petrologistics (along with other companies)

are exploring additional PDH units due to abundance of

propane.

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent. 40

Propylene Market ViewUS Weekly Propylene (Non-Fuel Use) Ending Stocks…..Close To Five Year

Lows Due To Unplanned Outages in Dec and Jan

Source: EIA, Data Through 26-October-12

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MM Barrels

5-Yr MIN-MAX Range 2011 2012 2013

EIA; Data through September 13 2013

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

PP North America Back in Growth Mode

40

50

60

70

80

90

100

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Domestic Demand Exports Total Capacity Imports Operating Rate

Million Metric Tons Operating Rate

2013 - 2018 AAGR

Total Capacity = 3.8%

Domestic Demand = 2.3%

Exports = 8.5%

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

Abundant Propane Drives InvestmentNorth America PG/CG Propylene Capacity Additions

Announced

Company Location Type

Capacity

KT Start-up Date

Debottlenecks /

New build

Dow Freeport, TX PDH 750 Q3 2015 NB

Enterprise Mont Belvieu, TX PDH 750 Q4 2015 NB

Formosa Point Comfort, TX PDH 600 Q3 2016 NB

Ascend Alvin, TX PDH 1000 Q1 2017 NB

Williams Redwater, Alberta PDH 500 Q2 2017 NB

Dow Freeport, TX PDH 750 Q3 2018 NB

Total 4350

On Hold

Company Location Type

Capacity

KT Start-up Date

Debottlenecks /

New Build

Petrologistics Houston, TX PDH 658 On hold DB/NB

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

PP Category Percent Change

Film 10 Mils and Below -5.0

Oriented Film -3.7

Non- Oriented Film -11.7

Sheet 10 Mills and Over

Packaging

4.0Other Sheet

Source: ACC, Plastics Division; Gov’t Trade Data

PP Film Demand 2012 vs. 2013

YTD July

-2.1

-5.8

© 2012, IHS Inc. No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent.

• Cost position to dampen short term domestic demand

• Ratio of PP/HDPE price and volatility restricting growth

• Excess propane from shale will drive new investments in on-purpose

propylene capacity

• A portion of that new propylene capacity will need to be monetized in the form of

polypropylene. Exports of PP will be concentrated within the America’s

• Prior to new on-purpose propylene capacity additions, volatility to

continue

• Propylene supply not expected to improve until late 2015

• Loss in PP capacity combined with decreased demand and increased propylene

inventory has helped rebalance the propylene market.

• Still, supply demand remains tight, and any unplanned outages have immediate

affects

North America Key Issues: Polypropylene