pp16832/01/2012 (029059) malaysia...

TRANSCRIPT

Kim Eng Hong Kong is a subsidiary of Malayan Banking Berhad

SEE APPENDIX I FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS

Malaysia

17 October 2011

PP16832/01/2012 (029059)

Sector Update 10 January 2012

PP16832/01/2012 (029059)

Page 1 of 2

Telecommunications Defensive but valuations a bugbear

Downgrade to Neutral. Economic growth is expected to slow but

telcos will continue to focus on expanding new earnings channels such

as mobile Internet and fixed broadband, as well as maintain cost control

through collaboration on physical infrastructure. Malaysia has a stable

competitive telco environment and well-established monetisation

strategies for mobile data. However, with valuations at a premium, we

downgrade the sector to Neutral, with Telekom being our top pick.

Margin pressure expected as handset subsidies expected to rise.

At the same time that dongle subscriber growth is slowing down, users

on smartphone mobile data plans are not growing as fast, most likely

due to the fact that smartphone penetration is still low. In order to attract

more users to purchase smartphones and take up data plans, telcos will

need to provide more handset subsidies in 2012. This will depress

margins until the subsidies are fully expensed off and the higher ARPUs

begin to filter through to telco margins.

Risks in spectrum refarming, more multiplay competition. There is

still no clarity on when and how MCMC will be refarming the current

spectra of the existing telcos when they expire in 2012 to 2015. The key

concern is whether spectrum bidding (if an auction is the chosen

method) will push prices too high. We also expect more competition in

the IPTV space, as telcos aim to improve their non-voice revenue and

do more bundling deals that can help improve customer stickiness.

Still, dividends should stay the course as capex trends down. For

the basket of telco stocks under our coverage, we project core earnings

growth of 6.0% in 2012, with average free cashflow yield of 7.1%

backing up average dividend yield of 4.5%, with the highest yields

coming from Maxis followed by Digi and Telekom. Capex is expected to

trend down following the earlier surge in 3G network investment and we

expect greater potential for cost savings from network collaboration to

flow through in 2012 for Telekom Malaysia, Axiata and Digi.Com.

Valuations not compelling relative to the region. Malaysian wireless

telco stocks lead the region in terms of valuations, trading at an

average PBR of 9.9x and PER of 18.2x based on FY12 forecasts,

compared to 3.2x and 12.1x respectively for the rest of the Asia Pacific

ex-Japan region. In balancing slowing economic growth ahead and a

potential margin squeeze by handset subsidies against stable forecasts

for earnings and cashflow, we are Neutral on the sector. Our sole Buy

call is on Telekom Malaysia.

Telco Sector – Peer Valuation Summary Source: Maybank IB

Stock Rec Shr px Mkt cap TP PER (x) PER (x) P/B (x) P/B (x) ROAE (%) ROAE (%) Div yld Div yld (RM) (RMm) (RM) CY11E CY12E CY11E CY12E CY11E CY12E FY11E FY12E Axiata Hold 5.00 40,881 5.10 15.6 14.0 2.0 1.8 13.4 13.5 2.1 2.1 DiGi.com Hold 3.70 27,524 3.46 24.9 23.6 23.2 25.3 87.4 102.7 4.6 4.6 Maxis Hold 5.48 40,650 5.40 18.6 19.0 5.2 5.8 26.5 28.8 7.4 7.4 Telekom Buy 4.73 15,597 4.84 23.8 21.2 2.0 2.0 8.5 9.6 4.5 4.5 Simple average 20.7 19.5 8.1 8.7 34.0 38.6 4.6 4.6

Neutral (from Overweight)

Wong Chew Hann [email protected] (603) 2297 8686

Gregory Yap [email protected] (65) 6432 1450

10 January 2012 Page 2 of 12

Telecommunications 17 October 2011

Page 1 of 2

Stable earnings growth, decent yields

Malaysia has one of the most defensive telco markets in the region with

a stable competitive environment and well-established monetisation

strategies for mobile data packages practised by the telcos. Risks exist,

true, especially in the areas of new competitors on the block and

uncertainties surrounding spectrum allocation, but generally, they are

well known and can be anticipated by the telcos.

