port finance international conference london · port finance international conference london ......

TRANSCRIPT

Container terminal ownership and operators

Port Finance International conferenceLondon

9 November 2011

2

Definitions of international terminal operators and owners

Measuring terminal operation and ownership

The main international players

Emerging international terminal operators

Remaining scope for terminal privatisation and M&A

Agenda

3

Definitions of international terminal operators and owners

Measuring terminal operation and ownership

The main international players

Emerging international terminal operators

Remaining scope for terminal privatisation and M&A

Agenda

4

What do we mean by terminal operation and ownership?

Terminal operator

Investor

Parent company Owner

Shareholder

Manager

HybridsShipping Lines

Stevedores

5

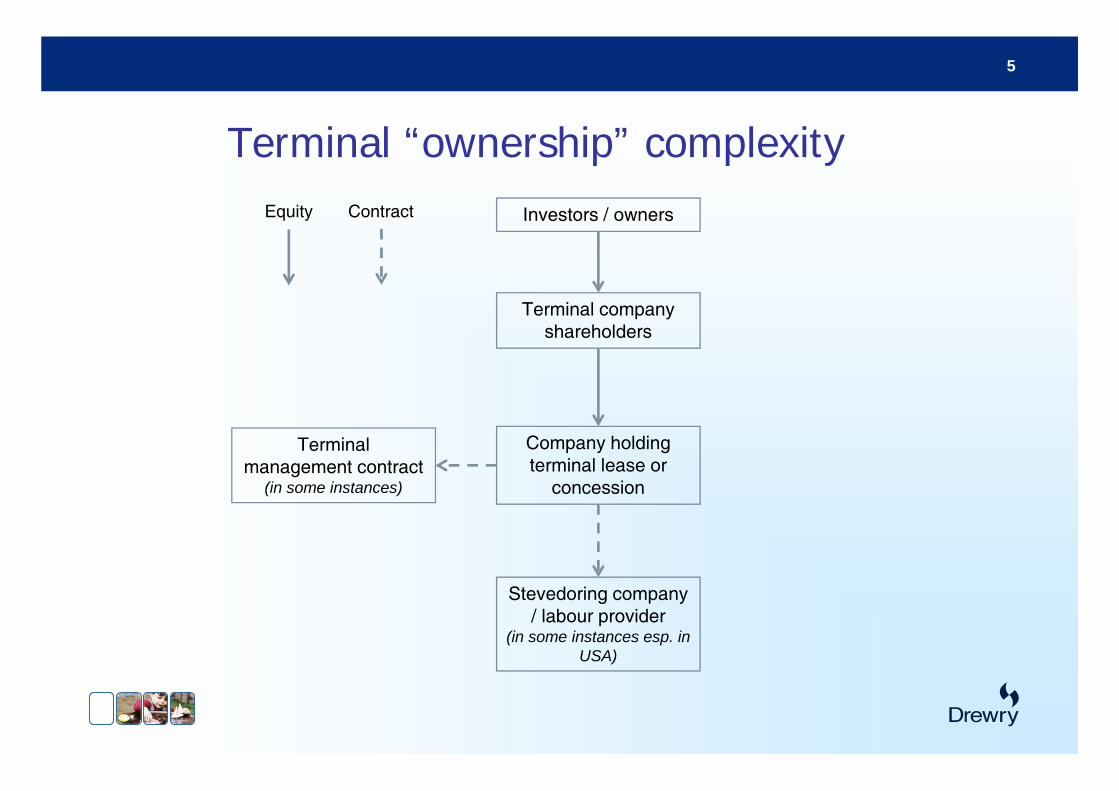

Terminal “ownership” complexity

Terminal company shareholders

Company holding terminal lease or

concession

Stevedoring company / labour provider

(in some instances esp. in USA)

Terminal management contract

(in some instances)

Investors / ownersEquity Contract

6

Terminal “ownership” complexityLarge financial institution +

other shareholders

International terminal operator

Major and minor shareholders

Shipping line

Terminal company

Stevedoring company

(in some instances)

