portuguese real estate investment survey 3rd q 2017 · comparative analysis ... the preferred...

TRANSCRIPT

Portuguese Real Estate Investment Survey – 3rd Q 2017A positive outlook for Portuguese real estateDeloitte Consultores, S.A.

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 2

Portuguese Real Estate Investment Survey – 3rd Q 2017

Preface

It is with great pleasure that we launch the 3rd edition of Deloitte’s Portuguese Real Estate Investment Survey. This survey analyses the insights of a selected panel of participants who act in the Portuguese real estate sector.

Our goal is to better understand the Portuguese real estate dynamic trends, analysing the investment and disinvestment strategies according to current and future circumstances. We address financial and strategic topics concerning real estate business which we considered to be useful for understanding the dynamics of the industry.

This initiative’s success depended, above all, on the involvement and participation of the Selected Panel, whom we thank in advance for its proactive contribution by sharing their experience with us, allowing to identify the main trends of the sector’s development.

We are at your entire disposal to discuss any relevant question.

Carefully,

Jorge Marrão

Jorge Sousa Marrão

Partner

Real Estate Leader

3Presentation title[To edit, click View > Slide Master > Slide Master] > ERASE THIS CAPTION IN THE END

Main conclusions

23Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A.

4Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A.

Overall, respondents aim to focus in an investment strategy in opposition to the portfolio management and divestment

strategies.

Regarding divestment strategy, respondents are more keen in selling “Core” assets (50%). Respondents

perceives a greater ease in attracting investors for assets acquisition.

Value added investments (69%) are perceived as the preferred investment strategy by respondents, with a more

optimistic fundraising perception when it comes to finance acquisitions.

Banks and Sovereign funds (38% each) stand out as the main business feeders of real estate acquisitions, as capital sources will mainly arise from Europe

(75%).

Funds of Funds (50%) and Insurance Companies (43%) are identified as the

main real estate buyers in Portugal. Capital sources mainly arises from

Europe (86%).

Regarding to the Portuguese real estate market, there is a perception of an

increase in the volume and sales price for residential, retail/ services and hotel

sectors, and a greater stability of profitability rates.

Main conclusions

Portuguese Real Estate Investment Survey – 3rd Q 2017

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 5

Real Estate strategy for 2017 Portuguese real estate market

2nd Quarter 3rd Quarter

36%

27%

41% Disposal of "Core" assets

Divestment in “Opportunistic

deals” represents only 27%

Funds of Funds are the main real

state purchasers, with Pension

Funds (27%) becoming more

relevant

2nd Quarter 3rd Quarter

Investment Policy Divestment Policy

Comparative analysis

Portuguese Real Estate Investment Survey – 3rd Q 2017

27% Only 27% of the respondents

invest in “Value Added” assets

41% “Core” investments are the

most representative

41% Banks are the main business

feeders

73% Capital arising from Europe

Compared to the 2nd quarter of 2017, portfolio management and divestment strategies lost their representativeness for the benefit of a investment strategy.

Respondents maintain the perception of an increase in the volume and sales

price for residential, retail/ services and hotel sectors, related to a greater

stability in the profitability rates.

77% Capital arising from Europe

69% “Value added” investments are

the most representative

44% 44% of the respondents invest in

“Core” assets

38% Banks e Sovereign funds are the

main business feeders

75% Capital arising from Europe

50%

29%

50% Disposal of “Core” assets

Divestment in “Opportunistic

deals” represents only 29%

Funds of Funds are the main real

state purchasers, with Insurance

companies (43%) becoming more

relevant

86% Capital arising from Europe

6Presentation title[To edit, click View > Slide Master > Slide Master] > ERASE THIS CAPTION IN THE END

Introduction

23Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A.

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 7

Portuguese Real Estate Investment Survey – 3rd Q 2017

Real Estate Asset Management Companies and Corporate Companies represent together 63% of the respondents.

Type of organization that respondents represent

13%Banks

19%Corporate

Companies

44%Real Estate Asset

Management

Companies

6%Private Equity

6%Insurance

companies

12%Others

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 8

Portuguese Real Estate Investment Survey – 3rd Q 2017

Real Estate strategy for 2017

For 2017, the preferred strategy option is the investment with 44%, followed by portfolio management and divestment strategy each representing 31% and 25%, respectively.