For telco stocks under coverage, we project core earnings growth of

6.0% in 2012, with average free cashflow yield of 7.1% backing up

average dividend yield of 4.5%, with the highest yields coming from

Maxis followed by DiGi and Telekom. With capex trending down after

an earlier surge in 3G network investment, capital management should

remain a recurring theme. Although economic growth is expected to

slow, we believe telcos will continue to focus on expanding new

earnings channels such as mobile Internet and fixed broadband.

However, high valuations are a bugbear as the defensiveness of the

industry is well-recognised. We recently downgraded DiGi.com

following a period of outperformance just prior to its 1-into-10 stock

split. Currently, the only buy call we have is in Telekom Malaysia. As

such, we have a neutral stance on the telco sector.

2012 earnings likely to remain defensive…

Defend the traditional, grow the new. In 2012, we expect telcos to

place emphasis on defending their traditional revenue sources and to

keep new sources of revenue such as data revving in third gear. On the

voice side, while Digi and Celcom have been able to sustain their voice

revenue, Maxis has seen voice revenue decline in the last two years. Its

latest response of increasing the charging block of its Hot Ticket

prepaid plan from 30 seconds to 60 seconds should help to stem the

steady erosion, at least for now. To mitigate the erosion in voice, we

expect all three mobile telcos to continue pushing for more mobile data

usage on their networks, coming out with more innovative pricing plans

and improving their brand image as well as make more innovative

applications available to increase subscriber stickiness.

Increasing shift from 2G to 3G to drive mobile data. Although

smartphone penetration in Malaysia is still low, estimated at only 20-

25% of the postpaid base compared to 70-75% for Singapore, we

believe this figure can only rise as people continue to switch from 2G to

3G driven by new applications such as social networking (eg

Facebook), video streaming (eg Youtube) and online chats. This

change in user behaviour is revolutionary, in our view, and will be

almost unstoppable.

In the latest “Global Mobile Data Traffic Forecast” white paper, global

networking equipment giant Cisco Systems noted that world mobile

data grew by almost 3x in 2010 from 2009, and expects it to increase

by another 26x by 2015. Further, it noted that smartphones represented

only 13% of total global handsets in use today, but they represented

over 78% of total mobile data traffic as the average amount of traffic per

smartphone doubled in 2010 to 79MB per month from 35MB per month.

Most notably for users in Singapore and Malaysia, Android phone users

are approaching iPhone levels of data use.

10 January 2012 Page 3 of 12

Telecommunications 17 October 2011

Page 1 of 2

According to Cisco, "it is a testament to the momentum of the mobile

industry that this growth persisted despite the continued economic

downturn, the introduction of tiered mobile data packages, and an

increase in the amount of mobile traffic offloaded to the fixed network”.

Cisco forecasts 2015 mobile data traffic to grow 26x over 2010

Source: Cisco VNI Mobile, 2011

Western Europe and Asia Pacific will account for over half of global mobile traffic by 2015

Source: Cisco VNI Mobile, 2011

New devices and applications carry higher multiplier effect. Having

said that, the growth of mobile broadband subscribers has been slowing

rapidly in Malaysia since it peaked in mid-2010. In our view, the

introduction of more tablet computers and high-end mobile handsets

onto mobile networks will be a major generator of mobile traffic to revive

this growth, because they will offer the consumer content and

applications not supported by previous generations of mobile devices.

As shown below, one smart phone can generate as much traffic as 24

feature phones and one tablet as much as 122 feature phones.

10 January 2012 Page 4 of 12

Telecommunications 17 October 2011

Page 1 of 2

High-end mobile devices can multiply traffic

Source: Cisco VNI Mobile, 2011

In this context, it is encouraging to see Android devices come into their

own against the iPhone, as generally these phones are more

affordable. Market research firm Gartner recently reported that

Android’s share of the worldwide smartphone market doubled to 52.3%

in 3Q11 from a year ago, while Apple’s iOS dropped to 15%.

