post conference 2009-mosl-co-part1-finalconference.motilaloswal.com/reports/agic2009.pdfdevelop...

TRANSCRIPT

Company ConnectKey takeaways from conference interactions

Research [email protected]

The companies which participated in the Motilal Oswal 5thAnnual Global Investor Conference offer a healthy varietyin terms of sector, size, geography, business model, etc.

One thing is common though: together, these companies formthe creamy layer of India’s capital markets. The 70 companiesare less than 2.5% of the total 3,000+ listed companies inIndia. But they account for 40% of sales, 57% of profitand 50% of India’s total listed market cap.

The following pages provide key takeaways from ourinteractions with these companies. We believe that many ofthese will be a significant beneficiary of India’s Next TrillionDollar opportunity.

2August 3 - 5, 2009

5th Annual Global Investor Conference

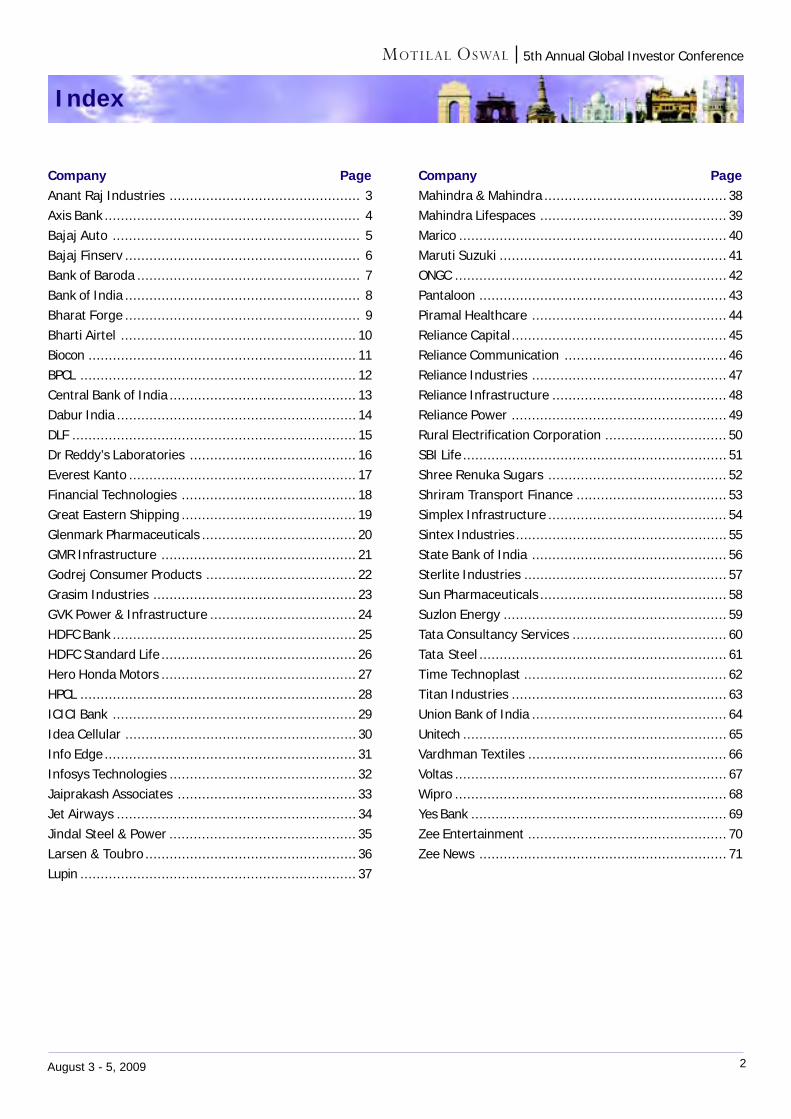

Company PageAnant Raj Industries ............................................... 3Axis Bank ............................................................... 4Bajaj Auto ............................................................. 5Bajaj Finserv .......................................................... 6Bank of Baroda ....................................................... 7Bank of India .......................................................... 8Bharat Forge .......................................................... 9Bharti Airtel .......................................................... 10Biocon .................................................................. 11BPCL .................................................................... 12Central Bank of India .............................................. 13Dabur India ........................................................... 14DLF ...................................................................... 15Dr Reddy’s Laboratories ......................................... 16Everest Kanto ........................................................ 17Financial Technologies ........................................... 18Great Eastern Shipping ........................................... 19Glenmark Pharmaceuticals ...................................... 20GMR Infrastructure ................................................ 21Godrej Consumer Products ..................................... 22Grasim Industries .................................................. 23GVK Power & Infrastructure .................................... 24HDFC Bank ............................................................ 25HDFC Standard Life ................................................ 26Hero Honda Motors ................................................ 27HPCL .................................................................... 28ICICI Bank ............................................................ 29Idea Cellular ......................................................... 30Info Edge .............................................................. 31Infosys Technologies .............................................. 32Jaiprakash Associates ............................................ 33Jet Airways ........................................................... 34Jindal Steel & Power .............................................. 35Larsen & Toubro .................................................... 36Lupin .................................................................... 37

Company PageMahindra & Mahindra ............................................. 38Mahindra Lifespaces .............................................. 39Marico .................................................................. 40Maruti Suzuki ........................................................ 41ONGC ................................................................... 42Pantaloon ............................................................. 43Piramal Healthcare ................................................ 44Reliance Capital ..................................................... 45Reliance Communication ........................................ 46Reliance Industries ................................................ 47Reliance Infrastructure ........................................... 48Reliance Power ..................................................... 49Rural Electrification Corporation .............................. 50SBI Life ................................................................. 51Shree Renuka Sugars ............................................ 52Shriram Transport Finance ..................................... 53Simplex Infrastructure ............................................ 54Sintex Industries .................................................... 55State Bank of India ................................................ 56Sterlite Industries .................................................. 57Sun Pharmaceuticals .............................................. 58Suzlon Energy ....................................................... 59Tata Consultancy Services ...................................... 60Tata Steel ............................................................. 61Time Technoplast .................................................. 62Titan Industries ..................................................... 63Union Bank of India ................................................ 64Unitech ................................................................. 65Vardhman Textiles ................................................. 66Voltas ................................................................... 67Wipro ................................................................... 68Yes Bank ............................................................... 69Zee Entertainment ................................................. 70Zee News ............................................................. 71

Index

3August 3 - 5, 2009

5th Annual Global Investor Conference

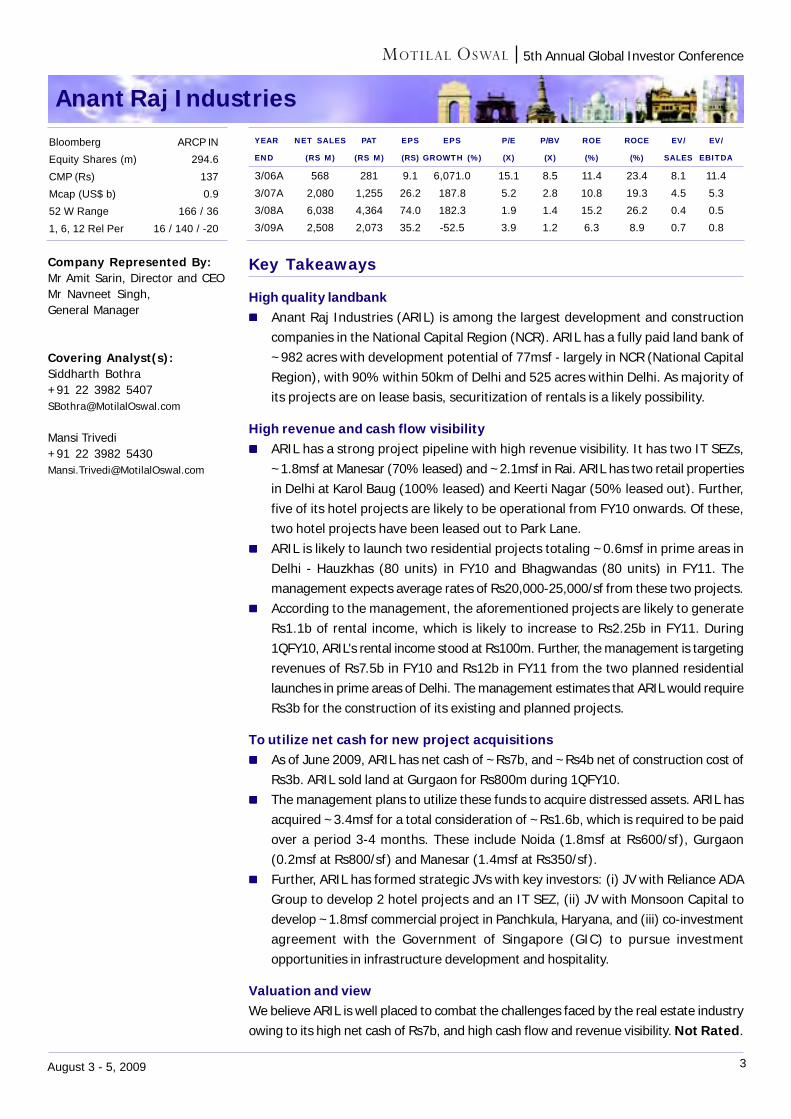

Anant Raj Industries

Key Takeaways

High quality landbankAnant Raj Industries (ARIL) is among the largest development and constructioncompanies in the National Capital Region (NCR). ARIL has a fully paid land bank of~982 acres with development potential of 77msf - largely in NCR (National CapitalRegion), with 90% within 50km of Delhi and 525 acres within Delhi. As majority ofits projects are on lease basis, securitization of rentals is a likely possibility.

High revenue and cash flow visibilityARIL has a strong project pipeline with high revenue visibility. It has two IT SEZs,~1.8msf at Manesar (70% leased) and ~2.1msf in Rai. ARIL has two retail propertiesin Delhi at Karol Baug (100% leased) and Keerti Nagar (50% leased out). Further,five of its hotel projects are likely to be operational from FY10 onwards. Of these,two hotel projects have been leased out to Park Lane.ARIL is likely to launch two residential projects totaling ~0.6msf in prime areas inDelhi - Hauzkhas (80 units) in FY10 and Bhagwandas (80 units) in FY11. Themanagement expects average rates of Rs20,000-25,000/sf from these two projects.According to the management, the aforementioned projects are likely to generateRs1.1b of rental income, which is likely to increase to Rs2.25b in FY11. During1QFY10, ARIL's rental income stood at Rs100m. Further, the management is targetingrevenues of Rs7.5b in FY10 and Rs12b in FY11 from the two planned residentiallaunches in prime areas of Delhi. The management estimates that ARIL would requireRs3b for the construction of its existing and planned projects.

To utilize net cash for new project acquisitionsAs of June 2009, ARIL has net cash of ~Rs7b, and ~Rs4b net of construction cost ofRs3b. ARIL sold land at Gurgaon for Rs800m during 1QFY10.The management plans to utilize these funds to acquire distressed assets. ARIL hasacquired ~3.4msf for a total consideration of ~Rs1.6b, which is required to be paidover a period 3-4 months. These include Noida (1.8msf at Rs600/sf), Gurgaon(0.2msf at Rs800/sf) and Manesar (1.4msf at Rs350/sf).Further, ARIL has formed strategic JVs with key investors: (i) JV with Reliance ADAGroup to develop 2 hotel projects and an IT SEZ, (ii) JV with Monsoon Capital todevelop ~1.8msf commercial project in Panchkula, Haryana, and (iii) co-investmentagreement with the Government of Singapore (GIC) to pursue investmentopportunities in infrastructure development and hospitality.

Valuation and viewWe believe ARIL is well placed to combat the challenges faced by the real estate industryowing to its high net cash of Rs7b, and high cash flow and revenue visibility. Not Rated.

Company Represented By:Mr Amit Sarin, Director and CEOMr Navneet Singh,General Manager

Covering Analyst(s):Siddharth Bothra+91 22 3982 [email protected]

Mansi Trivedi+91 22 3982 [email protected]

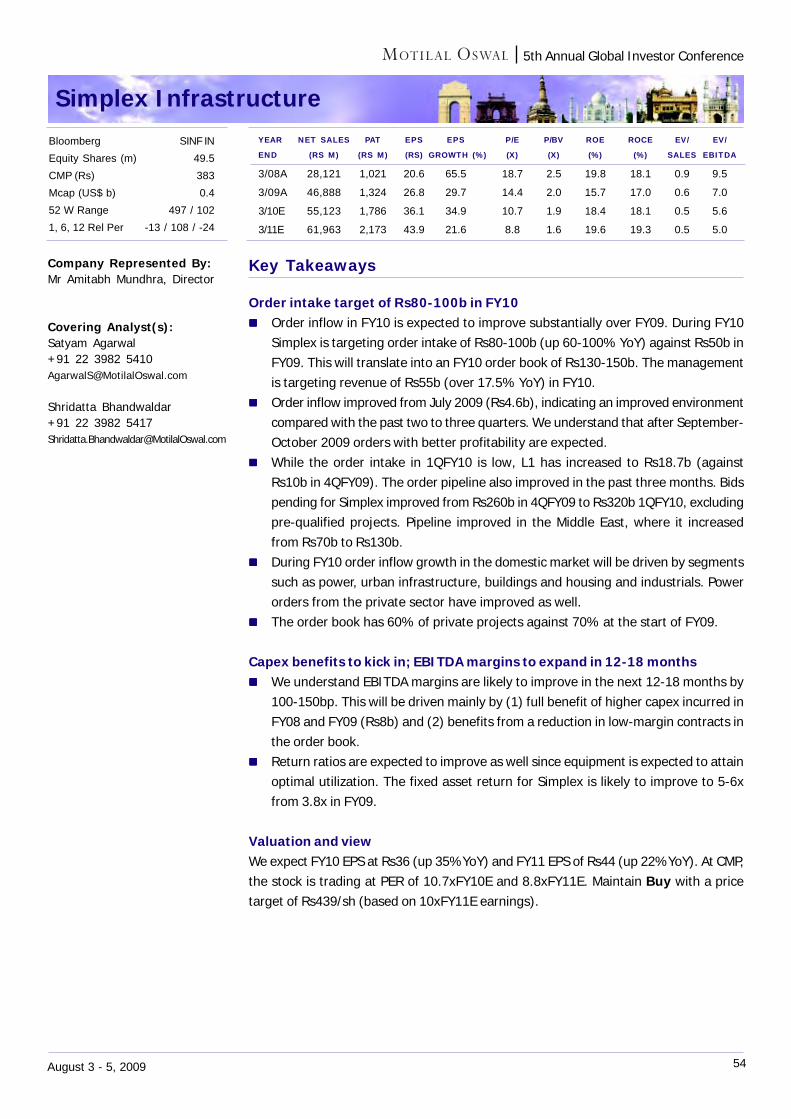

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

3/06A 568 281 9.1 6,071.0 15.1 8.5 11.4 23.4 8.1 11.43/07A 2,080 1,255 26.2 187.8 5.2 2.8 10.8 19.3 4.5 5.33/08A 6,038 4,364 74.0 182.3 1.9 1.4 15.2 26.2 0.4 0.53/09A 2,508 2,073 35.2 -52.5 3.9 1.2 6.3 8.9 0.7 0.8

Bloomberg ARCP INEquity Shares (m) 294.6CMP (Rs) 137Mcap (US$ b) 0.952 W Range 166 / 361, 6, 12 Rel Per 16 / 140 / -20

4August 3 - 5, 2009

5th Annual Global Investor Conference

Axis Bank

Key Takeaways

Growth outlook moderatedManagement sees industry loans growing 16-17% in FY10. Axis Bank aims to growits loan book at 20-25% instead of 25% as announced earlier. While sanctions arepicking up, disbursals could take longer.Infrastructure, cement, steel are likely to lead the growth based on existing sanctionsavailable. On the retail book, mortgages and car financing are the loan growthdrivers.While the yield on funds is expected to fall (due to pressure on loan growth andpricing), margins will stay at 3.25-3.5% as a fall in the cost of funds is expected tocompensate for falling yields.Management believes it can sustain a CASA ratio at 40% going forward.The borrower-wise outstanding restructured loan book was Rs22.6b or 2.9% of theloan book in June 2009. This number will rise in 2QFY10. Corporates including SME,comprise 90% of the restructured loans spread across 200 accounts.Management believes fee income will grow at least in line with loan-growth. Themanagement targets a cost-to-income ratio of 40-45% against 45-50% earlier.By the end of FY10, Tier-I CAR is seen falling to 8% from 9.4% currently.

