portfolio review 4th quarter 2014

TRANSCRIPT

Wendy J. Dominguez, MBAJerry Huggins, MBA, CFP®

PORTFOLIO REVIEW4th Quarter 2014

Rick Rodgers, AIFA®

Prepared by: Josh Bond

—

———

—

—

——

——

—

—

——

————

—

—

—

—

—

—

—

—

—

—

—

—

—

*As of January 2015

Privileged and Confidential

2INTEGRITY. BALANCE. OBJECTIVITY.

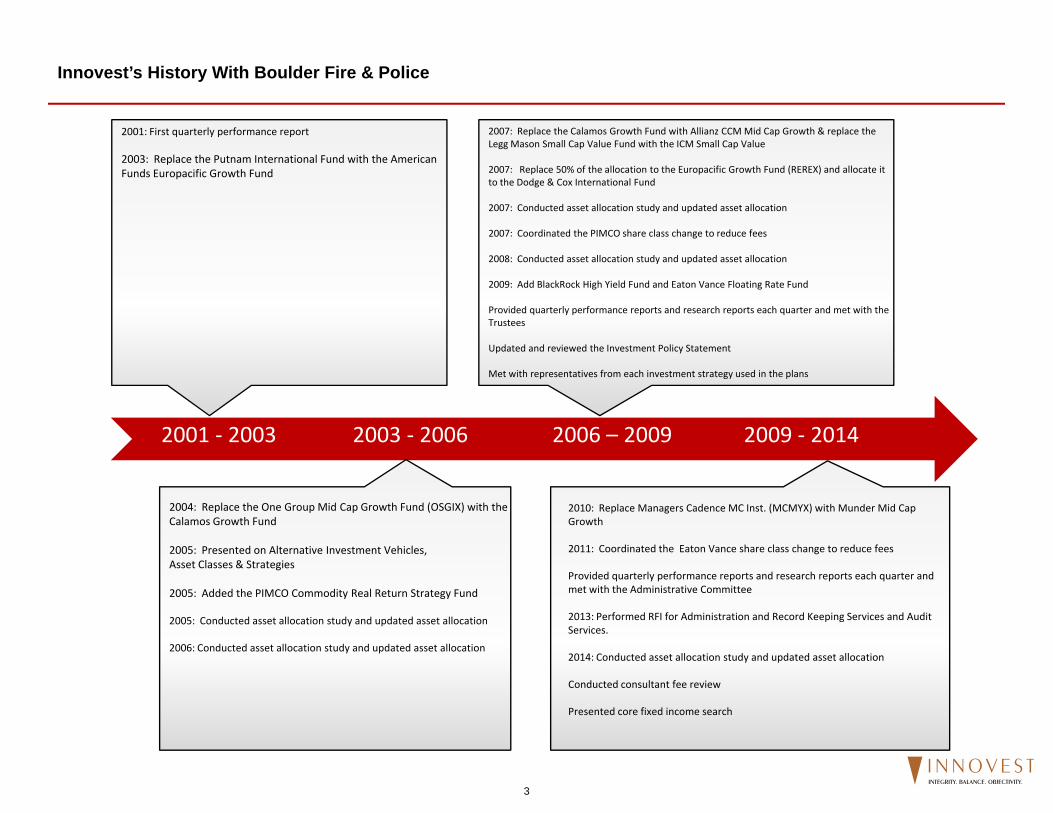

Innovest’s History With Boulder Fire & Police

2001: First quarterly performance report 2007: Replace the Calamos Growth Fund with Allianz CCM Mid Cap Growth & replace the Legg Mason Small Cap Value Fund with the ICM Small Cap Value

2003: Replace the Putnam International Fund with the American Funds Europacific Growth Fund 2007: Replace 50% of the allocation to the Europacific Growth Fund (REREX) and allocate it

to the Dodge & Cox International Fund

2007: Conducted asset allocation study and updated asset allocation

2007: Coordinated the PIMCO share class change to reduce fees

2008: Conducted asset allocation study and updated asset allocation

2009: Add BlackRock High Yield Fund and Eaton Vance Floating Rate Fund

Provided quarterly performance reports and research reports each quarter and met with the Trustees

Updated and reviewed the Investment Policy Statement

2001 ‐ 2003

Met with representatives from each investment strategy used in the plans

2003 ‐ 2006 2006 – 2009 2009 ‐ 2014

2004: Replace the One Group Mid Cap Growth Fund (OSGIX) with the Calamos Growth Fund

2005: Presented on Alternative Investment Vehicles,A Cl & S i

2010: Replace Managers Cadence MC Inst. (MCMYX) with Munder Mid Cap Growth

2011: Coordinated the Eaton Vance share class change to reduce feesAsset Classes & Strategies

2005: Added the PIMCO Commodity Real Return Strategy Fund

2005: Conducted asset allocation study and updated asset allocation

2006: Conducted asset allocation study and updated asset allocation

Provided quarterly performance reports and research reports each quarter and met with the Administrative Committee

2013: Performed RFI for Administration and Record Keeping Services and Audit Services.

2014: Conducted asset allocation study and updated asset allocation

Conducted consultant fee review

Presented core fixed income search

3INTEGRITY. BALANCE. OBJECTIVITY.

Performance Over Time

Risk and Return (Since Inception) Asset Allocation

Cumulative Performance over Time

Change in Account ValueMarket Value

As of10/01/2014

Market ValueAs of

12/31/2014Change

$

Boulder F & P Total Fund 121,276,831 124,267,664 2,990,833

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

SinceInception

InceptionDate

Boulder F & P Total Fund 2.56 5.50 5.50 12.18 10.16 5.98 8.72 07/01/1990Boulder F & P Custom BM 1.54 5.38 5.38 12.38 10.03 5.29 8.28Difference 1.02 0.12 0.12 -0.20 0.13 0.69 0.44

$0 $12,389,241 $24,778,482 $37,167,723 $49,556,964 $61,946,205

VT Retirement Income Advantage

JPMorgan High Yield Select

PIMCO Total Return; Inst

PIMCO Commodity Real Return

Victory Munder Mid Cap Core Growth

Eaton Vance Floating Rate; I

ICM Small Company

Vantage Trust Plus

Dodge & Cox Int'l

American Funds EuroPacific Gr

Boston Trust Fixed Income - Boulder F&P

Boston Trust Equity - Boulder F&P

$771,943

$2,257,480

$4,586,674

$4,782,424

$7,697,806

$7,905,261

$7,908,651

$8,032,773

$10,203,183

$10,522,108

$12,329,305

$47,270,058

8.7

9.0

9.3

9.6

9.9

Ret

urn

(%)

10.0 11.0 12.0 13.0 14.0 15.0 16.0 17.0Risk (Standard Deviation %)

S&P 500 Index

Boulder F & P Total Fund

Boulder F & P Total Fund Boulder F & P Custom BM

-250 %

0%

250%

500%

750%

1,000%

9/90 12/91 3/93 6/94 9/95 12/96 3/98 6/99 9/00 12/01 3/03 6/04 9/05 12/06 3/08 6/09 9/10 12/11 3/13 12/14

Executive SummaryDecember 31, 2014

4INTEGRITY. BALANCE. OBJECTIVITY.

December 31, 2014

20 00%

THE MARKETS

Investment Returns 2014

15.00%

20.00%S&P 500

Russell 2000Year 4Q14

13.69%

10.00%

MSCI EAFE

MSCI EM

Barclays US Agg Bond

13.69% 4.93%

4.89%5.97%

5.00%

y gg

9.73%

5.97% 1.79%

4.89%

-4.90%

-2.19%

-5.00%

0.00%

-2.19% -3.57%

-4.90% -4.50%

-10.00%

% %

-15.00%1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

5INTEGRITY. BALANCE. OBJECTIVITY.

December 31, 2014

CONTINUED CONCERNS FOR THE GLOBAL ECONOMY• China’s economy slowed in 2014 to the lowest growth rate

Fourth Quarter 2014 Capital Markets: HEADWINDS

China’s Recent Slowdown is Noteworthy• China s economy slowed in 2014 to the lowest growth rate

since Q1 2009, despite an equity market rally.• The Eurozone economy worsened in Q4 2014, while the

European inflation rate approached 0% at year-end.• Japan’s economy contracted unexpectedly in Q3 by 1.6%

annualized, as the country slipped into recession.• Weak demographic trends remain a headwind for the

Eurozone, Japan, Russia and China.

THE QUANDARY OF MONETARY STIMULUS Diverging Monetary Policy in 2014

Sources: J.P. Morgan and China National Bureau of Statistics. December 2014.

• Facing dire economic data, the European Central Bank is forced to reconsider quantitative easing.

• After massive stimulus measures, the Bank of Japan is left with fewer policy options in 2015.

• The U S Federal Reserve will consider raising short-termThe U.S. Federal Reserve will consider raising short term interest rates in 2015.

• Is bad news good news yet again for financial markets? Predicting the impact of future government policy is difficult.

6INTEGRITY. BALANCE. OBJECTIVITY.

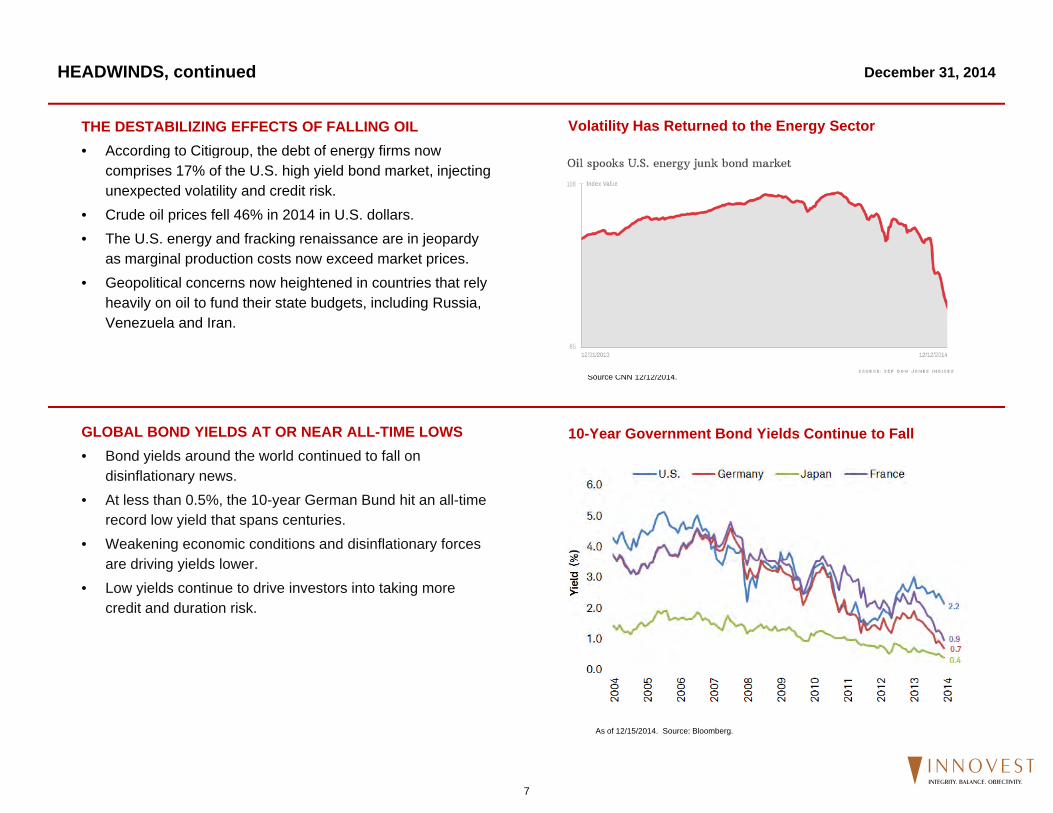

December 31, 2014HEADWINDS, continued

THE DESTABILIZING EFFECTS OF FALLING OIL• According to Citigroup the debt of energy firms now

Volatility Has Returned to the Energy Sector• According to Citigroup, the debt of energy firms now

comprises 17% of the U.S. high yield bond market, injecting unexpected volatility and credit risk.

• Crude oil prices fell 46% in 2014 in U.S. dollars.• The U.S. energy and fracking renaissance are in jeopardy

as marginal production costs now exceed market prices. • Geopolitical concerns now heightened in countries that rely

heavily on oil to fund their state budgets, including Russia, Venezuela and Iran.

GLOBAL BOND YIELDS AT OR NEAR ALL-TIME LOWS• Bond yields around the world continued to fall on

10-Year Government Bond Yields Continue to Fall

Source CNN 12/12/2014.

Bond yields around the world continued to fall on disinflationary news.

• At less than 0.5%, the 10-year German Bund hit an all-time record low yield that spans centuries.

• Weakening economic conditions and disinflationary forces d i i i ld lare driving yields lower.

• Low yields continue to drive investors into taking more credit and duration risk.

As of 12/15/2014. Source: Bloomberg.

7INTEGRITY. BALANCE. OBJECTIVITY.

December 31, 2014

A LONE BRIGHT SPOT: U.S. CONDITIONS IMPROVE• U S consumer confidence reached its highest level in

Fourth Quarter 2014 Capital Markets: TAILWINDS

U.S. Economic Confidence Index Highest Since 2007

• U.S. consumer confidence reached its highest level in seven years at year end.

• Revised U.S. GDP growth hit 5.0% in Q3, the fastest pace since 2003.

• Real personal consumption is up 2.8% in the last year, reflecting rising incomes.

• Unemployment is now at its lowest level since 2008.• The health of U.S. corporations remains very strong.

U.S. HOUSEHOLDS IN BETTER FINANCIAL SHAPE Massive Cost Savings for the Average FamilyU.S. HOUSEHOLDS IN BETTER FINANCIAL SHAPE• U.S. gasoline prices hit six-year lows, with the average

household expected to save $700 annually.• U.S. household debt service is at 9.9% of disposable

income, the lowest since the Fed began measuring in 1980

Massive Cost Savings for the Average Family

1980.• Improving trends in wage growth and employment

continued in 2014.• A rising U.S. dollar has improved consumer buying

power for foreign goods.

Sources: U.S. EIA as of 12/16/2014.

8INTEGRITY. BALANCE. OBJECTIVITY.

December 31, 2014TAILWINDS, continued

CONSUMER SPENDING REMAINS POSITIVEM th t thi d f th U S i d i b

Real U.S. Personal Consumption Still Rising

• More than two-thirds of the U.S. economy is driven by consumer spending.

• According to ShopperTrak and Bloomberg, 2014 U.S. holiday sales grew at the fastest pace since 2005.

• Improving labor market and consumer confidence have been a tailwind for consumer spending.

• 2014 U.S. vehicle sales hit their highest number since 2006.

COMPELLING NON-US EQUITY VALUATIONSE i k t iti i tt ti l i d l ith

International Stock Markets Remain Cheap• Emerging market equities remain attractively priced, along with

a superior growth and debt profile.• Developed international stock markets in Europe and Japan

have lagged the U.S. significantly coming out of the recession.• With dramatic sell-off in energy, new opportunities exist in

commodities and MLPs.

MSCI trailing price-to-book ratios as of 11/28/2014. Sources: Barclays and FactSet.

9INTEGRITY. BALANCE. OBJECTIVITY.

US Market Indices Performance US Market Sector Performance

Source: Investment Metrics, LLC

Source: Investment Metrics, LLCSource: Investment Metrics, LLC

1 Quarter

0.0

10.0

20.0

-10.0

-20.0

Re

turn

(%)

S&

P 5 0

0

I nd

e x

Ru s

s ell

2

0 00

I n

de x

MS

CI

E

AF

E

I nd

e x

MS

CI

E

AF

E LC

I nd

e xM

SC

I

Em

ergi

ng

Ma rk

ets

I n

de x

Bar

c lay s

Ca

pita

l

Ag g

r eg

a te

BC

Mu

nic

ipa l

B

on

dB

a rcla

ys U

.S.

C

or p

:

Hig

h

Yi e

ldB

C G

lob a

l

Ag

g r eg

ate

Ex U

SD

Em

ergi

ng

Ma rk

et D

ebt

S&

P/L

STA

Leve

rag e

d

Lo a

n

I nd

e x

MS

CI

U

.S.

