potential enhancements to fomc communication

TRANSCRIPT

Authorized for public release by the FOMC Secretariat on 01/29/2016

August 5, 2010

Potential Enhancements to FOMC Communication

Gauti Eggertsson, Krishna Guha, Andy Levin, Steve Meyer, and Simon Potter

In the current context of a subpar recovery and heightened economic uncertainty, policymakers may wish to consider enhancements to FOMC communications that would provide additional stimulus by reducing longer-term real interest rates, thereby helping to promote economic recovery and mitigate downside risks. This memo provides an overview of several potential enhancements: (i) elaborating the forward guidance in FOMC announcements by including sharper qualitative descriptions or quantitative indications of the economic conditions that would trigger an end to the extended period of exceptionally low targets for the federal funds rate; (ii) adding conditional funds rate forecasts to the Summary of Economic Projections (SEP); (iii) establishing an explicit long-run inflation objective; and (iv) adopting a quantitative policy framework such as price level targeting or nominal GDP targeting. We begin with a brief discussion of relevant conceptual issues and then consider each potential enhancement, recognizing that some of these approaches might require substantial further staff analysis and consideration of various practical details prior to implementation.

Conceptual Issues

Central bank communications can affect financial conditions by influencing investors’ expectations regarding the future path of short-term interest rates. Thus, enhanced communications would be most likely to generate more accommodative financial conditions under circumstances in which the central bank anticipates that the appropriate trajectory for the policy rate will be shallower than the path projected by investors. For example, when the policy rate is being held at its effective lower bound, financial market participants might expect an earlier liftoff and a faster pace of subsequent tightening than anticipated by policymakers. Such a divergence in expectations about the likely path of policy could occur for several reasons:

1. Market participants’ policy expectations might diverge from those of the central bank due to differing perceptions about the fundamentals of the economic outlook, that is, the shocks impinging on the economy and the structural mechanisms through which shocks are propagated. Even when investors and policymakers have similar forecasts of the likely evolution of output and inflation, they might have markedly different assessments about the underlying strength of aggregate demand and hence about the path of policy that would facilitate those outcomes. For example, policymakers might view aggregate demand as relatively weak and consequently expect that policy would need to remain extraordinarily accommodative over a longer horizon than anticipated by investors.

2. Investors’ expectations about the future path of short-term interest rates might diverge from those of policymakers due to misperceptions of the central bank’s policy strategy: how the central bank will adjust policy over time in response to changes in the economic outlook or the balance of risks to that outlook, and how it will weigh any near-term tradeoffs with respect to its stabilization objectives. For example, market

1 of 12

participants may be unsure about whether the central bank has an escalating degree of intolerance for particularly large deviations from its objectives, and they may not understand the extent to which the central bank has a preference for policy gradualism in a given context. Moreover, investors may be unsure about whether the central bank’s strategy is aimed at providing greater stimulus by committing to maintain a low policy rate even after the effective lower bound is no longer a binding constraint. All of these issues could be particularly acute when the economy is in uncharted territory and hence the central bank’s strategy differs from its typical approach.

3. Finally, the expectations of financial market participants and the decisions of wage- and price-setters depend in part on their perceptions of the central bank’s inflation goal. Those perceptions might be reasonably well-anchored under normal conditions but could start to drift downward in response to persistently low inflation outcomes.

Thus, when the central bank judges that the appropriate policy path will be shallower than anticipated by investors, policymakers might aim to narrow that gap through enhanced communication about the economic outlook, the policy strategy, and the longer-run inflation goal. Moreover, such enhancements in communication might well be helpful on an ongoing basis in limiting the size of future divergences in policy expectations.

While enhancements in central bank communication may result in more accommodative financial market conditions under certain circumstances, it should be noted that such an outcome is by no means inevitable. In some contexts, increased clarity about policymakers’ assessments regarding the fundamental weakness of the economy or the magnitude of downside risks could end up alarming investors and cause a widening of risk spreads and a drop in asset prices, thereby offsetting the stimulative effects of a lower anticipated path of short-term nominal interest rates. These considerations underscore the need to weigh the benefits and risks of various adjustments to the central bank’s communication strategy and the importance of considering specific design features that might be helpful in mitigating those risks.