50% 50%

100%

7

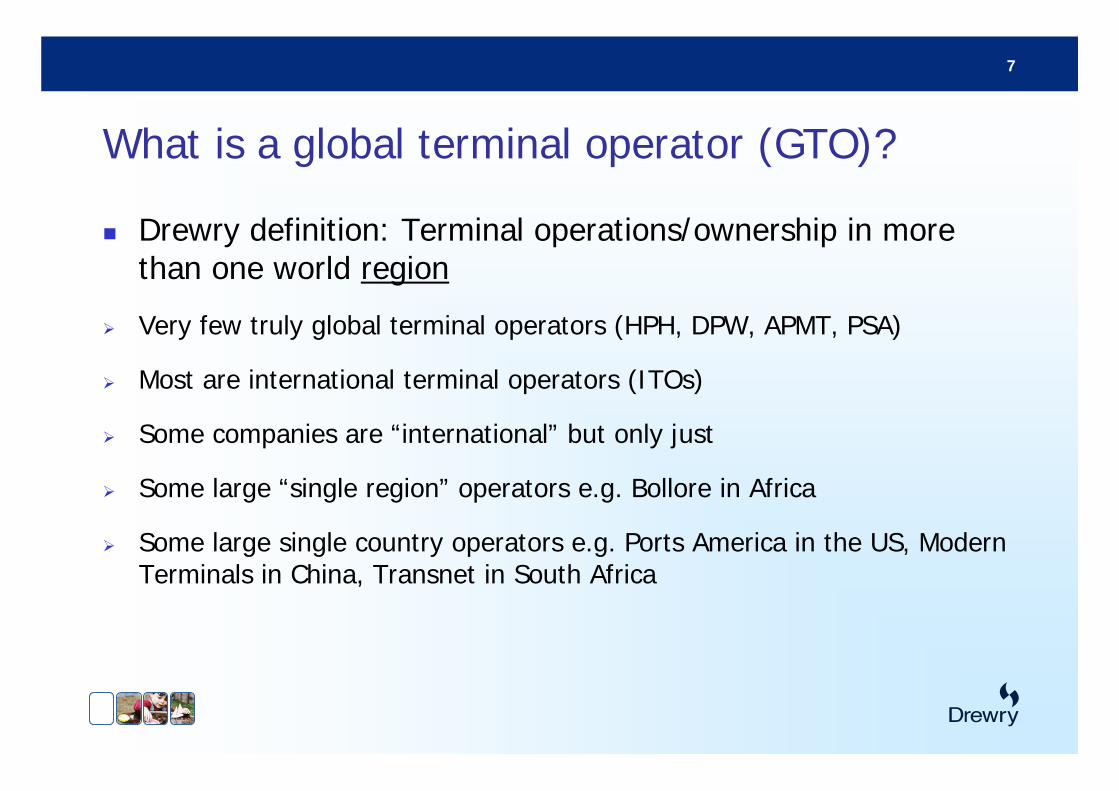

What is a global terminal operator (GTO)?

Drewry definition: Terminal operations/ownership in more than one world region

Very few truly global terminal operators (HPH, DPW, APMT, PSA)

Most are international terminal operators (ITOs)

Some companies are “international” but only just

Some large “single region” operators e.g. Bollore in Africa

Some large single country operators e.g. Ports America in the US, Modern Terminals in China, Transnet in South Africa

