powerpoint presentation management... · your buying power would be reduced to $10,000 you would...

TRANSCRIPT

SFC/US/45665/6.13/V4/07SEC419-12

SFC/US/45665/6.13/V4/07SEC419-12

An investor should carefully consider a fund’s risks, investment objectives, charges, and expenses before

investing. The prospectus contains this and other information about the fund. You can obtain a prospectus

from your PFSI Registered Representative. Please read and consider the prospectus carefully before

investing.

Investing in mutual funds entails some risk. Investment return and principal may fluctuate. Shares, when

redeemed, may be worth more or less than their original value.

Investments Offered By:

PFS Investments Inc.

1 Primerica Parkway

Duluth, GA 30099-0001

470-381-1000

NOTE TO REGISTERED REPRESENTATIVE: You must use the speaker’s notes included with this presentation.

Also, this presentation should accompany the client-approved Asset Management Brochure (Item #A8864).

Primerica and PFS Investments are affiliated companies.

SFC/US/45665/6.13/V4/07SEC419-12

Let Primerica help you make the most of your money.

• In business since 1977

• More than 2 million clients maintain investment accounts with us

• Investment clients have more than $40 billion in asset values in their PFSI investment accounts

Primerica refers to Primerica and its affiliated companies.

SFC/US/45665/6.13/V4/07SEC419-12

Most People Don’t Plan to Fail, They Fail to Plan.

SFC/US/45665/6.13/V4/07SEC419-12

Today’s Financial Challenges

… Six of every 10 workers “always” or “usually” live paycheck to paycheck. — finance.yahoo.com, viewed June 28, 2011

57% of Americans polled reported that they have less than $25,000 saved for retirement. — 2013 Retirement Confidence Survey

Only 13% of workers surveyed said they were “very confident” about having enough money to live comfortably through retirement. — 2013 Retirement Confidence Survey

Instead of doing a systematic calculation, 54% of workers continue to guess at how much they will need to accumulate for retirement. — 2013 Retirement Confidence Survey

How do you feel about your current financial situation?

SFC/US/45665/6.13/V4/07SEC419-12

Pay Yourself First!

1. Put yourself at the head of the line. • Rule of thumb: save 10% of your income

• Treat it as a bill that you owe to yourself and your family

2. Set up a complete savings program with three accounts. Account Purpose 1. Emergency Fund Cover unforeseen expenses 2. Short-Term Savings Vacation, new computer, etc... 3. Long-Term Savings Retirement, college, etc...

Do you have a program in place for a comfortable retirement?

SFC/US/45665/6.13/V4/07SEC419-12

How Most People Save

You invest $10,000 at a four percent rate of return with your local bank ...

You earn interest for the year: $400

But you pay $100 in taxes on that interest at 25%*: -$100

So your net earnings are: $300

Your resulting balance would be: $10,300

...but if inflation is 3%, your buying power would be reduced to $10,000

You would have actually earned no gain to your purchasing power!

*The 25% tax bracket is hypothetical and your tax bracket may be different. If your tax bracket is not 25%, the results will vary.

Can you afford a guarantee?

SFC/US/45665/6.13/V4/07SEC419-12

Become an Owner, Not a Loaner

Savings Accounts, CDs, Cash Value Life Insurance =

Historically Low Rates of Return

CDs and savings accounts are generally FDIC insured up to $250,000. The $250,000 limit expires December 31, 2013.

Your Money Global

Economy

SFC/US/45665/6.13/V4/07SEC419-12

The Rule of 72

72 ÷ 12% 6 Years

72 ÷ 4% 18 Years

72 ÷ 6% 12 Years

This simple calculation (72 ÷ the interest rate) gives you the approximate

number of years it will take to double your savings:

This table serves as a demonstration of how the Rule of 72 concept works from a mathematical standpoint. It is a hypothetical and is only an approximation of accumulations. It is not intended to represent any specific savings vehicle. The chart uses constant rates of return, unlike actual investments which will fluctuate in value. It does not include fees or taxes, which would lower performance.

SFC/US/45665/6.13/V4/07SEC419-12

The Rule of 72

# of Years 4% Return

0 $10,000

6

12

18 $20,000

24

30

36 $40,000

This table serves as a demonstration of how the Rule of 72 concept works from a mathematical standpoint. It is a hypothetical and is only an approximation of accumulations. It is not intended to represent any specific savings vehicle. The chart uses constant rates of return, unlike actual investments which will fluctuate in value. It does not include fees or taxes, which would lower performance.

A one-time

contribution of

$10,000 doubles

4 more times at

12% than at 4%.

6% Return

$10,000

$20,000

$40,000

$80,000

12% Return

$10,000

$20,000

$40,000

$80,000

$160,000

$320,000

$640,000

How many doubling periods do you have in your life?

SFC/US/45665/6.13/V4/07SEC419-12

Rate of Return Is the Key

Growth of a $10,000 Investment (December 31, 1982 to December 31, 2012)

Investing in mutual funds may be a very good way!

What kind of return do you need to reach your goals?

How can you invest to reach them?

S&P 500

Total Return 10.80% $217,197

Bonds 8.10% $103,534

30 Day T-Bills 4.29% $35,337

U.S. Inflation 2.91% $23,642

Source: Morningstar. Past performance is no guarantee of future results. This chart is for illustrative purposes and does not represent an actual investment. Further, the returns do not reflect the

past or future performance of any specific investment. All investments involve risk including loss of principal. The figures in the chart above assume reinvestments of dividends. They do not reflect

any fees, expenses or tax consequences, which would lower results. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their

performance. Investors cannot invest directly in any index. Government bonds and Treasury bills are guaranteed by the full faith and credit of the United States government as to the timely payment

of principal and interest, while stocks are not guaranteed and have been more volatile than other asset classes. As interest rates rise, bond prices fall.

The figures represent an initial investment of $10,000. The Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general. Bonds are

represented by the Barclays Capital Aggregate Bond Index is an intermediate term market capitalization — weighted index, meaning the securities in the index are weighted according to the market size of

each bond type. Most U.S. traded investment grade bonds are represented. Municipal bonds and treasury inflation-protected securities are excluded, due to tax treatment issues. The index includes treasury

securities, government agency bonds, mortgage-backed bonds, corporate bonds, and a small amount of foreign bonds traded in U.S. The U.S. 30-Day T-bills are government backed short-term investments

considered to be risk-free and as good as cash because the maturity is only one month and are represented by the IA SBBI US 30 Day TBill TR index. Inflation history is represented by the IA SBBI US Inflation

index. Small Company Stocks – Dimensional Fund Advisors, Inc. (DFA) U.S. Micro Cap Portfolio; Large Company Stocks – Standard & Poor’s 500 ©, which is an unmanaged group of securities, is considered to be

representative of the stock market in general; Long-Term Government Bonds – 20-year U.S Government Bond; Treasury Bills – 30-Day U.S. Treasury Bill; International Stocks – Morgan Stanley Capital

International Europe, Australasia, and Far East (EAFE) Index.

SFC/US/45665/6.13/V4/07SEC419-12

Think Long Term

Look at the record of positive results over calendar periods, from January 1, 1943 through December 31, 2012.

These rolling time periods begin January 1, 1943 with each subsequent time period beginning again January of the following year. The final rolling periods of each are as follows: 1-Year Periods (January 1, 2012 – December 31, 2012); 3-Year Periods (January 1, 2010 – December 31, 2012); 5-Year Periods (January 1, 2008 – December 31, 2012); 10-Year Periods (January 1, 2003 – December 31, 2012); and 20-Year Periods (January 1, 1993 – December 31, 2012).

