powerpoint presentationanimp.it/prodotti_editoriali/news/internazionalizzazione... ·...

TRANSCRIPT

1 Dec 2014

Dec 2014

2 Dec 2014

NPC Organization Chart

National Petrochemical Co. (NPC)

Projects Production

Control

Planning &

Development

Administration

& Training Finance

Ministry of Petroleum

3 Dec 2014

Iran’s Proven Oil Reserves

North America

13,2%

Venezuela

17,8%

Kazakhstan

1,8% Russian

Federation

5,2%

Iran

9,4%

Iraq

9,0% Kuwait

6,1%

Saudi Arabia

15,9%

United Arab

Emirates

5,9%

Africa

7,8%

Asia Pacific

2,5%

Other World

5,4%

Source: BP - Statistical review of world energy - 2013

Global Crude Oil Proven Reserves (End of 2012)

1,669 billion barrels

4 Dec 2014

Natural Gas Proven Reserves

US

4,5%

S. & Cent.

America

4,1%

Russian

Federation

17,6%

Europe &

Eurasia

13,6%

Iran

18,0%

Qatar

13,4%

Saudi Arabia

4,4%

Other World

8,5%

Africa

7,7%

Asia Pacific

8,3%

Source: BP - Statistical review of world energy - 2013

Global Natural Gas Proven Reserves (End of 2012):

187.3 trillion cubic meters

5 Dec 2014

Major Advantages of

Iran’s Petrochemical Industry

Availability of colossal oil-based feedstock

(world’s 4th largest oil reserves)

Availability of huge gas resources containing over

10% C2+ in gas-phase (world’s 2nd largest natural gas

reserves)

Well-developed export & import infrastructure (ports, …)

Iran has numerous advantages in petrochemical

industry

6 Dec 2014

Access to international waters

Large & growing domestic market

Qualified and trained manpower

50 years of experience in petrochemical industry,

the oldest in the Middle East

Major Advantages of

Iran’s Petrochemical Industry

7 Dec 2014

Proximity & access to European and Asian markets

especially the huge Indian & Chinese marketplaces

Development of metal (steel & aluminum) and other

energy-intensive industries

Existence of domestic engineering and availability of

contracting companies & equipment manufacturers

reducing costs of projects implementation

Major Advantages of

Iran’s Petrochemical Industry

8 Dec 2014

Chabahar

Special

Economic Zone

Petrochemical Development Zones

Petrochemical

Special Economic

Zone

Pars Special

Economic - Energy

Zone

Sarakhs

Qeshm Kish

Lavan

North Pars

Tehran

Caspian Sea

Iranshahr

9 Dec 2014

Petrochemical Special Economic Zone

Bandar Imam

(Mahshahr)