R

EIT

I n

de x

DJ -U

BS

Co

mm

od it

y

I nd

e x

HFR

I

Fo F

Co

mpo

sit e

I nd

e x

4.9

9.7

-3.5

1.8

-4.4

1.8 1.4

-1.0-3.0

-0.9 -0.5

14.3

-12.1

0.8

S&P 500 Consumer Discretionary S&P 500 Consumer Staples S&P 500 Energy

S&P 500 Financials S&P 500 Health Care S&P 500 Industrials

S&P 500 Information Technology S&P 500 Materials S&P 500 Telecom Services

S&P 500 Utilities

0.0

20.0

40.0

60.0

-20.0

-40.0

Re

turn

(%)

1

Quarter

1

Year

13.2

29.0

-4.2

3.0

-1.8

6.95.2

20.1

6.8 9.87.5

25.3

7.2

15.2

-10.7 -7.8

8.2

16.08.7 9.7

S&P 500 S&P 500 Growth S&P 500 Value

Russell Midcap Index Russell Midcap Growth Index Russell Midcap Value Index

Russell 2000 Index Russell 2000 Growth Index Russell 2000 Value Index

0.0

5.0

10.0

15.0

20.0

Re

turn

(%)

1

Quarter

1

Year

9.4

4.2

10.1

5.6

9.7

4.96.1

14.7

5.8

11.9

5.9

13.2

4.8

12.4

5.1

14.9

4.9

13.7

Quarterly Market Summary December 31, 2014

Copyright © 2014 Investment Metrics, LLC. All rights reserved.

10INTEGRITY. BALANCE. OBJECTIVITY.

Intl Equity Region PerformanceIntl Equity Indices Performance

Fixed Income Market Sector Performance

Source: Investment Metrics, LLC

Source: Investment Metrics, LLCSource: Investment Metrics, LLC

Barclays U.S. Aggregate Barclays U.S. Treasury Barclays U.S. Agency Barclays U.S. Credit Index Barclays U.S. MBS

Barclays U.S. ABS Barclays U.S. Corp: High Yield Barclays Global Aggregate JPM EMBI Global (USD)

0.0

4.0

8.0

12.0

-4.0

Re

turn

(%)

1

Quarter

1

Year

-1.6

5.5

-1.0

0.6

-1.0

2.5

0.5

1.91.8

6.1

1.8

7.5

1.2

3.6

1.9

5.1

1.8

6.0

MSCI Japan MSCI Pacific ex Japan MSCI United Kingdom MSCI Europe ex U.K.

-8.0

-6.0

-4.0

-2.0

0.0

Re

turn

(%)

1

Quarter

1

Year

-4.3

-5.8

-4.2

-5.4

-1.5

-0.3

-2.4

-3.7

MSCI EAFE Index MSCI EAFE Small Cap MSCI EAFE Growth Index

MSCI EAFE Value MSCI Emerging Markets

-8.0

-6.0

-4.0

-2.0

0.0

Re

turn

(%)

1

Quarter

1

Year

-4.4

-1.8

-4.8 -4.9

-2.3

-4.1

-2.2

-4.6

-3.5

-4.5

Quarterly Market Summary December 31, 2014

Copyright © 2014 Investment Metrics, LLC. All rights reserved.

11INTEGRITY. BALANCE. OBJECTIVITY.

Alternative Asset Class Returns December 31, 2014

Source: Christenson Investment Parnters Source: Christenson Investment Parnters

Source: Christenson Investment Parnters Source: Standard & Poors

19.7 19.0

10.4

‐2.2 ‐2.3

‐8.8

‐0.8

‐13.9

‐5.4 ‐5.9 ‐6.4 ‐7.6

0.4

‐11.7‐15.8

‐12.1

‐30.2 ‐32.5‐38.6 ‐40.5

‐50.0

‐40.0

‐30.0

‐20.0

‐10.0

0.0

10.0

20.0

30.0

Corn

Whe

at

Soybeans

Soybean Oil

Gold

Silver

Cattle

Hogs

Zinc

Copp

er

Alum

inum

Nickel

Cotton

Sugar

Coffe

e

Bloo

mbe

rg Com

m Inde

x

Heatin

g Oil

Natural Gas

Gasoline

Crud

e Oil

Commodity Sector Returns

16.7

‐3.9 ‐5.3 ‐6.2

‐12.0 ‐12.1

‐36.6‐40.0

‐30.0

‐20.0

‐10.0

0.0

10.0

20.0

Grains PreciousMetals

Livestock IndustrialMetals

Softs BloombergComm Index

Energy

Commodity Broad Sector Returns

11.3

2.31.1 0.9 0.5 0.3 0.0

‐2.2 ‐2.3 ‐2.5 ‐3.0‐6.0‐4.0‐2.00.02.04.06.08.010.012.014.0

Managed

Futures

Long/Sho

rt Equ

ity

Multi‐Strategy

HFRI FoF

Com

posite

Globa

l Macro

Equity M

arket N

eutral

Fixed Income Arbitrage

Even

t Driv

en

Distressed

Dedicated Short B

ias

Convertib

le Arbitrage

Hedge Fund Strategy Returns

14.0

10.3 10.3

5.44.0

2.51.3

‐0.9 ‐1.1 ‐2.1‐4.0‐2.00.02.04.06.08.010.012.014.016.0

U.S.

Hon

g Ko

ng

S&P De

velope

d RE

IT

United Kingdo

m

Australia

Europe

Emerging

Markets

Singap

ore

Japa

n

Canada

Global REIT Country and Regional Returns

12INTEGRITY. BALANCE. OBJECTIVITY.

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

HighCommodities

21.36 %REITs 35.97 %

Commodities16.23 %

Fixed Income5.24 %

Int'l Stocks31.78 %

REITs 28.60 %

REITs 9.24 %

REITs 17.59 %

Small Cap Stocks38.82 %

REITs 31.78 %

REITs 8.26%

REITs 26.31%

REITs 13.82 %

Int'l Stocks26.34 %

Int'l Stocks11.17 %

Hedge Funds‐21.37 %

REITs 28.60 %

Small Cap Stocks26.85 %

Fixed Income7.84 %

Int'l Stocks17.32 %

Large Cap Stocks32.38 %

Large Cap Stocks13.69 %

Small Cap Stocks7.77%

Small Cap Stocks19.67%

Int'l Stocks13.54 %

Small Cap Stocks18.37 %

Hedge Funds10.25 %

Diversifed Portfolio‐24.23%

Small Cap Stocks27.17 %

Commodi es16.83 %

Large Cap Stocks2.11 %

Small Cap Stocks16.35 %

Int'l Stocks22.78%

Fixed Income5.97 %

Large Cap Stocks7.67%

Int'l Stocks18.08%

Hedge Funds7.49 %

Large Cap Stocks15.79 %

Fixed Income6.97 %

Small Cap Stocks‐33.79 %

Large Cap Stocks26.46 %

Large Cap Stocks15.06 %

Diversified Portfolio‐0.50%

Large Cap Stocks16.00 %

Diversified Portfolio14.79%

Small Cap Stocks4.89 %

Diversified Portfolio5.70%

Commodities18.07%

Diversified Portfolio7.01 %

Diversified Portfolio13.25 %

Diversified Portfolio6.64 %

Commodities‐35.65 %

Diversified Portfolio19.48%

Diversified Portfolio12.25%

Small Cap Stocks‐4.18 %

Diversified Portfolio10.27%

Hedge Funds8.81 %

Diversified Portfolio5.44%

Fixed Income4.71%

Large Cap Stocks14.61%

Large Cap Stocks4.91 %

Hedge Funds10.39 %

Large Cap Stocks5.49 %

Large Cap Stocks‐37.00 %

Commodi es18.91 %

Int'l Stocks7.75 %

Hedge Funds‐5.72 %

Hedge Funds5.28 %

REITs 1.86 %

Hedge Funds3.19%

Int'l Stocks4.43%

Diversified Portfolio9.48%

Small Cap Stocks4.55 %

Fixed Income4.34 %

Small Cap Stocks‐1.57 %

REITs ‐39.20 %

Hedge Funds11.47 %

Fixed Income6.54 %

Int'l Stocks‐12.14 %

Fixed Income4.21 %

Fixed Income‐2.02 %

Int'l Stocks‐4.90%

Hedge Funds 3.02%

Hedge Funds5.49%

LowFixed Income

2.43 %Commodi es

2.07 %REITs

‐17.55 %Int'l Stocks‐43.38 %

Fixed Income5.93 %

Hedge Funds5.70 %

Commodities‐13.32 %

Commodities‐1.06 %

Commodi es‐9.53 %

Commodi es‐17.01 %

Commodities ‐1.86%

Fixed Income3.21%

Indices Used: Large Cap Stocks (S&P 500), Small Cap Stock (Russell 2000) Int'l Stocks (MSCI EAFE), Fixed Income (Barclays Aggregate), REITs (DJ‐Wilshire REIT)Hedge Funds (HFRI Fund of Funds Composite), Commodities (DJ‐UBS Commodity)Diversified Portfolio: 25% S&P 500, 10% Russell 2000, 12% MSCI EAFE, 25% BC Aggregate Bond, 5% DJ‐UBS Commodity, 5% DJ‐Wilshire REIT, 20% HFRI Fund of Funds Composite

Periodic Table of Returns 2005 ‐ 2014

Avg Annual Returns '05‐'14

Avg Annual Risk

'05‐'14

13INTEGRITY. BALANCE. OBJECTIVITY.

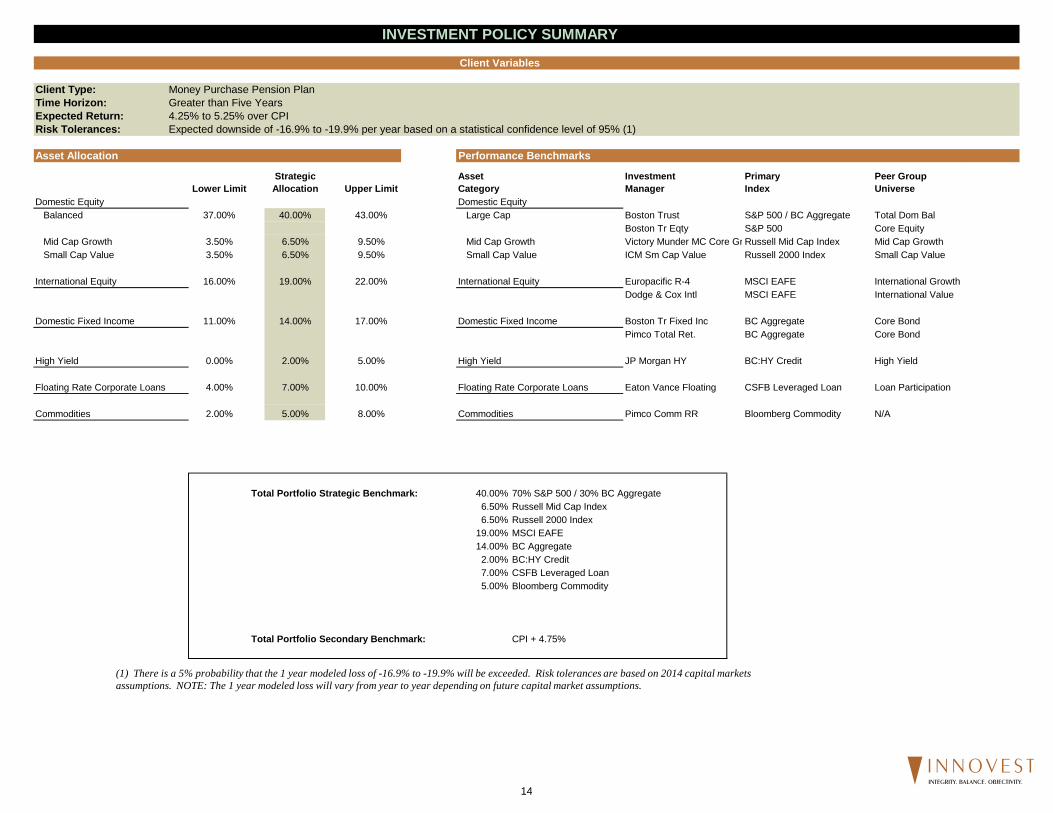

Client Type: Money Purchase Pension PlanTime Horizon: Greater than Five YearsExpected Return: 4.25% to 5.25% over CPIRisk Tolerances: Expected downside of -16.9% to -19.9% per year based on a statistical confidence level of 95% (1)

Asset Allocation Performance Benchmarks

Strategic Asset Investment Primary Peer GroupLower Limit Allocation Upper Limit Category Manager Index Universe

Domestic Equity Domestic Equity Balanced 37.00% 40.00% 43.00% Large Cap Boston Trust S&P 500 / BC Aggregate Total Dom Bal

Boston Tr Eqty S&P 500 Core Equity Mid Cap Growth 3.50% 6.50% 9.50% Mid Cap Growth Victory Munder MC Core Gr Russell Mid Cap Index Mid Cap Growth Small Cap Value 3.50% 6.50% 9.50% Small Cap Value ICM Sm Cap Value Russell 2000 Index Small Cap Value

International Equity 16.00% 19.00% 22.00% International Equity Europacific R-4 MSCI EAFE International GrowthDodge & Cox Intl MSCI EAFE International Value

Domestic Fixed Income 11.00% 14.00% 17.00% Domestic Fixed Income Boston Tr Fixed Inc BC Aggregate Core BondPimco Total Ret. BC Aggregate Core Bond

High Yield 0.00% 2.00% 5.00% High Yield JP Morgan HY BC:HY Credit High Yield

Floating Rate Corporate Loans 4.00% 7.00% 10.00% Floating Rate Corporate Loans Eaton Vance Floating CSFB Leveraged Loan Loan Participation

INVESTMENT POLICY SUMMARY

Client Variables

Commodities 2.00% 5.00% 8.00% Commodities Pimco Comm RR Bloomberg Commodity N/A

Total Portfolio Strategic Benchmark: 40.00% 70% S&P 500 / 30% BC Aggregate6.50% Russell Mid Cap Index 6.50% Russell 2000 Index

19.00% MSCI EAFE14.00% BC Aggregate2.00% BC:HY Credit 7.00% CSFB Leveraged Loan5.00% Bloomberg Commodity

Total Portfolio Secondary Benchmark: CPI + 4.75%

(1) There is a 5% probability that the 1 year modeled loss of -16.9% to -19.9% will be exceeded. Risk tolerances are based on 2014 capital markets assumptions. NOTE: The 1 year modeled loss will vary from year to year depending on future capital market assumptions.

14INTEGRITY. BALANCE. OBJECTIVITY.

Boulder Fire & PoliceAverage plan assets $112,249,407Estimated Investment, Recordkeeping and Administrative Costs 0.59%Estimated Total Plan Expenses 0.70%

Weighted average (bps)

Employer Paid Employee Paid TotalAsset based fee retained by funds 51 -$ 570,802$ 570,802$ Revenue sharing paid to plan provider 13 -$ 150,707$ 150,707$ Per participant fee 0 -$ -$ -$ Administration/Recordkeeping fee 0 -$ -$ -$ Custodial/Trust fees 0 -$ -$ -$ Direct participant paid fees

Loan origination 0 -$ -$ -$ Loan maintenance 0 -$ -$ -$ QDRO 0 -$ -$ -$ Miscellaneous 0 -$ -$ -$

Rebate to plan -5 -$ (55,295)$ (55,295)$

Total Investment, Recordkeeping and Administrative Costs 59 -$ 666,214$ 666,214$

Third party plan paid feesInvestment Consultant 7 37,360$ 37,360$ 74,719$

Operating BudgetAudit 1 9,000$ -$ 9,000$ Trustee Education 1 10,500$ -$ 10,500$ Insurance 1 9,000$ -$ 9,000$ Miscellaneous Expenses 0 1,500$ -$ 1,500$ Legal 2 20,000$ -$ 20,000$

Total Plan Expenses 70 87,360$ 703,574$ 790,934$

Total Plan Expenses in Basis Points 8 63

Fee review reflects an estimate for the following time period: 1/1/2014 - 12/31/2014

Benchmarking: The plan's estimated investment, recordkeeping and administrative costs of 0.59% as shown above, compare favorably to 401(k) Source data, a universe of 84 similarly sized 401(k) plans with an average investment, recordkeeping and administrative cost of 1.19%

Dollars ($)

Total Plan Expenses

Annual Fee Review

15INTEGRITY. BALANCE. OBJECTIVITY.