Potential Adjustments to FOMC Statement Language

Since December 2008, FOMC statements have included forward policy guidance to convey the Committee’s expectation that economic conditions would be likely to warrant a continuation of exceptionally low levels of the funds rate for more than a single intermeeting period. Initially, the statement said this policy stance was likely to continue “for some time.” In March 2009, the Committee substituted the phrase “for an extended period” to indicate that the duration was likely to be somewhat longer. Since November 2009, FOMC announcements have included a list of the economic conditions that are expected to warrant exceptionally low rates, namely, “low rates of resource utilization, subdued inflation trends, and stable inflation expectations.”1

1 Analysis of the policy expectations that are embedded in financial market prices suggest that investors generally understand the contingent nature of the forward policy guidance: They appear to understand that the Committee is unlikely to raise rates for a number of meetings, at least in the absence of a surprise

2 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016

Futures quotes, combined with the usual staff assumptions for term premiums, indicate that market participants now expect the federal funds rate to move above the current 0 to ¼ percent target range in the third quarter of 2011, about the same timing of policy liftoff as the consensus forecast in the latest Blue Chip survey. If Committee members anticipate that the funds rate is likely to follow a shallower trajectory than currently expected by financial market participants, then the Committee might wish to modify the forward guidance language to provide greater clarity about its policy outlook, thereby helping to bring investors’ policy expectations into closer alignment with those of policymakers.2

One option would be to provide more explicit information about the Committee’s conditional expectation regarding the likely timing of policy liftoff. For instance, the Committee could modify its forward guidance as follows: “Given the current outlook for economic activity and inflation, the Committee does not expect to raise the target for the federal funds rate before the third quarter of 2011.” Of course, the Committee’s expectations regarding the outlook and hence about the likely timing of policy liftoff might well evolve over time, and it would seem reasonable that the forward guidance could be adjusted as appropriate to reflect such changes.3

A second option would be to provide further information regarding the Committee’s policy reaction function. One such approach would be for the FOMC statement to connect the timing of policy liftoff to the pace of recovery or to a substantial narrowing of slack in resource utilization and of the deviation of actual inflation from its mandate-consistent rate. For example, the Committee could condition its forward guidance in terms of the degree of momentum by stating that the current target range for the federal funds rate will be maintained “at least until resource utilization and underlying inflation are clearly moving towards levels consistent with the dual mandate.” Alternatively, the Committee could place greater weight on the accumulated narrowing of the relevant gaps by indicating that the funds rate will remain exceptionally low “until resource utilization and underlying inflation have moved appreciably closer to levels consistent with the dual mandate.”

that would materially improve the contours of the economic outlook, and that the horizon over which the funds rate remains exceptionally low may be drawn out further in response to adverse news about real activity or inflation. For example, when the economic outlook deteriorated significantly over the weeks following the April FOMC meeting, the market priced in a substantially longer duration over which the funds rate would remain close to current levels.

2 Apart from modifying its forward guidance language, the Committee could consider reiterating its broader commitment to act as needed to fulfill the dual mandate, as in FOMC statements from December 2008 through mid-2009.

3 The Bank of Canada adopted this approach to communicating its policy expectations in April 2009, when it stated: “Conditional on the outlook for inflation, the target rate can be expected to remain at its current level until the end of the second quarter of 2010 in order to achieve the inflation target.” The Bank reiterated its conditional commitment at each policy meeting until April 2010, when it explicitly removed its forward guidance without changing its policy rate. On June 1, 2010, the Bank raised its policy rate and announced a return to its pre-crisis operating framework.

3 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016

Such language might lead investors to infer that the Committee was prepared to keep the funds rate close to the zero lower bound longer than they previously thought likely, especially in light of recent SEP results indicating that policymakers generally see trend inflation as lower than their assessments of the mandate-consistent inflation rate and the unemployment rate as well above their assessments of its longer-run sustainable level. In conjunction with the Minutes’ summary of the Committee’s discussion and further elaboration in speeches and testimony, policymakers could, if desired, provide fairly detailed information about the levels of resource utilization and underlying inflation that would be expected to prevail prior to the commencement of policy tightening.