Mobile operating system market shares

Operating

system

3Q11 Units

(‘000)

3Q11 Share

(%)

3Q10 Units

(‘000)

3Q10 Share

(%) Android 60,490.4 52.5 20,544.0 25.3

Symbian 19,500.1 16.9 29,480.1 36.3

iOS 17,295.3 15.0 13,484.4 16.6

RIM 12,701.1 11.0 12,508.3 15.4

Bada 2,478.5 2.2 920.6 1.1

Microsoft 1,701.9 1.5 2,203.9 2.7

Others 1,018.1 0.9 1,991.3 2.5

Total 115,185.4 100.0 81,132.6 100.0

Source: Gartner

Telcos will continue to upgrade regardless of economic

conditions. As the Malaysian telcos have invested heavily in HSDPA

(High Speed Downlink Packet Access, or 3.5G, capable of a maximum

downlink access speed of 14Mbps) networks, they will continue to push

for more mobile data usage on their networks. Operators are likely to

offer mobile broadband packages that are comparable in price and

speed to those of fixed broadband, thereby encouraging mobile

broadband substitution.

At the same time, Malaysian telcos are making steady progress toward

upgrading their 3G networks to support HSPA+ (Evolved High Speed

Packet Access, with a faster downlink speed of 42Mbps) and LTE. At

this point, DiGi and Celcom have awarded upgrade contracts to

vendors such as ZTE, Huawei and Ericsson, with completion planned

within the next two years. Maxis claims 95% of its network is HSPA

ready, while U Mobile, StarHub’s sister company, already has coverage

in the Klang Valley, JB, Butterworth and parts of Penang.

None of the Malaysian telcos has revealed any plans yet for

investments in LTE, given that the spectrum issue is still up in the air.

As it is almost already the year’s end and the licences are supposed to

start in Jan 2013, we would expect more to be announced on the LTE

front only in 2012.

10 January 2012 Page 5 of 12

Telecommunications 17 October 2011

Page 1 of 2

We are assuming the Malaysian regulator has yet to decide on the

proposed allocation of the 2.6GHz LTE/4G spectrum although it was

thought to have allocated 20MHz each to nine separate contenders. So

far, it has been reported that Maxis and Celcom have trialed LTE on the

900Mhz spectrum band but we understand that trials are not strictly

necessary as all the telcos are interested and ready for LTE. Given the

network collaboration between Celcom and DiGi, it would be

reasonable to assume that both may also collaborate on LTE.

HSPA+ and LTE upgrade path

Maxis In late 2009, Maxis first announced an upgrade of its 3G/HSDPA

network to HSPA+ with downlink speeds up to 21Mbps for two

areas in JB and KL on a trial basis. There has been no update

since then although Malaysian Wireless believes coverage areas

should have improved through 2010/2011 and downlink speeds

may have risen to 42Mbps.

Digi.Com In Apr 2011, Digi awarded a network contract to ZTE Corp to

build a unified network that will give the telco a combined

2G/3G/4G network, starting from 3Q11. The network will be

capable of delivering download speeds of up to 42Mbps using

HSPA+ and thereafter up to 4 times faster when the LTE

spectrum becomes available. The upgrade will involve over

5,000 existing sites over the next two years, with new sites to be

added for better capacity and coverage.

Celcom Axiata In Mar 2011, Celcom appointed Huawei and Ericsson to upgrade

its HSPA network to HSPA+ with a download speed of up to

42Mbps and build a new LTE network. This RM700m deal is

expected to be complete within 3 years.

U Mobile U Mobile first announced its upgrade to HSPA+ in Sep 2010 with

the first deployment in Berjaya Time Square where its

headquarters are. It has selected Ericsson as the technology

partner and the new deployment will allow download speeds up

to 42Mbps. Current coverage is available in Klang Valley, Johor

Bahru, Butterworth and parts of Penang.

