ppps in central and eastern european countries

DESCRIPTION

PPPs in Central and Eastern European countries. Peter Hodecek Austrian Waste Management Association (VOEB) / AVE Energie AG Umwelt GmbH. Tirana, 21.9.2011. Introduction: Who is „ “?. is one of the biggest private waste management companies in CEE: turnover: 500 MEUR - PowerPoint PPT PresentationTRANSCRIPT

PPPs in Central and Eastern European countries

Peter HodecekAustrian Waste Management Association (VOEB) /

AVE Energie AG Umwelt GmbH

Tirana, 21.9.2011

Introduction: Who is „ “?

is one of the biggest private waste management companies in CEE:

turnover: 500 MEUR staff: 5.400 employees

operates 160 locations in 9 countries (A, I, D, CZ, SK, H, RU, UA, MD)

owns a fleet with almost 2.600 trucks and special vehicles operates more than 50 wholly-owned waste treatment plants

which all comply with (higher) Austrian or at least with (lower) EU-standards

handles approx. 6,2 Mio. tons of waste annually serves 5.665 public (municipal) clients has successfully realised PPP-models for municipal waste

management, even with big cities

2

AVE‘s PPPs in CEE

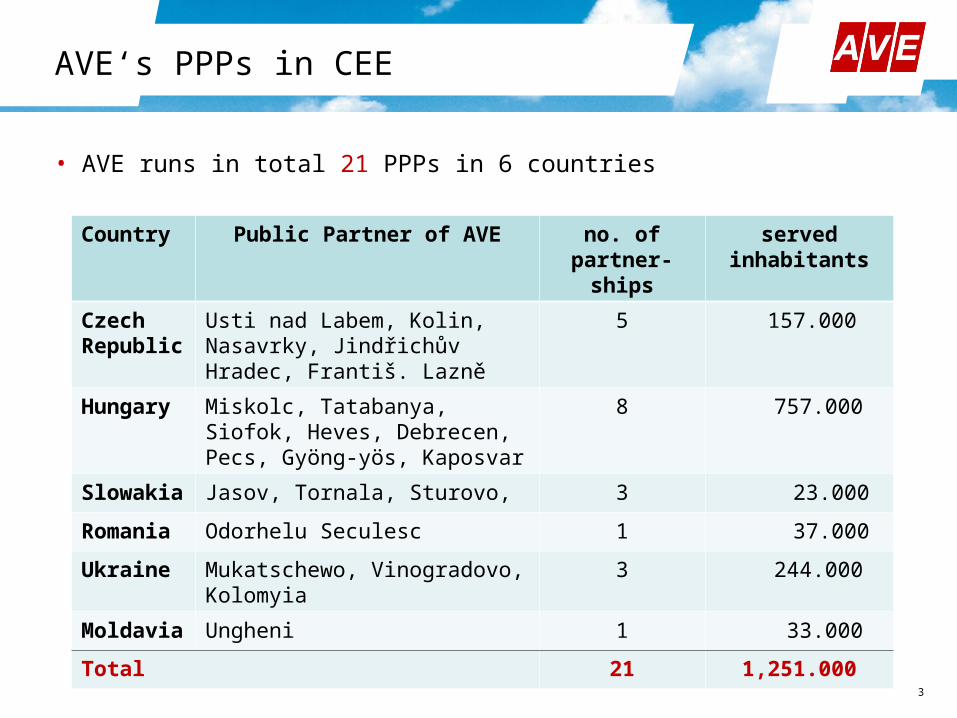