Valuation and viewWe expect Axis Bank to report EPS of Rs60 in FY10 and Rs73 in FY11. BV will be Rs333in FY10E and Rs392 in FY11E. ABV is expected to be Rs318 in FY10E and Rs370 inFY11E. RoA and RoE are seen to be strong at 1.3% and more than 19% over FY10-11E.Maintain Buy with a target price of Rs980 (2.5x FY11E BV).

Company Represented By:Mr Somnath Sengupta,President-Finance and AccountsMr Shishir Mankad,VP - Finance and Accounts

Covering Analyst(s):Ajinkya Dhavale+91 22 3982 [email protected]

Alpesh Mehta+91 22 3982 [email protected]

YEAR NET INCOME PAT EPS EPS P/E P/BV CAR ROAE ROAA P/ABV

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) (%) (X)

3/08A 43,808 10,710 29.9 28.0 28.4 3.5 13.7 17.6 1.2 3.5

3/09A 65,831 18,154 50.6 68.9 16.8 3.0 13.7 19.1 1.4 3.1

3/10E 81,507 21,554 60.0 18.7 14.2 2.6 12.4 19.4 1.3 2.7

3/11E 97,259 26,082 72.7 21.0 11.7 2.2 11.4 20.0 1.3 2.3

Bloomberg AXSB INEquity Shares (m) 357.7CMP (Rs) 851Mcap (US$ b) 6.452 W Range 974 / 2781, 6, 12 Rel Per -6 / 42 / 6

5August 3 - 5, 2009

5th Annual Global Investor Conference

Bajaj Auto

Key Takeaways

Product launches may drive volume growthBajaj Auto expects to post double-digit volume growth in FY10.It sees flat-to-marginally positive export volumes.Management hopes volume will be driven by new products such as Pulsar (35-40,000/month) and Discover 100 (25,000/month).Higher three-wheeler volume and the planned launch of three-wheeler goods andpassenger vehicles will support volumes.

EBITDA margins sustainable1QFY10 EBITDA margin improvement of 430bp QoQ (800bp YoY) to 19.5% wasdriven by higher hedged forex rate and higher operating leverage.The company has secured steel contracts until December as it entered into freshcontracts from July 1, which gave it a price rise of 2-3%. On aluminum it hascontracts until September 09.Hence EBITDA margins will be sustainable in 2QFY10.But the launch of the 100cc "volume" bike will dilute margins from 1QFY10 levels asit will earn lower-than-average margins.

Sees ramp-up at PantnagarBajaj Auto plans to ramp-up operations at its Pantnagar plant, where it enjoys fiscalincentives.From 41,000 units in April 09, it is targeting a ramp-up to 60,000/month (1,15,000units in 1QFY10).It makes the Platina, Platina 125 and XCD 135 at Pantnagar. It plans to produce 50%of its "volume" bike at Pantnagar and the rest at Chakan.

Other takeawaysFinance availability for two-wheelers not improved. Out of the 25% of vehicles soldon credit, Bajaj Auto Finance financed most of them.Indonesian operations, which lost Rs600m in FY09 (Rs110m loss in 1QFY10), isseen to break even in FY11.Focus on the African market, where competition comes from Chinese firms.Plans to boost market share by increasing investment in advertising, marketing anddistribution.

Valuations and viewVolume recovery in domestic and exports, coupled with higher hedged forex rates willboost profitability. Higher volumes and market share recovery will be a catalyst for thestock. It trades at 15.5x FY10E EPS and 14.5x FY11E EPS. Maintain Buy.

Company Represented By:Mr Kevin D'sa, VP - Finance

Covering Analyst(s):Jinesh Gandhi+91 22 3982 [email protected]

Bloomberg BJAUT INEquity Shares (m) 144.7CMP (Rs) 1,283Mcap (US$ b) 3.952 W Range 1358 / 2621, 6, 12 Rel Per 21 / 107 / 136

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

3/08A 90,462 8,241 57.0 20.2 10.5 51.9 42.4 1.8 12.4

3/09A 88,104 7,963 55.0 -3.4 23.3 11.0 47.2 36.3 2.1 15.3

3/10E 97,963 11,994 82.9 50.6 15.5 7.4 47.9 43.7 1.8 9.8

3/11E 105,177 12,828 88.7 6.9 14.5 5.5 38.1 38.5 1.6 8.9

6August 3 - 5, 2009

5th Annual Global Investor Conference

Bajaj Finserv

Key Takeaways

Life insurance business (Bajaj Allianz Life Insurance)The company will continue to focus on profitability and operational/capital efficiencyrather than market share. Over a longer period, it believes that 15-20% RoE ispossible from this business. While its reported NBAP is ~19%, it is having an expenseunder run currently.Private life insurance companies are expected to grow 10-15% annually. Bajaj AllianzLife Insurance would be content to consolidate for one or two years as the industryrationalizes before growing in double digits.Bajaj Allianz's business model includes: (1) higher exposure to low ticket sizes andTier III/IV cities, and (2) low cost working. The management believes this makes itsproposition unique for sustaining the downturn.The company expects distributors' commissions to decline so that the customergets the best return in the final analysis.Bajaj Allianz Life Insurance does not foresee strong competition from newer playersas ability to burn capital will be a constraint for them.

General insurance business (Bajaj Allianz General Insurance)Bajaj Allianz General Insurance will continue to focus on profitable motor and healthinsurance products.In the near term, the company will focus upon preserving profitability, maintainingmarket share and effectively utilizing capital.

Bajaj Auto FinanceThe company will focus on gradual pace of organic growth. It has also tightenedcredit standards.The company will also launch construction equipment finance business.For improving profitability the company plans to: (1) focus on reducing operatingexpenses, (2) explore portfolio acquisition (to leverage capital), and (3) cross-sellproducts.

Company Represented By:Mr Sanjiv Bajaj, MDMr Ranjit Gupta, President (Ins)Mr S Sreenivasan, CFO (Gen. Ins)

Covering Analyst(s):Ajinkya Dhavale+91 22 3982 [email protected]

Alpesh Mehta+91 22 3982 [email protected]

7August 3 - 5, 2009

5th Annual Global Investor Conference

Bank of Baroda

Key Takeaways

Focus on qualitative growthThe management is confident of growing assets at a pace higher than industry. Thebank's FY10 loan growth is seen at 22%.CASA remains the key focus area and management is reluctant to fund asset growththrough bulk deposits. BoB's CASA ratio at 35% and CASA growth at 18-20% is oneof the best among its peers.The 1QFY10 margin decline (2.37% from 2.91% in 4QFY09), is an aberration, not atrend. With loan growth picking up and downward re-pricing of deposits, managementis sure of achieving sustainable 2.7% NIM by FY10.Management believes fee-income growth will be at least in line with loan growthdue to the diversified nature of fee income.Management is focusing on improving its cost-to-income ratio and sees higheroperating leverage in future.BoB's asset quality is among the best with net NPA at 0.3% and coverage of 82%.Restructured loans, which comprise 2.8% of the book, remain the best among itspeer banks. The management foresees no large account restructuring in the nearfuture. Management indicated it would not compromise asset quality to gain marketshare.Management is confident of sustaining at least 1% RoA and 18% RoE.

Valuation and viewWe expect BoB to post EPS of Rs61 in FY10 and Rs76 in FY11.BV will be Rs364 in FY10E and Rs422 in FY11E.RoA will be 0.9-1%+ and RoE at 18-19% over the next two years.The stock trades at 1x FY11E BV and 5.7x FY11E EPS. Maintain Buy with top pickstatus.

Company Represented By:Mr R K Bakshi, EDDr Rupa Nitsure, Chief economist

Covering Analyst(s):Ajinkya Dhavale+91 22 3982 [email protected]

Alpesh Mehta+91 22 3982 [email protected]

YEAR NET INCOME PAT EPS EPS P/E P/BV CAR ROAE ROAA P/ABV

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) (%) (X)

3/08A 59,628 14,355 39.3 39.8 11.1 1.6 12.9 15.8 0.9 1.7

3/09A 78,811 22,272 60.9 55.1 7.2 1.4 14.1 20.9 1.1 1.4

3/10E 79,242 22,382 61.2 0.5 7.1 1.2 13.5 18.0 0.9 1.2

3/11E 93,671 27,878 76.3 24.6 5.7 1.0 12.9 19.4 1.0 1.1

Bloomberg BOB INEquity Shares (m) 365.5CMP (Rs) 437Mcap (US$ b) 3.452 W Range 485 / 1701, 6, 12 Rel Per -6 / 4 / 40

8August 3 - 5, 2009

5th Annual Global Investor Conference

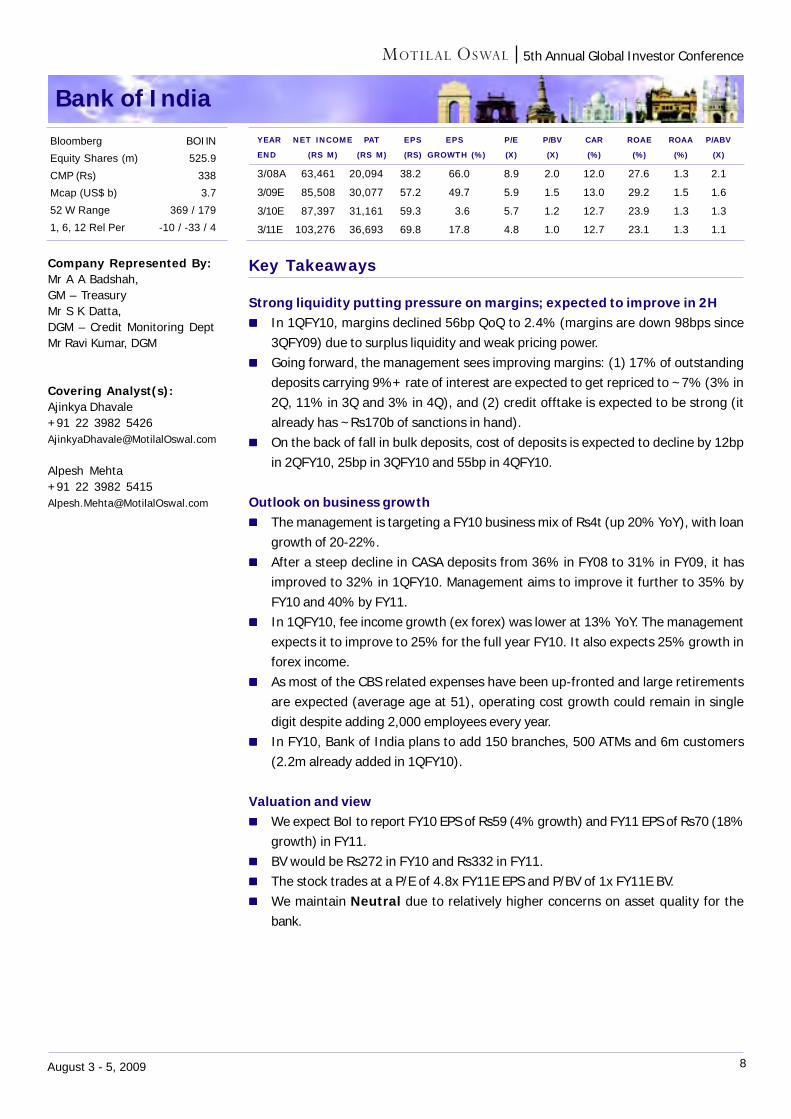

Bank of India

Key Takeaways

Strong liquidity putting pressure on margins; expected to improve in 2HIn 1QFY10, margins declined 56bp QoQ to 2.4% (margins are down 98bps since3QFY09) due to surplus liquidity and weak pricing power.Going forward, the management sees improving margins: (1) 17% of outstandingdeposits carrying 9%+ rate of interest are expected to get repriced to ~7% (3% in2Q, 11% in 3Q and 3% in 4Q), and (2) credit offtake is expected to be strong (italready has ~Rs170b of sanctions in hand).On the back of fall in bulk deposits, cost of deposits is expected to decline by 12bpin 2QFY10, 25bp in 3QFY10 and 55bp in 4QFY10.

Outlook on business growthThe management is targeting a FY10 business mix of Rs4t (up 20% YoY), with loangrowth of 20-22%.After a steep decline in CASA deposits from 36% in FY08 to 31% in FY09, it hasimproved to 32% in 1QFY10. Management aims to improve it further to 35% byFY10 and 40% by FY11.In 1QFY10, fee income growth (ex forex) was lower at 13% YoY. The managementexpects it to improve to 25% for the full year FY10. It also expects 25% growth inforex income.As most of the CBS related expenses have been up-fronted and large retirementsare expected (average age at 51), operating cost growth could remain in singledigit despite adding 2,000 employees every year.In FY10, Bank of India plans to add 150 branches, 500 ATMs and 6m customers(2.2m already added in 1QFY10).

Valuation and viewWe expect BoI to report FY10 EPS of Rs59 (4% growth) and FY11 EPS of Rs70 (18%growth) in FY11.BV would be Rs272 in FY10 and Rs332 in FY11.The stock trades at a P/E of 4.8x FY11E EPS and P/BV of 1x FY11E BV.We maintain Neutral due to relatively higher concerns on asset quality for thebank.