Source: Companies, various websites

But margins could come under pressure

Data subscriber growth rates slowing down. Despite kicking off

optimistically two years ago, mobile data adoption has slowed

considerably in the last few quarters. The following charts show how,

for the most part, wireless broadband subscribers accessing the

Internet on their laptops with USB modems have flattened out in the last

four quarters.

10 January 2012 Page 6 of 12

Telecommunications 17 October 2011

Page 1 of 2

Wireless broadband subscriber base

-

100

200

300

400

500

600

700

800

900

1,000

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

'000

Celcom Maxis Digi

Source: Companies, postpaid dongles only

Dongle net adds slowing down (% YoY chg)

-200

-100

0

100

200

300

400

500

600

700

800

900

2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11

(% YoY chg)

Celcom Maxis Digi

Source: Companies

Handset subsidies need to rise to drive smartphone penetration.

At the same time that dongle subscriber growth is slowing down, users

on smartphone mobile data plans are not growing as fast as earlier

thought. We think this is most likely due to the fact that smartphone

penetration in Malaysia is still low, estimated at only 20-25% of the

postpaid base compared to Singapore, currently at 70-75%. In order to

attract more users to purchase smartphones and take up the data

plans, we think the Malaysian telcos will need to provide more handset

subsidies in 2012. We reckon this will have the effect of depressing

margins in the initial phase until the subsidies are fully expensed off and

the higher ARPUs begin to filter through to telco margins.

Telcos moving to save costs through network sharing. With the

voice part of their revenue base under threat, telcos in Malaysia have

been aggressive in making structural changes to their cost base. Given

that network-related costs can account for north of 20% of running

costs and 60% of capital expenditure, telcos have been increasingly

using the network sharing approach to reduce operating costs as well

as cope with the need to keep investments in data capacity from

outrunning rapidly rising data demand. The network sharing will remove

the duplication and optimise the deployment of base stations, avoid

redeployment of equipment between redundant and new sites, reduce

utility bills and transmission costs as well as mitigate rising rental fees.

10 January 2012 Page 7 of 12

Telecommunications 17 October 2011

Page 1 of 2

There are 2 kinds of network sharing – sharing of the active

infrastructure or passive infrastructure. Passive infrastructure refers

mainly to the sharing of physical sites, buildings, shelters,

towers/masts, power supply and battery backup, etc, while active

infrastructure refers to active equipment e.g. antenna systems, cables,

filters, allocated frequency spectrum and backhaul transmission.

In Malaysia, both active and passive network sharing is used.

Celcom and DiGi are at the forefront of network sharing, having

signed a comprehensive agreement in Jan 2011. The scope of the

tie-up will initially focus on the sharing of telecommunication sites,

access transmission (microwave links), aggregation transmission

and trunk fibre transmission. Celcom has also been active in

hosting MVNOs such as Tune Talk, Merchantrade, XOX and

Redtone to eke out extra revenue from excess capacity. Both

Celcom and DiGi expect to save above RM100m-150m respectively

in 2012.

Most recently, Maxis and U Mobile announced in Oct 2011 that

Maxis will be opening up its 3G radio access network to U Mobile

for a period of 10 years. The agreement covers existing 3G

spectrum in non-urban centres such as Klang Valley, Penang, JB

and Ipoh where U Mobile already has active coverage, and may

include LTE subject to spectrum availability.

Fixed line growth prospects are roaring

Growth being driven by pent-up demand. Fixed broadband in

Malaysia, both in terms of connection speed and penetration, has long

lagged behind other countries in the region, as TM’s ADSL broadband

service Streamyx (with a maximum speed of only 4Mbps compared to

Singapore’s 100Mbps) was the only game in town until the arrival of

Unifi in 2010. With connection speeds of up to 20Mbps, Unifi subscriber

growth has accelerated every quarter since the high speed broadband

(HSBB) service was launched in 3Q10.