• AVE runs in total 21 PPPs in 6 countries

Country Public Partner of AVE no. of partner-ships

served inhabitants

Czech Republic

Usti nad Labem, Kolin, Nasavrky, Jindřichův Hradec, Františ. Lazně

5 157.000

Hungary Miskolc, Tatabanya, Siofok, Heves, Debrecen, Pecs, Gyöng-yös, Kaposvar

8 757.000

Slowakia Jasov, Tornala, Sturovo, 3 23.000

Romania Odorhelu Seculesc 1 37.000

Ukraine Mukatschewo, Vinogradovo, Kolomyia

3 244.000

Moldavia Ungheni 1 33.000

Total 21 1,251.000

3

AVE‘s PPPs in CEE

4

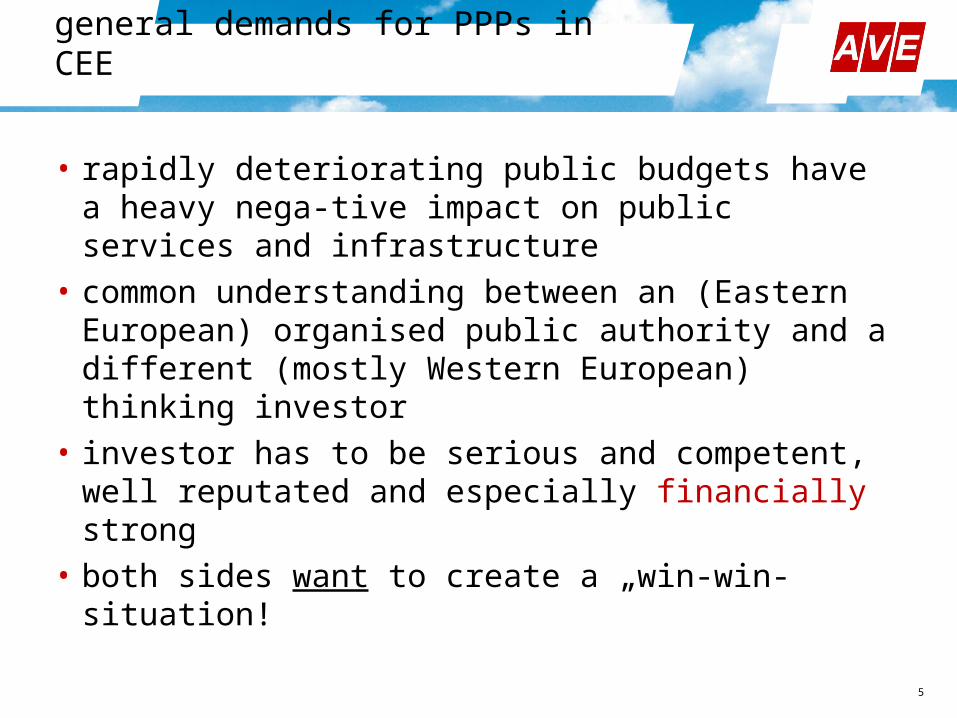

general demands for PPPs in CEE

• rapidly deteriorating public budgets have a heavy nega-tive impact on public services and infrastructure

• common understanding between an (Eastern European) organised public authority and a different (mostly Western European) thinking investor

• investor has to be serious and competent, well reputated and especially financially strong

• both sides want to create a „win-win-situation!

5

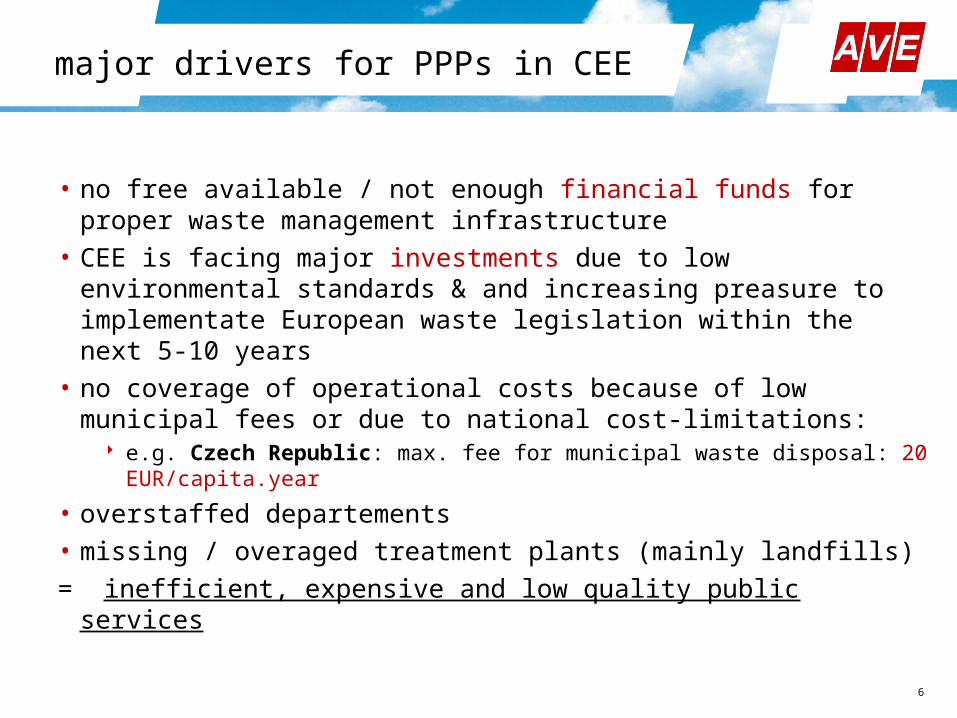

major drivers for PPPs in CEE

• no free available / not enough financial funds for proper waste management infrastructure