Company Represented By:Mr A A Badshah,GM – TreasuryMr S K Datta,DGM – Credit Monitoring DeptMr Ravi Kumar, DGM

Covering Analyst(s):Ajinkya Dhavale+91 22 3982 [email protected]

Alpesh Mehta+91 22 3982 [email protected]

YEAR NET INCOME PAT EPS EPS P/E P/BV CAR ROAE ROAA P/ABV

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) (%) (X)

3/08A 63,461 20,094 38.2 66.0 8.9 2.0 12.0 27.6 1.3 2.1

3/09E 85,508 30,077 57.2 49.7 5.9 1.5 13.0 29.2 1.5 1.6

3/10E 87,397 31,161 59.3 3.6 5.7 1.2 12.7 23.9 1.3 1.3

3/11E 103,276 36,693 69.8 17.8 4.8 1.0 12.7 23.1 1.3 1.1

Bloomberg BOI INEquity Shares (m) 525.9CMP (Rs) 338Mcap (US$ b) 3.752 W Range 369 / 1791, 6, 12 Rel Per -10 / -33 / 4

9August 3 - 5, 2009

5th Annual Global Investor Conference

Bharat Forge

Key Takeaways

Initial signs of improvement, after witnessing worst in 3Q/4QFY09Volumes in Bharat Forge's (BFL) key CV segment have witnessed improvement inall geographies as 3Q/4Q witnessed significant correction in inventory.BFL has taken initiatives to bring down breakeven capacity utilization in all thegeographies. Currently, it would breakeven at ~50% utilization in US & EU and~35% in India. Excluding one-offs, its global operations should be near break-evenlevels, whereas India operations are profit making.It has witnessed no bad debts in any of the geographies. It doesn't have any directexposure to OEMs like GM, Chrysler, etc; however, it supplies to them through tier-I vendors like ZF AG. Further, its exposure to GM has reduced from 60-65% to 35%.

Significant opportunity arising from structural shift in the industryThe global economic crisis has resulted in two key trends: (1) bankruptcy of itspeers, and (2) focus on small cars.Bankruptcy of its global competitors provides BFL an opportunity to move up thevalue chain, as global OEMs replace troubled tier-I suppliers with BFL.Shift in demand towards smaller fuel efficient cars augurs well for BFL, as globalOEM's with integrated facilities for SUVs and pick-ups, are not willing to invest innew facilities, resulting in higher outsourcing.

Focus on doubling non-auto contribution to revenues to 40% by FY13As against 20% currently, BFL is targeting 40% of revenue from non-auto businessesby 2012 and 60% by 2015. This is mainly turbine generators (TG), and heavy forgingsfor nuclear, hydro power and wind turbine generators. This is expected to improveEBITDA margin, RoCE and cash generation.BFL has entered into a 50:50 JV with Alstom for manufacturing supercritical TG withcapacity of 5,000MW by FY13. The JV has already participated in bulk project awardsfrom NTPC (11*660MW).BFL has also entered into a JV with Areva for heavy forgings to cater to the nuclearmarket in India. The JV would have assured procurement of up to 70% from Areva.The JV will cater to nuclear power, hydro power etc, and will have a 14,000 tonforging press which would be operational by 2012.The Maharashtra government has signed an LoI with Areva to set up 10,000MW ofnuclear power capacity at a cost of Rs650b. This could be substantial opportunityfor the forging JV.

Valuations and viewThe stock currently trades at 33x FY10E consolidated consensus EPS of Rs7.3 and 22.3xFY11E consolidated consensus EPS of Rs10.8. We do not have rating on the stock.

Company Represented By:Mr Amit Kalyani,Executive Director

Covering Analyst(s):Jinesh Gandhi+91 22 3982 [email protected]

Bloomberg BHFC INEquity Shares (m) 237.3CMP (Rs) 241Mcap (US$ b) 1.252 W Range 283 / 691, 6, 12 Rel Per 64 / 130 / -12

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

03/06A 29,715 2,505 10.8 -77.7 28.2 18.8

03/07A 41,489 2,835 12.1 12.0 20.6 14.0

03/08A 45,976 2,908 12.4 2.8 18.5 12.2

03/09A 47,112 411 1.7 -86.5 144.0 3.3 2.5 2.8 1.5 19.7

10August 3 - 5, 2009

5th Annual Global Investor Conference

Bharti Airtel

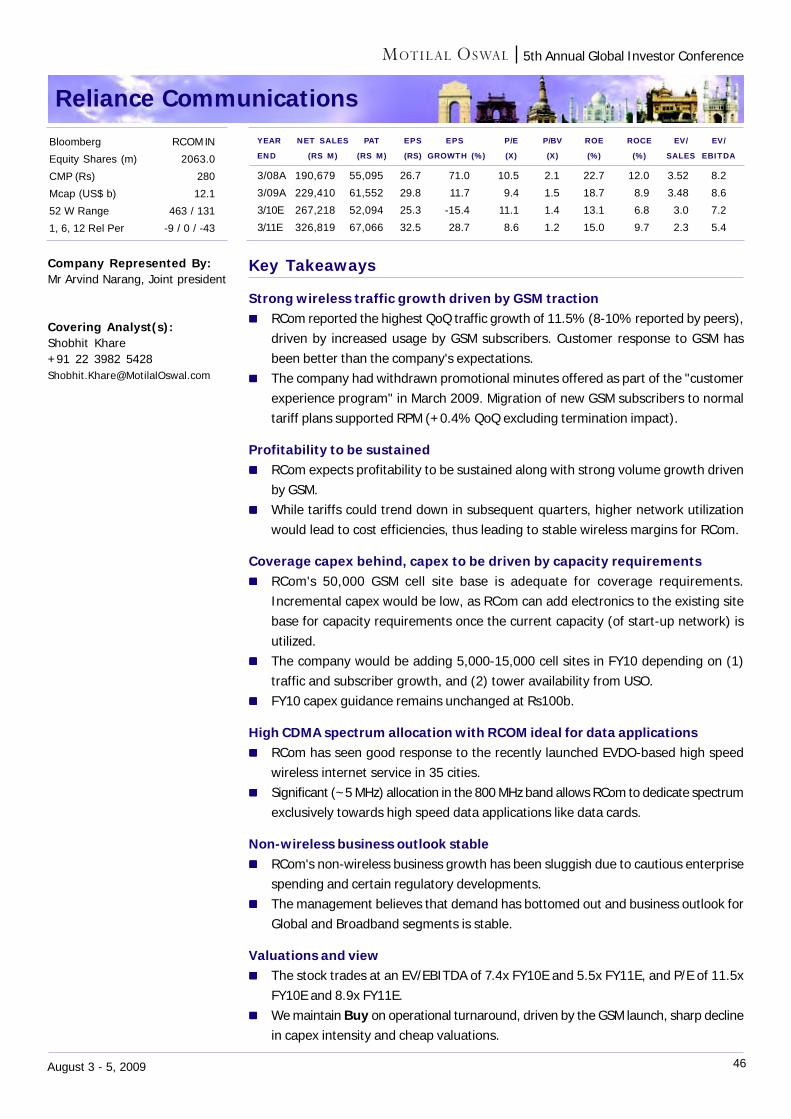

Key Takeaways

Rural market remains attractiveBharti remains sanguine about the rural markets and believes that economic growthin rural India would continue unabated.Rural India accounted for ~55% of wireless subscriber additions for Bharti in 4QFY09.This share is likely to expand going forward, as wireless penetration in rural Indiastill remains significantly low at 15-16% as against ~35% for the overall Indianmarket.ARPU in rural markets remains attractive at ~2/3rd of the overall Indian marketARPU.

Low tariffs (high affordability) is the safety net against competitionBharti believes that very low tariffs prevailing in the Indian market are the biggestsafety net for incumbents against increasing competition.Bharti's significant coverage advantage would ensure that incremental margins arein line with the current margin profile.Mr Gupta also emphasized on the secular demand growth in telecom services,which leads to stable industry outlook.

3G likely in late CY09/early CY10Bharti expects 3G spectrum auction/allocations in late CY09/early CY10.The company believes that wireless is the only viable option for India to improvebroadband reach.WCDMA/HSPA is likely to be the preferred technology for providing broadband.

High tariffs, low penetration makes Africa an attractive marketMr Gupta believes that high tariffs and relatively low penetration in Africa makes itan attractive market for Bharti.Scope for cost and tariff reductions could trigger significant volume growth opportunityin the African markets.

Valuations and viewBharti trades at an EV of 7.4x FY11E EBITDA and 12.9x FY11E EPS.Bharti remains best-placed, given low capex intensity, un-leveraged balance sheet,and scale advantage.Maintain Buy with a target of Rs492.

Company Represented By:Mr Akhil Gupta, DirectorMr Harjeet Kohli,Group Treasurer

Covering Analyst(s):Shobhit Khare+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

3/08A 270,250 67,008 17.7 57.4 22.7 6.7 36.9 25.8 5.8 13.8

3/09A 369,615 84,699 22.3 26.4 18.0 4.8 31.4 23.8 4.3 10.5

3/10E 420,025 104,388 27.5 23.2 14.6 4.0 30.0 21.5 3.7 8.7

3/11E 468,526 117,761 31.1 12.8 12.9 3.1 27.1 21.2 3.2 7.4

Bloomberg BHARTI INEquity Shares (m) 3795.2CMP (Rs) 401Mcap (US$ b) 32.152 W Range 518 / 2421, 6, 12 Rel Per -11 / -47 / -11

11August 3 - 5, 2009

5th Annual Global Investor Conference

Biocon

Key Takeaways

Contract research, insulin to be drive growth in the medium term; Long-termbenefits from BiogenericsContract research to grow at over 20% in FY10: Biocon's contract researchsubsidiary (Syngene) recently began to execute the BMS contract, which is likely togradually ramp up over the next few quarters. This business is expected to record over20% growth in FY10. We estimate 26% CAGR for this business over FY09-11.

Multiple initiatives in Insulin space: Biocon continues its insulin filings in emergingmarkets with few approvals to come through annually for the next two years. It alsohas tie-ups in regulated markets for supply of insulin crystals. Its oral insulin NCErecently started Phase-III trials in India. We believe Biocon's insulin initiative (API,formulation & NDDS) will be a key growth driver in the coming years.Biogeneric collaboration with Mylan is long-term positive: Biocon enteredinto collaboration with Mylan (USA) for development, manufacture and distributionof biogenerics. Mylan and Biocon will share development, capital and certain othercosts to commercialize biogenerics. This is a long-term positive for Biocon as it getsa partner to share development costs and Biocon can leverage Mylan's distributionstrengths in the US and Europe. The cost of sharing will ensure that Biocon's P&Ldoes not get overburdened by the costs of developing biogenerics. But revenuefrom this tie-up is expected to start accruing only after two or three years. In theinterim Biocon will be entitled to milestone payments from Mylan.Biocon to R&D expenses: Management says R&D expenses are likely to increaseto 8% of revenue over the next two years as some of the NCEs progress into clinicaltrials. Biocon expects to complete Phase-III trials for its oral insulin NCE in the next12 months and expects to launch it in India in FY11 after which it will explore thepossibility of out-licensing the NCE for developed markets.Targets domestic formulation revenue of Rs5b over 3-5 years: Bioconentered the domestic formulations market three years ago and generated revenueof over Rs1b in FY09. Management targets revenue of Rs5b from this initiative overthe next three to five years.

Valuation and viewKey growth drivers for FY10E will be traction in Biocon's insulin initiative, contributionfrom immuno-suppressants and ramp-up in the contract research business. But higherR&D costs, increased depreciation and higher expenses, linked to the scale-up of thedomestic formulations business, will continue to temper earnings growth. We expectFY10 EPS of Rs13 (up 176% on a low base) and FY11 EPS of Rs15.2 (up 17.8%). Thestock is valued at 18.2x FY10E and 15.5x FY11E earnings. Maintain Buy.

Company Represented By:Mr Murali Krishnan K NPresident - Group Finance

Covering Analyst(s):Nimish Desai+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

03/08A 10,542 2,250 22.5 12.4 10.4 1.6 15.2 13.6 4.2 14.9

03/09A 16,091 935 4.7 -79.2 50.2 3.1 6.2 6.2 3.0 14.9

03/10E 21,257 2,574 12.9 175.4 18.2 2.7 15.1 15.8 2.2 10.6

03/11E 23,616 3,033 15.2 17.8 15.5 2.4 15.6 16.2 1.9 9.3

Bloomberg BIOS INEquity Shares (m) 200.0CMP (Rs) 235Mcap (US$ b) 1.052 W Range 243 / 851, 6, 12 Rel Per -2 / 55 / 14