Fixed broadband user base

Source: Company

10 January 2012 Page 8 of 12

Telecommunications 17 October 2011

Page 1 of 2

We believe growth will continue to be driven by TM’s bundling of fixed

voice and broadband into this service, general pent-up demand for

faster broadband by both home and mobile users and the soaring

number of premises passed, which hit 1.029m premises in mid-Nov

2011 and is targeted to hit 1.3m in 2012. The fact that TM’s achieved

ARPU of RM184 is significantly higher than Streamyx’s maximum

monthly commitment fee of RM140 a month does not appear to have

dented demand, suggesting a high level of pent-up demand.

Further adding to TM’s prospects from soaring take-ups is the fact that

Celcom, Maxis and most recently, P1, a WiMax broadband operator,

have signed up to buy wholesale capacity on TM’s HSBB network,

although margins may be somewhat impacted.

Risks – spectrum, competition

Spectrum refarming still the biggest looming issue. Although 2011

is coming to an end, there is still no clarity on when and how the

regulator will be refarming the current spectra of the existing telcos as

and when they expire in 2012 to 2015. Refarmed spectra refer to

existing 800Mhz-900Mhz and 1800Mhz spectra that, upon expiry, will

be allocated back to the industry. Winning bidders will be able to utilise

the spectrum after they expire and control is relinquished by the

incumbents.

The key issue is whether spectrum bidding (if an auction is the chosen

method) will push prices too high, as there is always a fine balance

between governmental desire to maximise revenue from a scarce

resource and causing financial detriment to the industry. Depending on

the price, DiGi.com could turn out to be the biggest winner as it has the

scarcest spectra at the most flexible 800Mhz-900Mhz range.

Multi-play competition should intensify. We also expect more multi-

play competition as more players are entering the IPTV space, with an

aim to improve their non-voice revenue and do more bundling deals

that can help improve customer stickiness. Currently, there are two

IPTV services available – Hypp.TV by Telekom and DETV by MVNO

RedTone. Maxis has also teamed up with Australia-based Fetch TV to

launch IPTV by next year, while sister company Astro is reported to be

trialling an IPTV service in JV with Time Dot Com although coverage is

still quite small and limited to selected Klang Valley areas with

reportedly less than 200k premises passed.