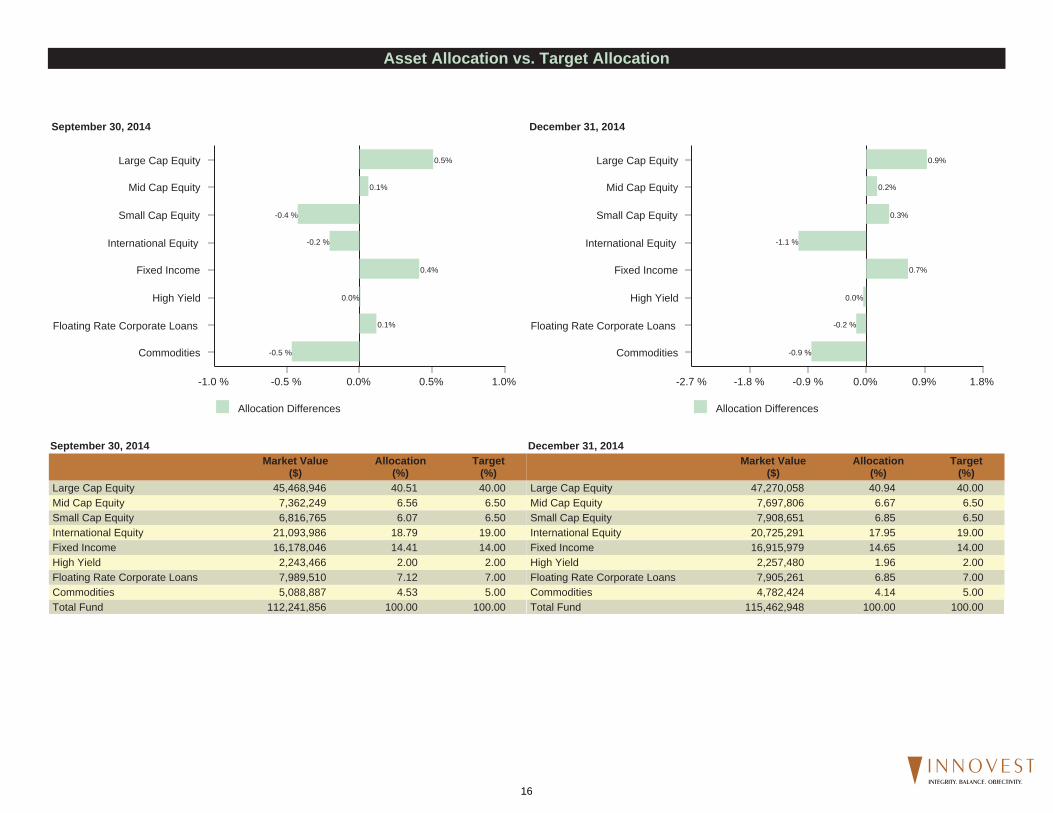

December 31, 2014

Allocation Differences

0.0% 0.9% 1.8%-0.9 %-1.8 %-2.7 %

Commodities

Floating Rate Corporate Loans

High Yield

Fixed Income

International Equity

Small Cap Equity

Mid Cap Equity

Large Cap Equity

-0.9 %

-0.2 %

0.0%

0.7%

-1.1 %

0.3%

0.2%

0.9%

September 30, 2014

Allocation Differences

0.0% 0.5% 1.0%-0.5 %-1.0 %

Commodities

Floating Rate Corporate Loans

High Yield

Fixed Income

International Equity

Small Cap Equity

Mid Cap Equity

Large Cap Equity

-0.5 %

0.1%

0.0%

0.4%

-0.2 %

-0.4 %

0.1%

0.5%

December 31, 2014Market Value

($)Allocation

(%)Target

(%)Large Cap Equity 47,270,058 40.94 40.00Mid Cap Equity 7,697,806 6.67 6.50Small Cap Equity 7,908,651 6.85 6.50International Equity 20,725,291 17.95 19.00Fixed Income 16,915,979 14.65 14.00High Yield 2,257,480 1.96 2.00Floating Rate Corporate Loans 7,905,261 6.85 7.00Commodities 4,782,424 4.14 5.00Total Fund 115,462,948 100.00 100.00

September 30, 2014Market Value

($)Allocation

(%)Target

(%)Large Cap Equity 45,468,946 40.51 40.00Mid Cap Equity 7,362,249 6.56 6.50Small Cap Equity 6,816,765 6.07 6.50International Equity 21,093,986 18.79 19.00Fixed Income 16,178,046 14.41 14.00High Yield 2,243,466 2.00 2.00Floating Rate Corporate Loans 7,989,510 7.12 7.00Commodities 5,088,887 4.53 5.00Total Fund 112,241,856 100.00 100.00

Asset Allocation vs. Target Allocation

16INTEGRITY. BALANCE. OBJECTIVITY.

Allocation

MarketValue

($)%

Performance(%)

LastQuarter

YearTo Date

1Year

3Years

5Years

10Years

SinceInnovestInception

SinceInception

InceptionDate

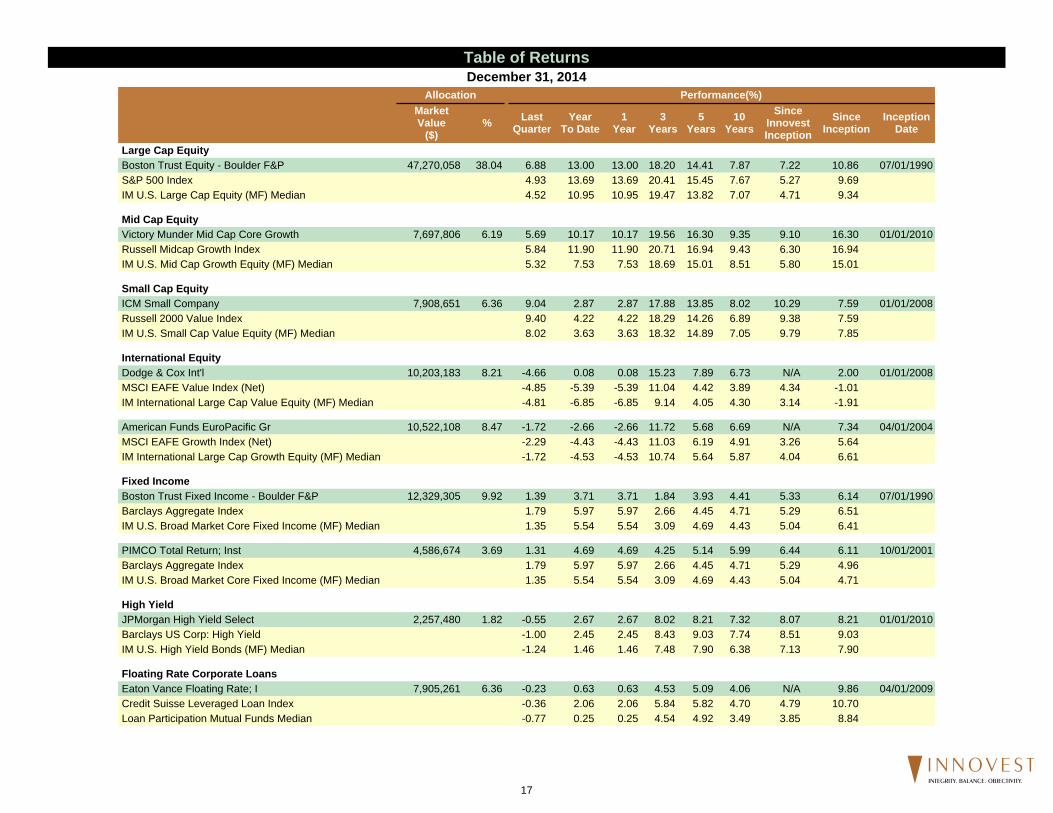

Large Cap Equity

Boston Trust Equity - Boulder F&P 47,270,058 38.04 6.88 13.00 13.00 18.20 14.41 7.87 7.22 10.86 07/01/1990S&P 500 Index 4.93 13.69 13.69 20.41 15.45 7.67 5.27 9.69IM U.S. Large Cap Equity (MF) Median 4.52 10.95 10.95 19.47 13.82 7.07 4.71 9.34

Mid Cap Equity

Victory Munder Mid Cap Core Growth 7,697,806 6.19 5.69 10.17 10.17 19.56 16.30 9.35 9.10 16.30 01/01/2010Russell Midcap Growth Index 5.84 11.90 11.90 20.71 16.94 9.43 6.30 16.94IM U.S. Mid Cap Growth Equity (MF) Median 5.32 7.53 7.53 18.69 15.01 8.51 5.80 15.01

Small Cap Equity

ICM Small Company 7,908,651 6.36 9.04 2.87 2.87 17.88 13.85 8.02 10.29 7.59 01/01/2008Russell 2000 Value Index 9.40 4.22 4.22 18.29 14.26 6.89 9.38 7.59IM U.S. Small Cap Value Equity (MF) Median 8.02 3.63 3.63 18.32 14.89 7.05 9.79 7.85

International Equity

Dodge & Cox Int'l 10,203,183 8.21 -4.66 0.08 0.08 15.23 7.89 6.73 N/A 2.00 01/01/2008MSCI EAFE Value Index (Net) -4.85 -5.39 -5.39 11.04 4.42 3.89 4.34 -1.01IM International Large Cap Value Equity (MF) Median -4.81 -6.85 -6.85 9.14 4.05 4.30 3.14 -1.91

American Funds EuroPacific Gr 10,522,108 8.47 -1.72 -2.66 -2.66 11.72 5.68 6.69 N/A 7.34 04/01/2004MSCI EAFE Growth Index (Net) -2.29 -4.43 -4.43 11.03 6.19 4.91 3.26 5.64IM International Large Cap Growth Equity (MF) Median -1.72 -4.53 -4.53 10.74 5.64 5.87 4.04 6.61

Fixed Income

Boston Trust Fixed Income - Boulder F&P 12,329,305 9.92 1.39 3.71 3.71 1.84 3.93 4.41 5.33 6.14 07/01/1990Barclays Aggregate Index 1.79 5.97 5.97 2.66 4.45 4.71 5.29 6.51IM U.S. Broad Market Core Fixed Income (MF) Median 1.35 5.54 5.54 3.09 4.69 4.43 5.04 6.41

PIMCO Total Return; Inst 4,586,674 3.69 1.31 4.69 4.69 4.25 5.14 5.99 6.44 6.11 10/01/2001Barclays Aggregate Index 1.79 5.97 5.97 2.66 4.45 4.71 5.29 4.96IM U.S. Broad Market Core Fixed Income (MF) Median 1.35 5.54 5.54 3.09 4.69 4.43 5.04 4.71

High Yield

JPMorgan High Yield Select 2,257,480 1.82 -0.55 2.67 2.67 8.02 8.21 7.32 8.07 8.21 01/01/2010Barclays US Corp: High Yield -1.00 2.45 2.45 8.43 9.03 7.74 8.51 9.03IM U.S. High Yield Bonds (MF) Median -1.24 1.46 1.46 7.48 7.90 6.38 7.13 7.90

Floating Rate Corporate Loans

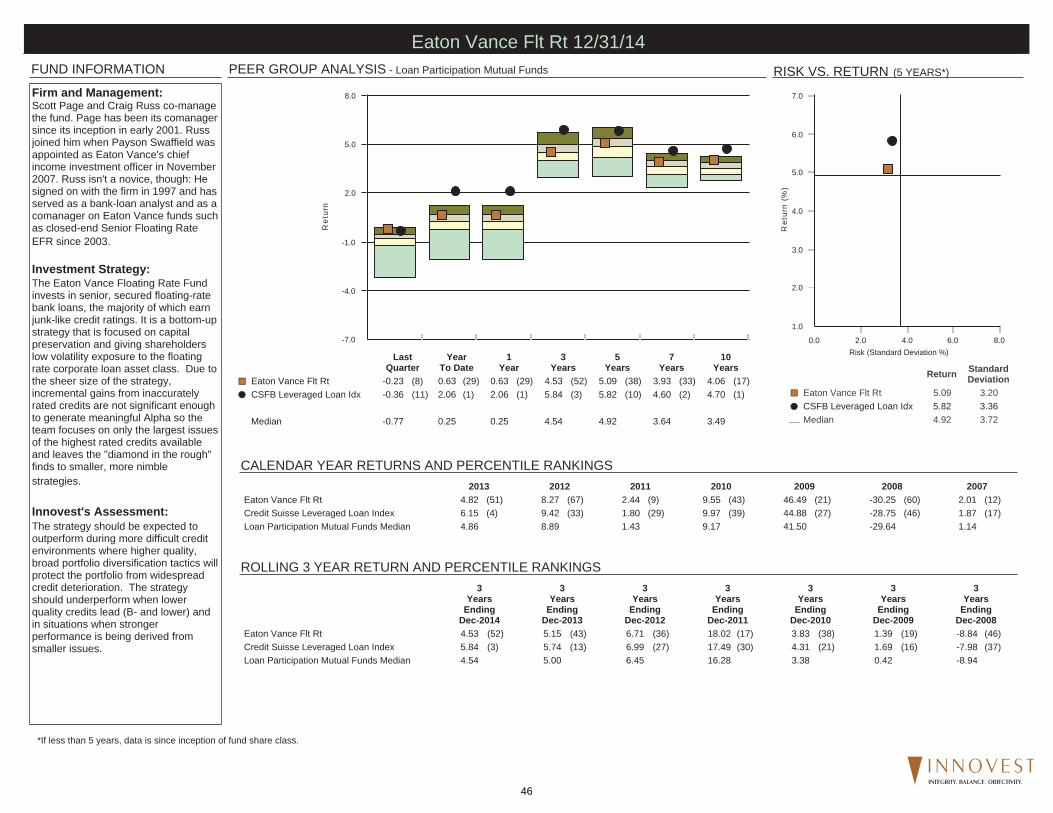

Eaton Vance Floating Rate; I 7,905,261 6.36 -0.23 0.63 0.63 4.53 5.09 4.06 N/A 9.86 04/01/2009Credit Suisse Leveraged Loan Index -0.36 2.06 2.06 5.84 5.82 4.70 4.79 10.70Loan Participation Mutual Funds Median -0.77 0.25 0.25 4.54 4.92 3.49 3.85 8.84

Table of ReturnsDecember 31, 2014

17INTEGRITY. BALANCE. OBJECTIVITY.