Source: Morningstar. Past performance is no guarantee of future results. This chart is for illustrative purposes and does not represent an actual investment. The returns do not reflect the past or future performance of any specific investment. All investments involve risk including loss of principal. The figures in the chart above assume reinvestments of dividends. They do not reflect any fees, expenses or tax consequences, which would lower results. The Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general. The data assumes reinvestment of all income and does not account for taxes or transaction costs. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index.

1-Year Periods

55 Positive periods

15 Negative periods

3-Year Periods

60 Positive periods

8 Negative periods

5-Year Periods

59 Positive periods

7 Negative periods

10-Year Periods

59 Positive periods

2 Negative periods

20-Year Periods

51 Positive periods

0 Negative periods

What has been your experience in the market?

SFC/US/45665/6.13/V4/07SEC419-12

What’s one of the most effective long-term investment vehicles? — Mutual Funds

What is a mutual fund?

Note: Each mutual fund invests differently. Read the mutual fund’s prospectuses to determine how a fund may invest and to determine its current holdings. Mutual funds are actively managed portfolios and incur advisory fees and internal management costs. Investment in mutual funds does not assure a profit. The value of funds fluctuates, and, when redeemed, may be worth less than their original value. List of companies does not constitute a recommendation to buy or sell securities.

Source: Morningstar. Average based on 3,276 U.S. domestic equity open-end funds.

Did you know?

The typical mutual fund holds more than 150 stocks on average.**

Professionally

Individual Investors Managed Money Top Holdings Examples

CONSUMER

The Procter & Gamble Company

(Folger’s, Crest, Duracell,

Gillette, Tide)

ENTERTAINMENT

The Walt Disney Company

(ABC Television Network, Disney

Channel, Walt Disney World

Theme Park)

PHARMACEUTICALS

Pfizer, Inc.

(Zyrtec, Zoloft, Celebrex)

TELECOMMUNICATIONS

Verizon Communications, Inc.

(Wireless, long-distance telephone,

broadband Internet)

CONSUMER

McDonald’s Corporation

TECHNOLOGY

Microsoft Corporation

(Windows computer software, Xbox

video game system)

SFC/US/45665/6.13/V4/07SEC419-12

Mutual funds earn money three ways:

1. Dividends

2. Capital Gains

3. Capital Appreciation

Should any of these be earned, they may be subject to taxation. Also note that the value of a fund may fluctuate.

SFC/US/45665/6.13/V4/07SEC419-12

5 Great Reasons to Own a Mutual Fund:

1. Professional money management

2. Diversification of assets

3. Growth potential

4. Affordability

5. Liquidity

Mutual funds are not guaranteed against a loss. Mutual funds also have costs and fees that are attributable to management and distribution.

SFC/US/45665/6.13/V4/07SEC419-12

A Tale of Five Investors

1. $10,000 invested August 31, 1987

2. Market crash in October 1987

3. Each investor left with $7,674

How did they react?

SFC/US/45665/6.13/V4/07SEC419-12

A Tale of Five Investors

Ending amounts as of December 31, 2012, based on five different actions taken on October

31, 1987.

Source: PFS Investments Inc. and Morningstar. The chart illustrates a hypothetical

investment of $10,000 invested in an investment that performed similar to the S&P 500 TR

Index on August 31, 1987, near the market high, and then the subsequent financial impact

of various investment strategies on a portfolio implemented on October 31, 1987, after the

market crash on October 19, 1987 through December 31, 2012. Investors 4 & 5’s monthly

contributions began November 30, 1987. The Standard & Poor’s 500 ®, which is an

unmanaged group of securities, is considered to be representative of the stock market in

general. An investor cannot invest directly in an index. The average annualized return of

the S&P 500 from the period 12/31/86 - 12/31/12 was 9.52%. The investor 2 & 4 examples

use Western Asset Liquid Reserves N (USD, CIRXX) as the basis for their dollar values. The

month end current 7-day yield was 0.01% as of October 31, 2012. Performance data

current to the most recent month-end can be located on the fund fact card, which is

available at www.leggmason.com/individualinvestors. Performance data quoted represents

past performance.

Past performance is no guarantee of future results. Principal value and investment

returns will fluctuate and, when redeemed, may be worth more or less than the

original cost. This chart is for illustrative purposes, does not illustrated an actual

investment, and the returns to not represent the past or future performance of any

specific investment. Investments in mutual funds involve risk including loss of principal.

The figures in the chart above assume reinvestments of dividends and do not reflect any

fees, expenses or tax consequences, which may lower results.

A money market fund is an investment company that invests in commercial paper,

banker’s acceptances, repurchase agreements, government securities, certificates of

deposit and other highly liquid securities, and pays money market rates of interest. Money

markets are not FDIC-insured nor are they guaranteed by any other government agency,

may lose money, and are not guaranteed by a bank or other financial institution. Although

the money market seeks to preserve a stable per share value (i.e., $1.00 per share), it is

possible to lose money by investment in the fund.

Systematic investing cannot assure a profit or protect against loss in declining markets.

Since systematic investing involves continuous investments over time regardless of

fluctuating price levels, the investor should consider his or her ability to continue to invest

in periods of low price levels. The value of stocks will fluctuate based on market

conditions. Stocks are not insured.

$18,981

Investor 2 sold the investment and put the money into a money market fund.

$76,808 Investor 3 held on to the investment, but did not begin their monthly investment program.

$215,367

Investor 4 sold the investment, reinvested the amount in a money market fund and began to invest $458 each month.

$488,744

Investor 5 held tight and started to invest $458 each month.

Outcomes for each of the five investors as of the end of 2012:

How would you react?

$7,674

Investor 1 sold the investment and put the money under a mattress.

SFC/US/45665/6.13/V4/07SEC419-12

It’s time, not timing, that matters

$10,000 investment for 20 years during worst times vs. best times

$10,000 investments are made immediately following market high (or market low) month-end date.

Example: In the market high scenario, the first $10,000 contribution is made immediately following the last trading day of the month.

*January dates denoted with an asterisk indicate the $10,000 was invested immediately prior to the first trading day of the year (January).

Source: Morningstar. Past performance is no guarantee of future results. This chart is for illustrative purposes and does not represent an actual investment but instead the performance of the S&P 500. The returns do not reflect the past or future performance of any specific investment. All investments involve risk including loss of principal. The figures in the chart above assume reinvestments of dividends and do not reflect any fees, expenses or tax consequences.

The Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general. The data assumes reinvestment of all income and does not account for taxes or transaction costs which may lower results. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index.

Invest Near Market Highs

Date Cumulative Account

Investment Value Dec. 31

Dec 93 $10,000 $10,000

Aug 94 $20,000 $19,887

Dec 95 $30,000 $37,331

Nov 96 $40,000 $55,749

Dec 97 $50,000 $84,345

Dec 98 $60,000 $118,450

Dec 99 $70,000 $153,374

Aug 00 $80,000 $148,141

Jan 01 $90,000 $139,043

Mar 02 $100,000 $116,082

Dec 03 $110,000 $159,380

Dec 04 $120,000 $186,724

Dec 05 $130,000 $205,895

Dec 06 $140,000 $248,415

Oct 07 $150,000 $281,578

Jan 08* $160,000 $177,400

Dec 09 $170,000 $234,348

Dec 10 $180,000 $279,649

Apr 11 $190,000 $294,918

Sep 12 $200,000 $352,078

Annualized Compound Return

(Dec 31, 1993 - Dec. 31, 2012):

+8.15%

Invest Near Market Lows

Date Cumulative Account

Investment Value Dec. 31

Jan 93* $10,000 $10,999

Mar 94 $20,000 $31,675

Jan 95* $30,000 $53,531

Jan 96* $40,000 $75,883

Jan 97* $50,000 $101,196

Aug 98 $60,000 $153,023

Jan 00* $70,000 $185,222

Nov 00 $80,000 $178,407

Sep 01 $90,000 $168,271

Sep 02 $100,000 $141,926

Feb 03 $110,000 $206,052

Jan 04* $120,000 $228,475

Apr 05 $130,000 $260,626

Jan 06* $140,000 $301,790

Feb 07 $150,000 $328,970

Nov 08 $160,000 $217,365

Feb 09 $170,000 $290,345

Jun 10 $180,000 $346,408

Sep 11 $190,000 $374,905

Jan 12* $200,000 $434,903

Annualized Compound Return

(Dec 31, 1993 - Dec. 31, 2012):

+8.25%

Do you see the importance of time in the market vs. timing?