10 Dec 2014

Pars Special Economic / Energy Zone

Assaluyeh

11 Dec 2014

West Ethylene Pipeline

3 Supplier complexes with 3.5 Million tons/yr capacity

11consumers with 3.2 Million tons/yr capacity

12 Dec 2014

0,1 2,7

3,1 5,4

10,3 10,6

14,2

14,5

18,2

20,4

51,1 54,5

57,1 60

0

10

20

30

40

50

60

70

Mil

lion

Ton

s

Capacity By the End of 2013

13 Dec 2014

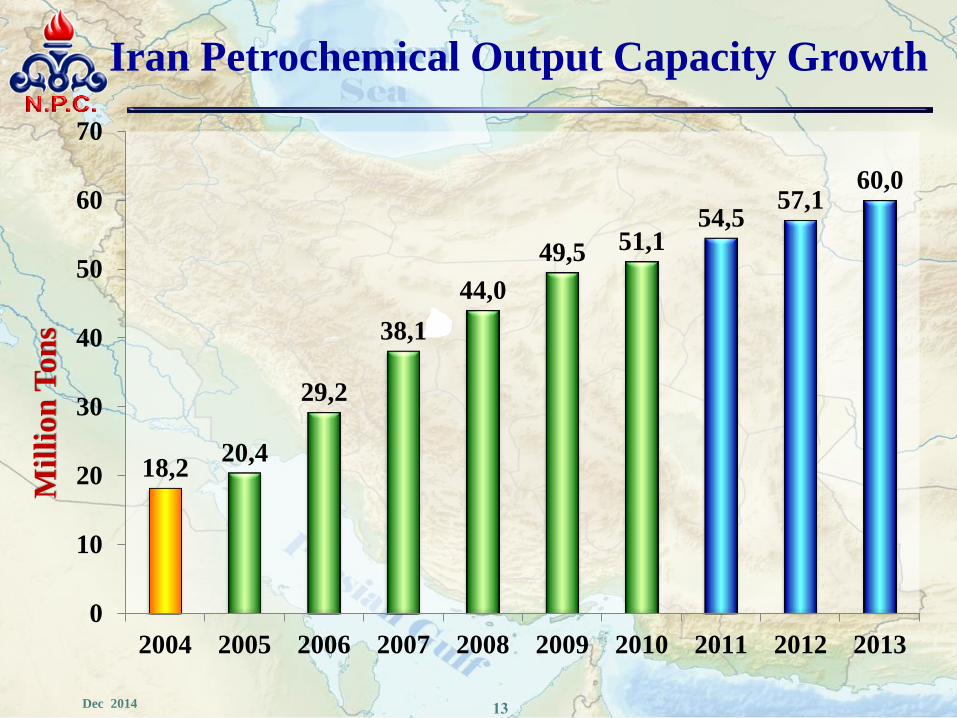

Iran Petrochemical Output Capacity Growth

18,2 20,4

29,2

38,1

44,0

49,5 51,1 54,5

57,1 60,0

0

10

20

30

40

50

60

70

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Mil

lio

n T

on

s

14 Dec 2014

Iran Petrochemical Export &

Domestic Demand

5,2 5,2 6

9,5

12,3

14,2

17,9 18,2

15,8

13

4,8 4,9 6,1 6,4

7,6 7,9

10,5

12 13,3

14.5

0

2

4

6

8

10

12

14

16

18

20

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Export Domestic Demand

Mil

lion t

on

s

15 Dec 2014

16 Dec 2014

No. of Projects 67

Design Capacity 61 Million Tons/Yr

Products Value 32 Billion USD/ Yr

Average Physical Progress 20 %

Total Capital Investment 39 Billion USD

Projects under Implementation

17 Dec 2014

No. of Projects 36

Design Capacity 60 Million Tons/ Yr

Saleable Products 28 Million Tons/ Yr

Value of Saleable Products 30 Billion USD/ Yr

Total Capital Investment 42 Billion USD

New Investment Opportunities

18 Dec 2014

PRIVATIZATION

Petrochemical industry’s privatization gained

momentum according to Article 44 of IRAN’s

Constitution.

Based on the Article, NPC, as a state-owned

company has investment restriction.

Best option for private sector investment is

investing in basic, mid & downstream

production chain projects.