12August 3 - 5, 2009

5th Annual Global Investor Conference

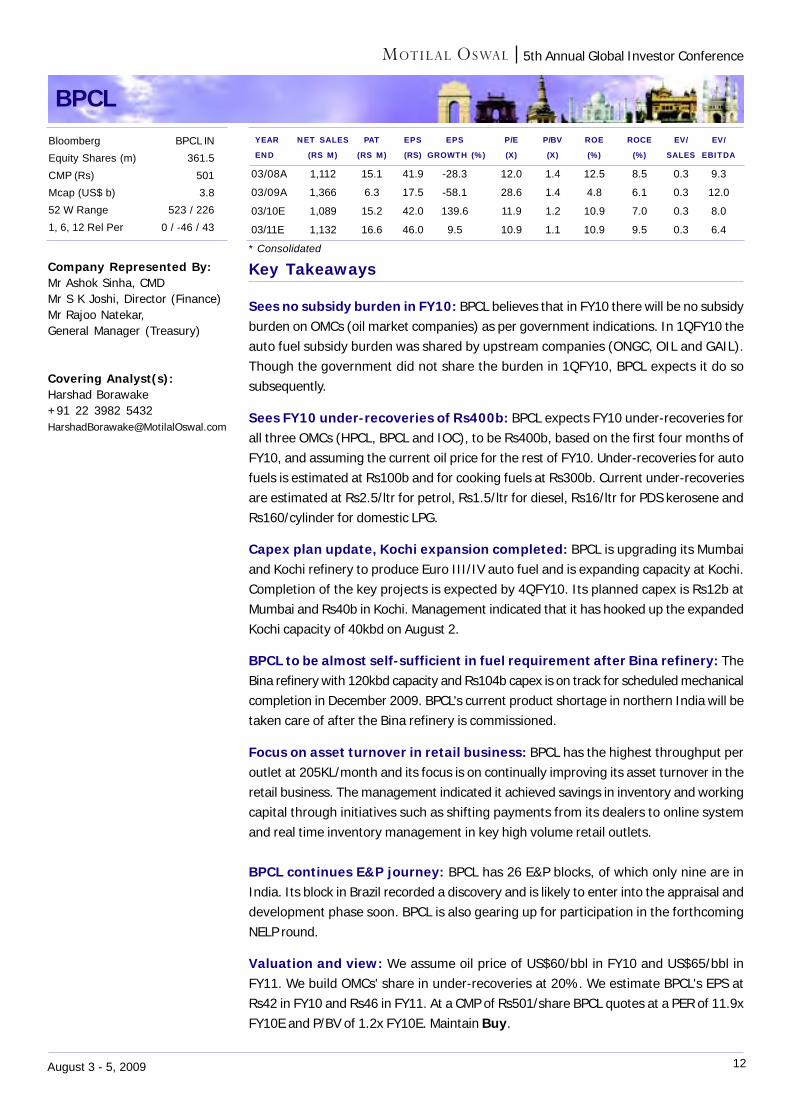

BPCL

Key Takeaways

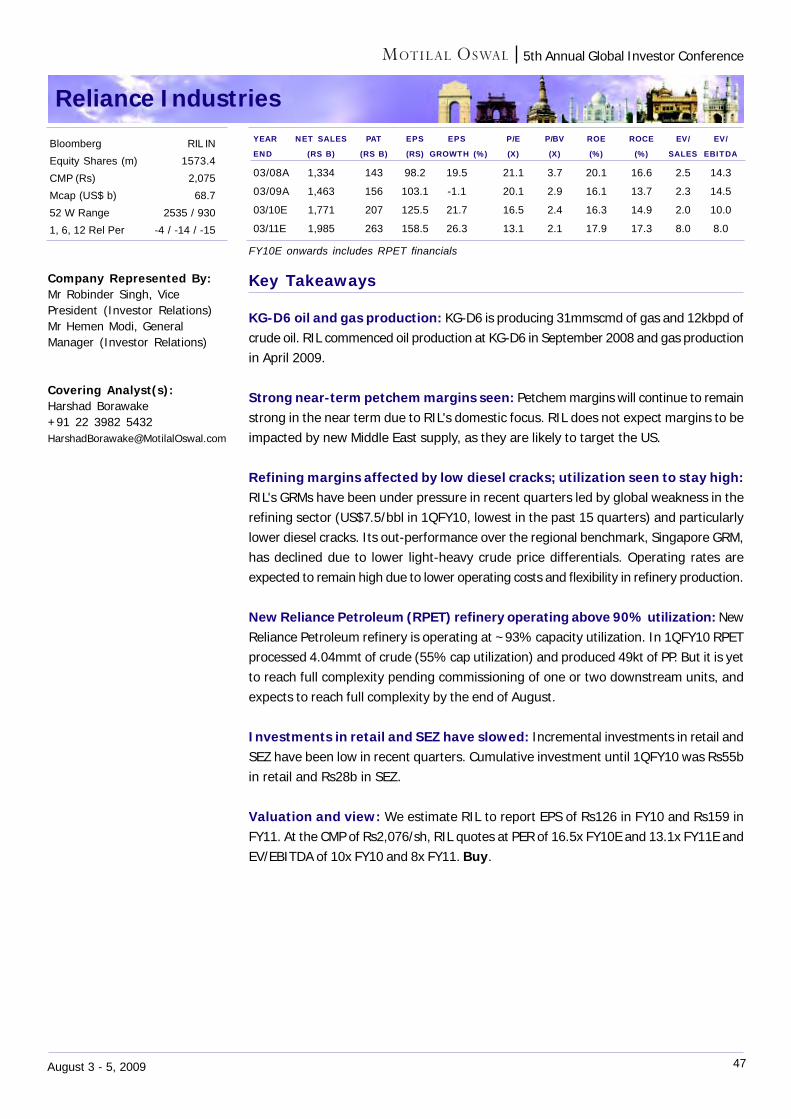

Sees no subsidy burden in FY10: BPCL believes that in FY10 there will be no subsidyburden on OMCs (oil market companies) as per government indications. In 1QFY10 theauto fuel subsidy burden was shared by upstream companies (ONGC, OIL and GAIL).Though the government did not share the burden in 1QFY10, BPCL expects it do sosubsequently.

Sees FY10 under-recoveries of Rs400b: BPCL expects FY10 under-recoveries forall three OMCs (HPCL, BPCL and IOC), to be Rs400b, based on the first four months ofFY10, and assuming the current oil price for the rest of FY10. Under-recoveries for autofuels is estimated at Rs100b and for cooking fuels at Rs300b. Current under-recoveriesare estimated at Rs2.5/ltr for petrol, Rs1.5/ltr for diesel, Rs16/ltr for PDS kerosene andRs160/cylinder for domestic LPG.

Capex plan update, Kochi expansion completed: BPCL is upgrading its Mumbaiand Kochi refinery to produce Euro III/IV auto fuel and is expanding capacity at Kochi.Completion of the key projects is expected by 4QFY10. Its planned capex is Rs12b atMumbai and Rs40b in Kochi. Management indicated that it has hooked up the expandedKochi capacity of 40kbd on August 2.

BPCL to be almost self-sufficient in fuel requirement after Bina refinery: TheBina refinery with 120kbd capacity and Rs104b capex is on track for scheduled mechanicalcompletion in December 2009. BPCL's current product shortage in northern India will betaken care of after the Bina refinery is commissioned.

Focus on asset turnover in retail business: BPCL has the highest throughput peroutlet at 205KL/month and its focus is on continually improving its asset turnover in theretail business. The management indicated it achieved savings in inventory and workingcapital through initiatives such as shifting payments from its dealers to online systemand real time inventory management in key high volume retail outlets.

BPCL continues E&P journey: BPCL has 26 E&P blocks, of which only nine are inIndia. Its block in Brazil recorded a discovery and is likely to enter into the appraisal anddevelopment phase soon. BPCL is also gearing up for participation in the forthcomingNELP round.

Valuation and view: We assume oil price of US$60/bbl in FY10 and US$65/bbl inFY11. We build OMCs' share in under-recoveries at 20%. We estimate BPCL's EPS atRs42 in FY10 and Rs46 in FY11. At a CMP of Rs501/share BPCL quotes at a PER of 11.9xFY10E and P/BV of 1.2x FY10E. Maintain Buy.

Company Represented By:Mr Ashok Sinha, CMDMr S K Joshi, Director (Finance)Mr Rajoo Natekar,General Manager (Treasury)

Covering Analyst(s):Harshad Borawake+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

03/08A 1,112 15.1 41.9 -28.3 12.0 1.4 12.5 8.5 0.3 9.3

03/09A 1,366 6.3 17.5 -58.1 28.6 1.4 4.8 6.1 0.3 12.0

03/10E 1,089 15.2 42.0 139.6 11.9 1.2 10.9 7.0 0.3 8.0

03/11E 1,132 16.6 46.0 9.5 10.9 1.1 10.9 9.5 0.3 6.4

Bloomberg BPCL INEquity Shares (m) 361.5CMP (Rs) 501Mcap (US$ b) 3.852 W Range 523 / 2261, 6, 12 Rel Per 0 / -46 / 43

* Consolidated

13August 3 - 5, 2009

5th Annual Global Investor Conference

Central Bank of India

Key Takeaways

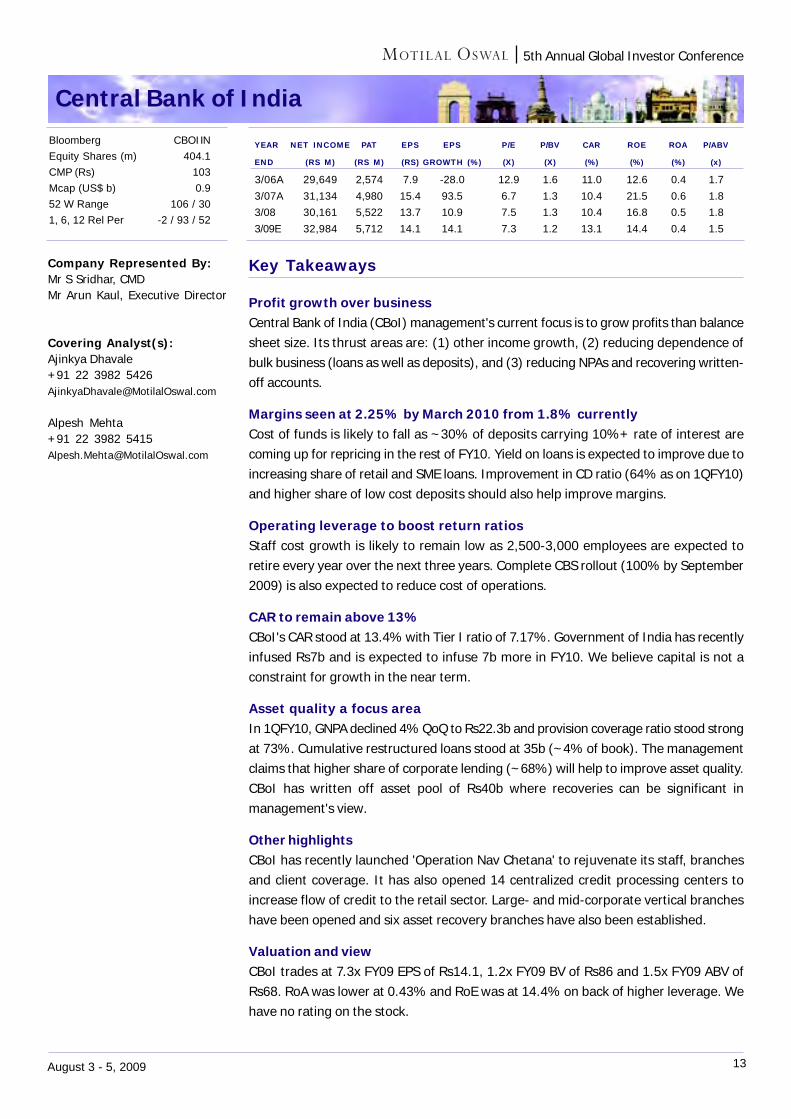

Profit growth over businessCentral Bank of India (CBoI) management's current focus is to grow profits than balancesheet size. Its thrust areas are: (1) other income growth, (2) reducing dependence ofbulk business (loans as well as deposits), and (3) reducing NPAs and recovering written-off accounts.

Margins seen at 2.25% by March 2010 from 1.8% currentlyCost of funds is likely to fall as ~30% of deposits carrying 10%+ rate of interest arecoming up for repricing in the rest of FY10. Yield on loans is expected to improve due toincreasing share of retail and SME loans. Improvement in CD ratio (64% as on 1QFY10)and higher share of low cost deposits should also help improve margins.

Operating leverage to boost return ratiosStaff cost growth is likely to remain low as 2,500-3,000 employees are expected toretire every year over the next three years. Complete CBS rollout (100% by September2009) is also expected to reduce cost of operations.

CAR to remain above 13%CBoI's CAR stood at 13.4% with Tier I ratio of 7.17%. Government of India has recentlyinfused Rs7b and is expected to infuse 7b more in FY10. We believe capital is not aconstraint for growth in the near term.

Asset quality a focus areaIn 1QFY10, GNPA declined 4% QoQ to Rs22.3b and provision coverage ratio stood strongat 73%. Cumulative restructured loans stood at 35b (~4% of book). The managementclaims that higher share of corporate lending (~68%) will help to improve asset quality.CBoI has written off asset pool of Rs40b where recoveries can be significant inmanagement's view.

Other highlightsCBoI has recently launched 'Operation Nav Chetana' to rejuvenate its staff, branchesand client coverage. It has also opened 14 centralized credit processing centers toincrease flow of credit to the retail sector. Large- and mid-corporate vertical brancheshave been opened and six asset recovery branches have also been established.

Valuation and viewCBoI trades at 7.3x FY09 EPS of Rs14.1, 1.2x FY09 BV of Rs86 and 1.5x FY09 ABV ofRs68. RoA was lower at 0.43% and RoE was at 14.4% on back of higher leverage. Wehave no rating on the stock.

Company Represented By:Mr S Sridhar, CMDMr Arun Kaul, Executive Director

Covering Analyst(s):Ajinkya Dhavale+91 22 3982 [email protected]

Alpesh Mehta+91 22 3982 [email protected]

YEAR NET INCOME PAT EPS EPS P/E P/BV CAR ROE ROA P/ABV

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) (%) (x)

3/06A 29,649 2,574 7.9 -28.0 12.9 1.6 11.0 12.6 0.4 1.73/07A 31,134 4,980 15.4 93.5 6.7 1.3 10.4 21.5 0.6 1.83/08 30,161 5,522 13.7 10.9 7.5 1.3 10.4 16.8 0.5 1.83/09E 32,984 5,712 14.1 14.1 7.3 1.2 13.1 14.4 0.4 1.5

Bloomberg CBOI INEquity Shares (m) 404.1CMP (Rs) 103Mcap (US$ b) 0.952 W Range 106 / 301, 6, 12 Rel Per -2 / 93 / 52

14August 3 - 5, 2009

5th Annual Global Investor Conference

Dabur India

Key Takeaways

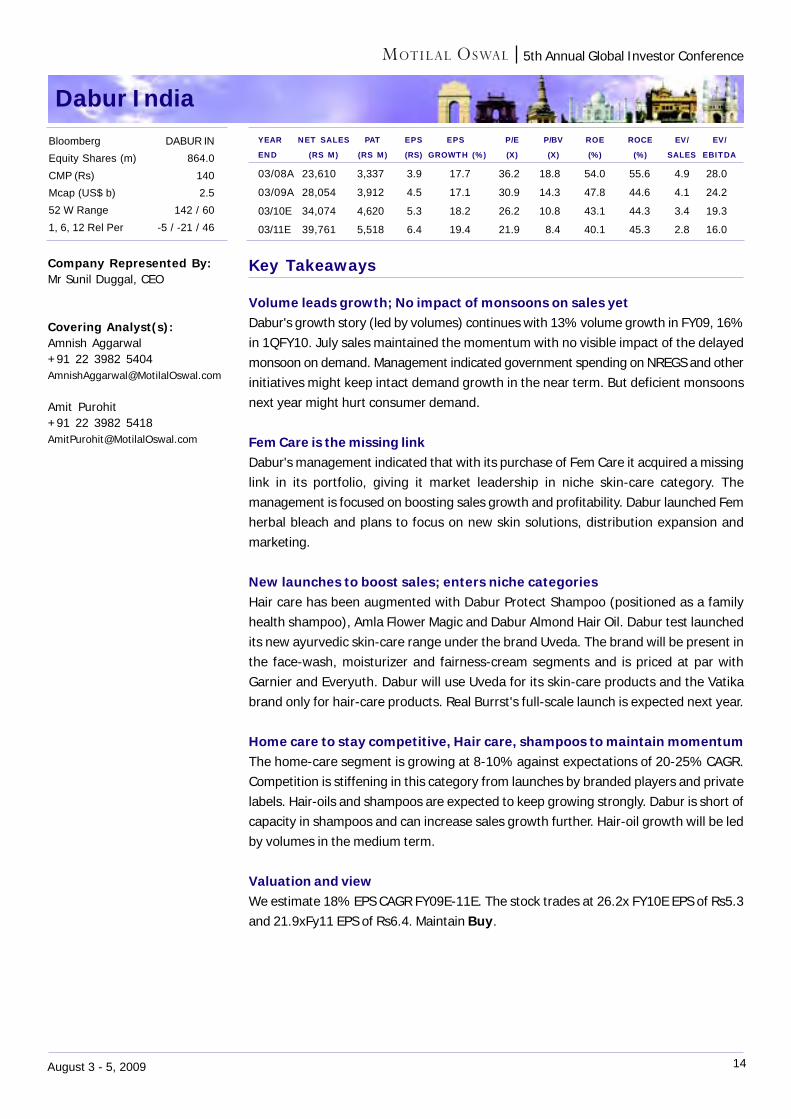

Volume leads growth; No impact of monsoons on sales yetDabur's growth story (led by volumes) continues with 13% volume growth in FY09, 16%in 1QFY10. July sales maintained the momentum with no visible impact of the delayedmonsoon on demand. Management indicated government spending on NREGS and otherinitiatives might keep intact demand growth in the near term. But deficient monsoonsnext year might hurt consumer demand.