• CEE is facing major investments due to low environmental standards & and increasing preasure to implementate European waste legislation within the next 5-10 years

• no coverage of operational costs because of low municipal fees or due to national cost-limitations:

e.g. Czech Republic: max. fee for municipal waste disposal: 20 EUR/capita.year

• overstaffed departements

• missing / overaged treatment plants (mainly landfills)

= inefficient, expensive and low quality public services

6

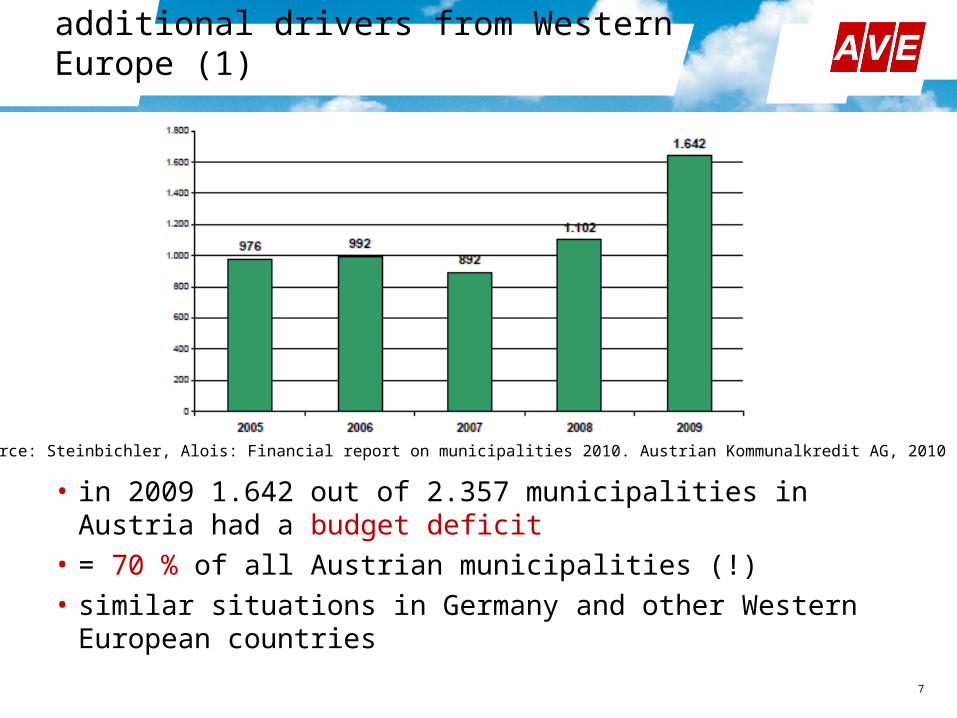

additional drivers from Western Europe (1)

• in 2009 1.642 out of 2.357 municipalities in Austria had a budget deficit

• = 70 % of all Austrian municipalities (!)• similar situations in Germany and other Western European

countries 7

source: Steinbichler, Alois: Financial report on municipalities 2010. Austrian Kommunalkredit AG, 2010

• disposal costs (including collection, transport and disposal) for residual waste in big cities in Germany and Austria:

(average anually waste generation of one household (2 persons): 3,12 m3/a or 60 l/week and 52 collections/a)

Berlin: ca. 72 EUR/household.aDüsseldorf: ca. 187 EUR/household.aVienna: ca. 110 EUR/household.a (+27 % within 5 yrs!)