10 January 2012 Page 9 of 12

Telecommunications 17 October 2011

Page 1 of 2

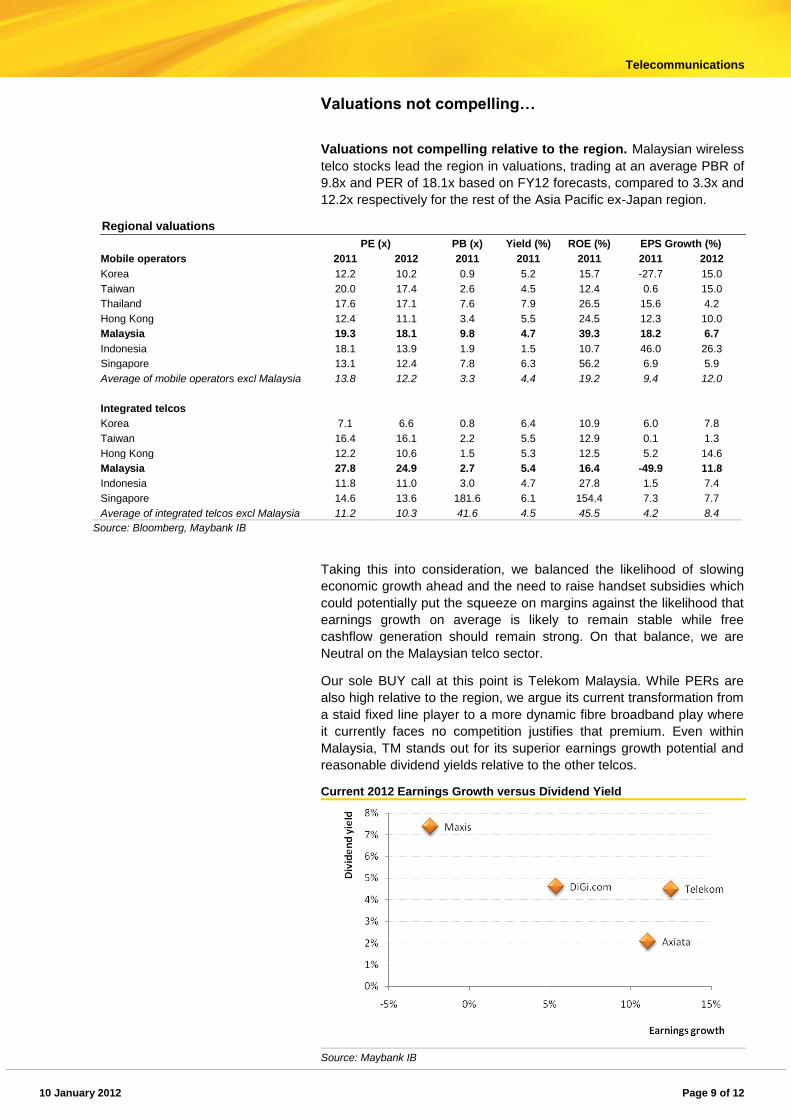

Valuations not compelling…

Valuations not compelling relative to the region. Malaysian wireless

telco stocks lead the region in valuations, trading at an average PBR of

9.8x and PER of 18.1x based on FY12 forecasts, compared to 3.3x and

12.2x respectively for the rest of the Asia Pacific ex-Japan region.

Regional valuations

PE (x) PB (x) Yield (%) ROE (%) EPS Growth (%)

Mobile operators 2011 2012 2011 2011 2011 2011 2012

Korea 12.2 10.2 0.9 5.2 15.7 -27.7 15.0

Taiwan 20.0 17.4 2.6 4.5 12.4 0.6 15.0

Thailand 17.6 17.1 7.6 7.9 26.5 15.6 4.2

Hong Kong 12.4 11.1 3.4 5.5 24.5 12.3 10.0

Malaysia 19.3 18.1 9.8 4.7 39.3 18.2 6.7

Indonesia 18.1 13.9 1.9 1.5 10.7 46.0 26.3

Singapore 13.1 12.4 7.8 6.3 56.2 6.9 5.9

Average of mobile operators excl Malaysia 13.8 12.2 3.3 4.4 19.2 9.4 12.0

Integrated telcos Korea 7.1 6.6 0.8 6.4 10.9 6.0 7.8

Taiwan 16.4 16.1 2.2 5.5 12.9 0.1 1.3

Hong Kong 12.2 10.6 1.5 5.3 12.5 5.2 14.6

Malaysia 27.8 24.9 2.7 5.4 16.4 -49.9 11.8

Indonesia 11.8 11.0 3.0 4.7 27.8 1.5 7.4

Singapore 14.6 13.6 181.6 6.1 154.4 7.3 7.7

Average of integrated telcos excl Malaysia 11.2 10.3 41.6 4.5 45.5 4.2 8.4

Source: Bloomberg, Maybank IB

Taking this into consideration, we balanced the likelihood of slowing

economic growth ahead and the need to raise handset subsidies which

could potentially put the squeeze on margins against the likelihood that

earnings growth on average is likely to remain stable while free

cashflow generation should remain strong. On that balance, we are

Neutral on the Malaysian telco sector.

Our sole BUY call at this point is Telekom Malaysia. While PERs are

also high relative to the region, we argue its current transformation from

a staid fixed line player to a more dynamic fibre broadband play where

it currently faces no competition justifies that premium. Even within

Malaysia, TM stands out for its superior earnings growth potential and

reasonable dividend yields relative to the other telcos.