Indeed, the Committee could choose to explicitly quantify the thresholds for the conditioning variables that would be used in determining the timing of policy liftoff. Formulating those quantitative thresholds might be challenging, given that participants have a diversity of views about the operation of the economy and the monetary policy transmission mechanism and a range of assessments regarding the longer-run sustainable rate of unemployment and the mandate-consistent inflation rate. Nonetheless, to the extent that more precise forward guidance is judged to be desirable, policymakers may prefer to do so by quantifying the relevant set of economic conditions rather than by specifying the likely timing in terms of calendar dates.4

For example, quantitative information could be introduced into the forward guidance roughly as follows: “The Committee expects to maintain the current target range for the federal funds rate at least until the unemployment rate has fallen below [x] percent or the underlying trend rate of consumer inflation (as measured by the annual average change in the price index for personal consumption expenditures, [excluding food and energy]) has moved above [y] percent.” The conjunction between the two conditions (“or”) would preserve optionality for initiating policy firming once either conditioning variable had passed its specified threshold.5 The phrase “currently expects” would leave open the possibility that the Committee could begin tightening sooner if warranted, while the phrase “at least” would allow for a longer duration of extraordinary policy accommodation. The inclusion of the bracketed phrase (“excluding food and energy”) would depend on whether policymakers wished to express the conditionality in terms of core vs. overall PCE inflation.

4 Such a commitment would be reminiscent of the Bank of Japan’s March 2001 commitment to maintain the zero interest rate policy (ZIRP) until the Japanese CPI (excluding perishables) stabilized or exhibited a year-on-year increase. This approach was viewed by many Bank of Japan officials at the time as a relatively high-risk strategy due to the possibility that current year-on-year CPI might not turn positive until a point at which forecasts of CPI inflation over subsequent years might be well above desirable levels. For precisely that reason, however, officials at the Bank of Japan believe that its policy framework and communication strategy had a strong influence on inflation expectations.

5 Alternatively, the conjunction “and” could be used to indicate that funds rate firming would be unlikely to commence until both conditions were satisfied, perhaps with correspondingly different specifications of the thresholds x and y.

4 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016

The forward guidance conditions could be quantified using a different set of variables or perhaps combined into a single condition expressed in terms of nominal GDP growth, “The Committee expects to maintain the current target range for the federal funds rate at least until the annual average growth rate of nominal gross domestic product has moved above [x] percent.” To a first approximation, nominal GDP growth equals the sum of real output growth and the inflation rate of the GDP price index; hence, this form of conditionality would indicate that policy firming would be unlikely to commence until real growth accelerated sufficiently or inflation picked up.

In establishing any set of qualitative or quantitative thresholds for the initiation of liftoff, the Committee could choose to specify those triggers in terms of economic forecasts rather than outcomes. For example, policymakers could indicate that the current target range for the federal funds rate is likely to be maintained “at least until the Committee’s projections of unemployment [and | or ] inflation at a horizon of about two years are close to rates judged to be consistent with its mandate of maximum employment and price stability.” A forecast-based approach could be linked directly to the information presented in the SEP and might be particularly appealing if the Committee preferred to minimize the risk of overshooting its goals for inflation and resource utilization.