Strategy

Divestment

Portfolio management

Investment

44%

31%

25%

9Presentation title[To edit, click View > Slide Master > Slide Master] > ERASE THIS CAPTION IN THE END

Investment strategy

23Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A.

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 10

38%

25%

69%

44%

31%

50%

Current Future

Portuguese Real Estate Investment Survey – 3rd Q 2017

Current and future investment strategy (1)

In both current and future strategies, respondents foresee that the most favourable strategy is the investment in Value Added assets representing 50% and 69%, respectively.

(1) Multiple choice question

Value added

Core

Opportunistic

deals

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 11

Portuguese Real Estate Investment Survey – 3rd Q 2017

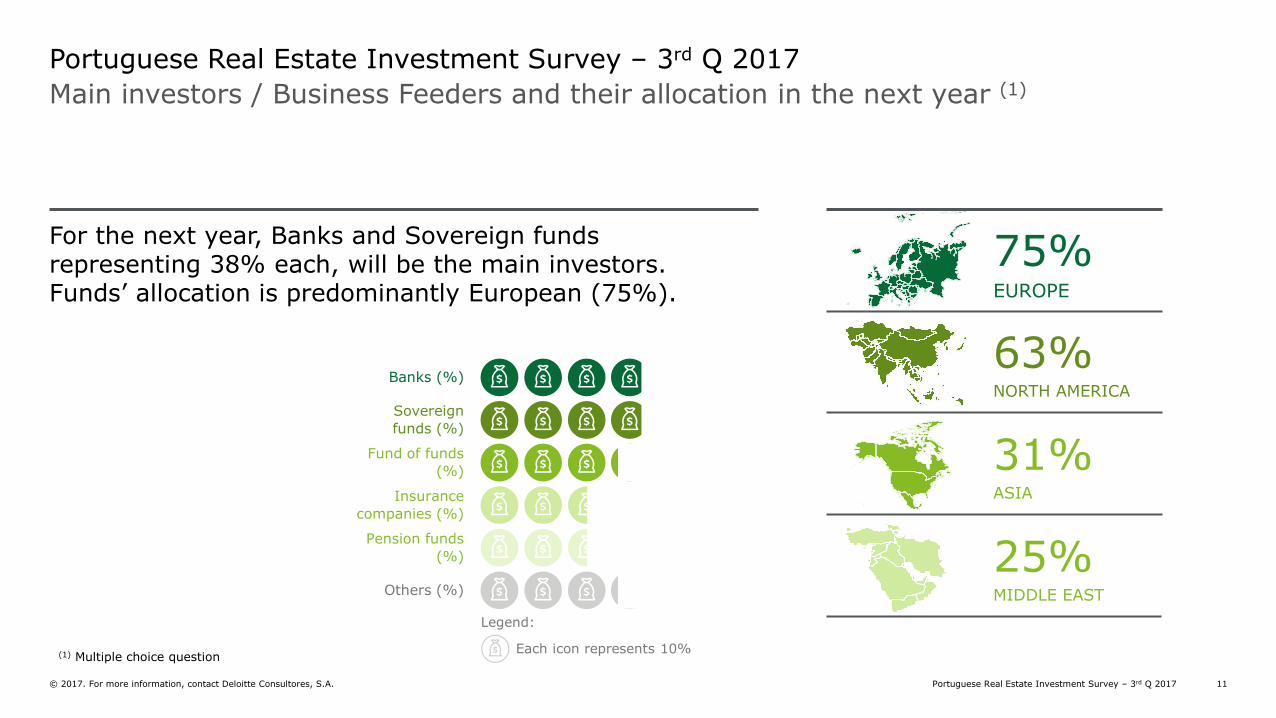

Main investors / Business Feeders and their allocation in the next year (1)

For the next year, Banks and Sovereign funds representing 38% each, will be the main investors. Funds’ allocation is predominantly European (75%).