Current 2012 Earnings Growth versus Dividend Yield

Source: Maybank IB

10 January 2012 Page 10 of 12

Telecommunications 17 October 2011

Page 1 of 2

Current 2012 Earnings Growth versus PER

Source: Maybank IB

10 January 2012 Page 11 of 12

Telecommunications 17 October 2011

Page 1 of 2

APPENDIX 1

Definition of Ratings

Maybank Investment Bank Research uses the following rating system:

BUY Total return is expected to be above 10% in the next 12 months

HOLD Total return is expected to be between -5% to 10% in the next 12 months

SELL Total return is expected to be below -5% in the next 12 months

Applicability of Ratings

The respective analyst maintains a coverage universe of stocks, the list of which may be adjusted according to needs. Investment ratings are

only applicable to the stocks which form part of the coverage universe. Reports on companies which are not part of the coverage do not

carry investment ratings as we do not actively follow developments in these companies.

Some common terms abbreviated in this report (where they appear):

Adex = Advertising Expenditure FCF = Free Cashflow PE = Price Earnings

BV = Book Value FV = Fair Value PEG = PE Ratio To Growth

CAGR = Compounded Annual Growth Rate FY = Financial Year PER = PE Ratio

Capex = Capital Expenditure FYE = Financial Year End QoQ = Quarter-On-Quarter

CY = Calendar Year MoM = Month-On-Month ROA = Return On Asset

DCF = Discounted Cashflow NAV = Net Asset Value ROE = Return On Equity DPS = Dividend Per Share

NTA = Net Tangible Asset ROSF = Return On Shareholders’ Funds

EBIT = Earnings Before Interest And Tax P = Price WACC = Weighted Average Cost Of Capital

EBITDA = EBIT, Depreciation And Amortisation P.A. = Per Annum YoY = Year-On-Year

EPS = Earnings Per Share PAT = Profit After Tax YTD = Year-To-Date

EV = Enterprise Value PBT = Profit Before Tax

Disclaimer

This report is for information purposes only and under no circumstances is it to be considered or intended as an offer to sell or a solicitation

of an offer to buy the securities referred to herein. Investors should note that income from such securities, if any, may fluctuate and that each

security’s price or value may rise or fall. Opinions or recommendations contained herein are in form of technical ratings and fundamental

ratings. Technical ratings may differ from fundamental ratings as technical valuations apply different methodologies and are purely based on

price and volume-related information extracted from Bursa Malaysia Securities Berhad in the equity analysis.Accordingly, investors may

receive back less than originally invested. Past performance is not necessarily a guide to future performance. This report is not intended to

provide personal investment advice and does not take into account the specific investment objectives, the financial situation and the

particular needs of persons who may receive or read this report. Investors should therefore seek financial, legal and other advice regarding

the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report.

The information contained herein has been obtained from sources believed to be reliable but such sources have not been independently

verified by Maybank Investment Bank Berhad and consequently no representation is made as to the accuracy or completeness of this report

by Maybank Investment Bank Berhad and it should not be relied upon as such. Accordingly, no liability can be accepted for any direct,

indirect or consequential losses or damages that may arise from the use or reliance of this report. Maybank Investment Bank Berhad, its

affiliates and related companies and their officers, directors, associates, connected parties and/or employees may from time to time have

positions or be materially interested in the securities referred to herein and may further act as market maker or may have assumed an

underwriting commitment or deal with such securities and may also perform or seek to perform investment banking services, advisory and

other services for or relating to those companies. Any information, opinions or recommendations contained herein are subject to change at

any time, without prior notice.

This report may contain forward looking statements which are often but not always identified by the use of words such as “anticipate”,

“believe”, “estimate”, “intend”, “plan”, “expect”, “forecast”, “predict” and “project” and statements that an event or result “may”, “will”, “can”,

“should”, “could” or “might” occur or be achieved and other similar expressions. Such forward looking statements are based on assumptions

made and information currently available to us and are subject to certain risks and uncertainties that could cause the actual results to differ

materially from those expressed in any forward looking statements. Readers are cautioned not to place undue relevance on these forward-

looking statements. Maybank Investment Bank Berhad expressly disclaims any obligation to update or revise any such forward looking

statements to reflect new information, events or circumstances after the date of this publication or to reflect the occurrence of unanticipated

events.