8

Definitions of international terminal operators and owners

Measuring terminal operation and ownership

The main international players

Emerging international terminal operators

Remaining scope for terminal privatisation and M&A

Agenda

9

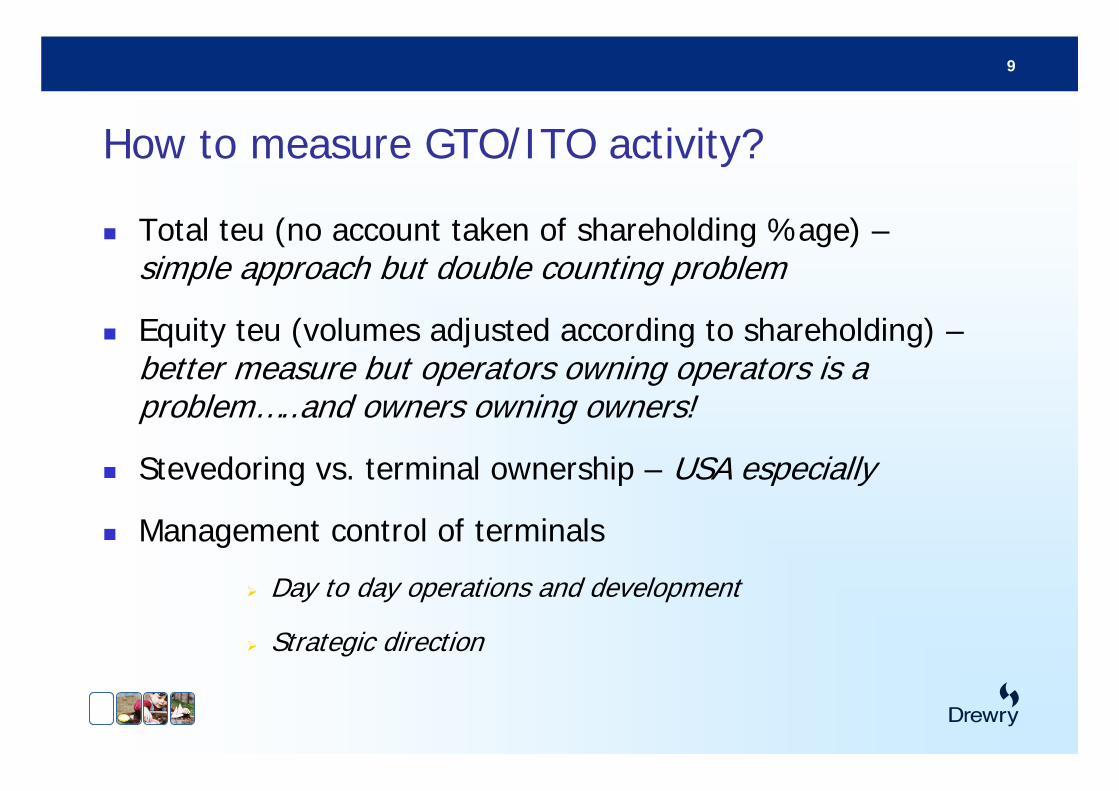

How to measure GTO/ITO activity?

Total teu (no account taken of shareholding %age) –simple approach but double counting problem

Equity teu (volumes adjusted according to shareholding) –better measure but operators owning operators is a problem…..and owners owning owners!

Stevedoring vs. terminal ownership – USA especially

Management control of terminals

Day to day operations and development

Strategic direction

10

Why bother measuring terminal operation and ownership?

Important to understand: the structure of the industry the strategies and motivations of

operators and investors who the key players are and why how things change over time what the future might hold what opportunities exist

11

Definitions of international terminal operators and owners

Measuring terminal operation and ownership

The main international players

Emerging international terminal operators

Remaining scope for terminal privatisation and M&A

Agenda

12

Top 15 GTOs/ITOs, 2010, million equity teu

Note: No adjustments to PSA and HPH figures to reflect PSA’s 20% stake in HPH

13

Top 10 GTOs/ITOs – Degree of internationalism

Proportion of 2010 equity teu derived from terminals outside the operators home base country

