post graduate diploma in islamic banking &...

TRANSCRIPT

www.alhudacibe.com/dlp

Flexible - Elegant - Convenient & Self-Managed Study

CENTRE OF ISLAMICBANKING & ECONOMICS

Simply the best Automated Learning Solution

POST GRADUATE DIPLOMA IN ISLAMIC BANKING & FINANCE

IB&F: 410: Sukuk (Islamic Bond)

SUKUK, ISLAMIC FUND & INVESTMENTS

AlHuda CIBE

SUKUK(ISLAMIC BOND)

IB&F: 410

"I believe in efficiency of markets, also Islamic markets, and I am pretty sure that the market will come to a certain consensus."

Geert Bossuyt, Deutsche Bank

C O N T E N T S

www.alhudacibe.com/dlp

01

27

30

11

22

29

30

l· Sukuk (Islamic Bond)l· A Glance at the Global Sukuk Marketl· Mechanism & structuring of Sukukl· Sukuk Structure Modelsl· Case Studyl· Summaryl· Discussion Questionsl· Supplement Material

13

01

SUKUK (ISLAMIC BOND)

Sukuk Market Overview

Recent innovations in Islamic finance have changed the dynamics of the Islamic finance industry. Especially in the area of bonds and securities the use of Sukuk or Islamic securities has become increasingly popular in the last few years, both as a means of raising government finance through sovereign issues, and as a way of companies obtaining funding through the offer of corporate Sukuk.

Beginning modestly in 2000 with total three Sukuk worth $336 millions the total number Sukuk by in first 9 months of 2011 has reached to USD 63 bn. (Figures by Adnan Halawi, Team leader – Fixed Income, Zawya).Sukuk has developed as one of the most significant mechanisms for raising finance in the international capital markets through islamically acceptable structures. Multinational corporations, sovereign bodies, state corporations and financial institutions use international Sukuk issuance as an alternative to syndicated financing.

IB&F: 410: Sukuk

Basics of Sukuk

Sukuk (plural of word Sukk) were extensively used by Muslims in the middle Ages as papers representing financial obligations originating from trade and other commercial activities. However, the present structure of Sukuk are different from the Sukuk originally used and are akin to the conventional concept of securitization, a process in which ownership of the underlying assets is transferred to a large number of investors through certificates representing proportionate value of the relevant assets.

Sukuk is popularly known as an Islamic or Shari'ah compliant 'Bond' whilst in actual fact and it is an asset-backed trust certificate. In its simplest form Sukuk is a certificate evidencing ownership of an asset or its usufruct. The Sukuk structures rely on the creation of a Special Purpose Vehicle (SPV). SPV would issue Sukuk certificates which represent for example the ownership of an asset, entitlement to a debt or to rental incomes or even accumulation of returns from various Sukuk (a hybrid Sukuk). The return provided to Sukuk holders therefore come in the form of profit from a sale, rental or a combination of both. Sukuk could be based on Mudaraba, Musharaka, Murabaha, Salam, Istisna, Ijarah or hybrid of these.

02

Sukuk is popularly

known as an Islamic

or Sharia’h

compliant ‘Bond’

whilst in actual fact

and it is an asset-

backed trust

certificate.

TIP

Glossary:

Sukuk: Sukuk (plural of Sak) is an Arabic word which means (Certificates). It has

similar characteristics to that of a conventional bond with the difference being

that they are asset backed; Sukuk represents proportionate beneficial ownership

in the underlying asset.

Securitization: Securitization refers to a process of converting something into

cash or cash equivalent in the form of papers that are tradable in the secondary

market.

Special Purpose Vehicle: The Special Purpose Vehicle is usually a subsidiary

company with an asset/liability structure and legal status that makes its

obligations secure even if the parent company goes bankrupt.

IB&F: 410: Sukuk

03

Definition of Sukuk

Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) defines Sukuk as being:

“Certificates of equal value representing after closing subscription, receipt of the value of the certificates and putting it to use as planned, common title to shares and rights in tangible assets, usufructs and services, or equity of a given project or equity of a special investment activity”.

Benefits and Features

Sukuk is tradable Shari'ah-compliant capital marketproduct which provides medium to long-term fixed or variable rates of return. They are assessed and rated by international rating agencies, which investors use as a guideline to assess risk/return parameters of a Sukuk issue. Sukuk gives regular periodic income streams during the investment period with easy and efficient settlement and a possibility of capital appreciation of

Keep In Mind

The Sukuk structures rely on the creation of a Special Purpose Vehicle (SPV).

SPV would issue Sukuk certificates which represent for example the

ownership of an asset, entitlement to a debt or to rental incomes or even

accumulation of returns from various Sukuk (a hybrid Sukuk).

Glossary:

Capital Market: Capital Market is the market in which long-term financial

securities are traded.

Capital Appreciation: A rise in the value of an asset based on a rise in market price.

Essentially, the capital that was invested in the security has increased in value, and

the capital appreciation portion of the investment includes all of the market value

exceeding the original investment or cost basis. Capital appreciation is one of the

two main sources of investment returns, with the other being dividend or interest

income.

Secondary Market: Secondary market is a market where previously issued

securities are traded.

