portugal - pkf international · • group taxation is available for all group companies that are...

TRANSCRIPT

2016/17

Portugal

PKF Worldwide Tax Guide 2016/17 1

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed? Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. As you will appreciate, the production of the WWTG is a huge team effort and we would like to thank all tax experts within PKF member firms who gave up their time to contribute the vital information on their country's taxes that forms the heart of this publication. The PKF Worldwide Tax Guide 2016/17 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of the world's most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current on 30 April 2016, while also noting imminent changes where necessary. On a country-by-country basis, each summary such as this one, addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country's personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments. While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice. Services provided by member firms include: Assurance & Advisory;

Financial Planning / Wealth Management;

Corporate Finance;

Management Consultancy;

IT Consultancy;

Insolvency - Corporate and Personal;

Taxation;

Forensic Accounting; and,

Hotel Consultancy. In addition to the printed version of the WWTG, individual country taxation guides such as this are available in PDF format which can be downloaded from the PKF website at www.pkf.com

Portugal

PKF Worldwide Tax Guide 2016/17 2

IMPORTANT DISCLAIMER This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication. This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication. The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication. Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances. PKF International Limited (PKFI) administers a family of legally independent firms. Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions of any individual member or correspondent firm or firms. PKF INTERNATIONAL LIMITED JUNE 2016 © PKF INTERNATIONAL LIMITED All RIGHTS RESERVED USE APPROVED WITH ATTRIBUTION

Portugal

PKF Worldwide Tax Guide 2016/17 3

STRUCTURE OF COUNTRY DESCRIPTIONS A. TAXES PAYABLE

COMPANY TAX: GENERAL REGIME CAPITAL GAINS TAX BRANCH PROFITS TAX VALUE ADDED TAX (VAT) FRINGE BENEFITS TAXATION OTHER TAXES MUNICIPAL TAX ON REAL ESTATE REAL ESTATE TRANSFER TAX

B. DETERMINATION OF TAXABLE INCOME

DEPRECIATION STOCKS / INVENTORY CAPITAL GAINS AND LOSSES DIVIDENDS INTEREST DEDUCTIONS LOSSES FOREIGN SOURCED INCOME INVESTMENT FUNDS INCENTIVES

C. FOREIGN TAX RELIEF D. CORPORATE GROUPS E. RELATED PARTY TRANSACTIONS F. WITHHOLDING TAX G. EXCHANGE CONTROL H. PERSONAL TAX I. TREATY AND NON-TREATY WITHHOLDING TAX RATES

Portugal

PKF Worldwide Tax Guide 2016/17 4

MEMBER FIRM City Name Contact information Lisbon José Parada Ramos +351 213 182 720 [email protected] Oporto José de Sousa Santos +351 223 389 479 [email protected] BASIC FACTS Full name: Portuguese Republic Capital: Lisbon Main language: Portuguese Population: 10.43 million (2014 estimate) Major religion: Christianity Monetary unit: Euro (EUR) Internet domain: .pt Int. dialing code: +351 KEY TAX POINTS • Resident corporations are subject to Portuguese corporate income tax (IRC) on their worldwide

income. Non-resident companies with a permanent establishment in Portugal are liable for IRC on the income imputable to that permanent establishment.

• Foreign-sourced income, gross of tax paid abroad, is included in taxable income. An unilateral credit for foreign income tax suffered can be set off against the Portuguese corporate tax.

• Group taxation is available for all group companies that are resident in Portugal. The parent company must hold, directly or indirectly, at least 75% in the share capital of companies covered by this tax regime.

• The standard rate of VAT is 23%. In addition, an intermediate rate of 13%, and a reduced rate of 6% are applicable to a range of goods and services.

• Transfer pricing legislation enables the tax authorities to make corrections to taxable income when the conditions (and prices) agreed between related parties are different from those that would have been agreed and accepted between independent entities.