14

Top 10 GTOs/ITOs – Degree of management control

Estimated proportion of 2010 equity teu under management control

15

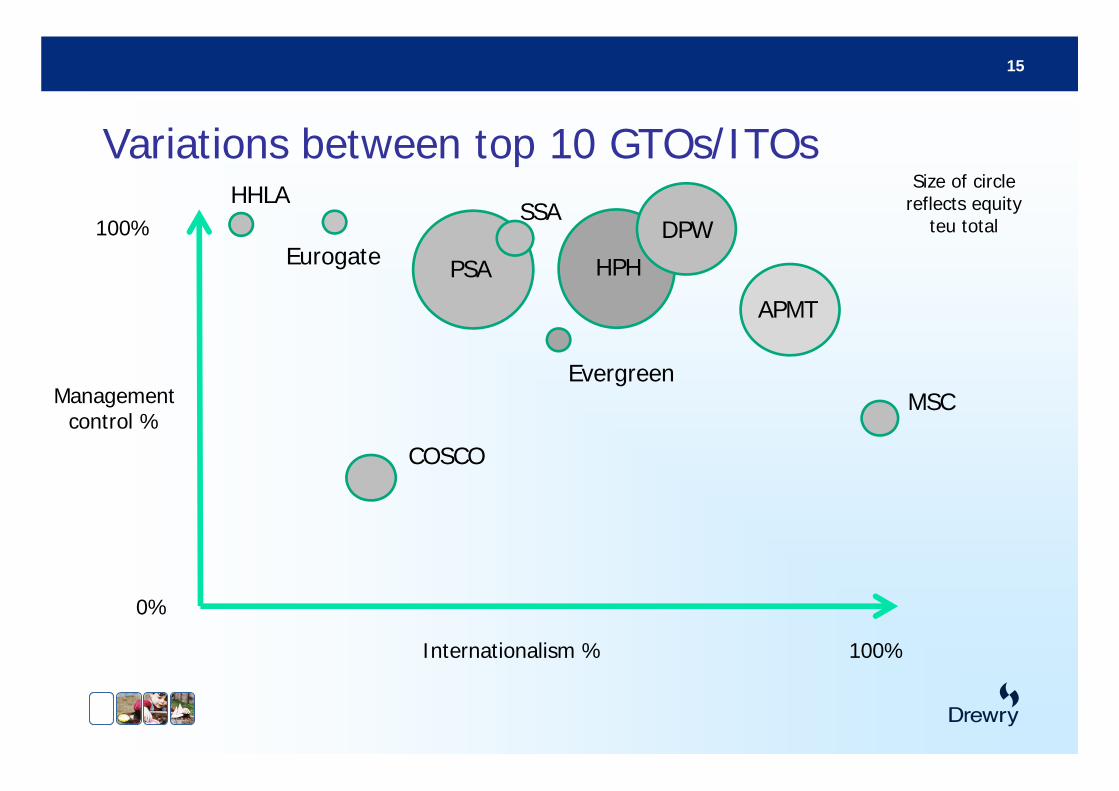

Variations between top 10 GTOs/ITOs

Internationalism %

Management control %

100%

100%

0%

PSA HPH

DPW

APMT

COSCO

MSC

SSA

Evergreen

Eurogate

HHLASize of circle

reflects equity teu total

16

Definitions of international terminal operators and owners

Measuring terminal operation and ownership

The main international players

Emerging international terminal operators

Remaining scope for terminal privatisation and M&A

Agenda

17

Emerging ITOs

Existing GTOs/ITOs are well established and highly experienced

But there are some new players emerging: China and Middle East: Cash rich organisations keen to

expand India: Political desire to expand overseas European and US based operators seeking to expand

selectively (OECD)

18

Emerging ITOs – Some examples

China Shipping – US west coast

SIPG – 25% stake in APMT Zeebrugge

China Merchants – purchased stake in terminal in Lagos, Nigeria, also investing in Colombo expansion and Vietnam

Gulftainer – Iraq and Brazil, also Russia (multi-purpose terminal)