IB&F: 410: Sukuk

the Sukuk. Sukuk are liquid instruments which are tradable in secondary market.

Difference between Conventional Bond and Sukuk

A bond is a contractual debt obligation whereby the issuer is contractually obliged to pay to bondholders, on certain specified dates, interest and principal.

In Sukuk structure the Sukuk holders each hold an undivided beneficial ownership in the underlying assets. Consequently, Sukuk holders are entitled to share in the revenues generated by the Sukuk assets as well as being unrestricted to share in the proceeds of the realization of the Sukuk assets. Sukuk in general may be understood as a Sharia'h compliant 'Bond'. The claim embodied in Sukuk is not simply a claim to cash flow but an ownership claim. This also differentiates Sukuk from conventional bonds as the latter proceed over interest bearing securities, whereas Sukuk are basically investment certificates consisting of ownership claims in a pool of assets.

04

The claim embodied

in Sukuk is not

simply a claim to

cash flow but an

ownership claim.

TIP

Keep In Mind

The claim embodied in Sukuk is not simply a claim to cash flow but an

ownership claim. This also differentiates Sukuk from conventional bonds as

the latter proceed over inte rest bearing securities, whereas Sukuk are

basically investment certificates consisting of ownership claims in a pool of

assets.

IB&F: 410: Sukuk

05

IB&F: 410: Sukuk

Similarities between Conventional Bond and Sukuk

There are some similarities between conventional bonds and Sukuk. The similarities are as follows:

n Marketability: Sukuk are floated in real assets that are liquid, easily transferred and traded in the financial markets.

n Ratability: Sukuk can be easily rated.n Enhance ability: Different Sukuk structures may allow for credit

enhancements.n Versatility: The variety of Sukuk structures (as many as over 27

possibilities).

06

IB&F: 410: Sukuk

Steps of Issuance of Sukuk

Sukuk are issued in a systematic way. The procedure is as follows:

n Preparing a detailed feasibility study (stating clear objectives to be achieved from the proposed Shari'ah-compliant business) and setting up of general framework and organizational structure to support the issuance process.

n Working out an appropriate Shari'ah structure to achieve the set objectives in compliance with Shari'ah.

n Arranging lead manager(s) to underwrite the Sukuk issue.n Arranging legal documentation around the agreed Shari'ah

structures (both from the Issuer's as well as arranger's perspective).n Setting up the SPV to represent the investors (Sukuk holders) and

putting the Sukuk into circulation.

Parties Involved in Sukuk

There are basically four parties involved in Sukuk. The parties are:

Originator: He is the initiator and owner of asset which will be used to issue Sukuk.

SPV: Special purpose vehicle or company is the intermediary company that works between the Sukuk holder and Originator. This company receives the amount form investors and pays to the originator of Sukuk and buy the ownership of that asset and it transform to Sukuk holders and also make a checkup on both parties and asset maintenance etc.

Investors: There are two types of investor that invest in Sukuk as primary and secondary market. They also are actual owner of specific portion of assets and free to sell it at any time in secondary market. And enjoy the profit in term of rent or profit at the end of month quarter, semi yearly or yearly basis.

Banks: Banks perform as Receiving and paying agent and provide security to both parties.

07

Parties involves in

Sukuk are:

originator, SPV,

Investors and bank.

TIP

IB&F: 410: Sukuk

08

Role of Sharia'h Advisors in Sukuk Issuance

Sharia'h advisor (Sharia'h scholars or Sharia'h advisory firms with recourse to Sharia'h scholars) have a significant role to play. Amongst others, following may be listed as examples:

n Advising on proposed Sukuk structure and suggest a Sharia'h structure which otherwise fulfils the set economic aims;

n Working closely with legal counsel of the issuer to ensure that the legal documents are in line with Sharia'h Principles.

There are some Shari'ah requirements as well, they are:

n Working closely with legal counsel of the arranger to ensure that the legal documents are in line with Sharia'h requirements.

n Issuing Fatwa on the whole Sukuk deal before the same can be put into circulation.

Uses of Sukuk Funds

The most common uses of Sukuk can be named as project specific, asset-specific, and balance sheet specific.

Project-Specific Sukuk

Under this category money is raised through Sukuk for specific project. For example, WAPDA has issued its first Sukuk in Pakistan in 2006 worth of Rs.8, 000 million to raise fund for upgrading the Mangla Dam for 7

Project-Specific

Sukuk is used to

raise money for

some specific

project.

TIP

Glossary:

Fatwa: A non-binding legal opinion giving by a Muslim jurist qualified to give such

opinions (a mufti).

KIBOR: KIBOR stands for Karachi Interbank Offering Rate. KIBOR is the average

asking price of the loans to be made by one bank to another, it has nothing to do

with the banks lending to corporate. That is why when banks quote KIBOR-based

prices for loans to their customers, it is the premium they demand over KIBOR, and

not KIBOR itself that really takes into account the credit worthiness of the borrower

and the prospects of loan recovery or default.

IB&F: 410: Sukuk

years. The structure of this Sukuk was on Ijarah Base and annual rate of profit was decided KIBOR + 35 bps.