Potential Enhancements to the SEP

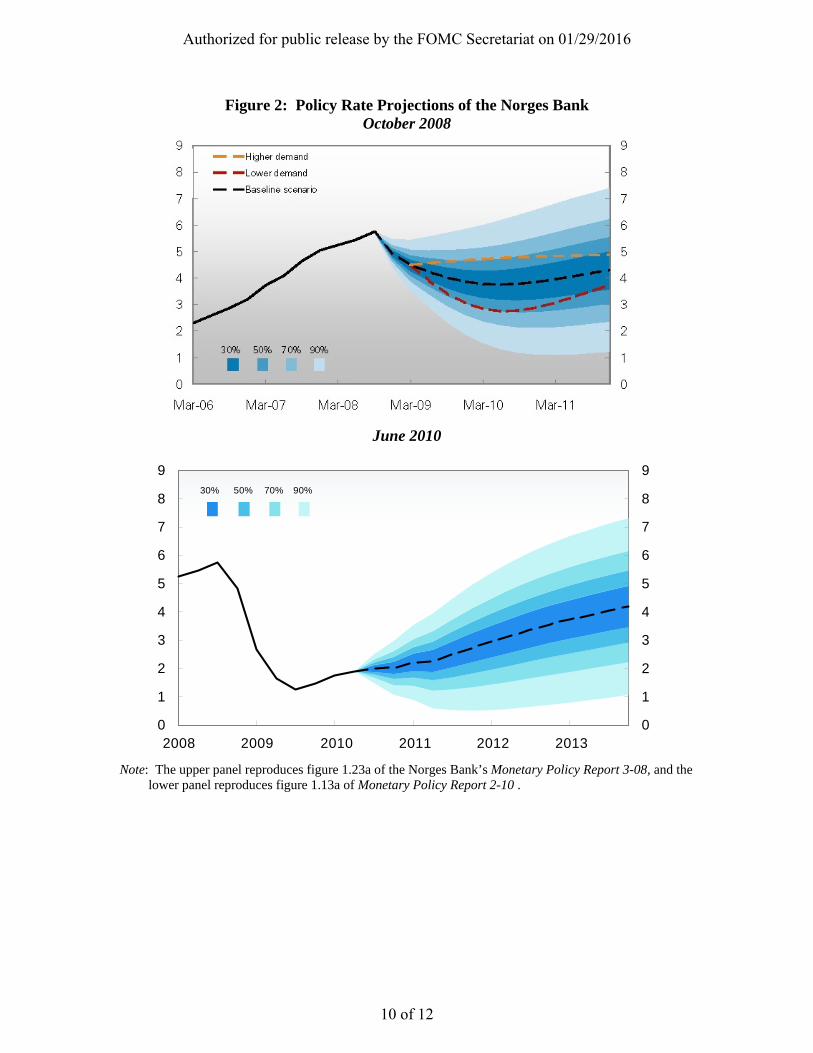

If Committee participants wished to provide quantitative information about their expectations regarding the likely path of the federal funds rate, the Committee might choose to follow an approach broadly similar to the communication strategies adopted by the central banks of New Zealand, Norway, and Sweden. For example, Figures 1 and 2 reproduce fan charts from the monetary policy reports of the central banks of Sweden and Norway, depicting the policy paths that were expected to be appropriate for promoting the stated objectives of each central bank as of autumn 2008 (the upper panels) and as of mid-2010 (the lower panels).6 These charts employ progressive shading to denote confidence intervals around the modal forecast, thereby highlighting the extent to which the policy projections are subject to substantial uncertainty. Each central bank’s monetary policy report includes extensive discussion of the factors shaping the outlook and the risks to that outlook, thereby illustrating the notion that quantitative and verbal forms of communication may be viewed as complements rather than substitutes.7 It is also noteworthy that neither central bank appears to have faced any ex post criticism for setting policy rates in 2009 that were well below the 5th percentile of the confidence intervals in the charts published in autumn 2008; in effect, those unexpected policy moves reflected the extraordinary nature of the global crisis and its spillover effects on small open economies like Norway and Sweden.

6 These monetary policy reports present the consensus projections of the policymakers at each central bank, whereas the SEP presents information about the central tendency and range of FOMC participants’ economic projections under their own individual assessments regarding the appropriate path of policy that best satisfies the dual mandate.

7 As in the upper panel of Figure 2, the Norges Bank’s fancharts have occasionally included alternative scenarios that underscore the conditionality of the benchmark forecast and provide further information about how the stance of policy might be adjusted in response to plausible deviations from the baseline outlook.