SFC/US/45665/6.13/V4/07SEC419-12

Unem

plo

ym

ent

reaches

9.7

%

Gre

ece B

ailout

Mort

gage f

ore

clo

sure

s sp

ike

Asi

an t

sunam

i st

rikes

Terr

ori

sts

att

ack A

meri

ca

Asi

a s

uff

ers

wid

esp

read f

inancia

l cri

sis

Okla

hom

a C

ity b

om

bin

g k

ills

168 p

eople

Bosn

ian w

ar

begin

s

Dow

dro

ps

190 p

oin

ts o

n O

cto

ber

13,

second w

ors

t dro

p in h

isto

ry

U.S

. bom

bs

Lib

ya

Double

-dig

it u

nem

plo

ym

ent

Ris

ing g

as

pri

ces

U.S

. in

vades

Iraq

Technolo

gy s

tock b

ubble

burs

ts

Milit

ant

Taliban leaders

take K

abul

Fed r

ais

es

inte

rest

rate

s si

x t

imes

U.S

. ente

rs G

ulf

War

to lib

era

te K

uw

ait

Junk b

ond d

eale

r M

ichael M

ilken c

harg

ed w

ith insi

der

tradin

g

U.S

. fa

ces

record

budget

defi

cit

s

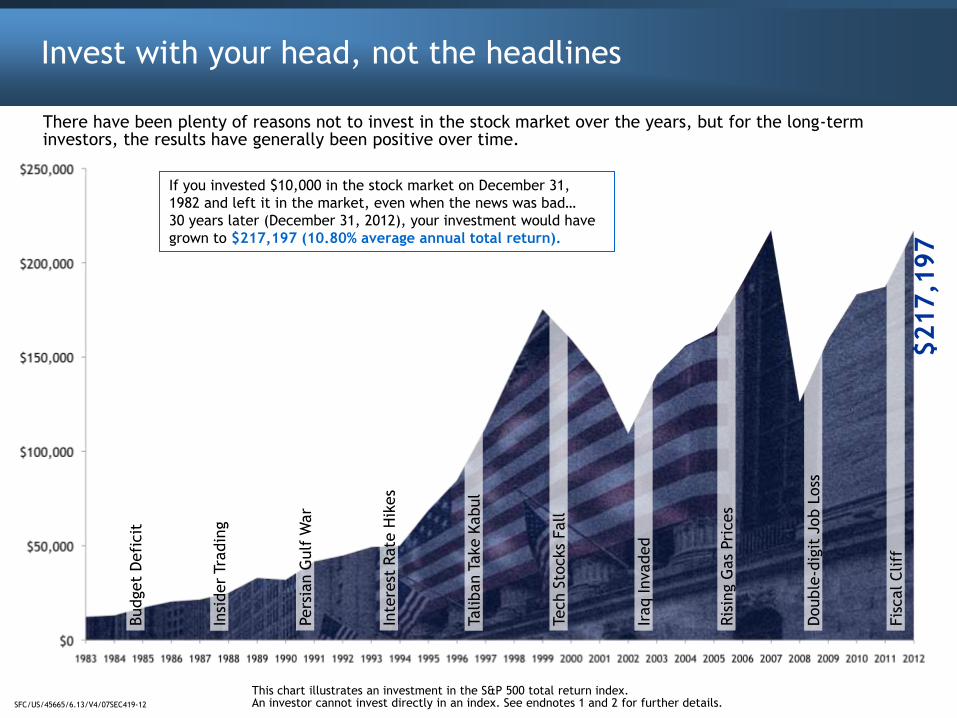

Invest with your head, not the headlines

This chart illustrates an investment in the S&P 500 total return index. An investor cannot invest directly in an index. See endnotes 1 and 2 for further details.

Fis

cal Cliff

Double

-dig

it J

ob L

oss

Ris

ing G

as

Pri

ces

Iraq Invaded

Tech S

tocks

Fall

Taliban T

ake K

abul

Inte

rest

Rate

Hik

es

Pers

ian G

ulf

War

Insi

der

Tradin

g

Budget

Defi

cit

There have been plenty of reasons not to invest in the stock market over the years, but for the long-term investors, the results have generally been positive over time.

If you invested $10,000 in the stock market on December 31,

1982 and left it in the market, even when the news was bad…

30 years later (December 31, 2012), your investment would have

grown to $217,197 (10.80% average annual total return).

$217,1

97

SFC/US/45665/6.13/V4/07SEC419-12

Source: Morningstar. Past performance is no guarantee of future results. This chart illustrates a hypothetical investment of $10,000 in an investment which performed similarly to the S&P 500 total return index. Dates reflected are from January 1 through December 31 of each year, respectively. This chart is for illustrative purposes and does not represent an actual investment. The returns do not reflect the past or future performance of any specific investment. All investments involve risk including loss of principal. The figures in the chart above assume reinvestments of dividends. They do not reflect any fees, expenses or tax consequences, which would lower results. The Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general. The data assumes reinvestment of all income and does not account for taxes or transaction costs which may lower results. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index. See next slide for additional notes.

Invest with your head, not the headlines

Average Annual Total Return: 10.80%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$ Market Value 140,749 156,065 163,731 189,591 217,197 126,209 159,356 183,361 187,233 217,197

Total % Return 28.68 10.88 4.91 15.79 5.49 -37.00 26.46 15.06 2.11 16.00

Events Iraq Asian Hurricane Rising Gas Mortgage Financial Double-digit Greece EU Debt Fiscal Invaded Tsunami Katrina Prices Crisis Crisis Job Loss Bailout Crisis Cliff

1983 1984 1985 1986 1987 1988 1989 1990 1991 1992

$ Market Value 12,256 13,024 17,157 20,359 21,428 24,987 32,904 31,883 41,596 44,765

Total % Return 22.56 6.27 31.73 18.67 5.25 16.61 31.69 -3.10 30.47 7.62

Events Massive Iran/Iraq Budget Libya Black Insider Market Airline Persian Bosnian Layoffs War Deficit Bombed Monday Trading Crash Bankruptcy Gulf War War

Do you see how, over time, you can achieve your investing goals regardless of the headlines?

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

$ Market Value 49,277 49,928 68,690 84,641 112,640 144,831 175,305 159,345 140,405 109,375

Total % Return 10.08 1.32 37.58 22.96 33.36 28.58 21.04 -9.10 -11.89 -22.10

Events WTC Interest Oklahoma Budget Taliban Asian Y2K Tech Terrorism Accounting Bombing Rate Hikes City Bombing Crisis Take Kabul Market Crash Fears Stocks Fall Attack Scandals

SFC/US/45665/6.13/V4/07SEC419-12

Invest with your head, not the headlines

1. The figures represent an initial investment of $10,000. The Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general. Bonds are represented by the Barclays Capital Aggregate Bond Index is an intermediate term market capitalization — weighted index, meaning the securities in the index are weighted according to the market size of each bond type. Most U.S. traded investment grade bonds are represented. Municipal bonds and treasury inflation-protected securities are excluded, due to tax treatment issues. The index includes treasury securities, government agency bonds, mortgage-backed bonds, corporate bonds, and a small amount of foreign bonds traded in U.S. The U.S. 30-Day T-bills are government backed short-term investments considered to be risk-free and as good as cash because the maturity is only one month. Morningstar collects yields on the T-bill on a weekly basis from The Wall Street Journal. Treasury Bills are secured by the full faith and credit of the U.S. Government and offer a fixed rate of return, while an investment in the stock market offers no such guarantee. Inflation history is gathered from the Ibbotson Stocks, Bonds, Bills and Inflation module.