There were following key objectives to issue the Sukuk:

n To raise financing in a cost efficient mannern Strengthen its presence in the local financial marketsn To diversify and cultivate WAPDA's investor basen Undertake a landmark transaction which will catalyze the promotion

of Islamic Financial instruments and lead the way for other public sector entities.

Assets-Specific Sukuk

Under this arrangement, the resources are mobilize by selling the beneficiary right of the assets to the investors. For example, the Government of Malaysia raised US$ 600 million through Ijarah Sukuk Trust Certificates (TCs) in 2002. Under this arrangement, the beneficiary right of the land parcels has been sold by the government of Malaysia to an SPV, which was then re-sold to investors for five years. The SPV kept the beneficiary rights of the properties in trust and issued floating rate Sukuk to investors.

Another example of Asset-specific Sukuk is US$250 million five-year Ijarah Sukuk issued to fund the extension of the airport in Bahrain. In this case the underlying asset was the airport land sold to an SPV.

Balance Sheet-specific Sukuk

An example of the balance sheet specific use of Sukuk funds is the Islamic Development Bank (IDB) Sukuk issued in August 2003. The IDB mobilized these funds to finance various projects of the member countries. The IDB made its debut resource mobilization from the international capital

09

Under Assets-

specific Sukuk, the

resources are

mobilize by selling

the beneficiary right

of the assets to the

investors.

TIP

Glossary:

Bps: bps stands for Basic points. It is a unit of measure, used in finance to describe

the percentage change in the value or rate of financial instruments, 1 bp is

equivalent to 0.01% or 0.0001 in decimal form. It refers to change in interest rates

and bond yields.

IB&F: 410: Sukuk

10

market by issuing US$ 400 million five-year Sukuk due for maturity in 2008.

IB&F: 410: Sukuk

A GLANCE AT THE GLOBAL SUKUK MARKET

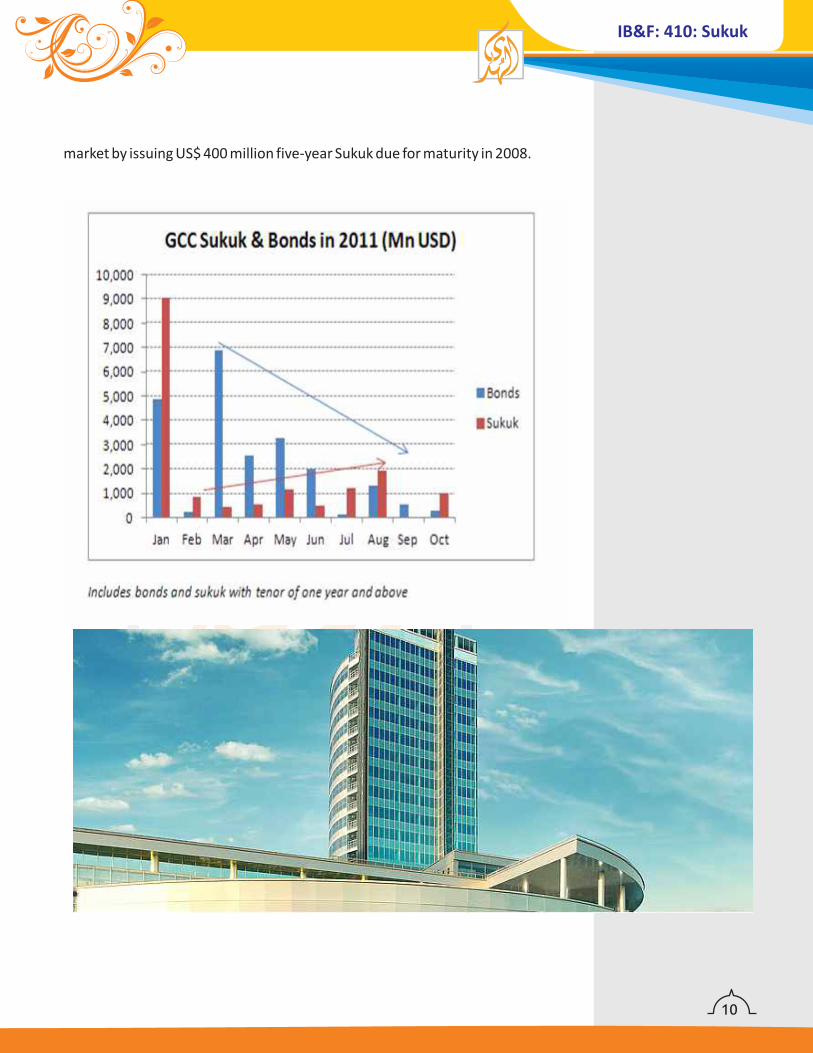

The Islamic bond has recorded an enormous growth in last five years as compared to traditional bond issuance. The Sukuk market has grown from $11bn issued in 2005 to $50bn in 2010, according to the Deutsche Bank Global Markets Research report on Islamic Finance.

However, the contribution of Sukuk market remains tiny compared with the conventional debt market, hovering around 1.4 percent of the total market in terms of volumes.

Given this low base, the report suggests that the Sukuk industry could continue to grow with pace for some time, providing significant upside to fee income growth for Islamic Financial Institutions involved in this market segment. Moreover, it has been witnessed that major corporate has also jumped into the untapped market to diversify their funding structure. The Islamic credit market represents a more feasible and shorter-term reality for the corporate sector.