• Income tax is payable by individuals on employment income. Resident individuals are subject to income tax on their worldwide income whilst non-residents are liable to income tax only on income sourced in Portugal. There is a special tax regime for non-habitual resident taxpayers

• Social security is due on remunerations at a 23.75% rate for the employee and 11% for the employer.

A. TAXES PAYABLE COMPANY TAX: GENERAL REGIME Resident corporations are subject to Portuguese corporate income tax (CIT) on their worldwide income. Resident companies are those which have their head office, or place of effective management, in Portugal. Non-resident companies with a permanent establishment in Portugal are liable for CIT on the income attributable to that permanent establishment. A non-resident company with no permanent establishment in Portugal is taxed on the following types of income sourced in Portugal: real estate, capital gains, dividends, services, interest and royalties. Taxable profit are taxed at 21%. Companies qualifying as small and medium enterprises are taxed at 17% on the first EUR 15,000 of taxable income. A municipal surcharge of up to 1.5% is levied on the taxable profit amount. An additional state surcharge is levied at the following progressive rates:

Portugal

PKF Worldwide Tax Guide 2016/17 5

Taxable Income (EUR)

Tax Rate

First 1.5 million 0%

Next 6 million 3%

Next 27.5 million 5%

Over 35 million 7% Certain expenses, such as costs related with vehicles and non-documented expenses, are subject to an autonomous taxation at rates varying from 5% (e.g. travel and kilometres allowances) to 50% (for confidential expenses; the rate is 70% for non-profitable entities). These rates are increased by an additional 10% in the years where a company has incurred in tax losses. The tax year usually coincides with the calendar year (1 January to 31 December). However, different tax years may be adopted. Tax is payable by the end of the fifth month following the end of the tax year – generally 31st of May. Payments on account of the final tax liability are due on July, September and 15 December. Such payments are computed by applying the following percentages to the previous tax year's CIT liability, net off any tax withheld at source, depending on the tax-payers turnover, as follows: • Three instalments of 26.67% each (total 80%) – for taxpayers with turnover below EUR

500,000.00. • Three instalments of 31.67% each (total 95%) – for taxpayers with turnover above EUR

500,000.00. Permanent establishments of non-resident companies are taxed at the rates applicable to resident companies. The tax rate for non-resident companies with no permanent establishment obtaining Portuguese sourced income is 25%, except for entities which are resident in a listed offshore jurisdiction in which case the rate is 35%. CAPITAL GAINS TAX Worldwide capital gains obtained by resident companies are included in taxable income. BRANCH PROFITS TAX All income attributable to a Portuguese branch (permanent establishment) is subject to corporation tax. No tax is imposed on the eventual remittances of profits to the head office. VALUE ADDED TAX (VAT) As a member of the European Union, Portugal has adopted VAT which is a sales tax levied on the supply of goods and services as well as on the import of goods from non EU countries into Portugal, including the Azores and Madeira islands, and on the acquisition of goods from other EU Member States. The standard rate is 23%. In addition, an intermediate rate of 13% and a reduced rate of 6% is applicable to a range of goods and services. The standard, intermediate and reduced VAT rates in the Azores are 18%, 10% and 5%, and in Madeira are 22%, 12% and 5%, respectively. FRINGE BENEFITS TAXATION In general, benefits provided to employees are added to their remuneration and taxed accordingly. There are, however, some exceptions, such as lunch allowances, travel allowances and the use of a car (provided such use is not formally agreed in the employment contract).