2. An investment such as stocks represented by the S&P Index may not be appropriate for an investor seeking a short-term investment or who is unwilling to experience the volatility, including the potential loss of principal. Source: PFS Investments Inc. and Morningstar. The chart above illustrates a hypothetical investment of $10,000 invested in the S&P 500 TR Index on August 31, 1987, near the market high, and then the subsequent financial impact of various investment strategies on a portfolio implemented on October 31, 1987, after the market crash on October 19,1987 through December 31, 2012. Investors 4 & 5’s monthly contributions began November 30, 1987. The Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general. An investor cannot invest directly in an index. Systematic investing cannot assure a profit or protect against loss in declining markets. Since systematic investing involves continuous investments over time regardless of fluctuating price levels, the investor should consider his or her ability to continue to invest in periods of low price levels. A money market fund is an investment company that invests in commercial paper, banker’s acceptances, repurchase agreements, government securities, certificates of deposit and other highly liquid securities, and pays money market rates of interest. Money markets are not FDIC-insured, may lose money, and are not guaranteed by a bank or other financial institution. Although the money market seeks to preserve a stable per share value (i.e., $1.00 per share), it is possible to lose money by investment in the fund. Principal value and investment returns will fluctuate and, when redeemed, may be worth more or less than the original investment amount.

3. An investment such as stocks represented by the S&P Index may not be appropriate for an investor seeking a short-term investment or who is unwilling to experience the volatility, including the potential loss of principal. The Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general. The data assumes reinvestment of all income and does not account for taxes or transaction costs. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index.

Government bonds and Treasury bills are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than the other asset classes. Furthermore, small company stocks are more volatile than large company stocks and are subject to significant price fluctuations, business risks and are thinly traded. International investments involve special risks such as fluctuations in currency, foreign taxation, economic and political risks, liquidity risks and differences in accounting and financial standards. The data assumes reinvestment of all income and does not account for taxes or transaction costs. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index.

SFC/US/45665/6.13/V4/07SEC419-12

Systematic Investing: A Proven Method

• Two investors • $100/month • Different Markets

Which example would you prefer?

Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

$20 18 16 14 12 10 8 6 4 2 0

Share

Pri

ce

A

Investor A

Systematic Investing allows you to use dollar-cost averaging to build wealth over the long term.

Investor A

invests $100 a month in a rising market.

Investor B

B

Investor B

invests $100 a month in a fluctuating market.

Dollar-cost averaging is a technique for lowering the average cost per share over time. While a continuous program of dollar-cost averaging can reduce cost per share over time, it cannot

assure a profit or protect against loss in declining markets. Since dollar-cost averaging involves continuous investments over time, the investor should consider his or financial ability to

continue purchases through low price levels. The values shown are hypothetical, not intended to reflect any specific market period but to demonstrate the effect of a fluctuating market.

SFC/US/45665/6.13/V4/07SEC419-12

Systematic Investing: A Proven Method

Put your investment program on autopilot. Enroll in Pre-Authorized Checking (PAC). Set up regularly scheduled automatic money transfers from your bank account to your investment account. Dollar-cost averaging is a technique for lowering the average cost per share over time. While a continuous program of dollar-cost averaging can reduce cost per share over time, it cannot assure a profit or protect against loss in declining markets. Since dollar-cost averaging involves continuous investments over time, the investor should consider his or her financial ability to continue purchases through low price levels. The values shown are hypothetical, not intended to reflect any specific market period but to demonstrate the effect of a fluctuating market.

Systematic Investing allows you to use dollar-cost averaging to build wealth over the long term.

Investor A Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Per share: $10 $12 $14 $16 $18 $20 # of shares: 10.00 8.33 7.14 6.25 5.56 5.00

Investor B Month 1 Month 2 Month 3 Month 4 Month 5 Month 6

Per share: $10 $7 $4 $2 $6 $10 # of shares: 10.00 14.29 25.00 50.00 16.67 10.00

Invests $100 per month

Invests $100 per month

Number of Shares Accumulated

42

Number of Shares Accumulated

126

Amount Invested Number of Shares Average Cost

in 6 months Accumulated

Per Share

A $600 42.28 $14.19

B $600 125.95 $4.76

SFC/US/45665/6.13/V4/07SEC419-12

Diversification is a time-tested principle.

Spread out your investment dollars to protect against market risk.

Source: Morningstar. Past performance is no guarantee of future results. This chart is for illustrative purposes only and does not represent an actual investment or the performance of any specific investment. All investments involve risk including loss of principal. Small Company Stocks—Russell 2000 Index; Large Company Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general; Long-Term Government Bonds—20-year U.S. Government Bond; Treasury Bills—30-day U.S. Treasury Bill; International Stocks—Morgan Stanley Capital International Europe, Australasia, and Far East (EAFE) Index. Government bonds and Treasury bills are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than the other asset classes. As interest rates rise, bond prices fall. Bond funds do not carry the same guarantees as bonds themselves. Furthermore, small company stocks are more volatile than large company stocks and are subject to significant price fluctuations, business risks and are thinly traded. International investments involve special risks such as fluctuations in currency, foreign taxation, economic and political risks, liquidity risks and differences in accounting and financial standards. The data assumes reinvestment of all income and does not account for taxes or transaction costs which may lower results. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index.

What is the ideal asset mix?