During last five years, several blue chip companies outside the Middle East and Southeast Asia have already tapped the Sukuk market to issue paper. One of the most visible issuers has been General Electric (GE), which issued $500 million Sukuk in late 2009, listed in Malaysia. Goldman Sachs also recently announced the creation of $2 billion Islamic funding program, although has not yet come to market.

According to the report, the ongoing deleveraging by major companies after the global financial turmoil would prompt other corporate houses to explore other alternatives to their traditional funding avenues.

11

Keep In Mind

During last five years, several blue chip companies outside the Middle East

and Southeast Asia have alre ady tapped the Sukuk market to issue paper.

One of the most visible issuers has been General Electric (GE), which issued

$500 million Sukuk in late 2009, listed in Malaysia. Goldman Sachs also

recently announced the creation of $2 billion Islamic funding program,

although has not yet come to market.

IB&F: 410: Sukuk

The potential of Islamic debt financing extends to government as well. The report revealed that, the issuance of Sukuk by the sovereign state is growing significantly and out of the $50 billion of Sukuk issued last year, over half were issued by the sovereign government. During the last year, Malaysian, Indonesian and Bahrain governments have been frequent issuers of the Islamic investment certificates.

The successful experience of Sukuk bond by the Islamic countries has also compelled countries from Europe and other regions to taste this alternative structure of funding. In recent years, the governments of France, United Kingdom and South Korea have made public acknowledgements that they were considering precisely such instruments, and the relevant legislation required to issue them.

The report disclosed that majority of governments around the world are in need in funding from a budgetary perspective. In the shorter term, they believe that some emerging economies, such as Egypt and other countries from the Europe, could become increasingly amenable to Sukuk issues given their pressing liquidity requirements.

The scope of Sukuk market looks bright all over the world keeping in view the liquidity constraint position of robust economies of the world. Major countries particularly in Europe are looking for alternative source of funding to support their budgetary expenditures and keep their fiscal deficit in control. Hence, the Islamic investment certificates could prove to be an absolute choice for them.

12

During the last year,

Malaysian,

Indonesian and

Bahrain

governments have

been frequent

issuers of the Islamic

investment

certificates.

TIP

Keep In Mind

Majority of governments around the world are in need in funding from a

budgetary perspective. In the shorter term, they believe that some

emerging economies, such as Egypt and other countries from the Europe,

could become increasingly amenable to Sukuk issues given their pressing

liquidity requirements.

IB&F: 410: Sukuk

MECHANISM AND STRUCTURING OF SUKUK

It is an Islamic bond which is structured by bundling leasing transactions, but behaves in practice like any highly-rated bond. Sukuk products are asset-backed, stable-income; tradable and Shari'ah-compatible trust certificates. The primary condition of the issuance of Sukuk is the existence of assets on the balance sheet of the government, the monetary authority, corporate bodies, banking and financial institutions or any entity which wants to mobilize financial resources.

A Sukuk represents proportionate beneficial ownership and may be described as an Islamic bond, for a defined period the risk and return associated with cash flows generated by a particular asset belong to investors (Sukuk holders). The characteristics of a Sukuk are similar to a conventional bond with the difference being that a Sukuk is asset backed.

13

The characteristics

of a Sukuk are

similar to a

conventional bond

with the difference

being that a Sukuk is

asset backed.

TIP

IB&F: 410: Sukuk

The growth of the Sukuk market may be attributed to the potential that it provides for liquidity management, which has been identified as one of the key ingredients necessary for the further development of the Islamic banking and finance industry. Under modern jurisprudence, Shari'ah prohibits financial institutions from trading short-term debt instruments at anything other than face value, or from drawing upon established interbank money-markets. A consequence of such prohibitions has been that Islamic financial institutions have maintained highly liquid balance sheets with limited investment opportunities for their assets. Sukuk have, over the past two years, created new possibilities for the short and medium term placement of funds.

Sukuk must be asset-backed and are often structured as bundles of Ijarah or leasing transactions, especially where the ability to trade on a secondary market is required. Backing by real assets ensures that a Sukuk is tradable, whereas one that is structured around a pure receivable (arising for example under a Murabaha sale) may encounter the Shari'ah prohibition on debt trading mentioned above.

To issue a Sukuk, a financial institution or other entity (such as a sovereign) will typically incorporate a special purpose company, an Islamic Global Sukuk Company (IGS). The IGS issues Sukuk certificates to investors and uses the proceeds rose to purchase a rental generating real property or other cash generating asset from the financial institution or other entity. The IGS in turn leases the property or asset back to the financial institution or other entity for a period corresponding to the duration of the tenure of the Sukuk certificates with the property or the asset being held on trust for the Sukuk holders. The rental payments due from the financial institution or other entity to the IGS will exactly match the periodic payments under the Sukuk holders.

14

Keep In Mind

The growth of the Sukuk market may be attributed to the potential that it

provides for liquidity management, which has been identified as one of the

key ingredients necessary for the further development of the Islamic

banking and finance industry.