(1) Multiple choice question

75%EUROPE

63%NORTH AMERICA

31%ASIA

25%MIDDLE EAST

Banks (%)

Sovereign

funds (%)

Fund of funds

(%)

Insurance

companies (%)

Pension funds

(%)

Others (%)

Legend:

Each icon represents 10%

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 12

Portuguese Real Estate Investment Survey – 3rd Q 2017

Fundraising approach, in the last 12 months and next 12 months

Fundraising perception for the next 12 months is slightly more optimistic compared to the last 12 months.

Difficult

Neutral

Easy

Last 12 months Next 12 months

38%

44%

18%

31%

25%

44%

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 13

12%

Low

69%

Significant

Portuguese Real Estate Investment Survey – 3rd Q 2017

Level of impact of the different factors affecting fundraising

Size of funds, range of investors and length of process are the most relevant factors affecting fundraising.19%

Very significant

Size of funds

Range of investors

13%

Very significant

31%

Low

56%

Significant

0%

Meaningless

31%

Low

56%

Significant

13%

Very significant

Length of process

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 14

Portuguese Real Estate Investment Survey – 3rd Q 2017

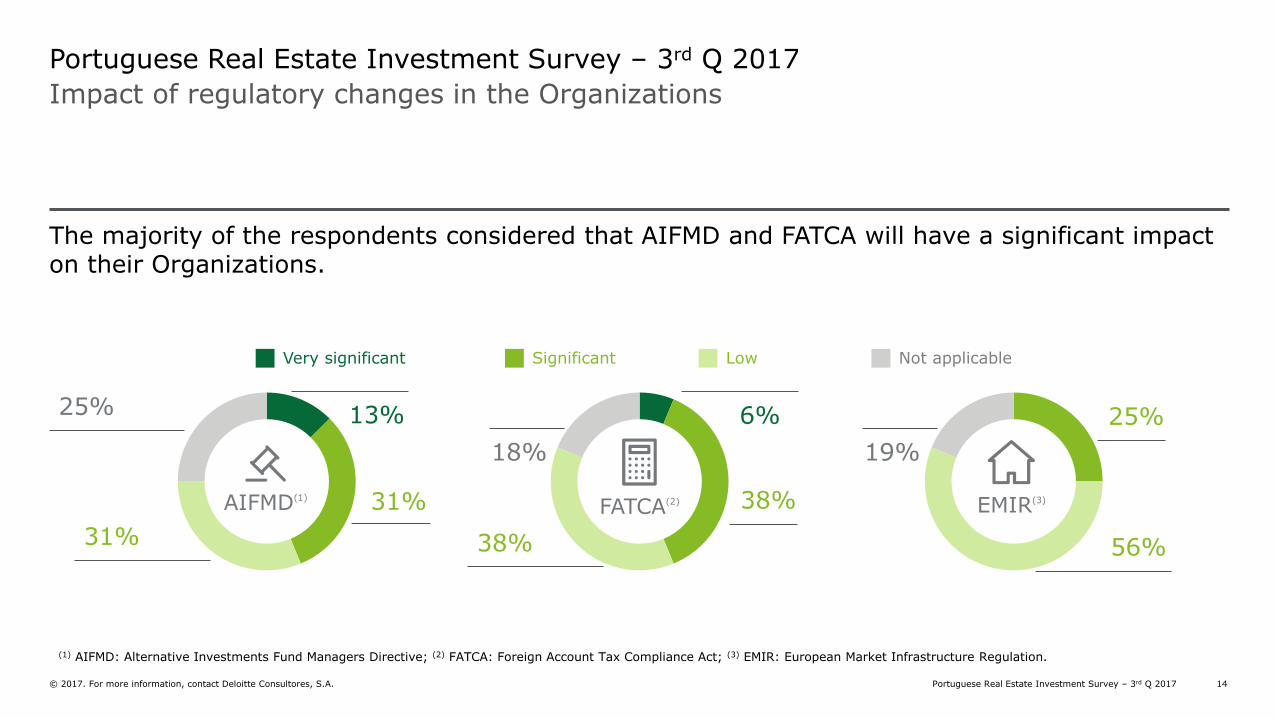

Impact of regulatory changes in the Organizations

The majority of the respondents considered that AIFMD and FATCA will have a significant impact on their Organizations.