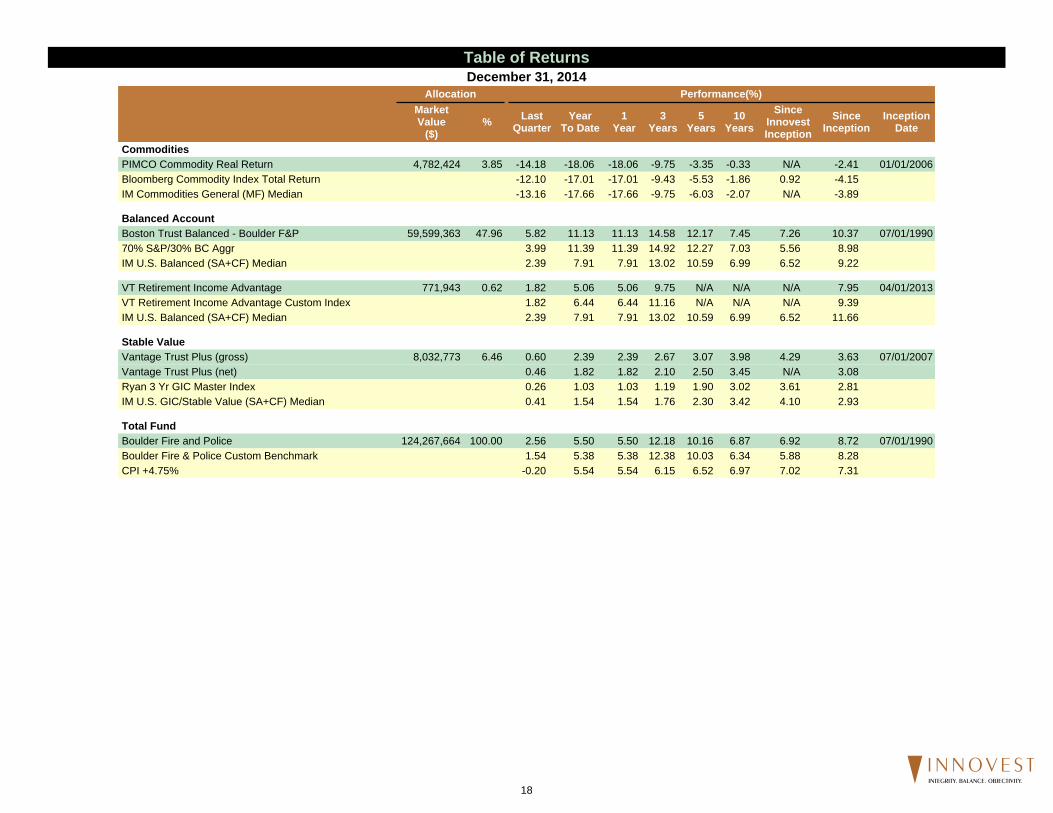

Table of ReturnsDecember 31, 2014

Allocation

MarketValue

($)%

Performance(%)

LastQuarter

YearTo Date

1Year

3Years

5Years

10Years

SinceInnovestInception

SinceInception

InceptionDate

Commodities

PIMCO Commodity Real Return 4,782,424 3.85 -14.18 -18.06 -18.06 -9.75 -3.35 -0.33 N/A -2.41 01/01/2006Bloomberg Commodity Index Total Return -12.10 -17.01 -17.01 -9.43 -5.53 -1.86 0.92 -4.15IM Commodities General (MF) Median -13.16 -17.66 -17.66 -9.75 -6.03 -2.07 N/A -3.89

Balanced Account

Boston Trust Balanced - Boulder F&P 59,599,363 47.96 5.82 11.13 11.13 14.58 12.17 7.45 7.26 10.37 07/01/199070% S&P/30% BC Aggr 3.99 11.39 11.39 14.92 12.27 7.03 5.56 8.98IM U.S. Balanced (SA+CF) Median 2.39 7.91 7.91 13.02 10.59 6.99 6.52 9.22

VT Retirement Income Advantage 771,943 0.62 1.82 5.06 5.06 9.75 N/A N/A N/A 7.95 04/01/2013VT Retirement Income Advantage Custom Index 1.82 6.44 6.44 11.16 N/A N/A N/A 9.39IM U.S. Balanced (SA+CF) Median 2.39 7.91 7.91 13.02 10.59 6.99 6.52 11.66

Stable Value

Vantage Trust Plus (gross) 8,032,773 6.46 0.60 2.39 2.39 2.67 3.07 3.98 4.29 3.63 07/01/2007Vantage Trust Plus (net) 0.46 1.82 1.82 2.10 2.50 3.45 N/A 3.08Ryan 3 Yr GIC Master Index 0.26 1.03 1.03 1.19 1.90 3.02 3.61 2.81IM U.S. GIC/Stable Value (SA+CF) Median 0.41 1.54 1.54 1.76 2.30 3.42 4.10 2.93

Total Fund

Boulder Fire and Police 124,267,664 100.00 2.56 5.50 5.50 12.18 10.16 6.87 6.92 8.72 07/01/1990Boulder Fire & Police Custom Benchmark 1.54 5.38 5.38 12.38 10.03 6.34 5.88 8.28CPI +4.75% -0.20 5.54 5.54 6.15 6.52 6.97 7.02 7.31

18INTEGRITY. BALANCE. OBJECTIVITY.

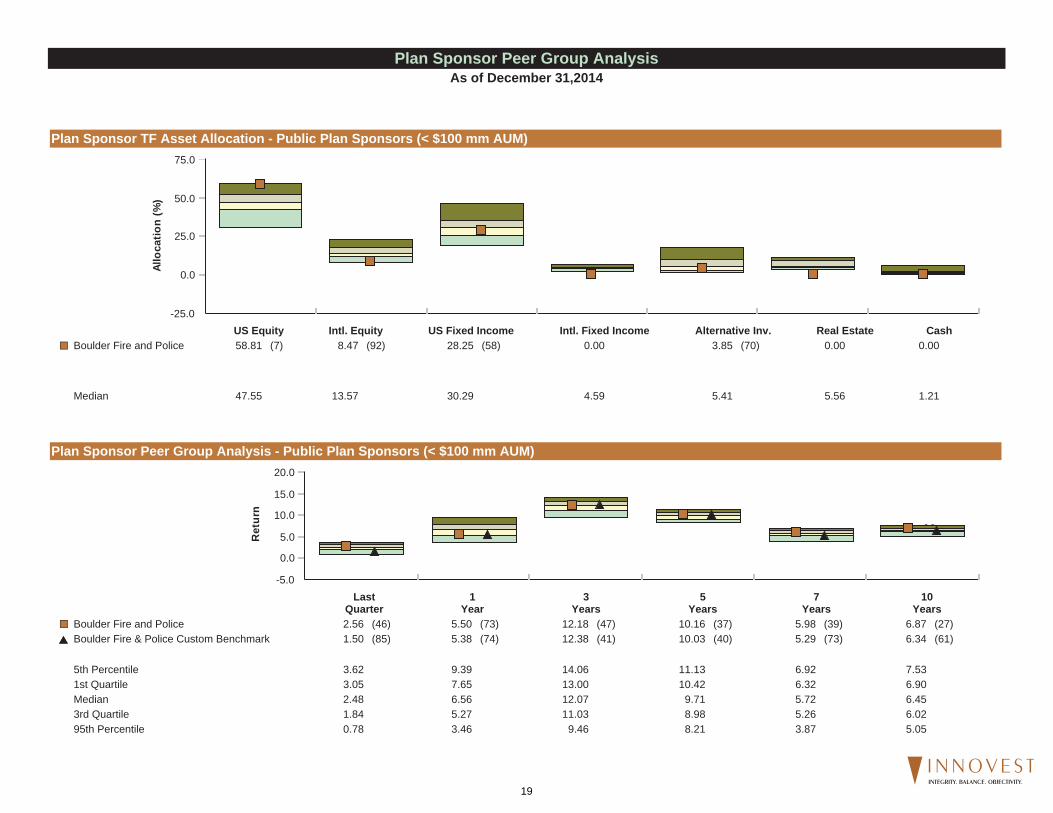

Plan Sponsor TF Asset Allocation - Public Plan Sponsors (< $100 mm AUM)

Plan Sponsor Peer Group Analysis - Public Plan Sponsors (< $100 mm AUM)

-25.0

0.0

25.0

50.0

75.0Al

loca

tion

(%)

US Equity Intl. Equity US Fixed Income Intl. Fixed Income Alternative Inv. Real Estate CashBoulder Fire and Police 58.81 (7) 8.47 (92) 28.25 (58) 0.00 3.85 (70) 0.00 0.00

5th Percentile 59.48 22.55 46.50 6.62 17.52 11.07 6.151st Quartile 52.19 17.30 35.91 4.94 10.15 9.05 2.20

Median 47.55 13.57 30.29 4.59 5.41 5.56 1.213rd Quartile 42.50 12.02 25.27 4.30 2.64 4.75 0.6795th Percentile 30.23 8.10 18.92 2.37 1.48 3.64 0.03

-5.0

0.0

5.0

10.0

15.0

20.0

Ret

urn

0.81.83.55.3

9.511.0

8.29.0

3.95.3 5.16.0

LastQuarter

1Year

3Years

5Years

7Years

10Years

Boulder Fire and Police 2.56 (46) 5.50 (73) 12.18 (47) 10.16 (37) 5.98 (39) 6.87 (27)

Boulder Fire & Police Custom Benchmark 1.50 (85) 5.38 (74) 12.38 (41) 10.03 (40) 5.29 (73) 6.34 (61)

5th Percentile 3.62 9.39 14.06 11.13 6.92 7.531st Quartile 3.05 7.65 13.00 10.42 6.32 6.90Median 2.48 6.56 12.07 9.71 5.72 6.453rd Quartile 1.84 5.27 11.03 8.98 5.26 6.0295th Percentile 0.78 3.46 9.46 8.21 3.87 5.05

Plan Sponsor Peer Group AnalysisAs of December 31,2014

19INTEGRITY. BALANCE. OBJECTIVITY.

Plan Sponsor TF Asset Allocation - Public Plan Sponors ($100mm - $1 Bln AUM)

Plan Sponsor Peer Group Analysis - Public Plan Sponors ($100mm - $1 Bln AUM)

-25.0

0.0

25.0

50.0

75.0Al

loca

tion

(%)

US Equity Intl. Equity US Fixed Income Intl. Fixed Income Alternative Inv. Real Estate CashBoulder Fire and Police 58.81 (4) 8.47 (95) 28.25 (34) 0.00 3.85 (92) 0.00 0.00

5th Percentile 55.81 33.21 48.63 14.57 31.77 12.79 6.231st Quartile 47.71 22.62 31.59 7.31 16.78 10.43 1.62

Median 39.54 18.47 23.75 5.01 11.35 8.07 0.813rd Quartile 32.84 13.70 18.69 4.43 5.50 5.37 0.1895th Percentile 21.20 8.14 15.09 3.04 2.75 2.67 0.02

-4.0

2.0

8.0

14.0

20.0

Ret

urn

0.31.22.75.0

7.8

11.2

7.09.1

3.85.0 5.56.1

LastQuarter

1Year

3Years

5Years

7Years

10Years

Boulder Fire and Police 2.56 (27) 5.50 (64) 12.18 (51) 10.16 (46) 5.98 (25) 6.87 (25)

Boulder Fire & Police Custom Benchmark 1.50 (67) 5.38 (67) 12.38 (46) 10.03 (48) 5.29 (62) 6.34 (63)

5th Percentile 3.19 8.11 14.86 11.79 6.96 7.801st Quartile 2.67 7.03 13.15 10.73 5.98 6.86Median 1.91 6.20 12.24 9.94 5.51 6.573rd Quartile 1.16 4.98 11.20 9.07 5.01 6.0995th Percentile 0.34 2.72 7.82 7.01 3.82 5.52

Plan Sponsor Peer Group AnalysisAs of December 31,2014

20INTEGRITY. BALANCE. OBJECTIVITY.

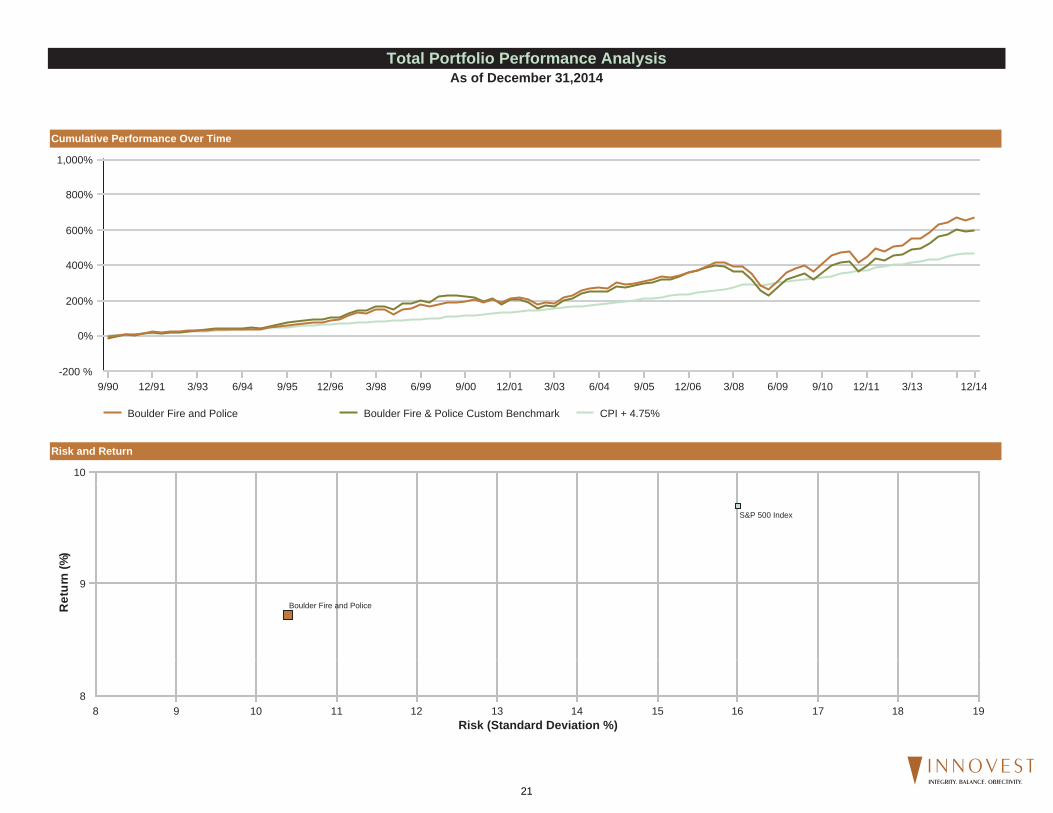

Cumulative Performance Over Time

Risk and Return

Boulder Fire and Police Boulder Fire & Police Custom Benchmark CPI + 4.75%

-200 %

0%

200%

400%

600%

800%

1,000%

9/90 12/91 3/93 6/94 9/95 12/96 3/98 6/99 9/00 12/01 3/03 6/04 9/05 12/06 3/08 6/09 9/10 12/11 3/13 12/14

8

9

10

Ret

urn

(%)

8 9 10 11 12 13 14 15 16 17 18 19Risk (Standard Deviation %)

Boulder Fire and Police

S&P 500 Index

Total Portfolio Performance AnalysisAs of December 31,2014

21INTEGRITY. BALANCE. OBJECTIVITY.

THIS PAGE LEFT INTENTIONALLY BLANK

22INTEGRITY. BALANCE. OBJECTIVITY.

Innovest’s investment performance analysis is not simply the production of a quarterly performance report.Our in-depth investment product analysis is extensive, continual and designed to reduce surprises.

ONGOING MONITORING

Occurrence Action

Daily We review trades and reconcile accounts. Manager due diligence meetings are held both on and off-site.

Weekly

The Investment Committee meets to review managers, client portfolios, and the financial markets. Special attention is reserved for managers with qualitative issues. Clients with objective changes and other issues are discussed by the committee.

MonthlyWe conduct quantitative analysis to identify outlier managers, both positive and negative, for comprehensive evaluation.

Quarterly

Each client’s account is reviewed for possible portfolio rebalancing. Manager calls are made and portfolio attribution is conducted to help determine “why” performance happened. Custom reports are developed for each client. Client meetings are conducted to review portfolio performance, managers, and policy.

Annually

We review the Due Diligence Questionnaire for every manager. Due diligence meetings are conducted and manager review documentation is created. Capital market assumptions are determined after thoughtful analysis. We conduct a formal Asset Allocation Study for every client and review their objectives, goals and investment policy.

23INTEGRITY. BALANCE. OBJECTIVITY.

Criteria

Organization People Philosophy& Process

StyleConsistency Asset Base Performance Expenses Overall

Costs

Exp Ratio(%)

MedianExp Ratio

(%)

Ratio ofExp to

Median (%)Boston Trust Balanced - Boulder F&P 0.64 1.15 55.00Victory:MC Core Gr;Y (MGOYX) 1.15 1.41 81.56ICM Small Company;Inst (ICSCX) 0.93 1.53 60.78Dodge & Cox Intl Stock (DODFX) 0.64 1.25 51.20American Funds EuPc;R-4 (REREX) 0.84 1.46 57.53PIMCO:Tot Rtn;Inst (PTTRX) 0.46 0.92 50.00Eaton Vance Flt Rt;Ins (EIBLX) 0.74 1.14 64.91JPMorgan:High Yield;Sel (OHYFX) 0.81 1.11 72.97PIMCO:Comm RR Str;Inst (PCRIX) 0.74 1.35 54.82Vantage Trust Plus 0.82 0.50 164.00VT Retirement Income Advantage 1.72 1.72 100.00

Legend For Overall CriteriaNo/Minimum ConcernsMinor ConcernMajor ConcernUnder Review

Manager Score Factor CommentsBoston Trust Balanced - Boulder F&P Performance With respect to the equity portion of the balanced fund, performance in 2012, 2013, and the first three quarters of 2014 has lagged

the benchmark and peers. This is because Boston Trust only invests in high quality companies. The high quality focus hascaused the fund to miss the high returns delivered by lower quality companies—those with lower growth, profitability, andstability—which drove higher median and benchmark returns. These results are consistent with Boston Trust’s quality-focusedstrategy, and we remain confident that this strategy will perform well in the long-term. Still, we will closely monitor performance forfuture deterioration.