5 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016

Federal Reserve policymakers could use the SEP to convey more information about their policy expectations—and about the conditional nature of those expectations—by including the central tendency and range of the values of the federal funds rate that each participant individually judges likely to be appropriate (as that term is defined in the SEP) over the projection horizon as well as over the longer run.8 Such information would presumably be accompanied by text emphasizing that those projections should not be interpreted as commitments and that participants’ views regarding the appropriate stance of policy would evolve over time in response to incoming information about the outlook for economic activity and inflation. Publishing these policy projections in the SEP might also be helpful in elucidating the Committee’s forecasts for output growth, unemployment, and inflation.

Establishment of an Explicit Inflation Goal

Research has highlighted the extent to which the firm anchoring of inflation expectations can be crucial for ensuring that a large contraction in aggregate demand does not push the economy into a liquidity trap.9 In practice, longer-term inflation expectations are presumably most likely to drift downward in response to a persistent drop in actual inflation.

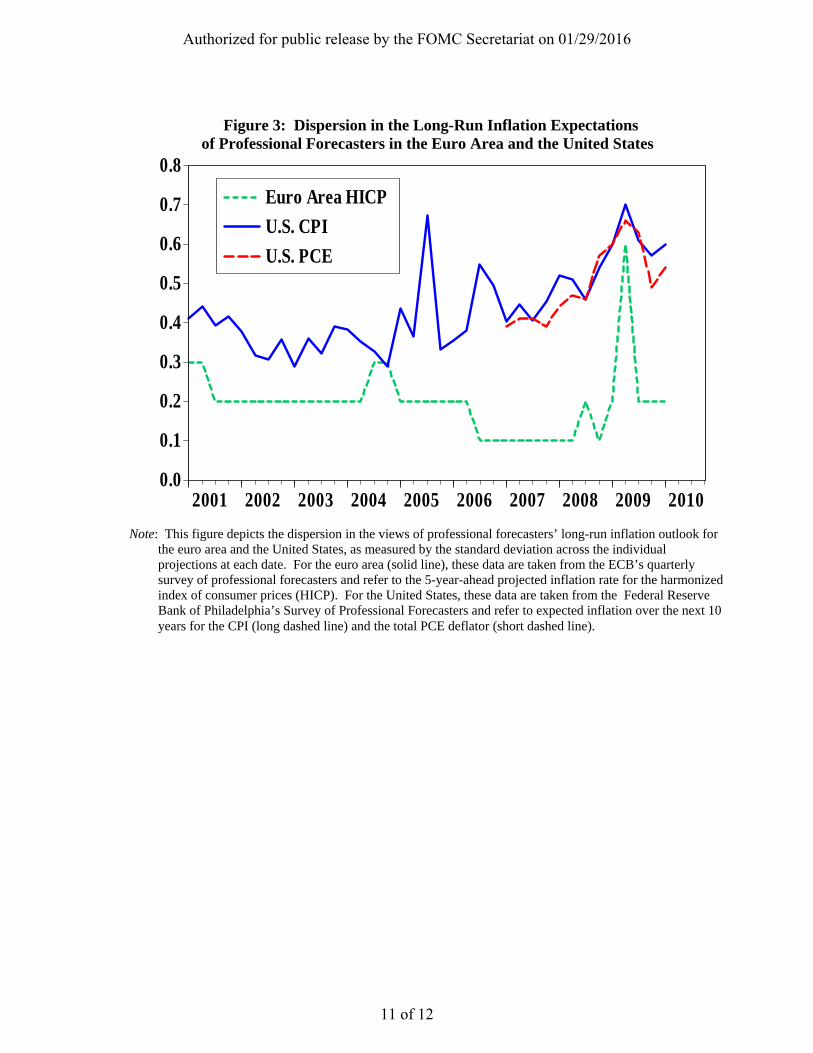

Since January 2009, the longer-run projections in the SEP have provided information about policymakers’ individual assessments of the mandate-consistent inflation rate. Nevertheless, empirical analysis indicates that the degree of uncertainty regarding the longer-run inflation outlook remains substantially higher in the United States than in the euro area. In particular, as shown in figure 3, the standard deviation across individual long-run inflation projections in the Philadelphia Fed Survey of Professional Forecasters averaged around 0.4 percentage points through most of the decade, and the degree of dispersion rose markedly after the onset of the financial crisis. In contrast, since the European Central Bank clarified its policy strategy as aimed at keeping inflation “below, but close to, 2 percent in the medium term”, professional forecasters’ projections of