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Large

Stocks

28.6%

Small

Stocks

29.8%

LT Gov’t

Bonds

21.5%

Small

Stocks

22.8%

LT Gov’t

Bonds

17.8%

Small

Stocks

60.7%

Int’l

Stocks

20.7%

Int’l

Stocks

14.0%

Int’l

Stocks

26.9%

Int’l

Stocks

11.6%

LT Gov’t

Bonds

25.9%

Int’l

Stocks

32.5%

Small

Stocks

31.3%

LT Gov’t

Bonds

28.2%

Small

Stocks

18.2%

Int’l

Stocks

20.3%

Int’l

Stocks

27.3%

30-Day

T-Bills

5.9%

30-Day

T-Bills

3.8%

30-Day

T-Bills

1.7%

Int’l

Stocks

39.2%

Small

Stocks

18.4%

LT Gov’t

Bonds

7.8%

Small

Stocks

16.2%

LT Gov’t

Bonds

9.9%

30-Day

T-Bills

1.7%

Small

Stocks

28.1%

Large

Stocks

15.1%

Large

Stocks

2.1%

Int’l

Stocks

17.9%

LT Gov’t

Bonds

13.1%

Large

Stocks

21.0%

Small

Stocks

-3.6%

LT Gov’t

Bonds

3.7%

Int’l

Stocks

-15.7%

Large

Stocks

28.7%

Large

Stocks

10.9%

Small

Stocks

5.7%

Large

Stocks

15.8%

Large

Stocks

5.5%

Small

Stocks

-36.7%

Large

Stocks

26.5%

LT Gov’t

Bonds

10.1%

30-Day

T-Bills

0.0%

Large

Stocks

16.0%

30-Day

T-Bills

4.9%

30-Day

T-Bills

4.7%

Large

Stocks

-9.1%

Large

Stocks

-11.9%

Small

Stocks

-13.3%

LT Gov’t

Bonds

1.5%

LT Gov’t

Bonds

8.5%

Large

Stocks

4.9%

30-Day

T-Bills

4.8%

30-Day

T-Bills

4.7%

Large

Stocks

-37.0%

30-Day

T-Bills

0.1%

Int’l

Stocks

8.2%

Small

Stocks

-3.3%

LT Gov’t

Bonds

3.3%

Small

Stocks

-7.3%

LT Gov’t

Bonds

-9.0%

Int’l

Stocks

-14.0%

Int’l

Stocks

-21.2%

Large

Stocks

-22.1%

30-Day

T-Bills

1.0%

30-Day

T-Bills

1.2%

30-Day

T-Bills

3.0%

LT Gov’t

Bonds

1.2%

Small

Stocks

-5.2%

Int’l

Stocks

-43.1%

LT Gov’t

Bonds

-14.9%

30-Day

T-Bills

0.1%

Int’l

Stocks

-11.7%

30-Day

T-Bills

0.1%

LO

WER R

ETU

RN

HIG

HER R

ETU

RN

Although diversification does not assure a profit or protect against loss, diversification may help spread out the risk in your portfolio. This chart shows how the returns in different asset classes have varied from one year to the next.

SFC/US/45665/6.13/V4/07SEC419-12

Volatility of Small Cap Stocks

Source: Morningstar. Past performance is no guarantee of future results. This chart is for illustrative purposes only and does not represent an actual investment or the performance of any specific investment. All investments involve risk including loss of principal. Small Company Stocks—Russell 2000 Index; Large Company Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general; Long-Term Government Bonds—20-year U.S. Government Bond; Treasury Bills—30-day U.S. Treasury Bill; International Stocks—Morgan Stanley Capital International Europe, Australasia, and Far East (EAFE) Index. Government bonds and Treasury bills are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than the other asset classes. As interest rates rise, bond prices fall. Bond funds do not carry the same guarantees as bonds themselves. Furthermore, small company stocks are more volatile than large company stocks and are subject to significant price fluctuations, business risks and are thinly traded. International investments involve special risks such as fluctuations in currency, foreign taxation, economic and political risks, liquidity risks and differences in accounting and financial standards. The data assumes reinvestment of all income and does not account for taxes or transaction costs which may lower results. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index. Diversification does not assure a profit or protect against loss.

See how returns vary from year to year?

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Large

Stocks

28.6%

Small

Stocks

29.8%

LT Gov’t

Bonds

21.5%

Small

Stocks

22.8%

LT Gov’t

Bonds

17.8%

Small

Stocks

60.7%

Int’l

Stocks

20.7%

Int’l

Stocks

14.0%

Int’l

Stocks

26.9%

Int’l

Stocks

11.6%

LT Gov’t

Bonds

25.9%

Int’l

Stocks

32.5%

Small

Stocks

31.3%

LT Gov’t

Bonds

28.2%

Small

Stocks

18.2%

Int’l

Stocks

20.3%

Int’l

Stocks

27.3%

30-Day

T-Bills

5.9%

30-Day

T-Bills

3.8%

30-Day

T-Bills

1.7%

Int’l

Stocks

39.2%

Small

Stocks

18.4%

LT Gov’t

Bonds

7.8%

Small

Stocks

16.2%

LT Gov’t

Bonds

9.9%

30-Day

T-Bills

1.7%

Small

Stocks

28.1%

Large

Stocks

15.1%

Large

Stocks

2.1%

Int’l

Stocks

17.9%

LT Gov’t

Bonds

13.1%

Large

Stocks

21.0%

Small

Stocks

-3.6%

LT Gov’t

Bonds

3.7%

Int’l

Stocks

-15.7%

Large

Stocks

28.7%

Large

Stocks

10.9%

Small

Stocks

5.7%

Large

Stocks

15.8%

Large

Stocks

5.5%

Small

Stocks

-36.7%

Large

Stocks

26.5%

LT Gov’t

Bonds

10.1%

30-Day

T-Bills

0.0%

Large

Stocks

16.0%

30-Day

T-Bills

4.9%

30-Day

T-Bills

4.7%

Large

Stocks

-9.1%

Large

Stocks

-11.9%

Small

Stocks

-13.3%

LT Gov’t

Bonds

1.5%

LT Gov’t

Bonds

8.5%

Large

Stocks

4.9%

30-Day

T-Bills

4.8%

30-Day

T-Bills

4.7%

Large

Stocks

-37.0%

30-Day

T-Bills

0.1%

Int’l

Stocks

8.2%

Small

Stocks

-3.3%

LT Gov’t

Bonds

3.3%

Small

Stocks

-7.3%

LT Gov’t

Bonds

-9.0%

Int’l

Stocks

-14.0%

Int’l

Stocks

-21.2%

Large

Stocks

-22.1%

30-Day

T-Bills

1.0%

30-Day

T-Bills

1.2%

30-Day

T-Bills

3.0%

LT Gov’t

Bonds

1.2%

Small

Stocks

-5.2%

Int’l

Stocks

-43.1%

LT Gov’t

Bonds

-14.9%

30-Day

T-Bills

0.1%

Int’l

Stocks

-11.7%

30-Day

T-Bills

0.1%

LO

WER R

ETU

RN

HIG

HER R

ETU

RN

SFC/US/45665/6.13/V4/07SEC419-12

Volatility of International Stocks

Source: Morningstar. Past performance is no guarantee of future results. This chart is for illustrative purposes only and does not represent an actual investment or the performance of any specific investment. All investments involve risk including loss of principal. Small Company Stocks—Russell 2000 Index; Large Company Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general; Long-Term Government Bonds—20-year U.S. Government Bond; Treasury Bills—30-day U.S. Treasury Bill; International Stocks—Morgan Stanley Capital International Europe, Australasia, and Far East (EAFE) Index. Government bonds and Treasury bills are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than the other asset classes. As interest rates rise, bond prices fall. Bond funds do not carry the same guarantees as bonds themselves. Furthermore, small company stocks are more volatile than large company stocks and are subject to significant price fluctuations, business risks and are thinly traded. International investments involve special risks such as fluctuations in currency, foreign taxation, economic and political risks, liquidity risks and differences in accounting and financial standards. The data assumes reinvestment of all income and does not account for taxes or transaction costs which may lower results. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index. Diversification does not assure a profit or protect against loss.

See how returns vary from year to year?