Portugal

PKF Worldwide Tax Guide 2016/17 6

OTHER TAXES MUNICIPAL TAX ON REAL ESTATE Owners of real estate properties are subject to tax at rates of 0.8% for rural properties and between 0.3% and 0.5% for urban properties on the notional net income derived from property. A 7.5% rate applies when the real estate property is owned by a resident of an offshore jurisdiction (as defined in a 'black list' published by the Finance Ministry). This tax is deductible against rental income. REAL ESTATE TRANSFER TAX Real Estate Transfer Tax is levied on the transfer of real estate property and is normally payable by the buyer. The rate for urban properties is 6.5% and 5% tor land for agriculture. Real Estate for habitation is subject to rates varying from 0% to 6%. A 10% rate applies when the purchaser of the property is a resident of a black-listed offshore jurisdiction. Transactions which are subject to this tax, are exempt from VAT. B. DETERMINATION OF TAXABLE INCOME (CIT) General regime: Taxable income is calculated by adjusting the accounting profits from non-taxable income and non-deductible expenses. As a general principle, costs are only deductible when necessarily incurred tor the purpose of producing income. Simplified scheme: Companies that i) during the previous year had a total income under EUR 200,000; and ii) whose total assets do not exceed EUR 500,000, may be taxed under the simplified taxation scheme. Under this scheme, the taxable amount is computed by applying the specific coefficients on certain types of income, as follows:

0.04 Sales and rendering of hotel activities’ services, food and beverage

0.75 Income from professional activities defined in the PIT Code

0.10 Other services and operating subsidies

0.30 Non-operating subsidies

0.95 Royalties, real estate income, capital gains/losses

1.00 Gratuities received DEPRECIATION Fixed and intangible assets can be depreciated for tax purposes. The depreciation rates are set by specific legislation and include 2% for office buildings and 5% for industrial buildings. No depreciation is allowed on land. The normal method of calculation is the straight-line basis but declining-balance method may be used except for items such as buildings, cars and office furniture. The acquisition cost of intangible assets with no limited period of exclusive use may be depreciated for 20 years (not applicable for the depreciation of the goodwill included on the acquisition of shares). STOCKS / INVENTORY Inventory must normally be valued at the effective cost of acquisition or production (historic cost). Other methods which may be adopted include: • The standard cost method, which must be calculated in accordance with the appropriate

technical and accounting principles; • The sale price method, based on the market value less a normal profit margin.

Portugal

PKF Worldwide Tax Guide 2016/17 7

CAPITAL GAINS AND LOSSES The gain (or loss) is calculated by the difference between the sales proceeds and the acquisition cost which may be updated using official inflation coefficients. If the proceeds of the sales are reinvested in other assets, 50% of the gain obtained (net of the related losses) will be excluded from taxation. For this purpose, reinvestments made in the preceding year, in the year of sale and in the two subsequent years will be taken into account. This is applicable to tangible, intangible and biological assets. When only part of the consideration is reinvested, only the corresponding part of the gain qualifies for the relief. Gains derived from the disposal of shares are not subject to taxation, if the participation has been held for at least 1 year and corresponds to a minimum of 10% of the share capital in the participated company. Gains obtained by non-resident entities from the disposal of shares are exempt from tax. However, some anti-avoidance provisions apply in order to prevent abuse of this concession. DIVIDENDS There is a full participation exemption on dividend payments between Portuguese resident companies when the recipient of the dividends is a company that has held a participation of not less than 10% of the share capital of the distributing company for a minimum period of one year. If such conditions are not met, the dividend amount is subject to taxation. The full participation exemption is also available for dividends derived from non-resident companies, provided the participation is of at least 5% of the share capital of the subsidiary and the related shares have been held for a period of two years, and some additional conditions apply. Dividends paid to non-resident shareholders are normally subject to withholding tax at 25% (or at the treaty rate if applicable). When the parent company is resident of an EU Member State or of a territory with which Portugal has signed a Double Tax Treaty, and has held a participation of at least 10% for a year in the share capital of the Portuguese company distributing the dividends, no withholding tax shall apply provided the company receiving the dividend is subject to one of the taxes listed in the parent/subsidiary directive, or, in case of non-EU shareholders, at a nominal rate of no less than 60% of the CIT rate. INTEREST DEDUCTIONS The deductibility of net financing costs is limited to the higher of: • EUR 1 million; or, • 40% of the annual earnings before tax, depreciation and net financing expenses (30% as from