Sukuk must be

asset-backed and

are often structured

as bundles of Ijarah

or leasing

transactions

TIP

IB&F: 410: Sukuk

These rental payments may be fixed, or under more recent jurisprudence, calculated with reference to the inter bank offered rate plus a margin which represents the market rate for rental payments. In structuring such transactions it is important to note that all amounts due to the IGS, including the rent that will fund the periodic payments under the Sukuk certificates are direct, unconditional and irrevocable obligations of the financial institution or other entity. The financial institution or other entity is obliged to purchase from the IGS the asset or property upon the maturity of the lease at an agreed price which will be used for the repayment of the principal to the Sukuk holders.

Islamic Features of a Sukuk

The Sukuk is rising in popularity as an investment instrument for Takaful companies in the current situation when the Islamic financial market is less developed than its conventional counterpart. Among other things, Sukuks form an asset class which allows the Takaful industry to create annuity-type products.

15

Reference:

Glossary:

The article “Islamic Features of Sukuk” is written by Hajah Salma Bee Haji Noor

Mohamed Abdul Latif, Director of the Centre for Islamic Banking, Finance and

Management Unit, and Dr Abul Hassan, Visiting Lecturer, Faculty of Business,

Economics and Policy Studies, Universiti Brunei Darussalam.

Annuity: annuity is a cash flow stream of equal amounts, paid at equal time

intervals for a specified number of periods.

Keep In Mind

The rental payments under Sukuk Certificate may be fixed, or under more

recent jurisprudence, calculated with reference to the inter bank offered

rate plus a margin which represents the market rate for rental payments.

Sukuks form an

asset class which

allows the Takaful

industry to create

annuity-type

products.

TIP

IB&F: 410: Sukuk

As the Takaful sector expands, so, too, will the market for Sukuks or Islamic bonds, and in turn, the increased availability of Shari'ah-compliant investment vehicles foster the development of Takaful in what is a virtuous cycle.

Thus, Sukuks are an invaluable part of the Islamic capital market.

Indeed, what is a Sukuk? It is an Islamic bond which is structured by bundling leasing transactions, but behaves in practice like any highly-rated bond.

In response to the emergence of interest in issuances of Islamic asset-backed financial instruments, the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) released an exposure draft of its Shari'ah standards concerning Sukuks in November 2002. According to the exposure draft, “Investment Sukuks are certificates of equal value representing, after closing subscription, receipt of the value of the certificates and putting it to use as planned, common title to shares and rights in tangible assets, usufructs, and services, or equity of a given project or equity of a special investment activity”.

Sukuks are important because firstly, they represent a new source of funds, generally at attractive rates. And secondly, they are vital to developing a deeper and more liquid Islamic capital market. There is a great deal of sur-plus cash sitting in Islamic financial institutions waiting to be tapped by new financial instruments. Sukuks can allow this pot of gold to be unlocked. If Sukuks can be competitively structured according to Shari'ah law and a market for them is developed, the economy will benefit. In this regard, we discuss the various Islamic Sukuk structures and their features which differ from a conventional bond or securities.

16

Keep In Mind

Sukuks are important because firstly, they represent a new source of funds,

generally at attractive rates. And secondly, they are vital to developing a

deeper and more liquid Islamic capital market. There is a great deal of sur -

plus cash sitting in Islamic financial institutions waiting to be tapped by

new financial instruments. Sukuks can allow this pot of gold to be unlocked.

IB&F: 410: Sukuk

Keep In Mind

The identification of suitable assets is the first, and arguably the most

integral step, in the process of issuing Sukuk certificates. Shari’ah

considerations dictate that the pool of assets should not comprise merely of

debts from Islamic financial contracts (e.g. Murabaha, Istisna).

17

Sukuk products are

asset-backed,

stable-income;

tradable and

Shari’ah-compatible

trust certificates.

TIP

Under Pure Ijarah

Sukuk, the rental

rates of returns on

these Sukuks can be

both fixed and

variable.

TIP

Sukuk Structures

Sukuk products are asset-backed, stable-income; tradable and Shari'ah-compatible trust certificates. The primary condition of the issuance of Sukuk is the existence of assets on the balance sheet of the government, the monetary authority, corporate bodies, banking and financial institutions or any entity which wants to mobilize financial resources.

The identification of suitable assets is the first, and arguably the most integral step, in the process of issuing Sukuk certificates. Shari'ah considerations dictate that the pool of assets should not comprise merely of debts from Islamic financial contracts (e.g. Murabaha, Istisna).

Types of Sukuk

The proper classification of asset classes will determine the type of Sukuk certificates to be issued. It is imperative to note that assets can be prepared for the issuance of trust certificates in a number of ways, subject to the need of the issuing entity.

Pure Ijarah Sukuk

This certificate is issued on stand-alone assets identified on the balance sheet. The assets can be parcels of land to be leased or leased equipment such as aircrafts and ships. The rental rates of returns on these Sukuks can be both fixed and floating, depending on the particular originator.

Hybrid/Pooled Sukuk

The underlying pool of assets can comprise of Istisna, Murabaha as well as ijarah. Indeed, having a portfolio of different classes of assets allows for greater mobilization of funds. Murabaha and Istisna assets can comprise a portfolio of funds. However, at least 51% of the pool must be

IB&F: 410: Sukuk

made up of Ijarah assets. Due to the fact the Murabaha and Istisna receivables are part of the pool, the return on these certificates can only be a pre-determined fixed rate of return.