Fem Care is the missing linkDabur's management indicated that with its purchase of Fem Care it acquired a missinglink in its portfolio, giving it market leadership in niche skin-care category. Themanagement is focused on boosting sales growth and profitability. Dabur launched Femherbal bleach and plans to focus on new skin solutions, distribution expansion andmarketing.

New launches to boost sales; enters niche categoriesHair care has been augmented with Dabur Protect Shampoo (positioned as a familyhealth shampoo), Amla Flower Magic and Dabur Almond Hair Oil. Dabur test launchedits new ayurvedic skin-care range under the brand Uveda. The brand will be present inthe face-wash, moisturizer and fairness-cream segments and is priced at par withGarnier and Everyuth. Dabur will use Uveda for its skin-care products and the Vatikabrand only for hair-care products. Real Burrst's full-scale launch is expected next year.

Home care to stay competitive, Hair care, shampoos to maintain momentumThe home-care segment is growing at 8-10% against expectations of 20-25% CAGR.Competition is stiffening in this category from launches by branded players and privatelabels. Hair-oils and shampoos are expected to keep growing strongly. Dabur is short ofcapacity in shampoos and can increase sales growth further. Hair-oil growth will be ledby volumes in the medium term.

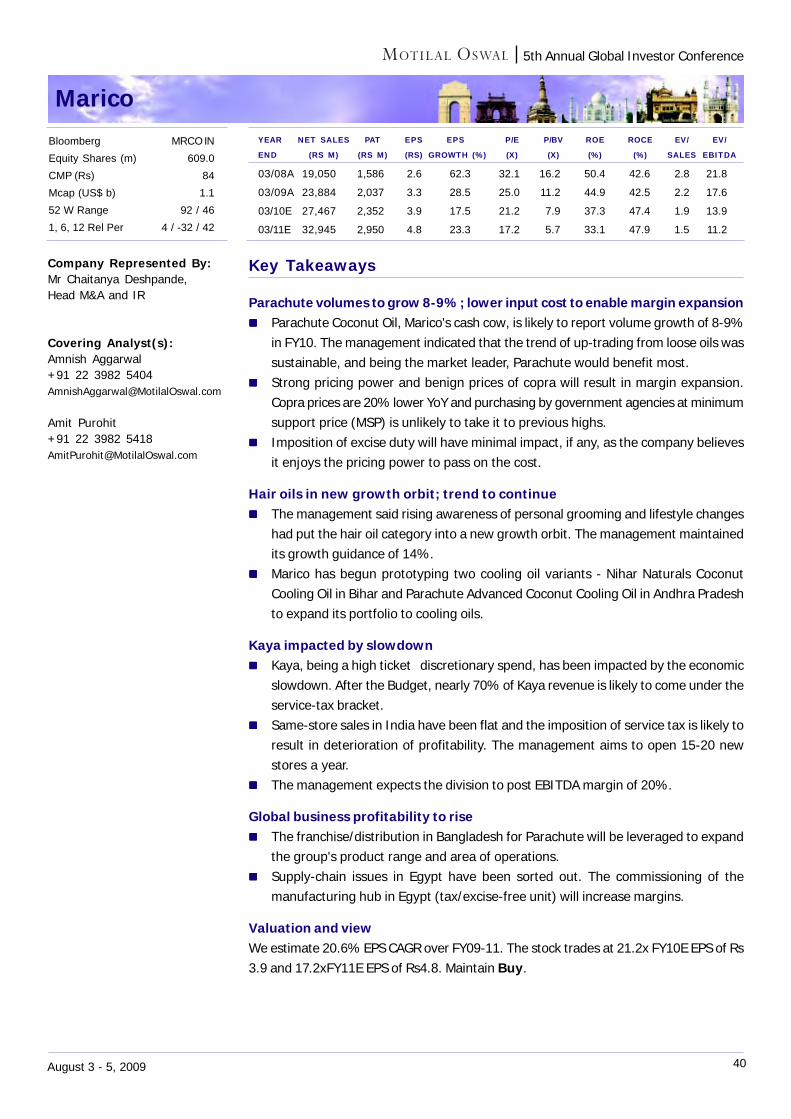

Valuation and viewWe estimate 18% EPS CAGR FY09E-11E. The stock trades at 26.2x FY10E EPS of Rs5.3and 21.9xFy11 EPS of Rs6.4. Maintain Buy.

Company Represented By:Mr Sunil Duggal, CEO

Covering Analyst(s):Amnish Aggarwal+91 22 3982 [email protected]

Amit Purohit+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

03/08A 23,610 3,337 3.9 17.7 36.2 18.8 54.0 55.6 4.9 28.0

03/09A 28,054 3,912 4.5 17.1 30.9 14.3 47.8 44.6 4.1 24.2

03/10E 34,074 4,620 5.3 18.2 26.2 10.8 43.1 44.3 3.4 19.3

03/11E 39,761 5,518 6.4 19.4 21.9 8.4 40.1 45.3 2.8 16.0

Bloomberg DABUR INEquity Shares (m) 864.0CMP (Rs) 140Mcap (US$ b) 2.552 W Range 142 / 601, 6, 12 Rel Per -5 / -21 / 46

15August 3 - 5, 2009

5th Annual Global Investor Conference

DLF

Key Takeaways

Concern on high outstandings from DAL reducesDuring 1QFY10, the promoters of DLF raised Rs38b by selling ~9.9% of their stakein DLF. Of this, ~Rs19b was utilized to reduce outstandings from DLF Assets (DAL)while the balance is likely to be utilized to buy out DE Shaw's 75% stake in DAL.The management stated that DLF is likely to pick up a stake in DAL based on thevaluation at which DLF buys out DE Shaw's stake in DAL. According to themanagement, the valuation exercise is currently underway and is likely to be finalizedover the next 2-3 months.

Debt to decline to Rs75b-80b in FY10, largely aided by asset salesNet debt is likely to be reduced to Rs75b-80b in FY10 from Rs140b during 1QFY10,mainly aided by sale of non-strategic assets. The company plans to reduce itsleverage to 0.3x in FY10 from 0.5x currently. DLF does not have any major debtrepayment obligation for another 2-3 years.The management is hopeful of achieving its target of Rs55b of asset sales in FY10.DLF is in advanced stages of negotiation for assets worth Rs25b-30b, which include(i) wind power assets - Rs10b, (ii) refund from government agencies for discontinuedprojects ~Rs4b, and (iii) land for hotel projects - Rs5b-6b.

Residential launch plans focus on lucrative city-centric projectsTo boost its cash flow position, DLF plans to focus on launching city-centric projects.It has plans to launch 17-18msf of residential projects in FY10 comprising (i) 8-9msfof city-centric projects priced at Rs5,000-8,000/sf across Chennai, Kochi, Delhi andGurgaon and (ii) 5-8msf of affordable/mid-income housing projects priced at Rs2,500-3,000/sf in key cities in South India and NCR.According to the management, DLF is likely to launch phase II of SBM, Delhi at 15-20% higher rates than its previous launch.

Construction activity has picked paceArea under construction increased by ~8msf to 42msf during 1QFY10, after aboutthree quarters of negligible activity. DLF has commenced construction on (i) residentialprojects in New Gurgaon and (ii) commercial complexes in New Delhi and Kolkata.Further, it is likely to commence construction on its SBM Delhi project during 2QFY10.

Valuation and viewOur NAV estimate for DLF is Rs360/share. Once DLF resolves its DAL outstanding issue,it would address much of the negative overhang on the stock. The stock trades at 2.5xits adjusted book value of Rs154 and 9% premium to its NAV of Rs360/share. Progresson debt leveraging and subsequent business revival in the commercial and retail verticalscould lead to higher valuation multiples for DLF. Maintain Buy.

Company Represented By:Mr Anurag Kalra,VP-Investor Relations

Covering Analyst(s):Siddharth Bothra+91 22 3982 [email protected]

Mansi Trivedi+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

3/08A 144,329 78,120 45.8 262.8 8.5 3.8 39.7 43.0 5.3 7.9

3/09A 100,440 46,292 26.9 -41.3 14.6 3.0 18.7 15.5 8.2 14.9

3/10E 58,593 23,246 13.5 -49.8 29.0 2.7 8.6 7.9 13.2 23.2

3/11E 74,404 32,871 19.1 41.4 20.5 2.4 10.9 11.2 10.1 16.4

Bloomberg DLFU INEquity Shares (m) 1714.4CMP (Rs) 391Mcap (US$ b) 14.152 W Range 580 / 1241, 6, 12 Rel Per 13 / 106 / -36

16August 3 - 5, 2009

5th Annual Global Investor Conference

Dr Reddy’s Laboratories

Key Takeaways

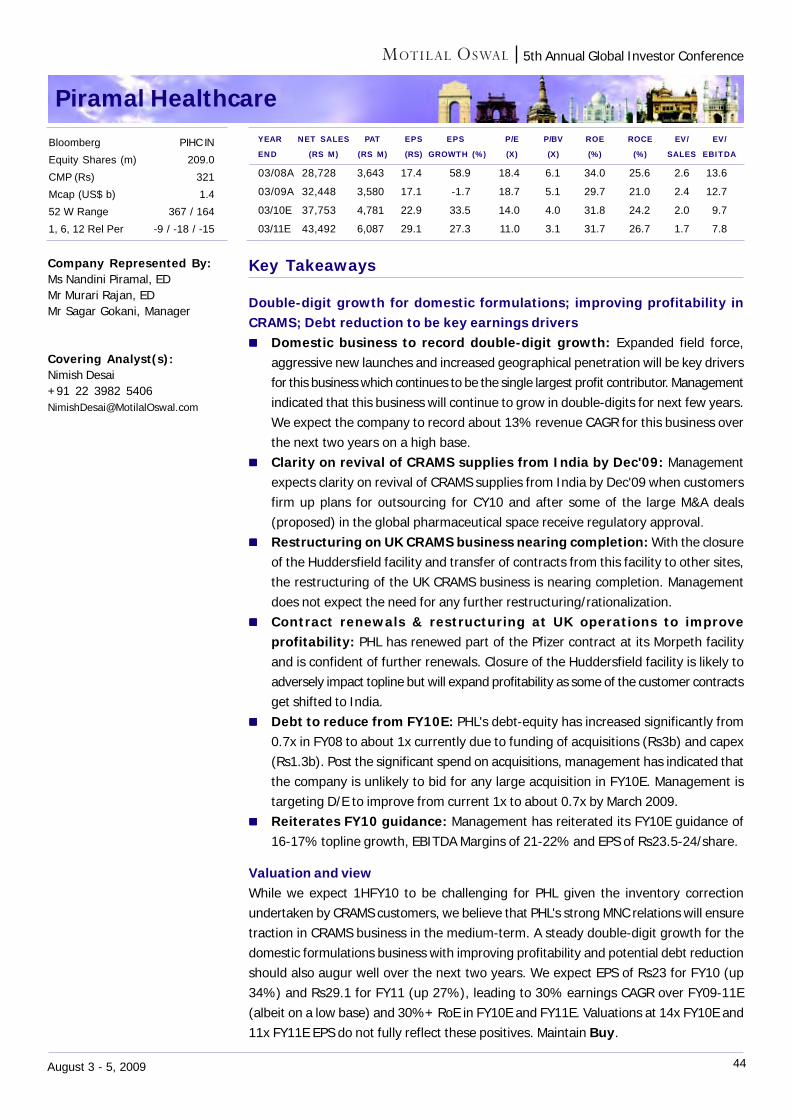

Strategic prioritization in generic markets: Dr Reddy's has recently initiatedthe process of realigning its presence internationally to focus on certain keygeographies and has decided to gradually exit from some of the small/marginalmarkets. Focus markets for the future will be US, India, Russia & CIS, UK andGermany.One/two low-competition product launches in the US every year: Mr Prasadindicated 1-2 such opportunities every year for the next five years. Visible opportunitiesinclude potential launch of generic Arixtra and Prilosec OTC. These opportunitiesspan across FY10/11. The company currently has a pipeline of 16 FTF, targetinginnovator market size of US$9b.Aims to become tier-I player in the US: Dr Reddy's is currently among the tier-II players in the US and is aiming to upgrade itself to tier-I status (implying increasein annual revenues from ~US$400m to US$1b) over the next few years. New launchesconsisting of normal, low-competition and patent challenge products will help it toachieve this goal.Restructuring of German operations: Given the shift from branded generics totender-based generics market, the company intends to restructure its Betapharmoperations, including reduction in sales force (from 110 to 50) and shift ofmanufacturing to India.Ramp-up in the biologics business: Dr Reddy's is targeting to ramp up its biologicsbusiness in emerging markets in the short-to-medium term and in regulated marketsin the long-term (possibly through partnerships).GSK tie-up to bring in long-term benefits: The tie-up with GSK gives Dr Reddy'saccess to many emerging markets through GSK's distribution network, with verylow incremental investments. The tie-up includes a basket of 100 products includingnormal and differentiated products. It may include biogenerics at a later date.Guidance: The company guided 10% topline growth and RoCE of mid-to-high teensfor FY10 on a high base of FY09. By FY13, it targets revenues of US$3b (implying21% CAGR over FY09-13) and 25% RoCE, led mainly by the above initiatives.

Valuation and viewTraction in the branded formulations and US businesses, and focus on improvingprofitability will be the key growth drivers for Dr Reddy's over the next two years.We expect EPS of Rs43.3 for FY10 (v/s net loss for FY09) and Rs50.8 for FY11 (up17.5%), leading to 22% EPS CAGR for FY08-11. The stock currently trades at 19xFY10E and 16.2x FY11E core earnings. Our DCF value of generic Arixtra, PrilosecOTC and Sumatriptan (the visible opportunities of the Para-IV/low-competitionpipeline) is Rs26/share. Maintain Buy.