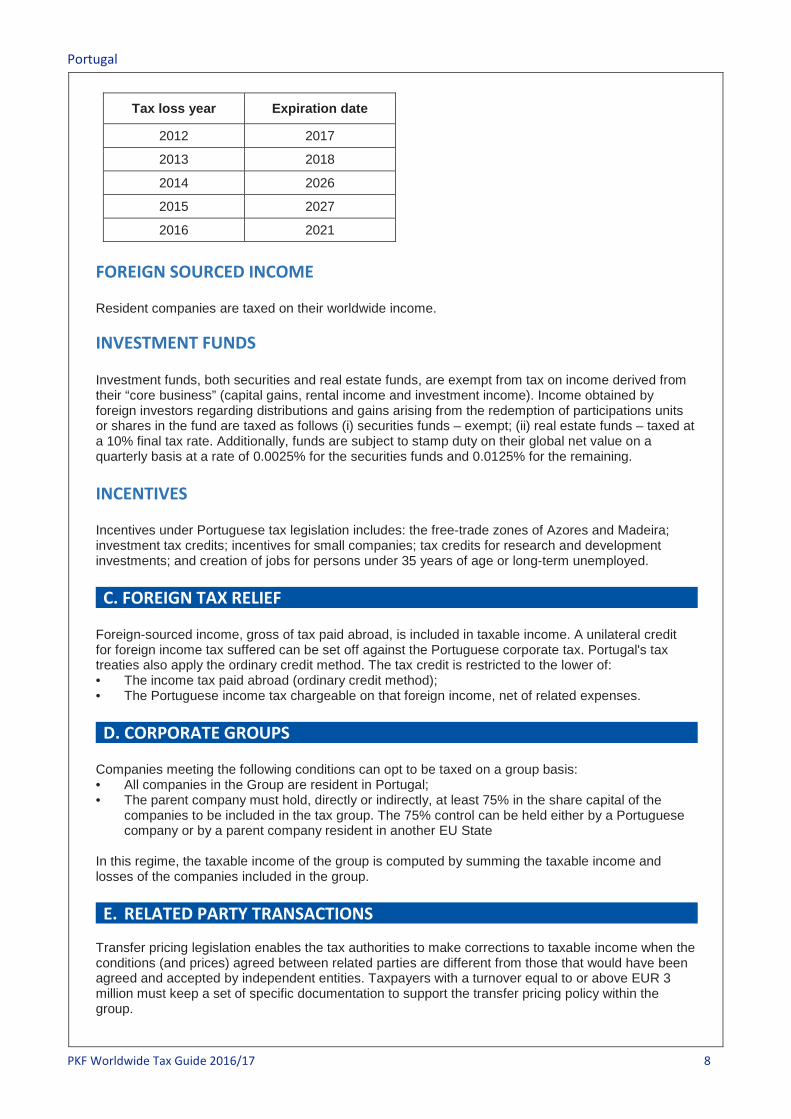

January 2017). The net financing expenses are calculated as the balance of financing costs and financing income. Non-deductible net financing costs may be deducted in the following five years, provided the total financial costs (costs of the year and costs carried forward) do not exceed the above limits. This limitation is not applicable to banks and other financial institutions. LOSSES Operating losses incurred by resident companies, or by a branch of a non-resident company, may be carried forward to be set off against taxable profits for five years. However, companies are only allowed to deduct tax losses up to 70% of the taxable profits in any given period. No deduction is allowed if the ownership of 50% or more of the share capital has changed, compared to the year in which the losses were incurred, unless the changes of ownership is justified by special economic relevance and the deduction is accepted by the tax authorities. In the table below we provide the expiration date of losses carry forward according to the year they were incurred:

Portugal

PKF Worldwide Tax Guide 2016/17 8

Tax loss year Expiration date

2012 2017

2013 2018

2014 2026

2015 2027

2016 2021 FOREIGN SOURCED INCOME Resident companies are taxed on their worldwide income. INVESTMENT FUNDS Investment funds, both securities and real estate funds, are exempt from tax on income derived from their “core business” (capital gains, rental income and investment income). Income obtained by foreign investors regarding distributions and gains arising from the redemption of participations units or shares in the fund are taxed as follows (i) securities funds – exempt; (ii) real estate funds – taxed at a 10% final tax rate. Additionally, funds are subject to stamp duty on their global net value on a quarterly basis at a rate of 0.0025% for the securities funds and 0.0125% for the remaining. INCENTIVES Incentives under Portuguese tax legislation includes: the free-trade zones of Azores and Madeira; investment tax credits; incentives for small companies; tax credits for research and development investments; and creation of jobs for persons under 35 years of age or long-term unemployed. C. FOREIGN TAX RELIEF Foreign-sourced income, gross of tax paid abroad, is included in taxable income. A unilateral credit for foreign income tax suffered can be set off against the Portuguese corporate tax. Portugal's tax treaties also apply the ordinary credit method. The tax credit is restricted to the lower of: • The income tax paid abroad (ordinary credit method); • The Portuguese income tax chargeable on that foreign income, net of related expenses. D. CORPORATE GROUPS Companies meeting the following conditions can opt to be taxed on a group basis: • All companies in the Group are resident in Portugal; • The parent company must hold, directly or indirectly, at least 75% in the share capital of the

companies to be included in the tax group. The 75% control can be held either by a Portuguese company or by a parent company resident in another EU State

In this regime, the taxable income of the group is computed by summing the taxable income and losses of the companies included in the group. E. RELATED PARTY TRANSACTIONS Transfer pricing legislation enables the tax authorities to make corrections to taxable income when the conditions (and prices) agreed between related parties are different from those that would have been agreed and accepted by independent entities. Taxpayers with a turnover equal to or above EUR 3 million must keep a set of specific documentation to support the transfer pricing policy within the group.

Portugal

PKF Worldwide Tax Guide 2016/17 9

F. WITHHOLDING TAX Certain types of earnings are subject to withholding tax rates generally at a 25%. In case of payments made to a listed offshore jurisdiction the withholding tax rate is 35%. The withholding tax rate may be reduced if there is a double tax treaty in force with the country where the income beneficiary is tax resident. G. EXCHANGE CONTROL There are no exchange control regulations. H. PERSONAL TAX Income tax is payable by individuals on income obtained from employment, a business activity or independent profession, investment income, immovable property, capital gains and pensions. Resident individuals are subject to income tax on their worldwide income while non-residents are liable to income tax only on income sourced in Portugal. Residence is determined by physical presence in Portugal for more than 183 days, consecutive or not, during any period of 12 months. Having remained for less time, residence is also determined by having a place of abode in a way that may lead to the supposition of an intention to keep and occupy it as a habitual home/ residence. When determining the taxable income, certain tax credits are allowed in addition to some specific deductions concerning each category of income. These include a percentage of expenses incurred on health, education and family overheads. Husbands and wives living together, and their dependent children, may opt to be taxed on their joint income. Normally, the tax year coincides with the calendar year but may be split in the year of marriage, divorce, separation or death. Special rules apply for the calculation of gains on immovable property, shares or other corporate rights, securities and patents. Exempt income includes various employment allowances (up to certain limits); a portion of pension income; capital gains from the sale of the habitual private residence, when the proceeds are reinvested in another private residence. Tax returns submitted in paper form are due between 15 March and 15 April of the subsequent tax year for taxpayers with income derived solely from employment or pensions. Tax returns submitted via the internet are also due between 15 March and 15 April of the subsequent tax year for taxpayers with income which derives solely from employment or pension or between 16 April and 16 May for taxpayers who receive any income other than from employment or pensions. The following progressive tax rates apply in tax year 2016 to the aggregate net results of employment income, business income, investment income (except interest on bonds and deposits), income from land, capital gains and income from pensions:

Taxable Income Tax Rates

First EUR 7,035 14.5%

Next EUR 13,065 28.5%

Next EUR 20,100 37%

Next EUR 39,800 45%

Over EUR 80,000 48% A surtax is also applied during 2016 over all taxable income, at the following rates:

Taxable Income Tax Rates

First EUR 7,070 0%

Portugal

PKF Worldwide Tax Guide 2016/17 10

Taxable Income Tax Rates

Next EUR 12,930 1%

Next EUR 20,000 1.75%

Next EUR 40,000 3%

Over EUR 80,000 3.5% Furthermore, an additional solidarity tax applies to taxpayers with taxable income between EUR 80,000 and EUR 250,000, at the following rates:

Taxable Income Tax Rates

First 80,000 0%

Next 170,000 2.5%

Over 250,000 5% Domestic income may attract withholding income tax. Tax withheld from residents represents a payment on account of the recipient's ultimate tax liability. In other cases, such as interests on bank deposits or dividends the tax withheld represents the final tax, but the individuals have an option to include such income in the tax return, in which case it will be treated as payment on account. Special Tax Regime for Non-Regular Residents A special tax regime for non-regular residents is available. Individuals becoming tax residents and who have not been resident in Portugal for tax purposes for the past five years may apply for being covered by this regime. Under this regime, certain foreign-sourced income, such as investment income, capital gains, and pension income may be exempt from taxation in Portugal, if certain conditions are met, for a period of 10 years. In addition, non-regular residents may benefit from a reduced tax rate of 20% on Portuguese sourced employment and self-employment income, if derived from high value added activities performed in Portugal. Such activities are defined as those with a scientific, artistic or technical nature, including: engineers, architects, consultants, doctors, designers, tax university lecturers and artists. I. TREATY AND NON-TREATY WITHHOLDING TAX RATES