Noatum – OECD focus for expansion beyond Spain

Ports America – US based but may expand overseas

IPH – Stake in Exolgan, Buenos Aires, plus Port of Brisbane

Yildirim – 20% stake in CMA CGM, plus 50% stake in Malta Freeport

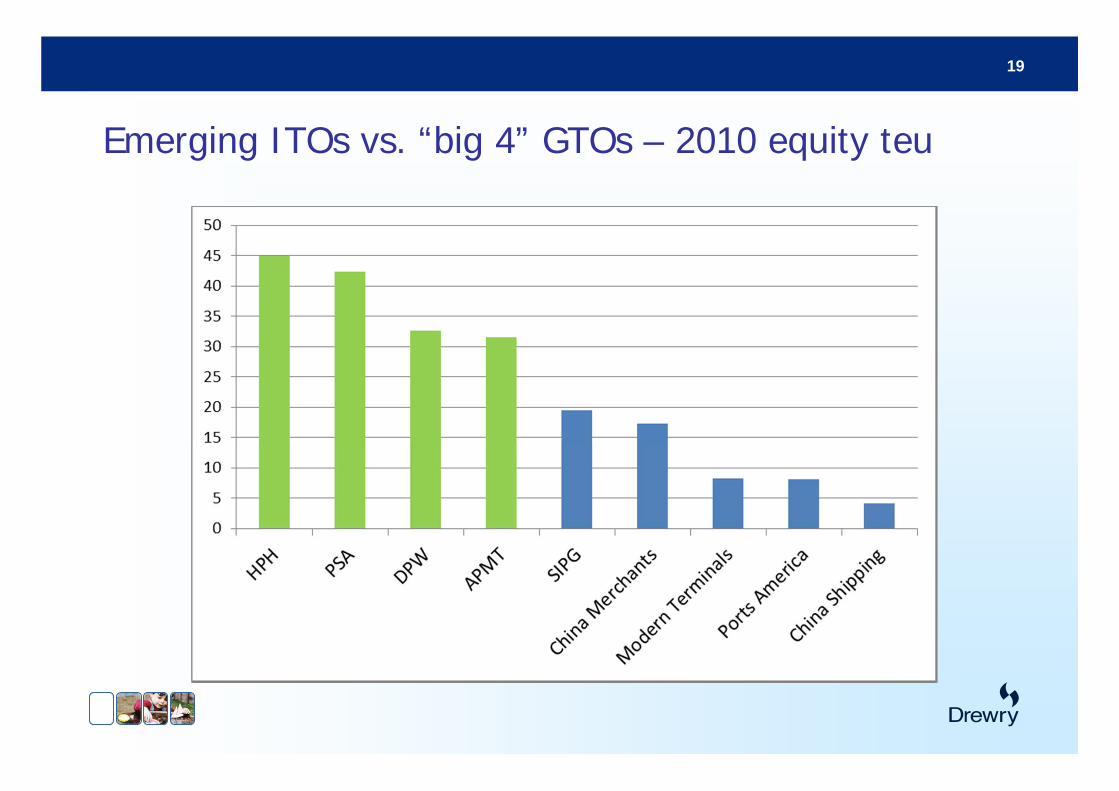

19

Emerging ITOs vs. “big 4” GTOs – 2010 equity teu

20

Definitions of international terminal operators and owners

Measuring terminal operation and ownership

The main international players

Emerging international terminal operators

Remaining scope for terminal privatisation and M&A

Agenda

21

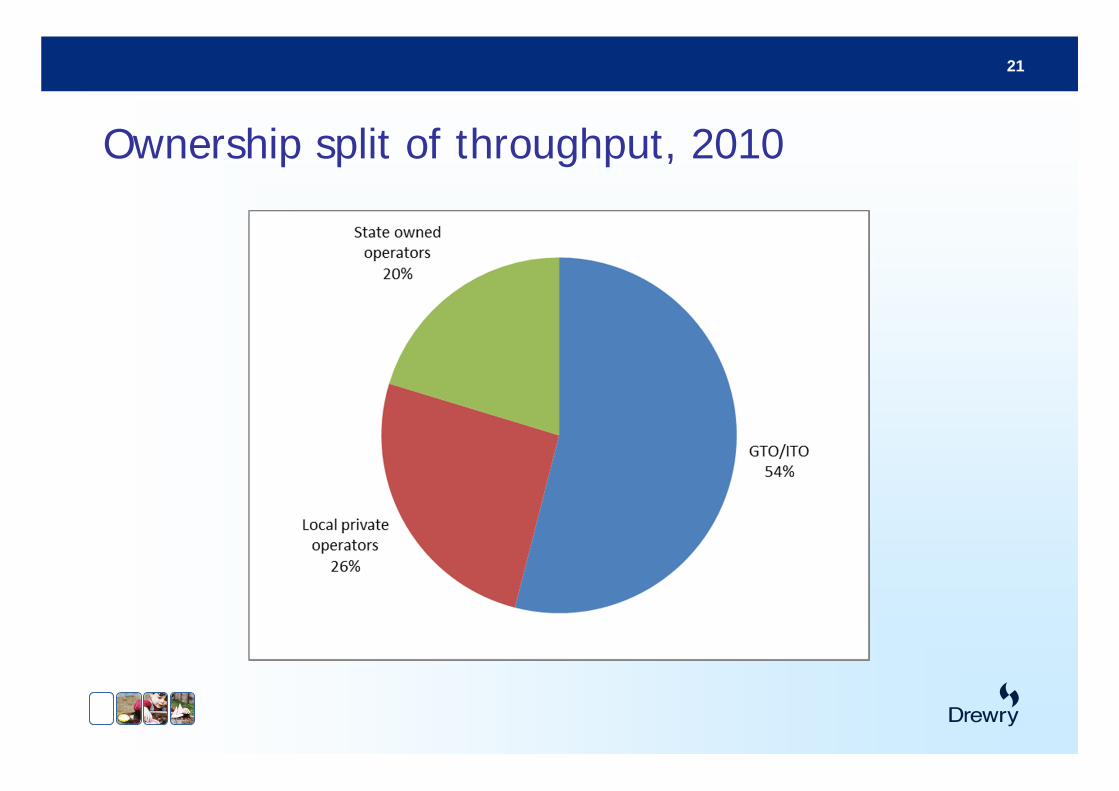

Ownership split of throughput, 2010

22

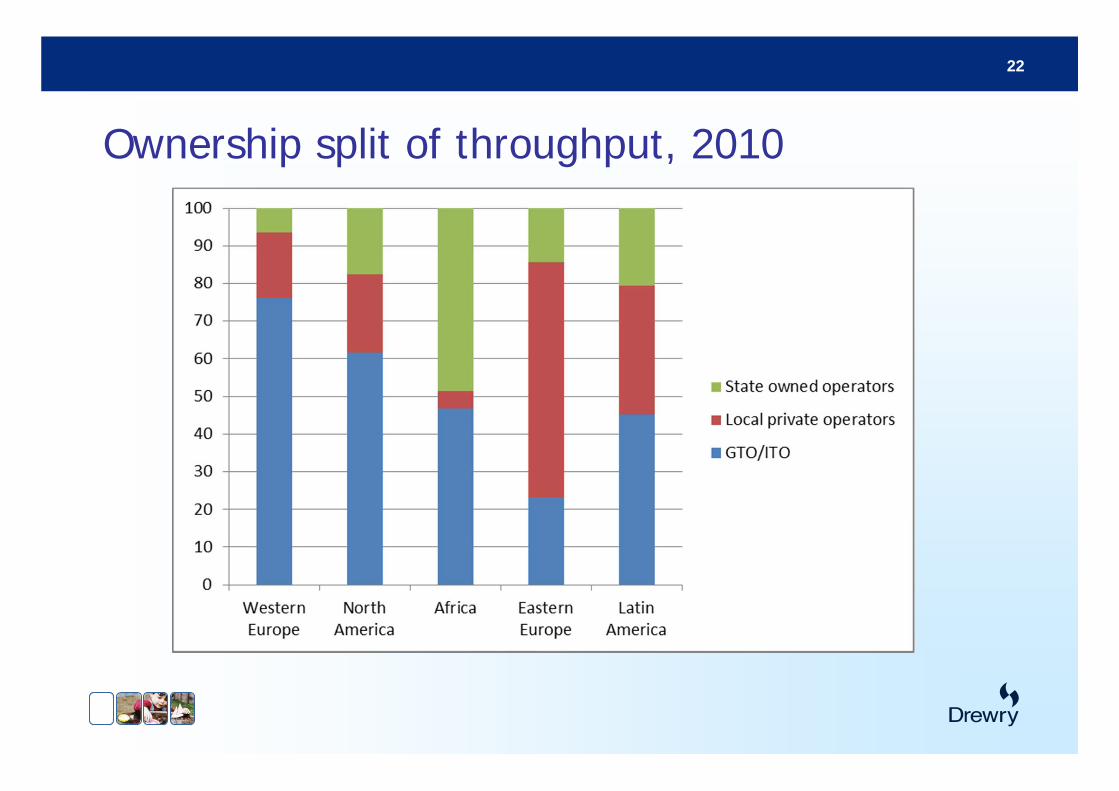

Ownership split of throughput, 2010

23

Remaining terminal privatisation potential

In 2010 there were about 50 terminals worldwide handling more than 250,000 teu p.a. and in state ownership.

Recent deals are reducing this number e.g. Gothenburg, Kingston, Puerto Limon

Most significant remaining locations today: South Africa Israel Iran Kenya Mauritius Egypt Sri Lanka Turkey

24

Privatisation of port authorities/companies is currently gaining momentum Brisbane and Abbot Point (done) Poti – Georgia (done) Monrovia – Liberia (done) Eilat (under way) Dover (planned) Piraeus & Thessaloniki (planned) Port Botany (Sydney) (planned)

In Australia, long term leases rather than outright sales in some instances e.g. Brisbane and Abbot Point (99 years)

Main reasons for the privatisation trend: access to private money access to expertise (developing world especially)

Privatisation potential – Port authorities/companies

25

Terminal ownership and operation is complex and can be looked at many ways

No definitive way of measuring but important to measure nevertheless

Drewry is developing new ways to analyse the industry

Some significant new international terminal operators/owners are likely to emerge in the coming years

Privatisation potential is still there, but getting more limited, especially for larger terminals

M&A activity likely to be an ongoing focus

Conclusions