(1) AIFMD: Alternative Investments Fund Managers Directive; (2) FATCA: Foreign Account Tax Compliance Act; (3) EMIR: European Market Infrastructure Regulation.

AIFMD(1)

FATCA(2) EMIR(3)

Very significant Significant Low Not applicable

25%

38%

25%

56%

18% 19%

13%

31%

31% 38%

6%

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 15

Portuguese Real Estate Investment Survey – 3rd Q 2017

Length of the real estate assets’ acquisition process

In general, real estate assets’ acquisition process takes from 3 to 6 months.

56%From 3 to 6

months

31%From 6 to 12

months

13%Up to 3

months

16Presentation title[To edit, click View > Slide Master > Slide Master] > ERASE THIS CAPTION IN THE END

Divestment strategy

23Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A.

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 17

50%

29%

50%

50%

36%

29%

Current Future

Portuguese Real Estate Investment Survey – 3rd Q 2017

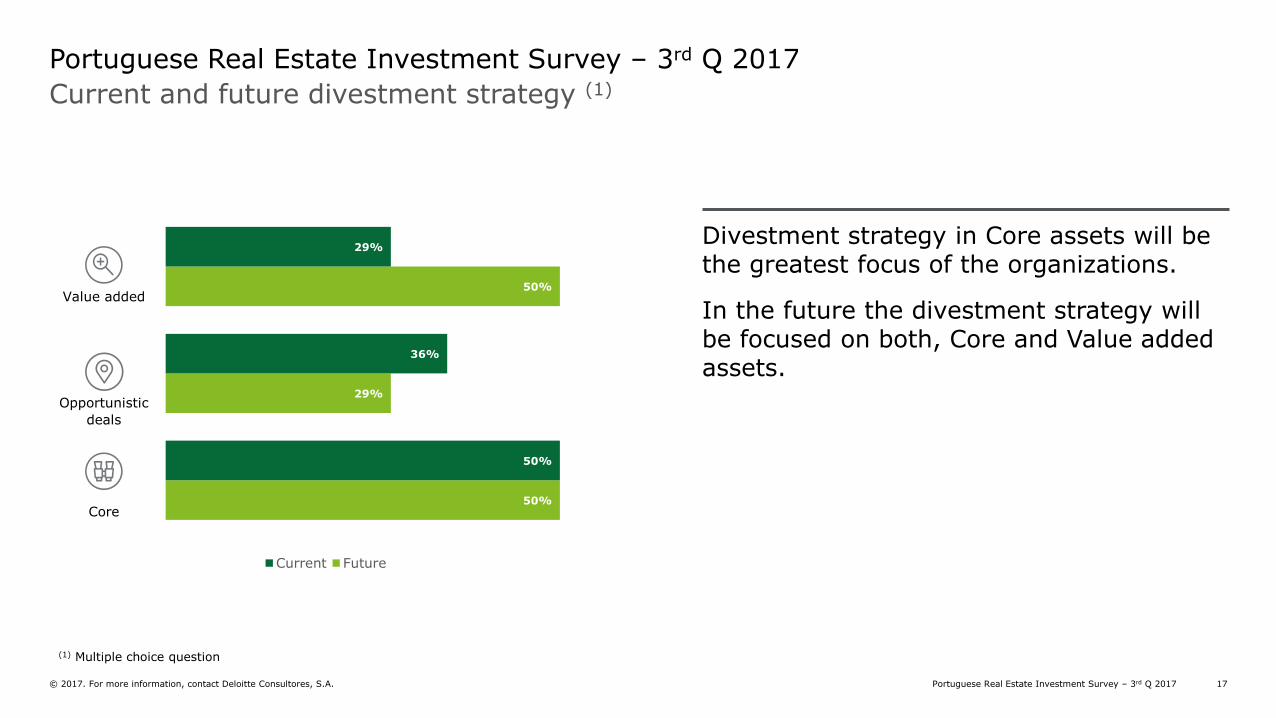

Current and future divestment strategy (1)

Divestment strategy in Core assets will be the greatest focus of the organizations.