Victory:MC Core Gr;Y (MGOYX) Organization Victory Capital Mangement Holdings Inc. acquired Munder Captial Managment (April, 2014). Victory manages $18 billion, as doesMunder. The combined company will form an independent investment management firm. It is expected that the investmentprocesses and decision-making that have been utilized by each money management team prior to the acquisition will remain inplace. It is also anticipated that there will be no changes to the Munder investment management teams. In addition, investmentmanagement teams are expected to remain in their current locations. Will monitor closely to ensure a smooth transition.

ICM Small Company;Inst (ICSCX) Performance The fund’s underperformance to the benchmark can be attributed to sector weighting as the fund has been underweight in RealEstate Investment Trusts which have been one of the best performing sectors in the Index. Stock selection of the fund managershas also been a detractor to performance specifically in the Technology and Materials sectors.

PIMCO:Tot Rtn;Inst (PTTRX) Organization The 2014 departures of the firm’s co-founder, Bill Gross, and his co-CIO, Mohamed El-Erian, will have significant implications forthe firm in the long run. In 2014 alone, PIMCO saw nearly $150 billion leave its assets under management. We are confident in thestructure of PIMCO, still one of the largest active fixed income managers in the world; however the rapid change in leadership andassets bears concern.

PIMCO:Tot Rtn;Inst (PTTRX) People PIMCO Co-Founder and Co-Chief Investment Officer Bill Gross has left the firm effective September 2014. As the Co-ChiefInvestment Officer, leader of the firm and lead manager of many of PIMCO’s bond funds, Gross had significant influence on thecompany’s long-term success. While Mr. Gross’s departure from PIMCO is a major event, it is important to keep in mind thatPIMCO has some of the best and brightest fixed income managers, co-CIO’s, and trading staff in the industry.

PIMCO:Tot Rtn;Inst (PTTRX) Overall .

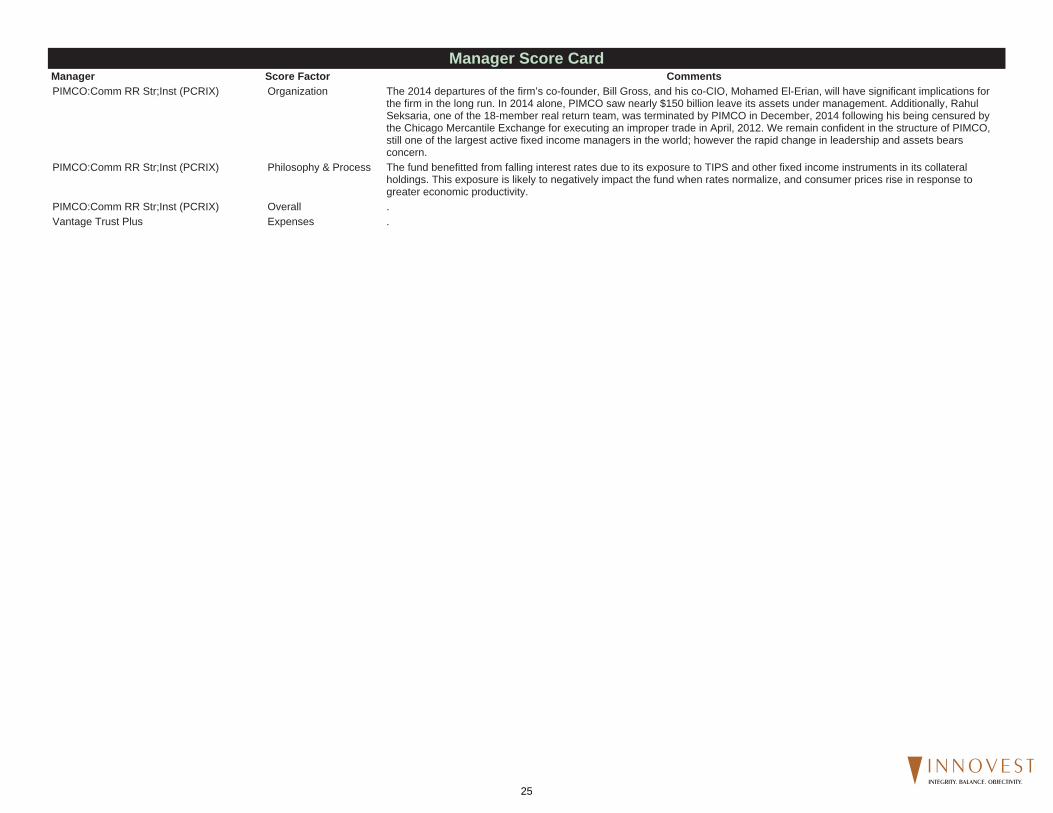

Manager Score Card

24INTEGRITY. BALANCE. OBJECTIVITY.

Manager Score CardManager Score Factor CommentsPIMCO:Comm RR Str;Inst (PCRIX) Organization The 2014 departures of the firm’s co-founder, Bill Gross, and his co-CIO, Mohamed El-Erian, will have significant implications for

the firm in the long run. In 2014 alone, PIMCO saw nearly $150 billion leave its assets under management. Additionally, RahulSeksaria, one of the 18-member real return team, was terminated by PIMCO in December, 2014 following his being censured bythe Chicago Mercantile Exchange for executing an improper trade in April, 2012. We remain confident in the structure of PIMCO,still one of the largest active fixed income managers in the world; however the rapid change in leadership and assets bearsconcern.

PIMCO:Comm RR Str;Inst (PCRIX) Philosophy & Process The fund benefitted from falling interest rates due to its exposure to TIPS and other fixed income instruments in its collateralholdings. This exposure is likely to negatively impact the fund when rates normalize, and consumer prices rise in response togreater economic productivity.

PIMCO:Comm RR Str;Inst (PCRIX) Overall .Vantage Trust Plus Expenses .

25INTEGRITY. BALANCE. OBJECTIVITY.

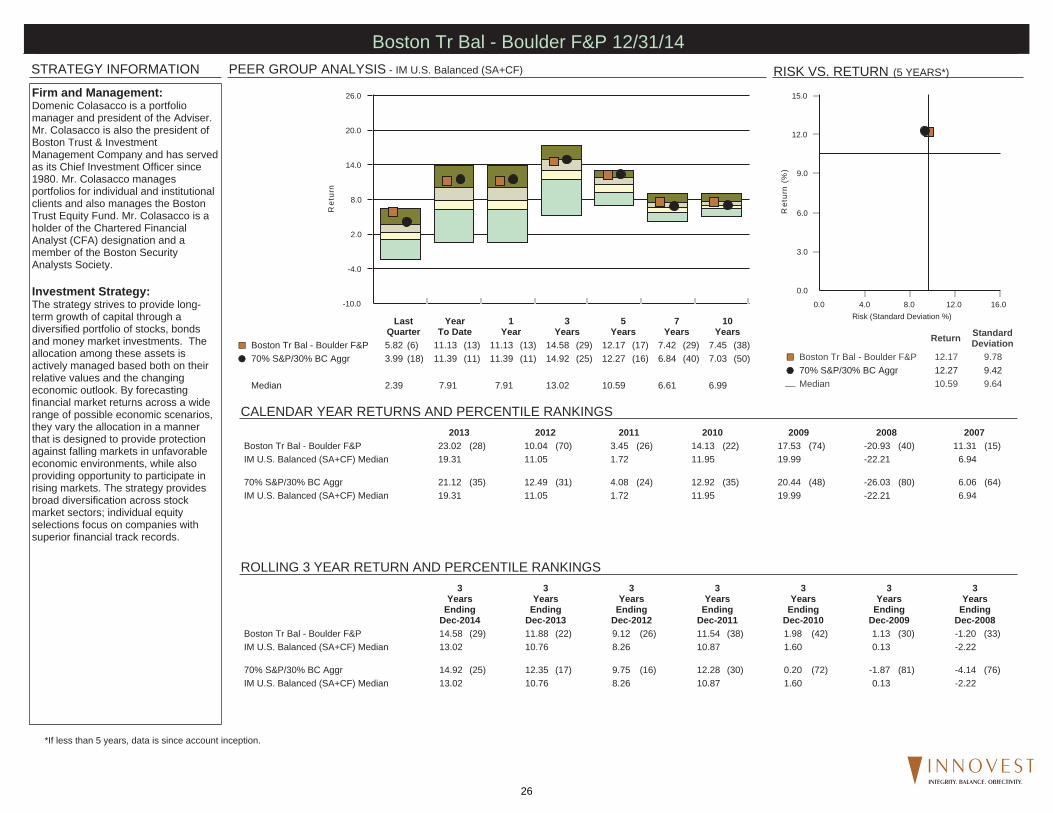

STRATEGY INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Balanced (SA+CF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since account inception.

Firm and Management:Domenic Colasacco is a portfoliomanager and president of the Adviser.Mr. Colasacco is also the president ofBoston Trust & InvestmentManagement Company and has servedas its Chief Investment Officer since1980. Mr. Colasacco managesportfolios for individual and institutionalclients and also manages the BostonTrust Equity Fund. Mr. Colasacco is aholder of the Chartered FinancialAnalyst (CFA) designation and amember of the Boston SecurityAnalysts Society.

Investment Strategy:The strategy strives to provide long-term growth of capital through adiversified portfolio of stocks, bondsand money market investments. Theallocation among these assets isactively managed based both on theirrelative values and the changingeconomic outlook. By forecastingfinancial market returns across a widerange of possible economic scenarios,they vary the allocation in a mannerthat is designed to provide protectionagainst falling markets in unfavorableeconomic environments, while alsoproviding opportunity to participate inrising markets. The strategy providesbroad diversification across stockmarket sectors; individual equityselections focus on companies withsuperior financial track records.

0.0

3.0

6.0

9.0

12.0

15.0

Ret

urn

(%)

0.0 4.0 8.0 12.0 16.0Risk (Standard Deviation %)

Return StandardDeviation

Boston Tr Bal - Boulder F&P 12.17 9.78

70% S&P/30% BC Aggr 12.27 9.42

Median 10.59 9.64

-10.0

-4.0

2.0

8.0

14.0

20.0

26.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Boston Tr Bal - Boulder F&P 5.82 (6) 11.13 (13) 11.13 (13) 14.58 (29) 12.17 (17) 7.42 (29) 7.45 (38)

70% S&P/30% BC Aggr 3.99 (18) 11.39 (11) 11.39 (11) 14.92 (25) 12.27 (16) 6.84 (40) 7.03 (50)

Median 2.39 7.91 7.91 13.02 10.59 6.61 6.99

2013 2012 2011 2010 2009 2008 2007Boston Tr Bal - Boulder F&P 23.02 (28) 10.04 (70) 3.45 (26) 14.13 (22) 17.53 (74) -20.93 (40) 11.31 (15)IM U.S. Balanced (SA+CF) Median 19.31 11.05 1.72 11.95 19.99 -22.21 6.94

70% S&P/30% BC Aggr 21.12 (35) 12.49 (31) 4.08 (24) 12.92 (35) 20.44 (48) -26.03 (80) 6.06 (64)IM U.S. Balanced (SA+CF) Median 19.31 11.05 1.72 11.95 19.99 -22.21 6.94

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

3Years

EndingDec-2008

Boston Tr Bal - Boulder F&P 14.58 (29) 11.88 (22) 9.12 (26) 11.54 (38) 1.98 (42) 1.13 (30) -1.20 (33)IM U.S. Balanced (SA+CF) Median 13.02 10.76 8.26 10.87 1.60 0.13 -2.22

70% S&P/30% BC Aggr 14.92 (25) 12.35 (17) 9.75 (16) 12.28 (30) 0.20 (72) -1.87 (81) -4.14 (76)IM U.S. Balanced (SA+CF) Median 13.02 10.76 8.26 10.87 1.60 0.13 -2.22

Boston Tr Bal - Boulder F&P 12/31/14

26INTEGRITY. BALANCE. OBJECTIVITY.

STRATEGY INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Large Cap Core Equity (SA+CF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since account inception.

Firm and Management:Domenic Colasacco is a portfoliomanager and president of the Adviser.Mr. Colasacco is also the president ofBoston Trust & InvestmentManagement Company and has servedas its Chief Investment Officer since1980. Mr. Colasacco managesportfolios for individual and institutionalclients and also manages the BostonTrust Equity Fund. Mr. Colasacco is aholder of the Chartered FinancialAnalyst (CFA) designation and amember of the Boston SecurityAnalysts Society.

Investment Strategy:The portfolio consists of stocks from allmarket capitalizations; small, mediumand large. The portfolio is constructedwith a bottom up approach to securityselection, however, macro themes areconsidered in deciding which sectorslook most attractive. Each potentialholding is put through a number ofscreens which consider earningsgrowth and relative valuation.

6.0

9.0

12.0

15.0

18.0

21.0

Ret

urn

(%)

0.0 5.0 10.0 15.0 20.0 25.0Risk (Standard Deviation %)

Return StandardDeviation

Boston TrEq - Boulder F&P 14.41 13.50

S&P 500 Index 15.45 14.04

Median 15.47 14.68

-4.0

4.0

12.0

20.0

28.0

36.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Boston TrEq - Boulder F&P 6.88 (14) 13.00 (54) 13.00 (54) 18.20 (81) 14.41 (72) 7.75 (51) 7.87 (75)

S&P 500 Index 4.93 (54) 13.69 (40) 13.69 (40) 20.41 (54) 15.45 (52) 7.27 (70) 7.67 (81)

Median 5.09 13.24 13.24 20.56 15.47 7.78 8.42

2013 2012 2011 2010 2009 2008 2007Boston TrEq - Boulder F&P 30.44 (80) 12.03 (86) 1.56 (56) 16.91 (26) 24.19 (65) -30.73 (17) 11.81 (18)IM U.S. Large Cap Core Equity (SA+CF) Median 33.42 15.68 1.93 14.85 26.59 -36.11 7.19

S&P 500 Index 32.39 (64) 16.00 (46) 2.11 (49) 15.06 (45) 26.46 (51) -37.00 (62) 5.49 (71)IM U.S. Large Cap Core Equity (SA+CF) Median 33.42 15.68 1.93 14.85 26.59 -36.11 7.19

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

3Years

EndingDec-2008

Boston TrEq - Boulder F&P 18.20 (81) 14.06 (82) 9.97 (65) 13.82 (57) 0.19 (18) -1.29 (16) -4.92 (22)IM U.S. Large Cap Core Equity (SA+CF) Median 20.56 16.38 10.67 14.09 -1.97 -4.36 -7.42

S&P 500 Index 20.41 (54) 16.18 (57) 10.87 (48) 14.11 (49) -2.85 (68) -5.63 (73) -8.36 (69)IM U.S. Large Cap Core Equity (SA+CF) Median 20.56 16.38 10.67 14.09 -1.97 -4.36 -7.42

Boston TrEq - Boulder F&P 12/31/14

27INTEGRITY. BALANCE. OBJECTIVITY.