19 Dec 2014

20 Dec 2014

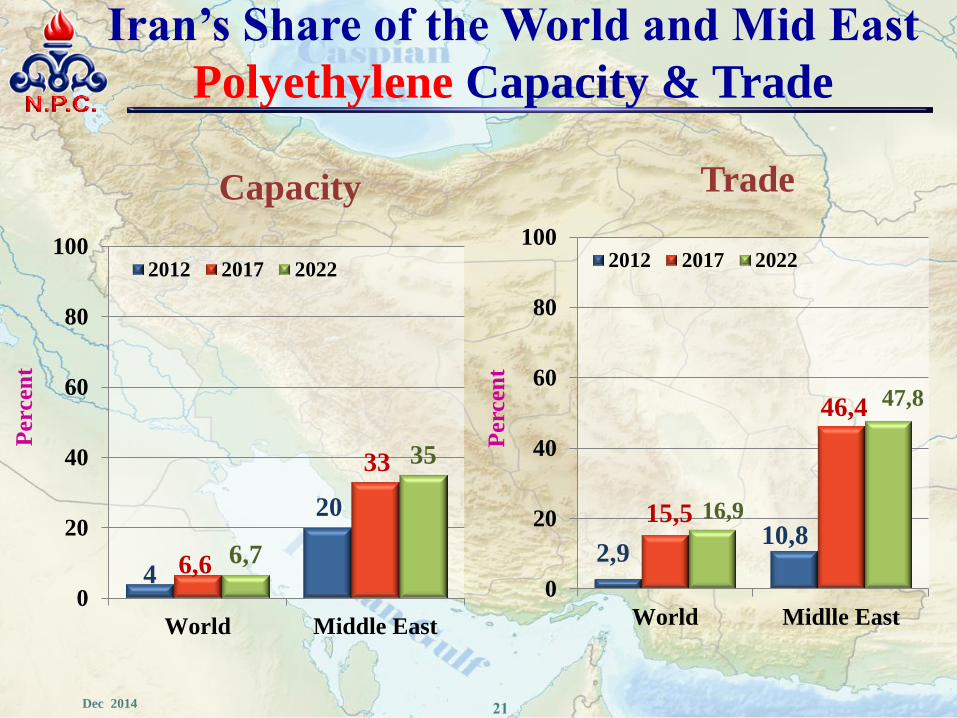

Iran’s Share of the World and Mid East

Ethylene Capacity

The international trade of ethylene is quite limited due to expenses associated with

transportation. As a result, most ethylene that crosses international borders is in the form of

derivative chemicals, such as polyethylene, ethylene glycol, and EDC.

4

22,1

7

32

7,5

32

0

10

20

30

40

World Middle East

Per

cen

t

2012 2017 2022

21 Dec 2014

4

20

6,6

33

6,7

35

0

20

40

60

80

100

World Middle East

Perc

en

t

Capacity

2012 2017 2022

2,9 10,8

15,5

46,4

16,9

47,8

0

20

40

60

80

100

World Midlle East

Perc

en

t

Trade

2012 2017 2022

Iran’s Share of the World and Mid East

Polyethylene Capacity & Trade

22 Dec 2014

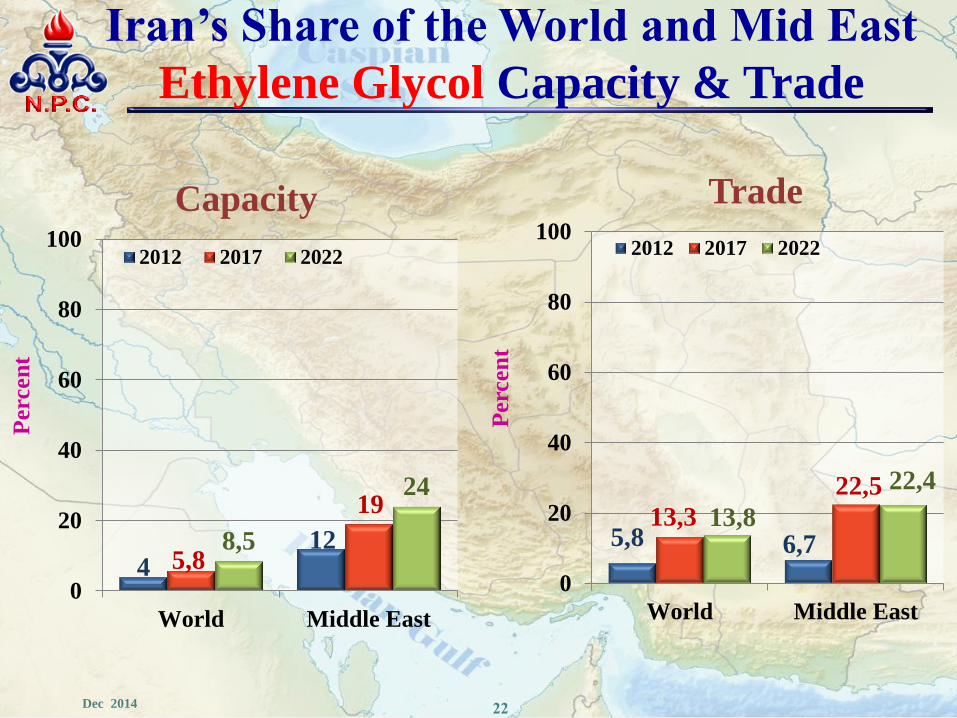

4 12

5,8

19

8,5

24

0

20

40

60

80

100

World Middle East

Perc

en

t

Capacity

2012 2017 2022

5,8 6,7 13,3

22,5

13,8

22,4

0

20

40

60

80

100

World Middle East

Perc

en

t

Trade

2012 2017 2022

Iran’s Share of the World and Mid East

Ethylene Glycol Capacity & Trade

23 Dec 2014

1

12

2,2

19

6,5

37

0

10

20

30

40

World Middle East

Perc

en

t

2012 2017 2022

Iran’s Share of the World and Mid East

Propylene Capacity

International trade of propylene monomer is quite limited because of the costs of

transporting highly pressurized or refrigerated liquids. Most of the propylene trade

crossing international borders is in the form of derivative chemicals, such as

polypropylene and acrylonytrile.