The above-mentioned two types of Sukuk would partially represent the strength of the issuer's balance sheet.

Variable Rate Redeemable Sukuk

Under some conditions, implementing Sukuk by representing the full strength of an issuer's balance sheet can prove to be beneficial. Several corporate entities refer to these Sukuks as Musharaka Term Finance Certificates (MTFCs). They can be considered as an alternative to the Sukuk because of their seniority to the issuer's equity, redemption features and relatively stable rate of return as compared to dividend payouts.

MTFCs have a few advantages. First, employing Musharaka returns is preferred by jurists as such an arrangement would strengthen the paradigm of Islamic banking that considers partnership contracts as the embodiment of core ideals.

Secondly, the floating rate of return on these certificates would not depend on benchmarking with market references such as the London Inter-bank Offer Rate (LIBOR), but would instead be contingent on the firm's balance sheet.

18

Keep In Mind

They can be considered as an alternative to the Sukuk because of their

seniority to the issuer’s equity, redemption features and relatively stable

rate of return as compared to dividend payouts.

Glossary:

LIBOR: A commonly used reference rate, derived daily from the interest

rates at which major international banks in London will lend to each other.

IB&F: 410: Sukuk

Zero-Coupon Non-Tradable Sukuk

Another possible Sukuk structure can be created where the assets to be mobilized do not exist yet. Consequently, the objective of the fund mobilization would be to create more assets through Istisna. However, certificates of this nature would not readily be tradable because of Shari'ah restrictions. The primary asset pools to be generated would be of a nature warranted by Istisna and installment purchase/sale contracts that would create debt obligations. The certificate on these debt arrangements can be termed as fixed-rate zero-coupon Sukuk.

Embedded Sukuk

These could be Sukuks whether zero-coupon, pure Ijarah or hybrid, with the embedded option to convert into other asset forms, subject to specified conditions.

Islamic Features of the Sukuk

Sukuks serve to replicate the functions of tradable securities in mobilizing resources from markets and injecting liquidity into the enterprise or government and in providing a stable source of income for investors. The Sukuk bears the financial risk, and it is distinguished from conventional bonds and asset securitization in several ways:

Conventional investors in corporate and government bonds hope to capitalize on favorable developments in interest rates. Capital gains are accumulated when fixed-rate bond prices rise as variable market indices fall. The legitimacy of Sukuk structures in the Shari'ah lie in the fact that they do not take advantage of interest rate movements.

Sukuk are directly linked with real sector activities, such as the funding of trade or production of tangible assets. Hence, these will not create short-term speculative movement of funds and potential financial crises.

Sukuk investors have an inherent right to information about the use of their investments, nature of the underlying assets, and other particulars that would be considered redundant in conventional investments. This will help to introduce discipline in the market.

19

Zero-coupon Sukuk

would not be easily

tradable because of

Shari’ah restrictions.

TIP

Sukuk are directly

linked with real

sector activities,

such as the funding

of trade or

production of

tangible assets.

TIP

IB&F: 410: Sukuk

The Sukuk market has emerged during the previous five years. First of all, Bahrain, in a pioneering move, issued domestic sovereign fixed-rate Ijarah and Salam Sukuks in 2001. It was followed by the issuance of floating-rate Ijarah Sukuks as well as pooled Sukuks by corporations and sovereigns in several countries. These Sukuks are based on Salam, Ijarah, Istisna, Istisna-cum-Ijarah and on the basis of pooled portfolios.

However, some corporate and sovereign Sukuk prospectuses have come under increased scrutiny for their Shari'ah suitability. The predominant feature of several of the prospectuses is the floating-rate return distributed to the certificate holders. The market reference used is LIBOR over which a competitive premium is added.

However, it should be observed that in the case of the Ijarah Sukuk arrangements, LIBOR serves as a market reference for the returns and the intrinsic distributions arise from the rentals pertaining to the leasing arrangements with the originator and special purpose vehicle.

The Sukuk issuance by the Jeddah-headquartered Islamic Development Bank serves as an excellent and promising example for future arrangements. The prospectus contains clear and precise Shari'ah considerations outlined by numerous leading scholars and involves an innovative portfolio combination of Ijarah, Murabaha and Istisna projects. Also, returns are not ambiguously related to market benchmarks, but a fixed rate of return is agreed on.

One dimension of the paradigm of Islamic finance that should not be lost upon compromises for increased profitability is altruism. In this regard, Sukuks have not only mobilized previously untapped public sector funds, but have also provided long-sought funding for development projects.

The Qatar Government issued Sukuk securities to fund a large medical complex (Hamad Medical City) in Doha, and the Malaysia Sukuk certificates raised funds for several government owned hospitals as well as offices.

20

First of all, Bahrain

issued domestic

sovereign fixed-rate

Ijarah and Salam

Sukuks in 2001.

TIP

IB&F: 410: Sukuk

Most significantly, the IDB Sukuks raised funds for projects in 21 developing nations in a wide range of schemes that include power transmissions, hospitals, steel manufacturing, mineral water networks, livestock breeding, sea port development, pharmacology research, agricultural irrigation, telecommunications projects, rural development and colleges.