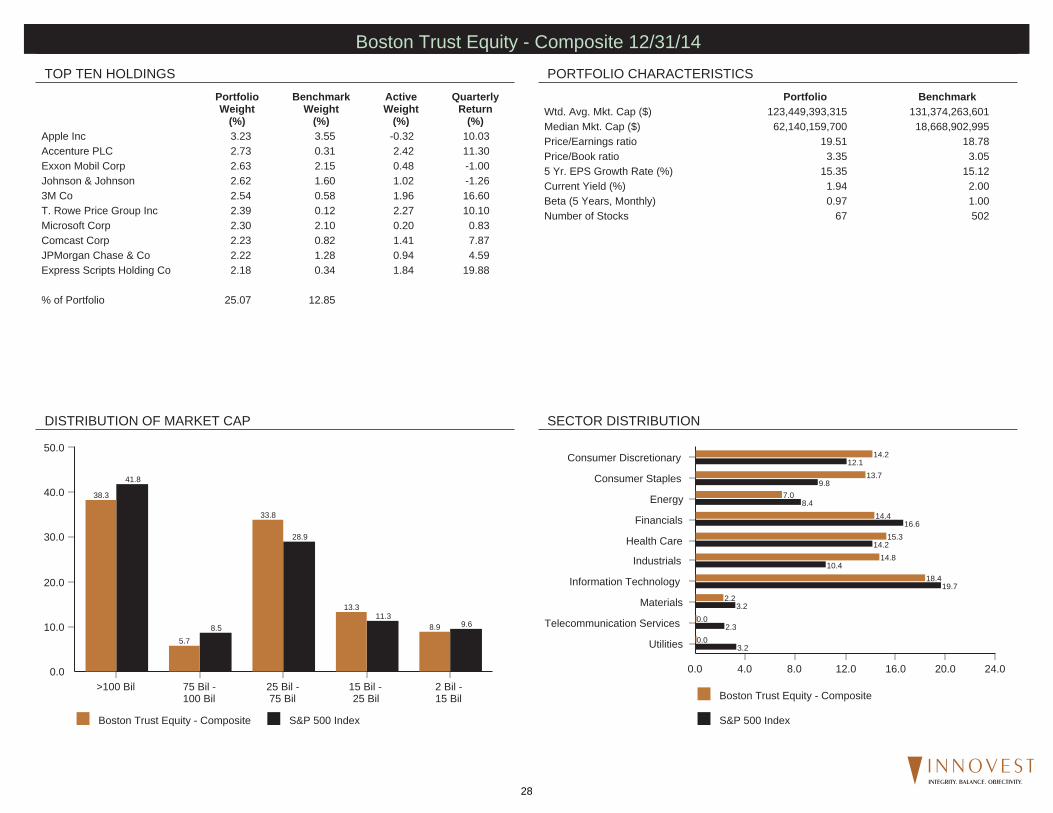

TOP TEN HOLDINGS PORTFOLIO CHARACTERISTICS

DISTRIBUTION OF MARKET CAP SECTOR DISTRIBUTION

Portfolio BenchmarkWtd. Avg. Mkt. Cap ($) 123,449,393,315 131,374,263,601Median Mkt. Cap ($) 62,140,159,700 18,668,902,995Price/Earnings ratio 19.51 18.78Price/Book ratio 3.35 3.055 Yr. EPS Growth Rate (%) 15.35 15.12Current Yield (%) 1.94 2.00Beta (5 Years, Monthly) 0.97 1.00Number of Stocks 67 502

PortfolioWeight

(%)

BenchmarkWeight

(%)

ActiveWeight

(%)

QuarterlyReturn

(%)Apple Inc 3.23 3.55 -0.32 10.03Accenture PLC 2.73 0.31 2.42 11.30Exxon Mobil Corp 2.63 2.15 0.48 -1.00Johnson & Johnson 2.62 1.60 1.02 -1.263M Co 2.54 0.58 1.96 16.60T. Rowe Price Group Inc 2.39 0.12 2.27 10.10Microsoft Corp 2.30 2.10 0.20 0.83Comcast Corp 2.23 0.82 1.41 7.87JPMorgan Chase & Co 2.22 1.28 0.94 4.59Express Scripts Holding Co 2.18 0.34 1.84 19.88

% of Portfolio 25.07 12.85

Boston Trust Equity - Composite

S&P 500 Index

0.0 4.0 8.0 12.0 16.0 20.0 24.0

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

0.0

0.0

2.2

18.4

14.8

15.3

14.4

7.0

13.7

14.2

3.2

2.3

3.2

19.7

10.4

14.2

16.6

8.4

9.8

12.1

Boston Trust Equity - Composite S&P 500 Index

0.0

10.0

20.0

30.0

40.0

50.0

>100 Bil 75 Bil - 100 Bil

25 Bil - 75 Bil

15 Bil - 25 Bil

2 Bil - 15 Bil

41.8

8.5

28.9

11.39.6

38.3

5.7

33.8

13.3

8.9

Boston Trust Equity - Composite 12/31/14

28INTEGRITY. BALANCE. OBJECTIVITY.

PERFORMANCE - 1 Quarter TOTAL ATTRIBUTION - 1 Quarter

ACTIVE RETURN - 1 Quarter

0.0 0.3 0.6 0.9-0.3-0.6-0.9

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

-0.2

0.2

0.3

0.4

0.2

0.3

-0.1

0.5

-0.3

0.3

Boston Trust Equity - Composite

S&P 500 Index

0.0 8.0 16.0 24.0-8.0-16.0

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

0.0

0.0

6.5

7.4

7.9

10.1

7.1

-5.9

4.7

10.9

13.2

-4.5

-1.7

5.3

6.8

7.5

7.3

-10.8

8.2

8.7

Buy-and-Hold Portfolio 6.56Portfolio Trading -0.71Actual Return 5.85Benchmark Return 4.93Actual Active Return 0.92

Stock Selection 1.54Sector Selection 0.10Interaction -0.01Total Selection 1.62

Portfolio Trading -0.71Benchmark Trading -0.01Active Trading Impact -0.70

Buy & Hold Active Return 0.92

Boston Trust Equity - Composite 12/31/14

29INTEGRITY. BALANCE. OBJECTIVITY.

PERFORMANCE - 3 Years TOTAL ATTRIBUTION - 3 Years

ACTIVE RETURN - 3 Years

0.0 0.4 0.8-0.4-0.8-1.2-1.6

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

0.0

0.2

0.4

-0.3

-0.9

-0.9

-0.8

0.0

-0.6

-0.1

Boston Trust Equity - Composite

S&P 500 Index

0.0 15.0 30.0 45.0-15.0-30.0

Utilities

Telecommunication Services

Materials

Information Technology

Industrials

Health Care

Financials

Energy

Consumer Staples

Consumer Discretionary

-7.7

-4.1

24.1

20.4

16.5

19.8

20.7

7.3

13.8

23.3

13.9

10.7

15.7

21.0

21.2

27.6

26.3

6.5

17.4

25.0

Buy-and-Hold Portfolio 17.46Portfolio Trading 0.33Actual Return 17.80Benchmark Return 20.41Actual Active Return -2.62

Stock Selection -2.50Sector Selection -0.12Interaction -0.40Total Selection -3.03

Portfolio Trading 0.33Benchmark Trading 0.02Active Trading Impact 0.31

Buy & Hold Active Return -2.72

Boston Trust Equity - Composite 12/31/14

30INTEGRITY. BALANCE. OBJECTIVITY.

THIS PAGE LEFT INTENTIONALLY BLANK

31INTEGRITY. BALANCE. OBJECTIVITY.

STRATEGY INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Fixed Income (SA+CF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since account inception.

Firm and Management:Domenic Colasacco is a portfoliomanager and president of the Adviser.Mr. Colasacco is also the president ofBoston Trust & InvestmentManagement Company and has servedas its Chief Investment Officer since1980. Mr. Colasacco managesportfolios for individual and institutionalclients and also manages the BostonTrust Equity Fund. Mr. Colasacco is aholder of the Chartered FinancialAnalyst (CFA) designation and amember of the Boston SecurityAnalysts Society.

Investment Strategy:Boston Trust's approach to fixedincome investing combines top downeconomic scenario forecasts withbottom up fundamental research. Usingmacroeconomic-based quantitativetools, the investment team forecastsinterest rate changes for a range ofpossible economic outcomes. Theseforecasts contribute to portfoliostrategies with respect to interest ratesand the yield curve. In selectingindividual securities, Boston Trustapplies long-held standards for superiorfinancial quality, appropriate risk, anddiversification.

-3.0

0.0

3.0

6.0

9.0

12.0

15.0

Ret

urn

(%)

-5.0 0.0 5.0 10.0 15.0Risk (Standard Deviation %)

Return StandardDeviation

Boston Tr FI - Boulder F&P 3.93 2.81

Barclays Agg 4.45 2.95

Median 5.16 2.98

-10.0

-4.0

2.0

8.0

14.0

20.0

26.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Boston Tr FI - Boulder F&P 1.39 (36) 3.71 (57) 3.71 (57) 1.84 (83) 3.93 (73) 4.27 (74) 4.41 (72)

Barclays Agg 1.79 (22) 5.97 (36) 5.97 (36) 2.66 (69) 4.45 (63) 4.77 (63) 4.71 (62)

Median 0.88 4.41 4.41 3.82 5.16 5.29 5.07

2013 2012 2011 2010 2009 2008 2007Boston Tr FI - Boulder F&P -2.15 (84) 4.08 (76) 7.76 (33) 6.55 (65) 4.93 (83) 5.33 (23) 8.43 (10)IM U.S. Fixed Income (SA+CF) Median -0.29 6.67 6.42 7.56 10.44 1.36 6.23

Barclays Agg -2.02 (81) 4.21 (75) 7.84 (32) 6.54 (65) 5.93 (78) 5.24 (24) 6.97 (33)IM U.S. Fixed Income (SA+CF) Median -0.29 6.67 6.42 7.56 10.44 1.36 6.23

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

3Years

EndingDec-2008

Boston Tr FI - Boulder F&P 1.84 (83) 3.15 (74) 6.12 (66) 6.41 (73) 5.60 (64) 6.22 (42) 5.81 (18)IM U.S. Fixed Income (SA+CF) Median 3.82 4.27 7.16 8.73 6.35 5.85 4.07

Barclays Agg 2.66 (69) 3.26 (72) 6.19 (66) 6.77 (70) 5.90 (59) 6.04 (46) 5.51 (24)IM U.S. Fixed Income (SA+CF) Median 3.82 4.27 7.16 8.73 6.35 5.85 4.07

Boston Tr FI - Boulder F&P 12/31/14

32INTEGRITY. BALANCE. OBJECTIVITY.

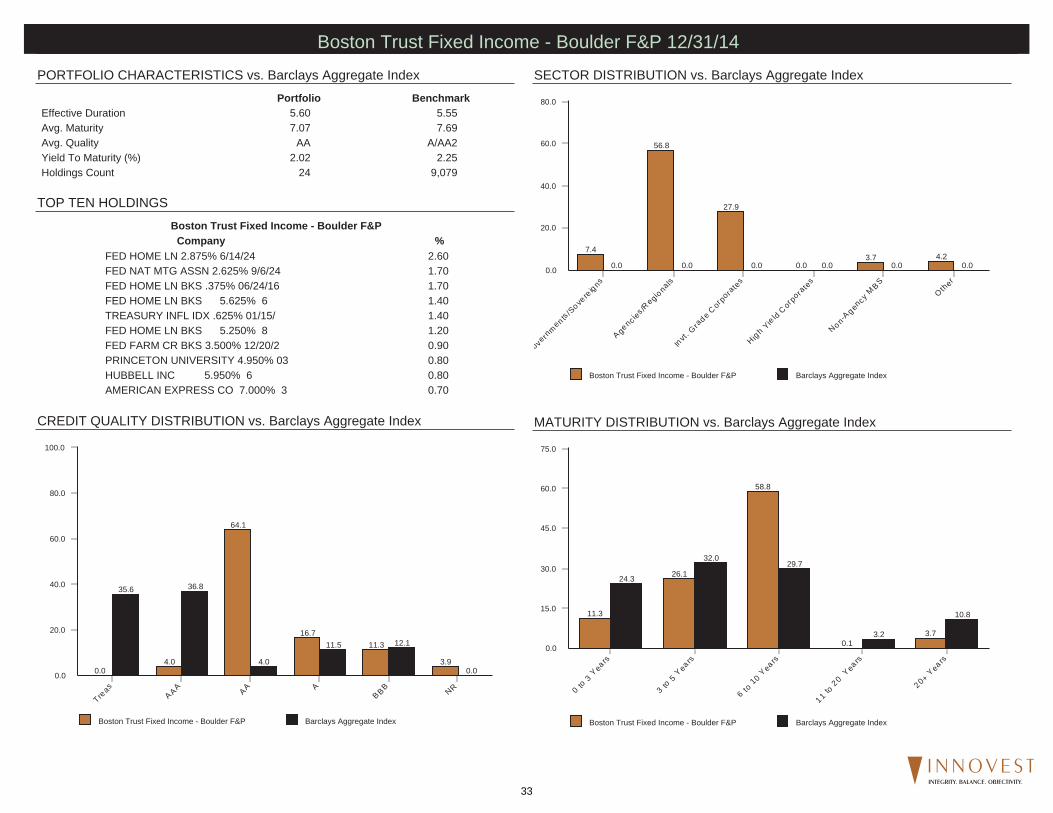

TOP TEN HOLDINGS

PORTFOLIO CHARACTERISTICS vs. Barclays Aggregate Index

CREDIT QUALITY DISTRIBUTION vs. Barclays Aggregate Index

SECTOR DISTRIBUTION vs. Barclays Aggregate Index

MATURITY DISTRIBUTION vs. Barclays Aggregate Index

Boston Trust Fixed Income - Boulder F&P Barclays Aggregate Index

0.0

20.0

40.0

60.0

80.0

overn

men ts /S

overe

igns

A gencie

s /Regio

nals

Invt.

Grade

Corpo

rate

s

H igh

Yield

Corpo

rate

s

Non-A gen

cy M BS

Other

0.0 0.0 0.0 0.0 0.0 0.0

7.4

56.8

27.9

0.03.7 4.2

Portfolio BenchmarkEffective Duration 5.60 5.55Avg. Maturity 7.07 7.69Avg. Quality AA A/AA2Yield To Maturity (%) 2.02 2.25Holdings Count 24 9,079

Boston Trust Fixed Income - Boulder F&PCompany %

FED HOME LN 2.875% 6/14/24 2.60FED NAT MTG ASSN 2.625% 9/6/24 1.70FED HOME LN BKS .375% 06/24/16 1.70FED HOME LN BKS 5.625% 6 1.40TREASURY INFL IDX .625% 01/15/ 1.40FED HOME LN BKS 5.250% 8 1.20FED FARM CR BKS 3.500% 12/20/2 0.90PRINCETON UNIVERSITY 4.950% 03 0.80HUBBELL INC 5.950% 6 0.80AMERICAN EXPRESS CO 7.000% 3 0.70

Boston Trust Fixed Income - Boulder F&P Barclays Aggregate Index

0.0

20.0

40.0

60.0

80.0

100.0

Treas

A AA AA AB BB NR

35.6 36.8

4.0

11.5 12.1

0.00.04.0

64.1

16.711.3

3.9

Boston Trust Fixed Income - Boulder F&P Barclays Aggregate Index

0.0

15.0

30.0

45.0

60.0

75.0

0 to

3 Y ea

rs

3 to

5 Y ea

rs

6 to

10 Y ea

rs

11 to

20 Y ea

rs

20+ Y ea

rs

24.3

32.029.7

3.2

10.811.3

26.1

58.8

0.13.7

Boston Trust Fixed Income - Boulder F&P 12/31/14

33INTEGRITY. BALANCE. OBJECTIVITY.

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Mid Cap Growth Equity (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and Management:Tony Dong has been the lead managerhere since February 2001. He's workedat Munder since 1988 and managedlarge-cap, growth-at-a-reasonable pricestrategies before taking over this fund.He's backed here by four comanagers:Andy Mui, Brian Matuszak, GeorgeSanders, and Geoffrey Wilson.

Investment Strategy:The Munder team seek companies thattrade cheaply relative to their growthprospects, using a broad range ofvaluation measures. They keep theFund's sector weightings within 3percentage points of those of the fund'sbenchmark, the S&P Midcap 400 Index.They'll typically hold 70-100 stocks andcap position sizes at 3%. And they'rerelatively patient investors; portfolioturnover has averaged around 50%.

Innovest's Assessment:Munder’s low beta bias is likely tooutperform during market drawdownsand when quality growth companies arein favor. Underperformance is expectedwhen low quality, high beta companiesoutpace high quality securities andduring speculative growth rallies.