8 Committee participants’ funds rate projections could be presented on a fourth-quarter average basis for each calendar year—the same approach currently used for presenting their unemployment projections. If the Committee wished to provide more specific information about the likely timing of policy liftoff, a separate exhibit could report on the central tendency and range of funds rate projections at a quarterly frequency. Policymakers might also consider publishing calendar year forecasts at a somewhat longer horizon—perhaps up to five years ahead—to provide a more complete depiction of the anticipated convergence to a balanced growth path.

9 For example, Bullard and Cho (2005) showed that the effects of large contractionary shocks are typically compounded when agents face uncertainty about the central bank’s inflation objective and hence must infer its value from recent economic outcomes. Similarly, Evans, Guse, and Honkapohja (2007) analyze a learning model in which low outcomes for actual inflation cause private agents to mark down their inflation forecasts; thus, when monetary policy becomes constrained by the zero lower bound, real interest rates start rising and choke off economic activity, leading to further downward revisions in the inflation outlook and in some cases to a full-blown deflationary spiral.

6 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016

longer-term inflation for the euro area have generally remained tightly clustered around an average forecast of about 1.9 to 2 percent, even in the wake of the financial crisis.10

The Swedish experience suggests that a transparent and credible inflation objective may be helpful in providing an anchor for long-run inflation expectations during a period of persistently low inflation. Figure 4 depicts the evolution of Swedish CPI inflation along with professional forecasters’ longer-run projections of Swedish inflation (as measured by Consensus Economics’ semiannual surveys). Notably, this measure of longer-term inflation expectations remained firmly anchored over the period from 2004 to mid-2007 when Swedish inflation outcomes were persistently low.11

Adoption of a Conditional Commitment Framework

If the economic outlook became dire or downside risks were judged to be particularly severe, the Committee could consider more substantial changes in its policy framework and communication strategy. In particular, policymakers might wish to establish a conditional commitment to maintain a relatively accommodative stance of policy for some period once the setting of the federal funds rate is no longer constrained by the zero lower bound. If the commitment strategy were sufficiently transparent and credible, investors would anticipate a lower trajectory for future short-term interest rates that would bring down current longer-term real interest rates and thereby provide near-term stimulus.

One possible form of commitment strategy would be to frame the Committee’s forward guidance in terms of deviations of the price level from a specified path. For example, the relevant portion of the FOMC statement might read roughly as follows: “The Committee expects to maintain the current target range for the federal funds rate until the unemployment rate has fallen below [x] percent [and/or] the price index for personal consumption expenditures has risen at an average annual rate of [y] percent from its level as of [month/year].” Such an approach would imply that any further shortfall in inflation would be countered by a longer duration of extraordinary policy accommodation in order to bring the price level back to the specified target path over time.

An alternative form of commitment strategy would be to specify a target path for the level of nominal GDP, perhaps using forward guidance along the following lines: “The Committee expects to maintain the current target range for the federal funds rate until nominal gross domestic product has risen at an average annual rate of [x] percent from its level as of [quarter/year].” To a rough approximation, the deviation of nominal GDP from its target path can be expressed as the sum of the real output gap and the deviation of the GDP price index from an appropriately defined target path. Thus, under this

10 The standard deviation across individual long-run inflation projections in the ECB SPF has been steady at 0.1 to 0.2 percent, with the exception of a transitory jump in dispersion in the March 2009 survey. For further analysis and discussion, see Beechey, Johannsen, and Levin (2010).

11 Refer to Gurkaynak, Levin, and Swanson (2009). While surveys of professional forecasters are a valuable source of quantitative information about longer-run inflation expectations in the euro area or Sweden, it should be recognized that such surveys are only an imperfect proxy for the expectations of financial market participants and wage- and price-setters.