Advantages of Sukuk for Issuer and Investors

There are several advantages of Sukuk for the issuer and investor. The advantages are as follows:

Advantages to Sukuk Issuer

n Diversification of funding sourcesn Creating and enhancing profile in international marketsn Secondary liquidityn Sizeable financingn Ease of clearing and settlement

Advantage of Sukuk Investor

n Diversification in Investmentn Provides Leveraging Capabilitiesn Secondary Market Liquidityn Ease of clearing and Settlementn Investment available to Institutional and Retail investors

Allows for many computation of Risk – Credit /Market/Duration etc.

21

IB&F: 410: Sukuk

22

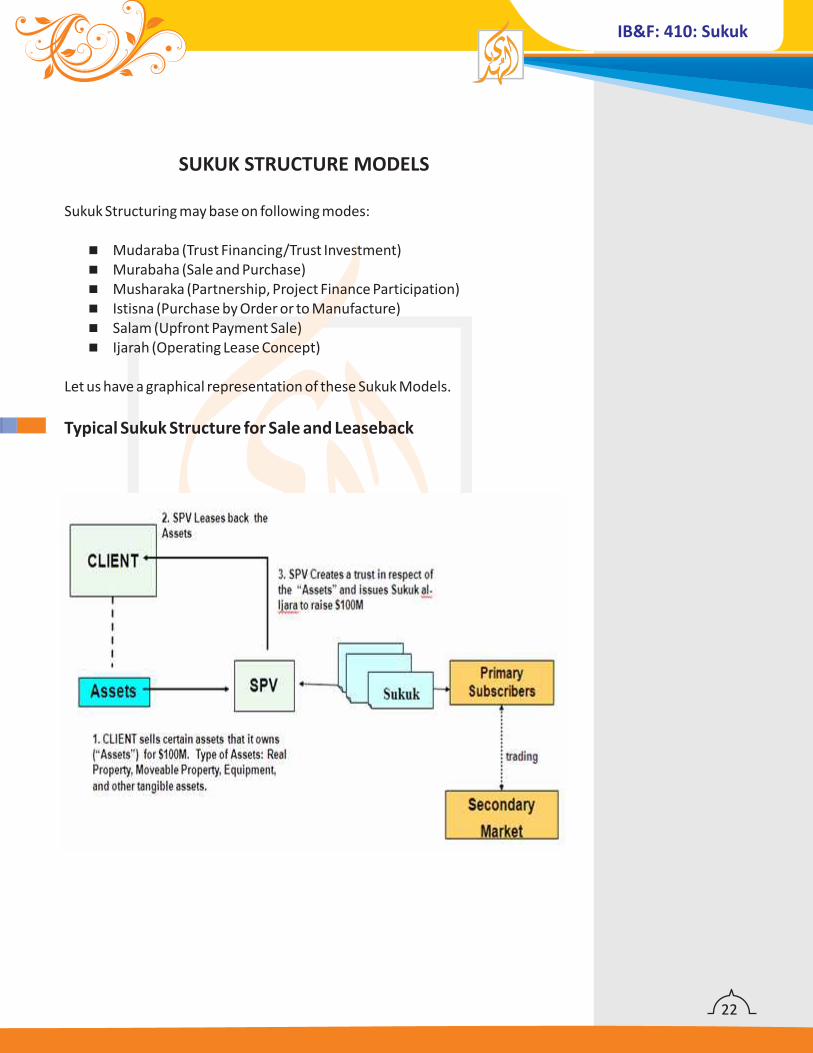

SUKUK STRUCTURE MODELS

Sukuk Structuring may base on following modes:

n Mudaraba (Trust Financing/Trust Investment)n Murabaha (Sale and Purchase)n Musharaka (Partnership, Project Finance Participation)n Istisna (Purchase by Order or to Manufacture)n Salam (Upfront Payment Sale)n Ijarah (Operating Lease Concept)

Let us have a graphical representation of these Sukuk Models.

Typical Sukuk Structure for Sale and Leaseback

IB&F: 410: Sukuk

Flow of Funds - Acquisition & Rentals

Flow of Funds - Repayment & Maturity

23

IB&F: 410: Sukuk

Sukuk Al-Ijarah Based Model

Steps involved are:

n SPC will buy the assets from corporate at say USD 500m.n SPC will lease the assets back to corporate for say 5 years.n Lease Rentals will be payable 6-monthly in arrears and will be

benchmarked on USD LIBOR plus a credit spread.n To raise USD 500m, SPC will issue Sukuk at par value of USD 500m.n Investor will subscribe to the Sukuk as primary subscribers (similar to

the primary subscription in a bond issue.)n SPC will collect the lease Rentals and distribute pro rata to the Sukuk

Holders.n The Sukuk can be listed, rated, cleared through Euroclear /

Clearstream and traded in the secondary market.n The kingdom of Bahrain Sukuk issues, the Federation of Malaysia the

State of Qatar and the Republic of Pakistan Sukuk issues were structured based on this concept.