• prices for municipal waste disposal are strongly increasing:transportation costs (fuel), separate collection, incineration,…..ageing populations demand more sophisticated services

8

additional drivers from Western Europe (2)

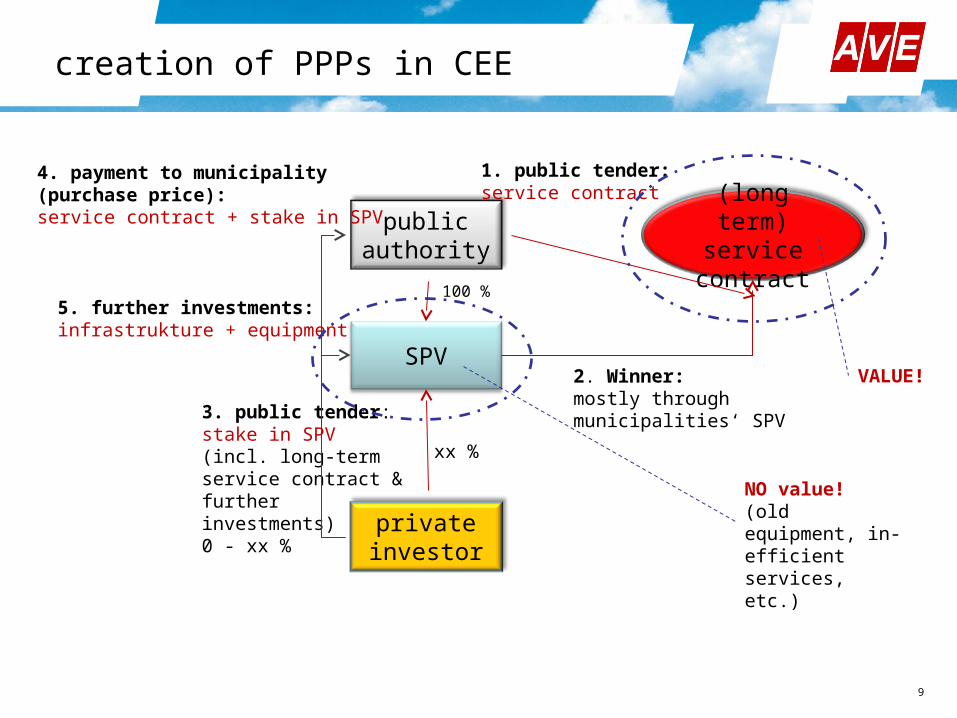

creation of PPPs in CEE

public authority

SPV

(long term) servicecontract

xx %

private investor

3. public tender:stake in SPV (incl. long-term service contract & further investments)0 - xx %

1. public tender:service contract

2. Winner:mostly throughmunicipalities‘ SPV

4. payment to municipality(purchase price):service contract + stake in SPV

VALUE!

5. further investments:infrastrukture + equipment

NO value!(old equipment, in-efficient services, etc.)

100 %

9

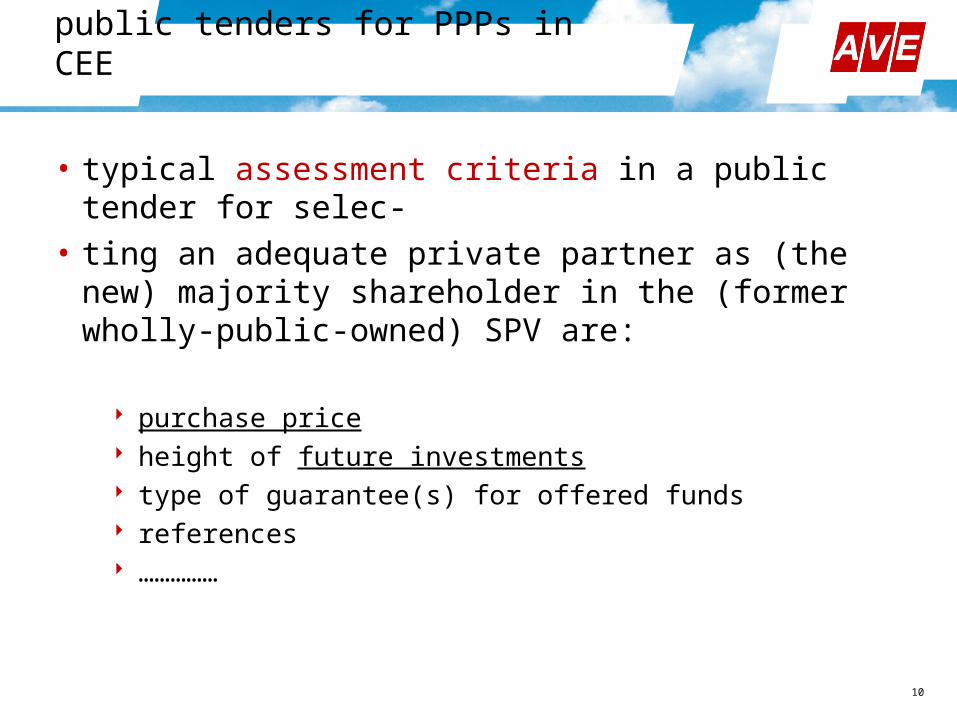

public tenders for PPPs in CEE

• typical assessment criteria in a public tender for selec-• ting an adequate private partner as (the new) majority