In the future the divestment strategy will be focused on both, Core and Value added assets.

Value added

Opportunistic

deals

Core

(1) Multiple choice question

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 18

Europe with 86%, will be the main real estate investment player, followed by North America with 57%.

(1) Multiple choice question.

Fund of funds

(%)

Insurance

companies (%)

Pension funds

(%)

Banks (%)

Sovereign funds

(%)

Others (%)

Legend:

Each icon represents 10%

Portuguese Real Estate Investment Survey – 3rd Q 2017

Main real estate investors and their allocation in the next year (1)

For the next year, Fund of Funds represent 50% of the main real estate investors/ buyers for entities seeking to divest.

86%EUROPE

57%NORTH AMERICA

36%ASIA

21%MIDDLE EAST

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 19

Last 12 months Next 12 months

Difficult

Neutral

Easy

Portuguese Real Estate Investment Survey – 3rd Q 2017

Fundraising approach, in the last 12 months and next 12 months

For the next 12 months, with regard to investors attraction for the acquisition of real estate assets, respondents perceive a greater easiness.

36%

36%

28%

50%

29%

21%

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 20

14%

Low

72%

Significant

Portuguese Real Estate Investment Survey – 3rd Q 2017

Level of impact of different factors affecting fundraising

The size of funds and length of process are the most relevant factors affecting fundraising.

The range of investors has an increasingly smaller impact on this process.

22%

Low

64%

Significant

14%

Very significant

Length of process

14%

Very significant

Size of funds

Range of investors

0%

Very significant

43%

Low

57%

Significant

0%

Meaningless

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 21

Portuguese Real Estate Investment Survey – 3rd Q 2017

Impact of regulatory changes in the Organizations

AIFMD and EMIR will, in general, have a low impact in the divestment of the organizations. FATCA will have a more significant impact in these operations.

Very significant Significant Low Not applicable

(1) AIFMD: Alternative Investments Fund Managers Directive; (2) FATCA: Foreign Account Tax Compliance Act; (3) EMIR: European Market Infrastructure Regulation.

36%

21%

36% 36%

14%

36%

21%

29%

43%AIFMD(1)

FATCA(2) EMIR(3)

14%

14%

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 22

Portuguese Real Estate Investment Survey – 3rd Q 2017

Length of the real estate assets’ selling process

In general, the real estate assets’ selling process takes from 3 to 12 months.

7%More than

12 months

50%From 3 to 6

months43%From 6 to 12

months

23Presentation title[To edit, click View > Slide Master > Slide Master] > ERASE THIS CAPTION IN THE END

Real Estate valuations

23Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A.

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 24

14%Reposition Cost

29%Capitalization

57%Comparative

Real Estate valuation methods (1)

The most used valuation method for land and other uses is the DCF.