Company Represented By:Mr GV Prasad,Vice Chairman & CEOMr Kedar Upadhye,Director - Corporate FinanceMr Raghavender R, DeputyManager - Investor Relations

Covering Analyst(s):Nimish Desai+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

03/09A* 69,441 -5,169 -30.7 -210.6 -26.8 3.3 -12.3 -3.3 2.2 12.003/10E* 70,832 8,020 47.603/10E 68,734 7,286 43.3 19.0 2.9 16.8 14.2 2.1 12.403/11E 76,031 8,557 50.8 17.4 16.2 2.6 15.9 13.8 2.0 11.903/11E* 79,481 10,121 60.1 38.9

Bloomberg DRRD INEquity Shares (m) 168.4CMP (Rs) 820Mcap (US$ b) 2.952 W Range 836 / 3551, 6, 12 Rel Per -6 / 8 / 33

* - includes patent challenge/low competition upsides

17August 3 - 5, 2009

5th Annual Global Investor Conference

Everest Kanto Cylinders

Key Takeaways

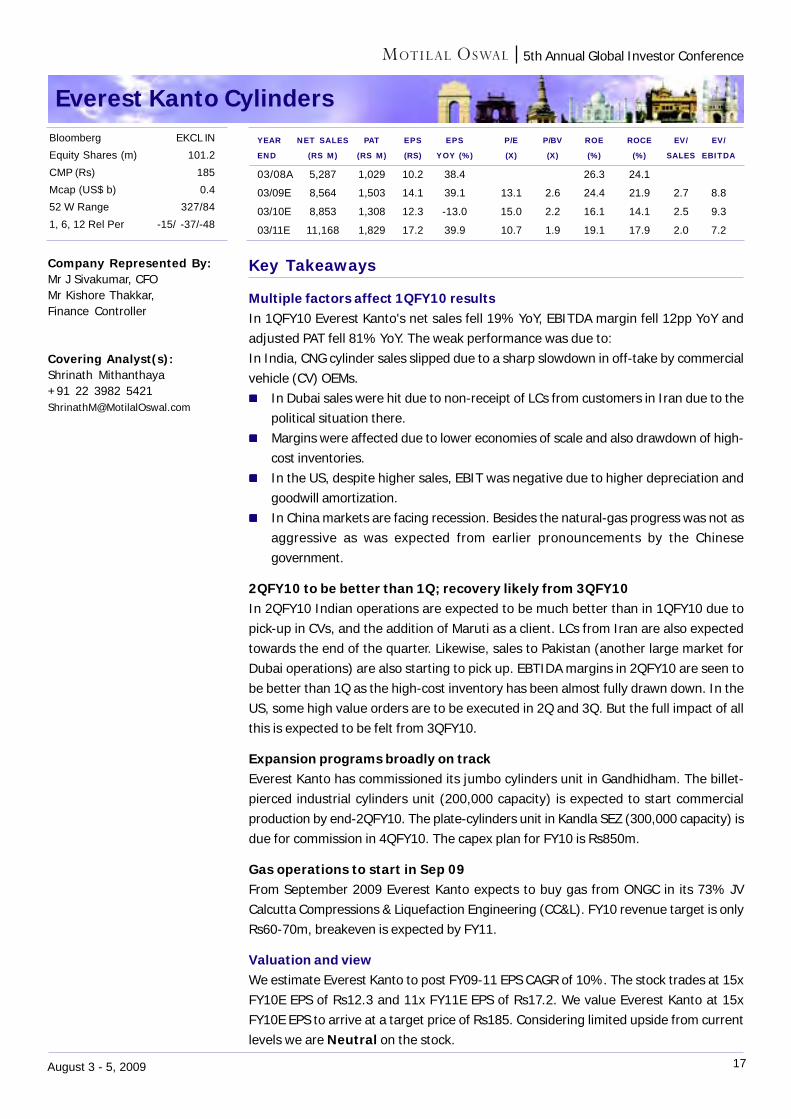

Multiple factors affect 1QFY10 resultsIn 1QFY10 Everest Kanto's net sales fell 19% YoY, EBITDA margin fell 12pp YoY andadjusted PAT fell 81% YoY. The weak performance was due to:In India, CNG cylinder sales slipped due to a sharp slowdown in off-take by commercialvehicle (CV) OEMs.

In Dubai sales were hit due to non-receipt of LCs from customers in Iran due to thepolitical situation there.Margins were affected due to lower economies of scale and also drawdown of high-cost inventories.In the US, despite higher sales, EBIT was negative due to higher depreciation andgoodwill amortization.In China markets are facing recession. Besides the natural-gas progress was not asaggressive as was expected from earlier pronouncements by the Chinesegovernment.

2QFY10 to be better than 1Q; recovery likely from 3QFY10In 2QFY10 Indian operations are expected to be much better than in 1QFY10 due topick-up in CVs, and the addition of Maruti as a client. LCs from Iran are also expectedtowards the end of the quarter. Likewise, sales to Pakistan (another large market forDubai operations) are also starting to pick up. EBTIDA margins in 2QFY10 are seen tobe better than 1Q as the high-cost inventory has been almost fully drawn down. In theUS, some high value orders are to be executed in 2Q and 3Q. But the full impact of allthis is expected to be felt from 3QFY10.

Expansion programs broadly on trackEverest Kanto has commissioned its jumbo cylinders unit in Gandhidham. The billet-pierced industrial cylinders unit (200,000 capacity) is expected to start commercialproduction by end-2QFY10. The plate-cylinders unit in Kandla SEZ (300,000 capacity) isdue for commission in 4QFY10. The capex plan for FY10 is Rs850m.

Gas operations to start in Sep 09From September 2009 Everest Kanto expects to buy gas from ONGC in its 73% JVCalcutta Compressions & Liquefaction Engineering (CC&L). FY10 revenue target is onlyRs60-70m, breakeven is expected by FY11.

Valuation and viewWe estimate Everest Kanto to post FY09-11 EPS CAGR of 10%. The stock trades at 15xFY10E EPS of Rs12.3 and 11x FY11E EPS of Rs17.2. We value Everest Kanto at 15xFY10E EPS to arrive at a target price of Rs185. Considering limited upside from currentlevels we are Neutral on the stock.

Company Represented By:Mr J Sivakumar, CFOMr Kishore Thakkar,Finance Controller

Covering Analyst(s):Shrinath Mithanthaya+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) YOY (%) (X) (X) (%) (%) SALES EBITDA

03/08A 5,287 1,029 10.2 38.4 26.3 24.1

03/09E 8,564 1,503 14.1 39.1 13.1 2.6 24.4 21.9 2.7 8.8

03/10E 8,853 1,308 12.3 -13.0 15.0 2.2 16.1 14.1 2.5 9.3

03/11E 11,168 1,829 17.2 39.9 10.7 1.9 19.1 17.9 2.0 7.2

Bloomberg EKCL INEquity Shares (m) 101.2CMP (Rs) 185Mcap (US$ b) 0.452 W Range 327/841, 6, 12 Rel Per -15/ -37/-48

18August 3 - 5, 2009

5th Annual Global Investor Conference

Financial Technologies

Key Takeaways

A unique business modelFinancial Technologies (FTIL) is the only integrated provider of exchanges,ecosystems and technology catering to market participants. It has 10 exchanges, 6ecosystem ventures and market leading position in products for exchanges andbrokerages like 'Dome' and 'Odin'.The company has a self-fueling business model with both the exchange andecosystem businesses feeding into each other.The management has a goal of having equal revenue contribution from technologyand exchanges over a longer term, and expects to grow through technology andmonetization of its stakes in exchanges.

Key differentiatorsDue to FTIL's extensive experience in the exchange business, its time to market is~1/3rd compared to that of competitors.FTIL requires lower investments to set up and run exchanges due to the use of in-house technology, which is ~1/10th of a comparable exchange.Capex requirement is up to US$10m for domestic exchanges, up to US$25m ininternational ventures and up to US$50m in exceptional ventures.

MCX continues its market leadership, MCX-SX showing strong tractionMCX's market share increased 100bp YoY to 86% in 1QFY10MCX-SX currently allows FX trading with regulatory approval expected shortly forequities, interest rate derivatives and bonds.The exchange currently enjoys 50% market share in currency trading with the other50% belonging to NSE.FTIL owns 31% in MCX and 49% in MCS-SX.

Ecosystem venturesFTIL has invested in eco system ventures to complement its exchanges business. Itcurrently has 6 such ventures in areas like warehousing, mobile payments, informationdissemination, services to credit markets, etc.With a warehousing capacity of 1.4m tons and 569 storage facilities, FTIL subsidiary,NBHC is the largest private player in warehousing related services.

Recent developmentsThe company intends to monetize its holding in MCX-SX to bring its stake in line withthe regulatory requirement of maximum 15% holding by one exchange in another, and5% by a corporate entity in an exchange. It expects this to happen by Aug-Sep 2009.

Valuation and viewFTIL stock currently trades at 28x FY09 earnings. Not rated.

Company Represented By:Ms Vaishali Kariya,SVP – Investor Relations

Covering Analyst(s):Ashwin Mehta+91 22 3982 [email protected]

Vihang Naik+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS ROE ROCE

END (RS M) (RS M) (RS) GR. (%) (%) (%)

3/06A 1,820 839 18.2 257.9 28.4 19.53/07A 2,645 1,036 20.3 11.6 22.3 8.83/08A 2,669 8,857 189.1 832.6 83.3 0.63/09A 3,164 2,457 53.5 -71.7 NA NA

Bloomberg FTECH INEquity Shares (m) 45.9CMP (Rs) 1,607Mcap (US$ b) 1.652 W Range 1625 / 3821, 6, 12 Rel Per 12 / 185 / 7

19August 3 - 5, 2009

5th Annual Global Investor Conference

Great Eastern Shipping

Key Takeaways

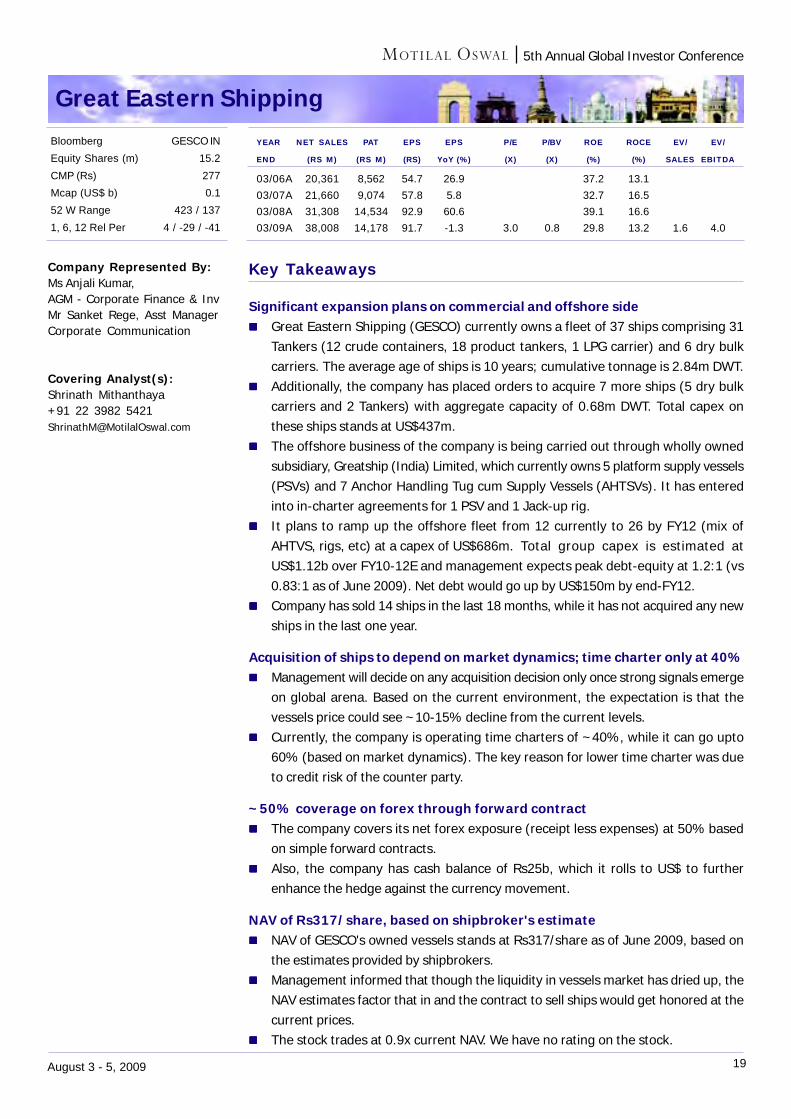

Significant expansion plans on commercial and offshore sideGreat Eastern Shipping (GESCO) currently owns a fleet of 37 ships comprising 31Tankers (12 crude containers, 18 product tankers, 1 LPG carrier) and 6 dry bulkcarriers. The average age of ships is 10 years; cumulative tonnage is 2.84m DWT.Additionally, the company has placed orders to acquire 7 more ships (5 dry bulkcarriers and 2 Tankers) with aggregate capacity of 0.68m DWT. Total capex onthese ships stands at US$437m.The offshore business of the company is being carried out through wholly ownedsubsidiary, Greatship (India) Limited, which currently owns 5 platform supply vessels(PSVs) and 7 Anchor Handling Tug cum Supply Vessels (AHTSVs). It has enteredinto in-charter agreements for 1 PSV and 1 Jack-up rig.It plans to ramp up the offshore fleet from 12 currently to 26 by FY12 (mix ofAHTVS, rigs, etc) at a capex of US$686m. Total group capex is estimated atUS$1.12b over FY10-12E and management expects peak debt-equity at 1.2:1 (vs0.83:1 as of June 2009). Net debt would go up by US$150m by end-FY12.Company has sold 14 ships in the last 18 months, while it has not acquired any newships in the last one year.

Acquisition of ships to depend on market dynamics; time charter only at 40%Management will decide on any acquisition decision only once strong signals emergeon global arena. Based on the current environment, the expectation is that thevessels price could see ~10-15% decline from the current levels.Currently, the company is operating time charters of ~40%, while it can go upto60% (based on market dynamics). The key reason for lower time charter was dueto credit risk of the counter party.

~50% coverage on forex through forward contractThe company covers its net forex exposure (receipt less expenses) at 50% basedon simple forward contracts.Also, the company has cash balance of Rs25b, which it rolls to US$ to furtherenhance the hedge against the currency movement.

NAV of Rs317/share, based on shipbroker's estimateNAV of GESCO's owned vessels stands at Rs317/share as of June 2009, based onthe estimates provided by shipbrokers.Management informed that though the liquidity in vessels market has dried up, theNAV estimates factor that in and the contract to sell ships would get honored at thecurrent prices.The stock trades at 0.9x current NAV. We have no rating on the stock.