shareholder in the (former wholly-public-owned) SPV are:

purchase price height of future investments type of guarantee(s) for offered funds references ……………

10

expectations of a private investor

• opening of new markets / further growth• long-term businesses with stable profits / cash-flows• partly share of investment risks• guarantee for long-term agreements• access to EU fundings for new waste management infra-

structure• transparency and fair competition / equal treatment during

the transaction process• political will for improvement of public services• no extraordinary legal barriers for private sector

11

expectations of a public authority

• free available financial funds!• preservation of control• increase of service quality, technological & environmen-tal

standards with same or even lower prices for citizens• access to financial ressources in order to modernise

waste management infrastructure (logistics, collection yards, administrative and operative buildings, disposal and recycling plants, etc.)

• transfer of operational risks to private partner• special minority rights (Management, Supervisory Board,

etc.)

12

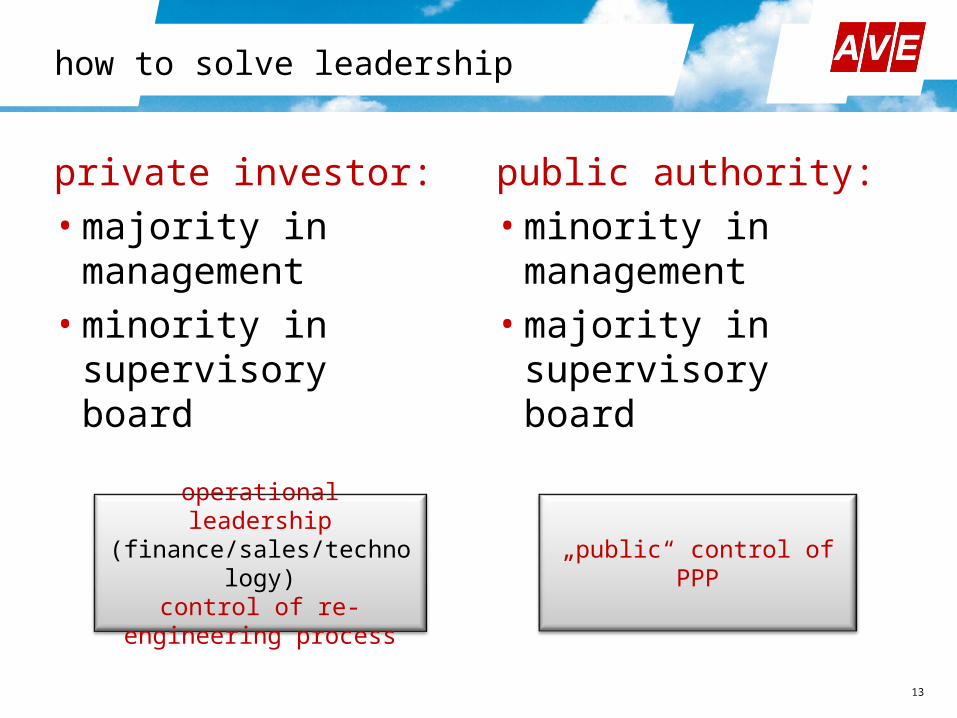

how to solve leadership

private investor:• majority in

management • minority in supervisory

board

public authority:• minority in

management• majority in supervisory

board

operational leadership (finance/sales/technology)control of re-engineering

process

„public“ control of PPP

13

necessary investments

1) purchase price• turnover < 3 MEUR: multiples = ca.1,0 • turnover > 3 MEUR: multiples = <<1,0

PPP 1

PPP 5

PPP 4

PPP 2

PPP 3

Private Co.