4.0

8.0

12.0

16.0

20.0

24.0

Ret

urn

(%)

9.0 12.0 15.0 18.0 21.0Risk (Standard Deviation %)

Return StandardDeviation

Victory Munder MC Core Gr 16.30 14.59

Russell Midcap Growth Index 16.94 15.34

Median 15.01 16.08

-4.0

2.0

8.0

14.0

20.0

26.0

32.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Victory Munder MC Core Gr 5.69 (39) 10.17 (25) 10.17 (25) 19.56 (38) 16.30 (21) 6.92 (51) 9.35 (29)

Russell Midcap Growth Index 5.84 (37) 11.90 (12) 11.90 (12) 20.71 (18) 16.94 (12) 8.59 (18) 9.43 (27)

Median 5.32 7.53 7.53 18.69 15.01 6.97 8.51

2013 2012 2011 2010 2009 2008 2007Victory Munder MC Core Gr 33.71 (67) 16.01 (27) -0.77 (24) 25.48 (54) 32.80 (74) -43.45 (38) 20.97 (28)Russell Midcap Growth Index 35.74 (51) 15.81 (30) -1.65 (28) 26.38 (49) 46.29 (25) -44.32 (43) 11.43 (74)IM U.S. Mid Cap Growth Equity (MF) Median 35.76 14.22 -4.65 26.11 40.65 -45.39 15.86

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

3Years

EndingDec-2008

Victory Munder MC Core Gr 19.56 (38) 15.46 (23) 13.04 (18) 18.25 (60) -1.96 (64) -3.15 (54) -8.55 (26)Russell Midcap Growth Index 20.71 (18) 15.63 (21) 12.91 (21) 22.06 (17) 0.97 (37) -3.18 (54) -11.79 (60)IM U.S. Mid Cap Growth Equity (MF) Median 18.69 13.99 11.11 19.03 -0.56 -2.94 -11.06

Victory Munder MC Core Gr 12/31/14

34INTEGRITY. BALANCE. OBJECTIVITY.

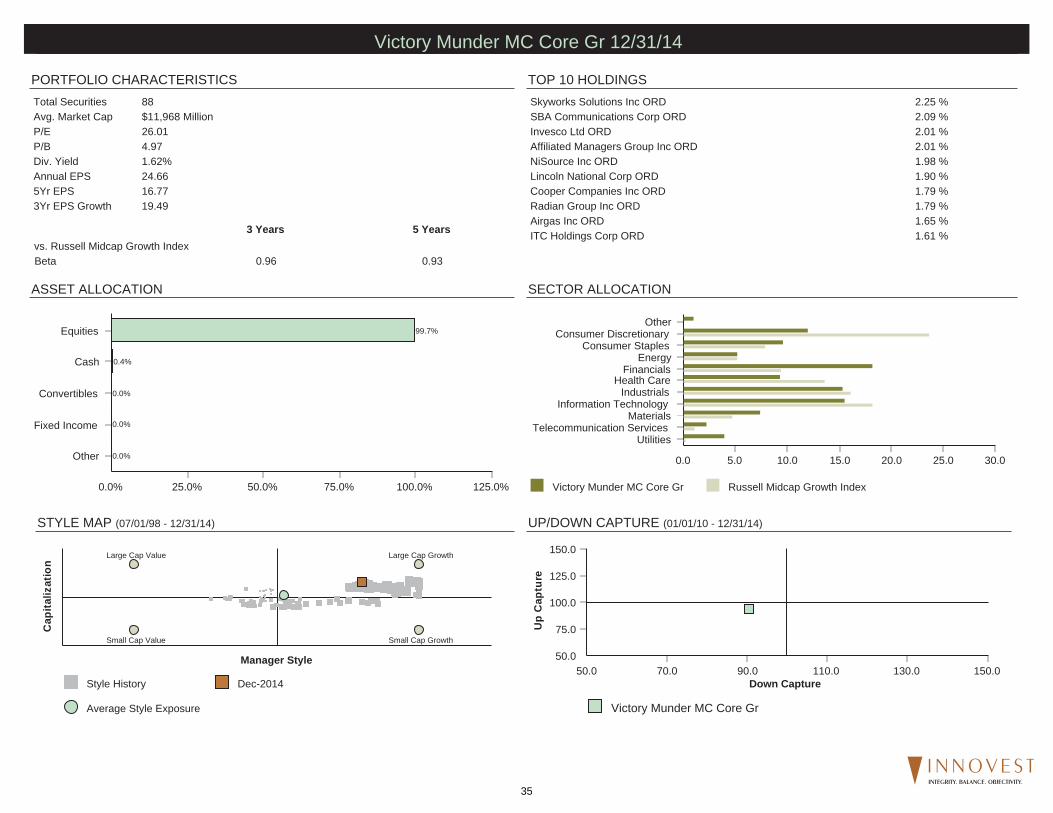

TOP 10 HOLDINGS

STYLE MAP (07/01/98 - 12/31/14)

SECTOR ALLOCATIONASSET ALLOCATION

PORTFOLIO CHARACTERISTICS

UP/DOWN CAPTURE (01/01/10 - 12/31/14)

Total Securities 88Avg. Market Cap $11,968 MillionP/E 26.01P/B 4.97Div. Yield 1.62%Annual EPS 24.665Yr EPS 16.773Yr EPS Growth 19.49

Skyworks Solutions Inc ORD 2.25 %SBA Communications Corp ORD 2.09 %Invesco Ltd ORD 2.01 %Affiliated Managers Group Inc ORD 2.01 %NiSource Inc ORD 1.98 %Lincoln National Corp ORD 1.90 %Cooper Companies Inc ORD 1.79 %Radian Group Inc ORD 1.79 %Airgas Inc ORD 1.65 %ITC Holdings Corp ORD 1.61 %3 Years 5 Years

vs. Russell Midcap Growth IndexBeta 0.96 0.93

0.0% 25.0% 50.0% 75.0% 100.0% 125.0%

Other

Fixed Income

Convertibles

Cash

Equities

0.0%

0.0%

0.0%

0.4%

99.7%

Victory Munder MC Core Gr Russell Midcap Growth Index

0.0 5.0 10.0 15.0 20.0 25.0 30.0

UtilitiesTelecommunication Services

MaterialsInformation Technology

IndustrialsHealth Care

FinancialsEnergy

Consumer StaplesConsumer Discretionary

Other

Style History Dec-2014

Average Style Exposure

Cap

italiz

atio

n

Manager Style

Large Cap Growth

Small Cap GrowthSmall Cap Value

Large Cap Value

Victory Munder MC Core Gr

50.0

75.0

100.0

125.0

150.0U

p C

aptu

re

50.0 70.0 90.0 110.0 130.0 150.0Down Capture

Victory Munder MC Core Gr 12/31/14

35INTEGRITY. BALANCE. OBJECTIVITY.

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Small Cap Value Equity (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and Management:ICM's Small Cap Value effort began in1989, and today Bill Heaphy, ChiefInvestment Officer, and Sim Wootenserve as co-portfolio managers of theICM Small Company Portfolio. Bothhave research responsibilities and Billserves as Director of Research for thesmall cap team. Gary Merwitz, RobJacapraro, Josh Overholt and MattFleming are analysts on the small capteam.

Investment Strategy:Management starts with a universe ofstocks with market caps of around $1billion and narrows the list throughscreens and company analysis. Theteam favors well-managed companieswith good growth prospects that aretrading at attractive valuations. It tendsto sell when valuations get too high orwhen the company doesn't meetexpectations.

Innovest's Assessment:The strategy should outperform in downand stable markets and when lessercapitalized companies are leading. Thefund should underperform during bullmarkets when companies with little orno earnings are in vogue due to itssensitivity to high valuations; althoughthis may be subdued due to its higherweighting of lesser capitalizedcompanies. The fund should alsounderperform when financials andutilities lead due to management'sperpetual aversion to the sectors.

3.0

6.0

9.0

12.0

15.0

18.0

21.0

Ret

urn

(%)

0.0 10.0 20.0 30.0Risk (Standard Deviation %)

Return StandardDeviation

ICM Small Company 13.85 18.25

Russell 2000 Value Index 14.26 17.57

Median 14.89 17.35

-12.0

-4.0

4.0

12.0

20.0

28.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

ICM Small Company 9.04 (38) 2.87 (62) 2.87 (62) 17.88 (62) 13.85 (76) 7.59 (58) 8.02 (18)

Russell 2000 Value Index 9.40 (33) 4.22 (41) 4.22 (41) 18.29 (51) 14.26 (61) 7.59 (58) 6.89 (54)

Median 8.02 3.63 3.63 18.32 14.89 7.85 7.05

2013 2012 2011 2010 2009 2008 2007ICM Small Company 36.16 (49) 16.93 (45) -4.85 (58) 22.73 (80) 34.46 (26) -35.11 (63) 3.35 (5)Russell 2000 Value Index 34.52 (65) 18.05 (33) -5.50 (66) 24.50 (61) 20.58 (76) -28.92 (22) -9.78 (67)IM U.S. Small Cap Value Equity (MF) Median 36.05 16.59 -4.00 25.40 27.89 -32.13 -6.98

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

3Years

EndingDec-2008

ICM Small Company 17.88 (62) 14.85 (54) 10.94 (63) 16.23 (39) 2.31 (57) -3.39 (13) -7.18 (15)Russell 2000 Value Index 18.29 (51) 14.49 (63) 11.57 (52) 12.36 (92) 2.19 (58) -8.22 (52) -7.49 (17)IM U.S. Small Cap Value Equity (MF) Median 18.32 14.99 11.79 15.73 2.50 -8.07 -9.89

ICM Small Company 12/31/14

36INTEGRITY. BALANCE. OBJECTIVITY.

TOP 10 HOLDINGS

STYLE MAP (05/01/89 - 12/31/14)

SECTOR ALLOCATIONASSET ALLOCATION

PORTFOLIO CHARACTERISTICS

UP/DOWN CAPTURE (01/01/10 - 12/31/14)

Total Securities 117Avg. Market Cap $1,544 MillionP/E 25.68P/B 1.94Div. Yield 2.20%Annual EPS 11.765Yr EPS 10.033Yr EPS Growth 9.79

Dreyfus Treasury Prime Cash Management;Inst 1.78 %Ameris Bancorp ORD 1.60 %Heartland Express Inc ORD 1.38 %Innophos Holdings Inc ORD 1.38 %Esco Technologies Inc ORD 1.37 %Integrated Device Technology Inc ORD 1.36 %NorthWestern Corp ORD 1.33 %Idacorp Inc ORD 1.33 %Rogers Corp ORD 1.29 %Coherent Inc ORD 1.29 %3 Years 5 Years

vs. Russell 2000 Value IndexBeta 1.03 1.03

0.0% 25.0% 50.0% 75.0% 100.0% 125.0%

Other

Fixed Income

Convertibles

Cash

Equities

0.0%

0.0%

0.0%

1.8%

98.2%

ICM Small Company Russell 2000 Value Index

0.0 10.0 20.0 30.0 40.0 50.0

UtilitiesTelecommunication Services

MaterialsInformation Technology

IndustrialsHealth Care

FinancialsEnergy

Consumer StaplesConsumer Discretionary

Other

Style History Dec-2014

Average Style Exposure

Cap

italiz

atio

n

Manager Style

Large Cap Growth

Small Cap GrowthSmall Cap Value

Large Cap Value

ICM Small Company

50.0

75.0

100.0

125.0

150.0U

p C

aptu

re

50.0 70.0 90.0 110.0 130.0 150.0Down Capture

ICM Small Company 12/31/14

37INTEGRITY. BALANCE. OBJECTIVITY.

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM International Large Cap Value Equity (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and ManagementThe International Stock Fund ismanaged by the InternationalInvestment Policy Committee. The ninemembers of this committee have anaverage tenure at Dodge & Cox of 24years. In addition, all the firm's analystsare involved in security selection due totheir global coverage responsibilities.

Investment StrategyThe Fund invests primarily in adiversified portfolio of equity securitiesissued by non-U.S. companies from atleast three different countries, includingemerging markets. The Fund focuseson countries whose economic andpolitical systems appear more stableand are believed to provide someprotection to foreign shareholders. TheFund invests primarily in medium-to-large well established companiesbased on standards of the applicablemarket. In selecting investments, theFund invests primarily in companiesthat, in Dodge & Cox’s opinion, appearto be temporarily undervalued by thestock market but have a favorableoutlook for long-term growth.

Innovest's AssessmentWe believe this collaborative researchapproach will continue generatingshareholder value over full marketcycles; however, performance maysuffer during periods driven by moremacroeconomic events or a disregardfor company specific fundamentals.The strategy’s notable allocation todeveloping countries also suggests thatrelative performance may be partiallydictated by the market’s preference foremerging market securities.

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

Ret

urn

(%)

12.0 14.0 16.0 18.0 20.0 22.0Risk (Standard Deviation %)

Return StandardDeviation

Dodge & Cox Intl 7.89 17.72

MSCI EAFE Value Idx 4.42 17.50

Median 4.05 17.74

-20.0

-12.0

-4.0

4.0

12.0

20.0

28.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

Dodge & Cox Intl -4.66 (33) 0.08 (1) 0.08 (1) 15.23 (1) 7.89 (1) 2.00 (8) 6.73 (16)

MSCI EAFE Value Idx -4.85 (56) -5.39 (25) -5.39 (25) 11.04 (1) 4.42 (34) -1.01 (38) 3.89 (57)

Median -4.81 -6.85 -6.85 9.14 4.05 -1.91 4.30

2013 2012 2011 2010 2009 2008 2007Dodge & Cox Intl 26.31 (2) 21.03 (13) -15.97 (83) 13.69 (6) 47.46 (6) -46.69 (66) 11.71 (29)MSCI EAFE Value Idx 22.95 (8) 17.69 (44) -12.17 (43) 3.25 (81) 34.23 (29) -44.09 (47) 5.95 (93)IM International Large Cap Value Equity (MF) Median 21.02 17.18 -12.93 5.39 27.98 -44.45 9.54

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

3Years

EndingDec-2008

Dodge & Cox Intl 15.23 (1) 8.71 (3) 4.96 (9) 12.10 (8) -3.67 (6) -4.24 (16) -8.65 (60)MSCI EAFE Value Idx 11.04 (1) 8.32 (11) 2.19 (57) 6.77 (33) -8.15 (41) -7.35 (48) -8.25 (52)IM International Large Cap Value Equity (MF) Median 9.14 6.97 2.58 6.16 -8.67 -7.39 -7.74

Dodge & Cox Intl 12/31/14

38INTEGRITY. BALANCE. OBJECTIVITY.