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Large

Stocks

28.6%

Small

Stocks

29.8%

LT Gov’t

Bonds

21.5%

Small

Stocks

22.8%

LT Gov’t

Bonds

17.8%

Small

Stocks

60.7%

Int’l

Stocks

20.7%

Int’l

Stocks

14.0%

Int’l

Stocks

26.9%

Int’l

Stocks

11.6%

LT Gov’t

Bonds

25.9%

Int’l

Stocks

32.5%

Small

Stocks

31.3%

LT Gov’t

Bonds

28.2%

Small

Stocks

18.2%

Int’l

Stocks

20.3%

Int’l

Stocks

27.3%

30-Day

T-Bills

5.9%

30-Day

T-Bills

3.8%

30-Day

T-Bills

1.7%

Int’l

Stocks

39.2%

Small

Stocks

18.4%

LT Gov’t

Bonds

7.8%

Small

Stocks

16.2%

LT Gov’t

Bonds

9.9%

30-Day

T-Bills

1.7%

Small

Stocks

28.1%

Large

Stocks

15.1%

Large

Stocks

2.1%

Int’l

Stocks

17.9%

LT Gov’t

Bonds

13.1%

Large

Stocks

21.0%

Small

Stocks

-3.6%

LT Gov’t

Bonds

3.7%

Int’l

Stocks

-15.7%

Large

Stocks

28.7%

Large

Stocks

10.9%

Small

Stocks

5.7%

Large

Stocks

15.8%

Large

Stocks

5.5%

Small

Stocks

-36.7%

Large

Stocks

26.5%

LT Gov’t

Bonds

10.1%

30-Day

T-Bills

0.0%

Large

Stocks

16.0%

30-Day

T-Bills

4.9%

30-Day

T-Bills

4.7%

Large

Stocks

-9.1%

Large

Stocks

-11.9%

Small

Stocks

-13.3%

LT Gov’t

Bonds

1.5%

LT Gov’t

Bonds

8.5%

Large

Stocks

4.9%

30-Day

T-Bills

4.8%

30-Day

T-Bills

4.7%

Large

Stocks

-37.0%

30-Day

T-Bills

0.1%

Int’l

Stocks

8.2%

Small

Stocks

-3.3%

LT Gov’t

Bonds

3.3%

Small

Stocks

-7.3%

LT Gov’t

Bonds

-9.0%

Int’l

Stocks

-14.0%

Int’l

Stocks

-21.2%

Large

Stocks

-22.1%

30-Day

T-Bills

1.0%

30-Day

T-Bills

1.2%

30-Day

T-Bills

3.0%

LT Gov’t

Bonds

1.2%

Small

Stocks

-5.2%

Int’l

Stocks

-43.1%

LT Gov’t

Bonds

-14.9%

30-Day

T-Bills

0.1%

Int’l

Stocks

-11.7%

30-Day

T-Bills

0.1%

LO

WER R

ETU

RN

HIG

HER R

ETU

RN

SFC/US/45665/6.13/V4/07SEC419-12

Volatility of Large Cap Stocks

Source: Morningstar. Past performance is no guarantee of future results. This chart is for illustrative purposes only and does not represent an actual investment or the performance of any specific investment. All investments involve risk including loss of principal. Small Company Stocks—Russell 2000 Index; Large Company Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general; Long-Term Government Bonds—20-year U.S. Government Bond; Treasury Bills—30-day U.S. Treasury Bill; International Stocks—Morgan Stanley Capital International Europe, Australasia, and Far East (EAFE) Index. Government bonds and Treasury bills are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than the other asset classes. As interest rates rise, bond prices fall. Bond funds do not carry the same guarantees as bonds themselves. Furthermore, small company stocks are more volatile than large company stocks and are subject to significant price fluctuations, business risks and are thinly traded. International investments involve special risks such as fluctuations in currency, foreign taxation, economic and political risks, liquidity risks and differences in accounting and financial standards. The data assumes reinvestment of all income and does not account for taxes or transaction costs which may lower results. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index. Diversification does not assure a profit or protect against loss.

See how returns vary from year to year?

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Large

Stocks

28.6%

Small

Stocks

29.8%

LT Gov’t

Bonds

21.5%

Small

Stocks

22.8%

LT Gov’t

Bonds

17.8%

Small

Stocks

60.7%

Int’l

Stocks

20.7%

Int’l

Stocks

14.0%

Int’l

Stocks

26.9%

Int’l

Stocks

11.6%

LT Gov’t

Bonds

25.9%

Int’l

Stocks

32.5%

Small

Stocks

31.3%

LT Gov’t

Bonds

28.2%

Small

Stocks

18.2%

Int’l

Stocks

20.3%

Int’l

Stocks

27.3%

30-Day

T-Bills

5.9%

30-Day

T-Bills

3.8%

30-Day

T-Bills

1.7%

Int’l

Stocks

39.2%

Small

Stocks

18.4%

LT Gov’t

Bonds

7.8%

Small

Stocks

16.2%

LT Gov’t

Bonds

9.9%

30-Day

T-Bills

1.7%

Small

Stocks

28.1%

Large

Stocks

15.1%

Large

Stocks

2.1%

Int’l

Stocks

17.9%

LT Gov’t

Bonds

13.1%

Large

Stocks

21.0%

Small

Stocks

-3.6%

LT Gov’t

Bonds

3.7%

Int’l

Stocks

-15.7%

Large

Stocks

28.7%

Large

Stocks

10.9%

Small

Stocks

5.7%

Large

Stocks

15.8%

Large

Stocks

5.5%

Small

Stocks

-36.7%

Large

Stocks

26.5%

LT Gov’t

Bonds

10.1%

30-Day

T-Bills

0.0%

Large

Stocks

16.0%

30-Day

T-Bills

4.9%

30-Day

T-Bills

4.7%

Large

Stocks

-9.1%

Large

Stocks

-11.9%

Small

Stocks

-13.3%

LT Gov’t

Bonds

1.5%

LT Gov’t

Bonds

8.5%

Large

Stocks

4.9%

30-Day

T-Bills

4.8%

30-Day

T-Bills

4.7%

Large

Stocks

-37.0%

30-Day

T-Bills

0.1%

Int’l

Stocks

8.2%

Small

Stocks

-3.3%

LT Gov’t

Bonds

3.3%

Small

Stocks

-7.3%

LT Gov’t

Bonds

-9.0%

Int’l

Stocks

-14.0%

Int’l

Stocks

-21.2%

Large

Stocks

-22.1%

30-Day

T-Bills

1.0%

30-Day

T-Bills

1.2%

30-Day

T-Bills

3.0%

LT Gov’t

Bonds

1.2%

Small

Stocks

-5.2%

Int’l

Stocks

-43.1%

LT Gov’t

Bonds

-14.9%

30-Day

T-Bills

0.1%

Int’l

Stocks

-11.7%

30-Day

T-Bills

0.1%

LO

WER R

ETU

RN

HIG

HER R

ETU

RN

SFC/US/45665/6.13/V4/07SEC419-12

Volatility of Long-Term Government Bonds

Source: Morningstar. Past performance is no guarantee of future results. This chart is for illustrative purposes only and does not represent an actual investment or the performance of any specific investment. All investments involve risk including loss of principal. Small Company Stocks—Russell 2000 Index; Large Company Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general; Long-Term Government Bonds—20-year U.S. Government Bond; Treasury Bills—30-day U.S. Treasury Bill; International Stocks—Morgan Stanley Capital International Europe, Australasia, and Far East (EAFE) Index. Government bonds and Treasury bills are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than the other asset classes. As interest rates rise, bond prices fall. Bond funds do not carry the same guarantees as bonds themselves. Furthermore, small company stocks are more volatile than large company stocks and are subject to significant price fluctuations, business risks and are thinly traded. International investments involve special risks such as fluctuations in currency, foreign taxation, economic and political risks, liquidity risks and differences in accounting and financial standards. The data assumes reinvestment of all income and does not account for taxes or transaction costs which may lower results. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index. Diversification does not assure a profit or protect against loss.

See how returns vary from year to year?