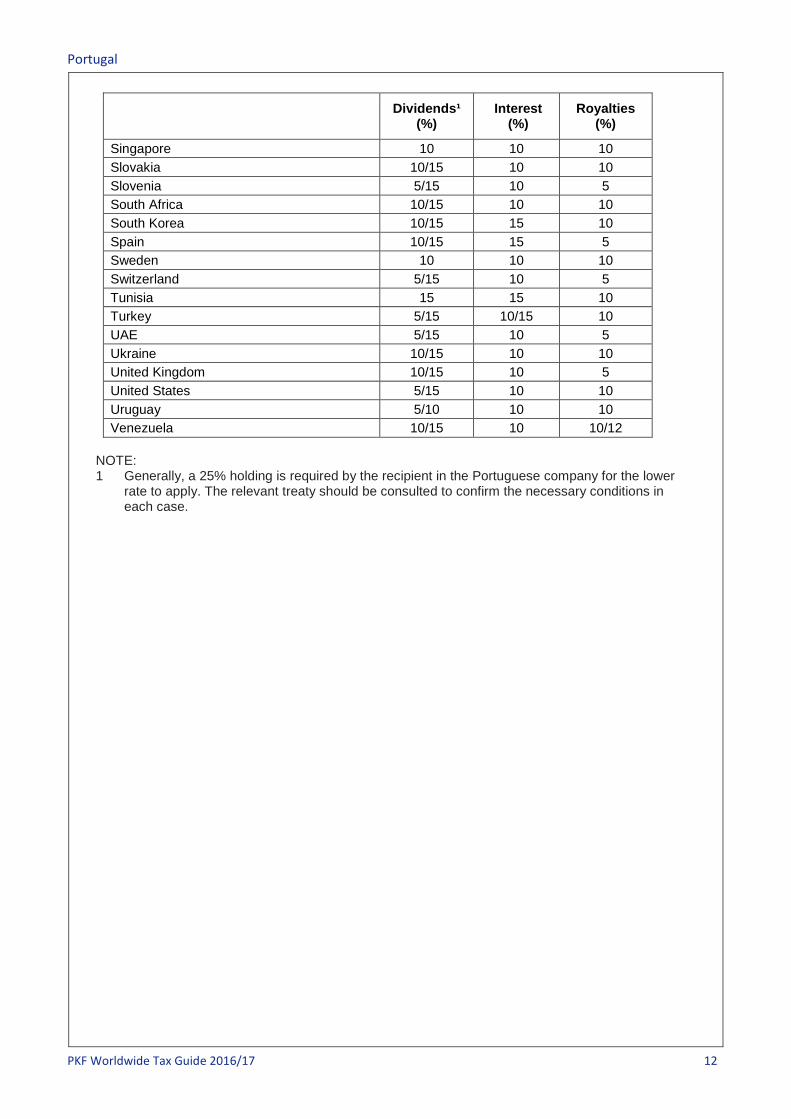

I. II. The following table is for general guidance only and reflects the lower of the treaty rate and the rate

under domestic tax law. The rates are applicable to payments by Portuguese companies to non-residents under the treaties currently in force.

Dividends¹ (%)

Interest (%)

Royalties (%)

Non-treaty countries: 25 25 26

Treaty countries: Algeria 15/10 15 10 Austria 15 10 5/10 Barbados 5/15 10 5 Belgium 15 15 10 Brazil 10/15 15 15 Bulgaria 10/15 10 10 Canada 15/10 10 10 Cape Verde 10 10 10 Chile 10/15 5/10 5/10

Portugal

PKF Worldwide Tax Guide 2016/17 11

Dividends¹ (%)

Interest (%)

Royalties (%)

China 10 10 10 Colombia 10 10 10 Croatia 5/10 10 10 Cuba 5/10 10 5 Cyprus 10 10 10 Czech Republic 10/15 10 10 Denmark 10 10 10 East Timor 5/10 10 10 Estonia 10 10 10 Ethiopia 5/10 10 5 Finland 10/15 15 10 France 15 10/12 5 Germany 15 10/15 10 Georgia 5/10 10 5 Greece 15 15 10 Guinea-Bissau 10 10 10 Hong Kong 5/10 10 5 Hungary 10/15 10 10 Iceland 10/15 10 10 India 10/15 10 10 Indonesia 10 10 10 Ireland 15 15 10 Israel 5/10/15 10 10 Italy 15 15 12 Japan 5/10 5/10 5 Korea, Republic of 10/15 15 10 Kuwait 5/10 10 10 Latvia 10 10 10 Lithuania 10 10 10 Luxembourg 15 10/15 10 Macau 10 10 10 Malta 10/15 10 10 Mexico 10 10 10 Moldova 10/5 10 8 Morocco 15/10 10 10 Mozambique 10 10 10 Netherlands 10 10 10 Norway 5/15 10 10 Pakistan 10/15 10 10 Panama 10/15 10 10 Peru 10/15 10/15 10/15 Poland 10/15 10 10 Qatar 5/10 10 10 Romania 10/15 10 10 Russia 10/15 10 10 San Marino 10/15 10 10 Senegal 5/10 10 10

Portugal

PKF Worldwide Tax Guide 2016/17 12

Dividends¹ (%)

Interest (%)

Royalties (%)

Singapore 10 10 10 Slovakia 10/15 10 10 Slovenia 5/15 10 5 South Africa 10/15 10 10 South Korea 10/15 15 10 Spain 10/15 15 5 Sweden 10 10 10 Switzerland 5/15 10 5 Tunisia 15 15 10 Turkey 5/15 10/15 10 UAE 5/15 10 5 Ukraine 10/15 10 10 United Kingdom 10/15 10 5 United States 5/15 10 10 Uruguay 5/10 10 10 Venezuela 10/15 10 10/12

NOTE: 1 Generally, a 25% holding is required by the recipient in the Portuguese company for the lower

rate to apply. The relevant treaty should be consulted to confirm the necessary conditions in each case.