24 Dec 2014

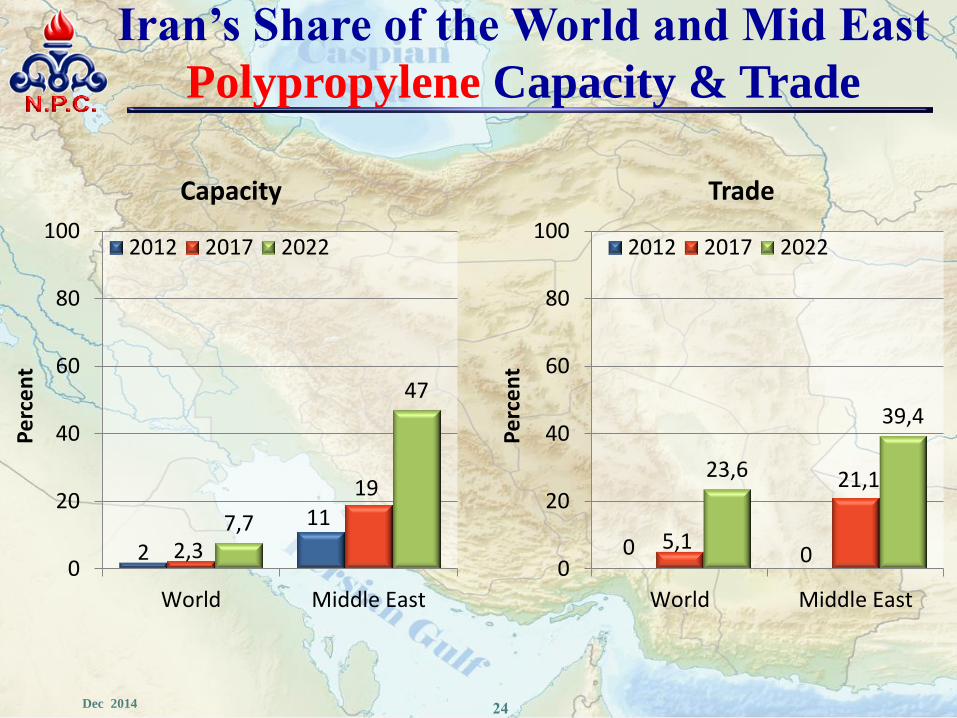

2

11

2,3

19

7,7

47

0

20

40

60

80

100

World Middle East

Pe

rce

nt

Capacity

2012 2017 2022

0 0 5,1

21,1 23,6

39,4

0

20

40

60

80

100

World Middle East

Pe

rce

nt

Trade

2012 2017 2022

Iran’s Share of the World and Mid East

Polypropylene Capacity & Trade

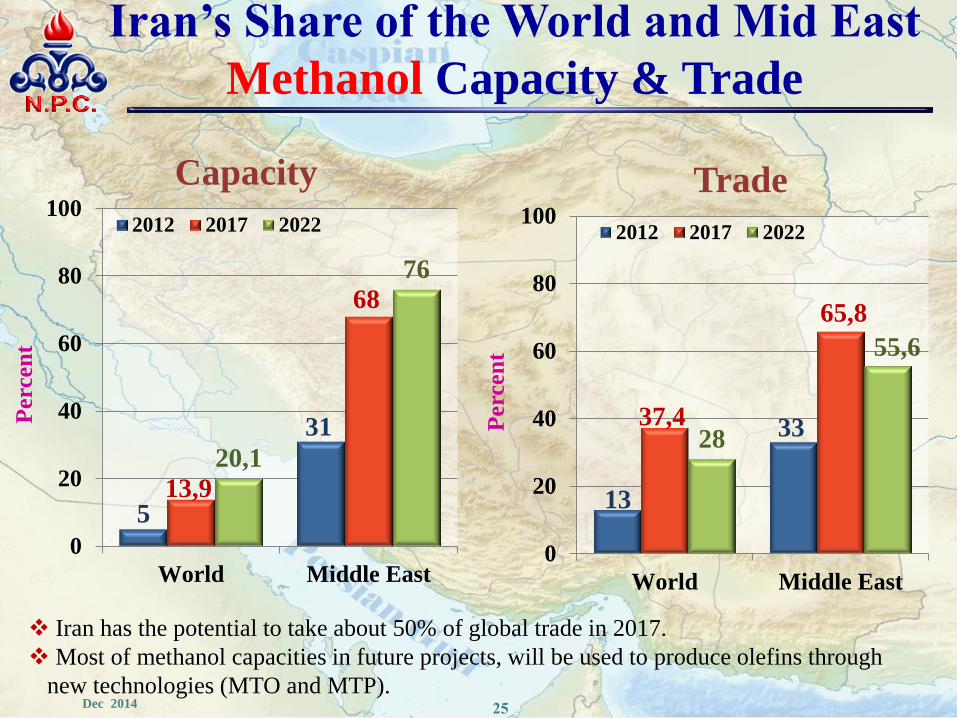

25 Dec 2014

5

31

13,9

68

20,1

76

0

20

40

60

80

100

World Middle East

Perc

en

t

Capacity

2012 2017 2022

13

33 37,4

65,8

28

55,6

0

20

40

60

80

100

World Middle East

Perc

en

t

Trade