PPP 6

0

1

2

3

4

5

6

7

0 1 2 3 4 5 6 7 8 9 10

turn

ov

er

in M

io. E

UR

purchase price in Mio. EUR

Axis 1:1

Axis 0,65:1

14

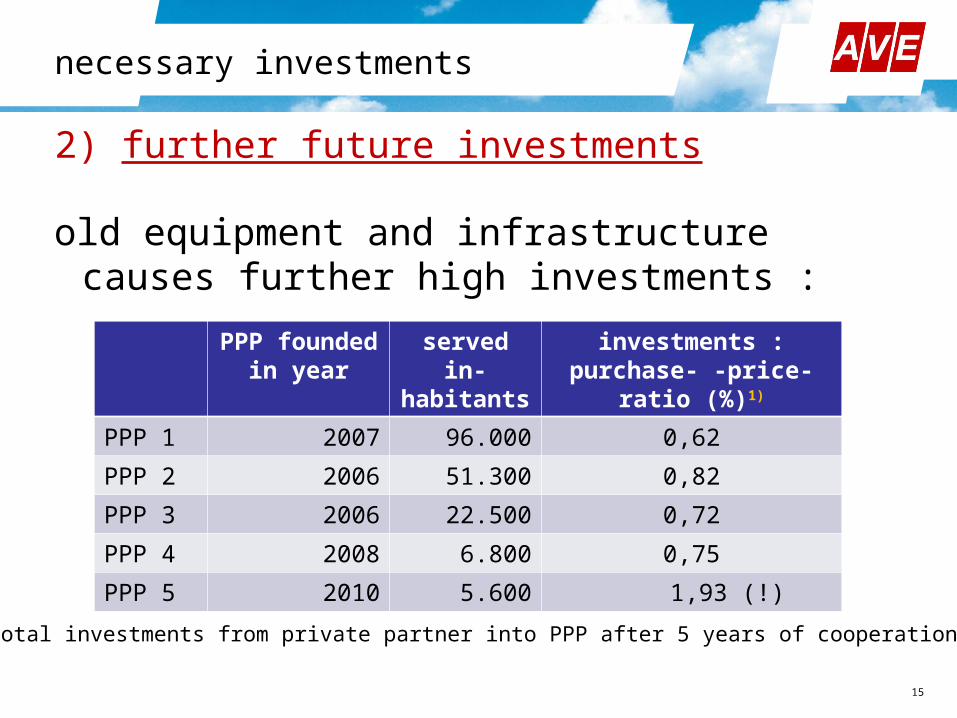

necessary investments

2) further future investments

old equipment and infrastructure causes further high investments :

PPP founded in year

served in-habitants

investments : purchase- -price-ratio (%)1)

PPP 1 2007 96.000 0,62

PPP 2 2006 51.300 0,82

PPP 3 2006 22.500 0,72

PPP 4 2008 6.800 0,75

PPP 5 2010 5.600 1,93 (!)