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Large

Stocks

28.6%

Small

Stocks

29.8%

LT Gov’t

Bonds

21.5%

Small

Stocks

22.8%

LT Gov’t

Bonds

17.8%

Small

Stocks

60.7%

Int’l

Stocks

20.7%

Int’l

Stocks

14.0%

Int’l

Stocks

26.9%

Int’l

Stocks

11.6%

LT Gov’t

Bonds

25.9%

Int’l

Stocks

32.5%

Small

Stocks

31.3%

LT Gov’t

Bonds

28.2%

Small

Stocks

18.2%

Int’l

Stocks

20.3%

Int’l

Stocks

27.3%

30-Day

T-Bills

5.9%

30-Day

T-Bills

3.8%

30-Day

T-Bills

1.7%

Int’l

Stocks

39.2%

Small

Stocks

18.4%

LT Gov’t

Bonds

7.8%

Small

Stocks

16.2%

LT Gov’t

Bonds

9.9%

30-Day

T-Bills

1.7%

Small

Stocks

28.1%

Large

Stocks

15.1%

Large

Stocks

2.1%

Int’l

Stocks

17.9%

LT Gov’t

Bonds

13.1%

Large

Stocks

21.0%

Small

Stocks

-3.6%

LT Gov’t

Bonds

3.7%

Int’l

Stocks

-15.7%

Large

Stocks

28.7%

Large

Stocks

10.9%

Small

Stocks

5.7%

Large

Stocks

15.8%

Large

Stocks

5.5%

Small

Stocks

-36.7%

Large

Stocks

26.5%

LT Gov’t

Bonds

10.1%

30-Day

T-Bills

0.0%

Large

Stocks

16.0%

30-Day

T-Bills

4.9%

30-Day

T-Bills

4.7%

Large

Stocks

-9.1%

Large

Stocks

-11.9%

Small

Stocks

-13.3%

LT Gov’t

Bonds

1.5%

LT Gov’t

Bonds

8.5%

Large

Stocks

4.9%

30-Day

T-Bills

4.8%

30-Day

T-Bills

4.7%

Large

Stocks

-37.0%

30-Day

T-Bills

0.1%

Int’l

Stocks

8.2%

Small

Stocks

-3.3%

LT Gov’t

Bonds

3.3%

Small

Stocks

-7.3%

LT Gov’t

Bonds

-9.0%

Int’l

Stocks

-14.0%

Int’l

Stocks

-21.2%

Large

Stocks

-22.1%

30-Day

T-Bills

1.0%

30-Day

T-Bills

1.2%

30-Day

T-Bills

3.0%

LT Gov’t

Bonds

1.2%

Small

Stocks

-5.2%

Int’l

Stocks

-43.1%

LT Gov’t

Bonds

-14.9%

30-Day

T-Bills

0.1%

Int’l

Stocks

-11.7%

30-Day

T-Bills

0.1%

LO

WER R

ETU

RN

HIG

HER R

ETU

RN

SFC/US/45665/6.13/V4/07SEC419-12

Volatility of 30-Day Treasury Bills

Source: Morningstar. Past performance is no guarantee of future results. This chart is for illustrative purposes only and does not represent an actual investment or the performance of any specific investment. All investments involve risk including loss of principal. Small Company Stocks—Russell 2000 Index; Large Company Stocks—Standard & Poor’s 500®, which is an unmanaged group of securities, is considered to be representative of the stock market in general; Long-Term Government Bonds—20-year U.S. Government Bond; Treasury Bills—30-day U.S. Treasury Bill; International Stocks—Morgan Stanley Capital International Europe, Australasia, and Far East (EAFE) Index. Government bonds and Treasury bills are guaranteed by the full faith and credit of the United States government as to the timely payment of principal and interest, while stocks are not guaranteed and have been more volatile than the other asset classes. As interest rates rise, bond prices fall. Bond funds do not carry the same guarantees as bonds themselves. Furthermore, small company stocks are more volatile than large company stocks and are subject to significant price fluctuations, business risks and are thinly traded. International investments involve special risks such as fluctuations in currency, foreign taxation, economic and political risks, liquidity risks and differences in accounting and financial standards. The data assumes reinvestment of all income and does not account for taxes or transaction costs which may lower results. Because these indices are not managed portfolios, there are no advisory fees or internal management expenses reflected in their performance and investors cannot invest directly in any index. Diversification does not assure a profit or protect against loss.

Do you understand the importance of diversification?

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Large

Stocks

28.6%

Small

Stocks

29.8%

LT Gov’t

Bonds

21.5%

Small

Stocks

22.8%

LT Gov’t

Bonds

17.8%

Small

Stocks

60.7%

Int’l

Stocks

20.7%

Int’l

Stocks

14.0%

Int’l

Stocks

26.9%

Int’l

Stocks

11.6%

LT Gov’t

Bonds

25.9%

Int’l

Stocks

32.5%

Small

Stocks

31.3%

LT Gov’t

Bonds

28.2%

Small

Stocks

18.2%

Int’l

Stocks

20.3%

Int’l

Stocks

27.3%

30-Day

T-Bills

5.9%

30-Day

T-Bills

3.8%

30-Day

T-Bills

1.7%

Int’l

Stocks

39.2%

Small

Stocks

18.4%

LT Gov’t

Bonds

7.8%

Small

Stocks

16.2%

LT Gov’t

Bonds

9.9%

30-Day

T-Bills

1.7%

Small

Stocks

28.1%

Large

Stocks

15.1%

Large

Stocks

2.1%

Int’l

Stocks

17.9%

LT Gov’t

Bonds

13.1%

Large

Stocks

21.0%

Small

Stocks

-3.6%

LT Gov’t

Bonds

3.7%

Int’l

Stocks

-15.7%

Large

Stocks

28.7%

Large

Stocks

10.9%

Small

Stocks

5.7%

Large

Stocks

15.8%

Large

Stocks

5.5%

Small

Stocks

-36.7%

Large

Stocks

26.5%

LT Gov’t

Bonds

10.1%

30-Day

T-Bills

0.0%

Large

Stocks

16.0%

30-Day

T-Bills

4.9%

30-Day

T-Bills

4.7%

Large

Stocks

-9.1%

Large

Stocks

-11.9%

Small

Stocks

-13.3%

LT Gov’t

Bonds

1.5%

LT Gov’t

Bonds

8.5%

Large

Stocks

4.9%

30-Day

T-Bills

4.8%

30-Day

T-Bills

4.7%

Large

Stocks

-37.0%

30-Day

T-Bills

0.1%

Int’l

Stocks

8.2%

Small

Stocks

-3.3%

LT Gov’t

Bonds

3.3%

Small

Stocks

-7.3%

LT Gov’t

Bonds

-9.0%

Int’l

Stocks

-14.0%

Int’l

Stocks

-21.2%

Large

Stocks

-22.1%

30-Day

T-Bills

1.0%

30-Day

T-Bills

1.2%

30-Day

T-Bills

3.0%

LT Gov’t

Bonds

1.2%

Small

Stocks

-5.2%

Int’l

Stocks

-43.1%

LT Gov’t

Bonds

-14.9%

30-Day

T-Bills

0.1%

Int’l

Stocks

-11.7%

30-Day

T-Bills

0.1%

LO

WER R

ETU

RN

HIG

HER R

ETU

RN

SFC/US/45665/6.13/V4/07SEC419-12

Take advantage of tax-deferred savings.

• Individual Retirement Account (IRA)

• Other Tax-Deferred Savings Accounts*

*Earnings from tax-deferred accounts may be subject to taxation upon withdrawal. This chart represents the growth of a hypothetical investment, assuming the stated annual nominal rate of return compounded monthly, over a specific time period. This example does not take inflation or applicable fees into account and should not be considered to be representative of the performance of any specific investment product or investment strategy.

For purposes of comparison, the taxable account is calculated using a 25% income tax bracket. Your actual annual rate of return could be more or less. Also, withdrawals before age 59 1/2 may be subject to a 10% penalty. Investors should consider their personal investment horizon and income tax bracket, both current and anticipated, when making investment decisions. Lower maximum tax rates on capital gains and dividends would make the return on the taxable investment more favorable.

Taxable $739,900

Invest $10,000 per year for 30 years at a 9% rate of return

Tax-deferred $1,537,100

SFC/US/45665/6.13/V4/07SEC419-12

Don’t pay the high cost of waiting.

• Age 27: Invest $100/month at 9% return

• By age 67, that investment is worth almost $471,640

• But start investing one year later and same investment only grows to $430,040

• You would miss out on nearly $42,000!