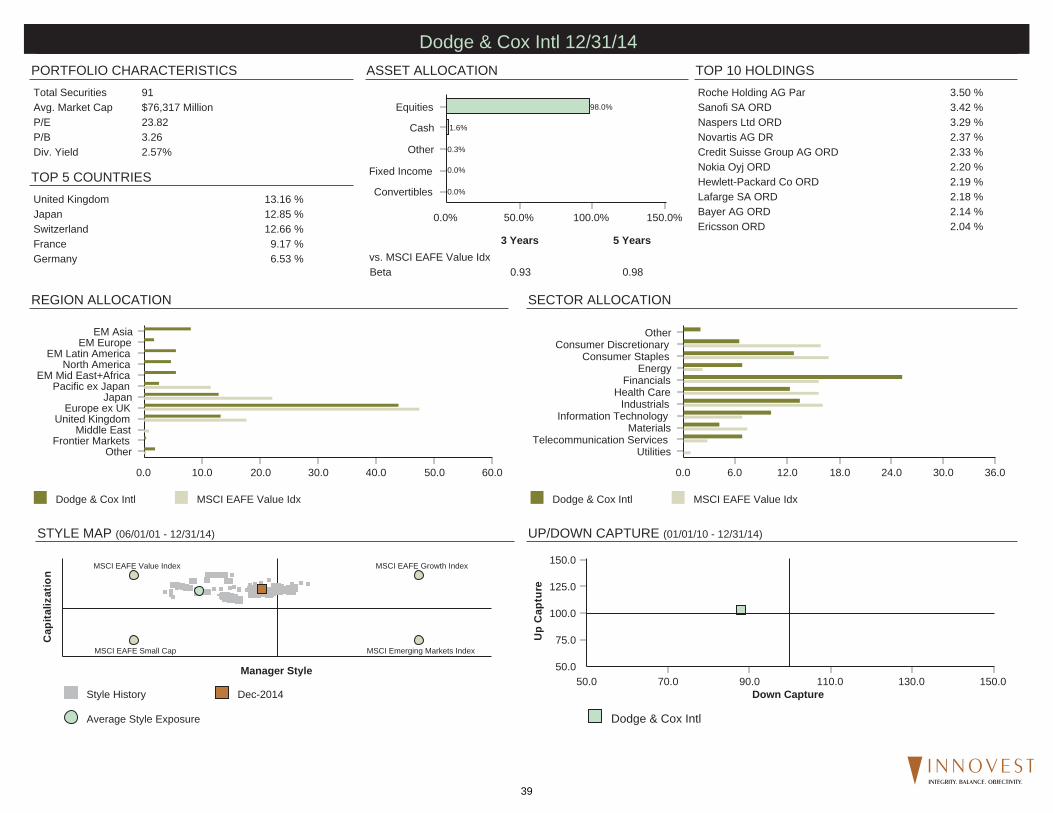

TOP 10 HOLDINGSPORTFOLIO CHARACTERISTICS

STYLE MAP (06/01/01 - 12/31/14)

SECTOR ALLOCATION

ASSET ALLOCATION

REGION ALLOCATION

TOP 5 COUNTRIES

UP/DOWN CAPTURE (01/01/10 - 12/31/14)

0.0% 50.0% 100.0% 150.0%

Convertibles

Fixed Income

Other

Cash

Equities

0.0%

0.0%

0.3%

1.6%

98.0%

Total Securities 91Avg. Market Cap $76,317 MillionP/E 23.82P/B 3.26Div. Yield 2.57%

Roche Holding AG Par 3.50 %Sanofi SA ORD 3.42 %Naspers Ltd ORD 3.29 %Novartis AG DR 2.37 %Credit Suisse Group AG ORD 2.33 %Nokia Oyj ORD 2.20 %Hewlett-Packard Co ORD 2.19 %Lafarge SA ORD 2.18 %Bayer AG ORD 2.14 %Ericsson ORD 2.04 %

United Kingdom 13.16 %Japan 12.85 %Switzerland 12.66 %France 9.17 %Germany 6.53 %

3 Years 5 Yearsvs. MSCI EAFE Value IdxBeta 0.93 0.98

Dodge & Cox Intl MSCI EAFE Value Idx

0.0 10.0 20.0 30.0 40.0 50.0 60.0

OtherFrontier Markets

Middle EastUnited Kingdom

Europe ex UKJapan

Pacific ex JapanEM Mid East+Africa

North AmericaEM Latin America

EM EuropeEM Asia

Dodge & Cox Intl MSCI EAFE Value Idx

0.0 6.0 12.0 18.0 24.0 30.0 36.0

UtilitiesTelecommunication Services

MaterialsInformation Technology

IndustrialsHealth Care

FinancialsEnergy

Consumer StaplesConsumer Discretionary

Other

Style History Dec-2014

Average Style Exposure

Cap

italiz

atio

n

Manager Style

MSCI EAFE Growth Index

MSCI Emerging Markets IndexMSCI EAFE Small Cap

MSCI EAFE Value Index

Dodge & Cox Intl

50.0

75.0

100.0

125.0

150.0

Up

Cap

ture

50.0 70.0 90.0 110.0 130.0 150.0Down Capture

Dodge & Cox Intl 12/31/14

39INTEGRITY. BALANCE. OBJECTIVITY.

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM International Large Cap Growth Equity (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and Management:Like all American Funds, this fundboasts many experienced managers,most of whom have been with thecompany for more than a decade. Thismultimanager system eases personneltransitions, like the June 2014departure of long-time manager RobertLovelace, who moved to an affiliate.Each of the fund's nine managers runsa portion of the fund's assetsindependently. In addition, a portion ofthe portfolio (less than 25% of assets)is run by the firm's analyst staff.

Investment Strategy:This fund's managers are focused onlong term capital growth. They primarilyinvest in common stocks of Europeanand Pacific Basin issuers that haveprospects of above average capitalappreciation. The managers may usecash to moderate volatility, typicallyholding 5-10% of fund assets in cash.The Fund usually has a stake inemerging-markets companies and willsometimes hold preferred stock andconvertibles debt.

Innovest's Assessment:The fund’s propensity to focus intenselyon bottom-up, fundamental factors canlead to periods of underperformancewhen the market is less concernedabout company fundamentals and moredriven by thematic and macroeconomicfactors. Additionally, the fund is likely tolag when highly cyclical stocks andgenerally lower quality companiessignificantly outperform the overallmarket. Finally, the fund’s immenseasset base is likely to present somechallenges in the fund’s ability to buildmeaningful positions in smallercompanies and opportunistically tradein less liquid markets.

-3.0

0.0

3.0

6.0

9.0

12.0

Ret

urn

(%)

9.0 12.0 15.0 18.0 21.0Risk (Standard Deviation %)

Return StandardDeviation

American Funds EuPc 5.68 15.80

MSCI EAFE Growth Index (Net) 6.19 16.02

Median 5.64 15.80

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

American Funds EuPc -1.72 (50) -2.64 (32) -2.64 (32) 11.72 (21) 5.68 (47) 1.25 (23) 6.71 (18)

MSCI EAFE Growth Index (Net) -2.29 (66) -4.43 (50) -4.43 (50) 11.03 (38) 6.19 (39) 0.01 (63) 4.91 (73)

Median -1.72 -4.53 -4.53 10.74 5.64 0.46 5.87

2013 2012 2011 2010 2009 2008 2007American Funds EuPc 20.15 (26) 19.21 (37) -13.58 (50) 9.40 (67) 39.10 (15) -40.53 (15) 18.96 (24)MSCI EAFE Growth Index (Net) 22.55 (10) 16.86 (69) -12.11 (33) 12.25 (40) 29.36 (66) -42.70 (45) 16.45 (47)IM International Large Cap Growth Equity (MF) Median 18.31 18.41 -13.60 11.34 32.40 -43.70 16.14

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

3Years

EndingDec-2008

American Funds EuPc 11.72 (21) 7.37 (47) 4.07 (61) 9.56 (40) -3.27 (12) -0.53 (6) -4.82 (21)MSCI EAFE Growth Index (Net) 11.03 (38) 7.97 (33) 4.85 (39) 8.47 (69) -5.94 (47) -4.78 (52) -6.54 (48)IM International Large Cap Growth Equity (MF) Median 10.74 7.35 4.37 9.25 -6.08 -4.76 -6.83

American Funds EuPc 12/31/14

40INTEGRITY. BALANCE. OBJECTIVITY.

TOP 10 HOLDINGSPORTFOLIO CHARACTERISTICS

STYLE MAP (01/01/99 - 12/31/14)

SECTOR ALLOCATION

ASSET ALLOCATION

REGION ALLOCATION

TOP 5 COUNTRIES

UP/DOWN CAPTURE (01/01/10 - 12/31/14)

0.0% 50.0% 100.0% 150.0%

Convertibles

Cash

Other

Fixed Income

Equities

0.0%

0.0%

0.2%

10.3%

89.5%

Total Securities 429Avg. Market Cap $59,458 MillionP/E 24.67P/B 4.75Div. Yield 2.08%

Novo Nordisk A/S ORD 5.04 %Bayer AG ORD 2.46 %Softbank Corp ORD 2.29 %Novartis AG ORD 2.21 %Prudential PLC ORD 1.80 %Barclays PLC ORD 1.71 %Murata Manufacturing Co Ltd ORD 1.57 %Baidu Inc DR 1.46 %Associated British Foods PLC ORD 1.45 %Samsung Electronics Co Ltd ORD 1.42 %

Japan 12.15 %United Kingdom 11.75 %United States 9.44 %Germany 7.08 %India 6.79 %

3 Years 5 Yearsvs. MSCI EAFE Growth Index (Net)Beta 0.95 0.97

American Funds EuPc MSCI EAFE Growth Index (Net)

0.0 10.0 20.0 30.0 40.0 50.0 60.0

OtherFrontier Markets

Middle EastUnited Kingdom

Europe ex UKJapan

Pacific ex JapanEM Mid East+Africa

North AmericaEM Latin America

EM EuropeEM Asia

American Funds EuPc MSCI EAFE Growth Index (Net)

0.0 5.0 10.0 15.0 20.0 25.0 30.0

UtilitiesTelecommunication Services

MaterialsInformation Technology

IndustrialsHealth Care

FinancialsEnergy

Consumer StaplesConsumer Discretionary

Other

Style History Dec-2014

Average Style Exposure

Cap

italiz

atio

n

Manager Style

MSCI EAFE Growth Index

MSCI Emerging Markets IndexMSCI EAFE Small Cap

MSCI EAFE Value Index

American Funds EuPc

50.0

75.0

100.0

125.0

150.0

Up

Cap

ture

50.0 70.0 90.0 110.0 130.0 150.0Down Capture

American Funds EuPc 12/31/14

41INTEGRITY. BALANCE. OBJECTIVITY.

FUND INFORMATION

ROLLING 3 YEAR RETURN AND PERCENTILE RANKINGS

PEER GROUP ANALYSIS - IM U.S. Broad Market Core Fixed Income (MF)

CALENDAR YEAR RETURNS AND PERCENTILE RANKINGS

RISK VS. RETURN (5 YEARS*)

*If less than 5 years, data is since inception of fund share class.

Firm and Management:PIMCO was founded in 1971, and isone of the world's largest fixed incomemanagers, with a presence in everymajor bond market. The fund's portfoliomanagement team - Scott Mather isCIO U.S. Core Strategies, Mark Kieselis CIO Global Credit and Mihir Worah isCIO Real Return and Asset Allocation -is supported by the full spectrum ofPIMCO's global resources.

Investment Strategy:The fund aims to provide investors witha combination of income and capitalappreciation potential. It emphasizeshigher-quality, intermediate-term bondsand aims to avoid concentration risk bybeing more globally diversified thanmany core bond funds. It also hasconsiderable flexibility to respond tochanging economic conditions, helpingto manage risk and increase total returnpotential. Major shifts in portfoliostrategy are driven by secular andcyclical outlooks as opposed to short-term market events or aberrations ininterest rates.

Innovest's Assessment:The fund attempts to add value throughtop-down positioning and byaggressively pursuing relativelyattractive sectors of the bond market.The fund's total return approach allowsthem to diversify from heavily weightedsectors in the benchmark. Historically,their sector allocation decisions haveresulted in strong relativeoutperformance; however, it isimportant to note that the fund’sintermediate duration mandate couldbecome a headwind to performance ina rising interest rate environment.PIMCO also has the potential tounderperform when its macroeconomicforecast is materially wrong, either froma timing perspective or a fundamentalperspective. PIMCO's approach willnot always be lockstep with the broadbond market index.

0.0

1.5

3.0

4.5

6.0

7.5

Ret

urn

(%)

0.7 1.4 2.1 2.8 3.5 4.2 4.9Risk (Standard Deviation %)

Return StandardDeviation

PIMCO Tot Rtn Inst 5.14 3.55

BC Aggregate Idx 4.45 2.66

Median 4.69 2.75

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

Ret

urn

LastQuarter

YearTo Date

1Year

3Years

5Years

7Years

10Years

PIMCO Tot Rtn Inst 1.31 (53) 4.69 (77) 4.69 (77) 4.25 (13) 5.14 (28) 6.30 (3) 5.99 (1)

BC Aggregate Idx 1.79 (7) 5.97 (27) 5.97 (27) 2.66 (68) 4.45 (60) 4.77 (46) 4.71 (35)

Median 1.35 5.54 5.54 3.09 4.69 4.68 4.43

2013 2012 2011 2010 2009 2008 2007PIMCO Tot Rtn Inst -1.92 (50) 10.35 (2) 4.16 (94) 8.86 (19) 13.87 (41) 4.82 (13) 9.08 (1)Barclays Aggregate Index -2.02 (55) 4.21 (81) 7.84 (11) 6.54 (69) 5.93 (90) 5.24 (10) 6.97 (9)IM U.S. Broad Market Core Fixed Income (MF) Median -1.94 6.04 6.66 7.25 12.24 -3.79 5.27

3Years

EndingDec-2014

3Years

EndingDec-2013

3Years

EndingDec-2012

3Years

EndingDec-2011

3Years

EndingDec-2010

3Years

EndingDec-2009

3Years

EndingDec-2008

PIMCO Tot Rtn Inst 4.25 (13) 4.08 (27) 7.76 (16) 8.89 (48) 9.12 (1) 9.20 (1) 5.94 (3)Barclays Aggregate Index 2.66 (68) 3.26 (61) 6.19 (68) 6.77 (82) 5.90 (48) 6.04 (26) 5.51 (7)IM U.S. Broad Market Core Fixed Income (MF) Median 3.09 3.52 6.70 8.80 5.81 5.11 1.68

PIMCO Tot Rtn Inst 12/31/14

42INTEGRITY. BALANCE. OBJECTIVITY.

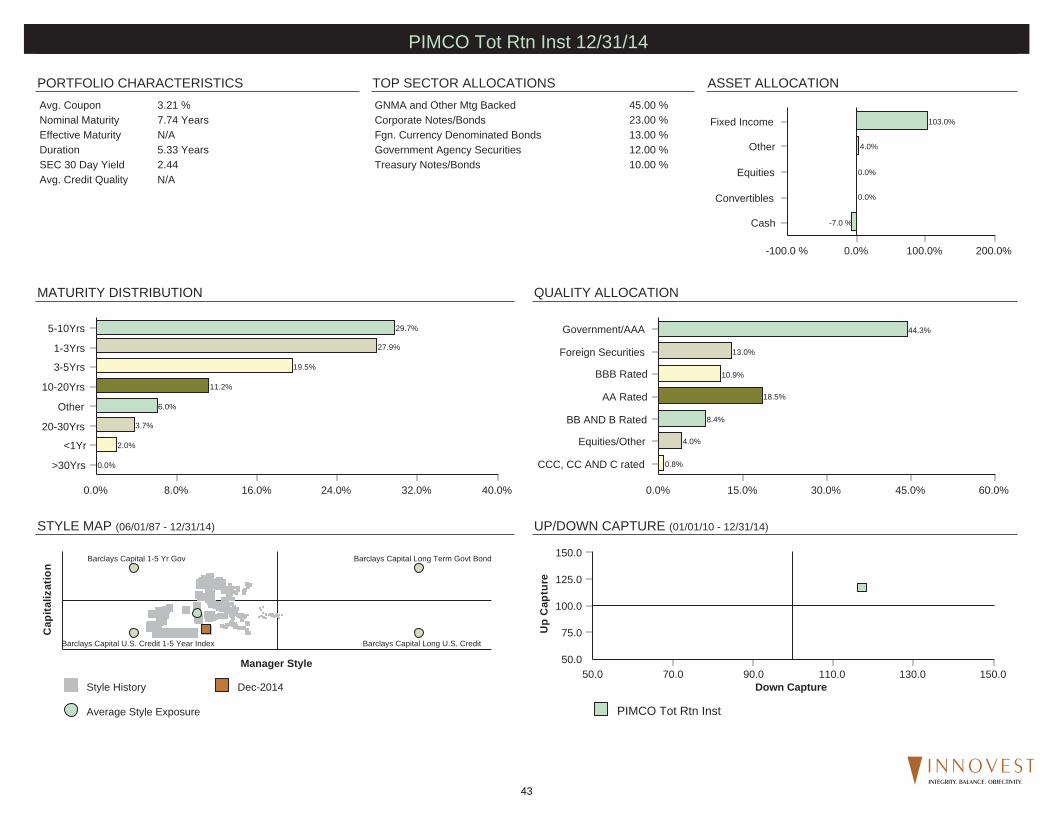

TOP SECTOR ALLOCATIONSPORTFOLIO CHARACTERISTICS

STYLE MAP (06/01/87 - 12/31/14)

QUALITY ALLOCATION

ASSET ALLOCATION

MATURITY DISTRIBUTION

UP/DOWN CAPTURE (01/01/10 - 12/31/14)

0.0% 100.0% 200.0%-100.0 %

Cash

Convertibles

Equities

Other

Fixed Income

-7.0 %

0.0%

0.0%

4.0%