1) total investments from private partner into PPP after 5 years of cooperation

15

Buildings & Infrastructure before/after privatisation

16

Logistics before/after privatisation

17

collecting yards & sorting plantsbefore/after privatisation

18

landfills before/after privatisation

19

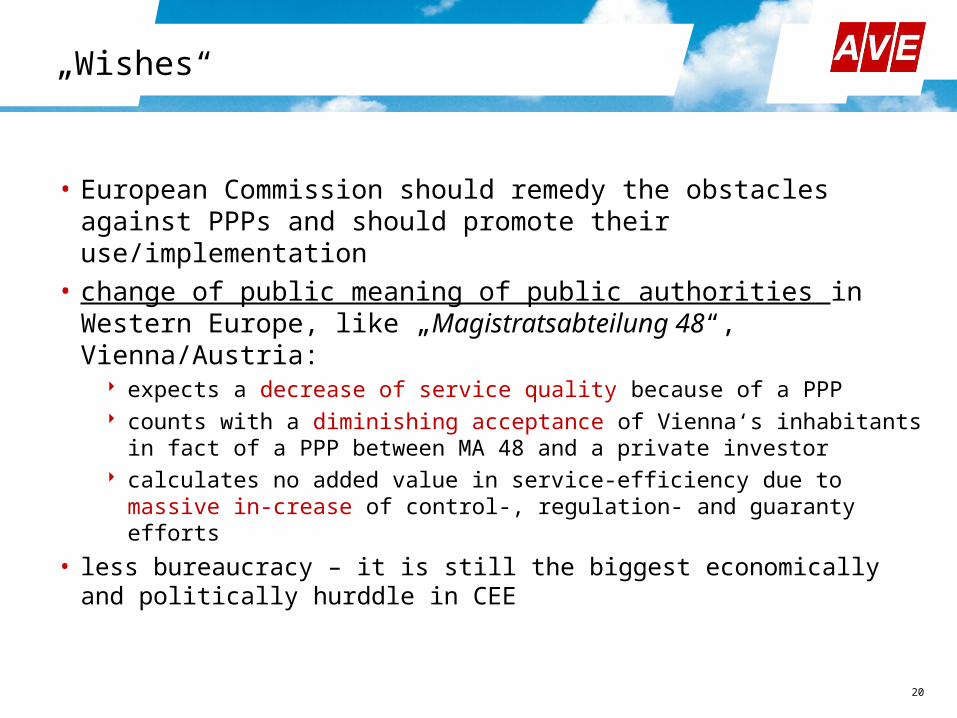

„Wishes“

• European Commission should remedy the obstacles against PPPs and should promote their use/implementation

• change of public meaning of public authorities in Western Europe, like „Magistratsabteilung 48“, Vienna/Austria:

expects a decrease of service quality because of a PPP counts with a diminishing acceptance of Vienna‘s inhabitants in

fact of a PPP between MA 48 and a private investor calculates no added value in service-efficiency due to massive in-

crease of control-, regulation- and guaranty efforts

• less bureaucracy – it is still the biggest economically and politically hurddle in CEE

20

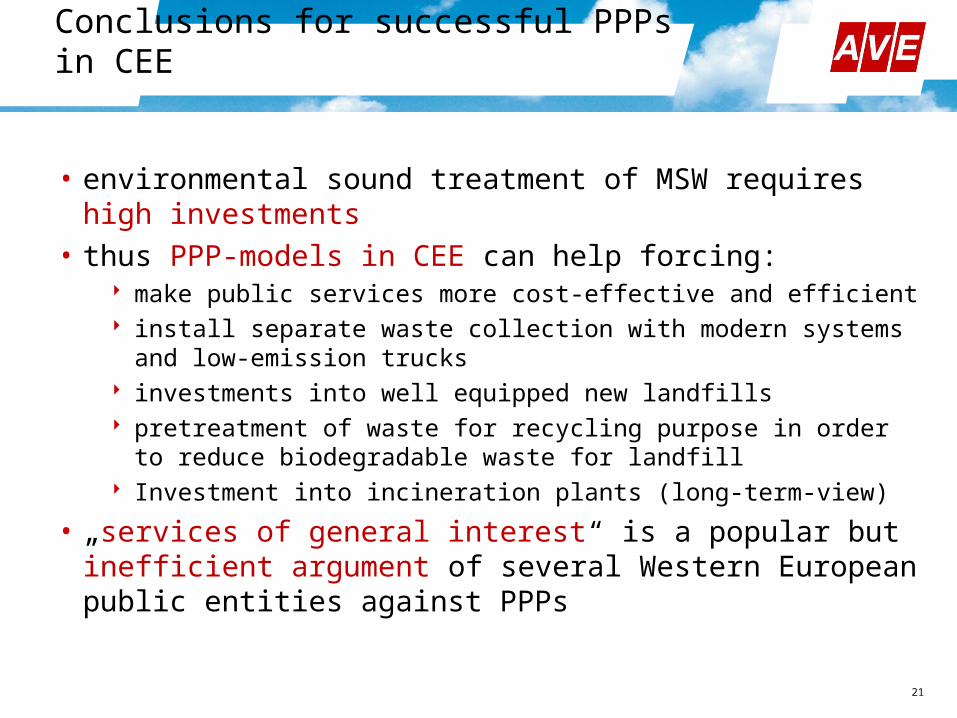

Conclusions for successful PPPs in CEE

• environmental sound treatment of MSW requires high investments

• thus PPP-models in CEE can help forcing: make public services more cost-effective and efficient install separate waste collection with modern systems and low-

emission trucks investments into well equipped new landfills pretreatment of waste for recycling purpose in order to reduce

biodegradable waste for landfill Investment into incineration plants (long-term-view)

• „services of general interest“ is a popular but inefficient argument of several Western European public entities against PPPs

21

Thank you very much for your attention!

22