Company Represented By:Ms Anjali Kumar,AGM - Corporate Finance & InvMr Sanket Rege, Asst ManagerCorporate Communication

Covering Analyst(s):Shrinath Mithanthaya+91 22 3982 [email protected]

Bloomberg GESCO INEquity Shares (m) 15.2CMP (Rs) 277Mcap (US$ b) 0.152 W Range 423 / 1371, 6, 12 Rel Per 4 / -29 / -41

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) YoY (%) (X) (X) (%) (%) SALES EBITDA

03/06A 20,361 8,562 54.7 26.9 37.2 13.103/07A 21,660 9,074 57.8 5.8 32.7 16.503/08A 31,308 14,534 92.9 60.6 39.1 16.603/09A 38,008 14,178 91.7 -1.3 3.0 0.8 29.8 13.2 1.6 4.0

20August 3 - 5, 2009

5th Annual Global Investor Conference

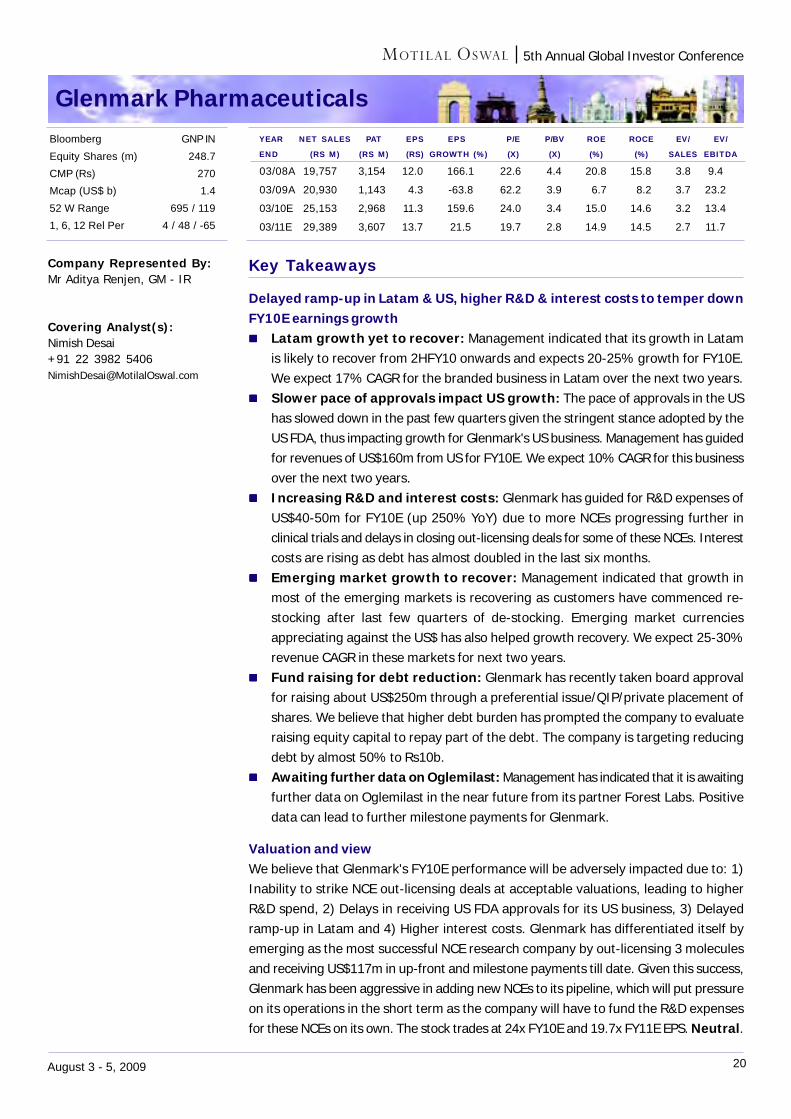

Glenmark Pharmaceuticals

Key Takeaways

Delayed ramp-up in Latam & US, higher R&D & interest costs to temper downFY10E earnings growth

Latam growth yet to recover: Management indicated that its growth in Latamis likely to recover from 2HFY10 onwards and expects 20-25% growth for FY10E.We expect 17% CAGR for the branded business in Latam over the next two years.Slower pace of approvals impact US growth: The pace of approvals in the UShas slowed down in the past few quarters given the stringent stance adopted by theUS FDA, thus impacting growth for Glenmark's US business. Management has guidedfor revenues of US$160m from US for FY10E. We expect 10% CAGR for this businessover the next two years.Increasing R&D and interest costs: Glenmark has guided for R&D expenses ofUS$40-50m for FY10E (up 250% YoY) due to more NCEs progressing further inclinical trials and delays in closing out-licensing deals for some of these NCEs. Interestcosts are rising as debt has almost doubled in the last six months.Emerging market growth to recover: Management indicated that growth inmost of the emerging markets is recovering as customers have commenced re-stocking after last few quarters of de-stocking. Emerging market currenciesappreciating against the US$ has also helped growth recovery. We expect 25-30%revenue CAGR in these markets for next two years.Fund raising for debt reduction: Glenmark has recently taken board approvalfor raising about US$250m through a preferential issue/QIP/private placement ofshares. We believe that higher debt burden has prompted the company to evaluateraising equity capital to repay part of the debt. The company is targeting reducingdebt by almost 50% to Rs10b.Awaiting further data on Oglemilast: Management has indicated that it is awaitingfurther data on Oglemilast in the near future from its partner Forest Labs. Positivedata can lead to further milestone payments for Glenmark.

Valuation and viewWe believe that Glenmark's FY10E performance will be adversely impacted due to: 1)Inability to strike NCE out-licensing deals at acceptable valuations, leading to higherR&D spend, 2) Delays in receiving US FDA approvals for its US business, 3) Delayedramp-up in Latam and 4) Higher interest costs. Glenmark has differentiated itself byemerging as the most successful NCE research company by out-licensing 3 moleculesand receiving US$117m in up-front and milestone payments till date. Given this success,Glenmark has been aggressive in adding new NCEs to its pipeline, which will put pressureon its operations in the short term as the company will have to fund the R&D expensesfor these NCEs on its own. The stock trades at 24x FY10E and 19.7x FY11E EPS. Neutral.

Company Represented By:Mr Aditya Renjen, GM - IR

Covering Analyst(s):Nimish Desai+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

03/08A 19,757 3,154 12.0 166.1 22.6 4.4 20.8 15.8 3.8 9.4

03/09A 20,930 1,143 4.3 -63.8 62.2 3.9 6.7 8.2 3.7 23.2

03/10E 25,153 2,968 11.3 159.6 24.0 3.4 15.0 14.6 3.2 13.4

03/11E 29,389 3,607 13.7 21.5 19.7 2.8 14.9 14.5 2.7 11.7

Bloomberg GNP INEquity Shares (m) 248.7CMP (Rs) 270Mcap (US$ b) 1.452 W Range 695 / 1191, 6, 12 Rel Per 4 / 48 / -65

21August 3 - 5, 2009

5th Annual Global Investor Conference

GMR Infrastructure

Key Takeaways

Power portfolio progress on track; strategy to keep ~40% under merchantbasis

In the power sector, GMR is looking at opportunities to buy-out projects which arestalled for funds. Recently, GMR Energy acquired 100% stake in EMCO Energy, whichis developing 600 MW coal based power plant in Maharashtra. Construction onproject is expected to begin in 3QFY10.GMR plans to keep ~60% of its power portfolio under long-term Power PurchaseAgreement (PPA), and the balance 40% on merchant basis.PPA has been signed for Kamalanga project (~30% of capacity) in Orissa and returnfor the same is based on new tariff norms i.e. 16% RoE, plus incentives. 350MWhas been sold out under Case 1 bidding to Haryana SEB, and balance will be kept onmerchant basis.

Roads projects portfolioGMR has commissioned Tindivanam-Ulundurpet highway project in July 2009 andwith this all its 6 roads projects are operational.Recently, it has emerged as preferred bidder for Hyderabad-Vijayawada road project(cost of Rs22b, 32% revenue sharing) and Chennai Outer Ring Road (cost of Rs11b,grant of Rs3b). The Hyderabad-Vijayawada project is toll-based, while the Chennaiproject is annuity-based (Rs621m semi-annually).

Real estate monetization at both airports to gain momentumSeven plots (22.5 acres) of land at Delhi airport have already been monetized,while it is in final negotiation for the eight plot of 7.7 acres. Total upfront deposit isexpected at Rs13-15b. Lease rental for first full year of operations for 30 acres isexpected to be ~Rs450-460m, to be escalated at 6.5% pa.At Hyderabad airport, an aviation SEZ is planned on 250 acres (MRO business +Aviation academy), while plans are on for additional 250 acres SEZ.Of the balance 1,000 acres at Hyderabad airport, 25 acres is being planned ashealth corridor (hospital, research facilities, etc) in discussion with several parties.For the balance land, development plan is being worked out.

Valuation and viewWe expect GMR's consolidated FY10 PAT at Rs1.5b and FY11 Rs2b. Based on SOTPvaluation methodology, we arrive at a target price of Rs105/share. We are Neutral onthe stock.

Company Represented By:Mr GBS Raju, DirectorMr Subba Rao Amarthaluru,CFO - Corp. Group IntegrationMr Ashutosh Aggarwala,CFO - Corp. Strategic FinanceMr Gaurang Vasani,Associate General ManagerStrategic Finance

Covering Analyst(s):Satyam Agarwal+91 22 3982 [email protected]

Nalin Bhatt+91 22 3982 [email protected]

Bloomberg GMRI INEquity Shares (m) 1820.7CMP (Rs) 140Mcap (US$ b) 5.452 W Range 184 / 461, 6, 12 Rel Per -8 / 26 / 27

YEAR NET SALES* PAT* EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

3/07A 16,967 1,744 1.1 - 133.2 11.7 8.8 6.9 15.0 46.73/08A 22,948 2,101 1.2 9.5 121.6 4.2 3.4 3.2 13.1 50.33/09E 40,192 2,795 1.5 32.1 92.0 4.0 4.4 4.0 7.9 29.93/10E 41,303 4,017 2.2 43.7 64.1 3.8 6.0 6.9 8.7 17.4

22August 3 - 5, 2009

5th Annual Global Investor Conference

Godrej Consumer Products

Key Takeaways

Value-for-money positioning boosts soap volumesGodrej Consumer's value-for-money positioning has helped it to post volume growthof 18% YoY in FY09 and 15% in 1QFY10. Good product quality (76% TFM), increaseddistribution and initiatives like low-priced packs (Rs5 SKU) have been key growthdrivers. The company is focusing on Godrej No1, which accounts for 60% of volumes.Palm-oil prices (22% of sales) are 40% down YoY, which will boost company marginsin FY10. GCPL entered into a long-term forward contract and booked its requirementsuntil January-February 2010. This will ensure margin-expansion through FY10.

Hair-color sales revive, reflect in market-share gainsInitiatives such as the re-launch of Godrej powder hair dye as Godrej Expert, launchof Renew powder hair dye and a 5% increase in trade margins have helped GCPLrevive hair-color sales and enhance market share.The management believes there is potential to upgrade consumers from unbrandedmehendi to branded mehendi, especially as GCPL expands in rural India.Management indicated that it is focusing on the hair-color market and is open toacquisitions in this segment

International businessHigher sales of Cuticura hand wash (anti-bacterial), as the swine flu scare increasedin Britain, drove Keyline's performance. With integration issues with Kinky sortedout, performance is expected to improve. GCPL plans to invest in enhancingdistribution in South Africa, which has big potential for hair-care products.The international market accounts for 25% of GCPL's revenue and this is indicatedto rise to 50% in the next three years through acquisitions in the hair-color category.

Godrej Sara LeeGCPL will continue to hold 49% in the Godrej Sara Lee JV after the current scheme ofarrangement. Acquisition of the remaining stake will be triggered after Sara Lee Global(US$2b turnover) plans to sell its global business. The valuation will be based on a pre-arranged price finalized at the time of entering into the JV. GCPL will get rights to SaraLee products only for the Indian markets.

Valuation and viewWe estimate 27.8% EPS CAGR for FY09-11. We estimate FY10 and FY11 EPS at Rs9.4and Rs10.9, excluding the acquisition of 49% stake in Godrej Sara Lee. The stock tradesat 23.8x FY10E and 20.4xFY11E EPS. We believe that acquisition of the remaining 51%in Godrej Sara Lee can re-rate the stock. Maintain Buy.

Company Represented By:Mr H K Press, Vice Chairman

Covering Analyst(s):Amnish Aggarwal+91 22 3982 [email protected]

Amit Purohit+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

03/08A 11,040 1,592 7.1 18.6 31.6 33.5 92.8 64.4 4.7 24.0

03/09A 13,930 1,726 6.7 -5.2 33.3 9.7 29.0 27.8 4.0 27.2

03/10E 16,344 2,414 9.4 40.0 23.8 8.5 35.6 36.2 3.4 18.1

03/11E 18,748 2,820 10.9 16.8 20.4 7.4 36.2 37.6 2.9 15.2

Bloomberg GCPL INEquity Shares (m) 258.1CMP (Rs) 223Mcap (US$ b) 1.252 W Range 250 / 901, 6, 12 Rel Per 23 / -6 / 78

23August 3 - 5, 2009

5th Annual Global Investor Conference

Grasim Industries

Key Takeaways

Cautious outlook for core businessExpects the cement industry to grow at 9% in FY10 (v/s 12.2% in 1QFY10). Thisalong with expected excess capacities from 2HFY10 will put pressure on prices.The management expects realization (+Rs5/bag QoQ in 2QFY10) and margins toimprove from 1QFY10 levels. But it is uncertain that it will sustain beyond 2QFY10especially because of the widening price differential between competing fibers,increased excise duty by 4-8% and the start of a downward trend in China.

Capex nearly completeCapex plan to add 14MT capacity would be completed by 3QFY10, taking total capacityto 49MT. Most of its capacity enhancement program has been completed and a 3MTgrinding unit at its Kotputli plant is expected to be commissioned in 3QFY10.Grasim will invest Rs43.3b over FY10-11 to augment its logistics infrastructure,waste heat recovery system, CPP, evacuation facility and on modernization.As a result, Grasim is seen to substantially increase its free cash flow from FY10(estimated at Rs45.7b in FY10 v/s Rs9.8b in FY09).

Cost savings to result in stable margins in FY10Stabilization of production at its recently expanded capacities will drive the group'svolume growth. It expects to gain market share as its volumes will grow faster thanthat of the industry.Softening of imported coal/pet coke prices (50% dependence) will benefit Grasim.Its commissioning of new CPPs 263MW (incl 40MW waste-heat recovery system)will increase its reliance on CPP to 80%.Grasim will also cut logistic costs. It will reduce the lead distance to its plants whenit opens new units and will enhance its logistics infrastructure by expanding thejetty at its Gujarat plant and setting up bulk terminals.

Other takeawaysStrong growth in rural/semi-urban markets has led to an increase in its share to30% from 12% earlier.No pick-up yet from organized real-estate sector.South India most prone to pricing power based on overcapacity.

Valuation and viewThe outlook for Grasim's core business has improved with higher volumes in VSF andhigher pricing in the cement business. Grasim is best placed among its peers, as thereis high visibility for volume growth and cost-savings triggers The stock is quoting at 9xFY10E consolidated EPS and 4.7x EV/EBTIDA. Maintain Buy.