Portuguese Real Estate Investment Survey – 3rd Q 2017

(1) Multiple choice question

64%DCF

0%Reposition Cost

7%Capitalization

Land

71%DCF

Other uses

57%Comparative

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 25

Portuguese Real Estate Investment Survey – 3rd Q 2017

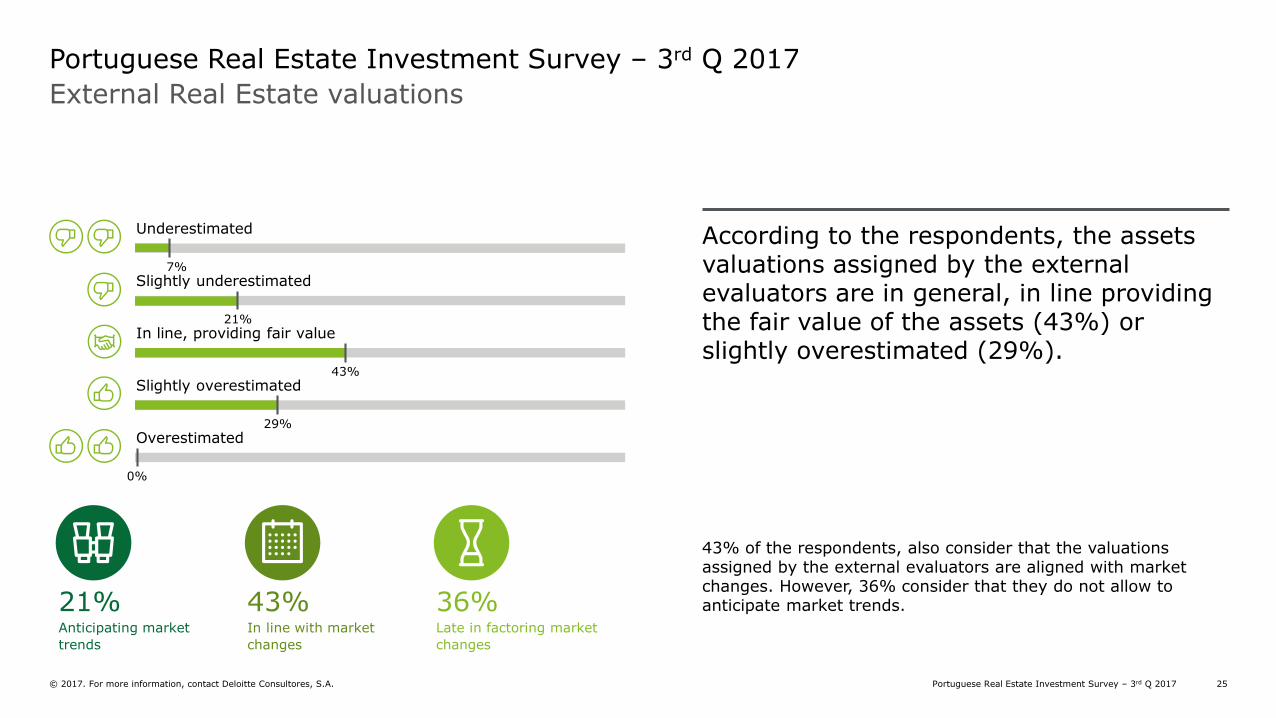

External Real Estate valuations

According to the respondents, the assets valuations assigned by the external evaluators are in general, in line providing the fair value of the assets (43%) or slightly overestimated (29%).

43% of the respondents, also consider that the valuations assigned by the external evaluators are aligned with market changes. However, 36% consider that they do not allow to anticipate market trends.21%

Anticipating market

trends

43%In line with market

changes

36%Late in factoring market

changes

Underestimated

Slightly underestimated

In line, providing fair value

Slightly overestimated

Overestimated

7%

21%

43%

29%

0%

26Presentation title[To edit, click View > Slide Master > Slide Master] > ERASE THIS CAPTION IN THE END

Real Estate market in Portugal

23Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A.