2012 2017 2022

Iran’s Share of the World and Mid East

Methanol Capacity & Trade

Iran has the potential to take about 50% of global trade in 2017.

Most of methanol capacities in future projects, will be used to produce olefins through

new technologies (MTO and MTP).

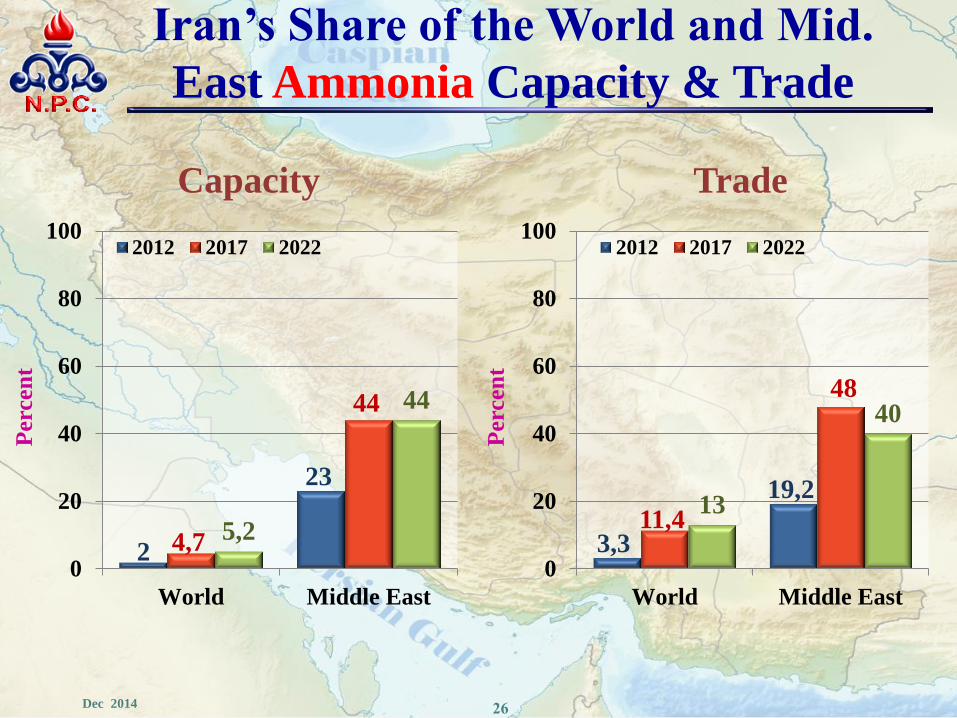

26 Dec 2014

2

23

4,7

44

5,2

44

0

20

40

60

80

100

World Middle East

Perc

en

t

Capacity

2012 2017 2022

3,3

19,2

11,4

48

13

40

0

20

40

60

80

100

World Middle East

Perc

en

t

Trade

2012 2017 2022

Iran’s Share of the World and Mid.

East Ammonia Capacity & Trade