Company Represented By:Mr Adesh Gupta, CFO

Covering Analyst(s):Jinesh Gandhi+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END* (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

03/08A 169,739 26,951 293.9 37.0 9.6 2.8 34.3 31.1 2.0 6.7

03/09A 184,039 21,867 238.5 -18.9 11.9 2.2 21.1 20.7 1.8 7.6

03/10E 202,243 28,846 314.6 31.9 9.0 1.8 22.2 24.8 1.4 4.7

03/11E 210,694 26,475 288.7 -8.2 9.8 1.6 15.8 24.1 1.2 4.5

Bloomberg GRASIM INEquity Shares (m) 91.7CMP (Rs) 2,829Mcap (US$ b) 5.552 W Range 2940 / 8241, 6, 12 Rel Per 10 / 38 / 34

* Consolidated

24August 3 - 5, 2009

5th Annual Global Investor Conference

GVK Power & Infrastructure

Key Takeaways

Roads and power are focus areasGVK Power & Infrastructure (GVKPIL) has identified roads and power sectors asfocus areas for the medium term. The company has taken a stance to participate inbidding for new road projects but with desired level of profitability (RoE of 16%+).In power, the company is open to inorganic growth and is evaluating acquisition ofinterest in a few projects. The company has been approached by various projectdevelopers with project sizes ranging from 600-1200MW. The company is in theprocess of obtaining necessary clearances.Additionally, the company is exploring capacity expansion at Gautami power projectby 800MW and JP Phase II by 400MW, given that land and other clearances are inplace.

Gas supply at existing projects in place, merchant sale clearance is expectedany time in 2QFY10

Gas supply at all three operating power projects, viz, JP Phase I & II and Gautami isavailable for 100% capacity and plants are currently operating at a PLF of 88-99%.Merchant sale from JP II and Gautami power project is expected to begin only from3QFY10 (hearing on 18th August 2009), as management expects approval for saleof merchant power by end 2QFY10.

Cash balance at ~Rs10b; no plans to divest stake in JKELCash on books as at June 2009 stands at Rs10b, and GVKPIL is fairly placed to meetequity funding over next two years towards existing projects. Estimated equityfounding requirement is Rs3-3.5b each in FY10 and FY11.The company is not looking to divest its stake in JKEL currently and if found attractive,it may securitize cash flows from the project.

Real estate monetization at Mumbai airport to begin from FY10Master plan for development is now completed with plots/zones identified for variouspurposes falling under commercial real estate development. GVKPIL is likely tomonetize 0.5msf by March 2010.Slum rehabilitation by HDIL is progressing with minor delay. Total ~20,000 familieswill be rehabilitated by HDIL.

Valuation and viewWe expect GVKPIL to report PAT of Rs2.5b in FY10 (up 136%) and Rs3.2b in FY11(up 26%). Maintain Buy with SOTP based target price of Rs54/share.

Company Represented By:Ms Mala Paropkari,Vice President - IRMr Viren Vijaya Shankar,Senior Manager - IR

Covering Analyst(s):Satyam Agarwal+91 22 3982 [email protected]

Nalin Bhatt+91 22 3982 [email protected]

Bloomberg GVKP INEquity Shares (m) 1,579CMP (Rs) 44Mcap (US$ b) 1.652 W Range 51 / 101, 6, 12 Rel Per -5 / 58 / 3

YEAR NET SALES* PAT* EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

3/08A 4,700 1,361 1.0 -34.6 45.3 2.8 6.2 4.6 3.7 9.33/09A 5,138 1,076 0.8 -20.9 57.2 2.7 4.7 2.1 6.7 19.53/10E 23,726 2,543 1.6 110.5 27.2 2.1 7.9 6.8 2.1 6.33/11E 25,014 3,192 2.0 7.4 21.7 2.0 9.2 6.3 2.4 7.3

*Consolidated

25August 3 - 5, 2009

5th Annual Global Investor Conference

HDFC Bank

Key Takeaways

Business environment favorable for HDFC BankMr Puri remains optimistic about India's growth prospects. He believes that theworst is behind for the economy and the banking industry.In India, demand for banking services remains higher than supply, and this willcontinue to provide significant opportunities for banks.The overall business environment remains favorable for HDFC Bank.

Focus on retail assets and liabilitiesPost merger with CBoP, HDFC Bank is in much better shape to grow its retail liabilities.Customer segmentation, product diversification, effective utilization of technology,and immaculate execution would continue to remain the key success factors for thebank.The bank will stick to its strategy of growing its middle and upper middle incomecustomer segments.

HDFC Bank will maintain above industry growth ratesIndustry loan growth is likely to be 18-20% in FY10 and HDFC Bank would maintainhigher than industry growth.Retail loans and working capital demand would continue to drive loan growth forHDFC Bank. However, corporate loan growth is likely to be higher than the growth inretail loans considering the rundowns in the acquired CBoP loan book.

Worst is behind on NPA front; equity dilution unlikely in next 3 yearsMr Puri believes that NPAs for HDFC Bank are near peak and upside from the currentlevels is very limited.HDFC Bank would not need equity capital for the next three years to manage itsgrowth.The bank is not considering international expansion, as the domestic economy offersimmense opportunities.

Valuation and viewWe expect HDFC Bank to report EPS of Rs63 in FY10 and Rs84 in FY11.BV would be Rs462 in FY10 and Rs528 in FY11.Stock trades at 3.1x FY11E BV and 17.2x FY11E EPS. Maintain Neutral as valuationsare fair.

Company Represented By:Mr Aditya Puri, MDMr Paresh Sukthankar, ED

Covering Analyst(s):Ajinkya Dhavale+91 22 3982 [email protected]

Alpesh Mehta+91 22 3982 [email protected]

YEAR NET INCOME PAT EPS EPS P/E P/BV CAR ROAE ROAA P/ABV

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) (%) (X)

3/08A* 88,403 17,530 41.3 22.1 35.0 4.5 13.6 16.2 1.3 4.6

3/09A 107,118 22,449 52.8 27.7 27.4 4.1 15.7 15.6 1.3 4.2

3/10E 129,473 28,494 63.1 19.6 22.9 3.1 15.2 15.9 1.4 3.2

3/11E 157,492 37,942 84.0 33.2 17.2 2.7 14.1 17.0 1.6 2.8

Bloomberg HDFCB INEquity Shares (m) 451.6CMP (Rs) 1,448Mcap (US$ b) 13.852 W Range 1584 / 7741, 6, 12 Rel Per -12 / -11 / 16

* Includes pro forma merged figures for HDFC Bank and CBoP

26August 3 - 5, 2009

5th Annual Global Investor Conference

HDFC Standard Life

Key Takeaways

The management's focus remains on profitable growth; market share is currentlylow priority. However, accounting break-even is expected to be a couple of yearsaway from now. (HDFC Standard Life reported a loss of Rs5b in FY09.)FY09 was the worst year for the company as business environment deterioratedsignificantly, soon after rapid expansion in branches/manpower, and massive adspends. This, coupled with deterioration in persistency ratio (dropped from 86% inFY08 to 65% in FY09), led to doubling of losses despite maintaining new businesspremium.The management's present focus is to optimize cost structure and improve efficiencyrather than go in for geographical expansion. It believes over the long term, salesand service would be the key differentiator among insurance companies.In management's view, the recently announced cap on charges for ULIP productswould certainly have impact on overall business profitability for all the players butquantifying the same is difficult at this point of time. However, structurally, thismove is a positive for customers and would lead to rationalization of distributioncommissions and other operating costs of life insurance companies.The management believes that life insurance business in India can sustain 10-15%growth, and that HDFC Standard Life would strive to grow in line with industry goingforward.

Company Represented By:Mr Paresh Parasnis,Principal officer and EDMs Vibha Padalkar, CFO

Covering Analyst(s):Ajinkya Dhavale+91 22 3982 [email protected]

Alpesh Mehta+91 22 3982 [email protected]

27August 3 - 5, 2009

5th Annual Global Investor Conference

Hero Honda Motors

Key Takeaways

Conservative guidanceThe company's conservative guidance of 4m units in FY10 is based on:

Uncertainty of the monsoon, the impact of which will be seen from 3QFY10Withdrawal of excise duty reduction can have short-term impactMore competition

However the management will review its guidance at the end of 1HFY10 and expectsthe following factors to positively impact volumes:

Any improvement in financeHigher government spending in rural areasLower channel inventory of 180,000 units against normal levels of 250,000-275,000 units

EBITDA margins should improve 2QFY10EBITDA margins at 16.8% in 1QFY10 will improve in 2QFY10 because:

Volumes in 2QFY10 will be higher than 1.1m units in 1QFY10Advertising spends at Rs500m in 1QFY10 will be lower in 2QFY10 as there areno special events, such as the IPL and the 20-20 World Cup, in the quarter.

The management doesn't expect commodity prices to rise substantially in the shortterm. It sources its monthly raw material requirement on a spot basis.

Haridwar plansThe company plans to add a fourth line at Haridwar, enhancing output to meetdemand.The company produces 4,000 units a day (about 350,000 units per quarter).Hero Honda makes Splendor at Haridwar and will produce Passion there as well.Vendor localization at Haridwar will increase from 30% to 65% by 3QFY10.

Other takeawaysStrong demand for some of its brands, such as Passion, is leading to a shortage.Plans to launch nine products (including a new model) from September will drivegrowth.Hero Honda plans 22 Just For Her scooter showrooms catering exclusively to women.Hero Honda and HMSI have a non-competing product portfolio.

Valuation and viewRecovery in domestic and export volumes coupled with higher hedged forex rates willhelp profitability. Continued volume improvement and recovery in market share will bea catalyst for the stock. The stock trades at 16x FY10E EPS and 14.6x FY11E EPS.Maintain Buy.

Company Represented By:Mr Ravi Sud, SVP & CFO

Covering Analyst(s):Jinesh Gandhi+91 22 3982 [email protected]

YEAR NET SALES PAT EPS EPS P/E P/BV ROE ROCE EV/ EV/

END (RS M) (RS M) (RS) GROWTH (%) (X) (X) (%) (%) SALES EBITDA

3/08A 103,318 9,679 48.5 12.8 29.4 9.5 35.5 45.7 2.5 19.2

3/09A 123,191 12,818 64.2 32.4 25.0 8.4 37.8 47.9 2.3 16.5

3/10E 149,946 19,968 100.0 55.8 16.0 6.1 44.3 53.7 1.8 10.9

3/11E 166,289 21,998 110.2 10.2 14.6 4.7 36.7 44.8 1.5 9.4

Bloomberg HH INEquity Shares (m) 199.7CMP (Rs) 1,604Mcap (US$ b) 6.752 W Range 1780 / 6611, 6, 12 Rel Per 5 / 8 / 87

28August 3 - 5, 2009

5th Annual Global Investor Conference

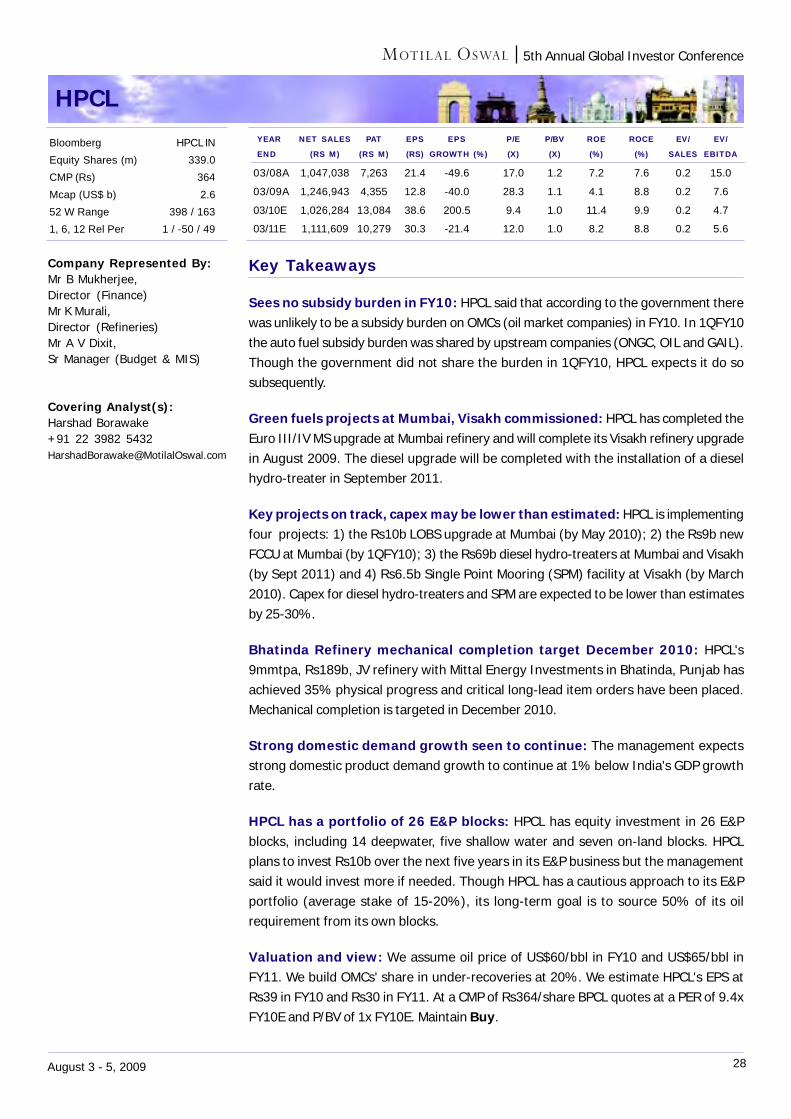

HPCL

Key Takeaways

Sees no subsidy burden in FY10: HPCL said that according to the government therewas unlikely to be a subsidy burden on OMCs (oil market companies) in FY10. In 1QFY10the auto fuel subsidy burden was shared by upstream companies (ONGC, OIL and GAIL).Though the government did not share the burden in 1QFY10, HPCL expects it do sosubsequently.

Green fuels projects at Mumbai, Visakh commissioned: HPCL has completed theEuro III/IV MS upgrade at Mumbai refinery and will complete its Visakh refinery upgradein August 2009. The diesel upgrade will be completed with the installation of a dieselhydro-treater in September 2011.

Key projects on track, capex may be lower than estimated: HPCL is implementingfour projects: 1) the Rs10b LOBS upgrade at Mumbai (by May 2010); 2) the Rs9b newFCCU at Mumbai (by 1QFY10); 3) the Rs69b diesel hydro-treaters at Mumbai and Visakh(by Sept 2011) and 4) Rs6.5b Single Point Mooring (SPM) facility at Visakh (by March2010). Capex for diesel hydro-treaters and SPM are expected to be lower than estimatesby 25-30%.

Bhatinda Refinery mechanical completion target December 2010: HPCL's9mmtpa, Rs189b, JV refinery with Mittal Energy Investments in Bhatinda, Punjab hasachieved 35% physical progress and critical long-lead item orders have been placed.Mechanical completion is targeted in December 2010.

Strong domestic demand growth seen to continue: The management expectsstrong domestic product demand growth to continue at 1% below India's GDP growthrate.