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 27

Portuguese Real Estate Investment Survey – 3rd Q 2017

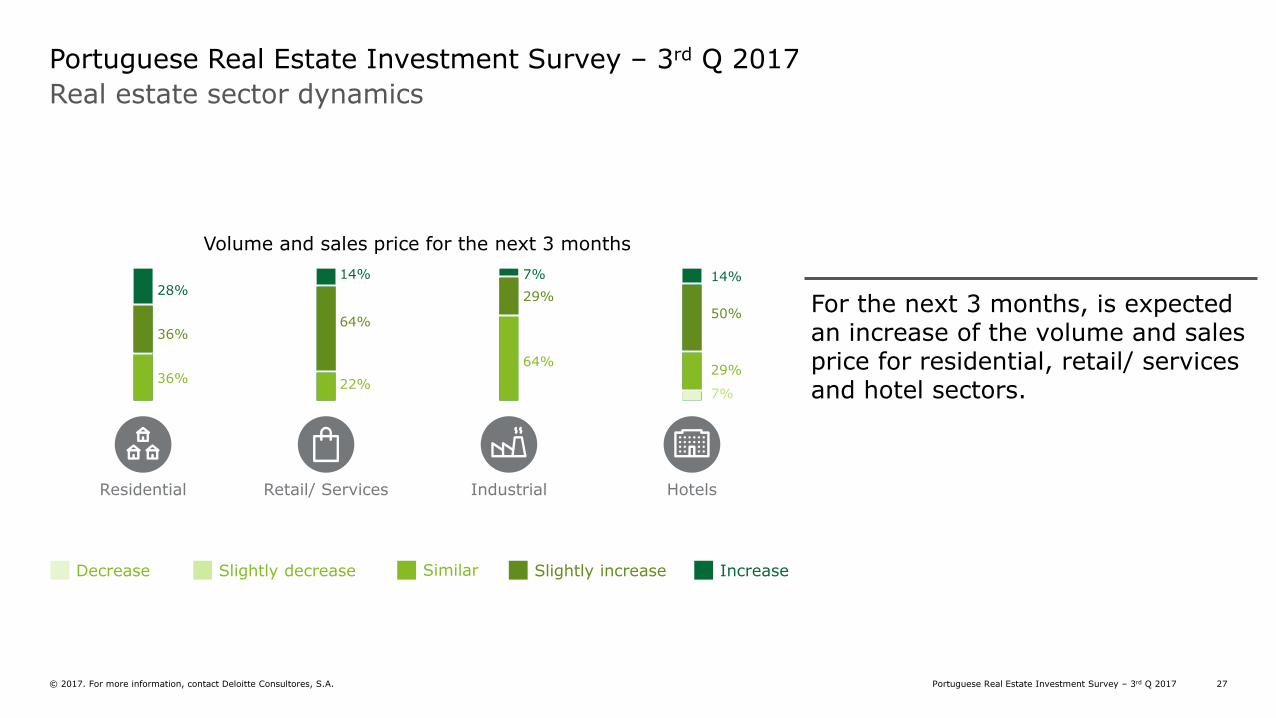

Real estate sector dynamics

Volume and sales price for the next 3 months

For the next 3 months, is expected an increase of the volume and sales price for residential, retail/ services and hotel sectors.