7 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016

approach, the timing of policy liftoff would be contingent on a combination of narrowing resource slack and an upward path of prices.

Adoption of either price-level targeting or nominal GDP targeting would essentially involve a shift towards making policy more history-dependent: The setting of the funds rate target would depend in part on past outcomes, not just on the economic outlook. Moreover, the benefits of such a policy tend to be front-loaded—that is, serving to reduce long-term real interest rates—while the costs are paid later in the form of elevated inflation; thus, the efficacy of such a strategy hinges crucially on the credibility of the monetary policy regime. In that light, it should be noted that no major industrial country has adopted price-level targeting during the modern era, and hence there is no empirical data on how such an approach would perform in practice.

References

Beechey, Meredith, Benjamin Johannsen, and Andrew Levin (2010). “Are Long-Run Inflation Expectations Anchored More Firmly in the Euro Area than in the United States?” Forthcoming, American Economic Journal-Macroeconomics.

Bullard, James, and In-Koo Cho (2005). “Escapist Policy Rules.” Journal of Economic Dynamics and Control, vol. 29, 1841-1865.

Evans, George, Eran Guse, and Seppo Honkapohja (2007). “Liquidity Traps, Learning, and Stagnation.” Manuscript, University of Oregon.

Gürkaynak, Refet, Andrew Levin, and Eric Swanson (2009). “Does Inflation Targeting Anchor Long-Run Inflation Expectations? Evidence from Long-Term Bond Yields in the U.S., U.K., and Sweden.” Forthcoming, Journal of the European Economic Association.

8 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016

Figure 1: Policy Rate Projections from the Sveriges Riksbank October 2008

July 2010

7 90% 75% 50% Outcome Forecast

7

6 6

5 5

4 4

3 3

2 2

1 1

0 0

-1 -1

04 05 06 07 08 09 10 11 12 13

Note: The upper and lower panels reproduce Figure 1 of the Sveriges Riksbank’s Monetary Policy Report

published in October 2008 and July2010, respectively.

9 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016

Figure 2: Policy Rate Projections of the Norges Bank October 2008

June 2010

9 9

8 30% 50% 70% 90%

8

7 7

6 6

5 5

4 4

3 3

2 2

1 1

0 0 2008 2009 2010 2011 2012 2013

Note: The upper panel reproduces figure 1.23a of the Norges Bank’s Monetary Policy Report 3-08, and the

lower panel reproduces figure 1.13a of Monetary Policy Report 2-10 .

10 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016

Figure 3: Dispersion in the Long-Run Inflation Expectations of Professional Forecasters in the Euro Area and the United States

0.8

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0.0

Euro Area HICP

U.S. CPI

U.S. PCE

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Note: This figure depicts the dispersion in the views of professional forecasters’ long-run inflation outlook for the euro area and the United States, as measured by the standard deviation across the individual projections at each date. For the euro area (solid line), these data are taken from the ECB’s quarterly survey of professional forecasters and refer to the 5-year-ahead projected inflation rate for the harmonized index of consumer prices (HICP). For the United States, these data are taken from the Federal Reserve Bank of Philadelphia’s Survey of Professional Forecasters and refer to expected inflation over the next 10 years for the CPI (long dashed line) and the total PCE deflator (short dashed line).

11 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016

Figure 4: Swedish Inflation Outcomes and Long-Run Inflation Expectations

Percent

5 Actual CPI Inflation Long-Run Expected Inflation

4

3

2

1

0 1994 1996 1998 2000 2002 2004 2006 2008

Note: Long-run expected inflation (solid line) denotes the median projection of Swedish CPI inflation 6-to-10-years ahead in the Consensus Economics semiannual survey of professional forecasters. Actual inflation (dashed line) denotes the four-quarter average Swedish CPI inflation rate, excluding household mortgage interest and the direct effects of changes in value-added taxes and subsidies.

12 of 12

Authorized for public release by the FOMC Secretariat on 01/29/2016