Hypothetical 9% rate of return not intended to represent any actual investment. Unlike actual investments, the accounts show a constant rate of return without any fees or charges. Tax-deferred growth and tax-deductible contributions are taxed upon withdrawal. Withdrawals prior to age 59 1/2 may be subject to a 10% penalty tax. Assumes payments are made at the beginning of compounding period with 9% rate of return compounded monthly.

Actual returns would differ and be significantly impacted by periods of negative returns, failure to make monthly contributions and any withdrawals.

Amount

of savings

High cost

of waiting

Start saving at: Age 27 Age 28 Age 32 Age 42

$471,640 $430,040 $112,950 $296,380

$41,600 $175,260 $358,690 The longer you wait to start saving for the future, the less time your money has to grow.

Even delaying your investing program a year or two can make a big difference in how much you end up with.

That’s because you pay “the high cost of waiting.”

The sooner you begin to save, the greater the growth potential of your investment

SFC/US/45665/6.13/V4/07SEC419-12

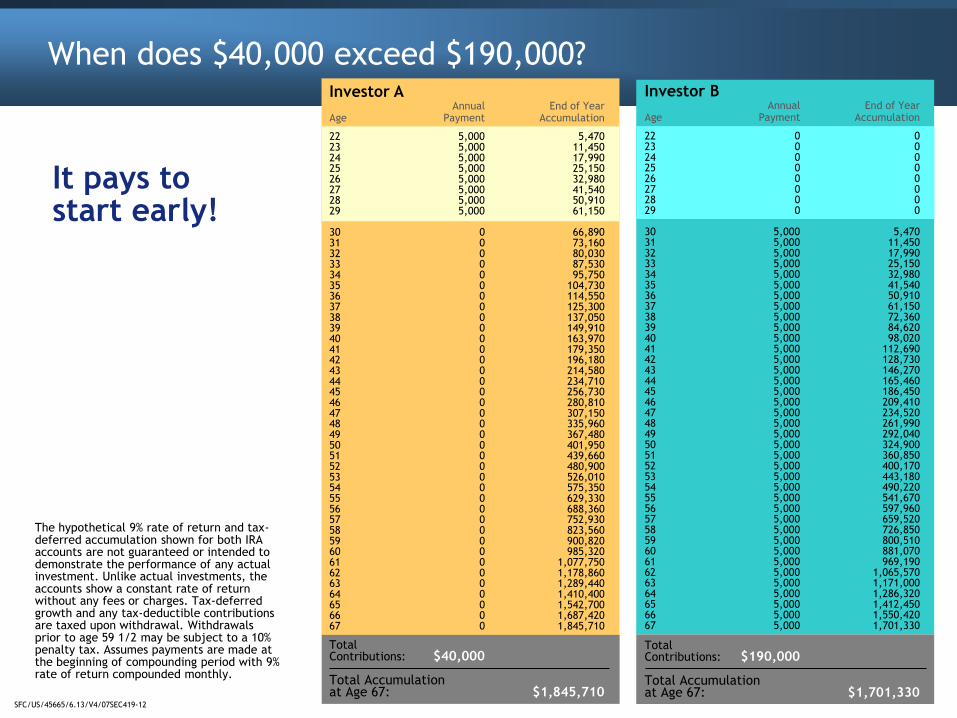

When does $40,000 exceed $190,000?

The hypothetical 9% rate of return and tax-deferred accumulation shown for both IRA accounts are not guaranteed or intended to demonstrate the performance of any actual investment. Unlike actual investments, the accounts show a constant rate of return without any fees or charges. Tax-deferred growth and any tax-deductible contributions are taxed upon withdrawal. Withdrawals prior to age 59 1/2 may be subject to a 10% penalty tax. Assumes payments are made at the beginning of compounding period with 9% rate of return compounded monthly.

It pays to start early!

Investor A Annual End of Year Age Payment Accumulation

22 5,000 5,470 23 5,000 11,450 24 5,000 17,990 25 5,000 25,150 26 5,000 32,980 27 5,000 41,540 28 5,000 50,910 29 5,000 61,150

30 0 66,890 31 0 73,160 32 0 80,030 33 0 87,530 34 0 95,750 35 0 104,730 36 0 114,550 37 0 125,300 38 0 137,050 39 0 149,910 40 0 163,970 41 0 179,350 42 0 196,180 43 0 214,580 44 0 234,710 45 0 256,730 46 0 280,810 47 0 307,150 48 0 335,960 49 0 367,480 50 0 401,950 51 0 439,660 52 0 480,900 53 0 526,010 54 0 575,350 55 0 629,330 56 0 688,360 57 0 752,930 58 0 823,560 59 0 900,820 60 0 985,320 61 0 1,077,750 62 0 1,178,860 63 0 1,289,440 64 0 1,410,400 65 0 1,542,700 66 0 1,687,420 67 0 1,845,710

Investor B Annual End of Year Age Payment Accumulation

22 0 0 23 0 0 24 0 0 25 0 0 26 0 0 27 0 0 28 0 0 29 0 0 30 5,000 5,470 31 5,000 11,450 32 5,000 17,990 33 5,000 25,150 34 5,000 32,980 35 5,000 41,540 36 5,000 50,910 37 5,000 61,150 38 5,000 72,360 39 5,000 84,620 40 5,000 98,020 41 5,000 112,690 42 5,000 128,730 43 5,000 146,270 44 5,000 165,460 45 5,000 186,450 46 5,000 209,410 47 5,000 234,520 48 5,000 261,990 49 5,000 292,040 50 5,000 324,900 51 5,000 360,850 52 5,000 400,170 53 5,000 443,180 54 5,000 490,220 55 5,000 541,670 56 5,000 597,960 57 5,000 659,520 58 5,000 726,850 59 5,000 800,510 60 5,000 881,070 61 5,000 969,190 62 5,000 1,065,570 63 5,000 1,171,000 64 5,000 1,286,320 65 5,000 1,412,450 66 5,000 1,550,420 67 5,000 1,701,330

Total Contributions: $40,000

Total Accumulation at Age 67: $1,845,710

Total Contributions: $190,000 Total Accumulation at Age 67: $1,701,330

SFC/US/45665/6.13/V4/07SEC419-12

Which type of investor are you?

Should you be Aggressive or Conservative?

Investments with the potential for greater returns also carry higher risks, including loss of principal and investment gains.

AGGRESSIVE Aggressive Equity Funds

Emerging Growth Funds

CONSERVATIVE Income Funds

Bond Funds

Municipal Bond Funds, Government Funds

MODERATE Large-Cap Equity Funds

Balanced Funds

Mid-Cap Funds, International Funds

SFC/US/45665/6.13/V4/07SEC419-12

Model Portfolios

Helps you create an investment program tailored to your investing style and goals.

Five basic models to meet the needs of most investors.

PFSI’s Intelligent Approach to Investing

Investment Profile Questionnaire helps determine your investing style.

1. Income

2. Conservative Growth

3. Moderate Growth

4. Growth

5. Aggressive Growth

SFC/US/45665/6.13/V4/07SEC419-12

Use asset allocation to reach your goals

• Portfolios composed of preset lists of funds researched by industry experts –Ibbotson Associates, a Morningstar Company.

• Relieves the burden of research into fund selection/allocation.

• Goal: Create a list of funds with better returns than average, while exposing the investment to roughly same or less risk.

SFC/US/45665/6.13/V4/07SEC419-12

Why Choose PFS Investments Inc.?

• Access to some of the most recognized and reputable portfolio managers in the industry

• Asset allocation guidance based on industry leading expertise from Ibbotson Associates

• Custom-built model portfolios to meet your investment objectives and risk tolerances

SFC/US/45665/6.13/V4/07SEC419-12

SFC/US/45665/6.13/V4/07SEC419-12