This report is prepared for the use of Maybank Investment Bank Berhad's clients and may not be reproduced, altered in any way, transmitted

to, copied or distributed to any other party in whole or in part in any form or manner without the prior express written consent of Maybank

Investment Bank Berhad and Maybank Investment Bank Berhad accepts no liability whatsoever for the actions of third parties in this respect.

This report is not directed to or intended for distribution to or use by any person or entity who is a citizen or resident of or located in any

locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

10 January 2012 Page 12 of 12

Telecommunications 17 October 2011

Page 1 of 2

APPENDIX 1

Additional Disclaimer (for purpose of distribution in Singapore)

This report has been produced as of the date hereof and the information herein maybe subject to change. Kim Eng Research Pte Ltd

("KERPL") in Singapore has no obligation to update such information for any recipient. Recipients of this report are to contact KERPL in

Singapore in respect of any matters arising from, or in connection with, this report. If the recipient of this report is not an accredited investor,

expert investor or institutional investor (as defined under Section 4A of the Singapore Securities and Futures Act), KERPL shall be legally

liable for the contents of this report, with such liability being limited to the extent (if any) as permitted by law.

As of 10 January 2012, KERPL does not have an interest in the said company/companies.

Additional Disclaimer (for purpose of distribution in the United States)

This research report prepared by Maybank Investment Bank Berhad is distributed in the United States (“US”) to Major US Institutional

Investors (as defined in Rule 15a-6 under the Securities Exchange Act of 1934, as amended) only by Kim Eng Securities USA, a broker-

dealer registered in the US (registered under Section 15 of the Securities Exchange Act of 1934, as amended).

All responsibility for the distribution of this report by Kim Eng Securities USA in the US shall be borne by Kim Eng. All resulting transactions

by a US person or entity should be effected through a registered broker-dealer in the US.

This report is for distribution only under such circumstances as may be permitted by applicable law. The securities described herein may not

be eligible for sale in all jurisdictions or to certain categories of investors. This report is not directed at you if Kim Eng Securities is prohibited

or restricted by any legislation or regulation in any jurisdiction from making it available to you. You should satisfy yourself before reading it

that Kim Eng Securities is permitted to provide research material concerning investments to you under relevant legislation and regulations.

Without prejudice to the foregoing, the reader is to note that additional disclaimers, warnings or qualifications may apply if the reader is

receiving or accessing this report in or from other than Malaysia.

As of 10 January 2012, Maybank Investment Bank Berhad and the covering analyst does not have any interest in in any companies

recommended in this Market themes report.

Analyst Certification:

The views expressed in this research report accurately reflect the analyst's personal views about any and all of the subject securities or

issuers; and no part of the research analyst's compensation was, is, or will be, directly or indirectly, related to the specific recommendations

or views expressed in the report.

Additional Disclaimer (for purpose of distribution in the United Kingdom)

This document is being distributed by Kim Eng Securities Limited, which is authorised and regulated by the Financial Services Authority and

is for Informational Purposes only.This document is not intended for distribution to anyone defined as a Retail Client under the Financial

Services and Markets Act 2000 within the UK. Any inclusion of a third party link is for the recipients convenience only, and that the firm does

not take any responsibility for its comments or accuracy, and that access to such links is at the individuals own risk. Nothing in this report

should be considered as constituting legal, accounting or tax advice, and that for accurate guidance recipients should consult with their own

independent tax advisers.

Published / Printed by

Maybank Investment Bank Berhad (15938-H)

(A Participating Organisation of Bursa Malaysia Securities Berhad) 33rd Floor, Menara Maybank, 100 Jalan Tun Perak, 50050 Kuala Lumpur

Tel: (603) 2059 1888; Fax: (603) 2078 4194 Stockbroking Business:

Level 8, Tower C, Dataran Maybank, No.1, Jalan Maarof 59000 Kuala Lumpur Tel: (603) 2297 8888; Fax: (603) 2282 5136

http://www.maybank-ib.com