Decrease Slightly decrease Similar Slightly increase Increase

HotelsRetail/ ServicesResidential Industrial

28%

36%

36%

14%

64%

22%

14%

50%

29%

7%

29%

64%

7%

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 28

Portuguese Real Estate Investment Survey – 3rd Q 2017

Real Estate sector dynamics

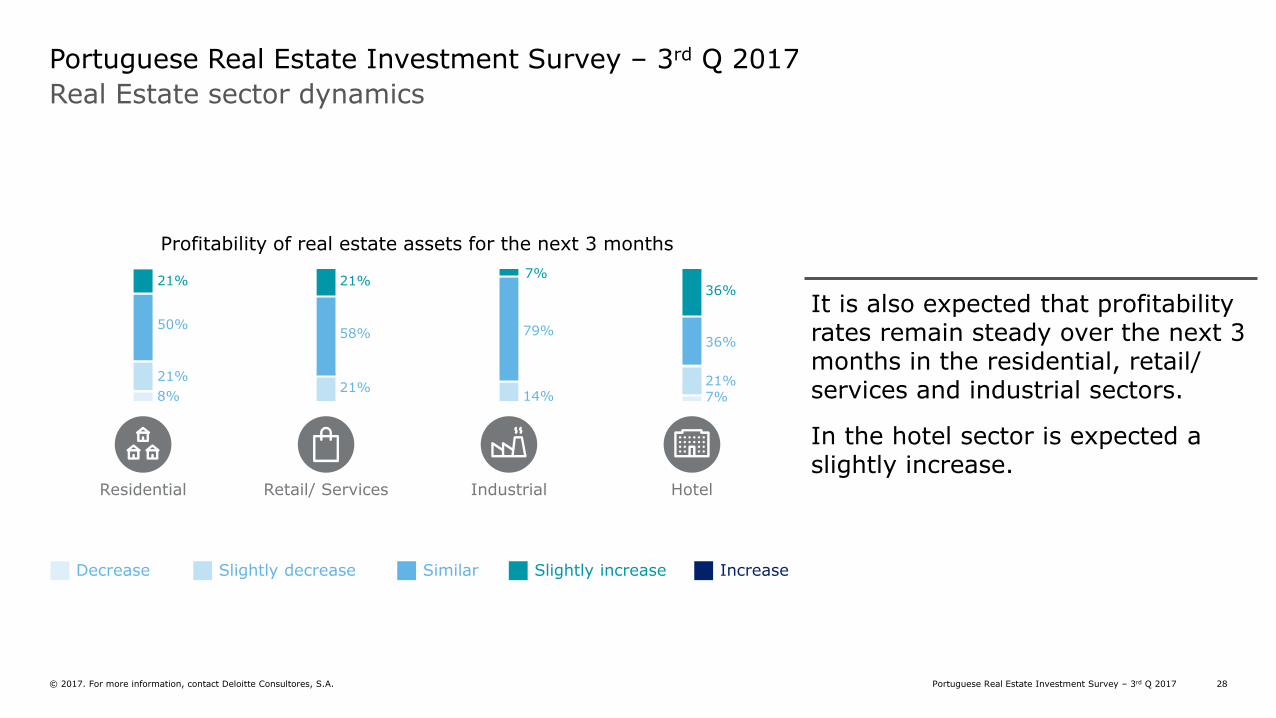

Profitability of real estate assets for the next 3 months

It is also expected that profitability rates remain steady over the next 3 months in the residential, retail/ services and industrial sectors.

In the hotel sector is expected a slightly increase.

HotelRetail/ ServicesResidential Industrial

Decrease Slightly decrease Similar Slightly increase Increase

21%

50%

21%

21%

58%

21%

14%

79%

21%

36%

36%

8%

7%

7%

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 29

New players

entranceBureaucracy Tax policy Political

situation

Demand Supply Foreign

investment

Positive

Negative

Neutral

Portuguese Real Estate Investment Survey – 3rd Q 2017

Impact of several variables in the Real Estate sector

For the next 3 months, the respondents consider that supply and foreign investment will have a positive impact in the real estate sector.

Political situation will gain representation in the positive impact that generates.

28%

36%

29%7%

36%

93% 71%

7%

57%

21%

71%

43%

57%

7%

57%36%

36%

Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A. 30

Technical Note

Portuguese Real Estate Investment Survey – 3rd Q 2017

The Portuguese Real Estate Investment Survey’s main goal is to assess:

• The perception of the real estate market evolution by the involved parties; and

• Understand which is the current and future strategy of the organizations.

The survey was sent to a Selected Panel of Participants on 21st September, the answers were obtain on 3rd October, and were subject to analysis.

In case of doubt, some additional information or any clarification, please contact:

Jorge Sousa MarrãoPartnerTlm.: +(351) 963 902 674Tel.: +(351) 210 422 [email protected]

Inês Cintra CostaManagerTlm.: +(351) 962 103 923Tel.: +(351) 210 427 [email protected]

31Portuguese Real Estate Investment Survey – 3rd Q 2017© 2017. For more information, contact Deloitte Consultores, S.A.

Contacts

Miguel Paiva Couceiro

Manager

Real Estate – Financial Advisory

Deloitte Portugal

Tlm. +(351) 917 240 884

Tel. +(351) 210 422 500

Jorge Sousa Marrão

Partner

Real Estate Leader

Deloitte Portugal

Tlm. +(351) 963 902 674

Tel. +(351) 210 422 503

Ricardo Reis

Partner

Real Estate - Tax

Deloitte Portugal

Tlm. +(351) 964 736 261

Tel. +(351) 210 427 564

Inês Cintra Costa

Manager

Real Estate – Financial Advisory

Deloitte Portugal

Tlm. +(351) 962 103 923

Tel. +(351) 210 422 500

Diogo Pires

Senior Manager

Real Estate - Tax

Deloitte Portugal

Tlm. +(351) 964 837 258

Tel. +(351) 210 427 541

© 2017. For more information, contact Deloitte Consultores, S.A.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about to learn more about our global network of member firms.

Deloitte provides audit, consulting, financial advisory, risk advisory, tax and related services to public and private clients spanning multiple industries. Deloitte serves four out of five Fortune Global 500® companies through a globally connected network of member firms in more than 150 countries bringing, world-class capabilities, insights, and high-quality service to address clients' most complex business challenges. To learn more about how Deloitte's approximately 245,000 professionals make an impact that matters, please connect with us on Facebook, LinkedIn or Twitter.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.