24

IB&F: 410: Sukuk

Sukuk al Istismar (51% Ijarah structuring)

25

IB&F: 410: Sukuk

26

CHALLENGES IN MAKING SUKUK SHARI'AH COMPLIANT

Sukuk are financial instruments that are income-generating. To be Shari'ah-compliant they must be based, wholly or mainly, on ownership in real (i.e. tangible) assets. Most Sukuk structures are based on leased real assets. Other structures are possible but will not be considered here.

There is a difference between financial instrument and a mode of finance. Sale for a deferred price is an Islamic mode of financing that is income-generating, as it includes the seller's profit, but cannot be used directly to create a financial instrument. This is so because the I.O.U. given by the buyer to the seller represents money debt, and as such is not negotiable in Shari'ah. Such debt cannot be discounted or sold for a price different from its face value. It is however transferable at face value, through hawalah, but this does not render it negotiable in the above sense. Sukuk challenges are as follows:

n Non existence secondary market mainly due to the lack of critical mass.

n What is the critical Mass required to stimulate trading?n Few or no market makersn Pricing the secondary market issues - area of inefficiency and

requires more transparencyn Benching marking and absence of Islamic Yield Curve which should

have no relations to LIBORn Limited awareness and flow of informationn Standardization of Contracts & market practices but keeping

innovation aliven Usage of Sukuk as a monetary management tool by regulatory

bodiesn Lack of Shari'ah harmonizationn Lender of last resort

There is a difference

between financial

instrument and a

mode of finance.

TIP

Reference:

The passages under “Challenges in Making Sukuk Shari'ah Compliant” are taken by the article of Dr. M. Anas Zarka from The International Investor Company, Kuwait.

IB&F: 410: Sukuk

27

CASE STUDY: WAPDA ISSUED SUKUK TO RAISE FUNDS FOR MANGLA

DAM

Introduction

WAPDA has issued its first Sukuk for Mangla Dam Raising Project in January 2006, whereas its second Sukuk was being issued in July, 2007. WAPDA's financing requirement was PKR 8,000 million to (partially) fund the Mangla Dam Raising Project.

Key objectives of WAPDA were:

§ To raise financing in a cost efficient manner.§ Strengthen its presence in the local financial markets.§ Diversify and cultivate WAPDA's investor base.§ Undertake a landmark transaction which will catalyze the promotion

of Islamic Financial instruments and lead the way for other public sector entities.

Transaction Structure

IB&F: 410: Sukuk

28

Offering Summary

IB&F: 410: Sukuk

n

n

n

Sukuk is popularly known as an Islamic or Shari'ah compliant 'Bond' whilst in actual fact and it is an asset-backed trust certificate. In its simplest form Sukuk is a certificate evidencing ownership of an asset or its usufruct. The Sukuk structures rely on the creation of a Special Purpose Vehicle (SPV). SPV would issue Sukuk certificates which represent for example the ownership of an asset, entitlement to a debt or to rental incomes or even accumulation of returns from various Sukuk (a hybrid Sukuk).In Sukuk structure the Sukuk holders each hold an undivided beneficial ownership in the underlying assets. Consequently, Sukuk holders are entitled to share in the revenues generated by the Sukuk assets as well as being unrestricted to share in the proceeds of the realization of the Sukuk assets.The Islamic bond has recorded an enormous growth in last five years as compared to traditional bond issuance. The Sukuk market has grown from $11bn issued in 2005 to $50bn in 2010, according to the Deutsche Bank Global Markets Research report on Islamic Finance.

29

Summary n During last five years, several blue chip

companies outside the Middle East and Southeast Asia have already tapped the Sukuk market to issue paper. One of the most visible issuers has been General Electric (GE), which issued $500 million Sukuk in late 2009, listed in Malaysia. Goldman Sachs also recently announced the creation of $2 billion Islamic funding program, although has not yet come to market.

n Sukuks are important because firstly, they represent a new source of funds, generally at attractive rates. And secondly, they are vital to developing a deeper and more liquid Islamic capital market. There is a great deal of surplus cash sitting in Islamic financial institutions waiting to be tapped by new financial instruments.

n Sukuk products are asset-backed, stable-income; tradable and Shari 'ah-compatible trust certificates. The primary condition of the issuance of Sukuk is the existence of assets on the balance sheet of the government, the monetary authority, corporate bodies, banking and financial institutions or any entity which wants to mobilize financial resources.

IB&F: 410: Sukuk

n

n

n

n

n

n

n

n

n

n

E-Library:

n

n

n

n

How would you define Sukuk?What are the differences between Conventional Bond and Sukuk?What are the similarities between Conventional Bond and Sukuk?What is the role of Shari'ah Advisors in Sukuk Issuance?Define the mechanism and structuring of Sukuk?What are the Challenges in Making Sukuk Shari'ah Compliant?

For further study, you can consult our CD or e-library by getting log-in to your account. You

would get number of books, presentations, literature and reports on the following topics:

Islamic Capital Market by Products by Salman Syed Ali

Malaysian Debt Security & Sukuk Market by Bank Negara and Securities Commission

Malaysia

Managing Financial Risk of Sukuk by Ali Arsalan Tariq

Overview of the Sukuk Market by Professor Rodney Wilson

BooksArticlesPresentationsReports

30

Discussion Questions

Supplement Material

IB&F: 410: Sukuk